GLS Group – Company presentation Presentation... · GLS | Company Overview, June 2016 Disclaimer...

18

GLS Group – Company presentation June 2016, Neuenstein

Transcript of GLS Group – Company presentation Presentation... · GLS | Company Overview, June 2016 Disclaimer...

GLS Group – Company presentation

June 2016, Neuenstein

GLS | Company Overview, June 2016

Disclaimer

2

“This presentation is being provided for informational purposes

only and is not intended to, nor does it, constitute investment

advice or any solicitation to buy, hold or sell securities or other

financial instruments.

None of Royal Mail, its affiliates or their respective directors,

officers and employees shall accept any liability whatsoever for

the consequences of any reliance upon or actions taken based

on any of the information in this presentation.”

GLS | Company Overview, June 2016

In what kind of market does GLS operate?

GLS operates in an attractive but challenging growth market

3

?

GLS | Company Overview, June 2016

GLS is a logistics provider mainly serving the CEP market segment

4

Market Definition

The broadest description for the industrial sector in which GLS operates is ‘Industrial Transportation’. This sector can be further segmented into Logistics

Logistics include the following segments:

o CEP (Courier, Express and Parcels)

o Letter

o Freight

o Storage/ Warehousing

GLS is mainly active in the CEP market segment

GLS | Company Overview, June 2016

Much of the growth in the European parcels sector has been driven by B2C deliveries

5

European Parcel Market*, Split by Segment (B2B, B2C, C2X)**, Revenue Bn. €, 2010-2015

36 36 35 35 35 35

6 6 7 8 8 9

7 8 10 12 14 15

0

5

10

15

20

25

30

35

40

45

50

55

60 57 +4%

2014 2013

55

2012

52

2011

50

2010

49

CAGR

+17%

-1%

• Expansion of eCommerce has made B2C deliveries a faster-growing segment growing on average by +17% p.a

• The market segment of parcels sent by consumers has been growing by +9% p.a.

• B2B revenue was impacted by the period of slow economic develop-ment, resulting in an average decline of -1% p.a.

C2X B2B Source: Apex Insight European Parcels: Market Insight Report, 2016

** All service levels are included (time definite and deferred). Adjacent services, such as mail, pallet distribution, groupage, freight forwarding, sameday courier and contract logistics are excluded

2015

59

B2C

+9%

* Includes: DE, UK, FRA, IT, ESP, NL, BE, PL, CH, SWE, NOR, AUT, DK, GR, FIN, PT, IRL, CZ, RO, HU, SVK, CR, HR, BG, SLO, SRB, LTU, LVA, LUX, EST, BIH, ISL, ALB, MKD, MLT, MNE

Bn. €

GLS | Company Overview, June 2016

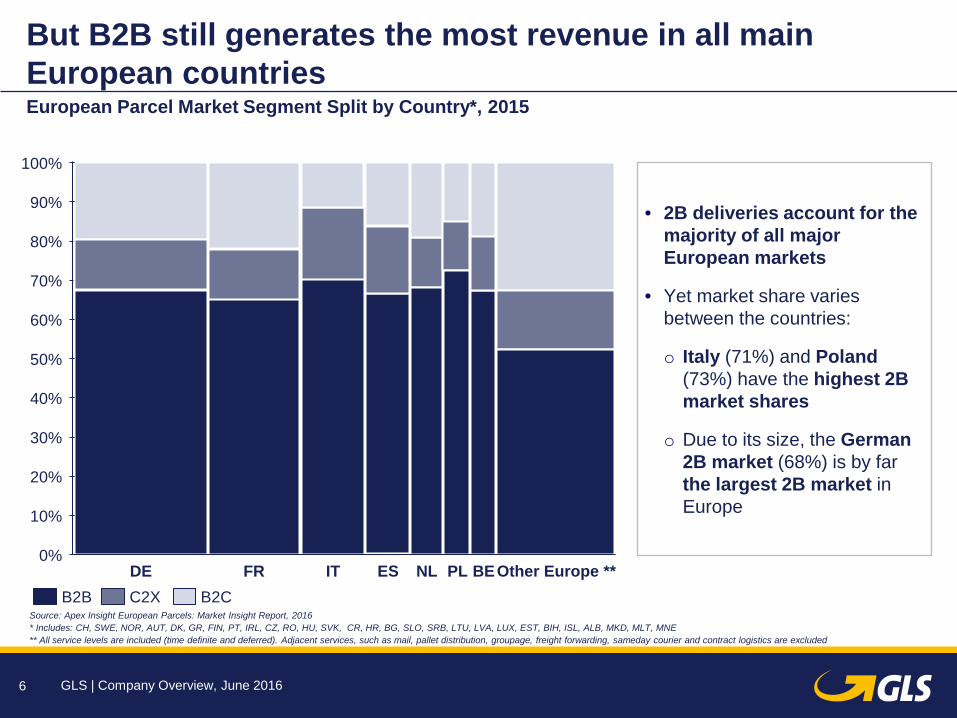

But B2B still generates the most revenue in all main European countries

6

European Parcel Market Segment Split by Country*, 2015

30%

20%

10%

100%

90%

80%

70%

60%

50%

40%

0% DE FR IT Other Europe ** PL BE NL ES

• 2B deliveries account for the majority of all major European markets

• Yet market share varies between the countries:

o Italy (71%) and Poland (73%) have the highest 2B market shares

o Due to its size, the German 2B market (68%) is by far the largest 2B market in Europe

C2X B2B Source: Apex Insight European Parcels: Market Insight Report, 2016

** All service levels are included (time definite and deferred). Adjacent services, such as mail, pallet distribution, groupage, freight forwarding, sameday courier and contract logistics are excluded

B2C

* Includes: CH, SWE, NOR, AUT, DK, GR, FIN, PT, IRL, CZ, RO, HU, SVK, CR, HR, BG, SLO, SRB, LTU, LVA, LUX, EST, BIH, ISL, ALB, MKD, MLT, MNE

GLS | Company Overview, June 2016

Competitive Landscape

7

Competitive Landscape European Parcel Market

Independent local services

• Independent / single country players which focus on niches

• Hermes, largest of the independent players (backed up by Otto Group parcel volume)

National postal companies

• Large providers which are strong in home market

• Providers in Southern Europe play much smaller role in national markets

Integrators

• DHL, overall leader across Europe • FedEx, became No 2 in Europe after

acquiring TNT • UPS, global leader and currently No

3 in Europe

European networks

• GLS, largest European network • DPD, second to DHL in the number

of parcels carried in Europe • Independent carriers which work in

partnerships (Eurodis)

Potential new entrants

• Retail companies could potentially in-source some of its parcels traffic (mainly for same day delivery) and thus raise standards

Four groups of distinct parcel carriers and potentially new entrants compete in the European market

GLS | Company Overview, June 2016

Growing E-Commerce, further pressure on prices and growing cross-border markets shape the parcel market

8

Three main structural Market Trends

E-Commerce is main growth factor

leading to convergence of parcels segments (B2B, B2C,

C2C)

CEP companies create service improvements particularly on

last mile delivery and communication with

consignees

Pressure on prices driven by large customers and pooled purchasing activities of

SME who themselves suffer from consolidation and increased

price pressure

CEP companies need improved productivity

Cross-border market grows faster than domestic segment and suffers strongly from price

pressure

CEP market starts to form country clusters which results

in (inter)national market consolidation

2

1 2 3

GLS | Company Overview, June 2016

Who is the GLS Group?

GLS covers 41 states in Europe with parcel services, the majority via own subsidiaries, others via partner companies

9

?

GLS | Company Overview, June 2016

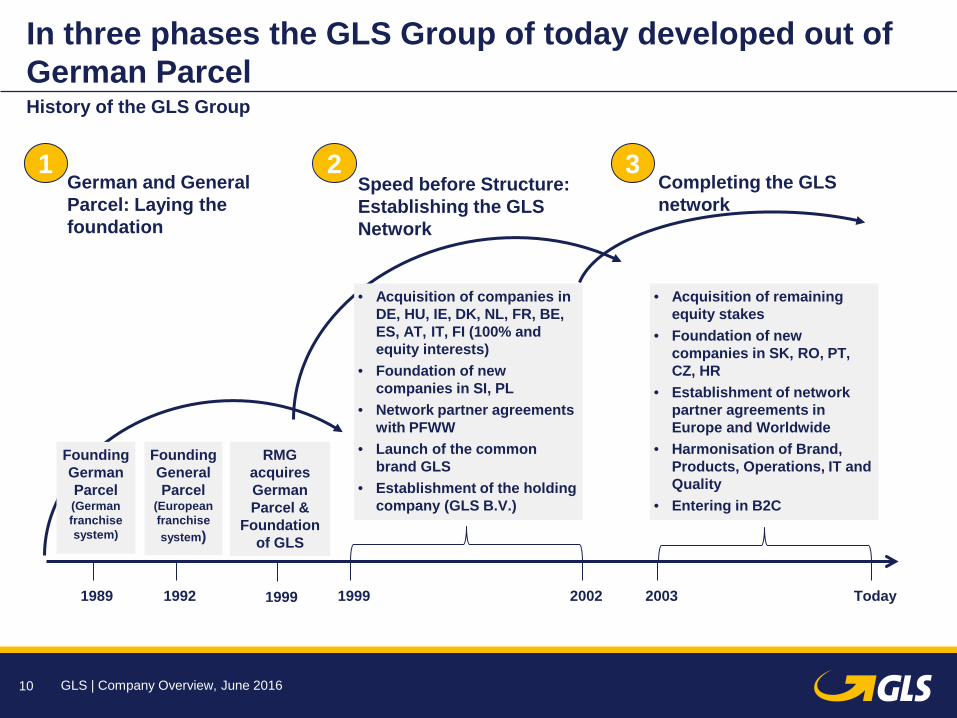

In three phases the GLS Group of today developed out of German Parcel

10

History of the GLS Group

1989 1992 1999

German and General Parcel: Laying the foundation

Speed before Structure: Establishing the GLS Network

Completing the GLS network

1999 2002 2003 Today

1 2 3

Founding German Parcel (German franchise system)

Founding General Parcel

(European franchise system)

RMG acquires German Parcel &

Foundation of GLS

• Acquisition of remaining equity stakes

• Foundation of new companies in SK, RO, PT, CZ, HR

• Establishment of network partner agreements in Europe and Worldwide

• Harmonisation of Brand, Products, Operations, IT and Quality

• Entering in B2C

• Acquisition of companies in DE, HU, IE, DK, NL, FR, BE, ES, AT, IT, FI (100% and equity interests)

• Foundation of new companies in SI, PL

• Network partner agreements with PFWW

• Launch of the common brand GLS

• Establishment of the holding company (GLS B.V.)

GLS | Company Overview, June 2016

Today, GLS is a leading player in the European parcel market with more than 2 bn. €uro turnover

11

Overview GLS 2016

Founded in 1999, with strong historical roots in nearly all domestic markets, GLS is one of the leading parcel service providers in Europe today

431 million parcels

(FY 2015/16)

> 220,000 customers*

€ 2.2 billion turnover

(FY 2015/16)

* Including franchisees in Italy

GLS | Company Overview, June 2016

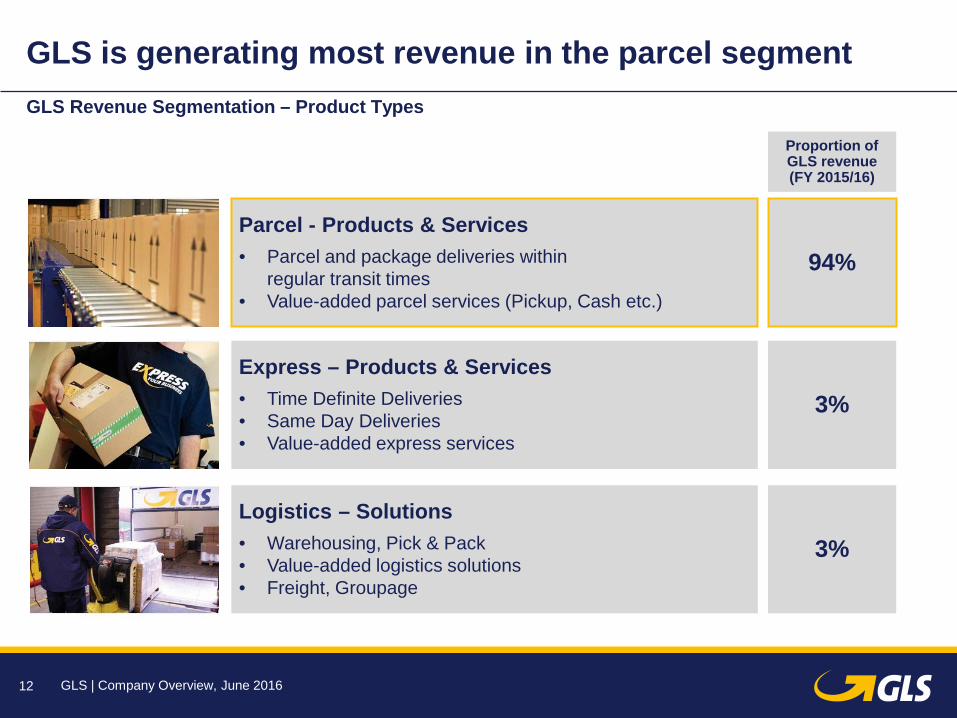

GLS is generating most revenue in the parcel segment

12

GLS Revenue Segmentation – Product Types

Proportion of GLS revenue (FY 2015/16)

Parcel - Products & Services • Parcel and package deliveries within

regular transit times • Value-added parcel services (Pickup, Cash etc.)

Express – Products & Services • Time Definite Deliveries • Same Day Deliveries • Value-added express services

Logistics – Solutions • Warehousing, Pick & Pack • Value-added logistics solutions • Freight, Groupage

94%

3%

3%

GLS | Company Overview, June 2016

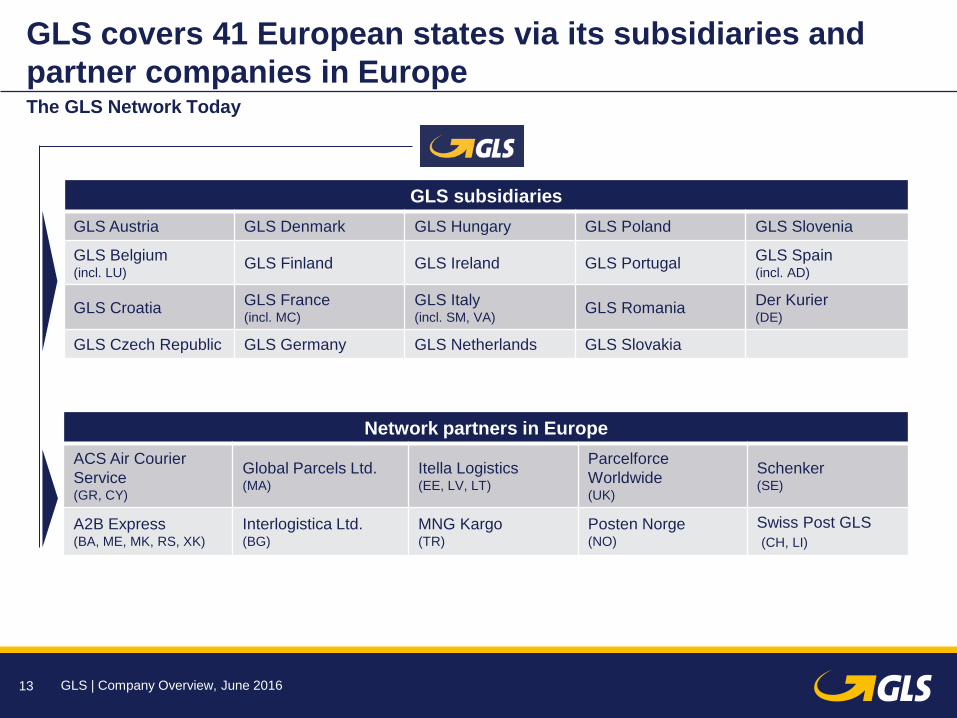

GLS covers 41 European states via its subsidiaries and partner companies in Europe

13

The GLS Network Today

GLS subsidiaries GLS Austria GLS Denmark GLS Hungary GLS Poland GLS Slovenia

GLS Belgium (incl. LU) GLS Finland GLS Ireland GLS Portugal GLS Spain

(incl. AD)

GLS Croatia GLS France (incl. MC)

GLS Italy (incl. SM, VA) GLS Romania Der Kurier

(DE)

GLS Czech Republic GLS Germany GLS Netherlands GLS Slovakia

Network partners in Europe ACS Air Courier Service (GR, CY)

Global Parcels Ltd. (MA)

Itella Logistics (EE, LV, LT)

Parcelforce Worldwide (UK)

Schenker (SE)

A2B Express (BA, ME, MK, RS, XK)

Interlogistica Ltd. (BG)

MNG Kargo (TR)

Posten Norge (NO)

Swiss Post GLS (CH, LI)

GLS | Company Overview, June 2016

• The GLS Network in Europe covers 41 states via a road-based system

• 18 states are operated by fully owned subsidiaries

• To do so, GLS employs approx.

• The vast majority of delivery vehicles

and trucks are sub-contracted

• GLS usually employs no own drivers

In Europe, 41 hubs and 713 depots are connected with each other through a road-based system

14

Business Model GLS: Key facts and figures (2015/16)

• c. 14,000 employees

• 41 Hubs and 713 Depots1

• c. 18,000 delivery vehicles

• c. 2,000 long-distance trucks

1including sub-depots and depots operated by partners in those countries where GLS has a subsidiary company

GLS | Company Overview, June 2016

Initiatives

Initiatives

• Profitable Growth and Excellent Services are the central objectives for the next years.

• Streamlined delivery processes, introduction of same-day deliveries and enhanced B2C capabilities

• Ongoing selective acquisition strategy • Continuing to strengthen brand awareness • Develop premium 2C services

Germany, France and Italy are the most important GLS countries

15

Overview Strategy GLS Germany, GLS France and GLS Italy

Germany

France

Italy

Market • Highly competitive market

conditions • Minimum wage legislation

impacting cost base • Growth in same-day segment

Market

Market

• Challenging market conditions – future B2C growth expected to be lower

• Relatively immature online

marketplaces • Lower B2C parcel market

penetration

Initiatives

• Continue the turnaround of GLS France. • Measures to promote top-line growth • Break-even planned for 2017/18

GLS | Company Overview, June 2016 16

GLS Group Strategy

GLS Group Strategy

France Germany Other Countries

Italy

IT Agenda 2020

Individual Country Strategies

• Foster European growth and development

• Steer and direct the individual countries in their strategic execution

• Development of the organization and financial controlling

• Group Strategic Goals as guideline for national strategies

• National strategies to: o Increase revenues and EBIT o Address specific challenges o Ensure customer proximity

• Technology Leadership

The GLS Holding steers and controls the Group, the countries implement the individual country strategies

GLS | Company Overview, June 2016

GLS aims to increase overall value for the Royal Mail Group

17

Outlook: Main targets GLS Group to increase value

Our biggest value increase for the Royal Mail Group can be achieved by

• Increasing scale and footprint of the European parcel network

• Focusing on B2B with selective B2C growth (Premium 2C)

• Technology leadership

GLS | Company Overview, June 2016