Greenville: An Upward Bound Economy in Transition The transforming economy Incomepatterns...

33

Greenville: An Upward Bound Economy in Transition • The transforming economy •Incomepatterns •natConverging but distinctive South Carolina’s Economy: Forecast & Indicators. Will South Carolina’s Flowers Bloom in the Newly Sprouted Knowledge Economy? Bruce Yandle Professor of Economics Emeritus, Clemson University [email protected]

-

Upload

mervyn-henry -

Category

Documents

-

view

215 -

download

1

Transcript of Greenville: An Upward Bound Economy in Transition The transforming economy Incomepatterns...

Greenville: An Upward Bound Economy in Transition

• The transforming economy

•Incomepatterns

•natConverging but distinctive

South Carolina’s Economy:Forecast & Indicators.

Will South Carolina’s Flowers Bloom in the Newly Sprouted Knowledge Economy?

Bruce Yandle

Professor of Economics Emeritus, Clemson University

Greenville: An Upward Bound Economy in Transition

• The transforming economy

•Incomepatterns

•natConverging but distinctive

What matters now are BRAINS.

How to get the brains…, and get them connected?

•

Average Annual Per Capita Real GDP Growth: 2000-2006

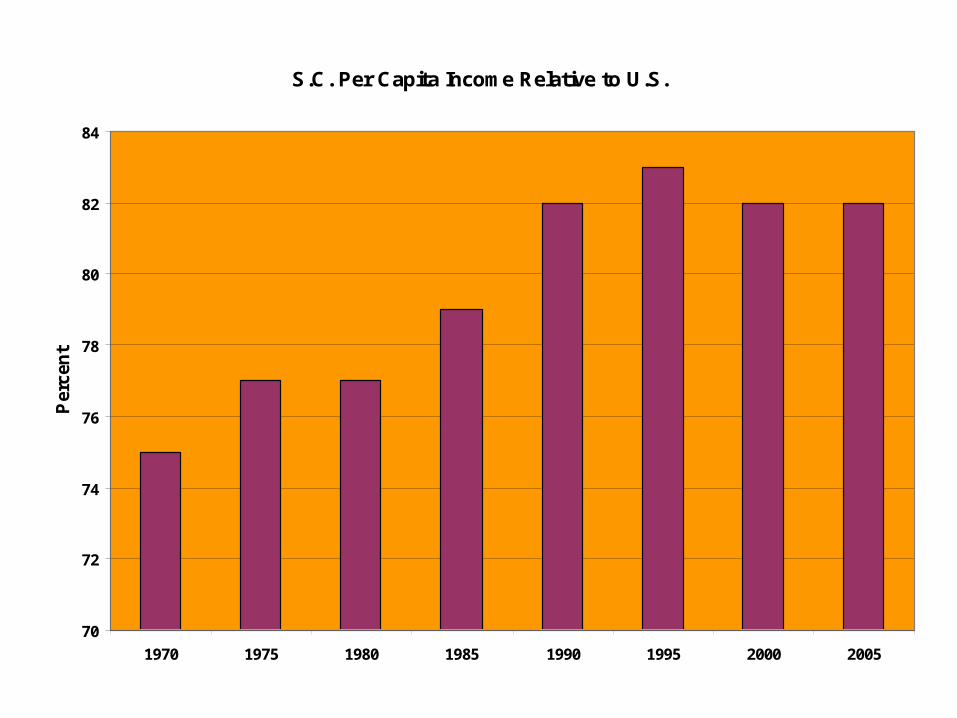

S.C. Per Capita Income Relative to U.S.

70

72

74

76

78

80

82

84

1970 1975 1980 1985 1990 1995 2000 2005

Per

cen

t

2005 Over 25 Population with High School Education

Percent of Population 25 or older with Bachelor’s Degree or Higher, 2005

Bachelor's Degrees & Per Capita GDP, 2006

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

0 10000 20000 30000 40000 50000 60000 70000

Per Capita GDP

Sh

are

of

abo

ve 2

5 w

ith

deg

rees

Delaware

W. Virginia

Massachusetts

S.C.

N.C.

Texas

Mich.Calif.

Conn.

New York

Miss.Nevada

Vermont

Maryland

Hawaii

Kansas

Alaska

La.

Ark

Colo.

N.J.

Wyoming.

Mont.

Tenn.

Va.

Let’s talk about where people work!And how that has changed.

U.S. EMPLOYMENT: 1940Non-Agricultural

MFG34%

CONST5%

TPU9%

TRADE22%

MIN3%

GVT13%

FIN & SVC14%

U.S. EMPLOYMENT: 2006

MFG11%

CONST5%

TPU4%

TRADE17%

0%

GVT17%

SVC &FIN45%

MIN1%

Source: Bureau of Labor Statistics

Percent Distribution of Percent Distribution of US Nonfarm Employment US Nonfarm Employment

by Industryby Industry20062006

Government16.2%

Leisure and Hospitality

9.6%

Education and Health Services

13.1%

Professional and Business Services

12.8%

Financial Activities6.2%

Information2.3%

Trade, Transportation and Utilities

19.2%

Manufacturing10.5%

Construction5.6%

Percent Distribution of Percent Distribution of SC Nonfarm Employment SC Nonfarm Employment

by Industryby IndustryJuly 2007July 2007

Government17.0%

Leisure and Hospitality

11.0%

Education and Health Services

11.0%

Professional and Business Services

11.0% Financial Activities5.0%

Information1.0%

Trade, Transportation and

Utilities19.0%

Manufacturing13.0%

Construction6.0%

Source: SCESC/LMI

Number of Employees: Professional, Scientific & Technical Services, 2005

Median Family Income, 2005

The Changing Industrial Scene

America is disintegrating!

Total Employed, 16 and Over, Seasonally AdjustedHousehold Survey, with Trend

1/1991 - 12//2007

105000

110000

115000

120000

125000

130000

135000

140000

145000

150000

Date

Apr-91

Aug-91

Dec-9

1

Apr-92

Aug-92

Dec-9

2

Apr-93

Aug-93

Dec-9

3

Apr-94

Aug-94

Dec-9

4

Apr-95

Aug-95

Dec-9

5

Apr-96

Aug-96

Dec-9

6

Apr-97

Aug-97

Dec-9

7

Apr-98

Aug-98

Dec-9

8

Apr-99

Aug-99

Dec-9

9

Apr-00

Aug-00

Dec-0

001

M401

M8

01M12

2-Apr

2-Aug

2-Dec

3-Apr

3-Aug

3-Dec

4-Apr

4-Aug

4-Dec

5-Apr

5-Aug

5-Dec

6-Apr

6-Aug

6-Dec

7-Apr

7-Aug

7-Dec

Th

ou

san

d

U.S. Manufacturing Output

1919-2006Federal Reserve Index 2000=100

y = 4.5606e0.0032x

R2 = 0.9694

0

20

40

60

80

100

120

140

Month/Year

Ind

ex

Percentage Change in Manufacturing Employment1992-2003

-30

-25

-20

-15

-10

-5

0

5C

anad

a

Norw

ay

Tai

wan

Ital

y

Sw

eden

Fra

nce

Kore

a

Net

her

lands

Bel

giu

m

U.S

.

U.K

.

Chin

a

Ger

man

y

Aust

ralia

Japan

Rat

e

Data for The Netherlands and China are for 1990-2002.Source: W.A. Ward, Manufacturing Productivity and the Shifting U.S., China, and Global Job Scenes, 1990-2005. Center for International Trade, Clemson University, Clemson, SC.

Unemployment Rates: S.C. & U.S.2005-2007

3.03.54.04.55.05.56.06.57.07.5

South Carolina U.S.

What lies ahead? When will the sub-prime problem end? Recession????

Money Supply Annual Growth1960 - 2006

-6

-4

-2

0

2

4

6

8

10

12

14

16

Annual G rowth in Indus trial P roduc tion and S .C . R eal T otal P ers onal Inc ome: 1971-2007

-10

-5

0

5

10

15

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

Indus trial P roduc tion R eal TP I

-2

-1

0

1

2

3

4

5

6

Growth

2005Q1 2005Q3 2006Q1 2006Q3 2007Q1 2007Q3 2008Q1 2008Q3

GDP Growth & Forecast

Actual GDP Growth Forecast

Forecast Time

Actual 12/31/06 Forecast 12/31/07 12/31/07 Forecast 12/08

• Real GDP Growth 3.2% 2.5% 2.6%* 2.2%

• CPI Inflation 2.6% 2.5% 4.3%** 3.0%

• 30-yr. Mortgage 5.82% 6.0% 5.84% 6.10%

• Unemploy Rate 4.5% 4.0% 5.0% 5.0%

• Prime 8.25% 7.75% 7.25% 6.00%

• Dow 12,460 13,200 13,264 14,200

• Employ Growth 150M 175M 120M 110M

• Oil $58 $45 $93 $80

• Gold $510 $600 $838 $700________________* Estimate. ** Through November 2007.