GROWTH COMPETING FROM AUSTRALIA

104

58 GROWTH CEDA GROWTH NO 58 JULY 2007 COMPETING FROM AUSTRALIA SUPPORTED BY

Transcript of GROWTH COMPETING FROM AUSTRALIA

58GROWTH

CEDA GROWTH NO 58 JULY 2007

COMPETING FROM AUSTRALIA

SUPPORTED BY

COMPETING FROM AUSTRALIA

About this paper

Growth 58: Competing from AustraliaISBN 0-85801-269-3ISSN 0085-1280

© Committee for Economic Development of Australia 2007

The views expressed in this paper are solely those of theauthor and should not be attributed to CEDA. CEDA’s objectivein publishing this paper is to encourage constructive discussionon matters of national, economic and social importance.Persons who act in reliance upon the material publisheddo so at their own risk.

The research for this project was coordinated by CEDA’sResearch Director, Dr Ian Marsh, and CEDA’s Policy andCommunications Director, David Walker.

This document has been prepared by CEDA’s Policyand Communications Department. Please direct commentsand suggestions to David Walker.

Copy editing: Margaret TrudgeonDesign: Robyn Zwar Design/Mary Callahan DesignPrinting: Braemar GraphicsCover photography: istockphoto.com

All contributions to this publication have been independentlyrefereed prior to publication.

About CEDA

CEDA (the Committee for Economic Development of Australia)connects leaders of Australian organisations to promoteAustralia’s economic development.

CEDA’s activities: CEDA holds more than 250 events,seminars and chief executive roundtables each year, and publishes a range of research papers.

CEDA’s mission: CEDA’s research and forums identify andexplore issues that influence the nation’s long-term economicand social development.

CEDA’s reach: CEDA draws its members, which numberaround 1000, from businesses, universities, governments andthe not-for-profit sector. During 2006 CEDA’s economic andbusiness events attracted more than 21,000 people.

CEDA’s independence: CEDA advocates policy in the nationalinterest, rather than lobbying on behalf of special interestgroups. It is staunchly non-partisan. CEDA’s funding comesfrom membership, events, grants and sponsorship.

Committee for Economic Development of AustraliaLevel 5/136 Exhibition StreetMelbourne 3000 AustraliaTelephone: (61 3) 9662 3544Fax: (61 3) 9663 7271Email: [email protected]: ceda.com.au

1COMPETING FROM AUSTRALIA

Foreword 3David ByersCEO CEDA

1. Summary 4CEDA

2. Distance – A key to Australia’s economic dilema 6Geoffrey BlaineyAustralia’s most eminent historian

3. A new generation of policy questions 10Professor Ian MarshResearch Director, CEDA

4. Can distance be defeated 18Professor Glenn Withers, AOProfessor of Public Policy, Crawford School of Economicsand Government, Australian National University

5. Export weakness, investment strength 28Dr John EdwardsChief economist HSBC, Australia

6. Competing through innovation 42Professor Roy GreenDean of the Graduate School of Management, Macquarie University

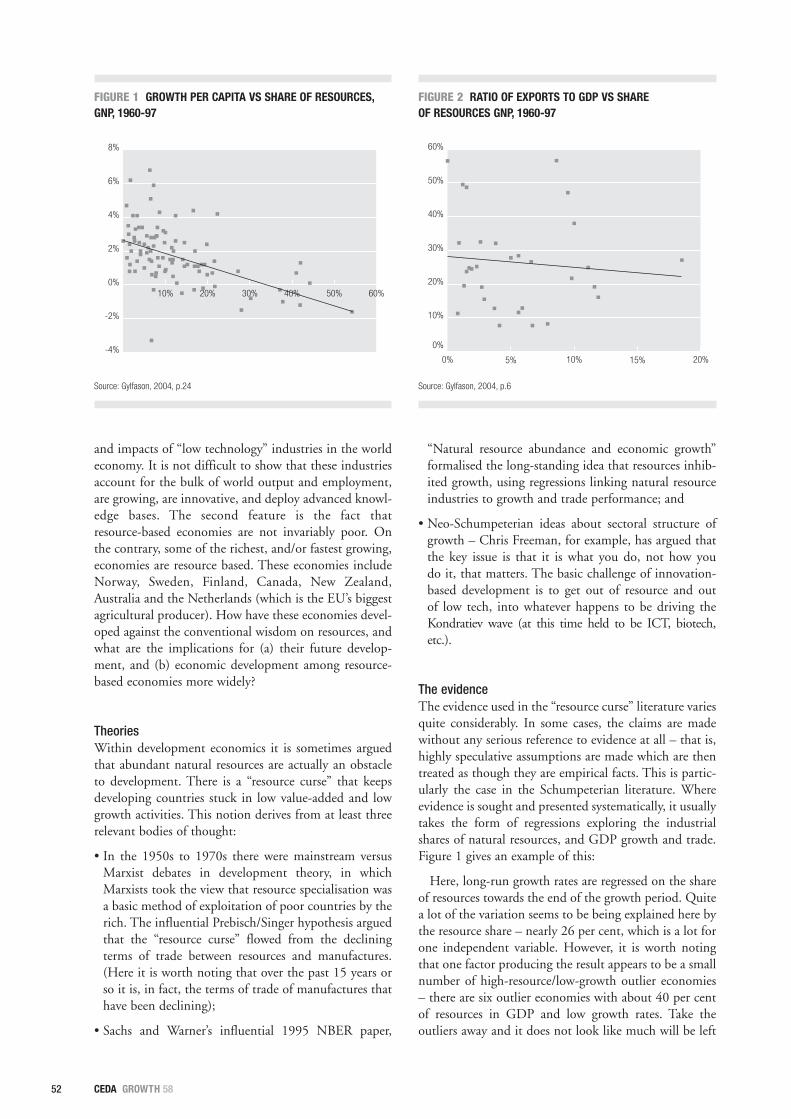

7. Innovation and growth in resource-based economies 50Professor Keith SmithChair in Innovation, University of Tasmania

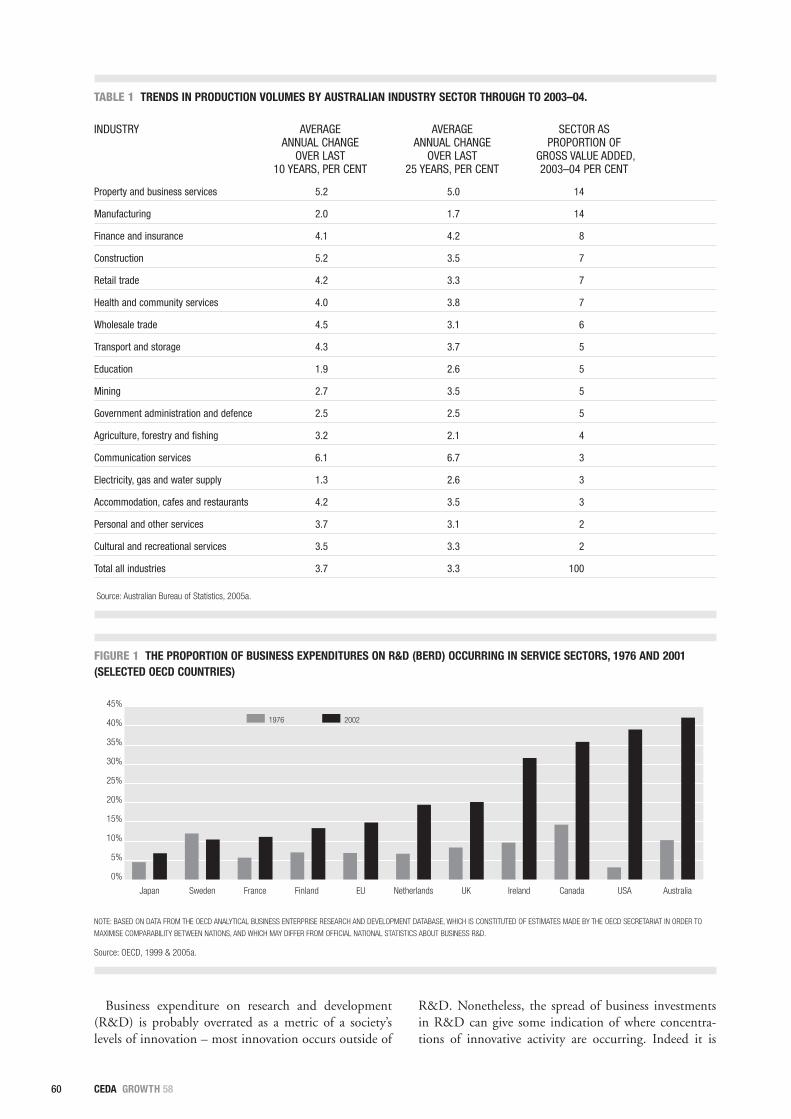

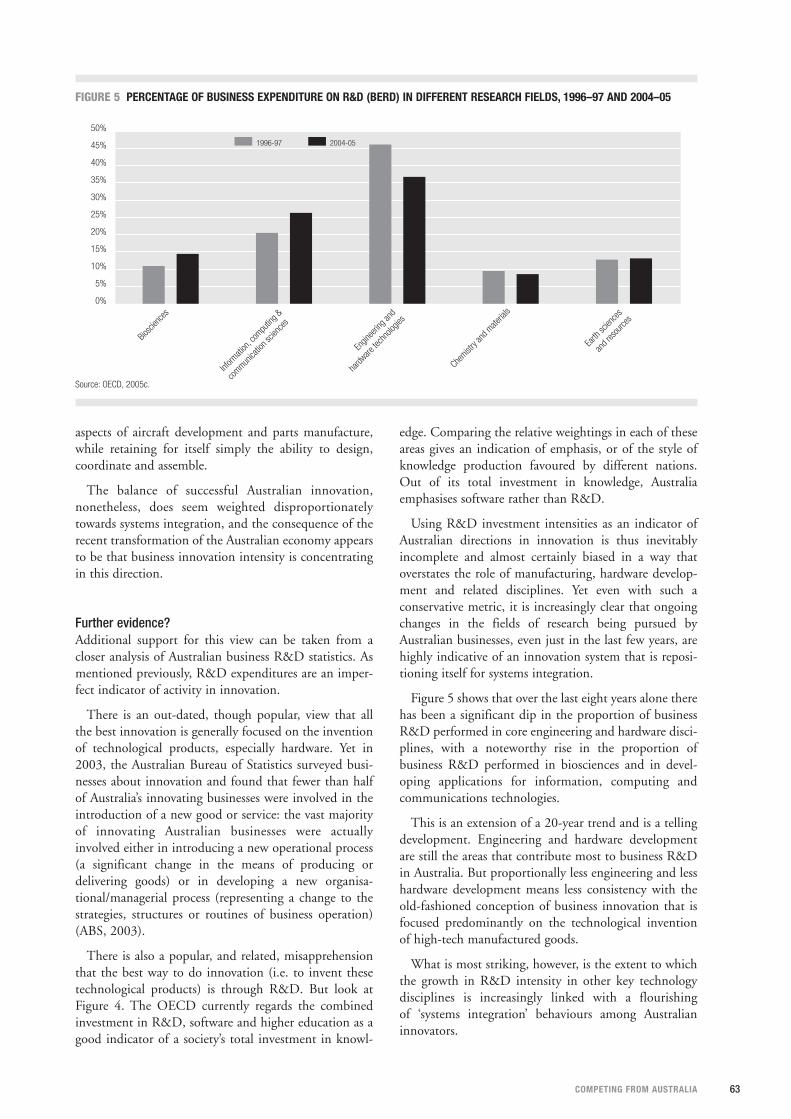

8. Australia’s capability for systems integration 58Dr Thomas BarlowBusiness and research strategy consultant, Barlow Advisory

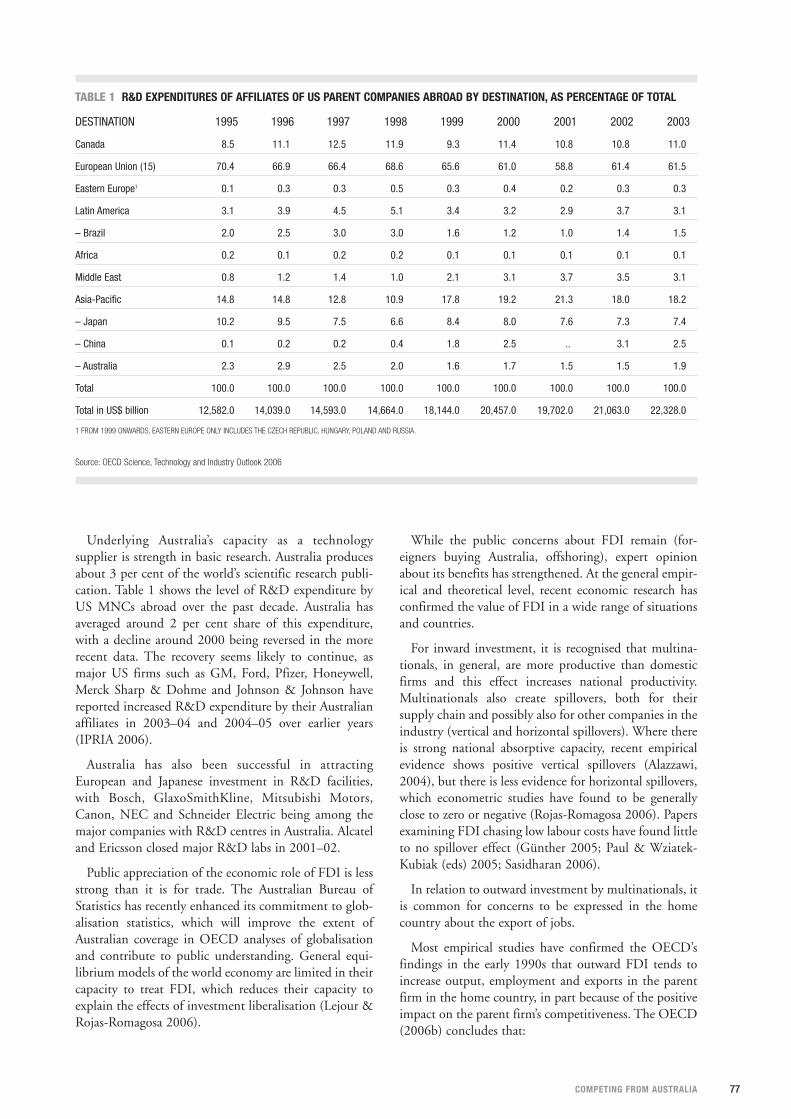

9. Multinational companies in Australia 66Andrew McCredieGlobal Opportunities Branch, Department of Industry, Tourismand Resources.

10. Global chains 84Professor John HoughtonProfessorial Fellow, Centre for Strategic Economic Studies(CSES), Victoria University

11. Appendix: Australia's 50 global leaders 98

contentscontentscontributorsand

Sponsor and contributor acknowledgements

CEDA would like to acknowledge the generous contributionsof the following organisations and individuals to theCompeting From Australia project.

Research sponsors

Export Finance and Insurance Corporation (EFIC) is a specialised financial services organisation supportingAustralian businesses exporting and investing overseas byproviding finance, finance guarantees, insurance and bondingfacilities. As well as working directly with exporters, it worksclosely with commercial financiers to support exporters.

Invest Victoria is responsible for attracting productive foreign direct investment into Victoria, and for promoting the state internationally as a world class investment location.It is a focus for the Victorian Government’s investmentattraction initiatives, providing quality services to investorclients in Australia and off-shore, as well as coordinating a range of investment and re-investment initiatives andprocesses within Government.

Research guidanceCEDA’s Research & Policy Committee has overseen the Competing From Australia project:

• Professor Percy Allan AM• Mr David Byers• Professor Peter Drake AM• Mr Saul Eslake• Mr John Harris• Professor Ian Marsh• Professor John Nevile• Professor John Nieuwenhuysen• Dr Suzanne Rickard• Mr Phil Ruthven• Mr David Walker• Ms Marina Williams-Wynn• Professor Kenneth Wiltshire• Professor Glenn Withers

Growth 58 text 21/6/07 12:34 PM Page 2

3COMPETING FROM AUSTRALIA

This CEDA collection of papers isone of our most ambitious. Likeseveral CEDA collections over our47 years’ existence, it seeks to plotout the economic frontiers for pol-icymakers, businesspeople and

citizens. It is the product of more than 18 months’ workby CEDA’s expert authors, staff and a number of CEDAtrustees and advisors.

The authors come from a wide variety of institutions,businesses and government bodies. Yet their ideas meshat many points. Competing From Australia unites afamiliar theme in Australian economic history – thetyranny of distance – with a number of new ideas aboutglobal connectedness and innovation. It seeks to ensureAustralia continues to engage more deeply with the restof the world, and to stay at the leading edge of economicactivity. It points to Australia’s recent economic andpolicy successes, including some – such as our success inraising our foreign direct investment – that have gonelargely unnoticed until now. But it also asserts that thereremains room to improve our performance further.

This project once again underlines the strength CEDAgains from its membership and from many of Australia’sleading public policy thinkers. It gained early focus andinsight from a CEDA reference group which broughttogether a number of leading CEDA trustees and outsideexperts in late 2005. It was this group which first high-lighted the rising significance of global supply chains.

Many of our authors also collaborated at a SydneyRoundtable in 2006, and the project’s themes emergedfurther there. As always, we owe a great debt to ourauthors for their generous contribution of time andideas.

We are also indebted to CEDA’s Research and PolicyCommittee and our Research Director, Professor IanMarsh, for their work on the project. Professor GlennWithers, head of our ACT advisory council and oneof Australia’s most distinguished economists, deserves aspecial mention both for his contribution as an authorand for his intellectual guidance throughout the project.

The papers already released as part of Competing FromAustralia have been well received. A great manyAustralians clearly share CEDA’s goal: to find ways,through debate and discussion, to continue and accel-erate Australia’s economic development.

David ByersChief Executive Officer, CEDA

forewordforeword

4

1

CEDA GROWTH 58

summarysummary

At the start of the 21st century, world economic production is yet again transforming. Several factors previously regarded as minor are becoming rapidly more important: cross-firm collaboration, world-scaleproduction efficiency, integration into global supplychains dominated by multinational corporations, anddirect communication between team members located in the same office, city or region. The common theme isincreasing connectedness between different firms,between different locations, and between people.

These changes challenge Australia. Distance and scale,in particular, loom as issues for Australia.

It is often suggested that advances in telecommunica-tions are making distance and scale less important andconnectedness less of a challenge – that “distance is dead”and that, as one popular book has put it, the globaleconomic playing field is now “flat” or at least flattening.

5COMPETING FROM AUSTRALIA

However, recent economic theory and data suggeststhe opposite – that “the tyranny of distance” has notabated and will continue into the future, and thatAustralia cannot rely on technological advances alone totie us more strongly into the world economy.

Australia can, however, take advantage of industry andtechnological trends which minimise or avoid the effectsof distance and scale. Australia already appears to betaking advantage of skills developed in response toAustralia’s small domestic market size and distance frommarkets - most notably its strongly developed businessservices sector and its “generalist” skills such as the abilityto integrate existing components into systems.

To engage more closely with the evolving world econ-omy, Australia will also need to:

• maximise its ability to interact with world markets;

• excel at remote delivery, supply chain management andlogistics;

• foster innovation, particularly in so-called “traditional”industries, including those industries that rely on theresources sector;

• minimise communications and transport costs;

• continue to emphasise economic openness and flexibility;

• continue to build human capital, both through immi-gration and through investment in education and skills;and

• continue to support inward and outward foreign directinvestment as well as trade.

Australia cannot rely on technological

advances alone to tie us more

strongly into the world economy.

From 1968 to 1988 GEOFFREY

BLAINEY was first Professor of

Economic History and then Ernest

Scott Professor of History at the

University of Melbourne; in 1982–83

he was Professor of Australian Studies at Harvard University.

His 1966 book The Tyranny of Distance was a landmark account

of Australia’s economic evolution. His other books include Triumph

of the Nomads, a prehistory of Aboriginal Australia; The Rush That

Never Ended: A History of Australian Mining and A Short History

of the World.

6

It is fascinating to read the essays here and to see thatdistance more often than not is deemed to be importantas an economic factor. Some of these essays view thetyranny of distance as a continuing liability. Indeed, theMacro Dynamics Unit of the Australian Treasury –whose work on distance is cited by Glenn Withers in thisvolume – argues that it is “unlikely that the costs ofdistance can ever be completely overcome”.

2

CEDA GROWTH 58

dilemma

distanceeconomicA K E Y T O A U S T R A L I A’ S

distance

© L

OUI S

ESEL

JA

7COMPETING FROM AUSTRALIA

When I coined the phrase “the tyranny of distance” forthe name of a book in 1966, I did not foresee how thepithy phrase would travel. The phrase had a looseness, aslightly abstract air, and that looseness enabled it to beused widely, serving all kinds of purposes. On the otherhand, the imprecision in the phrase led easily to misun-derstanding, and sometimes the phrase or slogan wasmisused. For example, many commentators said that fora long period it was the “tyranny of distance” whichretarded the flow of new ideas to Australia. But my view– I could be wrong – was that distance had far moreeffect on retarding the flow of commodities and peoplethan of ideas. While observing and even apologising thatthe phrase gives rise to misunderstanding, it says – atleast in my view – something important about Australia.

In its first 20 years, the book was reprinted on averageonce a year, and gave rise to intense debate among histo-rians. Their interest was in chapter 2 and especially onmy argument that distance as a factor threw strong lighton why Australia was settled by the British in 1788.However, the book, did not have an impact on mosteconomists, partly because it was not speaking theirlanguage. Admittedly, the transport economists, like the

geographers, were pleased to annex the phrase “tyrannyof distance”, but my attempt to analyse the origins of thebreak of gauge in the railways, and that break’s con-trasting effects on the economy in the short term andlong term, was not widely read. In hindsight, there wasanother valid reason why economists did not worryabout the book itself. Most Australian industries andprofessions already knew in general whether distance wasimportant or not to their well-being. Many knew farmore about distance in their particular realm than Icould possibly know.

The general economists were less interested in distanceas a concept. Even the book’s latest updating in 2001,when I added more pages pointing out how distance wasstrongly affecting the increasingly prominent service

PHOTO: iSTOCK

Some of these essays view

the tyranny of distance as

a continuing liability.

8

sector of Australia’s economy, had little impact. To thebest of my knowledge, it was hardly commented onpublicly by anybody in the next couple of years. And yetsomehow the phrase itself still lived on. I am not com-plaining: the book and its central idea has had a longinnings.

An important part of the concept of The Tyranny ofDistance is still relevant, as at least half of the essays inthis collection maintain. Several vividly point to thescatter or dispersal of population within Australia, and toits adverse economic effects. Where else, they ask, willyou find such a distance between the major cities? Onemight also ask the pertinent question: where else – exceptmaybe Siberia and Canada – would you find such crucialnational industries operating so far from a major city?Fortunately, as pointed out in this volume, Australia pos-sesses one notable concentration or clustering ofpopulation, even if it is not an intensive cluster byEuropean, North American or East Asian standards.

Michael Porter’s book of 1990 The CompetitiveAdvantage of Nations, placed innovative emphasis on therole of clusters in driving economic development. Aversion of “clustering” was one of the themes of TheTyranny of Distance, though the word and the intricaciesof its economic mechanism were unknown to me. Thebook pointed out that in 1966 the core of Australia’seconomy and the heartland of its population extendedaround the coast and a narrow hinterland that ran all theway from Brisbane past Sydney and Melbourne andAdelaide to Port Pirie. I should have added Whyalla and,perhaps even then, the Sunshine Coast. I christened itthe Boomerang Coast because of its shape, and pointedout that it held less than one-tenth of the nation’s areaand less than half of the nation’s natural resources(which, in retrospect, was a very rough guess), and yet itheld eight of every ten people. Chapter 6 concluded withthe sentences:

Through the concentration of population on the BoomerangCoast, Australia spends much less of its energy in carryinggoods and supplying services over vast distances. Its standardof living and its ability to support a larger population aremuch higher than if its main economic activities and itspopulation had been scattered around the rim of the conti-nent. The Boomerang Coast, and the dominant cities onthat coast, were the simplest solution to the problem ofdistance.

Interestingly, in the last 40 years, with the proportion-ately faster growth of Western Australia and Queensland,the Boomerang coast is not quite so dominant.

Elsewhere, but not in The Tyranny of Distance, I coinedthe phrase “the mating of resources” in an attempt todescribe how in certain areas the juxtaposition or clus-tering of very different resources, side by side, conferredbenefits on each resource or economic activity. TheBallarat district was probably the most successful zone of

CEDA GROWTH 58

inland development in the whole continent up to 1900,largely because of this mating and multiplying ofresources. Much of that district’s poorer, gold-bearingdeposits might not have been extracted at a profit exceptfor the fact that the cost of living and the general miningcosts at Ballarat were relatively low. Thus, at Ballarat thetimber for the mine props and the fuel for the steamboilers and their huge pumping engines came in massivequantities from nearby forests. As the forests were near,the firewood and timber were cheaper. In turn, theclearing of the forests laid open fertile land to smallfarms, which in turn helped to provide cheap food; thefoodstuffs being the largest component of the cost ofliving and indirectly of the miners’ wages. The ring offarms around Ballarat made it even more of a regionalcentre and service city than a mining city by the 1870s,and the aggregation of engineering skills required by themines gave rise to foundries and other industries thatserved one of the first Australian cities to make steamlocomotives. This is a highly simplified version of acomplex process of interaction seen especially at Ballaratand Bendigo, but far less important at remote BrokenHill and Kalgoorlie, with their arid soils and remotenessfrom the coast.

In contrast, a characteristic of today’s huge miningindustry is that it rarely gives rise to the mating ofresources. The fly-in, fly-out workforce, and the smallpopulation of the actual mining fields, is the new trend.Fly-in is as much an effect as a cause of the economicinsulation and the lack of clustering benefits of the latestgeneration of mining fields.

The service sector, now the employer of about 75 percent of the labour in Australia, obviously depends on amating process. Its resource endowment is not gold orpasture or arable soil. To some degree its resource isknowledge and information, both low grade and highgrade, if you like to use mining terminology. Informationis one of the new gold rushes, and presumably obeysseveral of the same economic laws, of which the price oftransport is one. In other words, distance is one determi-nant of whether the new information technology willreally flourish, creating jobs and wealth in one town orregion rather than another, or in one nation rather thananother.

It is understandable that alert

observers should argue that in the

last ten years the world has shrunk,

that distance is no longer decisive.

Is distance, once such an obstacle, now less important?It is understandable that alert observers should argue thatin the last ten years the world has shrunk, that distance isno longer decisive. Thomas Friedman’s book The Worldis Flat has won a vast audience for this proposition.Slightly earlier, Rupert Murdoch, with an almost unpar-alleled knowledge of the new and old media, announcedthat “the tyranny of distance” – this was the phrase heused – was dead. In 1997, in the UK, Frances Cairncrosscompleted an illuminating book, The Death of Distance,which predicted that the decline of distance will“probably be the single most important force shapingsociety” in our time. Part of what these trans-Atlanticobservers have predicted will probably occur. In thesemomentous times, numerous barriers are toppling. Whatthe observers don’t say, or say less emphatically, is that innearly every momentous change there are losers as well asgainers, and that certain nations, industries and citiesgain far more than others.

9COMPETING FROM AUSTRALIA

Many go-ahead observers insist that

… distance is dead. But Australia,

a first-rating testing ground of this

theory, seems to prove otherwise.

Is Australia a loser, relatively? The view of some distin-guished economists writing in this volume is thatAustralia in recent years has suffered because of distance– and the relative weakness of its economic clusteringinside the country. Perhaps because Australians have tra-ditionally been conscious of distance they are quick tonotice what their nation gains from the new communi-cations technologies and their assault on distance. Wethink we are gaining, compared to rival nations, in mostfacets of the assault, but maybe we are not. Australiagains much from, say, the communications revolution –mobile phones are almost an infection – and rejoices inthe visible effects. But its comparative economic gainfrom this network of allied industries, with their vastramifications, is perhaps not as large as the gains made bysome other countries with specific geographical advan-tages. According to Professor Houghton, “On many ofthe indicators of globalisation, Australia scores relativelylow”, and this applies especially to global productionsystems. One of the intriguing statistics cited in theseessays is that between 1995 and 2003, Australia’s share inthe world’s total export of services fell by 13 per cent.And yet that statistic is not easily analysed. Such majoreconomies as Italy, France and Japan experienced evenlarger falls in their share of service exports.

Many go-ahead observers insist that, in the era of theInternet and satellite, distance is dead. But Australia, afirst-rate testing ground of this theory, seems to proveotherwise.

10

Australia’s recent economic performance has been, onmost measures, outstanding. After such a protractedperiod of exceptional results it may seem churlish tobegin searching for new ways to speed up growth. But itis arguably best to search for new policy improvementsbefore medium-term economic growth slows. Seasonedobservers, notably the Governor of the Reserve Bank,have wondered out loud if there is not the need for a newimpetus.1 Saul Eslake, Chief Economist of the ANZBank, has been more explicit. He has charged the gov-ernment with wasting the windfall revenue gains fromthe resources boom. The Economist recently concluded:“Without further policy reform, the Australian kangaroorisks turning into a sleepy koala” (31 March 2007, p. 74).

3

CEDA GROWTH 58

PROFESSOR IAN MARSH is CEDA’s

research director and holds the

ANZSOG Chair of Public Manage-

ment at the University of Sydney.

Former appoint-ments included the

Research School of Social Sciences, ANU and the Australian

Graduate School of Management. He has also worked as research

director for the Liberal Party Federal Secretariat and as a

consultant with McKinsey & Company. His recent books include:

Globalisation and the People (2007); Into the Future: The Neglect

of the Long term in Australian Politics (2006), and Democracy

Governance and Regionalism in East and South East Asia (2006).

generationgenerationpolicy

A NEW

questions

OF

11COMPETING FROM AUSTRALIA

This year’s World Competitiveness Yearbook 2007 alsoemphasised Australia’s long-term economic developmentchallenge. Out of 55 countries, Australia scored poorlyon a number of economic infrastructure measures,including Internet costs (42nd), mobile telephone costs(38th) and availability of various types of skilled labour,such as qualified engineers (40th). It ranked only 12thfor education, 20th for scientific infrastructure and 21stfor technological infrastructure. Overall, Australiaranked 16th on economic infrastructure, just up from2006’s 17th position.

The need to renew Australia’s economic reformprogram was emphasised in CEDA’s earlier studies ofInnovating Australia (Growth 53) and Infrastructure –Getting on with the job (Growth 54). These reviews sug-gested that the current microeconomic reform agendahas realised the majority of its potential gains. Most ofthe policy changes associated with deregulation havebeen implemented – indeed, our recent performance tes-tifies to their cumulative impact. But different, oradditional, policy frameworks have been adopted inother relatively small, resource-intensive and openeconomies, such as Denmark, Sweden and Finland, and

their economic performance has equalled and, morerecently, surpassed, that of Australia. To the extent thatpolicy influences outcomes, it is hard to argue thatAustralia’s current strategy is the only or the bestapproach – or that it exhausts what might be done.

This consideration is reinforced by the papers in thiscurrent collection. Save for one contributor, they alladvocate a renewal of policy reform. However, their rec-ommendations vary. They approach the need for a freshpolicy effort from three overlapping (and potentiallycomplementary) perspectives: one perspective draws onthe features of our general economic circumstances,including new interpretations of the “tyranny ofdistance” and the recent deterioration in our export per-formance; a second approaches the need for new policyeffort from the perspective of innovation; and a third istaken from the perspective of the role of MNCs in globaltrade and R&D.

Deregulation and micro-economic reform involvewhat might now be seen as the first wave in the interna-tionalisation of the Australian economy. But they do notend the story. This first phase was powerfully based on

PHOTO: iSTOCK

12

paradigms drawn from neo-classical economic theory.The basic idea was that domestic and internationaleconomic arrangements should, as much as possible, useunfettered markets. In this perspective, exchange andcoordination are best achieved through arm’s length pricemediated transactions. Some also argue that this is thebest path to growth and dynamic efficiency. And someargue that, even in cases of market failure, interventionsby governments are likely to produce third-best or worseoutcomes. This is because of the risk of relevantprograms being captured by favoured interests. Australia’srecent success in rolling back protectionist and other reg-ulatory frameworks would seem to call this latterargument into question, at least as an unqualified gener-alisation.

More generally, in a neo-classical perspective, marketforces will drive down costs to an economically efficientlevel and market exchanges will allocate resources andpeople to their most productive uses. In Australia’s case,the elimination of tariffs, the floating of the exchangerate, the introduction of a vigorous competition regimeand, most recently, labour market reform, have all drawnon this theoretical tradition. Of course, the idea thatmarket signals could carry the entire policy load wasacknowledged as a gross simplification even by themarket-oriented reformers of the 1980s and 1990s. Inpractice, market failure was widely acknowledged. Inresponse, a variety of subsidies and incentive paymentshave been maintained. On some issues, coordination ofactivity or allocation of scarce resources has been orches-trated through governance rather than markets.

Transaction costs were also recognised as a criticaldeterminant of performance, costs that are often no lessimportant than direct production costs. Hence wide-spread programs of privatisation and commercialisationwere introduced, particularly involving public utilities.In general, Australia’s transformation in the post-1983period was a remarkable episode of national policychange. In just over a decade, policies, frameworks andapproaches that had guided national economic develop-ment broadly since 1909, were completely jettisoned.

Unfettered markets remain critical in efficient resourceallocation and ensuring that competitiveness is nothobbled by transaction costs. But other approaches meritassessment at this point in the reform process. Concernover Australia’s level of global engagement is just onefactor driving a fresh look at policy. Another factor is thepotential shift in industry structure that will result froman extended period of high commodity prices, a shiftexplored in a notable recent speech by Treasury SecretaryKen Henry2.

In addition, theoretical perspectives that complement,and in important respects qualify, the neo-classicalapproach to “best” strategies for building performancehave also emerged in recent years. They offer grounds forthinking about policy needs, instruments and settings

that encompass, but extend beyond, market failure.Because some grounding assumptions cut across those inthe neo-classical framing, these newer paradigms presentparticularly acute problems of assessment and evaluation.One perspective involves the international economy –and argues for the importance of multinational corpora-tions (MNCs) as primary gatekeepers in theinternational trading system. This analysis, based inpolitical economy, notes that some two-thirds of worldtrade passes through MNCs, either directly or via supplychains. These transactions are far from the textbookmodel of arm’s length, price mediated exchanges.Further, approximately one-third of private R&D is con-ducted by MNCs. States can seek to create infrastructuresand capabilities to attract this activity in the same way asthey now seek to entice MNC investment.

The second more recent theoretical paradigm concernsinnovation – and recognises the role of collaboration andlinkage in driving superior performance at the firm level.This framing holds the potential to change a number ofcurrent approaches to economic management (see e.g.Lipsey, Carlaw & Bekar, 2005). Innovation strategy inAustralia is currently primarily based on a linear, science-push conception of the process.3 This continues to berelevant. But science-based industries account for a tinyproportion of overall economic activity, generating pro-portionately very little employment or investment. Theyremain small proportions even of economies such as theUnited States, where high-tech sectors are largest andmost robust. In fact, most innovation occurs in estab-lished manufacturing and service industries.

The most challenging aspects of innovation theoryconcern the role of the state in facilitating upgrading andcontinuous knowledge development in these establishedareas of activity. There is at least one classic and home-grown example of this approach, involving the Australianwine industry. As its performance illustrates, collabora-tion around knowledge development can yield outcomessuperior to those available from the operation of marketforces alone, with the important proviso that this needsto work with the grain of markets. But the very successof this industry invites attention to the unique capabili-ties and knowledge infrastructures it has developed, andto the contribution of federal and state governments tothese outcomes.

All three segments in this collection of papers raisefresh questions about the strategic and catalytic role ofgovernments in facilitating economic activity. As already

CEDA GROWTH 58

Concern over Australia’s level of

global engagement is just one factor

driving a fresh look at policy.

13COMPETING FROM AUSTRALIA

noted, those in the first part propose a new salience forcommunications, transport and educational strategiesand for export development. Meantime the papers con-cerned with innovation and MNCs present, if anything,deeper challenges to current policy settings. All theseissues are currently being considered by Australia’s federaland state governments – with, it must be said, conspicu-ously variable energy. This collection asks if theirsignificance and/or implications are being adequatelyrecognised.

The first part of this collection looks at the implica-tions of the recent deterioration in aspects of oureconomic performance. In particular, the impact of geo-graphic location on trade performance and theimplications of recent developments affecting theexternal account are explored. A recent Treasury reviewsuggests that, allowing for the impact of distance,Australia’s export performance in manufactures andservices is actually above what might have been expectedfrom a country of our economic size and geographiclocation. Glenn Withers endorses this approach and citeswork that suggests the impact of distance, far fromdiminishing, is actually rising. This licenses fresh atten-tion to policy settings. In deciding what strategies areappropriate, Withers suggests we need look no furtherthan those which framed the very high levels of pros-perity that marked the latter part of the nineteenthcentury:

It is little known and little understood that Australia’searlier achievement as world’s best practice by 1890 sprangnot just from the luck of possession of natural resources. Itwas also the result of having the most skilled, educated andurbanised work force in the world and the most innovativepopulace. Australia spent more on education across more ofits people than any other country; it chose its migrants care-fully for their skills and it had the highest per capita patentsof any country.

The need now is to augment the policy framework.Withers suggests a wide-ranging agenda aimed at aug-menting human and knowledge capital. Attention tocommunications technologies and transport corridors isalso an imperative. More generally, domestic fertility and

skilled migration both need to be emphasised. Family-friendly policies that allow women (or men) to linkcareer and family development need to be instituted.

In the second paper, John Edwards presents both acomprehensive assessment of recent developmentsaffecting Australia’s trade and investment and an evalua-tion of their longer-term policy implications. In anutshell, Australia has done poorly at lifting its exportperformance since 2000, but Australian companies havedone very well at integrating themselves into the globaleconomy through foreign direct investment. His assess-ment of recent developments involves a detailed analysisof trends in the various categories of goods and servicesexports.

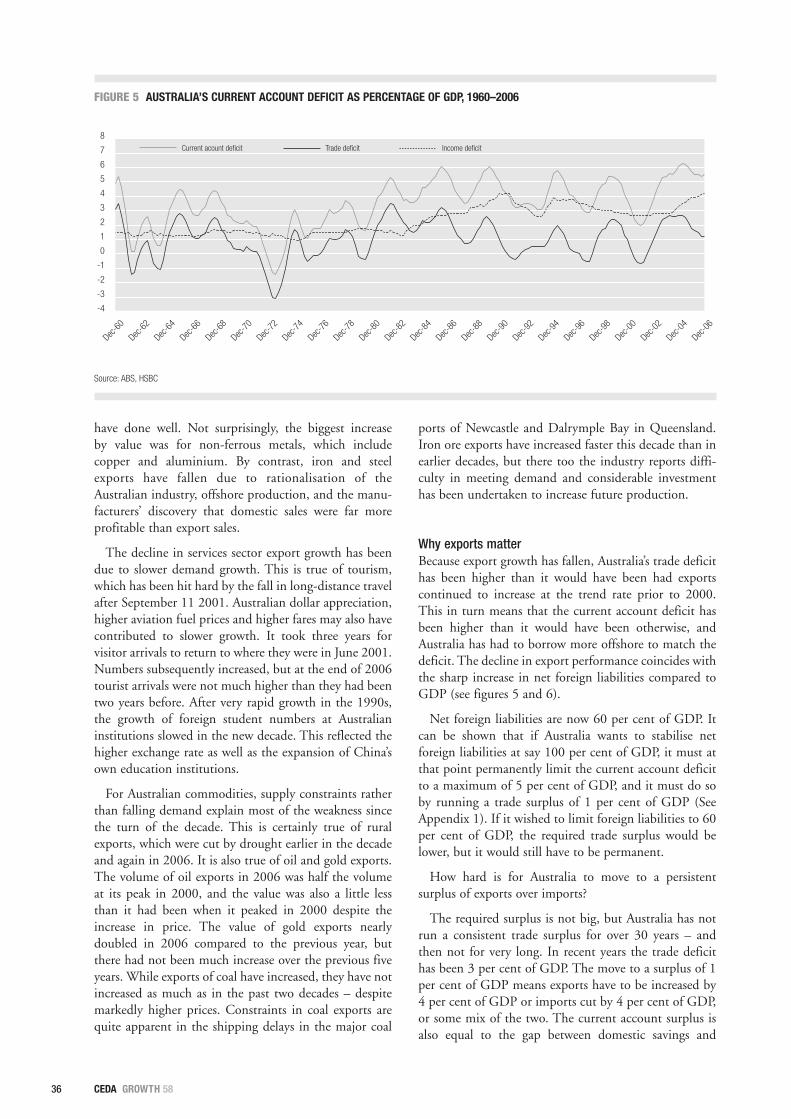

Export volumes grew by 56 per cent in the six years to2000. Since 2000, they have grown by just 9 per cent –a remarkable and unexpected slowdown. Most of theslowdown in export volume growth is due to thedownturn in the rate of growth of rural exports, oil,metals, gold, and services, including higher educationand overseas tourism. Roughly half the decline in the rateof growth is attributable to a decline in the rate of growthof minerals, metals and energy exports, a decline dis-guised by rising prices for key commodities, notably ironore and coal.

How can Australia improve its export performanceagain? While overseas demand for education and tourismhas had some impact, Australia’s challenge in areas suchas metals, energy and minerals is to improve its ability tosupply. While the mining investment boom in the threeyears to 2006 will likely result in higher export volumesin coming years, supply constraints are a relatively newchallenge for Australia. We need concentrated effort toremove infrastructure bottlenecks; to build additionalinfrastructure to meet expected demand; to educate,train and retrain Australians so as to increase the supplyof skilled workers; and to support innovation.

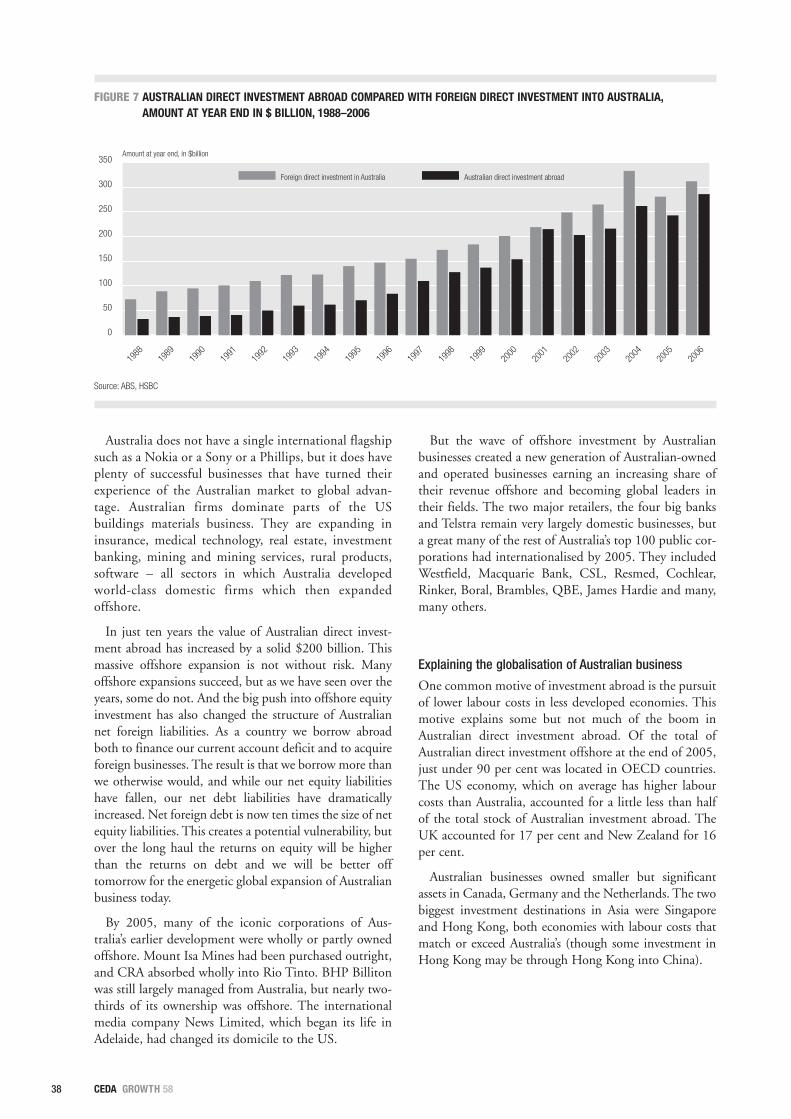

While export volume growth has flattened, exactly theopposite has happened to Australia’s outward directinvestment. Australian foreign direct investment (FDI)abroad has almost caught up with FDI in Australia.

Why has this happened? The typical Australian firminvesting offshore is one that has been successful inAustralia but outgrown the relatively small home market.Offshore investment reflects specialisation rather thansize. The typical successful business has intellectualproperty, marketing and management skills and abusiness concept that has been successful in Australia andcan be replicated elsewhere.

The second part of this collection explores themeaning and policy implications of innovation. This partconsists of three papers. Roy Green introduces the dis-cussion. He provides an overview of this activity, whichessentially entails the application of knowledge and cre-ativity to add value to products and processes. Higher

… Australia has done poorly at

lifting its export performance since

2000, but Australian companies

have done very well at integrating

themselves into the global economy

through foreign direct investment.

14

resources income, such as that delivered to Australia bythe rise of China, can be dissipated in sustaining currentprosperity – or used to enhance longer term economicsustainability. Green suggests that Norway and Finlandhave adopted approaches that do the latter, and heproposes that Australia learn from their experience. Atthe most general level, this requires much more invest-ment in human knowledge and infrastructure – both ofwhich have declined in recent years in Australia.

In categorising the scope of innovations, Green distin-guishes between “sustaining” (or incremental) and“disruptive” change. In each of these major categories,innovation could involve one or a combination of threeelements: technological change, organisational changeand institutional change. Meantime, much currentpolicy in Australia is concentrated on disruptive change(via science-based conceptions of innovation) and aimedonly at its technological dimension. This remains impor-tant, but it is far from the whole story. Australia’srelatively low spending on business R&D is often attrib-uted to the high proportion of low-tech industries in ourindustry structure. Green disagrees, arguing that “… thisjustification ignores the importance of R&D in miningand agriculture, and of innovation more broadly in ‘low-tech’ activities and services, where ‘absorptive capacity’for externally sourced technologies and skills may be thedriver of competitive advantage …”. He notes that onthe broadest possible definition only 35 per cent ofAustralian firms acknowledged making an innovation inthe 2001–03 survey period.

Drawing on a global survey, Green explores the lesswidely recognised role of organisational and institutionalinnovations. The importance of institutional stimuli toinnovation is emphasised in a recent IBM survey:“Extensive collaborators outperformed the competitionin terms of both revenue growth and average operatingmargin.” Green concludes with a detailed review ofAustralia’s innovation system. He emphasises that inno-vation is naturally not a task for governments alone. Buthe notes the lamentable decline in public spending onhigher and vocational education, despite politicalrhetoric vaunting individual skills and capabilities. Morebroadly, and at a strategic level, he laments the absence inAustralia of any overarching commitment, conceptuali-sation or vision. Government has failed to lead thedevelopment of public or stakeholder opinion. Becauseimplementation requires extensive new linkages andengagements between public and private sector actors, heargues, government has an unavoidable and quite novelleadership role in the innovation field.

In the second paper in this group, Keith Smith outlinesthe framework for a comparative study of approaches toinnovation in a number of resource-intensive economies.These are countries which all resemble Australia in theimportance of their resources sector, but which all have ahigh resource dependence associated with strong manu-facturing and/or services activity. Indeed, some of therichest and/or fastest growing economies are resource-based – Norway, Sweden, Finland, New Zealand,Canada, Australia and the Netherlands. This is incontrast to an influential strand of economic theory thatargues natural resource endowments can be a “curse”.

This “resource curse” is said to arise as a result ofimpacts on the exchange rate, precluding the develop-ment of other activities. However, Sweden, Finland andthe Netherlands, all resource-intensive economies, havealso all developed high-tech sectors that have supple-mented their much more extensive engagement in low-and medium-technology activities, allowing them toremain high-productivity nations.

In explaining this achievement, Smith focuses on howimpacts from initial resource developments ramifiedserially through three broad phases: initially, there wassignificant investment in knowledge upgrading inresources-based industries, followed by other flow-onconsequences as resource activities leveraged the develop-ment of downstream industry and services. In a thirdphase, a further round of opportunities developed fromthe extensive and deliberate use of knowledge infrastruc-tures to drive knowledge creation in other sectors. Smithrefers to the development of “vertical clusters” extendingup out of the resources sectors into manufacturing andservices. Smith concludes that if the detailed path bywhich the cited resource-rich countries progressivelytransformed their natural endowments into vibrant sec-ondary and tertiary sectors remains obscure, so too is thepath by which these outcomes might be preserved andmagnified. These questions – and processes – havespecial salience for Australia.

The third paper in the segment on innovation is byThomas Barlow. He reviews recent changes in policyframeworks designed to aid innovation. To highlighttheir impacts, he also reviews data about relative changesin Australia’s business structure. This emphasises thegrowing importance of services in the Australian

CEDA GROWTH 58

At the most general level, this

requires much more investment in

human knowledge and infrastructure

– both of which have declined in

recent years in Australia.

15COMPETING FROM AUSTRALIA

economy with property and business, finance and insur-ance and communications services all growing at muchfaster rates than manufacturing. This also partly reflectsthe very substantial new linkages between manufacturingand services. Barlow then turns to consider the patternsof innovation actually occurring in Australia. He arguesthat our characteristic approach (and strength) involveswhat he terms “systems integration”. This involves “astyle of innovation that is relatively high level, that is typ-ically generalist rather than specialist, that is focused onsystems rather than products, and that involves combi-nation and modification of existing technologies ratherthan the creation of new technology.”

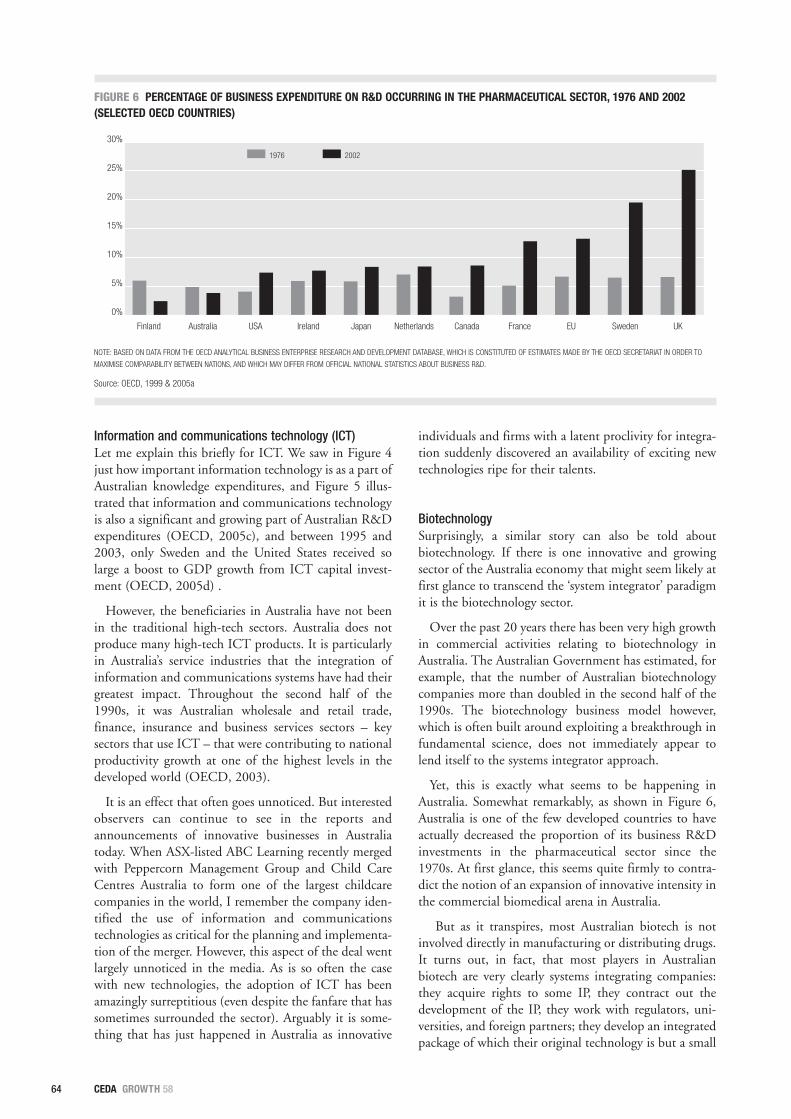

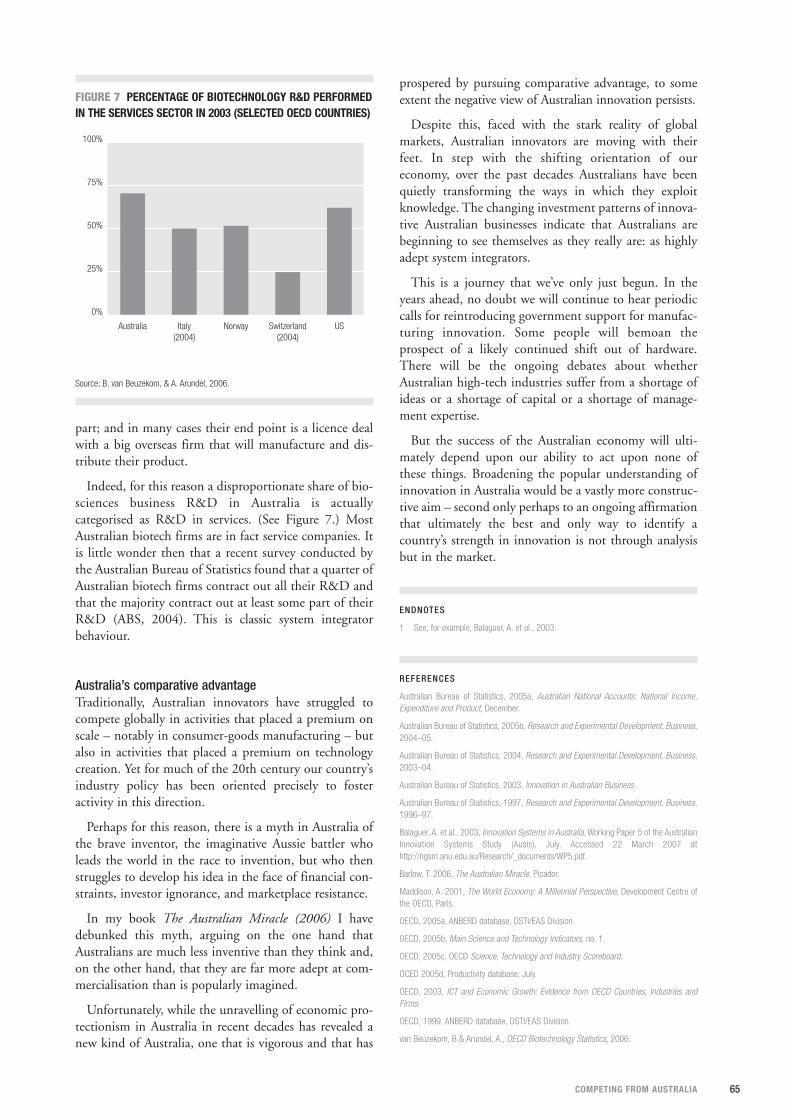

Evidence for the predominance of this approach is tobe found in fields as diverse as mining, construction andevent management. A practical example in yet anotherarea is Westfield’s success in shopping malls. In all ofthese cases the “product” is different in each version, buta creative solution, based on systems integration, is thecommon element everywhere. Barlow points to thegrowing place of software expenditure in Australia’s totalbusiness R&D spend as further evidence of this shift inAustralia’s characteristic approach. Indeed, informationand communications technology (ICT) developmentsprovide a particularly strong reinforcement of the thesis.Between 1985 and 2003, only Finland and Koreashowed a greater increase in ICT as a proportion of grossfixed capital formation. The beneficiaries of this invest-ment in Australia have been wholesale and retail trade,finance insurance and the business services sectors.System integration also characterises the approach ofcompanies in fields such as Australia’s growing biotech-nology sector.

Barlow argues at more length elsewhere that he seesthis as the characteristic strength of Australians in theirapproach to innovation.4 And, contrary to other contrib-utors in this collection, he concludes that whereinnovation is concerned, current policy settings are aboutright and further effort is best left wholly to decisionsmade in the marketplace.

The final group of two papers considers the role ofMNCs, both as integrators of international productionsystems and as the predominant patrons of R&D.Andrew McCredie introduces the discussion byreflecting on their global role, as well as on the engage-ment in trade by Australian firms. MNCs undertaketwo-thirds of world trade. The top 1,000 MNCs direct90 per cent of FDI and they undertake the bulk of worldbusiness expenditure on R&D. They have adopted newbusiness models which need to be factored into policythinking. According to Marc Singer (a Principal inMcKinsey’s Silicon Valley office):

In the industrial age companies were built on the principle:“Do more and do it cheaper.” The means were vast scale andscope as well as rapid internal control. In the informationage the watchwords are “fewer, faster, less” – fewer assets,faster growth, and less activity managed under one roof.These are the features of the networked organisation, abusiness model that may forever change the way companiescompete … Brought into existence by declining transactioncosts, tightly linked supply chains, and Internet-basedordering platforms, these companies have devised a mode ofinteraction among themselves, their business partners andtheir customers that promotes … collective learning in theorganisation, especially how to coordinate diverse produc-tion skills and to integrate multiple streams of technologies.5

These linkages, while geared to cost reduction as in theToyota “learning by doing” buyer–supplier model, arenevertheless far from the arm’s length, price mediatedexchanges of the international trade textbooks.6

McCredie illustrates the new patterns of outsourcingwith examples from the vehicle and constructionssectors. He argues that, for a country of our economicsize, relatively few companies are engaged in trade. Forexample, only just over 4,000 companies exported morethan $1 million of goods or services in 2005–06. Hefurther suggests that Australia’s distance from majorglobal centres is no ground for complacency. In decidinghow to develop trade, policy needs to focus on the role ofMNCs in both global trade and R&D. The structure ofAustralian industry is also a pertinent fact: Australianindustry is dominated by SMEs, which may lack theability to respond as needed to MNC demands.

In relation to R&D, he notes that major MNCs areestablishing research nodes where they find complemen-tary research or other capabilities, or where these cancontribute to longer term market access and develop-ment. According to a 2005 UNCTAD survey, Australiais ranked 16th out of 26 countries as a location for MNCR&D activity. As a prospective location its ranking hasfallen a further two places to 18th. Such perceptions arelargely socially constructed. Others are deliberately tar-geting R&D. This does not currently figure in Australia’spolicy repertoire.

… our characteristic approach

(and strength) involves what he

terms “systems integration”. This

involves a style of innovation that

is relatively high level, that is typically

generalist rather than specialist …

16

McCredie also explores the significance of Australia’sincreasing offshore FDI. He notes that were the incomefrom these investments to count as an export, it would bethird only to coal and iron ore. He concludes with aseries of policy recommendations, starting with an effortto build understanding and overcome information defi-ciencies among MNCs. The large number of MNCsalready located in Australia provide a primary potentialsource of intelligence about the requirements for con-necting local firms to their international parent supplychains. A similar intelligence opportunity exists inrelation to attracting R&D. Similarly, Australian firmsneed to be encouraged to see supply to global chains as apath for business growth. Programs may be needed todevelop capabilities for and reduce the risks of theseengagements. Finally, Asia may present special opportu-nities. The number of regional MNCs is multiplying andthere would appear to be many potential complementar-ities between Australian capabilities and their needs. Butonce again, more intelligence and a deliberate strategymay be required.

The final paper, by John Houghton, also explores thechanging role of supply chains in the global economyand the requirements for enhancing the participation ofAustralian firms. His analysis reinforces that of AndrewMcCredie. MNCs now dominate trade and their globaloutsourcing creates a new context for firms seeking togrow through international engagement. Houghtonreviews trade data that not only illustrates Australia’s rel-atively poor trading performance but also suggests thescale of the disconnection between local manufacturesand services and global supply chains. The metricsinclude trends in our share of IT-enabled servicesexports, intra-industry trade as a share of total manufac-turing trade, Australia’s share of foreign R&D locations,and trends in export market shares for both goods andservices. In all these cases we rank in the lowest deciles.Echoing the judgements of other contributors to this col-lection, Houghton concludes that our potential as agoods and services exporter depends above all on thedevelopment of education and skills, ICT infrastructureand on the ability of local suppliers to link into globalproduction systems and offer appropriate cost-effectivesolutions.

In general, the contributors to this collection urge thefurther development of government policies aimed atincreasing the international engagement of Australianfirms. The policies they variously propose pose challengesof varying degrees of difficulty. The proposals to buildeducation and training investment, lift communicationslinkages and emphasise export development, importantand far-reaching though they are, present the fewest dif-ficulties. All these recommendations are consistent withcurrent policy frameworks and approaches. They wouldrepresent a realignment of priorities and involve morespending, but they do not present any fundamental chal-lenge to overarching orientations.

Proposals to deliberately foster the links betweenAustralian firms, particularly SMEs, and MNCs involvea higher order of policy difficulty. This would represent aconsiderable extension of present approaches.

However, innovation as discussed here represents themost challenging of all these proposed fresh approaches.Currently national government strategies are largelyfocused on a science push view of this activity. The chal-lenge of adding a substantial demand-driven componentthat is focused on established services and manufacturingsectors is far from trivial, and far from a simple extensionof current approaches. It could involve such higher orderactivities as formulating a general vision that is ambi-tious, plausible and capable of inspiring effort. It couldinvolve a variety of sectoral activities that might be stim-ulated by governments but realised through relevantindustry associations and/or groups of firms. Forexample, clusters of firms might be encouraged to setgoals and targets, but in a frame that allows revision andadaptation as experience accumulates and contingenciesunfold. In other words, it would involve engagements ata sectoral level that cuts across present hostility to selec-tive interventions and discriminatory approaches. Butthe forms of engagement would also be novel – based oninformation and incentives to identify opportunities andto set ambitious goals and targets and reward designatedachievements rather than non-discriminatory regulatoryor financial inducements.

Such activities pose considerable challenges both to thestate and to business. For business, collaboration can bevery complex and demanding to establish. For the publicsector, the risks of capture would need to be deliberatelycountered. Fortunately there are abundant examples ofsuccessful approaches in other states. Perhaps the biggestchallenge concerns the degree to which such approachescut across current orthodoxies about the role of the stateand the relationship between public and private sectorswhich are championed by Australia’s political andbureaucratic elites. Concepts of partnership and collabo-rative engagement are currently generally discounted.They are the exception. Similarly, while ministers gestureto “joined up” approaches, practice shows only a fewexamples of effective concerted effort. Evolved forms ofinnovation strategy explicitly take account of the linkagesbetween industry policy and education, migration, com-munications, infrastructure and social policy. Suchholistic approaches are barely evident in the Australianpolicy system and, particularly where there is overlapbetween federal and state governments, often thwartedby make-believe political combat.

In other words, the adoption of innovation policies asenvisaged by some of the contributors to this volumewould represent at its furthest not just the evolution ofcurrent approaches, but a major shift towards a moreactive industry policy. As noted in the earlier papers,appropriate approaches are well developed in other coun-

CEDA GROWTH 58

17COMPETING FROM AUSTRALIA

tries, notably the Nordic block. However, policy transferis never merely straight copying and is always problem-atic – local conditions and circumstances, includingpolitical factors, necessarily obtrude. This is as it shouldbe.

In sum, the challenge in re-crafting Australia’s policyframeworks to lift international economic engagement toa new level could be unpacked in several different ways.The possibilities extend from shifting to new prioritieswithin present broad orientations to the adoption of newpolicy approaches, instruments and settings. Theachievements of the past couple of decades show whatdetermined and focused leadership can accomplish. Thenext phase, whatever its components, requires a renewalof motive and energy, and a fresh engagement with goals,means and purposes.

ENDNOTES

1 Evidence, 21 February 2007, House of Representatives Committee on Economics,Finance and Public Administration.

2 Managing Prosperity, Speech to the National Economic and Social Outlook Conference,2 November 2006.

3 Marsh & Edwards (2006) review the Innovation Summit as an exercise nominally posi-tioned as an assessment of alternative conceptions of ways to promote innovation.They conclude this was ultimately an elaborate exercise in outreach, basically designedto legitimise largely pre-determined positions. This has since locked Australia’s inno-vation strategy into a linear, science-push view of the process.

4 Barlow, 2006.

5 Singer, M., 2001.

6 See also Charles Sabel, 1994, Learning by monitoring: the institutions of economicdevelopment, in N Smeltser & R Swedborg (eds) Handbook of Economic Sociology,Princeton University Press, New Jersey.

REFERENCES

Barlow, T. 2006, The Australian Miracle: An Innovative Nation Revisited, Picador Pan-Macmillan, Sydney.

Lipsey R., Carlaw, K. & T. Bekar, 2005, Economic Transformations: General PurposeTechnologies and Long Term Economic Growth, Oxford: Oxford University Press.

Singer, M. 2001, “Beyond the unbundled corporation”, The McKinsey Quarterly, No. 3.

Smith K. & I. Marsh, 2007, “Wine production and economic development: Technological andmarket dynamics of the Australian wine industry”, International Journal of Technology andGlobalisation, Jan–Feb.

18

IntroductionTwo well-known books encapsulate much that is partic-ular to the challenges facing Australia today: DonaldHorne’s The Lucky Country and Geoffrey Blainey’s TheTyranny of Distance. Both titles have become part ofthe Australian lexicon and are keys to our sense of selfas a nation.

Horne’s phrase evokes in the minds of many thebounty of Australia possessing a continent rich in naturalresources, some of which comprise a large share indeedof the global resource endowment.

The continent has over 20 per cent and, in some cases,much more of the world’s known stock of recoverableuranium, iron ore, bauxite, diamonds and mineral sands.Proven black coal resources have centuries of life atcurrent extraction rates and millennia for brown coal.The land currently occupied by mining is 0.01 per centof the land area.

PROFESSOR GLENN WITHERS, AO,

is Professor of Public Policy at the

Crawford School of Economics and

Government at the Australian

National University. He works on

applied microeconomics, public economics, public policy and

administration, population policy and cultural economics. He

headed the Federal Government’s Economic Planning Advisory

Commission in the mid-1990s and has advised federal and state

governments, COAG, the Business Council of Australia and the

OECD. He is CEDA’s ACT president and a member of its Research

and Policy Committee.

4

CEDA GROWTH 58

distancedefeated?distance

BE

can

19COMPETING FROM AUSTRALIA

Australia’s relatively small population means that thisbounty can be shared and can support a good living,thanks to the fortune provided by nature and by isola-tion. Recognition of such a sentiment was reflected inthe Prime Minister’s recent comment on dealing withclimate change, that “we have to make sure that we do itin a way that preserves our natural advantages becausefuture generations will not thank us for squandering anatural advantage providence has given us”.1

Isolation is Blainey’s theme. The continent is geo-graphically separated from the historic centres of majorhuman population or, as Paul Keating once put it morecolourfully, “Australia is at the arse end of the universe”.(Some might say Keating’s comment neglects NewZealand and Tierra Del Fuego, but the point is clear.)Isolation is not just literal physical geography but also amatter of economic mass – and the most prosperous andpopulous are elsewhere. Canberra is 16,500 kms fromBonn, 16,000 kms from Washington, and 6,000 kmsfrom Tokyo, even in our own Asia Pacific region.

According to some historians, Australia may have hadan indigenous population of half a million before whitesettlement. Noel Butlin 1983) suggested this was amassive underestimate; in his view the number was morelike one million. However, disease (and not the frontierviolence that has so occupied the culture war historians)decimated this native population, leaving only 250,000

indigenous Australians by 1815 supplemented by 15,000Europeans; a tiny population for a continent of 3 millionsquare miles. Almost 200 years later the indigenous pop-ulation has risen back to half a million and the totalpopulation has passed 20 million.

Global integrationOne consequence of nature’s bounty has been a long his-torical reliance upon natural, resource-based exports as amajor component of Australian trade, as shown in Figure1. Wool, gold and other minerals alone have never beenless than 30 per cent of total Australian exports, puttingaside the years of war and depression.2 The reliance hasvaried over time and manufacturing and service exports(including sectors such as tourism and education) haveexpanded. But the natural resource base has remainedcrucially important and, in circumstances, such as therecent period of commodity price boom in response toChina’s fast growth, has accelerated to assume renewedprominence. And we have used our resources most efficiently, showing much higher labour productivity in these areas than comparable countries such as theUnited States.

The implications of bounty and distance for Australia’sgrowth, structure and stability are profound. How werespond to this bounty determines whether we continue

PHOTO: iSTOCK

20 CEDA GROWTH 58

as one of the group of countries to escape the “ResourceCurse” (Smith 2007). So many countries rich in natural,resource-based products have not used their bounty welland have suffered restricted growth. But countries suchas Canada, Australia, and Norway have developed asaffluent and stable democratic societies. Whether weshould have done even better is open for debate, but theneed to ensure that resource wealth flows are not wastedin the manner of the Spains and Portugals of centuriesago or some of the mid-East, African and SouthAmerican oil countries of modern times remains a policypriority.

The priority is recognised somewhat in Australiathrough the structural impacts associated with what localeconomists call the “Gregory Thesis” or, as it is calledelsewhere, “The Dutch Disease”. The exchange rateeffects of bountiful natural exports inhibit competitivemanufacturing and service exports and raise importcosts, so placing pressure on urban living standards andemployment.

Australia was the world’s first post-industrial society.Most industrial countries went through a major period oftransition from land-based production for domestic con-sumption, though a manufacturing revolution and thegrowth of urbanisation, to emerge as service societies. Inthis process, cheaper manufactures elsewhere undercutbasic domestic manufacturing, which then remainedwith specialised high-value-added niches. Australia wasreally born modern; a society that never possessed alanded peasantry, thoroughly urban from foundation,with well-constructed institutions of modern liberaldemocracy, the rule of law and efficient administration.

Its distance from markets meant that its naturalresource advantages dominated its global trade and notbasic manufacturing, which only really grew when force-fed by artificial protection. There is clear evidence thatapart from the costs of transport, which for Australia arelarge, there are also considerable advantages to scale inmanufacturing compared to most natural resource indus-tries. Figure 2 shows this clearly from recentinternational research (Antweiler & Trefler 2002) onscale advantages in global trade. And Blum and Leamer(2000) have further estimated that exporting a good to acountry 1,500 kms away is, on average, equivalent to animport tariff of between 7 and 17 per cent, depending onthe type of good. Or, to put the problem differently, ifAustralia was as close to other economies as is the UK, itstrade would be 50 per cent higher (Battersby & Ewing2005).

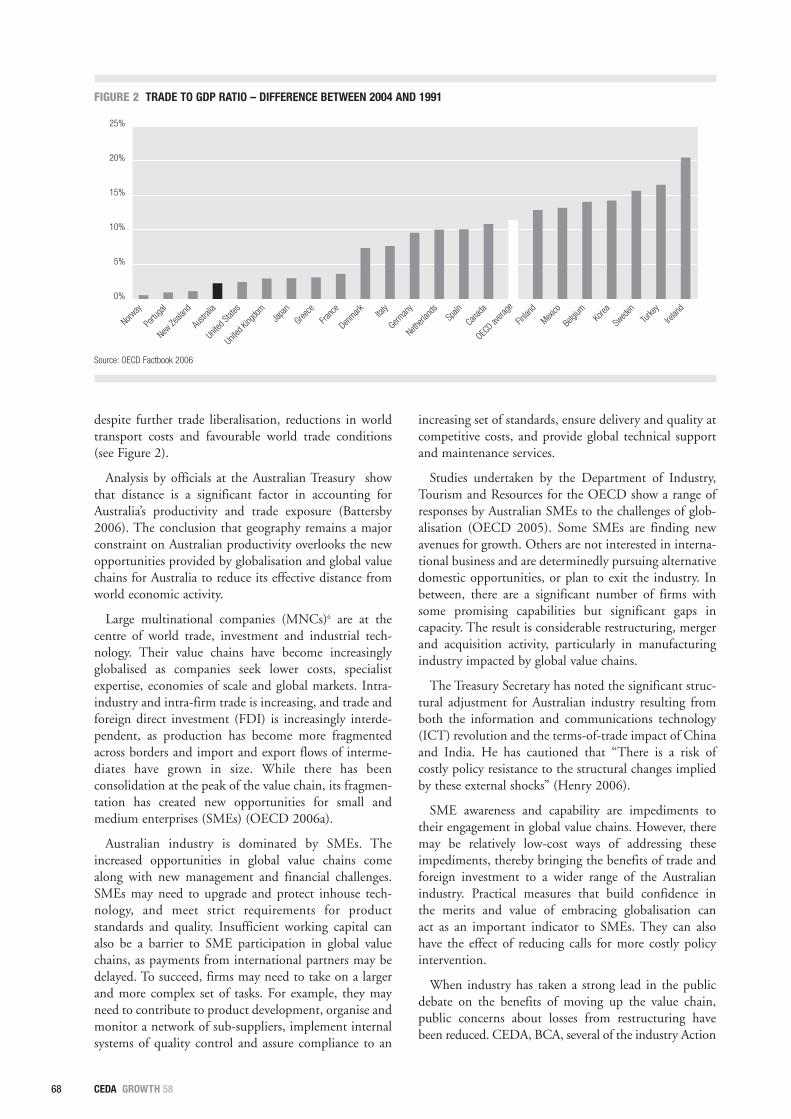

The result is a relatively low global integration forAustralia. The sum of exports and imports as a ratio toGDP puts Australia at the lower end of the OECDspectrum, as seen in Figure 3.

But at least historically for Australia a relatively effi-cient domestic construction and service sector was ableto flourish, and economic achievement could alsoembrace urban utilities and construction – as these werelargely non-traded – and both could benefit from ahealthy, educated, enterprising and growing population.With efficient land and capital-intensive mining andagriculture, and with human-capital-intensive serviceproduction, embedded in a rich foundation of institu-tional capital, Australia still could prosper and grow ahigh living standard. As Ed Leamer (2006) has shown,

FIGURE 1 AUSTRALIA’S EXPORT COMPOSITION, 1861–1991

0% 20% 40% 60% 80% 100%

OtherMineralsGoldWool

1861

1871

1881

1891

1901

1911

1947

1951

1961

1971

1981

1991

Source: McLean & Taylor (2001)

21COMPETING FROM AUSTRALIA

Australia and New Zealand were long the world’s cham-pions in challenging the tyranny of distance, as is seen inFigures 4 and 5. These show how both 30 years ago andin 1990, the two countries did “punch above theirweight”, though they have now been joined by somenewer success stories.

Redding and Venables (2000) found that market andsupplier access explain up to a third of variation in percapita income differences –as signalled in Figures 5 and6. Similarly, Australian Treasury (Battersby & Ewing2005) has calculated that Australia’s low global tradeintegration is above what would be predicted, given ourisolation.

Moreover, this was achieved with our own domesticmarket itself internally fractured by distance. TheAustralian pattern of settlement is a dispersed one. Itsstrength for economic activity is its concentration inlarge cities, more so than the Canadian case, for example.This does generate a range of urban scale economies atleast, plus the more recently recognised spillovers inurban density in the form of knowledge synergies andthick markets.

Scale economies in urban areas come from the reducedcost of connection to high overhead infrastructure provi-sion, such as in electricity distribution or suburban roadprovision. Additional benefits relate to how large con-glomerate population areas allow specialised skills andmarkets to emerge and be viable, ranging from high-levelhealth provision, such as specialised diagnostic andsurgical capabilities, to financial, accounting and legalservices and education provision. On top of this, the new

areas of recognition relate to how such people interactand exchange ideas, often serendipitously through inter-personal exchange and often in social as well as in worksituations.

The evidence is that these benefits strongly outweighthe congestion costs that also occur with urban concen-tration and scale. Indeed, across US cities a doubling ofdensity increases labour productivity overall by 6 per centon average (Quigley 1998). These notions have beenpopularised in recent times through Richard Florida’sbooks, especially The Rise of the Creative Class, which is apaen of praise to cosmopolitanism.

But Australia’s cities are far apart. McLean and Taylor(2001) have pointed out that no two Australian citieswith a population of over a million are within 600 kmsof each other. In California 34 million people live betweenSan Diego and Sacramento, a distance of 800 kms.

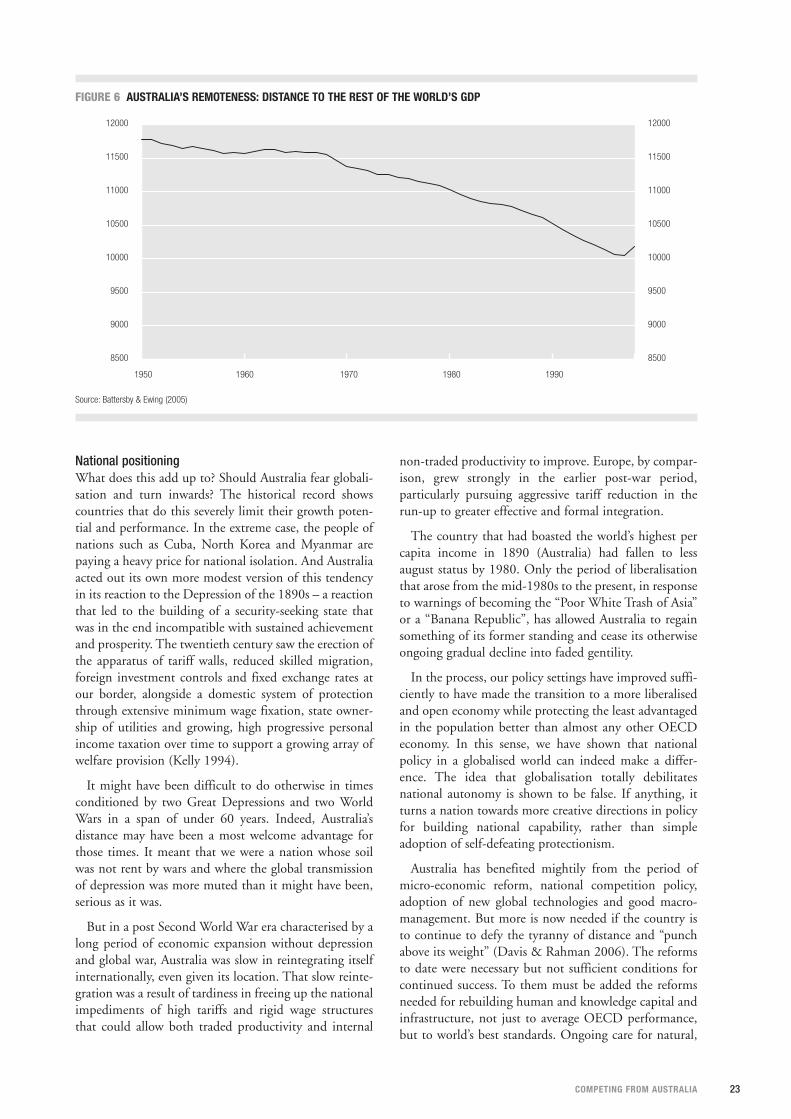

But surely all this is history? Has not distance beendefeated? The world’s economic mass is moving more inAustralia’s favour, transport costs are coming down andmodern communications are increasing Australia’s abilityto interact with the world and tap its knowledge base.This is certainly happening and can be documented. Forexample, in the second half of the twentieth century, theproportion of the world’s GDP within 12,000 kms ofSydney increased from 26 per cent to almost 38 per cent(Battersby & Ewing 2005)3 (see Figure 6).

So some things have improved. But perhaps not asmuch as is popularly believed. In particular, the commonassumption that modern communications technologyhas eradicated distance is not at all clear-cut. This is

FIGURE 2 ECONOMIES OF SCALE IN GLOBAL TRADE

0 0.2 0.4 0.6 0.8 1.0 1.2 1.4 1.6

Petroleum & Coal Products

Pharmaceuticals

Electric and Electronic Machinery

Petroleum Refineries

Forestry

Iron and Steel Basic Industries

Instruments

Machinery (Non-Electrical)

Livestock

Crude Petroleum & Natural Gas

Coal Mining

Source: Antweiler & Trefler (2002).

22 CEDA GROWTH 58

because as the world moves increasingly to become aglobal knowledge economy, much of the creative, high-level knowledge is tacit, not codified in formalcommunication, and serendipitous, conveyed in directpersonal interaction that is a function of co-location(Levy & Murnane 2004).

Indeed, there is evidence to suggest that the impact ofdistance is rising and not declining with time. Reddingand Schott (2003) have found that comparing 1990 with1970, a one per cent distance that previously reducedbilateral exports by 1.2 per cent in 1970 did so by 1.5 percent 20 years later.

In the world of ideas, which underpins value-addedeconomic activity, Keller (2002) has calculated how tech-nology is itself substantially local in use and not global,despite the communications revolution. What he meansis that the benefits from spillovers in using knowledgedecline dramatically with distance. The amount ofspillovers, meaning use of knowledge beyond formallycontracted parties to the technology development,declines by half on average for every 1,200 kms.

If we use Keller’s calculations to look at the averagebenefit to small industrial countries from the R&D in theG-5 nations of the US, UK, Japan, France and Germany,it is all too abundantly clear how proximity pays great div-idends in access to technology, as is shown in Figure 7.

FIGURE 4 GDP PER CAPITA AND DISTANCE TO WORLD GDP, 1960 FIGURE 5 GDP PER CAPITA AND DISTANCE TO WORLD GDP, 1990

0 1000 2000 3000 4000 5000 6000 7000 8000 9000

0

5000

10000

15000

TrinidadVenezuela

Australia, New Zealand

Uruguay

Mauritius

0 1000 2000 3000 4000 5000 6000 7000 8000

0

5000

10000

15000

20000

Australia

SingaporeNew Zealand

Taiwan

Source: Leamer (2006) Source: Leamer (2006)

FIGURE 3 TRADE INTENSITIES, 2001

Source: Battersby & Ewing (2005).

JapanUnited States

AustraliaUnited Kingdon

ItalyTurkeyFranceSpain

NorwayIceland

New ZealandPortugal

GermanyPortugal

DenmarkFinland

SwedenCanada

SwitzerlandAustria

NetherlandsIreland

23COMPETING FROM AUSTRALIA

National positioningWhat does this add up to? Should Australia fear globali-sation and turn inwards? The historical record showscountries that do this severely limit their growth poten-tial and performance. In the extreme case, the people ofnations such as Cuba, North Korea and Myanmar arepaying a heavy price for national isolation. And Australiaacted out its own more modest version of this tendencyin its reaction to the Depression of the 1890s – a reactionthat led to the building of a security-seeking state thatwas in the end incompatible with sustained achievementand prosperity. The twentieth century saw the erection ofthe apparatus of tariff walls, reduced skilled migration,foreign investment controls and fixed exchange rates atour border, alongside a domestic system of protectionthrough extensive minimum wage fixation, state owner-ship of utilities and growing, high progressive personalincome taxation over time to support a growing array ofwelfare provision (Kelly 1994).

It might have been difficult to do otherwise in timesconditioned by two Great Depressions and two WorldWars in a span of under 60 years. Indeed, Australia’sdistance may have been a most welcome advantage forthose times. It meant that we were a nation whose soilwas not rent by wars and where the global transmissionof depression was more muted than it might have been,serious as it was.

But in a post Second World War era characterised by along period of economic expansion without depressionand global war, Australia was slow in reintegrating itselfinternationally, even given its location. That slow reinte-gration was a result of tardiness in freeing up the nationalimpediments of high tariffs and rigid wage structuresthat could allow both traded productivity and internal

non-traded productivity to improve. Europe, by compar-ison, grew strongly in the earlier post-war period,particularly pursuing aggressive tariff reduction in therun-up to greater effective and formal integration.

The country that had boasted the world’s highest percapita income in 1890 (Australia) had fallen to lessaugust status by 1980. Only the period of liberalisationthat arose from the mid-1980s to the present, in responseto warnings of becoming the “Poor White Trash of Asia”or a “Banana Republic”, has allowed Australia to regainsomething of its former standing and cease its otherwiseongoing gradual decline into faded gentility.

In the process, our policy settings have improved suffi-ciently to have made the transition to a more liberalisedand open economy while protecting the least advantagedin the population better than almost any other OECDeconomy. In this sense, we have shown that nationalpolicy in a globalised world can indeed make a differ-ence. The idea that globalisation totally debilitatesnational autonomy is shown to be false. If anything, itturns a nation towards more creative directions in policyfor building national capability, rather than simpleadoption of self-defeating protectionism.

Australia has benefited mightily from the period ofmicro-economic reform, national competition policy,adoption of new global technologies and good macro-management. But more is now needed if the country isto continue to defy the tyranny of distance and “punchabove its weight” (Davis & Rahman 2006). The reformsto date were necessary but not sufficient conditions forcontinued success. To them must be added the reformsneeded for rebuilding human and knowledge capital andinfrastructure, not just to average OECD performance,but to world’s best standards. Ongoing care for natural,

FIGURE 6 AUSTRALIA’S REMOTENESS: DISTANCE TO THE REST OF THE WORLD’S GDP

Source: Battersby & Ewing (2005)

8500

9000

9500

10000

10500

11000

11500

12000

8500

9000

9500

10000

10500

11000

11500

12000

1950 1960 1970 1980 1990

24

social and institutional capital is needed to complementthis. Only if we do this across these many fronts and getthe balance right can we defy distance as we did in thenineteenth century. Because of distance, the policy task iseven more important for Australia.

It is little known and little understood that Australia’searlier achievement as world’s best practice by 1890sprang not just from the luck of possession of naturalresources. It was also the result of having the most skilled,educated and urbanised workforce in the world and themost innovative populace. Australia spent more on edu-cation across more of its people than any other country;it chose its migrants carefully for their skills and it hadthe highest per capita patents of any country (Pope &Withers 1989, 1996: Magee 2000). It was dynamic,flexible, open and free.

But there were some co-conditions for this success.One was good governance. While a democratic pioneer,Australia’s polity had degenerated into “crony capitalism”by the 1890s and the public and private investmentprocesses had spread into increasingly unsustainableactivities not subject to serious business testing (Butlin1964). The resultant collapse was predominantly inter-nally generated, though it was precipitated by a suddenloss of confidence by foreign investors and migrants,who caused a rapid drying up of global lubricationof an economy with serious domestic structural flawsthat had not been recognised in time. The resultantshocks from that Depression of the 1890s led to decadesof introversion.

Future policiesThere are lessons here. They are that openness and flexi-bility are essential; investment in national capability inbusiness, human and knowledge capital is also essential;and good governance must underpin the corporate andpolitical processes and ensure a fair social safety net.

Policies directly related to distance should be specifiedas the core of such a far-sighted package. Two particularrequirements are for Australia to ensure it has telecom-munications and transport provision at best practice andpeople movements correct. These are Australia’s essentiallinks to the global community. In the nineteenth century,Australia’s achievement of world-leading productivitywas underpinned by massive investment in steamshipping, railroads and the telegraph and in acceptingoverseas immigration. In the modern global knowledgeeconomy, the two contemporary equivalents are invest-ment in the best telecommunications and transportarrangements that we can devise, and ensuring again thata dynamic immigration and visitor entry program is inplace.

Telecommunications and transportIn relation to telecommunications and transport, theprincipal focus required is broadband. This is thedefining technology of the globalised economy andcrucial to reducing the disadvantage of our distance fromthe world’s knowledge centres. Regrettably, past policyfrom government of both persuasions has positionedAustralia poorly among industrial countries in terms ofthe timely introduction of, and access to, new tech-

CEDA GROWTH 58

0% 0.5% 1% 1.5% 2% 2.5% 3%

1970-82 1983-95

Sweden

Spain

Norway

Netherlands

Italy

Finland

Denmark

Canada

Australia

FIGURE 7 G-5 R&D SPILLOVER IMPACT ON OTHER COUNTRIES

Source: Keller (2002)

25COMPETING FROM AUSTRALIA

nology. This extends back to the introduction of colourtelevision and through to pay television, mobile phonesand broadband today. In each case Australia has been alaggard in permitting introduction of these advances incommunications. Yet, in each case once change is per-mitted, Australia’s take-up rate of these technologies istypically very rapid and the pay-off from informationand communications technology (ICT) has contributedmightily to sustaining our growth (Parham 2004). Thisis called “catch-up”.

In the case of broadband, according to OECDCommunications Outlook 2005, Australia ranks 23rdout of 32 OECD countries in terms of broadband accessrates. At the same time, Australia is the only OECDcountry where half the broadband users download at 512kilobytes a second or less. It is, of course, easier for geo-graphically smaller countries such as Korea or Japan toprovide such infrastructure, but we also fall well behindsimilarly placed countries to Australia such as Canada.Such have been the national logjams in this area thatstate and territory governments have been seeking tocompensate for the national problems in policy and reg-ulation in this sphere.4 And local possibilities for adecentralised policy have been recently defined forAustralia (Gans 2006).

Indeed, in order to keep information transaction costsdown and to allow the “new economy” industries toflourish (including “virtual” supply chains for export),and to contribute better to economic growth and socialbenefit (Economides 1996; Skilling & Boven 2007)), itmay be that such a move away from a national solutionto a more decentralised strategy is opportune. In partic-ular, on a global basis, broadband Internet access ispeaking and the next phase of global internet usage islikely to be a move from “wired” (DSL, optical fibre andcable modem) to “wireless”. This is being driven bygrowing notebook take-up and handheld mobile internetuse, and many developing country markets are movingstraight to this technology, leapfrogging the tetheredconnections (Ipsos 2007).

Australia could anticipate this. What is needed is a newbroadband strategy premised on opening up and facili-tating decentralisation. Opening up access to Telstraexchange interconnection and street conduits (“the lastmile”) on a local basis for conventional broadband, and

removing major regulatory obstacles to new wirelessbroadband are the core new steps needed for Australiaitself to “leapfrog” in provision, competition and pro-curement in broadband instead of being a perennialbridesmaid in telecommunications.

Greater progress is also needed on rationalisation oftransport infrastructure arrangements. Public transportand storage is about 4.5 per cent of GDP and total shareof GDP going to freight logistics is at least double this,5