GovMark Luncheon€¦ · Suggested Workflow Optimization Machine-Generated and -Managed Automation...

29

CONFIDENTIAL AND PROPRIETARY This presentation, including any supporting materials, is owned by Gartner, Inc. and/or its affiliates and is for the sole use of the intended Gartner audience or other intended recipients. This presentation may contain information that is confidential, proprietary or otherwise legally protected, and it may not be further copied, distributed or publicly displayed without the express written permission of Gartner, Inc. or its affiliates. © 2017 Gartner, Inc. and/or its affiliates. All rights reserved. GovMark Luncheon November 15, 2017 Katell Thielemann, Research VP

Transcript of GovMark Luncheon€¦ · Suggested Workflow Optimization Machine-Generated and -Managed Automation...

CONFIDENTIAL AND PROPRIETARYThis presentation, including any supporting materials, is owned by Gartner, Inc. and/or its affiliates and is for the sole use of the intended Gartner audience or other intended recipients. This presentation may contain information that is confidential, proprietary or otherwise legally protected, and it may not be further copied, distributed or publicly displayed without the express written permission of Gartner, Inc. or its affiliates. © 2017 Gartner, Inc. and/or its affiliates. All rights reserved.

GovMark Luncheon

November 15, 2017

Katell Thielemann, Research VP

1 © 2017 Gartner, Inc. and/or its affiliates. All rights reserved.

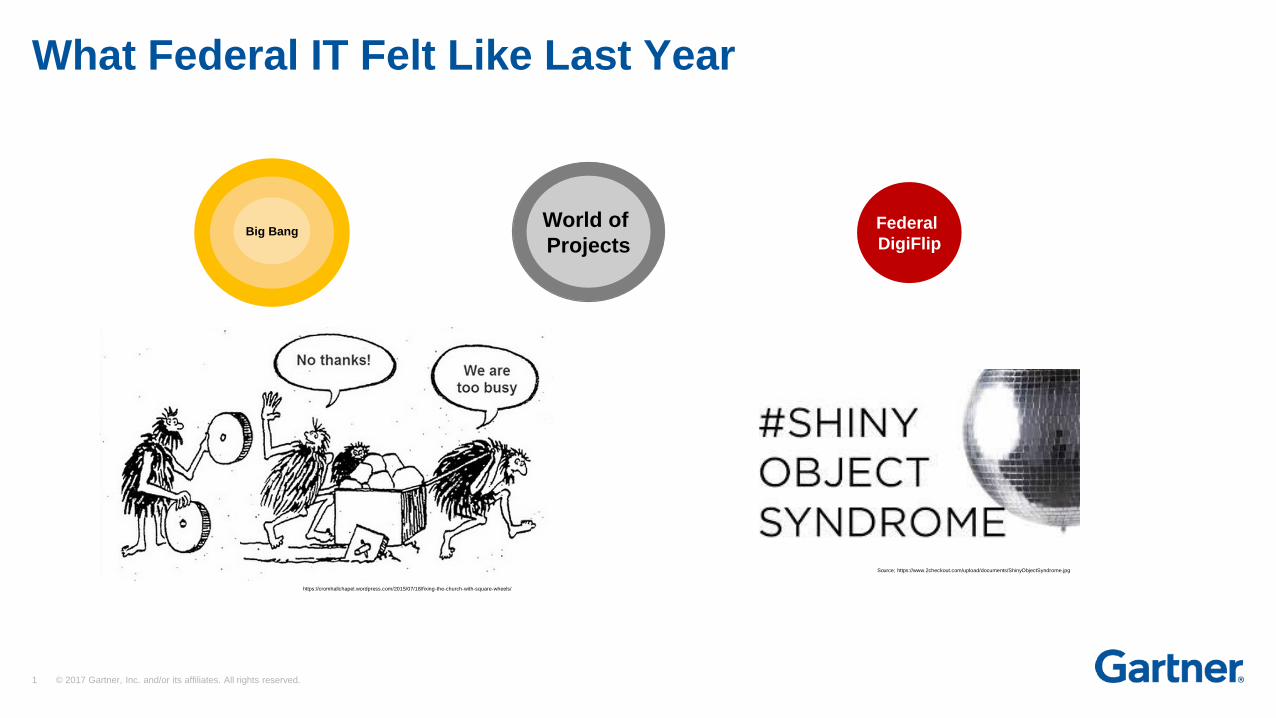

What Federal IT Felt Like Last Year

Source; https://www.2checkout.com/upload/documents/ShinyObjectSyndrome.jpg

https://cromhallchapel.wordpress.com/2015/07/18/fixing-the-church-with-square-wheels/

Big BangWorld of

ProjectsFederal

DigiFlipBig Bang

2 © 2017 Gartner, Inc. and/or its affiliates. All rights reserved.

What It Feels Like Today

3 © 2017 Gartner, Inc. and/or its affiliates. All rights reserved.

CYBERCOM

OPM

Hack

Shared

Services

NDAA

GWAC

Consolidation

FedRAMP

BPAs

Set-asides

NIST

SP 800-171

FITARA

/DCOI

XaaS

TechFAR

Category

MgtDigital

Natives

Moving In

Agile/DevOps

MEGABYTE

Act

Digital

Platforms

Federal

Natives

M&A

The Trail Has Become Increasingly Complex to Navigate

4 © 2017 Gartner, Inc. and/or its affiliates. All rights reserved.

And the Destination is Not Yet all that Clear

Executive - Policy

White House Office of American Innovation and American Technology Council

OMB Reorganization Memo and Capital Planning & Investment Control (CPIC) Process update

Cybersecurity Executive Order

IT Modernization Plan

DepSecDef Cloud Acceleration Memo

Legislative

DATA Act (financial transparency)

FITARA (CIO role)

MEGABYTE (Software)

PMIAA (Project Management)

NDAA – Changes in Roles; New Procurement Mandates

MGT Act (IT Modernization)

2018 and beyond Budget Requests

and IT Spend Priorities

5 © 2017 Gartner, Inc. and/or its affiliates. All rights reserved.5 © 2017 Gartner, Inc. and/or its affiliates. All rights reserved.

Yet the Path Forward is Marked – and Driven by Technology

6 © 2017 Gartner, Inc. and/or its affiliates. All rights reserved.6 © 2017 Gartner, Inc. and/or its affiliates. All rights reserved.

Markers Already Here

7 © 2017 Gartner, Inc. and/or its affiliates. All rights reserved.

Profound Shifts are Underway

“Butts in Seats”Automation,

Smart Machinesreduces need for

On-Prem InfrastructureCloud threatens business in

UpskillingSoftware Shift Increases need for

New EntrantsOpen Source, Falling costs,

Platforms, New Technologiesprovide opening for

Become SellersBuyers building own

Technology Expertiseallows buyers to

8 © 2017 Gartner, Inc. and/or its affiliates. All rights reserved.

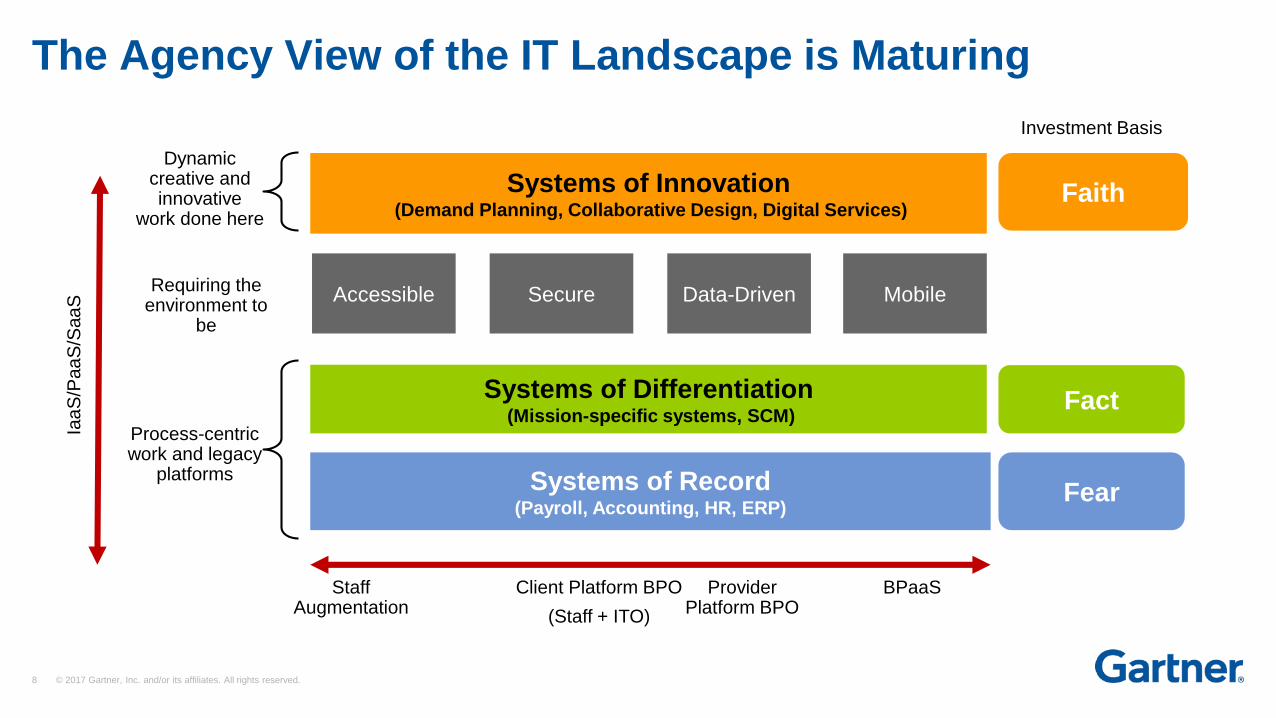

The Agency View of the IT Landscape is Maturing

Process-centric work and legacy

platforms

Dynamiccreative andinnovative

work done here

Requiring theenvironment to

be

Systems of Record(Payroll, Accounting, HR, ERP)

Systems of Differentiation(Mission-specific systems, SCM)

Systems of Innovation(Demand Planning, Collaborative Design, Digital Services)

Data-DrivenAccessible Secure Mobile

Staff Augmentation

Client Platform BPO

(Staff + ITO)

Provider Platform BPO

BPaaS

Iaa

S/P

aa

S/S

aa

S

Faith

Fact

Fear

Investment Basis

9 © 2017 Gartner, Inc. and/or its affiliates. All rights reserved.

© 2017 Gartner, Inc.

Base: All answering, excludes DK, n varies by segment

Showing the 10 most common answers per segment, coded open-text responses

Thinking about your organization as a whole, what would you say are its top business objectives for

the next two year (2017/2018)?

ID: 123456

Security and Cloud Remain Top of Mind

Ten Most Common Business Objectives

Rank U.S. Federal (n = 49) Total (n = 2,615)

1 Security, safety and risk 20% Growth/market share 26%

2Technology

initiatives/improvements

14% Digital business/digital

transformation

17%

3Service

improvements/optimization

14% Profit improvement/

profitability/asset monetization

10%

4Operations improvement/

efficiency/excellence

12% Innovation, R&D, new

products/services

10%

5Cost optimization/

management/reduction

10% Customer focus 9%

6Analytics/data/information 10% Corporate/M&A/new

business/consolidation

7%

7Digital business/digital

transformation

8% Technology initiatives/

Improvements

7%

8Innovation, R&D, new

products/services

6% Cost optimization/

management/reduction

6%

9 Workforce focus 6% New customers/retention/sales 6%

10Governance, compliance,

regulations

6% Operations improvement

/efficiency/excellence

6%

Percentage of respondents

© 2017 Gartner, Inc.

Base: All answering, excludes DK, n varies by segment

Showing the 10 most common answers per segment, coded open-text responses

Which technology area do you think is most important to helping your business differentiate and win?/is

most crucial to achieving your organization’s mission?

ID: 123456

Most Important Technology That Will Differentiate Business/Are Most Crucial to Achieving Organization’s Mission

Rank U.S. Federal (n = 55) Total (n = 2, 834)

1 Cloud services/solutions 35% BI/analytics 26%

2 BI/analytics 15% Digitalization/digital marketing 14%

3 Infrastructure/data center 11% Cloud services/solutions 10%

4 Mobility/mobile applications 9% Mobility/mobile applications 6%

5Networking, voice and data

communications7% Internet of things 6%

6 Virtualization 7%Customer relationship

management5%

7 Security and risk 5% Artificial intelligence 5%

8 Industry specific solutions 4% Enterprise resource planning 5%

9 Internet of things 4% Infrastructure/data center 5%

10 Integration/interoperability 4% Automation 4%

Percentage of respondents

10 © 2017 Gartner, Inc. and/or its affiliates. All rights reserved.

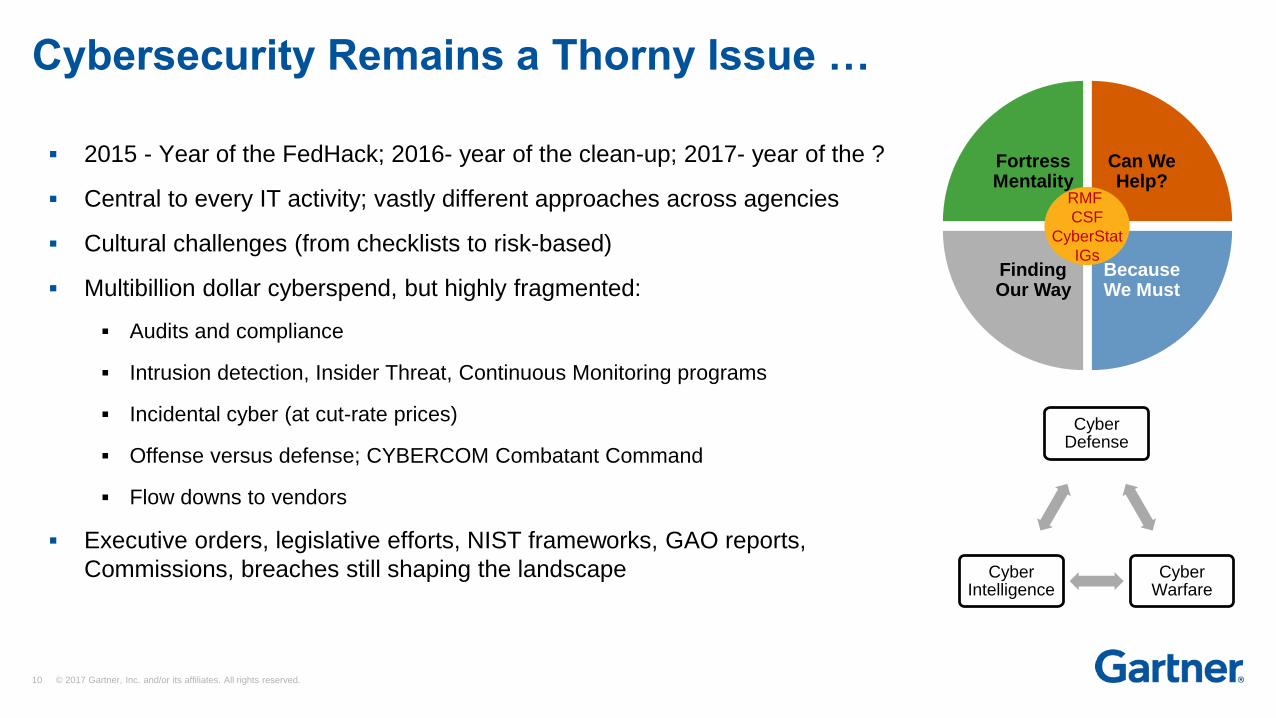

Cybersecurity Remains a Thorny Issue …

2015 - Year of the FedHack; 2016- year of the clean-up; 2017- year of the ?

Central to every IT activity; vastly different approaches across agencies

Cultural challenges (from checklists to risk-based)

Multibillion dollar cyberspend, but highly fragmented:

Audits and compliance

Intrusion detection, Insider Threat, Continuous Monitoring programs

Incidental cyber (at cut-rate prices)

Offense versus defense; CYBERCOM Combatant Command

Flow downs to vendors

Executive orders, legislative efforts, NIST frameworks, GAO reports,

Commissions, breaches still shaping the landscape

Fortress Mentality

Can We Help?

Because We Must

Finding Our Way

RMF

CSF

CyberStat

IGs

Cyber Defense

Cyber Warfare

Cyber Intelligence

11 © 2017 Gartner, Inc. and/or its affiliates. All rights reserved.

Network Segmentation

Fundamentals

Secure Web Gateway

Endpoint Protection

Firewall/IPS

From To

Tools Solutions; “aaS”

Labor Hours Automation

Check lists Risk Based

Process Outcomes/Behaviors

Rules-based Attributes-based

Defender Facilitator

Perimeter Bug bounties

Controlling Understanding

Security OF Security IN

the Cloud the cloud

… But is Also Evolving Rapidly

Advanced

Network Access Control

Mobile Device Security

App White/Black Listing

Security Info & Event Mgt

Next-generation Firewall

Next

Endpoint Threat Detection/Response

Payload Analysis

Network Traffic Analysis

Higher Trust User Authentication

Net/Computer Forensics

Cloud Access Security Broker

Behavior Analysis

So Much More in the Cloud,

in Weapons Systems,

at the Edge …

12 © 2017 Gartner, Inc. and/or its affiliates. All rights reserved.

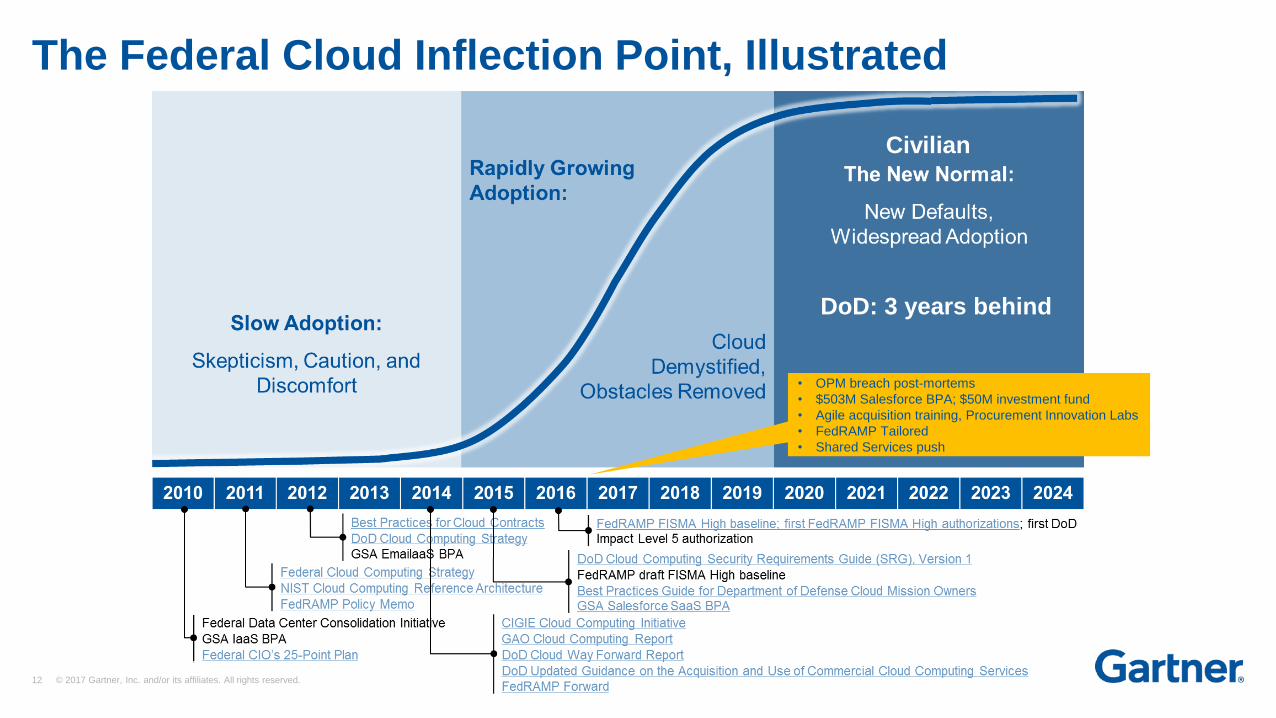

The Federal Cloud Inflection Point, Illustrated

• OPM breach post-mortems

• $503M Salesforce BPA; $50M investment fund

• Agile acquisition training, Procurement Innovation Labs

• FedRAMP Tailored

• Shared Services push

Civilian

DoD: 3 years behind

13 © 2017 Gartner, Inc. and/or its affiliates. All rights reserved.

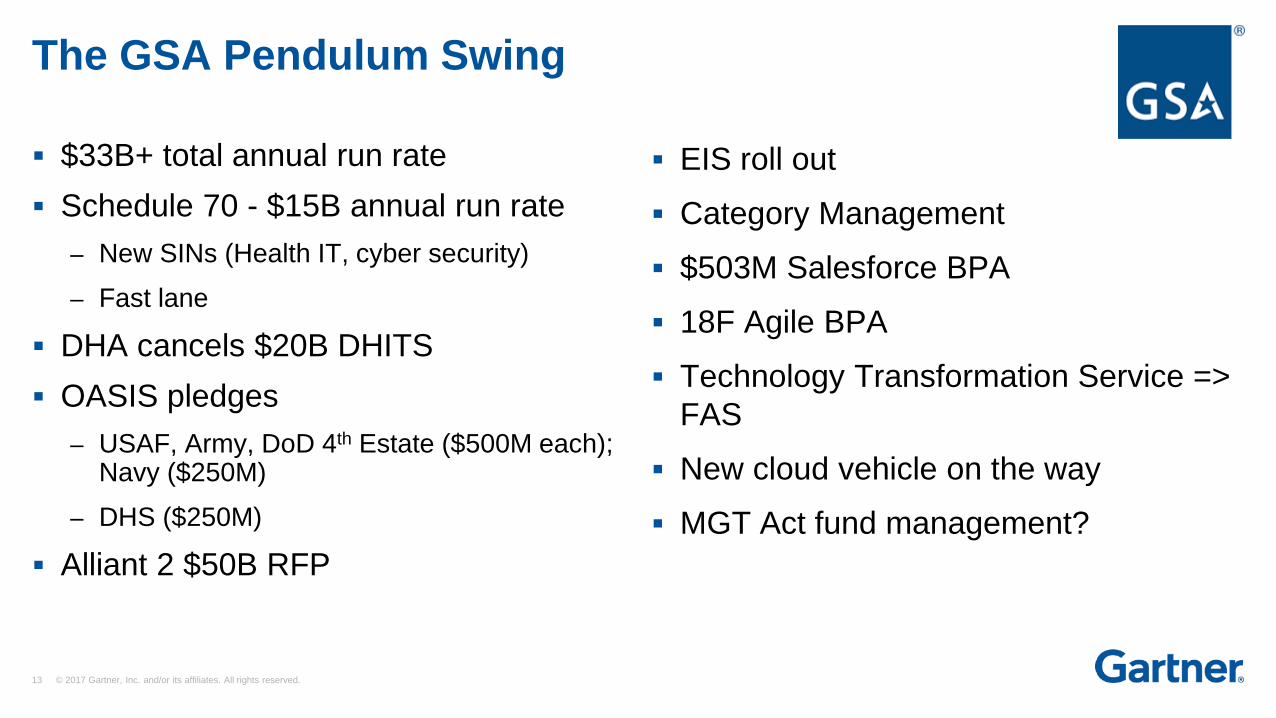

$33B+ total annual run rate

Schedule 70 - $15B annual run rate

– New SINs (Health IT, cyber security)

– Fast lane

DHA cancels $20B DHITS

OASIS pledges

– USAF, Army, DoD 4th Estate ($500M each); Navy ($250M)

– DHS ($250M)

Alliant 2 $50B RFP

EIS roll out

Category Management

$503M Salesforce BPA

18F Agile BPA

Technology Transformation Service =>

FAS

New cloud vehicle on the way

MGT Act fund management?

The GSA Pendulum Swing

14 © 2017 Gartner, Inc. and/or its affiliates. All rights reserved.

A Flurry of Recent Activity - Examples

– Lockheed Martin IS&GS => Leidos

– CSC => CSRA and DXC, then DXC + HPES =>NewCo

– Dell + EMC <=> NTT/Dell Services

– ASRC + Vistronix

– KBR + Wyle + HTSI

– CACI + Six3 Systems + L3 NSS

– BAH + Aquilent

– KEYW + Sotera

– ManTech + InfoZen

– Accenture: 7 Salesforce-related acquisitions since 2014

ClientHouse, Cloud Sherpas, CRMWaypoint, Media Hive,

New Energy Group, tquila, Phase One

Macro Trends in The Market

Weapons systems players will retrench to their core

Commoditized services providers will seek ways to

move up the tech value chain

Highly fragmented (e.g. cyber) markets will consolidate

Enterprise-oriented players will look for scale

Mission-oriented players will look for strategic niches

Set-asides and niche mid-tier will try to corner agile

and analytics markets, or develop platinum platform

relationships

Privatization considerations and Digital Ecosystems will

spur P3s and JV creation

M&A Trends are Solidifying

15 © 2017 Gartner, Inc. and/or its affiliates. All rights reserved.15 © 2017 Gartner, Inc. and/or its affiliates. All rights reserved.

Paths Coming Up

16 © 2017 Gartner, Inc. and/or its affiliates. All rights reserved.

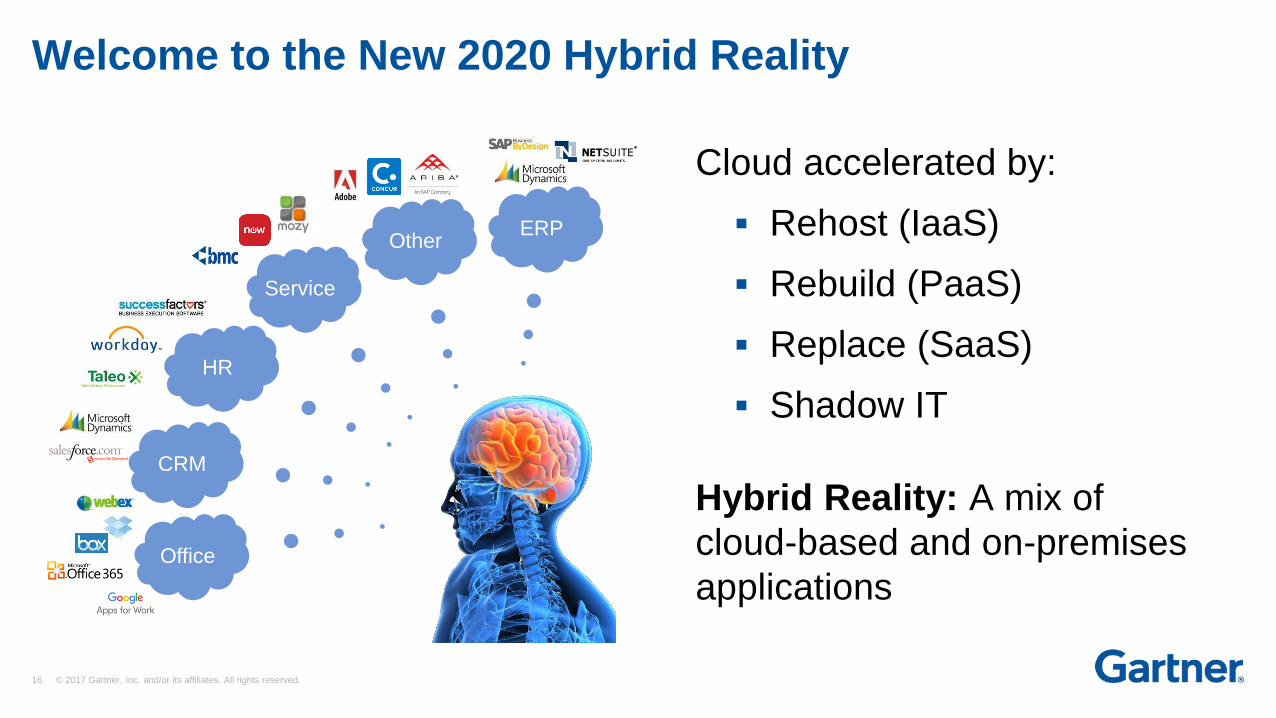

Welcome to the New 2020 Hybrid Reality

HR

Other

Service

ERP

CRM

Office

Cloud accelerated by:

Rehost (IaaS)

Rebuild (PaaS)

Replace (SaaS)

Shadow IT

Hybrid Reality: A mix of

cloud-based and on-premises

applications

17 © 2017 Gartner, Inc. and/or its affiliates. All rights reserved.

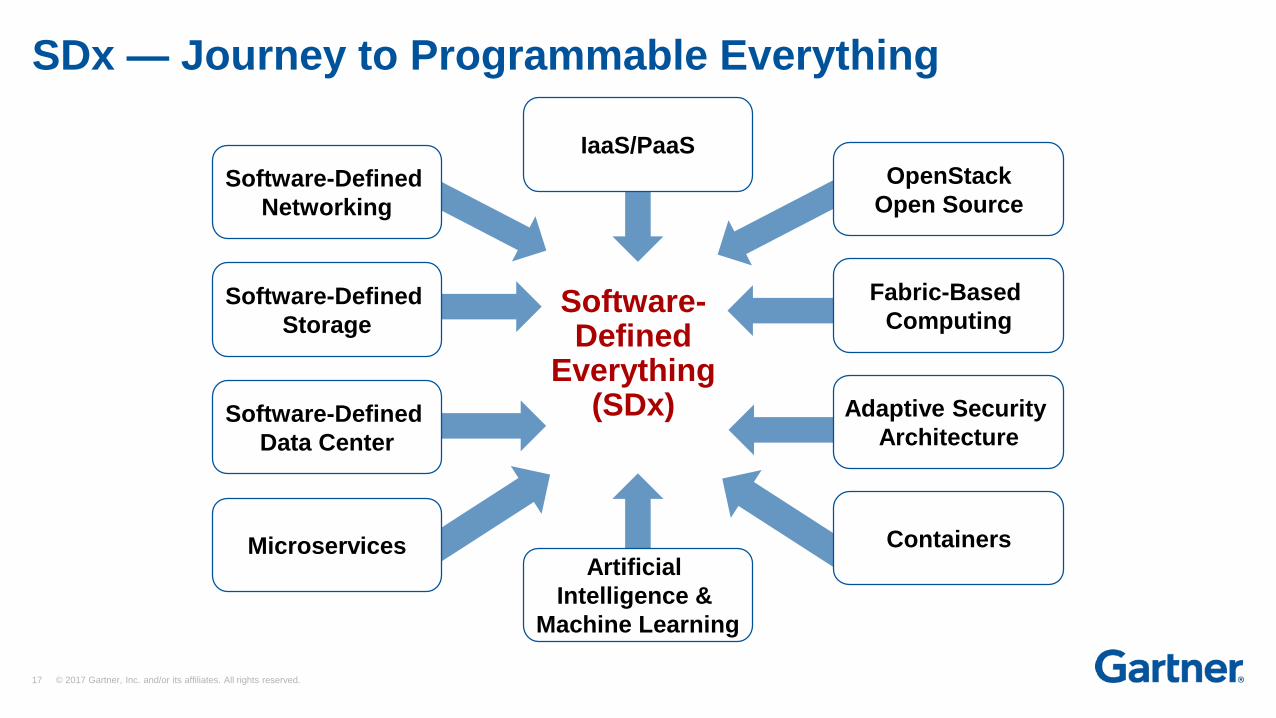

SDx — Journey to Programmable Everything

Software-Defined

Networking

Software-Defined

Storage

Software-Defined

Data Center

IaaS/PaaS

Adaptive Security

Architecture

Fabric-Based

Computing

Containers

OpenStack

Open Source

MicroservicesArtificial

Intelligence &

Machine Learning

Software-Defined

Everything(SDx)

18 © 2017 Gartner, Inc. and/or its affiliates. All rights reserved.

Enterprise Analytics Go Mainstream

Dynamically Adaptive Automation

Suggested Workflow Optimization

Machine-Generated and -Managed Automation

Contextualized Delivery of Services Across Devices

Assisted Collaboration

Intelligent Notification

Automated, "Big Data" Knowledge Management

Automation

Monitoring

Behavior Prediction

Automated Root-Cause Compare

Business Opportunity Discovery e.g., IoT

Support

BusinessValue

Dashboards

Intelligent Forecasting

Automated Business Opportunity Discovery

Dynamically Adaptive Decision Support

Machine Learning

MachineData

19 © 2017 Gartner, Inc. and/or its affiliates. All rights reserved.

From Call Centers to Engagement Hubs

1973

Voice-Only

"Call Center"

2005

Multichannel

"Contact Center"

2018

Dynamic, Multichannel

“Citizen Engagement

Center"

Cloud CRM CCaaS

VideoSocial Media Care

Self ServiceBehavioral Analytics

Cost Plus Fixed Fee per call agent

20 © 2017 Gartner, Inc. and/or its affiliates. All rights reserved.

XaaS

Agile Adoption

APIs

Low-code tools

Open source

Rise of the Digital Platforms and

Ecosystems

And Coming Soon to an Agency Near You

IntelligenceWeb

Interfaces

Mobile Interfaces

Conversational Interfaces

Citizen Experience Analytics

Citizen Experience Integration

Citizen Id and Authentication

Citizen Advisory Groups

Accessibility Compliance

Social Media

ERP

Identity and Access Management

Digital Workplace Services

Case Management

BPM

CRM

API Management

Open Data

Partner Portals

Procurement ServicesPayment Processing

Services

Data Sharing Agreements

AIMachine Learning

Geospatial and Location Analytics

Data Quality (Analytics)

Analytics Engines

BI

IoT Device Authentication

IoT Analytics

IoT GatewayIoT Security

IoT Hub

Event Stream Processing

IT Service

Management

Citizens

Collaboration

Supply Chain Management

IoT Sensors

Things

21 © 2017 Gartner, Inc. and/or its affiliates. All rights reserved.

A New Arbitrage Game

Labor Arbitrage

Better

Faster

Cheaper

Automation Arbitrage

Cheaper

Faster

Better

Intelligent Automation

Services

Next GenServices

ManagedServices

Consultingand SI

Business Strategy

Proof of Concept / Blueprint

Design/Configuration

Deploy/Integrate & Curate

Platform BPS

Managed Service of Custom Solution

Applications Management

Infrastructure Operations

Industry-specific BPaaS w/ Intelligent Automation “Platform”

Horizontal Utility Services

Ecosystems

22 © 2017 Gartner, Inc. and/or its affiliates. All rights reserved.22 © 2017 Gartner, Inc. and/or its affiliates. All rights reserved.

5 Strategic Must-Dos to Keep Heading True North

23 © 2017 Gartner, Inc. and/or its affiliates. All rights reserved.

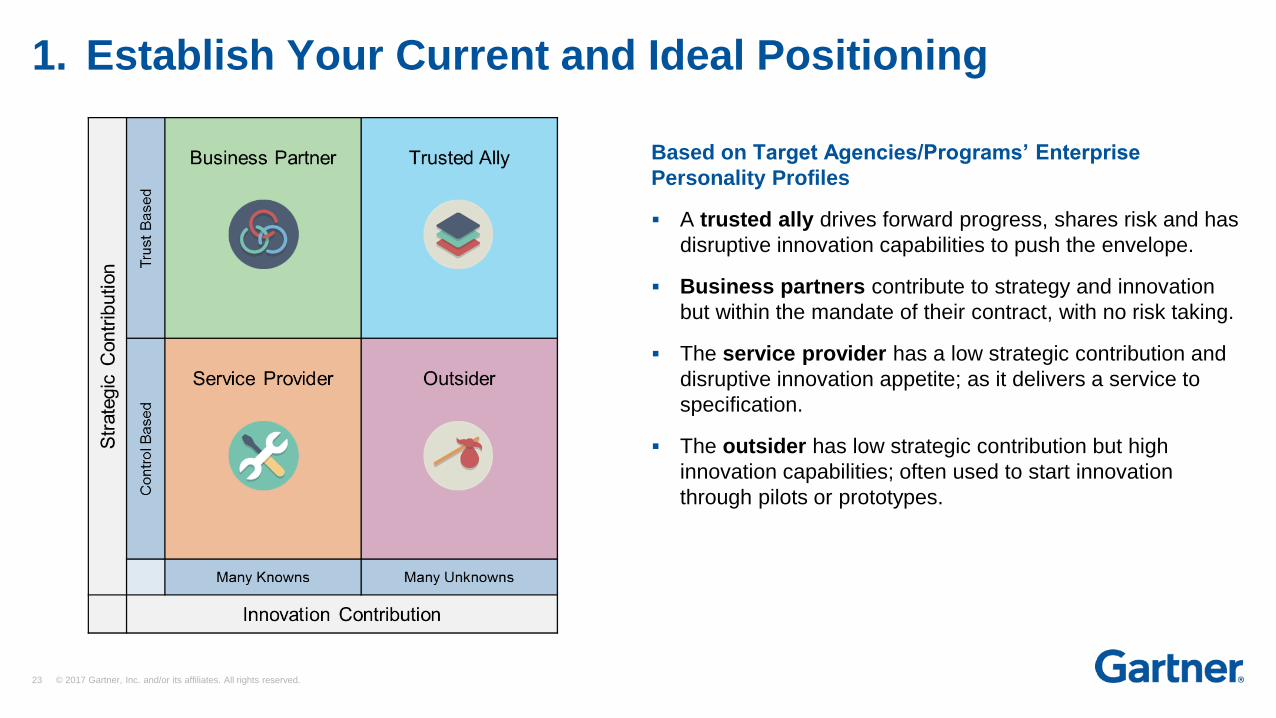

Based on Target Agencies/Programs’ Enterprise

Personality Profiles

A trusted ally drives forward progress, shares risk and has

disruptive innovation capabilities to push the envelope.

Business partners contribute to strategy and innovation

but within the mandate of their contract, with no risk taking.

The service provider has a low strategic contribution and

disruptive innovation appetite; as it delivers a service to

specification.

The outsider has low strategic contribution but high

innovation capabilities; often used to start innovation

through pilots or prototypes.

1. Establish Your Current and Ideal Positioning

24 © 2017 Gartner, Inc. and/or its affiliates. All rights reserved.

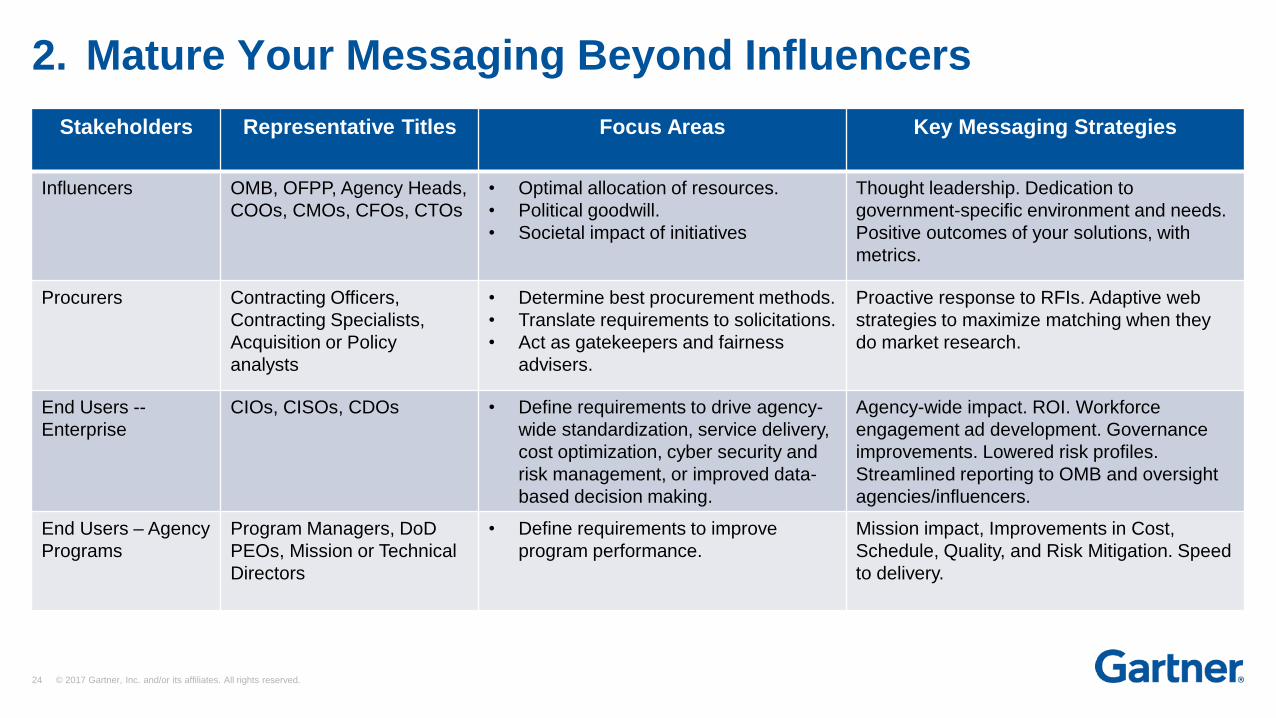

2. Mature Your Messaging Beyond Influencers

Stakeholders Representative Titles Focus Areas Key Messaging Strategies

Influencers OMB, OFPP, Agency Heads,

COOs, CMOs, CFOs, CTOs

• Optimal allocation of resources.

• Political goodwill.

• Societal impact of initiatives

Thought leadership. Dedication to

government-specific environment and needs.

Positive outcomes of your solutions, with

metrics.

Procurers Contracting Officers,

Contracting Specialists,

Acquisition or Policy

analysts

• Determine best procurement methods.

• Translate requirements to solicitations.

• Act as gatekeepers and fairness

advisers.

Proactive response to RFIs. Adaptive web

strategies to maximize matching when they

do market research.

End Users --

Enterprise

CIOs, CISOs, CDOs • Define requirements to drive agency-

wide standardization, service delivery,

cost optimization, cyber security and

risk management, or improved data-

based decision making.

Agency-wide impact. ROI. Workforce

engagement ad development. Governance

improvements. Lowered risk profiles.

Streamlined reporting to OMB and oversight

agencies/influencers.

End Users – Agency

Programs

Program Managers, DoD

PEOs, Mission or Technical

Directors

• Define requirements to improve

program performance.

Mission impact, Improvements in Cost,

Schedule, Quality, and Risk Mitigation. Speed

to delivery.

25 © 2017 Gartner, Inc. and/or its affiliates. All rights reserved.

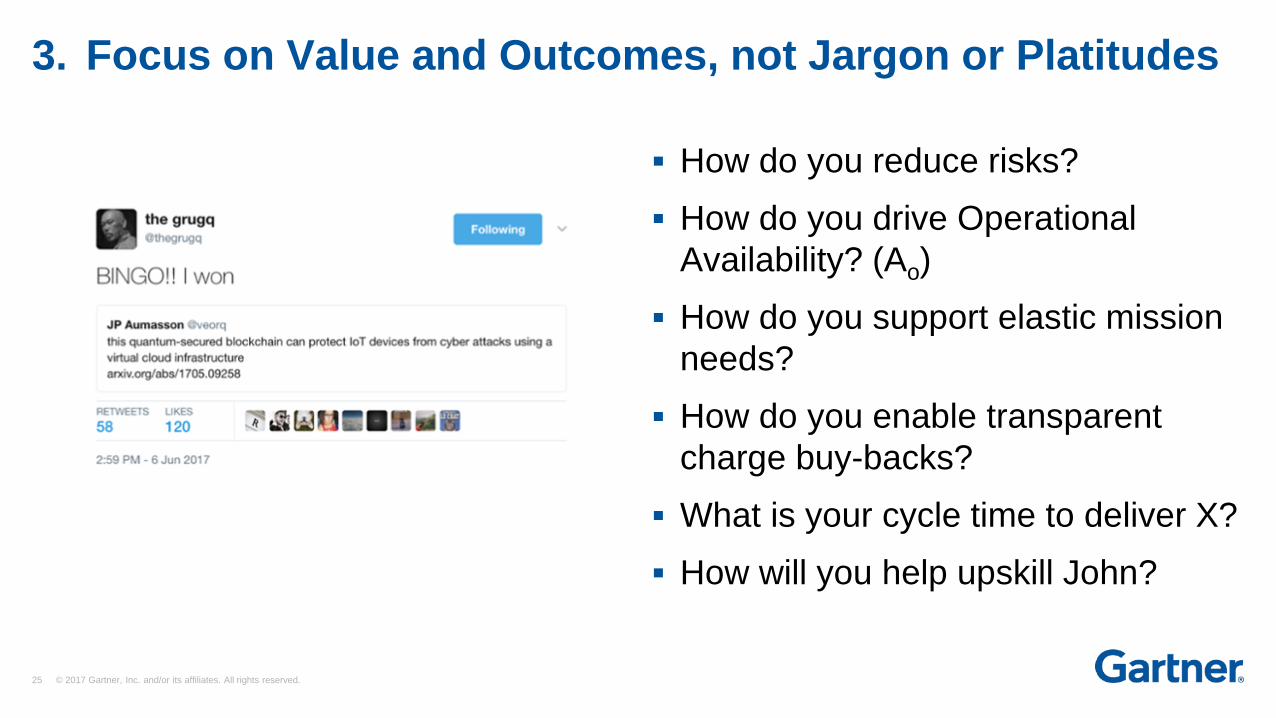

How do you reduce risks?

How do you drive Operational

Availability? (Ao)

How do you support elastic mission

needs?

How do you enable transparent

charge buy-backs?

What is your cycle time to deliver X?

How will you help upskill John?

3. Focus on Value and Outcomes, not Jargon or Platitudes

26 © 2017 Gartner, Inc. and/or its affiliates. All rights reserved.

Employees

Partners

4. Map Your Role in the Emerging World of Platforms

Citizens

Information

Systems

Platforms

Customer

Experience

Platforms

IoT Platforms

Mission Ecosystems

Platforms

Things

Analytics and

AlgorithmsPlatforms

27 © 2017 Gartner, Inc. and/or its affiliates. All rights reserved.

Federal-specific strategies

– AWS, MS Azure/Dynamics/365

– Salesforce, ServiceNow

– Cerner

– Esri ArcGIS, NVIDIA

– Splunk, Tableau, Cloudera, Palantir

Everything is a target

– Once-sacred space market is upside down

June 19 ATC “Government as a Service” meeting

– Accenture, Adobe, Akamai, Alphabet, Amazon, Apple, IBM, Intel, KBCP, Mastercard, Microsoft, OpenGov, Oracle, Palantir, Qualcomm, SAP, VMWare, P. Thiel

– “We will foster a new set of start-ups focused on government technology”

5. Ignore Tech Strategic Partnerships at Your Peril

What happens to the biometrics market when AWS rolls out

Rekognition?

What happens when vendors tap into the $50M Salesforce

fund?

What happens to the IC analytics market when NGA rolls out

its Ventures approach?

What could the Cloudera-enabled Medicaid/CHIPS data lake

mean to civilian and State-level eligibility programs?

What happens to the supply chain market when AWS Business

targets DLA and GSA?

What happens to the software services market when low-code

platforms deployments accelerate?

What happens to resellers when a software federal

marketplace is up and going?

28 © 2017 Gartner, Inc. and/or its affiliates. All rights reserved.

2017 Federal POV Summary

1. Disruption is the New Norm

2. The Enterprise IT versus Mission IT tug of war will intensify

3. Tech Modernization will accelerate disruption of:

1. Acquisition strategies

2. Budgeting/Appropriations

3. Delivery Models, Shared Services, Privatization

4. FedMarketing 2.0

5. Strategic Partnerships and M&A

Short Term: Scale versus Specialization Debate Still Dominates

Long Term: Advantage to Most Nimble and Elastic as Needs and Rules Evolve

People-Led Positioning

Technology and Services-Led Positioning

Business Value-Led Positioning