grad Macroeconomics I(SET4)

40

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 1 MACROECONOMICS BGSE/UPF LECTURE SLIDES SET 4 Professor Antonio Ciccone

Transcript of grad Macroeconomics I(SET4)

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 1

MACROECONOMICSBGSE/UPF

LECTURE SLIDES SET 4Professor Antonio Ciccone

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 2

3. Applications of the Ramsey-Cass-Koopmans (RCK) model

3.1 Government spending, consumption, and interest rates

3.2 Bond versus tax financed government spending

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 3

3.1 Government spending, consumption, and interest rates

- Comparative “dynamics” in the RCK model

- Permanent, surprise drop in output

- Temporary, surprise drop in output

- Wars, government expenditures and interest rates

- The role of expectations- Permanent, anticipated drop in output

- Temporary, anticipated drop in output

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 4

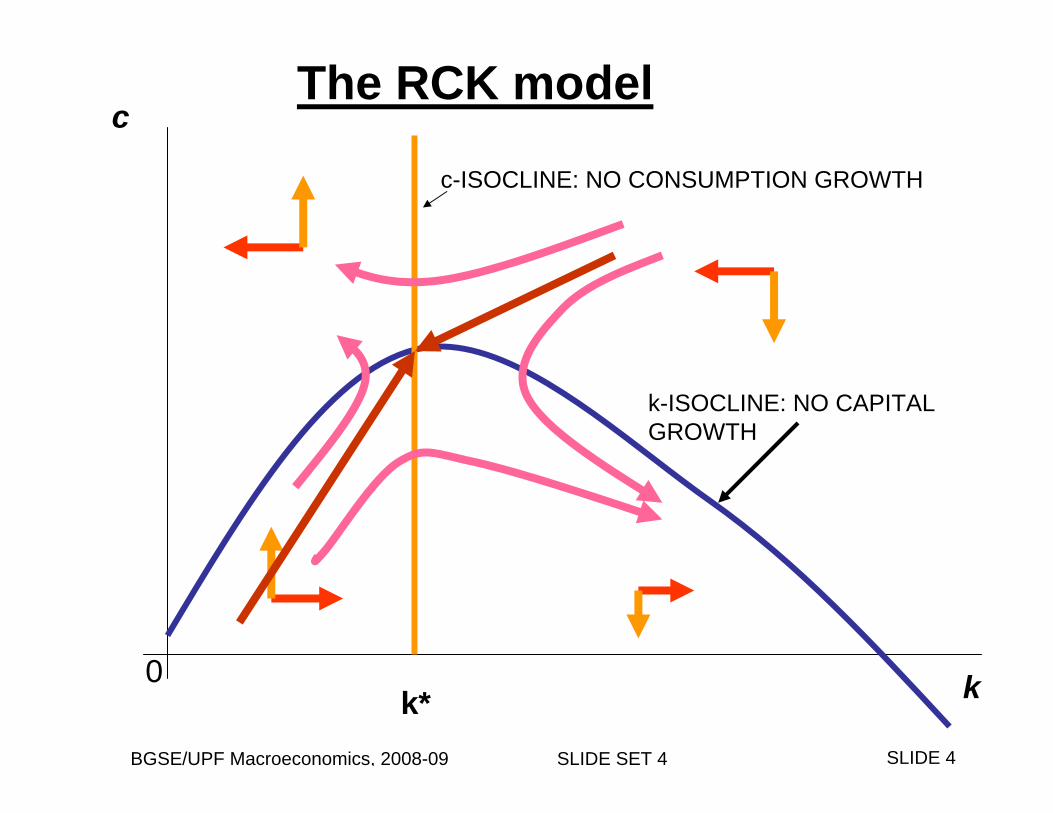

k

c

k-ISOCLINE: NO CAPITAL GROWTH

c-ISOCLINE: NO CONSUMPTION GROWTH

k*0

The RCK model

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 5

k

c

k-ISOCLINE: NO CAPITAL GROWTH

c-ISOCLINE: NO CONSUMPTION GROWTH

k*0

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 6

k

c

NEW k-ISOCLINE: NO CAPITAL GROWTH

c-ISOCLINE: NO CONSUMPTION GROWTH

k*0

Permanent, surprise fall in output for given k

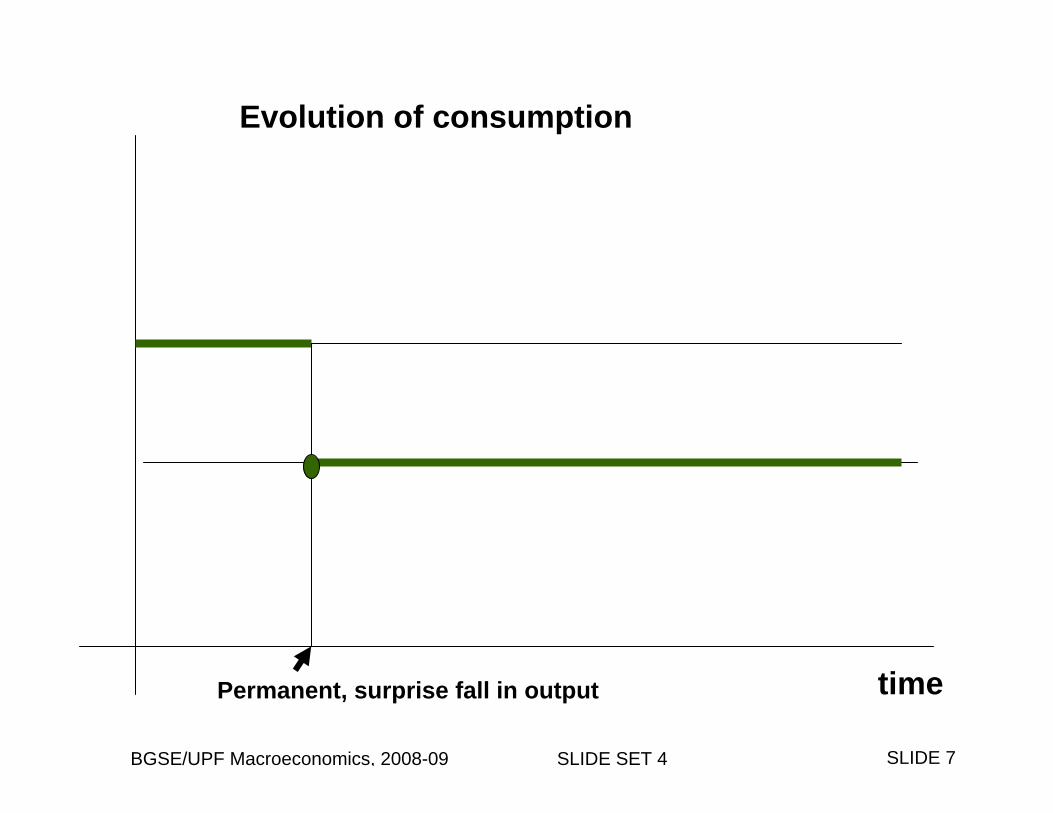

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 7

timePermanent, surprise fall in output

Evolution of consumption

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 8

timePermanent, surprise fall in output

Evolution of capital intensity

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 9

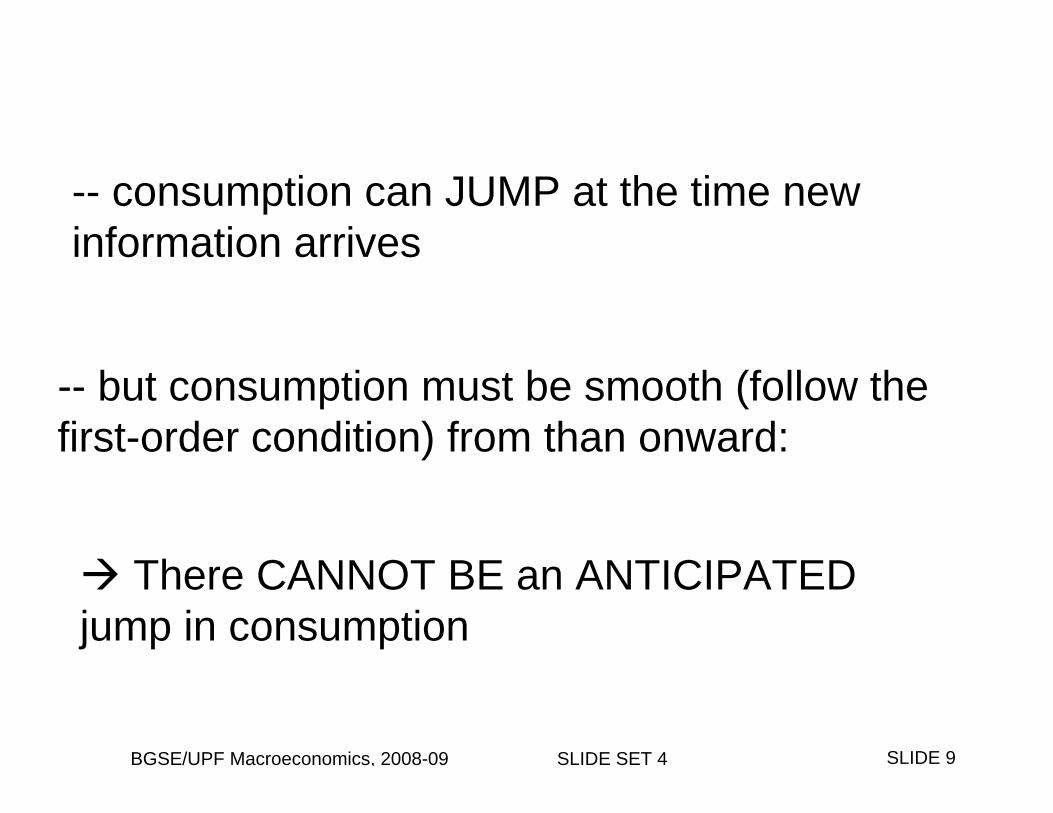

-- consumption can JUMP at the time newinformation arrives

-- but consumption must be smooth (follow thefirst-order condition) from than onward:

There CANNOT BE an ANTICIPATED jump in consumption

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 10

k

c

NEW k-ISOCLINE: NO CAPITAL GROWTH

c-ISOCLINE: NO CONSUMPTION GROWTH

k*0

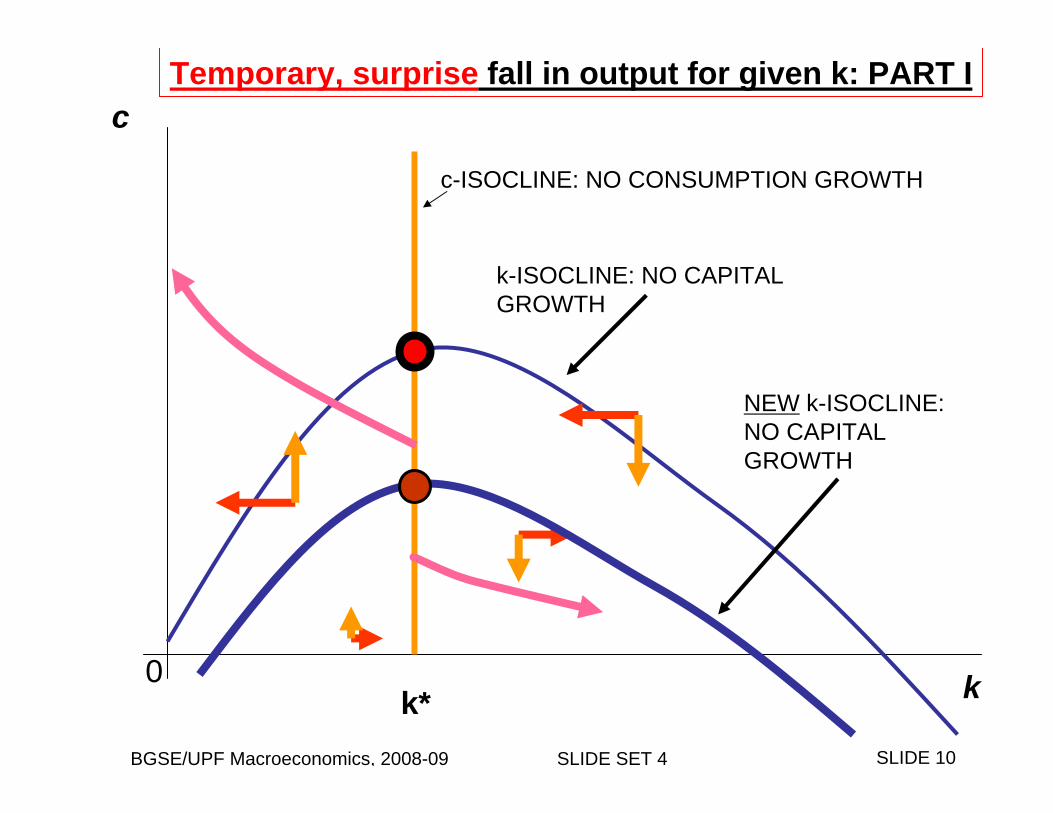

Temporary, surprise fall in output for given k: PART I

k-ISOCLINE: NO CAPITAL GROWTH

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 11

k

c

k-ISOCLINE: NO CAPITAL GROWTH

c-ISOCLINE: NO CONSUMPTION GROWTH

k*0

Temporary, surprise fall in output for given k: PART II

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 12

k

c

NEW k-ISOCLINE: NO CAPITAL GROWTH

c-ISOCLINE: NO CONSUMPTION GROWTH

k*0

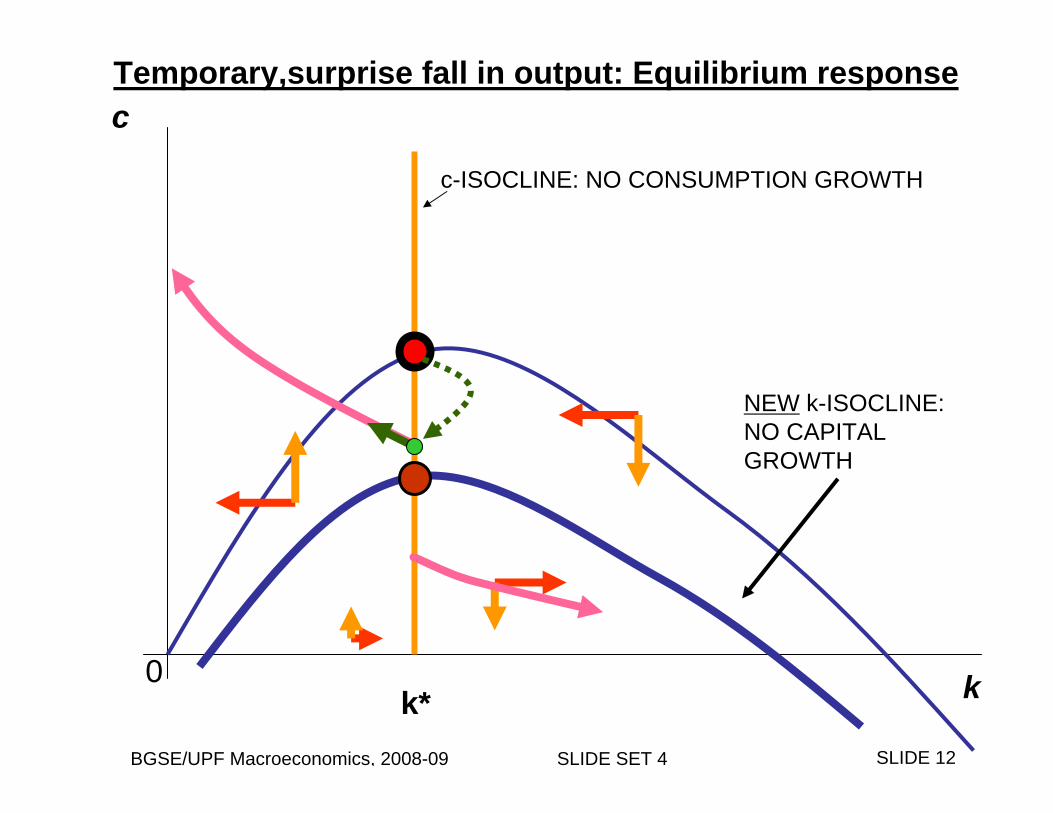

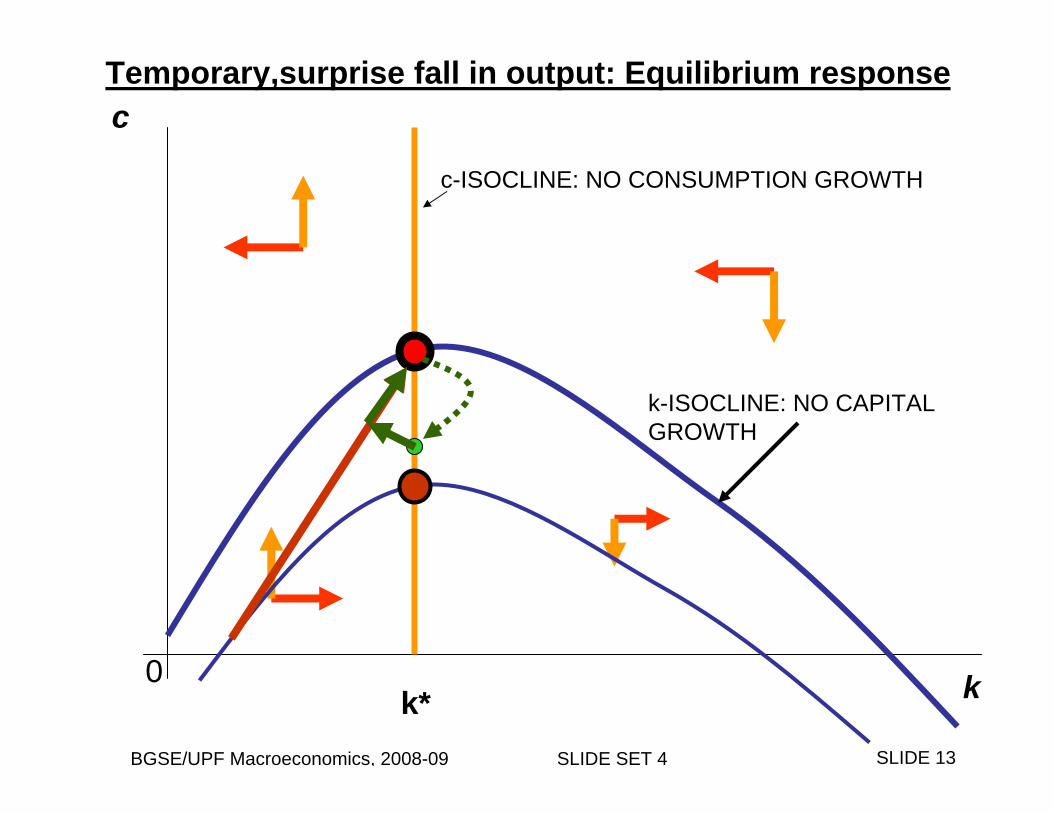

Temporary,surprise fall in output: Equilibrium response

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 13

k

c

k-ISOCLINE: NO CAPITAL GROWTH

c-ISOCLINE: NO CONSUMPTION GROWTH

k*0

Temporary,surprise fall in output: Equilibrium response

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 14

timeSTART of Tempfall in output

END of Tempfall in output

Evolution of the capital intensity

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 15

timeSTART of Tempfall in output

END of Tempfall in output

Evolution of real interest rate

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 16

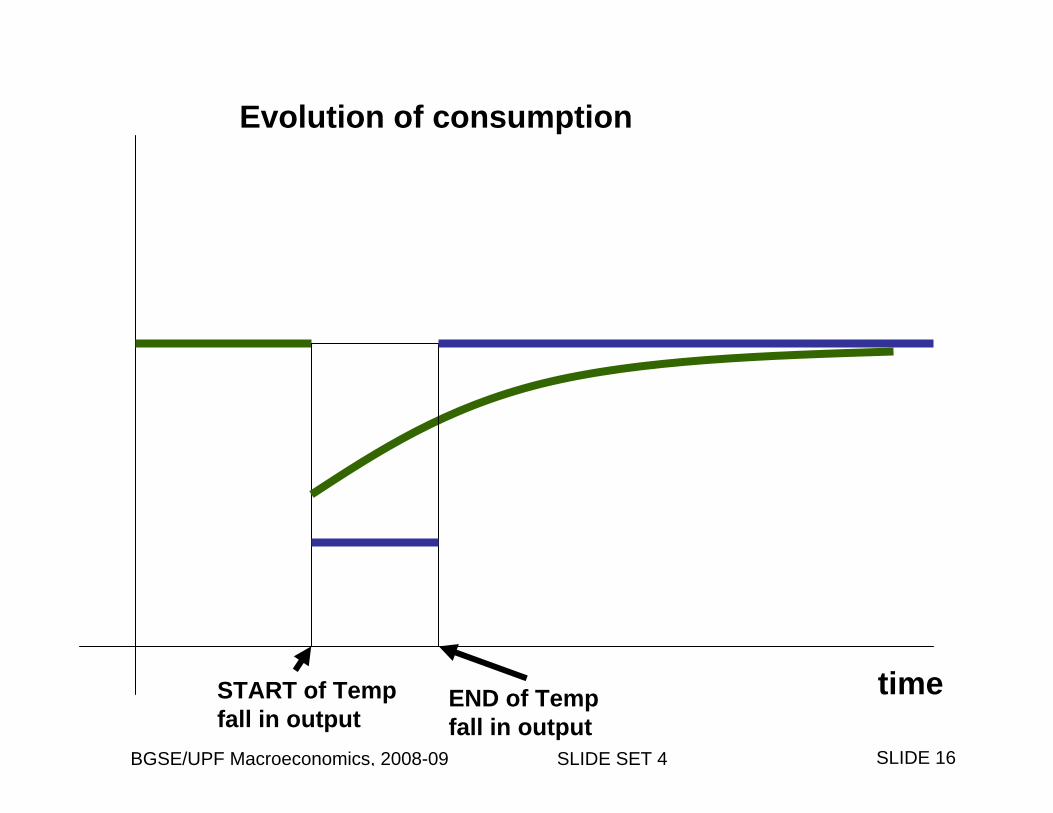

timeSTART of Tempfall in output

Evolution of consumption

END of Tempfall in output

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 17

Wars and real interest rates

-- Suppose government expenditures associated withwars are surprise, temporary events

-- Study the dynamic response of: capital, interest rates, and consumption to wars

-- Government expenditures associated with warsdecrease output available for consumption andinvestment

( , )F K L G C I− = +

INCREASE G Same effect as temporary fall in output

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 18

timeSTART of War END of War

Evolution of real interest rate

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 19

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 20

- The role of expectations

- Permanent, anticipated drop in output

- Temporary, anticipated drop in output

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 21

k

c

k-ISOCLINE: NO CAPITAL GROWTH

c-ISOCLINE: NO CONSUMPTION GROWTH

k*0

Permanent, anticipated fall in output: PART I

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 22

k

c

NEW k-ISOCLINE: NO CAPITAL GROWTH

c-ISOCLINE: NO CONSUMPTION GROWTH

k*0

Permanent, anticipated fall in output: PART II

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 23

k

c

NEW k-ISOCLINE: NO CAPITAL GROWTH

c-ISOCLINE: NO CONSUMPTION GROWTH

k*0

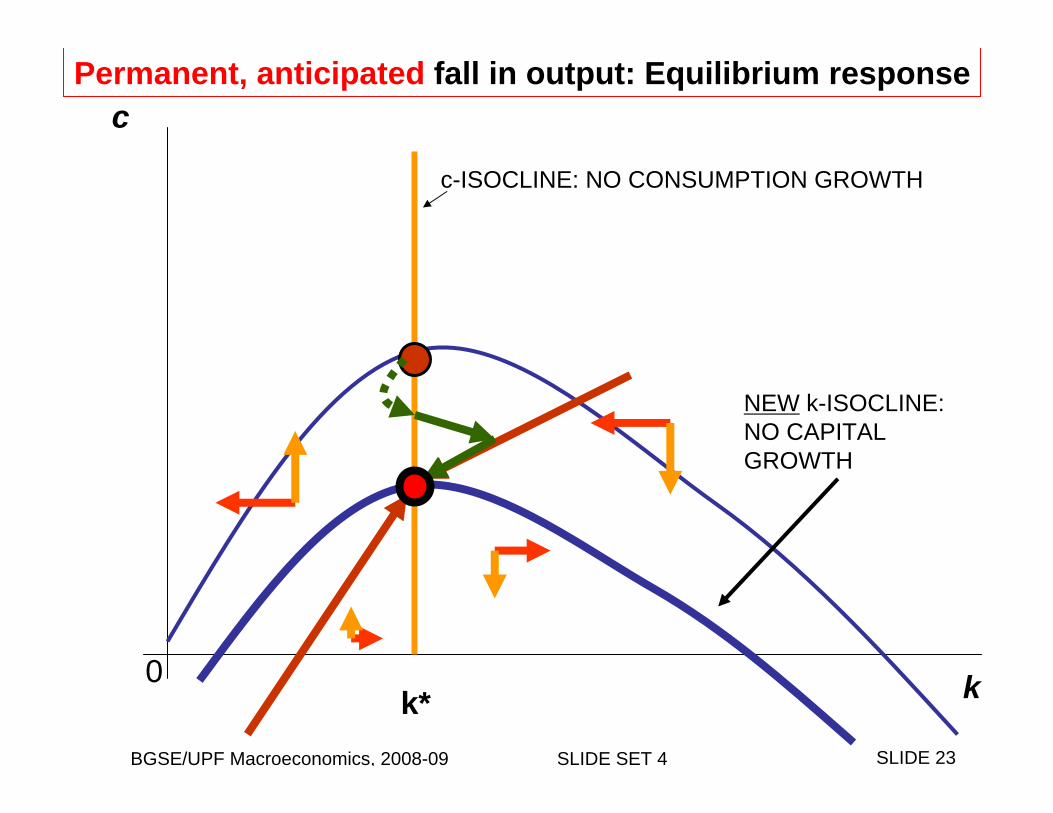

Permanent, anticipated fall in output: Equilibrium response

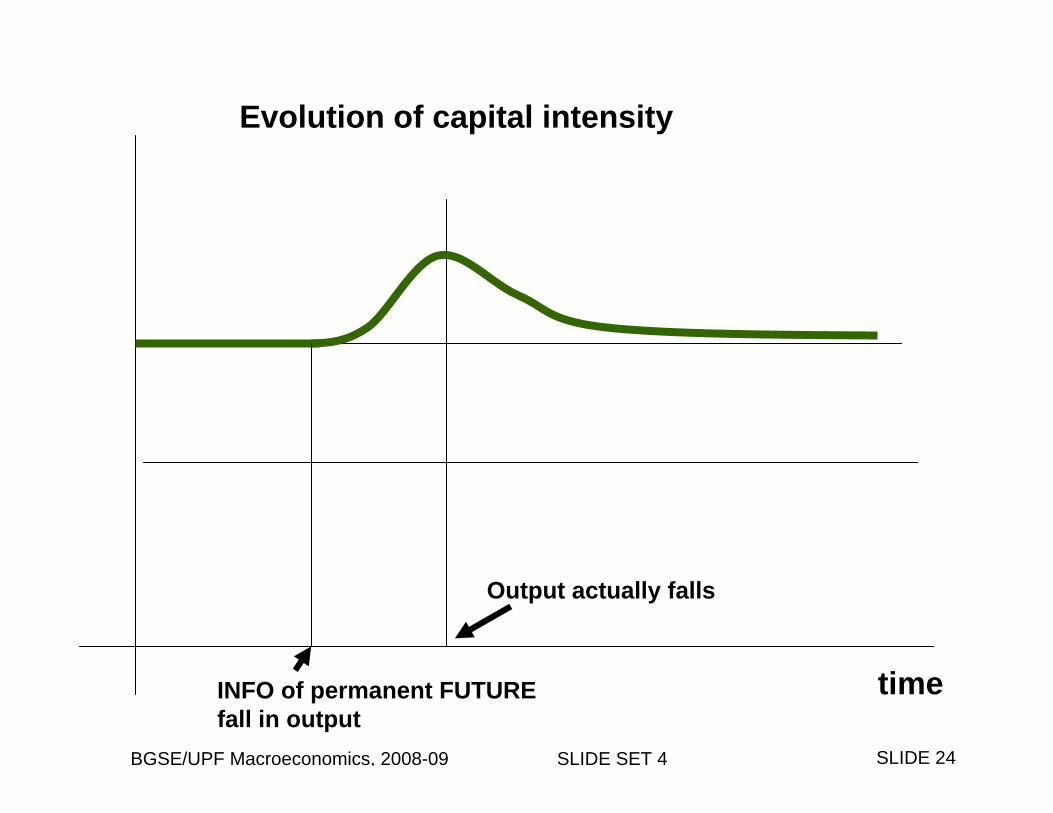

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 24

timeINFO of permanent FUTUREfall in output

Evolution of capital intensity

Output actually falls

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 25

timeINFO of permanent FUTUREfall in output

Evolution of consumption

Output actually falls

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 26

- The role of expectations

- Permanent, anticipated drop in output

- Temporary, anticipated drop in output

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 27

k

c

k-ISOCLINE: NO CAPITAL GROWTH

c-ISOCLINE: NO CONSUMPTION GROWTH

k*0

Temporary, anticipated fall in output for given k: PART I

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 28

k

c

NEW k-ISOCLINE: NO CAPITAL GROWTH

c-ISOCLINE: NO CONSUMPTION GROWTH

k*0

Temporary, anticipated fall in output for given k: PART II

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 29

k

c

k-ISOCLINE: NO CAPITAL GROWTH

c-ISOCLINE: NO CONSUMPTION GROWTH

k*0

Temporary, anticipated fall in output for given k: PART III

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 30

k

c

k-ISOCLINE: NO CAPITAL GROWTH

c-ISOCLINE: NO CONSUMPTION GROWTH

k*0

Temporary, anticipated fall in output: Equilibrium response

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 31

k

c

k-ISOCLINE: NO CAPITAL GROWTH

c-ISOCLINE: NO CONSUMPTION GROWTH

k*0

Temporary, anticipated fall in output: Equilibrium response

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 32

timeINFO of FUTURETemp fall in output

END of Tempfall in output

Evolution of the capital intensity

START of FUTURETemp fall in output

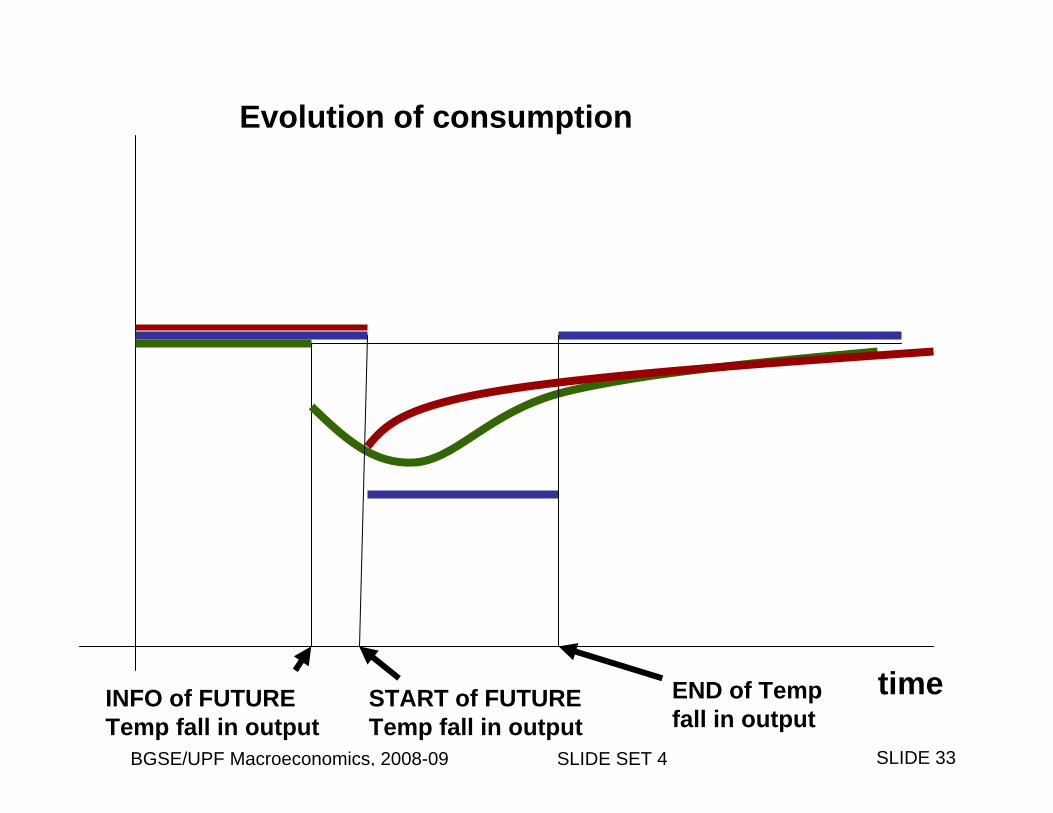

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 33

time

Evolution of consumption

INFO of FUTURETemp fall in output

END of Tempfall in output

START of FUTURETemp fall in output

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 34

3. Application of the Ramsey-Cass-Koopmans (RCK) model

3.1 Government spending, consumption, and interest rates

3.2 Bond versus tax financed government spending

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 35

Government expenditures and taxes

t t tGDEFICIT G T= −

Government intertemporal budget constraint

0 00 0

t t t t tPV T dt GWEALTH PV G dt∞ ∞

+ =∫ ∫

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 36

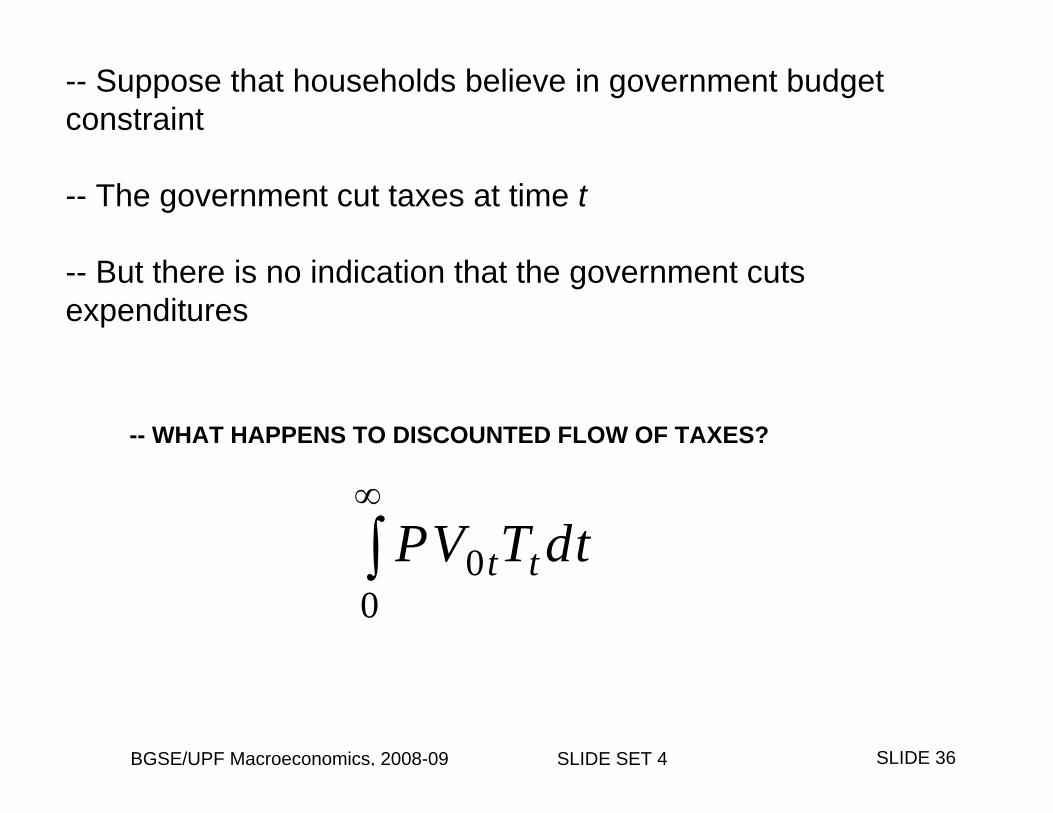

-- Suppose that households believe in government budgetconstraint

-- The government cut taxes at time t

-- But there is no indication that the government cutsexpenditures

00

t tPV T dt∞

∫

-- WHAT HAPPENS TO DISCOUNTED FLOW OF TAXES?

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 37

Nothing, because:

0 00 0

t t t t tPV T dt PV G dt GWEALTH∞ ∞

= −∫ ∫

and the right-hand side of this equation has not changed.

Government will have to compensate current tax cut by taxincrease sometime in the future.

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 38

Now let’s look at household intertemporal budget constraint:

0 00 0

0 00

t t t t

t t

PV C dt PV T dt

PV w Ldt Q

∞ ∞

∞

+

= +

∫ ∫

∫

-- current tax cut does NOT affect this constraint at all as onlythe DISCOUNTERD PRESENT VALUE OF TAXES MATTERS

-- and present value of taxes remains constant if expendituresdo not change

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 39

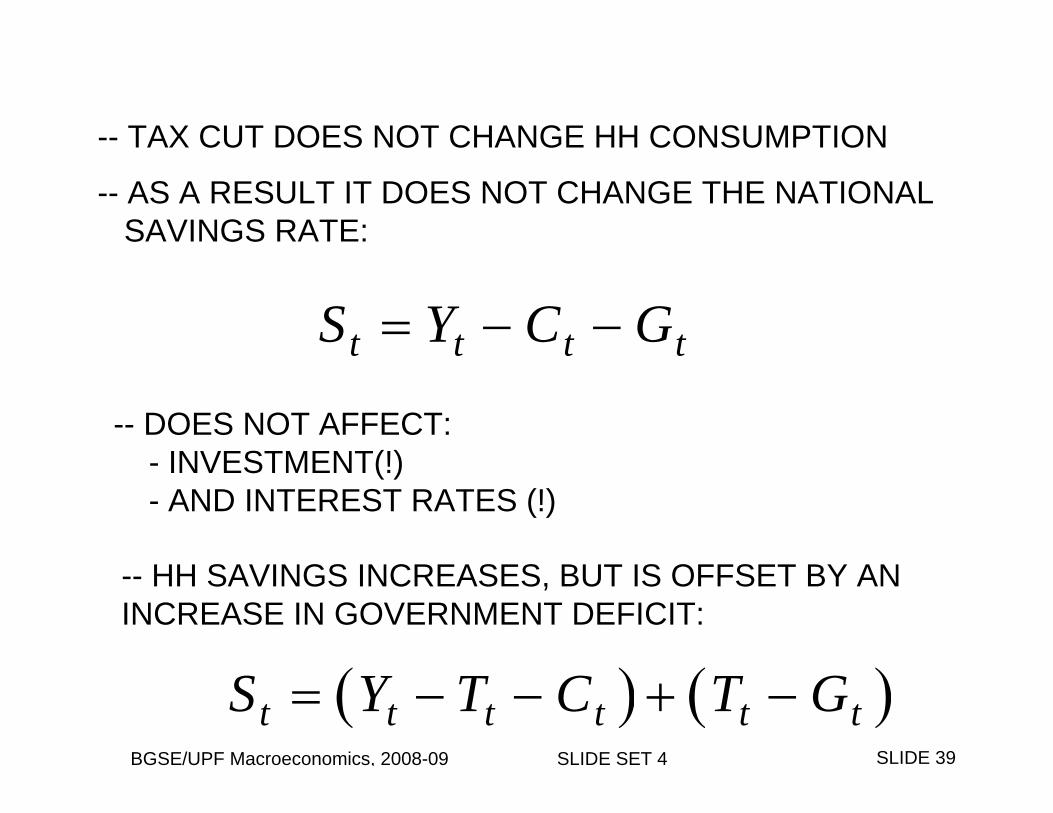

-- TAX CUT DOES NOT CHANGE HH CONSUMPTION

-- AS A RESULT IT DOES NOT CHANGE THE NATIONALSAVINGS RATE:

t t t tS Y C G= − −

-- DOES NOT AFFECT:- INVESTMENT(!) - AND INTEREST RATES (!)

-- HH SAVINGS INCREASES, BUT IS OFFSET BY AN INCREASE IN GOVERNMENT DEFICIT:

( ) ( )t t t t t tS Y T C T G= − − + −

BGSE/UPF Macroeconomics, 2008-09 SLIDE SET 4 SLIDE 40

Hence, government cuts taxes

Has to issue debt (government bonds)Government ensures that real interest rate on bond mimics

market interest rate (before issue of new bonds)Households buy these new bonds with their tax savings

Hence,Household use to buy government bonds what they “save”

in current taxes