GROWING -...

14

GROWING with our community. 2015 Annual Report

Transcript of GROWING -...

GROWINGwith our community.

2015 Annual Report

RIVERFALL CREDIT UNION

63rd ANNUAL MEMBERSHIP MEETINGMarch 1, 2016

Initiated in this area in 1985, the Adopt-A-School program is an effective grassroots partnership between education and the business and private sectors of Tuscaloosa County. The purpose of the program is to utilize the vast amounts of human resources and talents of the business community to strengthen, enhance, and enrich the quality of education in each of the public schools of the Tuscaloosa City and Tuscaloosa County School systems.

Adopt-A-School strengthens and improves our schools, creates a climate of involvement and interaction between businesses and schools and involves the community in pre-paring for its own economic future. RiverFall Credit Union proudly adopted Maxwell Elementary School in 2015. This partnership is a key component of our Community Reinvestment Plan and serves as an important symbol of our continued commitment and support of Tuscaloosa area schools and the communities we serve.

ADOPT-A-SChOOL

1

CALL TO ORDER

INVOCATION

RECOGNITION

ASCERTAINMENT OF A QUORUM

SECRETARY’S REPORT

CHAIRMAN’S REPORT

TREASURER’S REPORT

SUPERVISORY COMMITTEE REPORT

PRESIDENT’S REPORT

UNFINISHED BUSINESS

NEW BUSINESS OTHER THAN ELECTIONS

ELECTIONS

Board of Directors: Mr. Jack Gibson

Board of Directors: Mr. Neal Guy

Supervisory Committee: Mr. Don Kelly

DOOR PRIZES

ADJOURNMENT

AGENDA

2

RIVERFALL CREDIT UNIONFORMERLY TUSCALOOSA TEAChERS CREDIT UNION62nd ANNUAL MEMBERShIP MEETINGMARCh 3, 2015

CALL TO ORDER: The 62nd Annual Membership Meeting of RiverFall Credit Union, formerly Tuscaloosa Teachers Credit Union, was called to order by Chairman Mike Daria on March 3, 2015.

PRESIDING: Mike Daria, Chairman.

INVOCATION: Marlon Murray, Vice Chairman.

ASCERTAINMENT OF A QUORUM: Mike Daria welcomed members and declared a quorum present.

RECOGNITION: The head table was introduced and credit union employees were recognized.

SECRETARY’S REPORT: Byron Abston presented the Secretary’s Report as printed on pages 3 and 4 of the 2014 Annual Report. Don Kelly motioned approval of the 2014 meeting minutes, seconded by member Chrys Larsen.

CHAIRMAN’S REPORT: Chairman Mike Daria presented the Chairman’s Report. he referred to written material provided on page 10 in the 2014 Annual Report. he also spoke of the exciting and positive changes in our credit union.

TREASURER’S REPORT: Neal Guy, Treasurer, reviewed the printed report provided on page 8 in the 2014 Annual Report.

SUPERVISORY COMMITTEE REPORT: Don Kelly, Supervisory Committee member, presented the Supervisory Committee Report. he reviewed information from the 2014 Annual Report.

MINUTES

3

MINUTES

PRESIDENT’S REPORT: President Greg Sassaman spoke of our transition to RiverFall Credit Union and referred to his printed report. The floor was then opened for questions, of which there were none.

UNFINISHED BUSINESS: None.

NEW BUSINESS OTHER THAN ELECTIONS: None.

ELECTIONS: The following were nominated by the Nominating Committee for terms on the Board of Directors and Supervisory Committee. No petitions were presented by others interested.

• Board of Directors: Mr. Marlon Murray

• Board of Directors: Mrs. Deidra Charlton

• Supervisory Committee: Mr. Deron Cameron

The nominees were elected by acclamation.

DOOR PRIZES: Scott Ryan, Vice President of Member Service, conducted the drawings for door prizes.

ADJOURNMENT: After drawing for door prizes, the meeting was adjourned.

4

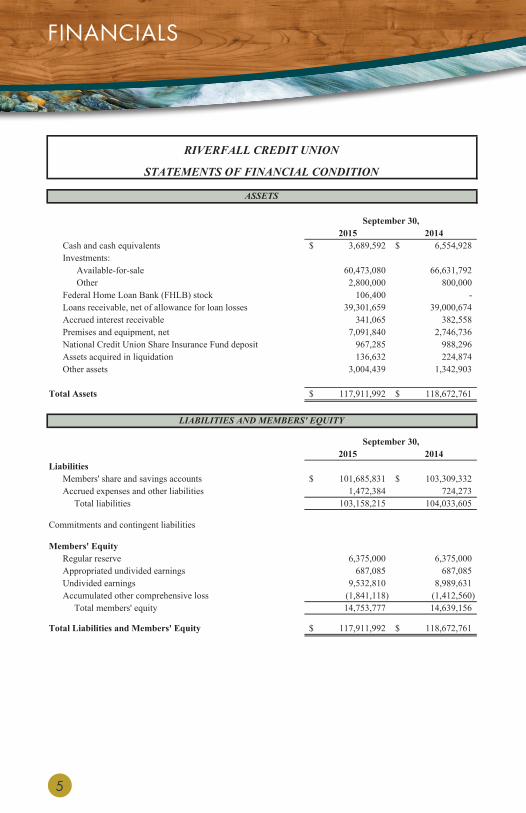

2015 2014 Cash and cash equivalents 3,689,592$ 6,554,928$ Investments: Available-for-sale 60,473,080 66,631,792 Other 2,800,000 800,000 Federal Home Loan Bank (FHLB) stock 106,400 - Loans receivable, net of allowance for loan losses 39,301,659 39,000,674 Accrued interest receivable 341,065 382,558 Premises and equipment, net 7,091,840 2,746,736 National Credit Union Share Insurance Fund deposit 967,285 988,296 Assets acquired in liquidation 136,632 224,874 Other assets 3,004,439 1,342,903

Total Assets 117,911,992$ 118,672,761$

2015 2014Liabilities Members' share and savings accounts 101,685,831$ 103,309,332$ Accrued expenses and other liabilities 1,472,384 724,273 Total liabilities 103,158,215 104,033,605

Commitments and contingent liabilities

Members' Equity Regular reserve 6,375,000 6,375,000 Appropriated undivided earnings 687,085 687,085 Undivided earnings 9,532,810 8,989,631 Accumulated other comprehensive loss (1,841,118) (1,412,560) Total members' equity 14,753,777 14,639,156

Total Liabilities and Members' Equity 117,911,992$ 118,672,761$

RIVERFALL CREDIT UNION

September 30,

September 30,

LIABILITIES AND MEMBERS' EQUITY

ASSETS

STATEMENTS OF FINANCIAL CONDITION

The accompanying notes are an integral part of these financial statements.A-3

FINANCIALS

5

2015 2014Interest Income Interest on loans receivable 1,863,081$ 1,911,511$ Interest on investments 1,223,493 1,436,662 Interest income 3,086,574 3,348,173

Interest Expense Dividends on members' share and savings accounts 750,787 789,030 Interest on borrowed funds 21 1,185 Interest expense 750,808 790,215

Net Interest Income 2,335,766 2,557,958

Provision for Loan Losses 100,120 25,097 Net Interest Income After Provision for Loan Losses 2,235,646 2,532,861

Non-Interest Income Fees and service charges 804,954 831,783 NCUSIF recapitalization 459,548 455,859 Non-interest income 1,264,502 1,287,642

3,500,148 3,820,503 Non-Interest Expense Compensation and employee benefits 1,292,115 1,272,403 Professional and outside services 647,433 630,121 Operations 492,885 401,800 Occupancy 264,704 276,264 Education and promotion 138,105 110,978 Loan servicing 118,461 109,670 Loss on disposition of assets acquired in liquidation, net 3,266 20,433 Non-interest expense 2,956,969 2,821,669

Net Income 543,179$ 998,834$

September 30,

RIVERFALL CREDIT UNION

STATEMENTS OF INCOME

The accompanying notes are an integral part of these financial statements.A-4

FINANCIALS

6

As of12/31/2014

As of12/31/2015

Assets

Shares

Loans

Members

$ 119,294,489

$ 103,363,108

$ 39,747,008

8,345

$ 117,675,804

$ 102,378,272

$ 40,594,225

8,599

($ 1,618,685)

($ 984,836)

$ 847,217

254

-1.4 %

-1.0 %

2.1 %

3.0 %

%Change

Amount ofChange

STATISTICS

Loans and Advances Made in 2015 12,047

Amount $ 15,527,811

Loans Charged-off in 2015 $ 120,581

Recoveries $ 23,137

Loans Charged-off Since Organization $ 4,564,809

Recoveries $ 1,640,574

Number of Members 8,599

COMPARISON OF 2014–2015 FIGURES

SOURCE AND USE OF FUNDS IN 2015

SOURCE OF FUNDS AMOUNTS % OF TOTAL

Loan Interest Income $ 1,852,729 43 %

Investment Income $ 1,169,657 27 %

Other Income $ 1,266,085 30 %

TOTAL $ 4,288,471 100 %

USE OF FUNDS

Dividends $ 733,406 17 %

Operating Expenses $ 3,061,610 71 %

Undivided Earnings $ 493,455 12 %

TOTAL $ 4,288,471 100 %

FINANCIALS

7

RiverFall Credit Union provides its members with sound financial services and solid credit union operations. Total assets for 2015 were $117,675,804. Shares for 2015 were $102,378,272. While both of these year-end totals decreased slightly from 2014, RiverFall continues to hold a strong financial position.

For the year 2015, RiverFall Credit Union made 12,047 loans to members. These loans totaled $15,527,811. This represented a 4.2% increase from the previous year. This loan growth is directly attributed to the commitment of RiverFall’s leader-ship to provide competitive rates to our members. Additionally, RiverFall returned to its members in the form of dividends over $733,000.

These numbers reflect RiverFall Credit Union’s sound financial standing. Significant and exciting progress was made in 2015 in facilities, branding, member services, and financial products and services. Next steps include focused planning efforts leading to development of a strategic plan to guide our credit union throughout 2016 and beyond. Your board is committed to ensuring that RiverFall continues to maintain stable and secure financial practices while seeking forward thinking ap-proaches to improvement and innovation. The board, along with the administra-tion, are striving to design operating procedures for all aspects of the credit union that mirror the new name, the new look, and a new attitude for RiverFall. We are pleased with the improvements to-date and look forward to working together to continue building a credit union that is focused on member services, relationships, and progress.

G. Neal Guy, Ed.S.

Treasurer

TREASURER’S REPORT

8

The Supervisory Committee of a credit union is created by law to act as the mem-bers’ representative in monitoring and guiding operations of the credit union, and is similar to an in-house audit committee found in many financial institutions. I have proudly served as chairman of the Committee this past year. Serving with me are Jennifer Box and Deron Cameron.

Responsibilities of the Committee include making sure the credit union has internal controls in place to protect credit union assets. During 2015, as in years past, we engaged the auditing firm Nearman, Maynard, Vallez, CPAs (NMV). This firm was selected from among several that were considered based on its principles, pricing, and references. It was formed in 1979 and has been serving only credit unions for more than 30 years.

NMV conducted three audits: (1) Certified Audit for the period October 1, 2014 through September 30, 2015; (2) ACh (Automated Clearing house) Compliance Review; (3) OFAC (Office of Foreign Assets Control) & BSA (Bank Secrecy Act) Compliance Review.

In addition to the annual, outsourced audits performed by NMV, the Supervisory Committee has also enlisted the assistance of, and delegated authority to, select credit union staff to perform various internal audit tasks on a periodic, ongoing basis. Some of these include random counts of teller drawers and vaults, review of account maintenance changes, and transaction verifications with members.

Adherence to regulations by RiverFall Credit Union is monitored, and the credit union remains sound and in compliance.

Don Kelly

Chairman

SUPERVISORY COMMITTEE REPORT

9

RiverFall Credit Union had another great year of service to our members and our local community. Our focus remains as clear as ever, to provide great banking to all who call Tuscaloosa home. Our community is strong, progressive, and vibrant. Your RiverFall Credit Union is proud to be a part of this community and its progres-sive future.

The most obvious signs of our progress can be seen in our new and renovated branches. In any visit to these branches, you will be served by professional, car-ing, and knowledgeable member service associates who will assist you at what-ever pace works for you. Our enhanced impact in our community is also seen with our work with local schools and agencies. We are proud to be a contributor to our community with our Pacesetter Awards, college scholarships, Adopt-a-School, char-ity drives, and participation in community events. Our expanded presence in our community is a source of pride for all of us.

In the fast pace of progress, our core values and mission remain unchanged. Riv-erFall Credit Union remains firm in its loyalty to the traditional values of service for our 8,599 members. Integrity, trust, and professionalism guide our decisions, ac-tions, and progress. Whatever your financial goals may be, RiverFall Credit Union remains committed to providing you with the education, service, and products to make them a reality.

The promise of our bright future is built on the strengths of our past. The Board of Directors is engaging in the next steps of its strategic planning process with an unwavering focus on enhancing member services, offering financial products to meet the various needs of our members, and continuing our role in the progress of our community.

As you review the Treasurer’s report, you will see that RiverFall Credit Union remains fiscally sound and secure. As our financial strength grows, we are able to provide more benefits and products for all of our members. RiverFall Credit Union continues to define itself with persistence, power, and strength that provide value in membership.

We are grateful and honored that you rely on RiverFall Credit Union to meet the needs of you and your family.

Mike Daria

Chairman

ChAIRMAN’S REPORT

10

hopefully during the past year you’ve become familiar with the phrase, “Find Your Pace.” Our use is not merely as a marketing element, even though we do try to in-corporate it consistently in various publications and communications. Much more than just a slogan, it is the commitment and ultimate objective of RiverFall Credit Union to provide the products and services you want and to do so in the manner you want them.

You likely see and hear advertising of this nature constantly, from many sources. Virtually all businesses claim to be dedicated to their customers/members and it is not our intention to critique others’ motivations or how successfully they follow through on promises. But RiverFall’s fulfillment of the pledge is tangible in a num-ber of forms, such as:

• In-office service via personal assistance and automated teller machine

• Drive-up service via personal assistance and automated teller machine

• Telephone service via personal assistance and automated audio response

• Electronic/remote service via website, home banking, and mobile

The principle behind everything RiverFall has worked toward through the transition is simple in concept but challenging to accomplish. It is to be accommodating. To offer you choices. To allow you to select how you prefer to be served. To em-power you to decide how you want to bank. Simply, to enable you to “Find Your Pace.” We have tried, and will continue, to provide alternatives and let you pick a personal favorite rather than dictating or limiting your options to the methods best for RiverFall.

This accommodative, something-for-everyone philosophy is contrary to the present day theory that a business must have one thing to ‘be the best,’ or that a business must target one thing to work at to ‘be the best.’ While it does sound impressive to ‘be the best’ at something, the reality is that West Alabama consists of almost 300,000 people. We are not presumptuous to determine what is best for all but instead want to ‘be the best’ we can at providing for all of you, for all of West Alabama.

We hope you find RiverFall’s approach refreshing. More importantly, we hope you find it practical and helpful for you to “Find Your Pace.”

Greg SassamanPresident

PRESIDENT’S REPORT

11

riverfallcu.com