Jaarrekening 2013 Land Aruba (10 juni 2014) (Annual Accounts Government of Aruba)

Two Steps AheadTourism Policy 2012

Minister of Tourism, Transportation and Labour

Government of Aruba

Two Steps AheadTourism Policy 2012

Two Steps Ahead Tourism Policy 2012

5

Preface Aruba has a successful history of tourism, not by chance but by design. The decision to establish tourism as an industry in the 1950’s was a strategic choice as was the renewed com-mitment in 1986 to establish tourism as the main economic activity of the island. Notwithstanding its volatility, competitive nature and dyna-mism, tourism has remained the pillar of our economy and there is no reason to believe it will change in the near future. As our most important economic activity, success in tour-ism is measured by key economic indicators. Our goal is to increase the economic benefits for the island through suc-cessful destination marketing and by contributing to an en-riching island experience. In this policy you will see the results up to June of this year for comparison purposes. However the July and August stay-over arrival numbers, room occupancy, ADR and RevPAR have continued to grow positively. Year to date August, RevPAR was up with 9.3%, ADR was up by 5.9%, room occupancy increased with 2.4% and tourism arrivals increased with 6.6 %.

Two Steps AheadTo fortify our competitiveness in the international market, we have to remain two steps ahead. Five fundamentals were taken care of: The tourism taxation was increased; systems were put in place to provide funds to the Aruba Tourism Au-thority (ATA) for marketing and to provide funds to improve the destination experience through the Tourism Product En-hancement Fund (TPEF); the ATA acquired a unique inde-pendent legal status within the public sphere; and public/pri-vate sector Boards were established to stimulate a national approach to tourism. We’ve established marketing objectives and strategies to meet the desirable goals. However, tourism as an industry is more competitive than ever: increasingly countries have turned to tourism as an economic activity and are investing more in marketing and in product improvement and inno-vation. Additionally, the internet and social media have in-creased the dynamism of the tourism industry tremendously. As a result of the economic times we live in, airlines continue to refine and change their strategies and as they play a cru-cial role in our success, we are working diligently to maintain current and open new gateways, and as part of our diversifi-cation policy we will continue to pursue additional airlift from

potential markets.To ensure we continue to make solid and strategic deci-sions, a lot of research and analysis has been conducted during the past year. We have listened to our potential con-sumers and we have consulted with a large amount of local and international stakeholders, ensuring a wide participa-tion and view of the tourism industry. The results and plans including innovative ideas on target market strategies to identify and profile the most appropriate and lucrative mar-ket segments, their behavior and preferences, are some of the information that will be presented in the new Strategic Plan for the Development of Tourism in December of 2011. We will be equipped with added tools to continue to make sound decisions and policies to remain two steps ahead for the next decade.

Un Aruba dushi pa biba ta un Aruba dushi pa bishita Tourism is experiential, experimental and existential. Our success in tourism depends a great deal on the total experi-ence that our visitors have on island. Our high percentage of repeat visitors is a living testimony of the experience they have on island. In my policy plan I have accentuated pro-grams that enrich our visitor’s experience while also benefit-ting our local community. The Linear Park will have biking and jogging paths, plazas, improved beaches and plenty of spaces for recreation and relaxation. The Aruba Certifica-tion Program will help increase the knowledge of our labour force; local entrepreneurs will have additional outlets for sale of local products; the island is cleaner, and increased se-curity has been provided in certain areas. There are several programs and projects in place or in the pipeline to enrich the visitor’s cultural experience. Beaches and beach facilities will receive great attention. While tourism has the largest positive economic impact on our economy, it also has an increasing impact on all our re-sources. The programs funded by the TPEF attempt to con-tribute to a more sustainable development in the areas of the environment, cultural heritage, security, natural attractions, hospitality and services and research. Soon, the results of a study assessing the baseline of our sustainable develop-ment will provide us with crucial information allowing us to shape strategic direction on policies moving forward.Tourism will remain our most important economic activity for now so with innovation and intelligence, we have to work towards a sustainable tourism development that ensures economic stability and growth, and a “one happy island” for all of us.

Minister of Tourism, Transportation and LabourOtmar E. Oduber, B.Sc.

Two Steps Ahead Tourism Policy 2012

6

Table of contents

1. Economic Importance of Tourism

2. Aruba Tourism Industry Performance

3. Tourism Policy

3.1. Objectives 2012

3.2. Product

3.2.1. Tourism Product Enhancement Fund

3.2.2. Accommodations

3.2.3. San Nicolas

3.3. Marketing

3.4. Air Service

3.5. Cruise

4. Aruba Tourism Authority Sui Generis

5. Aruba Airport Authority

6. Achievements

6.1. Linear Park

6.2. Aruba Certification Program

7. Public / Private Partnership

8. Future Outlook: Strategic Plan for the Development of Tourism in Aruba

9. Statistics

Two Steps Ahead Tourism Policy 2012

7

Global Performance*Tourism is one of the world’s largest and fastest growing economic sectors, emerging over the past fifty years as a key instrument for global growth, development and job cre-ation. Global tourism has grown from 25 million arrivals in 1950 to 919 million in 2008, a decrease to 877 million in 2009 and a recovery to 935 million in 2010. Global tour-ism receipts has risen from US$2.1 billion in the 1950’s to US$941 billion in 2008 with a decrease in 2009 to US$852 billion. Global tourism receipts showed a recovery in 2010 to US$919 billion.In real terms (adjusted for exchange rate fluctuations and inflation) international tourism receipts increased by 5% as compared to an almost 7% growth in arrivals, showing the close relation between both indicators and confirming that in recovery years, arrivals tend to pick up faster than receipts.Globally, tourism has become one of the major international trade categories. As an export category, tourism ranks fourth after fuels, chemicals and automotive products. For many developing countries it is one of the main income sources and the number one export category, creating much needed employment and opportunities for development and becom-ing a key “invisible” earner. Globally, in 2011 travel and tourism contributes directly with 3.4% of total employment and directly/indirectly with 8.8%. Global travel and tourism direct contribution to the GDP is forecasted to be US$1,850 billion in 2011, out of US$ 5,992

billion total direct/indirect contribution of travel and tourism to the GDP. The direct contribution for travel and tourism industry represents 2.8% of total global GDP and the total direct/indirect contribution of this industry will be 9.1% of total global GDP. *Source: UNWTO and WTTC

Caribbean Tourism Industry Performance* The Caribbean arrivals in 2008 were 19.7 million with a de-crease to 19.5 million in 2009. Caribbean arrivals showed a 3.9% growth to 20.3 million in 2010. The Caribbean tourism receipt also suffered a decline going from US$23.5 billion in 2008 to a decreased US$22.6 billion in 2009 and an in-crease of 4.4% to US$23.6 billion in 2010. The cruise visitor arrivals to the Caribbean grew with 6% from 2009 to 2010, respectively 19 million and 23 million.The Caribbean travel and tourism direct contribution to the GDP is expected to be US$ 15.8 billion, which is 4.6% of total Caribbean GDP. The total direct/indirect contribution of the tourism and travel to GDP is forecasted to be US$ 48.6 billion, representing 14.2% of the Caribbean GDP. Travel and tourism contributes directly with 4% of total em-ployment in 2011 and direct/indirectly with 12.6% of total employment in the Caribbean.The Caribbean average daily rate and revenue per available room declined with double digit numbers in 2009.

1. Economic Importance of Tourism

Two Steps Ahead Tourism Policy 2012

8

Caribbean hotel performance 2008-2010

2008 200908/09/

variation in %

201009/10

variationin %

Average occupancy rate of resorts (in percent) 64.8 60.7 -6% 61.1 0.7%

Average daily rate of resorts (in US$) 178.81 156.62 -12% 161.41 3.1%

Revenue per available room (in US$) 115.87 95.03 -18% 98.66 3.8%

Source: SmithStar Research

The Caribbean recovered slightly in 2010 from the econom-ic recession in 2009 in arrival numbers and in hotel perfor-mance. The occupancy grew slightly with 0.7%, and the av-erage daily rate and the revenue per available room showed an increase of 3.1% and 3.8%, lagging somewhat behind the growth in arrivals (see Table 1.1). *Source: WTO and WTTC

For the first six months of 2011, the hotel occupancy for the Caribbean showed an improvement over 2010 of 4.9%. The average daily rate showed a slight increase of 1% and the revenue per available room showed a significant growth of 6.1% for the first six months of 2011 (see Table 1.2).

Table 1.1

Table 1.2

Caribbean hotel performance YTD June 2011

2010 2011 variation in %

Average occupancy rate of resorts (in percent) 64.7 67.9 4.9%

Average daily rate of resorts (in US$) 175.72 177.56 1.0%

Revenue per available room (in US$) 113.75 120.65 6.1%

Source: SmithStar Research

Two Steps Ahead Tourism Policy 2012

9

The tourism industry has been Aruba’s main economic pillar and generator of employment for the past decades. According to the World Tourism Travel Council (WTTC), tour-ism’s expected direct contribution to employment in Aruba for 2011 is 26.2% of total (compared to 4% Caribbean and 3.4% global) and the direct/indirect contribution is 75.5% of total (compared to 12.6% Caribbean and 8.8% global). For travel and tourism’s direct contribution to employment, Aruba ranks #4 in the world and for its contribution to direct and indirect employment, Aruba ranks #2 in the world. The aforementioned figures accentuate the critical role that tour-ism plays within the overall economy of the island.For 2010 the estimated direct contribution of tourism to the GDP was 51.4%.The 2010 figures in Table 2.1 show a recovery in tourism’s contribution to Aruba’s foreign exchange earnings, Afl. 2,212 million in tourism receipts, an increase of 2.2% over 2009. Stay-over visitor arrivals showed an increase of 1.6%, from 812.600 to 825.500 visitor arrivals. Visitor nights, another important indicator, increased with 4.8% from 2009 to 2010, surpassing 2008 levels.In 2010, the tourism cruise passengers declined by 6.2%. The return of Carnival Cruise Line in November and Decem-ber contributed to 8496 extra visitors softening the decline for 2010. The occupancy rate and revenue per available room for the AHATA hotels indicated a growth for 2010. The AHATA ho-tels saw an increase of 2.4% in average occupancy rate,

the average daily rate was flat and the revenue per available room grew with 3%. The Timeshare resorts performance in 2010 showed a growth of 4.3% in average occupancy rate.Due to a strong contraction in stay-over visitor arrivals in the Caribbean compared to Aruba in 2009 and a larger growth differential for the Caribbean in 2010, there is a decrease in market share for Aruba in the Caribbean in 2010. The Aruba market share for cruise tourism in the Caribbean in 2010 suffered a decrease due to fewer calls and smaller ships to Aruba. (see table 2.1)

Main indicators of tourism activity YTD June 2011Table 2.2 indicates that the first quarter of 2011 recorded a notable increase of 6% over 2010 in tourism receipts, from Afl. 638.3 million to Afl. 676.8 million showing increased consumer confidence.The first six months of 2011 show signs of considerable im-provement over 2010. A noticeable growth of 6% in stay-over visitor arrivals and 10.7% for cruise visitor arrivals was achieved. The AHATA hotel performance showed an aver-age room occupancy rate of 77.9% in the first six months, an increase of 2.4%. The Timeshare resorts showed an aver-age occupancy rate increase of 1.7% in the first six months. The average daily rate was up by 5.9% from Afl.357.21 to Afl.378.21 and the revenue per available room grew with 8.4% from Afl.271.76 to Afl.294.63. The investment in mar-keting the destination, the diversification policy and the airlift

2. Aruba Tourism Industry Performance

Two Steps Ahead Tourism Policy 2012

10

strategy showed its results in addition to increased consum-er confidence. (see table 2.2)

Occupancy Aruba hotels compared to the CaribbeanIn the first six months of 2010 and 2011 as illustrated in Figure 2.1, Aruba performed better in hotel occupancy than the Caribbean. The Caribbean showed an average of 65% in 2010, and 68% in 2011. Aruba’s average occupancy rate of AHATA hotels for 2010 was 76%, 11% higher than the Ca-ribbean. In 2011 Aruba’s average occupancy rate of AHATA hotels was 78%, 10% higher than the Caribbean for the first six months of the year. The graph shows that the Caribbean followed a similar trend in hotel occupancy in 2011 as in

2010, while Aruba shows an increased January, May and June in 2011 compared to 2010 and a dip in April. The Timeshare resorts in Aruba show an average occupancy rate of 82.4% in 2010 and 83.8% year to date June 2011. (see figure 2.1)

Revenue per available room Aruba hotels compared to Caribbean The revenue per available room (RevPAR) for Aruba was considerably higher compared to the Caribbean for the first six months of 2010 and 2011 as is illustrated in Figure 2.2. The Aruba RevPAR of AHATA hotels averaged US$152 and US$ 164 respectively, compared to the Caribbean averaging US$114 and US$ 120 respectively. The RevPAR of Aruba’s

Main Indicators of tourism activity 2006-2010

2006 2007 2008 2009 2010

Tourism Receipts (in Afl. Million) 1895.5 2162.7 2400.5 2164.3 2212

Tourism Receipts (as a percentage of nominal GDP) 43.7 46.2 48.8 48.3 51.4

Tourism Receipts per capita (in Afl.) 18433 20794 22800 20304 20582

Stay-over visitors (in thousands) 694.4 772.1 826.8 812.6 825.5

Stay-over visitors per capita 6.8 7.4 7.9 7.6 7.7

Visitor nights (in thousands) 5470.5 5879.9 6264.7 6172.9 6466.2

Average daily expenditure (in Afl.) 197 175 173 184 n.a.

Average occupancy rate of Timeshare resorts (in percent)* 79.8 81.5 79.9 77.3 80.6

Average occupancy rate of AHATA hotels (in percent) 74.3 74.4 73.2 72 73.7

Average daily rate of AHATA hotels (in Afl.) 328 329 341 321 322

Revenue per available room (AHATA hotels in Afl.) 245 245 360 231 238

Cruise visitors (in thousands) 591.5 481.8 556.1 606.8 569.4

Aruba's market share in the Caribbean (in percent)

Stay-over visitors 3.5 3.8 4 4.1 3.9

Cruise tourism 3.1 2.5 2.9 3.1 2.7

Source: CBA, ATA, CBS Aruba, CTA, CTO *) this information is based on CBS data and is based on timeshare resorts only

Table 2.1

Table 2.2

Main tourism indicators YTD June 2010-2011

2010 2011 variation in %

Stay-over visitors ( in thousands) 409,829 434,287 6.0%

Average occupancy rate of Timeshare resorts (in percent) 82,4 83,8 1.7%

Average occupancy rate of AHATA resorts (in percent) 76,1 77,9 2.4%

Average daily rate of AHATA resorts (in Afl.) * 357.21 378.21 5.9%

Revenue per available room of AHATA resorts (in Afl.)* 271,76 294,63 8.4%

Cruise visitors ( in thousands) 341,237 377,857 10.7%

Source: ATA, AHATA, CBS *) The information is based on the AHATA hotel performance and therefore does not include the timeshare hotels

Two Steps Ahead Tourism Policy 2012

11

hotels is on average 35% higher than the Caribbean. Aruba has seen an increase of 8% in RevPAR in 2011 for the first six months of the year compared to an increase of about 6% for the Caribbean. The highest RevPAR month for the Caribbean was March for 2010 and 2011, respectively US$145 and US$147. Aruba’s RevPAR was at its highest in Feb-ruary for 2010 and 2011, respectively US$203 and US$215. (see figure 2.2)

Market Share The market share of visitor arrivals per country is pre-sented for 2011 Year to Date (YTD) June and the past 5 years (see Table 2.3). In four years, the U.S.A. mar-ket share has decreased with over 7% due to the di-versification policy, an increased air service from other markets and the effects of the economic crisis. Cana-da’s market share has grown steadily in the last years due to an increase in charters flight out of Toronto. The Netherlands and Colombia have remained stable. The Venezuelan market share suffered a decline last year due to the volatile economic and political situation and travel limitations, but is recovering well in 2011 with improved travel conditions. Brazil with its grow-ing economy and an increase in international travel has almost doubled its market share in 2010. Under the “other countries” category, United Kingdom and Scandinavia showed an increase in the past 2 years. 85% of Aruba’s stay-over visitors in 2010 originated from four countries: United States, Venezuela, The Netherlands and Canada.

0 10 20 30 40 50 60 70 80 90

100

Jan Feb Mar Apr May June

in percentages

Occupancy Aruba compared to Caribbean

Timeshare Aruba 2011 Timeshare Aruba 2010 AHATA hotels 2011 AHATA hotels 2010 Caribbean 2011

Caribbean 2010

$-‐

$50.00

$100.00

$150.00

$200.00

$250.00

Jan Feb Mar Apr May June

RevPAR Aruba compared to Caribbean

AHATA Hotels 2011 AHATA Hotels 2010 Caribbean 2011

Caribbean 2010

Figure 2.1

Figure 2.2

Source: Smithstar research and AHATA

Source: ATA

Source: SmithStar Research and AHATA

Market Share in percentages

2006 2007 2008 2009 2010

U.S.A 71.5 67.8 65.3 65 64.9

Venezuela 8.2 11.9 13.6 12.9 11

The Netherlands 5.3 4.9 5 5.1 4.9

Canada 3.3 3.3 3.9 4.2 4.6

Colombia 1.7 1.7 1.6 1.9 1.8

Brazil 1.0 1.0 1.0 1.3 2.5

Other countries 9.1 9.4 9.6 9.6 10.3

Market Share in percentages YTD June

2010 2011

U.S.A 69.96 65.36

Venezuela 7.37 9.64

The Netherlands 4.55 4.50

Canada 5.33 5.77

Colombia 1.53 1.91

Brazil 2.07 2.31

Other countries 9.19 10.51

Table 2.3

Two Steps Ahead Tourism Policy 2012

12

It is expected that in 2012, the global economic and finan-cial situation will continue to pose challenges for the travel industry. The recent downgrading of the US credit rating and its global effects, the European Union’s financial challenges, the increasing oil prices, high unemployment rates in devel-oped countries, unstable exchange rates, the challenging real estate market are factors that continue to impact con-sumer travel behavior. Tourism destinations like Aruba are challenged to strengthen their position in this volatile global economy with an intense competition from traditional and emerging tourism destinations, more destination marketing investments, improved products and services in competitive destinations, growth in available hotel rooms in the Caribbe-an and elsewhere and changing airline strategies. All of this leads to shifts in the tourism markets and in the consumer travel behavior. Aruba will continue to innovate both in marketing and visitor experience and take advantage of global opportunities to remain two steps ahead of the competition. Sustainable development In the past few years, there has been a growing global and local concern on the impact of tourism on the island’s envi-ronment, culture, authenticity, social behavior, amongst oth-ers. This is a valid concern. The solution to sustainability issues is not easy. Visitors have the biggest impact on all the island’s resources (the stay-over visitor per capita is 7.7 in

2010) and at the same time they have the biggest (positive) impact on the economy (tourism receipt per capita 2010 is Afl. 20582).The well-being and progress of the Aruban residents is a priority. The slogan “Un Aruba Dushi pa Biba ta un Aruba Dushi pa Bishita” describes the essence of a sustainable development. Tourism relies on the enjoyment of the destination’s environ-ment, infrastructure and other services. As such, tourism impacts the resources of the destination. However, there’s a convergence taking place. While the islands and communi-ties are demanding less impact on the society and environ-ment, the “new” traveler, is also demanding a more “authen-tic” experience and sustainable development as part of their vacation experience. That’s where tourism development and sustainability can converge.The TPEF projects and programs will address some con-cerns on sustainability. The new Strategic Plan will also pres-ent ways to continue to innovate and to generate sustain-able growth in the tourism sector in a socially acceptable, environmentally sound and economically viable manner.

VisionThe vision of the Minister of Tourism is for Aruba to excel as a tourism destination through sustainable development.To accomplish this, an emphasis will be placed on:

3. Tourism Policy

Two Steps Ahead Tourism Policy 2012

13

• The economic aspect: increased tourism receipts with distribution of benefits throughout the community

• The hospitality aspect: an enhanced and sustainable product development that enriches the destination ex-perience for visitors and the local community

• The marketing aspect: create demand and strengthen the Aruba image through innovative and effective mar-keting strategies

3.1 Objectives 2012

The main objectives determined for 2012 are as follows:

• Enhancement of the quality of the product to enrich the visitor experience while contributing to a sustainable tourism development;

• Increase the quality and, when necessary, the quantity of stay-over visitors throughout the year;

• Increase the quality and quantity of the cruise visitors, mainly during low season;

Based on the above, the main targeted result of these ob-jectives is an increase of 4.5% in the total tourism receipts1 and an increase in guest satisfaction of Aruba as a destina-tion. Stay-over arrivals is targeted at 3% and cruise visitor arrivals at 7%. The enhancement of the tourism experience will be measured through surveys.

The policy guidelines indicated to achieve the objectives are through marketing strategies, air service and cruise strategies and product enhancement strategies

3.2 Product

The product policy proposes an enhanced and sustainable product development that enriches the destination experi-ence for visitors and the local community

The objective of enhancing the quality of the product and the visitor destination experience is achieved by concen-trating on managing and improving the efforts through:

• Tourism Product Enhancement Fund (TPEF)

1 Until recently, the average daily expenditure as reported by the CBS was used as the main tool

for measurement of expenditure. The change in policy to use the tourism receipt as reported by the

Central Bank is due to the fact that the CBS only reports on limited stay-over visitor expenditures,

while the CBA tourism receipts includes cruise visitor and other relevant expenditures. However,

the tourism receipt of CBA is reported on a cash basis which registers payment for tourism related

products as reported by local exchange banks as well as foreign (bank) accounts held by residents.

In order to obtain more accurate information on tourism expenditure, CBA is working on providing

more detailed information for a more accurate analysis and correlation between CBA and CBS

reports..

• Integration of efforts

• Implementation of the new Strategic Plan for Tourism Development

3.2.1 Tourism Product Enhancement Fund

The Tourism Product Enhancement Fund (TPEF) was estab-lished and is effective as per September 1, 2010. The fund consists of the 2% percent of the tourism levy paid by the timeshare owners and for 2011 an additional three million florins will be contributed by the government. The TPEF supervisory board and the Ministry of Tourism work closely together with the other ministries and the pri-vate sector to plan, develop and execute projects and pro-grams. This assures an integrated approach and optimizes the coordination between the several ministries. The pro-posed projects and related estimates for 2011 and 2012 (see Table 3.1) are included as well as a review of the 2010 budget and projects (see Table 3.2). TPEF BoardThe Board of the Tourism Product Enhancement Fund (TPEF), in charge of the supervision of the fund, consists of representatives appointed by the Minister of Tourism, Minister of Culture, Minister of Infrastructure and repre-sentatives appointed by the Aruba Timeshare Association (ATSA). The Board Members appointed by ATSA are, Jan van Nes, Chairman; Lorraine de Souza, Treasurer; Joe Naj-jar; appointed by the Ministry of Culture, Arminda Ruiz; ap-pointed by the Ministry of Infrastructure, Marcial St. Jago; appointed by the Ministry of Tourism, Alejandro Muyale and Sjeidy Feliciano, Secretary.

The major areas addressed by the TPEF are Sustainability, Safety and Security, Environment, Heritage, Attractions, In-frastructure, Beaches, Cleanliness and Research.

Two Steps Ahead Tourism Policy 2012

14

Table 3.1

TOURISM PRODUCT ENHANCEMENT FUND - BUDGET 2011-2012BUDGET 2011 BUDGET 2012

Description Fixed M’tenance Total Fixed M’tenance TotalBEACHESCreation of Beaches - - - Maintenance of several beaches (incl. AMP)

- 260,000 260,000 260,000 260,000

260,000 260,000ENVIRONMENT - Solar Lights from Malmok to Arashi 168,000 - 168,000 183,000 - 183,000 Aruba Marine Park - startup (incl. coastal zone management)

350,000 - 350,000 250,000 - 250,000

Placement of Trash Cans/Collection Services

150,000 150,000 100,000 100,000

Projects to promote sustainable develop-ment

72,000 - 72,000

Programs to take care of stray cats and dogs

250,000 250,000 150,000 150,000

918,000 1,015,000SECURITYAH & SF project: certified lifeguards - - - AH & SF project: security cameras 540,000 - 540,000 540,000 - 540,000 AH & SF project: visibility teams - - - 60,000 60,000

540,000 600,000INFRASTRUCTURE - Aruba Linear Park - phase 2 3,000,000 3,000,000 Landscaping Tourism Corridors 450,000 - 450,000 850,000 - 850,000Maintenance Linear Park Phase 1 30,000 30,000 60,000 60,000

480,000 910,000

ATTRACTIONSEnhance attractions: Casibari, Natural Bridge, Ayo

250,000 250,000 50,000 - 50,000

Creation of new attractions: Serenity Park/Seroe Crystal

150,000 150,000 60,000 60,000

Birds conservation 50,000 50,000 20,000 20,000 Maintenance of attractions 580,000 580,000 300,000 300,000 Signage for roads to attractions (island-wide)

350,000 350,000 180,000 180,000

1,380,000 610,000HERITAGE - Signage historical locations: monument route

410,000 - 410,000 30,000 30,000

Heritage products 230,000 230,000 400,000 - 400,000 640,000 430,000

RESEARCH & DEVELOPMENTCertification Programs (OPC program Afl. 6.000)

160,000 - 160,000 120,000 - 120,000

Awareness Programs 240,000 - 240,000 400,000 - 400,000 Quality Assurance Projects 100,000 100,000 100,000 - 100,000 Research (beach and reef) 195,000 - 195,000 275,000 - 275,000

695,000 895,000CONTINGENCYContingency/emergency/ Program Direc-tor

33,910 33,910 140,000 140,000

6,927,444 1,020,000 4,946,910 3,680,000 920,000 4,600,000 in US$ 2,748,283 in US$ 2,555,555

Funds to be derived from Tourism Levy Additional Funds Government for 2011 Rollover from previous budget

Total

4,600,000 3,000,000

Funds TL in Afl. 4.600.000

346,910 -7,946,910

Two Steps Ahead Tourism Policy 2012

15

Within the TPEF framework the following projects and pro-grams will be implemented with the 2012 budget:

• The Linear Park: the first phase funded by the 2010 budget started in 2011 and is scheduled for comple-tion in 2011. The following planned phases of the Lin-ear Park, from 2011 to 2013, include the area between Wilhelmina Park and the former DOW building and from the Airport to the Plaza Turismo.

• Sustainability: projects and programs that will contrib-ute to the sustainability of Aruba and in line with the Oslo-statement on eco tourism will have priority. The results of the zero measurements study conducted in

2011 and the new Strategic Plan will identify additional areas for policy making and action plans for 2012.

• Hospitality and service: the Aruba Certification Pro-gram, after its introduction in 2011, will be continued in 2012 and beyond with the objective to heighten prod-uct knowledge, professionalism and quality of service of those working in tourism sector and related indus-tries. This program will make possible the use of con-sistent and factual information and will foster apprecia-tion of our island. The aim is to certify as many people as possible on an annual basis. Ensenañza pa Empleo will continue to execute this program.

TPEF 2010 Amount AWG

Status Deliverable

Linear Park First Phase from Surfside to Wilhelmina Park 3,000,000.00 To be com-pleted in October

An improved quality of life for locals and visitors: ocean vista, bike and jog-ging paths, plaza, parks

Report on Aruba’s status on sustainability 29,303.00 Completed Defined criteria for sustainability with quality requirements and meas-urable indicators to serve in policy and decision making

Increased security through AH&SF in the Cruise area during the cruise high season

40,000.00 Completed Increased safety and the feeling thereof

Aruba Marine Park Foundation 34,766.20 Ongoing Establish Blue Flag mem-bership and program to control the Lion Fish

Design and renovation of 10 Kiosks 87,533.00 To be Com-pleted by October

Increase local flavor through sale of locally made products in the Cruise Terminal

Designs of branded information signs 20,035.44 Completed Strengthen the brand

Construction and placement of Standardized and branded information signs

54,792.00 To be com-pleted in September

Better informed visitors

Task forces to maintain Clean tourism attractions and specific locations 80,000.00 Ongoing Feeling of well-being and safety. Image building

Enhancement of location for tour busses and kiosks outside of Cruise Terminal

166,660.00 Completed Orderly transportation and sales activities

Total Actual 2010 3,513,089.64

Budget 2010 3,860,000.00

2011 starting budget 346,910.36

Table 3.2

Two Steps Ahead Tourism Policy 2012

16

• Safety: promotion of safety and the feeling of safety. The 2012 program will continue in cooperation with the Aruba Hotel and Security Foundation (AHSF) with in-creased security in specific areas. The use of lifeguards at specific locations in cooperation with the Aruba Marine Park Foundation (AMPF) will also be funded in 2012.

• Quality standards: promotion of quality through imple-mentation of international quality standards throughout the hospitality industry. Research will determine the best quality standards to introduce.

• Protection of the beaches, coastal areas, and marine environment: the quality of these areas will be im-proved and where possible new beaches will be cre-ated. This project will be executed in close cooperation with Aruba Marine Park Foundation (AMPF). The efforts of AMPF to realize the certification of the Blue Flag is hereby also supported.

• The cleanliness and maintenance of locations visited by visitors: this will be a recurring activity on the TPEF program. For 2012 a total of 5 routes and 150 or more locations will be kept clean.

• Maintenance: to safeguard the quality of the product, the attractions and the beaches and the new products need to be maintained. For 2012, some of the projects will include maintenance of the cycling tracks at the Linear Park, landscaping of the Sasaki Boulevard, Ayo, Seroe Cristal, the “Santana di cacho” and other attrac-tions in the San Nicolas area.

• Heritage, Art and Cultural expressions and History: new products promoting cultural attractions will be identi-fied and developed. The projects that started in 2011 will continue in 2012, such as the monument route.

• Research and Development. Research related to up-grading and maintenance of the product in a sustain-able manner will be conducted.

• Develop and maintain national information and aware-ness programs. This program will start in 2011 and continue on a long term basis. Emphasis will be “haci Aruba un lugar dushi pa biba” and on “haci Aruba un lugar dushi pa bishita”. This program will also show the importance of everyone’s role in the community, espe-cially the younger generation. Special attention will be on using digital communication channels to reach this audience.

• Strategic Tourism Master Plan. The implementation of

the Master Plan will initiate, leading to innovative pro-grams and projects partially funded by the TPEF.

In addition to the TPEF projects and programs, the Ministry of Tourism will give priority to:

• Introduce the legislation on moratorium on construc-tion of hotels

• Integrate efforts with other ministries and other gov-ernmental departments in order to implement the beach policy

• Promote safety of the water sport activities by imple-menting and enforcing regulations

• Introduce changes to increase the hotel’s competitive-ness: make changes in the formulated IPC to stimulate investment by the hotels in their properties, encourage sustainable practices, find ways to decrease cost of doing business

• Stimulate the economic viability of San Nicolas

• Continue to enhance the cruise terminal area

3.2.2 Accommodations

In a time span of 10 years (1986-1996), the Aruba hotel and timeshare room inventory has increased with 165%, from 2524 to 6687 rooms. From the year 2000 to the year 2010 the room inventory of hotels and timeshare has increased with 19% from 6980 to 8288 rooms. Of the last 10 years, the largest growth is concentrated from 2007-2010 with 944 rooms of which 271 hotel rooms and 673 timeshare units. Separate from the hotel and timeshare sector, a strong growth has taken place in condominium projects from 189 rooms in 2007 to 807 in 2010.

In 2010 the total room inventory consisted of 4359 hotel units, 3929 timeshare units and 1696 other accommoda-tions including condominiums (see Figure 3.1). The grand

Figure 3.1

44%

39%

17%

2010 Room Inventory in Units

hotel units

timeshare units

Other Accomodations including condominium

Two Steps Ahead Tourism Policy 2012

17

total is 9984 rooms in all types of accommodations. Currently there are 27 companies that have permits to build about 4499 units on the island from 2011 onward. The 4499 planned expansion of room inventory consists of 1481 hotel rooms, 725 timeshare rooms and 2203 condominiums. The Ritz Carlton hotel has started construction in 2011 (320 rooms) and the Sunrise Development Group project (420 rooms) is pending start-up.

*Due to the effects of the economic crisis and other factors, 1087 of the 4499 planned construction of units will possibly not materialize.

To maintain a sustainable development, the government ad-heres to a minimum growth.

The following policy applies:

• Expansion in accommodations will be restricted to those that already have all necessary permits in place; permits that expire will not be re-issued

• New requests for permits will not be honored except for a total of 1500 rooms’ maximum in the San Nicolas area with a limited amount of “boutique hotels1

• Phasing of construction will be encouraged

• Property upgrade is encouraged rather than construc-tion of additional hotel rooms

During the last few years, the hotel sector made consider-able investments in the renovation and rejuvenation of their properties, increasing its competitive advantage and the potential for higher rates.

3.2.3 San Nicolas

1 A boutique hotel will have to comply with certain criteria: a limited amount of rooms, intimate,

luxurious and trendy property with personalized service. It will target a specific niche market.

The Seroe Colorado hotel project will activate the business-es and attract visitors and locals to San Nicolas. Activities, such as the Carubbian Festival, have already attracted thousands of visitors and have served as an impulse for visitors to get acquainted with San Nicolas. Other stimuli will be considered for 2012:

• Two small 50 room hotels will receive licenses to oper-ate a casino, in addition there is a possibility for two boutique hotels with a maximum of 50 rooms remains open. The total amount of rooms including the Seroe Colorado project will not exceed 1500 rooms.

• Additionally, a tourist information center will be opened in San Nicolas in partnership with the Aruba Tourism Authority.

• Currently, the Aruba Airport Authority is studying a pos-sible location for the development of a commuter air-port in San Nicolas. If the study results are positive, a feasibility study will be conducted.

Integration of EffortsThe destination experience requires an integrated approach between the government, the community and the private sector. The government is investing considerable funding in improving the quality of life through urban, district and infrastructure renewals and upgrading of facilities. The community projects promote the well-being of our citizens as a central goal. The tourism industry sector is increasing its efforts on resource efficiencies and green technologies and continuously invests in upgrades. The tourism policy for product is focused on investment in improving, preserv-ing, conserving our human capital and natural resources.

3.3 Marketing

Creating exceptional demand and strengthening the im-age of Aruba as the destination of choice is fundamental in reaching marketing objectives. The 2012 marketing poli-cies are to increase the quality and quantity, when neces-sary, of the stay-over visitors throughout the year.

The following policies serve to achieve the overall objectives:

• Marketing strategies: targeted, innovative and efficient strategies with high return on investment (ROI), with emphasis on effective strategies for online marketing and public relations.

• Marketing investment criteria: develop and update business intelligence to effectively evaluate marketing investments considering the developments in oil pric-

2007 2010 Planned ex-pansion 2011-

beyond*

Total

Hotel 4088 4359 1481 5840

Timeshare 3256 3929 725 4654

Condo 189 807 2203 3010

Other 835 889 90 979

Total 8368 9984 4499 14483

Table 3.3

Two Steps Ahead Tourism Policy 2012

18

es, airline strategies, market economies, global com-petition and trends in consumer travel and spending behavior.

• Diversification of Geographical markets: diversification of markets and strengthening of major/ traditional mar-kets. To ensure economic growth from tourism, and not rely heavily on a few markets, it is important to strengthen well performing markets and diversify into markets that have a high positive economic impact. Factors such as seasonality, air strategy and other in-vestment criteria must be considered.

• Targeted market group:

√ A visitor profile with high purchasing power and aligned with the product offering

√ Develop, refresh and diversify niches in line with the latest global trends, considering new potential segments such as sports, culture, health and eco in addition to the traditional niches of family, weddings and honeymoon, diving, golf and others

√ Intensify efforts in the lucrative Meetings, In-centives, Conventions and Exhibitions market (MICE) especially the incentive market.

• Marketing innovation: develop new products and packaging aligned with the demand of the consumer.

• Event marketing: invest in high profile events that bring a high return in PR value, targeting new visitors with high discretionary income. Promote local events that add positively to the overall experience of the visitor.

• Business intelligence: ATA will perform research and analysis to support strategic decision making in mar-keting and product for short, mid and long term

• Branding: continue national and international imple-mentation and promotion of the Aruba brand.

The marketing policy will be supported by an effective air service policy.

3.4 Air ServiceThe general tourism policy of Aruba has as its key objective to increase the quantity and quality of stay-over visitors, leading to an increase in tourism revenues. Air service is a critical tool in support of reaching that objective.A solid air service strategy must be maintained to achieve the required airline seat capacity for a continuous and sustainable

positive development of the tourism industry. The objective of the air service policy is to lay the basis to develop strategic choices in the maintenance and acquisition of the needed air seat capacity. The following points have been taken into consideration in de-termining the air service policy:

• Sustainable growth in air service leads to a stronger tour-ism industry

• Creating demand to profitably fill the airline seats is critical

• Increased diversity of air service is essential in view of the limitations of the airport facilities and in view of the depen-dency of source markets

• To engage commitment, partnerships with the airlines must be maintained through open communications, ex-ploring marketing opportunities, review of yield satisfac-tion and concerns, and discussing opportunities for sup-port

• New opportunities must be explored within key markets and feeder markets

• Airline strategies and consumer travel behavior need to be closely monitored

The air service policy has to be managed with the following in mind:

• The provision of high quality air service for stay-over visi-tors is the number one priority

• There has to be a balance between the number of rooms and airline seats taking into consideration seasonality, length of stay, visitor profile, average daily expenditure, revenue generation for the airport and the island in general

• Prioritize services based on Airport capacity and Cus-toms & Border Protection (CBP) services

• Creating a good fit between the strategies of airlines, air-port and destination

• Strive for quality tourism within the mix of Aruba’s product

The air service policy includes positions on the following key aspects:

• Airline Strategy: Aruba will attract, maintain and facili-tate air service that contributes to the general tourism policy objectives. Diversification in source markets,

Two Steps Ahead Tourism Policy 2012

19

high and low season considerations, airport and CBP capacity, return on investment, tourism revenue gen-eration, length of stay, consumer travel behavior, affinity with the Aruba products and services, are all factors that have to be taken into consideration when deter-mining airline source markets and strategy. To main-tain sustainability in air service, partnerships have to be established through win-win strategic cooperation. The understanding is that Aruba’s best investment is to primarily create and grow continuous and consistent demand to fill the available airline seats and to increase the potential for additional air seat capacity. It is un-derstood that through marketing support and airport incentives, Aruba supports airlines in operating a profit-able and sustainable route.

• Open Skies: Maintain Aruba’s Open Skies policy to keep strong competition in place, to stimulate explora-tion of profitable ventures and to ultimately provide the air service needs of the destination’s national economy.

• Diversification of Source Markets: Aruba will continue to invest in diversification into those source markets which will generate higher spending visitors and by so doing ensure less dependency on a few source mar-kets, for a better return on investment and increased revenues for the island.

• Scheduled Air Service and Charter Operations: Sched-uled service best answers travel flexibility demands of Aruba’s customer. Charter service may be required

and encouraged to open new markets, develop sec-ondary markets and to bring additional guests during off-season or peak periods. In the further development of Aruba’s tourism industry, both scheduled air service and charter operations play a role.

• Aruba’s Hub function: The tourism policy’s primary ob-jective is to meet the island’s tourism economic objec-tives and therefore must primarily support air traffic that delivers stay-over visitors to the island. A hub strategy is therefore of secondary importance and must be based on additional financial and tourism benefits that can be derived from the hub. The hub strategy could be promoted during mid-week periods or off-peak pe-riods with priority given to those flights with potential to generate for visitor stays on-island, as long as they do not encroach on services that deliver stay-over visitors.

• Home Porting for Cruise Lines: Aruba’s primary objec-tive is to meet the island’s tourism economic objectives and therefore must primarily serve air traffic that delivers stay-over visitors to the island. Any home porting strat-egy is therefore of secondary importance and must be based on additional financial and tourism benefits. Home Porting will only be pursued during mid-week or off-peak periods when the airport’s resources are available after serving Aruba’s main objective of increasing stay-over visitors. The Home Porting strategy must be maximized by offering pre- and post- stay-over packages.

• Private Aviation Services: The marketing for Private

Two Steps Ahead Tourism Policy 2012

20

Aviation Services supplements and complements Aru-ba’s destination awareness in a niche market with high potential for stay-over visitation. Aruba will continue to support the services of Private Aviation and a contin-ued expansion in infrastructure and services.

• Customs and Border Protection (CBP) services: Aruba will support the CBP facilities of pre-clearance for US immigration and customs as it provides Aruba with added benefits to the advantage of Aruba’s airline strategies. Continuous efforts must be made to explore maintenance and increased availability of the CBP ser-vices.

• Marketing Funds and Incentives: Aruba will create and maintain through ATA a separate fund for airlift mar-keting support and other incentives. The Aruba Airport Authority will maintain and improve its incentives if the market demands with airport’s financial viability in mind.

• Guarantees to airlines: The air service policy does not support the use of guarantees to airlines. However, the Minister reserves the right to consider such op-tion if it proves to be necessary to open a new mar-ket or to stimulate substantial growth in a market with the final objective of generating substantial economic growth on the island. The funding for guarantees will be through ATA.

The directives per market based on the marketing and airlift policies are:

North America• Restore air service capacity from the traditional mar-

kets, such as Boston, Philadelphia and New York, by non-stop service

• Align with the hub strategy of the airlines, restoring and/ or maintaining the total available seat capacity out of Charlotte, Atlanta and Miami

• Support new service out of the top feeder markets:

Detroit, Pittsburgh and the West Coast

• Increase the flights from markets outside the traditional North East market, such as Chicago, Houston, Atlanta, Ft. Lauderdale, Orlando and Baltimore

• Continued support to the Canadian charter carriers

Latin America• Support the introduction of non-stop service from key

markets. Primarily out of Brazil, Sao Paulo and sec-ondly out of Argentina, Buenos Aires

• Support expansion of service in line with an increase in expected demand out of Colombia and Venezuela

• Continued support of airlift over key hubs, such as Bo-gota and Panama

• Continued support of charter lift from secondary mar-kets that will be evaluated case by case

Europe• Continued support for scheduled airlift from the Neth-

erlands

• Encouraging improved connections with markets be-hind the Amsterdam hub in Europe

• Continued support to suitable charter services from the Netherlands, United Kingdom, Scandinavia and Italy

• Support to non-stop service from Germany

Caribbean• Support improved air service between Aruba, Bonaire

and Curacao and support for the reduction in cost of travel between these islands

• Explore and evaluate the opportunities for the develop-ment of service to other Caribbean islands.

Two Steps Ahead Tourism Policy 2012

21

3.5 Cruise

The tourism policy is to increase the quality and quantity of the cruise visitor arrivals mainly during low season. The cruise business adds to the economic activity and impact of Oranjestad, attractions and island activities. Cruise visi-tors are also a high prospect for repeat visitation as a stay-over visitor. In 2011, many upgrades in the cruise terminal and outside of the cruise terminal have been implemented to upgrade the experience of the cruise visitor.The cruise policy includes the following for 2012:

• Attract additional cruise visitors through additional cruise lines or calls, especially during low season

• Attract cruise lines with passengers with a higher spending power

• Enhance the quality of the cruise visitor experience

• Stimulate on island expenditure by cruise visitors and crew members, by implementing ‘incentive programs’

• Promote conversion of the cruise visitor into a returning stay-over visitor

• Maintain a close relationships with current and poten-tial cruise lines

• Pursue cruise home-porting in cooperation with Aruba Ports Authority (APA) and Aruba Airport Authority (AAA)

in accordance with the air service policy

• Improve the infrastructure around the harbor area as well as the accessibility within Oranjestad

As cruise business to the Caribbean decreases during the off season due to a high demand for Europe, Australia and Asia, incentives must be offered to attract off season vis-its. The Minister of Tourism, in cooperation with the Aruba Tourism Authority and Aruba Ports Authority will offer mar-keting incentives to the cruise lines in order to secure calls over the period of April to September. Marketing dollars and head-tax incentives will be offered per cruise line for a minimum of ten calls. Other incentives will be developed to open more possibilities.

In order for cruise ships to remain in port until 11 p.m., they will receive an additional incentive from the Government: upon the request of the cruise line they are permitted to open their casinos and shops in port after 7 p.m. A cruise committee is in place with private and public rep-resentatives to develop strategies to increase cruise busi-ness, enhance the visitor experience and increase on island expenditure.

Two Steps Ahead Tourism Policy 2012

22

The government departments Aruba Tourism Authority (ATA) and Aruba Cruise Tourism (ACT) were transformed to one unique independent legal entity in public sphere, Aruba Tour-ism Authority Sui Generis (ATA SG) on January 1st, 2011. 1 2011 is considered a year of transition for the organization.

ATA operates as the Destination Marketing Organization of Aruba. The objective of ATA SG is to refocus and reform by increasing the efficiency in the organization and create more funds for the marketing of Aruba as a destination. ATA is responsible for addressing and consolidating the tourism interest of stakeholders and partners on-island and abroad, coordinating marketing activities and business development for the destination. The main focus of ATA is to be able to act more flexible, ef-ficient, dynamic and less bureaucratic with a new financial structure. The flexibility will facilitate in responding to market opportunities due to consumer behavior and global trends.

1. 4.The State Ordinance in establishing Aruba Tourism Authority Sui Generis LV 10 states that the

ATA has certain responsibilities in regards to the policies of the Minister. The following is stated:

Art2.1 There is an organization aimed at promoting the tourism to Aruba in accordance with the

policy determined by the Minister referred to in Article 17.5 and operates under the name Aruba

Tourism Authority

Art 4.2 The Director should, in terms of management, referred in paragraph one, follow the content

of this State Ordinance and the directions of the Minister, as mentioned in article 20

Art 20.1 The Minister is entitled to give general indications to the Director regarding the execution of

her duties. The Director will follow the indications within the time frame indicated by the Minister.

Art 20.2 Before the Minister gives an indication as stated in the first paragraph, he will request the

advice of the Board. The Board will provide the advice as soon as possible, but before two weeks

time. The decision to not take the advice will be given a reason.

4. Aruba Tourism Authority Sui GenerisThe organizational structure and the internal process will be evaluated in 2011, based on flexibility, effectiveness, produc-tivity, competitive power and on the financial management. The vision of ATA will be achieved through 8 core objectives in a period of 3 years starting in 2011.

These objectives are:

1) Create an effective organization with clearly defined pro-cedures, which will lead to an organization that can re-spond to the needs of the markets and the industry

2) Financial independence and an effective administration

3) Produce relevant communication in the digital era

4) Focus on research, strategy and planning

5) Create a link between supply and demand: a strategic external sounding board

6) Offer products that are relevant to Aruba’s target mar-kets, in order to further drive competitive advantage

7) Visitor centers: Establish points of contact where the visitors can have access to information

8) Advertising and branding, including “merchandising”

Two Steps Ahead Tourism Policy 2012

23

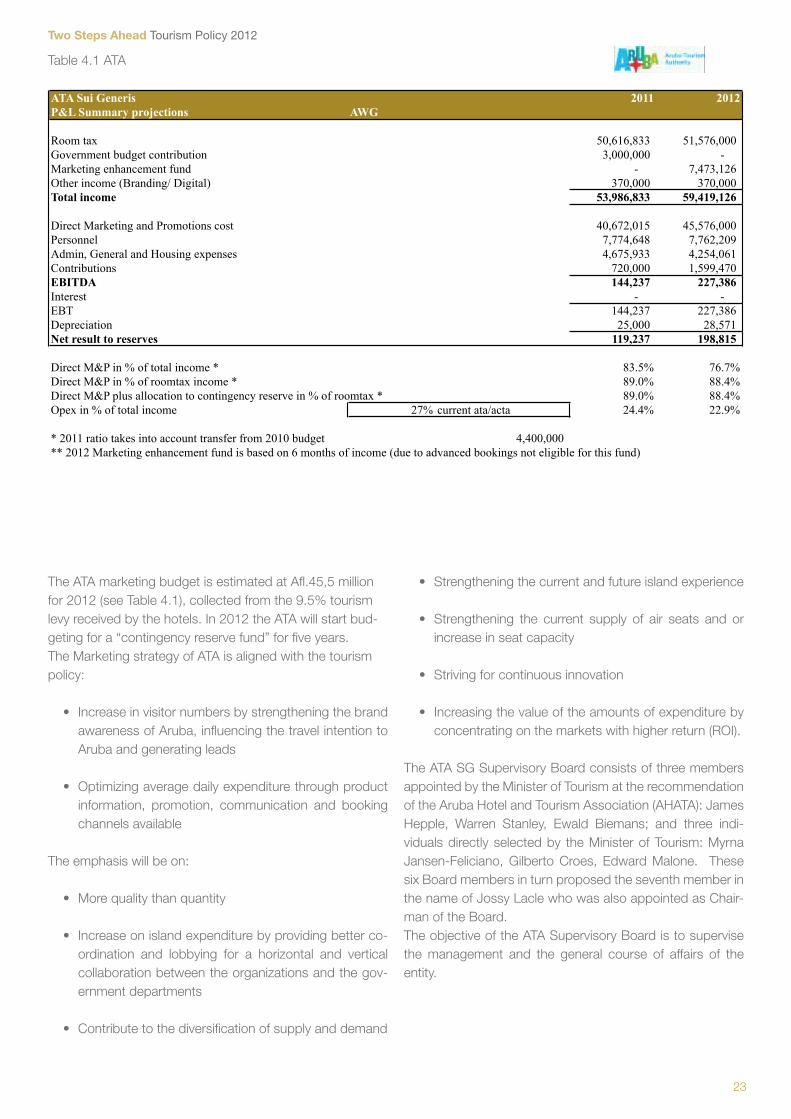

The ATA marketing budget is estimated at Afl.45,5 million for 2012 (see Table 4.1), collected from the 9.5% tourism levy received by the hotels. In 2012 the ATA will start bud-geting for a “contingency reserve fund” for five years. The Marketing strategy of ATA is aligned with the tourism policy:

• Increase in visitor numbers by strengthening the brand awareness of Aruba, influencing the travel intention to Aruba and generating leads

• Optimizing average daily expenditure through product information, promotion, communication and booking channels available

The emphasis will be on:

• More quality than quantity

• Increase on island expenditure by providing better co-ordination and lobbying for a horizontal and vertical collaboration between the organizations and the gov-ernment departments

• Contribute to the diversification of supply and demand

ATA Sui Generis 2011 2012P&L Summary projections AWG

Room tax 50,616,833 51,576,000 Government budget contribution 3,000,000 - Marketing enhancement fund - 7,473,126 Other income (Branding/ Digital) 370,000 370,000 Total income 53,986,833 59,419,126

Direct Marketing and Promotions cost 40,672,015 45,576,000 Personnel 7,774,648 7,762,209 Admin, General and Housing expenses 4,675,933 4,254,061 Contributions 720,000 1,599,470 EBITDA 144,237 227,386 Interest - - EBT 144,237 227,386 Depreciation 25,000 28,571 Net result to reserves 119,237 198,815

Direct M&P in % of total income * 83.5% 76.7%Direct M&P in % of roomtax income * 89.0% 88.4%Direct M&P plus allocation to contingency reserve in % of roomtax * 89.0% 88.4%Opex in % of total income 27% current ata/acta 24.4% 22.9%

* 2011 ratio takes into account transfer from 2010 budget 4,400,000 ** 2012 Marketing enhancement fund is based on 6 months of income (due to advanced bookings not eligible for this fund)

Table 4.1 ATA

• Strengthening the current and future island experience

• Strengthening the current supply of air seats and or increase in seat capacity

• Striving for continuous innovation

• Increasing the value of the amounts of expenditure by concentrating on the markets with higher return (ROI).

The ATA SG Supervisory Board consists of three members appointed by the Minister of Tourism at the recommendation of the Aruba Hotel and Tourism Association (AHATA): James Hepple, Warren Stanley, Ewald Biemans; and three indi-viduals directly selected by the Minister of Tourism: Myrna Jansen-Feliciano, Gilberto Croes, Edward Malone. These six Board members in turn proposed the seventh member in the name of Jossy Lacle who was also appointed as Chair-man of the Board. The objective of the ATA Supervisory Board is to supervise the management and the general course of affairs of the entity.

Two Steps Ahead Tourism Policy 2012

24

In 2012, Aruba Airport Authority (AAA) will continue with the beautification and upgrade of its product and services. The projects taking place are the upgrade of the arrivals terminal, the areas in front and between terminals and the departure gates. The Aruba branding is incorporated in the new design airport. AAA will carry forward projects to guarantee safe and ef-ficient air side operations in compliance to local and interna-tional regulations. AAA is investing heavily in airside capacity increases in the medium term, both commercial and general aviation. 2012 will see the first completion of two 737 type aircraft hangars.The AAA plays an important role in attracting and maintain-ing air service to the island through direct contact with air-lines and will continue to network, together with the ATA and the Ministry of Tourism, for a diversified and strong airline network to increase the flow of passengers to the island. AAA is a profitable enterprise that through taxes and divi-dends contributes to the general budget and tourism ori-ented projects by the Ministry of Tourism. Priorities of AAA in 2012:

• Maintain and leverage the relationship with Schiphol Group

• Emphasis on “Green”; special focus on energy sav-ing projects such as the introduction of a LED basis

5. Aruba Airport Authority

airfield, lighting system, a solar paneled car park, and reducing the carbon footprint of the airport

• Continue to improve the quality of the product and ser-vice

• Enhance the visitor experience with a flavor of local art

• Increase the airside capacity of aircraft and parking po-sitions and hangers

Total investment in 2012 is estimated at Afl. 44 million.

Two Steps Ahead Tourism Policy 2012

25

The Ministry of Tourism has achieved many of its objectives as delineated in the 2010-2011 tourism policy and plans. Amongst others:

• The new legal status of the Aruba Tourism Authority as per January 01, 2011

• The Tourism Product Enhancement Fund established as per September 01, 2010

• Increased hotel occupancies, average daily rates and revenue per available room

• Increased stay-over visitors year to date

• Carnival Cruise Lines has returned to Aruba in 2010. Calls have steadily increased from zero calls in 2009 to at least 23 calls in 2012

• KLM has returned to Aruba in 2010 with 2 weekly flights, has increased its direct flights to Aruba to 5 weekly flights in 2011 and has adjusted its departure time to Aruba to accommodate more passengers from other markets

• San Nicolas is bustling with the weekly Carubbian Fes-tival and will continue to receive proper attention with projects for upgrading of attractions

• Increased air service from all markets. Notwithstanding the challenges in air service, the winter of 2011/2012 is projected to have an increase of 3,5% in seats with a total amount of 11,119 additional seats and a 6,5% increase in flights compared to winter 2010/2011

• The Aruba Certification Program has initiated and will reach over two thousand people by the end of 2012

• The first phase of the Linear Park will be completed in October 2011

• TPEF has funded and completed the following projects amongst others: booths for the sale of locally made products, increased security in the cruise area, infor-mation signage, maintenance of a clean Aruba, and a sustainability report

• New gateways, Baltimore and Orlando have been add-ed, increasing the amount of gateways to Aruba out of the U.S. to a total of 14

6. Achievements 6.1 Linear Park

The first phase of the Linear Park from the roundabout of Las Americas to the Wilhelmina Park will enhance the Aruba experience of residents and visitors by providing beautiful vistas, jogging, bicycling and walking paths, plazas and more accessible beaches. The Linear Park connects well with the downtown Oranjes-tad urban renewal and revitalization project. When all phases are completed, the Linear Park will encom-pass a ten mile strip from the Reina Beatrix Airport to Arashi, beautifying the entire tourism corridor.

Two Steps Ahead Tourism Policy 2012

26

6.2 Aruba Certification Program

The Aruba Certification Program is another vision of the Min-ister of Tourism to increase the standards of service and im-prove the overall destination experience of the visitors. The program was designed by ATA and the Ministry of Tourism and is implemented by “Enseñanza pa Empleo” (EPE) and the Ministry of Tourism with funding from ATA and the TPEF. The program is designed primarily for the hospitality industry with consistent, accurate and uniformed information on the tourism destination product encompassing various subjects such as culture, history, fauna, archeology, service. The pur-pose is to rekindle the pride and unity of the Aruban com-munity through the awareness and education of the Aruban brand identity and brand promise resulting in One Happy Island. By investing in the quality of the people, level of pro-fessionalism and consistent knowledge of the Aruba prod-uct, the workforce will be highly motivated and be proud ambassadors of our beautiful island. The positive results of the Aruba Certification Program will lead to:

• Satisfied visitors, which will increase positive word of mouth

• Improved service and destination experience that will increase loyalty and repeat visitation

• Positive image of a structured and educated tourism hospitality services

• Higher industry standards, enhancing our quality of service

The program started officially in September 2011 and will continue during 2012 and beyond. Included for participa-tion are the taxi drivers, tour operators, customs and immi-gration officers, water sports operators, Visibility team and OPC members, retail stores/ restaurants/ hotel employees. The plan is to open this program for participation to the general public at a later date.

Mi compromisocu ArubaPrograma di Certificacion

Two Steps Ahead Tourism Policy 2012

27

To achieve a national approach to tourism, the Minister of Tourism has embraced Public/Private partnerships in all its endeavors.

• The Tourism Council consists of experienced individu-als in the tourism industry that functions as the sound-ing board to the Minister of Tourism. Members are: Michael Kuiperi, Rory Arends, Edward Malone, Mario Arends, Lisette Malmberg, and Anabela Peterson

• The Aruba Tourism Authority Board and the Tourism Product Enhancement Fund Board consist of a bal-anced representation between public and private sec-tor partner members to ensure that both groups have participation in important policies, strategies and pro-grams to stimulate the tourism industry

• From the onset, over 70 stakeholder groups were heard and their concerns were incorporated into poli-cies and action plans

• All tourism related taskforces and committees, such as the airlift committee, the beach policy committee have public and private member participation

• The research done to develop the new Strategic Plan for the Development of Tourism has massive input from

7. Private Public Partnership

GREENCORRIDOR

Public PrivatePartnershipAruba 2011P3

all stakeholders locally and internationally

• The Ministry of Tourism and the Aruba Tourism Author-ity, the Aruba Airport Authority and the Aruba Ports Au-thority are partners working in close collaboration with the private sector partners in the tourism industry

To achieve the objectives and capitalize on the potential of 2012, the Minister of Tourism will continue his policy of pub-lic/private partnership.

Two Steps Ahead Tourism Policy 2012

28

A new Strategic Plan for the Development of Tourism in Aru-ba will be presented in December 2011. The objective of this new plan is to maintain and improve Aruba’s competitive position in the Caribbean in the short, medium to long term. Additionally, this Strategic Plan will assist Aruba in gener-ating sustainable growth in the tourism sector in a socially acceptable, environmentally sound and economically viable manner. The outcome of the plan will allow the Government and the private sector to make clear policy choices and commit to a development strategy for tourism, while secur-ing and enhancing the quality of life of its citizens.

The plan is needed for several reasons. While it is known that tourism will continue to play a critical role in the econo-my of Aruba, the question lies if the current model of tourism specialization that has been used in the past will work in the future. Additionally, changing demographics of tourists have strong implications in understanding the visitor experience to Aruba. This plan will be one of the first to focus on the de-mand side of visitors’ preferences and expectations. Finally, the Strategic Plan will also shed insight into how tourism has affected the quality of life of residents.

A variety of research tools has been utilized. Individual stake-holder meetings with those in traditional fields (i.e. hotels and tourism policy makers) as well with those in non-traditional fields (i.e. cultural, religious, social leaders) have taken place. Focus groups in the areas of authenticity, productivity, part-nerships, food and generations have been organized from the supply side. Focus groups with visitors have also been conducted. A variety of surveys were created to understand tourist perceptions, their travel experiences and spending patterns in Aruba. Additionally, surveys were conducted to determine visitor preferences in areas of telecommunica-tions and gastronomy, cruise passenger experiences and vacation home preferences.

An employee survey has been carried out to gain information

regarding the employment and everyday life. A quality of life survey was conducted to gain knowledge on the quality of life of our residents and how tourism affects them and their communities. Data will also be obtained from key partners including Central Bureau of Statistics, Aruba Tourism Au-thority, Central Bank of Aruba, and others. Finally, the study also includes a latent demand analysis, which will provide a picture of potential demand throughout the USA, the Neth-erlands and Venezuela.

As a result, there will be a variety of tools that will be made available for decision making. Components of the Strategic Plan will include a tourism perception report, competitive-ness report, economic impact study of tourism in Aruba, tourism and quality of life report, demand analysis, including latent demand analysis and supply inventory with gap analy-sis, seasonality report, and effects of tourism specialization.

The vision and short to long-term strategies will be present-ed during the Aruba Tourism Summit in December 2011.

8. Future Outlook: Strategic Plan for the Development of Tourism in Aruba

Two Steps Ahead Tourism Policy 2012

29

Source: ATA

Stay-over Latin America 2006-2011Latin America had a substantial growth in 2008 (See Figure 9.3), as the Venezuelan market performed well. It can be seen that the Latin American stay-over visitors suffered a small drop in 2010; this had to do with the economic and political conditions in Venezuela. The Brazilian market grew with almost 100% in 2010, compensating the shortfall in visitors out of Venezuela. The stay-over arrivals of 2011 are over a six-month period, from January to June 2011, from 53,453 visitors in 2010 to 72,242 visitors in 2011, an in-crease of 35%.

Source: ATA

9. Statistics

Arrivals 1958-2010This arrival chart illustrates the growth of stay-over visitor ar-rivals over the past 50 years. The extreme growth occurred after the closing of the Exxon oil refinery “Lago” in 1985. The arrivals grew from 200,000 in 1986 to over 800,000 in stay-over visitors in 2010 as illustrated in Figure 9.1.

Stay-over Visitors North America 2006-2011North America is Aruba’s main market with 65% of our stay-over visitors coming from the USA. The North Ameri-can stay-over arrivals decreased in 2009 due to a lack in consumer confidence as North America was affected by an economic crisis. In 2010 a recovery was detected, as the 2010 North American arrivals were the highest in the last five years as shown in Figure 9.2. From January to June 2011, the stay-over arrivals accounted for 310,350 visitors, an increase of 0.1% from the 310,051 arrivals over the same period in 2010.

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1958 1960 1962 1964 1966 1968 1970 1972 1974 1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Arrivals

Total arrivals 1958-‐2010

515,875 546,033

570,903 561,960 573,310

310,051 310,350

2006 2007 2008 2009 2010 June YTD 2010

June YTD 2011

North American stay-‐over arrivals

Figure 9.1

Figure 9.3

Source: ATA

87,291

125,682

151,080 148,825 145,956

53,453

72,242

2006 2007 2008 2009 2010 June YTD 2010

June YTD 2011

Latin American stay-‐over arrivals

Figure 9.2

Two Steps Ahead Tourism Policy 2012

30

Source: ATA

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

2006 2007 2008 2009 2010 June YTD 2010

June YTD 2011

European Stay-over Arrivals

Stay-over Europe 2006-2011Europe has grown steadily in the past five years as seen in Figure 9.4, specifically due to an increase in charter service out of Scandinavia, Italy and the United Kingdom in the past years and additional air service out of the Netherlands. The stay-over arrivals for 2011 are over a six month period, from January to June 2011, from 34,196 in 2010 to 37,720 in 2011, an increase of 10% over the same period.

Source: ATA

Cruise Visitors 1980-2010The cruise visitor arrivals grew drastically in the year 2000 with over 200,000 additional visitors and over 100 calls in the following years. After the year 2000 the cruise calls re-mained above 300 per year, with the exception of 2001 and 2008 (see Figure 9.5). The best year for Aruba in cruise visi-tor arrivals was 2009, surpassing 600,000 passengers as il-lustrated in Figure 9.6.

Figure 9.4

0

50

100

150

200

250

300

350

400

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

Cruise Calls 1980-‐2010

0

100000

200000

300000

400000

500000

600000

700000

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Passengers

Source: ATA

Figure 9.5

Figure 9.6

Ministry of Tourism, Transportation and Labour

L.G.Smith Blvd. 76 | Oranjestad, Aruba

Tel. (297) 582 4900 | Fax. (297) 582 7556

Government of Aruba