Global trends in telecom development - ITU · Global trends in telecom development ... Digital...

35

Global trends in telecom development Seminar in Niamey, April 2001 The original document is elaborated by Dr Tim Kelly, ITU/SPU. It has completed by Saburo Tanaka and by Pape-Gorgui Toure. The views expressed in this presentation are those of the authors, a nd do not necessarily reflect the opinions of the ITU or its membership. Authors can be contacted by e -mail at: [email protected] [email protected] [email protected].

Transcript of Global trends in telecom development - ITU · Global trends in telecom development ... Digital...

Global trends in telecom development

Seminar in Niamey, April 2001

The original document is elaborated by Dr Tim Kelly, ITU/SPU. It has completed by Saburo Tanaka and by Pape-Gorgui Toure. The views expressed in this presentation are those of the authors, and do not necessarily reflect the opinions of the ITU or its membership. Authors can be contacted by e -mail at: [email protected] [email protected] [email protected].

Global trends in telecom Global trends in telecom developmentdevelopment

l The state of the industryð Fixed-linesð Mobileð The Internet

l The state of the marketð Increasing competitionð Private sector participationð Independent regulation

l Situation in Africað Addressing the digital divideð Traffic and tariffs trendsð Tariff rebalancing

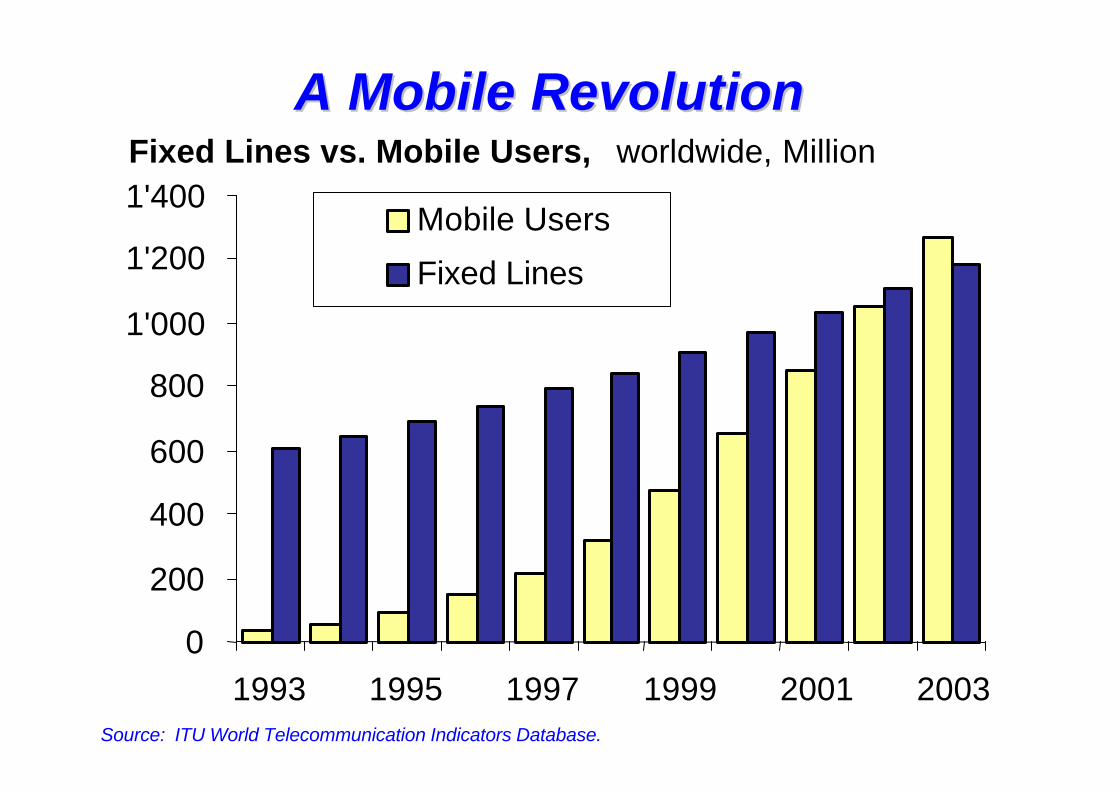

A Mobile RevolutionA Mobile Revolution

Source: ITU World Telecommunication Indicators Database.

0

200

400

600

800

1'000

1'200

1'400

1993 1995 1997 1999 2001 2003

Mobile Users

Fixed Lines

Fixed Lines vs. Mobile Users, worldwide, Million

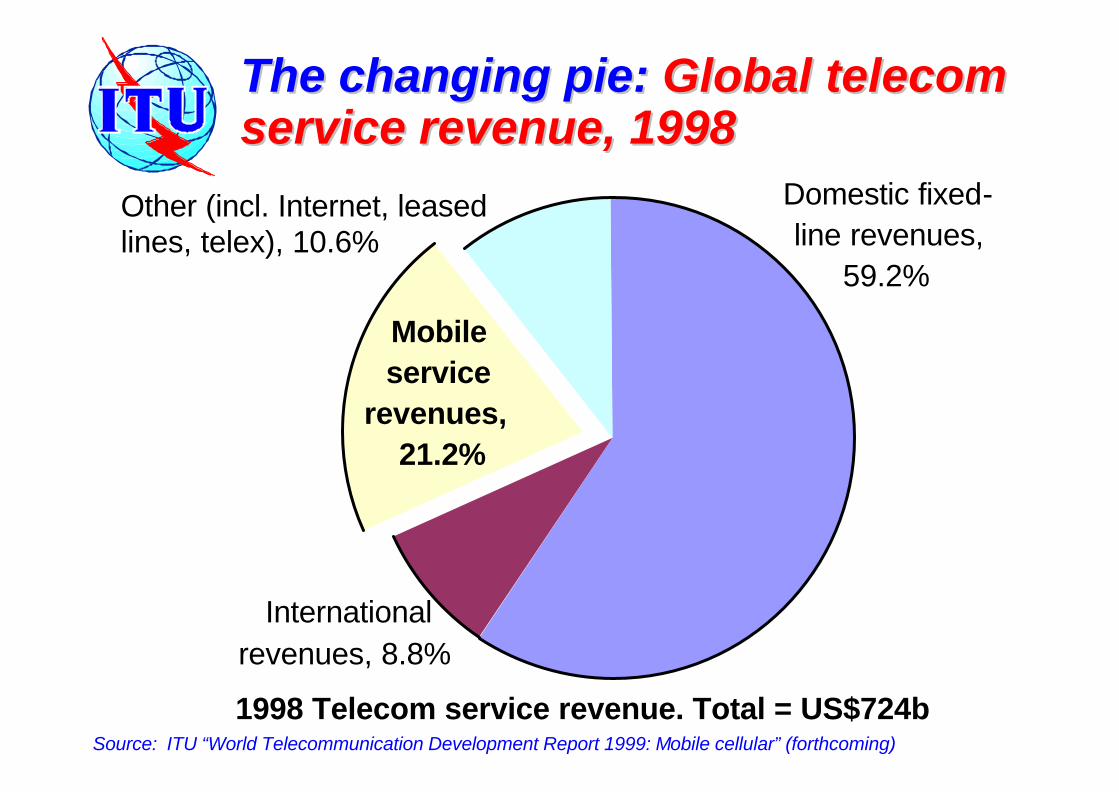

Domestic fixed-line revenues,

59.2%

International revenues, 8.8%

Mobile service

revenues, 21.2%

Other (incl. Internet, leased lines, telex), 10.6%

1998 Telecom service revenue. Total = US$724b

The changing pie: The changing pie: Global telecom Global telecom service revenue, 1998service revenue, 1998

Source: ITU “World Telecommunication Development Report 1999: Mobile cellular” (forthcoming)

0

100

200

300

400

500

600

700

800

900

1000

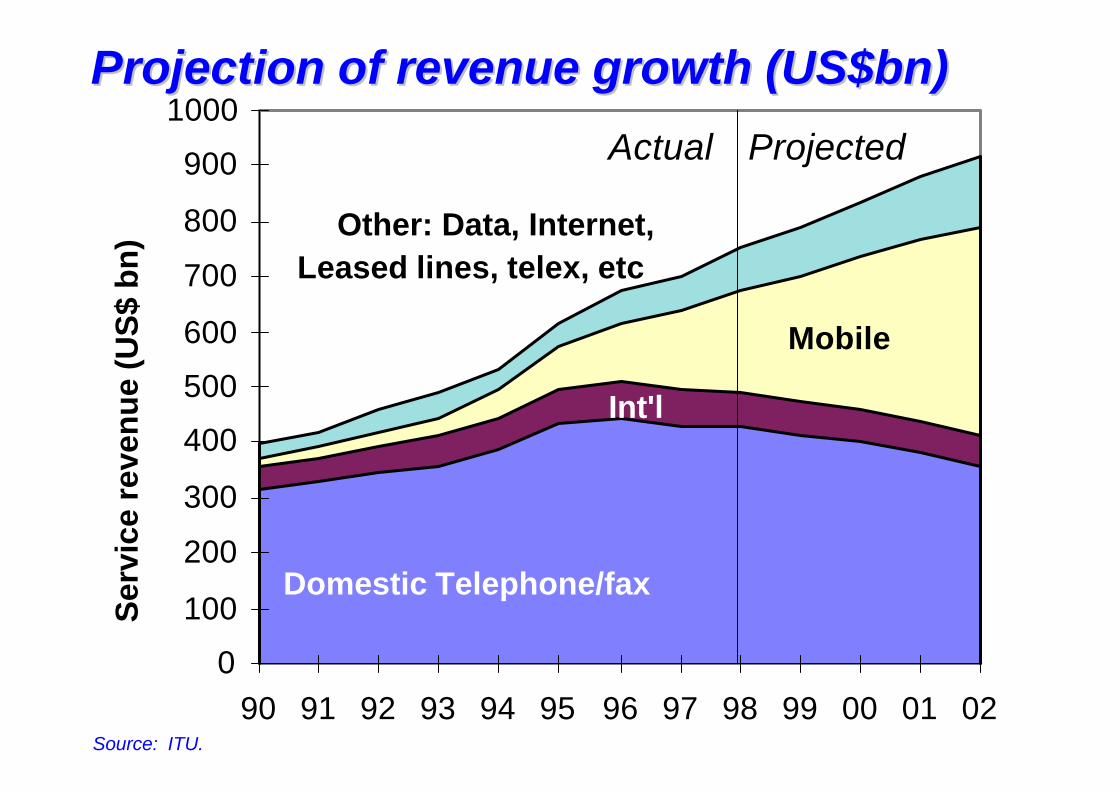

90 91 92 93 94 95 96 97 98 99 00 01 02

Ser

vice

rev

enu

e (U

S$

bn

)Actual Projected

Domestic Telephone/fax

Int'l

Mobile

Other: Data, Internet, Leased lines, telex, etc

Projection of revenue growth (US$bn)Projection of revenue growth (US$bn)

Source: ITU.

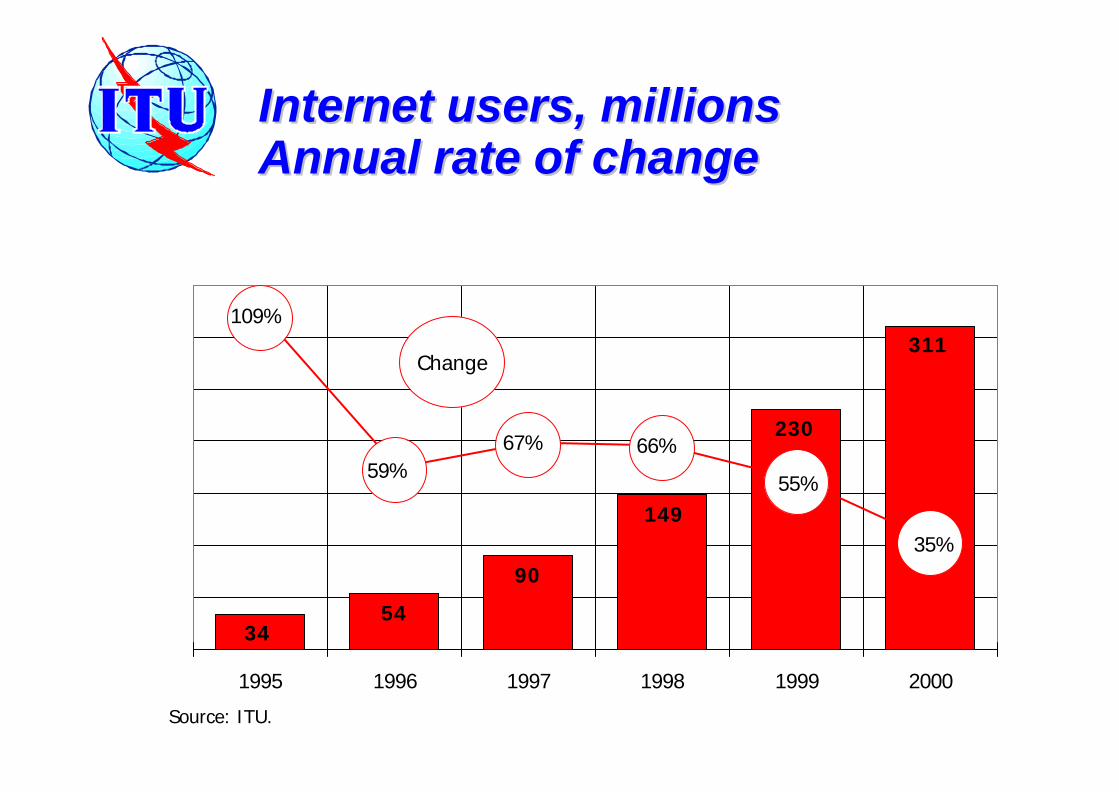

Internet users, millionsInternet users, millionsAnnual rate of changeAnnual rate of change

311

230

3454

90

14935%

55%

66%67%59%

109%

1995 1996 1997 1998 1999 2000

Change

Source: ITU.

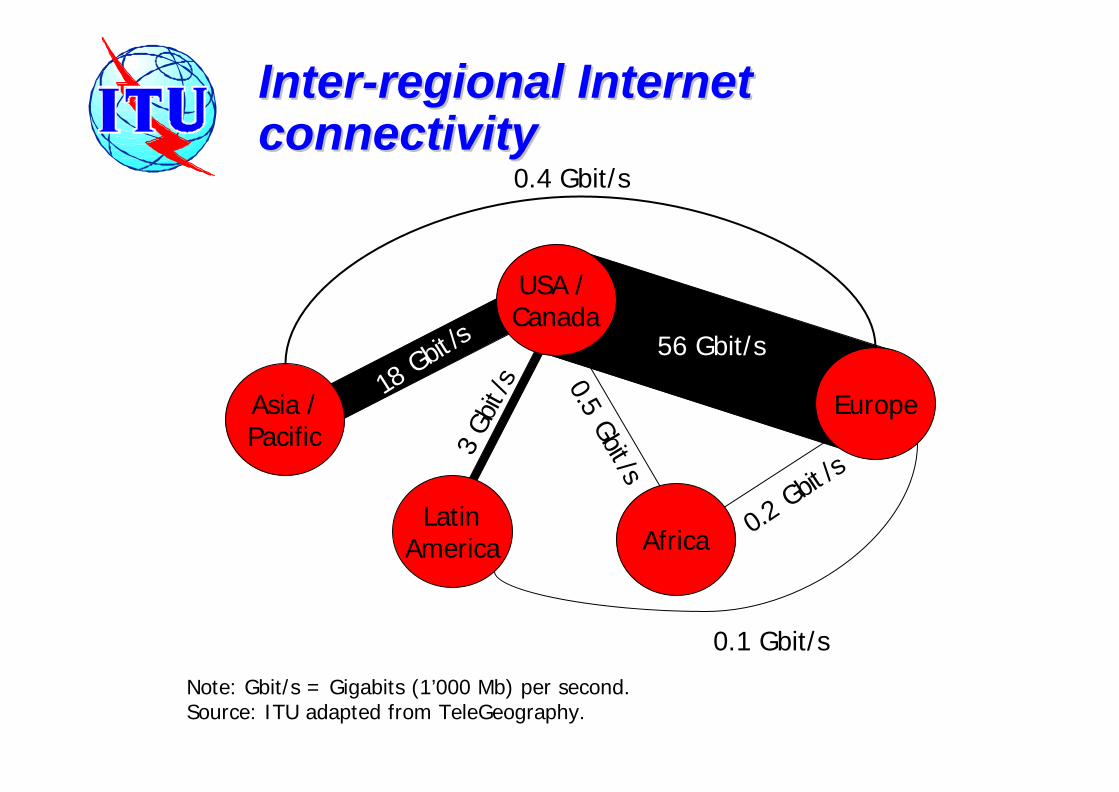

InterInter--regional Internet regional Internet connectivityconnectivity

Asia /Pacific

LatinAmerica

USA / Canada

Europe

Africa

56 Gbit/s

0.1 Gbit/s

0.5 Gbit/s

Note: Gbit/s = Gigabits (1’000 Mb) per second.Source: ITU adapted from TeleGeography.

18 Gbit /

s

0.4 Gbit/s

3 Gb

it /s

0.2 Gbit

/s

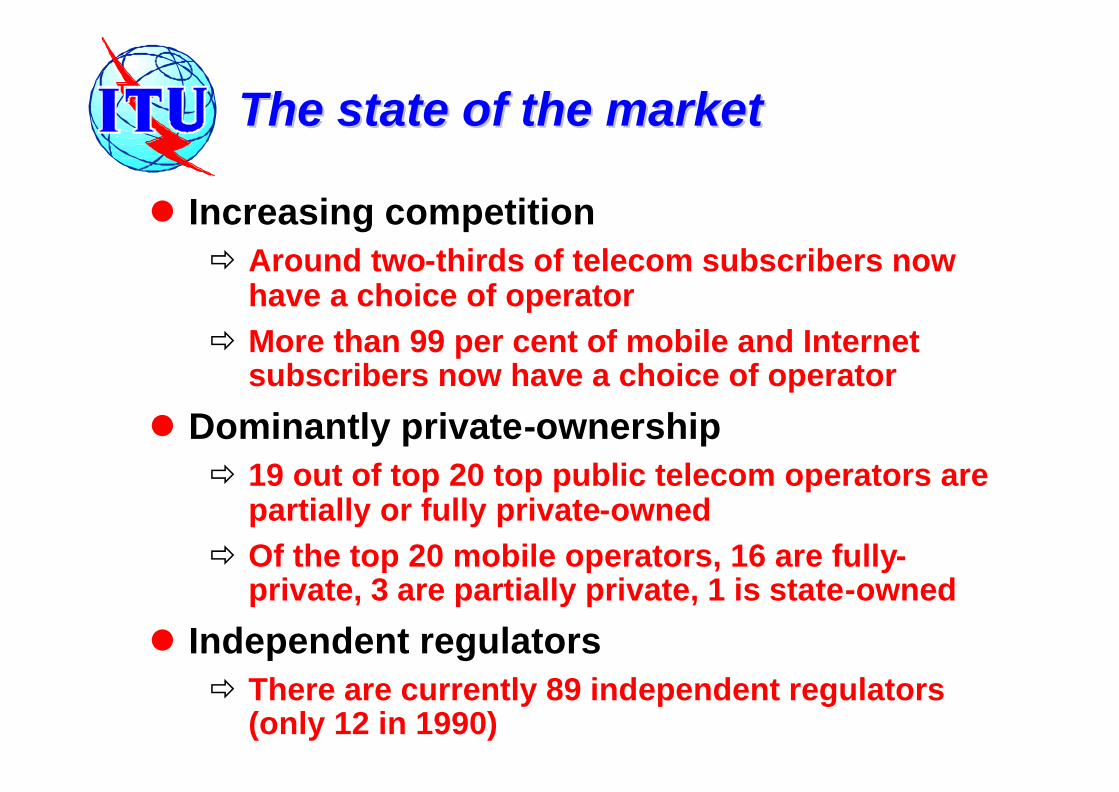

The state of the marketThe state of the market

l Increasing competitionð Around two-thirds of telecom subscribers now

have a choice of operatorð More than 99 per cent of mobile and Internet

subscribers now have a choice of operator

l Dominantly private-ownershipð 19 out of top 20 top public telecom operators are

partially or fully private-ownedð Of the top 20 mobile operators, 16 are fully-

private, 3 are partially private, 1 is state-owned

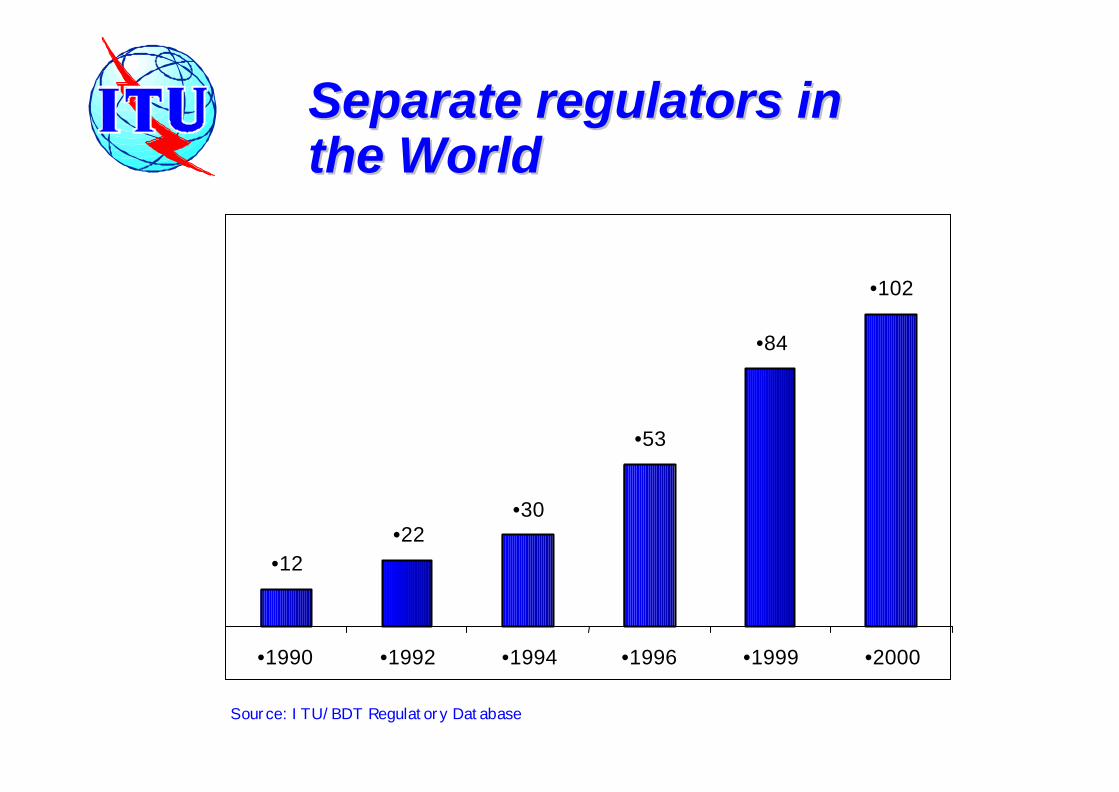

l Independent regulatorsð There are currently 89 independent regulators

(only 12 in 1990)

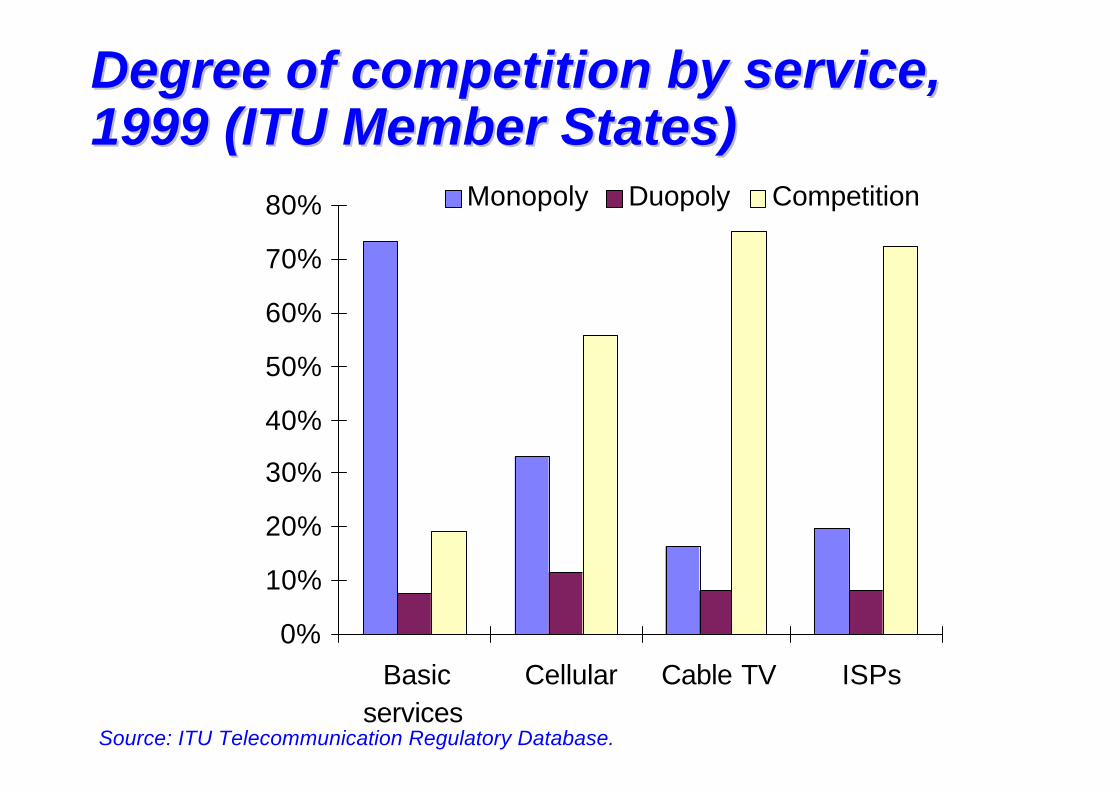

Degree of competition by service, Degree of competition by service, 1999 (ITU Member States)1999 (ITU Member States)

Source: ITU Telecommunication Regulatory Database.

0%

10%

20%

30%

40%

50%

60%

70%

80%

Basicservices

Cellular Cable TV ISPs

Monopoly Duopoly Competition

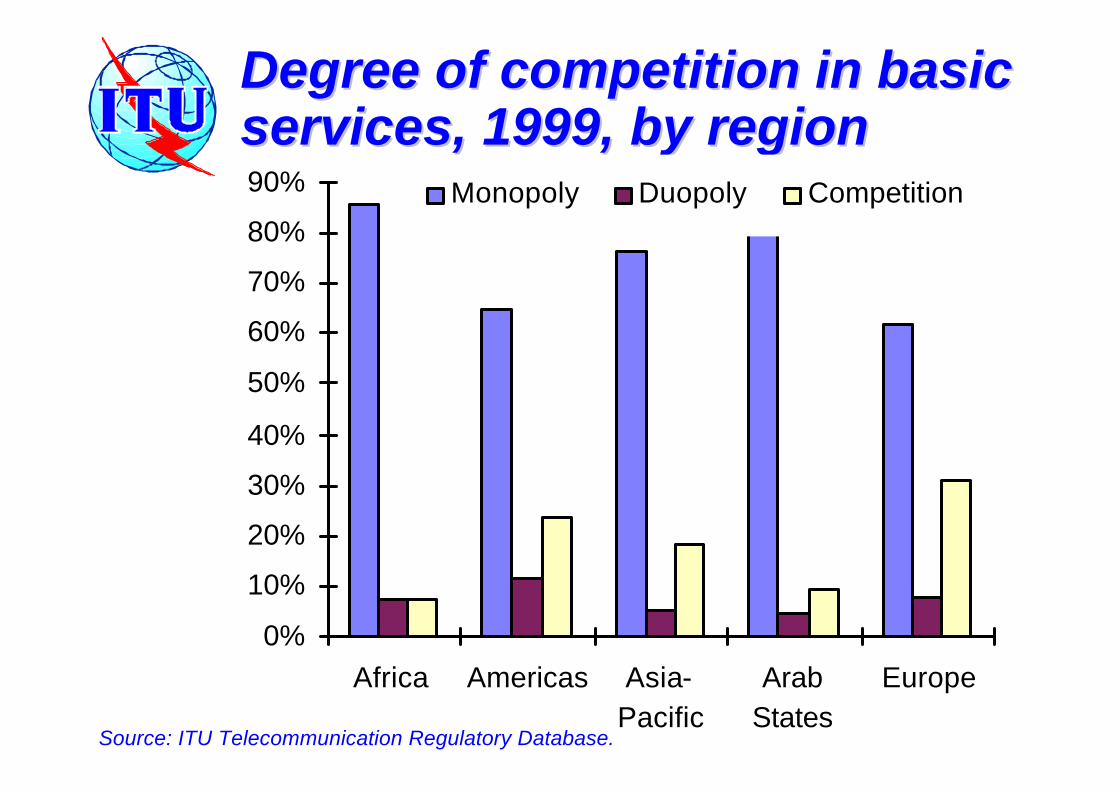

Degree of competition in basic Degree of competition in basic services, 1999, by regionservices, 1999, by region

Source: ITU Telecommunication Regulatory Database.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Africa Americas Asia-Pacific

ArabStates

Europe

Monopoly Duopoly Competition

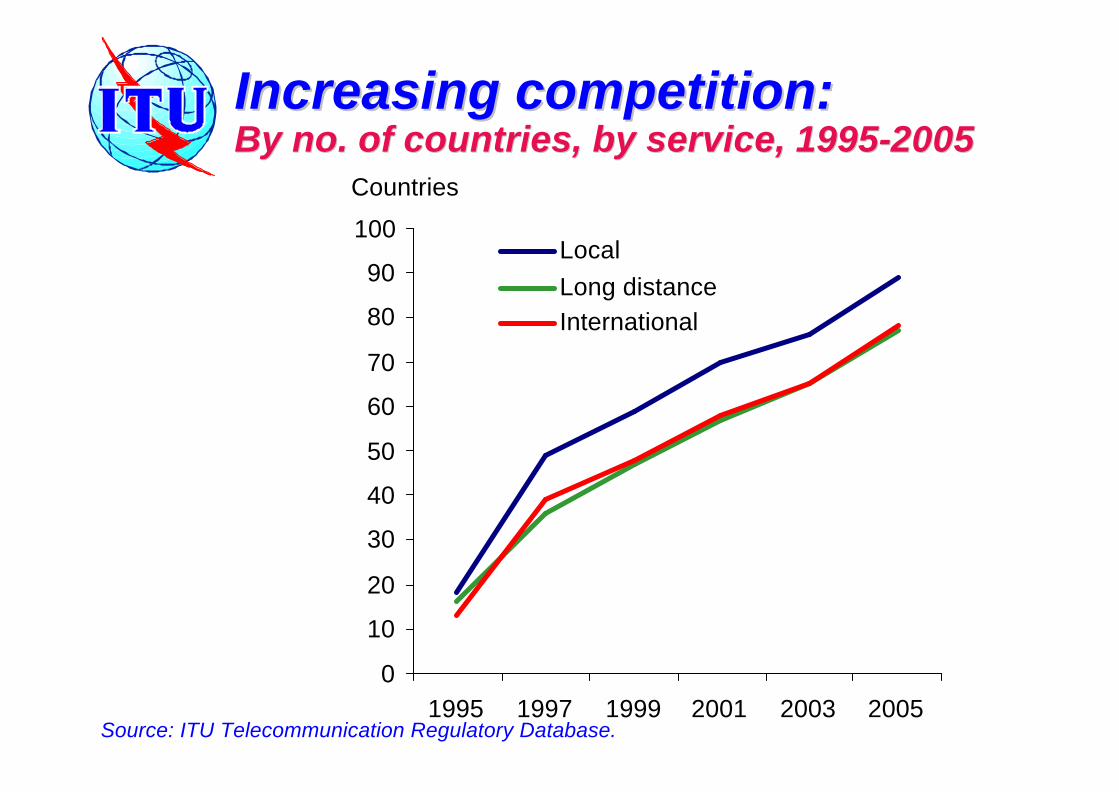

0

10

20

30

40

50

60

70

80

90

100

1995 1997 1999 2001 2003 2005

LocalLong distanceInternational

Countries

Increasing competition: Increasing competition: By no. of countries, by service, 1995By no. of countries, by service, 1995--20052005

Source: ITU Telecommunication Regulatory Database.

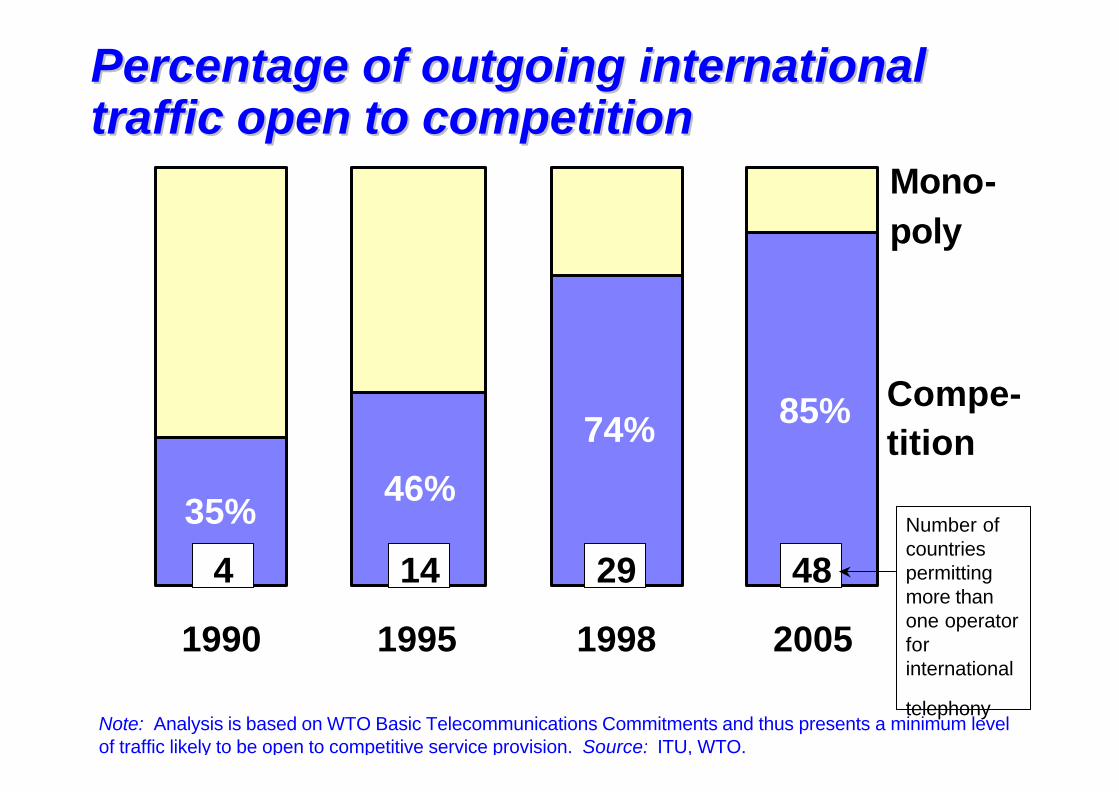

35%46%

74% 85%

1990 1995 1998 2005

Mono-poly

Compe-tition

4 14 29 48Number of countries permitting more than one operator for international

telephony

Percentage of outgoing international Percentage of outgoing international traffic open to competitiontraffic open to competition

Note: Analysis is based on WTO Basic Telecommunications Commitments and thus presents a minimum level of traffic likely to be open to competitive service provision. Source: ITU, WTO.

Recent privatisation transactionsRecent privatisation transactions

Source: ITU Telecommunication Regulatory Database. Note: Some countries made sales in severaltranches (e.g., Spain)

1995 1996 1997 1998Bolivia Belgium Armenia BrazilCape Verde Germany Australia Denmark (2)Cuba Ghana Cote d'Ivoire FranceCzech Rep. Greece France El SalvadorIndonesia Guinea Greece FinlandMongolia Hungary Hungary GuatemalaPortugal Indonesia India (MTNL) LithuaniaSpain Ireland India (VSNL) Malta

Korea Israel PolandPeru Italy Puerto RicoPortugal Kazakhstan RomaniaSingapore Panama SwitzerlandVenezuela Portugal

SenegalSerbiaSouth AfricaSri LankaSpain

0

20

40

60

80

100

120

140

160

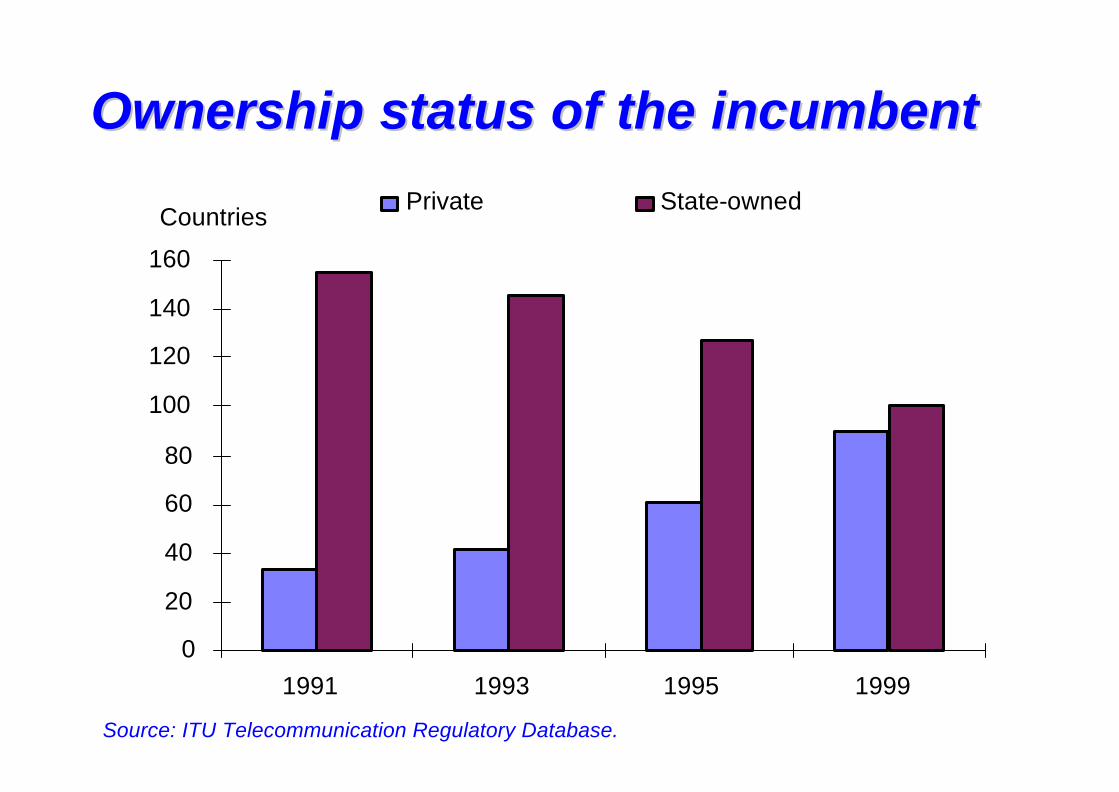

1991 1993 1995 1999

Private State-ownedCountries

Ownership status of the incumbentOwnership status of the incumbent

Source: ITU Telecommunication Regulatory Database.

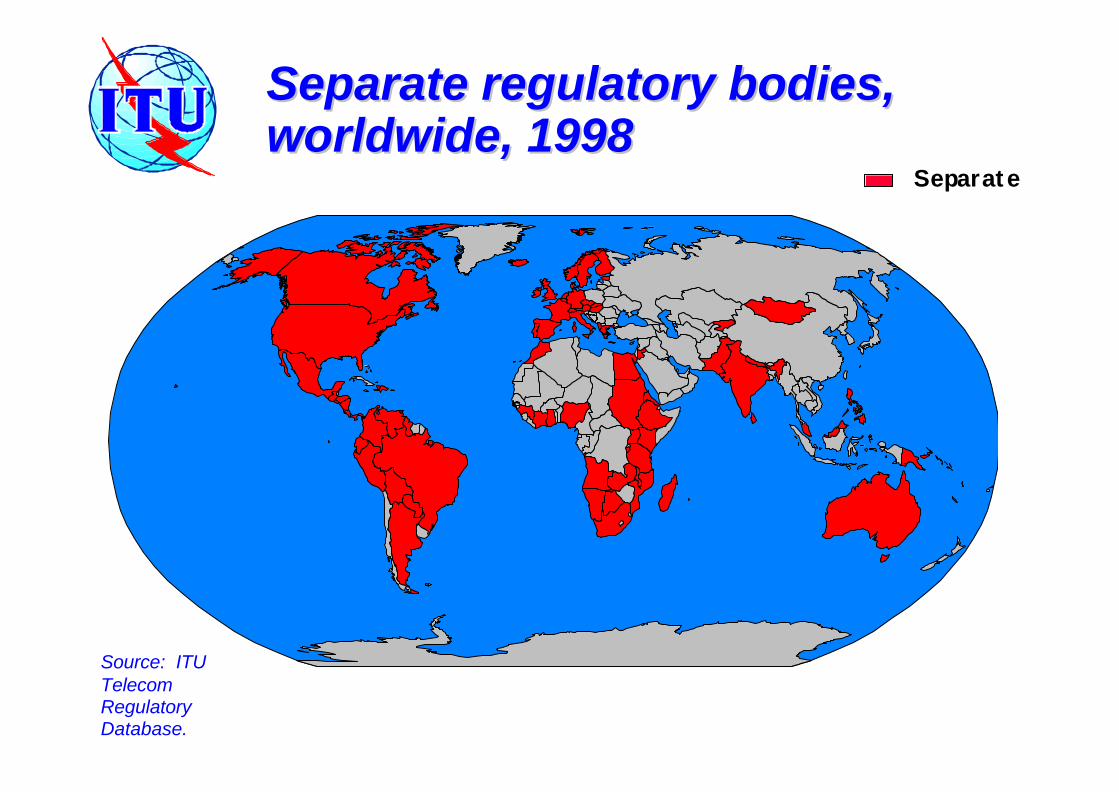

Separate

Separate regulatory bodies, Separate regulatory bodies, worldwide, 1998worldwide, 1998

Source: ITU Telecom Regulatory Database.

Source: ITU World Telecommunication Indicators Database.

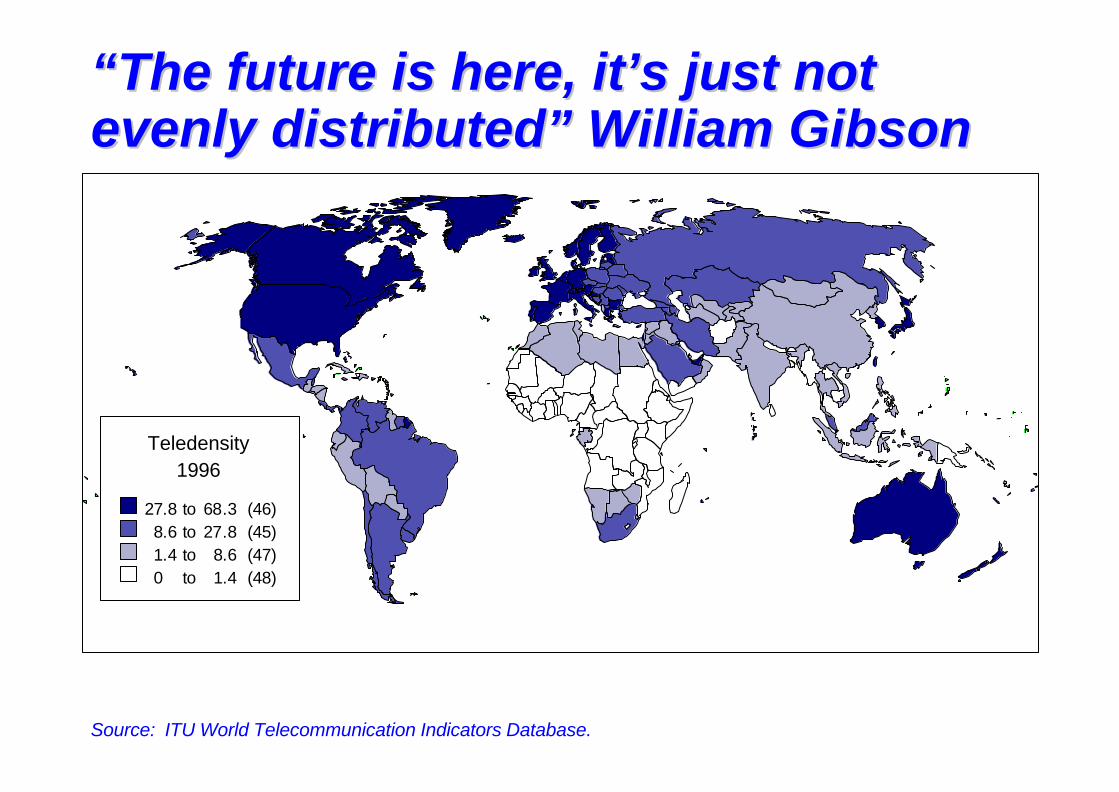

“The future is here, it’s just not “The future is here, it’s just not evenly distributed” William Gibsonevenly distributed” William Gibson

Teledensity1996

27.8 to 68.3 (46)8.6 to 27.8 (45)1.4 to 8.6 (47)0 to 1.4 (48)

0%10%20%30%40%50%60%70%80%90%

100%

Internetusers

Mobile users

Telephonelines

Popul-ation

High income

Upper-mid income

Lower-mid income

Low income

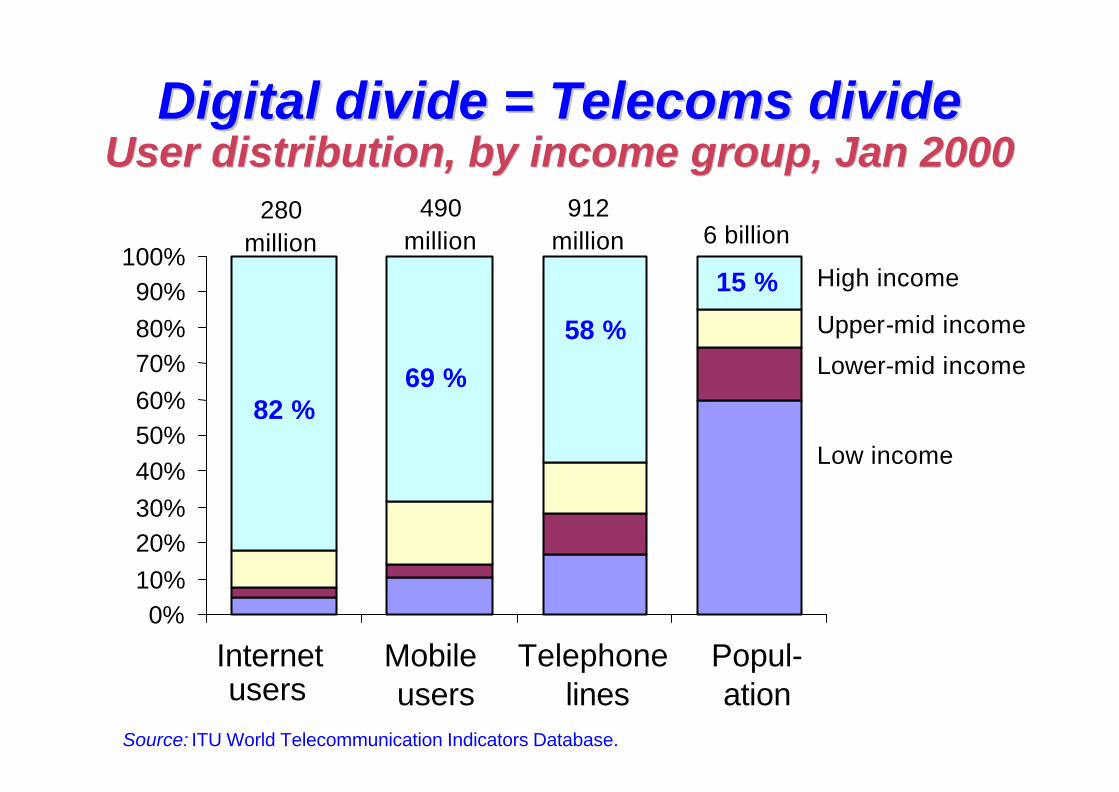

280 million

490 million

912 million 6 billion

82 %69 %

58 %

15 %

Digital divide = Telecoms divideDigital divide = Telecoms divideUser distribution, by income group, Jan 2000User distribution, by income group, Jan 2000

Source: ITU World Telecommunication Indicators Database.

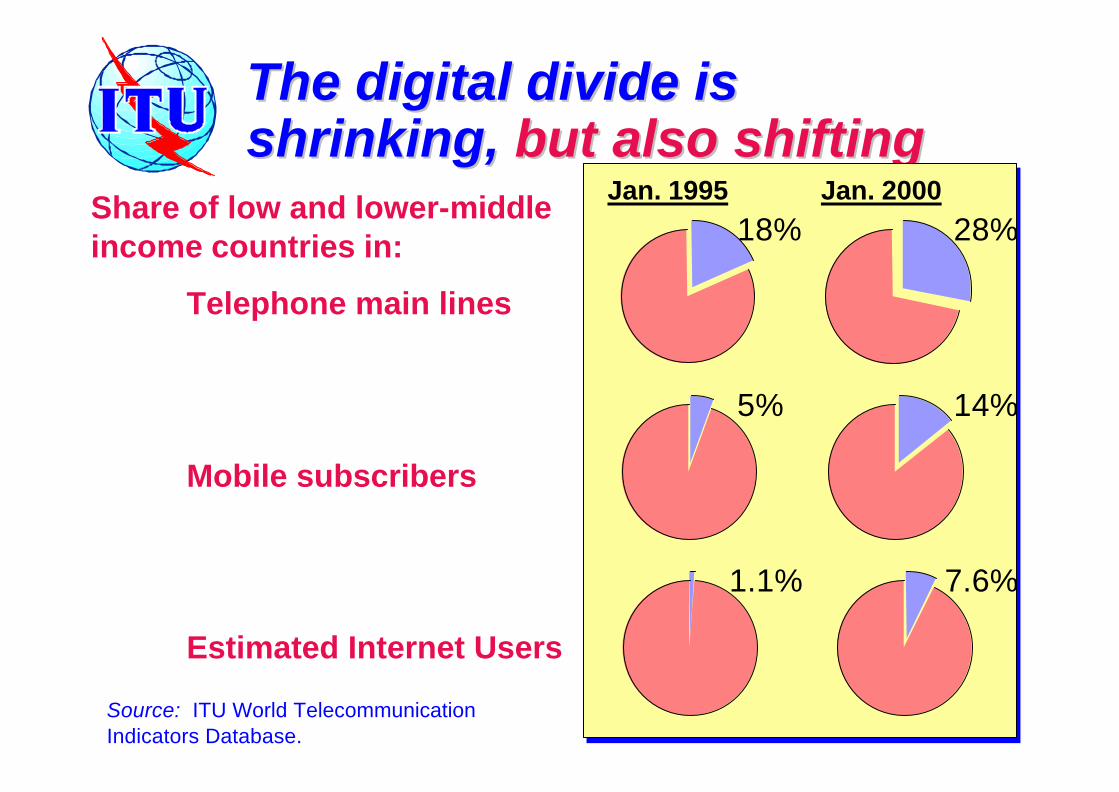

The digital divide is The digital divide is shrinking, shrinking, but also shiftingbut also shifting

Share of low and lower-middle income countries in:

Telephone main lines

Mobile subscribers

Estimated Internet Users

Source: ITU World Telecommunication Indicators Database.

18%Jan. 1995 Jan. 2000

28%

5% 14%

1.1% 7.6%

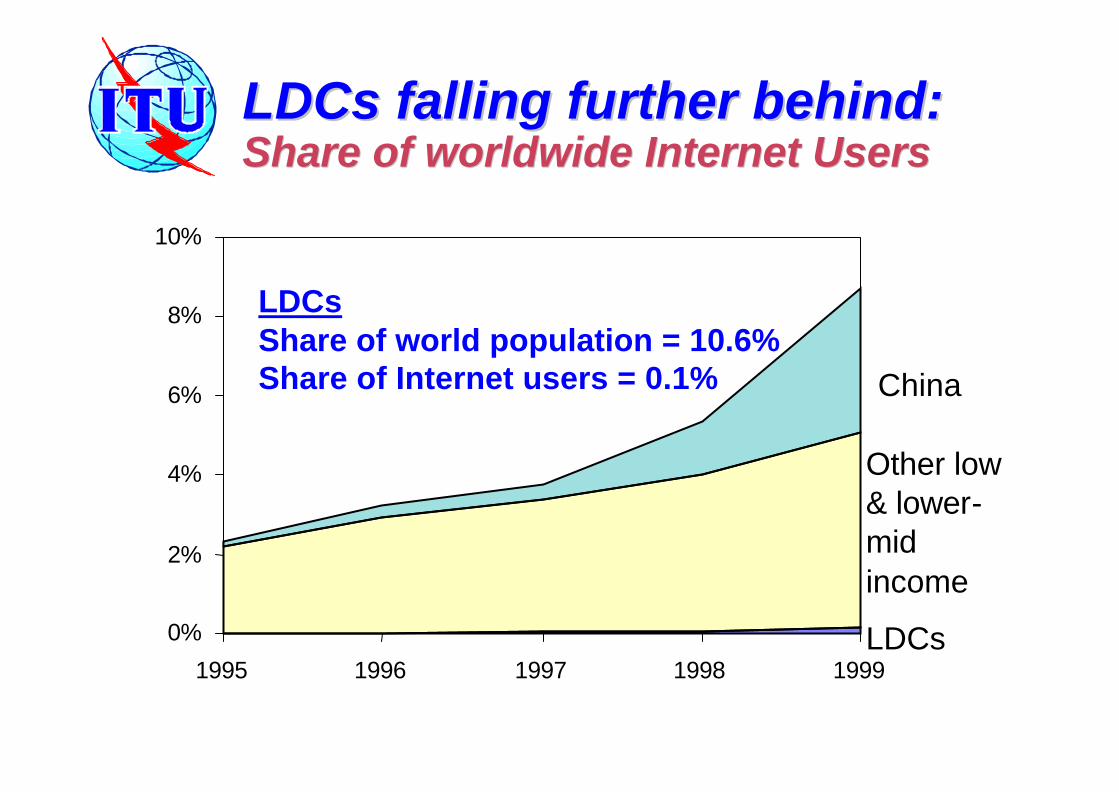

LDCs falling further behind:LDCs falling further behind:Share of worldwide Internet UsersShare of worldwide Internet Users

LDCsShare of world population = 10.6%Share of Internet users = 0.1%

0%

2%

4%

6%

8%

10%

1995 1996 1997 1998 1999

China

Other low & lower-mid income

LDCs

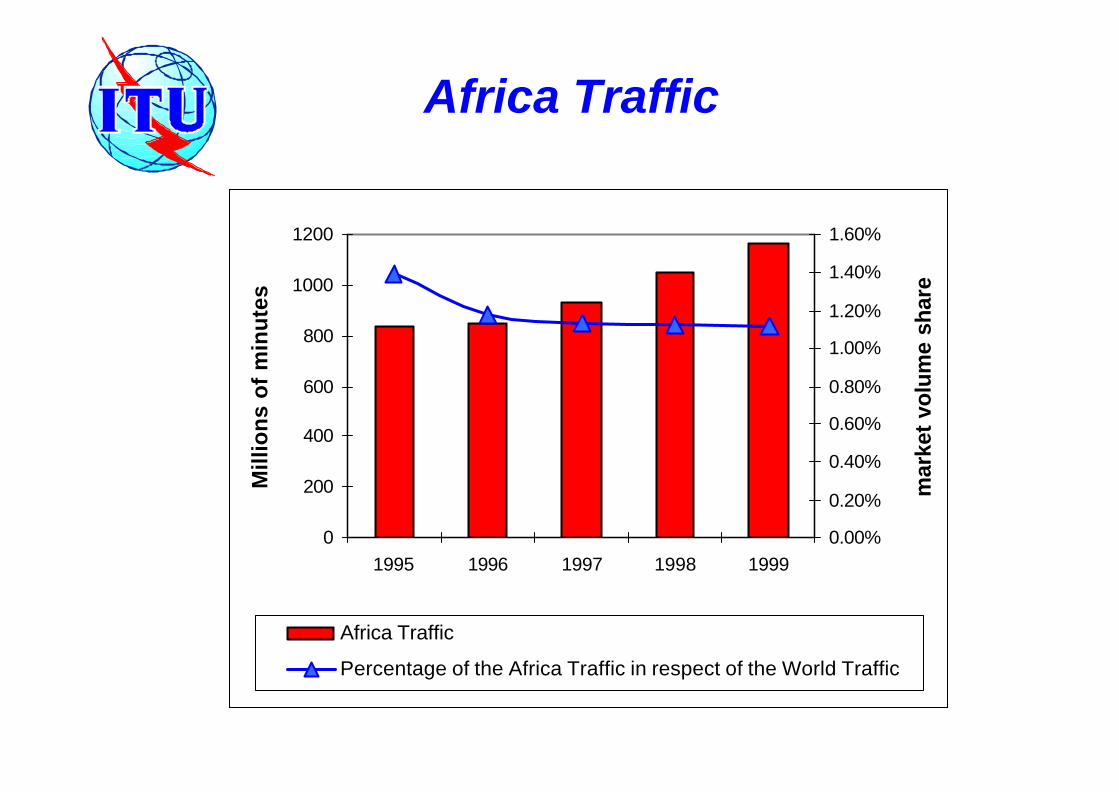

Africa Traffic

0

200

400

600

800

1000

1200

1995 1996 1997 1998 1999

Mill

ion

s o

f m

inu

tes

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

1.40%

1.60%

mar

ket

volu

me

shar

e

Africa Traffic

Percentage of the Africa Traffic in respect of the World Traffic

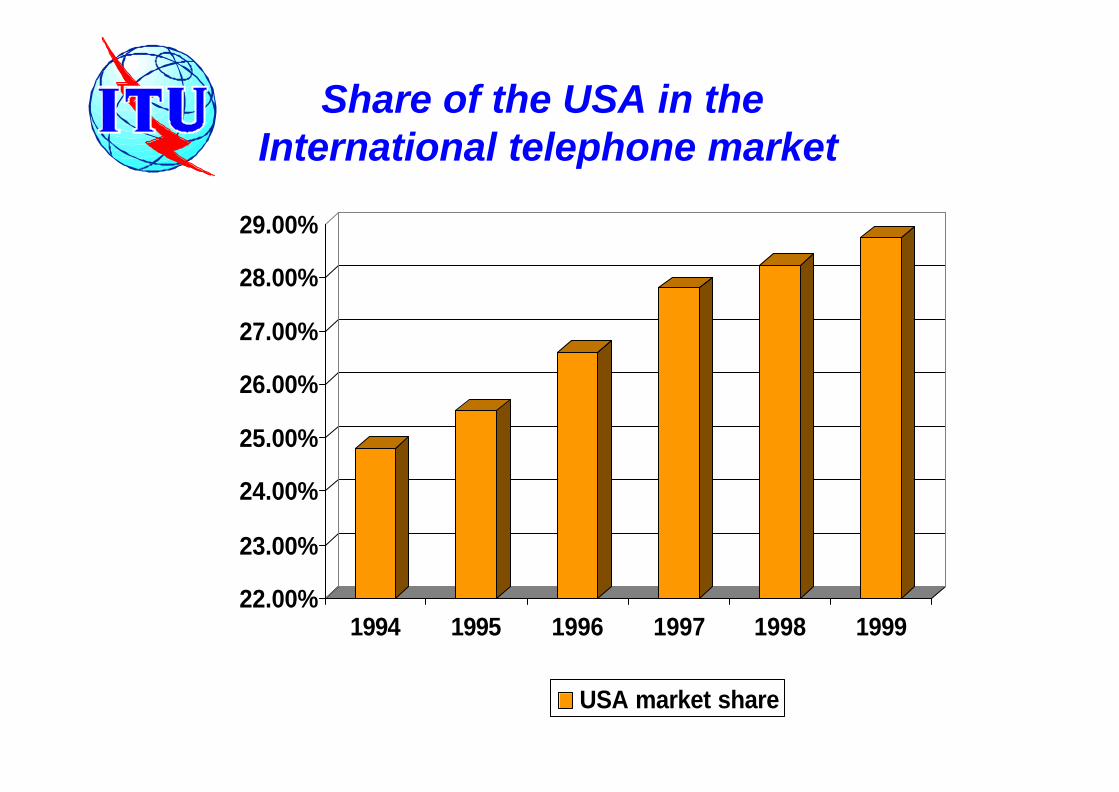

22.00%

23.00%

24.00%

25.00%

26.00%

27.00%

28.00%

29.00%

1994 1995 1996 1997 1998 1999

USA market share

Share of the USA in the International telephone market

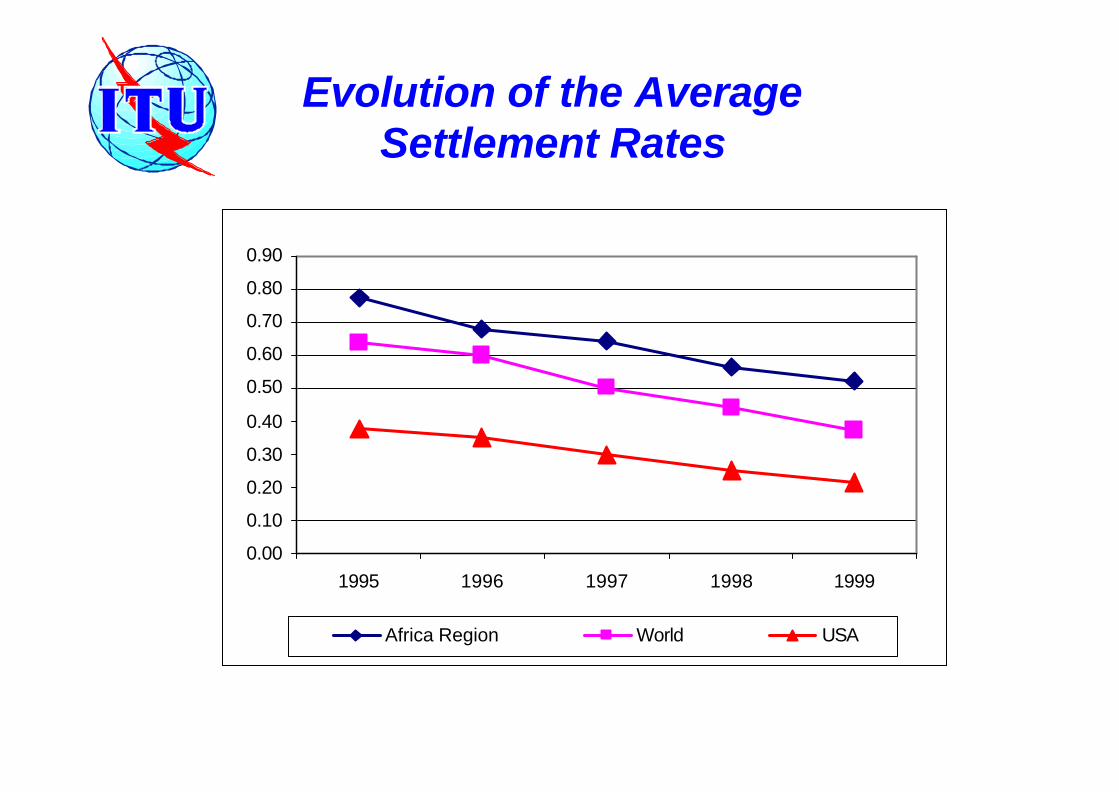

Evolution of the Average Settlement Rates

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1995 1996 1997 1998 1999

Africa Region World USA

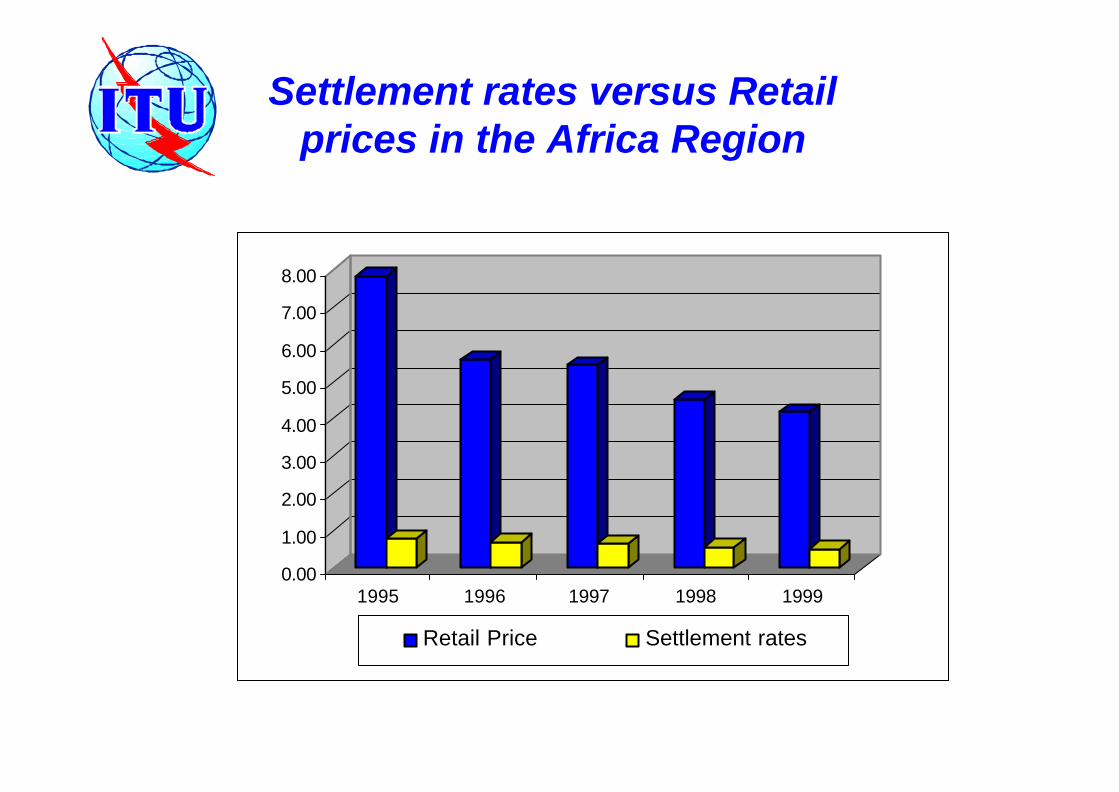

Settlement rates versus Retail prices in the Africa Region

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

1995 1996 1997 1998 1999

Retail Price Settlement rates

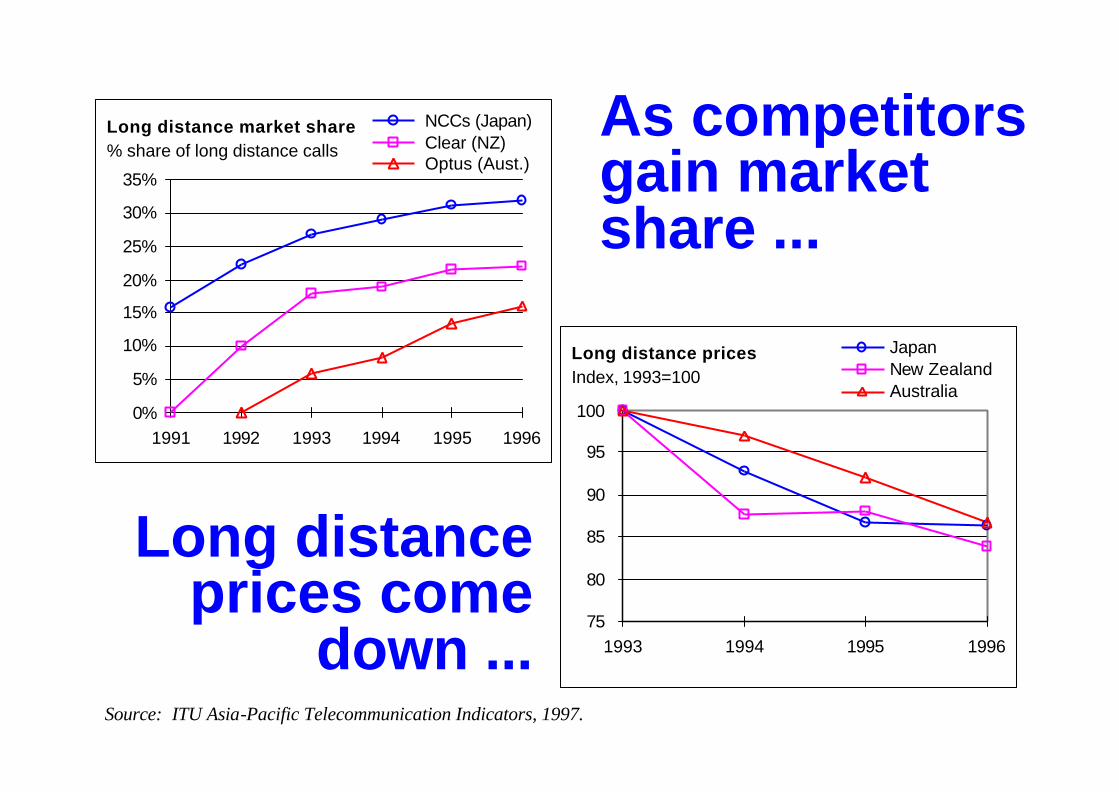

Long distance market share% share of long distance calls

0%

5%

10%

15%

20%

25%

30%

35%

1991 1992 1993 1994 1995 1996

NCCs (Japan) Clear (NZ) Optus (Aust.)

Long distance pricesIndex, 1993=100

75

80

85

90

95

100

1993 1994 1995 1996

JapanNew ZealandAustralia

As competitors gain market share ...

Long distance prices come

down ...Source: ITU Asia-Pacific Telecommunication Indicators, 1997.

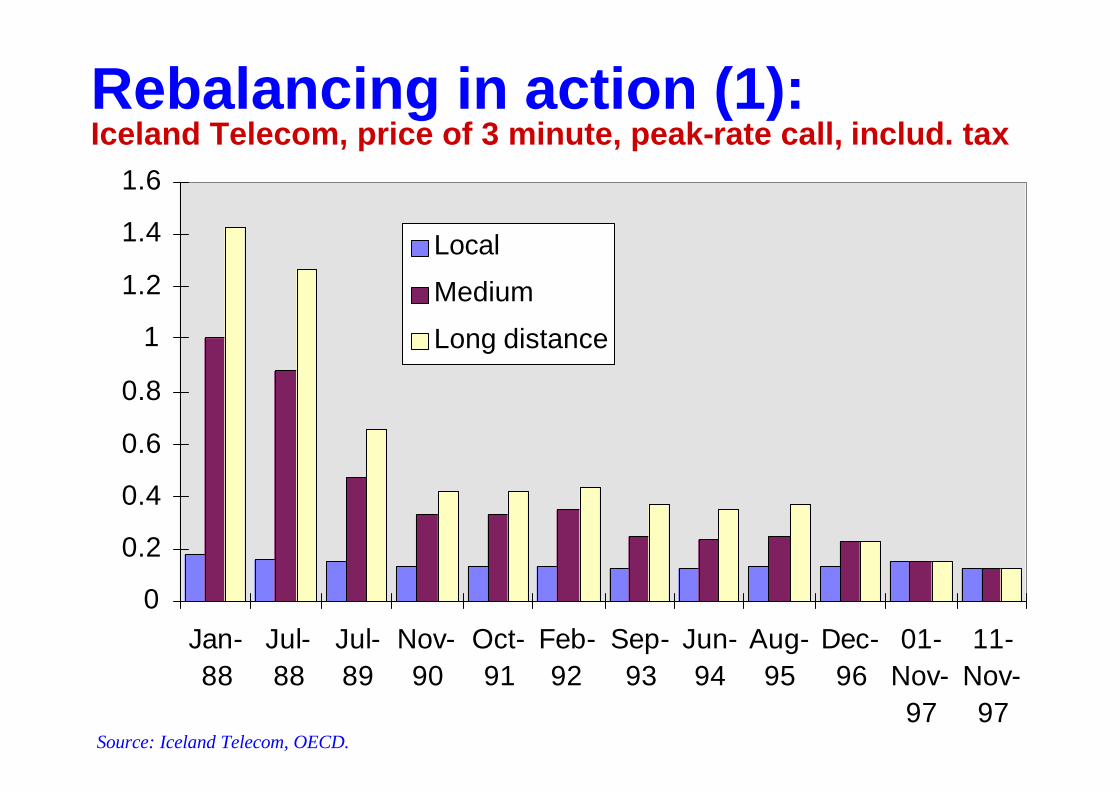

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

Jan-88

Jul-88

Jul-89

Nov-90

Oct-91

Feb-92

Sep-93

Jun-94

Aug-95

Dec-96

01-Nov-97

11-Nov-97

Local

Medium

Long distance

Rebalancing in action (1): Iceland Telecom, price of 3 minute, peak-rate call, includ. tax

Source: Iceland Telecom, OECD.

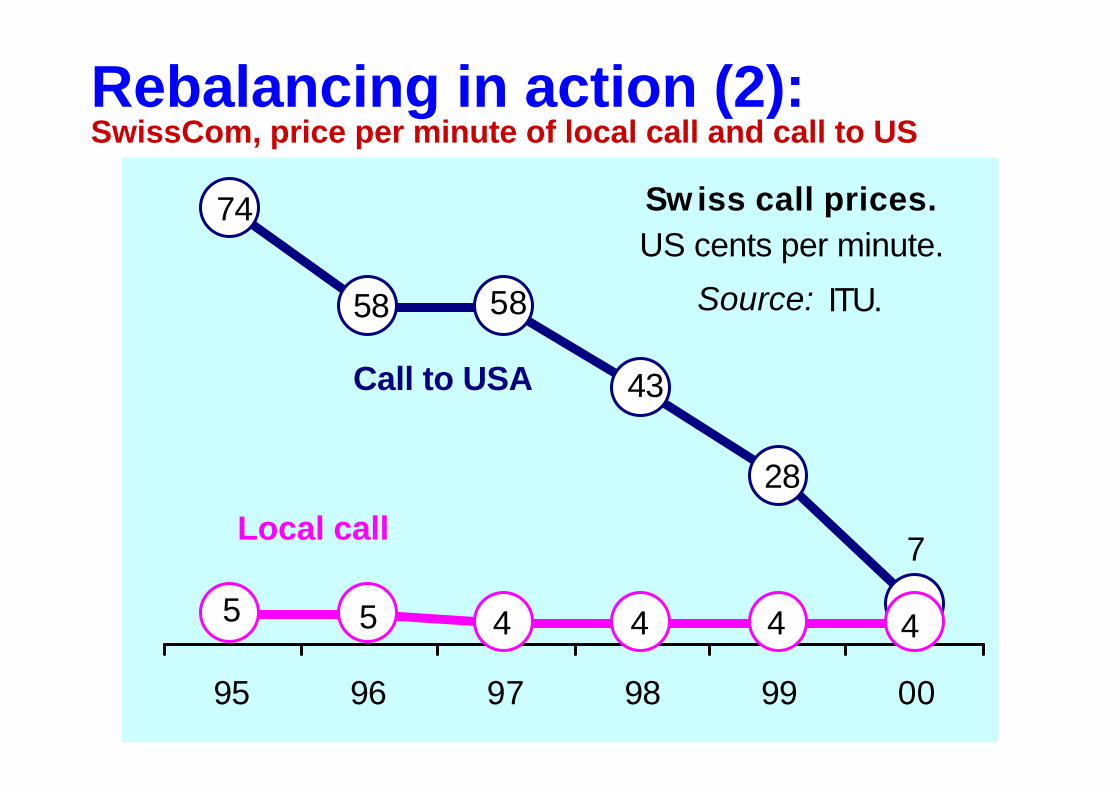

Rebalancing in action (2): SwissCom, price per minute of local call and call to US

7

28

43

5858

74

444455

95 96 97 98 99 00

Sw iss call prices. US cents per minute.

Source: ITU.

Call to USA

Local call

0

2

4

6

8

10

12

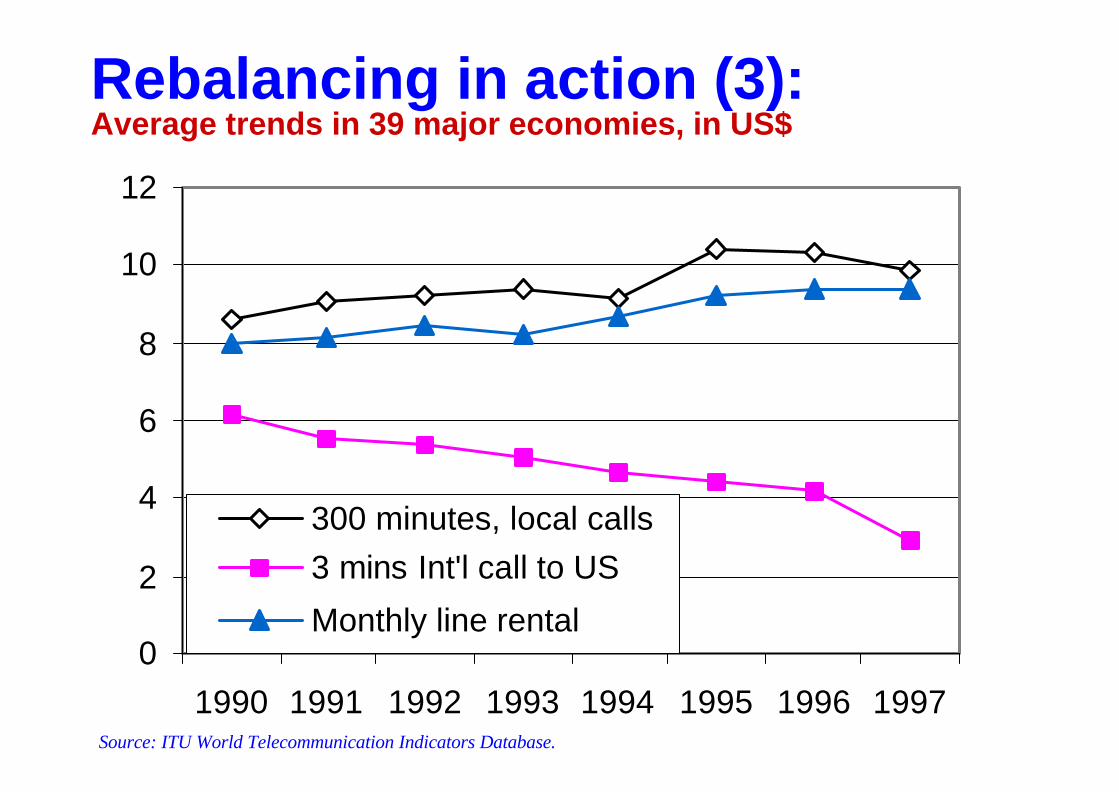

1990 1991 1992 1993 1994 1995 1996 1997

300 minutes, local calls3 mins Int'l call to US

Monthly line rental

Source: ITU World Telecommunication Indicators Database.

Rebalancing in action (3): Average trends in 39 major economies, in US$

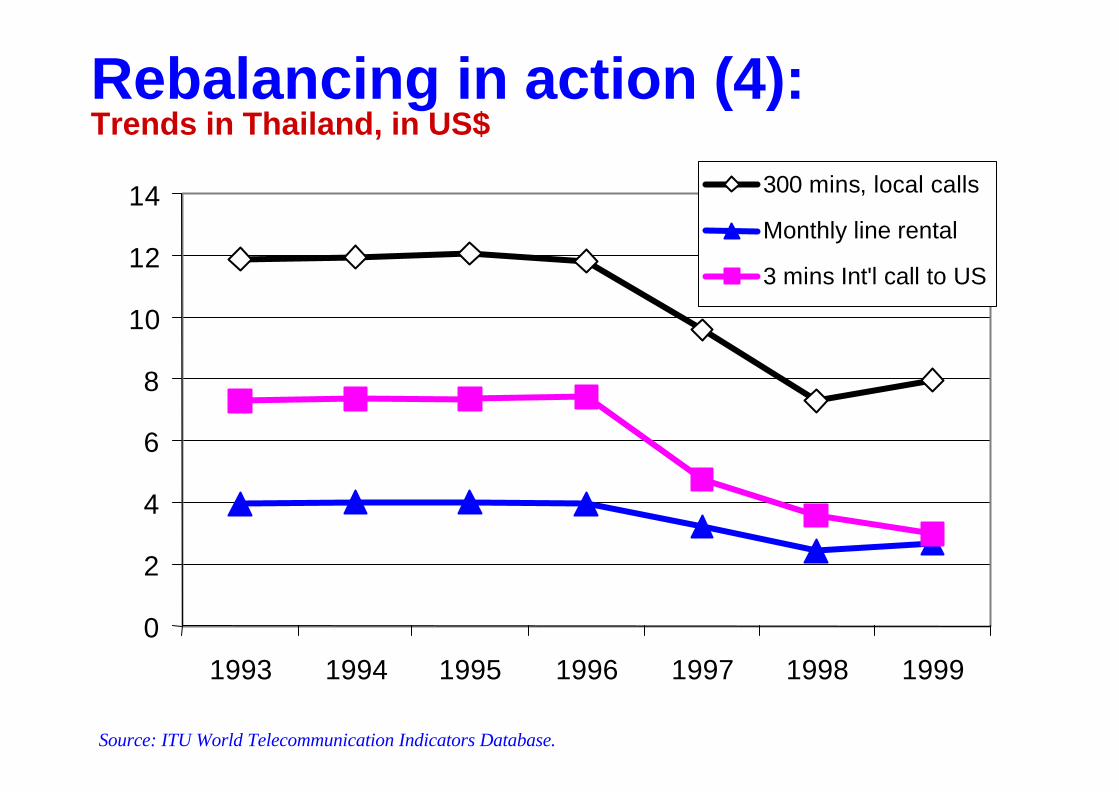

Rebalancing in action (4): Trends in Thailand, in US$

Source: ITU World Telecommunication Indicators Database.

0

2

4

6

8

10

12

14

1993 1994 1995 1996 1997 1998 1999

300 mins, local calls

Monthly line rental

3 mins Int'l call to US

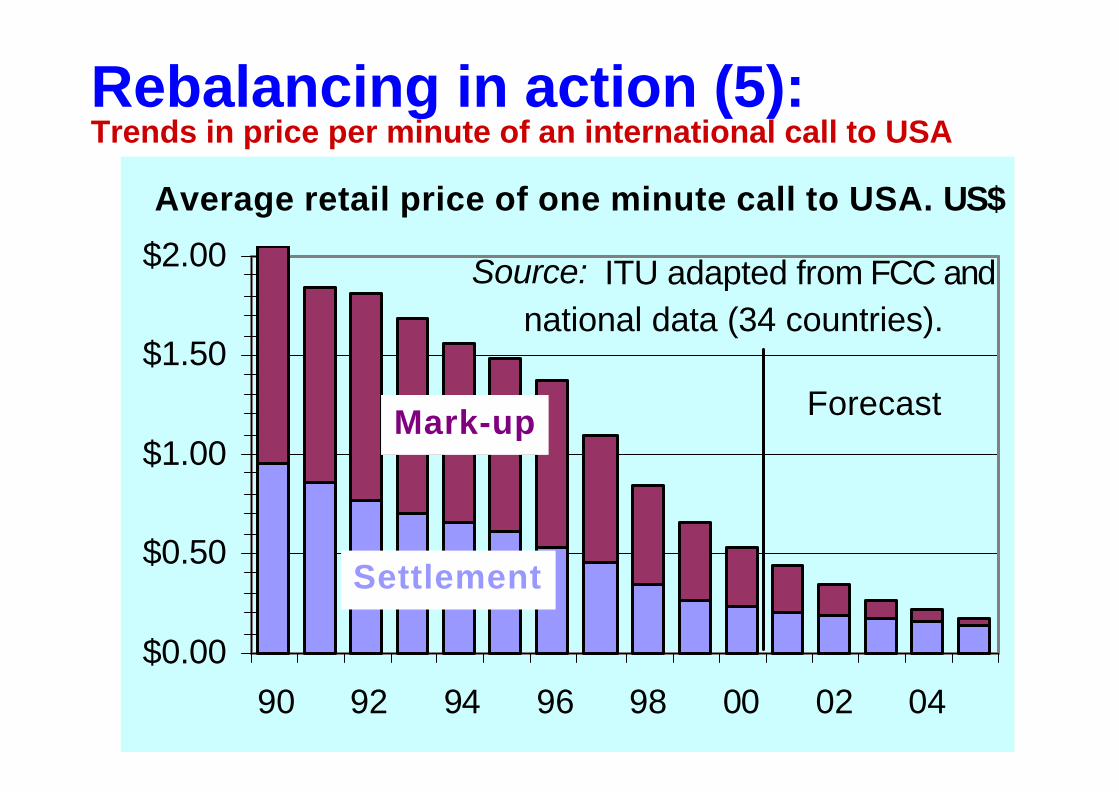

Rebalancing in action (5): Trends in price per minute of an international call to USA

$0.00

$0.50

$1.00

$1.50

$2.00

90 92 94 96 98 00 02 04

Average retail price of one minute call to USA. US$

Mark-up

Settlement

Source: ITU adapted from FCC and national data (34 countries).

Forecast

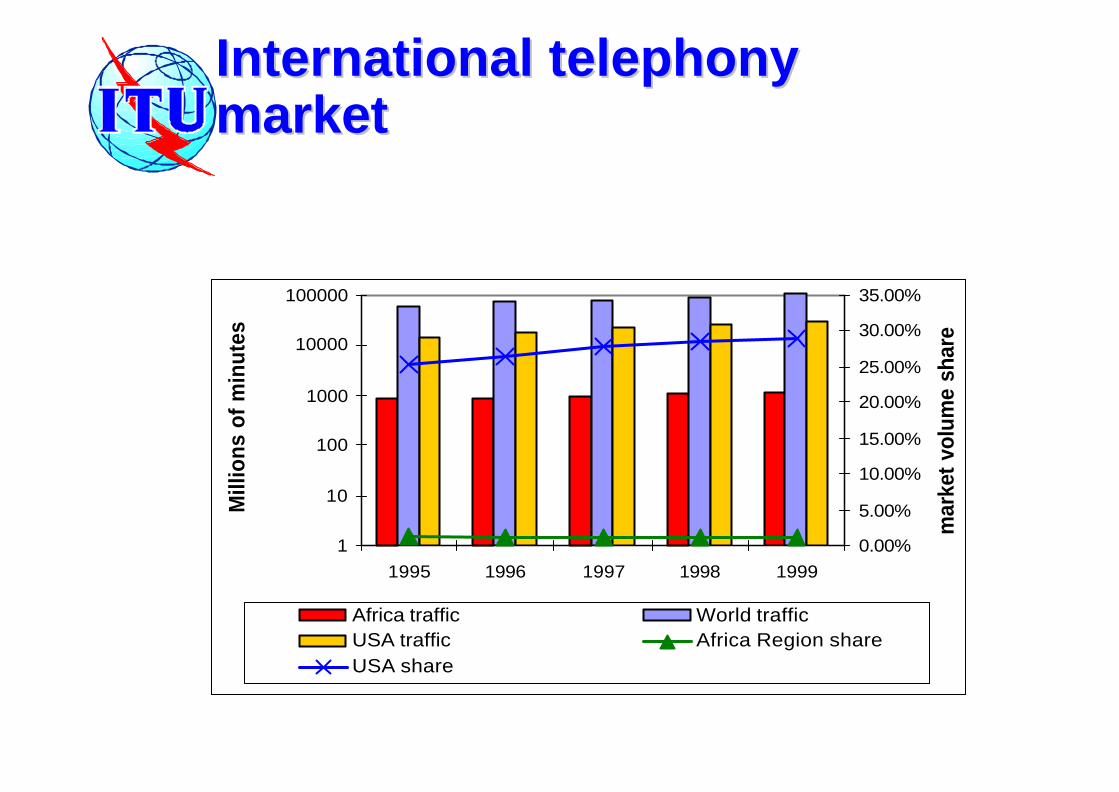

International International telephony telephony marketmarket

1

10

100

1000

10000

100000

1995 1996 1997 1998 1999

Mill

ions

of m

inut

es

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

mar

ket

volu

me

shar

e

Africa traffic World trafficUSA traffic Africa Region shareUSA share

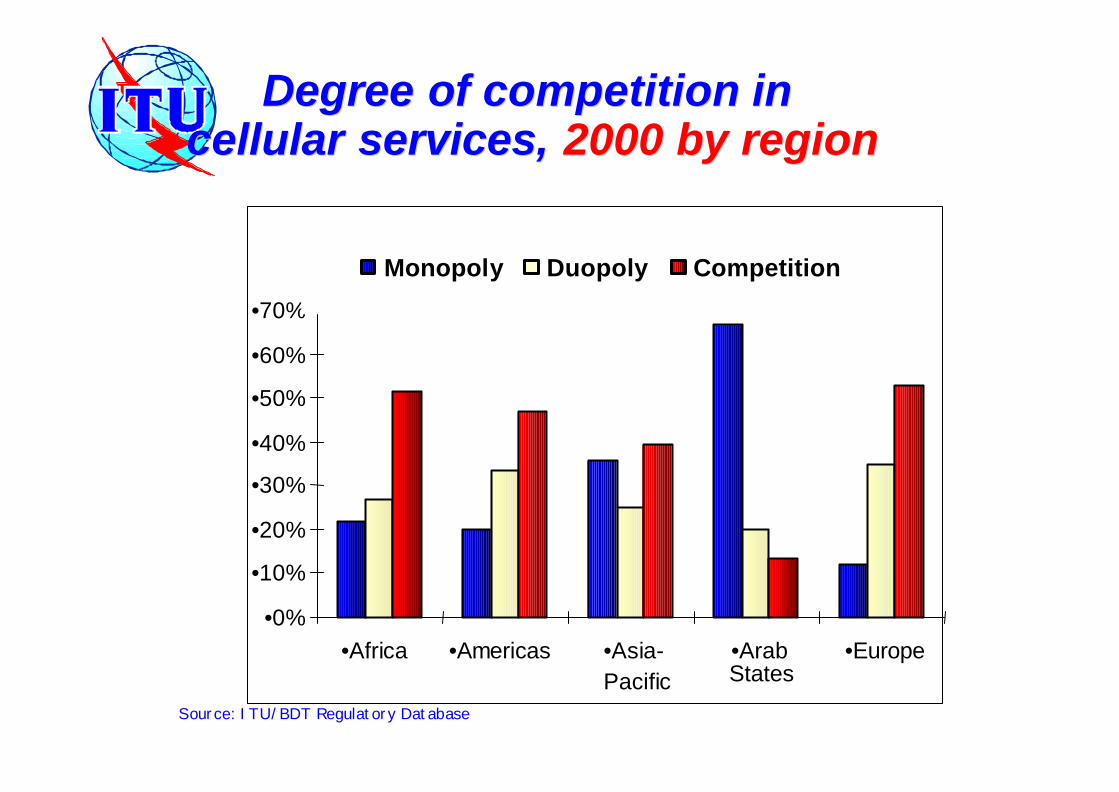

DegreeDegree of of competitioncompetition in in cellularcellular services,services, 20002000 by by regionregion

Source: ITU/BDT Regulatory Database

•0%

•10%

•20%

•30%

•40%

•50%

•60%

•70%

•Africa •Americas •Asia-Pacific

•ArabStates

•Europe

Monopoly Duopoly Competition

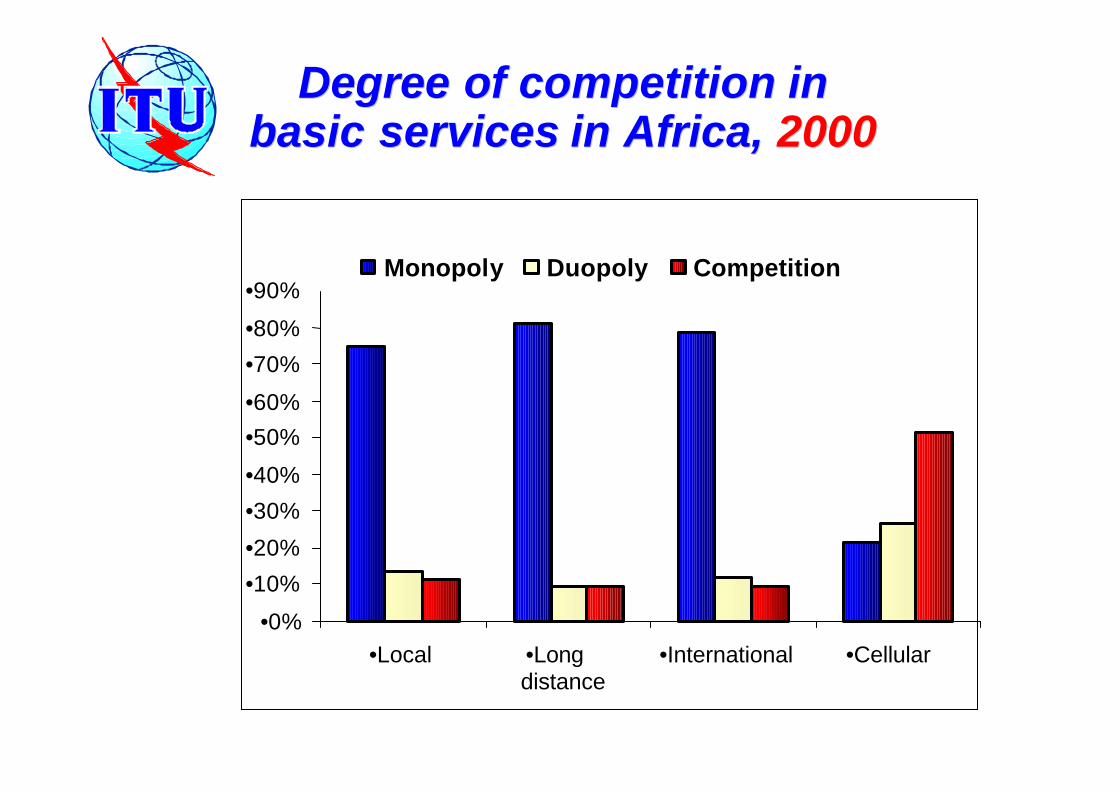

•0%

•10%

•20%

•30%

•40%

•50%

•60%

•70%

•80%

•90%

•Local •Longdistance

•International •Cellular

DegreeDegree of of competitioncompetition in in basic servicesbasic services in Africain Africa, , 20002000

Monopoly Duopoly Competition

Source: ITU/BDT Regulatory Database

Separate regulators in Separate regulators in the Worldthe World

•12•22

•30

•53

•84

•102

•1990 •1992 •1994 •1996 •1999 •2000

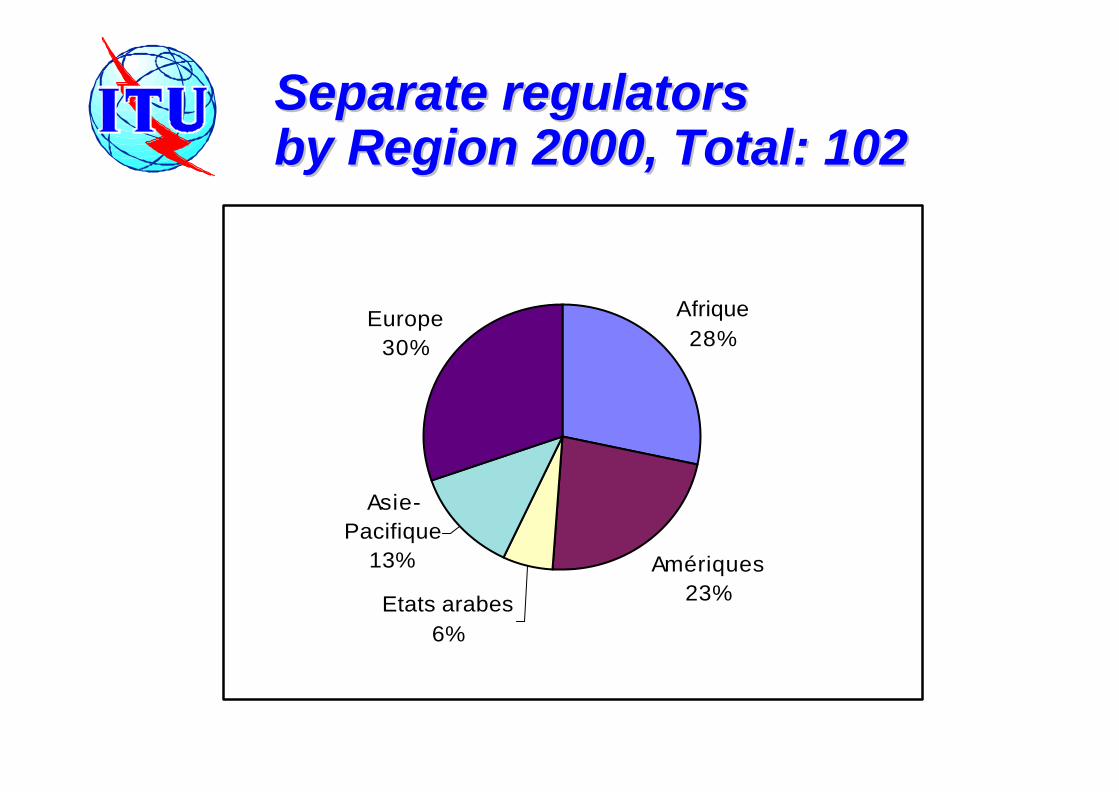

Separate regulators Separate regulators by Region 2000, Total: 102by Region 2000, Total: 102

Afrique28%

Amériques23%Etats arabes

6%

Asie-Pacifique

13%

Europe30%

Organismes séparés par région, 2000

Total: 102

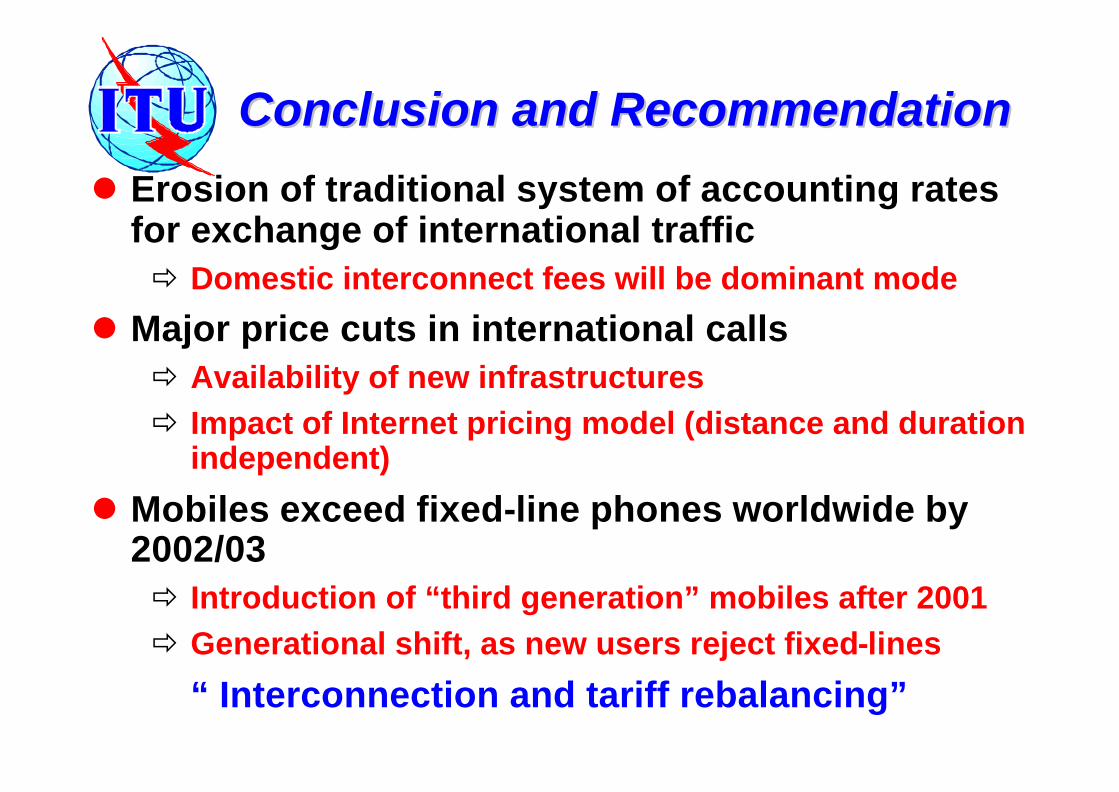

Conclusion and Recommendation Conclusion and Recommendation

l Erosion of traditional system of accounting rates for exchange of international trafficð Domestic interconnect fees will be dominant mode

l Major price cuts in international calls ð Availability of new infrastructuresð Impact of Internet pricing model (distance and duration

independent)

l Mobiles exceed fixed-line phones worldwide by 2002/03ð Introduction of “third generation” mobiles after 2001ð Generational shift, as new users reject fixed-lines

“ Interconnection and tariff rebalancing”