Global Life Actuarial INTERNAL USE ONLY ASSAL-IAIS Training Seminar: Risk Margin in the Swiss...

23

Global Life Actuarial INTERNAL USE ONLY ASSAL-IAIS Training Seminar: Risk Margin in the Swiss Solvency Test 22nd November 2012 Alex Summers

-

Upload

janis-booker -

Category

Documents

-

view

217 -

download

2

Transcript of Global Life Actuarial INTERNAL USE ONLY ASSAL-IAIS Training Seminar: Risk Margin in the Swiss...

Global Life Actuarial

INTERNAL USE ONLY

ASSAL-IAIS Training Seminar: Risk Margin in the Swiss Solvency Test

22nd November 2012Alex Summers

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 2

Important note

The views expressed in this presentation are the presenter’s own and do not necessarily represent the views of either Zurich Insurance Group (Zurich), or FINMA

I am very grateful to colleagues within Zurich and at FINMA for their assistance in preparation

Further information from FINMA on the Swiss Solvency Test can be found on FINMA’s website at http://www.finma.ch

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 3

Agenda

Purpose and relevance of the SST risk margin

Key principles and conceptual framework

Calculation including simplifications

Comparison against alternative approaches

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 4

The risk margin helps SST protect policyholders by giving a high probability of orderly run-off of the business

SST identifies insurers* at risk of being unable to honour their existing obligations

A ladder of intervention allows appropriate actions to be taken when insurers run into difficulties

SST sets capital requirements so that there is high probability after one year of

1. Still being solvent (Expected shortfall SCR)2. Having enough capital to fund future SCRs

over the life time of the business (Risk margin)

Risk margin should thus give just enough capital to allow orderly run-off of the business, whether internally or via transfer of liabilities to a third party if necessary

Both fulfilment and transfer value concepts are relevant for risk margin in the SST

Risk Total required 0 margin capital

SST ladder of intervention

Based on FINMA SST technical document p8

*: The term “Insurers” has been used throughout to indicate both insurance and reinsurance undertakings

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 5

Overview of risk margin in the SST

Risk margin is the extra amount needed above best estimate of liabilities to cover the cost of supporting risks the liabilities bring

Non-hedgeable risks only

Present value of opportunity cost of regulatory capital needed to support risks over the lifetime of the liabilities

Simplifications are needed in practice

SST risk margin is similar in nature to Solvency II risk marginDetails differ slightly

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 6

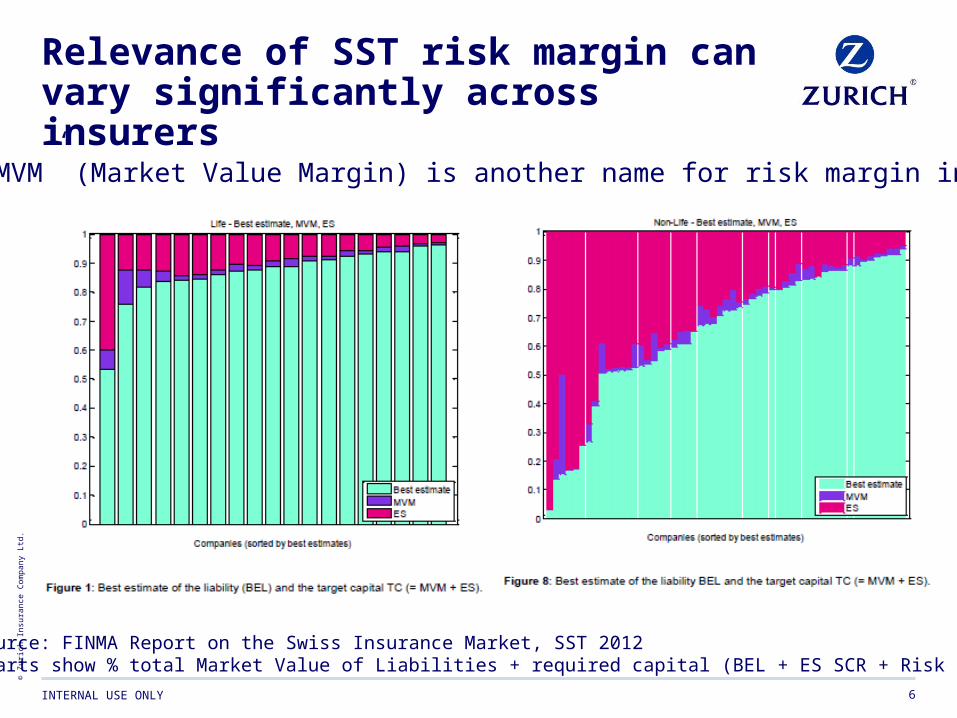

Relevance of SST risk margin can vary significantly across insurers

Source: FINMA Report on the Swiss Insurance Market, SST 2012Charts show % total Market Value of Liabilities + required capital (BEL + ES SCR + Risk Margin)

“MVM” (Market Value Margin) is another name for risk margin in SST

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 7

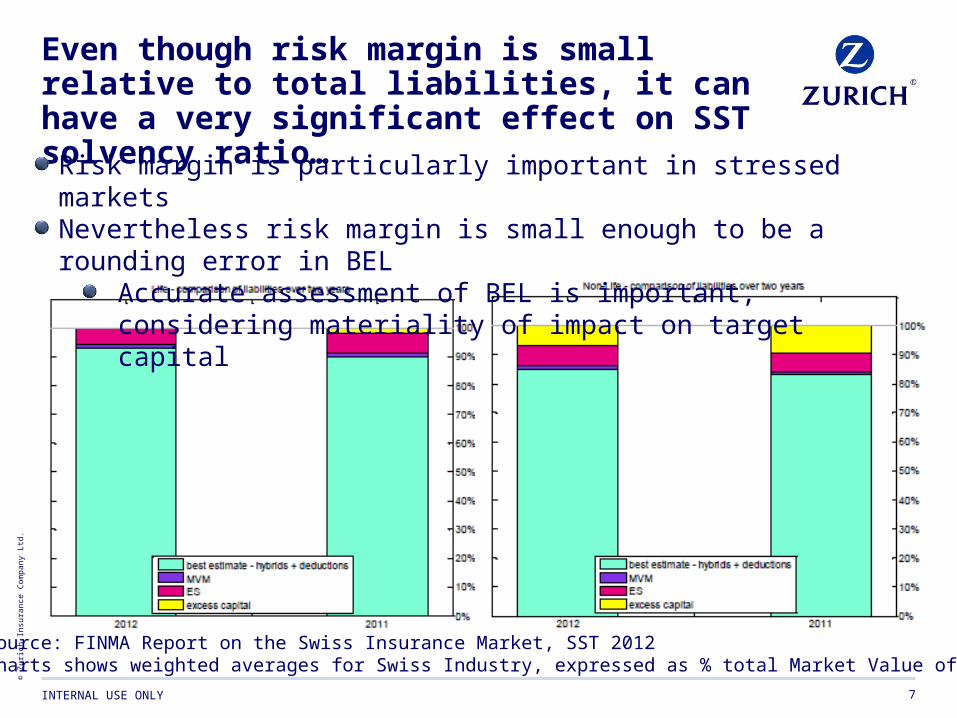

Even though risk margin is small relative to total liabilities, it can have a very significant effect on SST solvency ratio…

Source: FINMA Report on the Swiss Insurance Market, SST 2012Charts shows weighted averages for Swiss Industry, expressed as % total Market Value of Assets

Risk margin is particularly important in stressed marketsNevertheless risk margin is small enough to be a rounding error in BEL

Accurate assessment of BEL is important, considering materiality of impact on target capital

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 8

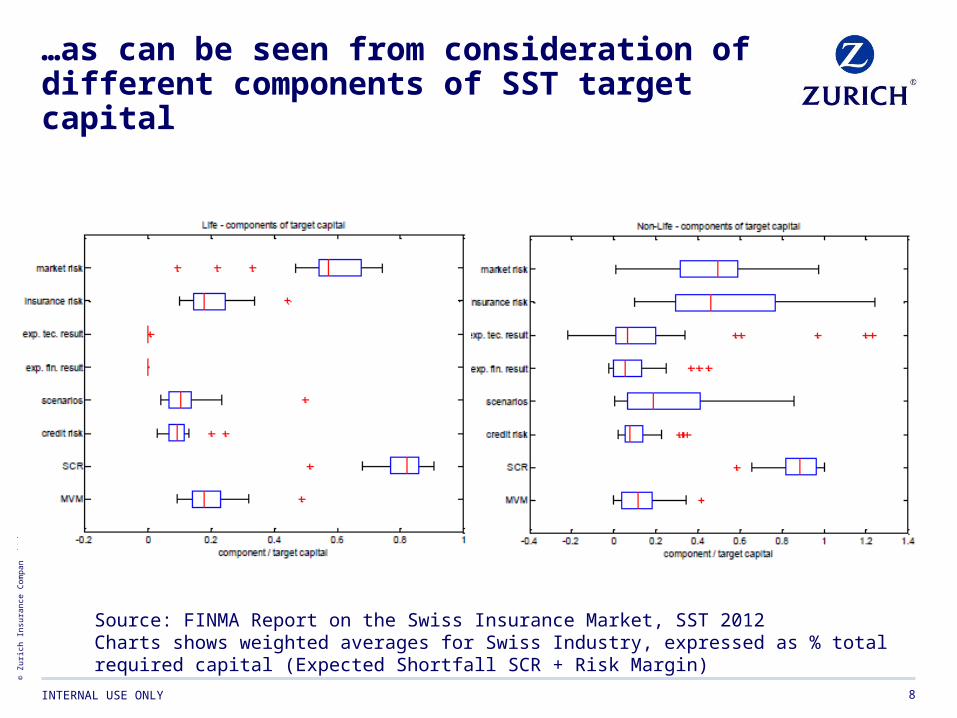

…as can be seen from consideration of different components of SST target capital

Source: FINMA Report on the Swiss Insurance Market, SST 2012Charts shows weighted averages for Swiss Industry, expressed as % total required capital (Expected Shortfall SCR + Risk Margin)

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 9

Agenda

Purpose and relevance of the SST risk margin

Key principles and conceptual framework

Calculation including simplifications

Comparison against alternative approaches

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 10

The SST risk margin is the expected amount of capital needed today to be able to support regulatory capital requirements over the lifetime of the business

1

1,1,,0t

ttcapital Requiredttcapital of Costtfactor Discountmargin Risk

1

1,,0%6t

ttcapital Requiredtfactor Discountmargin Risk

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 11

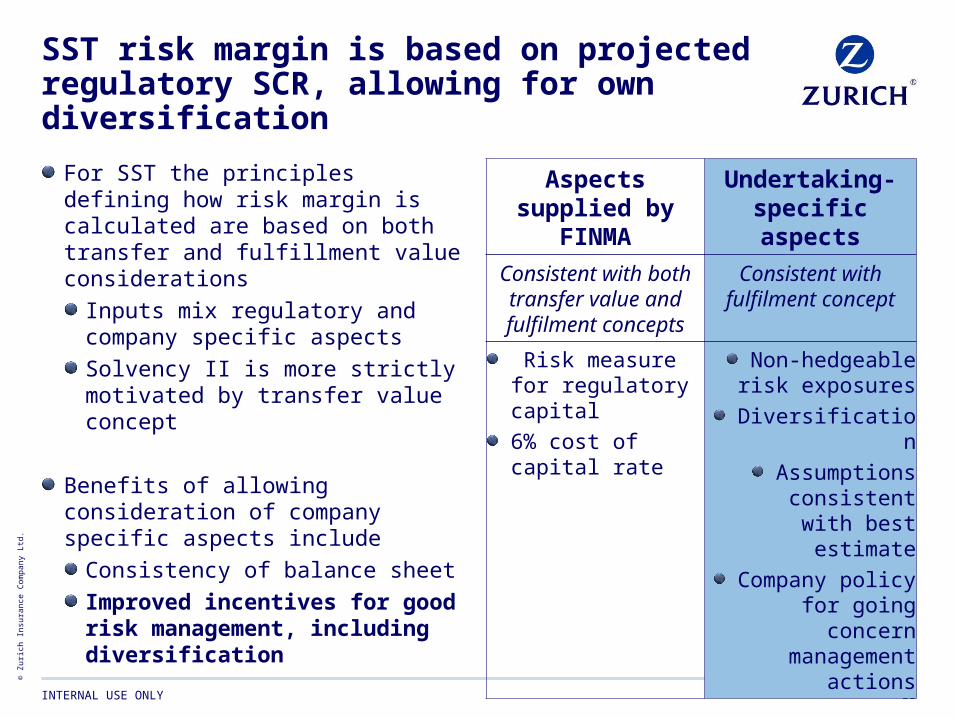

SST risk margin is based on projected regulatory SCR, allowing for own diversification

For SST the principles defining how risk margin is calculated are based on both transfer and fulfillment value considerations

Inputs mix regulatory and company specific aspectsSolvency II is more strictly motivated by transfer value concept

Benefits of allowing consideration of company specific aspects include

Consistency of balance sheetImproved incentives for good risk management, including diversification

Aspects supplied by

FINMA

Undertaking-specific aspects

Consistent with both transfer value and fulfilment concepts

Consistent with fulfilment concept

Risk measure for regulatory capital6% cost of capital rate

Non-hedgeable risk exposuresDiversification

Assumptions consistent with

best estimateCompany policy

for going concern management

actions

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 12

Only non-hedgeable risks need to be considered in SST risk margin

Practical policyholder protection

Theoretical robustness

Relevance of risk margin increases in a stressed solvency position

Considering non-hedgeable risks only is consistent with possible outcomes under ladder of intervention

Good value safeguarding industry competitiveness: minimum needed for policyholder protection

In market consistent framework, only compensated for risks that can’t be hedged or diversified

Consistent with view of total market value of liabilities as corresponding to value of an optimal replicating portfolio

No double counting

No penalty for market risk associated with free surplus

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 13

SST risk margin is consistent with other elements of the balance sheet, and required capital

Same assumptions should be used for valuing risk margin and best estimate discounted liabilities

In particular there should be a consistency of assumptions pertaining to

Own business policiesSettling own portfolioDiversificationOwn expense riskClient behaviour

This prevents distortions from artificial shortening of run-off period through inconsistencies in lapse assumptions, or assumption of aggressive run-off rather than treatment as a going concern

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 14

6% Cost of Capital rate corresponds to BBB credit rating

Derived considering opportunity cost of capital in excess of risk-freeSteady “through the cycle” assumption

BBB credit rating consistent with 99% Expected Shortfall risk measureHigher credit rating would give lower CoC rate, offsetting higher SCR

Using the same 6% rate for all insurers is consistent with a transfer value concept

Disproportionate effort for each company to calibrate a specific rate

Using same rate for all improves transparency

Other rates can be used e.g. lower rates used for MCEV Cost of Residual Non-Hedgeable Risks

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 15

Company-specific diversification is a key advantage of SST risk margin

Allowing for company-specific diversification recognises that diversification is at the heart of good risk management practice for insurance

So it’s not a disadvantage that company-specific diversification leads to a different “market” value of liabilities for different insurers

Consistent with fulfilment value conceptHopefully this should be more often relevant than transfer value!

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 16

Agenda

Purpose and relevance of the SST risk margin

Key principles and conceptual framework

Calculation including simplifications

Comparison against alternative approaches

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 17

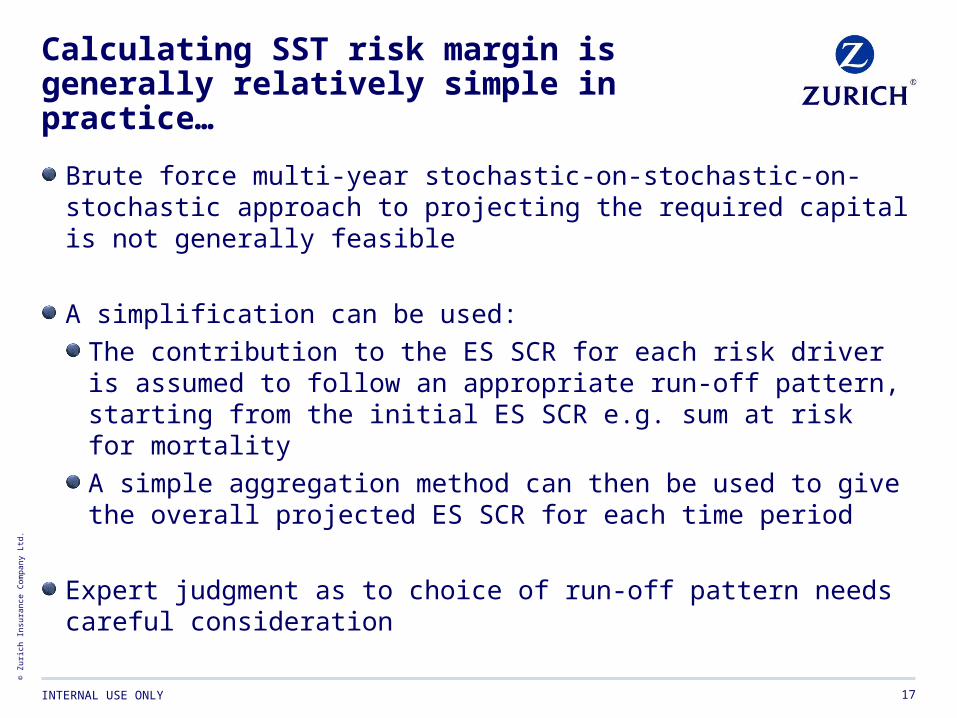

Calculating SST risk margin is generally relatively simple in practice…

Brute force multi-year stochastic-on-stochastic-on-stochastic approach to projecting the required capital is not generally feasible

A simplification can be used:The contribution to the ES SCR for each risk driver is assumed to follow an appropriate run-off pattern, starting from the initial ES SCR e.g. sum at risk for mortalityA simple aggregation method can then be used to give the overall projected ES SCR for each time period

Expert judgment as to choice of run-off pattern needs careful consideration

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 18

… although distinguishing non-hedgeable component of market risks can be a challenge

Non-hedgeable risks relate to components of the liabilities for which there is no liquid market

Expert judgment is needed in determining an optimal replicating portfolio

Good documentation needed

Non-market risks are often not hedgeable at low cost

However if replicating portfolios used for Internal Models, these can also be set up to consider only candidate assets for which there is a liquid market

Comparison with full “theoretical candidate asset” replicating portfolio across many real world scenarios can then inform estimate of non-hedgeable proportion of market risk

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 19

Agenda

Purpose and relevance of the SST risk margin

Key principles and conceptual framework

Calculation including simplifications

Comparison against alternative approaches

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 20

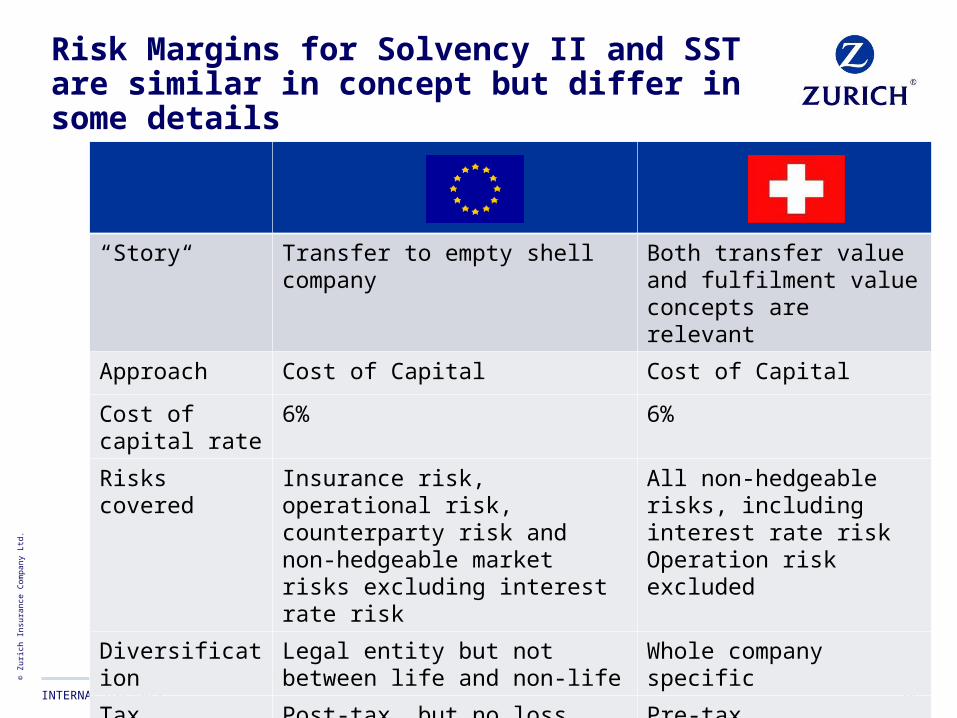

Risk Margins for Solvency II and SST are similar in concept but differ in some details

“Story“ Transfer to empty shell company

Both transfer value and fulfilment value concepts are relevant

Approach Cost of Capital Cost of Capital

Cost of capital rate

6% 6%

Risks covered Insurance risk, operational risk, counterparty risk and non-hedgeable market risks excluding interest rate risk

All non-hedgeable risks, including interest rate riskOperation risk excluded

Diversification Legal entity but not between life and non-life

Whole company specific

Tax Post-tax, but no loss absorbency of deferred taxes

Pre-tax

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 21

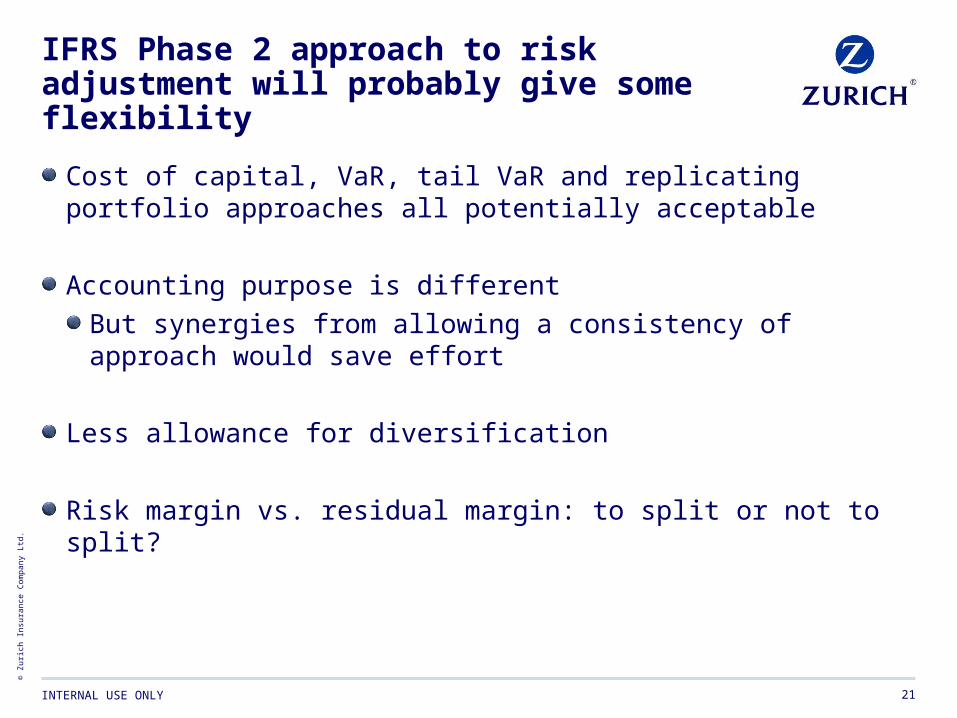

IFRS Phase 2 approach to risk adjustment will probably give some flexibility

Cost of capital, VaR, tail VaR and replicating portfolio approaches all potentially acceptable

Accounting purpose is differentBut synergies from allowing a consistency of approach would save effort

Less allowance for diversification

Risk margin vs. residual margin: to split or not to split?

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 22

Overview of risk margin in the SST

Risk margin is the extra amount needed above best estimate of liabilities to cover the risks the liabilities bring

Non-hedgeable risks only

Present value of opportunity cost of regulatory capital needed to support risks over the lifetime of the liabilities

Relevant for both transfer and fulfilment value concepts

Simplifications are needed in practice

SST risk margin is similar in nature to Solvency II risk marginDetails differ slightly

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 23

Thank you for your attention

Any further questions?