Goldman Sachs European Financials Conference 2007 · Goldman Sachs European Financials Conference...

21

Goldman Sachs – European Financials Conference 2007 Lisbon June 14, 2007 Renato Fassbind Chief Financial Officer

Transcript of Goldman Sachs European Financials Conference 2007 · Goldman Sachs European Financials Conference...

Goldman Sachs –European FinancialsConference 2007

LisbonJune 14, 2007

Renato FassbindChief Financial Officer

Goldman Sachs European Financials Conference 2007Slide 2

Cautionary statement

Cautionary statement regarding forward-looking and non-GAAP information

This presentation contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995.

Forward-looking statements involve inherent risks and uncertainties, and we might not be able to achieve the predictions, forecasts, projections and other outcomes we describe or imply in forward-looking statements.

A number of important factors could cause results to differ materially from the plans, objectives, expectations, estimates and intentions we express in these forward-looking statements, including those we identify in "Risk Factors" in our Annual Report on Form 20-F for the fiscal year ended December 31, 2006 filed with the US Securities and Exchange Commission, and in other public filings and press releases.

We do not intend to update these forward-looking statements except as may be required by applicable laws.

This presentation contains non-GAAP financial information. Information needed to reconcile such non-GAAP financial information to the most directly comparable measures under GAAP can be found in Credit Suisse Group's first quarter report 2007.

Goldman Sachs European Financials Conference 2007Slide 3

Agenda

Improving Operating Performance

Platform for Growth

Managing Risk and Capital

Goldman Sachs European Financials Conference 2007Slide 4

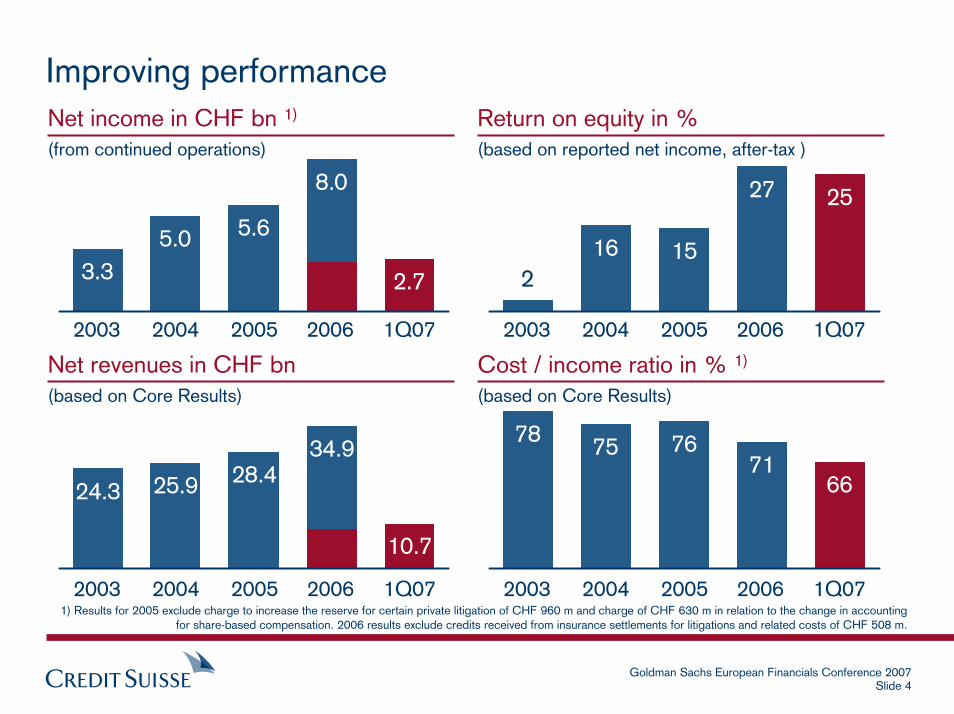

2.73.35.0

8.0

5.6

10.7

24.3 25.9

34.928.4

Improving performance

2003 2004 2005 2006

78 75 7671

66

Cost / income ratio in % 1)

(based on Core Results)

Net revenues in CHF bn(based on Core Results)

1) Results for 2005 exclude charge to increase the reserve for certain private litigation of CHF 960 m and charge of CHF 630 m in relation to the change in accounting for share-based compensation. 2006 results exclude credits received from insurance settlements for litigations and related costs of CHF 508 m.

16 15

27 25

2

Return on equity in %(based on reported net income, after-tax )

Net income in CHF bn 1)

(from continued operations)

1Q07 2003 2004 2005 2006 1Q07

2003 2004 2005 2006 1Q07 2003 2004 2005 2006 1Q07

Goldman Sachs European Financials Conference 2007Slide 5

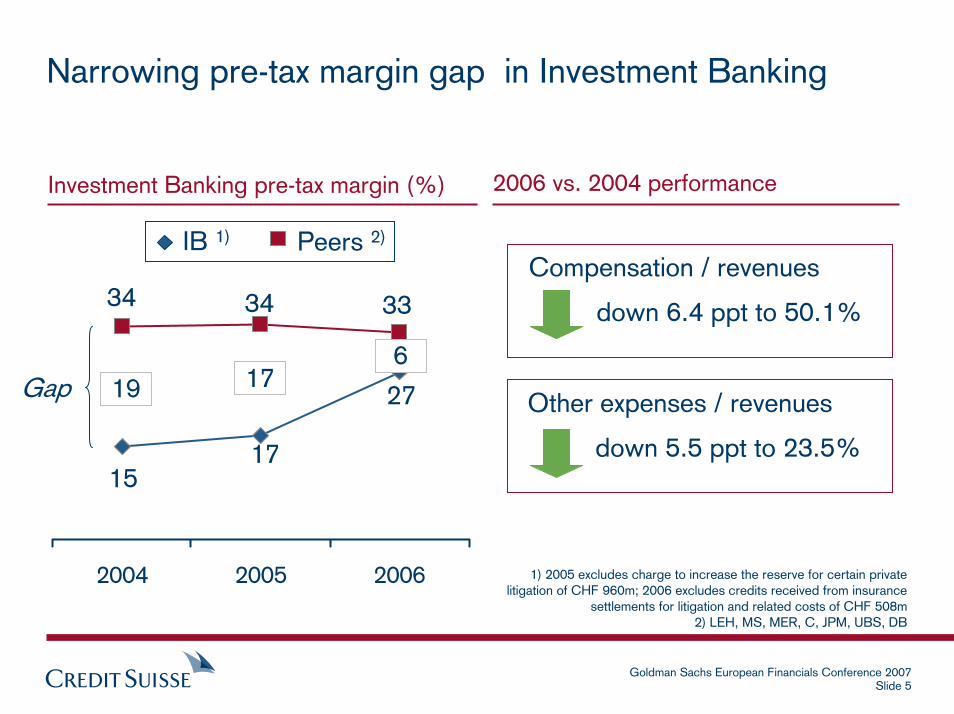

1) 2005 excludes charge to increase the reserve for certain private litigation of CHF 960m; 2006 excludes credits received from insurance

settlements for litigation and related costs of CHF 508m2) LEH, MS, MER, C, JPM, UBS, DB

Narrowing pre-tax margin gap in Investment Banking

Compensation / revenues

down 6.4 ppt to 50.1%

Other expenses / revenues

down 5.5 ppt to 23.5%

Investment Banking pre-tax margin (%) 2006 vs. 2004 performance

2004 2005 2006

1517

27

333434

17Gap 19

IB 1) Peers 2)

6

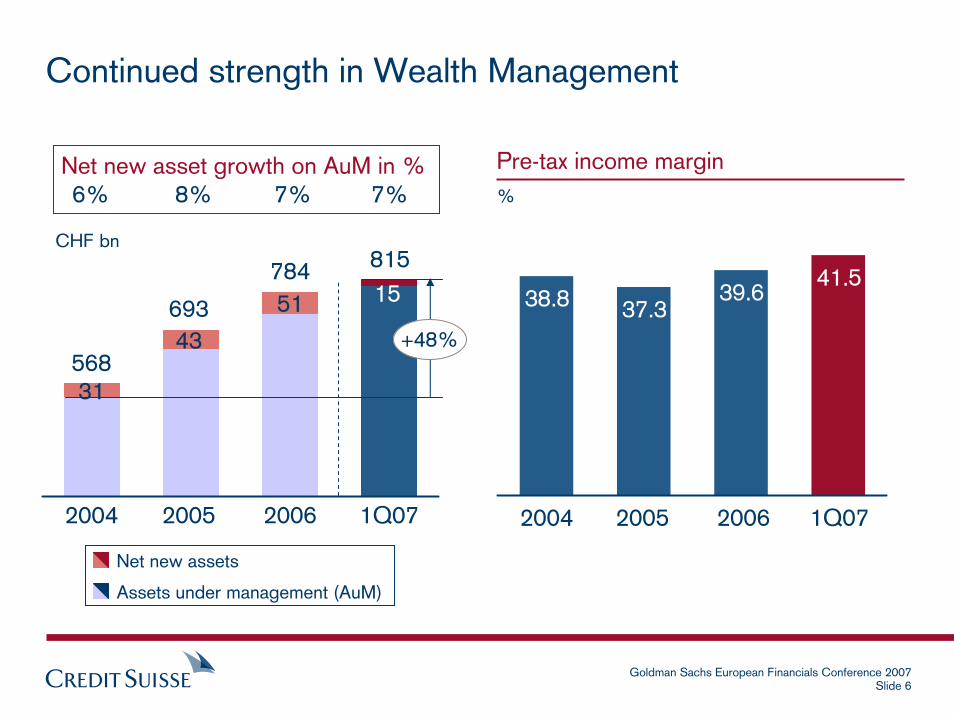

Goldman Sachs European Financials Conference 2007Slide 6

Continued strength in Wealth Management

38.8 37.339.6

41.5

2004 2005 2006 1Q072004 2005 2006 1Q07

31

15

CHF bn

Net new assets

Assets under management (AuM)

Net new asset growth on AuM in %6% 8% 7% 7%

815

568

693

784

43

51

Pre-tax income margin%

+48%

Goldman Sachs European Financials Conference 2007Slide 7

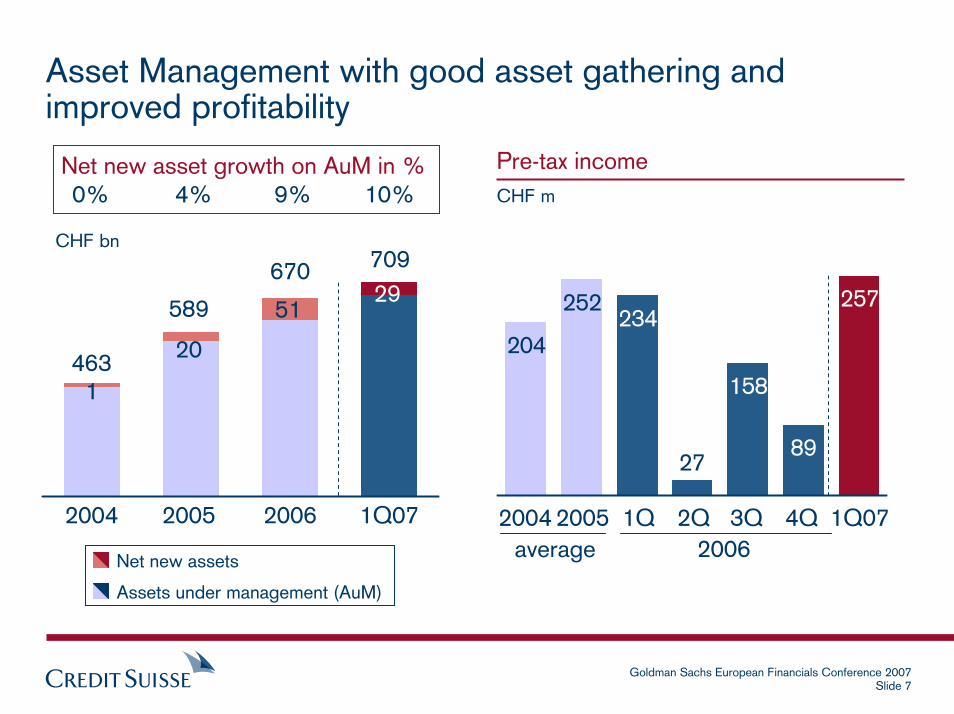

Asset Management with good asset gathering and improved profitability

234

158

89

257

204

252

27

2004 1Q2004 2005 2006 1Q07

1

29

CHF bn

Net new assets

Assets under management (AuM)

Net new asset growth on AuM in %0% 4% 9% 10%

709

463

589

670

20

51

Pre-tax incomeCHF m

2005 2Q 3Q 4Q 1Q072006average

Goldman Sachs European Financials Conference 2007Slide 8

Agenda

Improving Operating Performance

Platform for Growth

Managing Risk and Capital

Goldman Sachs European Financials Conference 2007Slide 9

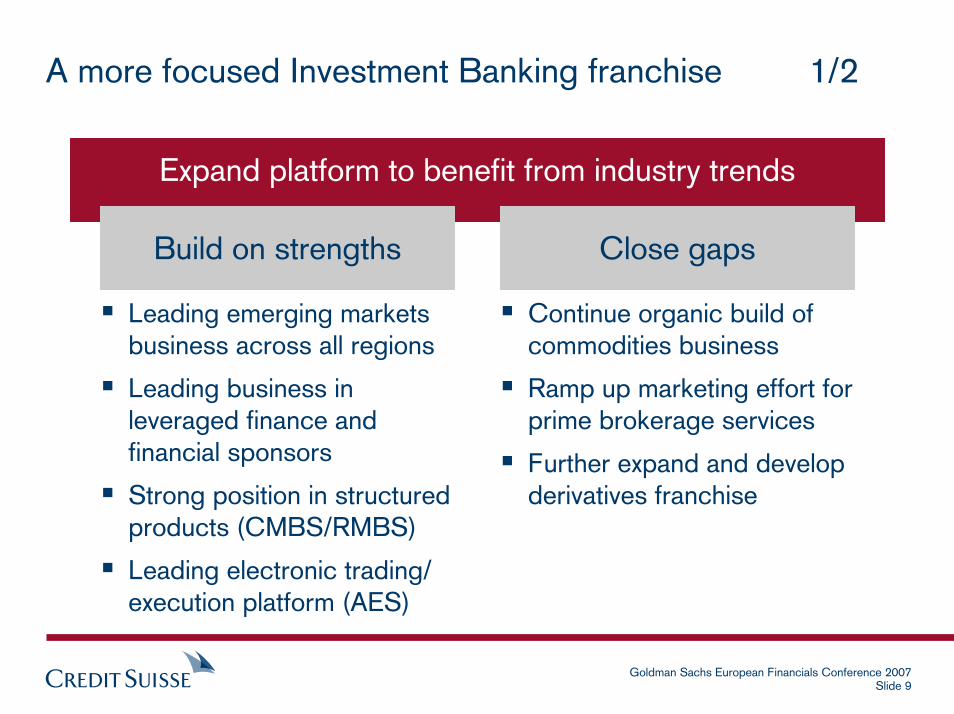

A more focused Investment Banking franchise 1/2

Expand platform to benefit from industry trends

Build on strengths

Leading emerging markets business across all regions

Leading business in leveraged finance and financial sponsors

Strong position in structured products (CMBS/RMBS)

Leading electronic trading/ execution platform (AES)

Close gaps

Continue organic build of commodities business

Ramp up marketing effort for prime brokerage services

Further expand and develop derivatives franchise

Goldman Sachs European Financials Conference 2007Slide 10

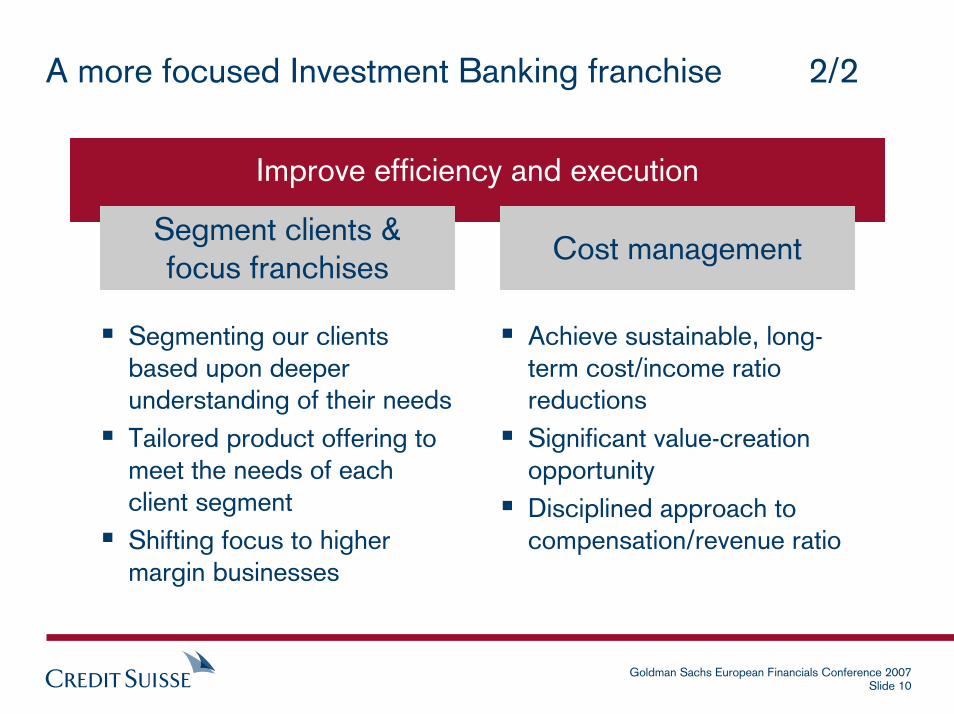

A more focused Investment Banking franchise 2/2

Improve efficiency and execution

Segment clients &focus franchises

Segmenting our clients based upon deeper understanding of their needsTailored product offering to meet the needs of each client segmentShifting focus to higher margin businesses

Cost management

Achieve sustainable, long-term cost/income ratio reductionsSignificant value-creation opportunityDisciplined approach to compensation/revenue ratio

Goldman Sachs European Financials Conference 2007Slide 11

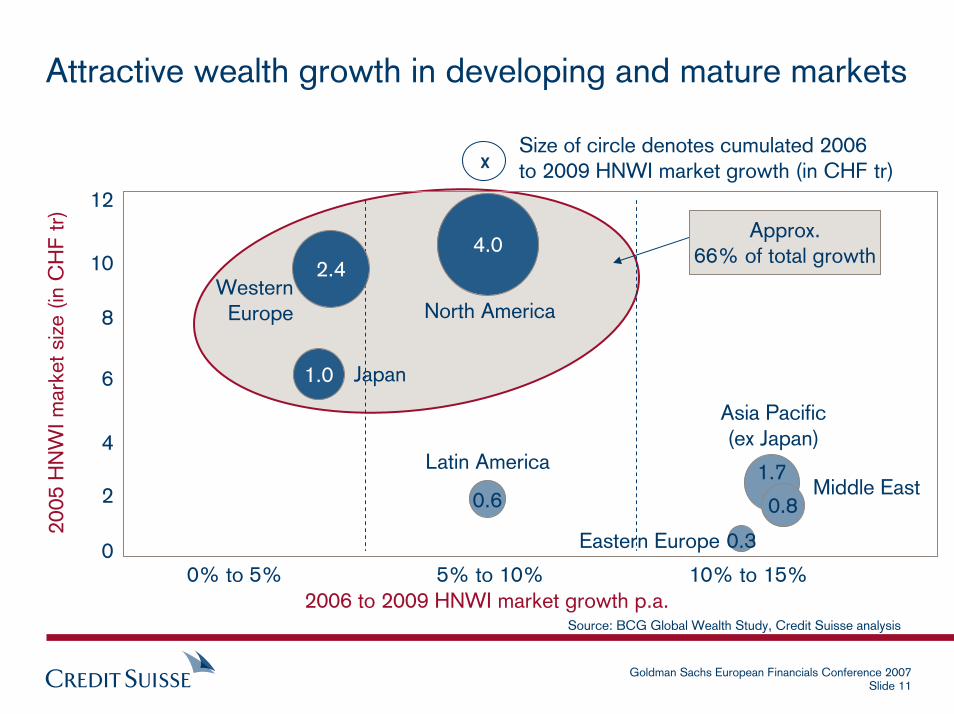

Attractive wealth growth in developing and mature markets

2

4

6

8

10

12

0% to 5% 5% to 10%

Source: BCG Global Wealth Study, Credit Suisse analysis

10% to 15%0

Asia Pacific(ex Japan)

Middle East

Eastern Europe 0.3

Japan1.0

Latin America

0.6

Western Europe

2.4

North America

4.0

2006 to 2009 HNWI market growth p.a.

2005

HN

WI m

arke

t siz

e (in

CH

F tr

)

xSize of circle denotes cumulated 2006to 2009 HNWI market growth (in CHF tr)

1.7

0.8

Approx.66% of total growth

Goldman Sachs European Financials Conference 2007Slide 12

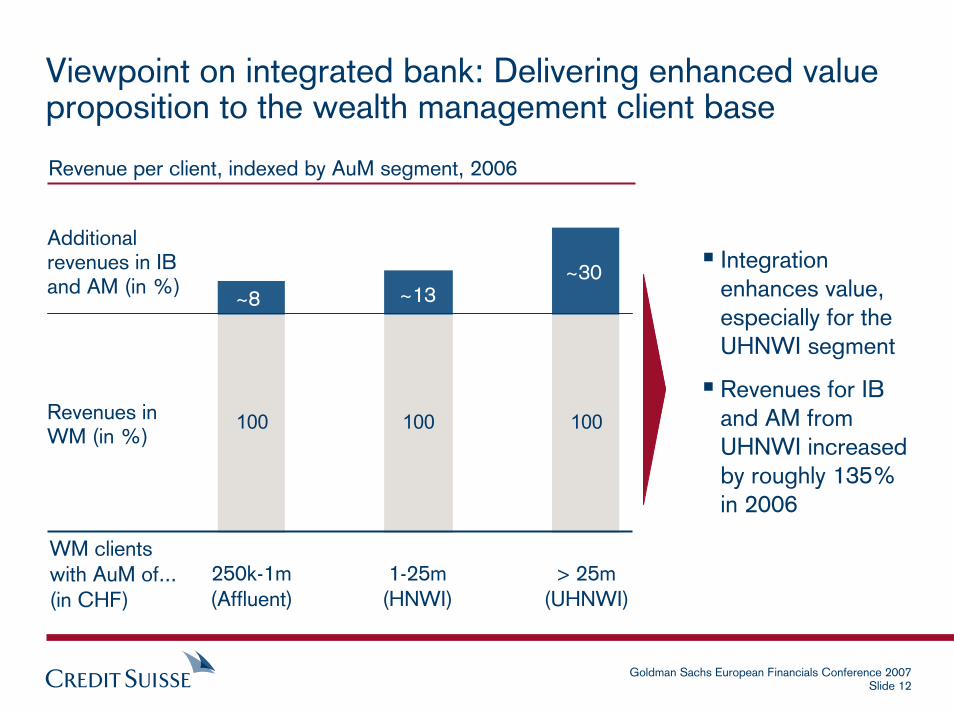

100 100 100

Viewpoint on integrated bank: Delivering enhanced value proposition to the wealth management client base

Revenue per client, indexed by AuM segment, 2006

250k-1m(Affluent)

1-25m(HNWI)

> 25m(UHNWI)

Revenues in WM (in %)

Additional revenues in IB and AM (in %)

WM clientswith AuM of...(in CHF)

~13~30

~8

Integration enhances value, especially for the UHNWI segment

Revenues for IB and AM from UHNWI increased by roughly 135% in 2006

Goldman Sachs European Financials Conference 2007Slide 13

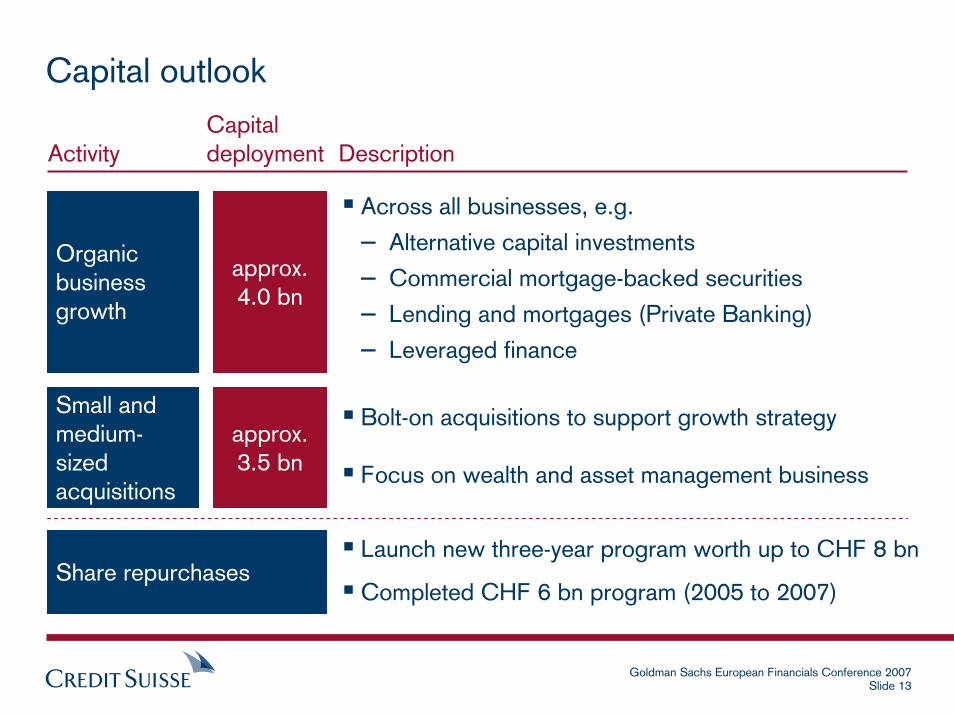

Capital outlook

Organic business growth

Small and medium-sized acquisitions

approx. 4.0 bn

approx. 3.5 bn

Across all businesses, e.g.

– Alternative capital investments

– Commercial mortgage-backed securities

– Lending and mortgages (Private Banking)

– Leveraged finance

CapitalActivity deployment Description

Bolt-on acquisitions to support growth strategy

Focus on wealth and asset management business

Launch new three-year program worth up to CHF 8 bn

Completed CHF 6 bn program (2005 to 2007)Share repurchases

Goldman Sachs European Financials Conference 2007Slide 14

Agenda

Improving Operating Performance

Platform for Growth

Managing Risk and Capital

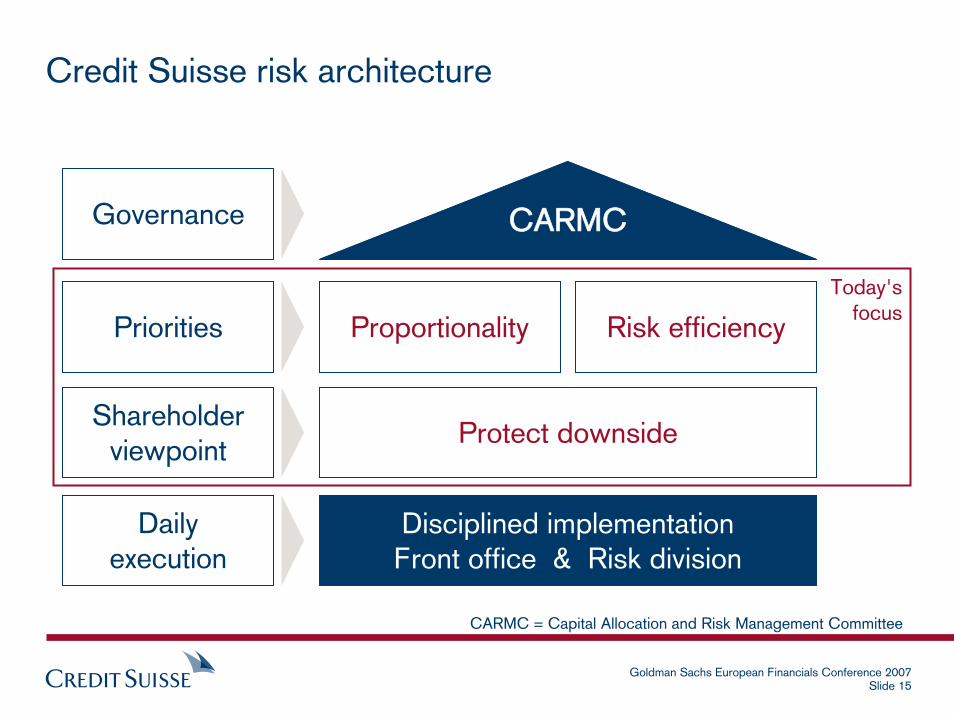

Goldman Sachs European Financials Conference 2007Slide 15

Credit Suisse risk architecture

CARMC

Disciplined implementationFront office & Risk division

Proportionality

Protect downside

Risk efficiency

Governance

Shareholderviewpoint

Priorities

Dailyexecution

CARMC = Capital Allocation and Risk Management Committee

Today'sfocus

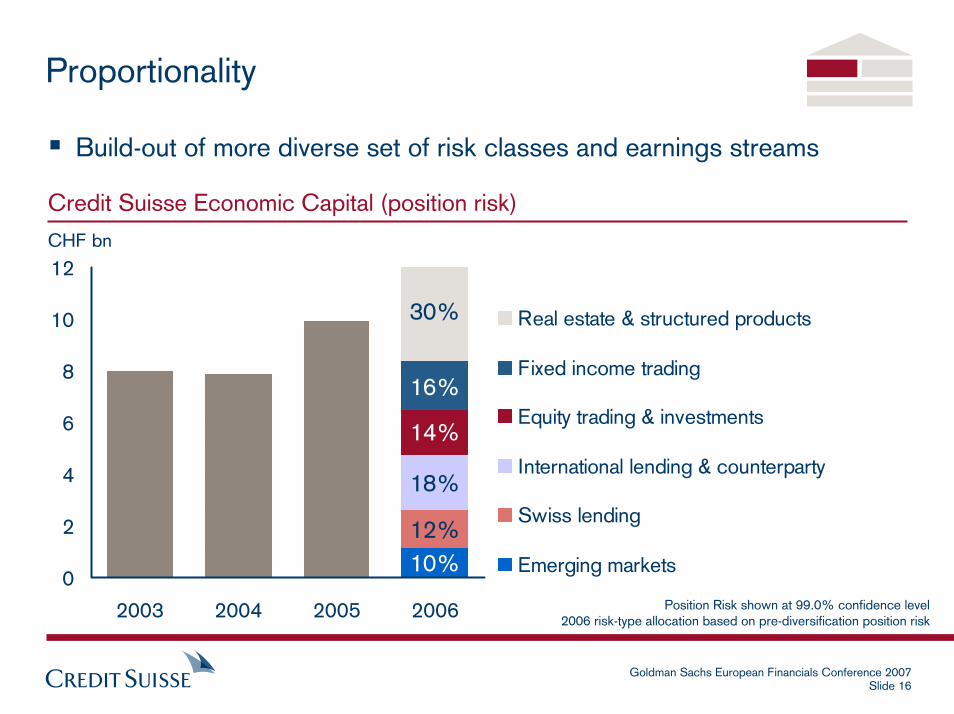

Goldman Sachs European Financials Conference 2007Slide 16

0

2

4

6

8

10

12

2003 2004 2005 2006

Real estate & structured products

Fixed income trading

Equity trading & investments

International lending & counterparty

Swiss lending

Emerging markets

Proportionality

Build-out of more diverse set of risk classes and earnings streams

Credit Suisse Economic Capital (position risk)

CHF bn

10%12%

18%

14%

16%

30%

Position Risk shown at 99.0% confidence level2006 risk-type allocation based on pre-diversification position risk

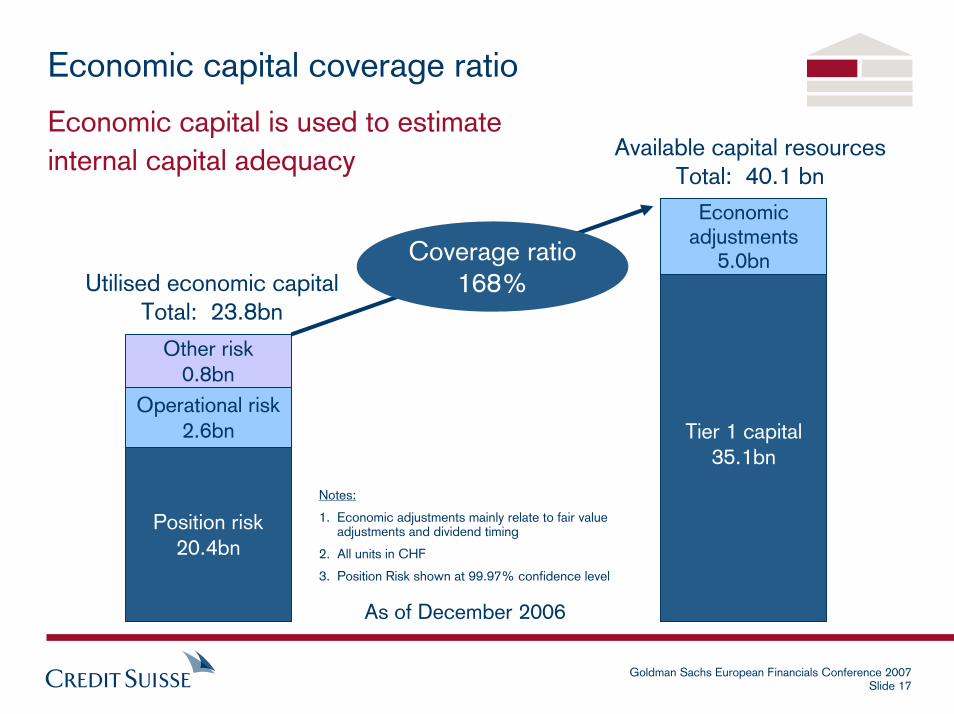

Goldman Sachs European Financials Conference 2007Slide 17

Notes:

1. Economic adjustments mainly relate to fair value adjustments and dividend timing

2. All units in CHF

3. Position Risk shown at 99.97% confidence level

Economic capital coverage ratio

Economic capital is used to estimate internal capital adequacy

Coverage ratio168%

Position risk20.4bn

Operational risk 2.6bn

Other risk 0.8bn

Tier 1 capital35.1bn

Economic adjustments

5.0bnUtilised economic capital

Total: 23.8bn

Available capital resourcesTotal: 40.1 bn

As of December 2006

Goldman Sachs European Financials Conference 2007Slide 18

Risk efficiency

Market can give early warning on changes

Closer touch with customers – sharper awareness

Makes capital 'work harder' for shareholders

Distribution as a structural objective

Hedging

Credit Suisse spent over CHF 500 m on hedging and mobility in 2006

– More consistent earnings by foregoing some upside in good times

– Better long term value through the cycle

Free-up capital and improve returns for less liquid areas

Goldman Sachs European Financials Conference 2007Slide 19

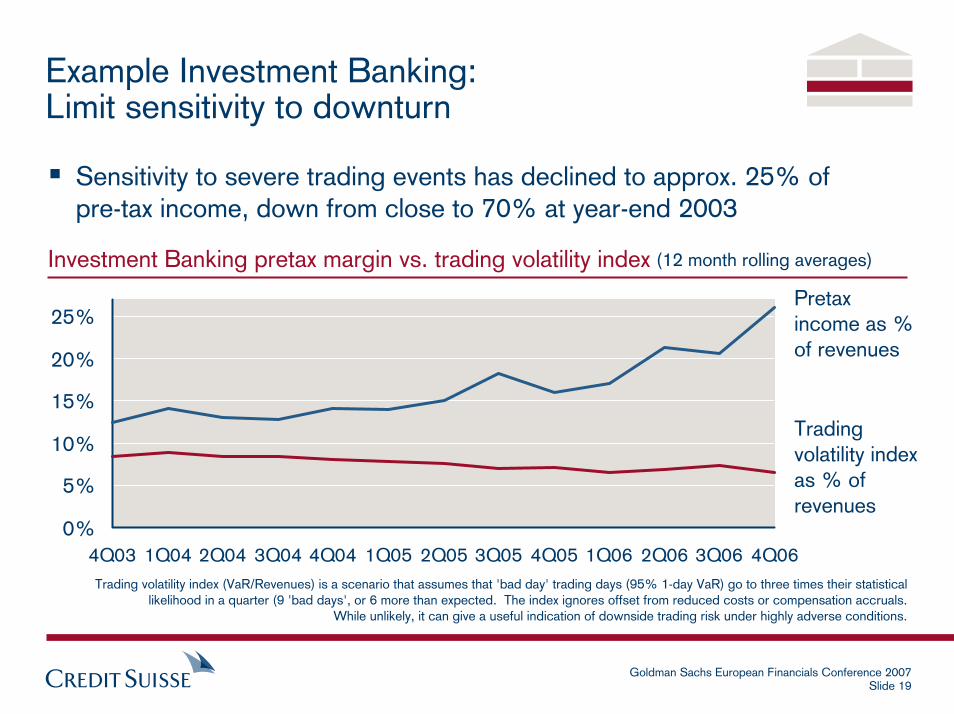

Example Investment Banking:Limit sensitivity to downturn

Trading volatility index (VaR/Revenues) is a scenario that assumes that 'bad day' trading days (95% 1-day VaR) go to three times their statistical likelihood in a quarter (9 'bad days', or 6 more than expected. The index ignores offset from reduced costs or compensation accruals.

While unlikely, it can give a useful indication of downside trading risk under highly adverse conditions.

Pretax income as % of revenues

Trading volatility indexas % of revenues

Sensitivity to severe trading events has declined to approx. 25% ofpre-tax income, down from close to 70% at year-end 2003

Investment Banking pretax margin vs. trading volatility index

0%

5%

10%

15%

20%

25%

4Q03 1Q04 2Q04 3Q04 4Q04 1Q05 2Q05 3Q05 4Q05 1Q06 2Q06 3Q06 4Q06

(12 month rolling averages)

Goldman Sachs European Financials Conference 2007Slide 20

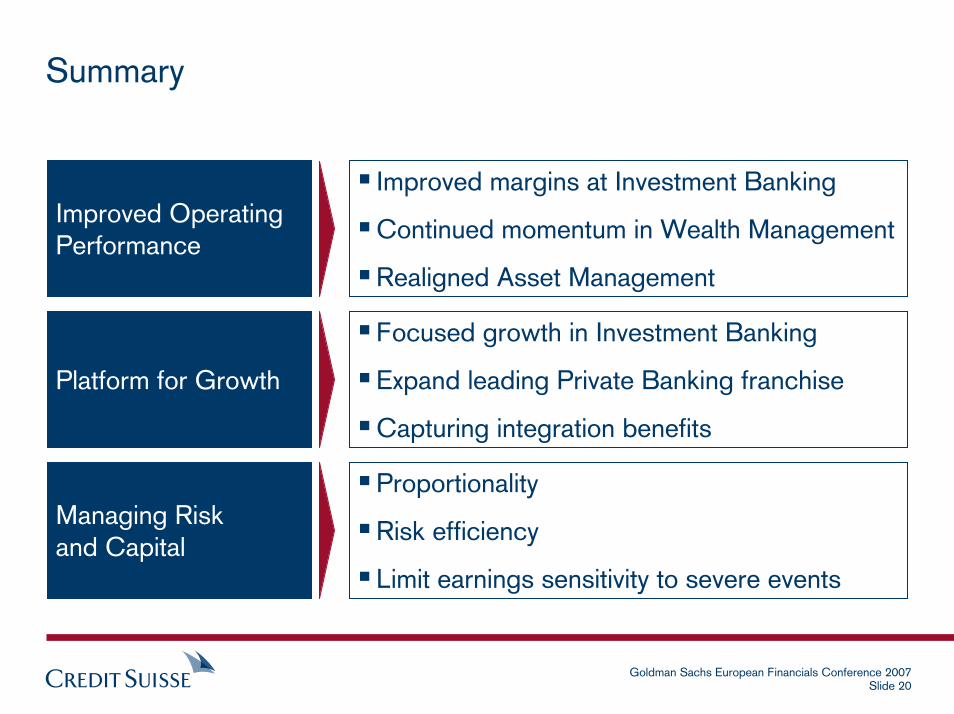

Summary

Improved Operating Performance

Platform for Growth

Managing Riskand Capital

Improved margins at Investment Banking

Continued momentum in Wealth Management

Realigned Asset Management

Focused growth in Investment Banking

Expand leading Private Banking franchise

Capturing integration benefits

Proportionality

Risk efficiency

Limit earnings sensitivity to severe events

Goldman Sachs European Financials Conference 2007Slide 21