Greek Economic Outlook 2015-1017

25

2015 - 2017 Outlook July 12 th Agreement: Negative but Manageable Economic Research July 2015 [email protected] Bloomberg Page: <PBGR> Ilias Lekkos [email protected] Irini Staggel [email protected] Dimitris Gavalas [email protected] Anastasia Aggelopoulou [email protected] Piraeus Bank 94, Vas. Sofias Ave. & 1, Kerassountos str., 115 28 Athens Τ: +30 210 3288187, F: +30 210 3739580

-

Upload

ilias-lekkos -

Category

Economy & Finance

-

view

94 -

download

2

Transcript of Greek Economic Outlook 2015-1017

2015 - 2017 Outlook July 12th Agreement: Negative but Manageable

Economic Research

July 2015

Bloomberg Page: <PBGR>

Ilias Lekkos [email protected] Irini Staggel [email protected] Dimitris Gavalas [email protected] Anastasia Aggelopoulou [email protected] Piraeus Bank 94, Vas. Sofias Ave. & 1, Kerassountos str., 115 28 Athens Τ: +30 210 3288187, F: +30 210 3739580

2

Economic Outlook (YoY% change, unless otherwise stated)

3

2014 2015 2016 2017

Real GDP 0.8 -2.0 -3.0 to -2.0 2.0 to 3.0

Nominal GDP -1.8 -4.0 -1.0 to -2.0 3.0 to 4.0

GDP Deflator -2.6 -2.0 0.5 to 1.5 1.0 to 2.0

CPI -1.3 -1.5 1.0 to 2.0 1.0 to 2.0

Unemployment

(% of labour force) 26.5 27.0 26.0 to 27.0 24.0 to 25.0

Source: ELSTAT, Piraeus Bank Research

4

• In 2015, the economy will return to recession due to the negative impact of the continuing uncertainty, the

capital controls and the new fiscal adjustment measures.

• Growth will pick up only in Q4 – 2016, assuming that structural reforms and an extended privatization

program will materialize. We expect the economy to maintain its momentum in 2017.

• In 2016, unemployment rate will range between 26% and 27%, close to the 2015 levels. In 2017,

unemployment rate will decline as the economy will return to growth.

• In Q4-2015, inflation will turn to positive territory due to the increase of VAT.

• Following the June 26 announcement of the referendum, events came thick and fast, resulting in the

achievement of an Agreement at the Euro Summit on July 12.

• In a first attempt to estimate the impact of the crisis, we present a partial equilibrium analysis, in which we

examine the impact of the measures on nominal households’ disposable income, consumption and GDP.

• The key conclusion is that the measures will be recessionary but manageable. Based on the decrease in

consumption alone, Nominal GDP is expected to contract aprox. by 0.5% in 2015H2 and by 1.0% .

• However, both investments and external trade are most affected by uncertainty, political stability and –

especially for investments – EU Funds inflows, which if utilized in due course could prove to be decisive.

5

• In 2015, the economy will return to recession due to the negative impact of the continuing

uncertainty, the capital controls and the new fiscal adjustment measures.

• In 2016, the significant contraction in Q4-15 creates a negative carry-over effect of approx. -3.0%.

Hence, we expect real GDP rate of recession to be similar to the 2015. However we expect a gradual

increase in GDP on a quarterly basis towards 2016 year-end as the impact of the measures will fade

away and a privatization program will be implemented.

• In 2017, the economy will maintain its momentum, as the previous year’s uncertainty declines.

Real GDP (% change)

-4.0

-3.5

-3.0

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

-12.0

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

Q1

/10

Q2

/10

Q3

/10

Q4

/10

Q1

/11

Q2

/11

Q3

/11

Q4

/11

Q1

/12

Q2

/12

Q3

/12

Q4

/12

Q1

/13

Q2

/13

Q3

/13

Q4

/13

Q1

/14

Q2

/14

Q3

/14

Q4

/14

Q1

/15

Q2

/15

Q3

/15

Q4

/15

Q1

/16

Q2

/16

Q3

/16

Q4

/16

Q1

/17

Q2

/17

Q3

/17

Q4

/17

QoQ (RHS) YoY (LHS )

6

2015: -2.0% YoY

Q1: +0.4% ΥοΥ (ELSTAT data). i.e. there is a positive impact on the 2015 year average.

Q2: approx. -0.5% QoQ (-0.4% ΥοΥ)

The continuing uncertainty due to the lack of an agreement is estimated to drag the quarterly GDP

growth rate into negative territory. Our -0.4% YoY forecast is predicated on a -0.7% within year

contraction, which is partially counterbalanced by a 0.3% positive carry-over effect.

The negative impact of the IMF and BoG arrears and the announcement of the referendum hasn’t been

reflected yet.

7

2015 (cont.)

Q3: between -2.5% and -2.0% QoQ, i.e. approx. -3.5% YoY with substantial negative dynamic

There is a negative contribution from the capital controls. This negative impact, however, is expected

to be manageable. Capital controls are estimated to negatively affect real GDP for 3 weeks (during the

bank holiday). On 20/7, the ongoing controls on businesses were partly and gradually removed

(approval from the "Approval Committee for Banking Transactions, General Accounting Office"), while

the limit on cash withdrawals is €420 per week and there are no restrictions on the use of either debit

or credit cards in the domestic market.

Private Consumption: Despite the restrictions on cash withdrawals there were no restrictions on

domestic electronic transactions. This, in combination with the fear of a possible haircut on deposits,

had a positive impact on private consumption mainly on consumer durable goods.

However, the new fiscal adjustment measures will have a negative impact on disposable income and

consequently on private consumption.

Tourism: Increased uncertainty led to a drop in tourism in July, but the established agreement is

expected to halt the cancelling of bookings during August-September.

Q4: between -2.5% and -2.0% QoQ i.e. approx. -5%ΥοΥ.

The full implementation of the new measures will have a negative impact on consumption and

business activity.

8

2016: between -3.0% and -2.0%

The significant contraction in Q4-15 creates a negative carry-over effect of approx. -3.0% in 2016.

Hence, we expect real GDP rate of contraction to be similar to the 2015.

In 2016H1, the full negative impact of the new measures will become apparent. On a quarterly basis,

we expect a further decline in Q1 by approx. -0.5% and relative stability in the second quarter.

However, on an annual basis, the base effect will lead to extremely negative y-o-y growth rates i.e. Q1:-

5.5% ΥοΥ, Q2: -5.0%.

However, the impact of the measures will fade away towards 2016 year-end, as the base effect will be

based on the low levels of disposable income, due to the burden of measures since mid-2015.

Moreover, according to the economic adjustment program, the government must implement an

extended privatization program.

Based on the above assumption, we expect a gradual quarterly increase in GDP during Q3 and Q4,

resulting in a deceleration in the pace of the recession in Q3 (around -1.8% YoY, + 1.0% QoQ) and a

return to growth in Q4 (approx. 2.5 % YoY).

2017: between 2.0% and 3.0%

We expect the economy to maintain its momentum in 2017 as the previous year’s uncertainty declines

and we have a positive carry – over effect (approx. 2.0 ppts)

9

In 2015, the job creation schemes in addition to the hiring of public sector employees are expected to

limit the impact of recession on employment. The unemployment rate will be close to 27.0%.

In 2016, we expect the unemployment rate to range between 26% and 27%, as we estimate that the

employment schemes will continue to support the labour market and that, towards the end of the

year, activity will strengthen.

In 2017, we expect the unemployment rate to range from 24% to 25%, as the economy will return to

growth and the first positive results of the privatizations will be reflected in the employment figures.

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Q1

/10

Q2

/10

Q3

/10

Q4

/10

Q1

/11

Q2

/11

Q3

/11

Q4

/11

Q1

/12

Q2

/12

Q3

/12

Q4

/12

Q1

/13

Q2

/13

Q3

/13

Q4

/13

Q1

/14

Q2

/14

Q3

/14

Q4

/14

Q1

/15

Q2

/15

Q3

/15

Q4

/15

Q1

/16

Q2

/16

Q3

/16

Q4

/16

Q1

/17

Q2

/17

Q3

/17

Q4

/17

UR (t) - UR (t-4), (LHS) UnRate (RHS )

Unemployment Rate

10

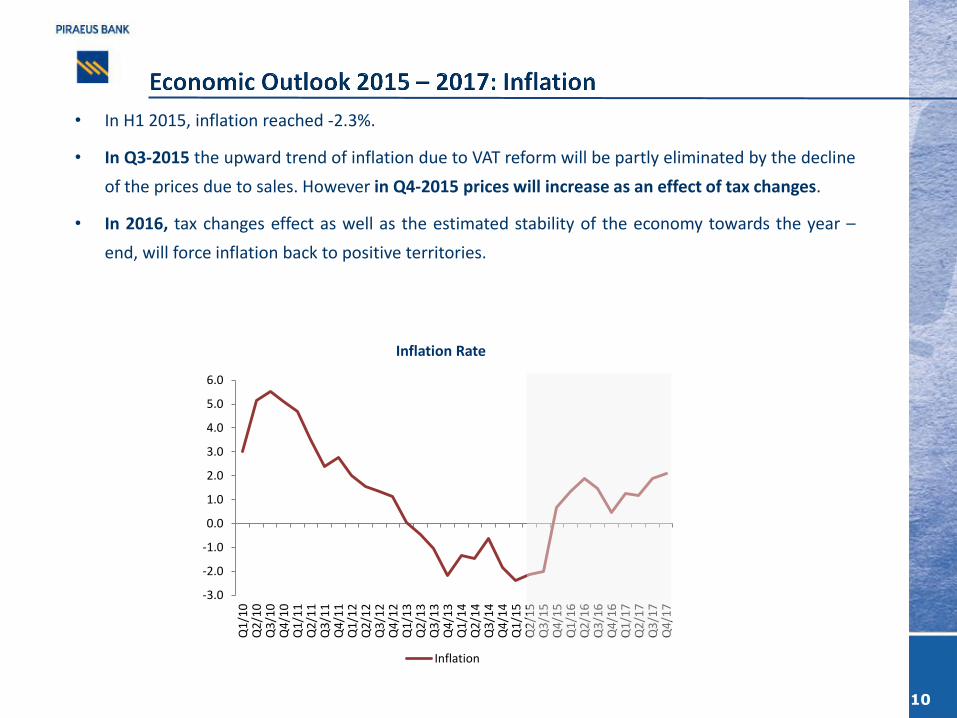

• In H1 2015, inflation reached -2.3%.

• In Q3-2015 the upward trend of inflation due to VAT reform will be partly eliminated by the decline

of the prices due to sales. However in Q4-2015 prices will increase as an effect of tax changes.

• In 2016, tax changes effect as well as the estimated stability of the economy towards the year –

end, will force inflation back to positive territories.

Inflation Rate

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Q1

/10

Q2

/10

Q3

/10

Q4

/10

Q1

/11

Q2

/11

Q3

/11

Q4

/11

Q1

/12

Q2

/12

Q3

/12

Q4

/12

Q1

/13

Q2

/13

Q3

/13

Q4

/13

Q1

/14

Q2

/14

Q3

/14

Q4

/14

Q1

/15

Q2

/15

Q3

/15

Q4

/15

Q1

/16

Q2

/16

Q3

/16

Q4

/16

Q1

/17

Q2

/17

Q3

/17

Q4

/17

Inflation

11

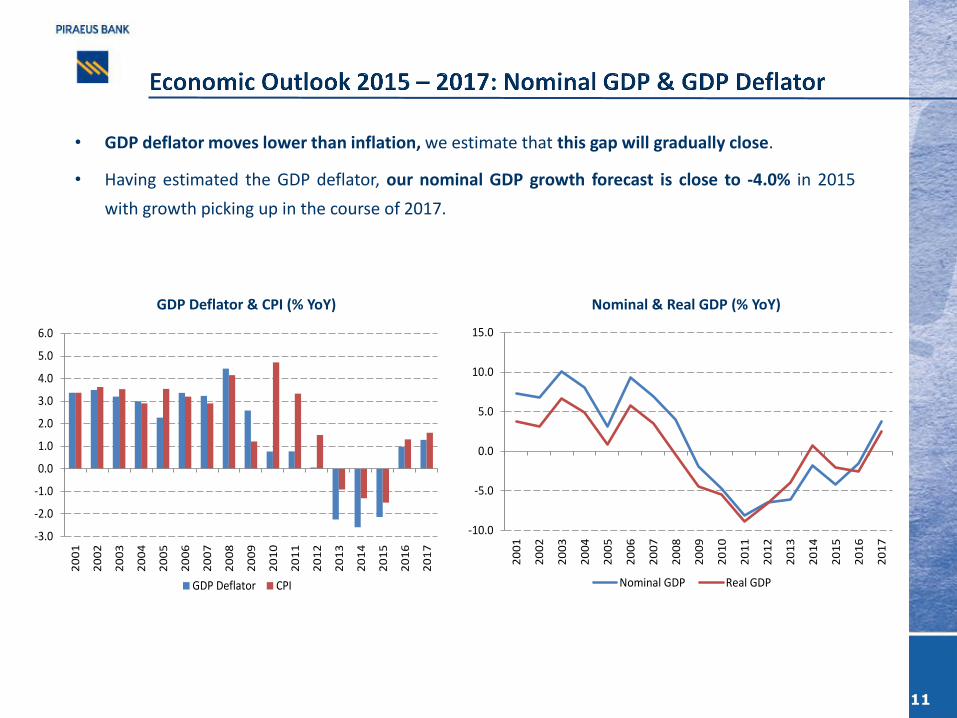

• GDP deflator moves lower than inflation, we estimate that this gap will gradually close.

• Having estimated the GDP deflator, our nominal GDP growth forecast is close to -4.0% in 2015

with growth picking up in the course of 2017.

GDP Deflator & CPI (% YoY) Nominal & Real GDP (% YoY)

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

GDP Deflator CPI

-10.0

-5.0

0.0

5.0

10.0

15.0

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

Nominal GDP Real GDP

12

Following the June 26 announcement of the referendum, events came thick and fast (see Annex:

Events Timeline), resulting in the achievement of an Agreement at the Euro Summit on July 12.

The Agreement can be summarized as having 3 main dimensions:

• Fiscal and structural reforms

• New OSI financing arrangement of circa €82 - €86 bn

• Public Debt Sustainability Analysis

13

• In a first attempt to estimate the impact of the crisis, we present a partial equilibrium analysis, in

which we examine the impact of the measures on household income, consumption and GDP.

• The key conclusion is that the measures will be recessionary but manageable. Based on the

decrease in consumption alone, nominal GDP is expected to contract by aprox. -0.5% in 2015H2

and by -1.0% in 2016.

• Of course the final extent of the recession will depend on the interaction of all the GDP

components.

• However, both investments and external trade are most affected by uncertainty, political stability

and – especially for investments – EU Funds inflows, which if utilized in due course could prove

to be decisive.

14

• On 15/7 a bill was passed for measures relating to taxation, the pension system, full legal

independence of the ELSTAT, the initiation of the operation of the Fiscal Council and the

introduction of quasi-automatic spending cuts in case of deviations from the primary surplus

targets.

• On 22/7 a bill was passed for measures relating to the adoption of the Code of Civil Procedure and

the transposition of the BRRD.

• The implementation of structural reforms is minimum requirement to start the negotiations with

the Greek Authorities for a Third Economic Adjustment Program.

15

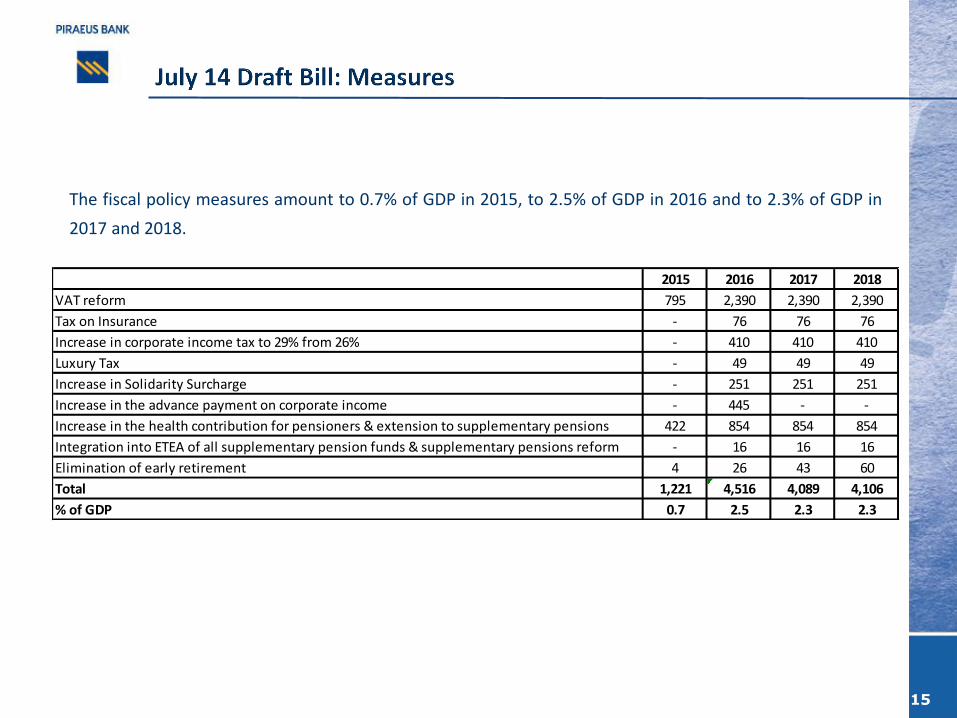

The fiscal policy measures amount to 0.7% of GDP in 2015, to 2.5% of GDP in 2016 and to 2.3% of GDP in

2017 and 2018.

2015 2016 2017 2018

VAT reform 795 2,390 2,390 2,390

Tax on Insurance - 76 76 76

Increase in corporate income tax to 29% from 26% - 410 410 410

Luxury Tax - 49 49 49

Increase in Solidarity Surcharge - 251 251 251

Increase in the advance payment on corporate income - 445 - -

Increase in the health contribution for pensioners & extension to supplementary pensions 422 854 854 854

Integration into ETEA of all supplementary pension funds & supplementary pensions reform - 16 16 16

Elimination of early retirement 4 26 43 60

Total 1,221 4,516 4,089 4,106

% of GDP 0.7 2.5 2.3 2.3

16

A significant proportion of the measures to be implemented based of the Agreement is directly linked

to households’ disposable income. These measures include the VAT reform, tax on insurance, luxury

tax, the increase in solidarity surcharge, the increase in the health contribution for pensioners and

supplementary pensions reforms.

The estimated total value of the measures is:

• 2015: €1.2 bn

• 2016: €3.6 bn

The question is to what extent these measures will affect consumption and, hence, Greek GDP.

17

These measures are expected to reduce household disposable income by around 2.0% YoY in 2015H2

and by -3.3% YoY in 2016H1. This impact is expected to weaken towards the end of 2016 (-1.0% YoY),

due to the base effect of the already low levels of disposable income resulting from the measures

implemented in mid-2015.

-1,000

-900

-800

-700

-600

-500

-400

-300

-200

-100

0

Q3/15 Q4/15 Q1/16 Q2/16 Q3/16 Q4/16

Impact of the Fiscal Measures on the Disposable Income (DI) on an

annual basis

DI(t) – DI(t-4)], mn. €

18

Household disposable income is directly linked to private consumption.

Hence, it is expected that a drop in disposable income will reduce private consumption by around

1.3% YoY in 2015H2 and -1.7% YoY in 2016.

-1,200

-1,000

-800

-600

-400

-200

0

H2-15 Q1/16 Q2/16 Q3/16 Q4/16

y = 0.6268x + 3.9207R² = 0.8508

10.25

10.30

10.35

10.40

10.45

10.50

10.55

10.60

10.65

10.70

10.10 10.20 10.30 10.40 10.50 10.60 10.70 10.80

ln (

Ho

use

ho

lds

Co

nsu

mp

tio

n)

ln(Households Disposable Income)

Impact of measures on Private Consumption (PC)

on an annual basis PC(t) – PC(t-4)], mn. €

Disposable Income and Private Consumption

Correlation

19

At the same time, private consumption is the main component of nominal GDP (approx. 70% of GDP).

Subsequently, it is estimated that the decrease in private consumption – via the impact of the

measures on household disposable income – will lead to a drop in nominal GDP of 0.5%YoY in

2015H2 and -1.0% YoY in 2016.

However, the macroeconomic aggregates will not only depend on the specific measures and their

corresponding impact on disposable income and consumer spending, but also on the overall

economic environment.

y = 1.1322x - 1.0183R² = 0.8599

10.60

10.65

10.70

10.75

10.80

10.85

10.90

10.95

11.00

11.05

11.10

10.30 10.40 10.50 10.60 10.70

ln(

No

min

al G

DP

)

ln (Households Consumption)

Impact of measures on Nominal GDP (NGDP) on

an annual basis NGDP(t) – NGDP(t-4), bn. € Nominal GDP and Private Consumption

Correlation

-1,200

-1,000

-800

-600

-400

-200

0

H2-15 Q1/16 Q2/16 Q3/16 Q4/16

20

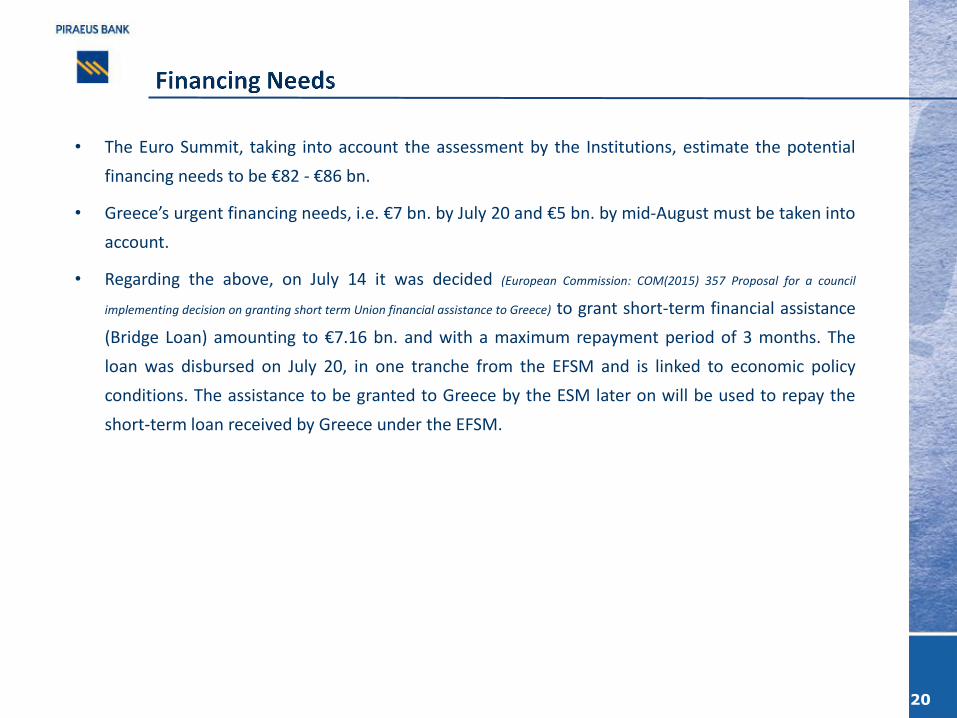

• The Euro Summit, taking into account the assessment by the Institutions, estimate the potential

financing needs to be €82 - €86 bn.

• Greece’s urgent financing needs, i.e. €7 bn. by July 20 and €5 bn. by mid-August must be taken into

account.

• Regarding the above, on July 14 it was decided (European Commission: COM(2015) 357 Proposal for a council

implementing decision on granting short term Union financial assistance to Greece) to grant short-term financial assistance

(Bridge Loan) amounting to €7.16 bn. and with a maximum repayment period of 3 months. The

loan was disbursed on July 20, in one tranche from the EFSM and is linked to economic policy

conditions. The assistance to be granted to Greece by the ESM later on will be used to repay the

short-term loan received by Greece under the EFSM.

21

• According to the “Greece - Assessment of the Commission, in liaison with the ECB, of the request

for stability support in the form of an ESM loan, 10 July 2015” the financing needs are expected to

amount to €81.7 bn from August 2015-July 2018.

New 3-year ESM programme

from the beginning Aug 15- end Jul 18

Gross financing needs 81.7

Amortisation 33.8

Repayment IMF and BoG loans 2.1

Interest payments 17.8

Arrears clearance 7

Cash buffer for deposit build-up 4.5

Privatisation (-) -2.5

Cash general government primary surplus* (-) -6

Bank recapitalisation 25

Potential Financing sources 7.7

SMP/ANFA profits 7.7

Financing gap 74

Note: The cash primary balance is calculated based on the accrual fiscal targets and adjusted to cash. Although the programme is expected to start only at the beginning of August, the programme financing envelope also covers the clearance of the external arrears and the financing gap of July.

• Regarding the IMF contribution, it is not possible to estimate the final amount of financing, as until

recently Greece was in arrears with the fund. Hence, no disbursement is allowed. However, according to

the Second Program (EFF), maturing on March 2016, a total amount of €16 bn. is available for

disbursement.

22

• Based on the most recent IMF report “An Update of IMF Staff’s Preliminary Public Debt

Sustainability Analysis, 14 July 2015”, Greece’s public debt has become significantly unsustainable.

• This is due to the policy relaxation last year and the recent deterioration of the domestic

macroeconomic and financial environment amidst the closing down of the banking system (bank

holiday).

• Public debt is expected to peak at 200% of GDP in the next two years, provided that there is be a

quick agreement on a new Memorandum of Understanding.

• Greek public debt can become sustainable only through relief measures that far exceed what

Europe has addressed so far. Among various options, if a debt relief through maturity extension

is chosen, there would have to be a very dramatic extension with grace periods of approximately

30 years on the entire stock of European debt, including the new assistance.

23

Based on the most recent: “Greece - Assessment of the Commission, in liaison with the ECB, of the

request for stability support in the form of an ESM loan, 10 July 2015”:

• According to the Baseline Scenario, public debt is expected to reach 165% of GDP in 2020, 150% in

2022 and 111% in 2030, while according to the Adverse Scenario public debt is expected to be 187%

in 2020, 176% in 2022 and 142% in 2030.

• The debt sustainability challenge can be addressed through the implementation of a comprehensive

and credible reform agenda. Debt relief measures will be proposed if the commitments for structural

reforms are implemented.

• A maturity extension of the existing and new loans, debt servicing extension and AAA rates will

smooth financing needs, although the debt to GDP ratio will remain high for a long period.

At the July 12 Euro Summit, it was emphasized that it is not possible to proceed with a nominal debt

haircut.

24

DATE EVENTS LINKS

NEGOTIATIONS FOR 3RD BAILOUT PROGRAMME

22/07/15 Greek Parliament votes for the 2nd set of prior actions

20/07/15 Repayment of ECB and BoG due obligations

20/07/15 Repayment by Greece of the totality of its due obligations to the IMF link

20/07/15 End of bank holiday with capital controls continuing

20/07/15 Bridge loan of €7.16 bn is paid from thee EFSM to Greece link

17/07/15 EU Commission approves the granting of the EFSM bridge loan link

17/07/15 ESM Governing Council approves in principle granting of stability support to Greece link

16/07/15 ECB agrees to increase support to Greek banks by €900 mn

16/07/15 Eurogroup decides to grant in principle 3-year ESM stability support to Greece link

15/07/15 Greek Parliament votes for urgent regulation (1st set of prior actions) for an ESM agreement link

12/07/15 EU Summit sets conditions for potential ESM programme approval link

PRE AGREEMENT

05/07/15 Referendum

30/06/15 Termination of the 2nd economic support programme of Greece

30/06/15 Non repayment of SDR 1.2 bn by Greece to IMF link

29/06/15 HCMC Legislative Act regarding ATHEX closure during bank holiday link

29/06/15 Bank holiday - capital controls begin (28/06 relevant decision)

28/06/15 ECB maintains ceiling for ELA unchanged link

27/06/15 Eurogroup – Verifies non agreement link

27/06/15 Referendum voted for by Greek Parliament

Disclaimer: This note constitute an investment advertisement, is intended solely for information purposes and it cannot in any way be considered investment

advice, offer or recommendation to enter into any transaction. The information included in this note may not be construed as suitable investment for the holder,

nor may it be considered as an instrument to accomplish specific investment goals or relevant financial needs of the holder and may neither be reckoned as a

substitute to relevant contractual agreements between the Bank and the holder. Before entering into any transaction each individual investor should evaluate the

information contained in this note and not base his/her decision solely on the information provided. This note cannot be considered investment research and

consequently it was not compiled by Piraeus Bank according to the requirements of the law that are intended to ensure independence in the sector of investment

research. Information comprised in this note is based on publically available sources that are considered to be reliable. Piraeus Bank cannot be held accountable

for the accuracy or completeness of the information contained in this note. Views and estimates brought forward in this note represent domestic and international

market trends on the date indicated in the note and they are subject to alteration without previous warning. Piraeus Bank may also include in this note investment

research done by third parties. This information is not modified in any way, consequently the Bank cannot be held accountable for the content. The Piraeus Bank

Group is and organization with a considerable domestic and international presence, and provides a great variety of investment services. In cases where conflicts

of interest issues should arise while Piraeus Bank or the rest of the companies of the group provide investment services in relation to the information provided in

this note, Piraeus Bank and the companies of the Group should be underlined that (the list is not exhaustive): a) No restrictions apply in dealing for own account,

or with regards to trading in relation to portfolios managed by Piraeus Bank or companies of its group before the publication of this note, or with regards to trading

before an initial public offer. b) It is possible that investment or additional services are provided to the issuers included in this note against a fee. c) It is possible

that Bank or any of its subsidiaries participate in the share capital of any of the issuers included in this note or may attract other interests financial or not from them.

d) The Bank or any of its subsidiaries may act a market maker or an underwriter for any of the issuers included in the note. e) Piraeus Bank may have issued

similar notes with different or incompatible content with the content of this note. It should be explicitly noted that: a) Figures refer to past performances and past

performances do not constitute a safe indication for future performances. b) Figures constitute simulation of past performances and they are not a safe indication

of future performances. c) Any projections or other estimates are not safe indications for future performances. d) Taxation treatment of information provided in this

note may differ according to the rules that govern each individual investor. Therefore the holder should seek independent advice in relation to taxation rules that

may affect him/her. e) Piraeus Bank is not under any obligation to keep data and information provided herein updated.

25