GOVERNMENT OF INDIA MINISTRY OF FINANCE ANNUAL … · B.2. Drawing & Disbursing Officers (DDOs)...

54

1 GOVERNMENT OF INDIA MINISTRY OF FINANCE ANNUAL REVIEW OF INTERNAL AUDIT WING 2011 – 12 GOVERNMENT OF INDIA OFFICE OF THE CHIEF CONTROLLER OF ACCOUNTS MINISTRY OF FINANCE NEW DELHI

Transcript of GOVERNMENT OF INDIA MINISTRY OF FINANCE ANNUAL … · B.2. Drawing & Disbursing Officers (DDOs)...

1

GOVERNMENT OF INDIA

MINISTRY OF FINANCE

ANNUAL REVIEW OF INTERNAL AUDIT WING

2011 – 12

GOVERNMENT OF INDIA

OFFICE OF THE CHIEF CONTROLLER OF ACCOUNTS

MINISTRY OF FINANCE

NEW DELHI

2

PREFACE

The Internal Audit Function has been viewed as an integral part of

Government Financial Management and is increasingly an instrument for

improving the performance of the Government. It covers a broad range of

activities, which have different objectives. The focus of Internal Audit, till now,

has been mainly on compliance audit, i.e. to ensure proper maintenance of Records,

proper application of Rules, Regulations and Instructions issued by the Government

of India from time to time and also to ensure accuracy in Accounts and efficiency

in operations. Keeping this aspect, the Annual Review highlights issues which

need immediate attention of the Heads of Department. Other matters pointed out in

the Audit Reports which are routine in nature, have been excluded from this Report.

Internal Audit in Central Government is a nebulous area which in today’s

economic scenario requires greater attention. Increasing awareness by an

empowered public along with legislative focus on outputs and outcomes has

precipitated the need for a paradigm shift in the functioning of Internal Audit in the

Government. Internal Audit needs a convergence of financial propriety, accounting

techniques, administrative mandate and refinement of personal skills to make it an

effective tool in the hands of the executive that will encompass the entire domain of

governance to achieve the stated outcomes. Therefore, in years to come, we hope

to make Internal Audit, an even more participative effort taking into account risks

and priorities in Government functioning.

I would like to place on record our deep appreciation for the co-operation

extended by various units of the Ministry of Finance during the course of Audit. I

also wish to acknowledge and appreciate the hard work of officers and staff of the

Internal Audit Wing.

The contents of the Review are based on the information elicited from

various units audited during the year 2011 - 12. Suggestions for improvement will

be gratefully appreciated and the same may be communicated to the Headquarters

of Internal Audit Wing, 4th

Floor, Room No. 413, A.G.C.R. Building, I.P. Estate,

New Delhi or may be conveyed through e-mail to [email protected].

(DR. D.N. PATHAK)

Chief Controller of Accounts

3

INDEX

S.

No. CONTENT

PAGE

NUMBER

1 Preview 4

2 Executive Summary 11

3 Targets & achievements during 2011 – 12 19

4 Major irregularities found during the year 2011 – 12 21

(A) DEPARTMENT OF ECONOMIC AFFAIRS 21

(i) National Savings Institute 21

(ii) PAOs / DDOs (Department of Economic Affairs) 24

(B) DEPARTMENT OF FINANCIAL SERVICES 27

(i) DRATs / DRTs 27

(ii) DDOs (Department of Financial Services) 32

(C) DEPARTMENT OF REVENUE 36

(i) Enforcement Directorate (FERA / FEMA) 36

(ii) Central Bureau of Narcotics / D.O.O. 36

(iii) PAOs / DDOs (Department of Revenue) 45

(D) DEPARTMENT OF EXPENDITURE 48

(i) PAOs / DDOs (Department of Expenditure) 48

(E) DEPARTMENT OF DISINVESTMENT 51

(F) PUBLIC SECTOR BANKS & GRANTEE INSTITUTIONS 51

4

PREVIEW

Internal Audit Inspection is conducted by way of “on-the-spot” verification with

a view to ensure that the initial records are maintained by the Executive Officers

properly, Rules, Regulations and Instructions issued by the Govt. of India from time to

time are complied with, uniform procedures are adopted in the matter of payment and

accounting, corrective measures, wherever necessary, are initiated promptly and

qualitative improvement is brought out. The Internal Audit also investigates the area of

economy for appropriate action and also provides feedback on the accounting formation

of the Ministry as an aid to management function. The Principal Accounts Office,

PAOs, DDOs, as well as Attached and Subordinate Offices of Department of

Economic Affairs, Department of Financial Services, Department of Revenue (except

accounting formation of Departments of CBDT and CBEC), Department of

Expenditure and Department of Disinvestment come within the jurisdiction of Internal

Audit.

In the last few years, there has been globalization of economy and international

business as well as co-operation has increased resulting in shift in the area of

governance. The emphasis is more on efficient and effective management of the

Government functions, explicit standards and measures of performance of Government

Officials and enhanced services rendered to the citizens of the country. These new

dimensions require that sources are discharged efficiently and effectively. Thus, a

systematic feedback mechanism needs to be installed to have an assurance that

functions of Government are being discharged efficiently and effectively. Internal

Audit is an effective tool for providing objective assurance and advice that adds value,

influences change that enhances governance, assist the management, performance of

units, control process and improve accountability of the result.

The Ministry of Finance has five Departments viz :-

(A) Department of Economic Affairs;

(A) Department of Financial Services;

(B) Department of Expenditure;

(C) Department of Revenue; and

(D) Department of Disinvestment.

The Principal Accounts Office, PAOs, DDOs as well as attached and

subordinate offices of Department of Economic Affairs, Department of Financial

Services, Department of Expenditure, Department of Revenue (except accounting

formations of CBDT and CBEC) and Department of Disinvestment come within the

jurisdiction of Internal Audit.

5

The periodicity and jurisdiction of audit has been proposed based on the

identified parameters like the budget being handled by the units, the nature of duties

including presence of procurement functions and activities related thereto, number of

officials serviced by the unit and strength of the audit parties coupled with the need to

cover as many units as possible at desired intervals.

During the financial year i.e. 2011-12, 79 units of various Departments of

Ministry of Finance were planned for audits. Out of which 52 units could be covered.

The targets could not be achieved because the available staff was deployed in some

important training programmes.

The Department-wise units details and their periodicity are appended below:-

(A) DEPARTMENT OF ECONOMIC AFFAIRS :

A.1 National Saving Institutions (NSI)

The National Savings Organization re-structured as National Savings Institute

(NSI) is under the Administrative control of Ministry of Finance, Department of

Economic Affairs (Budget Division), New Delhi. Its Headquarter is at Nagpur

(periodicity – Annual) and 10 Regional Offices (periodicity – Biennial) are located at

various places in India.

The re-structured NSI collects and collates data in respect of Small Savings,

generates studies and policy inputs related to Small Saving Instruments, their tenures,

interest rate structure, rules governing withdrawals etc. Apart from these, NSI deals

with the matters relating to training, product design, market research, international co-

operation and litigation etc.

A.2. Pay & Accounts Officers (PAOs) / Drawing & Disbursement Officers

(DDOs)

Under the provisions contained in Central Treasury Rules / Receipt and

Payment Rules, the drawl of money from the Government accounts and disbursements

are being handled by an officer called the “Drawing and Disbursing Officer” (DDO),

whose main function is to draw funds within the prescribed budget allocation, for

incurring expenditure and realize receipts for credit to Government Accounts on behalf

of the Head of Office.

The under mentioned Offices of the Department of Economic Affairs are

attached with the Pay and Accounts Office (Secretariat.), Department of Economic

Affairs, New Delhi :

6

1. PAO (Secretariat), New Delhi :-

(i) Under Secretary / DDO (Cash), DEA, New Delhi.

(ii) Under Secretary / DDO (IES), DEA, New Delhi.

(iii) DDO, Securities Appellate Tribunal, Mumbai.

List of other PAO’s under the Department of Economic Affairs :-

2. PAO (Establishment.), New Delhi

3. PAO (Banking) New Delhi

4. PAO (NSO) Nagpur

5. PAO (Internal Debt Accounting), New Delhi

(B) DEPARTMENT OF FINANCIAL SERVICES :

The Department of Financial Services was created on 28th

June, 2007 by

merging the erstwhile Banking and Insurance Divisions. Broadly, the functions of the

Department are related to banking, insurance and pension reforms. Policy support is

provided to the Public Sectors Banks (PSBs), Public Sector Insurance Companies and

Development Financial Institutions (DFIs) i.e. NABARAD, SIDBI, IIFCL, EXIM

Bank, IDFC, NHB and IWRFC, IIBI through policy Public Sectors Insurance

Companies and DFIs. Policy formulation in respect of Non-Banking Financial

Companies, private banks and foreign banks is also done by the Department of

Financial services which also provides support to regulatory authorities i.e. RBI, IRDA,

PFRDA, NHB and NABARD.

The Department of Financial Services is divided into following Categories :-

B.1. Debt Recovery Appellate Tribunals (DRATs) & Debt Recovery Tribunals

(DRTs)

The Parliament of India, enacted an Act called the “Recovery of Debts due to

Banks and Financial Institutions Act,1993” for establishment of Tribunals and

Appellate Tribunals for expeditious adjudications and recovery of debts due to Banks

and Financial Institutions and matters connected therewith or incidental thereto. The act

was notified on 27.08.1993 allowing creation of several Tribunals to be known as Debts

Recovery Tribunals / Appellate Tribunals in various States of India excluding state of

Jammu and Kashmir with defined jurisdiction. The units of DRATs / DRTs were

established under administrative control of Department of Economic Affairs.

Consequent upon creation of Department of Financial Services all these units were

transferred to the Department. At present there are 5 Debts Recovery Appellate

Tribunals and 33 Debts Recovery Tribunals, all over India. These Tribunals entertain

cases of Debts above Rs. Ten Lakh.

7

B.2. Drawing & Disbursing Officers (DDOs)

Under the provisions of Central Treasury Rules / Receipt and Payments Rules,

the drawl of money from the Government accounts and disbursements are being

handled by the Drawing and Disbursing Officer (DDOs), whose main function is to

draw funds within the prescribed budget allocation, for incurring expenditure and

realize receipts for credit to Govt. Accounts on behalf of the Head of Office. The under

mentioned offices of the Department of Financial Services are attached with the Pay

and Accounts Office (Banking ) New Delhi, Pay and Accounts Office (NSO) Nagpur

and Pay and Accounts Office (Secretariat), New Delhi and are declared as Non-cheque

Drawing and Disbursing Offices :

1. DDO (Cash), DFS, New Delhi

2. DDO (AAIFR), New Delhi

3. DDO (BIFR), New Delhi

4. DDO (Custodian), New Delhi

5. DDO (Spl. Court), Mumbai and

6. Asstt. Court Liquidator, Kolkata

Periodicity of Audit of all Offices is biennial except DDO (Cash), Department

of Financial Services, which is Audited every year.

(C) DEPARTMENT OF REVENUE :

C.1. Enforcement Directorate

There are 18 Zonal / Sub Zonal offices under Enforcement Directorate with

Head Quarter at New Delhi executing enforcement functions under FEMA / FERA.

The Directorate is mainly concerned with the enforcement of the provisions of Foreign

Exchange Management Act and Foreign Exchange Regulation Act. In pursuance of this

objective the function of the Directorate include, interalia, realization of penalty

imposed by Departmental adjudication orders. Apart from auditing the DDO /

Establishment, the Internal Audit Wing also checks the records connected with seizure

and realization of penalty money.

C.2. Central Bureau of Narcotics.

There are four Zonal offices at Gwalior, Lucknow, Kota and Neemuch under

Central Bureau of Narcotics (CBN) with Headquarter at Gwalior. There are three Govt.

Opium and Alkaloid Work Factories at Gwalior, Neemuch and Ghazipur under

administrative control of Chief Controller of Govt. Opium and Alkaloid Factories,

New Delhi. There are 17 Distt. Opium Offices under administrative control of

Commissioner, CBN, Gwalior.

8

C.3. Pay & Accounts Officers (PAOs) / Drawing & Disbursing Officers (DDOs) in

Department of Revenue

Apart from Enforcement Directorate and Central Bureau of Narcotics there

exist some other establishments under Department of Revenue. Payments for these

establishments are being made, receipts being realized and their accounts are being

maintained by the Drawing and Disbursing Officers of these offices :-

(i) DDO (Cash), Department of Revenue.

(ii) DDO, Appellate Tribunal for Forfeited Properties (ATFP), New Delhi.

(iii) DDO, Central Excise & Services Tax Appellate Tribunals at New Delhi,

Kolkata, Mumbai, Chennai & Bangalore.

(iv) DDO, Central Economic Intelligence Bureau (CEIB), New Delhi.

The periodicity of Audit of the Offices of Directorate of Enforcement and DDO

(Cash), Revenue is annual. Periodicity of Audit of the Offices of Narcotics and PAOs

are biennial and periodicity of other Offices is triennial.

(D) DEPARTMENT OF EXPENDITURE :

Functions of the Department.

The Department of Expenditure is the nodal Department for overseeing the

public financial management system in the Central Government and matters connected

with State finances. The principal activities of the Department include pre-sanction

appraisal of major schemes/projects (both Plan and non-Plan expenditure), handling the

bulk of the Central budgetary resources transferred to States, implementation of the

recommendations of the Finance and Central Pay Commissions, overseeing the

expenditure management in the Central Ministries/Departments through the interface

with the Financial Advisors and the administration of the Financial Rules / Regulations

/ Orders through monitoring of Audit comments/observations, preparation of Central

Government Accounts, managing the financial aspects of personnel management in the

Central Government, assisting Central Ministries/Departments in controlling the costs

and prices of public services, assisting organizational re-engineering through review of

staffing patterns and O&M studies and reviewing systems and procedures to optimize

outputs and outcomes of public expenditure. The Department has under its

administrative control the National Institute of Financial Management (NIFM),

Faridabad.

The business allocated to the Department of Expenditure is carried out through

its Establishment Division, Plan Finance- I and II Divisions, Finance Commission

Division, Staff Inspection Unit, Cost Accounts Branch, Controller General of Accounts

and the Central Pension Accounting office.

9

1. Pay & Accounts Officers (PAOs) / Drawing & Disbursing Officers (DDOs) in

Department of Expenditure

There are nine Offices (PAOs / DDOs) including three RTCs in the Department

of Expenditure under the Internal Audit jurisdiction of the O/o Chief Controller of

Accounts, Ministry of Finance.

(i) P.A.O. Expenditure, New Delhi.

(ii) P.A.O. C.G.A. New Delhi.

(iii) D.D.O. (Cash), Department of Expenditure New Delhi.

(iv) D.D.O. Cost Accounts Branch, New Delhi.

(v) D.D.O. Finance Commission Division, New Delhi.

(vi) D.D.O. INGAF, New Delhi

(vii) D.D.O. R.T.C. INGAF, Mumbai.

(viii) D.D.O. R.T.C. INGAF, Kolkata.

(ix) D.D.O. R.T.C. INGAF, Chennai.

The periodicity of Audit of above Offices is biennial except the DDO (Cash),

Department of Expenditure, New Delhi which is covered by annual audit programme.

(E) DEPARTMENT OF DISINVESTMENT :

There is only one unit i.e. DDO (Cash) Department of Disinvestment. The unit

has been transferred from Ministry of Industry and Internal Audit Wing has conducted

first time internal audit inspection of the unit during 2009-10. The periodicity of audit

of Cash Branch, Deptt. of Disinvestment is Annual similarly on the pattern of DDO

(Cash) of other 4 Departments of Ministry of Finance. The unit is Non-cheque Drawing

DDO submitting its bills to PAO (Expenditure/Disinvestment) New Delhi.

(F) PUBLIC SECTOR BANKS & GRANTEE INSTITUTIONS

1. Public Sector Banks :

The Internal Audit of Public Sector Banks, handling various Deposit Schemes

of Ministry of Finance, is being conducted by the Banking & Financial Intuitions Wing

of this Office. At present, Internal Audit is undertaken at the Focal Point Branch of

State Bank of India, its Associate Banks and Branches of other Nationalized Banks.

The Bank Audit, at present is limited to scrutiny of records relating to Government

transactions in respect of Public Provident Fund Scheme – 1968 and Senior Citizens

Saving Schemes – 2004 etc.. The primary focus of such Audit is to ensure that the

Codal Provisions of the schemes are adhered to by the Banks. Audit also examines the

transactional efficiencies of various Banks in dealing with Government transactions and

to monitor the collection and remittance of Government money into Government

Accounts. In case, where the receipts are not reported by the Focal Point Branches

within the prescribed time limit, Banks are liable to pay penal interest as per extant

instructions on the subject.

10

2. Grantee Institutions :

In exercise of the powers conferred under Rule 20 of the Delegation of

Financial Power Rules, 1978 the Department of Revenue and the Department of

Economic Affairs in the Ministry of Finance have been sanctioning Grants-in-aid to

various Institutions for different purposes and objectives, in accordance with the

provisions contained in Rule 206 of GFRs. Rule 210 enjoins upon a Grantee Institution

to have their Accounts audited / inspected by the grant sanctioning authority.

The various Grantee Institutions, under Finance Ministry such as National

Institute of Public Finance and Policies, Delhi and National Institute of Financial

Management (NIFM), Faridabad are being regularly audited by the Internal Audit

Wing as required vide Para 12.2.1 of the Civil Accounts Manual.

11

EXECUTIVE SUMMARY

Against the target of auditing 79 Auditee units under various departments of

Ministry of Finance for the financial year 2011-12, of various departments of

Ministry of Finance only 52 units could be covered. The targets could not be achieved

because the available staff was deployed to some important training programmes, other

administrative works and transferred to other Ministries.

A gist of audit para related to various departments under Ministry of Finance is

given as follows:

A. DEPARTMENT OF ECONOMIC AFFAIRS

(1) NATIONAL SAVINGS INSTITUTE

The National Savings Organization re-structured as National Savings Institute

(NSI) is under the administrative control of Ministry of Finance, Department of

Economic Affairs (Budget Division) New Delhi. It collects and collates data in regard

to small savings; generate studies and policy inputs in regard to Small Saving

Instruments, their tenures, interest rate structure, rules governing withdrawals etc..

Apart from these, NSI deals with the matters relating to training, product design,

market research, international co-operation and litigation.

In the year 2011 - 12, the Unit of NSI – Nagpur, Bangalore, Guwhati, Mumbai,

New Delhi & NSC – Nagpur were audited and some of the important observations are

as under:-

S.

NO.

NAME OF

UNIT

BRIEF DETAILS OF PARAS

REMARKS

01 NSI – Mumbai

(IR – 20)

Para 16. Colossal waste of Pay & Allowances on

A/C of re-deployment of surplus Staff.

Para 17. Un–avoidable payment of interest

amounting to Rs. 1.68 Lakh.

Details as per

Para A. (1) (i)

Details as per

Para A. (1) (ii)

02 NSI – New Delhi

(IR – 04)

Para 01. Payment of rent of Office Building Rs.

6,05,640/- w.e.f. 14.12.2010.

Para 05. Irregular payment of cash handling

allowance Rs. 300/- Smt. Meenu

Aggarwal, Cashier

Details as per

Para A. (1) (iii)

Details as per

Para A. (1) (iv)

03 NSC – Nagpur

(IR – 05)

Para 09. Bogus commission claims for Rs. 16762.60

by MPKBY Agents Smt. Chandra Devi

Srivastva of Joura (Dist. Murena).

Para 21. Review of LTC Register.

Details as per

Para A. (1) (v)

Details as per

Para A. (1) (vi)

12

(2) DDOs

Prior to conversion as an Autonomous Body, one Pay & Accounts Office each

was attached with all the nine Units of SPMCIL, all over India. Consequent upon its

conversion, all these nine Units have been transferred to that Autonomous Body w.e.f.

10/02/2006 and all the payments of Pay and Allowances and Office Expenses etc. of

these Units are being born by Autonomous Body itself. The work of

finalization of Pro-rata Pension cases in respect of the absorbed Employees of these

Unit is now over. There were approximately 11000 Pro-rata Pension Cases and

subsequent issuance of PPOs in all cases was targeted for authorization by

30/09/2010 which has also been achieved. The accounts of these Units have already

been inspected by Internal Audit Wing. At present DDO (Cash), DEA, DDO (IES),

S.A.T Mumbai, PAO (Estt.) DEA, PAO(NSO) Nagpur, PAO(Sectt.) DEA, and nine

PAOs attached in past with SPMCIL are Auditee Units in the Department of Economic

Affairs. Periodicity of the DDO (Cash), DEA is annual and periodicity of other Units is

biennial.

During the year 2011 - 12, 02 Units were Audited and some of the important

observations are summarized hereunder:-

3 GRANTEE INSTITUTE

Institute of Economic Growth, New Delhi is the only Grantee Institute in

Department of Economic Affairs which organizes the training to I.E.S.

Probationers/Officers. The Institute manages all its expenditures from the Grants

released by the DDO, Indian Economic Services, Department of Economic Affairs,

New Delhi.

S.

NO.

NAME OF

UNIT

BRIEF DETAILS OF PARAS

REMARKS

01 DDO (Cash)

DEA (IR-19)

Para 21. Non-adjustment of Contingent Advances

to the tune of Rs. 1.88 Crore

Details as per

Para A. (2) (i)

02 DDO (IES) New

Delhi (IR-35)

Para 03. Shortcomings/Omissions Detected in

maintenance of the Records of Grants-in –

Aids

Details as per

Para A. (2) (ii)

13

B. DEPARTMENT OF FINANCIAL SERVICES

There are 45 units in the Department of Financial Services, Ministry of Finance.

These offices include 01 Pay and Accounts Office, 38 Units of DRTs/DRATs and 6

other DDOs. The periodicity of DDO (Cash), DFS is annual and periodicity of other

Units is biennial.

(1) DRATs / DRTs

The DRATs / DRTs were created to impart speedy adjudication of cases on

recovery of debts due to Banks and Financial Institutions. After an order is pronounced

by the Tribunal and Recovery Certificate is issued by the Presiding Officer, the

Recovery Officer has to follow procedural instructions to recover loans even by

attaching property of the defaulters or by auction of the property of defaulter. The

Recovery Officer does not have any power to drop the proceedings and close the

recovery at his level.

During the period 2011 - 12 , 01 DRATs, 09 DRTs were audited and some of

the major irregularities, pointed-out by the Audit are summarized hereunder:-

S.

NO.

NAME OF

DRAT’s / DRT’s

(DFS)

BRIEF DETAILS OF PARAS REMARKS

01 DRT – Hyderabad

(IR – 24)

Para 9. Long Pendency cases for recovery before

Recovery Officer (R.O.)

Details as per Para

B. (1) (i)

02 DRT – Patna

(IR – 12)

Para 26. Pending Recovery Certificates.

Para 30. Status in respect of disposal of (Original

Applications) OAs.

Details as per Para

B. (1) (ii)

Details as per Para

B. (1) (iii)

03 DRT – Pune (IR –

17)

Para 3. Long Pendency of Recovery Certificates

before R.O.s.

Details as per Para

B. (1) (iv)

04 DRT– I,

Chandigarh (IR –

16)

Para 3. Compromising decision after the judgment

issued by the presiding officer

Para 05. Non-execution of Recovery certificates by

Recovery Officer (Rs.947.49 Crore)

Details as per Para

B. (1) (v)

Details as per Para

B. (1) (vi)

05 DRT–II,

Chandigarh (IR –

02)

Para–8: Pending recovery certificates

Para–9: Status in r/o disposal of OAs (Original

Applications)

Details as per Para

B. (1) (vii)

Details as per Para

B. (1) (viii)

14

(2) OTHER DDOs

During the period 2011 - 12 , five units amongst DDOs under Department of

Financial Services were audited and some of the major irregularities, noticed / pointed-

out by the Audit are as under :-

C. DEPARTMENT OF REVENUE

There are 52 Offices under the Department of Revenue containing 18 Units of

Directorate of Enforcement, 01 Unit pertaining to Chief Controller of Factories, 17

Units pertaining to Opium and Alkaloid, 03 DNC Offices, 03 Units of GOAW, 06

Units of other DDOs and 04 Units of PAOs. Internal Audit of all the Units of

Directorate of Enforcement are conducted on annual basis and the Units of Opium and

Alkaloid are conducted on biennial basis. Out of 08 other DDOs, DDO (Cash) Revenue

Audit is conducted on annual basis and remaining Units of other DDOs on triennial

basis and all PAOs on biennial basis. During the year 2011 - 12, 25 Units were audited

in all.

(1) CENTRAL BUREAU OF NARCOTICS

Central Bureau of Narcotics is responsible for authorization to Farmers for cultivation

of Opium, collection of raw Opium crop from Farmers, making payments of raw

Opium to Farmers including advance payments to Farmers against raw Opium Crop but

pending for test approval and processing of raw Opium at its Factories at Ghazipur and

Neemuch. During the course of Internal Audit on the accounts of various District

Opium Officers (under CBN) the following observations were made:-

S.

NO.

NAME OF UNIT

(DFS) OTHER

DDOs

BRIEF DETAILS OF PARAS REMARKS

01 DDO (BIFR), New

Delhi (IR – 25)

Para 19. Engagement of Security Guards. Details as per Para

B. (2) (i)

02 DDO (Custodian),

New Delhi (IR – 18)

Para 01. Non-Finalization of the lease deed of

office accommodation/Irregular payment

of rent of Rs. 68, 57,986/-.

Details as per Para

B. (2) (ii)

03 DDO (Spl. Court),

Mumbai (IR – 27)

Para 06. Non-Maintenance of stock Register of

Cheque Books.

Para 10. Irregular direct appointment of staff.

Para18. Irregular promotion during deputation.

Para 20. Improper maintenance of Receipt Books

Details as per Para

B. (2) (iii)

Details as per Para

B. (2) (iv)

Details as per Para

B. (2) (v)

Details as per Para

B. (2) (vi)

15

(2) DIRECTORATE OF ENFORCEMENT (FEMA/FERA)

The Directorate of Enforcement is responsible for prosecuting offenders under

Foreign Exchange Regulation Act, 1973 and Foreign Exchange Management Act, 1999

to adjudicate cases of violations, levying penalties and to realize the same. During the

period 2011 - 12 , 10 Regional Units of Directorate of Enforcement were inspected and

some of the important observations made are appended below :-

S.

NO.

NAME OF

UNIT

(REVENUE)

ED FEMA

BRIEF DETAILS OF PARAS REMARKS

01 ED – FEMA,

Lucknow (IR –

26)

Para 5. Pay fixation under the 6TH

CPC.

Para 9. Irregular grant of 3rd

MACP to the Grade pay

of Rs. 6.600 to Shri V.P. Gogia, Assistant

Director and Shri A.K. Mathur, AD-II..

Details as per

Para C. (2) (i)

Details as per

Para C. (2) (ii)

02 ED – FEMA,

Ahemdabad (IR

– 36)

Para 06. Non-Realization of Penalties amounting to

Rs. 7122.95 Lakhs under FERA.

Para 07. Non-Realization of Penalties amounting to

Rs. 459.39 Lakhs under FEMA

Details as per

Para C. (2) (iii)

Details as per

Para C. (2) (iv)

03 ED – FEMA,

Bangalore (IR –

32)

Para 11. Irregular Accountal of Income Tax

Recovered from the owner of the Building

hired by ED.

Para 13. Excess payment of TA claims for Rs. 4809/-

Details as per

Para C. (2) (v)

Details as per

Para C. (2) (vi)

04 ED – FEMA,

Chandigarh (IR –

15)

Para 01. Non-recovery of penalty Rs. 72.21 Crore

Para 02. Non-disposal of seized Indian currency and

foreign currency Rs. 1047.97 Lakh.

Details as per

Para C. (2) (vii)

Details as per

Para C. (2) (viii)

05 ED – FEMA,

Jaipur (IR – 23)

Para 05 Review of Penalties, seizure and confiscation

(Recovery of Rs. 44, 56,435/-)

Para 08. Irregular /over payment of Rs. 25,440/- on

account of CCA.

Details as per

Para C. (2) (ix)

Details as per

Para C. (2) (x)

S.

NO.

NAME OF

UNIT

(REVENUE)

DOO/DNC/GM

BRIEF DETAILS OF PARAS REMARKS

01 DOO –

Chittorgarh

(IR – 48)

Para 8 Irregular expenditure on Salary to canteen

staff for three posts against the sanctioned

strength of two posts.

Para-9. Non-Recovery of amount of over payment of

cost of opium paid to cultivators to the tune of

Rs. 19,13,986/- (as on 31.12.2011) including

Rs 36543/- for the financial year 2010-2011.

Details as per

Para C(I)(i)

Details as per

Para C(I)(ii)

16

06 ED – FEMA,

Mumbai (IR –

34)

Para 03. Fixed Deposits (Rs. 7.85 Crore)

Para 04. Non-disposal of seized Indian Currency and

foreign Currency Rs. 7.29 Crore.

Para 05. Irregular payment of Rent of Office Building

Rs. 7, 21, 66,539/-

Details as per

Para C. (2) (xi)

Details as per

Para C. (2) (xii)

Details as per

Para C. (2) (xiii)

07 ED – FEMA,

Varanasi (IR –

01)

Para 3. Irregular deduction allowed while computing

of Income Tax.

Para 4. Review of Penalties, confiscation, seizure off

Indian and Foreign currency and valuables

etc.-non realization of penalties amounting

to Rs. 77, 57, 30,332

Details as per

Para C. (2) (xiv)

Details as per

Para C. (2) (xv)

(3) OTHER DDOs

During the period 2011 - 12 , 03 DDO Units, under Department of Revenue

were inspected and some of the important observations made by the Audit are

summarized as under :-

S.

NO.

NAME OF UNIT

(REVENUE) ED

FEMA

BRIEF DETAILS OF PARAS REMARKS

01 DDO (Cash)

Revenue

{IR – 07}

Para 8. Short Recovery of income Tax and surcharge

amounting to Rs. 138307 during the

Financial Year 2000-01 as shown as

FORM-16

Para 21. (A) Non-Adjustment of LTC. Advance /

Claims.

Details as per

Para C. (3) (i)

Details as per

Para C. (3) (ii)

01 DDO (CESTAT)

{IR – 30}

Para 5. Wasteful Expenditure of Rs. 5.48 lakh on

account of pay and allowances of idle

driver.

Para 6. Irregular payments of Rs. 66,312 on account

of LTC Claims in violation of LTC Rules.

Para 10. Non-adjustment of contingent advance

amounting to Rs. 10.35 Lakhs.

Details as per

Para C. (3) (iii)

Details as per

Para C. (3) (iv)

Details as per

Para C. (3) (v)

17

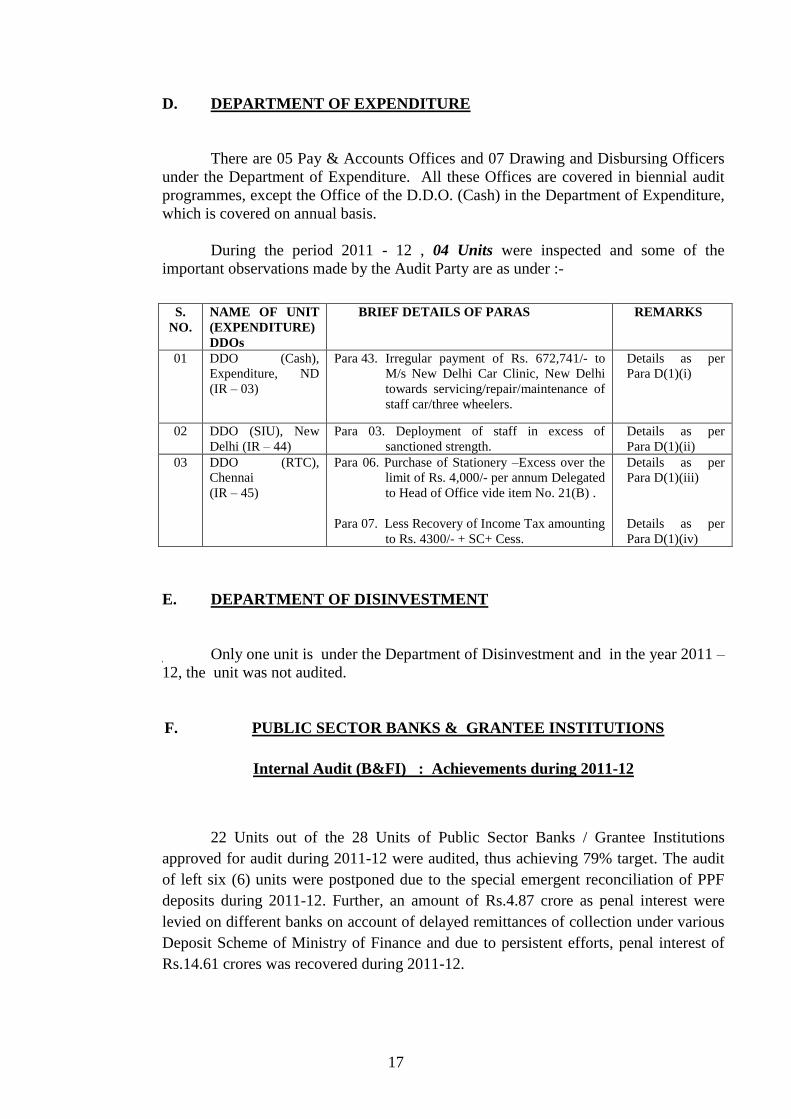

D. DEPARTMENT OF EXPENDITURE

There are 05 Pay & Accounts Offices and 07 Drawing and Disbursing Officers

under the Department of Expenditure. All these Offices are covered in biennial audit

programmes, except the Office of the D.D.O. (Cash) in the Department of Expenditure,

which is covered on annual basis.

During the period 2011 - 12 , 04 Units were inspected and some of the

important observations made by the Audit Party are as under :-

E. DEPARTMENT OF DISINVESTMENT

Only one unit is under the Department of Disinvestment and in the year 2011 –

12, the unit was not audited.

F. PUBLIC SECTOR BANKS & GRANTEE INSTITUTIONS

Internal Audit (B&FI) : Achievements during 2011-12

22 Units out of the 28 Units of Public Sector Banks / Grantee Institutions

approved for audit during 2011-12 were audited, thus achieving 79% target. The audit

of left six (6) units were postponed due to the special emergent reconciliation of PPF

deposits during 2011-12. Further, an amount of Rs.4.87 crore as penal interest were

levied on different banks on account of delayed remittances of collection under various

Deposit Scheme of Ministry of Finance and due to persistent efforts, penal interest of

Rs.14.61 crores was recovered during 2011-12.

S.

NO.

NAME OF UNIT

(EXPENDITURE)

DDOs

BRIEF DETAILS OF PARAS

REMARKS

01 DDO (Cash),

Expenditure, ND

(IR – 03)

Para 43. Irregular payment of Rs. 672,741/- to

M/s New Delhi Car Clinic, New Delhi

towards servicing/repair/maintenance of

staff car/three wheelers.

Details as per

Para D(1)(i)

02 DDO (SIU), New

Delhi (IR – 44)

Para 03. Deployment of staff in excess of

sanctioned strength.

Details as per

Para D(1)(ii)

03 DDO (RTC),

Chennai

(IR – 45)

Para 06. Purchase of Stationery –Excess over the

limit of Rs. 4,000/- per annum Delegated

to Head of Office vide item No. 21(B) .

Para 07. Less Recovery of Income Tax amounting

to Rs. 4300/- + SC+ Cess.

Details as per

Para D(1)(iii)

Details as per

Para D(1)(iv)

18

1. Penal Interest of Rs. 4.87 crores (approximately) was calculated for recovery

from State Bank of India and other Nationalised Banks on account of delayed

remittances of collections under various Deposit Schemes of Ministry of

Finance.

As per instructions contained in Reserve Bank of India circular number

13/4272/85-86 dated 7.4.1986, S.S. 381/99/9091 94-95 dated 9.5.1995 it was decided in

consultation with the, Ministry of Finance, and the Controller General of Accounts that

Banks handling transaction relating to Miscellaneous Govt. Schemes should report the

consolidated figures to GAD Mumbai for onward reporting to Reserve Bank of India,

Central Accounts Section, Nagpur for accountal in Government Accounts on a day to

day basis. Further, as per Reserve Bank of India, Central Office Mumbai Circular No.:

CODT 15-01-2001/1047/97-98 Dated 16-09-1997, 3 days grace period (excluding

holidays) is admissible for remittance of collections. Accordingly, penal interest is

payable by banks in all cases wherein the prescribed grace period of 3 clear working

days has been exceeded. Penal Interest on this account is recoverable for the entire

period of delay starting from date of receipt of the subscriptions at the receiving

branches till final credit of the amount to the Government Account.

During the inspection of various focal point branches of State Bank of India and

other Nationalised Banks, delay in remittance of amounts collected under various

Deposit Schemes of Govt. of India were noticed and penal interest amounting to Rs.

4.87 crores (approximately) payable to Government of India was reported as detailed in

first two paras.

The concerned branches of Bank have been advised to pay the amount of Penal

Interest mentioned against each immediately.

19

TARGET AND ACHIEVEMENTS

DURING THE FINANCIAL YEAR 2011 - 12

All the Offices of Department of Economic Affairs, Department of Financial

Services, Department of Revenue, Department of Expenditure and Department of

Disinvestment of Ministry of Finance are audited on Annual, Biennial or Triennial

basis, depending on the Budget Allotment, Sanctioned Strength and volume of work

with the Unit.

Targets fixed for number of Units to be audited and Units actually audited

during 2011 - 12 are as under :-

A. DEPARTMENT OF ECONOMIC AFFAIRS

B. DEPARTMENT OF FINANCIAL SERVICES

C. DEPARTMENT OF REVENUE

S.

No.

Name of Units (sector wise) Total Nos.

of Units

Nos. of

Units

Approved

Nos. of

Units

Audited

01 Drawing & Disbursing Offices (NSI) 11 08 06

02 Other DDO’s 03 03 01

03 PAOs 06 05 02

Total 20 16 09

S.

No.

Name of Units (sector wise) Total Nos.

of Units

Nos. of

Units

Approved

Nos. of

Units

Audited

01 DRATs & DRTs 38 16 10

02 Other DDO’s 06 07 05

Total 44 23 15

S.

No.

Name of Units (sector wise) Total Nos.

of Units

Nos. of

Units

Approved

Nos. of

Units

Audited

01 E.D. (FEMA) 18 17 10

02 Central Bureau of Narcotics/ D.O.O. 23 13 11

03 Other DDOs / PAO (GOAW) 12 04 03

Total 53 34 24

20

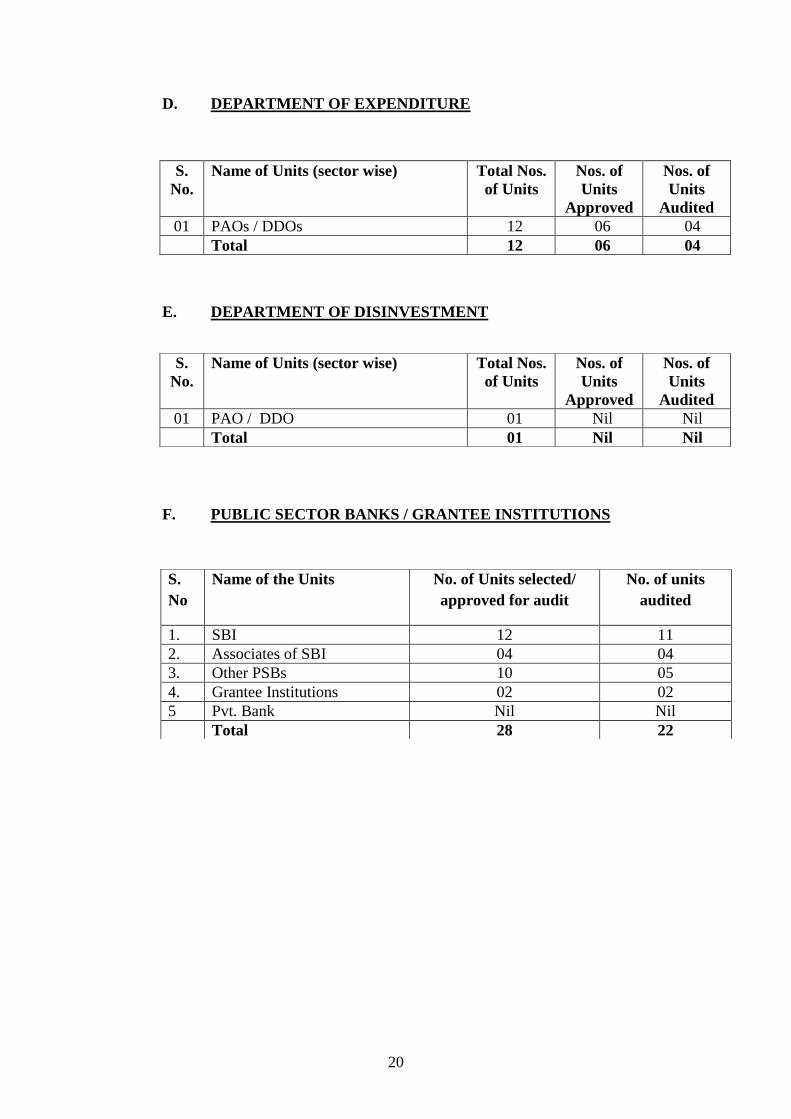

D. DEPARTMENT OF EXPENDITURE

E. DEPARTMENT OF DISINVESTMENT

F. PUBLIC SECTOR BANKS / GRANTEE INSTITUTIONS

S.

No.

Name of Units (sector wise) Total Nos.

of Units

Nos. of

Units

Approved

Nos. of

Units

Audited

01 PAOs / DDOs 12 06 04

Total 12 06 04

S.

No.

Name of Units (sector wise) Total Nos.

of Units

Nos. of

Units

Approved

Nos. of

Units

Audited

01 PAO / DDO 01 Nil Nil

Total 01 Nil Nil

S.

No

Name of the Units No. of Units selected/

approved for audit

No. of units

audited

1. SBI 12 11

2. Associates of SBI 04 04

3. Other PSBs 10 05

4. Grantee Institutions 02 02

5 Pvt. Bank Nil Nil

Total 28 22

21

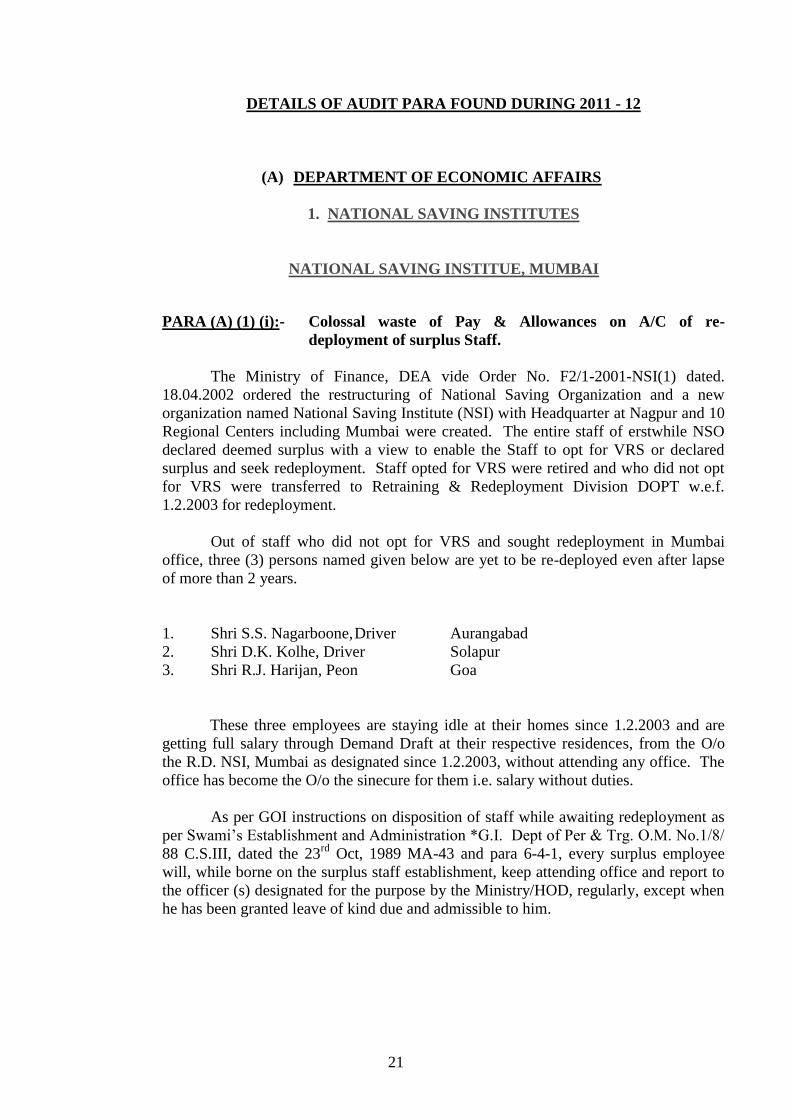

DETAILS OF AUDIT PARA FOUND DURING 2011 - 12

(A) DEPARTMENT OF ECONOMIC AFFAIRS

1. NATIONAL SAVING INSTITUTES

NATIONAL SAVING INSTITUE, MUMBAI

PARA (A) (1) (i):- Colossal waste of Pay & Allowances on A/C of re-

deployment of surplus Staff.

The Ministry of Finance, DEA vide Order No. F2/1-2001-NSI(1) dated.

18.04.2002 ordered the restructuring of National Saving Organization and a new

organization named National Saving Institute (NSI) with Headquarter at Nagpur and 10

Regional Centers including Mumbai were created. The entire staff of erstwhile NSO

declared deemed surplus with a view to enable the Staff to opt for VRS or declared

surplus and seek redeployment. Staff opted for VRS were retired and who did not opt

for VRS were transferred to Retraining & Redeployment Division DOPT w.e.f.

1.2.2003 for redeployment.

Out of staff who did not opt for VRS and sought redeployment in Mumbai

office, three (3) persons named given below are yet to be re-deployed even after lapse

of more than 2 years.

1. Shri S.S. Nagarboone, Driver Aurangabad

2. Shri D.K. Kolhe, Driver Solapur

3. Shri R.J. Harijan, Peon Goa

These three employees are staying idle at their homes since 1.2.2003 and are

getting full salary through Demand Draft at their respective residences, from the O/o

the R.D. NSI, Mumbai as designated since 1.2.2003, without attending any office. The

office has become the O/o the sinecure for them i.e. salary without duties.

As per GOI instructions on disposition of staff while awaiting redeployment as

per Swami’s Establishment and Administration *G.I. Dept of Per & Trg. O.M. No.1/8/

88 C.S.III, dated the 23rd

Oct, 1989 MA-43 and para 6-4-1, every surplus employee

will, while borne on the surplus staff establishment, keep attending office and report to

the officer (s) designated for the purpose by the Ministry/HOD, regularly, except when

he has been granted leave of kind due and admissible to him.

22

PARA (A) (1) (ii) Avoidable payment of interest amounting to Rs. 1.68 Lakh.

During the Scrutiny of file No. A-I/Legal (PBS)/09/2004, it has been revealed

that Shrimati Parvatibai (Ex-Watchman) retired from service on 1.2.2003 and payment

towards her retirement benefits were made from 21.1.2004 to 21.6.2007. Due to delay

in payment she knock the door of CAT and consequently CAT vides order (Court

judgment in O.A. No 2100/2008) 17.09.2009.Ordered the Deptt to pay interest on

delayed payment of her retirement benefits and Deptt had to pay interest amounting to

Rs. 1.68 Lakh.

As per letter dated 3.12.2009 issued by the Under Secretary MOF, DEA (NSI

Section) the Deptt was also asked to fix the responsibility for delayed payment in the

light of Rule 68 of CCS (Pension) Rule 1972, Delay in payment of retirement benefit

has resulted in avoidable payment of interest amounting to Rs. 1.68 Lakh.

The Deptt. neither challenged the verdict of the C.A.T. in the higher court of

law nor fix the responsibility on the official/officials who did not acquit oneself well, as

desired by the Under Secretary vide letter dated 3.12.2009, till date. The reason for

delayed payment of retrial benefits may be evinced/elucidated to audit.

NATIONAL SAVING INSTITUE, NEW DELHI

PARA (A) (1) (iii):- Irregular payment of rent of Office Building Rs. 6,05,640/-

w.e.f. 14.12.2010.

The O/o NSI Delhi is presently located in a rented building belonging to ICCW

Trust at 4, Deendayal Updhayay Marg, New Delhi. The building was initially occupied

as per the lease agreement dated 31.8.1990, and the present lease deed has been

renewed up to 12.12.2010 vide lease agreement dated 19.05.2010. As per item No. 16

of annexure to schedule of delegation of Financial Power Rules 1978, the lease deed is

required to be renewed on expiry of every five years, but in the present case, this has

been renewed up to 12.12.2010. The period of about six months had been lapsed on

the date of conducting the audit. The payment of rent is being made without and

valid/lease deed/rent agreement between ICCW & Govt. of India. No yearly sanction

of payment of rent is being accorded by the Competent Authority.

The Lease agreement w.e.f 14.12.2010 be got regularized along with the

payment of electricity & water charges.

The clause regarding payment of service tax is silent in the agreement. The RS/

NSI has paid Rs. 1,92,548/- during the year 2010-11.

23

PARA(A)(1)(iv) Irregular payment of cash handling allowance Rs. 300/- Smt.

Meenu Aggarwal, Cashier.

A cash handling allowance is admissible to LDC/UDC/Asstt. handling the cash

as per prescribed rates. The amount should be revised every financial year and

sanctioned on the basis of average amount of disbursement during the pervious

financial year. Every official appointed to work as cashier, unless he is exempted by

the competent authority should furnish security of the required amount. The security

bond of Smt. Meenu Aggarwal, cashier had already been expired on the midnight of

4/4/2011.

NATIONAL SAVING INSTITUE, NAGPUR

PARA (A) (1) (v):- Bogus commission claims for Rs. 16762.60 by MPKBY

Agents Smt. Chandra Devi Srivastva of Joura (District

Murena).

It was pointed out vide para 12.3.1. and 4 of the Inspection Report for the

period 7/84 to 7/86 to 11/88 to 11/90 and 12/90 to 9/92 and 10/92 to 3/95 respectively

that Smt. Chandra Devi Srivastava, MPKBY Agent C.A. No. National Savings

Commissioner 1977/Joura fraudulently received a sum of Rs. 16762.60 by submitting

bogus claims for the month of March 1981 to January 1983 as detailed below.

S. No. Month Amount No. of Schedule

enclosed

1 Mar-81 179.2 23

2 Apr-81 80.2 24

3 May-81 274.6 11

4 Jun-81 194 9

5 Jul-81 164.6 11

6 Aug-81 450 6

7 Sep-91 650 6

8 Oct-91 545.8 5

9 Nov-81 537.2 6

10 Dec-81 902.4 6

11 Jan-81 584.1 5

12 Feb-82 1058.1 6

13 Mar-82 1141.6 6

14 Apr-82 1160.8 6

15 Sep-82 600 3

16 Oct-92 2000 10

17 Nov-82 1872 10

18 Jan-82 200 12

19 Jan-83 2368 12

TOTAL 16762.60

24

PARA (A) (1) (vi):- Review of LTC Register.

During the course of Audit a LTC Register maintained by The National Saving

Institute, Office of the Director National Saving Institute, Nagpur has been verified and

found the following lapses.

1. As per the LTC Register, it is seen that for the Years of 2008-09 advance taken

by Sh. P.D. Sakharwade and Sh. M.B. Kumbhare for the Rs. 2250/- and Rs.

12000/- vide bill No.288 Dt. 16.12.2008 are still pending.

2. It is seen that in 2009-10, Sh. Mir Azmat Ali has drawn the advance of Rs.

12900/- vide bill No. 205 dated 26.10.2009 and his total claim was Rs. 11554/-

and amount Rs. 1346/- was required to be recovered from him along with penal

interest but it is seen that Rs. 1306/- was recover from him. Thus, Rs. 40/- short

recovered.

3. It is seen that Smt. S.R. Bagde drawn the advance of Rs. 11500/- vide Bill

No.390 dated 3.10.2010 and her total claim was Rs. 14546/- the amount of Rs.

3046/- was required to be paid to the official but less amount of Rs. 2786/- was

paid.

4. It is seen that some of the Officers have refunded the LTC advance, it is

required that at the time of refund of LTC advance ,10 days leave encashment

are also to be refunded.

DDO (CASH) DEA, NEW DELHI

PARA (A) (2) (i):- Non-adjustment of Contingent Advances to the tune of Rs.

1.88 Crore.

RULE POSITION

As per the provisions contained in Rule 292 (1) of GFRs, 2005, the

Head of Office may sanction Advances to a Government Servant for purchase

of Goods or Services or any other special purpose needed for the management

of the Office, subject to the following conditions:-

(i) The amount of expenditure being higher than the permanent advance available,

cannot be met out of it.

(ii) The purchase or other purpose can not be managed under the normal

procedures, envisaging post-procurement payment system.

(iii) The amount of Advance should not be more than the power delegated to the

Head of the Office for the purpose.

25

(iv) The Head of Office shall be responsible for timely recovery or adjustment of

the Advance.

The Rule 292 (2) of GFRs, 2005 further says that the adjustment bill

along-with the balance, if any, shall be submitted by the government Servant

within fifteen days of te drawal of Advance, failing which, the advance or

balance shall be recovered from his next Salary / Salaries.

STATUS

During the test check of contingent advance register for the period 2010-

11, maintained by the D.D.O. (Cash), Department of Economic Affairs, it has

been observed by the Audit that a sum of Rs. 1.88 Crore is pending in the

register to be adjusted since the year 2006-07. as per details below:-

S. NO. FIANCIAL YEAR AMOUNT

01 2006-07 1279557.00

02 2007-08 814597.00

03 2008-09 2650649.00

04 2009-10 420300.00

05 2010-11 13678177.00

TOTAL 18843280.00

IMPACT

(i) Violation of Rules & regulations framed by Government of India in this regard.

(ii) Chances of misuse of Advance since the Audit could not ascertain as to

whether the Advances drawn by the above officers/officials were actually used

for the official purposes or not.

RECOMMENDATIONS

Since the non adjustment of Contingent and Miscellaneous Advances is a

serious irregularity under Rules, it is, therefore, suggested that the Register may

immediately be reviewed and the above Contingent and Miscellaneous Advances may

immediately be adjusted with Penal Interest (wherever applicable),

26

DDO (IES), DEA, NEW DELHI

PARA (A) (2) (ii):- Shortcomings/Omissions detected in maintenance of the

records of Grants-in-Aids.

The following shortcomings were noticed while inspecting the records in

respect of Grant-in–aid to the Institute of Economic Growth, New Delhi for the

Financial 2009 -10 & 2010 -11.

(i) Date on which utilization certificate is requested to be furnished by the

sanctioning authority to the Audit Officer and /or Accounts Officer was not

found to have been mentioned in column 10 of the register in respect of Final

instalment of the grant as well as second instalment.

(ii) Grants-in-Aids bills the aforesaid 1st and 2

nd instalment were not found to have

been prepared in prescribed Performa GAR 34 in pursuance of the provision

contained vide rule 147 of the Receipt and Payment Rules. Instead of the same

were prepared in Form T.R.30.

(iii) The assets created by the Institute of Economic Growth out of this Grant should

be maintained in the register in form GFR 19 showing the assets of permanent

value& Machinery Equipment having a life span of not less than 5 years and

costing Rs. 10000 above. A copy of the same may be made available to the

Department. An agreement should be separately entered into between IEG &

the Department. Utilization certificate of assets created out of this grant was not

being furnished by the institution.

(iv) The Institution of Economic Growth is required to maintain subsidiary account

of Govt. Grant and furnish statement of account. This is not being received.

(v) On review of records of Grants-in-aids, it has came to notice that a debit

closing balance of Rs. 14804/- pertaining to 2006-07 of Institute of Economic

Growth (IEG) was carried forward. IEG is only one grantee Institute in the unit

(IES,DEA) arranging training for probationers/trainees of Institute of

Economic Services and dependent on Grant-in-aid provided to the unit for its

day to day expenditure. It is not known how the closing balance carried forward

had been worked out.

(vi) In future grant-in-aid may be released to institute on fulfilment of conditions

for sanction of grant-in-aid laid down in GFR. It is also mentioned that above

irregularities are of persistent nature and compliance report has been submitted

in this regard.

27

(B) DEPARTMENT OF FINANCIAL SERVICES

DRT HYDERABAD

PARA (B) (1) (i) Long Pendency of cases for recovery before Recovery Officer

In terms of section 25 of the Recovery Debts to Banks and Financial Institutions Act,

1993, Recovery Officer on receipt of copy of certificate shall proceed for the recovery of

amount of Debt specified in certificate. R.O. has to expedite the recovery as early as possible

but it was observed in DRT, Hyderabad that there were many long outstanding cases where

recovery was not made till date of audit .Some of the cases are more than 5 years old. Brief

details are as under:-

Year-wise break-up of Recovery pending as on 30.9.2011

Period of Pendency No. of cases Amount in Crore

More than 3years 1507 6758.75

Between 2-3 years 854 138.50

Between 1-2 years 716 136.23

Less than one year 393 213.76

Necessary steps for early recovery in all the above cases may be taken. In case the

recovery of full amount as per certificate not made, the purpose of issuance of Recovery

Certificate is defeated.

DRT PATNA

PARA (B) (1) (ii) Pending Recovery Certificates.

A report was obtained from Recovery Officer-I & Recovery Officer-II of the

DRT, Patna in r/o status of pending RCs as on 27.07.2011. The RCs pending as on

27.07.2011 were as follows:

Recovery Officer Amount of RCs No. of RCs Amount more

than 3 Years

RO-I 672.78 Crore 609 149.99 Crore

RO-II 81.30 Crore 409 44.97 Crore

TOTAL 754.08 Crore 1009 194.96 Crore

It was pertinent to mention that Rs. 194.96 Crore of pending RCs were more

than 3 Years old. As such efforts are required for settlement of the O/S RCs.

28

PARA (B) (1) (iii) Status in r/o disposal of OAs (Original Applications)

A report was obtained from the DRT, Patna regarding the status of disposal of

Original Applications (OAs) and it was noticed that 611 OAs (involving) Rs.642.64

were pending as on 31.03.2011.

All the said OAs were pending for more than one years. Whereas under the

DRT, Act 1993 the cases should have been settled/decided with in Six months.

Efforts needed to be taken to settle the OAs as early as possible.

DRT PUNE

PARA (B) (1) (iv) Long Pendency of Recovery Certificates before R.O.s.

Chapter V of the Recovery of Debts due to Banks and Financial Institution Act

1993 speaks about the Recovery of Debt determined by Tribunal. The Recovery officer

shall on receipt of the copy of the certificate proceed to recover the amount of debt

specified in the certificate. This recovery of debt should be as early as possible.

Scrutiny of records pertaining to DRT Pune reveals that large numbers of Recovery

Certificates are pending before Recovery Officer in which debt was not recovered.

Details of such cases as on 31-12-2011 was under:-

Statement Showing the Information of Pending Recovery Proceeding and

Decretal Amount as on 31-12-2010.

From the above details it is clear that some cases are pending more than five

years. In such circumstances, when recovery could not be made even after expiry of

such long period, purpose of Recovery Certificates has been failed.

Sl. No. YEAR No. of RP Cases Decretal Amount

1. 2001 29 14.00

2. 2002 88 132.95

3. 2003 98 136.65

4. 2004 218 515.95

5. 2005 84 126.50

6. 2006 49 59.55

7. 2007 114 80.42

8. 2008 105 80.42

9. 2009 178 380.12

10. 2010 244 324.32

11 2011 30 77.70

Total 19.28 Crores

29

DRT-I CHANDIGARH

PARA (B) (1) (v) Compromising decision after the judgment issued by the

Presiding Officer.

During the last audit of DRT Chandigarh, it was observed that 443 number of

Recovery Certificates were issued in which the recovery of Rs. 804.18 Crore was

involved. These cases were settled at a compromising amount of Rs. 74.57 Crore.

Similarly during the instant spell (2008-2011) of audit 184 no. of recovery certificates

were issued in which the recovery of Rs. 97.85 Crore was involved. These cases were

also settled at a compromised amount of Rs. 34.08 Crore. This is not in conformity of

DRT Act. In terms of Rule 26 of the Recovery of debts due to Banks and Financial

Management Act,1993.

Rule: 26- validity of certificates and amendment thereof:

1. It shall not be open to the defendant to dispute before the Recovery Officer the

correctness of the amount specified in the certificate, and no objection to the

certificate on any other ground shall also be entertained by the Recovery

Officer.

2. Not with standing the issue of a certificate to a Recovery Officer, the Presiding

Officer shall have power to withdraw the certificate or correct and clerical or

arithmetic mistake in the certificate by sending and intimation to the Recovery

Officer.

3. The Presiding Officer shall intimate to the Recovery Officer any order

withdrawing or cancelling or any correction made by him under sub-section

(2).

Apart from the rule positions mentioned above. Recovery Officers have no

power to amend the recovery certificate, as it was done by compromising the huge

amount of Recovery. This action of Recovery Officers is not in conformity of DRT Act

is against the provisions of the Act.

Hon’ble Presiding Officer is competent to make any correction in the recovery

amount. Any bank who wants to compromise and settle the recovery amount below the

recovery amount has to first deposit the recovery amount and also to move an

application before Hon’ble Presiding Officer regarding the compromise between the

bank and debtor, if any, Hon’ble Presiding Officer after going through the merits

decides/reject the compromise between bank and debtor. In case compromise is

approved by the Presiding Officer, an order in this regard is communicated to Recovery

Officer and the case file consigned to the records. The observations were also

highlighted in the annual Review of internal audit 2006-07.

30

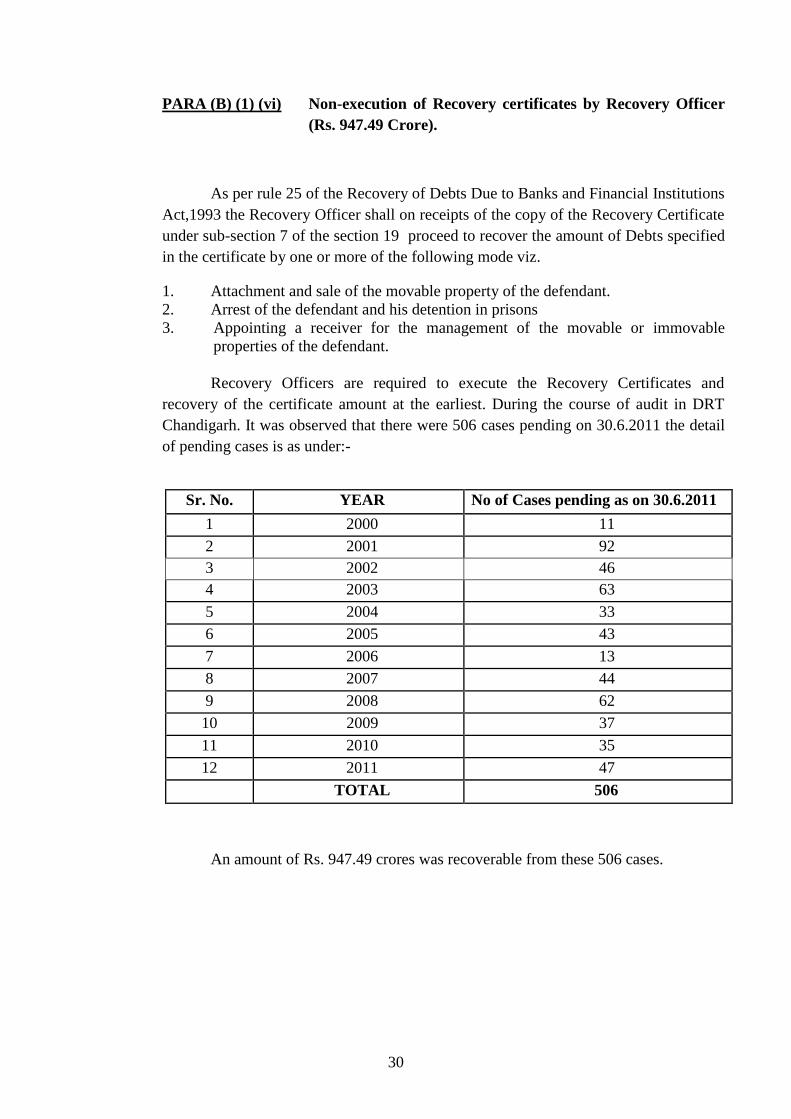

PARA (B) (1) (vi) Non-execution of Recovery certificates by Recovery Officer

(Rs. 947.49 Crore).

As per rule 25 of the Recovery of Debts Due to Banks and Financial Institutions

Act,1993 the Recovery Officer shall on receipts of the copy of the Recovery Certificate

under sub-section 7 of the section 19 proceed to recover the amount of Debts specified

in the certificate by one or more of the following mode viz.

1. Attachment and sale of the movable property of the defendant.

2. Arrest of the defendant and his detention in prisons

3. Appointing a receiver for the management of the movable or immovable

properties of the defendant.

Recovery Officers are required to execute the Recovery Certificates and

recovery of the certificate amount at the earliest. During the course of audit in DRT

Chandigarh. It was observed that there were 506 cases pending on 30.6.2011 the detail

of pending cases is as under:-

An amount of Rs. 947.49 crores was recoverable from these 506 cases.

Sr. No. YEAR No of Cases pending as on 30.6.2011

1 2000 11

2 2001 92

3 2002 46

4 2003 63

5 2004 33

6 2005 43

7 2006 13

8 2007 44

9 2008 62

10 2009 37

11 2010 35

12 2011 47

TOTAL 506

31

DRT-II CHANDIGARH

PARA (B) (1) (vii) Pending recovery certificates

A report was obtained from Recovery Officer-I & Recovery Officer-II of the

DRT-II, Chandigarh in r/o status of pending RCs as on 31/03/2011. The RCs pending

as on 31/03/2011 were as follows:

Amount of RCs No. of RCs O/s more than 3 years

RO-I 416.42 Crore 516 375

RO-II 626.67 Crore 483 369

TOTAL 1043.09 Crore 999 744

It was pertinent to mention that more than 74% of pending RCs were more than

3 years old. As such efforts were required to look into it for settlement of the o/s RCs.

PARA (B) (1) (viii) Status in r/o disposal of OAs (Original Applications)

A report was obtained from the DRT-II, Chandigarh regarding the status of

disposal (as on 31/03/2011) of Original Applications (OAs) and it was noticed that

1113 OAs (involving Rs.1620.84 Crore) were pending as on 31/03/2011:

Total No. of OAs : 1113

Amount : 1620.84 Crore

Pending for more than 1 year to 3 year : 684

Pending for more than 3 year : 429

All the OAs were pending for more than one years. Under the DRT, Act, 1993

the cases should have been settled/decided with in six months.

Efforts needed to be taken to settle the OAs as early as possible.

32

OTHER DDOs

DDO (BIFR), NEW DELHI

PARA(B)(2)(i) Engagement of Security Guards.

During the checking of File No. 01(01)/BIFR/GAS/02 O/o the BIFR, New

Delhi, regarding engagement of Security Guards, it was observed that the office of the

BIFR, New Delhi has been obtaining the services of M/s Manpower Security Services

for providing 12 Hrs. securities since year 2008. The contract with M/s Manpower

Security Services has the following flaws:-

The Firm’s offer for providing for 8 Hrs duty for one Security Guard @ Rs.

4299/-/P.M. as per comparative Statement dated 21-10-2008, was accepted by the

Office of BIFR, New Delhi, but the firm is charging for 12 Hrs. showing 8+4=12 Hrs

taking duty from the one security Guard, means a Security Guard has to perform

continuous duty for 12 Hrs but salary paid to him is of 8 Hrs, which is in contravention

of the Factory’s Act and the other Laws of the State which prohibit the working hours

to be beyond 8 Hrs in a day for watch and ward duty. Besides this the firm is also

exploiting the (4) four security guards engaged for the Security of the office of the

BIFR, for which they have forwarded the compliant against the contractor to the Deptt.

As per comparative statement dated 21-10-2008 the firm has not quoted the rate

of service charge due to which the firm become first lowest whereas at the time of

billing the firm is changing the Service Charges@10% which is irregular and recovery

may be made from the firm for payment made on account of service charge which is

the contractor’s liability as the rate for the same was not quoted by the firm.

Non deposit of Bid Security & Performance Security: As per Rule 157 &

158 Bid Security and Performance Security to be got deposited from the bidder before

opening the tender.

DDO (CUSTODIAN), NEW DELHI

PARA (B) (2) (ii):- Non-Finalization of the lease deed of office irregular

payment of rent of Rs.68, 57,986/-.

The Custodian has occupied the portion of 3rd

floor of the Bank of Baroda

Building, Parliament Street, New Delhi on rent for their office@ Rs. 27/- per square

feet per month and service charge@5/- per square feet per month.. The office has paid

rent upto 31.07.2011 provisionally pending finalization of the lease deed. On review of

file No. CUS/ADMN./BOB/506/VOL.III revealed that the office has sent the draft

format of the lease deed to the Zonal office of Bank of Baroda vide letter no. 695/

CUS/ADMN./MHA/PAS/06(5270) dated 09.08.2011 the following are the observations

of audit.

33

(i) The payment of rent amounting to Rs. 102358x67 months= 6,857,986/- is

irregular due to non-renewal of agreement w.e.f. 01.01.2006 to till date. The

payment of rent of the building occupied by the office without proper lease

deed is irregular.

(ii) The Bank of Baroda vide their letter dated 19.4.2011 had demanded Rs.

39130/- June,07 to March 08 and April 08 to March 09 alongwith the penal

interest @13% amounting to Rs. 14,434/-. The un-timely payment of dues

attracting penal interest be avoided in future.

DDO (Spl. Court) Mumbai

PARA(B)(2)(iii). Non-Maintenance of stock Register of Cheque Books.

The DDO with Cheque drawing powers will requisition their requirement of

cheque books from the concerned Pay and Accounts Office. The latter will supply to

the DDO the minimum number of cheque books, sufficient for his requirement for

three months. Issue of such cheque books will also be entered in the stock Register of

cheque books.

To keep an account of the receipts, issues and balance of cheque books/forms

shall maintain (FORM CAM 1). Each morning, the Cashier should take such cheque

books from the Officer-in-charge, as likely to be used during the course of the day and

should remain responsible for their use and return of the balance at the close of the day.

Another register should be maintained by the cashier for showing the cheque forms

received by him each day and those returned by him. The entry should be made by the

Cashier with his dated initials in this register.

PARA(B)(2)(iv) Irregular direct appointment of staff.

On review of records, it was observed that OSD, Spl. Court, Mumbai has made

following temporary appointments:

S.

No.

Name of the Staff

Member

Designation Date of

Appointment

Old pay scale Revised pay

scale

1 Smt. V.A.Tikam Court Steno 10/6/2008 8000-13500 15600-39100

Gr. Pay 5400

2. Mr. P.H. Padelkar Clerk 10/10/1995 3050-75-3950-80-

4590

5200-20200 Gr.

Pay 1900

3. Smt.U.U. Kambli Clerk 06/04/2005 3050-75-3950-80-

4500

5200-20200 Gr.

Pay 1900

4. Mr. N.P. Kadam Clerk 02/02/2006 3050-75-3950-80-

4590

5200-20200 Gr.

Pay 1900

5 Mr. J.M. Deshmukh Driver 16/10/2009 13000 16000

6. Mr. P.D. Tawade Peon 09/01/2006 3050-75-3950-80-

4590

5200-20200 Gr.

Pay 1900

7. Mr. K.Y. Deshmukh Peon 06/02/2006 2500-55-2660-60-

3200

5200-20200 Gr.

Pay 1800

34

8. Mr. K.D. Pawar Peon 20/03/2007 2500-55-2660-60-

3200

5200-20200 Gr.

Pay 1800

9. Mr. R.R. Pardeshi Peon 06/03/2007 2500-55-2660-60-

3200

5200-20200 Gr.

Pay 1300

10. Mr. H.N. Sarang Peon 02/03/2009 2500-55-2660-60-

3200

5200-20200 Gr.

Pay 1800

As per GFR Rule 253

1. Proposal for additional to Establishment: All proposal for additions to

establishment shall be submitted to sanctioning authority in accordance with

the instructions contained in Rule 11 of the Delegation of Financial Powers

rules and other such instructions which may be prescribed in this regard.

a) All proposals for creation of new establishment or a revision in an existing

establishment, whether temporary or permanent in excess of delegated power

should contain, inter-alia: - The present costs of the establishment in existence.

b) Cost implication of the charge proposed giving details of pay and allowances of

posts(s) proposed

c) Expenditure in respect of claim to pension or gratuity or other retirement

benefits that may arise in consequence of he proposals;

d) Details on how the expenditure is proposed to be met including proposed re-

appropriations.

2. A full review of the justifications for continuation or conversations of

temporary posts on consultations with Intergraded finance or Ministry of

Finance where necessary should precede any order for continuation of

temporary posts or conversion into permanent posts.

3. All proposals for increase in emoluments for an existing posts(s) shall be

referred to the Ministry of Finance for approval.

The following observations are made in respect of the above.

Authority of Govt. of India under which the above appointments were made

have not been referred in the above orders, nor could the same be produced to audit for

review. On personal discussion with the OSD, it was apprised to audit that the above

appointments have been made with concurrences of the Hon’able Lordship of High

Court.

It was irregular, as the Hon’able Lordship of High Court have no jurisdiction to

make such appointment in Govt. of India. Therefore, services of above incumbents

may, therefore, immediately be terminated and such appointments may please be made

from staff selection commission/surplus cell to avoid any subsequent legal

complications toward their claiming regular appointments in future.

35

Medical examination at the time of 1st entry in Govt Service is a statutory

requirement.

2. Medical exam had not been conducted as per G.I.MF OM No. 45(1)-E-V/54,

dated 24th

March ,1954. No.5/6/54-RPS dt. 28th

Sepetember,1956 and DP &

AR OM No. 15015/1/79-Estt(d) dt. 26th

June 1971, included in Chapter 13 of

DDO Manual (pt.II) whereas in the cases referred above no medical

examination have been conducted which is irregular and may immediately be

complied with.

3. Police Verification: It has been noticed that no police verification was

conducted by the office of the Spl. Court Mumbai which is also irregular.

PARA(B)(2)(v) Irregular promotion during deputation.

During the scrutiny of the records of the Special Court, Mumbai it has been

noticed that employee appointed on deputation were promoted to Higher Scales, details

given in Annexure-‘A’ which is irregular as per Para 7.1 of Chapter 19 of Swamy’s

Complete Manual on Establishment and Administration and Appendix-5 of Swamy’s

Compilation of F.R.S.R. Part-I. This list is illustrative and not exhaustive, so these

cases alongwith such similar may be reviewed.

PARA(B)(2)(vi) Improper maintenance of Receipt Books:

As per Rule 22(1) (2) and (3) of Swamy’s Compilation of Receipt and

Payments Rules, Receipt Book in machine numbers in form GAR 6 has been

prescribed for receiving Government money. The Receipts Books must be kept in the

personal custody of the officer to authorize to sign the receipt on behalf of the

Government. Before a receipt book is brought into use, the number of forms contained

therein shall be counted and the result recorded in a conspicuous place in the book over

the signature of Govt. Officer, in-charge of the book. Counter foils of every receipt

books shall be kept in his personal custody. No Govt. Officer may issue duplicate or

copies of receipts granted for money received on the allegation that the original has

been lost.

During the scrutiny of Receipt Book No. 3101 to 3200, which is being used in

the audit period i.e. 1/4/2007 to 31/03/2011. it has been seen that receipt books is not

being maintained properly. Certificate of number of pages has not been given by the

officer in charge of the book. Counter foils of receipt 3167 is missing in the book,

which has been tear off in between the pages and the officials maintaining the receipts

books cannot give any satisfactory reply. No money has been taken in cash book nor

demand draft has been sent to PAO, ( Banking), New Delhi, received through, receipt

no. 3167. Loss of receipt like this is a serious lapse and it can leads to

fraud/embezzlement. Investigations may be done as to how the receipt has been lost

and responsibility may be fixed accordingly.

36

(C) DEPARTMENT OF REVENUE

DOO - CHITORGARH

PARA (C)(1)(i) Irregular expenditure on Pay and Allowances of canteen

staff for three posts against the sanctioned strength of two

posts.

It has been observed that the pay and allowances for the canteen staff is being

drawn for 3 persons since 2006-07 to 2010-11 against the sanctioned strength of 02

persons. This has also been observed during the audit for the period of 04/07 to 03/09.

The said pay and allowances of one extra employee are being drawn against the

sanctioned post of the office of DOO Kota whereas the salary is being drawn under the

budget head of DOO Div-.I, Chittorgarh which is irregular.

PARA (C)(1)(ii) Non-Recovery of amount of over payment of cost of opium

paid to cultivators to the tune of Rs. 19,13,986/- (as on

31.12.2011) including Rs. 36543/- for the financial year 2010-

2011.

During the course of Inspection of Register of Recoveries maintained for the

period from 1999-2000 to 2011-12, it has been observed that an amount of Rs.

19,13,986/- (as on 31.12.2011) including Rs. 36543/- for the financial year 2010-2011

is pending for recovery from the opium cultivators against the over-payment of opium

cost during the past years.

It is therefore, suggested that the outstanding amount shown above should be

recovered from the concerned cultivators.

ED –FEMA LUCKNOW

PARA (C)(2)(i) Pay fixation under the 6TH

CPC

As Shri Umesh Chandra, Chowkidar / Peon does not posses the required

minimum qualification, the official shall be re trained along with other ‘D’ officials

for allowing PB-1.

(A) Sh. Rajeshwar Singh, AD-II/AD-I.

(i) The officer joined the office as AD-II on 05.12.2007 (A/N) on deputation basis

from “UP Police”. The officer was paid “40% arrears of 6th

CPC” for the

period from 01-01-2006 to 31-07-2008 (including the period pertaining to “UP

Police”). Therefore, action may be taken to raise the debit (for arrears

37

pertaining to 01.01.2006 to 05.12.2007) against the “Govt. of UP Police”

asking the latter to pay the amount of arrears pertaining to them.

(ii) It has also been noticed that the special pay (Rs. 450/-) was added to the pay in

the pay band and the salary was paid accordingly. This addition of special pay

was not in order. The pay should be as follows and special pay of Rs. 450/- (or

any revised amount under the 6th

CPC to be verified from “UP Police”) shall be

payable separately as fixed amount per month.

01-01-2006 18470+5400=23870

01-07-2006 19190+5400=24590

01-07-2007 19930+5400=25330

01-07-2008 20690+5400=26090

AD-1 22-10-2008 21480+6600=28080

The pay & allowance/amount of arrears may be revised accordingly. The debit

balance payable by the Govt. of U.P. (UP Police) may be worked out accordingly.

Imp. The intimation of the recovery of arrears paid/recovery made for the period

w.e.f. 1.1.2006 to 5.12.2007 from Govt. of U.P. Police may be sent to IAW (HQ) and

PAO, Deptt. Of Revenue, New Delhi.

PARA (C)(2)(ii) Irregular grant of 3rd

MACP to the Grade pay of Rs. 6.600 to

Shri V.P. Gogia, Assistant Director and Shri A.K. Mathur,

AD-II.

(I) As per para 2 of Annexure 1 to OM. No. 35034/3/2008-Estt. (D) dated

19.05.2009 for grant of MACP on recommendation of 6th

CPC, the MACP

envisages merely placement in the immediate, not higher grade pay in the

hierarchy of the recommended revised pay bands and grade pay as given in

section 1, Part A of the first schedule of the CCS (Revised Pay) Rules, 2008.

Shri V.P. Gugia, Assistant Director has been given 3rd

financial up-

gradation w.e.f. 01.09.2008 in the MACP scheme to the grade pay of Rs. 6600

in PB-3 (Rs. 15600-39100). Vide esstt. Under No. 22/2009 dated 19.11.2009

by Enforcement Directorate New Delhi.

Prior to this MACP, he was placed in grade pay Rs. 5400 (PB-2) in PB-

2 Rs. 9300-34800. Accordingly he should be given 3rd

MACP in Grade Pay

Rs. 5400 in PB-3 (Rs. 15600-39100).

The order issued by the Directorate of Enforcement, New Delhi is not in

accordance with provisions of MACP, scheme which requires modification.

38

(II) Shri A.K. Mathur, AD-II, in spite of vetting of pay fixation by previous audit

party, pay fixation was not revised and recovery also not made according to

instruction:-

S. No. w.e.f. Pay wrongly allowed Pay to be fixed

1. 28.10.2007 Rs. 22100+5400 Rs. 21290+5400

2. 01.07.2009 Rs. 22930+5400 Rs. 22090+5400

On 28th

October 2007, he was promoted but promotional benefits not to be

allowed since there is no change in “Grade Pay” in term of rule 13 of CCS (Revised

Pay ) Rules, 2008.

He was given 3rd

MACP vide Establishment Order No. 22/2009 dated

17.11.2009 of Directorate of Enforcement, New Delhi and A-40/01/LZO/201-592 dtd.

26.05.2011 of Directorate of Enforcement, Lucknow to the next Grade pay Rs. 6600/-

in PB-3 (15600-39100) w.e.f.01.09.2008. He was in PB2(9300+34800) with Grade

Pay Rs. 5400.

The up-gradation under MACP is to be granted in the immediate next higher

Grade Pay in the hierarchy of recommended revised pay band and Grade pay as given

in Section I, Part A of the 1st schedule of the CCS Revised Pay Rules 2008. Keeping in

view of this point, he should be given 3rd

MACP in Band Pay Rs. 15600-39100 with

Grade Pay Rs. 5400/-. Grant of grade pay Rs. 6600/- is not correct, so error may be

rectified and excess payment be recovered.

The Pay of Shri A.K. Mathur, AD-II should be fixed in following manner:-

Period w.e.f. Pay Wrongly allowed Pay to be allowed

1.01.2006 Rs. 19790+5400 Rs. 10250(old scale)

01.04.2006 Rs. 19790+5400 Rs. 10500/-