Surfing the Waves of Globalization: Asia and Financial Globalization

1

Globalization and its Impact:Globalization and its Impact:East Asia and VietnamEast Asia and Vietnam

Prepared for a Training of Trainers course on Trade Policy and WTO Accession, Hanoi, Vietnam, May 8-16, 2006

Yan Wang

The World Bank

2

Content•• Trends in Globalization / Trade /factor movementTrends in Globalization / Trade /factor movement

–– Goods, capital and laborGoods, capital and labor•• Underlying drivers /factors for GlobalizationUnderlying drivers /factors for Globalization

–– Theoretically, benefit of tradeTheoretically, benefit of trade–– Realistically, mixed results, why?Realistically, mixed results, why?

•• Trade integration in East AsiaTrade integration in East Asia

•• VietnamVietnam’’s trade and compositions trade and composition

•• SummarySummary

3

I. What is globalization?

• Global movements of goods, services and factors –capital, labor and ideas

• Global allocation of resources• Global sourcing /purchasing• Deeper division of labor / vertical and

horizontal / location flexible• More fierce competition /entry and exit

/Learning and Innovation crucial

4

TRADE:

• GOODS

• SERVICES

FACTOR MOBILITY:

Capital Human capital Labor

Substitutes:• labor• human capital

Complements or substitutes:• physical capital

Quest for diversification

Incomedifferentials

• Rising WTO power• Free-trade agreements

Technical change

Harmonization of values and rules

A Framework of Globalization: trade and factor mobility

Lower transport/telecom costs, internet

Lower trade barriers

Convergentconsumertastes

5

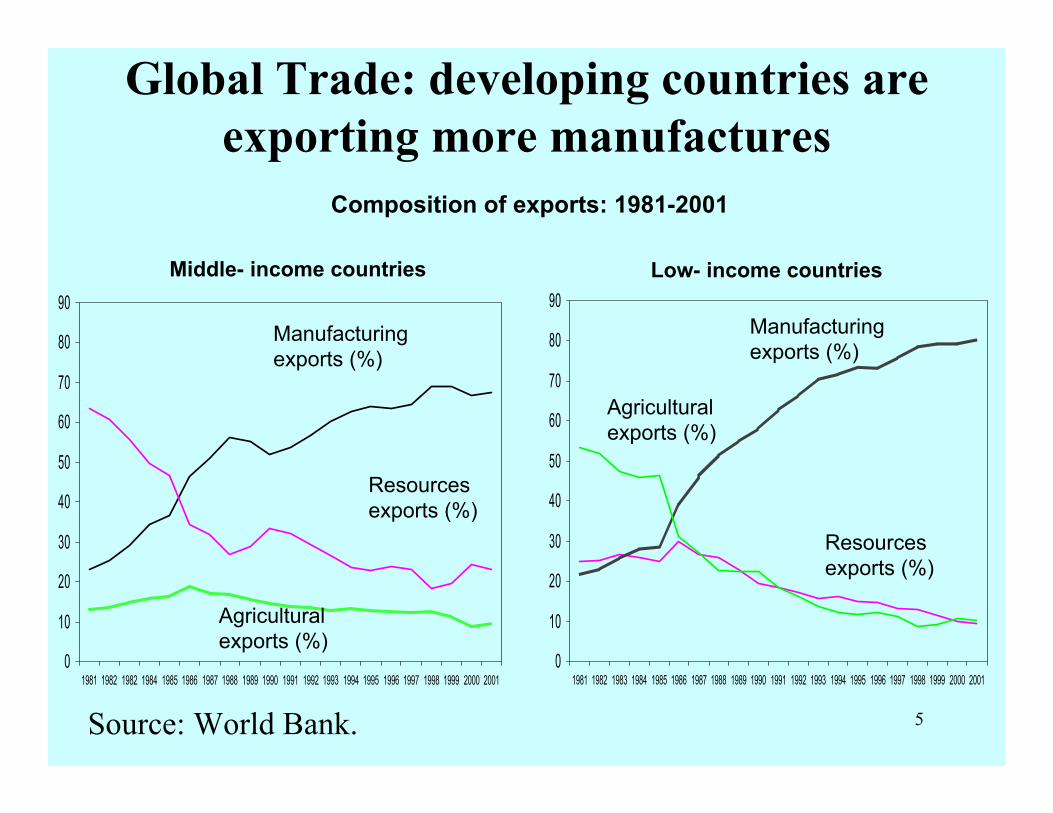

Global Trade: developing countries are exporting more manufactures

0

10

20

30

40

50

60

70

80

90

1981 1982 1982 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Manufacturing exports (%)

Resources exports (%)

Agricultural exports (%)

Composition of exports: 1981-2001

Middle- income countries

0

10

20

30

40

50

60

70

80

90

1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Low- income countries

Resources exports (%)

Agricultural exports (%)

Manufacturing exports (%)

Source: World Bank.

6

Significant trade reforms in the last two decades

0

5

10

15

20

25

30

35

40

SAS SSA LAC EAP MNA ECA OECD

Late 1980s

2004

Av. Tariffs %

Overall Trade Restrictiveness Index (OTRI), 2002

Source: World Bank.

7

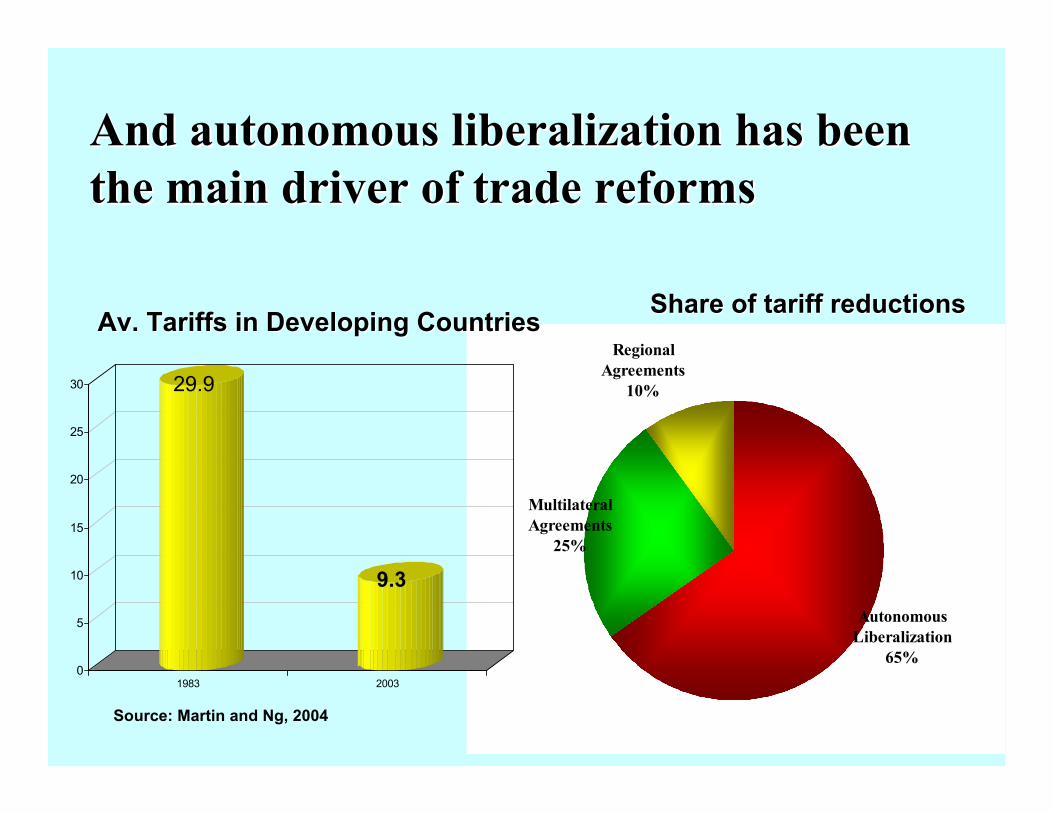

And autonomous liberalization has been And autonomous liberalization has been the main driver of trade reformsthe main driver of trade reforms

Regional Agreements

10%

Multilateral Agreements

25%

Autonomous Liberalization

65%

Share of tariff reductionsShare of tariff reductions

Source: Martin and Ng, 2004

0

5

10

15

20

25

30

1983 2003

Av. Tariffs in Developing CountriesAv. Tariffs in Developing Countries

29.9

9.3

8

–200

–100

0

100

200

300

82-892 90-942 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Total net private capital flowsNet direct investment Net private portfolio flows Other net private capital flows

1 In billions of US dollars. 2 Annual average.

Source: IMF, World Economic Outlook, September 2005.

Capital flows in emerging markets1

Int’l Capital Flows to Developing Countries

9

Labor Migration-- remittances are growing faster than Aid

020406080

100120140160180

Remittances FDI Private debt& equity

ODA

1995

2004

10

II. Underlying drivers /factors: - Pursuit of efficiency and growth- Lower trade barriers- Technical Progress --lower cost of transport- Pressure of international competition

• 1. Ricardo’s model is based on relative marginal cost

• 2. Heckscher-Ohlin model of comparative advantage is based on differences in factor endowments:– In each country the factor which is relatively abundant

will be relatively cheaper, and then the good which uses this factor relatively more intensively in its production will be relatively cheaper too. Therefore we expect a country to have its comparative advantage in goods relative intensive in the use of those factors which are in relatively abundant supply there.

11

Technological Advances has led to reduction in cost of transportation and ICT World transportation and insurance costs as a percentage of product value, 1950-93

Source : IMF, International Financial Statistics Yearbook

12

Global Local

Basic R&D

ComponentManufacturing

Product design

Marketing

Assembly

Global Allocation /Sourcing is possible:Local vs. global along the value chain

13

Theoretically under assumptions: Trade should benefit everyone

via factor price equalization• The third proposition of trade theory• 3. If trade is due to the existence of differences in

relative cost then free trade should eliminate such differences.

• In the case where comparative ad derives from differences in factor endowments, one expects that differences in domestic factor prices to be eliminated by trade.

• However, this depends on many assumptions including identical technology across countries.

• What is happening in reality?

14

Impact of globalization /trade reforms• Freer trade has led to rapid growth and poverty reduction in

some countries (East Asia, China, India, etc), but progress has been uneven:

• Some countries with solid export growth have not translated that into significant poverty reduction.

• There is growing anxiety in OECD countries with respect to the effects of globalization (high unemployment?);

• Developing countries could have done better if protection had been lower (particularly in agriculture).

• Roughly one-third of developing countries have not benefited significantly from trade expansion, some due to external factors such as domestic instability or civil wars.

• And many developing countries face significant supply constraints and infrastructure bottlenecks that hamper their integration into the world economy.

15

Skill Premium has been rising:Skilled/unskilled wage ratio, 1961-93

Sources: Sachs and Shatz (1995), Feenstra and Hanson (1995); Burtless (1995b)

16

Abundant in unskilled labor, scarce in capital

If protect Capital-Intensive Sectorstradeopens

K-intensive output expands, Labor-intensive output contracts,

Excess supply of unskilled labor

Unskilled wage is depressed

Both sectors becomemore intensive in unskilled labor

Full-employmentis preserved and poverty falls

If unskilled wage fixed, get unemployment

If abolish protection,Unemployment falls

The Stolper-Samuelson theorem: Relevant for Vietnam?

or

or

17

Employment and Real Wages (1970 = 100)

Source : OECD (1994), Part8, p.64 - Note : Real wages are total compensation per employee deflated by the GDP deflator.

18

Recent Studies reinforce effects of openness

• New endogenous growth model stress vertical innovations generated by research (Aghion and Howitt 1992) See also Melitz2003.

• New entrants with better products /services drive the old firms out--good for productivity.

• Frankel & Romer; Frankel and Rose; Noguer and Siscart (2005)– remove the effects of income from the export measure to confirm

implications of exports for growth• Findings corroborated by studies at firm level• Recent studies highlight importance of complementary policies

– Especially labor market flexibility to allow adjustment• Conclusion: Protection seems harmful for growth

19

III. Increased regional integration in EA

17.0%

9.0%

4.0% 3.0%

1.0%3.0%

0%2%4%6%8%

10%12%14%16%18%

Intra-regional trade as a share of GDP, 2003

Source: IMF DOT and WB WDI

East AsiaEast Asia Europe &Europe &Central AsiaCentral Asia

Latin Latin AmericaAmerica

Middle East Middle East & N. Africa& N. Africa

SouthSouthAsiaAsia

SubSub--Saharan Saharan AfricaAfrica

20

Trade Expansion in EAP (Export)(EAP, China, Japan and Korea)

EAP(not including Japan, Korea)

China

Japan

Korea, Rep.

0

200

400

600

800

1000

1200

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Expo

rt o

f Goo

ds &

Ser

vice

s(C

onst

ant 2

000

Bill

ion

US$

)

Source: World Development Indicators (April 2004)

21

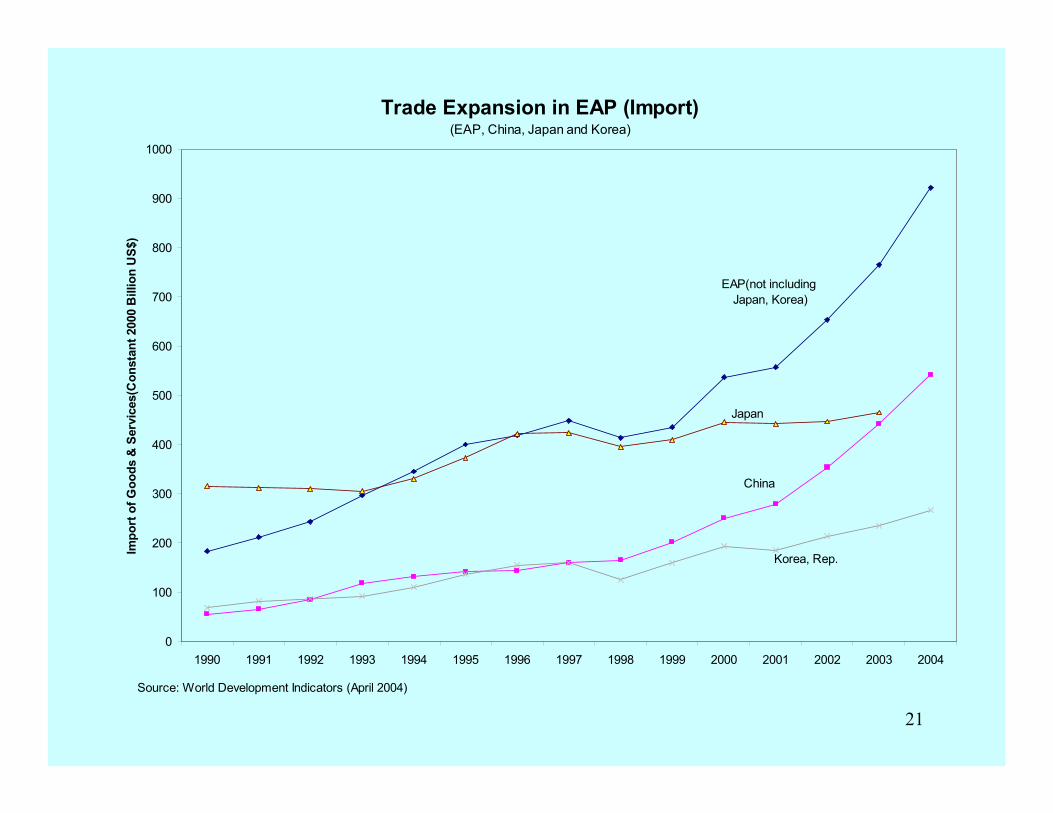

Trade Expansion in EAP (Import)(EAP, China, Japan and Korea)

EAP(not including Japan, Korea)

China

Japan

Korea, Rep.

0

100

200

300

400

500

600

700

800

900

1000

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Impo

rt o

f Goo

ds &

Ser

vice

s(C

onst

ant 2

000

Bill

ion

US$

)

Source: World Development Indicators (April 2004)

22

Trade Expansion in EAP (Export)(Cambodia, Indonesia, Mongolia, Philippines, Thailand, Vietnam)

Vietnam

Indonesia

Thailand

Philippines

MongoliaCambodia

0

10

20

30

40

50

60

70

80

90

100

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Expo

rt of

Goo

ds &

Ser

vice

s (C

onst

ant 2

000

Billi

on U

S$)

Source: World Development Indicators (April 2006)

IV. Vietnam’s Trade Expansion, Export

23

Trade Expansion in EAP (Import)(Cambodia, Indonesia, Mongolia, Philippines, Thailand, Vietnam)

Vietnam

Indonesia

Thailand

Philippines

MongoliaCambodia0

10

20

30

40

50

60

70

80

90

100

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Impo

rt of

Goo

ds &

Ser

vice

s (C

onst

ant 2

000

Bill

ion

US

$),

Source: World Development Indicators (April 2006).

Vietnam’s Trade Expansion: Import

24

Vietnam: Composition of Trade, 2000 and 2003

Food and live animals Beverages and tobaccoCrude materials, inedible, except f Mineral fuels, lubricants and relatAnimal and vegetable oils and fats ChemicalsManufact goods classif ied chiefly b Machinery and transport equipmentMiscellaneous manufactured articles Commod. & transacts. not class. acc

Export 2000

9%

0.1%

26%

3%

24%28%

6%

3%

1%0.4%

Import 2000

1%29%

6%

23%

15%

14%

4%4%3%

1%

Export 2003

21%

21%

3%

35%

1%

0.1%2%

7%9%

1%

Import 2003

1%

1%

14%

11%

4%5%5%0.1%

31%

28%

25

Vietnam: Direction of Trade--15 Biggest Trading Partners (1998-2003)Million US$

1998 1999 2000 2001 2002 2003Export

Japan 505 Japan 1786 Japan 2575 Japan 2510 USA 2453 USA 3939Korea Rep 479 Singapore 876 China 1536 China 1417 Japan 2437 Japan 2909USA 466 Australia 815 Australia 1272 USA 1066 China 1518 China 1883Thailand 381 China 746 Singapore 886 Singapore 1044 Australia 1328 Australia 1421Ukraine 360 Taiwan,China 682 Taiwan,China 757 Australia 1042 Singapore 961 Singapore 1025Free Zones 337 Germany 654 USA 733 Taiwan,China 806 Taiwan,China 818 Germany 855New Zealand 327 USA 504 Germany 730 Germany 722 Germany 729 UK 755UAE 323 UK 421 UK 479 UK 512 UK 572 Taiwan,China 749HK, China 319 Free Zones 420 Philippines 478 France 469 Korea, Rep. 473 France 494Myanmar 301 Philippines 393 Malaysia 414 Korea, Rep. 411 Iraq 440 Netherlands 493Lao PDR 252 France 354 Netherlands 391 Iraq 405 France 439 Korea, Rep. 492Singapore 250 Netherlands 343 France 382 Philippines 368 Netherlands 407 Indonesia 467Austria 241 Korea, Rep. 320 Thailand 372 Netherlands 367 Malaysia 348 Malaysia 454Canada 221 Thailand 313 Korea, Rep. 354 Belgium 341 HK, China 340 Belgium 391Taiwan,China 213 Belgium 307 Iraq 322 Malaysia 337 Belgium 337 HK, China 369

ImportKorea, Rep. 1155 Singapore 1878 Singapore 2694 Singapore 2478 Singapore 2533 China 3139Thailand 620 Japan 1618 Japan 2301 Japan 2183 Taiwan,China 2525 Japan 2979Germany 594 Taiwan,China 1566 Taiwan,China 1880 Taiwan, China 2009 Japan 2503 Taiwan,China 2915Netherlands 537 Korea, Rep. 1486 Korea, Rep. 1754 Korea, Rep. 1887 Korea, Rep. 2279 Singapore 2875Norway 473 China 673 China 1401 China 1606 China 2159 Korea, Rep. 2623Australia 469 Thailand 562 Thailand 811 Thailand 792 Thailand 955 Thailand 1282HK, China 393 HK, China 505 HK, China 597 HK, China 538 HK, China 803 United States 1141UK 376 USA 323 Malaysia 389 Malaysia 464 Malaysia 683 HK, China 974USA 374 Malaysia 305 USA 364 USA 411 Germany 558 Malaysia 925Taiwan,China 308 France 305 Indonesia 345 Germany 397 Russia 501 Germany 615Russia 303 Free Zones 287 France 331 Russia 376 USA 456 Indonesia 551New Zealand 303 Germany 269 Germany 295 France 300 Indonesia 363 Russia 492Japan 286 Russia 246 Australia 293 Indonesia 289 India 325 India 457Singapore 285 Australia 216 Russian Fede 240 Australia 266 France 294 France 405France 282 Lao PDR 197 India 178 India 228 Australia 286 Italy 374Source: World Integrated Trade Solution.

26

Conclusion• Globalization is inevitable, like it or not• Trade integration, int’l movements of goods, services

and factors are good for growth and poverty reduction [especially considering the new models of creative destruction]

• In reality, the full potential of trade and globalization has not been reached because of many distortions: protectionism, limitations on factor mobility, and domestic supply-side constraints, etc

• Therefore, complementary policies are needed to support the rural poor and vulnerable groups

• Vietnam has great potentials to compete in international market thanks to its comparative advantages, commitment to integrate, reform strategies that facilitate learning by doing.