Global Forum for Disaster Reduction (GFDR) A Seminar on Business Continuity Management November 28,...

32

Global Forum for Disaster Reduction (GFDR) A Seminar on Business Continuity Management November 28, 2007, Mumbai MANAGING RISKS --- A Step towards better Corporate Governance Paper presented by: Khushroo B. Panthaky --- Partner, Walker Chandiok & Co

-

Upload

mildred-wilkerson -

Category

Documents

-

view

213 -

download

0

Transcript of Global Forum for Disaster Reduction (GFDR) A Seminar on Business Continuity Management November 28,...

Global Forum for Disaster Reduction (GFDR)A Seminar on Business Continuity Management

November 28, 2007, Mumbai

MANAGING RISKS ---

A Step towards better Corporate Governance

Paper presented by: Khushroo B. Panthaky

--- Partner, Walker Chandiok & Co (A Member firm of Grant Thornton International)

Agenda

• Section I Conceptualizing Corporate Governance

• Section II The Need for Corporate Governance

• Section III Evolution of Corporate Governance

• Section IV Clause 49 of the Listing Agreement

• Section V Issues and Challenges in India

• Section VI Advantages of a well developed Corporate Governance framework

• Section VII Proposed Amendments

Walker, Chandiok & CoNovember 28, 2007

Slide 3 Corporate Governance

Conceptualizing Corporate Governance

Section I

Narrow definition

• A set of relationships between the company and shareholders, directors and management.

• Beneficiary of good governance - The Shareholders

Broad definition

• Looking to the implicit and explicit relationships of the company with employees, creditors, consumers, distributors, Govt. Authorities and local communities

• Beneficiary of good governance - Every Stakeholder

Walker, Chandiok & CoNovember 28, 2007

Slide 4 Corporate Governance

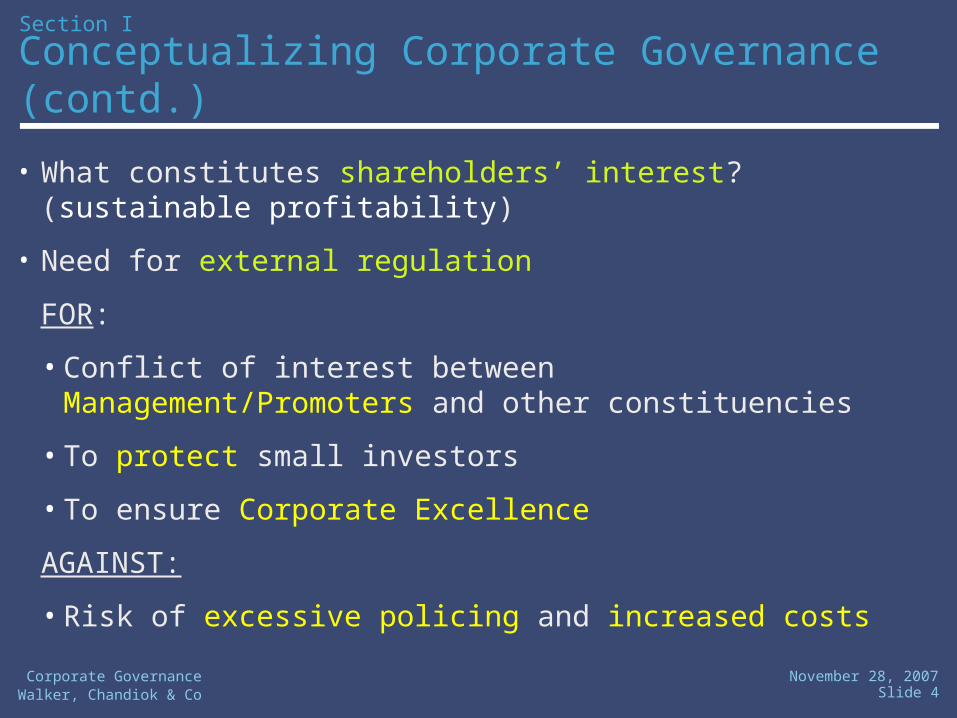

Conceptualizing Corporate Governance (contd.)

Section I

• What constitutes shareholders’ interest? (sustainable profitability)

• Need for external regulation

FOR:

• Conflict of interest between Management/Promoters and other constituencies

• To protect small investors

• To ensure Corporate Excellence

AGAINST:

• Risk of excessive policing and increased costs

Khushroo B. Panthaky

Walker, Chandiok & CoNovember 28, 2007

Slide 5 Corporate Governance

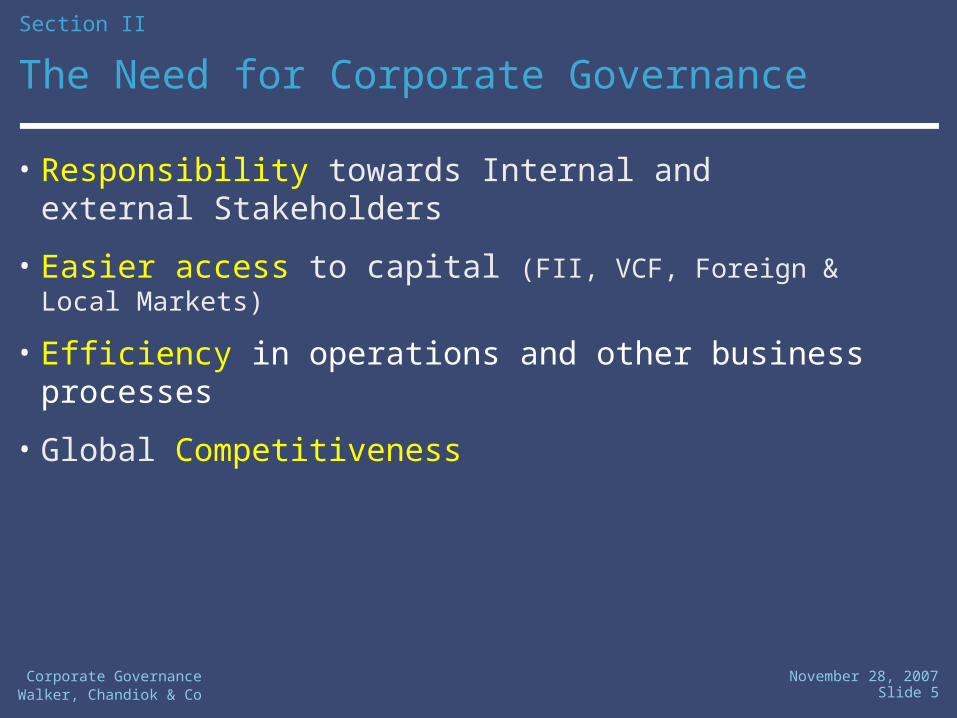

The Need for Corporate Governance

Section II

• Responsibility towards Internal and external Stakeholders

• Easier access to capital (FII, VCF, Foreign & Local Markets)

• Efficiency in operations and other business processes

• Global Competitiveness

Walker, Chandiok & CoNovember 28, 2007

Slide 6 Corporate Governance

The Evolution of Corporate Governance - Abroad

Section III

• Spate of high profile corporate frauds and collapses in the U.S sparked off the debate by investors and financial institutions on the need to protect their investments through regulations on Corporate Governance.

• The UK published the ‘Code of Best Practices’ in Corporate Governance in 1992 and it culminated in the Turnbull Guidelines in September,1999.

• The Sarbanes Oxley legislation was introduced in the U.S in July,2002.

• Other legislations on Corporate Governance were introduced in many countries.

Walker, Chandiok & CoNovember 28, 2007

Slide 7 Corporate Governance

The Evolution of Corporate Governance - India

Section III

• In India ‘Corporate Governance’ is still a catching up terrain.

• December 1995: CII sets up task force to design voluntary code of corporate governance

• April 1998: CII releases “Desirable Corporate Governance: A Code”

• May 1999: SEBI sets up the Kumar Mangalam Birla Committee

• February 2000: Clause 49 introduced pursuant to KM Birla Report

• Key aspects of financial disclosures,independence of boards etc were picked up from the Sarbanes Oxley Act.

• 2002: DCA sets up Naresh Chandra Committee- Report recommends financial and non-financial disclosures and independent auditing and board oversight of management

Walker, Chandiok & CoNovember 28, 2007

Slide 8 Corporate Governance

Section III

• 2002: Narayana Murthy Committee set up by SEBI to review clause 49

• 2003: Clause 49 modified to reflect some of Narayana Murthy’s recommendations

• December, 2005: Deadline for compliance with modified Clause 49

• The reporting is quarterly and starts from 15th April, 2006 for the period January to March, 2006.

• Amendments made to Clause 49 requirements from time to time

The Evolution of Corporate Governance – India (contd.)

Walker, Chandiok & CoNovember 28, 2007

Slide 9 Corporate Governance

Clause 49 of the Listing Agreement – Scope

Section IV

• The structuring of Boards e.g the ratio of Independent Directors and mandating its responsibilities .

• Board procedures and constitution of different committees like the audit committee, shareholders' grievances committee etc.

• Enhancing shareholder participation and protection of shareholders' interest through mandatory committees.

• Disclosure of financial information and institutionalizing Risk Management and Internal Control Frameworks - CEO and CFO made responsible for financials.

• Escalating legal compliance responsibilities to the Board

• An optional whistle blowers policy.

Walker, Chandiok & CoNovember 28, 2007

Slide 10 Corporate Governance

Clause 49 of the Listing Agreement

Section IV

Concerned with Independent Directors, Audit Committees, Disclosures, CEO/CFO Certification

Independent Directors

• Half of Board with executive Chairman to be independent; third of board with non executive Chairman to be independent.

• Definition of independent director:

Non executive

No Material pecuniary relationships or transactions with company, promoters, directors, senior management, holding company, subsidiaries or associates

Walker, Chandiok & CoNovember 28, 2007

Slide 11 Corporate Governance

Clause 49 of the Listing Agreement

Section IV

Definition of independent Director (…contd.)

• Not related to promoters, to board members or to persons holding managerial positions one level below board

• Has not been an executive in company in preceding three years

• Has not been a partner or executive in statutory audit firm or internal audit firm in the past 3 yeaars

• Has not been a partner or executive in law firm or consulting firm with material association to company in the past 3 years

• Is not a material supplier, service provider, customer, lessor or lessee of company

• Does not hold more than 2% shares in the company

Walker, Chandiok & CoNovember 28, 2007

Slide 12 Corporate Governance

Clause 49 of the Listing Agreement

Section IV

The Audit Committee

• Company to constitute an audit committee with terms of reference

• At least three members- two thirds independent

• Chairman to be independent- must attend every AGM

• All members financially literate & at least 1 member to be expert & CS to be thesecretary

• May meet with or without executives – generally CFO & CEO are invited

• Must meet at least 4 times a year - quorum = greater of 2 members or 2/3rd and at least 2 independent

Walker, Chandiok & CoNovember 28, 2007

Slide 13 Corporate Governance

Clause 49 of the Listing Agreement

Section IV

The Powers of the Audit Committee

• Investigate all matters within the terms of reference

• Seek information from any employee

• Obtain outside legal/ professional advice

• To invite outside experts

Walker, Chandiok & CoNovember 28, 2007

Slide 14 Corporate Governance

Clause 49 of the Listing Agreement

Section IV

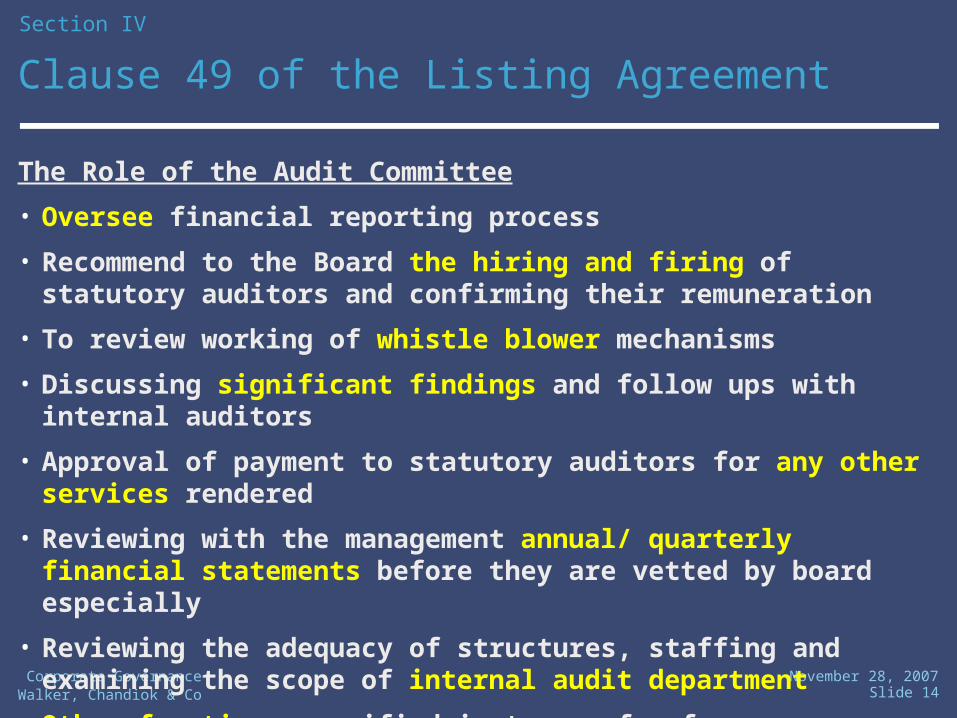

The Role of the Audit Committee

• Oversee financial reporting process

• Recommend to the Board the hiring and firing of statutory auditors and confirming their remuneration

• To review working of whistle blower mechanisms

• Discussing significant findings and follow ups with internal auditors

• Approval of payment to statutory auditors for any other services rendered

• Reviewing with the management annual/ quarterly financial statements before they are vetted by board especially

• Reviewing the adequacy of structures, staffing and examining the scope of internal audit department

• Other functions specified in terms of reference

Walker, Chandiok & CoNovember 28, 2007

Slide 15 Corporate Governance

Clause 49 of the Listing Agreement

Section IV

Audit Committee to review following information

• Statement of significant related party transactions submitted by management

• Management letters and letters of internal control weakness issued by the statutory auditors

• Internal audit reports relating to internal control weakness

• Review of appointment, removal and terms of remuneration of chief internal auditor

• Review of Management Discussion and Analysis (MDA) Report of financial condition and result of operations

Slide 16 Corporate GovernanceWalker, Chandiok & Co

November 28, 2007

Clause 49 of the Listing Agreement

Section IV

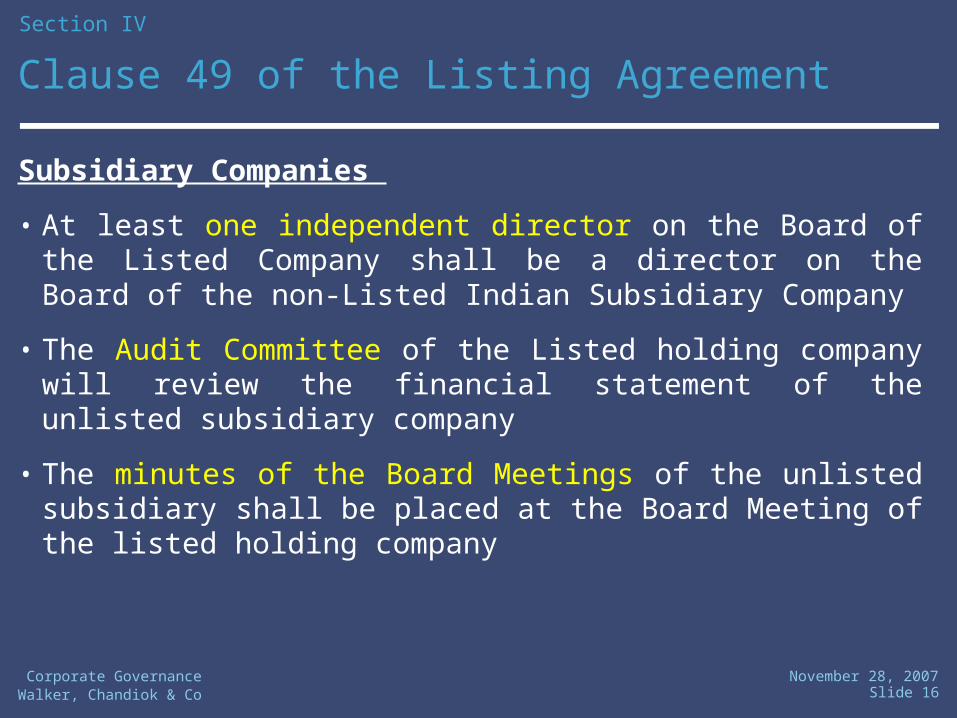

Subsidiary Companies

• At least one independent director on the Board of the Listed Company shall be a director on the Board of the non-Listed Indian Subsidiary Company

• The Audit Committee of the Listed holding company will review the financial statement of the unlisted subsidiary company

• The minutes of the Board Meetings of the unlisted subsidiary shall be placed at the Board Meeting of the listed holding company

Walker, Chandiok & CoNovember 28, 2007

Slide 17 Corporate Governance

Clause 49 of the Listing Agreement

Section IV

Responsibility of the Audit Committee and the Board for disclosures

• Related party transactions ~ Place before the audit committee:

summary of transactions in the ordinary course of business

details of transactions not in the ordinary course of business

details of transactions, with related parties or others, not on arms length basis

• If financial statements are prepared in a manner other than that prescribed in an accounting standard, the same has to be disclosed i.

• Disclose in the Annual Report all pecuniary relationship or transactions of the non-executive directors with the company; criteria for making payments to such directors and number of shares and convertible instruments held by them.

Walker, Chandiok & CoNovember 28, 2007

Slide 18 Corporate Governance

Clause 49 of the Listing Agreement

Section IV

Disclosures

• Disclose in the Annual Report all elements of remuneration package of independent directors; service contracts, notice period, severance fee and stock options details

• Senior Management shall make disclosures to the Board relating to all material financial and commercial transactions, where they have a personal interest that may have a potential to conflict with the interests of the Company

• On appointment of a new director or re-appointment of a director, provide information to the shareholders with respect to his expertise, about his membership/directorship in other companies and his shareholding in case he is a non-executive director.

• Quarterly results and presentations made by the Company to analysts shall be put on company’s website.

Walker, Chandiok & CoNovember 28, 2007

Slide 19 Corporate Governance

Clause 49 of the Listing Agreement

Section IV

CFO / CEO certification

• CEO = MD or Manager Appointed Under Companies Act

• CFO = Whole Time Finance Director or Other Person Heading the Finance Function

• CEO and CFO to certify to the board:

• that they have reviewed financial statements and to the best of their knowledge and belief:

No materially untrue statement/ omission of material fact/ misleading statement

Statements together present true and fair view of company’s state of affairs and its results of operations and are in compliance with existing accounting standards and relevant laws and regulations.

Walker, Chandiok & CoNovember 28, 2007

Slide 20 Corporate Governance

Clause 49 of the Listing Agreement

Section IV

CEO/ CFO to certify the following and report:

No transactions entered into by company during the year which are fraudulent, illegal or violative of the company’s code of conduct

Accept responsibility for internal control systems, have evaluated the effectiveness of the systems.

Significant changes in internal control during the year

Significant changes in accounting policies

Instances of significant fraud of which they have become aware

Walker, Chandiok & CoNovember 28, 2007

Slide 21 Corporate Governance

Clause 49 of the Listing Agreement

Section IV

Report and Compliance

• Separate section in annual report on compliance with corporate governance

• Quarterly compliance report to stock exchange signed by Compliance Officer or CEO

• Company to disclose compliance with non-mandatory requirements in annual reports

Slide 22 Corporate GovernanceWalker, Chandiok & Co

November 28, 2007

Amendements in Clause 49

Section IV

SEBI vide Circular SEBI/CFD/DIL/CG/1/2006/13 dated January 13, 2006, has made certain changes in the revised Clause 49.

The changes are covered hereunder –

1. Payment of sitting fee to Non-Executive Directors within the limits prescribed under the Companies Act, 1956 will not require prior approval of shareholders.

2. The maximum gap between two Board meetings has been increased to 4 months from 3 months.

3. Certification regarding degree of prevalence of internal controls underlying the systems will form part of overall certification by CEO & CFO and would be mandatory for the purpose of financial reporting.

Walker, Chandiok & CoNovember 28, 2007

Slide 23 Corporate Governance

Zero tolerance

compliance system

2Identify locations

and personnel

3List out statutory

compliance requirements at each location4

Fix compliance reporting methodologies

1Understand the

business process

5Implementation of

Compliance Reporting Structure

6Periodical Review

of compliances

7 Find out the

Gaps/ Instances of Non

Compliance

8Periodical reporting

to the Board on instances of Non Compliance along

with the steps taken to rectify

Suggested Statutory Compliance Reporting Structure

ILLUSTRATIVE

ILLUSTRATIVE

Slide 24 Corporate GovernanceWalker, Chandiok & Co

November 28, 2007

BoardApprove policy/strategy

Executive TeamSponsorship/operation

Board Audit & Risk CommitteeDelegated authority

Risk ManagerSubject matter

DepartmentsApply policy

Risk policy &guidelines

Risk information

Quarterly riskreporting

Suggested Risk Management Structure

ILLUSTRATIVE

ILLUSTRATIVE

Slide 25 Corporate GovernanceWalker, Chandiok & Co

November 28, 2007

Recommended solution to comply with Clause 49

EstablishRisk ManagementFramework

EstablishRisk ManagementFramework

At entity level At entity level

At Process levelAt Process level

Risk Register

Risk Register

Document Risk & Control

Document Risk & Control

Heat Maps

(Function/ Process)

Heat Maps

(Function/ Process)

Initial RiskAssessment

Initial RiskAssessment

Establishing Internal Control Framework

Establishing Internal Control Framework

CEO / CFOCertification

CEO / CFOCertification

Establishing legal compliance framework

Establishing legal compliance framework Reporting structure &

format

Reporting structure & format

Board Reporting

Board Reporting

ILLUSTRATIVE

ILLUSTRATIVE

Walker, Chandiok & CoNovember 28, 2007

Slide 26 Corporate Governance

Section V

• Building responsive boards - with a mechanism to create trust and responsibility.

• Finding appropriate Independent Directors in adequate numbers.

• Creating a climate where Corporate Governance norms are followed in spirit rather than just as a ‘tick the box’ activity.

• Fostering a corporate culture of transparency.

• Strengthening the weaker compliance mechanisms for adherence to statutory and regulatory requirements.

• Shareholders passivity.

• Tight insider/owner controls or government ownership.

• Lack of awareness of global best practices.

Issues and Challenges in India

Walker, Chandiok & CoNovember 28, 2007

Slide 27 Corporate Governance

Issues and Challenges in India

Section V

• Shareholders not sole beneficiary of corporate governance norms- other stakeholders need protection too

• Clause 49 disqualifies holder of more than 2% stake from being an independent director

Walker, Chandiok & CoNovember 28, 2007

Slide 28 Corporate Governance

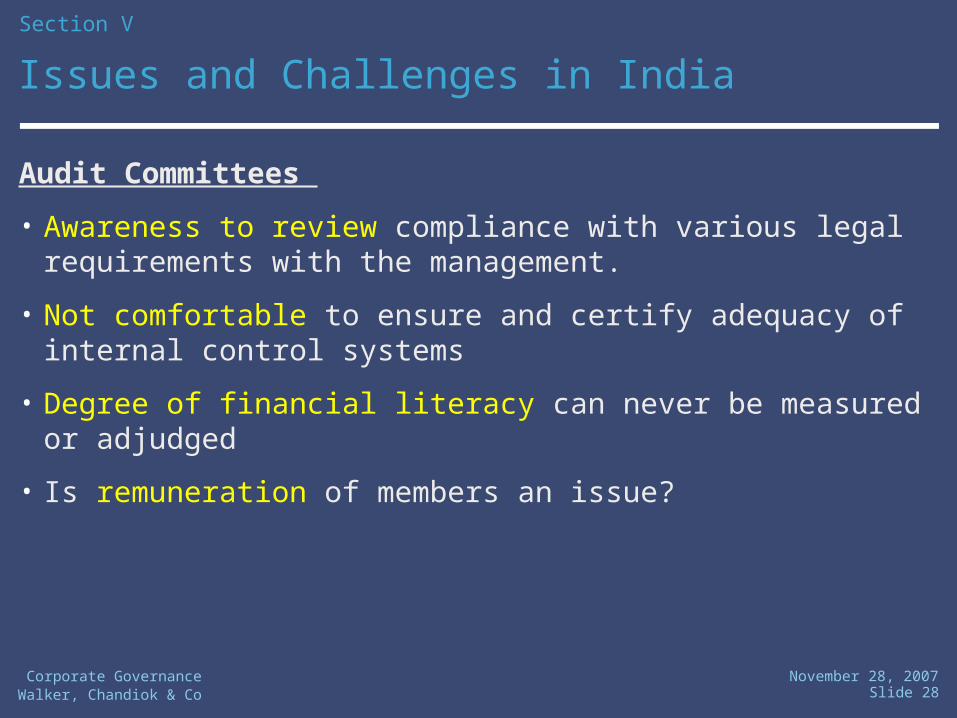

Section V

Audit Committees

• Awareness to review compliance with various legal requirements with the management.

• Not comfortable to ensure and certify adequacy of internal control systems

• Degree of financial literacy can never be measured or adjudged

• Is remuneration of members an issue?

Issues and Challenges in India

Walker, Chandiok & CoNovember 28, 2007

Slide 29 Corporate Governance

Section VI

Advantages of a well developed Corporate Governance framework

• Increased confidence of investors especially foreign investors as we now have one of the best developed mandatory Corporate Governance Codes.

• Streamlining of Corporate’s financial,risk management and legal compliance reporting frameworks resulting in efficiencies of operation.

• Greater transparency of corporate proceedings and an internal check through a whistle blowers policy-though optional, has been adopted by the larger corporations.

• Increased shareholder value.

Walker, Chandiok & CoNovember 28, 2007

Slide 30 Corporate Governance

Advantages of a well developed Corporate Governance framework (contd.)

• Increased emphasis on corporate governance being perceived as an effective investment criteria among large investors

• Improved Equity Price Performance

• Higher Valuations

• Respectable access to global markets

• Increased investor goodwill & confidence

Section VI

Walker, Chandiok & CoNovember 28, 2007

Slide 31 Corporate Governance

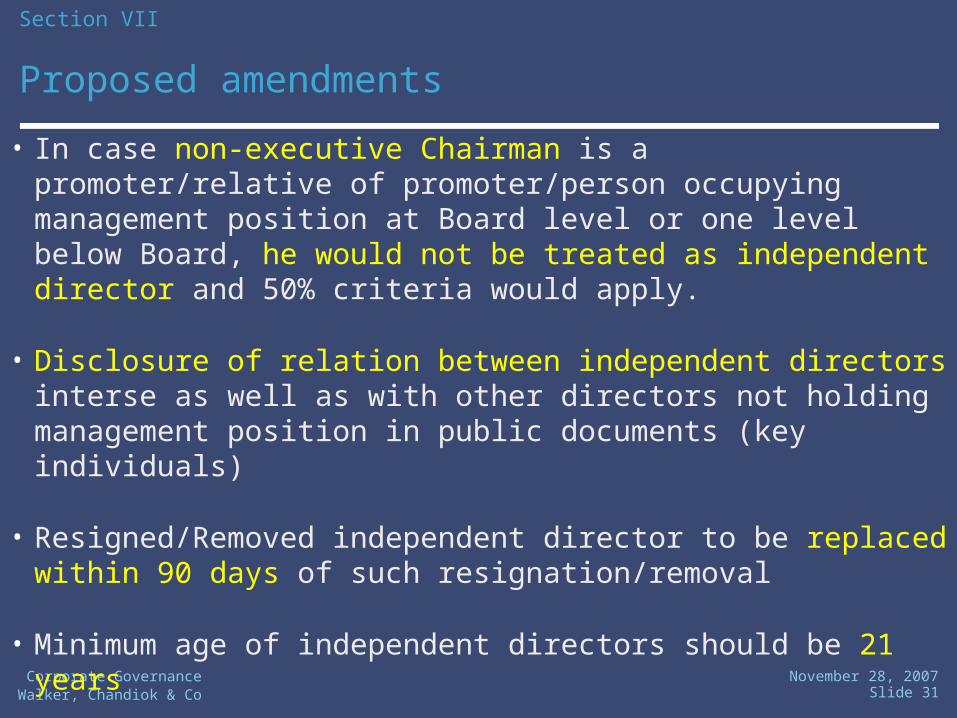

Proposed amendments

• In case non-executive Chairman is a promoter/relative of promoter/person occupying management position at Board level or one level below Board, he would not be treated as independent director and 50% criteria would apply.

• Disclosure of relation between independent directors interse as well as with other directors not holding management position in public documents (key individuals)

• Resigned/Removed independent director to be replaced within 90 days of such resignation/removal

• Minimum age of independent directors should be 21 years

• Nominee directors would not be considered as independent directors

Section VII

Slide 32 Corporate GovernanceWalker, Chandiok & Co

November 28, 2007

Thank you