Government Banking and BRICs in the Recent Financial Crisis

57

Observations on BRIC Government Banks and Financial Statecraft: Competitive Advantages since Liberalization and Policy Alternatives for Crisis and Social Inclusion Kurt von Mettenheim Paper to be presented to the workshop on Financial Statecraft and Ascendant Powers: Latin America and Asia after the 2008-10 Global Financial Crisis 5 April 2012, University of Southern California DRAFT FOR DISCUSSION. PLEASE DO NOTE CITE. COMMENTS WELCOME.

-

Upload

hatem-hassan -

Category

Documents

-

view

216 -

download

0

Transcript of Government Banking and BRICs in the Recent Financial Crisis

8132019 Government Banking and BRICs in the Recent Financial Crisis

httpslidepdfcomreaderfullgovernment-banking-and-brics-in-the-recent-financial-crisis 157

Observations on BRIC Government Banks and Financial Statecraft

Competitive Advantages since Liberalization

andPolicy Alternatives for Crisis and Social Inclusion

Kurt von MettenheimPaper to be presented to the workshop on

Financial Statecraft and Ascendant PowersLatin America and Asia after the 2008-10 Global Financial Crisis

5 April 2012 University of Southern California

DRAFT FOR DISCUSSION PLEASE DO NOTE CITE COMMENTS WELCOME

8132019 Government Banking and BRICs in the Recent Financial Crisis

httpslidepdfcomreaderfullgovernment-banking-and-brics-in-the-recent-financial-crisis 257

983106983122983113983107 983111983151983158983141983154983150983149983141983150983156 983106983137983150983147983155 983137983150983140 983110983145983150983137983150983139983145983137983148 983123983156983137983156983141983139983154983137983142983156

2

Introduction1

Until 2008 developing countries systematically fared worse during financial crises Afterdeclaration of moratorium on foreign debt payments by Mexico in August 1982 the globalsouth and east experienced financial crises in a seemingly endless sequence Panic in US

financial markets during 2007 quickly spread around the globe and crisis is far from overHowever it is clear that BRIC countries were better prepared to counter shocks and resumegrowth This paper explores our findings about Brazilian federal banks (that they havemodernized and realized competitive advantages since liberalization and provided criticalpolicy alternatives) to Russia India and China amidst crisis2 Although further research willbe required (and other factors mattered) evidence suggests that BRIC government bankshave indeed realized competitive advantages over private and foreign banks during the 2000sand helped provide counter cyclical credit to counter crisis We also argue that public banksmay accelerate social inclusion through new card payment and mobile banking technologies

These findings differ from the realist tradition of financial statecraft in internationalpolitical economy recent market-based banking theory and expectations that privatizations

and liberalization would reveal the greater efficiency of private banks and produce transitionsto market centered financial systems Instead evidence from Brazil and other BRICs (andrecent research on alternative banking in Europe)3 raises new questions about domestic financial statecraft social inclusion and political development We are currently workingwith a network of research and policy making institutions to promote the adoption of CorePrinciples for Alternative Banking and Social Inclusion at large public banks in advanceddeveloping and emerging countries (while supporting alternative banking groups of occupymovements in the US)4 Any shortcomings of this draft paper and our still incipient researchand policy agenda surely pale in comparison to the devastating consequences of misguidedneo-classical ideas in banking theory and neo-liberal excesses of deregulation

We define financial statecraft as the formulation of procedural rules and policies byagents empowered to act in the name of the state which mandate and regulate basicrelationships in state civil society and markets5 Financial statecraft requires balancingpolitical legitimacy and market confidence to regulate the allocation of household savings tofirms increase the mobility of capital and shape growth6 Financial statecraft is a specifictype of statecraft involving monetary financial and banking phenomena Like most conceptsin the social sciences financial statecraft cuts to essentially contested theories and concepts7 about government intervention free markets bureaucracy and policy capacities

1 Earlier versions of this paper were presented at the meeting of Association of BRICS Business Schools27 November 2010 Xavier Institute of Management and Entrepreneurship Bangalore and published as

ldquoGovernment Banking and BRICs in the Recent Financial Crisisrdquo Journal of Management and Entrepreneurship March 2011 I thank Maria Kravchenko RS Deshpande Huang Lei MihalisChasomeris CP Ravindranathan and Maria Antonieta del Tedesco Lins and anonymous reviewers forcomments and suggestions2 Mettenheim Kurt Federal Banking in Brazil Policies and Competitive Advantages London Pickeringand Chatto 20103 On alternative banking in Europe Ayadi et al (2009) Investigating diversity in the banking sector in

Europe the performance and role of savings banks (Brussels Center for European Policy Studies) andAyadi et al (2010) Investigating diversity in the banking sector in Europe key developments

performance and role of cooperative banks (Brussels Center for European Policy Studies)4 See appendix lsquoCore Principles for Alternative Banking and Social Inclusionrsquo5 Conaghan Catherine and James Malloy Unsettling Statecraft Democracy and Neoliberalism in the

Central Andes Pittsburgh University of Pittsburgh Press 19946

Sola Lourdes amp Whitehead Laurence eds Statecrafting Monetary Authority Democracy andFinancial Order in Brazil Oxford University of Oxford Centre for Brazilian Studies 20067 On essentially contested character of concepts in the social sciences see Gallie Collier Gerring

8132019 Government Banking and BRICs in the Recent Financial Crisis

httpslidepdfcomreaderfullgovernment-banking-and-brics-in-the-recent-financial-crisis 357

983106983122983113983107 983111983151983158983141983154983150983149983141983150983156 983106983137983150983147983155 983137983150983140 983110983145983150983137983150983139983145983137983148 983123983156983137983156983141983139983154983137983142983156

3

The comparative political economy of finance is especially contested Financialdeepening approaches and bank-centered finance strategies (and liberal and coordinatedpolitical economy approaches) often see the same phenomena from profoundly differentperspectives8 Liberal market-economies are driven by equity markets thrive on publicinformation and spurn coordination Coordinated market-economies are driven by bank

credit thrive on limited sharing of firm strategy with financiers and spurn markets fortheir excessive volatility that produce sub-optimal equilibrium9 From a market-centeredperspective neo-institutionalism is largely neo-protectionism From the perspective ofcoordinated capitalism and developmental states excessive liberalization andprivatization would simply throw babies -- cherished institutions of social policy anddomestic control ndash out with the bathwater In terms of finance theory marketapproaches insist that policies should free agents to lsquoget prices rightrsquo while coordinatedmarket and bank-centered approaches argue that enough credit be directed to accelerateinnovation and lsquoget planning rightrsquo10

These deep differences shape views of financial statecraft and governmentbanking in BRICs The question of social inclusion may provide more grounds for

agreement Given the huge decline in the number of bankless Brazilians (those withoutbank account) from 80 - 50 percent 2000-2010 the relation between financial statecraftand democratization appears more positive sum than supposed by most scholars ofpolitical economy Most research on domestic finance (and especially monetary theoryand policy) assumes zero sum relations between social inclusion and proper financefiscal and monetary policy However in contexts of high inequality and financialexclusion positive sum relations may obtain This counters conceptions of fiscalconstraints to change and reverses causal relations of independent central bankingInstead of seeking to ensure central bank independence from politics and social forces(Alesina and Summers 1993) or free markets and private banks through privatizationsand deregulation (Williamson 1990) the construction of financial and monetaryauthority in Brazil (Whitehead 2002 Sola and Whitehead 2006) has involved therealization of competitive advantage by large public banks (Mettenheim 2010)Moreover basic income policies (albeit conditional see Soares et al 2010) and othersocial services have proved more successful than private banking for reaching thebankless

Reforms during the 1990s and modernization of public (and central) banksduring the 2000s thus require rethinking constraints to change Since the end of theelectoral road to socialism exemplified by military coup in Chile against PresidentAllende on 11 September 1973 social scientists and policy communities have largelyconcurred that markets severely constrain social inclusion For Gold Lo and Wright

(1975) structural theories of the state replaced earlier instrumental and functionaltraditions in Marxism by better describing how markets constrain social policy and vetopolitical change Since then social scientists emphasize how markets cleared byindividual investors impose fiscal austerity and set constraints to change Much ofcritical and mainstream social science agree that social policies tend to pressure fiscalaccounts and lead either to tax increases or adjustment policies that reduced profits and

8 On bank-centered and market centered financial systems see Zysman John Governents Markets and

Growth Financial Systems and the Politics of Industrial Change Ithaca NY Cornell University Press19839 The terms of this dichotomy are from Hall Peter amp David Soskice eds Varieties of Capitalism The

Institutional Foundations of Comparative Advantage Oxford Oxford University Press 200110

This distinction between prices and planning is from Dymski Gary A lsquoBanking on TransformationFinancing Development Overcoming Povertyrsquo Paper presented to UFRJ Economics Institute September2003

8132019 Government Banking and BRICs in the Recent Financial Crisis

httpslidepdfcomreaderfullgovernment-banking-and-brics-in-the-recent-financial-crisis 457

983106983122983113983107 983111983151983158983141983154983150983149983141983150983156 983106983137983150983147983155 983137983150983140 983110983145983150983137983150983139983145983137983148 983123983156983137983156983141983139983154983137983142983156

4

tax revenue This in the worst cases caused political-economic crisis and led to thebreakdown of democracy in developing countries (OacuteDonnell 1973) Similar forces inadvanced economies led to stagflation in the 1970s and electoral turns to neo-conservative governments and neo-liberal policies in the 1980s designed to downsizeWelfare States (Pierson 1996)

These structural explanations are now incomplete Old views of fiscaldominance fail to capture the implications of advances in monetary economics duringthe 1990s and bank modernization during the 2000s Government bank modernizationnew regulatory frameworks and better supervision of banks and markets (contrary toderegulation in the US and a few tax havens and financial centers) provide a new settingfor what we call financial roads to social economies In other words structural theoriesof the state and conceptions of vicious cycles that emphasize fiscal constraints predate studies of the credit channel interest rate channel and the modernization of publicbanks

Old views of fiscal dominance remain so prevalent that austerity has oftenremained in place far beyond necessary in developing countries Many developing

countries have accumulated significant foreign reserves and sustained trade surplusesduring years of economic growth Moreover in Brazil transparent policy frameworkssuch as inflation targeting and flexible foreign exchange regimes have been in place forover a decade (Fraga et al 2004) The situation of many ergo developing countries isthus different Bank modernization the accumulation of immense foreign reserves andthe consolidation of reforms have approximated markets and public policy Newchannels for change are at hand Our research focuses on the modernization of socialbanking especially the ability of new technologies such as electronic card paymentchannels and mobile banking to bring income grants and access to banking and publicservices in vast numbers Since opening the Brazilian banking industry in 1995 a backto the future modernization of government banks and basic income policies are biglargely untold storiesl organizations the competitiveness of private banks or the greaterefficiency of market-centered microfinance firms or funds

This also implies that advocates of central bank independence beg the questionof financial statecraft in developing and emerging economies The construction ofmonetary authority in Brazil during the 1990s and 2000s differs from standard theoriesof central bank independence in three ways First rather than the imposition oforthodoxy the construction of monetary authority in Brazil involved heterodox policiesof inertial inflation that were used to reduce high and persistent inflation Second thesuccessful reduction of inflation while redistributing wealth to the poor provided thepolitical impetus and legitimation for monetary statecraft after military rule both in

terms of economic policies and party politics Third central bank authority and capacityemerged in Brazil in precisely the reverse causal order expected by economists Contrary to claims about the need to establish central bank independence to ensure pricestability the reverse occurred The Central Bank of Brazil expanded prerogatives andbuilt capacity after price stability was secured by heterodox policies in 1994

Domestic Financial Statecraft

Our approach to financial statecraft remits to a long tradition in comparative politicaleconomy that focuses on how politics and government policies shape markets Thisapproach is epitomized by Polanyrsquos The Great Transformation Shonfieldrsquos Modern

Capitalism Zysmanrsquos Governments Markets and Growth Gourevitchrsquos Politics in Hard Times Conaghan amp Malloyacutes Unsettling Statecraft and Sola amp Whiteheadacutes

8132019 Government Banking and BRICs in the Recent Financial Crisis

httpslidepdfcomreaderfullgovernment-banking-and-brics-in-the-recent-financial-crisis 557

983106983122983113983107 983111983151983158983141983154983150983149983141983150983156 983106983137983150983147983155 983137983150983140 983110983145983150983137983150983139983145983137983148 983123983156983137983156983141983139983154983137983142983156

5

Statecrafting Monetary Authority Democracy and Financial Order in Brazil PeterKingstoneacutes analysis of coalitions Christine Kearneyacutes analysis of neo-liberal policiesand studies of recentralization and federalism by Leslie Armijo Kent Eaton and DavidSamuels all explore the political determinants of economic policies in Brazil11

Polanyirsquos The Great Transformation and Shonefieldrsquos Modern Capitalism

remain canonic studies of financial statecraft Polanyi argued that laissez faire liberalism during the 19th century generated movements of social self-defense in theform of organized labor efforts to address the social question and central banking toprotect private banks from downturns and currency devaluation under the gold standardOther interventions such as tarrifs imperialist expansion subsidies to agriculture andindustry and top-down social policies also prevailed over liberalism and free marketsespecially after the 1873 depression Statecrafting often in authoritarian forms thusreappeared in the latter 19th century after decades of liberalism Thereafter two worldwars and recovery from economic depression meant that political imperatives continuedto dominate domestic policymaking After 1945 Shonefield argues that ContinentalEuropeans reshaped government ownership in response to the political and economic

imperatives of recovery rather than ideology or nationalist design This emphasis onnecessity and improvisation places the statecrafting tradition closer to Lindblomrsquosmuddling-through conception of policymaking than Marxist-Leninist or nationalisttheories that saw large state banks as means to ideological ends

Recent scholarship has returned to core ideas of statecrafting For Kirschnerbecause the impact of alternative financial arrangements and policies on welfare is oftenequal or unpredictable politics rather than independent economic judgements bothshape and explain policy choices and the configuration of markets12 Statecrafting thusdescribes the political construction of coalitions to support economic policies and theadoptionadaptation of policies to the particularities of domestic markets institutionsand politics13 Hoffman traces how political ideas periodically recast the US financialsystem during critical junctures of change since independence14 Laurence Toya andAmyx also argue that politics explain the origin character and implementation of lsquobigbangrsquo financial reforms in Great Britain and Japan in the 1980s15 Peacuterez describes howdomestic groups determined banking and finance reforms in Spain16 This is consistentwith Maxfieldrsquos description of how the formation of a bankeracutes coalition shapedfinancial reforms and policies in Mexico17 However during the last decades domesticeconomic statecrafting has become virtually synonomous with imposing liberal reformsWe report fundamentally different developments from the BRICS The realization ofcompetitive advantages by government banks since liberalization and the importance of

11

Our approach also can be described from Claus Offe as a sociological approach to political economy ndashone that focuses on how social organizations interests and political coalitions sustain economic policiesOffe Claus lsquoPolitical Economy Sociological Perspectivesrsquo in Goodin Robert E amp Klingemann Hans-Dieter (eds) A New Handbook of Political Science Oxford Oxford University Press 1998 pp 675-69012 Kirschner Jonathan (ed) Monetary Orders Ambiguous Economics Ubiquitous Politics Ithaca NYCornell University Press 200313 Conaghan Catherine M amp James M Malloy Unsettling Statecraft Democracy and Neoliberalism in

the Central Andes Pittsburgh PA University of Pittsburgh Press 199414 Hoffmann Susan Politics and Banking Ideas Public Policy and the Creation of Financial

Institutions Ithaca NY Cornell University Press 200115 Laurence Henry Money Rules The New Politics of Finance in Britain and Japan Ithaca NY CornellUniversity Press 200116 Peacuterez Sofiacutea Banking on Privilege The Politics of Spanish Financial Reform Ithaca NY Cornell

University Press 200317 Maxfield Sylvia Governing Capital International Finance and Mexican Politics Ithaca NY CornellUniversity Press 1990

8132019 Government Banking and BRICs in the Recent Financial Crisis

httpslidepdfcomreaderfullgovernment-banking-and-brics-in-the-recent-financial-crisis 657

983106983122983113983107 983111983151983158983141983154983150983149983141983150983156 983106983137983150983147983155 983137983150983140 983110983145983150983137983150983139983145983137983148 983123983156983137983156983141983139983154983137983142983156

6

these large institutions for domestic policy making particularly for counter-cyclicalcredit and social inclusion This comes at a critical time of reassessment in the US andadvanced economies

Errors of Deregulation and Crisis in the US

A clearer explanation of the financial panic in US sub-prime mortgage markets alsohelps explain why BRIC countries suffered less and recovered more quickly From theperspectives of BRICs the excesses of deregulation and market based banking are theanomalies ndash not the reality of smoothing the growth curve and encouraging socialinclusion Competing hypotheses rushed to explain the origin and evolution of the USfinancial panic and crisis (Gorton 2008) The US Government Commission (2010) splitwith dissenters presenting separate explanations However for purposes of comparisonto BRICs review of antecedents crisis mechanisms and policy responses suggest botherrors of deregulation and particular complementarities in market-centered financecapitalism Asset bubbles are not new to financial markets However the deregulation

of capital markets and the dual bubble of long-term housing prices and quick valuationof mortgage backed securities and other derivatives produced unprecedented crisis in2007 Policy statements national accounts Federal Reserve balance sheets and markettrends and working papers indicate the following causes and consequences

First the steep valuation of the Case-Schiller Home Price Index from 1988-2009suggests a long-term asset bubble has changed US political economy and producedstructural imbalances From 1895-1995 home prices largely accompanied inflation(Baker 2007) However from 1995 to June 2006 home prices outpaced inflation by anestimated 70 percent This produced a US$ 25 trillion home price bubble and a fullUS$ 80 trillion in housing related wealth effects Construction alone during this periodincreased from an estimated 4-6 percent of US GDP

Second policies designed to counter financial crisis in 2000 such as low interestrates fueled another round of home price increases while construction and consumptionwere encouraged by further deregulation of financial markets Revocation of the Glass-Steagal law (1999) the Commodities and Futures Act of 2000 and the ConsolidatedEntity Supervision Act of the Securities and Exchange Commission (2004) freed USbanks to sell and securitize mortgages and other assets virtually without supervisionInstead of convergence toward International Financial Reporting Standards and Bankfor International Settlements (BIS) Basel II Accord capital reserve requirements USbanks were permitted to leverage freely and sell largely without consumer protectionregulations The US turn to deregulation remains an outlier Elsewhere domestic

regulators banks and financial institutions have adopted policies and reforms toconverge toward BIS domestic bank regulations and more effective capital marketsupervision

Third the valuation of mortgage backed securities and derivatives created afundamentally new situation once problems appeared in 2007 Data from the SecuritiesIndustry and Financial Markets Association suggest how the value of asset backedsecurities exploded after deregulation Values of outstanding debt and new debt issuedfrom 1996-2008 reveal an abrupt capitalization of mortgage related and asset backedsecurities typical of asset bubbles Longstanding bond markets such as municipal bondstreasury bonds corporate debt federal agency securities money markets and assetbacked bonds all remained on relatively stable growth trajectories until crisis hit in

2007 In comparison the market value of mortgage related bonds almost doubled fromUS$35 trillion in 2000 to reach US$89 trillion before crisis in 2007

8132019 Government Banking and BRICs in the Recent Financial Crisis

httpslidepdfcomreaderfullgovernment-banking-and-brics-in-the-recent-financial-crisis 757

983106983122983113983107 983111983151983158983141983154983150983149983141983150983156 983106983137983150983147983155 983137983150983140 983110983145983150983137983150983139983145983137983148 983123983156983137983156983141983139983154983137983142983156

7

Fourth central drivers of the financial market bubble in the US were secondarymarkets for mortgage backed securities and derivatives For example throughout thefinancial panic and crisis municipal bond markets remained largely stable despitefalling tax receipts and the impact of crisis on sub-national government budgets Thevalue of US Treasury bonds also increased during crisis reflecting a flight to quality

much criticized by surplus countries such as China This remains a comparativeadvantage of market-centered finance capitalism Despite originating crisis a flight toquality cheapens counter cyclical policies Corporate bonds also increased during crisisas US Federal Reserve banks and treasury injected funds to keep US firms afloatFurther analysis is needed However data from bond markets suggest that marketcentered finance capitalism retains particular sets of complementarities and policyalternatives

Fifth both government policies during crisis and proposals for new regulatoryframeworks are designed to tap these complementarities After September 2008 USgovernment reserves increased from US$ 900 billion to over two trillion dollars largelythrough new credit facilities created by the Federal Reserve Board and regional banks of

the Federal Reserve System US government reserves first increased through massiveextension of credit then through central bank swaps then through acquisition of federalgovernment securities by the US central bank These policies suggest particularconfigurations and complementarities in market-centered finance capitalism

The first program introduced in February 2008 was the Federal Reserve PrimaryDealer Credit Facility an overnight loan facility to ensure funds for primary dealers oftreasury securities to sustain demand in financial markets US government primarycredit borrowing increased from under US$200 billion through September 2008 to overUS$1100 billion by December 2008 but decreased thereafter to under US$400 billionby April 2009 US Federal Reserve Banks also purchased massive amounts of assetbacked securities to sustain markets In November 2008 the Federal Deposit InsuranceCorporation created a Temporary Liquidity Guarantee Program one that provided overUS$3340 billion by April 2009 (Given that FDIC funds are taken from charges onsavings accounts this transfer of funds from savings accounts to emergency financialpolicy credits has attracted criticism from community banking association members)US monetary authority purchases of GSE mortgage backed securities also reachedUS$125 trillion in GSE ldquoagencyrdquo mortgage backed securities US$2000 billion indirect agency obligations and permitted purchase of up to US$3000 billion in treasurysecurities during 2009 The Federal Reserve Board also created a Term Asset-BackedSecurities Loan Facility

In September 2008 the Federal Reserve Board created an Asset-Backed

Commercial Paper Money Market Mutual Fund Liquidity Facility to stave off financialpanic Lending through the Federal Reserve Bank of Boston reached US$1500 billionby September 2008 However loans under this program declined to near zero in Apriland remained below US$200 billion in May 2009 The Federal Reserve Board alsocreated a Commercial Paper Funding Facility through the Federal Reserve Bank of NewYork to avert financial panic spreading into commercial paper markets Loans to banksunder this facility reached US$3500 billion in January 2009 but declined to underUS$1400 billion by June 2009 The Federal Reserve Board also created a TermAuction Facility in December 2009 to ensure liquidity in uninsured interbank lendingmarkets Lending through this facility remained at approximately US$1400 billion intoOctober 2008 but increased to almost US$US5000 billion in March 2009 before

declining to an estimated US$ 3200 billion outstanding in June 2009

8132019 Government Banking and BRICs in the Recent Financial Crisis

httpslidepdfcomreaderfullgovernment-banking-and-brics-in-the-recent-financial-crisis 857

8132019 Government Banking and BRICs in the Recent Financial Crisis

httpslidepdfcomreaderfullgovernment-banking-and-brics-in-the-recent-financial-crisis 957

983106983122983113983107 983111983151983158983141983154983150983149983141983150983156 983106983137983150983147983155 983137983150983140 983110983145983150983137983150983139983145983137983148 983123983156983137983156983141983139983154983137983142983156

9

but should not conceal the counter intuitive modernization of government banksalongside (and often ahead) of private and foreign banks

A third explanation draws from the institutional complementarity hypothesis toargue that different policies in BRICS captured particular complementarities in bankingand finance to avert more severe impacts on economic activity This is a promising

approach but one that exceeds our ability to retrace the domestic policies amidst crisisacross four major countriesA fourth explanation is taken from the World Capitalist System approach and

focuses on the profound structural changes implied by recent growth and betteradjustment in BRIC countries This perspective also provides significant opportunitiesfor reflection and interpretation that must remain beyond the scope of this paper Theemergence of BRIC nations as driving force in the global economy is a fundamentallynew situation for theories of center-periphery north-south dependent development andtheories that focus on the specific trajectories of nations in what used to be called latelate development

A final explanation of why BRIC countries have fared comparatively better in

the face of global financial crisis is scale The very large size of these economiesprovided policy options unavailable to smaller countries From this perspective closedeconomies are less subject to the impacts of sudden stops in foreign finance during andafter the financial crisis and less exposed to export declines during global downturnsMoreover large closed BRIC economies retain options of turning away from exportstoward domestic investment and consumption a characteristic especially importantgiven atrocious income distribution and social exclusion This dimension also remainsbeyond the scope of this paper on public banking and domestic financial statecraft

Unless we are mistaken these explanations are complementary to our core claimsthat government banks made a difference in terms of avoiding the creation of asset bubblesrealizing competitive advantages over private and foreign banks since liberalization andproviding counter cyclical policy alternatives to ameliorate downturn Case studies of theBRICs follow

Brazil

We begin with Brazil Our research on Brazil suggests that since price stability the return todemocracy and liberalization of the banking system in 1995 federal banks have realizedcompetitive advantage over private and foreign banks while providing policy alternatives topolitical and social forces This article extends this argument to suggest that these institutionshave modernized amidst liberalization and globalization across BRIC countries ldquojust in timerdquo

to retain client confidence and provide counter-cyclical credit to avert domestic downturns inthe face of global crisis

8132019 Government Banking and BRICs in the Recent Financial Crisis

httpslidepdfcomreaderfullgovernment-banking-and-brics-in-the-recent-financial-crisis 1057

983106983122983113983107 983111983151983158983141983154983150983149983141983150983156 983106983137983150983147983155 983137983150983140 983110983145983150983137983150983139983145983137983148 983123983156983137983156983141983139983154983137983142983156

10

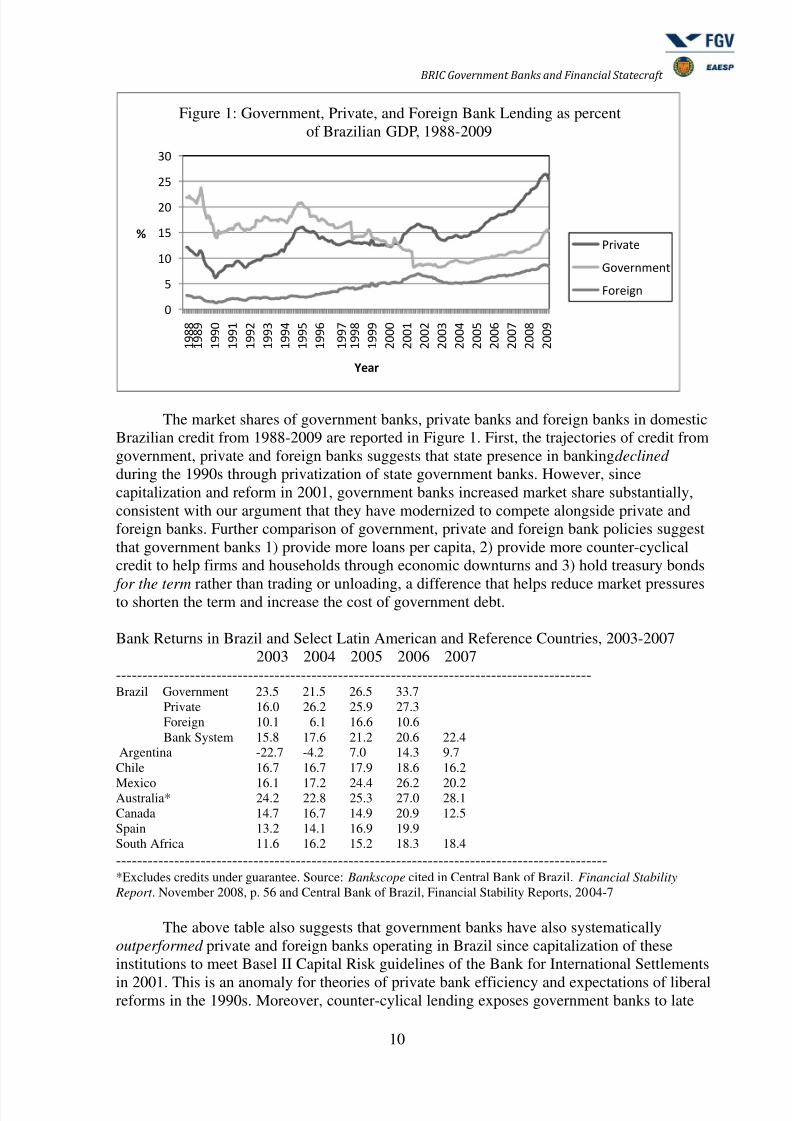

The market shares of government banks private banks and foreign banks in domesticBrazilian credit from 1988-2009 are reported in Figure 1 First the trajectories of credit fromgovernment private and foreign banks suggests that state presence in banking declined during the 1990s through privatization of state government banks However sincecapitalization and reform in 2001 government banks increased market share substantiallyconsistent with our argument that they have modernized to compete alongside private andforeign banks Further comparison of government private and foreign bank policies suggestthat government banks 1) provide more loans per capita 2) provide more counter-cyclicalcredit to help firms and households through economic downturns and 3) hold treasury bonds

for the term rather than trading or unloading a difference that helps reduce market pressuresto shorten the term and increase the cost of government debt

Bank Returns in Brazil and Select Latin American and Reference Countries 2003-20072003 2004 2005 2006 2007

------------------------------------------------------------------------------------------Brazil Government 235 215 265 337

Private 160 262 259 273Foreign 101 61 166 106Bank System 158 176 212 206 224

Argentina -227 -42 70 143 97Chile 167 167 179 186 162

Mexico 161 172 244 262 202Australia 242 228 253 270 281Canada 147 167 149 209 125Spain 132 141 169 199South Africa 116 162 152 183 184---------------------------------------------------------------------------------------------Excludes credits under guarantee Source Bankscope cited in Central Bank of Brazil Financial Stability

Report November 2008 p 56 and Central Bank of Brazil Financial Stability Reports 2004-7

The above table also suggests that government banks have also systematicallyoutperformed private and foreign banks operating in Brazil since capitalization of theseinstitutions to meet Basel II Capital Risk guidelines of the Bank for International Settlements

in 2001 This is an anomaly for theories of private bank efficiency and expectations of liberalreforms in the 1990s Moreover counter-cylical lending exposes government banks to late

983088

983093

983089983088

983089983093

983090983088

983090983093

983091983088

983089 983097 983096 983096

983089 983097 983096 983097

983089 983097 983097 983088

983089 983097 983097 983089

983089 983097 983097 983090

983089 983097 983097 983091

983089 983097 983097 983092

983089 983097 983097 983093

983089 983097 983097 983094

983089 983097 983097 983095

983089 983097 983097 983096

983089 983097 983097 983097

983090 983088 983088 983088

983090 983088 983088 983089

983090 983088 983088 983090

983090 983088 983088 983091

983090 983088 983088 983092

983090 983088 983088 983093

983090 983088 983088 983094

983090 983088 983088 983095

983090 983088 983088 983096

983090 983088 983088 983097

983077

983129983141983137983154

Figure 1 Government Private and Foreign Bank Lending as percent

of Brazilian GDP 1988-2009

983120983154983145983158983137983156983141

983111983151983158983141983154983150983149983141983150983156

983110983151983154983141983145983143983150

8132019 Government Banking and BRICs in the Recent Financial Crisis

httpslidepdfcomreaderfullgovernment-banking-and-brics-in-the-recent-financial-crisis 1157

983106983122983113983107 983111983151983158983141983154983150983149983141983150983156 983106983137983150983147983155 983137983150983140 983110983145983150983137983150983139983145983137983148 983123983156983137983156983141983139983154983137983142983156

11

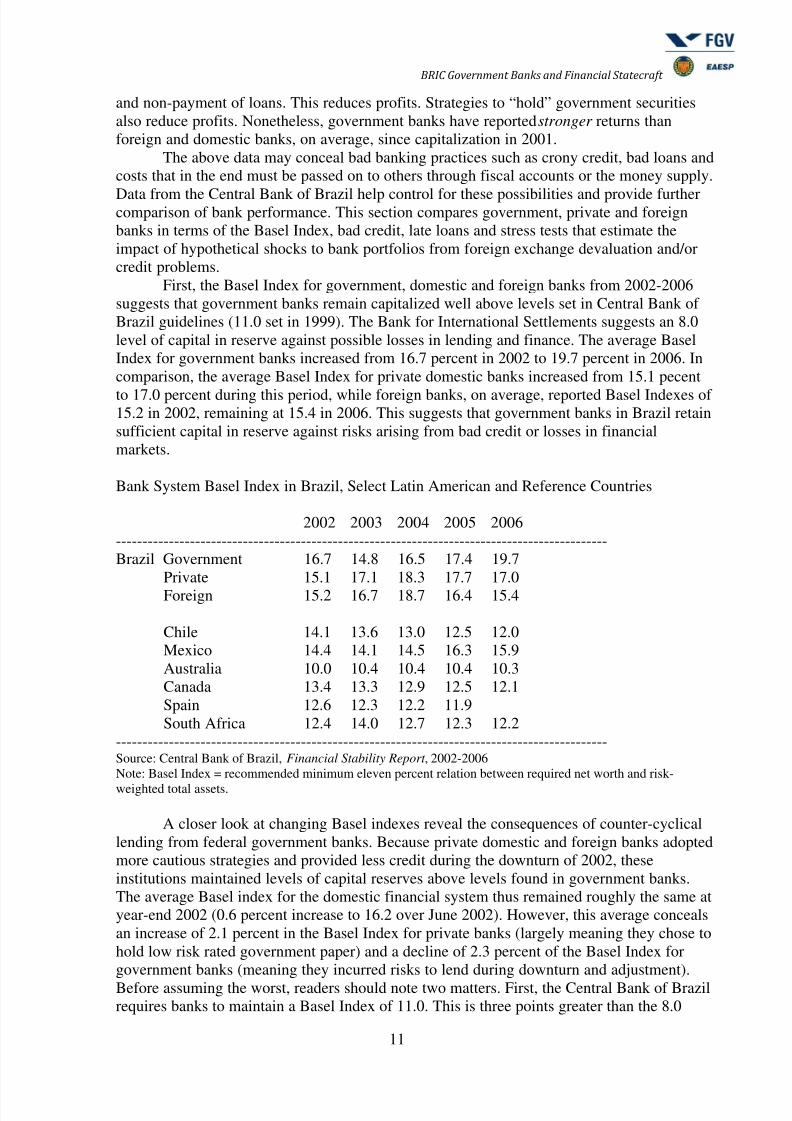

and non-payment of loans This reduces profits Strategies to ldquoholdrdquo government securitiesalso reduce profits Nonetheless government banks have reported stronger returns thanforeign and domestic banks on average since capitalization in 2001

The above data may conceal bad banking practices such as crony credit bad loans andcosts that in the end must be passed on to others through fiscal accounts or the money supply

Data from the Central Bank of Brazil help control for these possibilities and provide furthercomparison of bank performance This section compares government private and foreignbanks in terms of the Basel Index bad credit late loans and stress tests that estimate theimpact of hypothetical shocks to bank portfolios from foreign exchange devaluation andorcredit problems

First the Basel Index for government domestic and foreign banks from 2002-2006suggests that government banks remain capitalized well above levels set in Central Bank ofBrazil guidelines (110 set in 1999) The Bank for International Settlements suggests an 80level of capital in reserve against possible losses in lending and finance The average BaselIndex for government banks increased from 167 percent in 2002 to 197 percent in 2006 Incomparison the average Basel Index for private domestic banks increased from 151 pecent

to 170 percent during this period while foreign banks on average reported Basel Indexes of152 in 2002 remaining at 154 in 2006 This suggests that government banks in Brazil retainsufficient capital in reserve against risks arising from bad credit or losses in financialmarkets

Bank System Basel Index in Brazil Select Latin American and Reference Countries

2002 2003 2004 2005 2006---------------------------------------------------------------------------------------------Brazil Government 167 148 165 174 197

Private 151 171 183 177 170Foreign 152 167 187 164 154

Chile 141 136 130 125 120Mexico 144 141 145 163 159Australia 100 104 104 104 103Canada 134 133 129 125 121Spain 126 123 122 119South Africa 124 140 127 123 122

---------------------------------------------------------------------------------------------Source Central Bank of Brazil Financial Stability Report 2002-2006Note Basel Index = recommended minimum eleven percent relation between required net worth and risk-

weighted total assets

A closer look at changing Basel indexes reveal the consequences of counter-cyclicallending from federal government banks Because private domestic and foreign banks adoptedmore cautious strategies and provided less credit during the downturn of 2002 theseinstitutions maintained levels of capital reserves above levels found in government banksThe average Basel index for the domestic financial system thus remained roughly the same atyear-end 2002 (06 percent increase to 162 over June 2002) However this average concealsan increase of 21 percent in the Basel Index for private banks (largely meaning they chose tohold low risk rated government paper) and a decline of 23 percent of the Basel Index forgovernment banks (meaning they incurred risks to lend during downturn and adjustment)Before assuming the worst readers should note two matters First the Central Bank of Brazilrequires banks to maintain a Basel Index of 110 This is three points greater than the 80

8132019 Government Banking and BRICs in the Recent Financial Crisis

httpslidepdfcomreaderfullgovernment-banking-and-brics-in-the-recent-financial-crisis 1257

983106983122983113983107 983111983151983158983141983154983150983149983141983150983156 983106983137983150983147983155 983137983150983140 983110983145983150983137983150983139983145983137983148 983123983156983137983156983141983139983154983137983142983156

12

suggested in the 1988 Basel Accord and subsequent revisions for capital guidelines In otherwords Brazilian banks set aside almost half again more in additional capital reserves thanlevels recommended by the Bank for International Settlements Second the different BaselIndex ratings of government and private banks also reflects the greater weight of credit andtherefore credit risk in these institutions And data on bad and late loans since 2001 suggest

that the slight and temporarily higher levels of average Basel Indexes reported by governmentbanks do not reflect broader deterioration of portfoliosFurthermore Banks in Brazil and especially government banks tend to be more

conservative setting aside not only frac12 of deposits as compulsory reserves at the Central Bankof Brazil but also retaining additional reserves against bad loans and losses Firstcomparative data suggests that Brazilian banks tend to set considerably larger sums aside inreserve against bad loans and other losses Of the four large Latin American countries andfour further economies reported by the IMF and Central Bank of Brazil Brazil retainedsubstantially larger reserves against bad loans than any country except Spain during 2007This confirms the particular characteristics of banking in Brazil that of a higher cost andlower operating efficiency combined with larger reserves and provisions against losses

Bank Reserves as Percent of Overdue amp Late Loans in Brazil Select Latin American andReference Countries

2003 2004 2005 2006 2007 2008---------------------------------------------------------------------------------------------Brazil 3200 3719 2874 2800 2862 2709Argentina 792 1029 1251 1303 1303Chile 1309 1655 1776 1985 2107Mexico 1671 2018 2321 2074 1947Australia 1318 1829 2030 2052 1889Canada 435 477 493 553 449Spain 2454 2196 2518 2733South Africa 542 613 643---------------------------------------------------------------------------------------------Source IMF Global Financial Stability Report 2008 cited in Central Bank of Brazil Financial Stability

Report November 2008 p 56

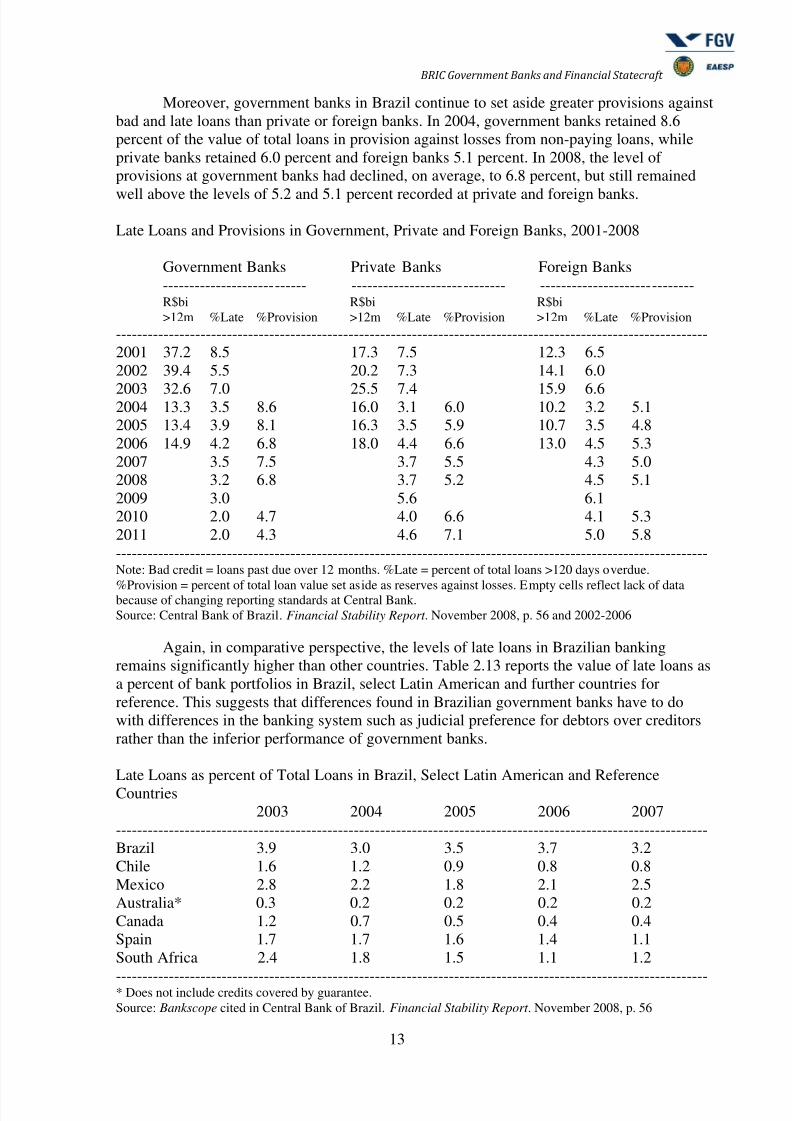

The level of bad and late loans in bank portfolios is another measure of bank solidityThe convergence of bad credit levels in government private and foreign banks from 1988-2008 introduced this study Further comparison suggests that although government banksretain higher levels of bad and late loans in specific sectors (especially home loans) the value

of late loans as a percent of total loans in government banks fell below levels in private andforeign banks during 2008 (See table on following page) The value of bad credit (loans over12 months past due) in government banks decreased from R$372 billion in 2001 to R$149billion in June 2006 This places the value of bad credit in government banks below the valuefound in private and foreign banks Bad credit in private banks increased from R$173 billionin 2001 to peak at R$255 billion during 2003 declining to R$180 billion in 2006 Foreignbanks also reported increased values of bad credit from R$123 billion in 2001 peaking atR$141 billion in 2003 and declining to R$130 billion in 2006 While late loans remained 85percent of total loans in government banks in 2001 (above 75 percent in private and 65percent in foreign banks) by 2008 the relation reverses In 2008 late loans declined to 32percent of total loans at government banks while remaining at 37 percent in private banksand 45 percent in foreign banks

8132019 Government Banking and BRICs in the Recent Financial Crisis

httpslidepdfcomreaderfullgovernment-banking-and-brics-in-the-recent-financial-crisis 1357

983106983122983113983107 983111983151983158983141983154983150983149983141983150983156 983106983137983150983147983155 983137983150983140 983110983145983150983137983150983139983145983137983148 983123983156983137983156983141983139983154983137983142983156

13

Moreover government banks in Brazil continue to set aside greater provisions againstbad and late loans than private or foreign banks In 2004 government banks retained 86percent of the value of total loans in provision against losses from non-paying loans whileprivate banks retained 60 percent and foreign banks 51 percent In 2008 the level ofprovisions at government banks had declined on average to 68 percent but still remained

well above the levels of 52 and 51 percent recorded at private and foreign banks

Late Loans and Provisions in Government Private and Foreign Banks 2001-2008

Government Banks Private Banks Foreign Banks--------------------------- ----------------------------- -----------------------------R$bi R$bi R$bigt12m Late Provision gt12m Late Provision gt12m Late Provision

----------------------------------------------------------------------------------------------------------------2001 372 85 173 75 123 652002 394 55 202 73 141 60

2003 326 70 255 74 159 662004 133 35 86 160 31 60 102 32 512005 134 39 81 163 35 59 107 35 482006 149 42 68 180 44 66 130 45 532007 35 75 37 55 43 502008 32 68 37 52 45 512009 30 56 612010 20 47 40 66 41 532011 20 43 46 71 50 58----------------------------------------------------------------------------------------------------------------Note Bad credit = loans past due over 12 months Late = percent of total loans gt120 days overdue

Provision = percent of total loan value set aside as reserves against losses Empty cells reflect lack of databecause of changing reporting standards at Central BankSource Central Bank of Brazil Financial Stability Report November 2008 p 56 and 2002-2006

Again in comparative perspective the levels of late loans in Brazilian bankingremains significantly higher than other countries Table 213 reports the value of late loans asa percent of bank portfolios in Brazil select Latin American and further countries forreference This suggests that differences found in Brazilian government banks have to dowith differences in the banking system such as judicial preference for debtors over creditorsrather than the inferior performance of government banks

Late Loans as percent of Total Loans in Brazil Select Latin American and ReferenceCountries

2003 2004 2005 2006 2007----------------------------------------------------------------------------------------------------------------Brazil 39 30 35 37 32Chile 16 12 09 08 08Mexico 28 22 18 21 25Australia 03 02 02 02 02Canada 12 07 05 04 04Spain 17 17 16 14 11South Africa 24 18 15 11 12

---------------------------------------------------------------------------------------------------------------- Does not include credits covered by guaranteeSource Bankscope cited in Central Bank of Brazil Financial Stability Report November 2008 p 56

8132019 Government Banking and BRICs in the Recent Financial Crisis

httpslidepdfcomreaderfullgovernment-banking-and-brics-in-the-recent-financial-crisis 1457

983106983122983113983107 983111983151983158983141983154983150983149983141983150983156 983106983137983150983147983155 983137983150983140 983110983145983150983137983150983139983145983137983148 983123983156983137983156983141983139983154983137983142983156

14

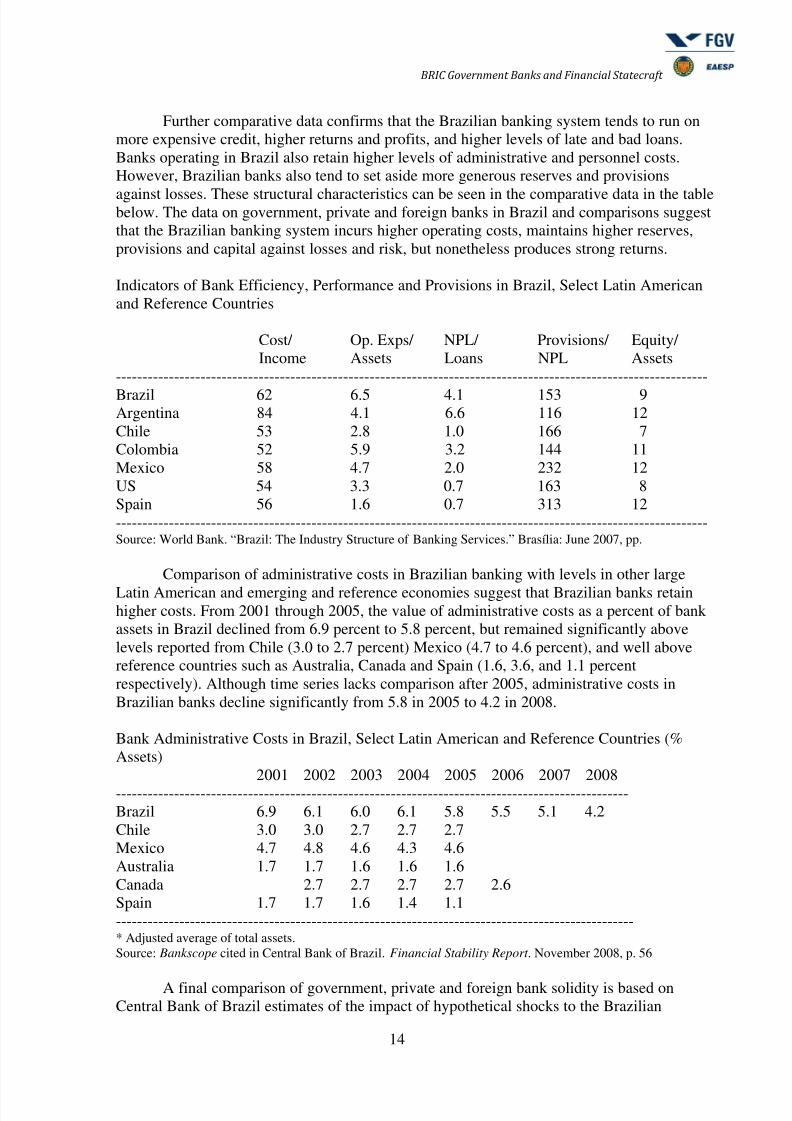

Further comparative data confirms that the Brazilian banking system tends to run onmore expensive credit higher returns and profits and higher levels of late and bad loansBanks operating in Brazil also retain higher levels of administrative and personnel costsHowever Brazilian banks also tend to set aside more generous reserves and provisions

against losses These structural characteristics can be seen in the comparative data in the tablebelow The data on government private and foreign banks in Brazil and comparisons suggestthat the Brazilian banking system incurs higher operating costs maintains higher reservesprovisions and capital against losses and risk but nonetheless produces strong returns

Indicators of Bank Efficiency Performance and Provisions in Brazil Select Latin Americanand Reference Countries

Cost Op Exps NPL Provisions EquityIncome Assets Loans NPL Assets

----------------------------------------------------------------------------------------------------------------

Brazil 62 65 41 153 9Argentina 84 41 66 116 12Chile 53 28 10 166 7Colombia 52 59 32 144 11Mexico 58 47 20 232 12US 54 33 07 163 8Spain 56 16 07 313 12----------------------------------------------------------------------------------------------------------------Source World Bank ldquoBrazil The Industry Structure of Banking Servicesrdquo Brasiacutelia June 2007 pp

Comparison of administrative costs in Brazilian banking with levels in other large

Latin American and emerging and reference economies suggest that Brazilian banks retainhigher costs From 2001 through 2005 the value of administrative costs as a percent of bankassets in Brazil declined from 69 percent to 58 percent but remained significantly abovelevels reported from Chile (30 to 27 percent) Mexico (47 to 46 percent) and well abovereference countries such as Australia Canada and Spain (16 36 and 11 percentrespectively) Although time series lacks comparison after 2005 administrative costs inBrazilian banks decline significantly from 58 in 2005 to 42 in 2008

Bank Administrative Costs in Brazil Select Latin American and Reference Countries (Assets)

2001 2002 2003 2004 2005 2006 2007 2008-------------------------------------------------------------------------------------------------Brazil 69 61 60 61 58 55 51 42Chile 30 30 27 27 27Mexico 47 48 46 43 46Australia 17 17 16 16 16Canada 27 27 27 27 26Spain 17 17 16 14 11-------------------------------------------------------------------------------------------------- Adjusted average of total assetsSource Bankscope cited in Central Bank of Brazil Financial Stability Report November 2008 p 56

A final comparison of government private and foreign bank solidity is based onCentral Bank of Brazil estimates of the impact of hypothetical shocks to the Brazilian

8132019 Government Banking and BRICs in the Recent Financial Crisis

httpslidepdfcomreaderfullgovernment-banking-and-brics-in-the-recent-financial-crisis 1557

983106983122983113983107 983111983151983158983141983154983150983149983141983150983156 983106983137983150983147983155 983137983150983140 983110983145983150983137983150983139983145983137983148 983123983156983137983156983141983139983154983137983142983156

15

economy on domestic banks These estimates are based on the revisions of the widely usedValue-at-Risk estimates proposed by Boudoukh Richardson and Whitelaw that adapts theoriginal VaR method developed and commercialised by JP Morgan19

Stress Tests for Impact of Credit Interest Rate and Foreign Exchange Shock on Basel Index

Comparison of Government Domestic and Foreign Banks 2001-2006

2002 2003 2004 2005 2006-------------------------------------------------------------------------------------------------------------

Government 112 104 114 113 109Domestic 112 132 126 121 103Private 103 131 135 108 84-------------------------------------------------------------------------------------------------------------Source Central Bank of Brazil Financial Stability Reports 2002-2006Note Basel Index = Capital risk guideline measure defined by Bank for International Settlements BaselCommittee that recommends 8 percent relation between PR and total assets weighted by risk level Since 2002Central Bank of Brazil minimum requirements of Basel Index remains 11 percent For methods of calculationsee Central Bank of Brazil Financial Stability Report Brasilia 2006 p 76

Central Bank of Brazil tests estimate that in the face of foreign currency valuationand interest rate shock government banks would nonetheless remain at or slightly below thecapital requirements against credit risk recommended by the central bank Again it should benoted that Basel Index levels recommended in the BIS Capital Requirements guidelines forthe Basel Index of banks are 80 while the Central Bank of Brazil has set minimum BaselIndex levels of 110 Given that federal government bank portfolios include more credit thanprivate banks and especially foreign banks the estimate of a shift to 109 in the averageBasle index for federal government banks in the face of a credit shock provides furtherevidence that these financial institutions are solid and their capital reserves sufficient Insum comparison of results for government private and foreign banks in the estimatesreported by the Central Bank of Brazil of the likely impact of a shock to the Brazilianeconomy in terms of interest rates and foreign exchange rates also suggests that governmentbanks appear solid The average Basel Index reported for government banks in this stress testwas 135 above the 110 Central Bank of Brazil guideline and well above the 80 levelsuggested by the BIS

Understanding the capacity of Brazilian banks to cope with shocks and risk is not justa theoretical exercise Since the currency crisis in Mexico during 1994-1995 the newlystabilized currency was tested by shocks from home and abroad Policies first dramaticallyincreased interest rates under a fixed exchange rate regime then freed the real to devalue

under a flexible foreign exchange rate regime in January 1999 The Asian currency crisesduring second semester 1997 led the Central Bank of Brazil to increase benchmark Selicinterest rates to 434 percent in November In August 1998 the declaration of moratorium onforeign debt payments by Russia the central bank to once again increase Selic interest ratesfrom 20 to 40 percent under the fixed exchange rate regime by November of that year Theseshocks from abroad coincided with preparations for national elections during 1998 leadingthe IMF and other official creditors to provide strong support for the Brazilan governmentNonetheless by January 1999 (after the election) market pressure led to the abandonment ofthe fixed foreign exchange rate regime that had served as nominal anchor for economic

19 Calculation first published in Resenha BMampF Vol 122 1998 (described in Central Bank of Brazil

Financial Stability Report 2002 amp 2003 then as Boudoukh Jacob Matthew Richardson RichardStanton amp Robert Whitelaw ldquoMaxVaR Long Horizon Value at Risk in a Mark-to-Market Environmentrdquo Journal of Investment Management 2004Vol 2 No 3 pp 14-19

8132019 Government Banking and BRICs in the Recent Financial Crisis

httpslidepdfcomreaderfullgovernment-banking-and-brics-in-the-recent-financial-crisis 1657

983106983122983113983107 983111983151983158983141983154983150983149983141983150983156 983106983137983150983147983155 983137983150983140 983110983145983150983137983150983139983145983137983148 983123983156983137983156983141983139983154983137983142983156

16

policy since 1994 The real quickly devalued from 121 to 20 against the US dollar by theend of January and led to considerable changes in policy (a flexible foreign exhange rateregime inflation targeting and the implementation of further fiscal reforms) Once the realrevalued from R$22 against the dollar in March to R$166 in April 1999 the governmentmoved to consolidate this new triad of economic policies Since 1999 flexible foreign

exchange markets inflation targeting and fiscal reform have remained in place This suggeststhat Brazilian banks have weathered volatile parameters and large risks during a markedpolitical business cycle One involving the transition from reformist President Cardoso to PTPresident Lula Since recovery of the economy during 2004 the coalition government underPT President Lula has sought to expand the contribution of government banks to accelerategrowth and social inclusion These policies have not undermined economic fundamentals oreroded the institutional foundations of comparative advantage retained by Brazilian federalgovernment banks

In sum the advances of Brazilian banking toward Basel Accord regulations during the1990s and 2000s the adoption of more transparent and timely reporting standards and themodernization of government banks under pressures from liberalization placed federal banks

in a new situation in the face of crisis once it hit the country in 2008 A closer look at the bigthree federal government banks is in order to better understand these changes

The Banco do Brasil

Upon taking office in 2003 President Lula retained the central economic policies of theCardoso administration such as inflation targeting tight fiscal and monetary policy andthe operational independence of the Banco do Brasil However the recovery of investorconfidence during 2003 and the return of stronger growth levels during 2004 led to aperiod of what the Central Bank of Brazil describes as organic growth at the Banco doBrasil From 2004-2008 the Banco do Brasil contributed to the deepning of domesticcredit markets and emerged as leading investment bank at the Bovespa stock marketFurthermore once the Bovespa collapsed credit became short and a sharp downturnensued during 2008 the Banco do Brasil provided emergency loans infusions of capitalthrough stock purchases and the acquisition of small and mid-sized firms and banksunable to weather the sharp decline and lack of credit Although the merger of Itauacute andUnibanco in 2008 displaced the Banco do Brasil as the largest financial institution inLatin America the bank retains powerful institutional foundations of comparativeadvantage and networks that cross Brazilian society politics and markets

The Banco do Brasil also remains at the center of Brazilian politics and policydisputes Indeed leaders of the PT party faction articulaccedilatildeo (articulation) includes

career employees of the Banco do Brasil and presidents of the Brazilian bank workersunion such as Luiz Gushiken and Ricardo Berzioni Both were nominated to ministerialposts by President Silva in January 2003 By August 2003 21 of 33 top positions at theBanco do Brasil had been filled by new representatives of the PT most Banco do Brasilemployees and members of the Brazilian bank workers union Critics decriedpoliticization However the resistance of bank representatives described above topresidential appeals to increase credit during 2003 was followed by more neutralappointments during 2004 When Banco do Brasil President Cassio Casseb Limaresigned in November 2004 (under charges of irregularities in consulting contracts atthe bank) President Lula nominated Rossano Maranhatildeo Pinto a career employee andBanco do Brasil vice president to head the bank Further appointments of PMDB

political leaders to cement support for the PT coalition government were also criticizedas politicization of the bank However Banco do Brasil officials responded that these

8132019 Government Banking and BRICs in the Recent Financial Crisis

httpslidepdfcomreaderfullgovernment-banking-and-brics-in-the-recent-financial-crisis 1757

983106983122983113983107 983111983151983158983141983154983150983149983141983150983156 983106983137983150983147983155 983137983150983140 983110983145983150983137983150983139983145983137983148 983123983156983137983156983141983139983154983137983142983156

17

experienced political leaders of the PMDB brought competitive advantages to the bankbased on their networks that cross the public and private sector These networks andrelations during the second PT coalition government of President Lula also appearsdifferent than the first given the departure from core offices of the presency bylongtime advisors to Lula that came from the Banco do Brasil and bank workers union

By late 2006 only one of seven vice presidents of the Banco do Brasil was a member ofPresident Lulaacutes Workersacute Party (PT)Again Banco do Brasil policies and growth since recovery of the economy in

2004 involved first a period of expansion during four years of growth followed by aturn to counter cyclical lending and finance once financial crisis abroad produced first asevere contraction in credit supply then a sharp economic downturn in fourth quarter2008 Institutional foundations of comparative advantage are behind Banco do Brasilpolicies during both periods First the capitalization of Brazilian firms on the Bovespastock market is closely related to the groups that cross politics government banks thepowerful bank worker labor union the Banco do Brasil employee private pension fundand bank consortia often led by the Banco do Brasil investment banking division (often

joined by the BNDESpar and Caixa investment banking division) Recent developmentsare complex and will require further research However rather than convergence towardprivate banking and a market-centered financial system examination of Banco do Brasilpolicies and market shares during the 2000s suggests that federal government banks notonly remain at the center of politics policy and development strategies but that theseinstitutions have modernized to compete against private and foreign banks

The large scale and scope of the Banco do Brasil has permitted use of the bankfor counter-cyclical lending and leadership in capital markets without deteriorating bankbalance sheets Since 2003 the Banco do Brasil has remained well within domesticbank regulations and Basel Accord guidelines During 2002 and 2003 reforms at theBanco do Brasil sought to reduce costs and increase efficiency ratings Indeed therelation between the Banco do Brasil and President Lula reversed past patterns In the1950s conflicts were between national developmentalist groups at the Banco do Brasiland more orthodox Ministers of Finance In 2003 and once again during the 2008financial crisis differences between President Lula and the Banco do Brasil were thereverse Banco do Brasil management refused to dramatically increase loans in 2003and resisted requests to reduce the price of credit in 2008 In 2003 the caution imposedby political risk perceptions led President Lula to respect the operational autonomy ofthe Banco do Brasil In April 2009 Banco do Brasil President Antonio Francisco deLima Neto was fired after refusing to reduce interest rates on loans This reversal ofpolicy positions from the 1950s suggests in a broader sense a transition from the

macroeconomics of populism to the microeconomics of government banking in the 21

st

century Government banks do not provide easy or all solutions Instead credit andfinance policies are subject to market discipline credit risk analysis and the realities ofbusiness cycles

Review of the Banco do Brasilrsquos balance sheet from 2002-2008 suggests that the bankdeveloped organically from 2002-2007 with gradual increases reflecting the competitiveadvantages at the top of Brazilian banking and finance Policies changed during 2007 and2008 as the credit shortage caused by international financial crisis led to the Banco do Brasilassuming once again lending of last resort functions by extending interbank investments andloans to small and medium sized banks to avert further declines in domestic liquidity TheBanco do Brasil also acquired a 51 percent stake in the Votarantim bank to avert a run on

deposits and possible failure while acquiring Satildeo Paulo state government savings bankNossa Caixa for R$76 billion in 2008 These acquisitions reflect concern about the

8132019 Government Banking and BRICs in the Recent Financial Crisis

httpslidepdfcomreaderfullgovernment-banking-and-brics-in-the-recent-financial-crisis 1857

983106983122983113983107 983111983151983158983141983154983150983149983141983150983156 983106983137983150983147983155 983137983150983140 983110983145983150983137983150983139983145983137983148 983123983156983137983156983141983139983154983137983142983156

18

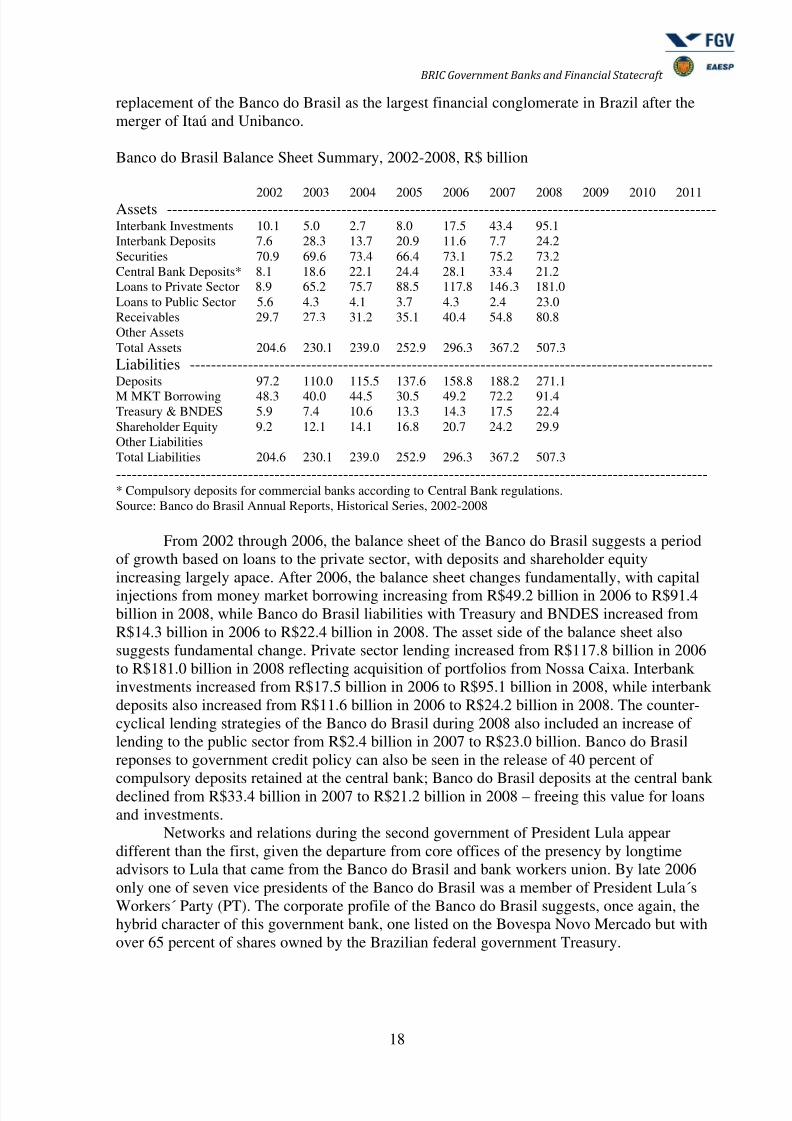

replacement of the Banco do Brasil as the largest financial conglomerate in Brazil after themerger of Itauacute and Unibanco

Banco do Brasil Balance Sheet Summary 2002-2008 R$ billion

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011Assets --------------------------------------------------------------------------------------------------------Interbank Investments 101 50 27 80 175 434 951Interbank Deposits 76 283 137 209 116 77 242Securities 709 696 734 664 731 752 732Central Bank Deposits 81 186 221 244 281 334 212Loans to Private Sector 89 652 757 885 1178 1463 1810Loans to Public Sector 56 43 41 37 43 24 230Receivables 297 273 312 351 404 548 808Other AssetsTotal Assets 2046 2301 2390 2529 2963 3672 5073Liabilities ---------------------------------------------------------------------------------------------------Deposits 972 1100 1155 1376 1588 1882 2711

M MKT Borrowing 483 400 445 305 492 722 914Treasury amp BNDES 59 74 106 133 143 175 224Shareholder Equity 92 121 141 168 207 242 299Other LiabilitiesTotal Liabilities 2046 2301 2390 2529 2963 3672 5073---------------------------------------------------------------------------------------------------------------- Compulsory deposits for commercial banks according to Central Bank regulationsSource Banco do Brasil Annual Reports Historical Series 2002-2008

From 2002 through 2006 the balance sheet of the Banco do Brasil suggests a periodof growth based on loans to the private sector with deposits and shareholder equityincreasing largely apace After 2006 the balance sheet changes fundamentally with capitalinjections from money market borrowing increasing from R$492 billion in 2006 to R$914billion in 2008 while Banco do Brasil liabilities with Treasury and BNDES increased fromR$143 billion in 2006 to R$224 billion in 2008 The asset side of the balance sheet alsosuggests fundamental change Private sector lending increased from R$1178 billion in 2006to R$1810 billion in 2008 reflecting acquisition of portfolios from Nossa Caixa Interbankinvestments increased from R$175 billion in 2006 to R$951 billion in 2008 while interbankdeposits also increased from R$116 billion in 2006 to R$242 billion in 2008 The counter-cyclical lending strategies of the Banco do Brasil during 2008 also included an increase oflending to the public sector from R$24 billion in 2007 to R$230 billion Banco do Brasilreponses to government credit policy can also be seen in the release of 40 percent of

compulsory deposits retained at the central bank Banco do Brasil deposits at the central bankdeclined from R$334 billion in 2007 to R$212 billion in 2008 ndash freeing this value for loansand investments

Networks and relations during the second government of President Lula appeardifferent than the first given the departure from core offices of the presency by longtimeadvisors to Lula that came from the Banco do Brasil and bank workers union By late 2006only one of seven vice presidents of the Banco do Brasil was a member of President LulaacutesWorkersacute Party (PT) The corporate profile of the Banco do Brasil suggests once again thehybrid character of this government bank one listed on the Bovespa Novo Mercado but withover 65 percent of shares owned by the Brazilian federal government Treasury

8132019 Government Banking and BRICs in the Recent Financial Crisis

httpslidepdfcomreaderfullgovernment-banking-and-brics-in-the-recent-financial-crisis 1957

8132019 Government Banking and BRICs in the Recent Financial Crisis

httpslidepdfcomreaderfullgovernment-banking-and-brics-in-the-recent-financial-crisis 2057

983106983122983113983107 983111983151983158983141983154983150983149983141983150983156 983106983137983150983147983155 983137983150983140 983110983145983150983137983150983139983145983137983148 983123983156983137983156983141983139983154983137983142983156

20

customers in 2008 reached 479 million with the bank retaining 39700 AMTs and 766million bank cards (239 million credit cards and 527 million debit cards) Like the CaixaEconocircmica Federal the Banco do Brasil also processes government payments withretirement and social security payments numbering 745 million transactions during 2008Although this implies administrative costs (and receipts) this also brings customers and

prospective customers into Banco do Brasil branch officesDuring 2008 the Banco do Brasil continued to expand operations form jointventures acquire private and government banks and modernize operations A secondaryoffering of stock in January 2008 granting of shares by VISA to the Banco do Brasil andupgrading of the bank to investment grade BB- by Standard amp Poors in April 2008 suggestthat market orientation of the bank continues during the Lula administration despite counter-cyclical credit policies A Lower Income Segment Department was also created to assumeBanco Popular do Brasil operations along with correspondent banking relations and regionalsustainable development programs The Banco do Brasil also received permission to usesavings accounts for home loans enabling the bank to compete on level ground with CaixaEconocircmica Federal During 2008 the Banco do Brasil also acquired the state government

banks Banco do Piaui Banco de Santa Catarina (33rd largest bank in Brazil with US$30billion assets at year end 2007) and Satildeo Paulo government savings bank Nossa Caixa (12thlargest Bank in Brazil with US$267 billion in assets at year end 2007) In sum the diversecorporate divisions and financial operations of the Banco do Brasil provided policy optionsduring 2008 to counter the credit shortage and help firms and domestic banks to adjust

Banco do Brasil and Private Bank Returns and Capital Adequacy 2002-2009

Basel Index Return on Assets Return on Liquid Assets----------------------------- ----------------------------- -----------------------------BB Itauacute Bradesco BB Itauacute Bradesco BB Itauacute Bradesco

--------------------------------------------------------------------------------------------------------------2002 122 184 179 12 26 20 302 288 2832003 137 198 199 11 28 16 231 297 2282004 152 206 188 13 30 23 240 292 3092005 171 170 173 12 37 26 187 353 2842006 173 171 188 28 31 25 267 288 2632007 156 179 156 14 32 22 222 321 2442008 152 161 169 25 19 16 304 221 2112009 150 165 166 12 13 14 238 182 195-------------------------------------------------------------------------------------------------------------- Annualized first quarter 2009 resultsSource Banco do Brasil Itauacute and Bradesco Annual Reports 2002-2009

Comparison of Banco do Brasil returns and capital adequacy with the two majorprivate Brazilian banks Itauacute and Bradesco suggests that the performance and solidity of theBanco do Brasil remains equal or superior to private banks During 2002 and 2003 thecapital adequacy of the Banco do Brasil and return on assets remained below levels reportedby the two largest Brazilian private banks suggesting the impact of counter-cyclical lendingHowever after 2004 the Basel index of the Banco do Brasil reached 171 far above BISstandards of 80 and Central Bank of Brazil requirements of 110 Furthermore from 2006through first quarter 2009 returns on assets returns on liquid assets and the Basel index ofthe Banco do Brasil exceed levels reported by Itauacute and Bradesco In sum despite providingcounter cyclical credit and despite having been replaced by the Itau-Unibanco merger as the

8132019 Government Banking and BRICs in the Recent Financial Crisis

httpslidepdfcomreaderfullgovernment-banking-and-brics-in-the-recent-financial-crisis 2157

983106983122983113983107 983111983151983158983141983154983150983149983141983150983156 983106983137983150983147983155 983137983150983140 983110983145983150983137983150983139983145983137983148 983123983156983137983156983141983139983154983137983142983156

21

largest Brazilian bank the performance and capital adequacy of the Banco do Brasil remainsat or above levels reported by the two largest private banks

In sum since liberalization of banking and finance and privatization of stategovernment banks during the 1990s the Banco do Brasil has been transformed from directstate owned bank into one of two very large financial conglomerates that dominate domestic

banking in Brazil Instead of retaining easy access to funds at Treasury to cover losses theBanco do Brasil has adopted international corporate governance standards to become listedon the Bovespa Novo Mercado and retains an important role in virtually every aspect ofBrazilian banking and finance Although sale of shares in the 1990s were designed to transfercorporate governance and control of the national bank to the private sector the federalgovernment retains 65 percent of stocks after two sale of stocks capitalized the bank duringthe 2000s The massive size and wide scope of Banco do Brasil networks across bankingfinancial markets political and social forces and business have led the bank to realize recordprofits during the period of growth from 2004-2008 and provide counter-cyclical credit toavert a further decline in industrial activity and the economy as the US and global financialcrisis hit Brazil first with a 50 percent decline in the Bovespa stock market and credit

shortage followed by a steep but short decline in industrial production in late 2008 Thetransparency of Banco do Brasil quarterly reports and advances in Central Bank of Brazilsupervision of domestic banking clarify the new tensions that have emerged during the PTgovernment of President Lula These tensions reflect the modernization and competitiveadvantages of the Banco do Brasil

Caixa Econocircmica Federal (Federal Savings Bank Caixa)

The third largest domestic bank the wholly government owned Federal Savings Bank Caixawas also called on by President Lula during the recent financial crisis to increase the pace ofgrowth provide counter cyclical credit during downturns and to reduce consumer andcorporate interest rates and bank spreads Review of balance sheets and policies since 2001suggest that the Caixa retains its core business in urban development home loans real estatetransfer of funds for government programs and services and lottery administration Howeverinvestment banking management of third party funds and the creation of of new products andservices have both increased profits and increased popular access to banking and socialservices The bank has recorded record profits since R$108 billion (2002) R$16 billion(2003) and R$14 billion (2004) The Caixa became the fourth largest Brazilian investmentbank by 2003 while gaining dealer status from the Central Bank of Brazil in primary andsecondary markets for government securities At year-end 2003 the bank retained anestimated R$767 billion of government paper (over ten percent of government paper) in its

portfolio assets earning over R$135 billion that year Since recovery of the Brazilianeconomy in 2004 the Caixa has reported strong profits and continued to improve thestructure of its balance sheet and converge toward international bank reporting standards

In terms of assets deposit base and the number of employees and branches the datasuggest that the Caixa has emerged from a process of rationalization and downsizing duringthe late 1990s and expanded ldquoorganicallyrdquo since capitalization in 2001 Assets declined fromover US$999 billion in 1997 to US$363 billion in 2002 after reorganization andcapitalization Deposits also declined from US$541 billion in 1997 to US$216 billion in2002 The number of employees and branches declined from 104253 and 2316 to 98971 and1803 respectively but returned to 104934 and 2428 by 2006 After reorganization andcapitalization in June 2001 Basel indexes and the ratio of fixed assets over equity indicate

substantial reform and transition toward international banking standards The Basel Index thatmeasures the adequacy of capital reserves against possible losses and risks increased from

8132019 Government Banking and BRICs in the Recent Financial Crisis

httpslidepdfcomreaderfullgovernment-banking-and-brics-in-the-recent-financial-crisis 2257

983106983122983113983107 983111983151983158983141983154983150983149983141983150983156 983106983137983150983147983155 983137983150983140 983110983145983150983137983150983139983145983137983148 983123983156983137983156983141983139983154983137983142983156

22

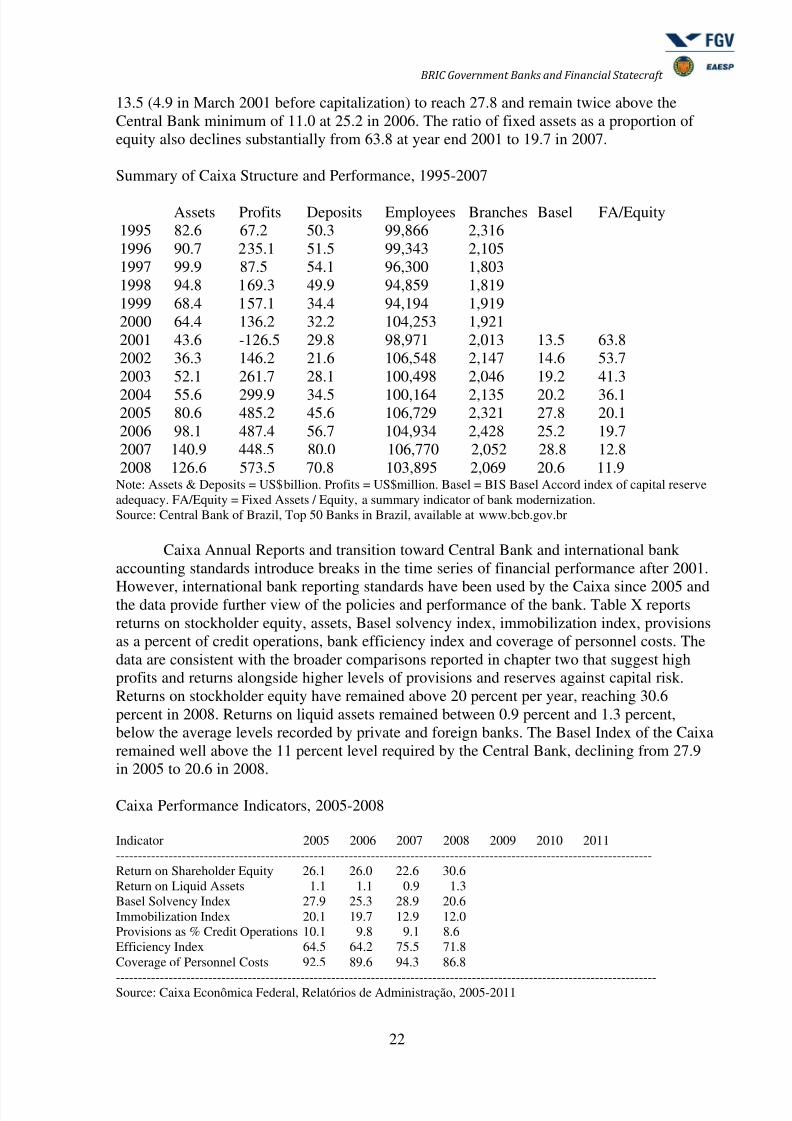

135 (49 in March 2001 before capitalization) to reach 278 and remain twice above theCentral Bank minimum of 110 at 252 in 2006 The ratio of fixed assets as a proportion ofequity also declines substantially from 638 at year end 2001 to 197 in 2007

Summary of Caixa Structure and Performance 1995-2007

Assets Profits Deposits Employees Branches Basel FAEquity1995 826 672 503 99866 23161996 907 2351 515 99343 21051997 999 875 541 96300 18031998 948 1693 499 94859 18191999 684 1571 344 94194 19192000 644 1362 322 104253 19212001 436 -1265 298 98971 2013 135 6382002 363 1462 216 106548 2147 146 5372003 521 2617 281 100498 2046 192 413

2004 556 2999 345 100164 2135 202 3612005 806 4852 456 106729 2321 278 2012006 981 4874 567 104934 2428 252 1972007 1409 4485 800 106770 2052 288 1282008 1266 5735 708 103895 2069 206 119

Note Assets amp Deposits = US$billion Profits = US$million Basel = BIS Basel Accord index of capital reserveadequacy FAEquity = Fixed Assets Equity a summary indicator of bank modernizationSource Central Bank of Brazil Top 50 Banks in Brazil available at wwwbcbgovbr

Caixa Annual Reports and transition toward Central Bank and international bankaccounting standards introduce breaks in the time series of financial performance after 2001

However international bank reporting standards have been used by the Caixa since 2005 andthe data provide further view of the policies and performance of the bank Table X reportsreturns on stockholder equity assets Basel solvency index immobilization index provisionsas a percent of credit operations bank efficiency index and coverage of personnel costs Thedata are consistent with the broader comparisons reported in chapter two that suggest highprofits and returns alongside higher levels of provisions and reserves against capital riskReturns on stockholder equity have remained above 20 percent per year reaching 306percent in 2008 Returns on liquid assets remained between 09 percent and 13 percentbelow the average levels recorded by private and foreign banks The Basel Index of the Caixaremained well above the 11 percent level required by the Central Bank declining from 279in 2005 to 206 in 2008

Caixa Performance Indicators 2005-2008

Indicator 2005 2006 2007 2008 2009 2010 2011--------------------------------------------------------------------------------------------------------------------------Return on Shareholder Equity 261 260 226 306Return on Liquid Assets 11 11 09 13Basel Solvency Index 279 253 289 206Immobilization Index 201 197 129 120Provisions as Credit Operations 101 98 91 86Efficiency Index 645 642 755 718Coverage of Personnel Costs 925 896 943 868

---------------------------------------------------------------------------------------------------------------------------Source Caixa Econocircmica Federal Relatoacuterios de Administraccedilatildeo 2005-2011

8132019 Government Banking and BRICs in the Recent Financial Crisis

httpslidepdfcomreaderfullgovernment-banking-and-brics-in-the-recent-financial-crisis 2357

983106983122983113983107 983111983151983158983141983154983150983149983141983150983156 983106983137983150983147983155 983137983150983140 983110983145983150983137983150983139983145983137983148 983123983156983137983156983141983139983154983137983142983156

23

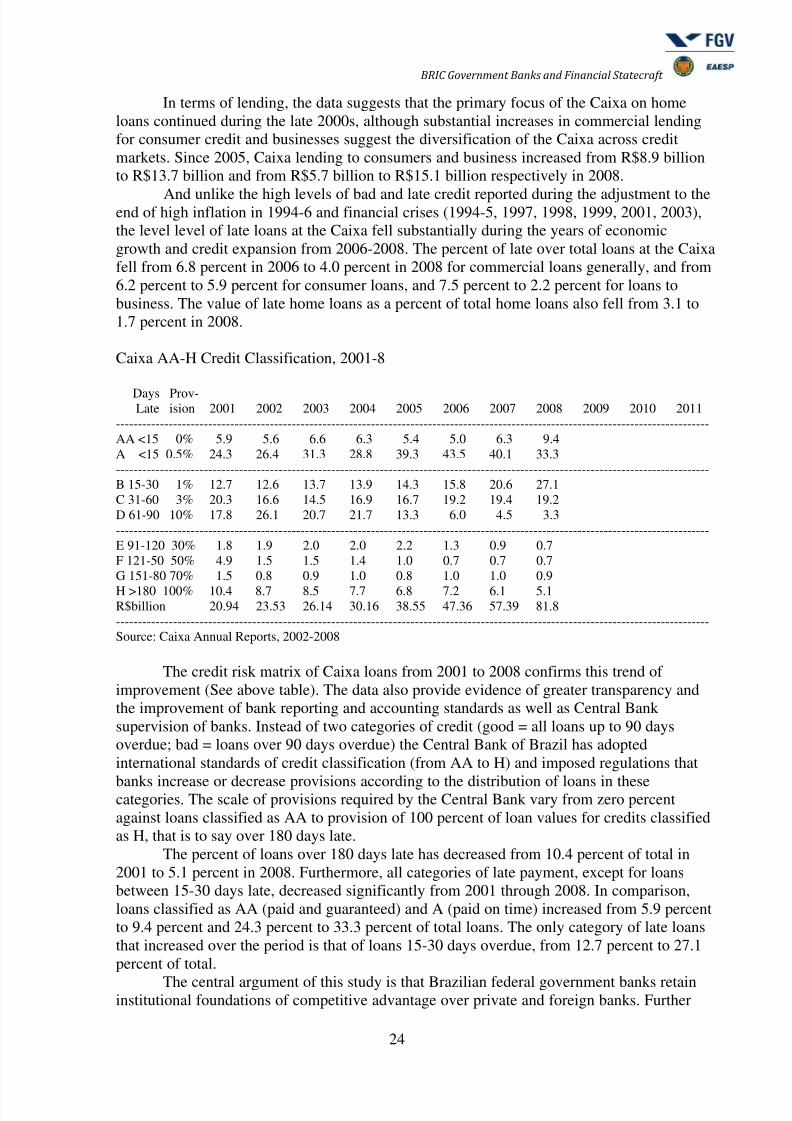

The immobilization index of the Caixa also declined from 201 percent in 2005 to120 percent in 2008 suggesting transition toward standard levels of international bankingHowever the value of provisions as a percent of credit operations remains much higher thaninternational bank practices albeit declining from 101 percent in 2005 to 86 percent in2008 Finally both the substantial increase in efficiency index from 645 to 718 percent