Marine Harvest Canada Wharfside newsletter June 2016 edition

GLOBAL MARKET UPDATE

August 2016 Volume 7 Issue No. 8

Fax (415)

458- 5160

CIATTI GLOBAL WINE & GRAPE BROKERS

1101 Fifth Avenue #170

San Rafael, CA 94901

Phone (415) 458-5150

Ciatti Global Market Update | August 2016

2

Volume 07, Issue No. 08, August 2016

July and early August have brought heat to the Northern

Hemisphere. California’s Central Valley experienced some

consecutive days of temperatures at 100˚F+ in early August;

in France’s Provence and Languedoc regions, water reserves

are low; in Italy, mildew and juice levels are a concern.

Overall, however, temperatures have not been abnormal

and notable problems with ripening have not been reported

in any country.

The growing seasons in France, Spain and Italy are two

weeks behind schedule; Italy’s lateness is causing stress for

Prosecco buyers in particular. As you will read, Prosecco is one

of the imported sparkling wines enjoying a “sensational growth

uptrend” in the US consumer market and supply of 2015

Prosecco is almost gone. The 2016 Prosecco can’t come soon

enough. Buyers cannot, however, count on lower prices when

the 2016 vintage does come online: supply increases are

tracking, not exceeding, the demand increase.

US demand for Prosecco will soon exceed demand from

the UK, where consumer confidence – as you can read in our

special report on page 14 – has taken a post-Brexit hit.

Respected UK analyst GFK’s monthly consumer confidence

survey registered an index of -12 in July, a decline of 11 points

from -1 in June, the sharpest monthly fall for 26 years. However,

there are two large caveats: first, the July survey was carried out

before the new Prime Minister was in place, after which full

political stability returned; second, confidence is down from a

very high base, higher even than in the years preceding the

2008-09 global financial crisis.

The preferential treatment EU wine suppliers have

enjoyed in the UK market may not survive the UK’s eventual EU

withdrawal: efforts to sell to the US and China may need to be

redoubled. A report on the booming imported wine market in

China, which is benefiting from a growing urban upper-middle

class as well as bilateral trade deals, is on page 15.

In the Southern Hemisphere, meanwhile, 2016 harvest

tonnage was up 6% in Australia and 34% in New Zealand. El

Niño weather patterns have left Argentina and Chile, and the

vines there are now experiencing a good, normal resting period.

Robert Selby

Argentina 2

Australia 3

California 4

Chile 5

France 6

Germany 7

Italy 8

New Zealand 9

South Africa 10

Spain 11

Market profile:

Scandinavia 12

Craft Beer 13

California 3

Argentina 5

Chile 6

France 7

Spain 9

Italy 10

South Africa 11

Australia 12

New Zealand 13

Brexit Update 14

Market Focus: China 15

Craft Beer Update 16

Contacts 17

No part of this publication may be reproduced or

transmitted in any form or by any means without

the written permission of Ciatti Company.

Ciatti Global Market Update | August 2016

3

CALIFORNIA

Harvest watch: looking good in quality,

average in size

TIME ON TARGET

The 2016 harvest is in its very early days –

having just commenced in the southern end of

California’s Central Valley and due to begin

any day now in the Central Coast – and the

crop looks good in quality and back up to

average-sized after last year’s smaller harvest.

There are no dramas: diligent spraying

programmes have fought mildew back, windy

afternoons have kept from settling in

vineyards any smoke blown in from distant

wildfires, and though some days have been

very hot, temperatures on the whole have not

been abnormal for this time of year.

Temperatures at the end of July into start

of August were at 100˚F-plus for 5-6 days

consecutively in the Central Valley, which might

have meant vine development halting temporarily

– or simply that it will be a good push to the

finish. It’s too early to give a complete analysis at

the moment. Overall, grapes are sizing nicely.

The 2016 crop, then, with most tonnage

figures returning to a five-year average, is very

unlikely to sway the marketplace in one direction

or another; prices are not going to rise another

15-20%, but the demand varietals will stay in

demand. There is not expected to be a bumper

Cabernet crop, for example, and its supply from

the premium regions will remain tight. The lion’s

share of new plantings in the past three years

have been Cabernet: some of it will contribute to

this year’s harvest but most won’t come online

until the 2017 harvest, when sizeable increases in

Cabernet tonnages are hoped for.

Buying activity has been steady: there is

excitement when a premium red wine becomes

available, such as a Napa or a Mendocino

Cabernet. In the whites, Pinot Grigio and Pinot

Noir are tight. Activity in lower-end and bulk

wines is ticking along, and none of the traditional

bulk suppliers are sitting on inventory they need

to shift, so non-traditional suppliers are receiving

enquiries.

According to Gomberg Wine Data,

Californian bottled wine exports in January-May

reached 8.8 million 9-litre cases, down 9.4% from

9.8 million cases in the equivalent period of 2015

(which itself was down from 10 million cases in

2014). Gomberg cautioned: “The growing strength

of the US dollar raised California wine retail prices

in foreign markets, hurting sales.” Also, big

players are increasingly bottling their wines in

foreign countries to save costs, further affecting

bottled wine export statistics. Overall, though,

Californian packaged shipments for January-May

2016 increased, reaching 99.6 million cases, a rise

of 2.5% on 97.1 million cases in 2015 (and also

just up on 99 million cases in 2014). This was

thanks to good demand from California (+4.8%)

and the rest of the US (+3.6%).

In May in the US, “imported sparklers

continued their sensational growth uptrend,”

Gomberg reported, as US consumers continue

trading up. While bottled table wine imports fell

by 271,000 cases (mostly Italian and French – wine

from other countries remained robust), Italian

Prosecco grew 32%, while French Champagne and

Vin Mousseux grew 27%.

SEE NEXT PAGE FOR PRICES & CONTACTS

KEY TAKEAWAYS

The harvest is proceeding without dramas but its

expected average size promises little relief on

the supply side; it probably isn’t going to help

buyers looking for discounted inventory in the

premium market. US bottled exporters need to

keep an eye on the strength of the US dollar and

ensure they’re not becoming uncompetitive on

price in foreign markets. Americans can’t get

enough of Italian Prosecco and French sparkling.

Ciatti Global Market Update | August 2016

4

CALIFORNIA – IMPORT / EXPORT

T. +415 458-5150

Greg Livengood (CEO) – [email protected]

Steve Dorfman – [email protected]

CALIFORNIA – DOMESTIC

T. +415 458-5150

John Ciatti – [email protected]

Glenn Proctor – [email protected]

John White – [email protected]

Chris Welch – [email protected]

California: Current Market Pricing (USD PER LITER)

Vintage Variety Price Trend Vintage Variety Price Trend

2015 Generic White 0.60 – 0.80 ↔ 2015 Generic Red 0.80 – 1.05 ↓

2015 Chardonnay 1.45 – 1.88 ↑ 2014/15 Cabernet Sauvignon 1.58 – 2.11 ↑

2015 Pinot Grigio 1.58 – 1.98 ↔ 2015 Merlot 1.18 – 1.58 ↔

2015 Muscat 0.92 – 1.32 ↓ 2015 Pinot Noir 1.85 – 2.25 ↑

2015 White Zinfandel 0.85 – 0.99 ↔ 2015 Syrah 1.18 – 1.58 ↔

2015 Colombard 0.73 – 0.99 ↔ 2014/15 Zinfandel 1.72 – 2.11 ↑

Ciatti Global Market Update | August 2016

5

ARGENTINA

Harvest watch: good snows and cold

temperatures bode well for 2016/17

TIME ON TARGET

El Niño has passed and weather conditions

have thankfully returned to normal: for this

time of year, that means cold temperatures

and snow in the mountains. There, snow has

been heavy, slowing shipments through Chile –

the border has been closed 3-4 days every

week – but boding well for the coming water

needs of Mendoza’s vineyards. Normal

seasonal temperatures also mean the vines can

undergo their normal growth cycle, so it’s a

good beginning.

Foreign and domestic buyers have been

reasonably active in the part of the Malbec market

where volume is available: at the high-end, where

Malbec can come in at USD1.70-2.50/litre. Malbec

at USD1.50/litre and below is becoming short due

to the small crop and domestic needs. Generic

reds are hot as domestic buyers search for supply:

prices are up 93% on last year, not ideal when

Argentinian consumers are struggling with a

recession. Half of domestic consumption is Tetra

Pak wine, some of which has lately risen in price

by 15-25 pesos. Domestic sales have thus fallen

and will continue to do so.

First-half export statistics are in from

industry body Bodegas de Argentina: bulk wine

export volumes in January-May 2016 were down

37.09% on the first six months of 2015, from 38.2

million litres to 23.7 million litres; bottled wine

export volumes were stable, 0.7% up on the first

six months of 2015 to 8.25 million litres. Bulk wine

exports to the leading destination, the US, were

down 71.6% from 25.7 million litres to 7.3 million

litres because buyers of generic Malbec pulled out

due to the higher pricing: this is reflected in the

fact that of the wine exported to the US this year,

the export price per litre was USD1.19/litre, up

from USD0.78/litre last year. A fall in export

volumes to the US will continue for the rest of

2016 due to the shortening supply and resulting

higher prices.

Bottled exports to the US (-5.8%) and

Canada (-4.7%) were down. This seems

counterintuitive, considering current US consumer

demand for premium wines; it is hoped this does

not mark the start of a trend. Exports to Brazil

were up 2.6%, but are expected to fall at any time

as Brazil’s economy downturns. Grape juice

concentrate prices remains at their high level of

USD1,300-1,400/MT and sales are slow.

KEY TAKEAWAY

Quantities of higher-end Malbec are available. The

low-end is short, and priced accordingly.

Ciatti Contact: Eduardo Conill

T. + 54 261 420 3434

Current Market Pricing (USD PER LITER; FCA WINERY)

Vintage Variety Price Trend Vintage Variety Price Trend

2016 Generic White 0.40 – 0.45 ↑ 2016 Bonarda 0.90 – 1.20 ↑

2016 Generic White (Criolla) 0.35 – 0.38 ↑ 2016 Generic Red 0.60 – 0.80 ↑

2016 Chardonnay 0.90 – 1.20 ↑ 2016 Cabernet Sauvignon 1.30 – 1.50 ↑

2016 Torrontes 0.60 – 1.00 ↑ 2016 Malbec Entry-Level 1.30 – 1.50 ↑

2016 Sauvignon Blanc 0.90 – 1.00 ↑ 2016 Malbec Premium 1.50 – 2.50 ↑

2016 Muscat 0.40 – 0.45 ↑ 2016 Syrah / Merlot 1.00 – 1.20 ↑

Ciatti Global Market Update | August 2016

6

CHILE

Harvest watch: larger than expected,

though still 21.2% down on 2015

TIME ON TARGET

The official production figure for the 2016 harvest has exceeded the 800-900 million litres expected:

total wine production in fact reached 1.014 billion litres, down 21.2% on 2015 but roughly in line

with the frost-hit harvest of 2014. Designation of Origin reds came in at 590 million litres; volumes

of DOC Carmenere (-36%), Merlot (-28%) and Cabernet (-27.6%) all came in lower than in 2015 (and

lower than in 2014 too).

Buyers should be aware that although the headline production figure is higher than expected, the

volume of quality in the red wine market will not exceed expectations. Wineries tried to crush as much as

possible, accepting grapes affected by the El Niño rains, so that affected wines – among which volatile

acidity is a problem – make up a small but significant percentage of red wine production: 20% is a widely-

held view. With this quality volume fall in addition to the overall volume fall, prices for the reds of good

quality will remain stable at best and likely rise steadily. For quality red varietals such as Cabernet, Merlot

and Carmenere, prices will go up, though will not reach the heights seen after the earthquake in 2010. The

message is: if you need good quality wines in large volume – particularly reds – don’t wait. On the flip-side,

there will be some very aggressively-priced low-end red wines available on the spot market.

In July, as most large buyers had already moved quickly to cover their needs, the export market was

mainly active in small volumes. The domestic market has been very active, driven by Chile’s big five players.

Most buyers have secured a big part – but not all – of their needs: the rest of the year will mainly see spot

deals. Some good quality wines may still be available late on, as a few wineries have held off from selling

until the market price rises to meet their expectations; by then, with supply very tight, buyers will not be

able to argue with a Cabernet price of perhaps USD1.05-1.10/litre.

Such a price could be even higher if Chile suffers from heavy frosts during the budding stage in

September, currently a widely-held fear not only among the wine business but Chile’s fruit industry too. It is

unknown where exactly this fear is founded: as the UK’s Met Office states, “forecasting air temperature and

frost more than a few days in advance can be complex”. One certainty is that El Niño has gone from Chile

and weather patterns have normalised: the country’s vines are currently getting a good rest.

Export Figures Wine

Export Figures

January 2015 - June 2015 January 2016 – June 2016 Volume

Million Liters

Million US$ FOB

Average Price

Million Liters

Million US$ FOB

Average Price

Variance %

Bottled 215,71 688,62 3,19 225,57 692,88 3,07 4,57

Bulk 177,29 126,85 0,72 204,75 129,48 0,63 15,49

Sparkling Wines

1,44 6,07 4,22 1,72 7,10 4,12 19,76

Packed Wines

13,16 22,74 1,73 15,53 26,54 1,71 18,04

Total 407,59 844,28 2,47 447,58 856,00 2,38 9,81

KEY TAKEAWAYS

Buyers should not wait to cover their needs – prices

will not fall for good quality wines, especially reds.

Lower quality wines will be priced very competitively.

Ciatti Contact

Marco Adam

T. +56 2 2363 9206 – or – T. +56 2 2363 9207

Ciatti Global Market Update | August 2016

7

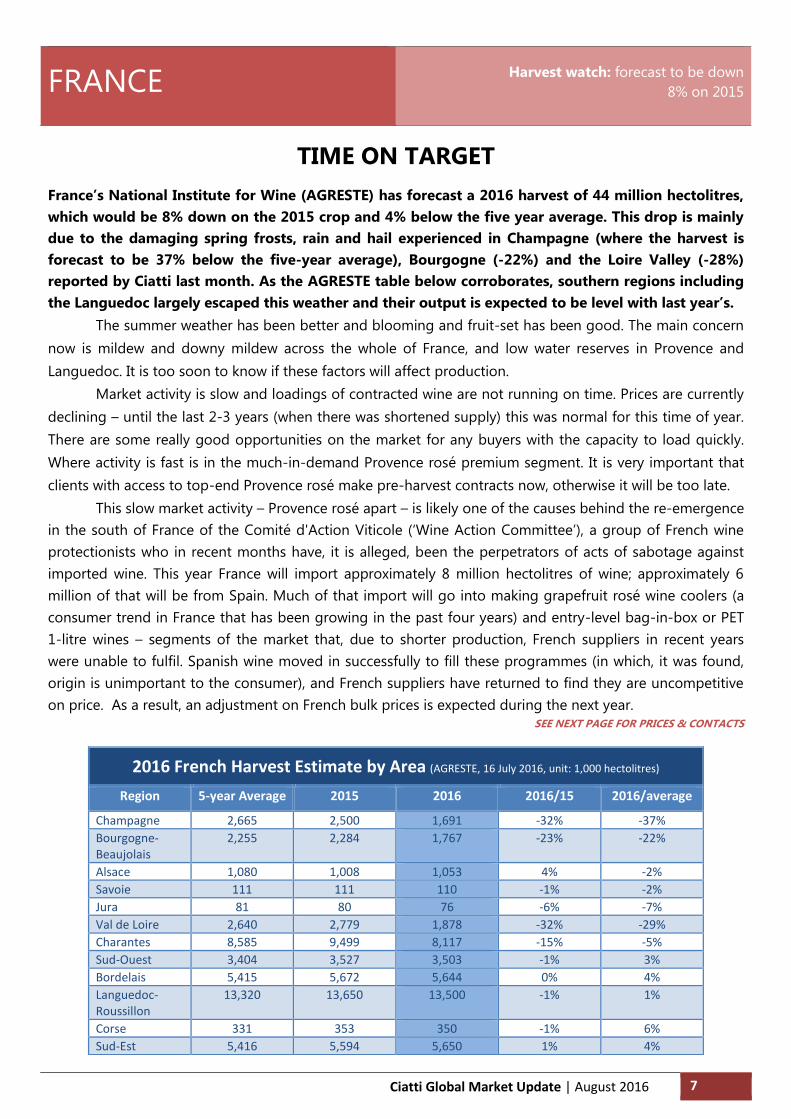

FRANCE

Harvest watch: forecast to be down

8% on 2015

TIME ON TARGET

France’s National Institute for Wine (AGRESTE) has forecast a 2016 harvest of 44 million hectolitres,

which would be 8% down on the 2015 crop and 4% below the five year average. This drop is mainly

due to the damaging spring frosts, rain and hail experienced in Champagne (where the harvest is

forecast to be 37% below the five-year average), Bourgogne (-22%) and the Loire Valley (-28%)

reported by Ciatti last month. As the AGRESTE table below corroborates, southern regions including

the Languedoc largely escaped this weather and their output is expected to be level with last year’s.

The summer weather has been better and blooming and fruit-set has been good. The main concern

now is mildew and downy mildew across the whole of France, and low water reserves in Provence and

Languedoc. It is too soon to know if these factors will affect production.

Market activity is slow and loadings of contracted wine are not running on time. Prices are currently

declining – until the last 2-3 years (when there was shortened supply) this was normal for this time of year.

There are some really good opportunities on the market for any buyers with the capacity to load quickly.

Where activity is fast is in the much-in-demand Provence rosé premium segment. It is very important that

clients with access to top-end Provence rosé make pre-harvest contracts now, otherwise it will be too late.

This slow market activity – Provence rosé apart – is likely one of the causes behind the re-emergence

in the south of France of the Comité d'Action Viticole (‘Wine Action Committee’), a group of French wine

protectionists who in recent months have, it is alleged, been the perpetrators of acts of sabotage against

imported wine. This year France will import approximately 8 million hectolitres of wine; approximately 6

million of that will be from Spain. Much of that import will go into making grapefruit rosé wine coolers (a

consumer trend in France that has been growing in the past four years) and entry-level bag-in-box or PET

1-litre wines – segments of the market that, due to shorter production, French suppliers in recent years

were unable to fulfil. Spanish wine moved in successfully to fill these programmes (in which, it was found,

origin is unimportant to the consumer), and French suppliers have returned to find they are uncompetitive

on price. As a result, an adjustment on French bulk prices is expected during the next year.

SEE NEXT PAGE FOR PRICES & CONTACTS

2016 French Harvest Estimate by Area (AGRESTE, 16 July 2016, unit: 1,000 hectolitres)

Region

5-year Average 2015 2016 2016/15 2016/average

Champagne 2,665 2,500 1,691 -32% -37%

Bourgogne-Beaujolais

2,255 2,284 1,767 -23% -22%

Alsace 1,080 1,008 1,053 4% -2%

Savoie 111 111 110 -1% -2%

Jura 81 80 76 -6% -7%

Val de Loire 2,640 2,779 1,878 -32% -29%

Charantes 8,585 9,499 8,117 -15% -5%

Sud-Ouest 3,404 3,527 3,503 -1% 3%

Bordelais 5,415 5,672 5,644 0% 4%

Languedoc-Roussillon

13,320 13,650 13,500 -1% 1%

Corse 331 353 350 -1% 6%

Sud-Est 5,416 5,594 5,650 1% 4%

Ciatti Global Market Update | August 2016

8

KEY TAKEAWAYS

Prices are softening and there are excellent

opportunities for any buyers with the capacity to

load quickly. Buyers wanting top-end Provence rosé

from the coming harvest should make their

reservations now.

Ciatti Contact

Florian Ceschi

T. +33 4 67 913532

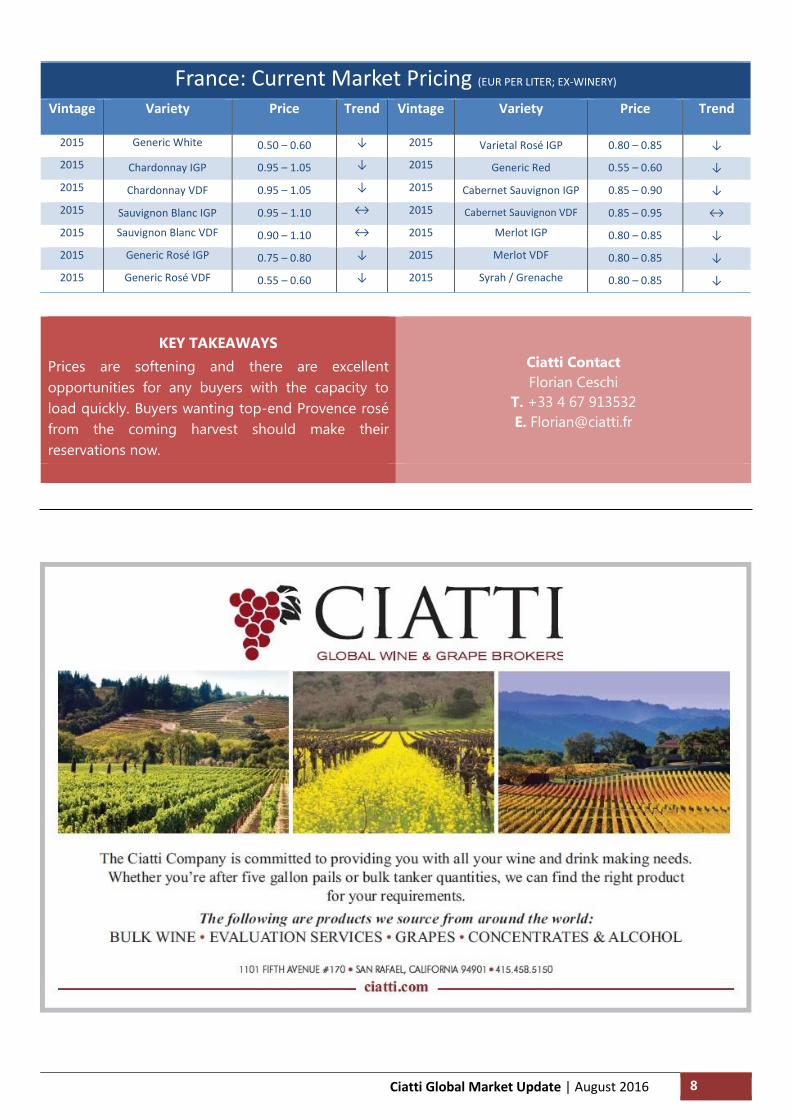

France: Current Market Pricing (EUR PER LITER; EX-WINERY)

Vintage Variety Price Trend Vintage Variety Price Trend

2015 Generic White 0.50 – 0.60 ↓ 2015 Varietal Rosé IGP 0.80 – 0.85 ↓

2015 Chardonnay IGP 0.95 – 1.05 ↓ 2015 Generic Red 0.55 – 0.60 ↓

2015 Chardonnay VDF 0.95 – 1.05 ↓ 2015 Cabernet Sauvignon IGP 0.85 – 0.90 ↓

2015 Sauvignon Blanc IGP 0.95 – 1.10 ↔ 2015 Cabernet Sauvignon VDF 0.85 – 0.95 ↔

2015 Sauvignon Blanc VDF 0.90 – 1.10 ↔ 2015 Merlot IGP 0.80 – 0.85 ↓

2015 Generic Rosé IGP 0.75 – 0.80 ↓ 2015 Merlot VDF 0.80 – 0.85 ↓

2015 Generic Rosé VDF 0.55 – 0.60 ↓ 2015 Syrah / Grenache 0.80 – 0.85 ↓

Ciatti Global Market Update | August 2016

9

SPAIN

Harvest watch: two weeks behind schedule,

expected to be 8-9% larger than in 2015

TIME ON TARGET The summer in Spain has been hot but

temperatures have thus far not reached as

high as those seen in the ‘Caliente’ or very hot

vintage of 2015. After a dry winter the

powerhouse Castilla-La Mancha region, which

produces over half of Spain’s wine, received

good spring rainfall that is helping to see it

through summer. With very few reports of

fungus, conditions for grape development

have been good. As mentioned last month,

vine development is approximately two weeks

behind schedule and there is a question mark

over the maturity of the reds.

As for harvest volume, early signs are that

it could come in roughly 8-9% larger than the

2015 harvest, when wine and grape juice

production reached 42 million hectolitres (a 3.3%

fall on 2014). Of that 2015 harvest, 37.2 million

hectolitres went into wine, and 4.8 million

hectolitres into grape must. Production of ‘PDO’ –

Designation of Origin – wines was up 4.5%;

production of ‘PGI’ – Indication of Origin – wines

was up 19%; other varietal wines were up 3.2%;

generics were down 17.7%. Castilla-La Mancha

remained the largest producer region with 22.5

million hectolitres, 53.5% of total production.

On the market, wine stocks are relatively

low. As a result, prices have remained pretty firm

and fewer massive purchases were made in July

this year than in July 2015. Currently there are no

deals for generic whites done below EUR2.40 per

hectograde (i.e. approximately EUR0.22/litre),

which is up on 2015, but still one of the cheapest

prices to be found globally. For generic reds,

behind whites in terms of production and loading,

the price is still up at EUR2.80/hectograde

(around EUR0.25/litre). Buyers who usually buy in

Chile have not yet been seen in huge numbers

prospecting the Spanish market.

KEY TAKEAWAY

The 2016 harvest is expected to come in larger

than that of 2015. Current stocks are on the low

side and prices are thus firm. However, Spanish

prices are still incredibly competitive and can, for

instance, compete with Chile in every category.

Ciatti Contact

Nicolas Pacouil

T. +33 4 67 913531

Current Market Pricing (EUR PER LITER; EX-WINERY)

Vintage Variety Price Trend Vintage Variety Price Trend

2015 Generic White 0.25 – 0.35 ↔ 2015 Generic Red 0.28 – 0.35 ↔

2015 White Blends

(High Quality)

0.40 – 0.60 ↔ 2015 Generic Red

(High Quality)

0.35 – 0.50 ↔

2015 Sauvignon Blanc 0.52 – 0.56 ↔ 2015 Cabernet Sauvignon 0.50 – 0.65 ↔

2015 Chardonnay 0.60 – 0.65 ↔ 2015 Merlot 0.55 – 0.70 ↔

2015 Generic Rosé 0.28 – 0.38 ↔ 2015 Tempranillo 0.40 – 0.60 ↔

2015 Varietal Rosé 0.40 – 0.50 ↔ 2015 Syrah 0.45 – 0.60 ↔

2015 Moscatel 0.40 –0.60 ↔

Ciatti Global Market Update | August 2016

10

ITALY

Harvest watch: two weeks behind schedule,

expected to be good

TIME ON TARGET The growing season in Italy, two weeks behind

schedule, is proceeding smoothly. Mildew has

been a problem, while some heavy rains at

flowering time have helped reduce any excess

clustering. Some harvesting is already

underway, and there has been concern that the

early grapes are containing less juice than

normal, but it is too early to say.

Prosecco contract renewals made July’s

business busier than in recent months. Away from

Prosecco, stocks of entry level product in July

were at rock bottom and many wineries,

especially in the south-central areas, will get to

harvest empty. How busy the Italian market is in

future will depend on how big the country’s 2016

harvest is in relation to Spain’s. If its harvest this

year is bigger than in 2015, Italy may be able to

compete better with Spain on entry level prices.

The new harvest won’t bring much relief

on Prosecco prices, as increased output is only

meeting – and not exceeding – the steadily

increasing demand. Prices will be stable or

increase slightly. Buyers are counting down the

days until the 2016 Prosecco is available because

stocks are running short – thus news of a harvest

two-weeks delayed is not welcome.

The industry is waiting to see if Brexit and

the resultant devaluation of pound sterling will

have a negative impact on sales in Prosecco’s

leading export market. Respected UK analyst

GFK’s monthly consumer confidence survey

registered an index of -12 in July, a decline of 11

points from -1 in June, the sharpest monthly fall

for 26 years (see chart, page 14). However, the

July survey was carried out before the new Prime

Minister was in place, after which full political

stability returned.

In better news, Prosecco sales to the US –

which will soon surpass the UK as its leading

destination anyway – are increasingly strongly

(see page 3) and will be helped by the strength of

the US dollar against the Euro. Gomberg Wine

Data shows that in January-May 2016, Italian

sparkling wine imports into the US reached 2.61

million 9-litre cases, up 14% from 2.29 million

cases in the same period of 2015, which itself was

up from 1.55 million cases in January-May 2014.

The new additional DOC appellation for

Pinot Grigio, DOC Della Venezia, has hit

bureaucratic snags, creating some uncertainty

among operators. It now seems 2016 will be an

intermediate year in which IGT or DOC

classification can be used by operators in that

appellation, with unified roll-out not until 2017.

KEY TAKEAWAYS

Stock of entry level wines and Prosecco are very

low ahead of the new harvest, which, two weeks

behind schedule, can’t come soon enough.

Prices are firm. Prosecco to the US is booming.

Ciatti Contacts

Florian Ceschi

T. +33 4 67 913532

Current Market Pricing (EUR PER LITER; EX-WINERY)

Vintage Variety Price Trend Vintage Variety Price Trend

2015 Generic White 0.32 – 0.35 ↔ 2015 Generic Red 0.32 – 0.35 ↔

2015 Chardonnay 0.60 – 0.85 ↔ 2015 Cabernet Sauvignon 0.60 – 0.80 ↔

2015 Pinot Grigio 1.05 – 1.15 ↔ 2015 Merlot 0.55 – 0.75 ↔

2015 Prosecco 2.50 – 2.60 ↔ 2015 Chianti 1.55 – 1.80 ↔

Ciatti Global Market Update | August 2016

11

SOUTH AFRICA

Harvest watch: cold temperatures means growing

season 2016/17 is off to a good start

TIME ON TARGET

South Africa is now in the middle of its winter

season and cold temperatures thus far have

meant excellent conditions for the resting

period of the vines. Good rainfall and, in the

mountains, snowfall is replenishing the

catchment dams which bodes well for the

coming growing season. It is still early days,

however; because of the exceedingly dry late

2015/early 2016 summer, catchment dams are

still barely at 45-50% level and much more

consistent rainfall is required to get the dams

approaching even 80-85% full.

As per every year in South Africa, July was

a relatively slow month activity-wise. Buyers

prospecting South Africa as an alternative source

of wine to Chile have not been as common as

perhaps expected, but this could change when

Europe and elsewhere return from summer

holidays. Exports have held steady, so too prices.

Cabernet, Sauvignon Blanc and Chardonnay

remain heavily in demand, and that is reflected in

the relatively high price they command: good

commercial-quality varietal-character Sauvignon

Blanc at ZAR8.0 per litre (USD0.57/litre) or below

is very difficult to find.

The biggest planting of Cabernet is in the

Stellenbosch-Paarl-Wellington-Swartland region

of the Western Cape, which last growing season

was disproportionately hit by the dry weather; as

a result, while South Africa’s overall 2016 harvest

was 6-7% down on 2015, Cabernet came in

approximately 15% down. In addition, in recent

years Cabernet vines have been steadily replaced

by Pinotage because the latter is a higher-yield

crop than the former. Chardonnay has been

steadily replaced by Chenin Blanc for the same

reason. But Cabernet is popular for blends, and

Chardonnay remains in demand in established

markets and become popular in certain new ones.

Premium and good commercial-quality

Sauvignon Blanc is very short, mainly due to the

harsh dry ripening season’s high temperatures,

resulting in much lower yields of typical varietal-

character product for the 2016 harvest, just when

demand for both bottled and bulk South African

Sauvignon Blanc is strong from markets such as

the UK, Germany, the Netherlands, and Russia.

KEY TAKEAWAYS

South Africa is very attractive in terms of price-

quality ratio – though Cabernet, Sauvignon Blanc

and Chardonnay command a high price.

Ciatti Contacts

Vic Gentis

T. +27 21 880 2515

-or-

Petrè Morkel

T. +27 82 33 88 123

Current Market Pricing (SA RAND PER LITER; FOB CAPE TOWN)

Vintage Variety Price Trend Vintage Variety Price Trend

2016 Generic White 4.95 – 5.35 ↑ 2016 Generic Red 5.80 – 6.60 ↔

2016 Chardonnay 6.70 – 7.80 ↑ 2016 Cabernet Sauvignon 7.00 – 8.50 ↑

2016 Sauvignon Blanc 6.80 – 8.50 ↑ 2016 Ruby Cabernet 6.00 – 6.50 ↔

2016 Chenin Blanc 5.30 – 6.20 ↑ 2016 Merlot 6.80 – 8.00 ↔

2016 Muscat 5.75 – 6.35 ↔ 2016 Pinotage 6.60 – 7.50 ↔

2016 Generic Rosé 4.95 – 6.00 ↔ 2016 Shiraz 6.90 – 8.25 ↔

2016 Cultivar Rosé 5.70 –6.60 ↔ 2016 Cinsaut 6.00 – 6.30 ↔

Ciatti Global Market Update | August 2016

12

AUSTRALIA

Harvest watch: up on last year by 6% in AU

and 34% in NZ

TIME ON TARGET

The 2016 Australian Vintage Report has been released by the Winemakers Federation (WFA) and has

revealed that the Australian wine grape crush was 1.81 million tonnes, a 6% increase on 2015. The

top three varieties – Shiraz, Chardonnay and Cabernet Sauvignon – all increased in crush volume and

price. The increased volume of fruit from cool and temperate regions drove these increases up 26%.

The average purchase price also increased by 14% to AUD526 per tonne, the highest average price

since 2009. See summary table below of the top white and red varieties.

The Wine Australia Export Report shows that for the 12 months to June 2016, the value of wine

exports grew by 11% to AUD2.11 billion, and volumes were up by 0.5% to 728 million litres. The US still

remains a vital market for Australian wine, growing by 8% last financial year to AUD449 million, despite

volumes dropping by 4% to 157 million litres. Despite China and the US spending the most on Australian

wine, the UK still buys the largest volumes, accounting for about one third of all exports. Most of the wine

shipped to the UK arrives in bulk containers, to be bottled and distributed within UK and to other markets

around Europe.

Casella Family Brands have been active buying in Australia, purchasing the historic fortified producer

Morris of Rutherglen from Pernod Ricard. They have also purchased a 162 hectare vineyard in McLaren Vale

which is focused on Shiraz and Cabernet Sauvignon. The purchase continues Casella Family Brands’

targeting of wineries and brands in premium wine areas, which resulted in its purchase of Brand’s Laira from

McWilliam’s Wine last year and Peter Lehmann Wines in late 2014. SEE NEXT PAGE FOR PER LITRE PRICES

Summary of 2016 Australian crush

Top 5 White Varieties

Crush in Tonnes

Chardonnay Sauvignon Blanc Pinot Grigio / Gris Semillon Muscat Gordo

406,028 100,769 73,372 64,066 56,710

↑ 6% ↑ 11% ↓ 4% ↓ 6% ↑ 1%

Average Price per Tonne (AUD)

Chardonnay Sauvignon Blanc Pinot Grigio / Gris Semillon Muscat Gordo

382 553 619 345 219

↑ 21% ↑ 8% ↑ 4% ↑ 11% ↓ 7%

Top 5 Red Varieties

Crush in Tonnes

Shiraz Cabernet Sauvignon Merlot Pinot Noir Petit Verdot

430,185 255,074 111,959 47,860 20,299

↑ 7% ↑ 20% ↑ 3% ↑ 9% ↓ 4%

Average Price per Tonne (AUD)

Shiraz Cabernet Sauvignon Merlot Pinot Noir Petit Verdot

684 652 433 891 350

↑ 14% ↑ 17% ↑ 4% ↑ 4% ↑ 2%

Ciatti Global Market Update | August 2016

13

Samples of 2016 Marlborough Sauvignon

Blanc are now readily available with a good

number of options available to taste. Pricing is

at NZD3.25-3.75 per litre (USD2.35-2.72/litre)

FOB of varying quality levels; pricing is

dependent on volume, terms and drawdown.

Yealands Family Wines has just become

the first winery in the world to carry the DQS

Green Company GC-Mark for its winery operation

at their Seaview winery in Marlborough. DQS

Group (DQS) based in Germany are one of the

leading certification bodies for management

systems worldwide. DQS have developed a

checklist of criteria to obtain a Green Company

GC-Mark that is based on national and

international recognized standards and

regulations. To receive a Green Company GC-

Mark, a company must succeed in minimising its

negative impact upon the environment.

One of Marlborough's last remaining

conventional sheep and beef farms in the lower

Awatere Valley has been sold to Yealands Estate

for vineyard development. The 266-hectare

property is on the boundary of the 1,000 hectare

Yealands Estate, near Seddon, and will be

developed into a vineyard.

Source: New Zealand Winegrowers

NEW ZEALAND

Current Market Pricing (AUD/litre unless otherwise stated)

Vintage Variety Price Trend Vintage Variety Price Trend

NV Dry White 0.60 – 0.75 ↔ NV Dry Red 0.75 – 0.90 ↔

2016 Chardonnay 0.85– 1.00 ↑ 2016 Cabernet Sauvignon 1.00 – 1.15 ↑

2016 Sauvignon Blanc 0.90 – 1.05 ↑ 2016 Merlot 0.95 – 1.10 ↑

2016 NZ Marlborough SB NZD3.20 – 4.00 ↔ 2016 Shiraz 1.00 – 1.15 ↑

2016 Pinot Gris 1.20 – 1.35 ↑ 2016 Muscat 0.75 – 0.90 ↔

AU & NZ KEY TAKEAWAYS

Australia’s 2016 harvest came in larger than 2015.

Tonnage prices have increased, particularly on

Chardonnay, Cabernet and Shiraz. The US is

becoming an increasingly lucrative export market.

Ciatti Contacts

Matt Tydeman

Simone George

T. +61 8 8361 9600

Ciatti Global Market Update | August 2016

14

BREXIT UPDATE

For the wine industry, Brexit is causing uncertainty and concern. Pound sterling has devalued, and

this, combined with the fall in UK consumer confidence (see graph below), has led to fears that wine

sales in the UK will suffer.

In the short term, wine suppliers must go about the difficult task of reducing costs so as to avoid –

as much as possible – passing on price increases to the UK consumer. However, producers in many supply

countries – especially South Africa and those in South America where inflation is running high – are already

struggling financially and they will have difficulty finding cost reductions. Consequently, as reported in the

media, the wine industry is being warned to be extra vigilant against unscrupulous practices.

Looking longer term, the wine industry is very concerned that Brexit may result in a hike in UK

import duties. Several important, non-EU exporter countries to the UK market – like Chile and South Africa –

enjoy specific trade agreements with the EU that allow their bulk and bottled wines to enter the bloc

(including the UK) with either reduced or zero import duties levied upon them. For trade between the UK

and the EU – where barriers are currently absent under the Common Market agreement – a deterioration

from preferential treatment is likely. The EU is the largest supplier of wine to the UK: France, Italy and Spain

alone supplied 60% of British imports in 2015. EU suppliers will now most likely redouble their efforts to sell

to alternative markets, such as the US, Russia, China, Japan, etc. Exports into the UK, both from countries

inside and outside the EU, could benefit from new, positive and open trade relations similar to those

currently in place. Presently, though, it is unclear what the new UK trade agreements will look like.

Positives? Well, the UK is yet to trigger Article 50 of the Lisbon Treaty, the formal mechanism for the

commencement of exit negotiations. When they do begin, the negotiations are expected to take two years:

for at least two more years, then, the UK will remain an EU member and benefit from EU trade agreements.

Also, new UK Prime Minister Theresa May has brought calm, waylaying fears of a chaotic transition.

Effect of Brexit on UK consumer confidence

rexit’ onn

Ciatti Global Market Update | August 2016

15

18.5

6.2 6.1 5.4

2.5

0

2

4

6

8

10

12

14

16

18

20

France Australia Spain Chile Italy

Top 5 origin countries of bottled wine imported

into China, 2015 (million 9-litre cases)

Source: IWSR via Wine Intelligence

MARKET FOCUS

CHINA

Despite the relative slowdown in China’s economy, the number of urban upper-middle class

imported wine drinkers in the country has risen by 10 million in just two years to stand at 48 million

people, according to the new ‘China Landscapes 2016’ report from Wine Intelligence.

The report quotes International Wine & Spirits Research (IWSR) who found that consumption of

imported wine in China rose by 37% in 2015 to reach 43.7 million 9-litre cases. “The continued rise in

disposable income, massive growth in e-commerce [the internet has surpassed hypermarkets and

department stores to become the second most popular channel for buying wine], and bilateral trade deals

[reducing import tariffs and helping imported wine sell at reasonable prices] have made imported wine

affordable and accessible to more households across the country,” the report said.

Wine Intelligence also found that consumption frequency among imported wine drinkers has risen:

in March 2016, some 35% of consumers surveyed stated that they drink imported wine on a weekly basis,

up from 23% in March 2015. In addition, a rising proportion of imported wine consumers are trading up,

with the number of consumers spending less than CNY100 (USD15.0) per bottle in the off-trade “seeing a

sharp drop”, and with a “corresponding rise” in those spending CNY200-299 (USD30-45/bottle).

This trend is expected to continue, Wine Intelligence said, because younger drinkers are growing

wealthier and more numerous: over 80% of 18-29 year olds believe that wine is reasonably priced,

compared with 66% of 40-54 year olds. Meanwhile, consumers in lower-tier cities (e.g. Wuhan, Shenyang,

etc.) are at an earlier stage in wine consumption: they are “prestige-seeking traditionalists” whose wine

choices are more risk-averse than consumers in higher-tier cities such as Shanghai and Beijing, placing

more emphasis on traditional-looking labels, for example.

“Overall we are seeing the normalisation of the market and the modernisation of its consumers,”

said Wine Intelligence senior research manager Chuan Zhou. “China will remain one of the world’s most

important markets for imported wine, but the nature of consumption is changing.”

“It is now more

important than ever

for wine businesses to

be highly strategic in

the way they pick their

targets. Taking the

time to implement the

correct strategy will

secure continued

growth and

profitability in the

world’s fifth-largest

wine market.”

Wine Intelligence’s

‘China Landscapes 2016’

report is available to

purchase here

Ciatti Global Market Update | August 2016

16

CRAFT BEER UPDATE

In 2015, for the first time in nearly 50 years,

the US was the biggest hop-growing country

in terms of planted area. Growth of 18% in

2015 and 17% forecasted for 2016 means that

total planted area is 21,600 hectares, about

3,000 hectares more than traditional market

leader, Germany. The Barth Haas Group,

collator of these statistics, put the US acreage

rise down to a “massive increase in the

planting of aroma/flavour varieties” to meet

domestic consumer demand for flavourful IPA

beers; Germany cultivates 32 hop varieties, the

US cultivates 83.

The USDA forecasts that area strung for

harvest in 2016 for Washington, Oregon, and

Idaho is 51,115 acres, 17% more than the 2015

crop of 43,633 acres. Washington, with 37,475

acres for harvest, accounts for 73% of the total.

Receiving some of the crop will be the growing

number of US craft brewers: as of 30 June 2016, a

record high of 4,656 breweries were operating in

the US, an increase of 917 on the prior year.

Approximately 2,200 breweries are in the planning

stage. Craft beer volumes grew by 8% in January-

May 2016, “reflecting the dynamic contributions

from small brewers all across the country,” the US

Brewers Association said. This percentage growth

figures was half that of the first six months of

2015 as the industry “enters a period of

maturation as the base gets larger”.

John Fearless Co. can supply the rapidly growing

number of craft breweries with a highly-

innovative product the company has created and

trademarked. Humuflor is a 100% water-based

hop extract – similar to fruit essences and fruit

aromas – that contains only hop aromas while

omitting the bitterness compounds. The benefits

of Humuflor being water-based are that it is clean,

easy to add, and can be added at whichever stage

of the brewing process the brewer desires –

primarily after the dry hop phase, for example, or

into the brite beer tanks prior to packaging. Beer

can lose some of its hop aroma at the

fermentation stage due to heat: more than simply

adding its own aromas into the beer, Humuflor

enhances the existing ones, boosting the beer’s

overall aroma impact.

Humuflor is already in use at breweries

and feedback has been very positive. This

competitively-priced product is available not only

to US brewers but to brewers across the world. In

this way, the product can bring the exciting US

hop innovation to brewers who lack that

innovation on their own doorsteps.

“The traditional extracts were developed

for the big brewers as a cost-effective and

efficient way of adding hops to beer,” said John

Fearless CEO, Rob Bolch. “Craft brewers have

wanted to move away from how the big guys do

it. Given that Humuflor is 100% water-based, with

no solvents, it’s just hop aromas in water, it has a

massive appeal because it’s pure, with no nasties.”

KEY TAKEAWAY

John Fearless has available aroma and bittering

hop inventory from the US and South Africa,

and can source hops from across the world. It

can assist craft brewers in their long-term

needs for: hops, hop extracts, Humuflor, fruit

purées, juices, concentrates, aged oak barrels.

FEARLESS CONTACT

Rob Bolch, CEO & Partner

T: + 1 800 288 5056

ARGENTINAVintage Variety Trend Vintage Variety Trend

2015 Generic White 0.40 - 0.45 ↑ 2015 Generic Red 0.60 - 0.80 ↑

2015 Generic White (Criolla) 0.35 - 0.38 ↑ 2015 Cabernet Sauvignon 1.30 - 1.50 ↑

2015 Chardonnay 0.90 - 1.20 ↑ 2015 Malbec Entry-Level 1.30 - 1.50 ↑

2015 Torrontes 0.60 - 1.00 ↑ 2015 Malbec Mid-Level 0.00 - 0.00 ↑

2015 Sauvignon Blanc 0.90 - 1.00 ↑ 2015 Malbec Premium 1.50 + ↑

2015 Muscat 0.40 - 0.45 ↑ 2015 Syrah / Merlot 1.00 - 1.20 ↑

2015 Bonarda 0.00 - 1.20 ↑ 2015 Tempranillo 0.00 - 0.00 ↑

Vintage Variety Trend Vintage Variety Trend

NV Dry White 0.46 - 0.58 ↔ NV Dry Red 0.58 - 0.69 ↔

2016 Chardonnay 0.66 - 0.77 ↑ 2016 Cabernet Sauvignon 0.77 - 0.89 ↑

2016 Sauvignon Blanc 0.69 - 0.81 ↑ 2016 Merlot 0.00 - 0.00 ↑

2015 NZ Marlborough SB 2.32 - 2.90 ↔ 2016 Shiraz 0.77 - 0.89 ↑

2016 Pinot Gris 0.93 - 1.04 ↑ 2016 Muscat 0.58 - 0.69 ↔

AUD Rate: 0.771344 NZD Rate: 0.724596

CALIFORNIAVintage Variety Trend Vintage Variety Trend

2014 Generic White 0.60 - 0.80 ↔ 2014 Generic Red 0.80 - 1.05 ↓

2014 Chardonnay 1.45 - 1.88 ↑ 2013/2014 Cabernet Sauvignon 1.58 - 2.11 ↑

2014 Pinot Grigio 1.58 - 1.98 ↔ 2014 Merlot 1.18 - 1.58 ↔

2014 Muscat 0.92 - 1.32 ↓ 2014 Pinot Noir 1.85 - 2.25 ↑

2014 White Zinfandel 0.85 - 0.99 ↔ 2014 Syrah 1.18 - 1.58 ↔

2014 Colombard 0.73 - 0.99 ↔ 2013/2014 Zinfandel 1.72 - 2.11 ↑

CHILEVintage Variety Trend Vintage Variety Trend

NV Generic White 0.55 - 0.60 ↑ NV Generic Red 0.55 - 0.60 ↑

2015 Chardonnay 0.80 - 1.00 ↑ 2015 Cabernet Sauvignon (Basic) 0.78 - 0.95 ↑

2015 Chardonnay (Varietal Plus) 1.10 - 1.25 ↑ 2015 Cabernet Sauvignon 1.00 - 1.50 ↑

2015 Sauvignon Blanc 0.70 - 1.10 ↑ 2014/2015 Cabernet Sauvignon

(High Quality)NA - NA ↑

2015 Pinot Noir 1.80 - 2.50 ↑ 2015 Merlot 0.78 - 0.95 ↑

2015 Syrah 0.85 - 0.95 ↑ 2015 Malbec NA - NA ↑

2015 Carmenere 0.78 - 1.05 ↑ 2015 Malbec (Varietal Plus) NA - NA ↑

AUSTRALIA & NEW ZEALAND

Export Pricing: USD per liter

Currency Conversion Rates as of August 11, 2016

Price Price

Pricing in bulk; FCA

Price Price

Price Price

Price Price

Pricing in bulk; FOB Chilean Port

Pricing in bulk; FCA

FRANCEVintage Variety Trend Vintage Variety Trend

2015 Generic White 0.56 - 0.67 ↓ 2015 Generic Red 0.61 - 0.67 ↓

2015 Chardonnay IGP 1.06 - 1.17 ↓ 2015 Cabernet Sauvignon IGP 0.95 - 1.00 ↓

2015 Chardonnay VDF 1.06 - 1.17 ↓ 2015 Cabernet Sauvignon VDF 0.95 - 1.06 ↔

2015 Sauvignon Blanc IGP 1.06 - 1.23 ↔ 2015 Merlot IGP 0.89 - 0.95 ↓

2015 Sauvignon Blanc VDF 1.06 - 1.23 ↔ 2015 Merlot VDF 0.00 - 0.00 ↓

2015 Generic Rosé IGP 0.61 - 0.67 ↓ 2015 Red Syrah / Grenache IGP 1.03 - 1.12 ↓

2015 Generic Rosé VDF 0.61 - 0.67 ↓

2015 Varietal Rosé IGP 0.89 - 0.95 ↓

Rate: 1.116510

GERMANYVintage Variety Trend Vintage Variety Trend

2014/2015 White Wine 0.67 - 0.78 ↔ 2014/2015 Red Wine 0.73 - 0.89 ↔

2014/2015 Pinot Grigio 1.06 - 1.34 ↔ 2014/2015 Dornfelder 1.06 - 1.17 ↔

2014/2015 Riesling 1.06 - 1.34 ↔ 2014/2015 Pinot Noir 0.95 - 1.12 ↔

Rate: 1.116510

ITALY

Vintage Variety Trend Vintage Variety Trend

2015 Generic White 0.36 - 0.39 ↔ 2015 Generic Red 0.36 - 0.39 ↔

2015 Chardonnay 0.67 - 0.95 ↔ 2015 Cabernet Sauvignon 0.67 - 0.89 ↔

2015 Pinot Grigio 1.17 - 1.28 ↔ 2015 Merlot 0.61 - 0.84 ↔

2015 Prosecco 2.79 - 2.90 ↔ 2015 Chianti 1.73 - 2.01 ↔

Rate: 1.116510

SOUTH AFRICAVintage Variety Trend Vintage Variety Trend

2015/2016 Generic White 0.37 - 0.40 ↑ 2015/2016 Generic Red 0.44 - 0.50 ↔

2015/2016 Chardonnay 0.50 - 0.59 ↑ 2015/2016 Cabernet Sauvignon 0.53 - 0.64 ↑

2015/2016 Sauvignon Blanc 0.51 - 0.64 ↑ 2015/2016 Ruby Cabernet 0.45 - 0.49 ↔

2015/2016 Chenin Blanc 0.40 - 0.47 ↑ 2015/2016 Merlot 0.51 - 0.60 ↔

2015/2016 Muscat 0.43 - 0.48 ↔ 2015/2016 Pinotage 0.50 - 0.56 ↔

2015/2016 Generic Rosé 0.37 - 0.45 ↔ 2015/2016 Shiraz 0.52 - 0.62 ↔

2015/2016 Cultivar Rosé 0.43 - 0.50 ↔ 2015/2016 Cinsaut 0.45 - 0.47 ↔

Rate: 0.075058

SPAINVintage Variety Trend Vintage Variety Trend

2015 Generic White 0.28 - 0.39 ↔ 2015 Generic Red 0.31 - 0.39 ↔

2015White Blends

(Higher Quality)0.45 - 0.67 ↔ 2015

Generic Red

(Higher Quality)0.39 - 0.56 ↔

2015 Sauvignon Blanc 0.58 - 0.63 ↔ 2015 Cabernet Sauvignon 0.56 - 0.73 ↔

2015 Chardonnay 0.67 - 0.73 ↔ 2015 Merlot 0.00 - 0.00 ↔

2015 Generic Rosé 0.31 - 0.42 ↔ 2015 Tempranillo 0.45 - 0.67 ↔

2015 Varietal Rosé 0.45 0.56 ↔ 2015 Syrah 0.50 - 0.67 ↔

2015 Moscatel 0.45 - 0.67 ↔

Rate: 1.116510

Pricing in bulk; FOB Cape Town

Pricing in bulk; Ex-Winery

Pricing in bulk; Ex-Winery

Pricing in bulk; Ex-Winery

Pricing in bulk; Ex-Winery

Price Price

Price Price

Price Price

Price Price

Price Price

Ciatti Global Market Update | August 2016

17

CONTACT US

ARGENTINA Eduardo Conill

T. +54 261 420 3434 E. [email protected]

AUSTRALIA / NEW ZEALAND

Matt Tydeman Simone George

T. +61 8 8361 9600 E. [email protected]

CALIFORNIA – IMPORT / EXPORT CEO – Greg Livengood

Steve Dorfman T. +415 458-5150

E. [email protected] E. [email protected]

CALIFORNIA – DOMESTIC

T. +415 458-5150 John Ciatti – [email protected]

Glenn Proctor – [email protected] John White – [email protected] Chris Welch – [email protected]

CONCENTRATE

Greg MaGill T. 559 977 4040

CANADA & US CLIENTS OUTSIDE OF CALIFORNIA

Dennis Schrapp T. 905/354-7878

CHILE Marco Adam

T. +56 2 2363 9206 or T. +56 2 2363 9207

CHINA/ASIA PACIFIC Simone George

T. +61 8 8361 9600 E. [email protected]

FRANCE/ITALY Florian Ceschi

T. +33 4 67 913532 E. [email protected]

GERMANY

Christian Jungbluth T. +49 6531 9734 555 E. [email protected]

SPAIN

Nicolas Pacouil T. +33 4 67 913531 E. [email protected]

UK / SCANDINAVIA / HOLLAND

Catherine Mendoza T. +33 4 67 913533

SOUTH AFRICA Vic Gentis

T. +27 21 880 2515 E: [email protected]

-or- Petrè Morkel

T. +27 82 33 88 123 E. [email protected]

JOHN FEARLESS CO. CRAFT HOPS & PROVISIONS

CEO - Rob Bolch T. + 1 800 288 5056