Global Financial Crisis: Impact and Responses in Nepal Presented by D. R. Khanal (Dr.) 14 Jan,2009.

34

Global Financial Crisis: Impact and Responses in Nepal Presented by D. R. Khanal (Dr.) 14 Jan,2009

-

Upload

ethan-lamb -

Category

Documents

-

view

227 -

download

0

Transcript of Global Financial Crisis: Impact and Responses in Nepal Presented by D. R. Khanal (Dr.) 14 Jan,2009.

Global Financial Crisis: Impact and Responses in Nepal

Presented by

D. R. Khanal (Dr.)

14 Jan,2009

Root Causes of Global Financial Crisis

• Present crisis worse after the great deprecation of 1929• Proved to be not only greedy but also anarchical • Most noticeable underlying reasons:

– Financialization a last resort to the greedy capitalists ( speculators) after continued stagnation and declining profit in the real sectors

– Even the neo-liberalism imposed under SAP and intensified in the form of globalization through ESAF, WTO and Washington Consensus could not prevent crisis or stagnation in the Capitalist countries

• IT bubble although resolved the crisis of early 1990s, stagnating trends reemerged in the beginning of 21st century in the US

• Increased profits, at the same time, were taken by newly emerging capitalist countries, thus falling profit in the US and other western capitalist countries

– This happened despite developing countries with pre, semi and non-capitalist characters integrated into the global capitalistic economic system.

– The over concentration of wealth and decline in the purchasing power of the working class amidst stagnation in a situation of overproduction was preventing to get higher profits by greedy capitalists.

– Then there was deliberate attempt at policy induced financialization for ensuring higher and overnight profits. The rate of interest was kept 1 percent since 2003 for sub-prime loans, at the same time without any stringent regulatory rules.

– The havoc created by Wall Street Meltdown and its contagion is before us.

– One feature of financialization has been such that it widened the gap between the production or output value in the real sector and the increased monetary value of wealth or profit in the hyper financial sector amidst too much income disparity in society in few years.

• For instance: In 1982 the profit of USA financial companies

accounted for 5 percent of total after tax corporate profit. In 2007 they made up 41 percent of corporate profit, rising six-fold as a share of GDP.

• Another example: Hedge funds president John Paulson took in dollar 3.7 billions in 2007 (by betting collapse of the sub-prime mortgage market) and the top fifty Hedge funds manager netted a combined sum of dollar 29 billions.

• At the same time, the growing consumption demand amidst enormous rise in trade deficit in the US was met by purchasing almost $ 2 billion every day from the market. There was some sort of siphoning of funds from surplus countries to the US at a low interest rate. Today US debt has reached more than $10 trillion.

• The persistence of huge budgetary or trade deficit additionally constraints bail out or recovery plan of the US.

• Rescue and bailout plans – Several bailout plans have either been implemented or they are in offing.

Discarding the neo-liberalism principles, state interventions, nationalization and direct support scheme are underway. Both easy monetary and fiscal stimulus packages are the major components to address financial as well as real sector crisis

– However, crisis is further deepening along with rising unemployment in US and other countries. Credit crunch and other problems are affecting real economy very seriously

– There are policy gaps and at the same time asymmetries are persisting • For revival purchasing capacity of workers has to be enhanced in addition to reducing

income inequality considerably which will take albeit longer time• In an integrated world, any reduced external demand of US will further aggravate crisis.• Similarly, as noted above, US has many constraints and limitations. For instance, rise

in $ will encourage imports requiring siphoning of reserves from the surplus countries. On the other hand, without a bubble, like in housing, there will be less attraction for investment in the US.

• Along with rise in unemployment in capitalist countries, the class contradiction is bound to trigger.

• Therefore, crisis will prolong and in a transition, a big push for correcting US dictated global economic system essential which has a big prospect as well

Probable Impact in the Nepalese Economy

• So far no bigger impact has been felt. The impact will depend on the prolonged crisis in the global economy and slowdown in India. But the vulnerability of the economy is high with some bubble type of characters in some sectors of the economy– One of the highly liberalized country in South Asia.

• Trade is completely deregulated and no trade and non-trade barriers including no support measures are there in exports

• Expect transportation and fertilizer subsidy in remote areas (now limited irrigation subsidy also), no subsidy is there

• In large and medium industries up to 100 percent foreign equity participation is allowed with repatriation facilities

• In banking three fourth and in insurance 100 percent foreign equity participation has been already allowed even if in a selected basis

• The actual average tariff rate has reduced to 5.13 percent in 2007 from 6.1 percent in 2003. Likewise, the imports tariff rate has gone down to 6.23 percent from 7.72 percent during the same period.

• Remittances is the major source of external inflow exceeding more than Rs. 140 billion. The increased inflow induces urban centric consumption expenses and unproductive investment in real estate activities. It also induces imports which again provides 60 percent of total tax revenue.

• The proliferation of banking and financial institutions is partly linked to the increased remittances inflow

• Trade is highly volatile with fragile bases and no diversification• Foreign aid is major source of development budget. Nepal has implemented

all conditions led aid programs including SAP, ESAF and PRSP. Increased aid partly is the outcome of this

• Labor market is predominated by informal sector employment which is almost 94 percent

• Income inequality is very high with increased tendency in recent years • Recently price rise has been a major concern at more than 14 percent in an

annualized basis

• More specifically, the impact will be transmitted through– Trade

• Goods• In a situation of fragile base, high volatility and high

country and commodity concentration, weakening of demand in India as well as other countries will affect exports including employment in exportable industries

Share of Trade in GDP

0.0

10.0

20.0

30.0

40.0

2004 2005 2006 2007 2008

Years

Export Import Trade

Share in Total Trade

0.000

5.000

10.000

15.000

20.000

25.000

30.000

2004 2005 2006 2007 2008

Years

Export Eport India Export Other Countries

Share of India and Other Countries in Total Export

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

2002/03 2003/04 2004/05 2005/06 2006/07 2007/08

Years

Shar

e in

%

India Other Countries

Exports of Major Commodities to India

0.0

5000.0

10000.0

15000.0

20000.0

25000.0

30000.0

35000.0

40000.0

45000.0

2003/04 2004/05 2005/06 2006/07 2007/08

Years

Rs in m

illio

ns

Total India Export Cardamom Chemicals Ghee (Vegetable) Juice

Jute Goods Polyster Yarn Readymade garment Textiles* Thread

Wire Zinc sheet Others

Exports of Major Commodities to Other Countries

0.0

5000.0

10000.0

15000.0

20000.0

25000.0

2003/04 2004/05 2005/06 2006/07 2007/08

Years

Rs

in m

illi

ons

Others Handicraft ( Metal and Wooden ) Nepalese Paper & Paper Products Pashmina.*

Pulses Readymade Garments Silverware and Jewelleries Tanned Skin

Woolen Carpet Totals

• Services – Most adverse effect would be through services – tourism

• In 2008 more than 8 lack tourists ( from India only tourists via air) came to Nepal. They provide employment to more than 83000 people directly. Tourist earnings is around 2.5 of GDP

• Foreign Employment– Major adverse effect would come through reduction in

foreign employment and remittances

Remittances Inflows

0

20000

40000

60000

80000

100000

120000

140000

160000

2003 2004 2005 2006 2007 2008

Fiscal Year

NR

s in

mil

lins

Remittances (RRTN)

Share of Remittance Inflows in GDP

0.0

5.0

10.0

15.0

20.0

2003 2004 2005 2006 2007 2008

Share

Country-wise Flow of Foreign Employment

0

50000

100000

150000

200000

250000

300000

2005 2006 2007 2008

Fiscal Year

Num

ber

Malaysia

Qatar

Saudi Arab

UAE

Kuwait

South Korea

Oman

Others

Total

Share in Total Foreign Employment

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

2005 2006 2007 2008

Fiscal Year

Shar

e in

Per

cent

age

Malaysia

Qatar

Saudi Arab

UAE

Kuwait

South Korea

Oman

Others

– Symptom of reduction in out flow is already there. In 4

to 5 months, the adverse effect is most likely in Nepal– That will have wide-ranging impact

• Employment• Remittances • Imports • Government revenue • Banking and Finance• Real estate prices and transactions • Stock market • Economy wide growth and domestic employment

• Banking and Finance– Some pressures on interest rate is already

there as reflected by inter-bank and treasury bill rates.

– The earnings of more than Rs 47 billion balance in foreign banks will also be affected as a result of drastic cut in interest rates in the US

– The weakening of lending capacity will have effect on entire money and capital market

Share of Total Deposits and Loans and Advances in GDP

0.0

10.0

20.0

30.0

40.0

50.0

60.0

2003 2004 2005 2006 2007 2008

Fiscal Year

Rs

is in

mil

lion

Total Deposits Loans and Advances

Trends of Sectorwise Credit Flows of Commercial Banks

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

2003 2004 2005 2006 2007 2008

Years

Sh

are

in

%

Agriculture ProductionConsturction Metal, TransporationWholesaler and Retailers Finance, Inusrance and Fixed AssetsReal Estates Others

• Foreign Aid/Debt Servicing – Foreign aid contributes almost 60 percent in

development budget– Nepal does not face so much aid constraint

as Nepal has implemented SAP,ESAF and PRSP under donor conditions.

– During the SAP and ESAF period, loan component was high and increased rapidly. Now there is some increment in grants

Trends of Direct External Debt

0

2000

4000

6000

8000

10000

12000

14000

1987 1990 1993 2000 2004 2007

Years

NR

s in

mill

ions

Total Borrowing

Borrowing - ADB

Borrowing - IDA

Repayment of Principal

Payment of Interest andFees

Interest - ADB

Interest - IDA

Net Flow of Loan and Grant

-5000

0

5000

10000

15000

20000

2001 2002 2003 2004 2005 2006 2007

Fiscal Year

NRs i

n Mill

ions

Debt Servicing

Foreign Loan

Foreign Grants

Net Grant

Net Loan

• So far aid commitments is continuing. But it may also be gradually affected with direct effect on budget, more so on social services and infrastructure development programs

• Instantly the rise in $ rate would have direct impact on debt servicing. In this fiscal year it will have additional liability of more than Rs 1 billion. Since July, $ has appreciated by more than 20 percent.

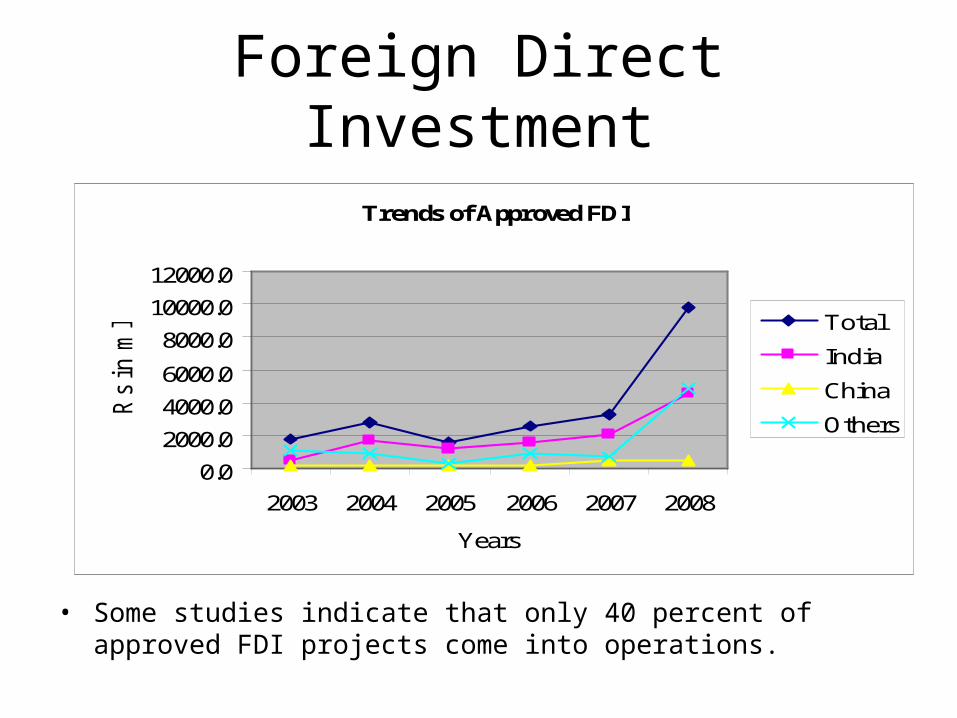

• Foreign Direct Investment– Nepal had high expectation on foreign direct

investment – There are announcements of generating 10

mw electricity in two years primarily through FDI

– Indications are that FDI will be highly affected

Foreign Direct Investment

• Some studies indicate that only 40 percent of approved FDI projects come into operations.

Trends of Approved FDI

0.0

2000.0

4000.0

6000.0

8000.0

10000.0

12000.0

2003 2004 2005 2006 2007 2008

Years

Rs

in m

lns

Total

India

China

Others

Growth, Employment and Wages -Slowdown in trade, banking and finance, industry and government

budget would have adverse effect on domestic employment too. -More unskilled workers will loose their job and predominant

informal labor market would have adverse effect on the wages of unskilled workers.-Apart from drastic reduction in cottage and small scale industry in recent years, there is decline in the employment of manufacturing industries hiring 10 and more than 10 employees as well. The employment in this will be further adversely affected.-The budget has targeted 7 percent growth rate. The IMF projection shows 5.5 percent. It may be in the range of 4.5 to 5 percent. As our assessment indicates, next year in may be further reduced.

0 100000 200000 300000

Number

1992

2002

2007

Yea

rComparison of Inter Census Persons Engaged and

Employees

Total number ofemployees

Total number ofperson engaged

• Responses ( Donors)– Multilateral donors are advising to follow the same old

policies– Advising to adopt tight monetary and fiscal policies– Advising to pursue flexible labor policy– The conditions imposed are enact- best case is hike

of water services charge two three days ago – The increased aid flow most noticeably the grant is

outcome of the continuation of donor led condition or otherwise policies by the present government

• Responses( Internal)– Formation of special committee-no actions or plan so

far – Truly, in the budget expanded safety net, social

security and grass root programs following UML budget of 1994/95.

– In terms of policy regime change, no breakthrough is visible. Some stress on private public partnership which is vague

– The government is arguing time and again that the economy is strong means no overhauling of neo-liberalism/donor led policies is essential. This has raised many big question marks.