Housing Market Forecasts - Hamptons International Market Forecasts Autumn 2013

Upload

sean-corriganCategory

view

174download

3

Unconventional Wisdom. Original Thinking.

hindesightletters.com

Please see disclaimer at the end of this document 1

Sean Corrigan

Thoughts on GoldSean Corrigan

Unconventional Wisdom. Original Thinking.

hindesightletters.com

Please see disclaimer at the end of this document 2

Sean Corrigan

Rationale

Unconventional Wisdom. Original Thinking.

hindesightletters.com

Please see disclaimer at the end of this document 3

Sean Corrigan

-0.8

-0.6

-0.4

-0.2

0.0

0.2

80

120

160

200

240

Ap

r-80

Ap

r-85

Ap

r-90

Ap

r-95

Ap

r-00

Ap

r-05

Ap

r-10

Ap

r-15

Non-PM Commodities/Gold (t+3) v Detrended Log Nominal UST10 yields, 6mma: Source, IMF, CRB, Bloomberg

IMF-AU (lhs)

UST10 Nom (rhs)

Sean Corrigan

Breakdown to peak

of 'Super-Cycle'

GFC/QE

discontinuity

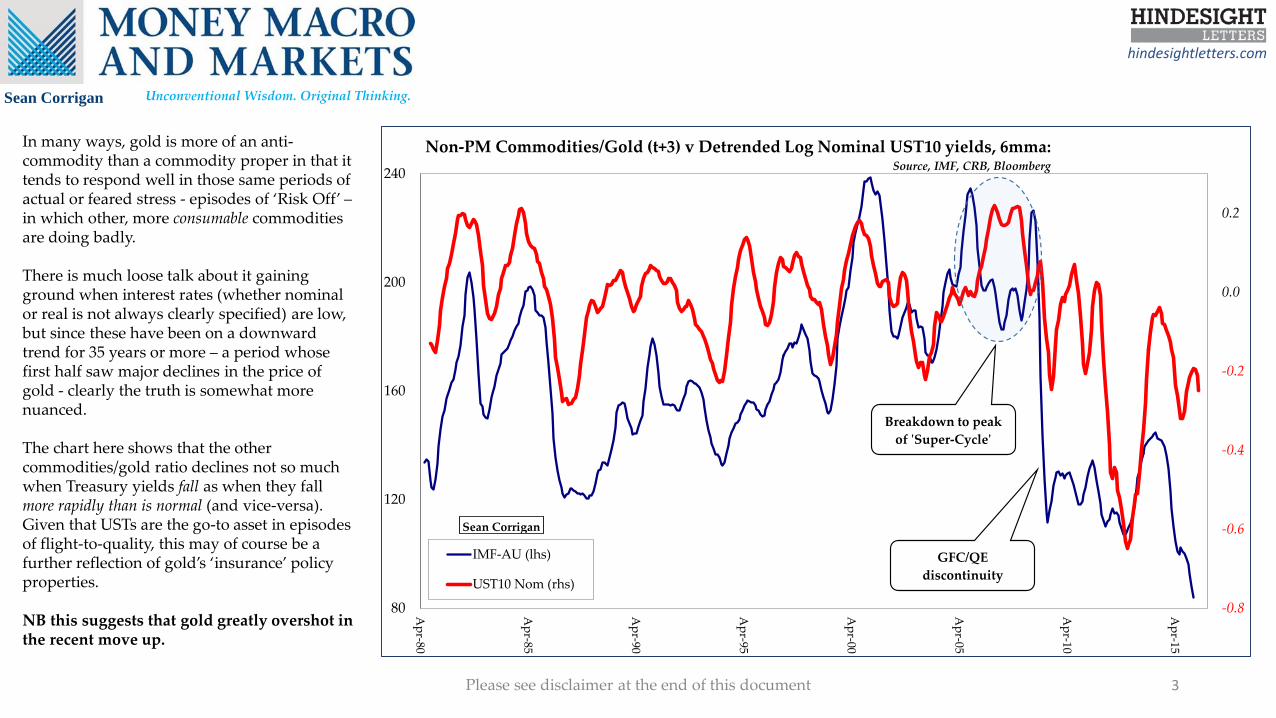

In many ways, gold is more of an anti-commodity than a commodity proper in that it tends to respond well in those same periods of actual or feared stress - episodes of ‘Risk Off’ –in which other, more consumable commodities are doing badly.

There is much loose talk about it gaining ground when interest rates (whether nominal or real is not always clearly specified) are low, but since these have been on a downward trend for 35 years or more – a period whose first half saw major declines in the price of gold - clearly the truth is somewhat more nuanced.

The chart here shows that the other commodities/gold ratio declines not so much when Treasury yields fall as when they fall more rapidly than is normal (and vice-versa).Given that USTs are the go-to asset in episodes of flight-to-quality, this may of course be a further reflection of gold’s ‘insurance’ policy properties.

NB this suggests that gold greatly overshot in the recent move up.

Unconventional Wisdom. Original Thinking.

hindesightletters.com

Please see disclaimer at the end of this document 4

Sean Corrigan

$600

$900

$1'200

$1'500

$1'800

€0

€200

€400

€600

€800

€1'000

Dec-06

Dec-07

Dec-08

Dec-09

Dec-10

Dec-11

Dec-12

Dec-13

Dec-14

Dec-15

Gold v TARGET2: Source - BUBA, Bloomberg

BUBA T2 (lhs)

SNB+BUBA

Gold (rhs)

Sean Corrigan

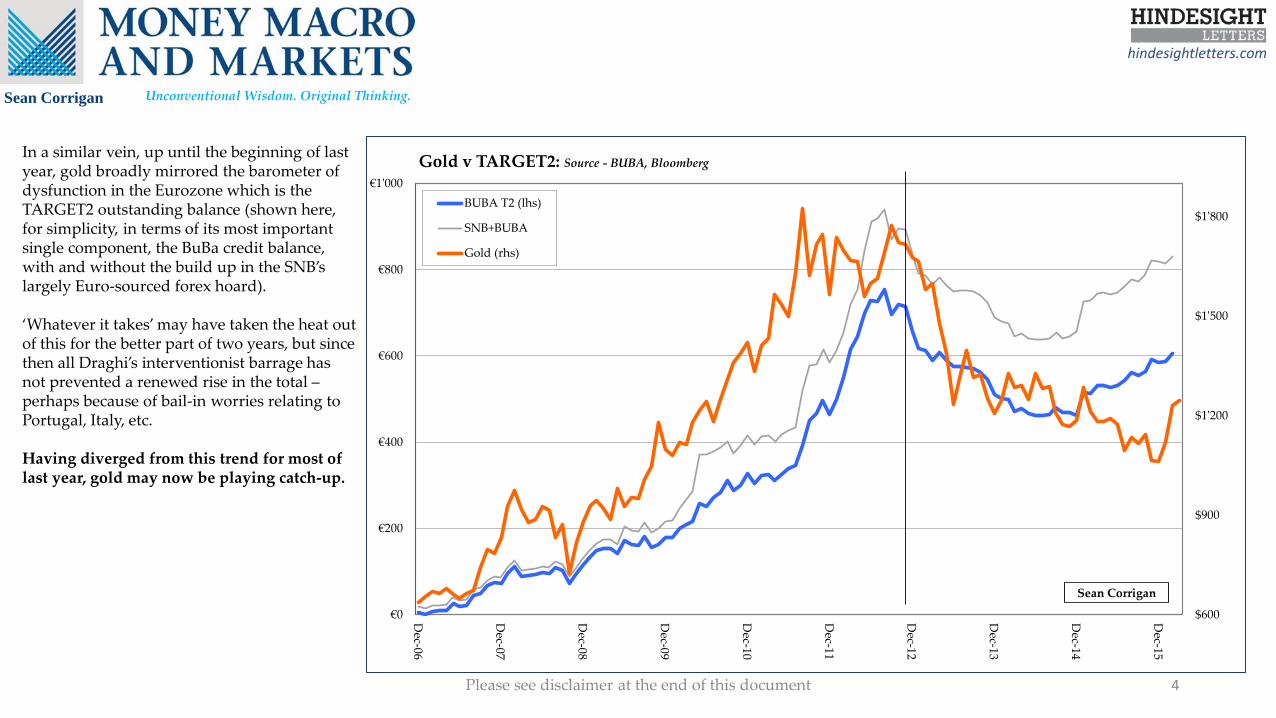

In a similar vein, up until the beginning of last year, gold broadly mirrored the barometer of dysfunction in the Eurozone which is the TARGET2 outstanding balance (shown here, for simplicity, in terms of its most important single component, the BuBa credit balance, with and without the build up in the SNB’s largely Euro-sourced forex hoard).

‘Whatever it takes’ may have taken the heat out of this for the better part of two years, but since then all Draghi’s interventionist barrage has not prevented a renewed rise in the total –perhaps because of bail-in worries relating to Portugal, Italy, etc.

Having diverged from this trend for most of last year, gold may now be playing catch-up.

Unconventional Wisdom. Original Thinking.

hindesightletters.com

Please see disclaimer at the end of this document 5

Sean Corrigan

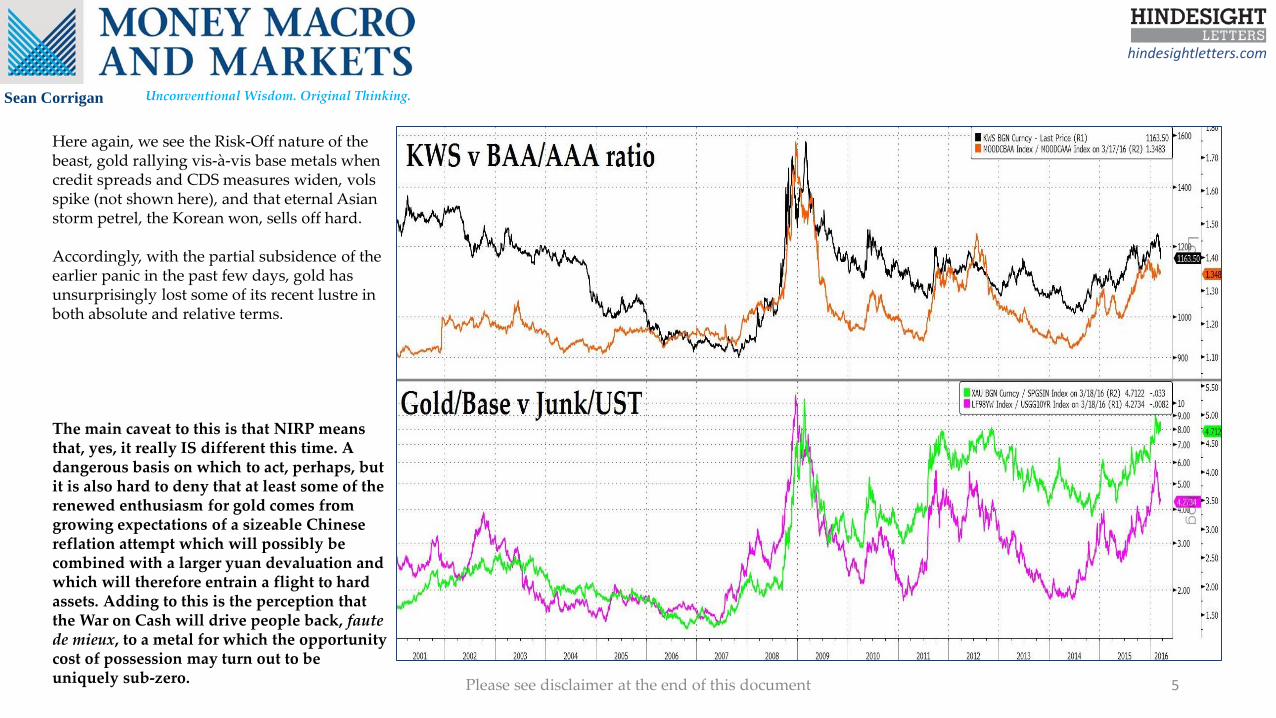

Here again, we see the Risk-Off nature of the beast, gold rallying vis-à-vis base metals when credit spreads and CDS measures widen, volsspike (not shown here), and that eternal Asian storm petrel, the Korean won, sells off hard.

Accordingly, with the partial subsidence of the earlier panic in the past few days, gold has unsurprisingly lost some of its recent lustre in both absolute and relative terms.

The main caveat to this is that NIRP means that, yes, it really IS different this time. A dangerous basis on which to act, perhaps, but it is also hard to deny that at least some of the renewed enthusiasm for gold comes from growing expectations of a sizeable Chinese reflation attempt which will possibly be combined with a larger yuan devaluation and which will therefore entrain a flight to hard assets. Adding to this is the perception that the War on Cash will drive people back, fautede mieux, to a metal for which the opportunity cost of possession may turn out to be uniquely sub-zero.

Unconventional Wisdom. Original Thinking.

hindesightletters.com

Please see disclaimer at the end of this document 6

Sean Corrigan

History

Unconventional Wisdom. Original Thinking.

hindesightletters.com

Please see disclaimer at the end of this document 7

Sean Corrigan

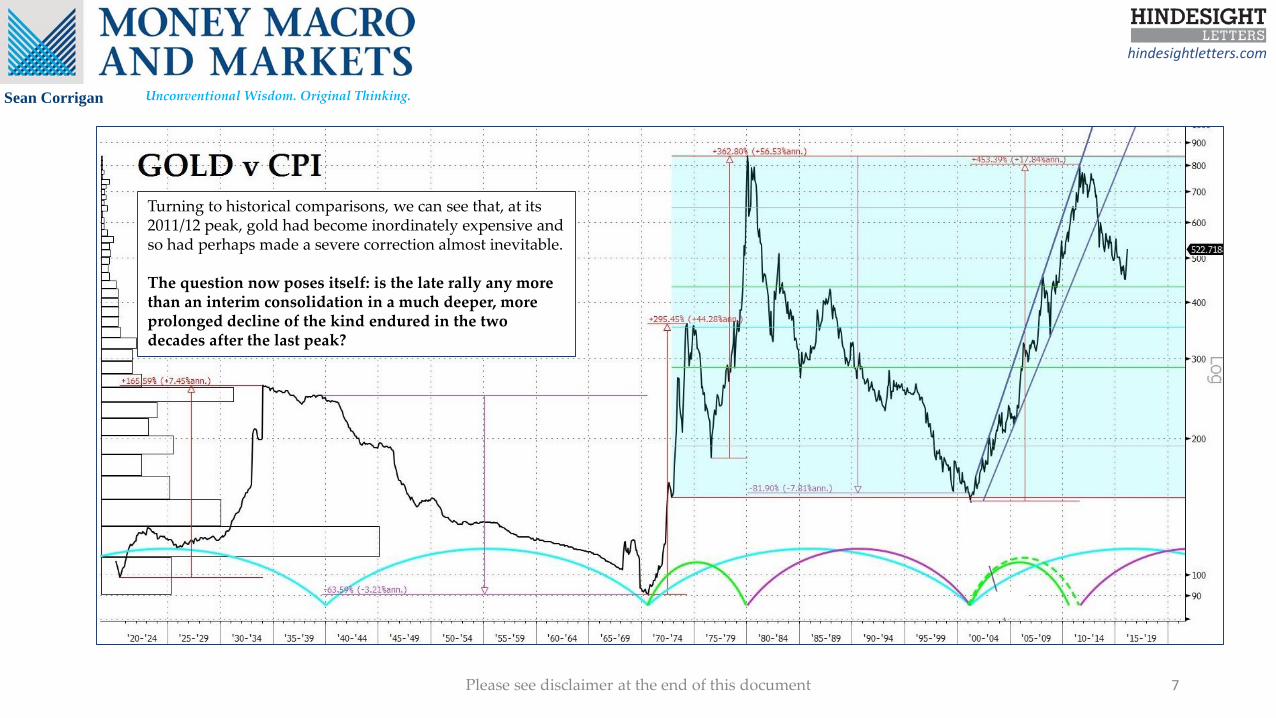

Turning to historical comparisons, we can see that, at its 2011/12 peak, gold had become inordinately expensive and so had perhaps made a severe correction almost inevitable.

The question now poses itself: is the late rally any more than an interim consolidation in a much deeper, more prolonged decline of the kind endured in the two decades after the last peak?

Unconventional Wisdom. Original Thinking.

hindesightletters.com

Please see disclaimer at the end of this document 8

Sean Corrigan

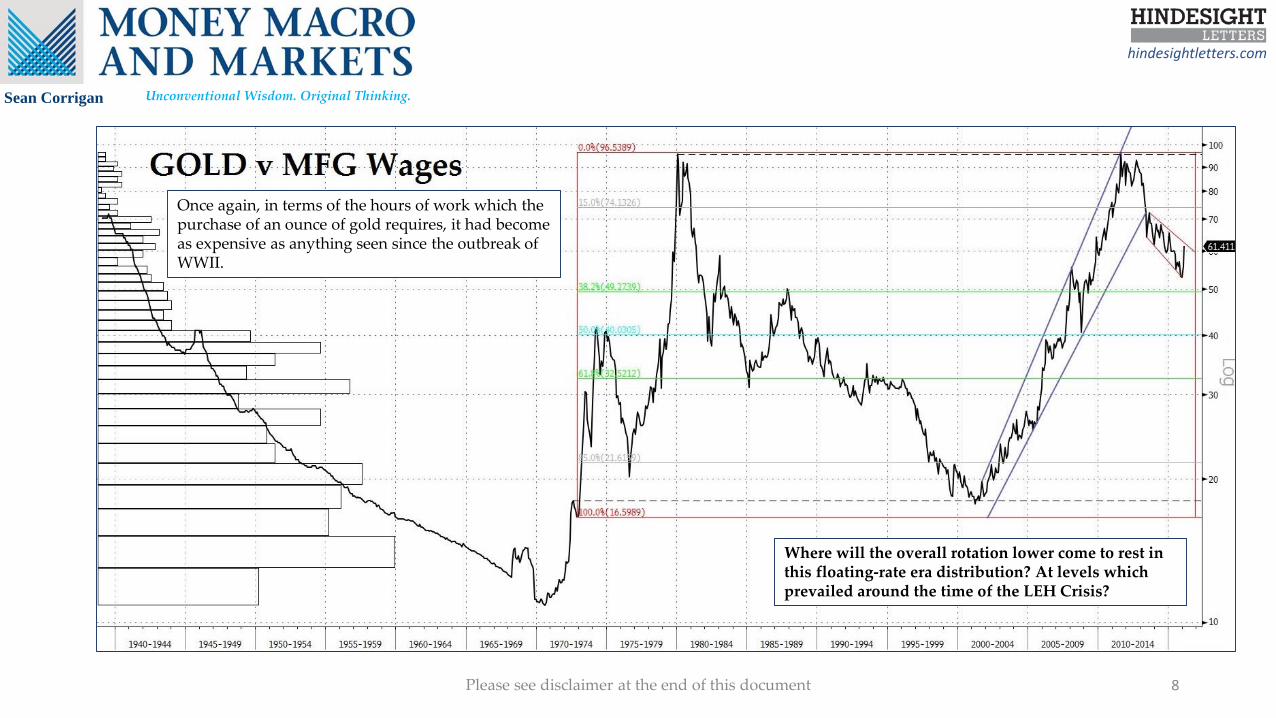

Once again, in terms of the hours of work which the purchase of an ounce of gold requires, it had become as expensive as anything seen since the outbreak of WWII.

Where will the overall rotation lower come to rest in this floating-rate era distribution? At levels which prevailed around the time of the LEH Crisis?

Unconventional Wisdom. Original Thinking.

hindesightletters.com

Please see disclaimer at the end of this document 9

Sean Corrigan

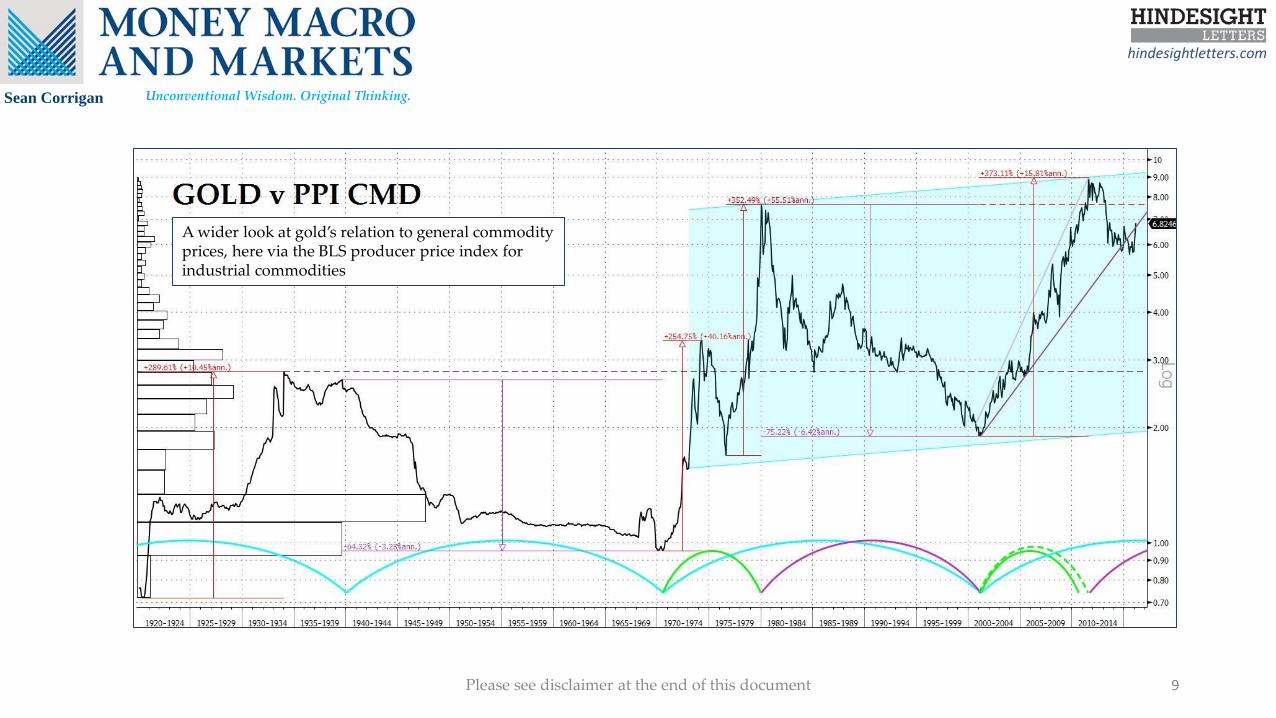

A wider look at gold’s relation to general commodity prices, here via the BLS producer price index for industrial commodities

Unconventional Wisdom. Original Thinking.

hindesightletters.com

Please see disclaimer at the end of this document 10

Sean Corrigan

-50.0

0.0

50.0

100.0

150.0

200.0

250.0

Dec-71

Dec-75

Dec-79

Dec-83

Dec-87

Dec-91

Dec-95

Dec-99

Dec-03

Dec-07

Dec-11

Dec-15

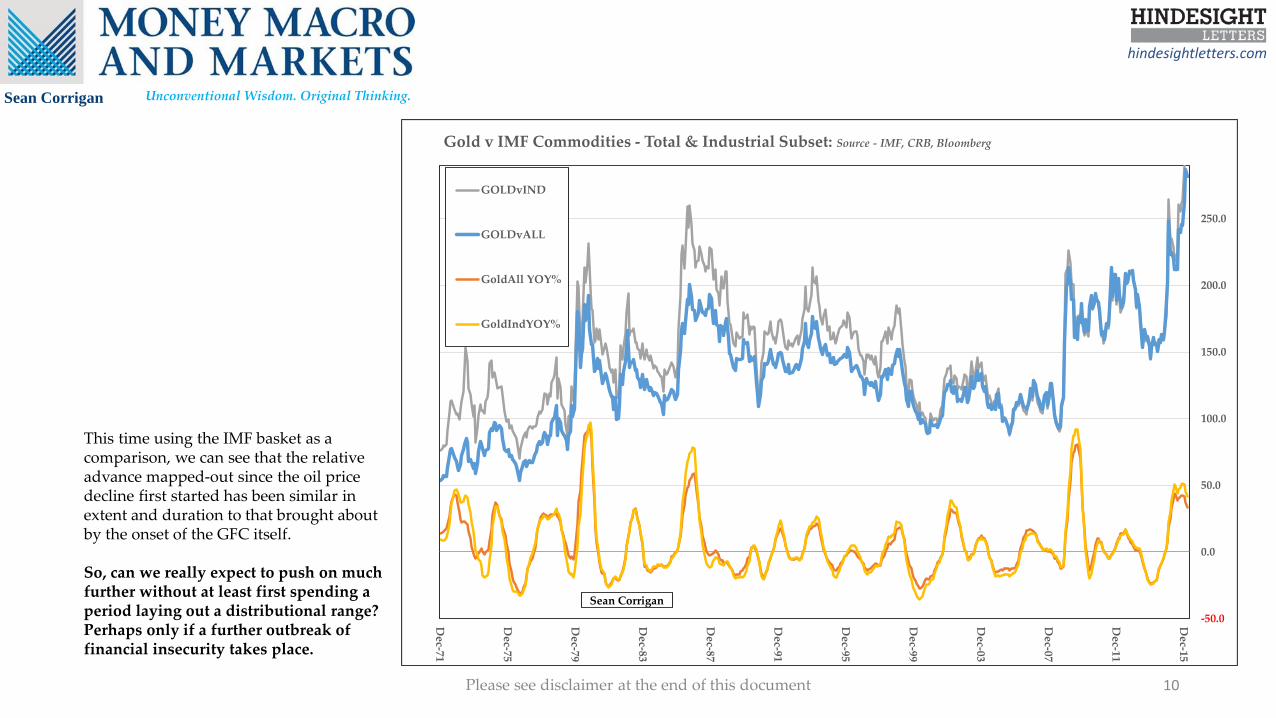

Gold v IMF Commodities - Total & Industrial Subset: Source - IMF, CRB, Bloomberg

GOLDvIND

GOLDvALL

GoldAll YOY%

GoldIndYOY%

Sean Corrigan

This time using the IMF basket as a comparison, we can see that the relative advance mapped-out since the oil price decline first started has been similar in extent and duration to that brought about by the onset of the GFC itself.

So, can we really expect to push on much further without at least first spending a period laying out a distributional range? Perhaps only if a further outbreak of financial insecurity takes place.

Unconventional Wisdom. Original Thinking.

hindesightletters.com

Please see disclaimer at the end of this document 11

Sean Corrigan

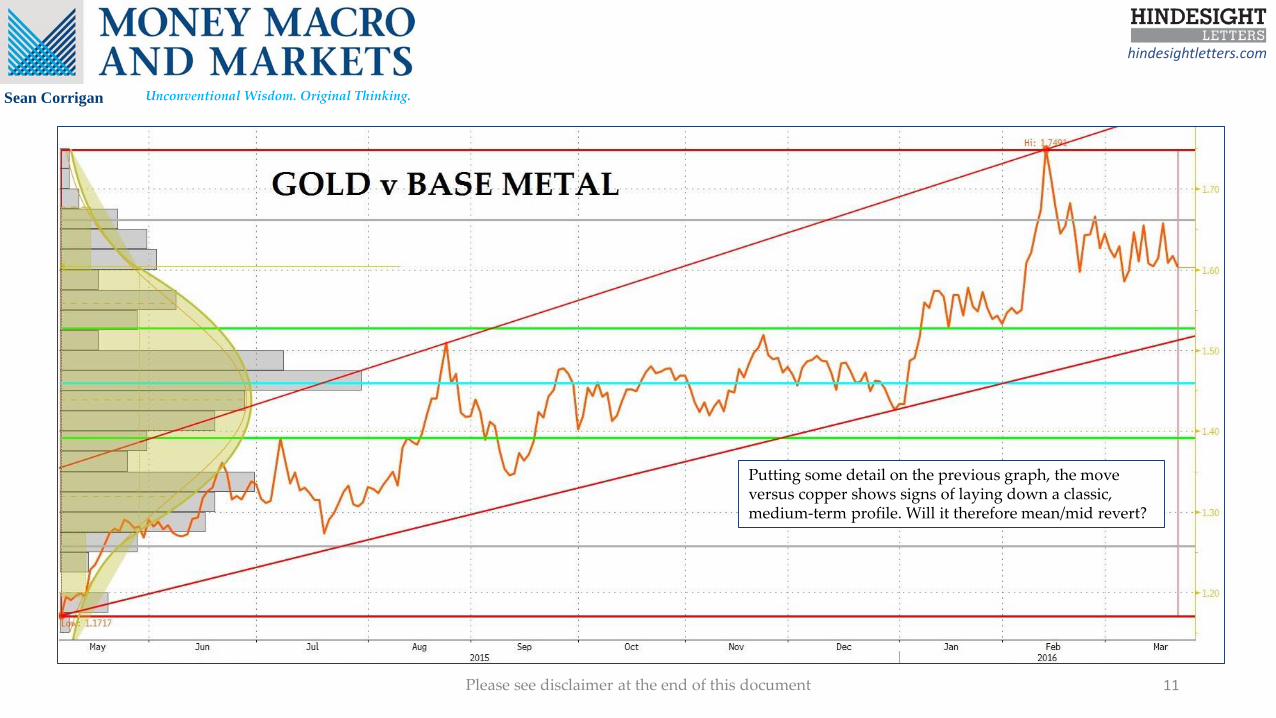

Putting some detail on the previous graph, the move versus copper shows signs of laying down a classic, medium-term profile. Will it therefore mean/mid revert?

Unconventional Wisdom. Original Thinking.

hindesightletters.com

Please see disclaimer at the end of this document 12

Sean Corrigan

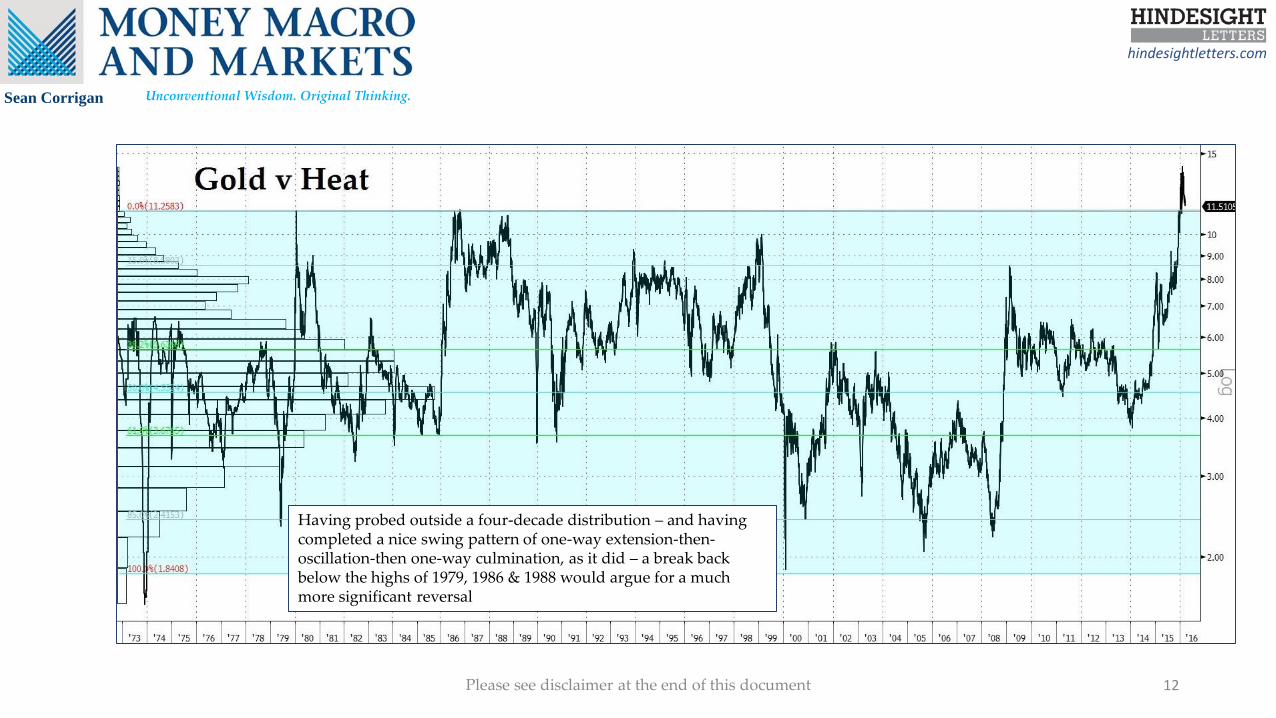

Having probed outside a four-decade distribution – and having completed a nice swing pattern of one-way extension-then-oscillation-then one-way culmination, as it did – a break back below the highs of 1979, 1986 & 1988 would argue for a much more significant reversal

Unconventional Wisdom. Original Thinking.

hindesightletters.com

Please see disclaimer at the end of this document 13

Sean Corrigan

Indeed, against crude oil, such a rejection of those new highs has already taken place.

Unconventional Wisdom. Original Thinking.

hindesightletters.com

Please see disclaimer at the end of this document 14

Sean Corrigan

One of the few comparisons in which it has not this time reached extremes, but rather has returned the ratio to the (decidedly off-centre) high-volume area of the last 20 years’ distribution

Unconventional Wisdom. Original Thinking.

hindesightletters.com

Please see disclaimer at the end of this document 15

Sean Corrigan

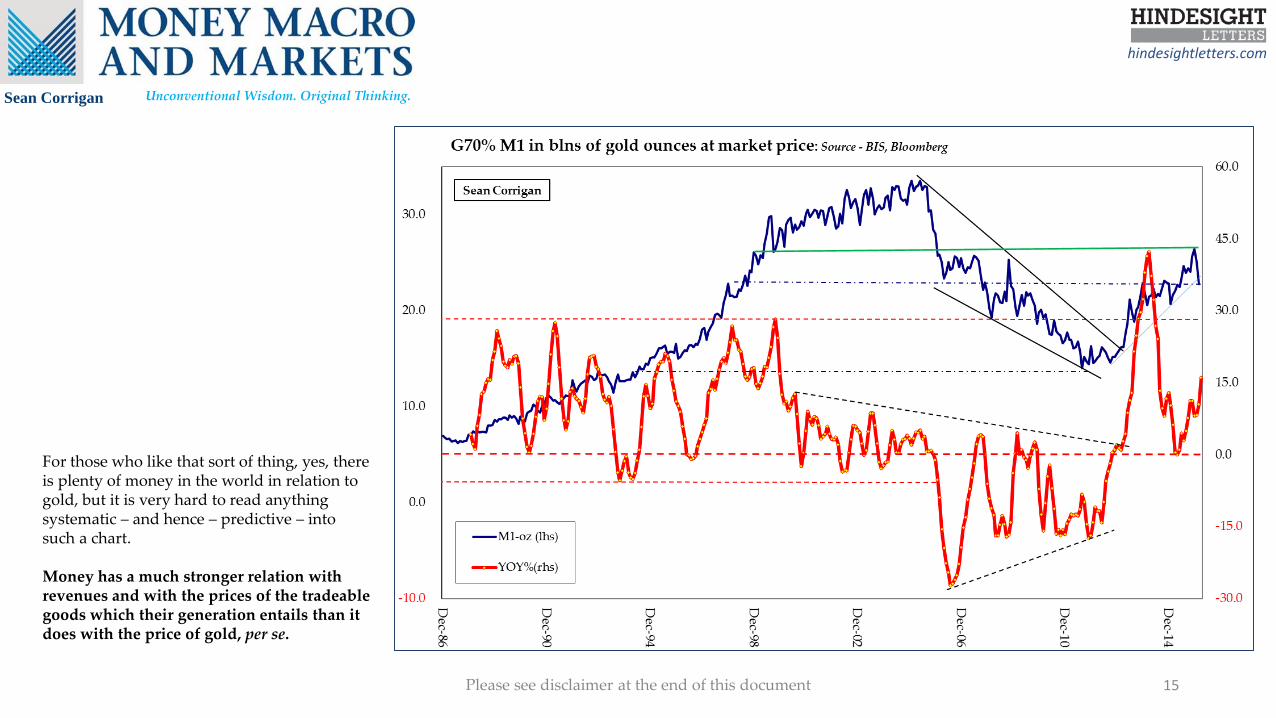

For those who like that sort of thing, yes, there is plenty of money in the world in relation to gold, but it is very hard to read anything systematic – and hence – predictive – into such a chart.

Money has a much stronger relation with revenues and with the prices of the tradeable goods which their generation entails than it does with the price of gold, per se.

Unconventional Wisdom. Original Thinking.

hindesightletters.com

Please see disclaimer at the end of this document 16

Sean Corrigan

Diggers v the Dug

Unconventional Wisdom. Original Thinking.

hindesightletters.com

Please see disclaimer at the end of this document 17

Sean Corrigan

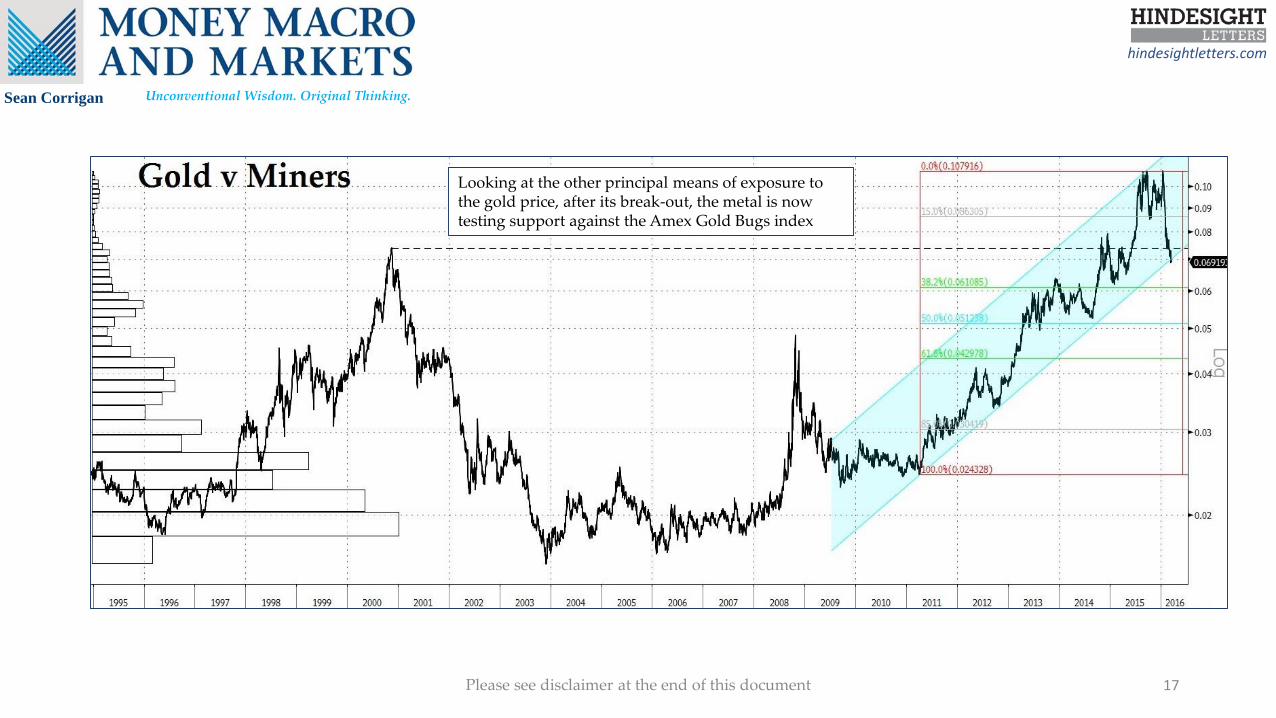

Looking at the other principal means of exposure to the gold price, after its break-out, the metal is now testing support against the Amex Gold Bugs index

Unconventional Wisdom. Original Thinking.

hindesightletters.com

Please see disclaimer at the end of this document 18

Sean Corrigan

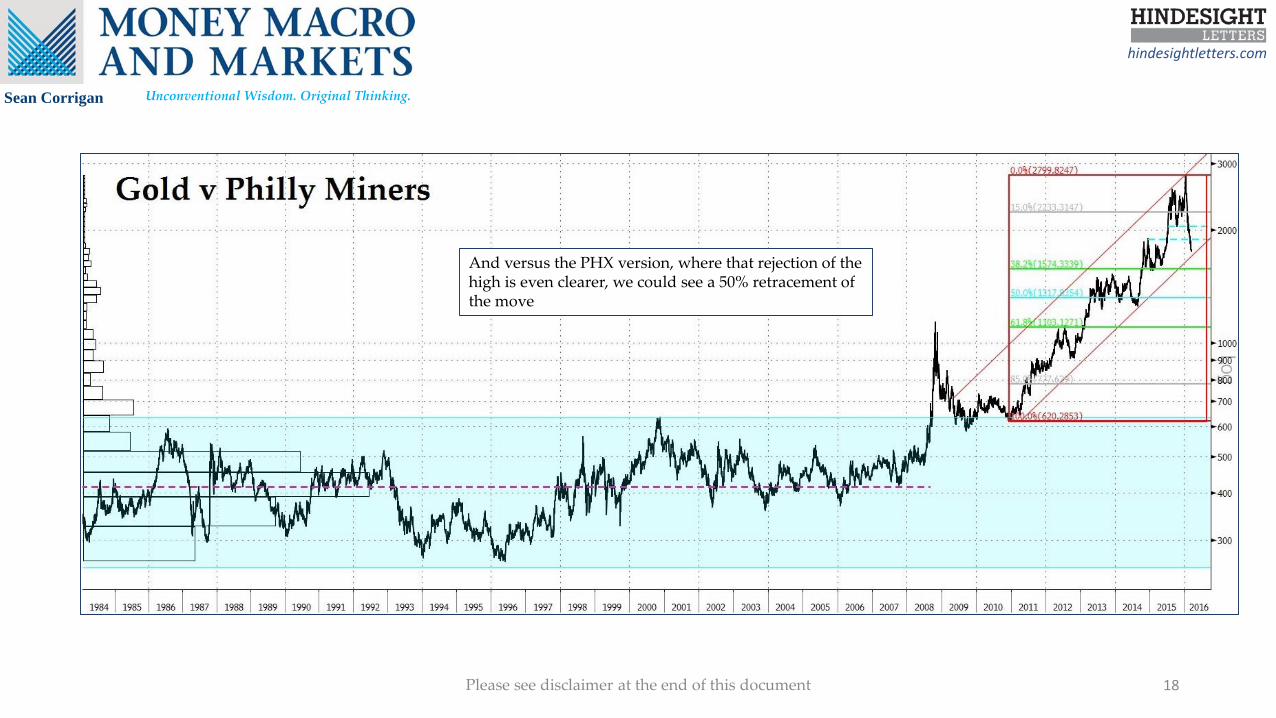

And versus the PHX version, where that rejection of the high is even clearer, we could see a 50% retracement of the move

Unconventional Wisdom. Original Thinking.

hindesightletters.com

Please see disclaimer at the end of this document 19

Sean Corrigan

Positioning

Unconventional Wisdom. Original Thinking.

hindesightletters.com

Please see disclaimer at the end of this document 20

Sean Corrigan

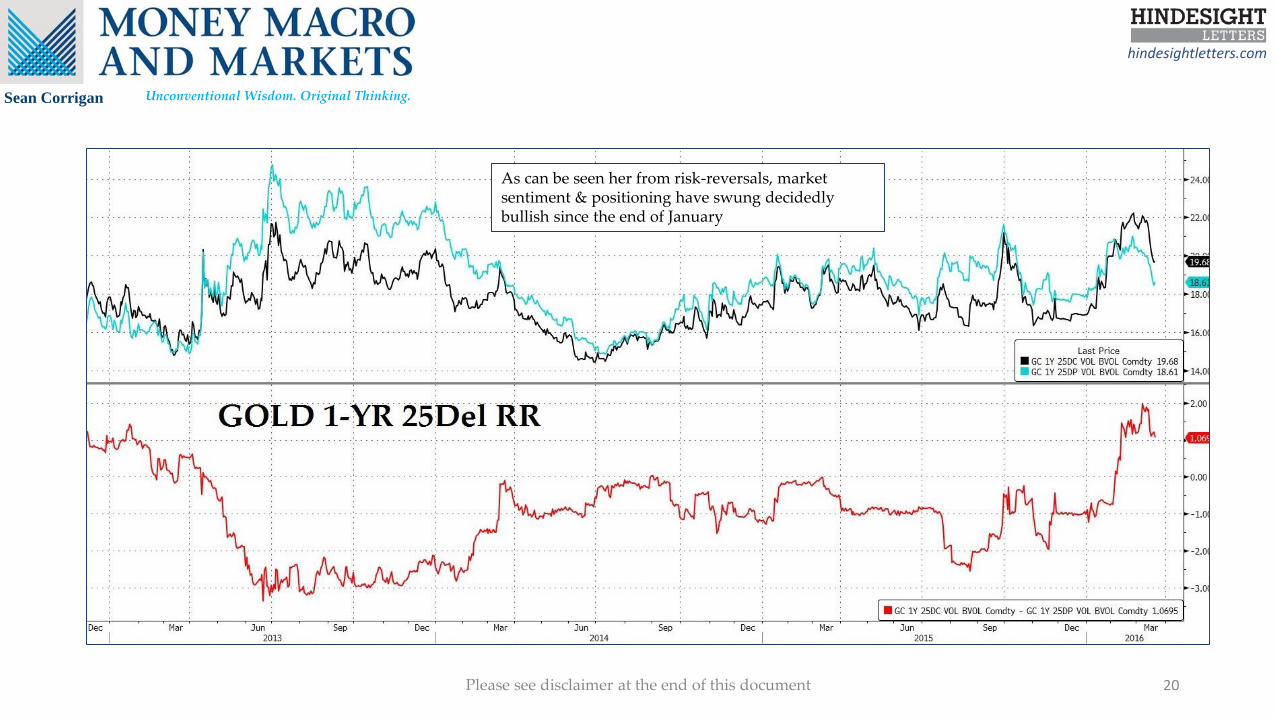

As can be seen her from risk-reversals, market sentiment & positioning have swung decidedly bullish since the end of January

Unconventional Wisdom. Original Thinking.

hindesightletters.com

Please see disclaimer at the end of this document 21

Sean Corrigan

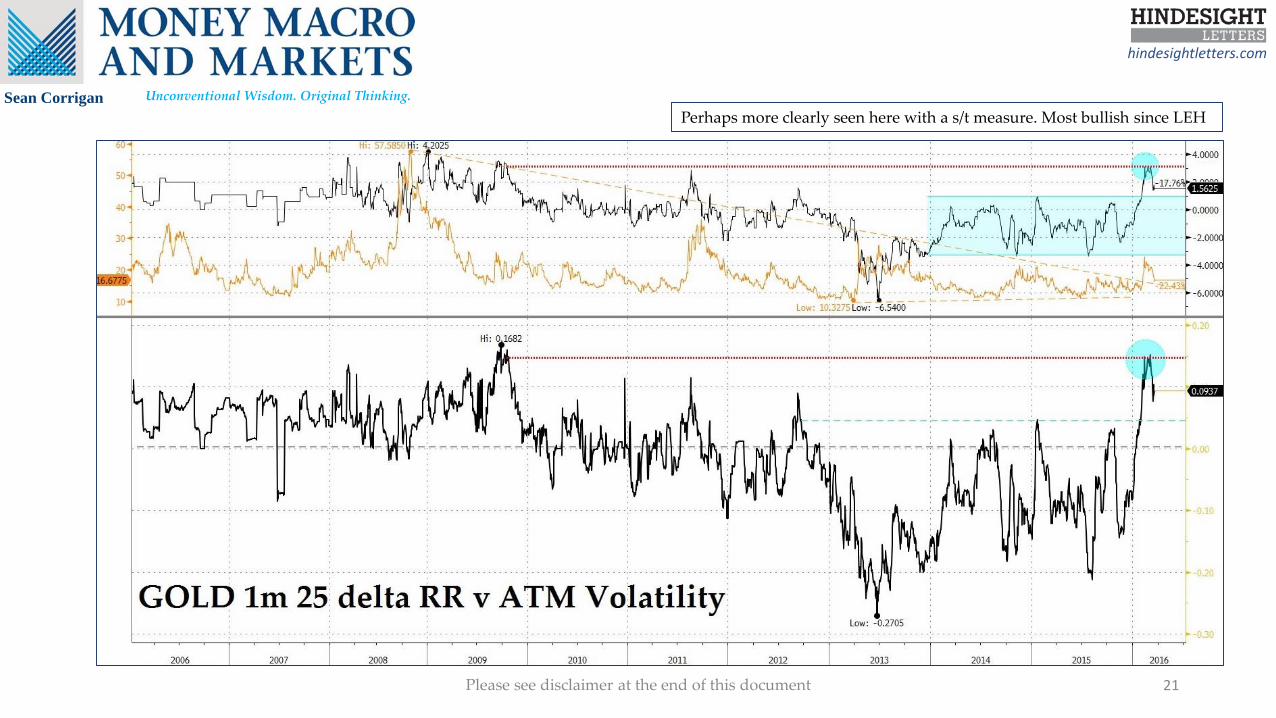

Perhaps more clearly seen here with a s/t measure. Most bullish since LEH

Unconventional Wisdom. Original Thinking.

hindesightletters.com

Please see disclaimer at the end of this document 22

Sean CorriganNot much short interest in the ETF

Unconventional Wisdom. Original Thinking.

hindesightletters.com

Please see disclaimer at the end of this document 23

Sean Corrigan

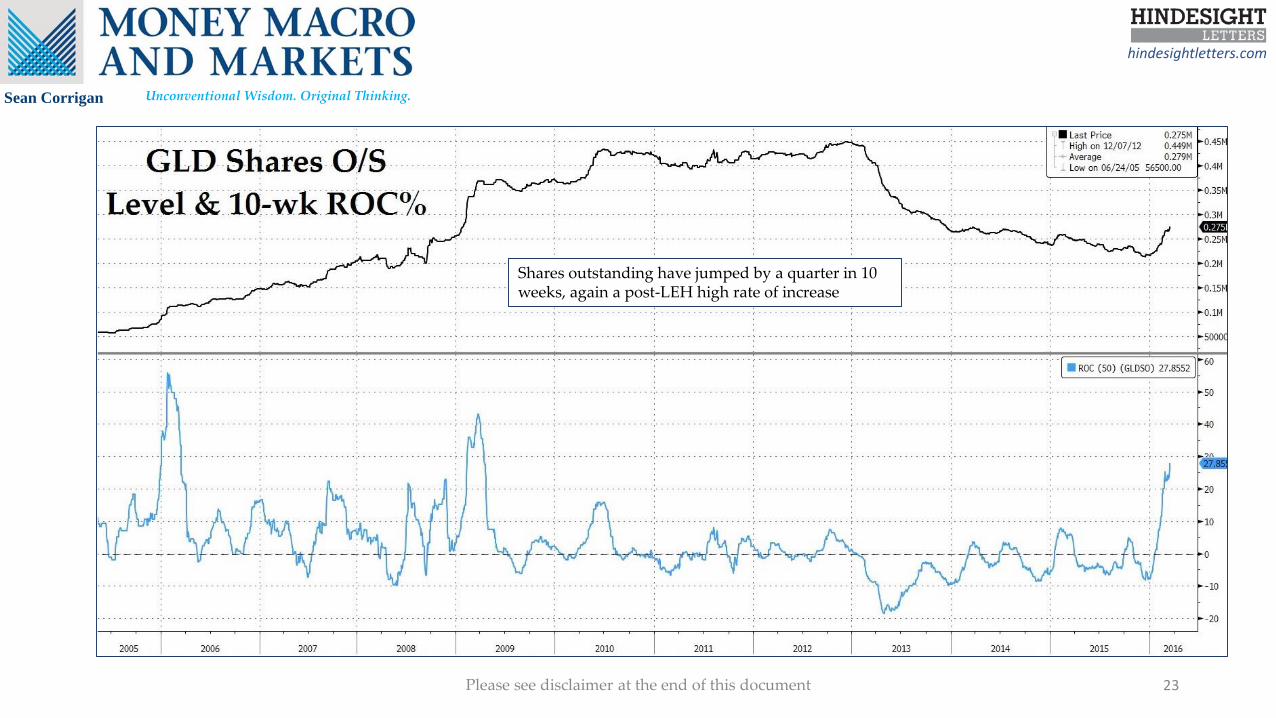

Shares outstanding have jumped by a quarter in 10 weeks, again a post-LEH high rate of increase

Unconventional Wisdom. Original Thinking.

hindesightletters.com

Please see disclaimer at the end of this document 24

Sean Corrigan

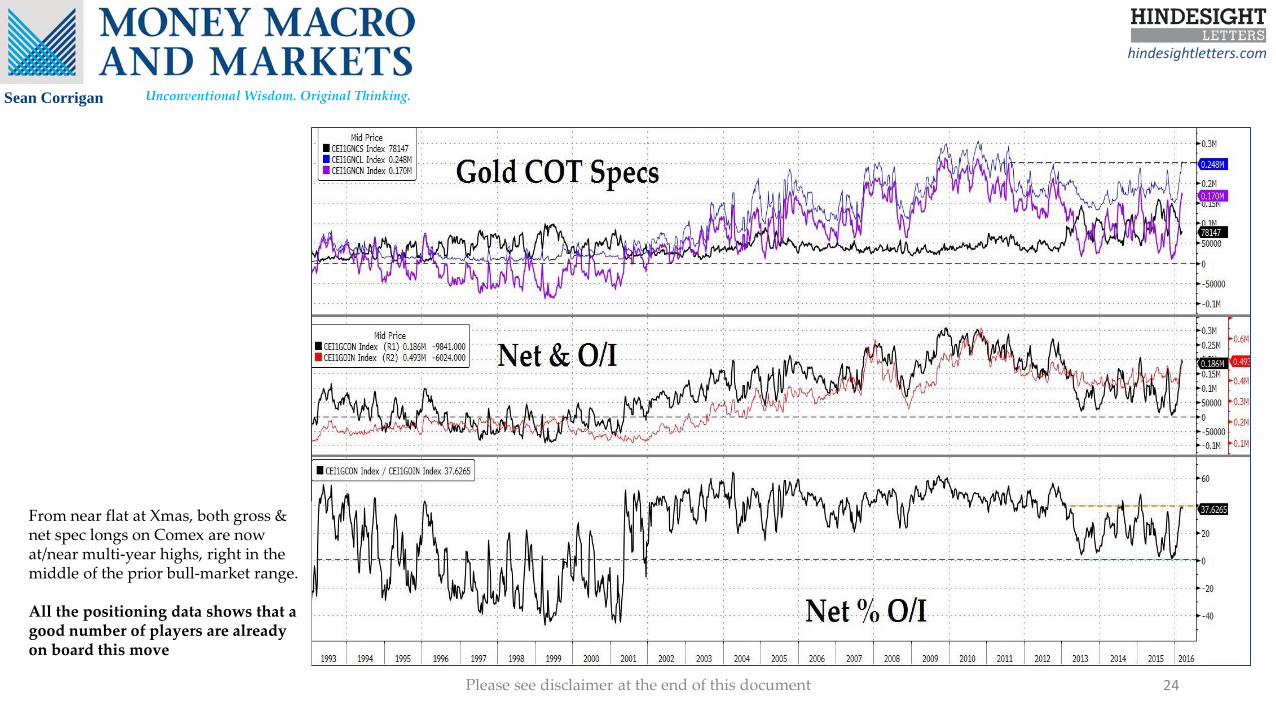

From near flat at Xmas, both gross & net spec longs on Comex are now at/near multi-year highs, right in the middle of the prior bull-market range.

All the positioning data shows that a good number of players are already on board this move

Unconventional Wisdom. Original Thinking.

hindesightletters.com

Please see disclaimer at the end of this document 25

Sean Corrigan

Technicals

Unconventional Wisdom. Original Thinking.

hindesightletters.com

Please see disclaimer at the end of this document 26

Sean Corrigan

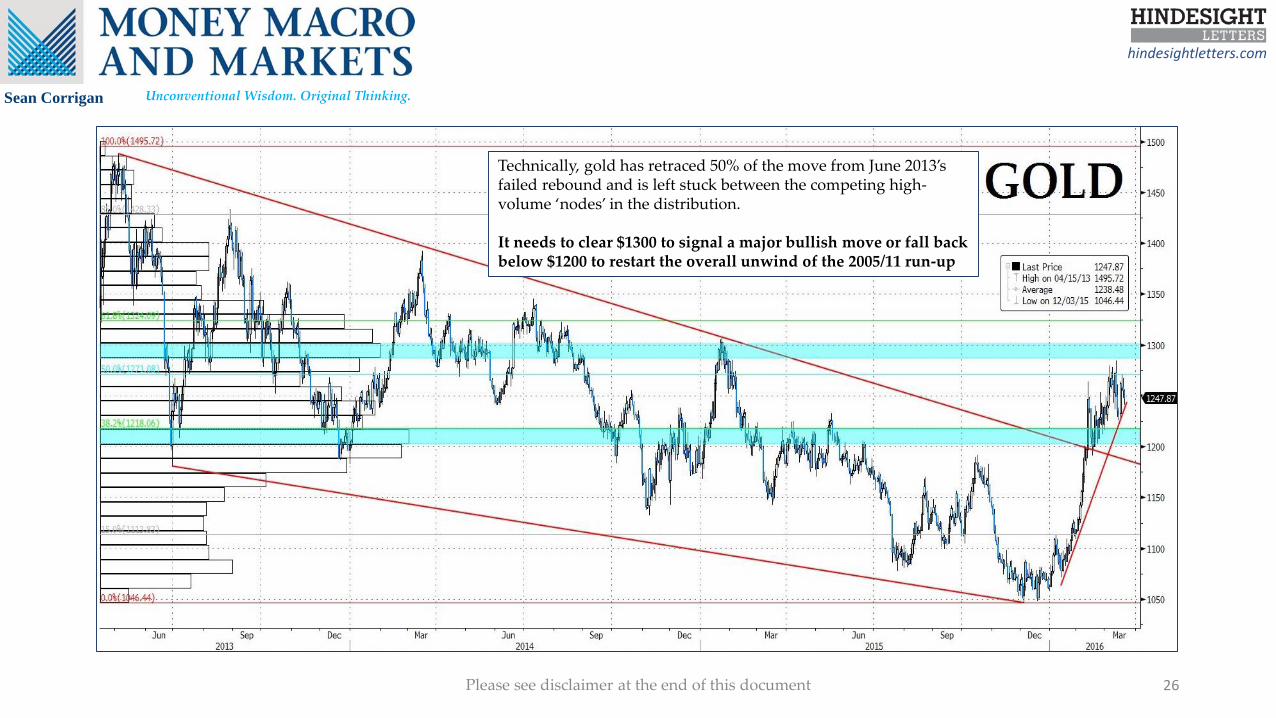

Technically, gold has retraced 50% of the move from June 2013’s failed rebound and is left stuck between the competing high-volume ‘nodes’ in the distribution.

It needs to clear $1300 to signal a major bullish move or fall back below $1200 to restart the overall unwind of the 2005/11 run-up

Unconventional Wisdom. Original Thinking.

hindesightletters.com

Please see disclaimer at the end of this document 27

Sean Corrigan

Abstracting from changes in the US dollar’s value, things are more unequivocally positive in that we have left behind the 2013/15 balance area and are once more bumping against the lower bound of 2011/13’s record-setting sub-range.

The potential buyer is, however, parting with his cash (negative-yielding or not) at all but unprecedented levels, so no downside stubbornness should be indulged in and not too much toleration of any loss of momentum would seem to be the watchwords.

Active risk management in such a circumstance is something my colleagues at Hinde Capital would be happy to discuss with you

Unconventional Wisdom. Original Thinking.

hindesightletters.com

DISCLAIMER

This newsletter is intended to give general advice only on the importance of Macro investments. The investments mentioned are not necessarily suitable for any individual, and you should use this information in conjunction with other advice and research to determine its suitability for your own circumstances and risk preferences. The value of all securities and investments, and the income from them, can fall as well as rise. Your investments may be subject to sudden and large falls in value and you may get back nothing at all. You should not buy any of the securities or other investments mentioned with money you cannot afford to lose. In some cases there may be significant charges which may reduce the value of your investment. You run an extra risk of losing money when you buy shares in certain securities where there is a big difference between the buying price and the selling price. If you have to sell them immediately, you may get back much less than you paid for them. The price may change quickly, particularly if the securities have an element of gearing. In the case of investment trusts and certain other funds, they may use or propose to use the borrowing of money to increase holdings of investments or invest in other securities with a similar strategy and as a result movements in the price of the securities may be more volatile than the movements in the price of underlying investments. Some investments may involve a high degree of ‘gearing’ or ‘leverage’. This means that a small movement in the price of the underlying asset may have a disproportionately dramatic effect on your investment. A relatively small adverse movement in the price of the underlying asset can result in the loss of the whole of your original investment. Changes in rates of exchange may have an adverse effect on the value or price of the investment in sterling terms, and you should be aware they may be additional dealing, transaction and custody charges for certain instruments traded in a currency other than sterling. Some investments may not be quoted on a recognised investment exchange and as a result you may find them to be ‘illiquid’. You may not be able to trade your illiquid investments, and in certain circumstances it may be difficult or impossible to sell or realise the investment. Investment in any of the assets mentioned may have tax consequences and on these you should consult your tax adviser. The opinions of the authors and/or interviewees of/in each article are their own, and are not necessarily those of the publisher. We have taken all reasonable care to ensure that all statements of fact and opinion contained in this publication are fair and accurate in all material respects. All data is from sources we consider reliable but its accuracy cannot be guaranteed. Investors should seek appropriate professional advice if any points are unclear. HindeSight Publishing Ltd is responsible for the research ideas contained within. They or any of the contributors or other associates of the publisher may have a beneficial interest in any of the investments mentioned in this newsletter.Disclosures of holdings: None relevant to any content discussed within this issue of the newsletter

Copyright ©HindeSight Publishing 2016. Any disclosure, copy, reproduction by any means, distribution or other action in reliance on the contents of this document without the prior written consent of HindeSight Publishing is strictly prohibited and could lead to legal action.

28

Sean Corrigan