Global Medium and Heavy Duty Truck Transmission Study

21

Executive Analysis of the Global Medium and Heavy Duty Truck Transmissions Market By 2025, 44% of New Trucks Globally to Feature AMT or AT NF9E-18 January 2016 BRIEF SUMMARY

-

Upload

silpa-paul -

Category

Automotive

-

view

1.215 -

download

0

Transcript of Global Medium and Heavy Duty Truck Transmission Study

Executive Analysis of the Global Medium and Heavy

Duty Truck Transmissions Market By 2025, 44% of New Trucks Globally to Feature AMT or AT

NF9E-18

January 2016

BRIEF SUMMARY

2 NF9E-18

Contents

Section Slide Number

Executive Summary 3

Research Scope, Objectives, Methodology, and Background 9

Definitions and Segmentation 16

Mega Trends and Industry Convergence Implications 20

Major Trends Influencing Conventional Truck Transmission Technologies 22

Advanced Transmission Technologies 30

Global Commercial Trucks Overview 36

Drivers and Restraints 42

Supplier Profiles 53

Regional Transmissions Market Outlook 58

Conclusions & Future Outlook 65

Appendix 70

Return to contents

3 NF9E-18

Executive Summary

4 NF9E-18

Executive Summary—Key Findings

MD-HD Truck Transmissions Market: Key Findings, Global, 2015–2025

Key: TRIAD—The European Union, North America, and Japan; OEM—Original Equipment Manufacturer;

GVWR—Gross Vehicle Weight Rating Source: Frost & Sullivan

With 32.5% share of the total 4.2 million annual Medium Duty (MD)-Heavy Duty (HD) truck market by 2025,

AMTs are expected to experience the highest rate of adoption in the next decade at a CAGR of 12.5% from

2015–2025. ATs are also expected to increase their share from 8.5% in 2015 to 11.5% in 2025. TRIAD markets

are most favorable for ECT adoption.

2

1

Electronically Controlled Transmissions (ECTs)—Automated Manual Transmissions (AMTs) and Automatic

Transmissions (ATs)—presently have an incremental cost of $600–$10,000 and offer -5% to 10% fuel savings,

depending on truck GVWR and duty cycle, over baseline manual transmissions. The typically high incremental

cost versus fuel savings is the primary factor presently inhibiting mass adoption of ECTs.

Downspeeding, leading to engine downsizing, coupled with increasing vertical integration of transmissions in

North America (NA), Europe, and Asia is catalyzing the adoption of ECTs. ECTs are favored by truck OEMs to

meet the higher torque requirements placed by powertrain downspeeding. European truck manufacturers

already offer AMTs as standard fitment in MD-HD trucks. This technology has a share of 55.4% in the EU

market in 2015.

3

Fuel economy benefits of ECTs in higher GVWR vehicles (more than 16 tons) are yet to be conclusively

proven. Therefore, this segment is still dominated by conventional Manual Transmissions (MTs), with skilled

drivers, across regions. MTs account for 81.4% the global HD truck segment in 2015. However, the share of

MTs is forecasted to decline steadily during the forecast period to 65.5% by 2025.

4

Better fuel economy of ECTs, narrowing price difference with MTs (due to improving economies of scale),

exacerbating skilled driver shortage, and increasing level of automated driving across developed economies on

both sides of the Atlantic are expediting the adoption of ECTs. 5

5 NF9E-18

71.2%

25.6%

3.2% 64.0%

31.2%

4.7%

62.9%

28.8%

8.3% 19.7%

65.9% 14.4%

27.1% 29.4%

43.5%

China India

South America

Russia Europe

North America

Next 11+ RoW

~156,000

69.1% 26.9%

4.0%

~1.0 Million

55.1%

37.2%

7.7%

~254,000

Size and values of pie charts denote truck transmission market size in terms of unit shipment.

~618,000

~1.2 Million ~509,000

~404,000

MT AMT AT

MD-HD Truck Transmissions Market: Unit Shipment Forecast for Top Regions, Global, 2025

(2.7%)

3.9%

2.9%

MT

AMT

AT(4.7%)

4.1%

14.7%

MT

AMT

AT

5.9%

17.2%

25.7%

MT

AMT

AT

4.2%

38.3%

---

MT

AMT

AT

(0.5%)

23.7%

22.2%

MT

AMT

AT

2.7%

8.3%

13.7%

MT

AMT

AT3.9%

32.7%

---

MT

AMT

AT

C

A

G

R

C

A

G

R

C

A

G

R

C

A

G

R

C

A

G

R

C

A

G

R

C

A

G

R

CAGR calculated for 2015–2025.

Executive Summary—Global MD-HD Truck Transmission Forecast 2025 ECTs are expected to experience strong adoption by 2025 with AMTs and ATs growing at a CAGR of 12.5%

and 7.7%, respectively, from 2015.

Note: All figures are rounded. The base year is 2015. Source: Frost & Sullivan

6 NF9E-18

MD-HD Truck Transmissions Market: Technology Roadmap, Global, 1950–2025

Dog Clutch and Synchronized

Manual

AT

Electronically Controlled

Transmissions

AMT

AT

DCT

IVT

CVP

Skilled Driver Shortage:

As truck drivers from the ―baby-

boomer‖ generation retire to be

replaced by ―millennials‖, training and

retention costs are escalating

because these young drivers lack

basic familiarity with manuals,

especially in NA, where passenger

cars are largely AT driven.

As ECTs are easier to operate, fleet

owners believe they will help with

hiring and retention.

1950–1980 1980–2010 2010–2025

Fleet Operation Cost:

Fuel costs can account for 50%–65% of a

fleet’s operating costs, making it the highest

cost component for fleets. Studies show that

adoption of AMTs and ATs can improve truck

fuel efficiency in varying degrees depending

on truck operating duty cycle. AMTs are

especially beneficial in drive cycles with high

idling time in comparison to MTs and

conventional ATs.

Use of ECTs also reduces the variability in fuel

economy—the variance between the best and

worst fuel economy among trucks in a fleet.

Emission Regulations:

US EPA Phase 2 GHG regulations

demand a 40%–50% fuel economy over

existing models. The European Union

(EU) and China are also looking to apply

stringent diesel emission norms, as

diesel emissions are increasingly being

viewed as carcinogenic.

Tightening diesel powertrain emission

norms are forcing truck manufacturers to

adopt new technologies such as ECTs.

Key: DCT—Dual Clutch Transmissions, IVT—Infinitely Variable Transmission, CVP—Continuously

Variable Planetary, US EPA—US Environmental Protection Agency, GHG—Green House Gas.

Key Technology Adoption Influencers

Executive Summary—Transmissions Technology Evolution Skilled driver shortage, coupled with rising operating cost and emission compliance challenges, is driving the

adoption of ECT technologies such as AMT and AT.

Source: Frost & Sullivan

7 NF9E-18

Characteristics Stepped Manual [MT] Automated Manual [AMT]

Stepped Automatic

[AT] Dual Clutch [DCT]

Shift Time [ms] 1,500-2,000 1,000–1,500 500–700 600–800

Fuel Consumption

Savings Baseline

MD +3-+10%

HD +0–+8%

MD +1-+6%

HD -5–+1%*

MD +3–+5%

HD NA

Weight Baseline MD +5-+10%

HD -10–+70%

MD Similar to AMT

HD +70–+80%

MD +0%-+50%

HD +70-+90%

Cost [$] Baseline MD +600-3,000

HD + 1,000–5,000

MD +3,600-6,000

HD +6,000–10,000

MD +3,000-6,000

HD +5,000–10,000

CO2 Reduction Baseline 3–5% 3-8% 4–8%

Key Suppliers ZF, Eaton, Shaanxi Fast

Gear, Wanliyang

ZF, Eaton, Shaanxi Fast

gear Allison ZF, Eaton

Key Vertically

Integrated OEM

Groups

CNHTC, FAW, Dongfeng,

Tata, Ashok Leyland

Daimler, Volvo, VW,

CNHTC, FAW, Dongfeng,

Tata, Ashok Leyland

None Daimler, Volvo

End Consumer

Feedback/

Acceptance

• Low cost

• High fuel efficiency

• Ease of maintenance

• Poor shift quality

• Improved fuel efficiency

in most duty cycles

• High comfort levels

and shift quality

• Higher price

• Good shift quality

• Expensive

• Bulkiest/Heaviest

2025 Growth

Potential Low High Medium Medium

*Allison’s TC10 are reported to have a 3-5% fuel saving.

Executive Summary—Truck Transmission Technology Comparison The dual clutch transmission is increasingly identified as the best of both worlds, combining the comfort of an

automatic and fuel consumption benefits of a manual.

Source: Frost & Sullivan

8 NF9E-18

Parameters Current Outlook (2015) Future Outlook (2025)

Market

Status

This market globally continues to be dominated by

MTs whereas TRIAD markets have already

adopted widely developed AMTs with 55.4% and

22.8% penetration in EU and NA, respectively.

AMTs are expected to be the fastest growing transmission type

with 12.5% CAGR between 2015 and 2025.

Competition

It is a highly oligopolistic market with top 3 tier-I

suppliers accounting for more than 47% of the

market.

Chinese transmission manufacturers are expected to begin

supplying to overseas markets and/or customers, creating a

greater threat of substitution for foreign transmission suppliers.

Value

Proposition

Truck manufacturers are offering customized

(downsped) powertrains to fleets so as to offer

greater fuel economy benefits. The resulting higher

torque at cruise speeds drive the demand for ECTs

which arrest the damage caused to transmission

through improper manual handling.

Driver shortage, health, wellness, and wellbeing factors,

combined with the trend toward autonomous trucks will drive the

demand for ECTs that can retain or improve the fuel efficiency

of manuals while reducing driver-control.

Technology

Current key technologies are MTs, AMTs, and

conventional stepped ATs. DCTs are garnering

interest in the truck segment. ZF already has a

revenue stream from telematics (openmatics).

Truck OEMs and tier-I transmission suppliers are investing in

technologies such as CVP by Fallbrook Technologies and IVT

by Torotrak. These are expected to be mass produced by 2020.

Further, following the implication of connectivity and big data in

trucks, more tier-I suppliers will look to integrate telematics into

their revenue stream.

Market Entry

Barriers

The high level of market consolidation among large

and established suppliers is a great hurdle for new

entrants.

Increasing vertical integration by truck OEMs

decrease market attractiveness.

There will be a widespread need to adapt strategic pricing

methods, and incorporate advanced communication, sensing,

power, and tracking technologies

MD-HD Truck Transmissions Market: Current and Future Outlook, Global, 2015 and 2025

Executive Summary—Key Findings and Future Outlook Oligopolistic competitive landscape will remain; threat to tier-I suppliers due to greater vertical integration of

transmission systems by OEMs; telematics to be targetted for a new revenue stream.

Source: Frost & Sullivan

Return to contents

9 NF9E-18

Research Scope, Objectives, Background, and

Methodology

10 NF9E-18

Research Scope

Commercial Trucks Vehicle Type

2016–2025 Forecast Period

2015–2025 Study Period

2015 Base Year

Global

• North America consists of the United States, Canada, and Mexico

• South America includes all other countries of Latin America

• Europe consists of the EU and non-EU countries in Europe other

than Russia.

• China

• India

• Russia

• Next 11 (Egypt, Indonesia, Iran, Mexico, Nigeria, Pakistan, the

Philippines, Turkey, South Korea, Vietnam, and Bangladesh)

• Rest of the world (RoW)

Geographical Scope

Source: Frost & Sullivan

11 NF9E-18

Research Aims and Objectives

Aim

• The aim of the study is to offer an outlook of the global MD-HD truck transmissions market for the 2015–

2025 period. The study also offers actionable information and forecasts of the key trends and metrics

that are likely to influence the growth and development of the global MD-HD commercial truck

transmission systems market.

Objectives

• To provide market size and forecasts of truck transmission systems for 2015–2025.

• To provide a strategic overview of the market share of various transmission system suppliers and

outlook.

• To provide strategic insights and deep-dive analyses of product strategy of global truck OEMs and tier-I

transmission system suppliers.

• To provide strategic insight into OEM and tier-I supplier global growth initiatives, capabilities, and

activities toward enhancing product profitability and technology in truck transmission systems.

• To analyze competitive factors, competitor market shares, and product portfolio and capabilities.

• To develop an actionable set of recommendations for market growth and sustenance.

Source: Frost & Sullivan

12 NF9E-18

Key Questions This Study Will Answer

What are the key trends impacting the MD-HD truck transmissions market?

How will transmission systems evolve by 2025? What will be the market share of each technology?

What will be the product focus of key transmission suppliers in each region?

What will be the transmission strategy for truck OEMs across regions?

What is the projected volume of transmission sales in 2025?

What are the drivers and restraints for various transmission technologies?

Source: Frost & Sullivan

13 NF9E-18

Research Background

This research builds on the content from Frost & Sullivan’s recently published studies in the area of

business strategy and innovation:

NEC5-18 Strategic Outlook for Autonomous Heavy-duty Trucks (2015)

NF51-18 Executive Outlook of Hyundai’s Global Commercial Vehicle Market Activities (2015)

NF8D-18 Executive Analysis of Medium-Duty and Heavy-Duty Value Truck Market in Select Emerging

Economies (2015)

NFAB-01 Executive Profiles of Key Truck Telematics Vendors—PART 1(2015)

NE05-18 Executive Outlook of the Global Medium- and Heavy-Duty Low-Cost Truck Market (2015)

P895-18 Strategic Analysis of Chinese Light, Medium, and Heavy-Duty Commercial Truck Market (2015)

ND32-18 Strategic Analysis of Global City Truck Market (2014)

NC9A-18 Commercial Vehicles 2020 Vision (2014)

NE67-18 Executive Impact Analysis of Big Data in the Trucking Industry (2014)

This study is also supplemented by ongoing interactions with vehicle manufacturers and suppliers in the

area of business strategy and innovation.

Source: Frost & Sullivan

14 NF9E-18

Research Methodology: Frost & Sullivan’s research services are based on secondary and primary

research data.

Secondary Research: Extraction of information from existing reports and project material within the

Frost & Sullivan database includes data and information gathered from technical papers, specialized

magazines, seminars, and Internet research.

Primary Research: More than 15 interviews have been conducted over the phone by senior consultants

and industry analysts with original equipment suppliers, regulation authorities, and distributors. Primary

research accounts for 80% of the total research.

Note on Images: Images have been used with permission of the copyright holder.

Research Methodology

Source: Frost & Sullivan

15 NF9E-18

Key OEMs Compared in This Study

Group CV OEMs

Daimler

Mercedes-Benz, Freightliner,

Western Star, Fuso, Thomas

Built, Bharat Benz, Setra

Volvo Volvo, UD, Renault, Mack,

Eicher

Volkswagen Volkswagen Commercial

Vehicles, MAN, Scania, SEAT

BAIC Foton Motor

Navistar Navistar, IC bus, SST Truck

Company

Hyundai Motor

Group (HMG)

Hyundai, Kia, Sichuan

Hyundai Motor Company

Group CV OEMs

Dongfeng DFM, Dongfeng Peugeot-Citreon

Paccar DAF, Kenworth

Ford Ford

Tata Tata Motors

CNH Iveco, Iveco Astra, Heuliez Bus

Toyota Toyota, Daihatsu, Hino

CNHTC Sinotruck

FAW FAW

The following OEM groups are compared in this study:

Source: Frost & Sullivan

Return to contents

16 NF9E-18

Definitions and Segmentation

17 NF9E-18

Product/Technology Segmentation

MD-HD Truck Transmissions Market: Product/Technology Segmentation, Global, 2015

Automated Manual

Transmission (AMT) Automatic Transmission

Dual Clutch

Transmission (DCT)

Stepped

Automatic Transmission (AT)

Transmission Technologies

Infinitely Variable

Transmission (IVT)

Manual Transmission

(MT)

Continuously Variable

Planetary (CVP)

Twin Counter-shaft

Automatic Transmission (TC10)

Electronically controlled

Transmissions (ECT)

Commercialized Technology

Technology in the Incubation Stage Source: Frost & Sullivan

18 NF9E-18

Product/Technology Segmentation (continued)

• MTs require the driver to operate the clutch through a pedal or a lever and engage the gears (shift

up/down) by using a gear shift lever.

• AMTs or semi-automatic transmissions operate like a MT but without a clutch pedal. The shifting can be

entirely computer controlled or driver controlled through shifter paddles or buttons mounted on the

steering wheel.

• DCT is a type of AMT which encompasses two gearboxes (one housing the odd gears and the other

even gears) with a separate clutch for each. This setup, therefore, allows for the pre-selection of the next

expected gear ratio while driving the current gear, with timed engaging and disengaging of the

respective clutches. Thus it allows for fast and smooth gear shifting and no torque interruptions. It is

operated generally in the automatic D mode but some also have the option of manual shifting.

• A stepped AT automatically changes gear ratios in response to the speed of the vehicle without any

external command from the driver. It encompasses a planetary gear set and a torque converter. An AT

is predominantly hydraulically operated. The planetary gear set uses the same set of gears to provide

different gear ratios as opposed to using different sets of gears as in an MT. The torque converter

connects the engine to transmissions. It is a type of fluid coupling that provides torque multiplication at

low engine speed.

• Allison Transmissions offers a new AT technology which uses 2 countershafts and a torque converter.

This product is called TC10 (for Twin Countershaft and Torque Converter) plus 10 speeds. This

technology is patented by Allison and allows shifts without interrupting engine torque. It has very fast

shift times, the same as a traditional automatic (AT).

• This study groups AMT, DCT, and AT as ECTs.

Source: Frost & Sullivan

19 NF9E-18

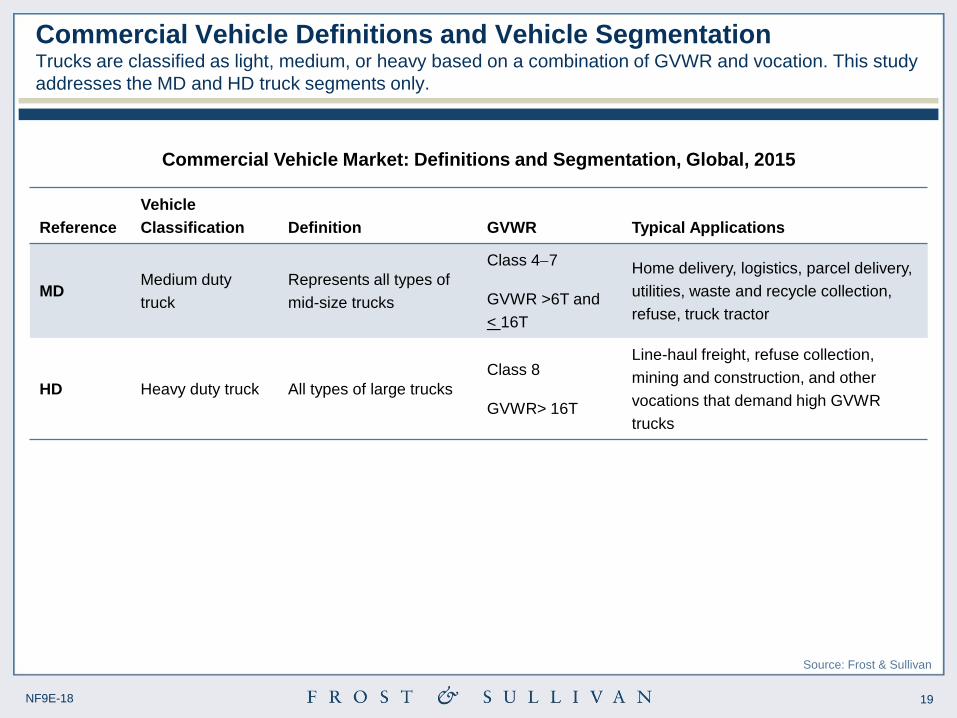

Reference

Vehicle

Classification Definition GVWR Typical Applications

MD Medium duty

truck

Represents all types of

mid-size trucks

Class 47

GVWR >6T and

< 16T

Home delivery, logistics, parcel delivery,

utilities, waste and recycle collection,

refuse, truck tractor

HD Heavy duty truck All types of large trucks

Class 8

GVWR> 16T

Line-haul freight, refuse collection,

mining and construction, and other

vocations that demand high GVWR

trucks

Commercial Vehicle Definitions and Vehicle Segmentation Trucks are classified as light, medium, or heavy based on a combination of GVWR and vocation. This study

addresses the MD and HD truck segments only.

Commercial Vehicle Market: Definitions and Segmentation, Global, 2015

Source: Frost & Sullivan

20 NF9E-18

The Last Word—3 Big Predictions

2 Telematics will be a major revenue stream for both tier-I transmission suppliers and

OEMs that will be driven by the increasing integration of connectivity, Big Data,

telematics, and autonomous driving technology in trucks.

3 By 2025 China will be the largest market for AMTs, accounting for 28% of global AMT

sales and NA will be the largest market for ATs accounting for 55.7% of the global AT

sales in the MD-HD truck market.

1 Greater vertical integration by OEMs will result in further consolidation in the truck

transmissions market, with OEMs accounting for a majority 33% market share by

2025 followed by top 3 tier-I suppliers accounting for close to 50% market share.

Source: Frost & Sullivan

21 NF9E-18

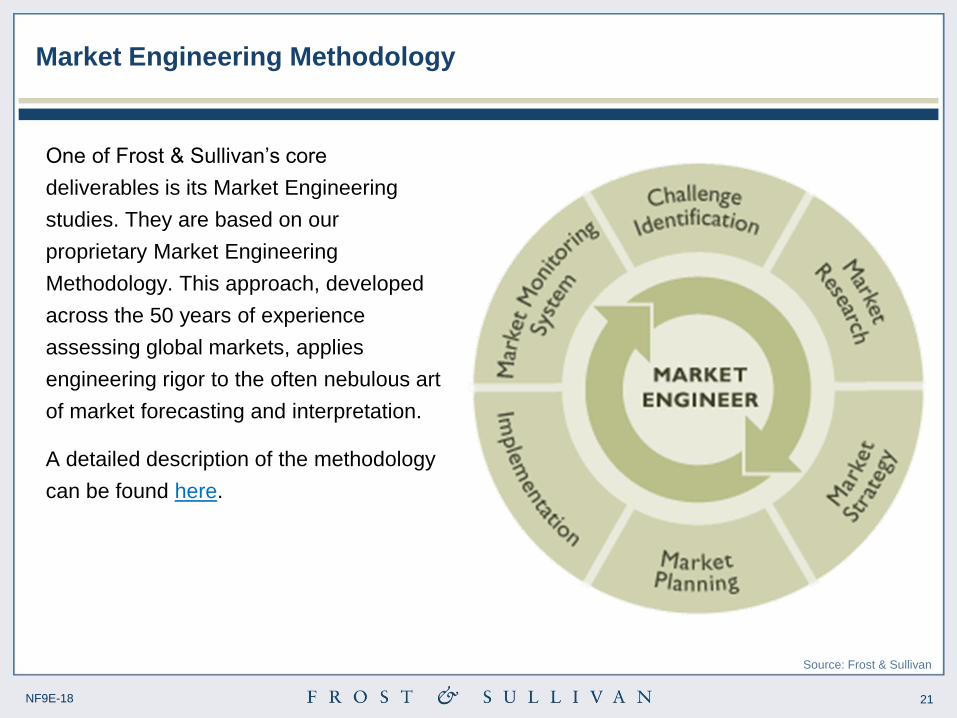

Market Engineering Methodology

One of Frost & Sullivan’s core

deliverables is its Market Engineering

studies. They are based on our

proprietary Market Engineering

Methodology. This approach, developed

across the 50 years of experience

assessing global markets, applies

engineering rigor to the often nebulous art

of market forecasting and interpretation.

A detailed description of the methodology

can be found here.

Source: Frost & Sullivan

![Bosch ESI[truck] Heavy Duty Truck Software Update – Q1 ...€¦ · Bosch ESI[truck] Heavy Duty Truck Software Update | Ver 2019/1 6 | 41 41135 42908 45411 47482 37000 38000 39000](https://static.fdocuments.in/doc/165x107/600ed0e779e62601223e82fb/bosch-esitruck-heavy-duty-truck-software-update-a-q1-bosch-esitruck-heavy.jpg)

![Bosch ESI[truck] Heavy Duty Truck Software Update – Q3 ...€¦ · Bosch ESI[truck] Heavy Duty Truck Software Update | Ver 2019/3 7 | 34 2. STATISTICS 10 New Makes 391 New Models](https://static.fdocuments.in/doc/165x107/5fdc21500e0e776d1608582f/bosch-esitruck-heavy-duty-truck-software-update-a-q3-bosch-esitruck-heavy.jpg)