Goldman Sachs Conference - Church & Dwight Co., Inc.

53

Presentation by: Jim Craigie, Chairman & CEO Matt Farrell, EVP & CFO May 12, 2011 Goldman Sachs Conference

Transcript of Goldman Sachs Conference - Church & Dwight Co., Inc.

Presentation by:

Jim Craigie, Chairman & CEO

Matt Farrell, EVP & CFO

May 12, 2011

Goldman Sachs Conference

Safe Harbor Statement

This presentation contains forward-looking statements relating, among others, to sales and earnings growth, including

growth for the laundry detergent business, cash flow, margin improvement, marketing spending, new product

introductions, contribution to revenue, growth and gross margin expansion by the new laundry detergent manufacturing

plant and warehouse facility, capital expenditures and cash transition expenses related to the new facility, forecasted

organic sales growth and earnings per share growth, the Company’s focus on targeted marketing and new product

introductions and investment in a global information systems project. These statements represent the intentions, plans,

expectations and beliefs of the Company, and are subject to risks, uncertainties and other factors, many of which are

outside the Company’s control and could cause actual results to differ materially from such forward-looking

statements. The uncertainties include assumptions as to market growth and consumer demand (including the effect of

political and economic events on consumer demand), retailer actions in response to changes in consumer demand and

the economy, raw material and energy prices, the financial condition of major customers and vendors, interest rate and

foreign currency exchange rate fluctuations and changes in marketing and promotional spending. With regard to the new

product introductions referred to generally in this release, there is particular uncertainty relating to trade, competitive and

consumer reactions. Other factors that could materially affect actual results include the outcome of contingencies,

including litigation, pending regulatory proceedings, environmental matters and the acquisition or divestiture of

assets. For a description of additional factors that could cause actual results to differ materially from the forward looking

statements, please see the Company’s quarterly and annual reports filed with the SEC, including information in the

Company’s annual report on Form 10-K in Item 1A, “Risk Factors.”

2

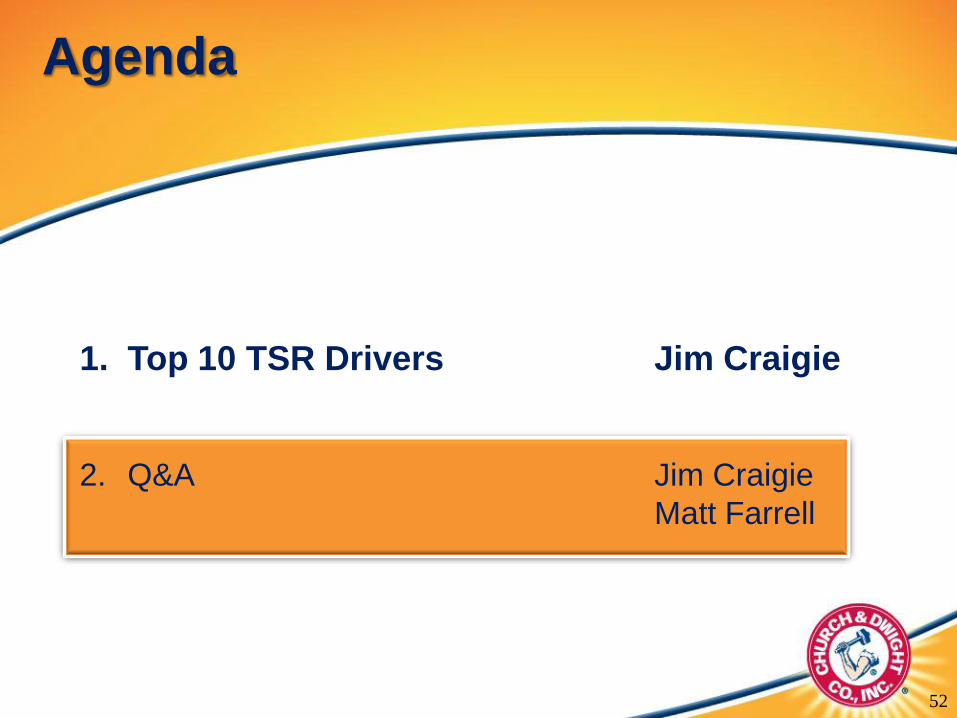

1. Top 10 TSR Drivers Jim Craigie

2. Q&A Jim Craigie

Matt Farrell

Agenda

3

1. Recession Resistant

Product Portfolio

4

Top 10 TSR Drivers

Our Unique Product Portfolio Has Both Value and Premium Products

5

Our Value Brands Thrive in a Recessionary Economy

6

Era

Purex

Arm & Hammer

Sun

XTRA

Our Value Brands Offer Significant Savings

7

Cost Per Load - Index vs. Tide

100

80

75

70

55

150 oz.

50

40

40

28

26

150 oz.

Tide

Gain

Cheer

Wisk

all

2. Build Power Brands

8

Top 10 TSR Drivers

We Have Over 80 Brands, But Our 8 Power Brands Generate . . .

9

=80%

of

Sales &

Profits

10

Our Power Brands are Market Leaders

A&H brands are in 86% of households in America

#1 Condom Brand

#1 Laundry Additive Brand

#1 Battery Powered Toothbrush Brand

#1 Pregnancy Kit Brand

#1 Depilatory Brand

#1 Oral Care Pain Relief Brand

#1 Extreme Value Laundry Detergent

Arm & Hammer

Trojan

OxiClean

Spinbrush

First Response

Nair

Orajel

XTRA

11

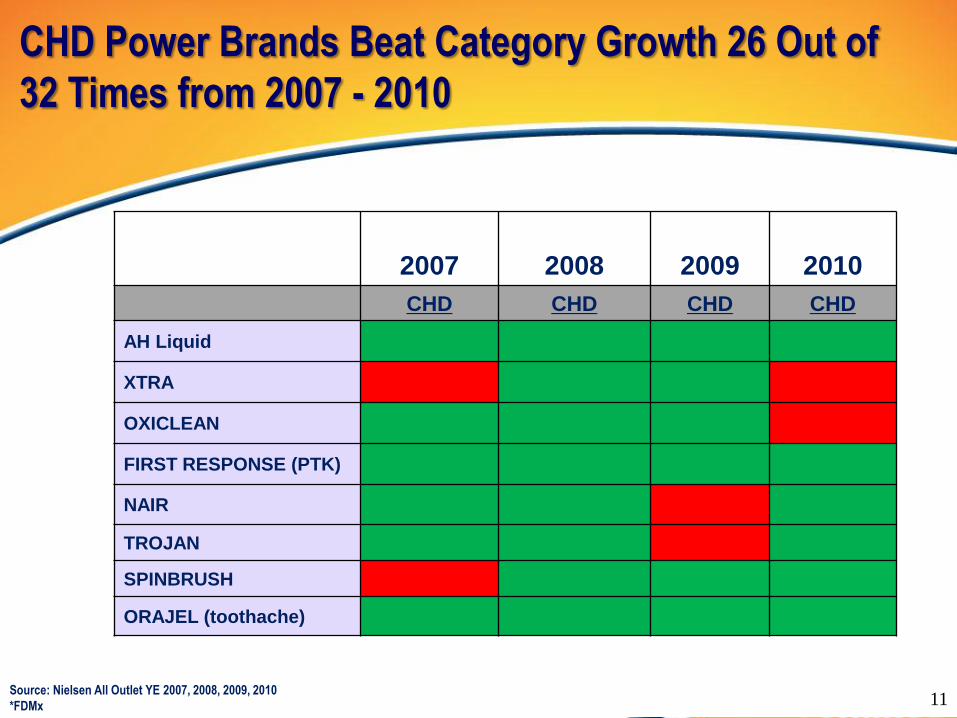

2007 2008 2009 2010

CHD CHD CHD CHD

AH Liquid

XTRA

OXICLEAN

FIRST RESPONSE (PTK)

NAIR

TROJAN

SPINBRUSH

ORAJEL (toothache)

CHD Power Brands Beat Category Growth 26 Out of

32 Times from 2007 - 2010

Source: Nielsen All Outlet YE 2007, 2008, 2009, 2010

*FDMx

3. Ferociously Defend Our

Brands

12

Top 10 TSR Drivers

1313

Ferociously Defend our Brands

OxiClean Case Study

14

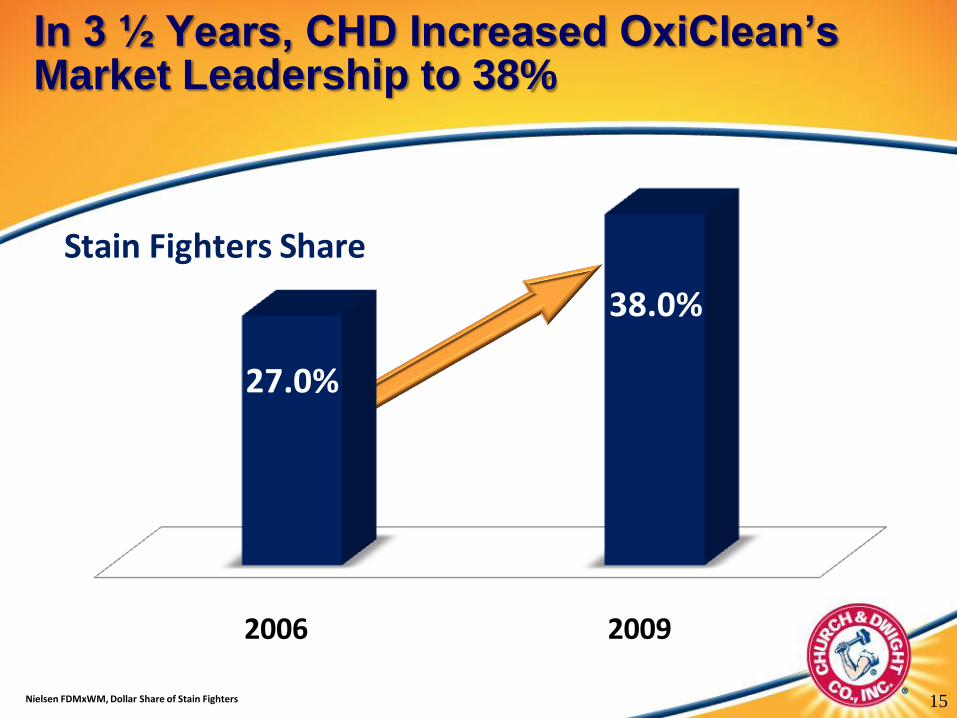

CHD Acquired OxiClean in 2006

- #1 Laundry Additive

- 27% Market Share

C

2006 2009

27.0%

38.0%

Stain Fighters Share

In 3 ½ Years, CHD Increased OxiClean’s Market Leadership to 38%

Nielsen FDMxWM, Dollar Share of Stain Fighters 15

We Did This Through Innovative Forms, New Products, and Claims…..

2007

Increased Pretreat support

“See it Work before your

eyes”

2009-10

Versatility emphasis

“Gets tough stains out all around the

home”

2008

Premium Pretreatline extension

“The Best in Stain Removal”

2009

Increased Liquid support

“Cleaner, Whiter, Brighter””

16

0

50

100

150

200

250

300

350

400

450

500

2006 2009

Annual Marketing Index

17Source: First Response Actual Yearly Marketing Spending

…And Increased Marketing

Spending 400%

100

500

17

18

In Mid-2009, the #1 Laundry Brand Entered the Category

CHD Ferociously Defended OxiClean With Innovative New Products:

Clings to and breaks down stains

More Power In Every Drop!

Seeks out stains in your

wash!

19

20

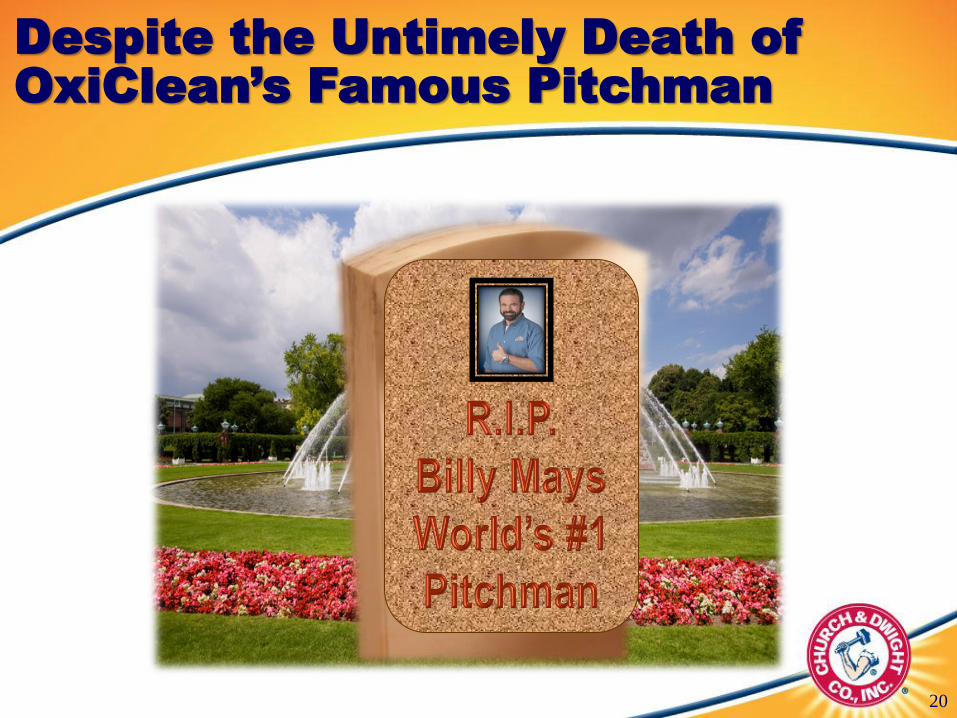

Despite the Untimely Death of

OxiClean’s Famous Pitchman

OxiClean is Still #1 – 2x the Closest Competitor

2009 2010 Change

OxiClean 39.9 38.8 -1.1

P&G 10.4 17.5 7.1

Reckitt 15.0 12.3 -2.7

SC Johnson 17.8 17.0 -0.8

Market Share

21

Market share is Nielsen 52-week 12/25/10 All-Outlet

4. Driving International

Growth

22

Top 10 TSR Drivers

CHD has transformed from almost

totally a U.S. business to more of a global player.

INTERNATIONAL - 2%

2001 2010

INTERNATIONAL - 19%

CHD 2001 – 2010 Geographic Mix Transformation

23

2010 Was a Stellar Year for International

2010 vs. 2009

Net Sales +7%

Gross Profit +10%

Operating Profit +25%

24

Capping 5 Stellar Years of Strong Growth

2005 vs. 2010 CAGR

Net Sales +7%

Gross Profit +8%

Operating Profit +18%

25

Key Drivers of Continued Strong Growth

Increase scale in our subsidiary companies by:

Expanding corporate power brands

Focus resources on corporate and international power

brands

Leveraging ‘one company’ strengths across all

functions

Enter new markets by:

Driving export growth

Acquisition

26

5. Expanding Gross

Margin

27

Top 10 TSR Drivers

CHD 2001 – 2010 Gross Margin Expanded 1,560 bps.

2001 2003 2005 2007 2008 2009 2010

30.0%29.1%

36.7%39.1%

40.5%

44.7%44.8%

28

Gross Margin Growth Driven by 4 Key Factors

Good to Great Cost

Optimization Program

Supply Chain

Restructuring

Acquisition Synergies

Price / Mix

29

Reformulation, reduce

packaging, reduce SKU’s,

laundry compaction,

hedges

New Laundry Plant

Acquire higher margin

brands and implement

cost synergies

Launch higher margin

new products

Actions Examples

New Laundry Plant Built in 2009

30

The Davies Plant; York, Pennsylvania

6. Superior Overhead

Management

31

Top 10 TSR Drivers

32

11.6% 11.1%

13.9% 13.7% 13.9% 14.1%13.5%

2001 2003 2005 2007 2008 2009 2010

2001 – 2010 SG&A Increased 190 bps Due to

International Expansion and Stock Option

Expense

33

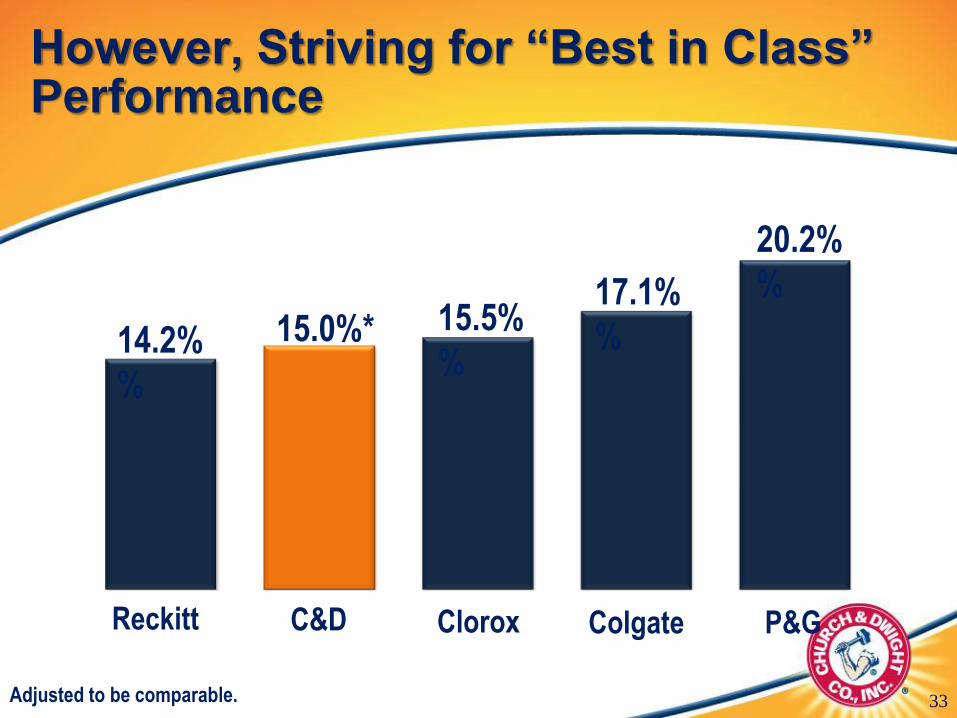

However, Striving for “Best in Class” Performance

14.2%

%

15.5%

%

17.1%

%

20.2%

%

15.0%*

* Increased 1.5% to make expenses from Marketing to SG&A for

Apples-to-Apples comparison.

Reckitt C&D Clorox Colgate P&G

Adjusted to be comparable.

34

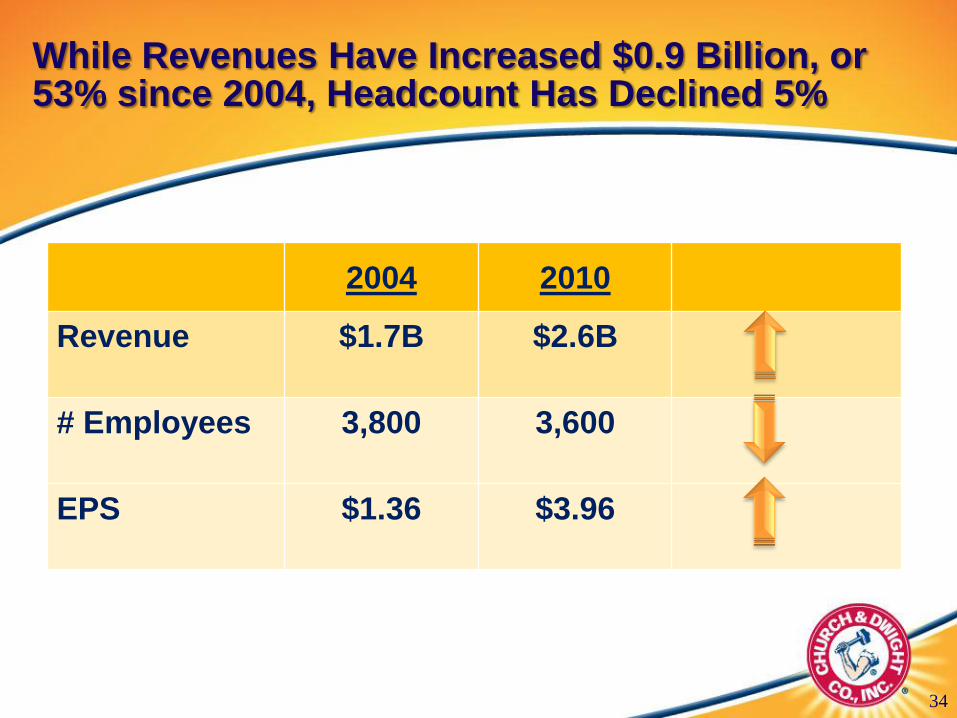

While Revenues Have Increased $0.9 Billion, or 53% since 2004, Headcount Has Declined 5%

2004 2010

Revenue $1.7B $2.6B

# Employees 3,800 3,600

EPS $1.36 $3.96

35

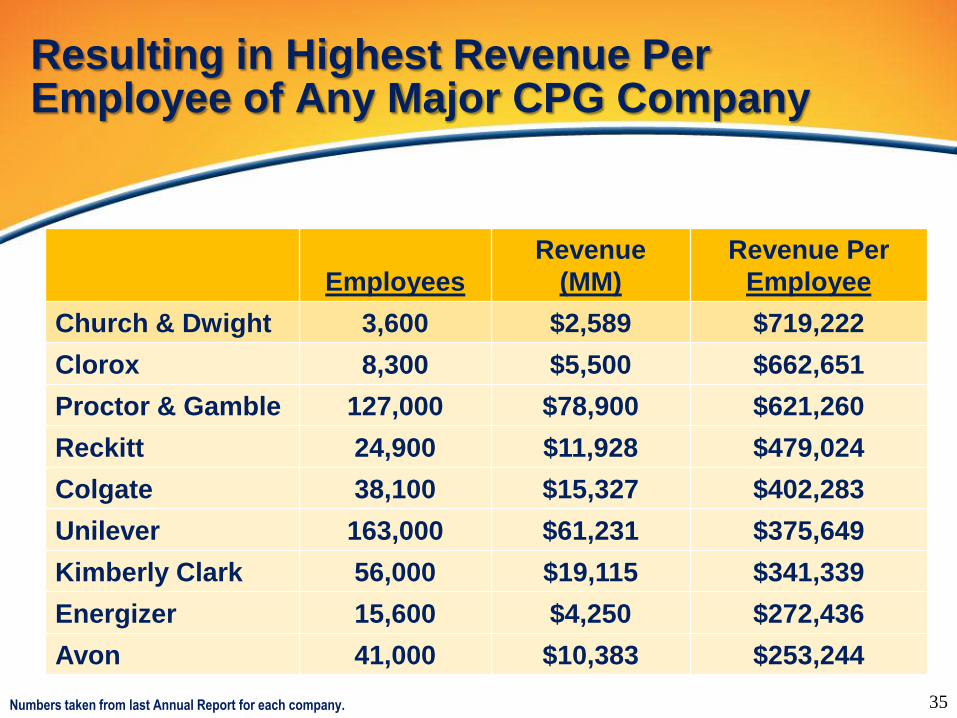

Employees

Revenue

(MM)

Revenue Per

Employee

Church & Dwight 3,600 $2,589 $719,222

Clorox 8,300 $5,500 $662,651

Proctor & Gamble 127,000 $78,900 $621,260

Reckitt 24,900 $11,928 $479,024

Colgate 38,100 $15,327 $402,283

Unilever 163,000 $61,231 $375,649

Kimberly Clark 56,000 $19,115 $341,339

Energizer 15,600 $4,250 $272,436

Avon 41,000 $10,383 $253,244

Resulting in Highest Revenue Per Employee of Any Major CPG Company

Numbers taken from last Annual Report for each company. 35

7. Expert Management

Team

36

Top 10 TSR Drivers

37

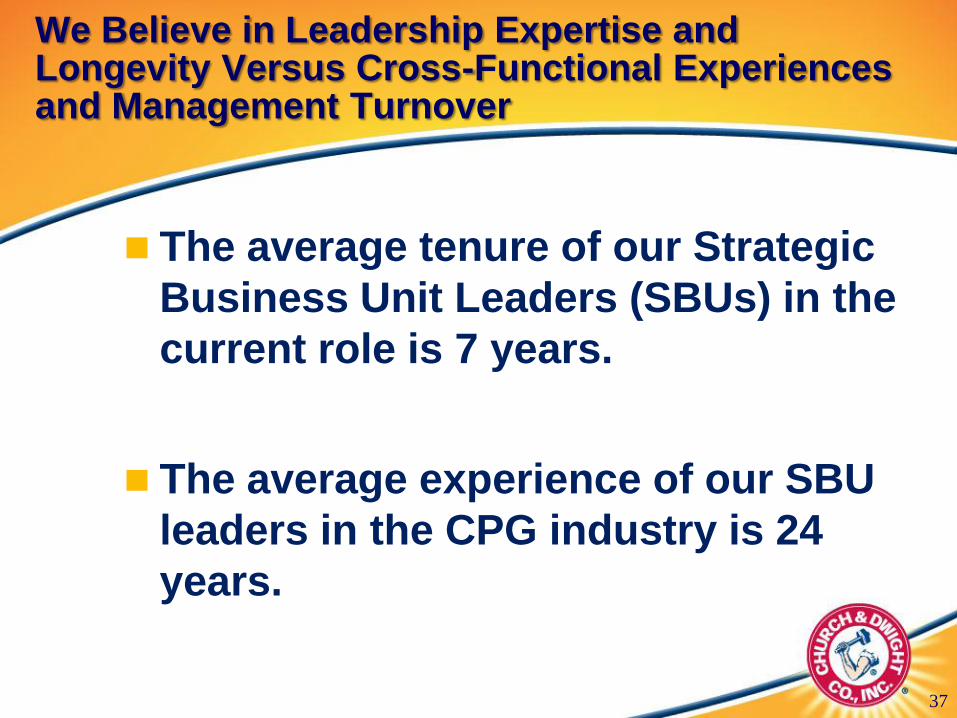

We Believe in Leadership Expertise and Longevity Versus Cross-Functional Experiences and Management Turnover

The average tenure of our Strategic

Business Unit Leaders (SBUs) in the

current role is 7 years.

The average experience of our SBU

leaders in the CPG industry is 24

years.

8. Proven Track Record on

Acquisitions

38

Top 10 TSR Drivers

We Have Tight Acquisition Guidelines to Ensure Accretive Acquisitions

Primarily #1 or #2 Share Brands

Higher Growth, Higher Margin Brands

Asset Light

Leverage CHD Capital Base in

Manufacturing, Logistics and Purchasing

Deliver Sustainable Competitive

Advantage

39

$691

$960 $1,047 $1,057

$1,462$1,737

$1,946

$2,221

$2,404 $2,521 $2,589

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

SPINBRUSH

ARMKEL

JV (50%)

CHURCH & DWIGHT REVENUE DEVELOPMENT – PAST 10 YEARS

UNILEVER

ORAL

CARE

SIMPLY

SALINE

USA

DETERGENTS

CARTER-

WALLACEORANGE

GLO

ORAJEL

40

FELINE

PINE

Proven Track Record on Acquisitions Has Been

a Key Driver of CHD Growth

41

YEAR

ACQUIRED

Arm & Hammer $1 Billion Brand ---

Trojan #1 Condom Brand 2001

OxiClean #1 Laundry Additive Brand 2006

Spinbrush #1 Battery Powered Toothbrush Brand 2005

First Response #1 Pregnancy Kit Brand 2001

Nair #1 Depilatory Brand 2001

Orajel #1 Oral Care Pain Relief Brand 2008

XTRA #1 Extremely Value Laundry Detergent 2001

7 of 8 Power Brands Acquired Since 2000

42

We Integrate Acquisitions Quickly and Build

Them Into Power Brands

Nielsen FDMx 52 Week Dollar Share for 2005 and Later

IRI FDMx Prior to 2005

Nair: Depilatories, Wax and Bleach

$ ShareBrand Position

in Category

Pre-acquisition 2010 Pre-acquisition 2010

Trojan 68.9 75.5 #1 #1

First Response 12.0 27.7 #3 #1

Nair 22.8 27.6 #2 #2

Spinbrush 30.1 44.9 #2 #1

OxiClean 26.1 37.0 #1 #1

Orajel Toothache 60.9 59.7 #1 #1

9. Best in Class Free

Cash Flow Conversion

43

Top 10 TSR Drivers

44

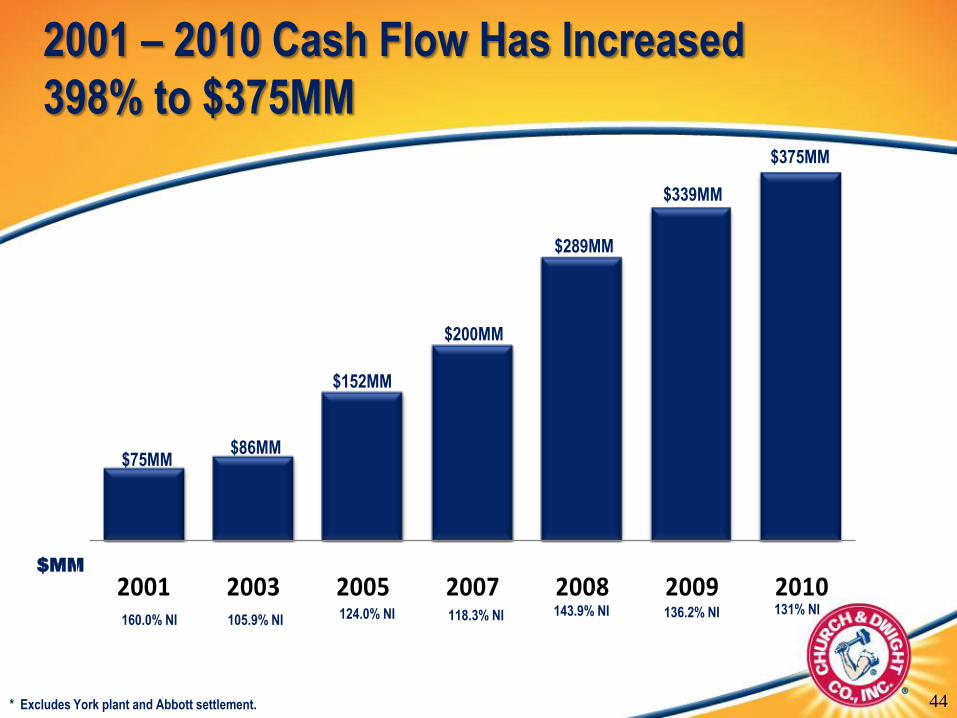

2001 2003 2005 2007 2008 2009 2010160.0% NI

$MM

105.9% NI 124.0% NI 118.3% NI 143.9% NI 131% NI

2001 – 2010 Cash Flow Has Increased

398% to $375MM

136.2% NI

* Excludes York plant and Abbott settlement.

$75MM$86MM

$152MM

$200MM

$289MM

$339MM

$375MM

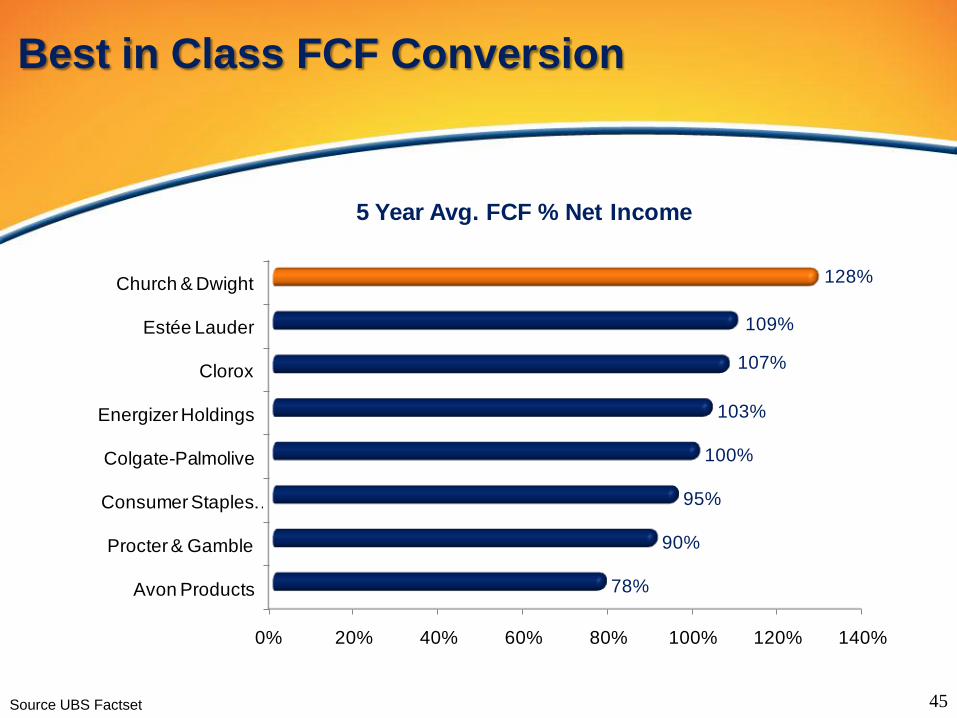

Best in Class FCF Conversion

0% 20% 40% 60% 80% 100% 120% 140%

Avon Products

Procter & Gamble

Consumer Staples …

Colgate-Palmolive

Energizer Holdings

Clorox

Estée Lauder

Church & Dwight

78%

90%

95%

100%

103%

107%

109%

128%

5 Year Avg. FCF % Net Income

Source UBS Factset 4545

10. TSR Junkies

46

Top 10 TSR Drivers

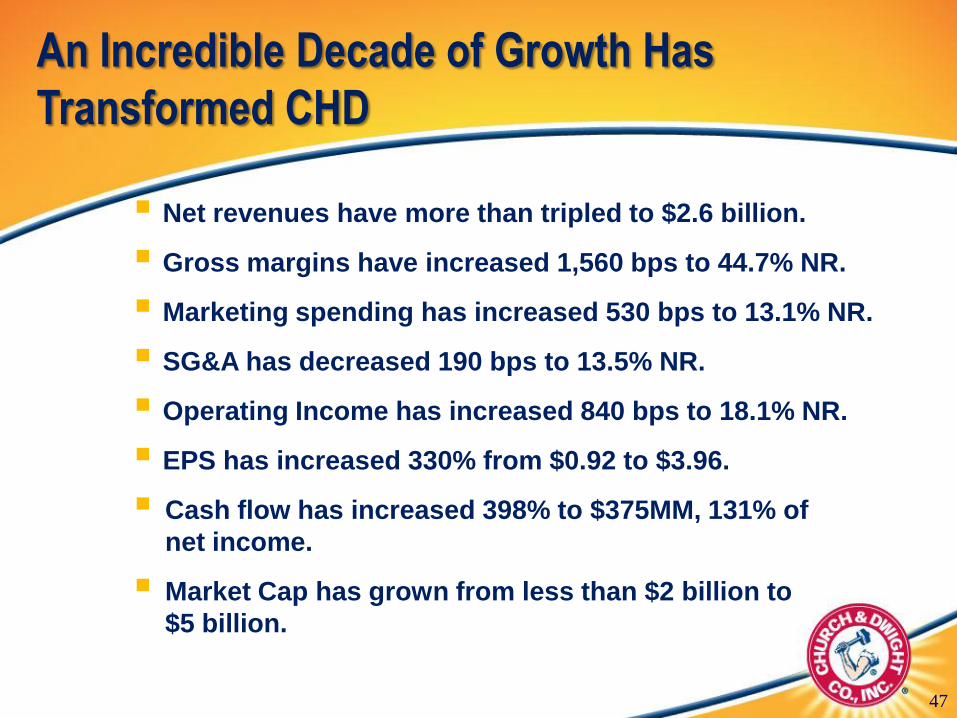

Net revenues have more than tripled to $2.6 billion.

Gross margins have increased 1,560 bps to 44.7% NR.

Marketing spending has increased 530 bps to 13.1% NR.

SG&A has decreased 190 bps to 13.5% NR.

Operating Income has increased 840 bps to 18.1% NR.

EPS has increased 330% from $0.92 to $3.96.

Cash flow has increased 398% to $375MM, 131% of

net income.

Market Cap has grown from less than $2 billion to

$5 billion.

47

An Incredible Decade of Growth Has

Transformed CHD

And Delivered Outstanding Returns to Our Shareholders

48

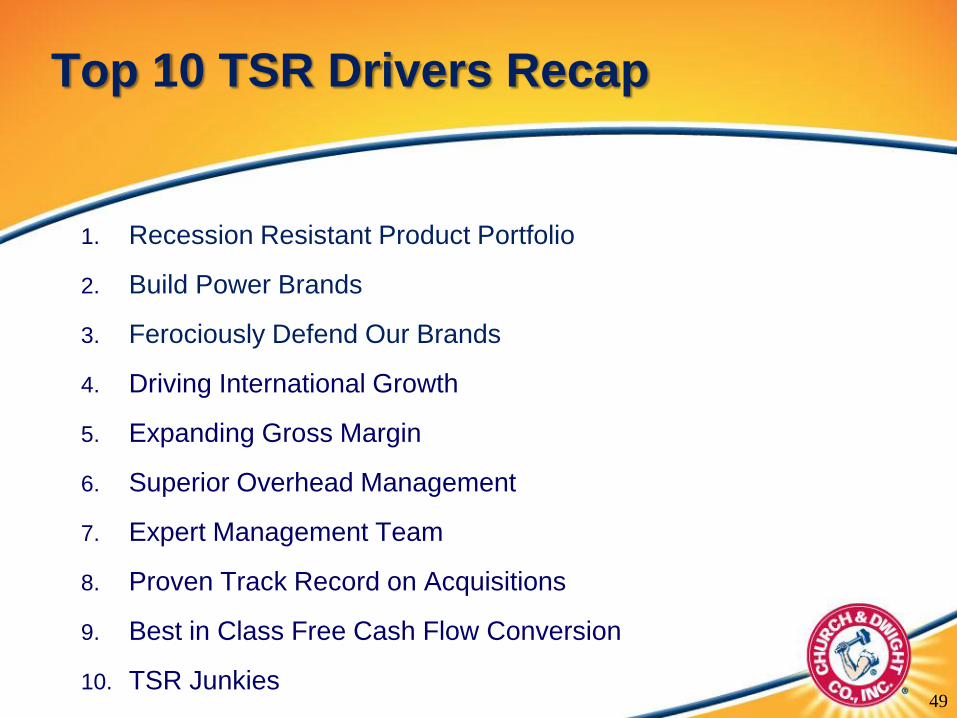

1. Recession Resistant Product Portfolio

2. Build Power Brands

3. Ferociously Defend Our Brands

4. Driving International Growth

5. Expanding Gross Margin

6. Superior Overhead Management

7. Expert Management Team

8. Proven Track Record on Acquisitions

9. Best in Class Free Cash Flow Conversion

10. TSR Junkies49

Top 10 TSR Drivers Recap

2011 Guidance

2011

May Guidance

Organic Sales +3-4%

Gross Margin +50-100 bps

Marketing +0-50 bps

EPS $4.35 – $4.40 (+10-11%)

Dividend 2%

50

Headed for “10 for 20” Club:Still Time to Get on Board

51

51

1. Top 10 TSR Drivers Jim Craigie

2. Q&A Jim Craigie

Matt Farrell

Agenda

52