Globefish Seafood Highlights - fao.org · Difficult squid market 2008 was again a year of low...

34

SEAFOOD HIGHLIGHTS Feature Special Seabass Special Special Se Special Salmon Farmed Special Seabream Seabass Shrimp sector under stress During the first quarter of 2008, the shrimp sector continued to suffer from soar- ing fuel prices and from the general economic slow down. Due to the general reduction of the purchasing power in major shrimp importing countries, consumers were more reluctant to buy relatively expensive food commodities like shrimp, and also dropped the habit of going out to restaurants, the main outlet for shrimp consump- tion. Record skipjack prices Tuna for canning continued to be in short supply worldwide. The current import price in Bangkok is about US$2000/MT for fro- zen skipjack, the highest in history. The impact of increasing raw material on canned tuna is already visible with strong growth in prices everywhere. Groundfish prices go up The upward trend in Alaska pollack prices is impacting the world groundfish market. Decreasing catch quotas led to a 16% increase in prices during the first half of the year. Difficult squid market 2008 was again a year of low prices, created by heavy landings of Illex squid. Argentine traders were, similar to what happened in the previous year, unable to take advantage of good supplies, and discounted Illex prices to extremely low levels. Less fishmeal production Fishmeal production was quite disappointing in May 2008, after a good produc- tion month in April. Prices started to move up in the course of 2008. Fish oil prices sky high The current high price for vegeta- ble oil has an impact on higher prices for fish oil. Fish oil prices started to decline in June 2008, after record highs. Seabreamp prices extremely low The present situation in bass and bream markets is somewhat particular with prices for bass fairly stable at acceptable levels for producers. At the same time, bream prices are record low for this period of the year. Economic crisis impacts salmon market The major factor impacting world farmed salmon markets at present is the economic situation influencing demand and the supplies from Nor- way and Chile. Salmon volumes are holding up quite well but there still is pressure on prices. Lower Chinese tilapia production and exports The impact of the loss of tilapia production during the last cold winter becomes apparent on the world tilapia market. Prices of tilapia are increasing very strongly in all main markets. Tilapia Shrimp p. 1 Tuna p. 7 Groundfish p. 12 Cephalopods p. 16 Fishmeal p. 20 Fish Oil p. 22 Seabass/bream p. 23 Salmon p. 26 Tilapia p. 30 18/07/2008 GLOBAL TECHNICAL AND TRADE CONFERENCE O SHRIMP 6 - 9 November 2008, Guangzhou, China For further information please visit: www.infofish.org

Transcript of Globefish Seafood Highlights - fao.org · Difficult squid market 2008 was again a year of low...

SEAFOODHIGHLIGHTS

HIGHLIGHTS 27-05-2003 13:30 Page 1

1GLOBEFISH Seafood Highlights 2003 1

18/04/2008

Feature

Special Seabass

Special

Bivalves

Special Se

SpecialSalmon

Farmed

Special

Seabream

Seabass

Shrimp sector under stress

During the first quarter of 2008,

the shrimp sector continued to suffer from soar-

ing fuel prices and from the general economic

slow down. Due to the general reduction of the

purchasing power in major shrimp importing

countries, consumers were more reluctant to buy

relatively expensive food commodities like shrimp,

and also dropped the habit of going out to

restaurants, the main outlet for shrimp consump-

tion.

Record skipjack prices

Tuna for canning continued to

be in short supply worldwide. The current import

price in Bangkok is about US$2000/MT for fro-

zen skipjack, the highest in history. The impact

of increasing raw material on canned tuna is

already visible with strong growth in prices

everywhere.

Groundfish prices go up

The upward trend in Alaska

pollack prices is impacting the world groundfish

market. Decreasing catch quotas led to a 16%

increase in prices during the first half of the

year.

Difficult squid market

2008 was again a year of low prices, created by

heavy landings of Illex squid. Argentine traders

were, similar to what happened in the previous

year, unable to take advantage of good supplies,

and discounted Illex prices to extremely low

levels.

Less fishmeal production

Fishmeal production was quite

disappointing in May 2008, after a good produc-

tion month in April. Prices started to move up in

the course of 2008.

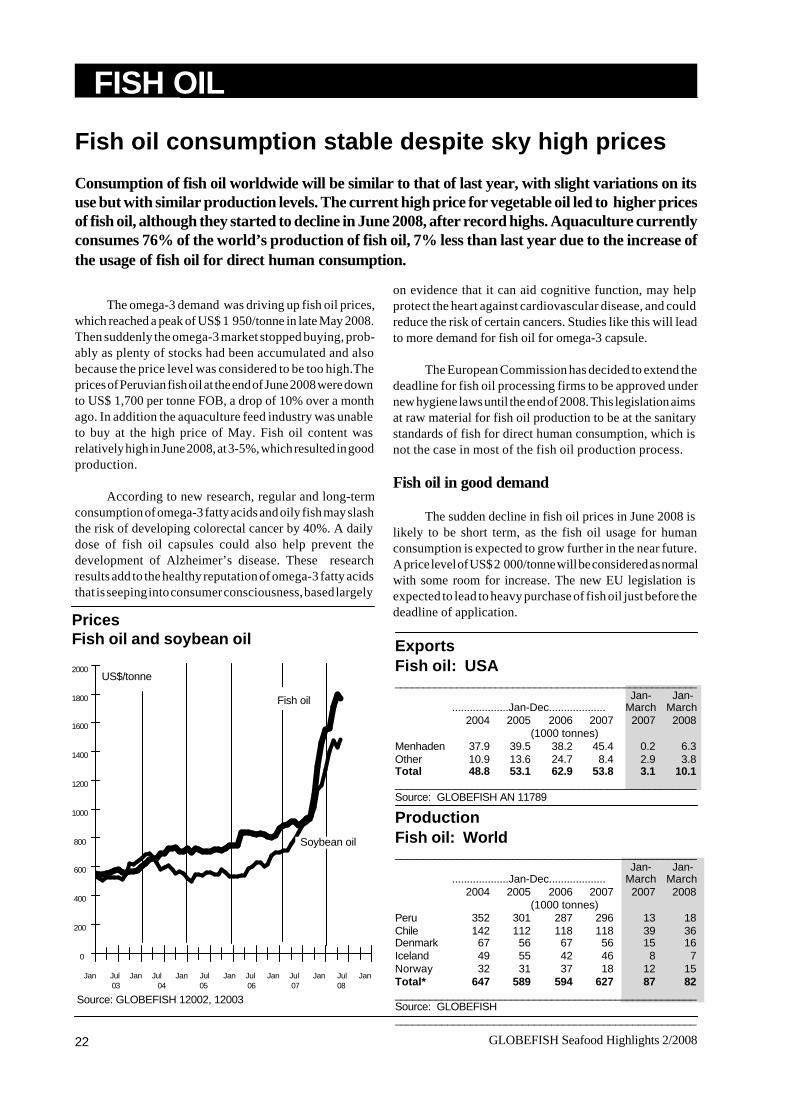

Fish oil prices sky high

The current high price for vegeta-

ble oil has an impact on higher prices for fish oil.

Fish oil prices started to decline in June 2008, after

record highs.

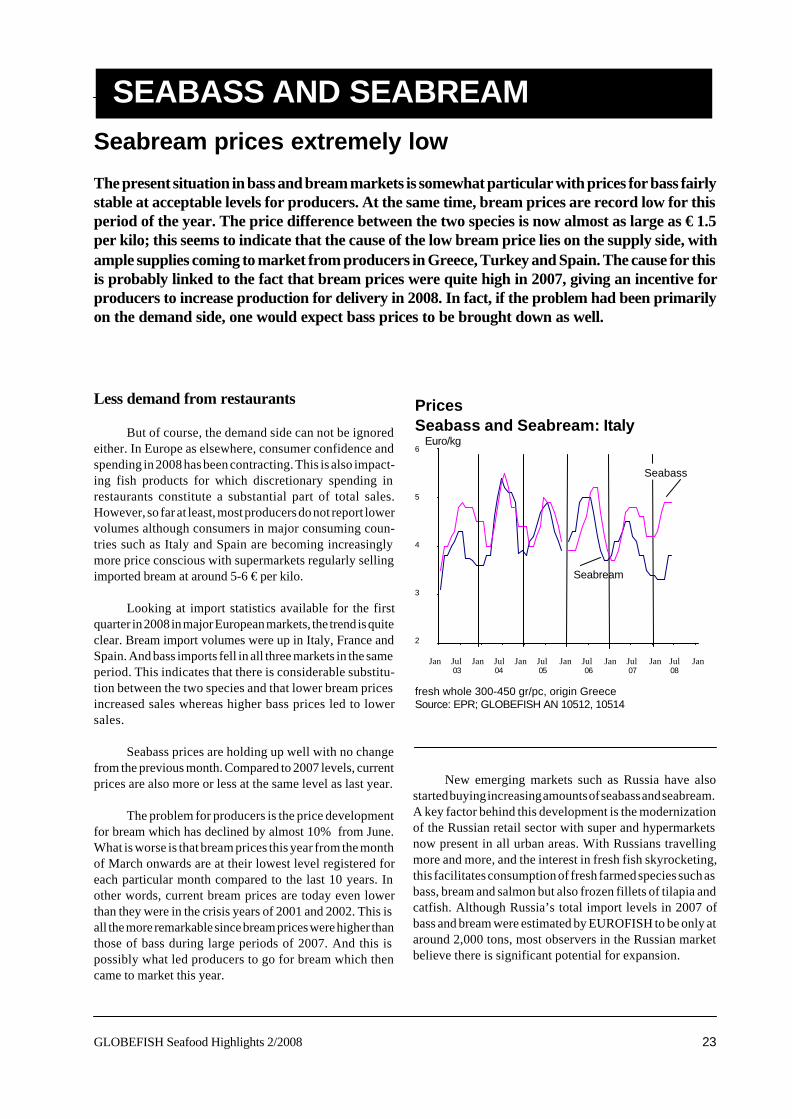

Seabreampprices

extremely low

The present situation in bass and bream markets

is somewhat particular with prices for bass fairly

stable at acceptable levels for producers. At the

same time, bream prices are record low for this

period of the year.

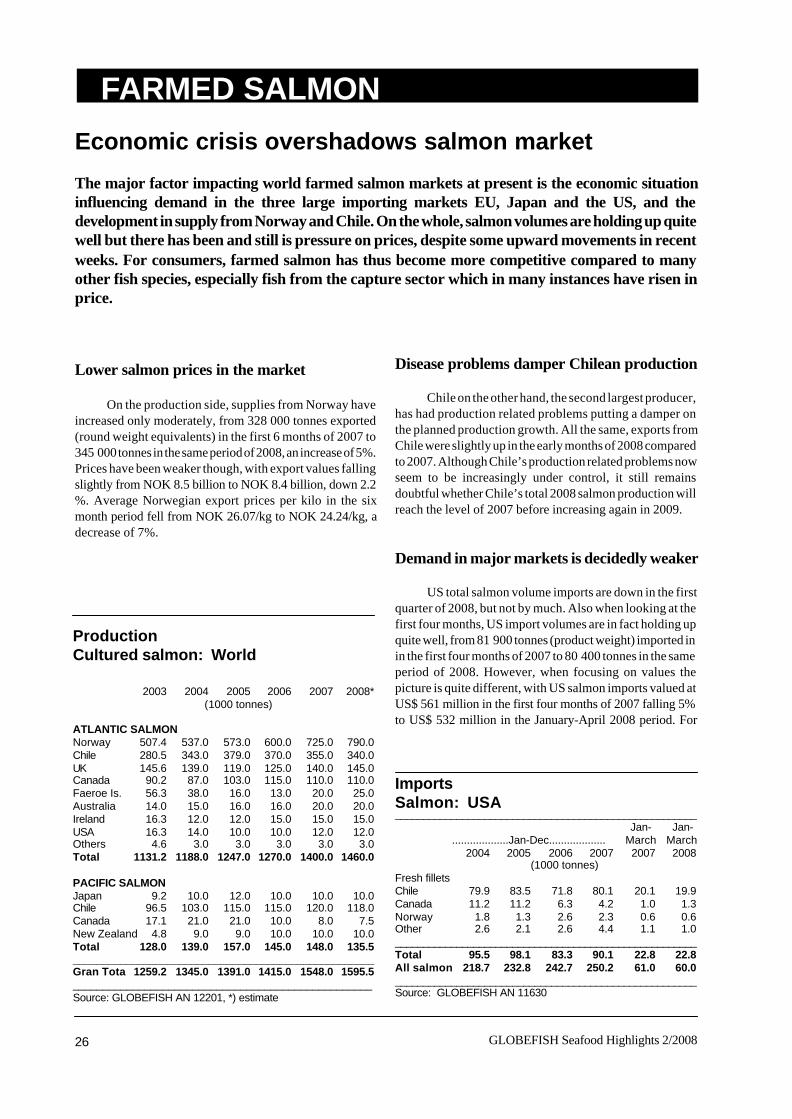

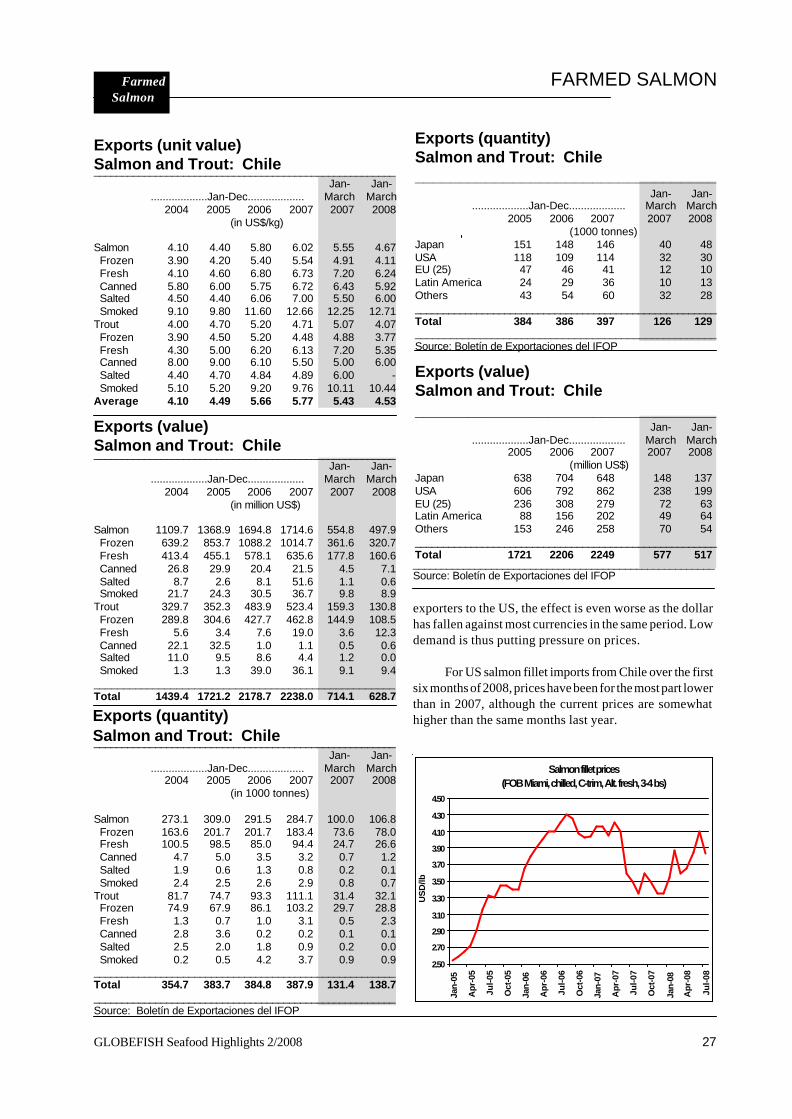

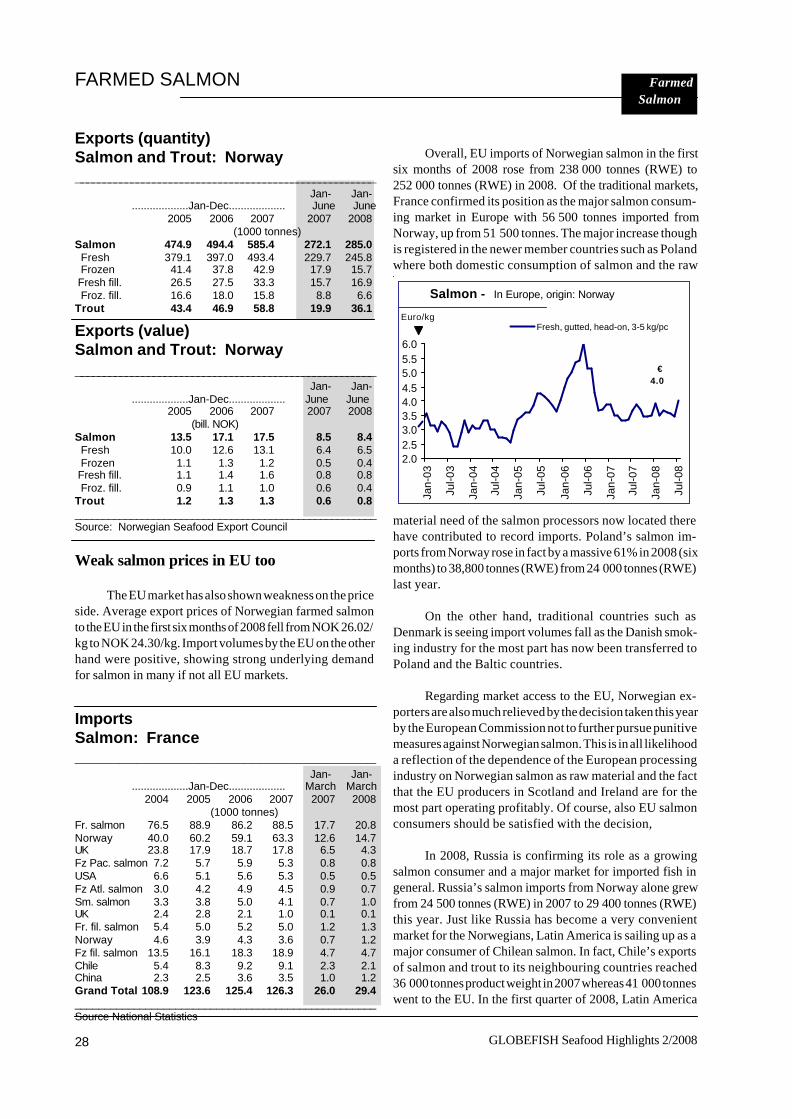

Economic crisis impacts

salmon market

The major factor impacting world farmed salmon

markets at present is the economic situation

influencing demand and the supplies from Nor-

way and Chile. Salmon volumes are holding up

quite well but there still is pressure on prices.

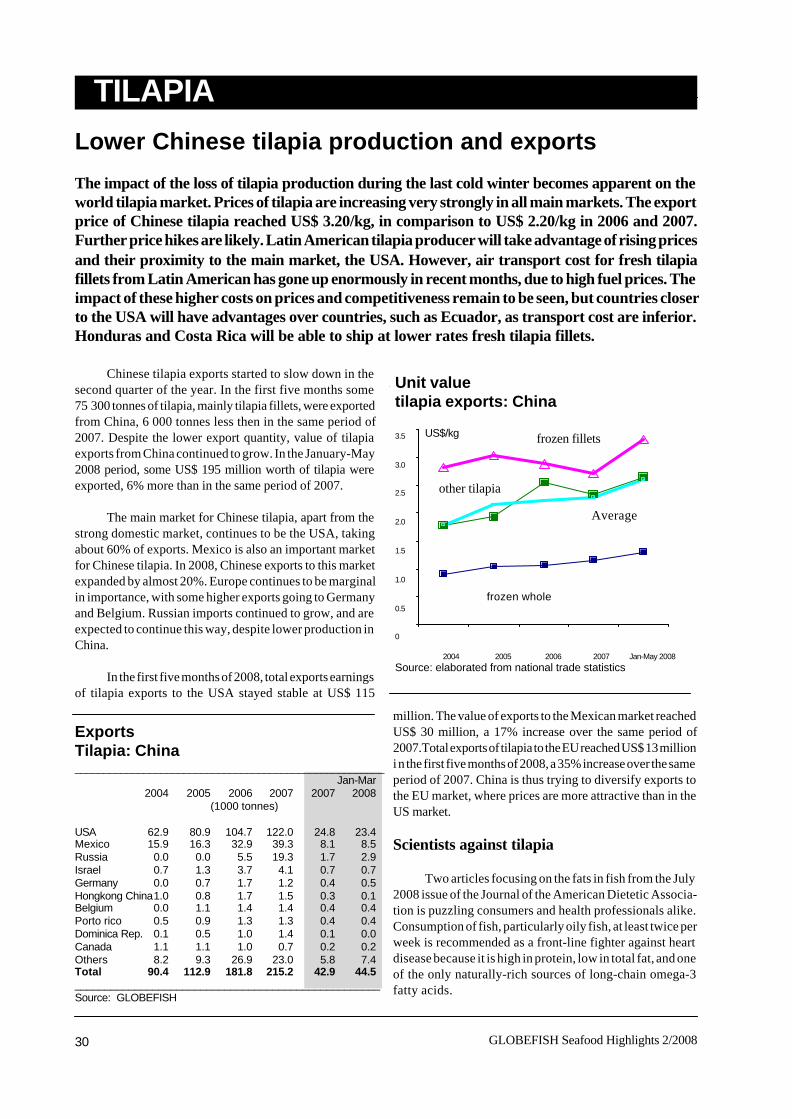

Lower Chinese tilapia

production and exports

The impact of the loss of tilapia production

during the last cold winter becomes apparent on

the world tilapia market. Prices of tilapia are

increasing very strongly in all main markets.

Tilapia

Shrimp p. 1

Tuna p. 7

Groundfish p. 12

Cephalopods p. 16

Fishmeal p. 20

Fish Oil p. 22

Seabass/bream p. 23

Salmon p. 26

Tilapia p. 30

18/07/2008

GLOBAL TECHNICAL AND TRADE CONFERENCE O SHRIMP6 - 9 November 2008, Guangzhou, China

For further information please visit: www.infofish.org

About GLOBEFISH

GLOBEFISH forms part of the Fish Utilization and Marketing Service of the FAO Fisheries Department and is part of the FISH INFOnetwork (see below). It collects information from the main market areas in developed countries. Part of its services is an electronic databank and the distribution of information through the GLOBEFISH European Fish Price Report, the GLOBEFISH Seafood Highlights , the GLOBEFISH Research Programme and the GLOBEFISH Commodity Updates . The GLOBEFISH Seafood Highlights are based on information available in the databank, supplemented by market information from six regional services which form the FISH INFOnetwork: INFOFISH (Asia and the Pacifi c), INFOPESCA (Latin America and the Caribbean), INFOPECHE (Africa), INFOSAMAK (Arab countries), EUROFISH (Eastern Europe) and INFOYU (China). GLOBEFISH Seafood Highlights are distributed to the subscribers of: INFOFISH Trade News, INFOPESCA Noticias Comerciales, INFOPECHE Nouvelles Commerciales, through EUROFISH and INFOYU. GLOBEFISH Seafood Highlights are also available in electronic form. Authors: Karine Boisset (shrimp), Paola Sabatini and Javier Lopez (groundfish), Nicki Holmyard (small pelagics), Helga Josupeit (tuna, cephalopods, tilapia, .fishmeal and oil), Audun Lem (salmon, seabass and seabream). The statistics were put together by Paola Sabatini , Karine Boisset, and Javier Lopez.

For subscription details please contact: GLOBEFISH, FIIU/FAO Tel: (39-06) 5705 6313

Viale delle Terme di Caracalla Fax: (39-06) 5705 5188 00100 Rome, Italy Email: [email protected]

Web: www.globefish.org All rights reserved. No part of FAO/GLOBEFISH Highlights may be reproduced, stored in a retrieval system, or transmitted in any form or by any means (electronic, mechanical, photocopying or otherwise), without the prior permission of FAO. Requests for use of this material (including purpose and extent) should be addressed to the Director, Publications Division, Food and Agriculture Organization of the United Nations, Viale delle Terme di Caracalla, 00100 Rome, Italy.

Bibliographic reference: FAO/GLOBEFISH Seafood Highlights. A quarterly up-date based 2008 on the GLOBEFISH FAO/GLOBEFISH Seafood Highlights, Databank (2/2008): p. 32

1GLOBEFISH Seafood Highlights 2/2008 1

SHRIMP

ImportsShrimp (frozen raw): Japan______________________________________________________

Jan- Jan- ...................Jan-Dec................... March March

2004 2005 2006 2007 2007 2008(1000 tonnes)

Viet Nam 55.5 54.6 51.1 40.0 5.3 7.3Indonesia 48.6 45.6 43.7 37.1 8.1 8.4India 31.6 26.3 28.5 27.0 4.8 5.0China 22.6 24.1 22.8 24.0 4.8 4.0Thailand 17.2 18.4 20.1 26.4 4.1 4.4Russia 8.9 10.4 9.5 8.9 2.3 2.7Canada 8.5 8.1 8.7 7.6 1.6 1.2Greenland 7.7 7.5 6.8 5.4 1.1 1.0Philippines 6.3 6.2 5.3 4.3 0.8 0.6Argentina 2.4 0.6 3.4 1.9 0.3 0.2Australia 3.6 3.6 3.2 1.9 0.2 0.2Malaysia 3.2 3.1 3.1 4.2 0.7 0.9Others 25.3 23.9 23.8 18.6 4.7 3.8_____________________________________________________

Total 241.4 232.4 230.0 207.3 38.8 39.7_____________________________________________________Source: GLOBEFISH AN 10127

Wholesale pricesShrimp*: Japan

21

19

17

15

13

11

9

7

5

Jan Jul Jan Jul Jan Jul Jan Jul Jan Jul Jan Jul 03 04 05 06 07 08

*Black tiger, headless, shell-on, origin: IndonesiaSource: INFOFISH Trade News; GLOBEFISH AN 10226

US$/kg

31/40

16/20

Shrimp sector under stress

During the first quarter of 2008, the shrimp sector continued to suffer from soaring fuel pricesand from the general economic slow down in the main importing countries. On the one hand,production and transport costs increased further and availability from major shrimp suppliersdeclined. On the other hand, due to the general reduction of the purchasing power in major shrimpimporting countries, consumers were more reluctant to buy relatively expensive food commoditieslike shrimp, and also to go to restaurants, the main outlet for shrimp consumption in the mainconsuming areas.

Situation of workers in shrimp industry underreview

The shrimp sector was also shaken by a new reportwhich points the finger at human rights abuse and environ-mental disasters linked to shrimp production and process-ing. The report which was issued by the Solidarity Center(an organization of America’s Union Movement), andmainly blamed Thailand and Bangladesh, was object todebate and scepticism. Shrimp farming and processing isa sector which has developed very rapidly in recent yearsand has generated income in many countries but has alsobeen cause of concern with respect to environmental andsocial issues. In this context, FAO with NACA/UNEP/WB/WWF developed the “International Principles forResponsible Shrimp Farming” in 2006 in order to providea basis for a more sustainable development of shrimp

farming. There have been clear improvements in this area inrecent years but one should always be on the lookout toprevent possible abuses but also to make sure that allega-tions are justified since they jeopardize work in poor coun-tries.

Japanese market stable

Japanese demand is expected to increase in July, whenthe mid year salary bonus will reach many households. It isinteresting to note, that the price margin of black tiger versusvannamei shrimp is shrinking in Japan probably as a reactionto more black tiger reaching the market. Indications for wildcaught shrimp, both warm and coldwater species, are stabledespite the continuing upward trend in fuel prices which islikely to maintain demand for higher prices in this category.Overall, there is not much margin for the expected priceincreases.

GLOBEFISH Seafood Highlights 2/20082

Wholesale pricesShrimp*: USA, Japan

10

9

8

7

6

5

4

Jan Jul Jan Jul Jan Jul Jan Jul Jan Jul Jan Jul Jan 03 04 05 06 07 08

*Frozen, headless, shell-on, 16-20 countSource: INFOFISH Trade News, GLOBEFISH AN 10205,10206

SHRIMP

US$/lb

Gulf brown, New York

Indian white, Tokyo

ImportsShrimp: USA__________________________________

...................Jan-March........................2003 2004 2005 2006 2007 2008

(1000 tonnes)

Thailand 22.9 49.1 31.6 34.1 39.7 35.0Indonesia 4.5 6.6 12.8 17.1 12.5 20.7Ecuador 8.1 11.5 12.0 15.9 17.2 15.7China 9.5 25.6 9.9 12.8 17.7 12.9Viet Nam 10.1 14.2 10.5 8.3 5.9 8.6Malaysia 0.4 0.3 2.9 4.4 4.6 7.1Mexico 4.2 4.4 4.9 4.9 6.9 6.5India 11.3 15.2 8.0 7.3 4.1 2.9Bangladesh 0.8 1.1 2.0 3.4 3.1 2.8Guyana 3.5 2.7 2.0 2.4 2.6 2.5Venezuela 2.9 4.4 3.9 2.6 3.0 2.1Peru 0.5 0.6 1.0 1.1 1.5 1.7Others 15.9 13.6 10.8 10.3 7.3 5.3___________________________________________________TOTAL 94.5 149.3 112.4 124.6 126.2 123.8

Source: NMFS

For the first time in many years, Japanese imports ofraw frozen shrimp showed a growth, although minimal,corresponding to the first quarter of the year. Backed by thestrong and stable yen, imports increased from most of themajor sources: from Indonesia to Bangladesh, with theexception of China. Considering the species farmed inthese countries, it appears obvious that imports of blacktiger shrimp also increased during this period, particularlyfrom India, Myanmar, Bangladesh but also from Vietnamand Indonesia; however vannamei were also imported fromthe last two sources.

Upward price trend for vannamei has created strongerdemand for black tiger shrimp. For this year’s Golden Weekfestival, Japanese supermarkets launched promotional cam-paigns for black tiger shrimp along with vannamei.

Low US shrimp demand

A survey based on a representative sample of 5 000US households indicates that consumer confidencedropped sharply in June, to a level which is the fifth-lowestever. But, how much this is effectively affecting shrimpconsumption, is not very clear. Traditionally, shrimp isconsidered an upper-end product, and economic crisis inthe USA have always resulted in lower shrimp consump-tion. However, some recent reports indicate that shrimpmight be less affected by the present crisis than other foodproducts.

US imports of shrimp in the first quarter of 2008 totaled123 800 tonnes worth US$ 862 million. These figures showa 2% reduction in quantity and a 0.7% increase in value,compared to the same period in 2007. Monthly shrimpimports in the USA are generally slow until May, after whichthey start to recover, just before the offset of summer.

ImportsShrimp (by product forms): USA__________________________________

.........................Jan-March................................2007 2008

Tonnes 1000 US$ Tonnes 1000 US$

Peeled frozen 36 199.3 274 661.4 39 985.5 286 311.9Other frozen 25 912.5 175 206.4 19 257.3 139 498.4Breaded 12 828.6 63 481.3 10 538.2 49 613.4Other pre. 269.7 1 595.1 328.9 1 632.9Headless shell-on frozen All sizes

49 740.9 330 699.2 52 287.3 373 230.7< 15 5 858.6 70 533.6 5 708.1 72 061.9> 70 3 732.9 15 135.2 2 229.8 9 293.115/20 3 547.6 32 468.4 3 908.3 39 571.821/25 4 354.1 36 407.9 6 011.5 52 851.826/30 5 167.6 36 861.8 7 964.5 56 330.331/40 8 735.5 51 488.2 8 967.1 53 734.841/50 6 093.8 30 318.5 7 190.8 38 849.851/60 8 094.6 39 669.8 6 476.1 32 770.061/70 4 156.1 17 815.8 3 831.1 17 767.3Other prod 1 204.5 10 496.7 1 402.1 11 631.1___________________________________________________TOTAL 126 155.5 856 140.2 123 799.3 861 918.3Source: NMFS

3GLOBEFISH Seafood Highlights 2/2008 3

ImportsShrimp: Spain______________________________________________________

.......................Jan/Mar.................................2003 2004 2005 2006 2007 2008

China 0.3 0.3 4.3 6.9 7.8 6.6Ecuador 0.8 1.5 1.5 3.3 4.5 4.2Morocco 1.5 1.6 2.0 1.5 1.6 1.7Argentina 2.6 4.1 0.8 1.1 3.8 1.6Colombia 0.9 0.9 1.2 1.0 1.2 1.1Belgium 0.4 0.6 0.7 0.6 1.0 0.8Senegal 0.6 0.9 1.1 0.6 0.9 0.8Cuba 0.2 0.2 0.2 0.9 1.1 0.8Nicaragua 0.1 0.4 0.5 1.0 1.0 0.7Netherlands 0.8 0.9 1.1 1.0 1.1 0.7Venezuela 0.2 0.6 0.7 1.0 0.9 0.6Others 11.7 15.3 10.1 10.8 9.4 6.4__________________________________________________Grand Total 19.9 27.3 24.0 29.7 34.3 26.0Source: GLOBEFISH AN 010150

SHRIMP

In the first quarter of 2008, the main imported productwas headless shell-on frozen shrimp, with 52 300 tonnesaccounting for 42% of total imports. This category reporteda 5% growth compared with the same period of 2007. Theunit value of this product grew by 7%, and as a result, totalvalue of imports of this category rose by 13% reaching US$373 million.

The second most imported product during the periodunder review was peeled frozen shrimp, which accountedfor 32% of total foreign supply of shrimp (40 000 tonnesworth US$ 286 million). Compared to the first quarter of 2007sales of this product to the US grew by 11% in terms ofvolume and by 4% in terms of value. Breaded frozen shrimpand other frozen preparations continued to show the de-creasing trend already experienced in 2007, and imports fellfor both categories.

Thailand remained the leading supplier of shrimp tothe US market with 35 000 tonnes in the first three monthsof 2008, representing 28% of the total volume. Sales fromthis country fell by 12% (both in volume and value).Indonesia was the second main supplier, with 20 700 tonnesand a remarkable growth in sales, both in volume and value.It is interesting to note that in terms of volume, the thirdsupplier was Ecuador, with 15 700 tonnes, while in terms ofvalue, the third exporter to the US was Viet Nam (US$ 95million). Probably the main reason for this difference is dueto Ecuadorian sales which are mainly frozen shell-on while46% of total Vietnamese sales are peeled frozen shrimp,which have a higher unit value.

Chinese sales have not recovered from the problemssuffered during 2007, and registered once more a reductionin trade. Sales in the first quarter of 2008 from this countrywere 27% and 28% lower both in terms of volume and value(12 900 tonnes; U$S 60.5 million). China remained the topsupplier of breaded frozen shrimp, with 62% of total USimports, however, sales of this product fell significantly (-37%), and Thailand managed to seize this market window.Sales from this nation grew by 53% in the period reviewed.

Asian nations accounted for almost 80% of the totalsupply of peeled frozen and for over 95% of other frozenpreparations and breaded frozen to the US market, whilefrozen shell-on shrimp has a higher share of Latin Americansupplies.

After the WTO ruling against the anti-dumping poli-cies of the US, India is trying to obtain yet another rulingfrom the Organization to assure that the US does not applyother mechanisms like the bond requirement - apart from theanti-dumping duties - since they consider it would be anadditional barrier to trade.

The US domestic shrimp supply in the first quarter of2008 was 5% lower than in 2007. This sector is beingnegatively affected by the continuous increase in fuelprices, which has had a direct impact on operational costs.On the other hand, shrimpers cannot transfer the highercosts to consumers, since imported shrimp sets a ceiling topotential price increases. Consequently, many fishermenare reducing their fishing effort to reduce costs. Someanalysts see in the sector a need to upgrade their technol-ogy and procedures in order to obtain a higher qualityproduct, that could enhance the efforts that the industry iscurrently making to differentiate wild shrimp fromaquaculture imported products.

Higher shrimp imports into the EU

Total EU shrimp imports continued to expand in thefirst quarter of 2008 with 174 000 tonnes, a 5% increasecompared to the same period last year. However, the expan-sion was more significant for intra-EU imports (50 000tonnes, +8%, with a boom in chilled/cooked Crangon im-ports (+58%)) than for extra-EU imports (124 000tonnes,+3%). In general, the average unit value remained stablecompared to 2007 levels on almost all market.

Notwithstanding the general upward trend of totalEU shrimp imports, individual trends for key importingcountries in this region were not always positive and wereoften in contradiction with 2007 developments.

Southern Europe buys less shrimp in 2008

Spain and Italy which have experienced a constantexpansion of their shrimp imports in recent years, recordeda sudden decrease at the beginning of this year with only26 000tonnes imported by Spain (a 24% drop in volume and

GLOBEFISH Seafood Highlights 2/20084

SHRIMP

ImportsShrimp: Italy______________________________________________________

....................Jan/March..........................2005 2006 2007 2008

Ecuador 2.5 3.5 4.5 3.9India 1.0 1.0 1.0 1.3Denmark 1.2 1.2 1.4 1.2Spain 0.5 0.7 1.0 0.9Argentina 0.2 0.4 0.7 0.5Netherlands 0.5 0.6 0.6 0.5Malaysia 0.8 0.6 0.7 0.4UK 0.5 0.6 0.4 0.4China 0.4 0.4 0.9 0.4Others 5.1 3.9 3.7 3.3__________________________________________________Total 12.7 12.9 14.9 12.8_____________________________________________________Source: GLOBEFISH AN 010148

a 29% drop in value compared to the same period last year)and only 13 000 tonnes imported by Italy ( a 14% drop involume and a 15% drop in value). This decrease was mainlydue to lower shipments from major suppliers and in particu-lar from Argentina.

After having regained its leading position amongshrimp exporters to Spain at the end of 2007, Argentinaplummeted again to the fourth position and to the fifthposition in Italy. As anticipated in the previous GLOBEFISHHighlights, Argentine shrimp catches were exceptionallylow during the first quarter of 2008 (-78% on 2007 figures).Moreover, the situation is not expected to improve sinceofficial catch figures for April and May also appear ex-tremely low. However, the decrease in imports was not onlycaused by the lack of availability of Argentine Pleoticusmuelleri. Indeed, all major suppliers to Spain and Italyregistered a drop in their exports to these two markets andthis is particularly true for Vannamei producing countries.The two exceptions to this decrease among top supplierswere Morocco (+8% - mainly Parapenaeus longirostris) onthe Spanish market and India (+27% - mainly Black tiger) onthe Italian market.

China, current leading supplier to Spain, saw itsexports decrease by 16% on this market and by 57% on theItalian market. Ecuador also diminished exports to Spain(with a 6% drop in volume) and to Italy (with a 13% drop -still remaining, however, by far the number one supplierwith 31% market share) and chose to exports more productsto France. In terms of value, the decline was even moreimportant as far as major exporters to Spain and Italy areconcerned. Argentina recorded a striking 66% drop invalue on the Spanish market. Consequently, the averageunit value for all suppliers and all categories combined, lost

0.31cents/kg compared to last year on the Spanish market.For Pleoticus muelleri from Argentina the decrease was ofminus €1.22/kg compared to last year unit value and of minus€5.75 on 2006 unit value.

Malaysia saw its shrimp exports decrease on allEuropean markets during the first quarter of 2008 (-3% on theFrench market, -44% on the Italian market, -33% on the UKmarket) and the situation is expected to worsen in thecoming months due to a recent voluntary suspension ofseafood exports to EU by Malaysian authorities followingan EU inspection mission and in order to avoid a ban.

French market in further expansion

Contrary to Spain and Italy, France continued toexpand its shrimp imports in the first quarter of 2008 with23 500 tonnes worth 11.3 million euro, an 11% increase onthe same period last year in both volume and value terms.It is mainly in the frozen whole category that the expansionoccurred (+ 15%), whereas processed products decreasedby 4% and chilled products by 19%. Ecuador confirmed itsposition as the number one supplier to France with anoutstanding 63% increase of its exports compared to lastyear (4 700 tonnes) strengthening its market share (20%).India reached the second place among top suppliers toFrance with a 4% increase. Brazil continued to loose groundwith only 1 900 tonnes corresponding to a 42% decrease onlast year figures. The general growth of shrimp imports inFrance was also due to the recovery of Madagascan exports(+50% on last year figures). Madagascar has always beena traditional supplier of high value shrimp to the Frenchmarket but demand had somewhat shrank in recent years tobenefiting countries producing cheaper products. Colom-bian exports to the French market, which have been growingconstantly in recent years, also recorded a notable 62%increase.

ImportsShrimp: France______________________________________________________

....................Jan/March..........................2005 2006 2007 2008

Ecuador 1.4 2.3 2.9 4.7India 1.2 1.9 2.0 2.1Brazil 5.1 3.2 3.3 1.9Madagascar 1.6 1.3 1.3 1.9Colombia 0.7 0.7 1.1 1.8Netherlands 2.2 1.4 1.4 1.5Belgium 1.0 1.3 1.1 1.1Others 7.5 7.6 8.3 8.4____________________________________________________Grand Total 20.6 19.8 21.4 23.5______________________________________________________Source: GLOBEFISH

5GLOBEFISH Seafood Highlights 2/2008 5

ImportsShrimp: UK______________________________________________________

Jan- Jan- ...................Jan-Dec................... March March

2004 2005 2006 2007 2007 2008(1000 tonnes)

Shell-on ColdwaterDenmark 2.0 2.6 2.8 2.4 0.6 0.8Others 2.4 1.3 1.8 2.4 0.3 0.3Total 4.4 3.9 4.6 4.8 0.9 1.1

Shell-on WarmwaterIndia 10.8 10.8 11.3 10.5 2.7 1.6Indonesia 4.8 6.1 5.2 6.3 1.0 1.6Bangladesh 8.2 9.0 6.2 5.7 1.0 1.0Thailand 0.4 0.6 1.2 4.1 0.5 1.1Ecuador 3.0 2.6 3.3 3.3 0.4 0.6Honduras * * 1.2 1.3 0.2 0.2China 0.1 0.8 1.2 1.1 0.2 0.1France 0.9 1.1 1.0 1.0 0.1 0.2Others 9.9 8.4 7.4 5.4 0.0 0.0Total 38.1 39.4 38.0 38.7 7.6 8.1

Cooked & PeeledIceland 20.8 17.7 16.9 15.3 0.9 0.8Denmark 4.9 5.4 6.6 6.9 1.2 1.2Thailand 2.1 2.6 3.9 5.2 0.8 0.6Canada 4.7 4.9 4.5 3.9 0.3 0.2Norway 5.6 4.5 3.5 2.7 0.3 0.6Indonesia 1.3 2.4 3.1 2.6 0.6 0.5Malaysia 2.3 2.3 1.9 1.5 0.3 0.3Viet Nam 0.9 1.5 1.5 1.2 0.2 0.3Others 8.7 5.3 4.7 4.7 0.0 0.0Total 51.3 46.6 46.6 44.0 7.1 3.9______________________________________________________Grand Total 93.8 89.9 89.2 87.5 15.6 15.9___________________________________________________Source: GLOBEFISH AN 010141

SHRIMP

Limited coldwater shrimp supply to UK market

Since 2003,UK shrimp imports have continuouslyshown a negative trend. At the beginning of 2008 thesituation changed with a slight increase in total shrimpimports: +3% in volume and +9% in value. In volume terms,this expansion concerned the frozen-whole category only(+8%) while the processed category registered a 3% de-crease. In value terms, the situation was more positiveparticularly for the prepared and preserved sector whereproducts entered the UK market at a higher unit value (+32cents/kg). Traditional suppliers to the USA continued toincrease their market shares in UK due to the unfavourablesituation in the US market. Indonesia took the lead amongwarmwater shrimp suppliers with a 13% market share (+19%on last year figures).

Thailand continued to strengthen its position in theUK and increased the volume of its exports to this countryby 45%. The increase was also due to growing volumes ofshrimp imports from Vietnam and Ecuador. On the opposite,

Indian exports to the UK shrunk (-40% on last year figures),mainly due to high prices of black tiger (main speciesproduced in India) compared to Vannamei.

The proportion of coldwater shrimp imports in the UKcontinued to be much lower than in the past, but, despitethe decrease experienced, UK remained the only significantmarket for coldwater shrimp in Europe with 5 800 tonnesimported in the first three months of 2008. In this sector,Icelandic exports continued to decline and lost a further10% at the beginning of 2008 compared to last year figures.Danish shrimp exports to the UK remained roughly stableand amounted to 1 841 tonnes. Norway doubled its exportsin 2008, but exports to the UK were much lower than in theyears prior to 2007. During the first months of 2008, pricesfor Norwegian peeled Pandalus borealis on the UK marketshowed an upward trend. On average, prices in June 2008increased by almost 20% compared to last year.

Slow down of German imports

The first quarter of 2008 put an end to the outstandingboom in German shrimp imports. Far from the 22% growthof 2007, shrimp imports during the first three months of 2008increased by only 2% in volume and by 3% in value.

Thailand continued to gain ground on the Germanymarket, with a 18% market share and it remained the numberone supplier to this country. Viet Nam also expanded on theGerman market both for frozen and processed products. Inthe frozen category, Vietnam increased its exports by 58%on last year figures. India lost ground in Germany andregistered a 22% decrease in its exports.

ImportsShrimp: Germany______________________________________________________

Jan- Jan- ...................Jan-Dec................... March March

2004 2005 2006 2007 2007 2008(1000 tonnes)

Thailand 2.2 3.5 4.0 8.9 1.3 2.0Viet Nam 1.5 3.3 4.0 5.7 1.0 1.5India 3.7 4.2 5.3 6.4 1.8 1.3Netherlands 3.0 3.6 4.1 5.7 1.7 1.3Bangladesh 2.1 2.7 3.0 3.1 0.4 0.6Belgium 2.5 2.5 2.8 2.6 0.7 0.7Denmark 1.8 2.1 1.5 2.6 0.3 0.8UK 2.4 3.0 3.1 2.5 0.8 0.5Others 10.8 10.2 12.1 11.4 2.7 2.2_____________________________________________________Total 30.0 35.1 39.9 48.8 10.7 10.9_____________________________________________________Source: GLOBEFISH AN 010146

GLOBEFISH Seafood Highlights 2/20086

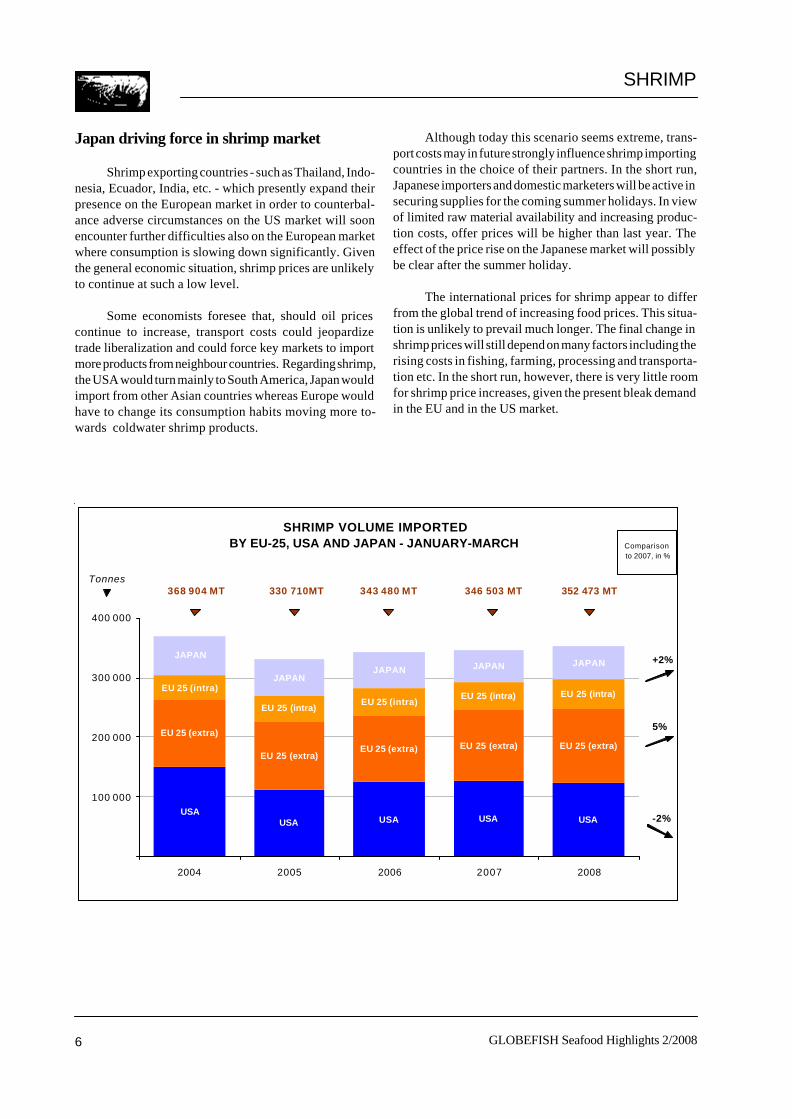

SHRIMP VOLUME IMPORTED BY EU-25, USA AND JAPAN - JANUARY-MARCH

USAUSA USA USA USA

EU 25 (extra)

EU 25 (extra)EU 25 (extra) EU 25 (extra) EU 25 (extra)

EU 25 (intra)

EU 25 (intra)EU 25 (intra) EU 25 (intra)

JAPAN

JAPANJAPAN JAPAN JAPAN

EU 25 (intra)

100 000

200 000

300 000

400 000

2004 2005 2006 2007 2008

Tonnes

Comparison to 2007, in %

346 503 MT

5%

+2%

343 480 MT330 710MT368 904 MT

-2%

352 473 MT

Japan driving force in shrimp market

Shrimp exporting countries - such as Thailand, Indo-nesia, Ecuador, India, etc. - which presently expand theirpresence on the European market in order to counterbal-ance adverse circumstances on the US market will soonencounter further difficulties also on the European marketwhere consumption is slowing down significantly. Giventhe general economic situation, shrimp prices are unlikelyto continue at such a low level.

Some economists foresee that, should oil pricescontinue to increase, transport costs could jeopardizetrade liberalization and could force key markets to importmore products from neighbour countries. Regarding shrimp,the USA would turn mainly to South America, Japan wouldimport from other Asian countries whereas Europe wouldhave to change its consumption habits moving more to-wards coldwater shrimp products.

Although today this scenario seems extreme, trans-port costs may in future strongly influence shrimp importingcountries in the choice of their partners. In the short run,Japanese importers and domestic marketers will be active insecuring supplies for the coming summer holidays. In viewof limited raw material availability and increasing produc-tion costs, offer prices will be higher than last year. Theeffect of the price rise on the Japanese market will possiblybe clear after the summer holiday.

The international prices for shrimp appear to differfrom the global trend of increasing food prices. This situa-tion is unlikely to prevail much longer. The final change inshrimp prices will still depend on many factors including therising costs in fishing, farming, processing and transporta-tion etc. In the short run, however, there is very little roomfor shrimp price increases, given the present bleak demandin the EU and in the US market.

SHRIMP

7GLOBEFISH Seafood Highlights 2/2008 7

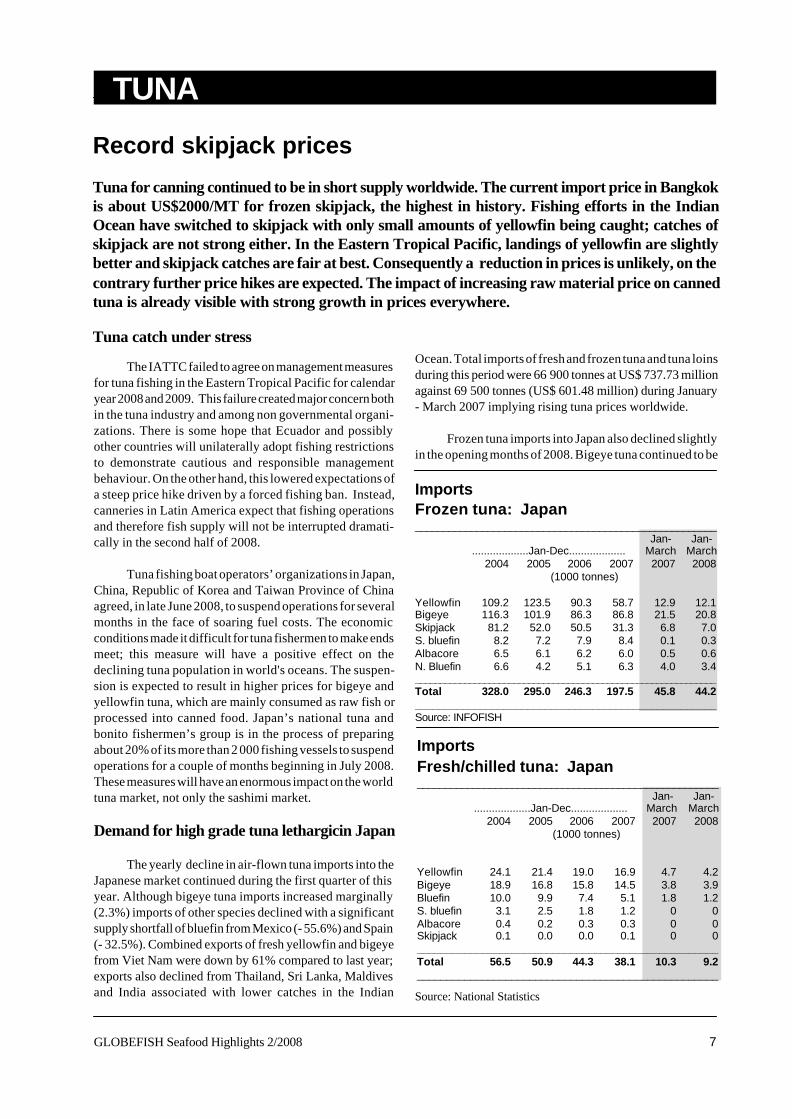

Frozen tuna: Japan______________________________________________________

Jan- Jan- ...................Jan-Dec................... March March

2004 2005 2006 2007 2007 2008(1000 tonnes)

Yellowfin 109.2 123.5 90.3 58.7 12.9 12.1Bigeye 116.3 101.9 86.3 86.8 21.5 20.8Skipjack 81.2 52.0 50.5 31.3 6.8 7.0S. bluefin 8.2 7.2 7.9 8.4 0.1 0.3Albacore 6.5 6.1 6.2 6.0 0.5 0.6N. Bluefin 6.6 4.2 5.1 6.3 4.0 3.4_____________________________________________________________Total 328.0 295.0 246.3 197.5 45.8 44.2___________________________________________________Source: INFOFISH

Imports

TUNA

Fresh/chilled tuna: Japan______________________________________________________

Jan- Jan- ...................Jan-Dec................... March March

2004 2005 2006 2007 2007 2008(1000 tonnes)

Yellowfin 24.1 21.4 19.0 16.9 4.7 4.2Bigeye 18.9 16.8 15.8 14.5 3.8 3.9Bluefin 10.0 9.9 7.4 5.1 1.8 1.2S. bluefin 3.1 2.5 1.8 1.2 0 0Albacore 0.4 0.2 0.3 0.3 0 0Skipjack 0.1 0.0 0.0 0.1 0 0___________________________________________________Total 56.5 50.9 44.3 38.1 10.3 9.2___________________________________________________

Imports

Source: National Statistics

Record skipjack prices

Tuna for canning continued to be in short supply worldwide. The current import price in Bangkokis about US$2000/MT for frozen skipjack, the highest in history. Fishing efforts in the IndianOcean have switched to skipjack with only small amounts of yellowfin being caught; catches ofskipjack are not strong either. In the Eastern Tropical Pacific, landings of yellowfin are slightlybetter and skipjack catches are fair at best. Consequently a reduction in prices is unlikely, on thecontrary further price hikes are expected. The impact of increasing raw material price on cannedtuna is already visible with strong growth in prices everywhere.

Tuna catch under stress

The IATTC failed to agree on management measuresfor tuna fishing in the Eastern Tropical Pacific for calendaryear 2008 and 2009. This failure created major concern bothin the tuna industry and among non governmental organi-zations. There is some hope that Ecuador and possiblyother countries will unilaterally adopt fishing restrictionsto demonstrate cautious and responsible managementbehaviour. On the other hand, this lowered expectations ofa steep price hike driven by a forced fishing ban. Instead,canneries in Latin America expect that fishing operationsand therefore fish supply will not be interrupted dramati-cally in the second half of 2008.

Tuna fishing boat operators’ organizations in Japan,China, Republic of Korea and Taiwan Province of Chinaagreed, in late June 2008, to suspend operations for severalmonths in the face of soaring fuel costs. The economicconditions made it difficult for tuna fishermen to make endsmeet; this measure will have a positive effect on thedeclining tuna population in world's oceans. The suspen-sion is expected to result in higher prices for bigeye andyellowfin tuna, which are mainly consumed as raw fish orprocessed into canned food. Japan’s national tuna andbonito fishermen’s group is in the process of preparingabout 20% of its more than 2 000 fishing vessels to suspendoperations for a couple of months beginning in July 2008.These measures will have an enormous impact on the worldtuna market, not only the sashimi market.

Demand for high grade tuna lethargicin Japan

The yearly decline in air-flown tuna imports into theJapanese market continued during the first quarter of thisyear. Although bigeye tuna imports increased marginally(2.3%) imports of other species declined with a significantsupply shortfall of bluefin from Mexico (- 55.6%) and Spain(- 32.5%). Combined exports of fresh yellowfin and bigeyefrom Viet Nam were down by 61% compared to last year;exports also declined from Thailand, Sri Lanka, Maldivesand India associated with lower catches in the Indian

Ocean. Total imports of fresh and frozen tuna and tuna loinsduring this period were 66 900 tonnes at US$ 737.73 millionagainst 69 500 tonnes (US$ 601.48 million) during January- March 2007 implying rising tuna prices worldwide.

Frozen tuna imports into Japan also declined slightlyin the opening months of 2008. Bigeye tuna continued to be

GLOBEFISH Seafood Highlights 2/20088

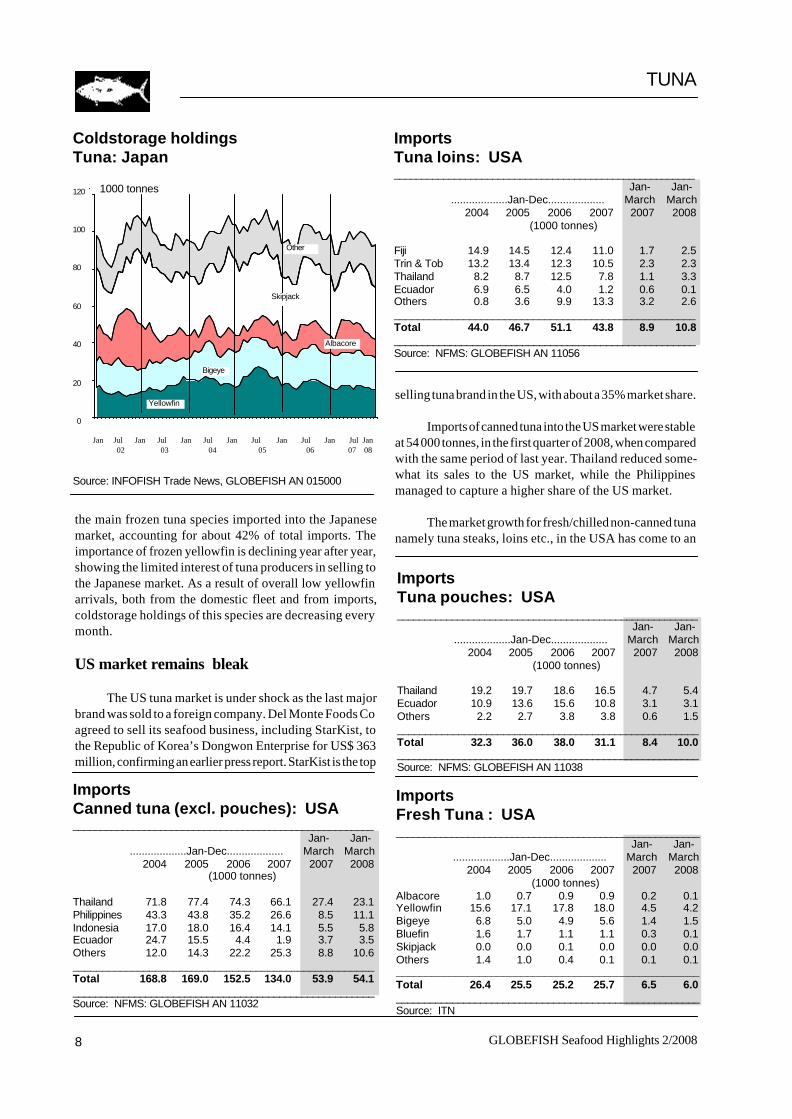

Coldstorage holdingsTuna: Japan

120

100

80

60

40

20

0

Jan Jul Jan Jul Jan Jul Jan Jul Jan Jul Jan Jul Jan 02 03 04 05 06 07 08

Source: INFOFISH Trade News, GLOBEFISH AN 015000

1000 tonnes

Yellowfin

Bigeye

Albacore

Other

Skipjack

the main frozen tuna species imported into the Japanesemarket, accounting for about 42% of total imports. Theimportance of frozen yellowfin is declining year after year,showing the limited interest of tuna producers in selling tothe Japanese market. As a result of overall low yellowfinarrivals, both from the domestic fleet and from imports,coldstorage holdings of this species are decreasing everymonth.

US market remains bleak

The US tuna market is under shock as the last majorbrand was sold to a foreign company. Del Monte Foods Coagreed to sell its seafood business, including StarKist, tothe Republic of Korea’s Dongwon Enterprise for US$ 363million, confirming an earlier press report. StarKist is the top

ImportsTuna pouches: USA_______________________________________________________

Jan- Jan- ...................Jan-Dec................... March March

2004 2005 2006 2007 2007 2008(1000 tonnes)

Thailand 19.2 19.7 18.6 16.5 4.7 5.4Ecuador 10.9 13.6 15.6 10.8 3.1 3.1Others 2.2 2.7 3.8 3.8 0.6 1.5______________________________________________________Total 32.3 36.0 38.0 31.1 8.4 10.0______________________________________________________Source: NFMS: GLOBEFISH AN 11038

ImportsFresh Tuna : USA_______________________________________________________

Jan- Jan- ...................Jan-Dec................... March March

2004 2005 2006 2007 2007 2008(1000 tonnes)

Albacore 1.0 0.7 0.9 0.9 0.2 0.1Yellowfin 15.6 17.1 17.8 18.0 4.5 4.2Bigeye 6.8 5.0 4.9 5.6 1.4 1.5Bluefin 1.6 1.7 1.1 1.1 0.3 0.1Skipjack 0.0 0.0 0.1 0.0 0.0 0.0Others 1.4 1.0 0.4 0.1 0.1 0.1___________________________________________________Total 26.4 25.5 25.2 25.7 6.5 6.0______________________________________________________Source: ITN

selling tuna brand in the US, with about a 35% market share.

Imports of canned tuna into the US market were stableat 54 000 tonnes, in the first quarter of 2008, when comparedwith the same period of last year. Thailand reduced some-what its sales to the US market, while the Philippinesmanaged to capture a higher share of the US market.

The market growth for fresh/chilled non-canned tunanamely tuna steaks, loins etc., in the USA has come to an

ImportsCanned tuna (excl. pouches): USA_______________________________________________________

Jan- Jan- ...................Jan-Dec................... March March

2004 2005 2006 2007 2007 2008(1000 tonnes)

Thailand 71.8 77.4 74.3 66.1 27.4 23.1Philippines 43.3 43.8 35.2 26.6 8.5 11.1Indonesia 17.0 18.0 16.4 14.1 5.5 5.8Ecuador 24.7 15.5 4.4 1.9 3.7 3.5Others 12.0 14.3 22.2 25.3 8.8 10.6___________________________________________________Total 168.8 169.0 152.5 134.0 53.9 54.1______________________________________________________Source: NFMS: GLOBEFISH AN 11032

ImportsTuna loins: USA_______________________________________________________

Jan- Jan- ...................Jan-Dec................... March March

2004 2005 2006 2007 2007 2008(1000 tonnes)

Fiji 14.9 14.5 12.4 11.0 1.7 2.5Trin & Tob 13.2 13.4 12.3 10.5 2.3 2.3Thailand 8.2 8.7 12.5 7.8 1.1 3.3Ecuador 6.9 6.5 4.0 1.2 0.6 0.1Others 0.8 3.6 9.9 13.3 3.2 2.6____________________________________________________Total 44.0 46.7 51.1 43.8 8.9 10.8______________________________________________________Source: NFMS: GLOBEFISH AN 11056

TUNA

9GLOBEFISH Seafood Highlights 2/2008 9

halt this year. With shrinking consumer disposable in-come, the market can barely support the global rise in tunaprices. The retail price for fresh tuna steaks ranges betweenUS$ 15-20/lb in the US supermarkets. The quarterly importsof air-flown tuna fell below 6000 tonnes for the first time inmany years. However, imports of frozen tuna, tuna loins/fillets, steaks, saku blocks etc. increased to 5 300 tonnescompared to last year’s figure of 5 100 tonnes. Theseproduct forms include frozen natural and carbon monoxide(CO) treated products. There is a growing preference for COtreated products in the US market because of the colourretention compared to the natural “brown” tuna.

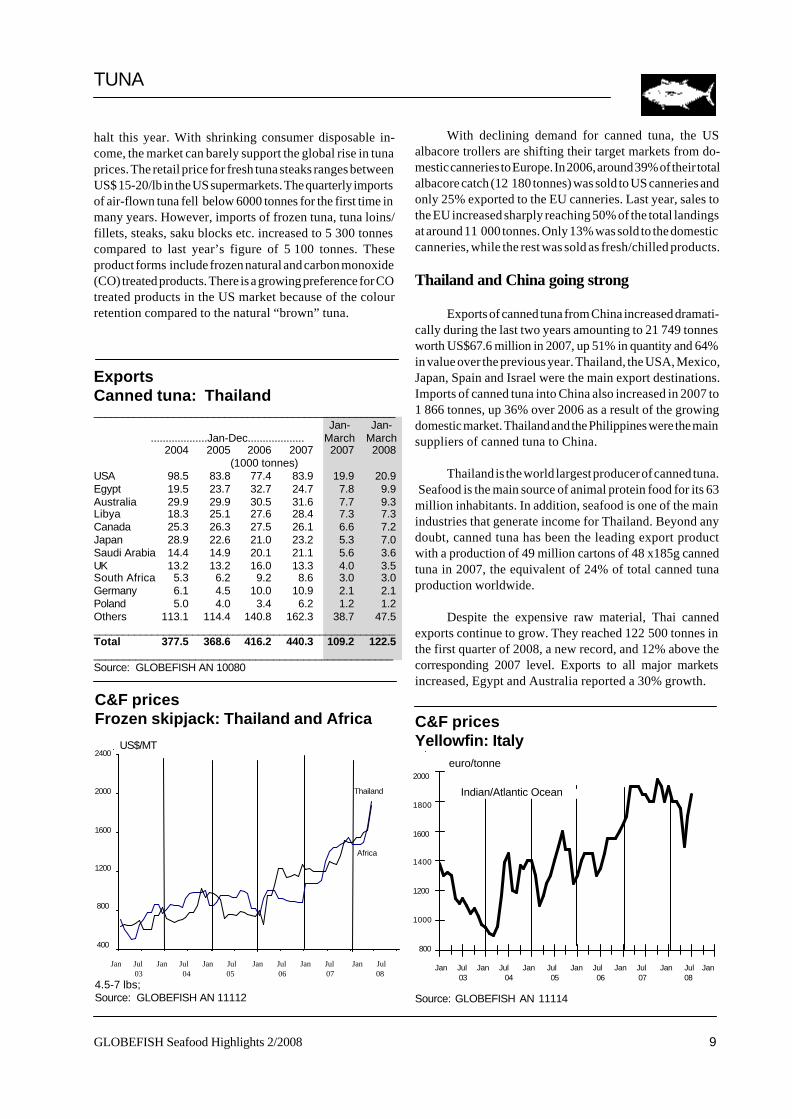

ExportsCanned tuna: Thailand_____________________________________________________

Jan- Jan- ...................Jan-Dec................... March March

2004 2005 2006 2007 2007 2008(1000 tonnes)

USA 98.5 83.8 77.4 83.9 19.9 20.9Egypt 19.5 23.7 32.7 24.7 7.8 9.9Australia 29.9 29.9 30.5 31.6 7.7 9.3Libya 18.3 25.1 27.6 28.4 7.3 7.3Canada 25.3 26.3 27.5 26.1 6.6 7.2Japan 28.9 22.6 21.0 23.2 5.3 7.0Saudi Arabia 14.4 14.9 20.1 21.1 5.6 3.6UK 13.2 13.2 16.0 13.3 4.0 3.5South Africa 5.3 6.2 9.2 8.6 3.0 3.0Germany 6.1 4.5 10.0 10.9 2.1 2.1Poland 5.0 4.0 3.4 6.2 1.2 1.2Others 113.1 114.4 140.8 162.3 38.7 47.5____________________________________________________Total 377.5 368.6 416.2 440.3 109.2 122.5__________________________________________________Source: GLOBEFISH AN 10080

C&F pricesFrozen skipjack: Thailand and Africa

2400

2000

1600

1200

800

400

Jan Jul Jan Jul Jan Jul Jan Jul Jan Jul Jan Jul 03 04 05 06 07 084.5-7 lbs;Source: GLOBEFISH AN 11112

US$/MT

Africa

Thailand

With declining demand for canned tuna, the USalbacore trollers are shifting their target markets from do-mestic canneries to Europe. In 2006, around 39% of their totalalbacore catch (12 180 tonnes) was sold to US canneries andonly 25% exported to the EU canneries. Last year, sales tothe EU increased sharply reaching 50% of the total landingsat around 11 000 tonnes. Only 13% was sold to the domesticcanneries, while the rest was sold as fresh/chilled products.

Thailand and China going strong

Exports of canned tuna from China increased dramati-cally during the last two years amounting to 21 749 tonnesworth US$67.6 million in 2007, up 51% in quantity and 64%in value over the previous year. Thailand, the USA, Mexico,Japan, Spain and Israel were the main export destinations.Imports of canned tuna into China also increased in 2007 to1 866 tonnes, up 36% over 2006 as a result of the growingdomestic market. Thailand and the Philippines were the mainsuppliers of canned tuna to China.

Thailand is the world largest producer of canned tuna. Seafood is the main source of animal protein food for its 63million inhabitants. In addition, seafood is one of the mainindustries that generate income for Thailand. Beyond anydoubt, canned tuna has been the leading export productwith a production of 49 million cartons of 48 x185g cannedtuna in 2007, the equivalent of 24% of total canned tunaproduction worldwide.

Despite the expensive raw material, Thai cannedexports continue to grow. They reached 122 500 tonnes inthe first quarter of 2008, a new record, and 12% above thecorresponding 2007 level. Exports to all major marketsincreased, Egypt and Australia reported a 30% growth.

2000

1800

1600

1400

1200

1000

800

Jan Jul Jan Jul Jan Jul Jan Jul Jan Jul Jan Jul Jan 03 04 05 06 07 08

Source: GLOBEFISH AN 11114

C&F pricesYellowfin: Italy

euro/tonne

Indian/Atlantic Ocean

TUNA

GLOBEFISH Seafood Highlights 2/200810

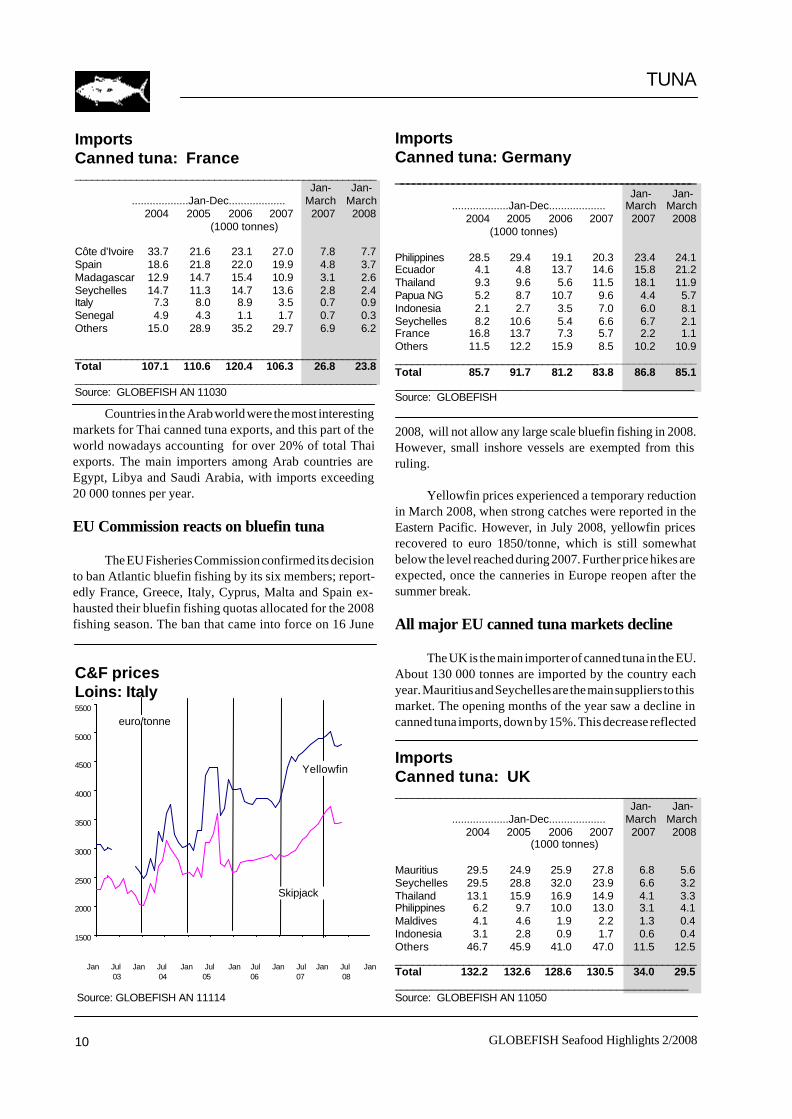

ImportsCanned tuna: Germany_____________________________________________________

Jan- Jan- ...................Jan-Dec................... March March

2004 2005 2006 2007 2007 2008(1000 tonnes)

Philippines 28.5 29.4 19.1 20.3 23.4 24.1Ecuador 4.1 4.8 13.7 14.6 15.8 21.2Thailand 9.3 9.6 5.6 11.5 18.1 11.9Papua NG 5.2 8.7 10.7 9.6 4.4 5.7Indonesia 2.1 2.7 3.5 7.0 6.0 8.1Seychelles 8.2 10.6 5.4 6.6 6.7 2.1France 16.8 13.7 7.3 5.7 2.2 1.1Others 11.5 12.2 15.9 8.5 10.2 10.9_____________________________________________________Total 85.7 91.7 81.2 83.8 86.8 85.1__________________________________________________Source: GLOBEFISH

5500

5000

4500

4000

3500

3000

2500

2000

1500

Jan Jul Jan Jul Jan Jul Jan Jul Jan Jul Jan Jul Jan 03 04 05 06 07 08

Source: GLOBEFISH AN 11114

C&F pricesLoins: Italy

Skipjack

ImportsCanned tuna: France______________________________________________________

Jan- Jan- ...................Jan-Dec................... March March

2004 2005 2006 2007 2007 2008(1000 tonnes)

Côte d’Ivoire 33.7 21.6 23.1 27.0 7.8 7.7Spain 18.6 21.8 22.0 19.9 4.8 3.7Madagascar 12.9 14.7 15.4 10.9 3.1 2.6Seychelles 14.7 11.3 14.7 13.6 2.8 2.4Italy 7.3 8.0 8.9 3.5 0.7 0.9Senegal 4.9 4.3 1.1 1.7 0.7 0.3Others 15.0 28.9 35.2 29.7 6.9 6.2

_____________________________________________________Total 107.1 110.6 120.4 106.3 26.8 23.8_____________________________________________________Source: GLOBEFISH AN 11030

ImportsCanned tuna: UK_____________________________________________________

Jan- Jan- ...................Jan-Dec................... March March

2004 2005 2006 2007 2007 2008(1000 tonnes)

Mauritius 29.5 24.9 25.9 27.8 6.8 5.6Seychelles 29.5 28.8 32.0 23.9 6.6 3.2Thailand 13.1 15.9 16.9 14.9 4.1 3.3Philippines 6.2 9.7 10.0 13.0 3.1 4.1Maldives 4.1 4.6 1.9 2.2 1.3 0.4Indonesia 3.1 2.8 0.9 1.7 0.6 0.4Others 46.7 45.9 41.0 47.0 11.5 12.5_____________________________________________________Total 132.2 132.6 128.6 130.5 34.0 29.5_________________________________________________Source: GLOBEFISH AN 11050

euro/tonne

Yellowfin

Countries in the Arab world were the most interestingmarkets for Thai canned tuna exports, and this part of theworld nowadays accounting for over 20% of total Thaiexports. The main importers among Arab countries areEgypt, Libya and Saudi Arabia, with imports exceeding20 000 tonnes per year.

EU Commission reacts on bluefin tuna

The EU Fisheries Commission confirmed its decisionto ban Atlantic bluefin fishing by its six members; report-edly France, Greece, Italy, Cyprus, Malta and Spain ex-hausted their bluefin fishing quotas allocated for the 2008fishing season. The ban that came into force on 16 June

2008, will not allow any large scale bluefin fishing in 2008.However, small inshore vessels are exempted from thisruling.

Yellowfin prices experienced a temporary reductionin March 2008, when strong catches were reported in theEastern Pacific. However, in July 2008, yellowfin pricesrecovered to euro 1850/tonne, which is still somewhatbelow the level reached during 2007. Further price hikes areexpected, once the canneries in Europe reopen after thesummer break.

All major EU canned tuna markets decline

The UK is the main importer of canned tuna in the EU.About 130 000 tonnes are imported by the country eachyear. Mauritius and Seychelles are the main suppliers to thismarket. The opening months of the year saw a decline incanned tuna imports, down by 15%. This decrease reflected

TUNA

11GLOBEFISH Seafood Highlights 2/2008 11

C&F pricesCanned tuna*: USA, Europe

30

26

22

18

14

10

Jan Jul Jan Jul Jan Jul Jan Jul Jan Jul Jan Jul Jan 03 04 05 06 07 08

*48x6.5oz Europe, 48x6 oz USA, chunk, origin ThailandSource: GLOBEFISH AN 11101, 11102

ImportsCanned tuna: Italy_____________________________________________________

Jan-March2004 2005 2006 2007 2007 2008

(1000 tonnes)

Spain 36.1 37.0 36.7 39.7 9.3 9.2Colombia 6.4 7.0 5.0 6.6 1.4 2.0Cote d’Ivoire 14.0 8.9 9.1 10.0 2.2 1.8Seychelles 4.6 7.0 6.9 3.9 1.6 1.4France 6.1 4.6 3.4 5.3 1.3 1.3Portugal 2.6 2.8 2.6 2.4 0.5 0.5Others 4.3 4.2 5.8 9.0 1.3 2.5_____________________________________________________

Total 74.1 71.5 69.5 76.9 17.6 18.7

__________________________________________________Source: GLOBEFISH

Europe

US$/carton

USA

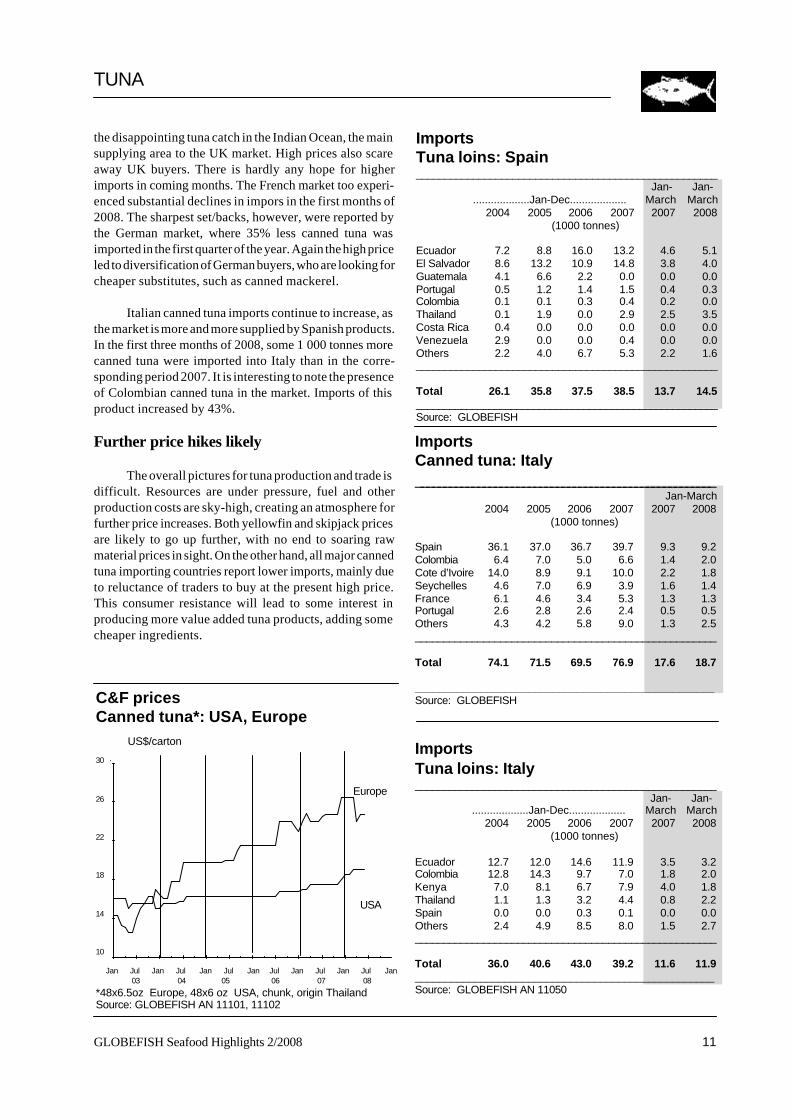

the disappointing tuna catch in the Indian Ocean, the mainsupplying area to the UK market. High prices also scareaway UK buyers. There is hardly any hope for higherimports in coming months. The French market too experi-enced substantial declines in impors in the first months of2008. The sharpest set/backs, however, were reported bythe German market, where 35% less canned tuna wasimported in the first quarter of the year. Again the high priceled to diversification of German buyers, who are looking forcheaper substitutes, such as canned mackerel.

Italian canned tuna imports continue to increase, asthe market is more and more supplied by Spanish products.In the first three months of 2008, some 1 000 tonnes morecanned tuna were imported into Italy than in the corre-sponding period 2007. It is interesting to note the presenceof Colombian canned tuna in the market. Imports of thisproduct increased by 43%.

Further price hikes likely

The overall pictures for tuna production and trade isdifficult. Resources are under pressure, fuel and otherproduction costs are sky-high, creating an atmosphere forfurther price increases. Both yellowfin and skipjack pricesare likely to go up further, with no end to soaring rawmaterial prices in sight. On the other hand, all major cannedtuna importing countries report lower imports, mainly dueto reluctance of traders to buy at the present high price.This consumer resistance will lead to some interest inproducing more value added tuna products, adding somecheaper ingredients.

ImportsTuna loins: Spain_____________________________________________________

Jan- Jan- ...................Jan-Dec................... March March

2004 2005 2006 2007 2007 2008(1000 tonnes)

Ecuador 7.2 8.8 16.0 13.2 4.6 5.1El Salvador 8.6 13.2 10.9 14.8 3.8 4.0Guatemala 4.1 6.6 2.2 0.0 0.0 0.0Portugal 0.5 1.2 1.4 1.5 0.4 0.3Colombia 0.1 0.1 0.3 0.4 0.2 0.0Thailand 0.1 1.9 0.0 2.9 2.5 3.5Costa Rica 0.4 0.0 0.0 0.0 0.0 0.0Venezuela 2.9 0.0 0.0 0.4 0.0 0.0Others 2.2 4.0 6.7 5.3 2.2 1.6_____________________________________________________

Total 26.1 35.8 37.5 38.5 13.7 14.5______________________________________________________Source: GLOBEFISH

ImportsTuna loins: Italy_____________________________________________________

Jan- Jan- ...................Jan-Dec................... March March

2004 2005 2006 2007 2007 2008(1000 tonnes)

Ecuador 12.7 12.0 14.6 11.9 3.5 3.2Colombia 12.8 14.3 9.7 7.0 1.8 2.0Kenya 7.0 8.1 6.7 7.9 4.0 1.8Thailand 1.1 1.3 3.2 4.4 0.8 2.2Spain 0.0 0.0 0.3 0.1 0.0 0.0Others 2.4 4.9 8.5 8.0 1.5 2.7_____________________________________________________

Total 36.0 40.6 43.0 39.2 11.6 11.9__________________________________________________Source: GLOBEFISH AN 11050

TUNA

GLOBEFISH Seafood Highlights 2/200812

C&F pricesGroundfish blocks: USA

3

2.5

2

1.5

1

0.5

0 Jan Jul Jan Jul Jan Jul Jan Jul Jan Jul Jan Jul 03 04 05 06 07 08

Source: GLOBEFISH AN 010805, 10806, 10834

GROUNDFISH

US$/lb

Cod

Hake

Alaska pollack

ImportsCod-like groundfish: USA_____________________________________________________

Jan- Jan- ...................Jan-Dec................... March March

2004 2005 2006 2007 2007 2008(1000 tonnes)

FilletsChina 73.4 89.8 91.3 74.5 20.2 18.8Iceland 20.4 16.5 16.0 11.1 4.1 2.6Canada 10.3 6.7 9.7 5.5 1.1 1.1Norway 2.4 1.2 2.1 0.2 0.4 0.2Others 9.5 8.9 9.0 6.4 1.0 1.5Total 116.0 123.1 128.1 97.7 26.8 24.2

Blocks/SlabsChina 33.2 32.2 25.4 41.7 14.2 12.6Argentina 3.9 2.9 2.9 2.0 0.9 0.8Iceland 3.2 1.9 0.6 0.8 0.2 0.1Norway 1.2 1.4 0.5 0.1 0.0 0.0Russian Fed. 1.6 1.1 0.5 0.8 0.1 0.2Canada 8.2 0.6 0.5 2.1 0.7 0.8Korea Rep. 0.1 0.0 0.0 0.0 0.0 0.0Others 10.0 2.6 2.0 1.7 1.0 1.1Total 61.4 42.7 32.4 49.2 17.1 15.6______________________________________________________Gr. Total 177.4 165.8 160.5 146.9 43.9 39.8

_____________________________________________________Source: NMFS

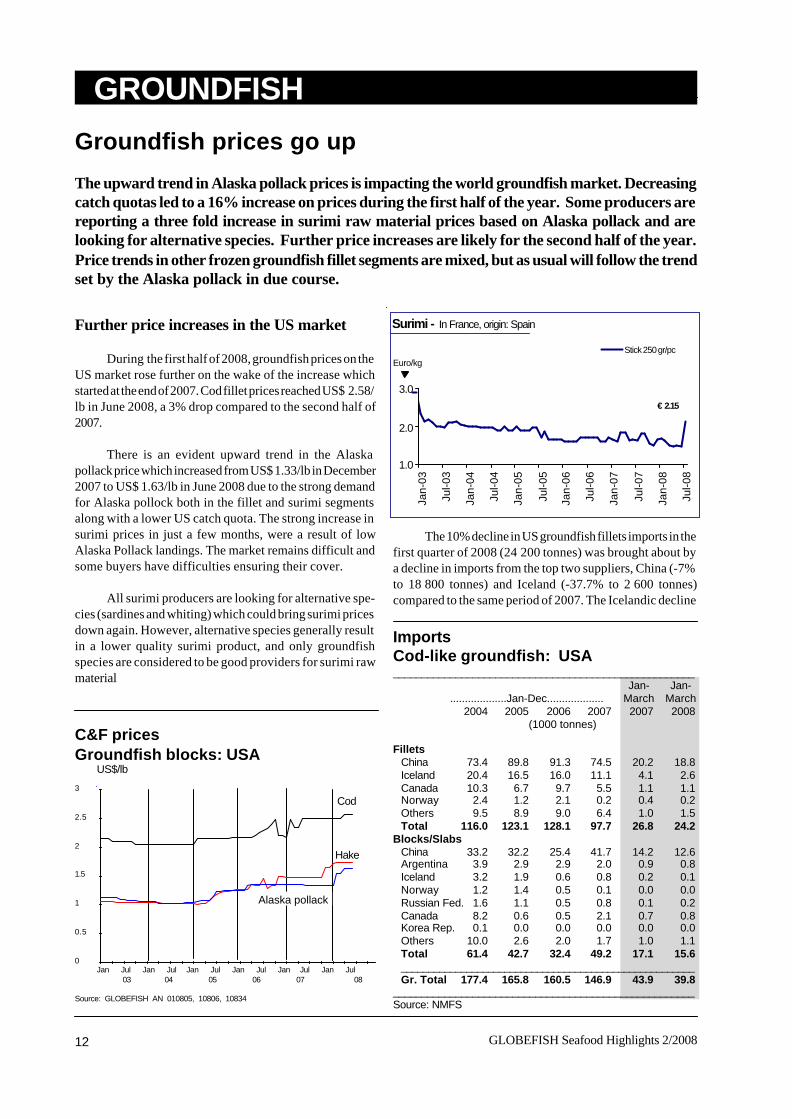

Groundfish prices go up

The upward trend in Alaska pollack prices is impacting the world groundfish market. Decreasingcatch quotas led to a 16% increase on prices during the first half of the year. Some producers arereporting a three fold increase in surimi raw material prices based on Alaska pollack and arelooking for alternative species. Further price increases are likely for the second half of the year.Price trends in other frozen groundfish fillet segments are mixed, but as usual will follow the trendset by the Alaska pollack in due course.

Further price increases in the US market

During the first half of 2008, groundfish prices on theUS market rose further on the wake of the increase whichstarted at the end of 2007. Cod fillet prices reached US$ 2.58/lb in June 2008, a 3% drop compared to the second half of2007.

There is an evident upward trend in the Alaskapollack price which increased from US$ 1.33/lb in December2007 to US$ 1.63/lb in June 2008 due to the strong demandfor Alaska pollock both in the fillet and surimi segmentsalong with a lower US catch quota. The strong increase insurimi prices in just a few months, were a result of lowAlaska Pollack landings. The market remains difficult andsome buyers have difficulties ensuring their cover.

All surimi producers are looking for alternative spe-cies (sardines and whiting) which could bring surimi pricesdown again. However, alternative species generally resultin a lower quality surimi product, and only groundfishspecies are considered to be good providers for surimi rawmaterial

The 10% decline in US groundfish fillets imports in thefirst quarter of 2008 (24 200 tonnes) was brought about bya decline in imports from the top two suppliers, China (-7%to 18 800 tonnes) and Iceland (-37.7% to 2 600 tonnes)compared to the same period of 2007. The Icelandic decline

Surimi - In France, origin: Spain

1.0

2.0

3.0

Jan-

03

Jul-0

3

Jan-

04

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Stick 250 gr/pcEuro/kg

€ 2.15

13GLOBEFISH Seafood Highlights 2/2008 13

GROUNDFISH

_____________________________________________________Jan- Jan-

...................Jan-Dec................... March March2004 2005 2006 2007 2007 2008

(1000 tonnes)China 16.1 14.3 18.6 18.6 4.7 5.7USA 12.8 12.5 10.8 10.3 2.5 2.3Germany 6.0 5.8 6.3 4.4 1.2 1.1Russian Fed. 4.6 2.1 4.3 4.0 1.6 1.5Others 1.9 1.4 0.6 0.7 0.1 0.1____________________________________________________Total 41.4 36.1 40.8 38.0 10.1 10.7______________________________________________________Source: National Trade Statistics

ImportsFrozen Alaska pollock fillets: France

_____________________________________________________Jan- Jan-

...................Jan-Dec................... March March2004 2005 2006 2007 2007 2008

(1000 tonnes)

China 59.2 58.1 88.0 78.5 19.7 20.8USA 51.2 47.0 39.4 55.2 15.4 17.8Russia 22.0 15.5 27.6 25.4 7.3 4.9Others 4.2 3.0 6.1 5.3 2.0 0.9____________________________________________________Total 136.6 123.6 161.1 164.4 44.4 44.4______________________________________________________Source: Statistisches Bundesamt

ImportsFrozen Alaska pollock fillets: Germany

___________________________________________________Jan- Jan-

...................Jan-Dec................... March March2004 2005 2006 2007 2007 2008

(1000 tonnes)

Russia 28.8 36.9 13.0 4.1 0.8 0.1Denmark 17.6 16.7 16.9 12.4 4.9 2.1China 15.0 16.5 23.2 21.9 8.2 6.3Iceland 16.9 14.8 16.1 18.0 6.2 4.0Norway 8.8 9.0 14.0 11.4 3.2 3.9Faroe Is. 7.0 4.9 6.5 4.4 0.1 0.9Germany 3.0 1.3 1.9 4.5 0.7 0.3Poland 1.6 1.3 6.5 3.6 1.0 0.9Others 4.5 7.3 8.2 6.0 1.9 0.2___________________________________________________Total 103.2 108.5 106.3 86.3 27.0 18.7_______________________________________________________Source: Seafish/national trade statistics

ImportsFrozen cod: UK

was mainly caused by the sharply reduced cod catchquotas for 2008. An analogous drop in imports was regis-tered by groundfish blocks (-9%) when the first threemonths of this year are compared to the correspondingperiod of 2007. China, the main supplier of groundfishblocks to the USA, reduced its shipments to this market by11% compared to last year and whereas other countrieshave kept their export levels stable.

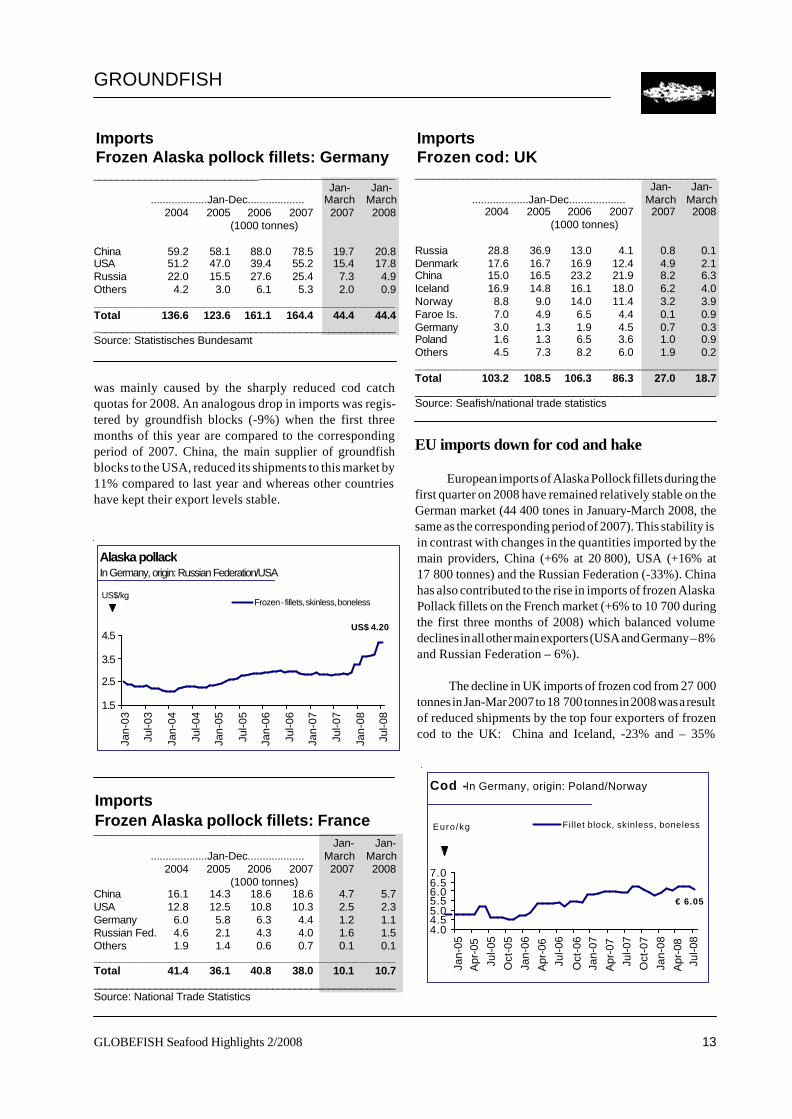

EU imports down for cod and hake

European imports of Alaska Pollock fillets during thefirst quarter on 2008 have remained relatively stable on theGerman market (44 400 tones in January-March 2008, thesame as the corresponding period of 2007). This stability isin contrast with changes in the quantities imported by themain providers, China (+6% at 20 800), USA (+16% at17 800 tonnes) and the Russian Federation (-33%). Chinahas also contributed to the rise in imports of frozen AlaskaPollack fillets on the French market (+6% to 10 700 duringthe first three months of 2008) which balanced volumedeclines in all other main exporters (USA and Germany – 8%and Russian Federation – 6%).

The decline in UK imports of frozen cod from 27 000tonnes in Jan-Mar 2007 to 18 700 tonnes in 2008 was a resultof reduced shipments by the top four exporters of frozencod to the UK: China and Iceland, -23% and – 35%

Alaska pollack In Germany, origin: Russian Federation/USA

1.5

2.5

3.5

4.5

Jan-

03

Jul-0

3

Jan-

04

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Frozen - fillets, skinless, bonelessUS$/kg

US$ 4.20

Cod -In Germany, origin: Poland/Norway

4.04.55.05.56.06.57.0

Jan-

05A

pr-0

5

Jul-0

5

Oct

-05

Jan-

06

Apr

-06

Jul-0

6

Oct

-06

Jan-

07

Apr

-07

Jul-0

7

Oct

-07

Jan-

08

Apr

-08

Jul-0

8

Fillet block, skinless, bonelessEuro/kg

€ 6.05

GLOBEFISH Seafood Highlights 2/200814

GROUNDFISH

_____________________________________________________Jan- Jan-

...................Jan-Dec................... March March2004 2005 2006 2007 2007 2008

(1000 tonnes)

China 4.7 8.3 8.1 12.2 3.0 3.8Russia 1.5 1.1 2.4 1.1 0.5 0.5Poland 4.4 2.1 1.4 3.8 1.5 0.6Denmark 1.0 1.4 1.2 1.5 0.3 0.7Norway 1.4 1.9 0.6 0.6 0.1 0.1Iceland 0.8 1.0 0.5 0.3 0.0 0.1Others 3.0 1.4 1.8 2.7 0.6 0.3____________________________________________________Total 16.8 17.2 16.0 22.2 6.0 6.1_______________________________________________________Source: Statistisches Bundesamt

ImportsFrozen cod fillets: Germany

respectively during the first quarter of this year comparedto Jan-Mar 2007.

The German cod fillet market does not appear asdynamic as the UK one despite the important increase involume in 2007 compared to 2006 as a consequence ofincreased Chinese supplies. Comparing the frozen cod filletimports by Germany of first quarter of 2008 with the samemonths of 2007 no evident change can be noted since therise in Chinese cod fillet exports to Germany (+27%) werecounterbalanced by reduced shipments from Poland (-60%).

_____________________________________________________Jan- Jan-

...................Jan-Dec................... March March2004 2005 2006 2007 2007 2008

(1000 tonnes)Argentina 4.8 5.8 6.9 6.1 1.5 0.8USA 2.5 3.6 4.4 6.1 2.2 2.0Peru 2.1 4.1 4.1 4.1 1.1 1.5Chile. 3.6 2.0 2.2 1.0 0.7 0.3Russian Fed. * 6.2 0.2 0.0 0.0 0.0Others 9.0 7.1 6.6 4.5 1.8 1.0______________________________________________________Total 22.0 28.8 24.4 21.8 7.3 5.6__________________________________________________Source: Statistisches Bundesamt

ImportsFrozen hake fillets: Germany

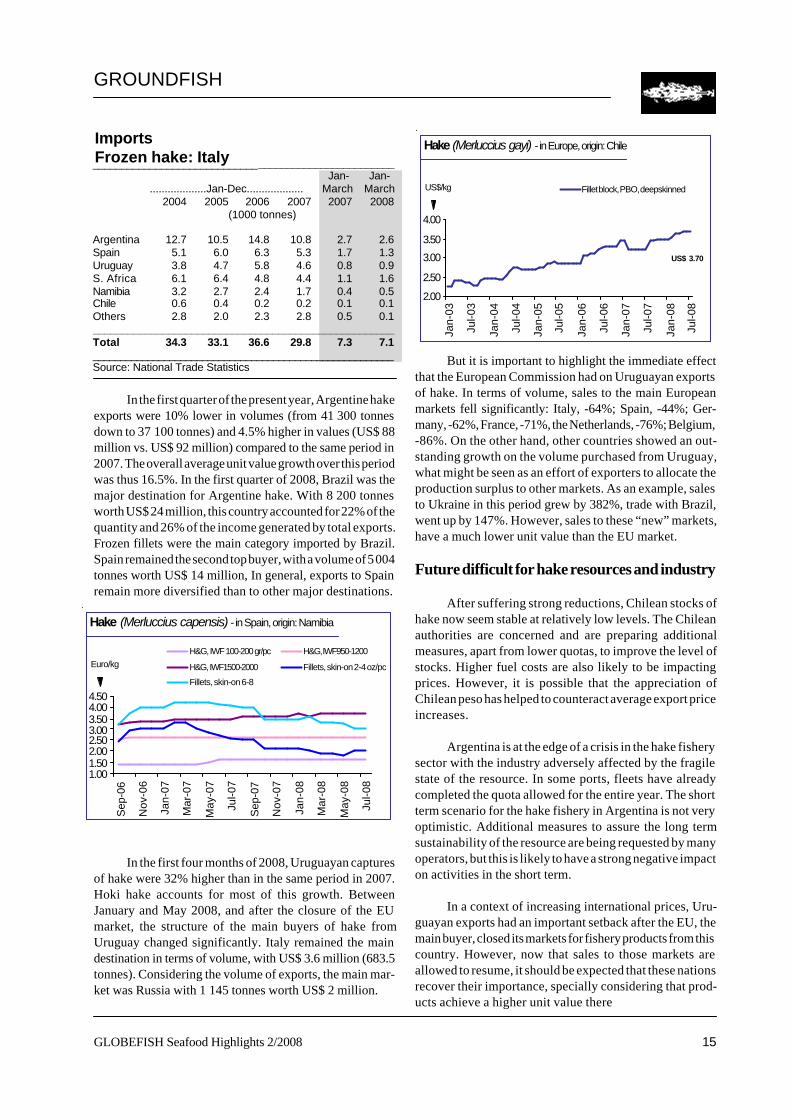

1.2% down on the same period in 2007. Lower landings ofcommon and southern hake were balanced by higher land-ings of hoki. The latter species accounted for 39% oflandings in the period under review, and grew 12% com-pared to the figures of the previous years. The other twospecies showed a reduction in landings, -7% for commonhake, and -11% for southern hake. The evolution of landingsbetween January and April for the last three years can beobserved in the following graph.

Between January and March 2008, Spain and the USAremained the main buyers of Chilean hake in terms of value(US$ 18.3 million and US$ 1.8 million respectively), as wellas in terms of volume (4 396 tonnes and 730 tonnes respec-tively). The Spanish share in total exports, was higher in thecurrent period (55% and 76% respectively in terms ofquantity and value). The third market in importance wasPortugal (300 tonnes worth US$ 1.5 million, followed byGermany and France. Venezuela again is placed as one of themain markets for Chilean hake in terms of value with thehighest unit value (although lower than the level for 2007 ofUS$ 8.1/kg).

Between January and May 2008, landings of hake inArgentina were 167 000 tonnes which represents a declineof 11%, compared to the same period in 2007. Hubbsi hakehad a 69% share in total landings, followed by hoki with 30%.Landings were lower for all species with hoki showing themost significant drop at -19%. As a consequence of thedeterioration of the state of the resource, the Agriculture,Livestock, Fishing and Food Secretary (SAGPyA) cut thetotal allowable catch (TAC) of hubbsi hake by 20% for 2008,from 340 000 tonnes in 2007 to 270 000 tonnes. That TACwas set also for the next five years. On the other hand,according to several reports of the National Institute ofFisheries Research and Development (INIDEP), the stocksare formed mainly by juveniles, which implies special meas-ures to preserve them. The effects of the lower quotas anda raw material shortage are starting to show.

Further price hikes likely

Groundfish resources continue to be under stress inalmost all fishing areas. Demand for whitefish productsstays strong, which leads to higher offer prices in allmarkets. In addition to the traditional markets – EU andUSA – new markets are emerging, mainly Brazil and Russia.Difficult supply situation for hake

Difficult supply situation for hake

In the first quarter of 2008 hake imports into Italy andGermany experienced a decline (-3% and -23% respec-tively) as a result of lower arrivals from Argentina comparedto the January-March 2007 period. This country remainsthe top supplier to the Italian marked but has lost its leadingposition to the USA on the German market. Spanish frozenhake exports to Italy dropped by 24% during the sameperiod.

During the first four months of 2008, Chilean land-ings of hake (including hoki) amounted to 33 500 tonnes,

15GLOBEFISH Seafood Highlights 2/2008 15

GROUNDFISH

In the first quarter of the present year, Argentine hakeexports were 10% lower in volumes (from 41 300 tonnesdown to 37 100 tonnes) and 4.5% higher in values (US$ 88million vs. US$ 92 million) compared to the same period in2007. The overall average unit value growth over this periodwas thus 16.5%. In the first quarter of 2008, Brazil was themajor destination for Argentine hake. With 8 200 tonnesworth US$ 24 million, this country accounted for 22% of thequantity and 26% of the income generated by total exports.Frozen fillets were the main category imported by Brazil.Spain remained the second top buyer, with a volume of 5 004tonnes worth US$ 14 million, In general, exports to Spainremain more diversified than to other major destinations.

In the first four months of 2008, Uruguayan capturesof hake were 32% higher than in the same period in 2007.Hoki hake accounts for most of this growth. BetweenJanuary and May 2008, and after the closure of the EUmarket, the structure of the main buyers of hake fromUruguay changed significantly. Italy remained the maindestination in terms of volume, with US$ 3.6 million (683.5tonnes). Considering the volume of exports, the main mar-ket was Russia with 1 145 tonnes worth US$ 2 million.

But it is important to highlight the immediate effectthat the European Commission had on Uruguayan exportsof hake. In terms of volume, sales to the main Europeanmarkets fell significantly: Italy, -64%; Spain, -44%; Ger-many, -62%, France, -71%, the Netherlands, -76%; Belgium,-86%. On the other hand, other countries showed an out-standing growth on the volume purchased from Uruguay,what might be seen as an effort of exporters to allocate theproduction surplus to other markets. As an example, salesto Ukraine in this period grew by 382%, trade with Brazil,went up by 147%. However, sales to these “new” markets,have a much lower unit value than the EU market.

Future difficult for hake resources and industry

After suffering strong reductions, Chilean stocks ofhake now seem stable at relatively low levels. The Chileanauthorities are concerned and are preparing additionalmeasures, apart from lower quotas, to improve the level ofstocks. Higher fuel costs are also likely to be impactingprices. However, it is possible that the appreciation ofChilean peso has helped to counteract average export priceincreases.

Argentina is at the edge of a crisis in the hake fisherysector with the industry adversely affected by the fragilestate of the resource. In some ports, fleets have alreadycompleted the quota allowed for the entire year. The shortterm scenario for the hake fishery in Argentina is not veryoptimistic. Additional measures to assure the long termsustainability of the resource are being requested by manyoperators, but this is likely to have a strong negative impacton activities in the short term.

In a context of increasing international prices, Uru-guayan exports had an important setback after the EU, themain buyer, closed its markets for fishery products from thiscountry. However, now that sales to those markets areallowed to resume, it should be expected that these nationsrecover their importance, specially considering that prod-ucts achieve a higher unit value there

1.001.502.002.503.003.504.004.50

Sep

-06

Nov

-06

Jan-

07

Mar

-07

May

-07

Jul-0

7

Sep

-07

Nov

-07

Jan-

08

Mar

-08

May

-08

Jul-0

8

H&G, IWF 100-200 gr/pc H&G, IWF950-1200

H&G, IWF1500-2000 Fillets, skin-on 2-4 oz/pc

Fillets, skin-on 6-8

Euro/kg

Hake (Merluccius capensis) - in Spain, origin: Namibia

_____________________________________________________Jan- Jan-

...................Jan-Dec................... March March2004 2005 2006 2007 2007 2008

(1000 tonnes)

Argentina 12.7 10.5 14.8 10.8 2.7 2.6Spain 5.1 6.0 6.3 5.3 1.7 1.3Uruguay 3.8 4.7 5.8 4.6 0.8 0.9S. Africa 6.1 6.4 4.8 4.4 1.1 1.6Namibia 3.2 2.7 2.4 1.7 0.4 0.5Chile 0.6 0.4 0.2 0.2 0.1 0.1Others 2.8 2.0 2.3 2.8 0.5 0.1____________________________________________________Total 34.3 33.1 36.6 29.8 7.3 7.1_______________________________________________________Source: National Trade Statistics

ImportsFrozen hake: Italy

2.00

2.50

3.00

3.50

4.00

Jan-

03

Jul-0

3

Jan-

04

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Fillet block, PBO, deepskinnedUS$/kg

US$ 3.70

Hake (Merluccius gayi) - in Europe, origin: Chile

GLOBEFISH Seafood Highlights 2/200816

Wholesale pricesOctopus: Japan

14

13

12

11

10

9

8

7

6

5

4

3

2

1

0

Jan Jul Jan Jul Jan Jul Jan Jul Jan Jul Jan Jul Jan 03 04 05 06 07 08

Source: INFOFISH Trade News, GLOBEFISH AN 10507

CEPHALOPODS

ImportsOctopus: Japan_____________________________________________________

Jan- Jan- ...................Jan-Dec................... March March

2004 2005 2006 2007 2007 2008(1000 tonnes)

Mauritania 14.5 19.5 16.6 14.0 3.8 4.0China 13.1 9.9 8.2 7.2 1.3 2.3Spain 5.9 6.2 4.0 1.8 0.5 1.2Viet Nam 5.9 5.6 5.5 4.8 1.1 0.8Morocco 5.2 8.7 8.7 10.3 1.6 0.5Thailand 1.8 3.0 1.9 1.8 0.5 0.3Others 6.9 2.6 3.5 6.9 0.5 2.3_____________________________________________________Total 53.3 55.5 48.4 46.8 9.3 11.4_____________________________________________________Source: GLOBEFISH AN 10438

US$/kg 2.0-3.0 kg/pc

0.3-0.5 kg/pc

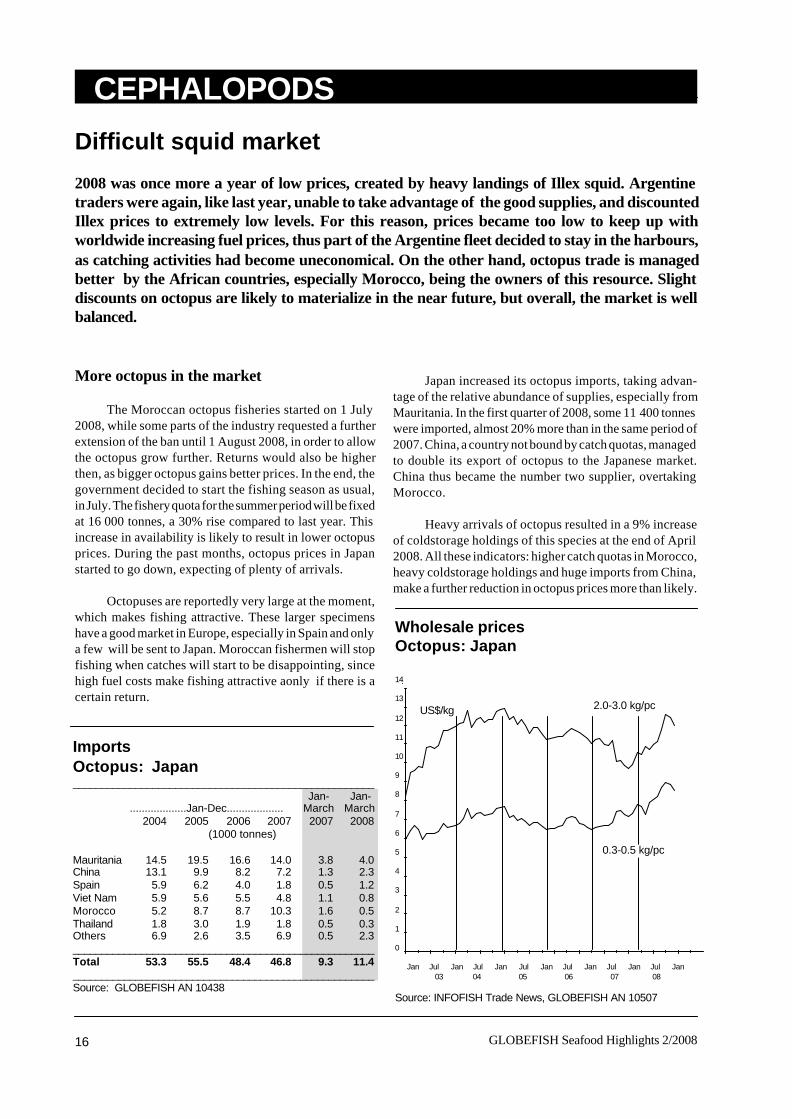

Difficult squid market

2008 was once more a year of low prices, created by heavy landings of Illex squid. Argentinetraders were again, like last year, unable to take advantage of the good supplies, and discountedIllex prices to extremely low levels. For this reason, prices became too low to keep up withworldwide increasing fuel prices, thus part of the Argentine fleet decided to stay in the harbours,as catching activities had become uneconomical. On the other hand, octopus trade is managedbetter by the African countries, especially Morocco, being the owners of this resource. Slightdiscounts on octopus are likely to materialize in the near future, but overall, the market is wellbalanced.

More octopus in the market

The Moroccan octopus fisheries started on 1 July2008, while some parts of the industry requested a furtherextension of the ban until 1 August 2008, in order to allowthe octopus grow further. Returns would also be higherthen, as bigger octopus gains better prices. In the end, thegovernment decided to start the fishing season as usual,in July. The fishery quota for the summer period will be fixedat 16 000 tonnes, a 30% rise compared to last year. Thisincrease in availability is likely to result in lower octopusprices. During the past months, octopus prices in Japanstarted to go down, expecting of plenty of arrivals.

Octopuses are reportedly very large at the moment,which makes fishing attractive. These larger specimenshave a good market in Europe, especially in Spain and onlya few will be sent to Japan. Moroccan fishermen will stopfishing when catches will start to be disappointing, sincehigh fuel costs make fishing attractive aonly if there is acertain return.

Japan increased its octopus imports, taking advan-tage of the relative abundance of supplies, especially fromMauritania. In the first quarter of 2008, some 11 400 tonneswere imported, almost 20% more than in the same period of2007. China, a country not bound by catch quotas, managedto double its export of octopus to the Japanese market.China thus became the number two supplier, overtakingMorocco.

Heavy arrivals of octopus resulted in a 9% increaseof coldstorage holdings of this species at the end of April2008. All these indicators: higher catch quotas in Morocco,heavy coldstorage holdings and huge imports from China,make a further reduction in octopus prices more than likely.

17GLOBEFISH Seafood Highlights 2/2008 17

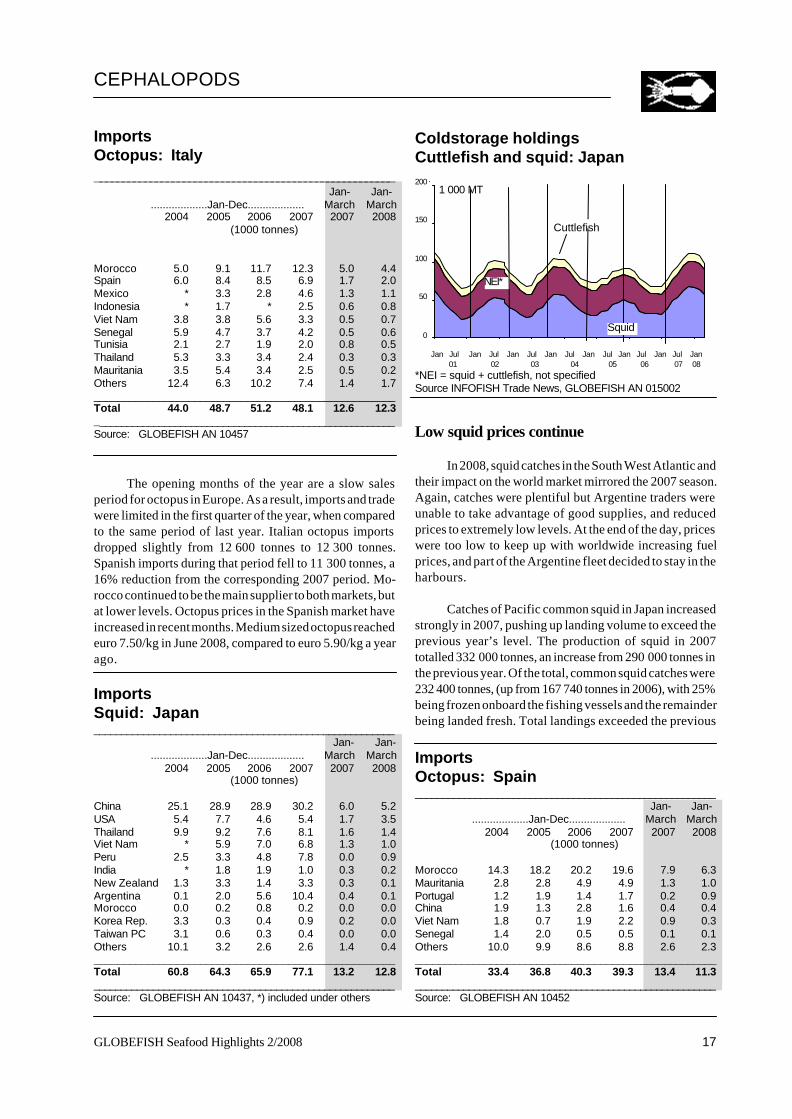

Coldstorage holdingsCuttlefish and squid: Japan200

150

100

50

0

Jan Jul Jan Jul Jan Jul Jan Jul Jan Jul Jan Jul Jan Jul Jan 01 02 03 04 05 06 07 08*NEI = squid + cuttlefish, not specifiedSource INFOFISH Trade News, GLOBEFISH AN 015002

ImportsSquid: Japan_______________________________________________________

Jan- Jan- ...................Jan-Dec................... March March

2004 2005 2006 2007 2007 2008(1000 tonnes)

China 25.1 28.9 28.9 30.2 6.0 5.2USA 5.4 7.7 4.6 5.4 1.7 3.5Thailand 9.9 9.2 7.6 8.1 1.6 1.4Viet Nam * 5.9 7.0 6.8 1.3 1.0Peru 2.5 3.3 4.8 7.8 0.0 0.9India * 1.8 1.9 1.0 0.3 0.2New Zealand 1.3 3.3 1.4 3.3 0.3 0.1Argentina 0.1 2.0 5.6 10.4 0.4 0.1Morocco 0.0 0.2 0.8 0.2 0.0 0.0Korea Rep. 3.3 0.3 0.4 0.9 0.2 0.0Taiwan PC 3.1 0.6 0.3 0.4 0.0 0.0Others 10.1 3.2 2.6 2.6 1.4 0.4___________________________________________________Total 60.8 64.3 65.9 77.1 13.2 12.8________________________________________________________Source: GLOBEFISH AN 10437, *) included under others

CEPHALOPODS

ImportsOctopus: Italy______________________________________________________

Jan- Jan- ...................Jan-Dec................... March March

2004 2005 2006 2007 2007 2008(1000 tonnes)

Morocco 5.0 9.1 11.7 12.3 5.0 4.4Spain 6.0 8.4 8.5 6.9 1.7 2.0Mexico * 3.3 2.8 4.6 1.3 1.1Indonesia * 1.7 * 2.5 0.6 0.8Viet Nam 3.8 3.8 5.6 3.3 0.5 0.7Senegal 5.9 4.7 3.7 4.2 0.5 0.6Tunisia 2.1 2.7 1.9 2.0 0.8 0.5Thailand 5.3 3.3 3.4 2.4 0.3 0.3Mauritania 3.5 5.4 3.4 2.5 0.5 0.2Others 12.4 6.3 10.2 7.4 1.4 1.7___________________________________________________Total 44.0 48.7 51.2 48.1 12.6 12.3________________________________________________________Source: GLOBEFISH AN 10457

NEI*

1 000 MT

Cuttlefish

Squid

The opening months of the year are a slow salesperiod for octopus in Europe. As a result, imports and tradewere limited in the first quarter of the year, when comparedto the same period of last year. Italian octopus importsdropped slightly from 12 600 tonnes to 12 300 tonnes.Spanish imports during that period fell to 11 300 tonnes, a16% reduction from the corresponding 2007 period. Mo-rocco continued to be the main supplier to both markets, butat lower levels. Octopus prices in the Spanish market haveincreased in recent months. Medium sized octopus reachedeuro 7.50/kg in June 2008, compared to euro 5.90/kg a yearago.

Low squid prices continue

In 2008, squid catches in the South West Atlantic andtheir impact on the world market mirrored the 2007 season.Again, catches were plentiful but Argentine traders wereunable to take advantage of good supplies, and reducedprices to extremely low levels. At the end of the day, priceswere too low to keep up with worldwide increasing fuelprices, and part of the Argentine fleet decided to stay in theharbours.

Catches of Pacific common squid in Japan increasedstrongly in 2007, pushing up landing volume to exceed theprevious year’s level. The production of squid in 2007totalled 332 000 tonnes, an increase from 290 000 tonnes inthe previous year. Of the total, common squid catches were232 400 tonnes, (up from 167 740 tonnes in 2006), with 25%being frozen onboard the fishing vessels and the remainderbeing landed fresh. Total landings exceeded the previous

ImportsOctopus: Spain_______________________________________________________

Jan- Jan- ...................Jan-Dec................... March March

2004 2005 2006 2007 2007 2008(1000 tonnes)

Morocco 14.3 18.2 20.2 19.6 7.9 6.3Mauritania 2.8 2.8 4.9 4.9 1.3 1.0Portugal 1.2 1.9 1.4 1.7 0.2 0.9China 1.9 1.3 2.8 1.6 0.4 0.4Viet Nam 1.8 0.7 1.9 2.2 0.9 0.3Senegal 1.4 2.0 0.5 0.5 0.1 0.1Others 10.0 9.9 8.6 8.8 2.6 2.3____________________________________________________Total 33.4 36.8 40.3 39.3 13.4 11.3________________________________________________________Source: GLOBEFISH AN 10452

GLOBEFISH Seafood Highlights 2/200818

ImportsSquid: Spain_______________________________________________________

Jan- Jan- ...................Jan-Dec................... March March

2004 2005 2006 2007 2007 2008(1000 tonnes)

Argentina 30.2 46.6 83.6 61.3 8.0 4.2Falkland/Malv. 28.4 48.0 42.4 40.3 7.0 3.5India 16.4 20.1 18.2 12.8 3.1 2.3China 12.5 7.0 8.1 6.4 1.8 1.9Morocco 2.6 3.7 4.5 1.4 0.4 0.6South Africa 6.8 5.0 4.0 3.5 1.0 1.2USA 5.8 3.6 3.9 1.7 0.6 1.0Korea Rep. 2.8 4.8 2.5 2.0 0.6 1.0Peru 9.8 3.7 1.8 4.5 1.1 0.3New Zealand 15.0 0.1 0.0 0.1 0.0 0.0Others 15.5 13.1 12.2 11.8 1.7 4.1___________________________________________________Total 145.8 155.7 181.2 145.8 25.3 20.1________________________________________________________Source: GLOBEFISH AN 10450

CEPHALOPODS

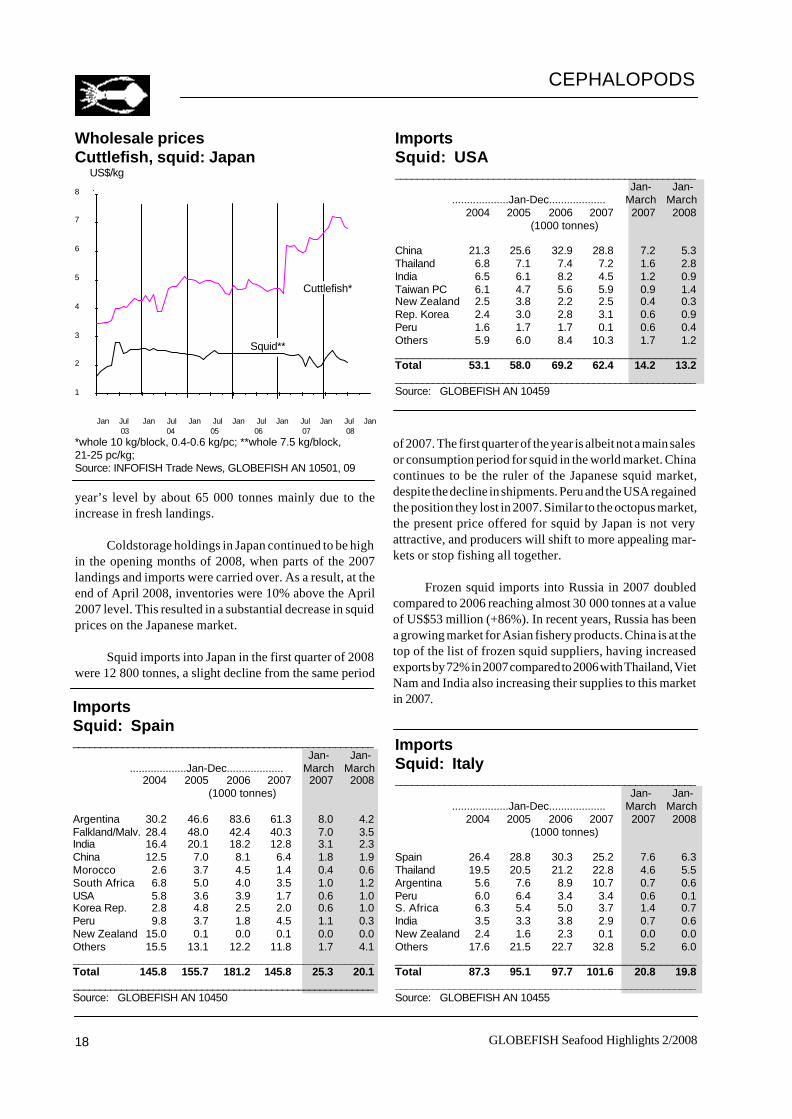

Wholesale pricesCuttlefish, squid: Japan

8

7

6

5

4

3

2

1

Jan Jul Jan Jul Jan Jul Jan Jul Jan Jul Jan Jul Jan 03 04 05 06 07 08*whole 10 kg/block, 0.4-0.6 kg/pc; **whole 7.5 kg/block,21-25 pc/kg;Source: INFOFISH Trade News, GLOBEFISH AN 10501, 09

US$/kg

Squid**

Cuttlefish*

ImportsSquid: Italy_______________________________________________________

Jan- Jan- ...................Jan-Dec................... March March

2004 2005 2006 2007 2007 2008(1000 tonnes)

Spain 26.4 28.8 30.3 25.2 7.6 6.3Thailand 19.5 20.5 21.2 22.8 4.6 5.5Argentina 5.6 7.6 8.9 10.7 0.7 0.6Peru 6.0 6.4 3.4 3.4 0.6 0.1S. Africa 6.3 5.4 5.0 3.7 1.4 0.7India 3.5 3.3 3.8 2.9 0.7 0.6New Zealand 2.4 1.6 2.3 0.1 0.0 0.0Others 17.6 21.5 22.7 32.8 5.2 6.0___________________________________________________Total 87.3 95.1 97.7 101.6 20.8 19.8________________________________________________________Source: GLOBEFISH AN 10455

ImportsSquid: USA_______________________________________________________

Jan- Jan- ...................Jan-Dec................... March March

2004 2005 2006 2007 2007 2008(1000 tonnes)

China 21.3 25.6 32.9 28.8 7.2 5.3Thailand 6.8 7.1 7.4 7.2 1.6 2.8India 6.5 6.1 8.2 4.5 1.2 0.9Taiwan PC 6.1 4.7 5.6 5.9 0.9 1.4New Zealand 2.5 3.8 2.2 2.5 0.4 0.3Rep. Korea 2.4 3.0 2.8 3.1 0.6 0.9Peru 1.6 1.7 1.7 0.1 0.6 0.4Others 5.9 6.0 8.4 10.3 1.7 1.2___________________________________________________Total 53.1 58.0 69.2 62.4 14.2 13.2________________________________________________________Source: GLOBEFISH AN 10459

year’s level by about 65 000 tonnes mainly due to theincrease in fresh landings.

Coldstorage holdings in Japan continued to be highin the opening months of 2008, when parts of the 2007landings and imports were carried over. As a result, at theend of April 2008, inventories were 10% above the April2007 level. This resulted in a substantial decrease in squidprices on the Japanese market.

Squid imports into Japan in the first quarter of 2008were 12 800 tonnes, a slight decline from the same period

of 2007. The first quarter of the year is albeit not a main salesor consumption period for squid in the world market. Chinacontinues to be the ruler of the Japanese squid market,despite the decline in shipments. Peru and the USA regainedthe position they lost in 2007. Similar to the octopus market,the present price offered for squid by Japan is not veryattractive, and producers will shift to more appealing mar-kets or stop fishing all together.