GST on Real Estate and Works Contracts - Komandoor

22

GST Impact on Real Estate and Works Contract By CA L.Gopal Shah Komandoor & Co LLP Bhubaneswar, Odisha [email protected] [email protected] M: 9437124361

Transcript of GST on Real Estate and Works Contracts - Komandoor

GST Impact on Real Estate and

Works Contract

By

CA L.Gopal ShahKomandoor & Co LLP

Bhubaneswar, [email protected]

[email protected]: 9437124361

2

✓ GST on Works Contracts

✓ GST on Real Estate Transactions

✓ CBIC – FAQ on real estate sector on New Scheme

Agenda

3

➢ Understanding Supply

➢ Works Contract under Pre GST Regime

➢ Works Contract under GST Regime

➢ GST Rate on Various Works Contract

GST on Works Contract

❑ GST is levy on Supply of Goods or Services or both

❑ ‘Supply’ as defined under Section 7(1) of CGST Act, 2017

❑ All forms of supply of goods or services or both such as sale, transfer, barter, exchange, license, rental, lease or

disposal made or agreed to be made for consideration by a person in the course or furtherance of business

❑ Import of services for a consideration whether or not in the course or furtherance of business

❑ Activities specified in Schedule I, made or agreed to be made without consideration

❑ Activities to be treated as supply of goods or supply of services as referred to in Schedule II.

❑ Section 7(2) provides that activities specified in schedule III are neither supply of goods nor services

Understanding Supply

4

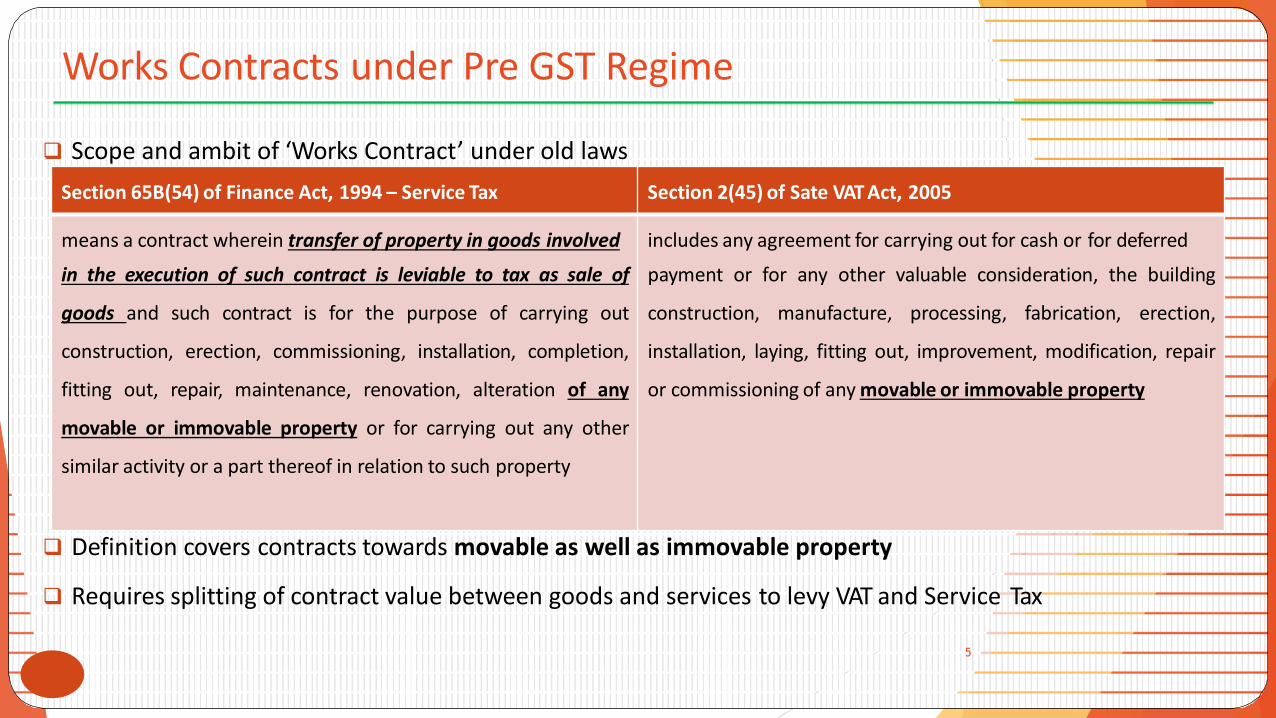

❑ Scope and ambit of ‘Works Contract’ under old laws

Works Contracts under Pre GST Regime

5

❑ Definition covers contracts towards movable as well as immovable property

❑ Requires splitting of contract value between goods and services to levy VAT and Service Tax

Section 65B(54) of Finance Act, 1994 – Service Tax Section 2(45) of Sate VAT Act, 2005

means a contract wherein transfer of property in goods involved

in the execution of such contract is leviable to tax as sale of

goods and such contract is for the purpose of carrying out

construction, erection, commissioning, installation, completion,

fitting out, repair, maintenance, renovation, alteration of any

movable or immovable property or for carrying out any other

similar activity or a part thereof in relation to such property

includes any agreement for carrying out for cash or for deferred

payment or for any other valuable consideration, the building

construction, manufacture, processing, fabrication, erection,

installation, laying, fitting out, improvement, modification, repair

or commissioning of any movable or immovable property

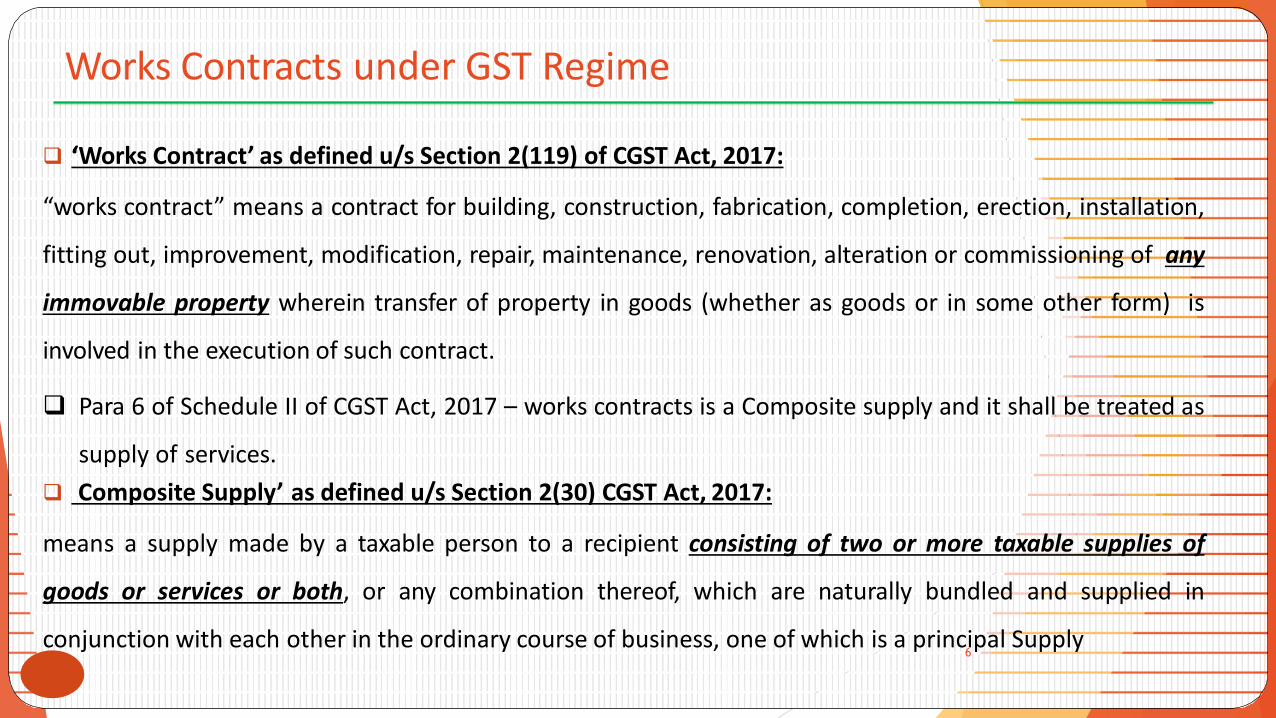

❑ ‘‘Works Contract’ as defined u/s Section 2(119) of CGST Act, 2017:

“works contract” means a contract for building, construction, fabrication, completion, erection, installation,

fitting out, improvement, modification, repair, maintenance, renovation, alteration or commissioning of any

immovable property wherein transfer of property in goods (whether as goods or in some other form) is

involved in the execution of such contract.

❑ Para 6 of Schedule II of CGST Act, 2017 – works contracts is a Composite supply and it shall be treated as

supply of services.

❑ Composite Supply’ as defined u/s Section 2(30) CGST Act, 2017:

means a supply made by a taxable person to a recipient consisting of two or more taxable supplies of

goods or services or both, or any combination thereof, which are naturally bundled and supplied in

conjunction with each other in the ordinary course of business, one of which is a principal Supply

Works Contracts under GST Regime

6

❑ Works Contracts will be a composite supply in GST regime

❑ Works Contracts towards immovable property are alone considered as works contracts under GST

❑ Works Contracts towards movable property are composite supplies and not works contracts under GST.❑ For example : Given contractor to a carpenter for preparing furniture is not a Works Contractor. It will be a

composite supply or mixed supply

❑ Such movable property contracts are subject to GST either as goods or as services on the basis of principle supply.

Works Contracts under GST Regime

7

❑ Works contracts in general are subject to GST at 18%

❑ Specified works contracts are subject to GST at 12%

❑ Govt related works contracts provided by main contractor are taxable at 12% while sub-contractors are taxable at1 2 % / 18%

❑ All construction related labour contracts are subject to GST at 18% / 12%

❑ Only Labour contracts relating to single residential unit are exempt while the related works contracts (include Labourand material) are taxable at 12%

GST Rates on Works Contracts

8

GST on Real Estate

9

❑Para 5(b) of Schedule II treats Builder’s Activity as Supply of Service:

construction of a complex, building, civil structure or a part thereof, including a complex or building

intended for sale to a buyer, wholly or partly, except where the entire consideration has been received

after issuance of completion certificate, where required, by the competent authority or after its first

occupation, whichever is earlier

❑ Para 5 of Schedule III excludes transactions in immovable property from the scope of ‘Supply’:

Sale of land and, subject to clause (b) of paragraph 5 of Schedule II, sale of buildingIt means the following:There shall be no GST on sale of land and no GST on unsold flat after getting completion certificate or after its first occupation , whichever is earlier

❑ Rate of GST is 18% with 1/3rd deduction towards land value (GST Rate till 31/03/2019)

GST Implications on Builder for Sale of Flats/Villas

10

Affordable residential apartment:- a residential apartment in a project having carpet area not exceeding 60 square meter in metropolitan cities or 90 square meter in cities or towns other than metropolitan cities and for which the gross amount charged is not more than Rs. 45 Lakhs.

Real Estate Project (REP) :- Real Estate Project shall have the same meaning as assigned to it in in clause (zn) of section 2 of the Real Estate (Regulation and Development) Act, 2016 (16 of 2016);As per RERA act REP means the development of a building or a building consisting of apartments, or converting an existing building or a part thereof into apartments, or the development of land into plots or apartment , as the case may be, for the purpose of selling all or some of the said apartments or plots or buildings, as the case may be, and includes the common areas, the development works, all improvements and structure thereon, and all easement , right and appurtenances belonging thereto.

Important Definition for New Scheme In Real Estate Projects w.e.ffrom 1st April 2020

11

Residential Real Estate Project (RREP) :- Residential Real Estate Project shall mean a REP in which the carpet area of the commercial apartments is not more than 15 per cent of the total carpet area of all the apartments in the REP.

Apartment shall have the same meaning as assigned to it in clause (e) of section 2 of the Real Estate (Regulation and Development) Act, 2016 (16 of 2016).

Floor space index (FSI) shall mean the ratio of a building’s total floor area (gross floor area) to the size of

the piece of land upon which it is built.

Promoter shall have the same meaning as assigned to it in in clause (zk) of section 2 of the Real Estate (Regulation and Development) Act, 2016 (16 of 2016).

Developer- promoter is a promoter who constructs or converts a building into apartments or develops a plot for sale

Important Definition for New Scheme In Real Estate Projects w.e.f from 1st April 2020 (Cont….)

12

Residential Real Estate Project (RREP) :- Residential Real Estate Project shall mean a REP in which the carpet area of the commercial apartments is not more than 15 per cent of the total carpet area of all the apartments in the REP.

Apartment shall have the same meaning as assigned to it in clause (e) of section 2 of the Real Estate (Regulation and Development) Act, 2016 (16 of 2016).

Floor space index (FSI) shall mean the ratio of a building’s total floor area (gross floor area) to the size of

the piece of land upon which it is built.

Promoter shall have the same meaning as assigned to it in in clause (zk) of section 2 of the Real Estate (Regulation and Development) Act, 2016 (16 of 2016).

Developer- promoter is a promoter who constructs or converts a building into apartments or develops a plot for sale

Important Definition for New Scheme In Real Estate Projects w.e.f from 1st April 2020 (Cont….)

13

Real Estate Project

w.e.f. 1st April 2019 Project will have to be

divided in two parts

New Scheme

Ongoing Projects

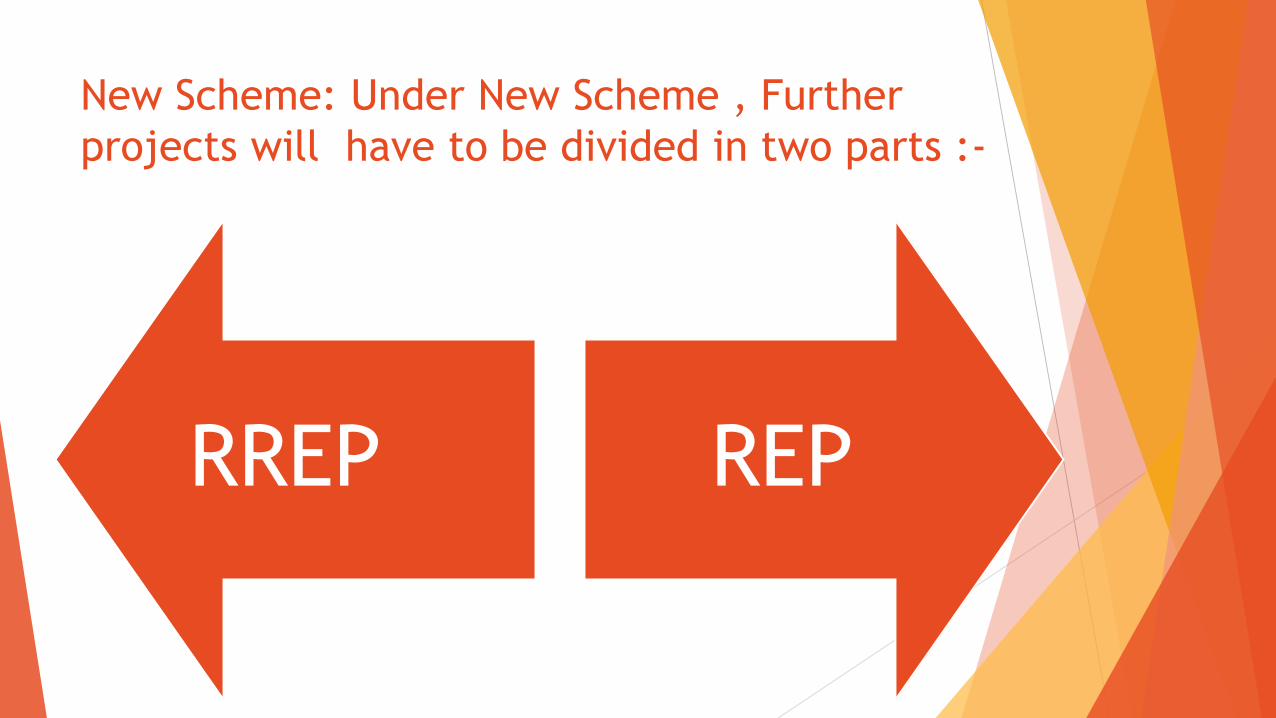

New Scheme: Under New Scheme , Further

projects will have to be divided in two parts :-

RREP REP

GST rate w.e.f from 1st April 2019 on Real Estate

SN Description of Services Type of Project Existing GST Rate

New GST Rate (w.e.f1st April 2019)

1 Construction of affordable residential apartments

Residential Real Estate Project (RREP)

8% 1%

2 Construction of residential apartments other than affordable residential

12% 5%

3 Construction of commercial apartments (shops, offices, godowns etc.)

12% 5%

4 Construction of affordable residential apartments

Real Estate Project (REP)

8% 1%

5 Construction of residential apartments other than affordable residential

12% 5%

6 Construction of commercial apartments (shops, offices, godowns etc.)

12% 12%

❑ In case of RREP and REP which commence on or after 1st April 2019, the above new rate are mandatory .

❑ The above rates given in previous slide is applicable to all ongoing project also where promoter has not exercise the option to pay GST at old / existing rate.

❑ In case of ongoing projects , promoter has an option to opt for existing rate otherwise new rate would be applicable by default.

❑ Options to continue with the existing / old rate has to be exercise before 10th may 2019.

❑ GST shall not be payable where the entire consideration has been received after issuance of completion certificate , where required, by the competent authority or after its first occupation , whichever is earlier.

New GST Rate versus old GST Rate: Conditions

17

GST on reverse charge on Inputs

18

A promoter shall purchase at least 80% of the value of input and input services from the registered suppliers. For calculating this threshold, the value of services by way of grant of development rights, long term lease of land, floor space index, or the value of electricity, high speed diesel, motor spirit and natural gas used in the construction of residential apartments in project shall be excluded.

If the value of input and input services is less than 80% then the promoter has to pay GST @ 18% on reverse charge basis except cement on which tax has to be paid by the promoter on reverse charge basis at the rate 28% (CGST – 14% + SGST – 14%).

GST on reverse charge on Inputs (Cont..)

19

The promoter shall maintain project wise account of inward supplies from registered and unregistered supplier and calculate tax payments on the shortfall at the end of the financial year and shall submit the same in the prescribed form electronically on the common portal by end of the quarter following the financial year.

The tax liability on the shortfall of inward supplies from unregistered person so determined shall be added to his output tax liability in the month not later than the month of June following the end of the financial year

❑Para 5 of Schedule III provides that sale of land is neither a supply of goods nor services.

❑Therefore, no GST is applicable in general on plot sales.

❑ If the sale consideration is split between land value and development cost— GST may

get attracted on development

❑As this is exempt activity, ITC is required to be reversed…

GST Implications on Plot Sales

20

CBIC – FAQ on real estate sector on New

Scheme

F.No:354/32/2019- TRU dated: 7th May 2019 total 41 Points

F.No:354/32/2019- TRU dated: 14th May 2019 total 27 Points

Copy attached below

Thank You

![Penalties Proposed under GST - GST panaceagstpanacea.com/.../Penalties-Proposed-under-GST-Regime.pdfOffences & Penalties [Section 66] According to GST law Penalty means under section](https://static.fdocuments.in/doc/165x107/5f0beedd7e708231d432ef1d/penalties-proposed-under-gst-gst-offences-penalties-section-66-according.jpg)