Global Equities in the Year of the Rooster · 2015 2016 For Professional Investors only ... Source:...

22

Global Equities in the Year of the Rooster Bill Maldonado Global CIO Equities

Transcript of Global Equities in the Year of the Rooster · 2015 2016 For Professional Investors only ... Source:...

Global Equities in the Year of the Rooster

Bill Maldonado

Global CIO Equities

2

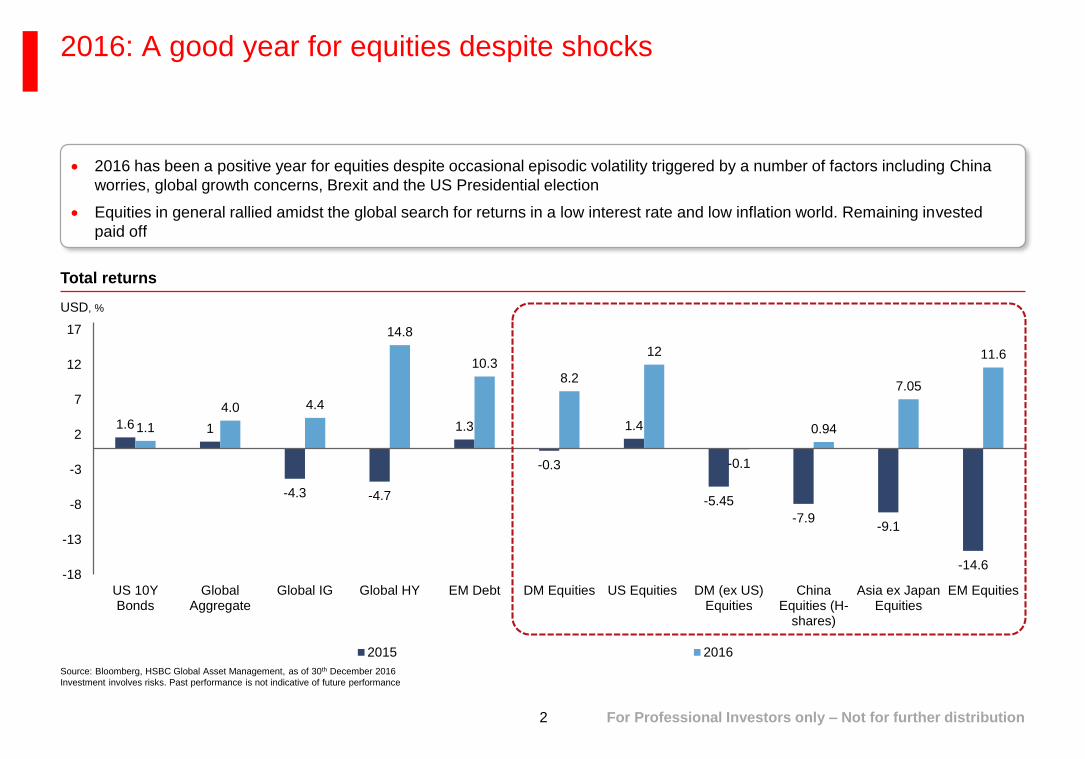

2016: A good year for equities despite shocks

Source: Bloomberg, HSBC Global Asset Management, as of 30th December 2016

Investment involves risks. Past performance is not indicative of future performance

2016 has been a positive year for equities despite occasional episodic volatility triggered by a number of factors including China

worries, global growth concerns, Brexit and the US Presidential election

Equities in general rallied amidst the global search for returns in a low interest rate and low inflation world. Remaining invested

paid off

1.6 1

-4.3 -4.7

1.3

-0.3

1.4

-5.45

-7.9-9.1

-14.6

1.1

4.0 4.4

14.8

10.38.2

12

-0.1

0.94

7.05

11.6

-18

-13

-8

-3

2

7

12

17

US 10YBonds

GlobalAggregate

Global IG Global HY EM Debt DM Equities US Equities DM (ex US)Equities

ChinaEquities (H-

shares)

Asia ex JapanEquities

EM Equities

2015 2016

For Professional Investors only – Not for further distribution

Total returns

USD, %

3

Many strategists argue that equities are overvaluedBut assuming a mean reversion of conventional valuation metrics is naïve

Source: HSBC AMG Global Investment Strategy, as of December 2016

0

5

10

15

20

25

30

35

40

45

50

1881 1900 1919 1938 1957 1976 1996 2015

Cyclically adjusted Price Earnings Ratio

Historic average P/E

0

2

4

6

8

10

12

14

16

18

US 10-year Government Bond Yield

0

100

200

300

400

500

600

700

1919 1932 1945 1959 1972 1985 1999 2012

Moody's Corporate BAA spread

Many market observers conclude that “everything is overvalued” when looking across conventional valuation metrics

For equities, some analysts cite a range of price metrics (P/Es, Equity/Gold ratios and Tobin’s Q etc). They argue that multiples

are significantly above historic norms and must adjust. Even if this takes place over a multi-year time frame, it would imply very

poor prospective returns from a core return-seeking asset class

Is this view right?

Global bonds at historically low yields… …Credit spreads are tight… …And equity ratings are high

bp

4

…We disagreeValuation needs to be done “in context”

Valuation analysis needs to be done “in context” of:

– (i) the macro-economic and interest rate regime we are in

– (ii) the available opportunity set (ie a cross-asset perspective)

This means that we want to think about valuation in a structured and integrated way

– We don’t think it is right to use ad hoc metrics – ie comparing bond yields vs credit spreads vs equity PEs makes no sense

to us

– And we need to avoid the biases of hindsight and regret

The starting point to think about today’s investment opportunities needs to be an understanding of the

growth/inflation environment we are in and the policy regime we are likely to face

Once we have this, we think hard about the valuation position of each asset class to understand the “implied

odds” that the market is offering us today

Valuation is Key

5

Risk premia todayWhere are valuation opportunities?

Note:1. Global Fixed Income assets are shown hedged to USD. Local EM debt, Equity and Real Estate assets are shown unhedged

Source: HSBC AMG Global Investment Strategy, December 2016

Any forecast, projection or target contained in this presentation is for information purpose only and is not guaranteed in any way. HSBC Global Asset Management accepts no liability for any failure to meet such forecasts, projections or

targets. For illustrative purpose only

Chart shows today’s implied returns (based on current pricing) for a range of asset classes

US TIPS

UK IL Gilts

US Tsy

UK Gilts

Germany Bunds

Japan JGBs

US Corp

US HY

GBP Corp

EUR Corp

EM Sovs USD

EM CreditUS Equity

UK Equity

Japan Equity

EM Equity

AC World Equity

Asia ex Japan Equity

Global Gov

Global Credit

Global ILBs

Global HY

Euro ABSUS 5y Tsy

UK 5y Gilts

Local EM Debt

Europe x UK Equity (H)

UK Equity (H)

Japan Equity (H)

Canada EquityCanada Equity (H)

-2

0

2

4

6

8

10

0 2 4 6 8 10 12 14 16 18 20 22 24 26

Current pecking order of asset classes1

Expected Risk Premia (%, Nominal, USD)

Expected Volatility (%)

Sharpe Ratio = 0.25

Sharpe Ratio = 0.10

6

Global EquitiesThe equity premium is still high

Source: HSBC Global Asset Management, Global Investment Strategy, as of December 2016.

Any forecast, projection or target contained in this presentation is for information purpose only and is not

guaranteed in any way. HSBC Global Asset Management accepts no liability for any failure to meet such forecasts,

projections or targets. For illustrative purpose only

0

5

10

15

20

2005 2007 2009 2011 2013 2015

MSCI US MSCI US (ex AMG)MSCI US (Sector-Neutral) MSCI US (ex Oil & Gas)

The implied expected return on global equities is

around 5.5%. This is hardly inspiring relative to

history and investors need to be realistic about the

sustainable returns on offer

However, the equity risk premium remains high

relative to our expectations for cash interest rates

and relative to government bonds even after the

recent sell-off

The equity vs bonds decision seems clear

A reflationary environment favours global equities

relative to competing asset classes

In the absence of an imminent recession and sharply

deteriorating corporate fundamentals, harvesting the

equity premium makes sense

Cyclical data looks good and recession probability

models suggest a low chance of an imminent recession

Recent US macro profits data illustrates relatively stable

corporate fundamentals

President-elect Trump’s policies appear capital-friendly

200

250

300

350

400

450

500

0

500

1,000

1,500

2,000

2,500

2005 2007 2009 2011 2013 2015

US Corporate Profits - Total, LHSUS Corporate Profits - Domestic, LHSUS Corporate Profits - Rest of the World, RHS

US Corporate profits

MSCI US

USDbn USDbn

ROE, %

7

Europe/Japan Equity MarketsRelatively high implied premia

Source: HSBC Global Asset Management, Global Investment Strategy, December 2016

6000

8000

10000

12000

14000

16000

18000

20000

22000

60

70

80

90

100

110

120

130

2010 2011 2012 2013 2014 2015 2016

JPY/USD (LHS) Nikkei 225 (RHS)

0

5

10

15

20

Jan 14 May 14 Sep 14 Jan 15 May 15 Sep 15 Jan 16 May 16 Sep 16

Eurozone Japan

In Japan, the ERP is around 5%. With “yield curve

control” proving effective so far, is the Bank of

Japan guaranteeing us the equity premium?

– A move towards more co-ordinated fiscal-monetary

policy, in addition to BOJ ETF buying, should be

supportive for equities

Eurozone equity valuations also remain attractive.

Implied premia close to 5% in some markets (eg

Germany) and the profits catch-up story remains in

play

– Activity data is also encouraging. Growth is running well

above trend. With continued ECB support, this could be

sustained

We want to hedge Japan and European equity

market exposures (from the perspective of USD

investors). We want to be exposed to equity market

returns driven by sustained local currency

weakness

JPY and Nikkei

12m forward earnings in Europe and Japan

JPY/USD Index

Y-o-y%

8

Asia/Emerging MarketsAsia/EM risk is also attractively priced

Source: HSBC Global Asset Management, Global Investment Strategy, as of December 2016

Investment involves risks. Past performance is not indicative of future performance

-40

-30

-20

-10

0

10

20

30

2011 2012 2013 2014 2015 2016

Earnings Growth Multiple Expansion Dividend Yield FX Total Return

10

12

14

16

18

20

2005 2007 2009 2011 2013 2015

MSCI EM MSCI EM (ex Oil & Gas and Basic Materials)

Asia/EM equities have been a major laggard over

the last decade. Disappointing earnings growth,

multiple contraction and depreciating currencies

have all weighed on total returns

Today, (i) equity valuations look reasonable, (ii)

Asia/EM currencies look undervalued, (iii)

profitability and cyclical indicators are improving

We estimate the implied sustainable return on

Asia/EM equities at around 9% in USD terms

Weak profitability over the past three years has

been primarily driven by commodity-related sectors

(see chart)

Interest rates remain high in many markets. There

is potential for a secular equity market re-rating

Political concerns and dis-continuities from dollar

strength/more aggressive Fed scenario are

important risks however. There is a lot of

uncertainty here. We need to be comfortable that

we are being compensated for the risk

MSCI Emerging Markets Index (USD) Total Return

Decomposition

MSCI EM

%

ROE, %

Key themes for 2017

10

Beneficiaries of reflationary and pro-growth policies

Source: Datastream, UBS as of November 2016.

Rebased

The near-term growth outlook for the US has improved with the turn up in PMIs and the expected fiscal policy proposals of

President-elect Trump which will likely boost GDP growth in 2017

Emerging market cyclical indicators have been improving. Equity earnings expected to pick up further as better macro data

supports the corporate environment

S&P 500 earnings expected to continue to grow

MSCI Emerging Markets universe earnings revisions have

bottomed

Any forecast, projection or target contained in this presentation is for information purposes only and is not guaranteed in any way. HSBC accepts no liability for any failure to meet such forecasts, projections or targets. For illustrative

purpose only

11

Emerging market vs developed market equities

Source: HSBC Global Asset Management, Bloomberg as at 30 December 2016. For illustrative purposes. Any performance information shown refers to the past and should not be seen as an indication of future returns

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

De

c-0

4

Jun-0

5

De

c-0

5

Jun-0

6

De

c-0

6

Jun-0

7

De

c-0

7

Jun-0

8

De

c-0

8

Jun-0

9

De

c-0

9

Jun-1

0

De

c-1

0

Jun-1

1

De

c-1

1

Jun-1

2

De

c-1

2

Jun-1

3

De

c-1

3

Jun-1

4

De

c-1

4

Jun-1

5

De

c-1

5

Jun-1

6

De

c-1

6

Difference in 5-year annualized return of EM and DM Equities

EM equities have been a major laggard over the last decade, as disappointing earnings growth, multiple contraction and

depreciating currencies have all weighed on total returns

EM equities have lagged DM peers in the last decade

12

The case for emerging market equities

Source: HSBC Global Asset Management, DataStream as at 30 September 2016. For illustrative purposes only

-2%

0%

2%

4%

6%

19

81

19

86

19

91

19

96

20

01

20

06

20

11

20

16

Emerging markets Developed markets

Emerging markets now contribute about a third of global GDP and half of global GDP growth

In the short to medium term, we expect economic fundamentals to be supportive for EM equities

Continued, rapid, industrialisation will boost growth while potential moves up the value chain could improve corporate earnings in

some economies

Contribution to global GDP growth

13

The case for emerging market equities II

Source: HSBC Global Asset Management, DataStream as at 30 September 2016. For illustrative purposes only

Emerging market equities – MSCI Emerging Markets Index, Developed Market Equities – MSCI World Index

0.0

1.0

2.0

3.0

4.0

De

c-9

9

De

c-0

1

De

c-0

3

De

c-0

5

De

c-0

7

De

c-0

9

De

c-1

1

De

c-1

3

De

c-1

5

Emerging Markets Developed Markets

0%

5%

10%

15%

20%

Jan-9

5

Jan-9

7

Jan-9

9

Jan-0

1

Jan-0

3

Jan-0

5

Jan-0

7

Jan-0

9

Jan-1

1

Jan-1

3

Jan-1

5

Emerging Markets Developed Markets

Today, (i) equity valuations look reasonable, (ii) EM currencies look undervalued, (iii) profitability and cyclical indicators are

improving

Emerging market equities expected returns appear attractive versus bonds and cash

Valuations: Price-Book Return on Equity (RoE)

14

Asia ex Japan equities favoured amongst peers

Source: Bloomberg, MSCI, HSBC Global Asset Management, as of December 2016. Investment involves risks. Past performance is not indicative of future performance

0.5

1.0

1.5

2.0

2.5

3.0

1996 1999 2002 2005 2008 2011 2014

Asia ex-JP - Trailing PB

1.41x now

1.23x in

Feb 090.94x in

Aug 98

1.22x in

Mar 03

1.23x on

21 Jan

Avg: 1.77x

1.19x in

Sep 01

-1.6

-1.4

-1.2

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

8/11 8/12 8/13 8/14 8/15 8/16

Asia ex Japan forward P/B vs. EU Asia ex Japan forward P/B vs. US

MSCI Asia ex Japan has rallied strongly since Brexit, led by cyclical sectors including materials, energy and financials

Even after recent rally, Asia is still trading at a 17% discount to average historic levels

Discount to developed markets has not narrowed significantly, despite an improving outlook

Asian equities likely to remain in favour, supported by improving earnings outlook and compelling valuations

Asia ex Japan P/B valuation vs developed markets Asia exJ trailing P/B at 20% discount to normalised levels

15

Asia ex Japan equity earnings outlook improving

Source: CLSA, Credit Suisse, HSBC Global Asset Management, data as of January 2017

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Dec-95 Dec-98 Dec-01 Dec-04 Dec-07 Dec-10 Dec-13 Dec-16

Asia ex-JP - ROE

9.9% now

13.8% Dec 10

low 11.5% in 2009

low 1.7% in 1998

10% 6 months ago

-7

-6

-5

-4

-3

-2

-1

0

1

2

Jan16

Feb16

Mar16

Apr16

May16

Jun16

Jul16

Aug16

Sep16

Oct16

Nov16

Dec16

Earnings revisions appear to have bottomed, percentage of companies missing their earnings estimates has trended down

recently

Rising consumption, stable commodity prices and supportive monetary policy (rate cuts) are all tailwinds for earnings in Asia

The rate of decline in RoE for MSCI Asia ex Japan has slowed to just 0.1% over the past six months, one third of the 0.3% decline

in MSCI US RoE

MSCI Asia ex Japan earnings revisions have bottomed MSCI Asia ex Japan RoEs starting to bottom

L3M earnings revision (17F, %)

16

Chinese market still highly inefficient; earnings revisions abound

Significant earnings revisions in Chinese equities for the past 2 years

– For 2014, 21% of companies beat consensus by more than 10%, 38% of companies missed consensus by more than 10%

– For 2015, 28% of companies beat consensus by more than 10%, 30% of companies missed consensus by more than 10%

– For 2016, 13% of companies had more than 10% upward earnings revisions, 35% have more than 10% downward earnings revision

Our internal earnings estimates could be 6-12 month ahead of the market

– Proprietary demand/supply analyses enable us to come up with better margin estimates

Source: Goldman Sachs, as of December 2016

For illustrative purposes only and does not constitute any investment recommendation in the above-mentioned securities. Past performance is not indicative of future performance

Any forecast, projection or target contained in this presentation is for information purposes only and is not guaranteed in any way. HSBC accepts no liability for any failure to meet such forecasts, projections or targets

2014 2015 2016

Sectors

Net Income

actual vs

Jan

Consensus

Net Income

actual vs

July

Consensus

Net Income

actual vs

Jan

Consensus

Net Income

actual vs

July

Consensus

Net Income

Dec vs Jan

Energy -2% -16% -62% -33% -29%

Materials -49% -40% -37% -27% 26%

Industrials -21% 34% -10% -15% -10%

Consumer Discretionary -19% -6% -28% -22% -10%

Consumer Staples -30% -23% -29% -20% -22%

Health Care -33% -17% -2% -1% -3%

Banks -8% -2% -7% -2% 0%

Insurance -9% 19% 35% 5% -21%

Property 5% 14% 0% 14% -22%

Information Technology -21% 0% -3% 20% -5%

Telecommunication Services -5% 4% -5% -3% -15%

Utilities -26% -17% -4% -7% -24%

MSCI China -9% -1% -11% -4% -8%

% of

stocks Distribution of YTD performance

MSCI

China<-20% -20%~ -10% -10% ~0% 0%~+10% +10~+20% >+20% Universe

2014 21% 16% 14% 16% 10% 23% 100%

2015 28% 15% 18% 9% 9% 22% 100%

2016 27% 19% 18% 16% 8% 12% 100%

% of

stocks Distribution of earnings revision

MSCI

China<-20% -20%~ -10% -10% ~0% 0%~+10% +10~+20% >+20% Universe

2014 26% 12% 20% 21% 11% 10% 100%

2015 23% 7% 27% 17% 9% 19% 100%

2016 21% 14% 27% 25% 3% 10% 100%

Earnings revision and price performance for MSCI ChinaMSCI China – Consensus vs actual earnings

17

Chinese equity valuations

Source: MSCI, Bloomberg, Credit Suisse, HSBC Global Asset Management, data as of 31 December 2016. Investment involves risks. Past performance is not indicative of future performance

MSCI China is still trading below its average historic valuation

Investors need to be selective in terms of opportunities

0

1

2

3

4

5

6

1/96 1/98 1/00 1/02 1/04 1/06 1/08 1/10 1/12 1/14 1/16

12-month return

112.6%

12-month return

-5.4%

12-month return

60.2%

12-month return

82.5%12-month return

?

0.43x

Aug 98

0.54x

Feb 00

1.22x

Apr 03

1.51x

Oct 08

1.56x

Now

10-year average: 2.11x

Price-to-book (x)

18

Shenzhen-Hong Kong Stock Connect – Gateway to opportunity

Source: Bloomberg, MSCI, as of December 2016

Shenzhen-Hong Kong Stock Connect opens up a brand new universe for international investors to potentially monetise compelling

growth opportunities

The Shenzhen equity market offers investors a wider and deeper hunting ground for new economy sectors such as consumer

discretionary, consumer staples and information technology, which boast higher earnings growth and are arguably better placed to

benefit from ongoing economic reforms

On the other hand, the opening up of the HK small cap universe allows an expanded channel for mainland investors to effectively

diversify their assets and FX allocations.

Source: Bloomberg, FactSet, Goldman Sachs Global Investment Research, as of January 2017

0.1

0.6

1.1

1.6

2.1

2.6

4/14 7/14 10/14 1/15 4/15 7/15 10/15 1/16 4/16 7/16 10/16 1/17

HSSI SME ChiNext100 HSMI

0.98x

1.22x

0.69x

0.47x

0%

20%

40%

60%

80%

100%

Shanghai Shenzhen MSCI China

Consumer discretionary Consumer staples EnergyFinancials Health care IndustrialsInformation technology Materials Real estateTelecom services Utilities

Sector allocation of Shanghai, Shenzhen and offshore

Chinese equity marketsSmall-mid caps in HK seem more attractively valued than their

onshore peers

Trailing 12m PEG (X)

In conclusion

20

Impact of unexpected events diluted in long term

0

50

100

150

200

250

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

S&P 500 Total return index MSCI ACWI (USD) Total Return Index

Hurricane Katrina

hit the Gulf Coast

of the US, almost

destroying New

Orleans

London

bombings

North Korea’s

1st nuclear test

Saddam Hussein is

executed

Multiple suicide

bombings in

northern Iraq

Thailand rocked

by bombs

The US sub-

prime housing

crisis

Icelandic and

Russian

Financial Crisis

Global Financial

Crisis

Israel invaded

Gaza

The US withdrew

from Iraq

Lehman

Brothers

collapsed

Oil price swings

between US$145 –

US$32 p.b.

North Korea

fired missiles

Haiti

earthquake

European

sovereign debt

crisis

Japan’s

nuclear

disaster

1st Libyan civil

war

Gold skyrocketed to ~US$1,900

per ounce

Arab Spring

Uprising

Israel and

Gaza conflict is

reignited

Kenyan

shopping mall

attack

North Korea’s

3rd nuclear test

Spain accepted

EUR100 bn

bailout deal

The US reached a

crisis point nearly

defaulting on public

debt

DJI dropped 634

pts. in 1 day

The Hang Seng

Index dropped

2,100 pts in 1 dayRise of ISIS in

the Middle East

and on the world

stage

2nd Libyan civil

war

US stocks sink

as oil price hits

$40

Charlie Hebdo

attack Paris

Russian

Financial Crisis

Russia made

incursions into

Ukraine

DJI dropped 9%

between 21 – 24

Aug

Greek banks

shut for 6 days

Bond yields

turned negative

as central banks

rolled out asset-

purchase

programs

Chinese stock

market slump

Deutsche

announces to

cut 9,000 jobs in

2015 - 2018

Investors retreat

from

commodities on

concerns over

China’s Growth.

Glencore

plunged 31% in

Oct.

“Brexit”

Source: Bloomberg, HSBC Global Asset Management as of 30th December 2016

Past performance is not an indication of future returns. The performance may go down as well as up

US

election

OPEC

meeting

21

Looking ahead – 2017 and beyond

Global economy remains in a state of fragile equilibrium with a low growth/inflation mix

Combination of reflationary policies, corporate fundamentals and compelling valuations form a supportive

backdrop for equities in the year ahead

Equity premiums look attractive in a low return world, especially when compared with government bonds

Emerging market equities, particularly in Asia, continue to stand out in terms of growth prospects, positive

earnings revisions and valuations

The Year of the Rooster will see an overhang from many of the risks that materialised in the previous year and

new ones including de-globalisation and potential policy missteps

On a longer time perspective, geopolitical events play much less important role than fundamentals and

economic and market development

22

Important Information

This presentation is intended for Professional Clients only and should not be distributed to or relied upon by Retail Clients.

The contents of this presentation are confidential and may not be reproduced or further distributed to any person or entity, whether in whole or in part, for

any purpose. The material contained herein is for information only and does not constitute investment advice or a recommendation to any reader of this

material to buy or sell investments. This document is not intended for distribution to or use by any person or entity in any jurisdiction or country where such

distribution or use would be contrary to law or regulation. This document is not and should not be construed as an offer to sell or the solicitation of an offer

to purchase or subscribe to any investment.

HSBC Global Asset Management has based this presentation on information obtained from sources it believes to be reliable but which it has not

independently verified HSBC Global Asset Management and HSBC Group accept no responsibility as to its accuracy or completeness.

This presentation is intended for discussion only and shall not be capable of creating any contractual or other legal obligations on the part of HSBC Global

Asset Management or any other HSBC Group company. Care has been taken to ensure the accuracy of this presentation but HSBC Global Asset

Management accepts no responsibility for any errors or omissions contained therein.

This presentation and any issues or disputes arising out of or in connection with it (whether such disputes are contractual or non-contractual in nature, such

as claims in tort, for breach of statute or regulation or otherwise) shall be governed by and construed in accordance with English law.

The views expressed above were held at the time of preparation and are subject to change without notice. Any forecast, projection or target where provided

is indicative only and is not guaranteed in any way. HSBC Global Asset Management accepts no liability for any failure to meet such forecast, projection or

target.

The value of investments and any income from them can go down as well as up and investors may not get back the amount originally invested. Where

overseas investments are held the rate of currency exchange may also cause the value of such investments to fluctuate. Stockmarket investments should

be viewed as a medium to long term investment and should be held for at least five years. Any performance information shown refers to the past and should

not be seen as an indication of future returns. The value of the underlying assets is strongly affected by interest rate fluctuations and by changes in the

credit ratings of the underlying issuer of the assets.

HSBC Global Asset Management (UK) Limited provides information to Institutions, Professional Advisers and their clients on the investment products and

services of the HSBC Group.

This presentation has been produced by HSBC Global Asset Management (Hong Kong) Limited and has been approved for issue in the United Kingdom by

HSBC Global Asset Management (UK) Limited. Authorised and regulated by the Financial Conduct Authority. www.assetmanagement.hsbc.com/uk

Copyright © HSBC Global Asset Management (UK) Limited 2017. All rights reserved 17-I-00274/SC/Asian EqCNY/26/01/2017/LB EXP 31/03/2017