GST-HST 2013 new - Farro · Importers • Failure to understand and plan appropriately for GST/HST...

17

September 2013 GST/HST | Page 1 Goods & Services Tax and Harmonized Sales Tax September 24 - 25, 2013 Slide 2 Agenda • What is Goods & Services Tax (GST)? • What is Harmonized Services Tax (HST)? • Registration • GST paid at Time of Importation (Division III Tax) • GST Invoiced to Customer (Division II Tax) • Place of Supply Rules • Recovery of GST/HST • Recordkeeping • Audits Slide 3 GST/HST • The recent increase in audit activity and denials of recovery for GST in cross-border trade reminds us that there are many tips and traps involved for Non-Resident Importers • Failure to understand and plan appropriately for GST/HST and/or customs issues can result in unforeseen - and potentially costly - consequences

Transcript of GST-HST 2013 new - Farro · Importers • Failure to understand and plan appropriately for GST/HST...

September 2013 GST/HST | Page 1

Goods & Services Tax and Harmonized Sales Tax

September 24 - 25, 2013

Slide 2

Agenda

• What is Goods & Services Tax (GST)?

• What is Harmonized Services Tax (HST)?

• Registration

• GST paid at Time of Importation (Division III Tax)

• GST Invoiced to Customer (Division II Tax)

• Place of Supply Rules

• Recovery of GST/HST

• Recordkeeping

• Audits

Slide 3

GST/HST

• The recent increase in audit activity and denials of recovery for GST in cross-border trade reminds us that there are many tips and traps involved for Non-Resident Importers

• Failure to understand and plan appropriately for GST/HST and/or customs issues can result in unforeseen - and potentially costly - consequences

September 2013 GST/HST | Page 2

Slide 4

Importing into Canada

• Registered for Goods & Services Tax (GST) or Not Registered for Goods & Services Tax (GST)

• If you act as the Importer of Record you will pay the GST at time of import

• Whether you are registered or not will dictate how you recover, or if you can recover the GST

• During the presentation today we will discuss both options and the benefits and challenges to your organization

Slide 5

What is Goods and Services Tax

• The Goods and Services Tax is a Federal Tax levied on all goods and services sold throughout Canada

• The GST was implemented on January 1, 1991

• It also applies to the supply of most property and services in Canada

• GST rate is 5%

• Some commodities are exempt from GST, (i.e.) basic groceries, medical equipment

Slide 6

What is Harmonized Sales Tax

• The Harmonized Sales Tax is a blended tax comprising the Federal GST and the Provincial Sales Tax = HST

• The HST only applies to participating Provinces, at different rates

� Nova Scotia 15%

� New Brunswick 13%

� Prince Edward Island 14%

� Newfoundland and Labrador 13%

� Ontario 13%

September 2013 GST/HST | Page 3

Slide 7

How it works

• There are taxes that must be paid and there are taxes that must be billed

• Once registered for GST you, in essence, act as if you are operating in Canada

• All companies in Canada that sell a good or service must bill their customers the GST or HST

• Many Non-Resident Importers believe that once they pay the GST on importation, their responsibility is complete, that is not true

Slide 8

Goods and Services Tax

• The GST/HST is a tax on final consumption, however, unlike a retail sales tax, the GST has a multistage collection process

• Canada Border Services Agency (CBSA) & Canada Revenue Agency (CRA) interact with all businesses through a Business Number

• Businesses must be registered in order to submit an “Input Tax Credit” (ITC) to invoice or recover GST /HST

• If not registered, only GST paid may be recovered by the flow through method

Slide 9

Registration

• Non-Resident importers that have a business number does not mean you are registered for GST

• A Business number is a 9 digit number followed by a program identifier and a 4 digit reference number

� Business number 123456789

� Importing number 123456789RM0001

� GST number 123456789RT0001

September 2013 GST/HST | Page 4

Slide 10

Registration

• Form RC-1 is used to register for both an importer number and for GST/HST

• Registrants must be considered as “Carrying on Business in Canada”

� As example - if a company is only sending samples or trade information, chances are, Canada Revenue Agency (CRA) will deny the application for registration

• A security deposit is usually required for non-resident importers

Slide 11

Security

• The initial amount of the security deposit is 50% of your estimated net tax, whether positive or negative, during the 12-month period after you register

• The maximum security deposit that may be required is $1 million, and the minimum is $5,000

• Your security deposit may be in the form of cash, certified cheque, money order, or a qualifying bond

Slide 12

Goods and Services Tax – how it works!

• As a Non-Resident Importer there is much to know and understand about the rules and regulations for GST/HST

� GST at time of Importation

� GST/HST Invoiced to your Customers

� Place of Supply Rules – What rate to bill at

� Input Tax Credits

September 2013 GST/HST | Page 5

Slide 13

GST Paid on Importation

• GST is paid on all importation into Canada, with some exceptions

• Commercial goods are subject to only the GST component – 5%

• Whoever is the Importer of Record must pay the GST, resident or non-resident – registered or not registered, unless the goods are exempt

Slide 14

GST paid on Import

• GST is paid on the value of the goods plus the duty, including anti-dumping duties, at time of importation

� Sales price $1000.00

� Duty 6.5% $ 65.00

� Total $ 1065.00

� GST 5% $ 53.25

� Grand Total $ 1118.25

Slide 15

Exceptions

• GST/HST does not apply to goods that are exported from Canada, it only applies to goods and services within Canada

• GST/HST does not apply to Exempt Goods

• Example

� Basic groceries, milk, bread, vegetables

� Prescription drugs

� Medical devices

� Agricultural products, wheat grain, raw wool, etc

� Canadian Goods Returned

September 2013 GST/HST | Page 6

Slide 16

GST/HST Invoiced to your Customers

• If a company is registered for GST legislation requires the seller to bill the GST/HST to their customer

• Place of supply rules apply, based on Participating Provinces

• Applies if the goods are “made available to Canada”

• So once registered, any sales or shipments made to Canada, regardless of who is the Importer of Record, must be invoiced the appropriate tax amount

Slide 17

Place of Supply Rules

• The application of the “Place of Supply Rules” is generally based on the Province in which legal delivery of the goods to the recipient occur

• If the Province has blended their provincial tax with the GST they are considered a “Participating Province” and the rate for that province, where the goods will be delivered, must be billed

Slide 18

Provincial GST/HST Rates

• Nova Scotia 15%

• New Brunswick 13%

• Prince Edward Island 14%

• Newfoundland and Labrador 13%

• Ontario 13%

• Territories and all other provinces 5%

September 2013 GST/HST | Page 7

Slide 19

Provincial Rates

Slide 20

Must be Visible

• The GST/HST is a visible tax, in other words, it is added to the sales price and not included, it must be shown as a separate line item on an invoice or sales receipt

Slide 21

Example 1 – Registered NRI

• Goods are sold to a purchaser in Prince Edward Island (PEI).

• Based on the terms of delivery in the agreement for the sale of the goods, legal delivery of the goods to the purchaser occurs in PEI

• Goods are subject to HST rate of 14%.

September 2013 GST/HST | Page 8

Slide 22

Example 2 – Registered NRI

• Goods are sold to a purchaser in British Columbia (BC)

• The goods are shipped directly to the purchaser in BC

• Because the goods are delivered in BC – the goods are subject to a GST rate of 5%

Slide 23

Example 3 – Registered NRI

• NRI sells goods to a purchaser in Alberta

• However, the customer requests the goods be shipped to an address in Ontario

• Delivery of the goods to the purchaser is considered to occur in Ontario even though the sale was to a company in Alberta

• The supply of the goods is therefore made in Ontario and HST will apply at a rate of 13%.

Slide 24

Example 4 – Registered NRI

• A U.S. Companies sells goods to another U.S. Company (who may or may not be registered for GST)

• The contract requires the U.S. Company to ship the goods to Canada

• Assuming the U.S. Company is registered for GST/HST, regardless of who acts as the Importer of Record – the exporter has made the goods “available” to Canada, the GST must be invoiced based on the place of supply rules

September 2013 GST/HST | Page 9

Slide 25

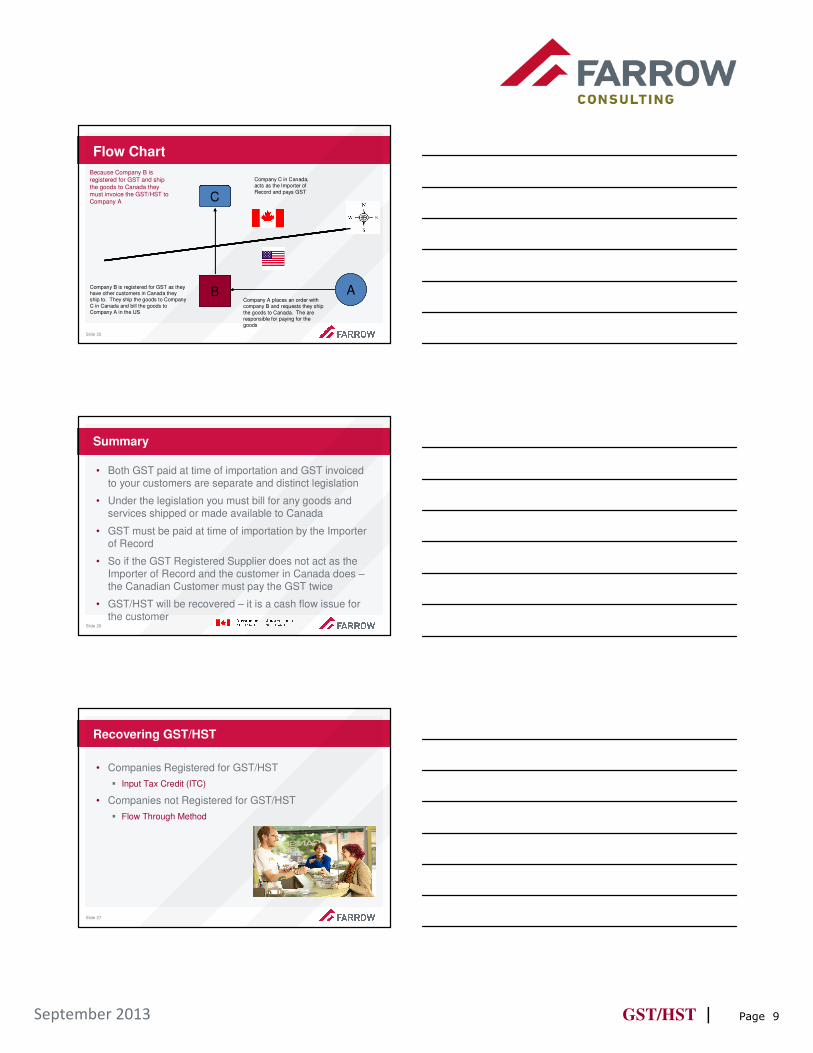

Flow Chart

B A

C

Company A places an order with company B and requests they ship the goods to Canada. The are responsible for paying for the goods

Company B is registered for GST as they have other customers in Canada they ship to. They ship the goods to Company C in Canada and bill the goods to Company A in the US

Company C in Canada, acts as the Importer of Record and pays GST

Because Company B is registered for GST and ship the goods to Canada they must invoice the GST/HST to Company A CCCC

B

C

B

C

AB

C

AB

C

Slide 26

Summary

• Both GST paid at time of importation and GST invoiced to your customers are separate and distinct legislation

• Under the legislation you must bill for any goods and services shipped or made available to Canada

• GST must be paid at time of importation by the Importer of Record

• So if the GST Registered Supplier does not act as the Importer of Record and the customer in Canada does –the Canadian Customer must pay the GST twice

• GST/HST will be recovered – it is a cash flow issue for the customer

Slide 27

Recovering GST/HST

• Companies Registered for GST/HST

� Input Tax Credit (ITC)

• Companies not Registered for GST/HST

� Flow Through Method

September 2013 GST/HST | Page 10

Slide 28

Input Tax Credit

• The registrant charges their customers GST/HST on the taxable goods and services supplied

• The registrant pays the GST at time of import

• Most companies use two General Ledger (GL) codes to manage the GST/HST, one for sales and the other for purchases

• At the end of the reporting period the two GL’s are totaled and one will offset the other, you will either owe CRA money or they will owe you money

Slide 29

Parties to the Transaction

• In order to submit an Input Tax Credit (ITC) – both entities must be considered “Parties to the Transaction”

• What this means is if a Non Registered company in the US sells goods to a Canadian company but uses their Canadian subsidiary to act as Importer of Record, they are not entitled to recover the GST through an ITC

• Best practice is to either Register for GST/HST or sell the goods to the Canadian subsidiary and have them sell the goods to the Canadian customer

Slide 30

Individual Example - HST

• 5% GST is paid at the border and billed by your customs broker

• Shipment is delivered in Ontario – you will invoice your customer 13% HST

• GST paid on $1000 - $ 50.00

• HST collected on $1000 - $ 130.00

• Balance owing to CRA - $ 80.00

September 2013 GST/HST | Page 11

Slide 31

Individual Example - GST

• GST paid on Import $1000.00 - $50.00

• GST Billed on invoice $1000.00 - $50.00

(goods shipped to Alberta)

• Balance owing to CRA nil

• Nil reports must be filed for the reporting period

Slide 32

Filing the Input Tax Credit

• Input Tax Credits (ITC) are filed, Monthly, Quarterly or Yearly based on your sales

• Must be declared and paid in Canadian FundsGST/HST Collected

on Sales GST/HST Paid

January $1,942.26 $1,526.91

February $1,418.62 $525.68

March $1,625.99 $725.62

Total $4,986.87 $2,778.21

Difference you must submit $2,208.66

Slide 33

GST34-2 E (11)

• A personalized document will be mailed based on your reporting period

• You will need to enter your total Sales for the period

• The amount of GST/HST paid

• The amount of GST/HST invoiced

• The difference between the above two points is either owed to CRA or what they owe you

• You may be able to file electronically

September 2013 GST/HST | Page 12

Slide 34

Benefit of being Registered for GST

• You can take the complications of the border away from your customers and act as a Canadian Company

• You are able to recover all the GST/HST paid on goods or services, assuming you follow the regulations

• Depending on your reporting period, you could earn interest on GST/HST paid to you by your customer that you do not need to pay to the Canada Revenue Agency for a period of time

Slide 35

Challenges of being Registered for GST/HST

• Subject to audits by Canada Revenue Agency

• Possibility of additional funds payable from mismanagement or misunderstanding requirements

• Subject to penalties

Slide 36

Flow Through Method

• A Non Registered Company pays GST at the border they are not entitled to file an input tax credit for recovery

• They may use, with co-operation of their Customer, who must be registered, a program called “Flow Through”

• The GST paid at time of importation is billed to the customer in Canada, supported by a copy of the B3 –Canada Customs Coding Document from your broker

• The Canadian Company, with this proof that the GST has been paid, may file the amount on their Input Tax Credit

September 2013 GST/HST | Page 13

Slide 37

Benefits of Flow Through

• Not subject to audits by CRA

• Do not have to worry about Place of Supply Rules

• Do not need to submit Input Tax Credit

Slide 38

Challenges with the Flow Through Method

• In the case of a Post Entry Adjustment and additional GST/HST is owed you must deal with your customer in order to recover it

• What if that customer has gone out of business, or your business relationship has soured, you may not have an avenue to recover the GST and it will be a cost to your bottom line

Slide 39

Refunds

• Companies registered for GST will always recover or pay any GST/HST through their ITC

� If an error occurs and GST is overpaid to CBSA the only means of recovery is through the ITC process

• If a Non-Registered company has an overpayment of GST/HST– they must file a refund to be entitled to the difference

September 2013 GST/HST | Page 14

Slide 40

Record Keeping

• As a Non-Resident Importer – you must have approval to keep your books and records outside of Canada, regardless of whether you are registered for GST/HST or not

• D-Memo (Customs Regulations) D17-1-21 details your responsibility

• Basically, in the event of an audit you could be expected to pay for the privilege of being audited

• Audit period – 4 years

Slide 41

Audits

• Canada Revenue Agency (CRA) is ramping up their audits on NRI’s

• There are a number of cases recently where the Registered Non Resident Importer is not correctly invoicing the GST/HST and is owing a substantial amount of money, one recently was over $4 million, a few others in the $50,000 to $100,000 range

• In order to be compliant, it is important that you understand the regulations and comply

Slide 42

Sample Penalties

• Late filing 1% of the amount owing plus 25% of the 1% times the number of months outstanding

• Failure to accurately report information

• Generally 5% of the amount plus 1% per month of the difference until it is corrected to a maximum of 10%

September 2013 GST/HST | Page 15

Slide 43

Voluntary Disclosure Program

• If you conduct a review of your procedures and find that you are in violation of the regulations there is a program that you can apply for, if approved, will eliminate penalties owing

• A valid disclosure must be:

� Voluntary – once an audit is initiated by CRA it is too late

� Complete

� Involve a Penalty

� Generally include information that is 1 year overdue

Slide 44

Tips and thoughts

• GST paid on importation should be recoverable and should not become a sunken cost, but recovery of the tax is not a given and careful planning is required

• Identifying the best party to act as the importer of record is crucial

• Non-resident companies face particular challenges when planning to import goods into Canada in their own name

Slide 45

Check List

• Are you registered for GST/HST? The web site below will allow you to input your business number and determine if you are registered

• http://www.cra-arc.gc.ca/esrvc-srvce/tx/bsnss/gsthstrgstry/menu-eng.html

• Have you billed the GST/HST based on the place of supply rules?

• Have you filed your Input Tax Credits?

September 2013 GST/HST | Page 16

Slide 46

Final Comment

• The import and export process in Canada operates under a complex legal and regulatory framework

• It is important to have cross-border transactions reviewed in detail to ensure the best treatment under Canadian tax and customs law and to avoid unintended consequences

• Furthermore, anyone who enters Canada and charges admission to an event such as a show or a concert, a seminar or an activity, must register for GST/HST before doing so

Slide 47

Services we can offer

• We can provide you the expertise and experience in all aspects of your international trade, such as

� GST audits & advice

� Customs issues, audits and advice

Slide 48

Publications

• Available as a download after the presentation

� Presentation slides

� RC1 - Registration Form

� RC2 - The Business Number and Your Canada Revenue Agency Program Accounts

� RC4027 - Doing Business in Canada –GST/HST Information for Non-Residents

� D17-1-21 - Record Maintenance Outside of Canada

� GST34-2 E - Input Tax Credit sample form

September 2013 GST/HST | Page 17

Slide 49

Web Sites

• www.farrow.com

• www.cra-arc.gc.ca

• ww.cbsa-asfc.gc.ca

• www.statcan.ca

* The information in this webinar is of a general nature and is not to be construed as legal advice. Attendees and readers should consult with their professional advisors for advice regarding their particular circumstances.

Slide 50

Contact Information

• Farrow International Trade Consulting

• Jennifer Deans

• Director

• 416 622-9327 ext 216

Thank you!

PAGE 51