Global trends in low cost vehicles and implications for indonesia

24

Global Trends in Low Cost Vehicles and Implications for Indonesia Indonesia May 2010

-

Upload

frost-sullivan -

Category

Business

-

view

2.820 -

download

0

Transcript of Global trends in low cost vehicles and implications for indonesia

Global Trends in Low Cost Vehicles and Implications for Indonesia

IndonesiaMay 2010

2

Frost & Sullivan is a global Growth Consulting Company

The Growth Consulting Company

• Founded in 1961

• Over 1,700 Consultants / Analysts across 38 global

locations

• 10,000+ clients worldwide including emerging

companies, the global 1000, and the investment

community

• Offer the exclusive Growth System including:

Growth Partnership Services, Growth Consulting

and Growth Team Membership

• Developers of the Growth Excellence Matrix –

industry leading growth positioning tool for corporate

executives

• Developers of T.E.A.M. Methodology, proprietary

process to ensure that clients receive a 360o

perspective of technology, markets and growth

opportunities

3

Frost & Sullivan: The Global Growth Consulting Company

Growth Partnership Subscription

Growth Consulting

Best

Practices

Key Clients

Founded in 1961 in US, now operating in all continents

Over 10,000+ clients, 1,700 Consultants / Analysts across 35 global locations

Offer the exclusive Growth System including: Growth Partnership Services, Growth Consulting and Growth Team Membership

Developers of T.E.A.M. Methodology, proprietary process covering technology, economics, application and marketing behind Growth Opportunities

4

Frost & Sullivan’s Positioning & Thought Leadership

Frost & Sullivan

Automotive Domain knowledge

Research Capabilities

HighLow

Low

High

Consumer research

companies

Automotive data and

forecast providers

General Consulting

Companies

Coverage

Global

Local

Balance of domain

knowledge and research

capabilities across the

globe

Sought after by media across

the globe

5

Low Cost Cars : Top level strategic fact sheet

• Global suppliers are partnering increasingly with local regional suppliers for low-cost

competence and understanding of local market know-how

• In addition to local players, all key European, Japanese and American VMs are planning on

huge investments to make India as a low-cost car hub

0.00

1.25

2.50

3.75

5.00

Africa Asia Eastern

Europe

Middle

East

North

America

South

America

Western

Europe

2005 2013

Millio

n u

nit

s

Base Year is 2007. Source: Frost & Sullivan

Global Production of Low-cost cars – by Country, 2007

Regional Presence Global Presence

Lo

w-c

ost

tech

no

log

y e

xp

erti

se

Renault Group

Lo

wH

igh

Global Market Position of Low-cost cars VMs, 2007

Tata Motors

Maruti

Suzuki

Chery

BYD

Hyundai Group

Note: Arrows represent future direction of the VM’s business

Sourc

e:

Fro

st

& S

ulliv

an

Toyota Group

Volkswagen Group

General Motors

Ford

6

0

12,500

25,000

37,500

50,000

0 200 400 600

Passenger Cars (Per 1,000 people)

GD

P b

ase

d o

n P

PP

- P

er

ca

pit

a

Source: Key Development Data & Statistics, The World Bank World

Economic Outlook Database, October 2007

• Emerging economies have a very low

penetration of cars – India and China have

tremendous opportunities, with less than

10 people per 1,000 owing a car

• The Indian and Chinese automotive

industries have been growing at an above

average CAGR of more than 15% and 30%

respectively between 2004 and 2006

(growth of vehicle unit volumes)

• Many global vehicle manufacturers (VMs)

have planned capacity expansions in India

by 2010, while China has already witnessed

a huge surge in production capacity

United States

UK

Germany

Poland

Russia

Brazil

India

China

Opportunity for VMs

Price Range for Low-cost cars – by Country, 2007

BRIC, Eastern Europe and Asia will be the growth engines for automotive production in the next 10 years

Vehicle Purchasing Patterns in Developing countries

7

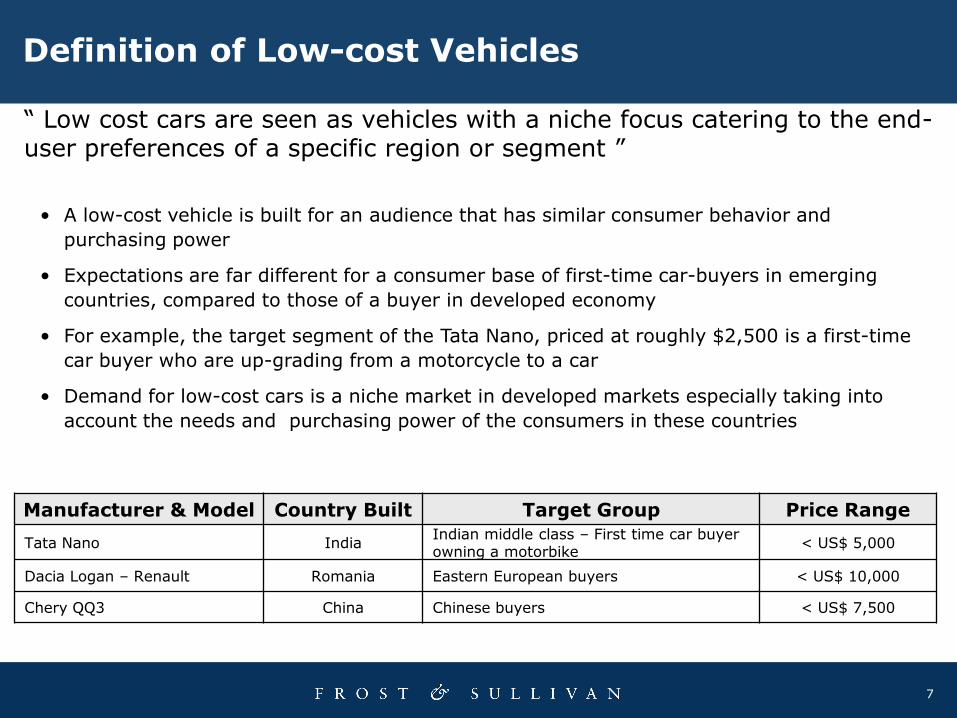

Definition of Low-cost Vehicles

“ Low cost cars are seen as vehicles with a niche focus catering to the end-user preferences of a specific region or segment ”

• A low-cost vehicle is built for an audience that has similar consumer behavior and

purchasing power

• Expectations are far different for a consumer base of first-time car-buyers in emerging

countries, compared to those of a buyer in developed economy

• For example, the target segment of the Tata Nano, priced at roughly $2,500 is a first-time

car buyer who are up-grading from a motorcycle to a car

• Demand for low-cost cars is a niche market in developed markets especially taking into

account the needs and purchasing power of the consumers in these countries

Manufacturer & Model Country Built Target Group Price Range

Tata Nano IndiaIndian middle class – First time car buyer owning a motorbike

< US$ 5,000

Dacia Logan – Renault Romania Eastern European buyers < US$ 10,000

Chery QQ3 China Chinese buyers < US$ 7,500

8

Definition of Low-cost Vehicles

The cost range of low-cost cars differs by geography

with higher costs in developed economies such as Japan, Europe and North

America

0

3000

6000

9000

12000

India China Eastern

Europe

Europe Japan North

America

Price Range for Low-cost cars – by Country, 2007

Note: Price ranges are indications based on existing /

future planned car models in respective regions

So

urc

e:

Fro

st

& S

ulliv

an

Tata Nano

Maruti 800

Chery QQ3

GM Spark

BYD F1

Dacia

Logan Kei

Daihatsu Sonica

Mitsubishi I

Suzuki Cervo

GM Spark

Dacia Logan

Hyundai Accent

Chevy Aveo

Kia Rio

Price Ceiling for Low-cost cars

9

Definition of Low-cost Vehicles

€ 0

€ 2,500

€ 5,000

€ 7,500

€ 10,000

INDIA CHINAEASTERNEUROPE

JAPAN

Maruti 800

Hyundai Santro

Tata Indica

Maruti AltoChery QQ3

GM Spark

Xiali Wei Zhi

Fiat Panda **

Renault Clio #

Dacia Logan *

Suzuki Wagon R

LOW-COST CARS

Source: Frost & Sullivan

Reta

il P

ric

e o

f V

eh

icle

Mod

els

Note: Bubble Size represents the production volumes of the vehicle models in 2007.$ - For Future vehicles, bubble size does not represent production volumes

* - Does not include Iran

** - Price in Poland

# - Price in Slovenia (Although a basic Clio is priced relatively less in Slovenia, <10,000 cars are sold in

Slovenia and most of the volumes are exported to Western Europe, where it is much more expensive)

Price positioning of vehicle models and their production estimates – by Country, 2007

FUTURE VEHICLES$

Tata Nano

Hyundai LCC

VW Low-cost car

ToyotaLow-cost car

BYD F1

Price Ceiling for Low-cost cars

10

Drivers and Restraints for Low cost carsM

ark

et

Dri

ve

rsM

ark

et

Re

str

ain

ts

New vehicle segment constituting first-

time car buyers and people switching

from two-wheelers to cars

Increasing purchasing power of

a growing middle class in emerging

markets –increasing demand for affordable cars

Government policy encouraging small-displacement and low-emission cars

Low-margins and fear of bleak chances for profitability

So

urc

e:

Fro

st

& S

ulliv

an

Increase in vehicle costs due to

legislations on safety and

emission standards

Limited public transportation infrastructure

and a demand for affordable

transportation

Increasing interest of global

automakers to tap the low-cost car segment and

create new products

Brand image erosion

Competition from used-car market

Lack of infrastructure to support growing

vehicle population

11

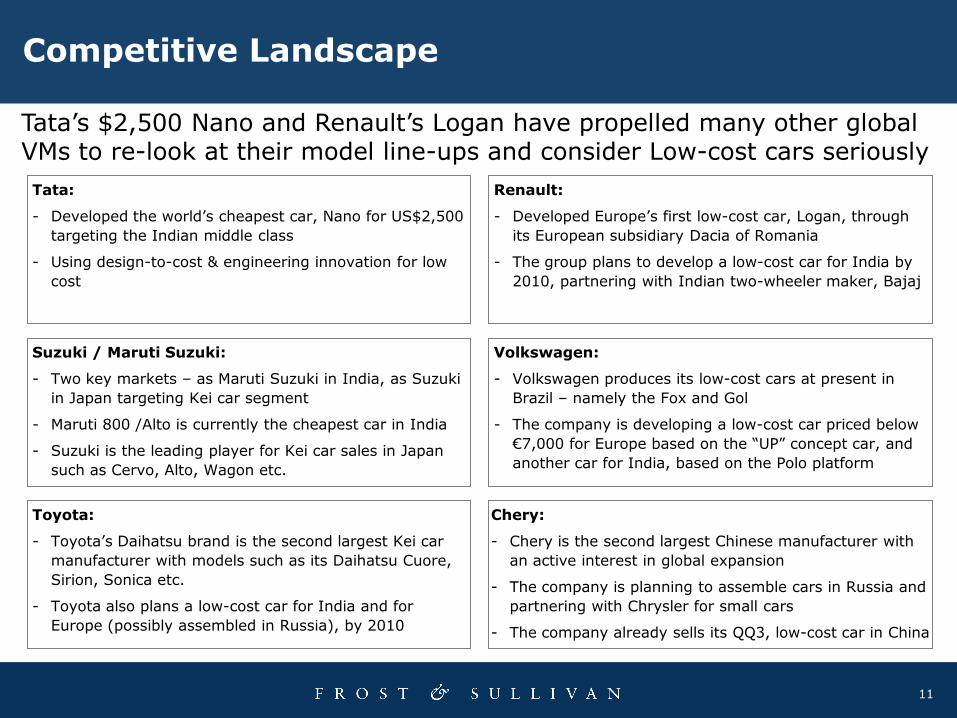

Competitive Landscape

Tata’s $2,500 Nano and Renault’s Logan have propelled many other global VMs to re-look at their model line-ups and consider Low-cost cars seriously

Tata:

- Developed the world’s cheapest car, Nano for US$2,500

targeting the Indian middle class

- Using design-to-cost & engineering innovation for low

cost

Renault:

- Developed Europe’s first low-cost car, Logan, through

its European subsidiary Dacia of Romania

- The group plans to develop a low-cost car for India by

2010, partnering with Indian two-wheeler maker, Bajaj

Suzuki / Maruti Suzuki:

- Two key markets – as Maruti Suzuki in India, as Suzuki

in Japan targeting Kei car segment

- Maruti 800 /Alto is currently the cheapest car in India

- Suzuki is the leading player for Kei car sales in Japan

such as Cervo, Alto, Wagon etc.

Volkswagen:

- Volkswagen produces its low-cost cars at present in

Brazil – namely the Fox and Gol

- The company is developing a low-cost car priced below

€7,000 for Europe based on the “UP” concept car, and

another car for India, based on the Polo platform

Chery:

- Chery is the second largest Chinese manufacturer with

an active interest in global expansion

- The company is planning to assemble cars in Russia and

partnering with Chrysler for small cars

- The company already sells its QQ3, low-cost car in China

Toyota:

- Toyota’s Daihatsu brand is the second largest Kei car

manufacturer with models such as its Daihatsu Cuore,

Sirion, Sonica etc.

- Toyota also plans a low-cost car for India and for

Europe (possibly assembled in Russia), by 2010

12

Competitive Landscape

Hyundai:

- Hyundai manufactures a few models such as the Atos

and Picanto which are low-cost in South Korea

- The company is also evaluating to produce a model

priced at $3,500 in India, to compete against other

models such as Tata Nano and Renault – Bajaj’s car

Fiat Auto:

- Fiat has produced some global car models, especially its

successful Palio and Uno global platforms

- The company has plans to develop a US$ 7,000 car to

be built in South America

- Fiat also has plans to build a LCC for Europe through its

partnership with its Turkish partner Tofas

Other Car Makers:

- Geely offers its CK1 sedan starting at a price of €4,000

- BYD is expected to replace its existing low-cost car,

Flyer with the F1 in mid-2008 priced at around €3,500

- Ford is investing 500 million in its plant in Chennai,

India for a small car plant with capacity of 150,000

13

Suzuki Group,

13.7%

Others, 33.3%

Hyundai Group,

10.4%

Indian

Manufacturers,

17.1%

Chinese

Manufacturers,

8.7%

Renault-Nissan

Group, 16.9%

Estimated Market Share of Low-cost car Manufacturers, 2013

Units: 560,155

Key VMs: Chery, BYD, Changan, Hafei

Regions: Eastern Europe/Russia, China

Units: 664,454

Key VMs: Kia, Hyundai

Regions: India, South Korea

Units: 878,474

Key VMs: Maruti, Suzuki

Regions: India, Japan (Suzuki-Kei cars)

Units: 1,082,795

Key VMs: Renault, Dacia & Nissan

Regions: Eastern EU / Russia, Japan (Nissan-Kei), South America, S. Africa

Units: 2,135,731

Key VMs: GM, VW, Toyota, Fiat and Honda (Kei cars)

Regions: Across all geographies

Units: 1,094,499

Key VMs: TATA, Bajaj + Renault

Regions: India, South Africa

Tata, Renault and Suzuki are expected to account for about 50% of the global Low-cost car production by 2013

Competitive Landscape

14

Global Vehicle Production Forecasts and Trends for Low-cost Vehicles

Low

Medium

High

Low-cost car

Production

India, China, Thailand, Romania, Turkey to emerge as key low-cost production hubs in the future

Asia

2007: 2.14 million

2013: 4.41 million

CAGR: 12.9%

South America

2007: 0.34 million

2013: 0.65 million

CAGR: 11.2%

Eastern EU & Russia

2007: 0.26 million

2013: 0.96 million

CAGR: 24.6%

Africa

2007: 0.01 million

2013: 0.14 million

CAGR: 57.7%

• Tata Motors

• Renault + Bajaj

• Maruti Suzuki

• Hyundai

• Chery

• GM – WULING

• Chang’an

• Geely

• BYD

• Tianjin-FAW

• Renault – Dacia

Middle East

2007: 0.12 million

2013: 0.26 million

CAGR: 13.1%

15

0.0

1.0

2.0

3.0

4.0

5.0

Africa Asia Eastern

Europe

Middle East North

America

South

America

Western

Europe

Units

Global Vehicle Production Forecasts and Trends for Low-cost Vehicles

2007 2013

Unit Shipments in 2013

2.9 million

6.4 million

CAGR : 14.4%

Global Production of Low-cost cars – by Country, 2007 – 2013

Millio

n u

nit

s

Note: Base Year is 2007. CAGR calculated only for the forecast period between 2007 and 2013

More than 4.4 million vehicles to be produced in Asia by 2013 – India to emerge as the low-cost car production hub

0.14 m

4.41 m

0.96 m

0.26 m

0.65 m

16

Indonesia is the most populous country in ASEAN

Historic Trend 2004 2007 2010

(F)

Population (million) 217.5 228.1 235.8

Real GDP Growth (%) 5.1 6.3 6.0

GDP (USD Billion) 257.3 428.8 587.8

GDP Per capita (USD) 1,187 1,880 2,493

Exchange rate (v/s USD) 8,937 9,393 9,830

• Capital : Jakarta

• Languages: Bahasa Indonesia, English, Dutch and local dialects

• Ethnicity: Javanese 45%, Sundanese 14%, Madurese 7.5%, coastal

Malays 7.5%, other 26%

• Population: 228.1 Million. Sumatra 17.9%, Java 39.4%, Sulawesi

7.2%, Kalimantan 33.6%, Sunda Islands 1.1%, Maluku Islands 0.8%

• Indonesia is the largest, most populous and

fastest growing economy in the region

• It is one of the largest exporter of natural gas,

manufacturing contributes to about 45% of

GDP

• Under current regime Indonesia has made

progress in attracting investments but

infrastructure bottlenecks still remain key

problems

17

Brunei

Singapore

Malayasia

Thailand

Indonesia

Philippines

0

50

100

150

200

250

300

350

400

Malaysia is in growth zone and Thailand, Indonesia and Philippines are in rapid growth zone

$50,000$10,000$7,000$3,000

C4 C

3

C

2C

1

Position of ASEAN Countries on Growth Curve

Cluster 1 : nearing

stagnation

Brunei, Singapore

Cluster 2 :Steady

growth

Malaysia

Cluster 3 :High Growth

Thailand

Indonesia

Philippines

Cluster 4 : Markets of

tomorrow

Vietnam

Laos, Cambodia

Mynmar

Rapid Growth

Growth

18

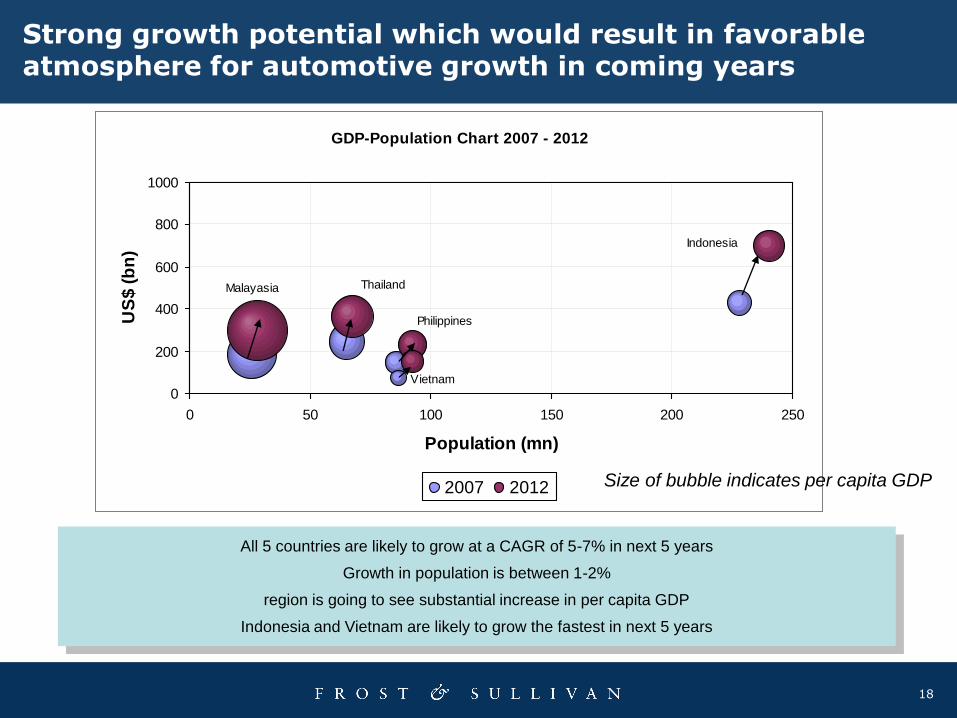

GDP-Population Chart 2007 - 2012

Vietnam

Thailand

Philippines

Malayasia

Indonesia

0

200

400

600

800

1000

0 50 100 150 200 250

Population (mn)

US

$ (

bn

)

2007 2012

Strong growth potential which would result in favorable atmosphere for automotive growth in coming years

All 5 countries are likely to grow at a CAGR of 5-7% in next 5 years

Growth in population is between 1-2%

region is going to see substantial increase in per capita GDP

Indonesia and Vietnam are likely to grow the fastest in next 5 years

Size of bubble indicates per capita GDP

19

Significant young population and large number of middle income households

Source: Asian Development Bank (ADB)

• Significant young population

• Average 5 members per family

• About 45% falls under the age bracket of

first time car buyers (20 to 39)

• Income skewed towards extremely lower

end leaving very small number of buyers

out of the whole population

Indonesia Population by age group

69.3

57.2

45.1

28.7

17.1

10.5

0

20

40

60

80

0 - 19 20 - 29 30 - 39 40 - 49 50 - 59 60 +

Millio

ns

30.3%

25%

19.7%

12.5%

7.4%4.6%74%

Annual HH income Indonesia

0%

3%

8%

12%

29%

19%

27%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

> Rp27mRp21m-27mRp15m-21mRp9.6m-15mRp7.2m-9.6mRp4.8m-Rp7.2m<Rp4.8m

Vehicle Parc & Density 2004 2007 2010

Car Parc (‘000) 1,005 1,169 1,442

Car Density (‘000) 4.6 5.2 6.2

LCV (incl MUV) 4,737 5,766 6,992

LCV Density 21.4 25.27 29.65

Two wheeler parc (‘000) 28,400 42,247 50,700

Two wheeler density (‘000) 133 185 215

20

High fuel prices resulted in increase in Transportation expense

• Continuous fuel price increase has taken

a toll on transportation expenses

• Transportation is the only major expense

head that has increased in top 5 expense

heads

• Diesel prices are growing faster than

Petrol prices and catching up with Petrol

Fuel Price Movement

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

2000 2002 2004 2006 2007

US

$ c

en

ts /

lit

Diesel

Petrol

38%

21%

21

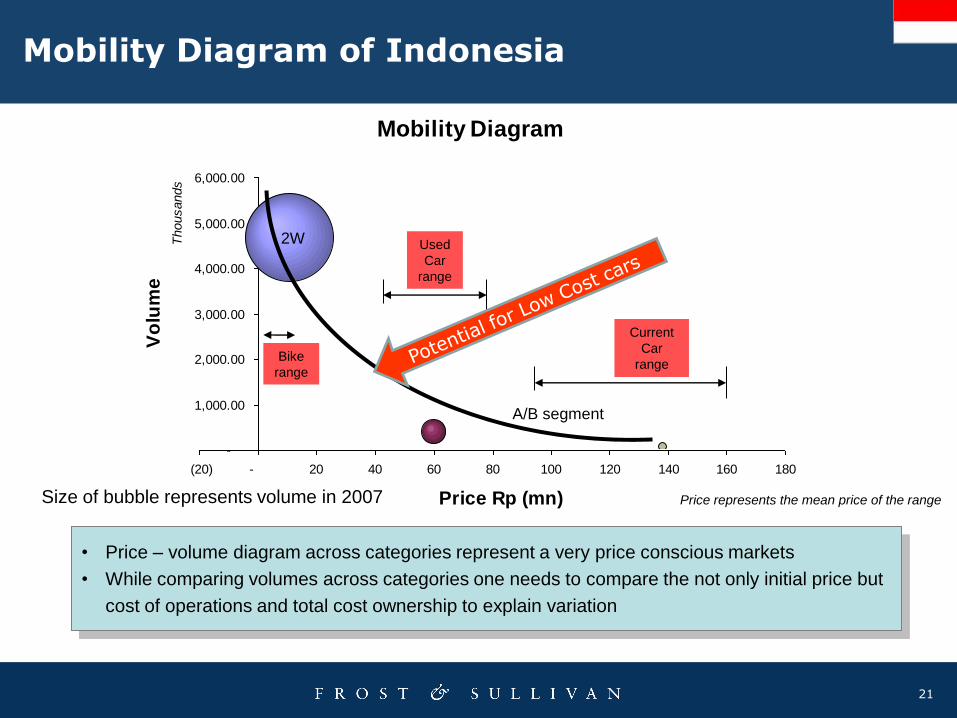

Mobility Diagram

-

1,000.00

2,000.00

3,000.00

4,000.00

5,000.00

6,000.00

(20) - 20 40 60 80 100 120 140 160 180

Thousands

Price Rp (mn)

Vo

lum

e

Mobility Diagram of Indonesia

Bike

range

Used

Car

range

Current

Car

range

Size of bubble represents volume in 2007

• Price – volume diagram across categories represent a very price conscious markets

• While comparing volumes across categories one needs to compare the not only initial price but

cost of operations and total cost ownership to explain variation

A/B segment

Price represents the mean price of the range

2W

22

• Low cost cars sold in developed economies

need to conform to a higher standard of

safety, emission and advanced technology

required in these markets

• Value-for money is the success factor rather

than price in these markets

Industry Challenges for Low cost cars

• Eg., Chinese manufacturer, ChangAn

estimates its profit margin at less than 5

per cent for a single car due to increasing

production costs and price competition

Cannibalization

Brand image

erosion – low-cost

image

Price competition

– Reduced profit

per car sold

• Sales cannibalization is especially a problem for Indian

and Chinese VMs who already sell low-cost cars at present

• For example, sales of the Maruti 800 was severely hit

when Maruti Suzuki launched its Alto model in India

Challenges for

Low-cost cars

• Consumers sometimes consider low-cost cars as a product

with low price, low technology and low safety quotient

• For example, consumers attribute some low-cost Chinese

brands to low safety and emission standards

Providing low-cost

products with

acceptable quality

and performance

• Low margins is definitely the norm

with Low-cost cars and chances of

profitability would depend solely on

the sales volumes generated

• Suppliers and OEMs need to generate

innovative design concepts to reduce

system costs without loss of quality

and offering the same functionality

Keeping prices low in

developed markets in

spite of offering

advanced features

23

Key Conclusions

Low Cost car is one of the key segments in emerging markets

Growing income, government support and OEM focus are the key drivers

Indonesia is one of the key growth drivers for the region

Considering the macro-economic parameters, Indonesia is on a threshold of rapid growth in cars in next few years

Economic, sociological indicators suggest that low cost cars can succeed Indonesia

Indonesian automotive industry need to come together to determine what type of car would be ideally suited for Indonesia

24

Dewi NurainiCorporate Communications

Indonesia

Phone : (021) 571.0838 / 571.3246

Email : [email protected]

For Additional Information

www.frost.com