Global trade governance & 21 century trade

23

Global trade governance & 21 st century trade Richard Baldwin Graduate Institute, Geneva & University of Oxford

Transcript of Global trade governance & 21 century trade

Global trade governance & 21st century trade

Richard Baldwin Graduate Institute, Geneva &

University of Oxford

Misthinking globalisation • Conventional: Globalisation = Autarky to free

trade, slowly. • But pervasive sense that today’s globalisation

is different …

1870 – 1980: Globalisation is all about trade costs

1870 1880 1890 1900 1910 1920 1930 1940 1950 1960 1970 1980

16

1.1 10

12

14

1.2 1.3 1.4 1.5 1.6 1.7 1.8 1.9

1912

1870-1914: Falling trade costs dominant

1914- 1940: Rising tariffs dominant

1950

1980

1950-1980: Falling tariffs & transport costs dominant

Source: Gravity model based estimates of trade costs (Jacks, Meissner, Novy 2011).

Estimates trade costs (global average)

1870 1880 1890 1900 1910 1920 1930 1940 1950 1960 1970 1980

16

1.1 10

12

14

1.2 1.3 1.4 1.5 1.6 1.7 1.8 1.9

1912

1950

1980

World trade flows (in logs)

Classical trade theory developed

Neoclassical trade theory developed

Add trade flows Globalisation = lower trade costs & more trade in goods

Big picture impact, 1870-1980s • G7’s share of world exports & income

Globalisation = G7’s trade & income share rises

New RTAsNew WTO members

GATT Rounds

World average tariff (right scale)

0%

2%

4%

6%

8%

10%

12%

14%

16%

0

5

10

15

20

25

30

35

40

45

50

1947

1952

1957

1962

1967

1972

1977

1982

1987

1992

1997

2002

2007

GATT does a great job Globalisation = • Tariff cutting by reciprocal negotiation. • Rich nations cut tariffs; developing nations

don’t. • GATT attracts new members.

Something changed: Trade costs fell little; trade kept growing

• ‘Distance puzzle’! • Hummel cannot find the drop in transport costs!

1912

1950

19741980

10

12

14

16

1.1

1.2

1.3

1.4

1.5

1.6

1.7

1.8

1.918

70

1880

1890

1900

1910

1920

1930

1940

1950

1960

1970

1980

1990

2000

Something changed: G7 world shares drop

• “Emerging economies”! • “East Asian miracle”!

1991, 52%

20%

30%

40%

50%

60%19

4819

5319

5819

6319

6819

7319

7819

8319

8819

9319

9820

0320

08Source: WTO database

G7 world export share

1950, 55%

1988, 67%

45%

50%

55%

60%

65%

70%

1948 1958 1968 1978 1988 1998 2008Source: World Databank from 1960; Maddison pre-1960

G7 world GDP share

Something changed: Nature of North-South trade changes

1990

1986

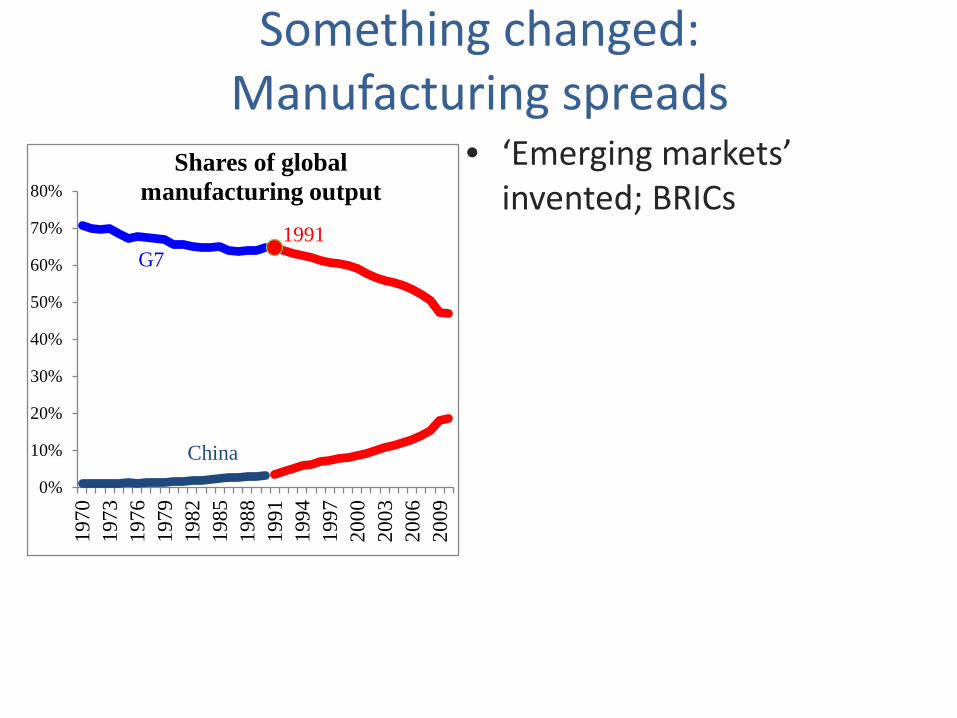

Something changed: Manufacturing spreads

• ‘Emerging markets’ invented; BRICs

1991G7

China0%

10%

20%

30%

40%

50%

60%

70%

80%

1970

1973

1976

1979

1982

1985

1988

1991

1994

1997

2000

2003

2006

2009

Shares of global manufacturing output

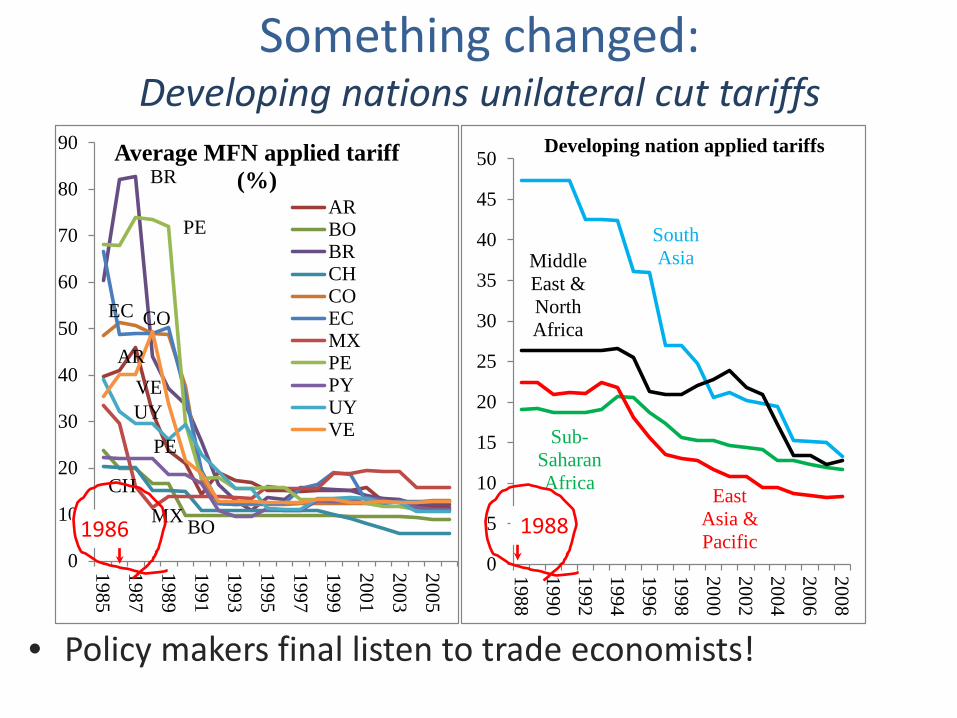

Something changed: Developing nations unilateral cut tariffs

• Policy makers final listen to trade economists!

AR

BO

BR

CH

COEC

MX

PE

PE

UYVE

0

10

20

30

40

50

60

70

80

90

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

Average MFN applied tariff (%)

ARBOBRCHCOECMXPEPYUYVE

South Asia

Sub-Saharan Africa

Middle East & North Africa

East Asia & Pacific

0

5

10

15

20

25

30

35

40

45

50

19881990199219941996199820002002200420062008

Developing nation applied tariffs

1986 1988

Something changed: FDI and BITs boom

• FDI popularity booms with developing nations! • They agree concessions to attract FDI (BITs)!

New BITs signed

Cumulative BITs

FDI ($ billion)

-

500

1,000

1,500

2,000

2,500

-

50

100

150

200

25019

5919

6119

6319

6519

6719

6919

7119

7319

7519

7719

7919

8119

8319

8519

8719

8919

9119

9319

9519

9719

9920

0120

0320

0520

07

Something changed: RTAs ‘deep’ provisions

• RTAs include beyond WTO provisions: – Competition policy, IPR, investment, capital movements, etc.

0

5

10

15

20

25

30

35

40

4519

58

1963

1968

1973

1978

1983

1988

1993

1998

2003

2008

Deep RTA provisions

Globalisation as 2 unbundlings • 1st unbundling = traditional view • 2nd unbundling = ’21st century globalisation’

14

Global dispersion of production, but local clustering into factories: due to Coordination costs not trade costs

1st unbundling

Bay B Bay A

Bay C

Steam revolution

Relaxing the coordination constraint

• ICT revolution seems to start between 1985 & 1995.

1995

Phones

1995

Internet Users

1985

Internet Hosts (right

scale, in logs)

-

5

10

15

20

25

-

1

2

3

4

5

6

1975

1980

1985

1990

1995

2000

2005

2010

billions

Source: WDI for phone and internet users; www.isc.org for internet hosts

Bay B

Bay A

Bay C

ICT revolution

Dispersion of production stages, but regional clustering (‘factory Asia’, ‘factory EU’, etc.)

2nd unbundling

Bay B Bay A

Bay C

Global dispersion of production, but local clustering into factories: Coordination costs not trade costs

1st unbundling

Bay B Bay A

Bay C

Steam revolution

#1. International commerce transformed

Bay B

Bay A

Bay C

Bay B

Bay A

Bay C

Bay B

Bay A

Bay C

1) Two-way flows of goods, ideas, technology, capital, and technicians.

2) Investment and application of technical, managerial and market know-how abroad.

Connecting factory & doing business abroad: The “trade-investment-services nexus”

#2. New governance demands

19

Bay B

1) Necessary trade & service links Connecting factories - Trade policy barriers; - Transportation services; - Business mobility; - Communication services.

2) Necessary “Behind the border barriers” (BBB) reform Doing business abroad - International investment; - Application of home’s technology abroad; - Local availability of business services.

#3. Different political economy • 1st unbundling political economy logic =

exchange of market access. • 2nd unbundling political economy logic =

Northern factories for Southern reform. – Supply chains mostly regional, so deeper

integration mostly regional. • No factories on offer in Geneva

Implications: Trade governance • ‘Fact’ 1: Doha won’t finish this decade. • Fact 2: Demand & supply for deeper discipline

is huge. – Being filled outside the WTO.

• Implication: The WTO will not be involved in setting these ‘21st century trade’ rules.

• Plurilaterals: Services? Investment? • Mega-regionals:

– TPP may fail, but if not will be the template.

21

WTO scenarios • HOT: WTO concludes DDA & turns to TPP-like

discipline after 2020. – WTO centrality restored as rule keeper & judge.

• WARM: WTO continues central to 20th century disciplines, but irrelevant to 21st century disciplines. – “Marrakesh pillar” in multi-pillar global governance.

• COLD: WTO fails to update 20th century rules; fails to multilateralise 21st century rules & bicycle falls over. – Great Powers global trade governance: TPP,

TransAtlantic Partnership? China bloc? 22

CGE call to arms • 21st trade opens up the production function. • GTAP has decades experience in this. • There is not good, real data. • Door open to lots of empirical studies on

simulated data. – Political economy of unilateral tariff liberalisation; – Moving up the value chain; – Smile curve; – Mapping the world’s supply chain trade. – Modelling deeper RTAs without trade diversion.