Government of Haryanaaghr.cag.gov.in/FSVol-1_15-16( Eng).pdfHaryana for the year ending 31 March...

82

Finance Accounts (Volume- I) 2015-16 Government of Haryana

-

Upload

dinhnguyet -

Category

Documents

-

view

214 -

download

0

Transcript of Government of Haryanaaghr.cag.gov.in/FSVol-1_15-16( Eng).pdfHaryana for the year ending 31 March...

Finance Accounts (Volume- I)

2015-16

Government of Haryana

(i)

TABLE OF CONTENTS

Subject Page(s)

VOLUME-I

Certificate of the Comptroller and Auditor General of India (iii)-(v)

Guide to Finance Accounts (vii-xii)

1. Statement of Financial Position 1-2

2. Statement of Receipts and Disbursements 3-8

3. Statement of Receipts (Consolidated Fund) 9-11

4. Statement of Expenditure (Consolidated Fund) 12-18

5. Statement of Progressive Capital Expenditure 19-25

6. Statement of Borrowings and other Liabilities 26-30

7. Statement of Loans and Advances given by the Government 31-33

8. Statement of Investments of the Government 34

9. Statement of Guarantees given by the Government 35

10. Statement of Grants-in-aid given by the Government 36-37

11. Statement of Voted and Charged Expenditure 38

12. Statement on Sources and Application of Funds for Expenditure other than

on Revenue account

39-43

13. Summary of Balances under Consolidated Fund, Contingency Fund and

Public Account

44-47

Notes to Accounts 48-67

VOLUME-II

PART I

14. Detailed Statement of Revenue and Capital Receipts by Minor Heads 71-107

15. Detailed Statement of Revenue Expenditure by Minor Heads 108-169

16. Detailed Statement of Capital Expenditure by Minor Heads and Subheads 170-225

17. Detailed Statement of Borrowings and Other Liabilities 226-245

18. Detailed Statement of Loans and Advances given by the Government 246-273

19. Detailed Statement of Investments of the Government 274-289

20. Detailed Statement of Guarantees given by the Government 290-294

21. Detailed Statement on Contingency Fund and Other Public Account transactions 295-312

22. Detailed Statement on investment of Earmarked Balances 313-318

(ii)

TABLE OF CONTENTS

PART II APPENDICES

I. Comparative Expenditure on Salary 321-331

II. Comparative Expenditure on Subsidy 332-336

III. Grants-in-aid/Assistance given by the State Government

(Institution-wise and Scheme-wise)

337-358

IV. Details of Externally Aided Projects 359

V. Plan Scheme Expenditure

A. Centrally Sponsored Schemes and Central Plan Schemes

B. State Plan Schemes

360-368

VI. Direct transfer of Central Scheme Funds to Implementing Agencies in the State

(Funds routed outside State Budget) (Unaudited figures)

369-371

VII. Acceptance and Reconciliation of Balances 372-375

VIII. Financial Results of Irrigation Schemes 376-378

IX. Commitments of the Government-List of Incomplete Capital Works 379-387

X. Maintenance Expenditure with segregation of Salary and Non-Salary portion 388-393

XI. Major Policy Decisions of the Government during the year or new schemes

proposed in the Budget

394-395

XII. Committed Liabilities of the Government. 396

XIII. Re-organisation of the States-Items for which allocation of balances

between/among the States has not been finalized

397-398

(iii)

Certificate of the Comptroller and Auditor General of India

This compilation, containing the Finance Accounts of the Government of

Haryana for the year ending 31 March 2016, presents the financial position along with

accounts of the receipts and disbursements of the Government for the year. These accounts

are presented in two volumes, Volume I contains the consolidated position of the state of

finances and Volume II depicts the accounts in detail. The Appropriation Accounts of the

Government for the year for Grants and Charged Appropriations are presented in a

separate compilation.

The Finance Accounts have been prepared under my supervision in

accordance with the requirements of the Comptroller and Auditor General’s (Duties,

Powers and Conditions of Service) Act, 1971 and have been compiled from the vouchers,

challans and initial and subsidiary accounts rendered by the treasuries, offices and

departments responsible for the keeping of such accounts functioning under the control of

the Government of Haryana and the statements received from the Reserve Bank of India.

Statements (8, 9, 19 & 20), explanatory notes to Statements (6, 14, 15 & 20) and

appendices (IV, VIII, IX, X & XIII) in this compilation have been prepared directly from

the information received from the Government of Haryana/Corporations/

Companies/Societies who are responsible to ensure the correctness of such information.

Appendix VI has been prepared from the details collected from the Public Financial

Management System portal of the Controller General of Accounts.

The treasuries, offices, and/or departments functioning under the control of

the Government of Haryana are primarily responsible for preparation and correctness of

the initial and subsidiary accounts as well as ensuring the regularity of transactions in

accordance with the applicable laws, standards, rules and regulations relating to such

accounts and transactions. I am responsible for preparation and submission of Annual

Accounts to the State Legislature. My responsibility for the preparation of accounts is

discharged through the office of the Accountant General (A&E). The audit of these

accounts is independently conducted through the office of the Principal Accountant

General (Audit) in accordance with the requirements of Articles 149 and 151 of the

Constitution of India and the Comptroller and Auditor General’s (Duties, Powers and

Conditions of Service) Act, 1971, for expressing an opinion on these Accounts based on

the results of such audit. These offices are independent organizations with distinct cadres,

separate reporting lines and management structure.

(v)

The audit was conducted in accordance with the Auditing Standards

generally accepted in India. These Standards require that we plan and perform the audit to

obtain reasonable assurance that the accounts are free from material misstatement. An

audit includes examination, on a test basis, of evidence relevant to the amounts and

disclosures in the financial statements.

On the basis of the information and explanations that my officers required

and have obtained, and according to the best of my information as a result of test audit of

the accounts and on consideration of explanations given, I certify that, to the best of my

knowledge and belief, the Finance Accounts read with the explanatory ‘Notes to Accounts’

give a true and fair view of the financial position, and the receipts and disbursements of the

Government of Haryana for the year 2015-16.

Points of interest arising from study of these accounts as well as test audit

conducted during the year or earlier years are contained in my Reports on the Government

of Haryana being presented separately for the year ended 31 March 2016.

(SHASHI KANT SHARMA)

Date: 13 October 2016

Place: New Delhi

Comptroller and Auditor General of India

(vii)

Guide to Finance Accounts

A. Broad overview of the structure of Government accounts

1. The Finance Accounts of the State of Haryana present the accounts of receipts and outgoings of

the Government for the year, together with the financial results disclosed by the Revenue and

Capital accounts, the accounts of the Public Debt and the liabilities and assets of the State

Government as worked out from the balances recorded in the accounts.

2. The Accounts of the Government are kept in three parts:

Part I: Consolidated Fund: This Fund comprises all revenues received by the State Government,

all loans raised by the State Government (market loans, bonds, loans from the Central Government,

loans from Financial Institutions, Special Securities issued to National Small Savings Fund, etc.),

Ways and Means advances extended by the Reserve Bank of India and all moneys received by the

State Government in repayment of loans. No moneys can be appropriated from this Fund except in

accordance with law and for the purposes and in the manner provided by the Constitution of India.

Certain categories of expenditure (e.g., salaries of Constitutional authorities, loan repayments etc.),

constitute a charge on the Consolidated Fund of the State (Charged expenditure) and are not subject

to vote by the Legislature. All other expenditure (Voted expenditure) is voted by the Legislature.

The Consolidated Fund comprises two sections: Revenue and Capital (Public Debt, Loans and

Advances). These are further categorised under ‘Receipts’ and ‘Expenditure’. The Revenue

Receipts section is divided into three sectors, viz., ‘Tax Revenue’, ‘Non Tax Revenue’ and ‘Grants

in Aid and Contributions’. These three sectors are further divided into sub-sectors like ‘Taxes on

Income and Expenditure’, ‘Fiscal Services’, etc. The Capital Receipts section does not contain any

sectors or sub-sectors. The Revenue Expenditure section is divided into four sectors, viz., ‘General

Services’, ‘Social Services’, ‘Economic Services’ and ‘Grants in Aid and Contributions’. These

sectors in the Revenue Expenditure section are further divided into sub-sectors like, ‘Organs of

State’, ‘Education, Sports, Art and Culture’ etc. The Capital Expenditure section is sub-divided into

seven, sectors viz., ‘General Services’, ‘Social Services’, ‘Economic Services’, ‘Public Debt’,

‘Loans and Advances’, ‘Inter-State Settlement’ and ‘Transfer to Contingency Fund’.

Part II: Contingency Fund: This Fund is in the nature of an imprest which is established by the

State Legislature by law, and is placed at the disposal of the Governor to enable advances to be

made for meeting unforeseen expenditure pending authorisation of such expenditure by the State

Legislature. The fund is recouped by debiting the expenditure to the concerned functional major

head relating to the Consolidated Fund of the State. The Contingency Fund of the Government of

Haryana for 2015-16 is ` 200 crore.

Part III: Public Account: All other public moneys received by or on behalf of the Government,

where the Government acts as a banker or trustee, are credited to the Public Account. The Public

Account includes repayables like Small Savings and Provident Funds, Deposits (bearing interest

and not bearing interest), Advances, Reserve Funds (bearing interest and not bearing interest),

Remittances and Suspense heads (both of which are transitory heads, pending final booking). The

net cash balance available with the Government is also included under the Public Account. The

Public Account comprises six sectors, viz., ‘Small Savings, Provident Funds etc.’, ‘Reserve Funds’,

‘Deposit and Advances’, ‘Suspense and Miscellaneous’, ‘Remittances’, and ‘Cash Balance’. These

sectors are further sub-divided into sub-sectors. The Public Account is not subject to the vote of the

Legislature.

(viii)

3. Government accounts are presented under a six tier classification, viz., Major Heads (four digits),

Sub-Major Heads (two digits), Minor Heads (three digits), Sub-Heads (two characters), Detailed

Heads (two digits), and Object Heads (two digits). Major Heads represent functions of

Government, Sub- Major Heads represent sub-functions, Minor Heads represent programmes/

activities, Sub-Heads represent schemes, Detailed Heads represent sub-schemes, and Object Heads

represent purpose/ object of expenditure.

4. The main unit of classification in accounts is the Major Head which contains the following

coding pattern (according to the List of Major and Minor Heads corrected upto 31 March 2016)

0020 to 1606 Revenue Receipts

2011 to 3606 Revenue Expenditure

4000 Capital Receipts

4046 to 7810 Capital Expenditure (including Public Debt, Loans and Advances)

7999 Appropriation to the Contingency Fund

8000 Contingency Fund

8001 to 8999 Public Account

5. The Finance Accounts, generally (with some exceptions), depict transactions upto the Minor

Head. The figures in the Finance Accounts are depicted at net level, i.e., after accounting for

recoveries as reduction of expenditure. This treatment is different from the depiction in the

Demands for Grants presented to the Legislature and in the Appropriation Accounts, where,

expenditure is depicted at the gross level.

6. A pictorial representation of the structure of accounts is given below:

33.

Structure of Government Accounts

Government Accounts

Consolidated Fund

Revenue Capital, Public Debt,

Loans etc.

Contingency Fund Public Account

Receipts Expenditure

General Services, Social

Services, Economic Services,

Grants- in -Aid

Expenditure/

Payments Receipts

General Services, Social Services,

Economic Services, Public Debt,

Loans and Advances, Inter-State

Settlement, Transfer to Contingency

Fund

Small Savings, Provident Fund

etc., Reserve Funds, Deposits and

Advances, Suspense, Remittances

and Cash Balance

Tax, Non Tax and

Grants- in -Aid

(ix)

B. What the Finance Accounts contain

The Finance Accounts are presented in two volumes.

Volume I contains the Certificate of the Comptroller and Auditor General of India, the Guide to the

Finance Accounts, 13 statements which give summarised information on the financial position and

transactions of the State Government for the current financial year, Notes to Accounts and annexure

to the Notes to Accounts. Details of the 13 statements in Volume I are given below:

1. Statement of Financial Position: This statement depicts the cumulative figures of assets and

liabilities of the State Government, as they stand at the end of the year, and as compared to

the position at the end of the previous year.

2. Statement of Receipts and Disbursements: This statement depicts all receipts and

disbursements of the State Government during the year in all the three parts in which

Government accounts are kept, viz., the Consolidated Fund, Contingency Fund and Public

Account. In addition, it contains an annexure, showing alternative depiction of Cash

Balances (including investments) of the Government. The Annexure also depicts the Ways

and Means position of the Government in detail.

3. Statement of Receipts (Consolidated Fund): This statement comprises revenue and capital

receipts and borrowings and repayments of loans given by the State Government. This

statement corresponds to detailed statements 14, 17 and 18 in Volume II of the Finance

Accounts.

4. Statement of Expenditure (Consolidated Fund): In departure from the general depiction of

the Finance Accounts up to the Minor Head level, this statement gives details of expenditure

by nature of activity (objects of expenditure) also. This statement corresponds to detailed

statement 15, 16, 17 and 18 in Volume II.

5. Statement of Progressive Capital Expenditure. This statement corresponds to the detailed

statement 16 in Volume II.

6. Statement of Borrowings and Other Liabilities: Borrowings of the Government comprise

market loans raised by it (Internal Debt) and Loans and Advances received from the

Government of India. ‘Other Liabilities’ comprise ‘Small Savings, Provident Funds etc.’,

‘Reserve Funds’ and ‘Deposits’. The statement also contains a note on service of debt, and

corresponds to the detailed Statement 17 in Volume II.

7. Statement of Loans and Advances given by the Government: This statement depicts all

loans and advances given by the State Government to various categories of loanees like

Statutory Corporations, Government Companies, Autonomous and Other Bodies/ Authorities

and recipient individuals (including Government servants). This statement corresponds to the

detailed statement 18 in Volume II.

8. Statement of Investments of the Government: This statement depicts investments of the

State Government in the equity capital of Statutory Corporations, Government Companies,

other Joint Stock Companies, Cooperative institutions and Local Bodies. This statement

corresponds to the detailed statement 19 in Volume II.

9. Statement of Guarantees given by the Government: This statement summarises the

guarantees given by the State Government on repayment of principal and interest on loans

raised by Statutory Corporations, Government Companies, Local Bodies and Other

institutions. This statement corresponds to the detailed statement 20 in Volume II.

10. Statement of Grants in Aid given by the Government: This statement depicts all Grants in

Aid given by the State Government to various categories of grantees like Statutory

Corporations, Government Companies, Autonomous and Other Bodies/ Authorities and

individuals. Appendix III .provides details of the recipient institutions.

(x)

11. Statement of Voted and Charged Expenditure: This statement assists in the agreement of

the net figures appearing in the Finance Accounts with the gross figures appearing in the

Appropriation Accounts.

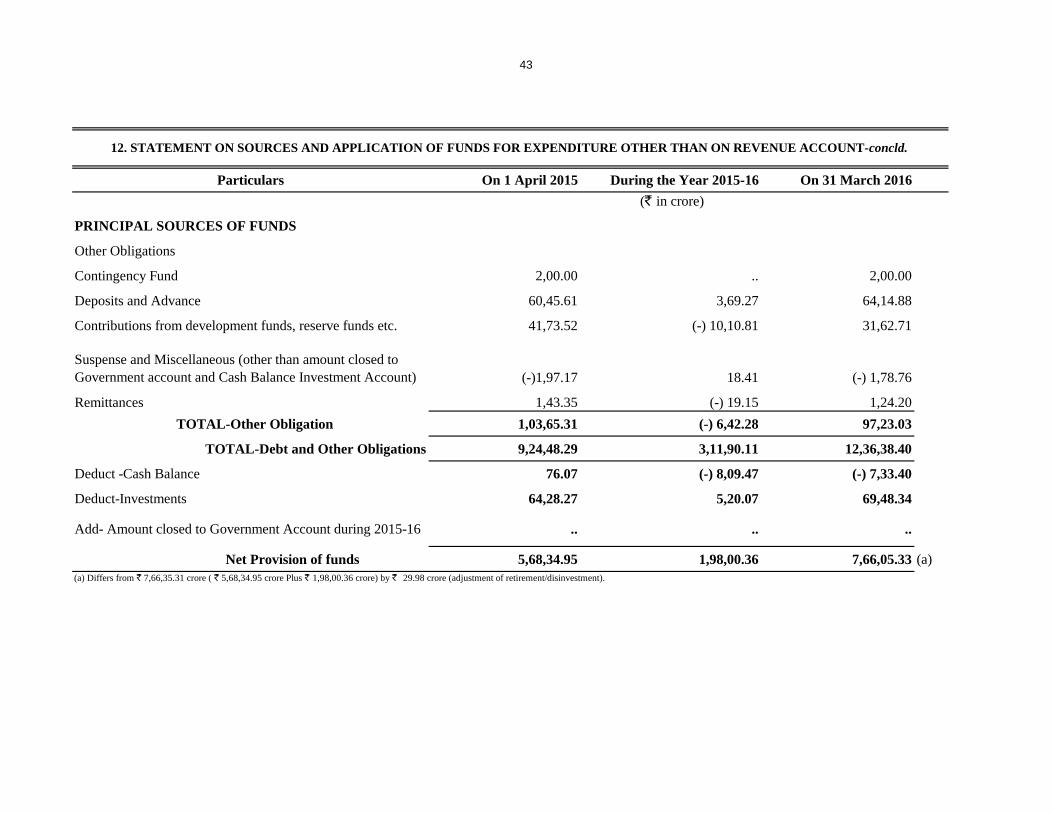

12. Statement on Sources and Application of Funds for Expenditure other than on Revenue

Account: This statement is based on the principle that revenue expenditure is expected to be

defrayed from revenue receipts, while capital expenditure of the year is met from revenue

surplus, net credit balances in the public account, cash balance at the beginning of the year,

and borrowings.

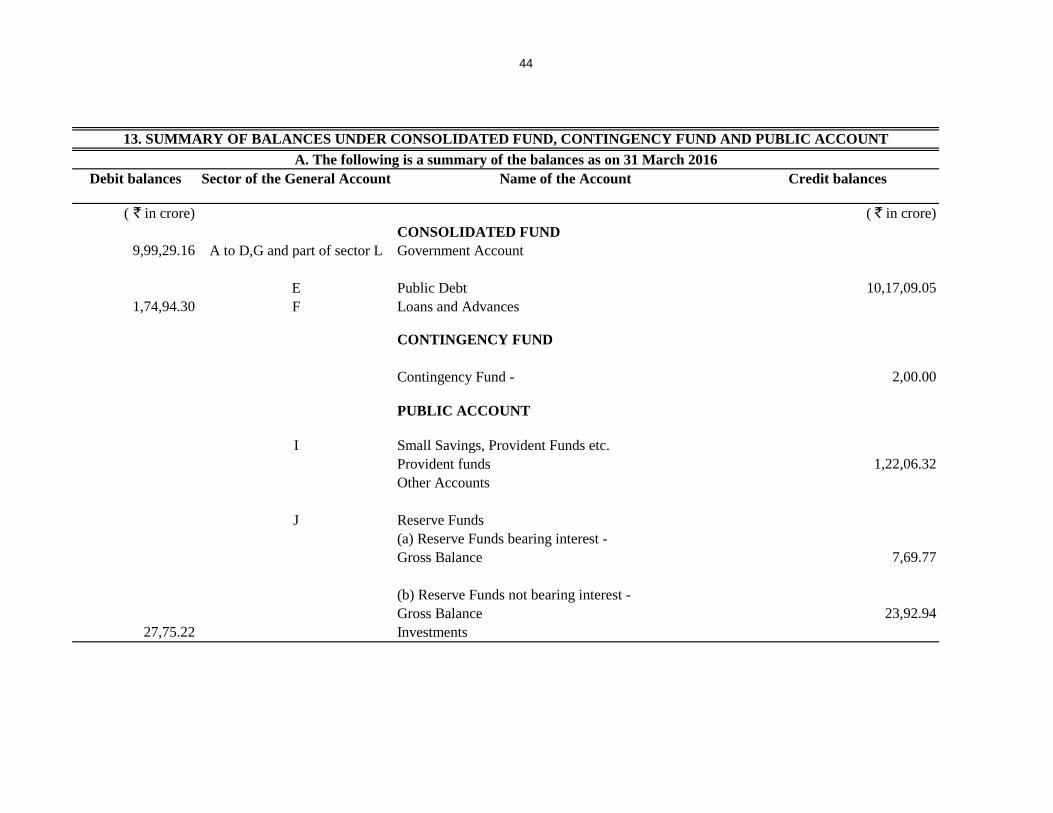

13. Summary of balances under Consolidated Fund, Contingency Fund and Public

Account: This statement assists in proving the accuracy of the accounts. The statement

corresponds to the detailed statement 14, 15, 16, 17, 18 and 21 in Volume II

Volume II of the Finance Accounts contains two parts-nine detailed statement in Part I and 13

Appendices in Part II.

Part I of Volume II

14. Detailed Statement of Revenue and Capital Receipts by Minor Heads: This statement

corresponds to the summary statement 3 in Volume I of the Finance Accounts.

15. Detailed Statement of Revenue Expenditure by Minor Heads: This statement, which

corresponds to the summary statement 4 in Volume I, depicts the revenue expenditure of the

State Government under Plan (State Plan, Central Assistance to State Plan, Centrally

Sponsored Schemes and Central Plan Schemes) and Non Plan. Charged and Voted

expenditure are exhibited distinctly.

16. Detailed Statement of Capital Expenditure by Minor Heads and Subheads: This

statement, which corresponds to the summary statement 5 in Volume I, depicts the capital

expenditure (during the year and cumulatively) of the State Government under Plan (State

Plan, Central Assistance to State Plan, Centrally Sponsored Schemes and Central Plan

Schemes) and Non Plan. Charged and Voted expenditure are exhibited distinctly. In addition

to representing details of capital expenditure at Minor Head level, in respect of significant

schemes, this statement depicts details at Subhead levels also.

17. Detailed Statement of Borrowings and Other Liabilities: This statement, which

corresponds to the summary statement 6 in Volume I, contains details of all loans raised by

the State Government (market loans, bonds, loans from the Central Government, loans from

Financial Institutions, Special Securities issued to National Small Savings Fund, etc.), and

Ways and Means advances extended by the Reserve Bank of India. This statement presents

the information on loans under three categories: (a) details of individual loans; (b) maturity

profile, i.e., amounts payable in respect of each category of loans in different years; and (c)

interest rate profile of outstanding loans and annexure depicting Market Loans.

18. Detailed Statement of Loans and Advances given by the Government: This statement

corresponds to the summary statement 7 in Volume I.

19. Detailed Statement of Investments of the Government: This statement depicts details of

investments entity wise and Major and Minor Head wise details of discrepancies, if any,

between Statements 16 and 19. This statement corresponds to Statement 8 in Volume I.

20. Detailed Statement of Guarantees given by the Government: This statement depicts

entity wise details of government guarantees. This statement corresponds to Statement 9 in

Volume I.

(xi)

21. Detailed Statement on Contingency Fund and Other Public Account transactions: This

statement depicts at Minor Head level the details of unrecouped amounts under Contingency

Fund, consolidated position of Public Accounts transactions during the year, and outstanding

balances at the end of the year.

22. Detailed Statement on Investment of Earmarked Balances: This statement depicts details

of investments from the Reserve Funds and Deposits (Public Account).

Part II of Volume II

Part II contains 13 appendices on various items including salaries, subsidies, grants-in-aid,

externally aided projects, scheme wise expenditure in respect of major Central schemes and State

Plan schemes, etc. These details are presented in the accounts at Sub head level or below (i.e. below

Minor Head levels) and so are not generally depicted in the Finance accounts. A detailed list of

appendices appears at the ‘Table of Contents’ in Volume I or II. The statements read with the

appendices give a complete picture of the state of finances of the State Government.

C. Ready Reckoner

The section below links the summary statements appearing in Volume I with the detailed

statements and appendices in Volume II (Appendices which do not have a direct link with the

Summary Statements are not shown below).

D. Periodical adjustments and Book adjustments:

Certain transactions that appear in the accounts do not involve actual movement of cash at

the time of booking. Some of these transactions take place at the level of the account rendering

units (e.g. treasuries, divisions etc.) themselves. For instance, transactions involving adjustment of

all deductions (GPF, recoveries of advances given etc.) from salaries are recorded by debiting

functional major heads (pertaining to the concerned department) by book adjustment to revenue

receipt/loans/public account. Similarly ‘nil’ bills where moneys transferred between the

Consolidated Fund and Public Account represent non-cash transactions occurring at the level of the

accounts rendering units.

Parameter Summary

Statements

(Volume I)

Detailed

Statements

(Volume II)

Appendices

Revenue Receipts (including

Grants received), Capital

Receipts

2, 3 14

Revenue Expenditure 2, 4 15 I (Salary), II (Subsidy)

Grants-in-Aid given by the

Government

2,10 -- III (Grants-in-Aid)

Capital expenditure 1, 2, 4,5,12 16 I (Salary)

Loans and Advances given by

the Government

1, 2, 7 18

Debt Position/Borrowings 1, 2, 6 17

Investments of the

Government in Companies,

Corporations etc

8 19

Cash 1, 2,12,13

Balances in Public Account

and investments thereof

1, 2,12,13 21, 22

Guarantees 9 20

Schemes IV (Externally Aided

Projects), V (Plan Scheme

expenditure)

(xii)

In addition of the above the Principal Accountant General/Accountant General (A&E)

carries out periodical adjustments and book adjustments of the following nature in the accounts of

the State Government, details of which appear in Annexure to Notes to Accounts (Volume I) and

footnotes to the relevant statements.

Examples of periodical adjustments and book adjustments are given below:

(1) Creation of funds/ adjustment of contribution to Funds in Public Account by debit to

Consolidated Fund e.g., State Disaster Response Fund, Central Road Fund, Reserve Funds, Sinking

Fund, etc.

(2) Crediting of deposit heads of accounts in Public Account by debit to Consolidated Fund.

(3) Annual adjustment of interest on General Provident Fund(GPF) and State Government

Group Insurance Scheme where interest is adjusted by debiting Major Head 2049-Interest and

crediting Major Head 8009-State Provident Fund and 8011- Insurance and Pension Fund.

(4) Adjustment of Debt waiver under the scheme of Government of India based on the

recommendations of the Central Finance Commissions. These adjustments (where Central loans are

written off by crediting Major Head 0075-Misc. General Services by contra entry in the Major

Head 6004-Loans and Advances from the Central Government) impact both Revenue Receipts and

Public Debt heads.

E. Rounding:

Difference of ` 0.01 lakh/crore, wherever occurring, is due to rounding.

1

Notes to

Accounts

Statement

21 62,17.73 65,07.52

(i) Cash in Treasuries and

Local Remittances

0.54 0.54

(ii) Departmental Balances 21 2.68 3.07

(iii) Permanent Imprest 21 0.11 0.11

(iv) Investments of Cash

Balance

21 41,73.12 25,71.52

(v) Deposits with Reserve

Bank of India

21 (-) 7,33.94 75.53

(vi) Investments from

Earmarked Funds

22 27,75.22 38,56.75

16 5,90,24.03 5,21,45.68

(i) Investments in shares of

Companies, Corporations

etc.

19 93,72.44 75,00.22

(ii) Other Capital Expenditure 16 4,96,51.59 4,46,45.46

.. ..

3(iii) 18 1,74,94.30 45,72.29

21 0.72 0.72

3(vi) 21 1,75.97 1,93.99

21 .. ..

12 4,09,05.13 2,92,25.98

12,38,17.88 9,26,46.18

*

[1]

[2]

Total

In this statement the line item ‘Suspense and Miscellaneous Balances’ does not include ‘Cash Balance Investment Account’ ,

which is included separately above, though the latter forms part of this sector elsewhere in these Accounts.

The cumulative excess of receipts over expenditure or expenditure over receipts is different from and not the fiscal/revenue

deficit for the current year.

The figures of assets and liabilities are cumulative figures. Please also see Para 1(ii) in the section 'Notes to Accounts'.

(` in crore)

Contingency Fund

(unrecouped)

Loans and Advances

1. STATEMENT OF FINANCIAL POSITION

Reference

(Sr. No.)

Capital Expenditure

As on

31 March 2015

Cumulative excess of

expenditure over receipts[2]

Suspense and Miscellaneous

Balances[1]

Advances with departmental

officers

As on

31 March 2016

Assets*

Cash

Remittance Balances6

2

Notes to

Accounts

Statement

(i) Internal Debt 17 9,96,60.13 6,87,97.47

(ii) Loans and Advances from

Central Government

17 20,48.92 21,27.83

Non-Plan Loans 45.29 47.16

Loans for State Plan

Schemes

19,97.30 20,74.34

Loans for Central Plan

Schemes

.. ..

Loans for Centrally

Sponsored Plan Schemes

6.33 6.33

Other loans .. ..

21 2,00.00 2,00.00

21

(i) Small Savings, Provident

Funds, etc.

1,22,06.32 1,11,57.68

(ii) Deposits 64,15.60 60,46.33

(iii) Reserve Funds 31,62.71 41,73.52

(iv) Suspense and

Miscellaneous Balances

.. ..

(v) Remittance Balances 1,24.20 1,43.35

.. ..

12,38,17.88 9,26,46.18Total

Liabilities on Public Account

Cumulative excess of receipts

over expenditure

Borrowings (Public Debt)

Contingency Fund (balance)

1. STATEMENT OF FINANCIAL POSITION-concld.

As on

31 March 2016

As on

31 March 2015

Reference

(Sr. No)

Liabilities

(` in crore)

3

2015-16 2014-15 2015-16 2014-15

4,75,56.55 4,07,98.66 Revenue

Expenditure (Ref. Statement 4-A, 4-B & 15)

5,92,35.70 4,91,17.87

3,09,29.09 2,76,34.57 Salaries[1]

(Ref. Statement 4-B & Appendix-I)

1,45,32.18 1,37,58.52

47,52.48 46,13.12 Subsidies[1]

(Ref. Appendix-II)

68,98.81 56,93.34

Grants-in-aid[2]

(Ref. Statement 4-B, 10 & Appendix-III)

1,07,65.97 61,06.00

10,87.49 9,33.59 General Services (Ref. Statement 4 & 15)

1,47,93.79 1,30,42.06

36,64.99 36,79.53 Interest Payment and

service of debt (Ref. Statement 4 -A, 4-B & 15)

85,46.55 69,28.27

47,52.48 46,13.12 Pension (Ref. Statement 4 -A, 4-B & 15)

54,13.28 46,02.00

54,96.22 35,48.09Others (Ref. Statement 4-B)

8,33.96 15,11.79

Total (Ref. Statement 4-A & 15)

1,47,93.79 1,30,42.06

Social Servies (Ref. Statement 4-A & 15)

87,40.66 73,65.04

Economic Services (Ref. Statement 4-A & 15)

32,11.14 30,08.32

63,78.76 50,02.88 Compensation and

Assignment to

Local Bodies and

Panchayati Raj

Institutions (Ref. Statement 4-A & 15)

2,93.15 1,44.59

1,16,79.15 83,19.21 Revenue Surplus .. ..

[1]

[2]

2. STATEMENT OF RECEIPTS AND DISBURSEMENTS

Receipts

Part-I Consolidated Fund

Section-A: Revenue

(` in crore)

Disbursements

Tax Revenue

(raised by the State) (Ref. Statement 3 & 14)

Non-tax Revenue (Ref. Statement 3 & 14)

Others (Ref. Statement 3)

Interest receipts (Ref. Statement 3 & 14)

Grants from

Central Government (Ref. Statement 3 & 14)

Total (Ref. Statement 3 & 4)

Share of Union

Taxes/Duties (Ref. Statement 3 & 14)

Grant-in-aid comprises the total of the Object Heads (code 09 and 43 ) across all the Major Heads and totals of Minor Heads

191,192,193,196,197 and 198. Grants-in-aid are given to statutory corporations, companies, autonomous bodies, local bodies etc by the

Government which is included as a line item above. These grants are distinct from compensation and assignments of taxes, duties to the Local

Bodies which is depicted as a separate line item ‘Compensation and Assignment to Local Bodies and Panchayati Raj Institutions'.

Revenue Receipts (Ref. Statement 3 & 14)

Revenue Deficit

Salary, Subsidy and Grants-in-aid figures have been summed up across all sectors to present a consolidated figure. The expenditure in this

statement under the sectors ‘Social’, ‘General’ and ‘Economic’ Services does not include expenditure on Salaries, Subsidies and Grants-in-

Aid (explained in footnote 2).

4

2015-16 2014-15 2015-16 2014-15

29.98 18.74 Capital Expenditure (Ref. Statement 4-A, 4-B & 16)

69,08.33 37,15.53

General Services (Ref. Statement 4-A & 16)

4,60.56 2,90.70

Social Services (Ref. Statement 4-A & 16)

15,39.99 18,97.56

Economic Services (Ref. Statement 4-A & 16)

49,07.78(a) 15,27.27(b)

3,28.28 2,72.82 Loans and

Advances disbursed (Ref. Statement 4-A, 7 & 18)

1,32,50.29 8,42.87

General Services (Ref. Statement 4-A, 7 & 18)

.. ..

Social Services (Ref. Statement 4-A, 7 & 18)

.. ..

Economic Services (Ref. Statement 4-A, 7 & 18)

1,29,75.09 5,46.58

Loans to Government

Servants (Ref. Statement 4-A, 7 & 18)

2,75.20 2,96.29

3,79,98.43 1,88,58.75 Repayment of

Public Debt (Ref. Statement 4-A, 6 & 17)

72,14.68 82,27.41

3,79,01.20 1,87,27.99 Internal Debt

(Market loans, NSSF

etc.) (Ref. Statement 4-A, 6 & 17)

70,38.54 80,73.67

97.23 1,30.76 Loans from

Government of India (Ref. Statement 4-A, 6 & 17)

1,76.14 1,53.74

.. .. Inter-State

Settlement Account

(Net)

.. ..

8,59,13.24 5,99,48.97 Total Expenditure

Consolidated Fund (Ref. Statement 4)

8,66,09.00 6,19,03.68

6,95.76 19,54.71 Surplus in

Consolidated Fund

.. ..

(b) Includes ` 3,97.30 crore on account of Salary.

2. STATEMENT OF RECEIPTS AND DISBURSEMENTS-contd.

Receipts

(a) Includes ` 4,93.06 crore on account of Salary.

Recoveries of Loans

and Advances (Ref. Statement 3, 7 & 18)

Public Debt Receipts (Ref. Statement 3, 6 & 17)

Internal Debt

(Market loans, NSSF

etc.) (Ref. Statement 3, 6 & 17)

Disbursements

Section-B: Capital

Deficit in

Consolidated Fund

Total Receipts

Consolidated Fund (Ref. Statement 3)

Inter-State

Settlement Account

(Net)

Loans from

Government of India (Ref. Statement 3, 6 & 17)

Capital Receipts (Ref. Statement 3 & 14)

(` in crore)

Part-I Consolidated Fund

5

2015-16 2014-15 2015-16 2014-15

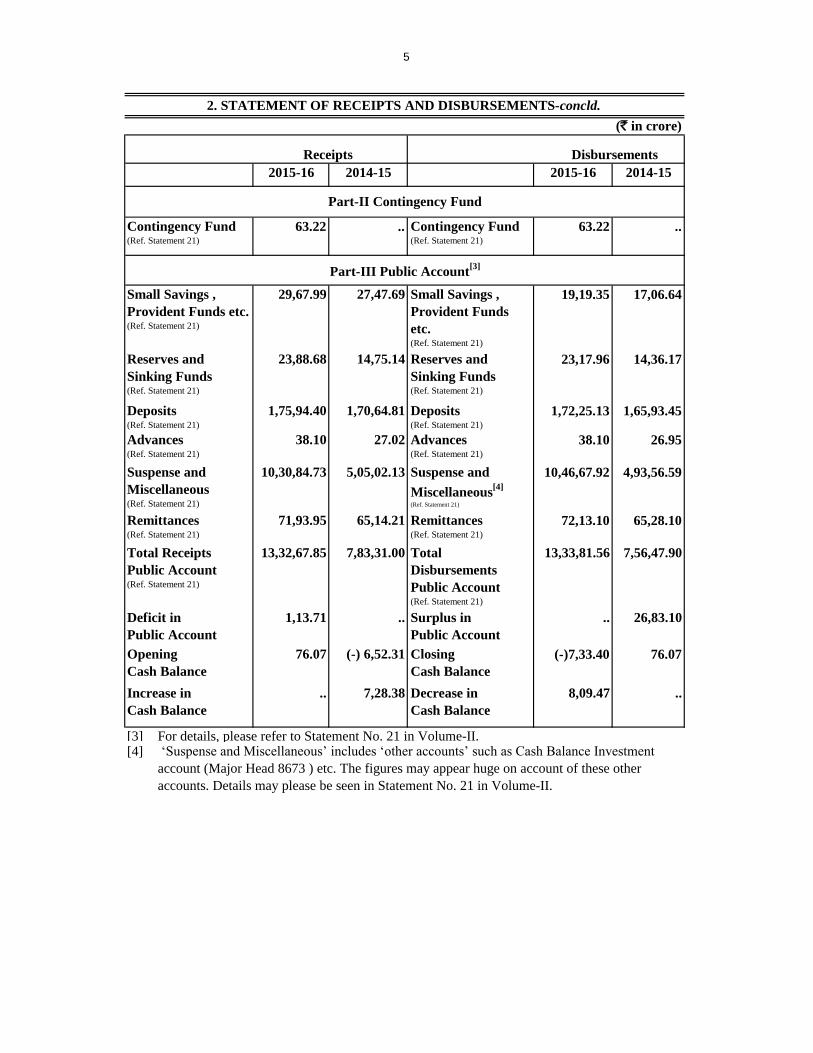

63.22 .. Contingency Fund (Ref. Statement 21)

63.22 ..

29,67.99 27,47.69 Small Savings ,

Provident Funds

etc. (Ref. Statement 21)

19,19.35 17,06.64

23,88.68 14,75.14 Reserves and

Sinking Funds (Ref. Statement 21)

23,17.96 14,36.17

1,75,94.40 1,70,64.81 Deposits (Ref. Statement 21)

1,72,25.13 1,65,93.45

38.10 27.02 Advances (Ref. Statement 21)

38.10 26.95

10,30,84.73 5,05,02.13 Suspense and

Miscellaneous[4]

(Ref. Statement 21)

10,46,67.92 4,93,56.59

71,93.95 65,14.21 Remittances (Ref. Statement 21)

72,13.10 65,28.10

13,32,67.85 7,83,31.00 Total

Disbursements

Public Account (Ref. Statement 21)

13,33,81.56 7,56,47.90

1,13.71 .. Surplus in

Public Account

.. 26,83.10

76.07 (-) 6,52.31 Closing

Cash Balance

(-)7,33.40 76.07

.. 7,28.38 Decrease in

Cash Balance

8,09.47 ..

[3][4]

Receipts Disbursements

(` in crore)

2. STATEMENT OF RECEIPTS AND DISBURSEMENTS-concld.

‘Suspense and Miscellaneous’ includes ‘other accounts’ such as Cash Balance Investment

account (Major Head 8673 ) etc. The figures may appear huge on account of these other

accounts. Details may please be seen in Statement No. 21 in Volume-II.

Deficit in

Public Account

Opening

Cash Balance

Increase in

Cash Balance

Advances (Ref. Statement 21)

Suspense and

Miscellaneous (Ref. Statement 21)

Remittances (Ref. Statement 21)

Total Receipts

Public Account (Ref. Statement 21)

Small Savings ,

Provident Funds etc. (Ref. Statement 21)

For details, please refer to Statement No. 21 in Volume-II.

Part-II Contingency Fund

Reserves and

Sinking Funds (Ref. Statement 21)

Deposits (Ref. Statement 21)

Part-III Public Account[3]

Contingency Fund (Ref. Statement 21)

6

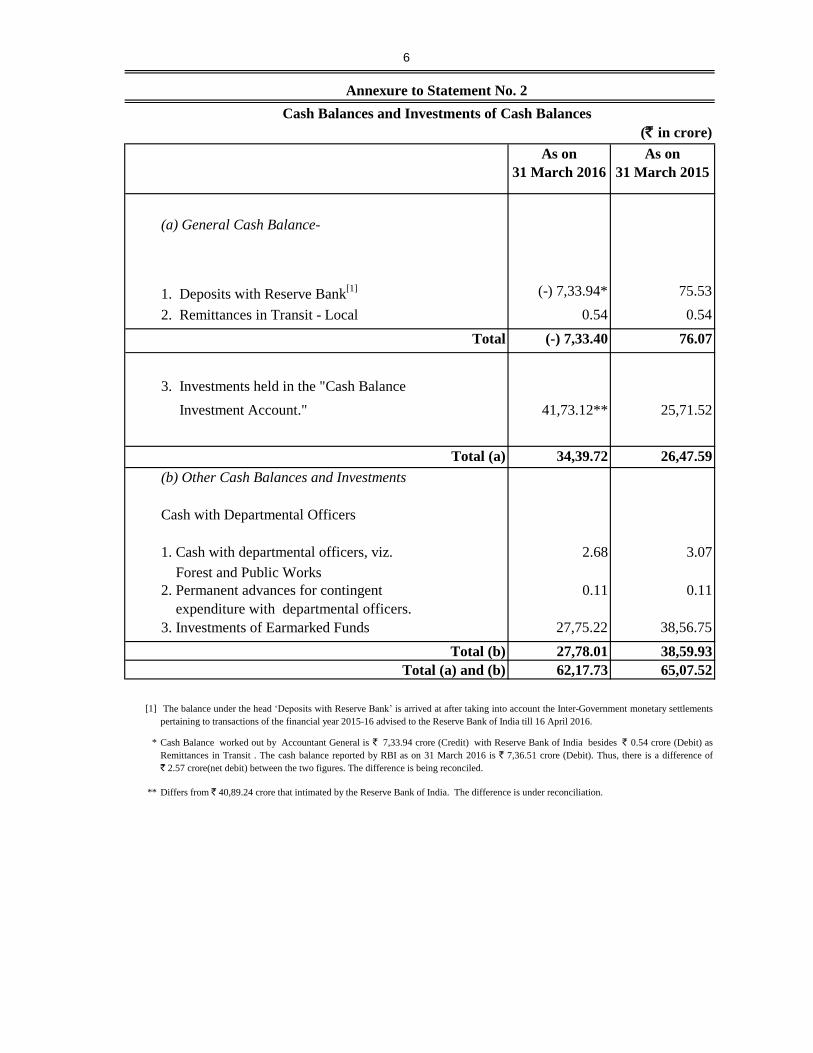

As on

31 March 2016

As on

31 March 2015

(a) General Cash Balance-

1. Deposits with Reserve Bank[1] (-) 7,33.94* 75.53

2. Remittances in Transit - Local 0.54 0.54

Total (-) 7,33.40 76.07

3. Investments held in the "Cash Balance

Investment Account." 41,73.12** 25,71.52

Total (a) 34,39.72 26,47.59

(b) Other Cash Balances and Investments

Cash with Departmental Officers

1. Cash with departmental officers, viz. 2.68 3.07

Forest and Public Works

2. Permanent advances for contingent 0.11 0.11

expenditure with departmental officers.

3. Investments of Earmarked Funds 27,75.22 38,56.75

Total (b) 27,78.01 38,59.93

Total (a) and (b) 62,17.73 65,07.52

[1]

*

**

Annexure to Statement No. 2

Cash Balances and Investments of Cash Balances

(` in crore)

The balance under the head ‘Deposits with Reserve Bank’ is arrived at after taking into account the Inter-Government monetary settlements

pertaining to transactions of the financial year 2015-16 advised to the Reserve Bank of India till 16 April 2016.

Cash Balance worked out by Accountant General is ` 7,33.94 crore (Credit) with Reserve Bank of India besides ` 0.54 crore (Debit) as

Remittances in Transit . The cash balance reported by RBI as on 31 March 2016 is ` 7,36.51 crore (Debit). Thus, there is a difference of

` 2.57 crore(net debit) between the two figures. The difference is being reconciled.

Differs from ` 40,89.24 crore that intimated by the Reserve Bank of India. The difference is under reconciliation.

7

For arriving at the daily cash balance[2]

for the purpose of grant of Ways and Means

advances/Overdraft, the RBI evaluates the holdings of the 14 day treasury bills along with

the transactions reported (at RBI counters, Inter-Government transactions and Treasury

transactions reported by the agency banks) for the day. To the cash balance so arrived, the

maturity of 14 day Treasury Bills if any, is added and excess balance, if any, after

maintaining the minimum cash balance is reinvested in Treasury Bills. If the net cash

balance arrived at results in less than the minimum cash balance or a credit balance and if

there are no 14 day treasury bills maturing on that day, RBI rediscounts the holdings of the

14 day Treasury Bills and makes good the shortfall. If there is no holding of 14 day Treasury

Bills on that day the State Government applies for Ways and Means Advances/Special Ways

and Means Advances/ Over Draft.

(b) Daily Cash Balance: Under an agreement with the Reserve Bank of India, the State

Government has to maintain a minimum cash balance of ` 1.14 crore with the Bank. If the

balance falls below the agreed minimum on any day, the deficiency is made good by taking

ordinary and special ways and means advances/overdrafts from time to time.

[2]The cash balance (Deposits with Reserve Bank of India) above is the closing cash balance

of the year as on 31 March 2016 but worked out by 16 April and not simply the daily

balance on 31 March 2016.

(c) The limit for ordinary ways and means advances to the State Government was

` 4,42.50 crore during 1 April 2015 to 31 January 2016 and `9,15.00 crore during 1 February

2016 to 31 March 2016. The Bank has also agreed to give special ways and means advances

against the pledge of Government Securities. The limit of special ways and means advances

is revised by the Bank from time to time.

(a) Cash and Cash Equivalents: Cash and cash equivalents consist of cash in treasuries

and deposit with Reserve Bank of India and other Banks and Remittances in Transit, as

stated in the pre-page statement. The balance under the head ‘Deposits with Reserve Bank’

depicts the combined balance of the Consolidated Fund, Contingency Fund and the Public

Account at the end of the year. To arrive at the overall cash position, the cash balances with

treasuries, departments and investments out of the cash balances/reserve funds etc. are added

to the balance in ‘Deposits with Reserve Bank of India’.

Annexure to Statement No. 2-contd.

Cash Balances and Investments of Cash Balances

Explanatory Notes

8

(i) Number of days on which the minimum balance was maintained 366

without taking any advance

(ii) Number of days on which the minimum balance was maintained by ..

taking ordinary ways and means advance

(iii) ..

(iv) Number of days on which there was shortfall in minimum balance ..

even after taking the above advances, but no overdraft was taken

(v) Number of days on which overdrafts were taken ..

At the close of the year 2014-15 no amount was outstanding under ways and means advances

and overdraft. During 2015-16, no ways and means advance or overdraft was taken.

The amounts invested out of earmarked funds are shown in Statement No. 22.

The State Government has invested ` 41,73.12 crore in the Government of India Securities

under Cash Balance Investment Account. Interest realised during the year on these

investments was ` 1,86.49 crore which was ` 1,06.79 crore more than that realised during

last year. The interest rate on investment varied from 5 per cent to 5.5 per cent during the

year.

Number of days on which the minimum balance was maintained by taking

special ways and means advance

The extent to which the Government maintained the minimum cash balance with the Reserve

Bank during 2015-16 is given below:-

Cash Balances and Investments of Cash Balances

Annexure to Statement No. 2-concld .

9

2015-16 2014-15

A.

A.1 3,09,29.09 2,76,34.57

14.97 15.28

31,91.21 31,08.70

43,71.08 34,70.45

2,10,60.23 1,89,93.25

5,54.25 5,27.07

14,00.38 11,91.50

80.31 88.58

2,56.66 2,39.74

A.2 54,96.22 35,48.09

17,33.37 12,39.11

12,04.79 8,84.83

0.03 0.03

0.40 3.35

8,80.83 5,73.87

7,33.13 3,24.04

9,39.76 5,22.86

3.91 ..

3,64,25.31 3,11,82.66

B

12,54.55 12,35.31

10,87.49* 9,33.59

6,37.42 5,64.48

2,71.61 43.46

98.21 1,22.26

4,21.95 8,61.11

1,15.65 95.73

41.39 20.38

51.90 44.29

1,51.70 67.82

1,42.06 1,45.50

94.78 83.10

3,83.77 3,96.09

47,52.48 46,13.12Total B

* Includes ` 7,91.60 crore as book adjustment of interest.

Medical and Public Health

Customs

Education,Sports,Art and Culture

Non-Ferrous Mining and Metallurgical Industires

Others

Police

Water Supply and Sanitation

Forestry and Wild Life

Urban Development

Other Administrative Services

Non-tax Revenue

Service Tax

Road Transport

Total A

Interest Receipts

Miscellaneous General services

Union Excise Duties

Major Irrigation

Land Revenue

Stamps and Registration fees

State Excise

Taxes on goods and passengers

Sales Tax

Share of net proceeds of Taxes

Corporation Tax

Other Taxes and Duties on Commodities and Services

Taxes on Wealth

3. STATEMENT OF RECEIPTS (CONSOLIDATED FUND)

Tax Revenue

Own Tax Revenue

ActualsDescription

I-TAX AND NON-TAX REVENUE

(` in crore)

Other Taxes on Income and Expenditure

Other Taxes and Duties on Commodities and Services

Taxes on Vehicles

Taxes and Duties on Electricity

Taxes on Income other than Corporation Tax

10

2015-16 2014-15

C

C.1 37,44.39 17,23.20

Grants under the proviso to

Article 275 (1) of the

Constitution

5,05.99 8,42.67

Grants towards contribution to

State Disaster Response Fund

2,03.43 2,55.41

Other Grants 30,34.97 6,25.12

C.2 Grants for State Plan Schemes 22,68.18 28,15.36

Block Grants 77.39 2,49.40

Grants under the proviso to

Article 275 (1) of the

Constitution

..

Grant for Central Road Fund 78.65 73.73

Other Grants 21,12.14 24,92.23

C.3 Grants for Central Plan

Schemes 27.53 24.57

C.4 Grants for Centrally

Sponsored Plan Schemes 3,38.66 4,39.75

63,78.76 50,02.88

Total Revenue

Receipts (A+B+C)4,75,56.55 4,07,98.66

3. STATEMENT OF RECEIPTS (CONSOLIDATED FUND)-contd.

ActualsDescription

(` in crore)

Total C

Grants

Non Plan Grants

II-GRANTS FROM GOVERNMENT OF INDIA

11

2015-16 2014-15

D.

29.98 18.74

29.98 18.74

E.

1,40,99.99 1,32,00.00

Ways and Means Advances

from the Reserve Bank of India

.. ..

1,73,00.00 ..

46,41.45 41,02.79

Special Securities issued to

National Small Savings Fund

17,21.40 12,51.31

1,38.36 1,73.89

3,79,01.20 1,87,27.99

F.

.. ..

97.23 1,30.76

.. ..

.. ..

.. ..

97.23 1,30.76

G.

3,28.28 2,72.82

8,59,13.24 5,99,48.97

Actuals

(` in crore)

Loans from Financial Institutions

1Details are in Statements No.7 in Volume I and 18 in Volume II

3. STATEMENT OF RECEIPTS (CONSOLIDATED FUND)-concld.

Total D

Description

Market Loans

Loans for Central Plan Schemes

Loans and advances by State Government

(Recoveries)1

Total Receipts in Consolidated Fund

(A+B+C+D+E+F+G)

Loans for Centrally Sponsored Plan Schemes

Disinvestment proceeds

Loans for State Plan Schemes

Other Loans

Public Debt Receipts

Internal Debt

Loans and Advances from Central Government

Non Plan Loans

Other Loans

Total E

Capital Receipts

Bonds

Total F

III CAPITAL, PUBLIC DEBT AND OTHER RECEIPTS

12

Revenue Capital Loans and

Advances

Total

A General Services

A.1 Organs of State

Parliament/State/Union Territory

Legislatures

52.22 .. .. 52.22

President, Vice President/Governor,

Administrator of Union Territories

12.27 .. .. 12.27

Council of Ministers 1,12.44 .. .. 1,12.44

Administration of Justice 5,10.09 .. .. 5,10.09

Election 55.64 .. .. 55.64

A.2 Fiscal Services

Land Revenue 1,61.13 .. .. 1,61.13

Stamps and Registration 15.37 .. .. 15.37

State excise 31.08 .. .. 31.08

Taxes on Sales, Trade etc. 1,28.50 .. .. 1,28.50

Taxes on Vehicles 18.72 .. .. 18.72

Other Taxes and Duties on Commodities and

Services

5.71 .. .. 5.71

Other Fiscal Services 0.81 .. .. 0.81

Appropriation for Reduction or Avoidance of

Debt

2,62.50 .. .. 2,62.50

Interest Payments 82,84.05 .. .. 82,84.05

A.3 Administrative Services

Public Service Commission 25.83 .. .. 25.83

Secretariat-General Services 1,15.57 .. .. 1,15.57

District Administration 1,58.03 .. .. 1,58.03

Treasury and Accounts Administration 54.08 .. .. 54.08

Police 27,36.31 2,27.65 .. 29,63.96

Jails 1,79.39 .. .. 1,79.39

Supplies and Disposals 2.37 .. .. 2.37

Stationery and Printing 21.60 0.45 .. 22.05

Public Works 2,24.49 2,32.46 .. 4,56.95

Other Administrative Services 1,02.72 .. .. 1,02.72

4. STATEMENT OF EXPENDITURE (CONSOLIDATED FUND)

A. EXPENDITURE BY FUNCTION

Description

(` in crore)

13

Revenue Capital Loans and

Advances

Total

A General Services- concld.

A.4 Pension and Miscellaneous General

ServicesPensions and Other Retirement Benefits 54,13.28 .. .. 54,13.28

Miscellaneous General Services 29.13 .. .. 29.13

Total A : General Services 1,87,13.33 4,60.56 .. 1,91,73.89

B Social Services

B.1 Education, Sports Art and Culture

General Education 92,93.78 1,53.34 .. 94,47.12

Technical Education 3,80.24 43.81 .. 4,24.05

Sports and Youth Services 2,31.47 5.01 .. 2,36.48

Art and Culture 11.04 .. .. 11.04

B.2 Health & Family Welfare

Medical and Public health 23,48.46 35.20 .. 23,83.66

Family Welfare 1,41.24 .. .. 1,41.24

B.3 Water Supply, Sanitation, Housing and

Urban Development

Water Supply and Sanitation 16,53.34 8,35.42 .. 24,88.76

Housing 25.65 80.03 .. 1,05.68

Urban Development 19,63.19 2,18.06 .. 21,81.25

B.4 Information and Broadcasting

Information and Publicity 1,05.17 .. .. 1,05.17

B.5 Welfare of Scheduled Caste, Scheduled

Tribes and other Backward Classes

Welfare of Scheduled Caste, Scheduled

Tribes and other Backward Classess

3,33.60 2.24 .. 3,35.84

B.6 Labour and Labour Welfare

Labour and Employment 3,06.50 .. .. 3,06.50

B.7 Social Welfare & Nutrition

Social Security and Welfare 40,94.91 57.45 .. 41,52.36

Nutrition 1,41.15 .. .. 1,41.15

Relief on account of Natural Calamities 5,00.50 ....

5,00.50

Description

(` in crore)

4. STATEMENT OF EXPENDITURE (CONSOLIDATED FUND)-contd .

A. EXPENDITURE BY FUNCTION

14

Revenue Capital Loans and

Advances

Total

B Social Services- concld.

B.8 Others

Other Social Services 2.27 1,09.43 .. 1,11.70

Secretariat- Social Services 6.35 .. .. 6.35

Total B : Social Services 2,15,38.86 15,39.99 .. 2,30,78.85

C Economic Services

C.1 Agriculture and Allied Activities

Crop Husbandry 6,50.08 .. 40.13 6,90.21

Soil & Water Conservation 52.72 .. .. 52.72

Animal Husbandry 5,26.50 9.59 .. 5,36.09

Dairy Development 0.72 .. .. 0.72

Fisheries 37.25 0.06 .. 37.31

Forestry and Wild Life 3,06.34 .. .. 3,06.34

Food Storage and Warehousing 1,20.47 3,03.56 .. 4,24.03

Agricultural Research and Education 3,20.52 .. .. 3,20.52

Co-operation 2,79.09 87.69 8.95 3,75.73

Other Agricultural Programmes 1.45 .. .. 1.45

C.2 Rural Development

Special Programmes for Rural Development 67.81 .. 0.58 68.39

Rural Employment 2,85.98 .. .. 2,85.98

Land Reforms 10.54 .. .. 10.54

Other Rural Development Programmes 14,86.34 .. 14,86.34

C.4 Irrigation and Flood Control

Major Irrigation 9,76.69 2,31.21 .. 12,07.90

Medium Irrigation 2,08.98 4,39.81 .. 6,48.79

Minor Irrigation 7.12 .. .. 7.12

Flood Control Project .. 2,05.19 .. 2,05.19

Command Area Development 2,12.59 .. .. 2,12.59

Description

4. STATEMENT OF EXPENDITURE (CONSOLIDATED FUND)-contd .

(` in crore)

A. EXPENDITURE BY FUNCTION

15

Revenue Capital Loans and

Advances

Total

C Economic Services- concld.

C.5 Energy

Power 1,02,15.89 15,97.50 1,22,66.83 2,40,80.22

Non-Concventional Sources of Energy 4.03 .. .. 4.03

New and Renewable Energy .. .. .. ..

C.6 Industry and Minerals

Village and Small Industries 30.93 .. 12.60 43.53

Telecommunication and Electronic

Industries

.. 0.01 .. 0.01

Industries 54.18 .. 6,46.00 7,00.18

Non-Ferrous Mining & metallurgical

Industries

9.67 .. .. 9.67

C.7 Transport

Civil Aviation 1.78 1.28 .. 3.06

Roads and Bridges 8,18.71 18,98.78 .. 27,17.49

Road Transport 17,74.69 1,11.14 .. 18,85.83

C.9 Science and Technology

Other Scientific Research 27.69 .. .. 27.69

Ecology and Envioronment 5.84 .. .. 5.84

C.10 General Economic Services

Secretariat- Economic Services 1,62.27 .. .. 1,62.27

Tourism 2.14 21.96 .. 24.10

Census Surveys and Statistics 16.98 .. .. 16.98

Civil Supplies 8.38 .. .. 8.38

Other General Economic Services 5.99 .. .. 5.99

Total C: Economic Services 1,86,90.36 49,07.78 1,29,75.09 3,65,73.23

D. Loans, Grants-in-aid and Contributions

Compensation and Assignments to Local

Bodies and Panchayati Raj Institutions

2,93.15 .. .. 2,93.15

Total D: Loans, Grants-in-aid and

Contributions2,93.15 .. .. 2,93.15

Description

(` in crore)

4. STATEMENT OF EXPENDITURE (CONSOLIDATED FUND)-contd .

A. EXPENDITURE BY FUNCTION

16

Revenue Capital Loans and

Advances

Total

E. Loans to Government Servants etc.

Loans to Government Servants etc. .. .. 2,75.20 2,75.20

F. Public Debt

Internal Debt of the State Government .. .. 70,38.54 70,38.54

Loans and Advances from the

Central Government .. .. 1,76.14 1,76.14

G. Inter State Settlement .. .. .. ..

H. Appropriation to Contingency Fund .. .. .. ..

Total Consolidated Fund Expenditure 5,92,35.70 69,08.33 2,04,64.97 8,66,09.00

Description

4. STATEMENT OF EXPENDITURE (CONSOLIDATED FUND)-contd .

(` in crore)

A. EXPENDITURE BY FUNCTION

17

Revenue Capital Total Revenue Capital Total Revenue Capital Total

Loans .. 2,04,64.97 2,04,64.97 .. 90,70.28 90,70.28 .. 88,52.87 88,52.87

Grant-in-Aid 1,07,65.97 .. 1,07,65.97 61,06.00 . 61,06.00 56,12.15 .. 56,12.15

Interest 89,05.42 2,07.76 91,13.18 75,03.20 2,29.88 77,33.08 63,74.80 3,86.36 67,61.16

Salaries 77,00.98 4,93.06 81,94.04 76,52.10 3,97.30 80,49.40 66,21.61 3,69.56 69,91.17

Pension 75,29.86 0.51 75,30.37 62,66.37 0.60 62,66.97 50,96.13 0.60 50,96.73

Advances 91.50 69,89.28 70,80.78 62.04 52,36.89 52,98.93 57.00 48,27.46 48,84.46

Subsidies 68,98.81 .. 68,98.81 56,93.34 . 56,93.34 56,81.12 .. 56,81.12

Dearness

Allowance64,88.79 .. 64,88.79 58,09.20 .. 58,09.20 45,71.98 .. 45,71.98

Major works 8.76 37,31.09 37,39.85 11.43 34,29.91 34,41.34 4.65 37,46.39 37,51.04

Other Charges 29,74.90 0.08 29,74.98 9,08.99 0.07 9,09.06 6,79.71 0.25 6,79.96

Investment 2,90.92 16,09.95 19,00.87 6,53.50 1,17.47 7,70.97 .. 1,47.86 1,47.86

Special Component

for SCs11,80.23 4,71.79 16,52.02 11,25.90 4,07.88 15,33.78 4,93.81 3,30.39 8,24.20

Energy Charges 10,69.51 .. 10,69.51 7,79.91 .. 7,79.91 7,49.06 .. 7,49.06

Maintenance 10,50.90 .. 10,50.90 10,19.24 .. 10,19.24 10,38.06 .. 10,38.06

Compensation 7,25.93 1,43.18 8,69.11 5,56.08 1,00.47 6,56.55 5,90.05 92.11 6,82.16

Gratuities 7,77.84 .. 7,77.84 6,85.99 .. 6,85.99 6,83.48 .. 6,83.48

Motor Vehicle 5,28.57 .. 5,28.57 6,29.15 .. 6,29.15 5,77.04 .. 5,77.04

Minor Works 3,64.77 1,24.11 4,88.88 3,18.26 136.14 4,54.40 2,79.42 1,36.45 4,15.87

Honorarium 4,79.54 .. 4,79.54 4,41.68 .. 4,41.68 3,47.51 .. 3,47.51

Leave Travel

Concession 3,42.42 .. 3,42.42 2,97.22 .. 2,97.22 1,13.06 .. 1,13.06

Scholarship and

Stipends3,37.77 .. 3,37.77 2,75.03 .. 2,75.03 2,68.82 .. 2,68.82

Ex-gratia 3,23.58 .. 3,23.58 2,84.83 .. 2,84.83 2,10.06 .. 2,10.06

Contributions 3,05.97 .. 3,05.97 5,25.86 .. 5,25.86 4,50.80 .. 4,50.80

Wages 2,69.06 .. 2,69.06 2,03.53 .. 2,03.53 1,40.14 .. 1,40.14

Material and

Supplies2,50.30 .. 2,50.30 2,81.03 .. 2,81.03 2,80.32 .. 2,80.32

Office Expenses 2,40.85 .. 2,40.85 2,67.37 87.88 3,55.25 1,90.63 85.80 2,76.43

Medical Re-

imbursement2,08.09 .. 2,08.09 1,82.17 .. 1,82.17 1,63.36 .. 1,63.36

Contractrual

Services2,04.20 .. 2,04.20 1,37.37 .. 1,37.37 1,20.03 .. 1,20.03

Rent Rates &

Taxes1,28.87 .. 1,28.87 1,20.93 .. 1,20.93 1,06.13 .. 1,06.13

Travel Expenses 1,12.42 .. 1,12.42 1,13.66 .. 1,13.66 1,20.66 .. 1,20.66

B. EXPENDITURE BY NATURE

(` in crore)

4. STATEMENT OF EXPENDITURE (CONSOLIDATED FUND)-contd.

2015-16 2014-15 2013-14Object of

Expenditure

18

Revenue Capital Total Revenue Capital Total Revenue Capital Total

Feeding 1,12.34 .. 1,12.34 1,07.56 .. 1,07.56 96.60 .. 96.60

Discretionary

grants1,06.05 .. 1,06.05 1,27.00 .. 1,27.00 85.10 .. 85.10

Lands 1.06 99.96 1,01.02 1.06 33.55 34.61 1.42 1,03.58 1,05.00

Machinery and

Equipment62.33 35.66 97.99 87.40 49.81 1,37.21 33.81 43.41 77.22

Petrol, Oil and

Lubricant74.67 .. 74.67 76.54 .. 76.54 1,02.53 .. 1,02.53

Computerisation 44.46 .. 44.46 32.29 .. 32.29 57.27 .. 57.27

Depreciation 42.89 .. 42.89 39.87 .. 39.87 33.94 .. 33.94

Profesional &

Special Services42.60 .. 42.60 25.31 .. 25.31 22.55 .. 22.55

Advertising and

Publicity41.95 .. 41.95 32.56 .. 32.56 36.68 .. 36.68

Unemployment

Allowance31.21 .. 31.21 34.77 .. 34.77 36.00 .. 36.00

Miscellaneous 26.04 .. 26.04 47.21 .. 47.21 19.73 .. 19.73

Purchases 2.75 22.07 24.82 3.92 1,36.70 1,40.62 2.40 1,44.14 1,46.54

Building 0.03 21.15 21.18 0.04 28.00 28.04 0.23 18.79 19.02

Commitment

charges18.99 .. 18.99 18.45 .. 18.45 .. .. ..

Election

Expenditure18.24 .. 18.24 .. .. .. .. .. ..

Research &

Development .. 16.79 16.79 .. 14.39 14.39 .. .. ..

Legal Fee .. .. .. 10.14 .. 10.14 .. .. ..

Others 42.12 1.90 44.02 41.04 2.55 43.59 (-)1,82.04 (-)3.09 (-)1,85.13

Suspense (-) 1,77.50 0.21 (-) 1,77.29 (-) 1,88.19 (-) 0.54 (-) 1,88.73 .. .. ..

Deduct Recoveries 18,11.26 70,60.22 88,71.48 2,90.48 66,93.42 69,83.90 80.71 64,95.46 65,76.17

Total 5,92,35.70 2,73,73.30 8,66,09.00 4,91,17.87 1,27,85.81 6,19,03.68 4,18,87.10 1,27,87.47 5,46,74.57

(` in crore)

2015-16 2014-15

B. EXPENDITURE BY NATURE

2013-14Object of

Expenditure

4. STATEMENT OF EXPENDITURE (CONSOLIDATED FUND)-concld .

19

Major

Head Description

Expenditure

during

2014-15

Progressive

expenditure

upto 2014-15

Expenditure

during

2015-16

Progressive

expenditure

upto 2015-16

Percentage

Increase (+)/

Decrease (-)

A. CAPITAL ACCOUNTS OF GENERAL SERVICES-

4055 Capital Outlay on Police 1,20.16 8,94.27 2,27.65 11,21.92 89.46

4058 Capital Outlay on Stationery and Printing .. 8.96 0.45 9.41 100.00

4059 Capital Outlay on Public Works 1,70.54 15,35.32 2,32.46 17,67.78 36.31

Total-A. Capital Account of General Services 2,90.70 24,38.55 4,60.56 28,99.11 58.43

B. CAPITAL ACCOUNT OF SOCIAL SERVICES-

(a)

4202 Capital Outlay on Education, Sports, Art and

Culture

1,86.07 11,64.66 2,02.16 13,66.82 8.65

Total- (a) Capital Account of Education, Sports,

Art and Culture1,86.07 11,64.66 2,02.16 13,66.82 8.65

(b) Capital Account of Health and Family Welfare-

4210 Capital Outlay on Medical and Public Health 64.87 5,64.79 35.20 5,99.99 (-) 45.74

4211 Capital Outlay on Family Welfare .. 40.81 .. 40.81 ..

Total- (b) Capital Account of Health and Family

Welfare64.87 6,05.60 35.20 6,40.80 (-) 45.74

(c) Capital Account of Water,Supply,

Sanitation,Housing and Urban Development

4215 Capital Outlay on Water Supply and Sanitation 9,59.96 92,41.78 8,35.42 1,00,77.20 (-) 12.97

4216 Capital Outlay on Housing 30.51 3,33.67 80.03 4,13.70 162.31

4217 Capital Outlay on Urban Development 4,27.77 18,36.78 2,18.06 20,54.84 (-) 49.02

Total-(c) Capital Account of Water Supply,

Sanitation, Housing and Urban Development 14,18.24 1,14,12.23 11,33.51 1,25,45.74 (-) 20.08

5. STATEMENT OF PROGRESSIVE CAPITAL EXPENDITURE

(` in crore)

Capital Account of Education, Sports, Art and Culture-

20

Major

Head Description

Expenditure

during

2014-15

Progressive

expenditure

upto 2014-15

Expenditure

during

2015-16

Progressive

expenditure

upto 2015-16

Percentage

Increase (+)/

Decrease (-)

B. Capital Account of Social Services-concld.

(d) Capital Account of information and Broadcasting-

4220 Capital Outlay on Information and Publicity .. 1.15 .. 1.15 ..

Total-(d) Capital Account of Information and

Broadcasting

.. 1.15 .. 1.15 ..

(e) Capital Account of Welfare of Scheduled Castes,

Scheduled Tribes and other Backward Classes-

4225 Capital Outlay on Welfare of Scheduled Castes,

Scheduled Tribes and other Backward Classes

1.25 51.04 2.24 53.28 79.20

Total-(e) Capital Account of Welfare of

Scheduled Castes,Scheduled Tribes and other

Backward Classes

1.25 51.04 2.24 53.28 79.20

(g) Capital Account of Social Welfare and Nutrition-

4235 Capital Outlay on Social Security and Welfare 56.84 2,38.40 57.45 2,95.85 1.07

Total-(g) Capital Account of Social Welfare and

Nutrition56.84 2,38.40 57.45 2,95.85 1.07

(h) Capital Account of Other Social Services-

4250 Capital Outlay on other Social Services 1,70.29 7,60.59 1,09.43 8,69.57(a) (-) 35.74

Total-(h) Capital Account of Other Social

Services1,70.29 7,60.59 1,09.43 8,69.57(a) (-) 35.74

Total-B. Capital Account of Social Services 18,97.56 1,42,33.67 15,39.99 1,57,73.21(a) (-) 18.84

(a) Decreased proforma by ` 0.45 crore from the closing balance due to retirement of capital/disinvestment.

5. STATEMENT OF PROGRESSIVE CAPITAL EXPENDITURE-contd.

(` in crore)

21

Major

Head Description

Expenditure

during

2014-15

Progressive

expenditure

upto 2014-15

Expenditure

during

2015-16

Progressive

expenditure

upto 2015-16

Percentage

Increase (+)/

Decrease (-)

C. CAPITAL ACCOUNT OF ECONOMIC SERVICES-

(a) Capital Account of Agriculture and Allied Activities-

4401 Capital Outlay on Crop Husbandry .. 1.62 .. 1.62 ..

4402 Capital Outlay on Soil and Water Conservation .. 1.37 .. 1.37 ..

4403 Capital Outlay on Animal Husbandry 4.50 10.19 9.59 19.78 113.11

4404 Capital Outlay on Dairy Development .. 18.55 .. 18.55 ..

4405 Capital Outlay on Fisheries .. 3.42 0.06 3.48 100.00

4406 Capital Outlay on Forestry and Wild Life .. 1.57 .. 1.57 ..

4408 Capital Outlay on Food Storage and Warehousing (-)11,21.43 18,70.13 3,03.56 21,73.69 127.07

4416 Investments in Agricultural Financial Institutions .. 0.53 .. 0.53 ..

4425 Capital Outlay on Co-operation 63.89 3,23.88 87.69 3,82.05(a) 37.25

4435 Capital Outlay on Other Agricultural Programmes .. (-)2.08 .. (-) 2.08 ..

Total- (a) Capital Account of Agricultre and

Allied Activities(-)10,53.04 22,29.18 4,00.90 26,00.56(a) 138.07

(d) Capital Account of Irrigation and Flood Control-

4700 Capital Outlay on Major Irrigation 2,21.59 46,23.93 2,31.21 48,55.14 4.34

4701 Capital Outlay on Medium Irrigation 5,22.22 54,33.54 4,39.81 58,73.35 (-) 15.78

4702 Capital Outlay on Minor Irrigation .. 5,50.71 .. 5,50.71 ..

4711 Capital Outlay on Flood Conrtol Projects 2,21.52 15,33.19 2,05.19 17,38.38 (-) 7.37

Total-(d) Capital Account of Irrigation and Flood

Control9,65.33 1,21,41.37 8,76.21 1,30,17.58 (-) 9.23

(a) Decreased proforma by ` 29.52 crore from the closing balance due to retirement of capital/disinvestment.

5. STATEMENT OF PROGRESSIVE CAPITAL EXPENDITURE-contd.

(` in crore)

22

Major

Head Description

Expenditure

during

2014-15

Progressive

expenditure

upto 2014-15

Expenditure

during

2015-16

Progressive

expenditure

upto 2015-16

Percentage

Increase (+)/

Decrease (-)

C. CAPITAL ACCOUNT OF ECONOMIC SERVICES-contd.

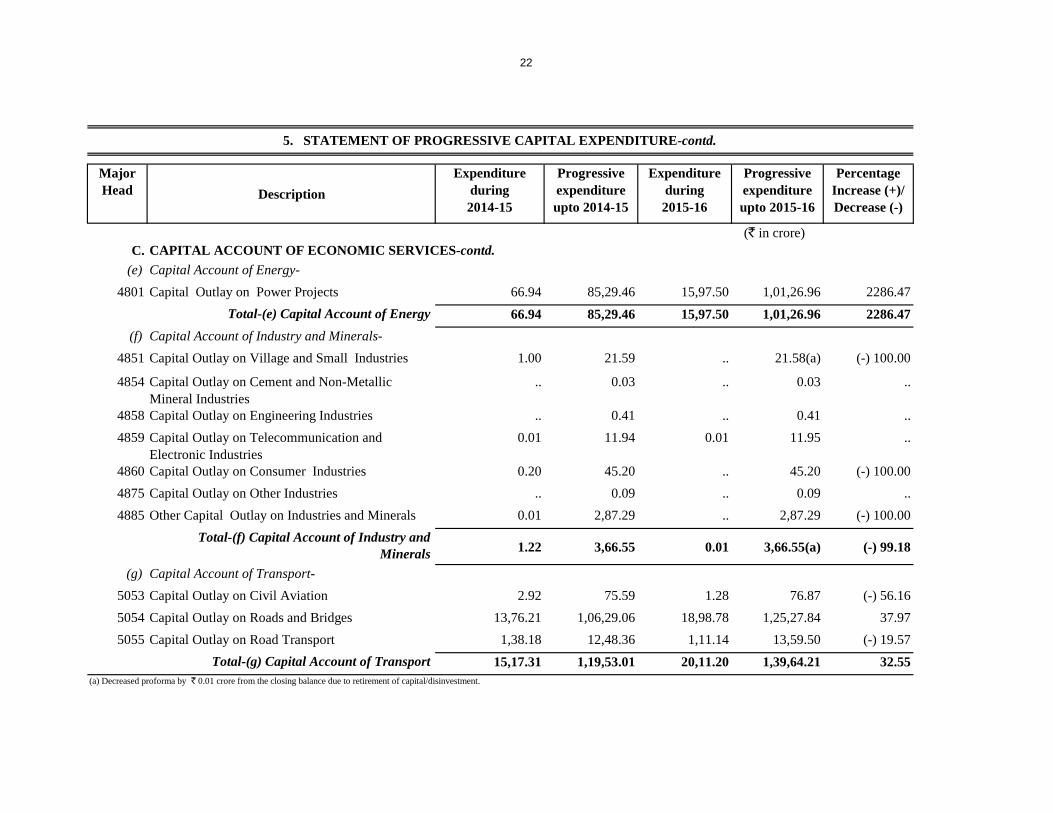

(e) Capital Account of Energy-

4801 Capital Outlay on Power Projects 66.94 85,29.46 15,97.50 1,01,26.96 2286.47

Total-(e) Capital Account of Energy 66.94 85,29.46 15,97.50 1,01,26.96 2286.47

(f) Capital Account of Industry and Minerals-

4851 Capital Outlay on Village and Small Industries 1.00 21.59 .. 21.58(a) (-) 100.00

4854 Capital Outlay on Cement and Non-Metallic

Mineral Industries

.. 0.03 .. 0.03 ..

4858 Capital Outlay on Engineering Industries .. 0.41 .. 0.41 ..

4859 Capital Outlay on Telecommunication and

Electronic Industries

0.01 11.94 0.01 11.95 ..

4860 Capital Outlay on Consumer Industries 0.20 45.20 .. 45.20 (-) 100.00

4875 Capital Outlay on Other Industries .. 0.09 .. 0.09 ..

4885 Other Capital Outlay on Industries and Minerals 0.01 2,87.29 .. 2,87.29 (-) 100.00

Total-(f) Capital Account of Industry and

Minerals1.22 3,66.55 0.01 3,66.55(a) (-) 99.18

(g) Capital Account of Transport-

5053 Capital Outlay on Civil Aviation 2.92 75.59 1.28 76.87 (-) 56.16

5054 Capital Outlay on Roads and Bridges 13,76.21 1,06,29.06 18,98.78 1,25,27.84 37.97

5055 Capital Outlay on Road Transport 1,38.18 12,48.36 1,11.14 13,59.50 (-) 19.57

Total-(g) Capital Account of Transport 15,17.31 1,19,53.01 20,11.20 1,39,64.21 32.55

(a) Decreased proforma by ` 0.01 crore from the closing balance due to retirement of capital/disinvestment.

5. STATEMENT OF PROGRESSIVE CAPITAL EXPENDITURE-contd.

(` in crore)

23

Major

Head Description

Expenditure

during

2014-15

Progressive

expenditure

upto 2014-15

Expenditure

during

2015-16

Progressive

expenditure

upto 2015-16

Percentage

Increase (+)/

Decrease (-)

C. CAPITAL ACCOUNT OF ECONOMIC SERVICES-concld.

(j) Capital Account of General Economic Services-

5452 Capital Outlay on Tourism 29.51 2,53.89 21.96 2,75.85 (-) 25.58

Total-(j) Capital Account of General Economic

Services29.51 2,53.89 21.96 2,75.85 (-) 25.58

15,27.27 3,54,73.46 49,07.78 4,03,51.71(a) 221.34

Grand Total 37,15.53 5,21,45.68 69,08.33 5,90,24.03(b) 85.93

(a) Decreased proforma by ` 29.53 crore from the closing balance due to retirement of capital/disinvestment.

(` in crore)

(b) Decreased proforma by ` 29.98 crore from the closing balance due to retirement of capital/disinvestment.

Total-C. Capital Account of Economic Services

5. STATEMENT OF PROGRESSIVE CAPITAL EXPENDITURE-contd.

24

Sr.

No.

Undertaking/Scheme Major Head under which

working expenses are

accounted for

Year of

Account

Capital

employed

Profit(+)

or Loss(-)

Percentage of

profit or loss

in relation to

capital employed

1 Printing and Stationery Department

Nationalised Text Book Scheme

4058 -Capital Outlay on

Stationery and Printing

2007-08 17.97 (+) 1.74 (+) 9.68

2 Agriculture Department-

(i) Seed Depot Scheme 4401- Capital outlay on

Crop Husbandry

1988-89 ..(a) (-)0.01 ..(a)

(ii) Purchase and Distribution of

pesticides

4401- Capital outlay on

Crop Husbandry

1986-87 0.82 (+)0.13 (+)15.85

5. STATEMENT OF PROGRESSIVE CAPITAL EXPENDITURE-contd.

In 2015-16, the Government invested ` 19,02.20 crore, in Government Companies (` 18,13.64 crore) and Co-operative Institutions ( ` 88.56 crore).

Further out of investments in Co-operative Institutions ` 29.98 crore retired during the year.

1. The details of Government investments in the shares of Statutory Corporations, Government companies, Joint Stock Companies and Co-operative

Institutions are given in Statement No. 19.

Explanatory Notes

The total investments of the Government in the share capital of different concerns at the end of 2013-14, 2014-15 and 2015-16 were ` 73,78.87

crore, ` 75,00.22 crore and ` 93,72.44 crore respectively. The dividend received thereon during the three years was ` 6.49 crore (0.09 per cent ),

`5.80 crore (0.08 per cent ) and `15.89 crore (0.17 per cent ) crore respectively . Further details are given in Statement No. 19.

2. The Financial results of the irrigation works, for which capital and revenue accounts are kept, are given in Appendix. VIII.

(a) Information has not been received from the department (August, 2016).

3. The details of incomplete projects in the form of statement of commitments are given in Appendix-IX.

4. The proforma accounts for 2015-16 for five departmentally managed government commercial and quasi-commercial undertakings, the net

expenditure which is shown in the table below have not been prepared (August, 2016).

Summary of the financial results of the working of these departmentally managed Government undertakings as disclosed by the latest available

proforma acounts is given below:-

( ` in crore )

25

Sr.

No.

Undertaking/Scheme Major Head under which

working expenses are

accounted for

Year of

Account

Capital

employed

Profit(+)

or Loss(-)

Percentage of

profit or loss

in relation to

capital employed

3 Food and Supplies Department-

Grain Supply Scheme

4408 -Capital Outlay on

Food Storage and

Warehousing

2013-14 63,32.83 (+)1,61.74 (+)2.55

4 Transport Department- Haryana

Roadways

5055 -Capital Outlay on

Road Transport

2010-11 7,74.86 (-)2,95.54 (-) 38.14

Explanatory Notes

( ` in crore )

5. STATEMENT OF PROGRESSIVE CAPITAL EXPENDITURE-concld.

26

Nature of Borrowings Balance as on

1 April 2015

Receipts during

the year

Repayments

during the year

Balance as on

31 March 2016

As per cent

of Public

debt & other

liabilities

Amount Per cent

6003 Internal Debt of the State

Government

Market Loans 5,26,52.83 1,40,99.99 9,31.70 6,58,21.12 1,31,68.29 25.01 54.52

Ways and Means Advances from

the RBI

.. .. .. .. .. .. ..

Bonds 2,02.23 1,73,00.00 2,02.23 1,73,00.00 1,70,97.77 8454.62 14.33

Loans from Financial Institutions 22,90.95 46,41.45 48,16.03 21,16.37 (-)1,74.58 (-)7.62 1.75

Special Securities issued to

National Small Savings Fund

1,22,39.17 17,21.40 7,09.29 1,32,51.28 10,12.11 8.27 10.98

Other Loans 14,12.29 1,38.36 3,79.29 11,71.36 (-)2,40.93 (-)17.06 0.97

Total - 6003 Internal Debt of the

State Government 6,87,97.47 3,79,01.20 70,38.54 9,96,60.13 3,08,62.66 44.86 82.55

6004 Loans and Advances from

the Central Government 21,27.83 97.23 1,76.14 20,48.92 (-)78.91 (-)3.71 1.70

A Total Public Debt 7,09,25.30 3,79,98.43 72,14.68 10,17,09.05 3,07,83.75 43.40 84.25

[1] Detailed Account is in Statement No. 17 and Statement No. 21.

6. STATEMENT OF BORROWINGS AND OTHER LIABILITIES

Net Increase (+) /

Decrease(-)

A Public Debt

(` in crore)

(1) Statement of Public Debt and Other Liabilities [1]

27

Nature of Borrowings Balance as on

1 April 2015

Receipts during

the year

Repayments

during the year

Balance as on

31 March 2016

As per cent

of Public

debt & other

liabilities

Amount Per cent

State Provident Fund 1,11,50.63 29,33.34 18,88.86 1,21,95.11 10,44.48 9.37 10.10

Insurance and Pension Fund 7.05 34.65 30.49 11.21 4.16 59.01 0.01

Reserve Funds bearing Interest 3,00.98 75.98 19.75 3,57.21 56.23 18.68 0.30

Reserve Funds not bearing Interest 15.79 14.49 .. 30.28 14.49 91.77 0.03

Deposits bearing Interest 13.11 9,47.15 5,96.49 3,63.77 3,50.66 2674.75 0.30

Deposits not bearing Interest 60,33.22 1,66,47.25 1,66,28.63 60,51.84 18.62 0.31 5.01

Total other liabilities 1,75,20.78 2,06,52.86 1,91,64.22 1,90,09.42 14,88.64 8.50 15.75

B Total Public Debt and other

liabilities 8,84,46.08 5,86,51.29 2,63,78.90 12,07,18.47 3,22,72.39 36.49 100.00

[1] Detailed Account is in Statement No. 17 and Statement No. 21.

B Other liabilities

(` in crore)

6. STATEMENT OF BORROWINGS AND OTHER LIABILITIES-contd.

Net Increase (+) /

Decrease(-)

(1) Statement of Public Debt and Other Liabilities [1]

28

1 Amortisation arrangements

Balance on Additions Withdrawals Balance on

1 April 2015 during the year during the year 31 March 2016

1 0.22 .. .. 0.22

2 1.91 .. .. 1.91

3 11,51.17 3,65.76 .. 15,16.93

Total 11,53.30 3,65.76 .. 15,19.06

2.

Loans received for Bhakra

Nangal Project by the Composite

State of Punjab

Loans received out of consolidated

6. STATEMENT OF BORROWINGS AND OTHER LIABILITIES-contd.

Explanatory Notes

The State Government has made amortisation arrangements for the repayement of the following loans :-

(` in crore)

Name of Sinking FundSr.

No.

Loans from Small Saving Fund – Loans out of the collection in the ‘Small Savings Schemes’ and ‘Public Provident Fund’ in the Post offices are

being shared between the State Government and the Central Government in the ratio of 3:1. A separate fund viz. ‘National Small Savings Fund’

was created in 1999-2000 for the purpose of release of loans out of Small Savings collections. The loans received during 2015-16 amounted to

` 17,21.40 crore and ` 7,09.29 crore was repaid during the year. The balance outstanding at the end of the year was ` 1,32,51.28 crore which was

10.98 per cent of the total Public Debt and other liabilities of the State Government as on 31 March 2016.

Amortisation of Market Loans

open market borrowings of the

Out of total balances of ` 15,19.06 crore in the Sinking funds, ` 15,16.93 crore were invested in Securities of the Government of India.

Government of India

A large chunk of small savings collected from the States is given back to the State Governments as loans against which they are required to issue special 2. Loans and Advances from the Central Government- Details of the loans and advances taken from the Government of India are given in Statement No. 17. Rehabiliation Loans- On re-organisation of the Punjab State the outstanding amount of loans (Rs. 1.09 crores) which awaited write off by the Government of India was allocated

In addition to the above, the balances at the credit of earmarked and other Funds, as also certain deposits to the extent to which they have not invested, but are merged with

Under Section 54(1) of Punjab Re-organisation Act, the Public Debt of the composite State of Punjab attributable to loans raised by issue of Government

29

3. Internal Debt of the State Government-

Amount met from revenue during 2014-15 and 2015-16 as interest charges are shown below :-

2015-16 2014-15 Net increase(+)

or decrease(-)

Gross debt and other obligations at the end of the year 12,07,18.47 8,84,46.08 3,22,72.39

(i) Interest paid by the Government -

(a) On Public Debt and Small Savings, Provident Funds 75,12.62 68,99.22 6,13.40

(b) On other obligations 7,71.43 29.05 7,42.38

Total 82,84.05 69,28.27 13,55.78

(ii) Deduct

Interest received on loans and advances given by the Govt. 46.69 39.83 6.86

Interest realised on investment of cash balances 1,86.49 79.70 1,06.79

(iii) Net amount of interest charges 80,50.87 68,08.74 12,42.13

Ten Market loans of ` 1,41,00.00 crore (` 25,00.00 crore carrying 8.51 per cent interest, ` 11,00.00 crore carrying 8.38 per cent redeemable in the

year 2026, and ` 10,00.00 crore carrying 8.23 per cent , ` 10,00.00 crore carrying 8.29 per cent , ` 10,00.00 crore carrying 8.16 per cent

`9,00.00 crore carrying 8.30 per cent , 10,00.00 crore carrying 8.29 per cent ` 10,00.00 crore carrying 8.22 per cent ` 17,00.00 crore carrying

8.15 per cent , ` 29,00.00 crore carrying 8.27 per cent redeemable in the year 2025 ) were raised by the Government during the year. The whole

amount was realised in cash.The total payment against the matured loan during the period from 1967-68 to 2015-16 was ` 56,42.47 crore. The

outstanding liability against matured loan was ` 2.28 crore.

The particulars of outstanding market loans are given in Annexure to Statement No. 17. The loans from the Reserve Bank of India represent

adjustment relating to the short fall from the agreed minimum cash balance and borrowing purely of temporary character, viz; ordinary and special

ways and means advances and overdraft from the Bank. The particulars of the transactions are given in the explanatory notes below Annexure to

Statement No. 2.

Loans and Advances from the Central Government- Details of the loans and advances taken from the Government of India are given in Statement

No. 17.

( ` in crore)

6. STATEMENT OF BORROWINGS AND OTHER LIABILITIES-contd.

The transactions relating to loans raised in the open market, the loans received from the Reserve Bank of India, the Life Insurance Corporation of

India, the National Bank for Agriculture and Rural Development, the National Co-operative Development Corporation, General Insurance

Corporation of India etc. are recorded under this head.

In addition to the above, the balances at the credit of earmarked and other Funds, as also certain deposits to the extent to which they have not invested, but are merged with

30

2015-16 2014-15 Net increase(+)

or decrease(-)

(iv) Percentage of Gross interest item (i) to total revenue receipts 17.42 16.98 0.44

(v) Percentage of Net interest item (iii) to total revenue receipts 16.93 16.69 0.24

(B) Appropriation for reduction or avoidance of debt

(i) Contribution to Saving Funds 2,62.50 .. 2,62.50

(ii) Other appropriation .. .. ..

In addition, there were adjusment of interest charges of ` 8,29.16 crore on account of interest received from departmental commercial

undertakings and ` 25.14 crore on account of premium on market loans.

The Government also received during the year ` 15.89 crore as dividend on investments in Public Sector Undertakings and other investments.

6. STATEMENT OF BORROWINGS AND OTHER LIABILITIES-concld.

( ` in crore)

31

Loanee Group Balance on

1 April

2015

Disbursements

during the year

Repayments

during the

year

Written-off of

irrecoverable

Loans and

Advances

Balance on

31 March

2016

Net increase/

decrease

during the year

(2-6)

Interest

payment in

arrears

1 2 3 4 5 6 7 8

(` in crore)