Global income changes: effects on export opportunities for developing countries Jörg Mayer Division...

17

Global income changes: effects on export opportunities for developing countries Jörg Mayer Division on Globalisation and Development Strategies UNCTAD UNCTAD Training Course on Key Issues on the International Economic Agenda Global income and trade trends: Implications for export opportunities for developing countries Geneva, 7 March 2013

-

Upload

francis-oconnor -

Category

Documents

-

view

214 -

download

0

Transcript of Global income changes: effects on export opportunities for developing countries Jörg Mayer Division...

Global income changes: effects on export

opportunities for developing countries

Jörg MayerDivision on Globalisation and Development Strategies

UNCTAD

UNCTAD Training Course onKey Issues on the International Economic Agenda

Global income and trade trends: Implications for export opportunities for developing

countries

Geneva, 7 March 2013

Main points – diagnosis• What happened? Onset of current crisis led

to global trade collapse with ensuing loss of dynamism in consumer goods imports by the US

• Why is this important?– US-consumption was a key driver of global growth

in pre-crisis period

– The growth slowdown in advanced economies is unlikely to be a temporary phenomenon

– Crisis transmission through trade channel affects products whose exports to developed countries boosted developing country growth prior to the crisis and that have historically supported productive transformation

Main points – response

• What to do? Develop domestic and South-South markets to compensate for loss of export potential to advanced economies

• Is demand in developing countries large enough to compensate for lower demand growth in developed countries? In some sectors, demand in the large emerging economies is likely to exceed that in developed countries within the coming 10–15 years

• Policy implications? Pursue macroeconomic, trade and industrial policies that allow creating employment and purchasing power – to support demand – and expanding productive capacity – to benefit from arising market opportunities

Overview

1. The great trade collapse – evidence for selected product categories

3. Potential growth of consumer demand in developing countries

4. Policy considerations

5. Conclusions

1. The global trade collapse in 2008–2009

• The sharp, sudden and synchronized fall in trade in 2008–09 is striking because real world trade fell by about 15%, exceeding the fall of real world GDP roughly by a factor of 4

• Changes in real final expenditure bear main responsibility

• Reasons for large size of impact: high import content of exports (GVCs) and high import content of household consumption in developed countries, especially the US

• The widely expected slow recovery towards a weak growth path in advanced economies is reducing the opportunities to export to these countries beyond the short term, during which developing countries might compensate resulting potential growth shortfalls by countercyclical macroeconomic policies

The impact of the global trade collapse varied considerably across individual economies,

depending on their pattern of export specialization

The price and volume effects of the global trade collapse in 2008–09, selected developing economies, trade shock as a percent of GDP

Economies with more than 40 per cent of exports in the manufacturing sector

-35 -25 -15 -5 5

Singapore

Hong Kong SAR of China

Malaysia

Viet Nam

Taiwan Province of China

Cambodia

Thailand

Mexico

China

Tunisia

Demand effect ToT effect

Economies with more than 40 per centof exports in the energy sector

-35 -25 -15 -5 5

Brunei Darussalam

Bahrain

Iraq

Gabon

Saudi Arabia

Trinidad and Tobago

Kuwait

Oman

Qatar

Algeria

Demand effect ToT effect

US-imports of consumer goods lost pre-crisis dynamism

Consumer goods imports, United States, 1999 I – 2012 III, $bn

0

20

40

60

80

100

120

140

160

99-I

00-I

01-I

02-I

03-I

04-I

05-I

06-I

07-I

08-I

09-I

10-I

11-I

12-I

Automotive vehicles, parts, and engines

Consumer goods (nonfood), except automotive

Linear (trend 1999 I – 2008 II): automotive vehicles, parts, and engines)

Linear (trend 1999 I – 2008 II): consumer goods (nonfood), except automotive)

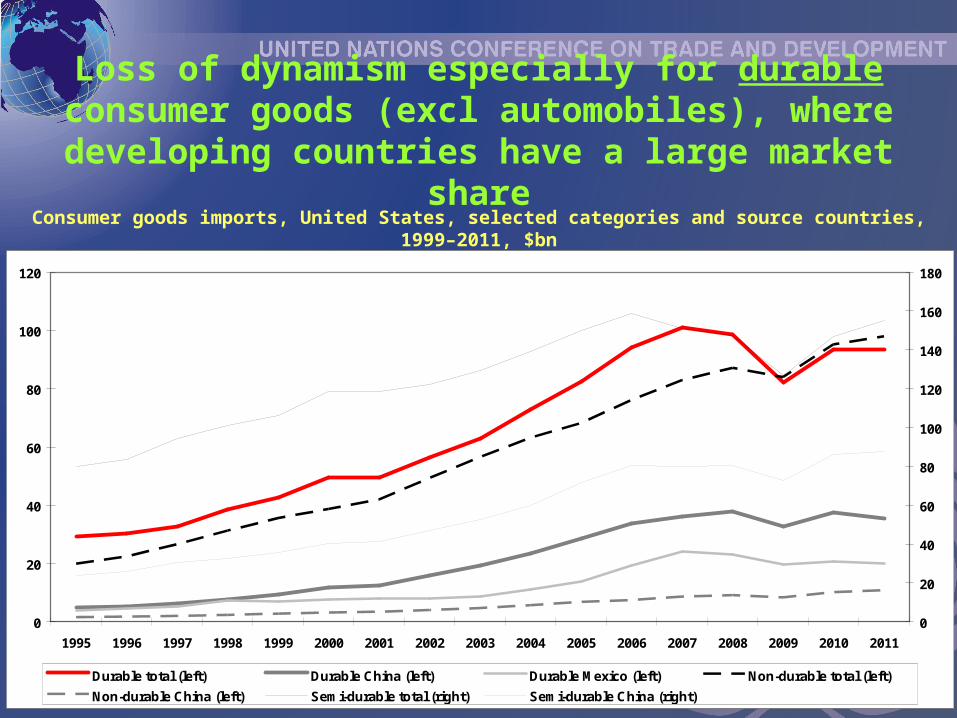

Loss of dynamism especially for durable consumer goods (excl automobiles), where

developing countries have a large market shareConsumer goods imports, United States, selected categories and source countries,

1999–2011, $bn

0

20

40

60

80

100

120

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

0

20

40

60

80

100

120

140

160

180

Durable total (left) Durable China (left) Durable Mexico (left) Non-durable total (left)

Non-durable China (left) Semi-durable total (right) Semi-durable China (right)

2. Potential growth of consumer demand in developing countries

• The potential growth of consumer demand in developing countries depends on five variables:

– Income elasticity of demand– Export orientation– Income distribution– Per-capita income growth– Demographic developments

• Simulations indicate that, in some sectors, demand in large emerging economies will exceed that in developed countries within the coming 10–15 years

Demand for consumer goods goes through periods of acceleration and deceleration – rapidly growing

developing countries are in acceleration phaseRelationship between per capita income and income elasticity of demand, selected consumer

good categories

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

0 10000 20000 30000 40000 50000 60000 70000

Per capita income (constant 2005 international dollars)

Inc

om

e el

asti

city

(cr

oss

-co

un

try

aver

ag

es;

77

cou

ntr

ies;

19

90–2

011)

Durables Semi-durables Food and non-alcoholic beverages

Services United States China

Brazil India Indonesia

Germany Japan

India Indon-esia

China

Brazil

JapanGermany

United States

Country-specific positions and movements relative to the cross-country benchmark are related to the

importance of consumption and exports in aggregate demandRelationship between per capita income and expenditure on durable consumer goods, selected

economies, ‘90–‘11

0

500

1000

1500

2000

2500

3000

3500

4000

4500

0 5000 10000 15000 20000 25000 30000 35000 40000 45000

Per capita income (ourchasing power in 2005 prices)

Ex

pe

nd

itu

re o

n d

ura

ble

co

ns

um

er

go

od

s,

co

ns

tan

t U

S d

oll

ars

in

20

11

pri

ce

s

United States

Germany

Japan

Indo-nesia

Brazil

Chile

China

Taiwan Province of China

Rep of Korea

Czech Republic

Income distribution affects the number of people that belong to the

middle classPer capita income and different income classes, selected countries, 2005

2.5

3.0

3.5

4.0

4.5

5.0

5.5

0 1 2 3 4 5 6 7 8 9 10

Country decile

Lo

g o

f p

er c

apit

a in

com

e (p

urc

has

ing

po

we

r p

arit

y in

20

05

pri

ces)

India

China

Brazil

United States

Russian Fed

Nigeria

Indonesia

Per-capita expenditure on durable consumer goods in some developing and transition economies may overtake that in the United States within a decade

or twoProjections based on assumed growth rates, 2011–2050

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

2011 2013 2015 2017 2019 2021 2023 2025 2027 2029 2031 2033 2035 2037 2039 2041 2043 2045 2047 2049

Per capita income (purchasing power parity in 2005 prices)

Co

ns

tan

t d

ollars

in

20

11 p

ric

es

India China US Brazil Russian Federation

3. Policy considerations• Demand potential in developing

countries provides sizeable opportunities for development of productive capacity and boost productive transformation, driven by fixed investment

• Wage and employment policies must ensure sufficient growth of domestic purchasing power to create middle class

• Macroeconomic, trade and industrial policies must ensure that domestic firms meet emerging demand

Why developing country enterprises may be well placed to meet newly

arising demand• MNEs used “their existing high-end products and

services through standard distribution channels to target the most affluent tier of customers in the largest cities” (Boston Consulting Group)

• Due to differences in consumer tastes etc., proximity to markets is important when targeting less affluent consumers – path of innovation

• Developing country firms can develop less material- and energy-intensive consumer goods, which may not match existing technologies or appeal to Western consumers, and preserve their environment – green industrial policies

4. Conclusions• Policies in developed economies should strive for

sustained rapid growth and refrain from protectionism

• Yet, the two-speed world economy makes export-led growth strategies less viable in developing countries

• Greater importance of domestic consumption in developing countries lowers the per capita income of the median global consumer with attendant changes in the composition of demand

• Developing country enterprises may be well placed to meet newly arising demand

• Not all developing countries can easily change their production structure to match the emerging domestic demand structure – international trade remains important