Global Debates Playbook Asset Class Views (6 … O R G A N S T A N L E Y R E S E A R C H Global...

51

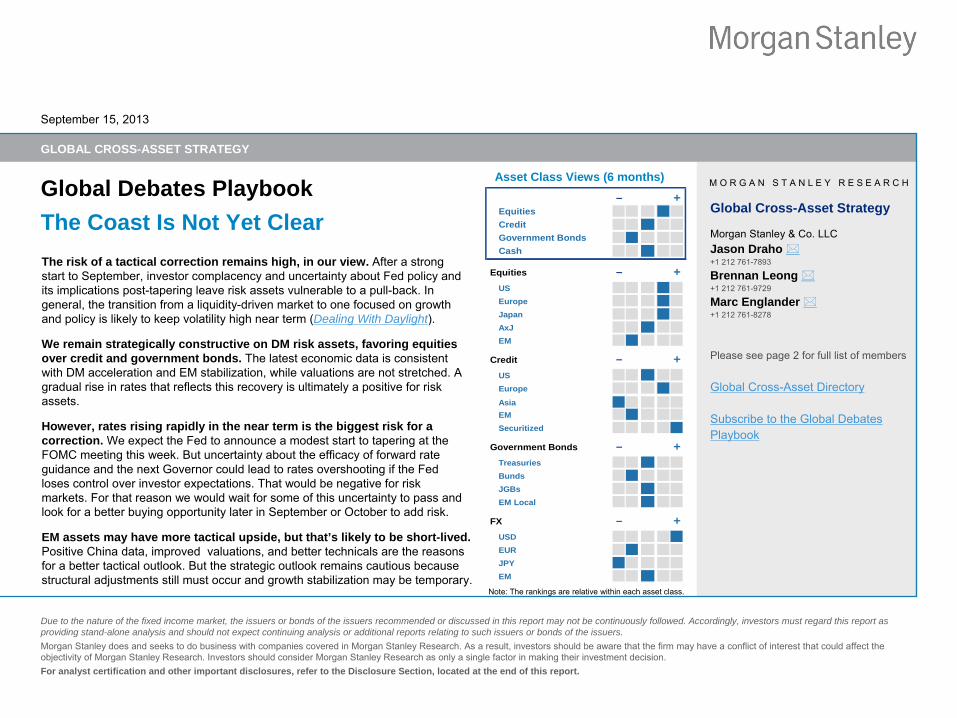

Global Debates Playbook The Coast Is Not Yet Clear M O R G A N S T A N L E Y R E S E A R C H September 15, 2013 GLOBAL CROSS-ASSET STRATEGY Due to the nature of the fixed income market, the issuers or bonds of the issuers recommended or discussed in this report may not be continuously followed. Accordingly, investors must regard this report as providing stand-alone analysis and should not expect continuing analysis or additional reports relating to such issuers or bonds of the issuers. Morgan Stanley does and seeks to do business with companies covered in Morgan Stanley Research. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of Morgan Stanley Research. Investors should consider Morgan Stanley Research as only a single factor in making their investment decision. For analyst certification and other important disclosures, refer to the Disclosure Section, located at the end of this report. Global Cross-Asset Strategy Morgan Stanley & Co. LLC Jason Draho +1 212 761-7893 Brennan Leong +1 212 761-9729 Marc Englander +1 212 761-8278 Please see page 2 for full list of members Global Cross-Asset Directory Subscribe to the Global Debates Playbook Asset Class Views (6 months) The risk of a tactical correction remains high, in our view. After a strong start to September, investor complacency and uncertainty about Fed policy and its implications post-tapering leave risk assets vulnerable to a pull-back. In general, the transition from a liquidity-driven market to one focused on growth and policy is likely to keep volatility high near term (Dealing With Daylight ). We remain strategically constructive on DM risk assets, favoring equities over credit and government bonds. The latest economic data is consistent with DM acceleration and EM stabilization, while valuations are not stretched. A gradual rise in rates that reflects this recovery is ultimately a positive for risk assets. However, rates rising rapidly in the near term is the biggest risk for a correction. We expect the Fed to announce a modest start to tapering at the FOMC meeting this week. But uncertainty about the efficacy of forward rate guidance and the next Governor could lead to rates overshooting if the Fed loses control over investor expectations. That would be negative for risk markets. For that reason we would wait for some of this uncertainty to pass and look for a better buying opportunity later in September or October to add risk. EM assets may have more tactical upside, but that’s likely to be short-lived. Positive China data, improved valuations, and better technicals are the reasons for a better tactical outlook. But the strategic outlook remains cautious because structural adjustments still must occur and growth stabilization may be temporary. Note: The rankings are relative within each asset class. – + Equities Credit Government Bonds Cash Equities – + US Europe Japan AxJ EM Credit – + US Europe Asia EM Securitized Government Bonds – + Treasuries Bunds JGBs EM Local FX – + USD EUR JPY EM

Transcript of Global Debates Playbook Asset Class Views (6 … O R G A N S T A N L E Y R E S E A R C H Global...

Global Debates PlaybookThe Coast Is Not Yet Clear

M O R G A N S T A N L E Y R E S E A R C H

September 15, 2013

GLOBAL CROSS-ASSET STRATEGY

Due to the nature of the fixed income market, the issuers or bonds of the issuers recommended or discussed in this report may not be continuously followed. Accordingly, investors must regard this report as providing stand-alone analysis and should not expect continuing analysis or additional reports relating to such issuers or bonds of the issuers.Morgan Stanley does and seeks to do business with companies covered in Morgan Stanley Research. As a result, investors should be

aware that the firm may have a conflict of interest that could affect the objectivity of Morgan Stanley Research. Investors should consider Morgan Stanley Research as only a single factor in making their investment decision.For analyst certification and other important disclosures, refer to the Disclosure Section, located at the end of this report.

Global Cross-Asset Strategy

Morgan Stanley & Co. LLCJason Draho +1 212 761-7893

Brennan Leong +1 212 761-9729

Marc Englander +1 212 761-8278

Please see page 2 for full list of members

Global Cross-Asset Directory

Subscribe to the Global Debates Playbook

Asset Class Views (6 months)

The risk of a tactical correction remains high, in our view. After a strong start to September,

investor complacency and uncertainty about Fed policy and its implications post-tapering leave risk assets vulnerable to a pull-back. In general, the transition from a liquidity-driven market to one focused on growth and policy is likely to keep volatility high near term (Dealing With Daylight).

We remain strategically constructive on DM risk assets, favoring equities over credit and government bonds. The latest economic data is consistent with DM acceleration and EM stabilization, while valuations are not stretched. A gradual rise in rates that reflects this recovery is ultimately a positive for risk assets.

However, rates rising rapidly in the near term is the biggest risk for a correction. We expect the Fed to announce a modest start to tapering at the FOMC meeting this week. But uncertainty about the efficacy of forward rate guidance and the next Governor could lead to rates overshooting if the Fed loses control over investor expectations. That would be negative

for risk markets. For that reason we would wait for some of this uncertainty to pass and look for a better buying opportunity later in September or October to add risk.

EM assets may have more tactical upside, but that’s likely to be short-lived. Positive China data, improved valuations, and better technicals

are the reasons for a better tactical outlook. But the strategic outlook remains

cautious because structural adjustments still must occur and growth stabilization

may be temporary.Note: The rankings are relative within each asset class.

– +EquitiesCreditGovernment BondsCash

Equities – +USEuropeJapanAxJEM

Credit – +USEurope

AsiaEMSecuritized

Government Bonds – +TreasuriesBundsJGBsEM Local

FX – +USDEURJPYEM

M O R G A N S T A N L E Y R E S E A R C H

Global Debates PlaybookSeptember 15, 2013

21 Morgan Stanley & Co. LLC

2 Morgan Stanley & Co. International plc 3 Morgan Stanley Asia Limited 4 Morgan Stanley Australia Ltd 5 Morgan Stanley MUFG Securities + Analysts employed by non-U.S. affiliates are not registered with FINRA, may not be associated persons of the member and may not be subject to NASD/NYSE restrictions on communications with a subject company, public appearances and trading securities held by a research analyst account.

Economics Joachim Fels2

+44 (0)20 7425 6138Vincent Reinhart1

+1 212 761 3537Elga

Bartsch2

+44 (0)20 7425 5434Robert Feldman5

+81 3 5424 5285Helen Qiao3

+852 2848 6511Chetan

Ahya3

+852 2239 7812Gray Newman1

+1 212 761 6510Tevfik

Aksoy2

+44 (0)20 7677-6917Manoj

Pradhan2

+44 (0)20 7425-3805

Strategy Neil McLeish2+

+44 (0)20 7677 7481Jason Draho1

+1 212 761-7893Matthew Hornbach1

+1 212 761-1837Anthony O’Brien2+

+44 (0)20 7677 7748Anton Heese2+

+44 (0)20 7677 6951Le Ngoc Nhan5+

+81 3 5424-7698Rashique

Rahman1

+1 212 761-6533Hans Redeker2+

+44 (0)20 7425 2430Gabriel de Kock1

+1 212 761-5154Adam Parker1

+1 212 761-1755Graham Secker2+

+44 (0)20 7425 6188Jonathan Garner3+ +852 2848 7288Adam Richmond1

+1 212 761-1485Andrew Sheets2+

+44 (0)20 7677 2905Viktor Hjort3+

+852 2848 7479Vishwanath

Tirupattur1

+1 212 761 1043Sivan Mahadevan1

+1 212 761 1349

Global Cross-Asset Strategy Market Commentary

3Morgan Stanley Key Economic Forecasts

18Morgan Stanley Asset Class Forecasts

19

Risk-Reward Views: EconomicsGlobal Economics

20US

21Europe

22Japan

23China

24Asia ex-Japan

25Brazil

26India

27Russia

28

Risk-Reward Views: Strategy US Rates

29Europe Rates

30Japan Rates

31UK Rates

32EM Fixed Income

33G10 Currency

34EM Currency

35US Equities

36Europe Equities

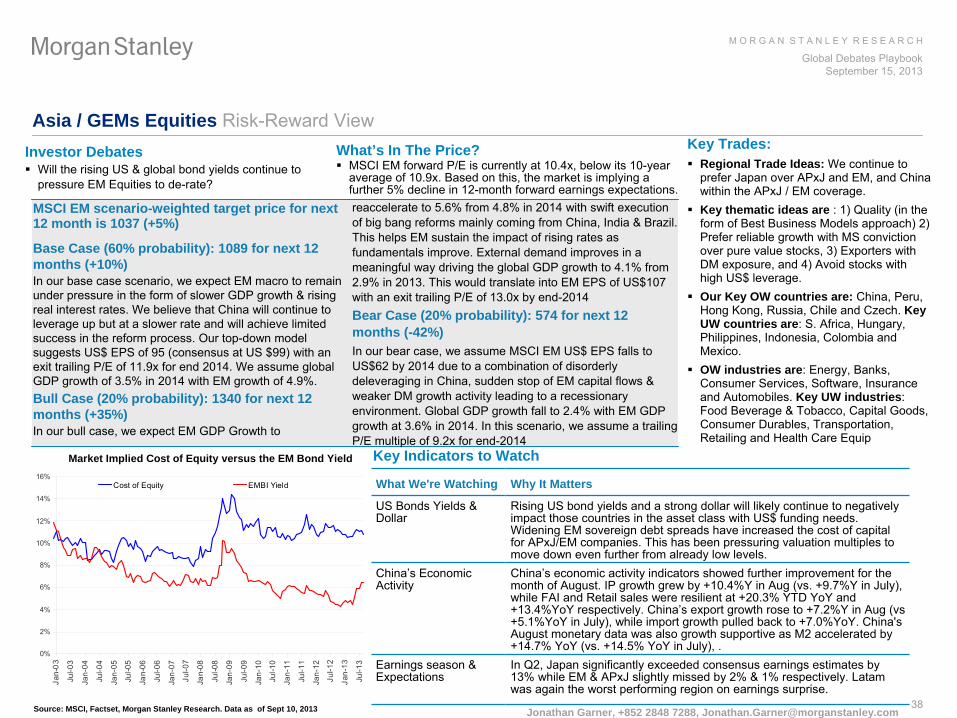

37Asia / GEMs

Equities

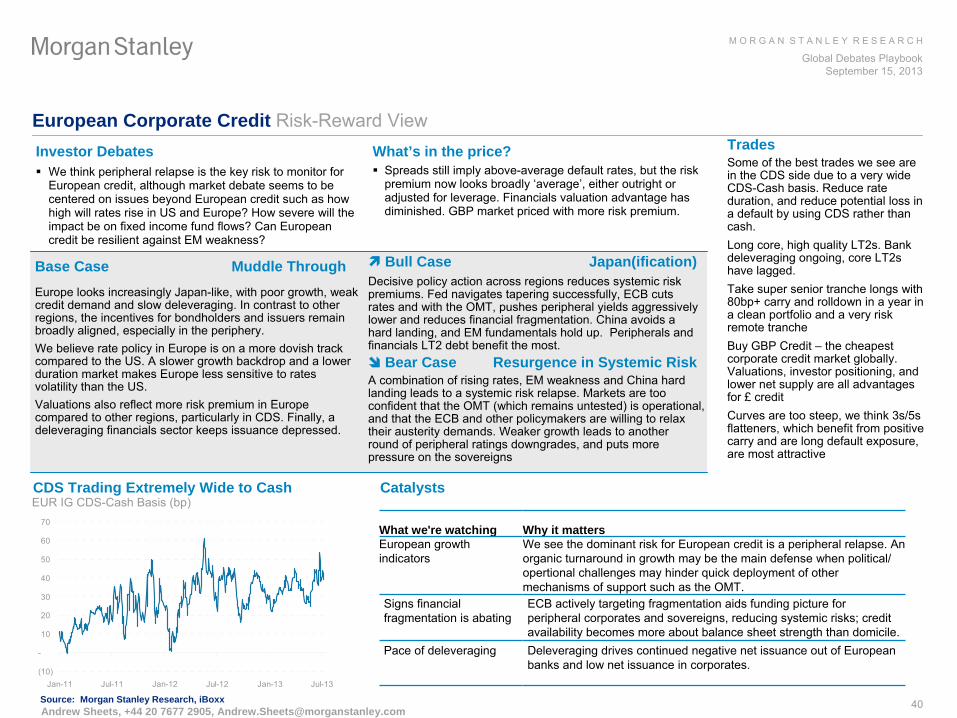

38US Corporate Credit 39Europe Corporate Credit

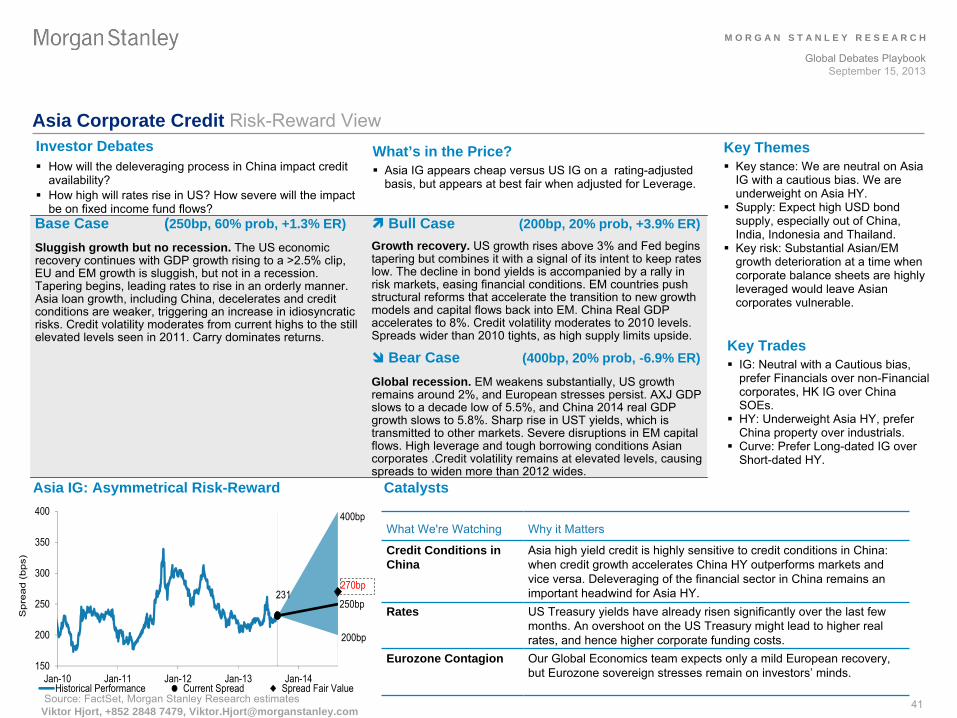

40Asia Corporate Credit

41Securitized Credit

42Global Credit Derivatives

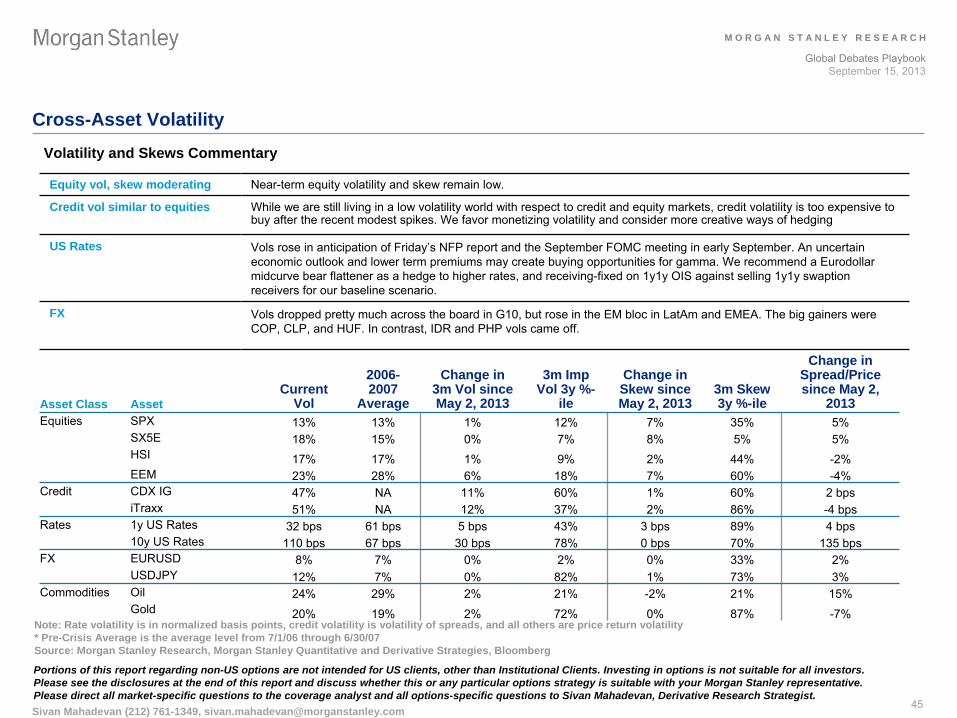

43Crude Oil 44Cross-Asset Volatility

45

Table of Contents Global Cross-Asset Strategy Group

M O R G A N S T A N L E Y R E S E A R C H

Global Debates PlaybookSeptember 15, 2013

3

The Coast Is Not Yet Clear

The risk of a tactical correction remains elevated, in our view. Improving PMIs

globally, better-than-expected data in China, and easing Middle East geopolitical tensions, and with it the price of oil, have certainly provided a tailwind for the markets to start September. Yet the primary reason for tactical caution that we laid out in our Back-to-School Global Strategy Outlook hasn’t changed (Dealing With Daylight, September 3). Specifically, that the transition from a liquidity-driven market to one focused on growth, policy and valuation differentials will be challenging, and keep volatility elevated near term. Investor complacency about downside risks –

the put-call ratio recently hit a YTD low (Exhibit 1) –

suggest otherwise, and that adds to the risk of a correction.

Rates that continue to rise is the biggest risk for a correction. The current risk rally in spite of rising rates is a positive development, if it reflects policy normalization and economic recovery (Exhibit 2). Three things concern us that this dynamic won’t continue to be so benign. First, the mid-cycle correction was relatively mild compared to other cycles when policy became less

accommodative. Second, uncertainty about Fed policy won’t fall with the likely tapering announcement this week, as it has already shifted to forward rate guidance and the next Governor. Third and related, this uncertainty could lead to rates overshooting if the Fed loses control over investor expectations. It’s hard to see risk assets not reacting negatively to that scenario.

EM assets have rebounded, but that’s likely to be short-lived. Positive China data, improved valuations, and better technicals

are the reasons why our EM fixed income strategy team just upgraded their tactical outlook for EM FX and local rates to Accumulate (Near-Term Stability, Medium-Term Adjustment). For now, the risk of an EM unwind is low without a big move in US rates. But the medium term outlook for EM remains cautious because structural adjustments still must occur, while China’s growth spurt may be temporary.

Tactical risks aside, we stay strategically constructive on developed markets. The latest economic data is consistent with DM acceleration and

EM stabilization. A gradual rise in rates that reflects this recovery is ultimately a positive for risk assets. But the uncertain transition to that stage should keep volatility elevated and possibly cause a correction. For that reason we would wait for a better buying opportunity later in September or October to add risk.

Exhibit 1: The low put-call ratio suggests investor complacency

Source: Bloomberg, Morgan Stanley Research

Exhibit 2: Equities and rates have risen in September

Source: Bloomberg, Morgan Stanley Research

0.4

0.5

0.6

0.7

0.8

0.9

Sep-12 Nov-12 Jan-13 Mar-13 May-13 Jul-13

Put-Call Ratio10-Day MA

1.40%

1.60%

1.80%

2.00%

2.20%

2.40%

2.60%

2.80%

3.00%

3.20%

1400

1450

1500

1550

1600

1650

1700

1750

Jan-13 Mar-13 May-13 Jul-13 Sep-13

S&P 500US 10yr (RHS)

M O R G A N S T A N L E Y R E S E A R C H

Global Debates PlaybookSeptember 15, 2013

4

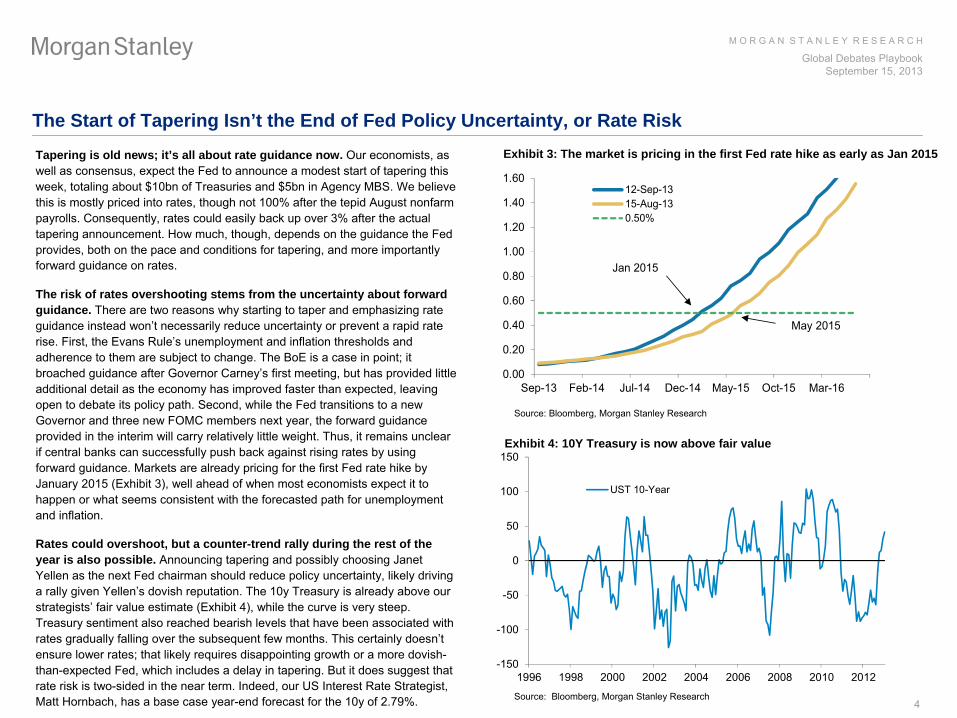

The Start of Tapering Isn’t the End of Fed Policy Uncertainty, or Rate Risk

Tapering is old news; it’s all about rate guidance now. Our economists, as well as consensus, expect the Fed to announce a modest start of tapering this week, totaling about $10bn of Treasuries and $5bn in Agency MBS.

We believe this is mostly priced into rates, though not 100% after the tepid August nonfarm payrolls. Consequently, rates could easily back up over 3% after

the actual tapering announcement. How much, though, depends on the guidance

the Fed provides, both on the pace and conditions for tapering, and more

importantly forward guidance on rates.

The risk of rates overshooting stems from the uncertainty about forward guidance. There are two reasons why starting to taper and emphasizing rate guidance instead won’t necessarily reduce uncertainty or prevent a rapid rate rise. First, the Evans Rule’s unemployment and inflation thresholds and adherence to them are subject to change. The BoE is a case in point; it broached guidance after Governor Carney’s first meeting, but has provided little additional detail as the economy has improved faster than expected, leaving open to debate its policy path. Second, while the Fed transitions to a new Governor and three new FOMC members next year, the forward guidance provided in the interim will carry relatively little weight. Thus, it remains unclear if central banks can successfully push back against rising rates by using forward guidance. Markets are already pricing for the first Fed rate hike by January 2015 (Exhibit 3), well ahead of when most economists expect it to happen or what seems consistent with the forecasted path for unemployment and inflation.

Rates could overshoot, but a counter-trend rally during the rest of the year is also possible. Announcing tapering and possibly choosing Janet Yellen

as the next Fed chairman should reduce policy uncertainty, likely driving a rally given Yellen’s

dovish reputation. The 10y Treasury is already above our strategists’

fair value estimate (Exhibit 4), while the curve is very steep.

Treasury sentiment also reached bearish levels that have been associated with rates gradually falling over the subsequent few months. This certainly doesn’t ensure lower rates; that likely requires disappointing growth or

a more dovish-

than-expected Fed, which includes a delay in tapering. But it does suggest that rate risk is two-sided in the near term. Indeed, our US Interest Rate Strategist,

Matt Hornbach, has a base case year-end forecast for the 10y of 2.79%.

Exhibit 3: The market is pricing in the first Fed rate hike as early as Jan 2015

Source: Bloomberg, Morgan Stanley Research

Exhibit 4: 10Y Treasury is now above fair value

Source: Bloomberg, Morgan Stanley Research

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

Sep-13 Feb-14 Jul-14 Dec-14 May-15 Oct-15 Mar-16

12-Sep-1315-Aug-130.50%

Jan 2015

May 2015

-150

-100

-50

0

50

100

150

1996 1998 2000 2002 2004 2006 2008 2010 2012

UST 10-Year

M O R G A N S T A N L E Y R E S E A R C H

Global Debates PlaybookSeptember 15, 2013

5

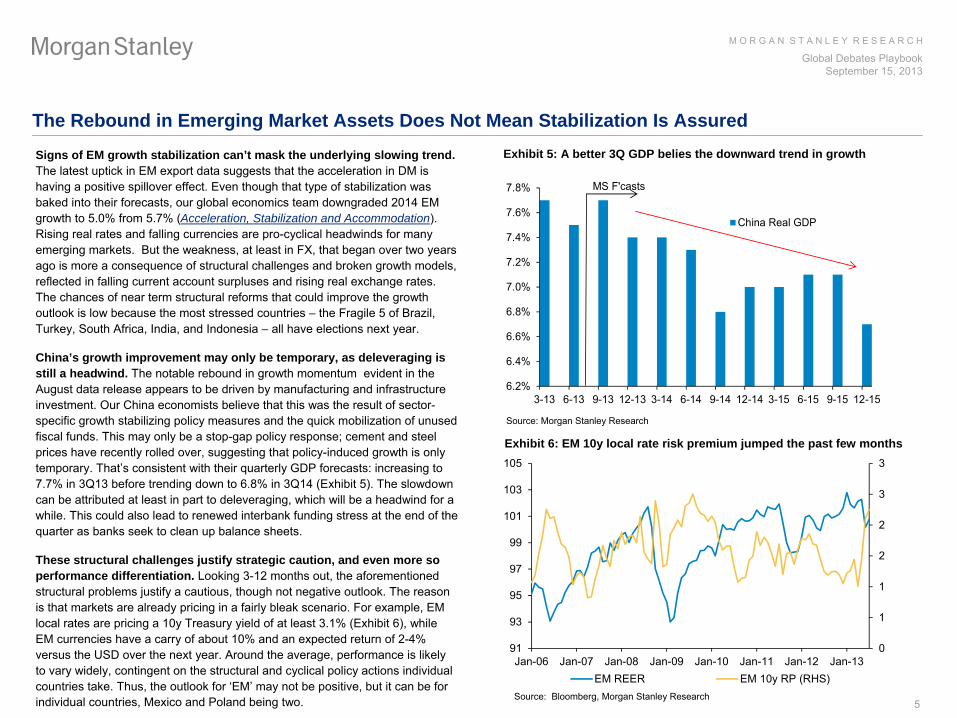

The Rebound in Emerging Market Assets Does Not Mean Stabilization Is Assured

Signs of EM growth stabilization can’t mask the underlying slowing trend. The latest uptick in EM export data suggests that the acceleration in DM is having a positive spillover effect. Even though that type of stabilization was baked into their forecasts, our

global economics team downgraded 2014 EM growth to 5.0% from 5.7% (Acceleration, Stabilization and Accommodation). Rising real rates and falling currencies are pro-cyclical headwinds for many emerging markets. But the weakness, at least in FX, that began over two years ago is more a consequence of structural challenges and broken growth models, reflected in falling current account surpluses and rising real exchange rates. The chances of near term structural reforms that could improve the growth outlook is low because the most stressed countries –

the Fragile 5 of Brazil, Turkey, South Africa, India, and Indonesia –

all have elections next year.

China’s growth improvement may only be temporary, as deleveraging is still a headwind. The notable rebound in growth momentum evident in the August data release appears to be driven by manufacturing and infrastructure investment. Our China economists believe that this was the result of sector-

specific growth stabilizing policy measures and the quick mobilization of unused fiscal funds. This may only be a stop-gap policy response; cement and steel prices have recently rolled over, suggesting that policy-induced growth is only temporary. That’s consistent with their quarterly GDP forecasts: increasing to 7.7% in 3Q13 before trending down to 6.8% in 3Q14 (Exhibit 5). The slowdown can be attributed at least in part to deleveraging, which will be a headwind for a while. This could also lead to renewed interbank funding stress at the end of the quarter as banks seek to clean up balance sheets.

These structural challenges justify strategic caution, and even more so performance differentiation. Looking 3-12 months out, the aforementioned structural problems justify a cautious, though not negative outlook. The reason is that markets are already pricing in a fairly bleak scenario. For example, EM local rates are pricing a 10y Treasury yield of at least 3.1% (Exhibit 6), while EM currencies have a carry of about 10% and an expected return of 2-4% versus the USD over the next year. Around the average, performance is likely to vary widely, contingent on the structural and cyclical policy

actions individual countries take. Thus, the outlook for ‘EM’

may not be positive, but it can be for individual countries, Mexico and Poland being two.

Exhibit 5: A better 3Q GDP belies the downward trend in growth

Source: Morgan Stanley Research

Exhibit 6: EM 10y local rate risk premium jumped the past few months

Source: Bloomberg, Morgan Stanley Research

0

1

1

2

2

3

3

91

93

95

97

99

101

103

105

Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13EM REER EM 10y RP (RHS)

6.2%

6.4%

6.6%

6.8%

7.0%

7.2%

7.4%

7.6%

7.8%

3-13 6-13 9-13 12-13 3-14 6-14 9-14 12-14 3-15 6-15 9-15 12-15

China Real GDP

MS F'casts

M O R G A N S T A N L E Y R E S E A R C H

Global Debates PlaybookSeptember 15, 2013

6

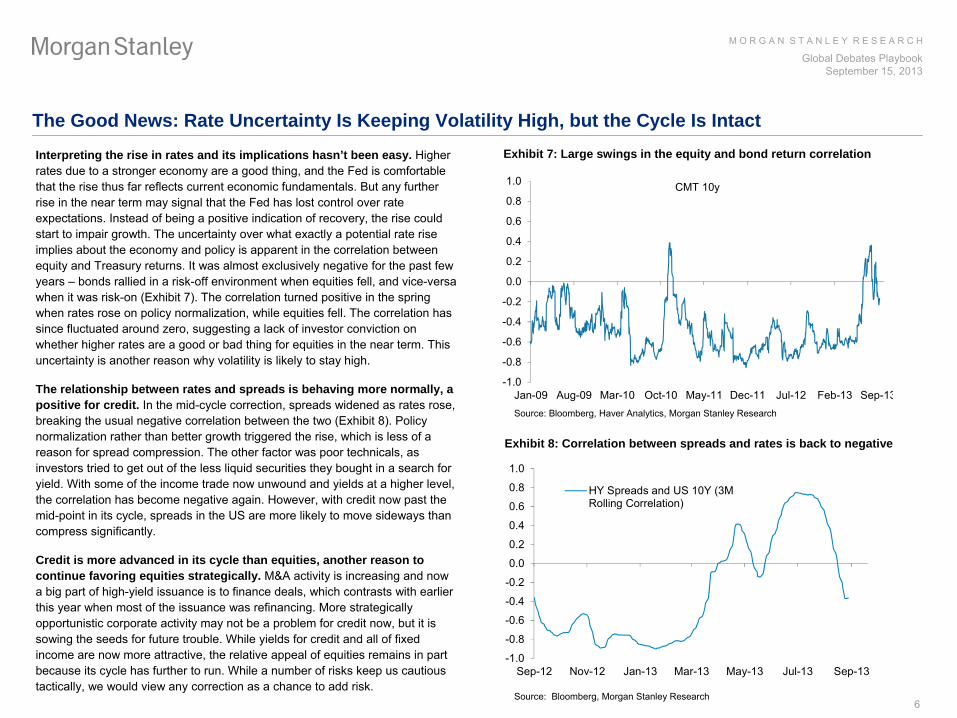

The Good News: Rate Uncertainty Is Keeping Volatility High, but the Cycle Is Intact

Interpreting the rise in rates and its implications hasn’t been easy. Higher rates due to a stronger economy are a good thing, and the Fed is comfortable that the rise thus far reflects current economic fundamentals. But any further rise in the near term may signal that the Fed has lost control over rate expectations. Instead of being a positive indication of recovery, the rise could start to impair growth. The uncertainty over what exactly a potential rate rise implies about the economy and policy is apparent in the correlation between equity and Treasury returns. It was almost exclusively negative for the past few years –

bonds rallied in a risk-off environment when equities fell, and vice-versa when it was risk-on (Exhibit 7). The correlation turned positive in the spring when rates rose on policy normalization, while equities fell. The correlation has since fluctuated around zero, suggesting a lack of investor conviction on whether higher rates are a good or bad thing for equities in the

near term. This uncertainty is another reason why volatility is likely to stay high.

The relationship between rates and spreads is behaving more normally, a positive for credit. In the mid-cycle correction, spreads widened as rates rose, breaking the usual negative correlation between the two (Exhibit

8). Policy normalization rather than better growth triggered the rise, which is less of a reason for spread compression. The other factor was poor technicals, as investors tried to get out of the less liquid securities they bought in a search for yield. With some of the income trade now unwound and yields at a

higher level, the correlation has become negative again. However, with credit now past the mid-point in its cycle, spreads in the US are more likely to move sideways than compress significantly.

Credit is more advanced in its cycle than equities, another reason to continue favoring equities strategically. M&A activity is increasing and now a big part of high-yield issuance is to finance deals, which contrasts with earlier

this year when most of the issuance was refinancing. More strategically opportunistic corporate activity may not be a problem for credit

now, but it is sowing the seeds for future trouble. While yields for credit and

all of fixed income are now more attractive, the relative appeal of equities remains in part because its cycle has further to run. While a number of risks keep us cautious tactically, we would view any correction as a chance to add risk.

Exhibit 7: Large swings in the equity and bond return correlation

Source: Bloomberg, Haver

Analytics, Morgan Stanley Research

Exhibit 8: Correlation between spreads and rates is back to negative

Source: Bloomberg, Morgan Stanley Research

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

Jan-09 Aug-09 Mar-10 Oct-10 May-11 Dec-11 Jul-12 Feb-13 Sep-13

CMT 10y

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

Sep-12 Nov-12 Jan-13 Mar-13 May-13 Jul-13 Sep-13

HY Spreads and US 10Y (3MRolling Correlation)

M O R G A N S T A N L E Y R E S E A R C H

Global Debates PlaybookSeptember 15, 2013

7

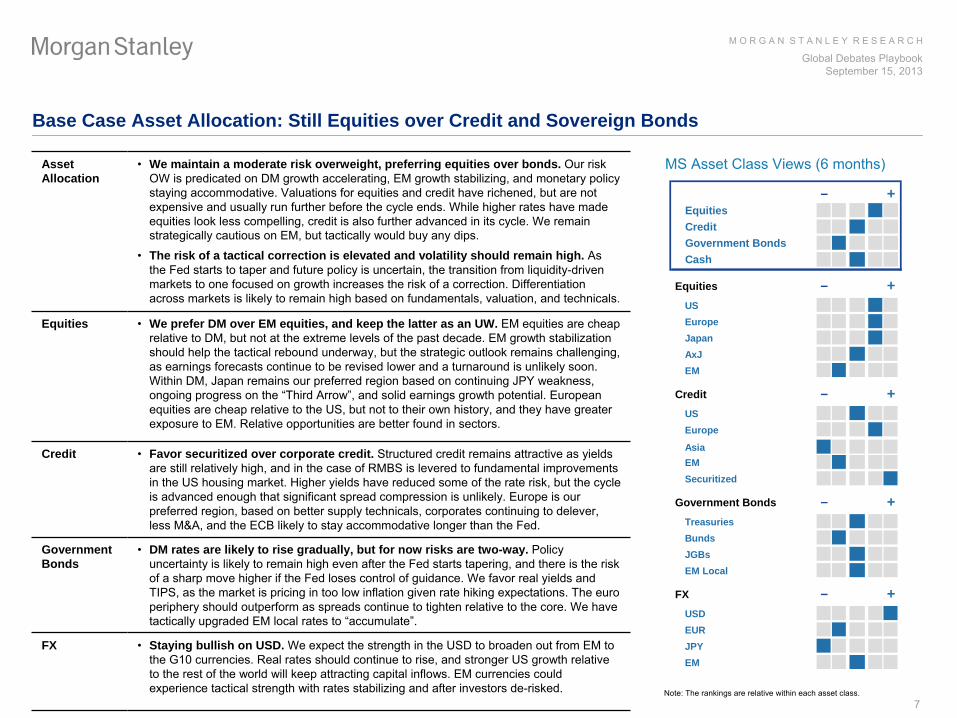

Base Case Asset Allocation: Still Equities over Credit and Sovereign Bonds

MS Asset Class Views (6 months)

Note: The rankings are relative within each asset class.

Asset Allocation

•

We maintain a moderate risk overweight, preferring equities over bonds. Our risk OW is predicated on DM growth accelerating, EM growth stabilizing, and monetary policy staying accommodative. Valuations for equities and credit have richened, but are not expensive and usually run further before the cycle ends. While higher rates have made equities look less compelling, credit is also further advanced in its cycle. We remain strategically cautious on EM, but tactically would buy any dips.

•

The risk of a tactical correction is elevated and volatility should remain high. As the Fed starts to taper and future policy is uncertain, the transition from liquidity-driven markets to one focused on growth increases the risk of a correction. Differentiation across markets is likely to remain high based on fundamentals, valuation, and technicals.

Equities •

We prefer DM over EM equities, and keep the latter as an UW. EM equities are cheap relative to DM, but not at the extreme levels of the past decade. EM growth stabilization should help the tactical rebound underway, but the strategic outlook remains challenging, as earnings forecasts continue to be revised lower and a turnaround is unlikely soon. Within DM, Japan remains our preferred region based on continuing JPY weakness, ongoing progress on the “Third Arrow”, and solid earnings growth potential. European equities are cheap relative to the US, but not to their own history, and they have greater exposure to EM. Relative opportunities are better found in sectors.

Credit •

Favor securitized over corporate credit. Structured credit remains attractive as yields are still relatively high, and in the case of RMBS is levered to

fundamental improvements in the US housing market. Higher yields have reduced some of the

rate risk, but the cycle is advanced enough that significant spread compression is unlikely. Europe is our preferred region, based on better supply technicals, corporates

continuing to delever, less M&A, and the ECB likely to stay accommodative longer than the Fed.

Government Bonds

•

DM rates are likely to rise gradually, but for now risks are two-way. Policy uncertainty is likely to remain high even after the Fed starts tapering, and there is the risk of a sharp move higher if the Fed loses control of guidance. We favor real yields and TIPS, as the market is pricing in too low inflation given rate hiking expectations. The euro periphery should outperform as spreads continue to tighten relative to the core. We have tactically upgraded EM local rates to “accumulate”.

FX •

Staying bullish on USD. We expect the strength in the USD to broaden out from EM to the G10 currencies. Real rates should continue to rise, and stronger US growth relative to the rest of the world will keep attracting capital inflows. EM currencies could experience tactical strength with rates stabilizing and after investors de-risked.

– +EquitiesCreditGovernment BondsCash

Equities – +USEuropeJapanAxJEM

Credit – +USEurope

AsiaEMSecuritized

Government Bonds – +TreasuriesBundsJGBsEM Local

FX – +USDEURJPYEM

M O R G A N S T A N L E Y R E S E A R C H

Global Debates PlaybookSeptember 15, 2013

8

•

The latest economic data supports DM growth acceleration and EM stabilizing, as the latter has experienced an uptick in exports and better responses from policy-

makers in the ‘Fragile Five’

(Brazil, India, Indonesia, South Africa, Turkey).

•

But EM is still weighed down by current accounts that remain sticky, and the negative feedback from the summer sell-off that has yet to be felt, while stable US rates and stronger China growth are likely to be temporary.

•

Higher rates could slow the US recovery, but not stall it. In particular, the housing recovery should stay resilient. The strong recovery in prices over the past year was likely to slow anyway, but housing affordability remains high, and the slowdown in new housing starts should be only temporary.

DM Growth Is Accelerating and EM Is Stabilizing for Now, but China’s Need to Delever Is a Headwind

Source: Federal Reserve, Morgan Stanley Research

Source: BIS, Morgan Stanley Research

Source: IMF, Markit, National Sources, Haver

Analytics, Morgan Stanley Research

EM exports are starting to grow again

US housing affordability is still relatively low after the rate rise China has built up a lot of leverage the past five years

Source: CEIC, CBRC, Wind, Morgan Stanley Research

PMIs

in DM are accelerating, only stabilizing in EM

30

35

40

45

50

55

60

Jun-03 Jun-05 Jun-07 Jun-09 Jun-11 Jun-13

DM EM

-50-40-30-20-10

0102030405060

Jun-03 Jun-05 Jun-07 Jun-09 Jun-11 Jun-13

AxJ

Latam

CEEMEA

10%

12%

14%

16%

18%

20%

22%

24%

26%

28%

30%

87 89 91 93 95 97 99 01 03 05 07 09 11 13

Monthly Paymentas % of IncomeLong-runAverage

20.8% 21.6% 20.6% 18.9% 18.6%

15.8% 25.0% 25.3% 24.6% 27.7%

73.6%81.1% 83.5% 84.7%

99.2%

34.5%

39.6%52.6% 51.9%

53.5%

11.9%

16.2%18.7% 18.8%

20.1%

0%

50%

100%

150%

200%

250%

2008 2009 2010 2011 2012

Central government Local governments Mid/large corporates

Small business Consumers

M O R G A N S T A N L E Y R E S E A R C H

Global Debates PlaybookSeptember 15, 2013

9

•

Volatility for all asset classes except for rates has stayed relatively contained since rising in the May/June correction. Rate volatility is likely to remain high until there is more clarity on the path of policy and forward guidance under the new Fed chairman.

•

The rise in volatility has had relatively little effect on cross-asset correlations, which have fallen sharply over the past year to pre-

crisis levels. Differentiation in performance across markets should remain high as valuations are around fair value, with company, sector and country fundamentals being the main driver.

•

High rate volatility could continue to weigh on other markets, including equities, as it’s a proxy for the uncertainty about Fed policy and implications.

Fed Policy Uncertainty Will Keep Volatilities High, but Not a ‘Market of One’

Source: Bloomberg, Morgan Stanley Research

Source: Bloomberg, Morgan Stanley Research

Source: Bloomberg, Morgan Stanley Research

Cross-asset correlations remain moderate

Higher rates volatility has corresponded to equity weakness

35%

40%

45%

50%

55%

60%

65%

70%

75%

03 04 05 06 07 08 09 10 11 12 13

%var explained by 1st principal component

-1.00

-0.80

-0.60

-0.40

-0.20

0.00

0.20

0.40

0.60

0.80

Jan-10 Aug-10 Mar-11 Oct-11 May-12 Dec-12 Jul-13

30d Correlation

90100110120130140150160170180190200210220

1 6 11 16 21 26 31 36 41 46 51 56 61 66 71 76 81 86 91

EquityFXRatesCredit

Indexed to 100 as of most recent trough

Days Since Trough

Volatilities for all asset classes have risen recently

M O R G A N S T A N L E Y R E S E A R C H

Global Debates PlaybookSeptember 15, 2013

10

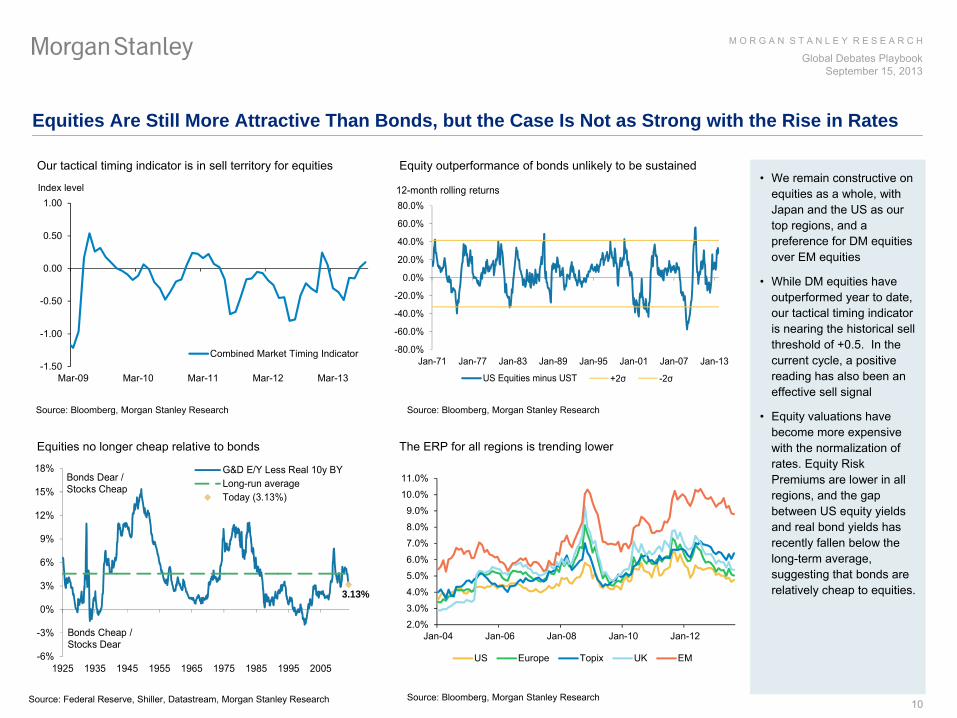

•

We remain constructive on equities as a whole, with Japan and the US as our top regions, and a preference for DM equities over EM equities

•

While DM equities have outperformed year to date, our tactical timing indicator is nearing the historical sell threshold of +0.5. In the current cycle, a positive reading has also been an effective sell signal

•

Equity valuations have become more expensive with the normalization of rates. Equity Risk Premiums are lower in all regions, and the gap between US equity yields and real bond yields has recently fallen below the long-term average, suggesting that bonds are relatively cheap to equities.

Equities Are Still More Attractive Than Bonds, but the Case Is Not as Strong with the Rise in Rates

Source: Bloomberg, Morgan Stanley Research

Source: Federal Reserve, Shiller, Datastream, Morgan Stanley Research

Source: Bloomberg, Morgan Stanley Research

Equity outperformance of bonds unlikely to be sustained

Equities no longer cheap relative to bonds The ERP for all regions is trending lower

Source: Bloomberg, Morgan Stanley Research

-1.50

-1.00

-0.50

0.00

0.50

1.00

Mar-09 Mar-10 Mar-11 Mar-12 Mar-13

Combined Market Timing Indicator

Index level

-80.0%

-60.0%

-40.0%

-20.0%

0.0%

20.0%

40.0%

60.0%

80.0%

Jan-71 Jan-77 Jan-83 Jan-89 Jan-95 Jan-01 Jan-07 Jan-13

US Equities minus UST +2σ -2σ

12-month rolling returns

3.13%

-6%

-3%

0%

3%

6%

9%

12%

15%

18%

1925 1935 1945 1955 1965 1975 1985 1995 2005

G&D E/Y Less Real 10y BYLong-run averageToday (3.13%)

Bonds Cheap / Stocks Dear

Bonds Dear / Stocks Cheap

Our tactical timing indicator is in sell territory for equities

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

11.0%

Jan-04 Jan-06 Jan-08 Jan-10 Jan-12

US Europe Topix UK EM

M O R G A N S T A N L E Y R E S E A R C H

Global Debates PlaybookSeptember 15, 2013

11

•

The rise in rates has pushed Treasury, Bund, and Gilt yields back around fair value. The 2s10s curve in the US is also within about 40bps of its high over the past 40 years. Neither of these factors would keep 10y yields from overshooting if the Fed makes a policy mistake, but they do suggest an upper limit of how far rates will rise.

•

Sentiment on Treasuries remains very bearish. When sentiment was at this level during the past decade, the 10y yield gradually drifted about 40bps lower over the subsequent six months. Since sentiment recently troughed, the yield has gone even higher.

Fed Policy Mistakes Could Lead to Higher Rates, but the Upside Looks Limited Near Term

Source: Bloomberg, Morgan Stanley Research

Source: Bloomberg, Morgan Stanley Research

Source: US Economics Team, Morgan Stanley Research

The yield curve is also very steep

Investor bearishness on Treasuries is high… …and that has corresponded to rates drifting lower

Source: Bloomberg, Morgan Stanley Research

Treasury, Bund and Gilt 10y yields are back to fair value

-200

-150

-100

-50

0

50

100

150

200

1996 1998 2000 2002 2004 2006 2008 2010 2012

UST 10-YearDBR 10-Year

-300

-200

-100

0

100

200

300

400

76 79 82 85 88 91 94 97 00 03 06 09 12

2s10s curve

0102030405060708090

100

Jan-03 Jan-06 Jan-09 Jan-12T-Bonds 20-day MA

% of traders bullish

-50-40-30-20-10

0102030405060

t + 0 t + 30 t + 60 t + 90 t + 120

Average since 2003

Bps change in 10-year yield since July 1

Basis point change from bearish sentiment reading

M O R G A N S T A N L E Y R E S E A R C H

Global Debates PlaybookSeptember 15, 2013

12

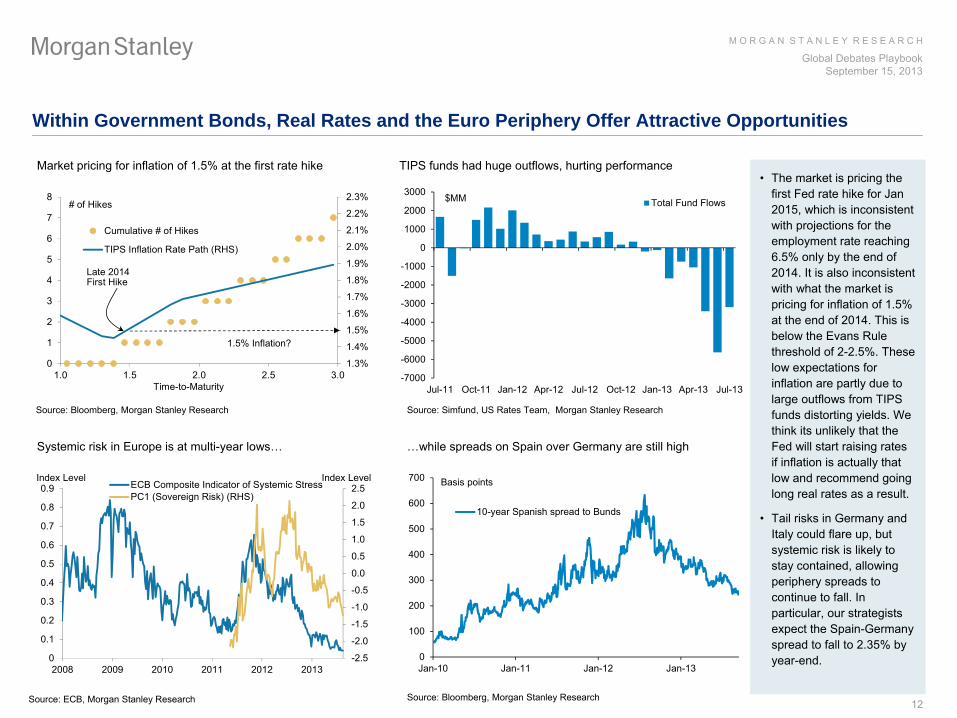

•

The market is pricing the first Fed rate hike for Jan 2015, which is inconsistent with projections for the employment rate reaching 6.5% only by the end of 2014. It is also inconsistent with what the market is pricing for inflation of 1.5% at the end of 2014. This is below the Evans Rule threshold of 2-2.5%. These low expectations for inflation are partly due to large outflows from TIPS funds distorting yields. We think its unlikely that the Fed will start raising rates if inflation is actually that low and recommend going long real rates as a result.

•

Tail risks in Germany and Italy could flare up, but systemic risk is likely to stay contained, allowing periphery spreads to continue to fall. In particular, our strategists expect the Spain-Germany spread to fall to 2.35% by year-end.

Within Government Bonds, Real Rates and the Euro Periphery Offer Attractive Opportunities

Source: Simfund, US Rates Team, Morgan Stanley Research

Source: ECB, Morgan Stanley Research

Source: Bloomberg, Morgan Stanley Research

Systemic risk in Europe is at multi-year lows…

Source: Bloomberg, Morgan Stanley Research

Market pricing for inflation of 1.5% at the first rate hike TIPS funds had huge outflows, hurting performance

-7000

-6000

-5000

-4000

-3000

-2000

-1000

0

1000

2000

3000

Jul-11 Oct-11 Jan-12 Apr-12 Jul-12 Oct-12 Jan-13 Apr-13 Jul-13

Total Fund Flows$MM

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

2008 2009 2010 2011 2012 2013

Index LevelIndex Level ECB Composite Indicator of Systemic StressPC1 (Sovereign Risk) (RHS)

0

100

200

300

400

500

600

700

Jan-10 Jan-11 Jan-12 Jan-13

10-year Spanish spread to Bunds

Basis points

…while spreads on Spain over Germany are still high

1.3%

1.4%

1.5%

1.6%

1.7%

1.8%

1.9%

2.0%

2.1%

2.2%

2.3%

0

1

2

3

4

5

6

7

8

1.0 1.5 2.0 2.5 3.0

Cumulative # of Hikes

TIPS Inflation Rate Path (RHS)

# of Hikes

Time-to-Maturity

Late 2014 First Hike

1.5% Inflation?

M O R G A N S T A N L E Y R E S E A R C H

Global Debates PlaybookSeptember 15, 2013

13

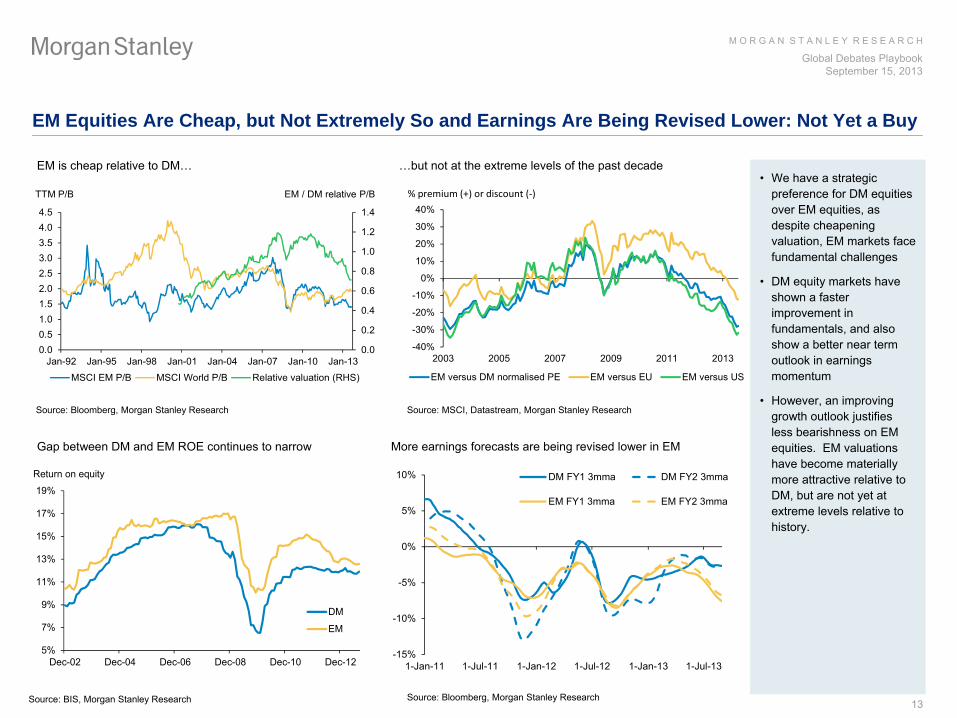

•

We have a strategic preference for DM equities over EM equities, as despite cheapening valuation, EM markets face fundamental challenges

•

DM equity markets have shown a faster improvement in fundamentals, and also show a better near term outlook in earnings momentum

•

However, an improving growth outlook justifies less bearishness on EM equities. EM valuations have become materially more attractive relative to DM, but are not yet at extreme levels relative to history.

EM Equities Are Cheap, but Not Extremely So and Earnings Are Being Revised Lower: Not Yet a Buy

Source: MSCI, Datastream, Morgan Stanley Research

Source: BIS, Morgan Stanley Research

Source: Bloomberg, Morgan Stanley Research

…but not at the extreme levels of the past decade

Gap between DM and EM ROE continues to narrow More earnings forecasts are being revised lower in EM

Source: Bloomberg, Morgan Stanley Research

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

0.00.51.01.52.02.53.03.54.04.5

Jan-92 Jan-95 Jan-98 Jan-01 Jan-04 Jan-07 Jan-10 Jan-13

MSCI EM P/B MSCI World P/B Relative valuation (RHS)

TTM P/B EM / DM relative P/B

-15%

-10%

-5%

0%

5%

10%

1-Jan-11 1-Jul-11 1-Jan-12 1-Jul-12 1-Jan-13 1-Jul-13

DM FY1 3mma DM FY2 3mma

EM FY1 3mma EM FY2 3mma

5%

7%

9%

11%

13%

15%

17%

19%

Dec-02 Dec-04 Dec-06 Dec-08 Dec-10 Dec-12

DM

EM

Return on equity

EM is cheap relative to DM…

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

2003 2005 2007 2009 2011 2013

EM versus DM normalised PE EM versus EU EM versus US

% premium (+) or discount (‐)

M O R G A N S T A N L E Y R E S E A R C H

Global Debates PlaybookSeptember 15, 2013

14

•

We are overweight both US and European equities, with an improving European outlook justifying a more bullish stance

•

However, valuations for both US and European equities are close to long-

term averages, although European equities remain slightly cheaper than those of the US

•

One of the many reasons one may consider an overweight in Europe relative to the US is lower valuation and a high recovery potential –

this is very obvious in a sector like the Financials, with notable gaps in forward P/Es and ROE

Europe’s Outlook Has Improved, but European Equities Aren’t a Better Buy Than the US

Source: , Morgan Stanley Research

Source: IBES, MSCI, Datastream, Morgan Stanley Research

Source: Morgan Stanley Research

Europe’s ROE is lower, an opportunity and constraint

Europe Financials are relatively cheap to the US…

Source: MSCI, Datastream, Morgan Stanley Research

US and Europe both near long-term average valuations

…and the lower ROE should improve with the recovery

-2.00

-1.50

-1.00

-0.50

0.00

0.50

1.00

1.50

2.00

ROE TTM P/E P/Book P/Cash D/YUSA Europe

Z-Score

-15%

-10%

-5%

0%

5%

10%

15%

20%

Jan-04 Jan-06 Jan-08 Jan-10 Jan-12

Europe Financials

US Financials0

5

10

15

20

25

Jan-95 Jan-98 Jan-01 Jan-04 Jan-07 Jan-10 Jan-13

US Financials

EU Financials

NTM P/E

5%

7%

9%

11%

13%

15%

17%

19%

Dec-02 Dec-04 Dec-06 Dec-08 Dec-10 Dec-12

US

Europe

M O R G A N S T A N L E Y R E S E A R C H

Global Debates PlaybookSeptember 15, 2013

15

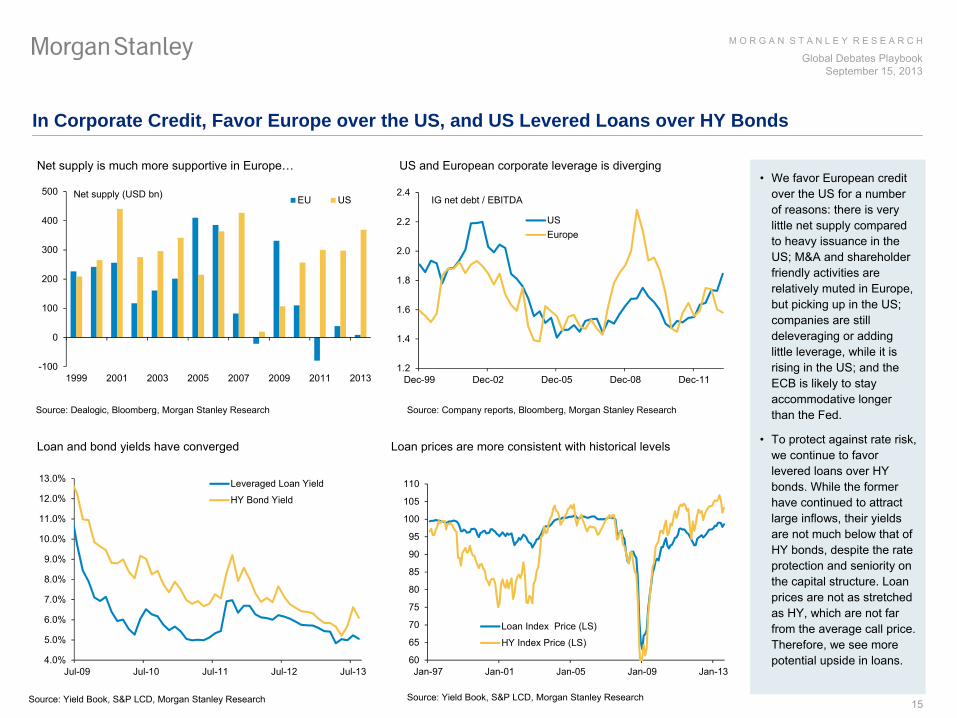

•

We favor European credit over the US for a number of reasons: there is very little net supply compared to heavy issuance in the US; M&A and shareholder friendly activities are relatively muted in Europe, but picking up in the US; companies are still deleveraging or adding little leverage, while it is rising in the US; and the ECB is likely to stay accommodative longer than the Fed.

•

To protect against rate risk, we continue to favor levered loans over HY bonds. While the former have continued to attract large inflows, their yields are not much below that of HY bonds, despite the rate protection and seniority on the capital structure. Loan prices are not as stretched as HY, which are not far from the average call price. Therefore, we see more potential upside in loans.

In Corporate Credit, Favor Europe over the US, and US Levered Loans over HY Bonds

Source: Company reports, Bloomberg, Morgan Stanley Research

Source: Yield Book, S&P LCD, Morgan Stanley Research

Source: Dealogic, Bloomberg, Morgan Stanley Research

US and European corporate leverage is diverging

Loan and bond yields have converged Loan prices are more consistent with historical levels

Source: Yield Book, S&P LCD, Morgan Stanley Research

Net supply is much more supportive in Europe…

-100

0

100

200

300

400

500

1999 2001 2003 2005 2007 2009 2011 2013

EU USNet supply (USD bn)

1.2

1.4

1.6

1.8

2.0

2.2

2.4

Dec-99 Dec-02 Dec-05 Dec-08 Dec-11

USEurope

IG net debt / EBITDA

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

11.0%

12.0%

13.0%

Jul-09 Jul-10 Jul-11 Jul-12 Jul-13

Leveraged Loan Yield

HY Bond Yield

60

65

70

75

80

85

90

95

100

105

110

Jan-97 Jan-01 Jan-05 Jan-09 Jan-13

Loan Index Price (LS)

HY Index Price (LS)

M O R G A N S T A N L E Y R E S E A R C H

Global Debates PlaybookSeptember 15, 2013

16

•

EM FX and local rates have both cheapened significantly and are pricing in fairly bearish scenarios. EM currencies have a carry of about 10% and an expected return of 2-4% versus the USD over the next year. Local rates are pricing in a 10y Treasury yield of at least 3.1%. Better valuations, combined with stabilizing in US rates and China and investors building better cash positions, warranted a tactical upgrade to both.

•

However, much of EM still faces structural challenges, primarily stemming from a loss of competitiveness from rising real exchange rates, leading to smaller current account surpluses and slower FX reserve accumulation. Countries that undertake policy reforms to address these problems are likely to outperform in risk markets.

Valuations Help the Tactical Appeal of EM Fixed Income, but Not Enough to Offset Structural Issues

Source: Bloomberg, Morgan Stanley Research

Note: EM yields compiled from Turkey, South Africa, Poland, Hungary, Indonesia, Malaysia, Thailand, South Korea, and Mexico. DM refers to the US and Germany

Source: Bloomberg, Morgan Stanley Research

Source: US Economics Team, Morgan Stanley Research

Real exchanges rates are lower, especially for Fragile 5 But the growth in EM central bank reserves has halted

Source: Haver

Analytics, Morgan Stanley Research Note: Assumes IMF COFER weights

Average carry for EM FX is up over 3% the past few months EM local bonds now offer good value relative to DM

-10%-5%0%5%

10%15%20%25%30%35%

Jan-05 Jan-07 Jan-09 Jan-11 Jan-13AXJ (ex China) CEEMEA LatAm

YoY change in EM Central Bank FX Reserves

1.5%

2.5%

3.5%

4.5%

5.5%

6.5%

7.5%

8.5%

87

89

91

93

95

97

99

101

103

105

107

Jan-10 Aug-10 Mar-11 Oct-11 May-12 Dec-12 Jul-13

USD/EM

EMFX Avg Carry (Implied ForwardRate, RHS)

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

Apr-09 Nov-09 Jun-10 Jan-11 Aug-11 Mar-12 Oct-12 May-13EM-DM Spread (RHS) EM 10y DM 10y

80

85

90

95

100

105

110

115

120

Jan 03 Jun 04 Nov 05 Apr 07 Sep 08 Feb 10 Jul 11 Dec 12

EM REERFragile Five REER

M O R G A N S T A N L E Y R E S E A R C H

Global Debates PlaybookSeptember 15, 2013

17

Risk-Reward Views

M O R G A N S T A N L E Y R E S E A R C H

Global Debates PlaybookSeptember 15, 2013

18Source: Morgan Stanley Research forecasts

Note: *US GDP forecast for current quarter is tracking estimate.

**Global is comprised of G10, BRICs, and Korea

Economic Forecasts

2012 2013E 2014EReal GDP (%Q, SAAR) Bear Base Bull Base 3QE 4QE 1QE 2QE 3QE 4QEGlobal 3.2 2.6 2.9 3.2 3.5 3.8 3.7 3.4 3.2 3.7 3.9G10 1.5 0.8 1.0 1.2 2.0 1.7 2.1 2.3 1.5 1.9 2.1

US 2.8 1.6 1.6 1.7 2.7 2.1 2.7 2.8 2.9 2.8 2.8Euro Area -0.5 -0.7 -0.5 -0.3 0.9 0.4 0.9 0.9 1.0 1.2 1.2Japan 2.0 1.1 1.6 1.8 1.3 2.2 2.9 3.3 -3.5 0.3 1.3UK 0.2 1.3 1.4 1.5 2.4 3.6 2.0 2.4 2.0 2.0 2.0

EM (%Y) 4.9 4.2 4.8 5.1 4.9 5.0 4.5 4.7 4.9 4.8 5.1China (%Y) 7.7 7.0 7.6 7.7 7.1 7.7 7.4 7.4 7.3 6.8 7.0India (%Y) 5.1 4.1 4.4 4.6 4.6 4.5 3.9 3.8 4.2 5.0 5.1Brazil (%Y) 0.9 1.5 2.1 2.4 1.7 1.8 1.5 1.9 0.6 2.3 2.0Russia (%Y) 3.4 1.5 2.2 2.9 3.1 2.4 2.9 3.4 3.9 3.0 2.8

Consumer Price Inflation (%Y)Global 3.3 2.9 3.3 3.4 3.0 3.2 3.3 3.2 3.5 3.3 3.3G10 1.9 1.4 1.5 1.6 1.7 1.8 1.5 1.3 1.5 1.5 1.4

US 2.1 1.5 1.6 1.6 1.4 1.6 1.5 1.3 1.7 1.4 1.3Euro Area 2.5 1.5 1.5 1.6 1.6 1.4 1.5 1.6 1.8 1.5 1.4Japan -0.1 -0.1 0.2 0.4 2.3 0.5 0.7 0.8 2.8 2.7 2.7UK 2.8 2.7 2.7 2.7 2.7 2.8 2.6 2.6 2.8 2.8 2.6

EM 4.8 4.4 5.1 5.2 4.3 4.6 5.0 5.0 5.4 5.0 5.0China 2.6 1.5 2.6 2.6 1.8 3.0 2.6 1.5 2.2 1.9 1.5India 9.3 10.2 10.8 11.6 7.4 10.9 9.9 8.3 8.0 6.7 6.5Brazil 5.4 6.0 6.2 6.5 6.1 6.1 5.8 5.8 5.8 6.2 6.5Russia 5.1 6.0 6.5 7.0 4.9 6.1 5.5 5.2 4.8 4.7 5.0

Monetary Policy Rate (% p.a.)Global 3.3 2.9 2.9 3.0 2.9 2.8 2.9 2.8 2.9G10 0.6 0.5 0.3 0.5 0.5 0.4 0.4 0.3 0.3

US 0.2 0.2 0.2 0.2 0.2 0.2 0.2 0.2 0.2Euro Area 0.8 0.3 0.3 0.5 0.3 0.3 0.3 0.3 0.3Japan 0.1 0.1 0.1 0.1 0.1 0.1 0.1 0.1 0.1UK 0.5 0.5 0.5 0.5 0.5 0.5 0.5 0.5 0.5

EM 6.2 5.4 5.5 5.7 5.4 5.4 5.5 5.5 5.5China 6.0 6.0 5.5 6.0 6.0 6.0 5.8 5.8 5.5India 8.0 7.3 7.3 7.3 7.3 7.3 7.3 7.3 7.3Brazil 7.3 9.8 9.8 9.0 9.8 9.8 9.8 9.8 9.8Russia 5.5 5.0 4.8 5.3 5.0 4.8 4.8 4.8 4.8

2014E2013EAnnual Quarterly

M O R G A N S T A N L E Y R E S E A R C H

Global Debates PlaybookSeptember 15, 2013

19Source: Morgan Stanley Research forecasts

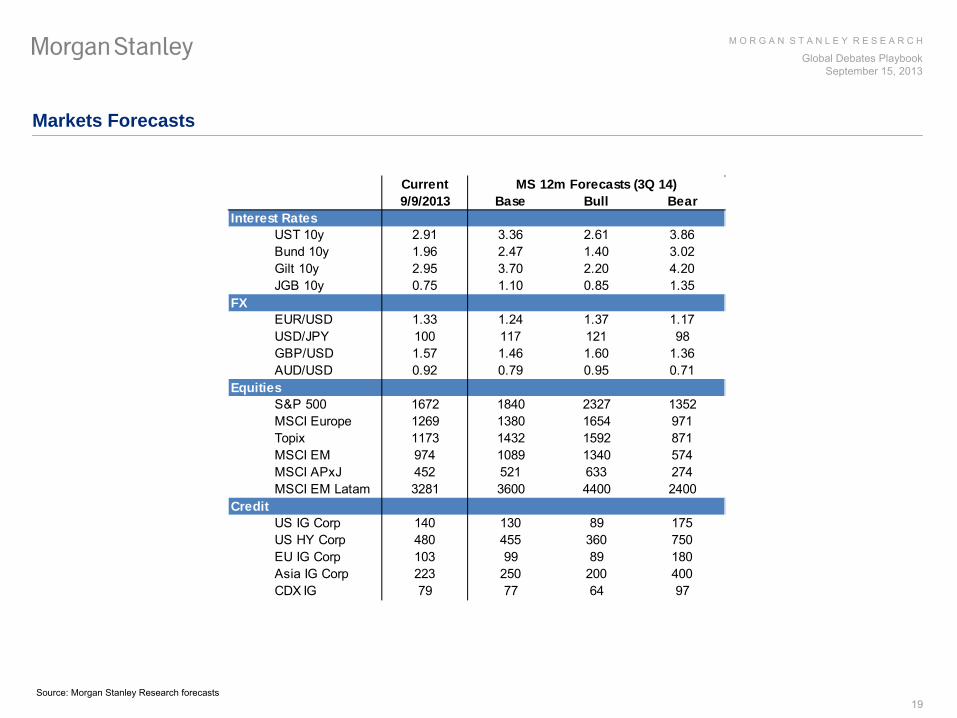

Markets Forecasts

Current9/9/2013 Base Bull Bear

Interest RatesUST 10y 2.91 3.36 2.61 3.86Bund 10y 1.96 2.47 1.40 3.02Gilt 10y 2.95 3.70 2.20 4.20JGB 10y 0.75 1.10 0.85 1.35

FXEUR/USD 1.33 1.24 1.37 1.17USD/JPY 100 117 121 98GBP/USD 1.57 1.46 1.60 1.36AUD/USD 0.92 0.79 0.95 0.71

EquitiesS&P 500 1672 1840 2327 1352MSCI Europe 1269 1380 1654 971Topix 1173 1432 1592 871MSCI EM 974 1089 1340 574MSCI APxJ 452 521 633 274MSCI EM Latam 3281 3600 4400 2400

CreditUS IG Corp 140 130 89 175US HY Corp 480 455 360 750EU IG Corp 103 99 89 180Asia IG Corp 223 250 200 400CDX IG 79 77 64 97

MS 12m Forecasts (3Q 14)

M O R G A N S T A N L E Y R E S E A R C H

Global Debates PlaybookSeptember 15, 2013

20

Global Economics Risk-Reward ViewInvestor Debates

DM: How long can monetary policy stay accommodative?

US: What is the profile for tapering?

ECB: Further easing measures to go?

Japan: What next for the consumption tax?

EM: Is stabilization finally here?

What’s in the price?

Central banks’

forward guidance being discounted by markets.

Fed tapering likely to be accompanied by attempt to prevent another rise in interest rates.

Markets not pricing more easing measures from the ECB.

Markets question Japan’s ability to deliver on structural reforms.

Weaker US payrolls numbers mean EM markets adequatelyreflect near-term risk.

Signposts

September 18, 2013 FOMC meeting, SEP and press conference

September 22, 2013 German parliamentary elections

October 2, 2013 ECB council meeting and press conference

October 2013Japan deadline for decision on consumption tax hike timing

November 2013Third Plenary session of 18th

Central Committee of CPC

February 1, 2014 Term begins for new chairman of the US Federal Reserve

March 1, 2014 ECB expected to assume supervisory tasks within Single Supervisory Mechanism

Joachim Fels, Manoj Pradhan (44 207) 425-6138, [email protected]

Key Indicators A Global Expansion Now Led by DM Growth

Source: Morgan Stanley Research

Base Case 2014 Global GDP: 3.5%We recently downgraded our global GDP forecasts by two-

tenths to 2.9% for 2013 and four-tenths to 3.5% for 2014. Our global narrative for the next 6-12 months rests on three pillars: An acceleration of growth in DM, stabilisation

in EM economies (with downside risks) and continued accommodation by central banks.

We continue to expect the DM economies to accelerate from twilight to daylight, taking leadership of the global economic cycle. EM growth should stabilise at a lower level, although we remain concerned about the structural and cyclical fragilities. Global monetary policy is likely to remain accommodative, as DM central banks are likely to continue to push back on market expectations of earlier rate hikes.

Bull Case 2014 Global GDP: 4.1%In our bull scenario, benign US rates, sustained growth in China, and encouraging progress on EM reforms propel a more rapid acceleration to above 4% GDP growth in 2014.

Bear Case 2014 Global GDP: 2.4%In our bear scenario, US bond yields surge sharply to around 4.0% in the next few months and China growth slows down into a 5.5-6.0%Y range in late 2013 and much of 2014. This scenario marks the next global recession, with global GDP growth falling below the 2.5% threshold.

CZE COL

CHL

Growth bottoming

Growth peaking

THL

IDN, MAL

IND, BRA CHN, RUS, NGR, GHA

TUR

KOR, TWN, KEN

MEX, POL, HUN, ISR, SAF, PEREA,

US, CAN

JPN, UK, SWE

2013E 2014E 2015E

Global GDPBear 2.6 2.4 2.7Base 2.9 3.5 3.7

Bull 3.2 4.1 4.4

G10 GDPBear 0.8 1.1 1.0Base 1.0 2.0 2.0Bull 1.2 2.6 2.7

EM GDPBear 4.2 3.6 4.2Base 4.8 4.9 5.2

Bull 5.1 5.6 5.9Global

Inflation (CPI)

Bear 2.9 2.0 2.1Base 3.3 3.0 3.1Bull 3.4 3.6 3.9

M O R G A N S T A N L E Y R E S E A R C H

Global Debates PlaybookSeptember 15, 2013

21

-0.60

-0.40

-0.20

0.00

0.20

0.40

0.60

0.80

1.00

1.20

Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug

Aggregate Weekly Payrolls: Total Private Industries% Change MoM

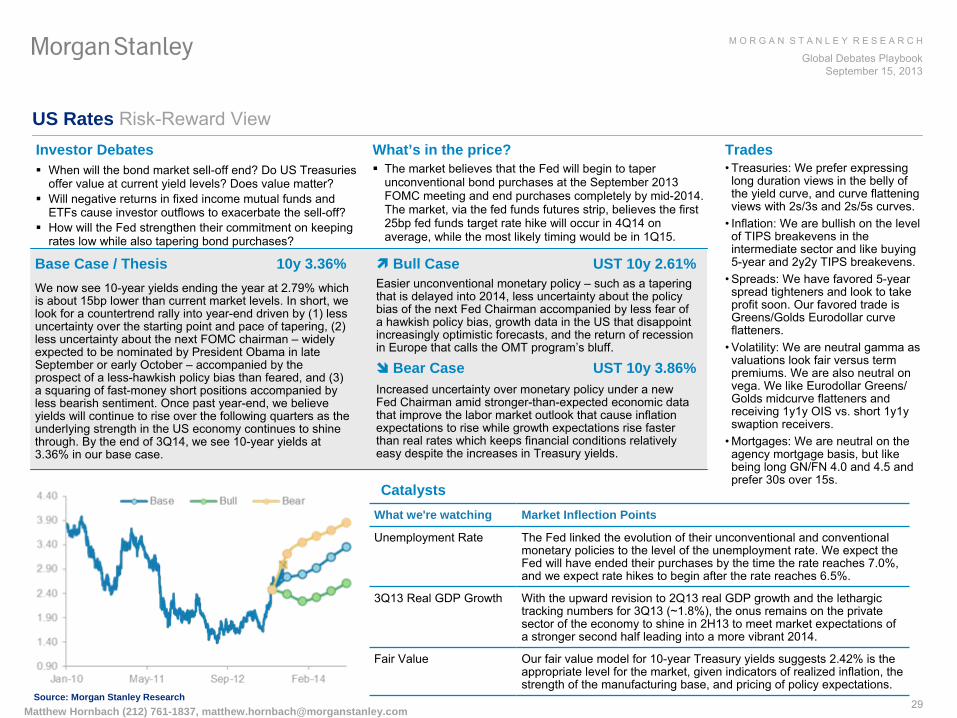

US Economics Risk-Reward ViewInvestor Debates

When will the Fed begin to taper asset purchases?

How sensitive is the economy to higher interest rates?

What’s in the price?

A mixed run of key initial economic data for August appears to have left investors more confident in a turn higher in economic growth and so pricing an earlier start to and more rapid pace of

Fed rate normalization in coming years but a bit less certain that QE tapering will be announced on September 18.

SignpostsSeptember 17-18FOMC Meeting / SEP

October 4September Employment

October 9FOMC Minutes

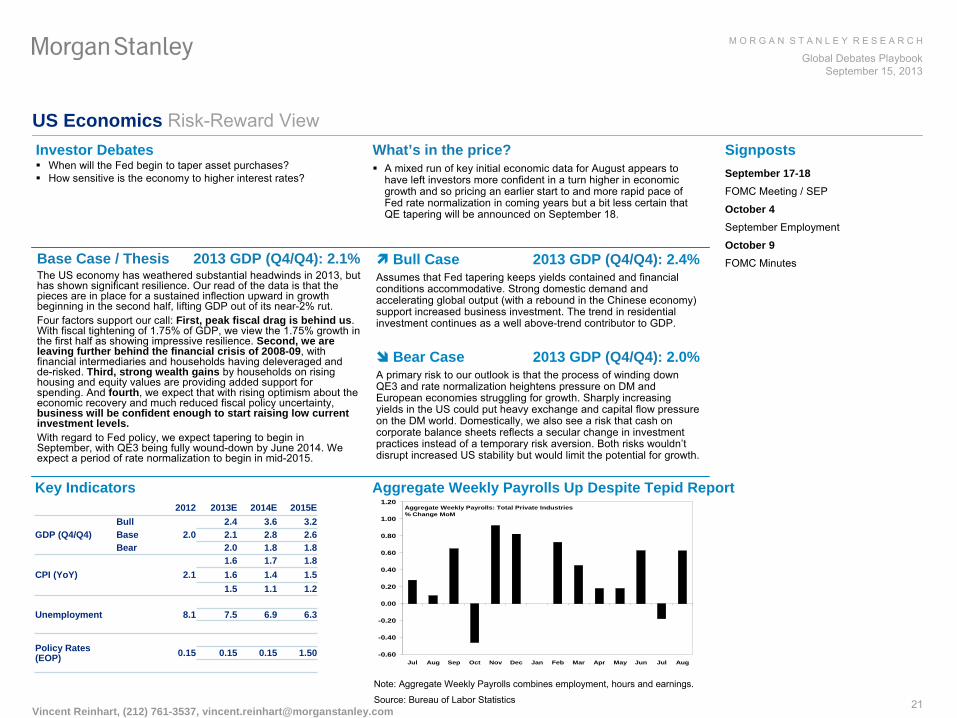

Key Indicators Aggregate Weekly Payrolls Up Despite Tepid Report

Base Case / Thesis 2013 GDP (Q4/Q4): 2.1%The US economy has weathered substantial headwinds in 2013, but has shown significant resilience. Our read of the data is that the pieces are in place for a sustained inflection upward in growth beginning in the second half, lifting GDP out of its near-2% rut.Four factors support our call: First, peak fiscal drag is behind us. With fiscal tightening of 1.75% of GDP, we view the 1.75% growth

in the first half as showing impressive resilience. Second, we are leaving further behind the financial crisis of 2008-09, with financial intermediaries and households having deleveraged and de-risked. Third, strong wealth gains by households on rising housing and equity values are providing added support for spending. And fourth, we expect that with rising optimism about the economic recovery and much reduced fiscal policy uncertainty, business will be confident enough to start raising low current investment levels.With regard to Fed policy, we expect tapering to begin in September, with QE3 being fully wound-down by June 2014. We expect a period of rate normalization to begin in mid-2015.

Bull Case 2013 GDP (Q4/Q4): 2.4%Assumes that Fed tapering keeps yields contained and financial conditions accommodative. Strong domestic demand and accelerating global output (with a rebound in the Chinese economy) support increased business investment. The trend in residential investment continues as a well above-trend contributor to GDP.

Bear Case 2013 GDP (Q4/Q4): 2.0%A primary risk to our outlook is that the process of winding down QE3 and rate normalization heightens pressure on DM and European economies struggling for growth. Sharply increasing yields in the US could put heavy exchange and capital flow pressure on the DM world. Domestically, we also see a risk that cash on corporate balance sheets reflects a secular change in investment

practices instead of a temporary risk aversion. Both risks wouldn’t disrupt increased US stability but would limit the potential for

growth.

Note: Aggregate Weekly Payrolls combines employment, hours and earnings.

Source: Bureau of Labor StatisticsVincent Reinhart, (212) 761-3537, [email protected]

2012 2013E 2014E 2015E

GDP (Q4/Q4)Bull 2.4 3.6 3.2Base 2.0 2.1 2.8 2.6Bear 2.0 1.8 1.8

CPI (YoY)1.6 1.7 1.8

2.1 1.6 1.4 1.51.5 1.1 1.2

Unemployment 8.1 7.5 6.9 6.3

Policy Rates (EOP) 0.15 0.15 0.15 1.50

M O R G A N S T A N L E Y R E S E A R C H

Global Debates PlaybookSeptember 15, 2013

22

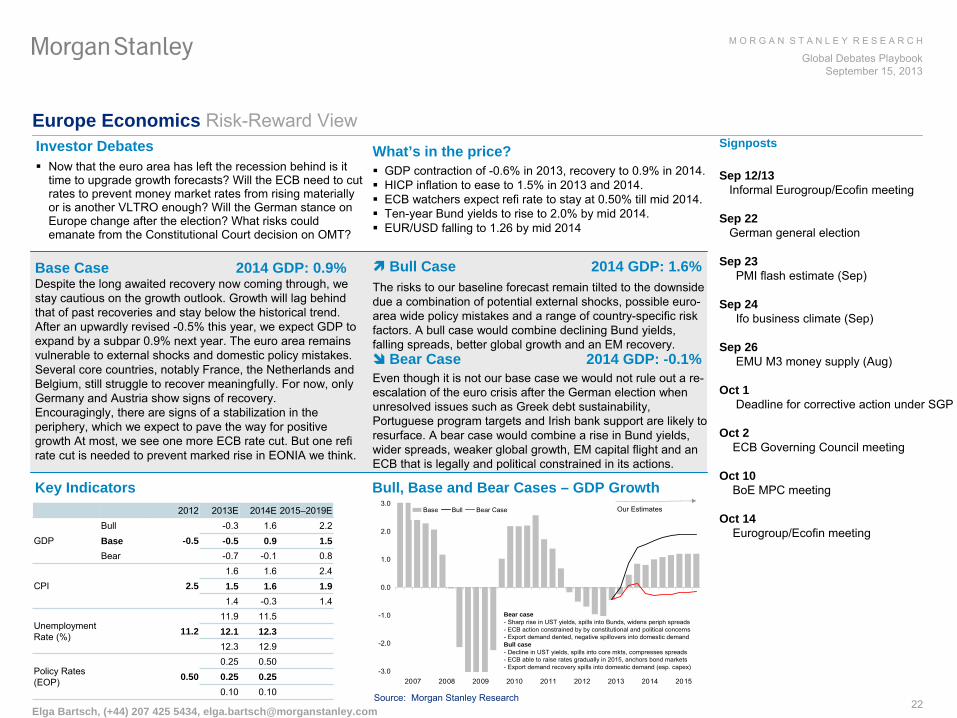

Europe Economics Risk-Reward ViewInvestor Debates

Now that the euro area has left the recession behind is it time to upgrade growth forecasts? Will the ECB need to cut rates to prevent money market rates from rising materially or is another VLTRO enough? Will the German stance on Europe change after the election? What risks could emanate from the Constitutional Court decision on OMT?

What’s in the price?

GDP contraction of -0.6% in 2013, recovery to 0.9% in 2014.

HICP inflation to ease to 1.5% in 2013 and 2014.

ECB watchers expect refi

rate to stay at 0.50% till mid 2014.

Ten-year Bund yields to rise to 2.0% by mid 2014.

EUR/USD falling to 1.26 by mid 2014

Signposts

Sep 12/13Informal Eurogroup/Ecofin

meeting

Sep 22German general election

Sep 23 PMI flash estimate (Sep)

Sep 24 Ifo

business climate (Sep)

Sep 26 EMU M3 money supply (Aug)

Oct 1Deadline for corrective action under SGP

Oct 2 ECB Governing Council meeting

Oct 10 BoE MPC meeting

Oct 14 Eurogroup/Ecofin

meeting

Elga Bartsch, (+44) 207 425 5434, [email protected]

Key Indicators Bull, Base and Bear Cases – GDP Growth

Base Case 2014 GDP: 0.9% Despite the long awaited recovery now coming through, we stay cautious on the growth outlook. Growth will lag behind that of past recoveries and stay below the historical trend. After an upwardly revised -0.5% this year, we expect GDP to expand by a subpar 0.9% next year. The euro area remains vulnerable to external shocks and domestic policy mistakes. Several core countries, notably France, the Netherlands and Belgium, still struggle to recover meaningfully. For now, only Germany and Austria show signs of recovery. Encouragingly, there are signs of a stabilization in the periphery, which we expect to pave the way for positive growth At most, we see one more ECB rate cut. But one refi

rate cut is needed to prevent marked rise in EONIA we think.

Bull Case 2014 GDP: 1.6%The risks to our baseline forecast remain tilted to the downside

due a combination of potential external shocks, possible euro-

area wide policy mistakes and a range of country-specific risk factors. A bull case would combine declining Bund yields, falling spreads, better global growth and an EM recovery.

Bear Case 2014 GDP: -0.1%Even though it is not our base case we would not rule out a re-

escalation of the euro crisis after the German election when unresolved issues such as Greek debt sustainability, Portuguese program targets and Irish bank support are likely to resurface. A bear case would combine a rise in Bund yields, wider spreads, weaker global growth, EM capital flight and an ECB that is legally and political constrained in its actions.

2012 2013E 2014E 2015–2019E

GDPBull

-0.5-0.3 1.6 2.2

Base -0.5 0.9 1.5Bear -0.7 -0.1 0.8

CPI 2.51.6 1.6 2.41.5 1.6 1.91.4 -0.3 1.4

Unemployment Rate (%) 11.2

11.9 11.512.1 12.312.3 12.9

Policy Rates (EOP) 0.50

0.25 0.500.25 0.250.10 0.10 Source: Morgan Stanley Research

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

2007 2008 2009 2010 2011 2012 2013 2014 2015

Base Bull Bear Case Our Estimates

Bear case- Sharp rise in UST yields, spills into Bunds, widens periph spreads- ECB action constrained by by constitutional and political concerns- Export demand dented, negative spillovers into domestic demandBull case- Decline in UST yields, spills into core mkts, compresses spreads- ECB able to raise rates gradually in 2015, anchors bond markets- Export demand recovery spills into domestic demand (esp. capex)

M O R G A N S T A N L E Y R E S E A R C H

Global Debates PlaybookSeptember 15, 2013

23

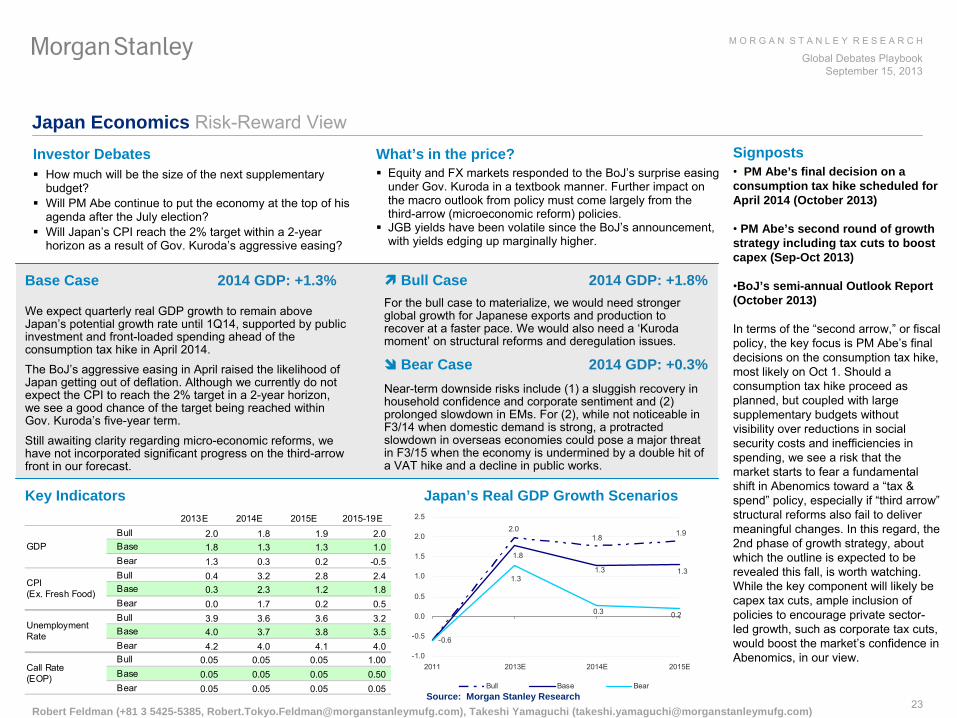

Japan Economics Risk-Reward View

Robert Feldman (+81 3 5425-5385, [email protected]), Takeshi Yamaguchi ([email protected])

Japan’s Real GDP Growth Scenarios

Investor Debates

How much will be the size of the next supplementary budget?

Will PM Abe continue to put the economy at the top of his agenda after the July election?

Will Japan’s CPI reach the 2% target within a 2-year horizon as a result of Gov. Kuroda’s aggressive easing?

What’s in the price?

Equity and FX markets responded to the BoJ’s

surprise easing under Gov. Kuroda in a textbook manner. Further impact on the macro outlook from policy must come largely from the third-arrow (microeconomic reform) policies.

JGB yields have been volatile since the BoJ’s

announcement, with yields edging up marginally higher.

Signposts•

PM Abe’s final decision on a consumption tax hike scheduled for April 2014 (October 2013)

•

PM Abe’s second round of growth strategy including tax cuts to boost capex (Sep-Oct 2013)

•BoJ’s semi-annual Outlook Report (October 2013)

In terms of the “second arrow,”

or fiscal policy, the key focus is PM Abe’s final decisions on the consumption tax hike, most likely on Oct 1. Should a consumption tax hike proceed as planned, but coupled with large supplementary budgets without visibility over reductions in social security costs and inefficiencies in spending, we see a risk that the market starts to fear a fundamental shift in Abenomics

toward a “tax & spend”

policy, especially if “third arrow”

structural reforms also fail to deliver meaningful changes. In this regard, the 2nd phase of growth strategy, about which the outline is expected to be revealed this fall, is worth watching. While the key component will likely be capex

tax cuts, ample inclusion of policies to encourage private sector-

led growth, such as corporate tax cuts, would boost the market’s confidence in Abenomics, in our view.

Key Indicators

Base Case 2014 GDP: +1.3%

We expect quarterly real GDP growth to remain above Japan’s potential growth rate until 1Q14, supported by public investment and front-loaded spending ahead of the consumption tax hike in April 2014. The BoJ’s

aggressive easing in April raised the likelihood of Japan getting out of deflation. Although we currently do not expect the CPI to reach the 2% target in a 2-year horizon, we see a good chance of the target being reached within Gov. Kuroda’s five-year term.

Still awaiting clarity regarding micro-economic reforms, we have not incorporated significant progress on the third-arrow front in our forecast.

Bull Case 2014 GDP: +1.8%For the bull case to materialize, we would need stronger global growth for Japanese exports and production to recover at a faster pace. We would also need a ‘Kuroda moment’

on structural reforms and deregulation issues.

Bear Case 2014 GDP: +0.3%Near-term downside risks include (1) a sluggish recovery in household confidence and corporate sentiment and (2) prolonged slowdown in EMs. For (2), while not noticeable in F3/14 when domestic demand is strong, a protracted slowdown in overseas economies could pose a major threat in F3/15 when the economy is undermined by a double hit of a VAT hike and a decline in public works.

2013E 2014E 2015E 2015-19EBull 2.0 1.8 1.9 2.0Base 1.8 1.3 1.3 1.0Bear 1.3 0.3 0.2 -0.5Bull 0.4 3.2 2.8 2.4Base 0.3 2.3 1.2 1.8Bear 0.0 1.7 0.2 0.5Bull 3.9 3.6 3.6 3.2Base 4.0 3.7 3.8 3.5Bear 4.2 4.0 4.1 4.0Bull 0.05 0.05 0.05 1.00Base 0.05 0.05 0.05 0.50Bear 0.05 0.05 0.05 0.05

GDP

CPI(Ex. Fresh Food)

UnemploymentRate

Call Rate(EOP)

-0.6

2.01.8 1.9

1.8

1.31.31.3

0.20.3

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

2011 2013E 2014E 2015E

Bull Base BearSource: Morgan Stanley Research

M O R G A N S T A N L E Y R E S E A R C H

Global Debates PlaybookSeptember 15, 2013

24

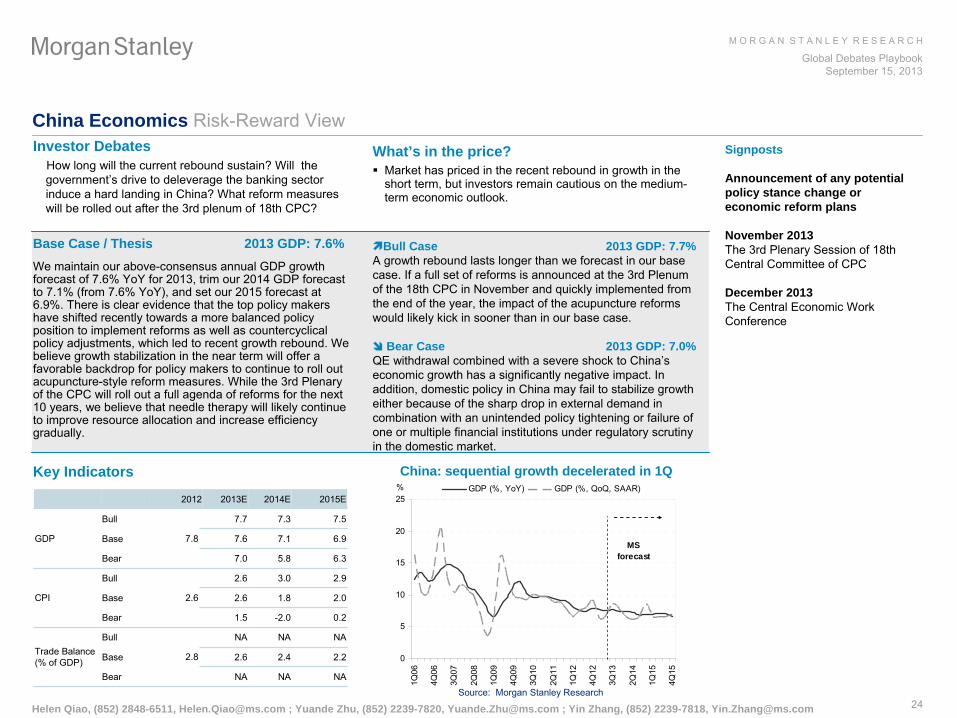

China Economics Risk-Reward ViewInvestor Debates

How long will the current rebound sustain? Will the government’s drive to deleverage the banking sector induce a hard landing in China? What reform measures will be rolled out after the 3rd plenum of 18th CPC?

What’s in the price?

Market has priced in the recent rebound in growth in the short term, but investors remain cautious on the medium-

term economic outlook.

Signposts

Announcement of any potential policy stance change or economic reform plans

November 2013The 3rd Plenary Session of 18th Central Committee of CPC

December 2013The Central Economic Work Conference

Key Indicators China: sequential growth decelerated in 1Q

Base Case / Thesis 2013 GDP: 7.6%We maintain our above-consensus annual GDP growth forecast of 7.6% YoY

for 2013, trim our 2014 GDP forecast to 7.1% (from 7.6% YoY), and set our 2015 forecast at 6.9%. There is clear evidence that the top policy makers have shifted recently towards a more balanced policy position to implement reforms as well as countercyclical policy adjustments, which led to recent growth rebound. We believe growth stabilization in the near term will offer a favorable backdrop for policy makers to continue to roll out acupuncture-style reform measures. While the 3rd Plenary of the CPC will roll out a full agenda of reforms for the next 10 years, we believe that needle therapy will likely continue to improve resource allocation and increase efficiency gradually.

Bull Case 2013 GDP: 7.7%A growth rebound lasts longer than we forecast in our base case. If a full set of reforms is announced at the 3rd Plenum of the 18th CPC in November and quickly implemented from the end of the year, the impact of the acupuncture reforms would likely kick in sooner than in our base case.

Bear Case 2013 GDP: 7.0%QE withdrawal combined with a severe shock to China’s economic growth has a significantly negative impact.

In addition, domestic policy in China may fail to stabilize growth either because of the sharp drop in external demand in combination with an unintended policy tightening or failure of one or multiple financial institutions under regulatory scrutiny

in the domestic market.

Source: Morgan Stanley Research

Helen Qiao, (852) 2848-6511, [email protected] ; Yuande Zhu, (852) 2239-7820, [email protected] ; Yin Zhang, (852) 2239-7818, [email protected]

2012 2013E 2014E 2015E

GDP

Bull

7.8

7.7 7.3 7.5

Base 7.6 7.1 6.9

Bear 7.0 5.8 6.3

CPI

Bull

2.6

2.6 3.0 2.9

Base 2.6 1.8 2.0

Bear 1.5 -2.0 0.2

Trade Balance

(% of GDP)

Bull

2.8

NA NA NA

Base 2.6 2.4 2.2

Bear NA NA NA

0

5

10

15

20

25

1Q06

4Q06

3Q07

2Q08

1Q09

4Q09

3Q10

2Q11

1Q12

4Q12

3Q13

2Q14

1Q15

4Q15

GDP (%, YoY) GDP (%, QoQ, SAAR)%

MS forecast

M O R G A N S T A N L E Y R E S E A R C H

Global Debates PlaybookSeptember 15, 2013

25

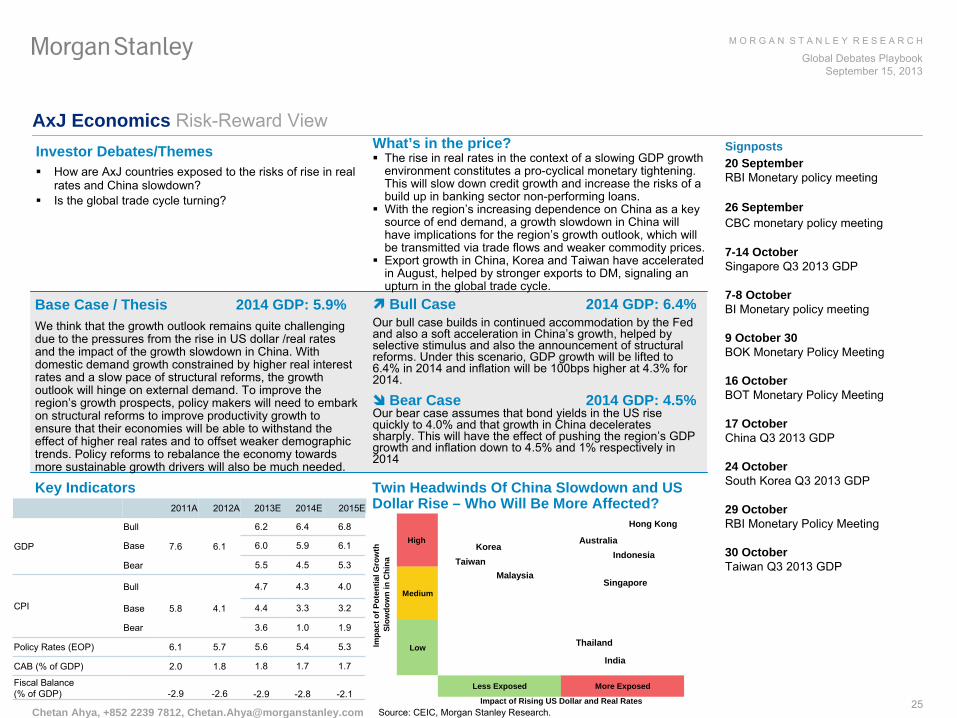

AxJ Economics Risk-Reward ViewInvestor Debates/Themes

How are AxJ

countries exposed to the risks of rise in real rates and China slowdown?

Is the global trade cycle turning?

What’s in the price?

The rise in real rates in the context of a slowing GDP growth environment constitutes a pro-cyclical monetary tightening. This will slow down credit growth and increase the risks of a build up in banking sector non-performing loans.

With the region’s increasing dependence on China as a key source of end demand, a growth slowdown in China will have implications for the region’s growth outlook, which will be transmitted via trade flows and weaker commodity prices.

Export growth in China, Korea and Taiwan have accelerated in August, helped by stronger exports to DM, signaling an upturn in the global trade cycle.

Chetan Ahya, +852 2239 7812, [email protected]

Key Indicators

Base Case / Thesis 2014 GDP: 5.9%We think that the growth outlook remains quite challenging due to the pressures from the rise in US dollar /real rates and the impact of the growth slowdown in China. With domestic demand growth constrained by higher real interest rates and a slow pace of structural reforms, the growth outlook will hinge on external demand. To improve the region’s growth prospects, policy makers will need to embark on structural reforms to improve productivity growth to ensure that their economies will be able to withstand the effect of higher real rates and to offset weaker demographic trends. Policy reforms to rebalance the economy towards more sustainable growth drivers will also be much needed.

Bull Case 2014 GDP: 6.4%Our bull case builds in continued accommodation by the Fed and also a soft acceleration in China’s growth, helped by selective stimulus and also the announcement of structural reforms. Under this scenario, GDP growth will be lifted to 6.4% in 2014 and inflation will be 100bps higher at 4.3% for 2014.

Bear Case 2014 GDP: 4.5%Our bear case assumes that bond yields in the US rise quickly to 4.0% and that growth in China decelerates sharply. This will have the effect of pushing the region’s GDP growth and inflation down to 4.5% and 1% respectively in 2014

2011A 2012A 2013E 2014E 2015E

GDP

Bull

7.6 6.1

6.2 6.4 6.8

Base 6.0 5.9 6.1

Bear 5.5 4.5 5.3

CPI

Bull 4.7 4.3 4.0

Base 5.8 4.1 4.4 3.3 3.2

Bear 3.6 1.0 1.9

Policy Rates (EOP) 6.1 5.7 5.6 5.4 5.3

CAB (% of GDP) 2.0 1.8 1.8 1.7 1.7

Fiscal Balance (% of GDP) -2.9 -2.6 -2.9 -2.8 -2.1

Source: CEIC, Morgan Stanley Research.

Signposts20 SeptemberRBI Monetary policy meeting

26 SeptemberCBC monetary policy meeting

7-14 OctoberSingapore Q3 2013 GDP

7-8 OctoberBI Monetary policy meeting

9 October 30BOK Monetary Policy Meeting

16 OctoberBOT Monetary Policy Meeting

17 OctoberChina Q3 2013 GDP

24 October South Korea Q3 2013 GDP

29 OctoberRBI Monetary Policy Meeting

30 OctoberTaiwan Q3 2013 GDP

Twin Headwinds Of China Slowdown and US Dollar Rise – Who Will Be More Affected?

High

Medium

Low

Less Exposed More Exposed

Impa

ct o

f Pot

entia

l Gro

wth

Sl

owdo

wn

in C

hina

Impact of Rising US Dollar and Real Rates

KoreaTaiwan

AustraliaIndonesia

Singapore

Thailand

India

Hong Kong

Malaysia

High

Medium

Low

Less Exposed More Exposed

Impa

ct o

f Pot

entia

l Gro

wth

Sl

owdo

wn

in C

hina

Impact of Rising US Dollar and Real Rates

KoreaTaiwan

AustraliaIndonesia

Singapore

Thailand

India

Hong Kong

Malaysia

M O R G A N S T A N L E Y R E S E A R C H

Global Debates PlaybookSeptember 15, 2013

26

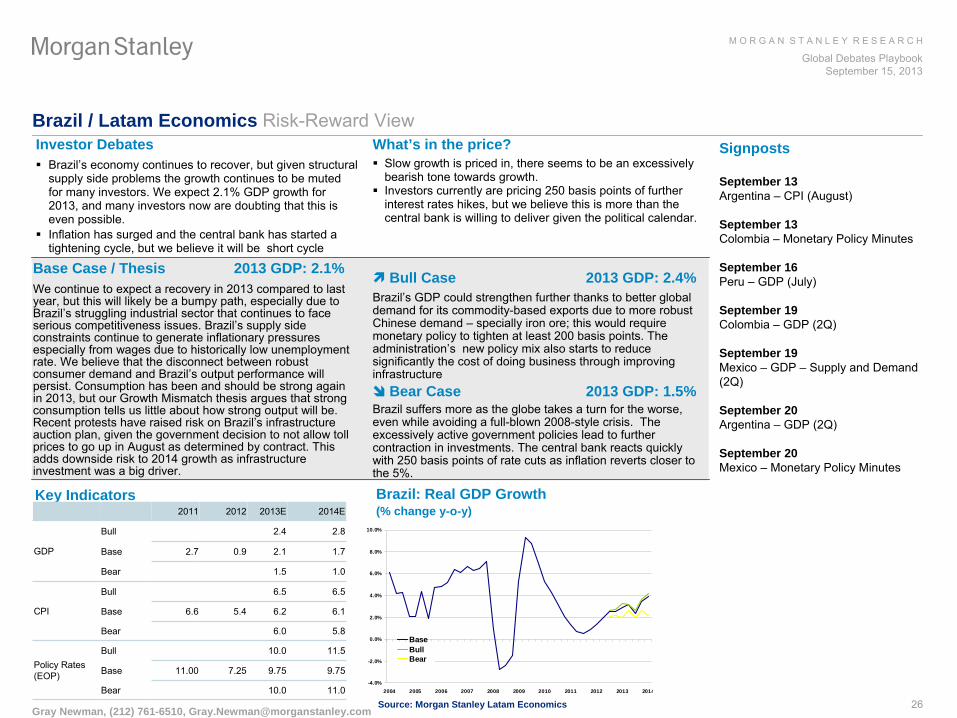

Brazil / Latam Economics Risk-Reward ViewInvestor Debates

Brazil’s economy continues to recover, but given structural supply side problems the growth continues to be muted for many investors. We expect 2.1% GDP growth for 2013, and many investors now are doubting that this is even possible.

Inflation has surged and the central bank has started a tightening cycle, but we believe it will be short cycle

What’s in the price?

Slow growth is priced in, there seems to be an excessively bearish tone towards growth.

Investors currently are pricing 250 basis points of further interest rates hikes, but we believe this is more than the central bank is willing to deliver given the political calendar.

Signposts

September 13Argentina –

CPI (August)

September 13Colombia –

Monetary Policy Minutes

September 16Peru –

GDP (July)

September 19Colombia –

GDP (2Q)

September 19Mexico –

GDP –

Supply and Demand (2Q)

September 20Argentina –

GDP (2Q)

September 20Mexico –

Monetary Policy Minutes

Gray Newman, (212) 761-6510, [email protected]

Key Indicators Brazil: Real GDP Growth(% change y-o-y)

Base Case / Thesis 2013 GDP: 2.1%We continue to expect a recovery in 2013 compared to last year, but this will likely be a bumpy path, especially due to Brazil’s struggling industrial sector that continues to face serious competitiveness issues. Brazil’s supply side constraints continue to generate inflationary pressures especially from wages due to historically low unemployment rate. We believe that the disconnect between robust consumer demand and Brazil’s output performance will persist. Consumption has been and should be strong again in 2013, but our Growth Mismatch thesis argues that strong consumption tells us little about how strong output will be. Recent protests have raised risk on Brazil’s infrastructure auction plan, given the government decision to not allow toll prices to go up in August as determined by contract. This adds downside risk to 2014 growth as infrastructure investment was a big driver.

Bull Case 2013 GDP: 2.4%Brazil’s GDP could strengthen further thanks to better global demand for its commodity-based exports due to more robust Chinese demand –

specially iron ore; this would require monetary policy to tighten at least 200 basis points. The administration’s new policy mix also starts to reduce significantly the cost of doing business through improving infrastructure

Bear Case 2013 GDP: 1.5%Brazil suffers more as the globe takes a turn for the worse, even while avoiding a full-blown 2008-style crisis. The excessively active government policies lead to further contraction in investments. The central bank reacts quickly with 250 basis points of rate cuts as inflation reverts closer to the 5%.

Source: Morgan Stanley Latam Economics

2011 2012 2013E 2014E

GDP

Bull 2.4 2.8

Base 2.7 0.9 2.1 1.7

Bear 1.5 1.0

CPI

Bull 6.5 6.5

Base 6.6 5.4 6.2 6.1

Bear 6.0 5.8

Policy Rates (EOP)

Bull 10.0 11.5

Base 11.00 7.25 9.75 9.75

Bear 10.0 11.0-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

BaseBullBear

M O R G A N S T A N L E Y R E S E A R C H

Global Debates PlaybookSeptember 15, 2013

27

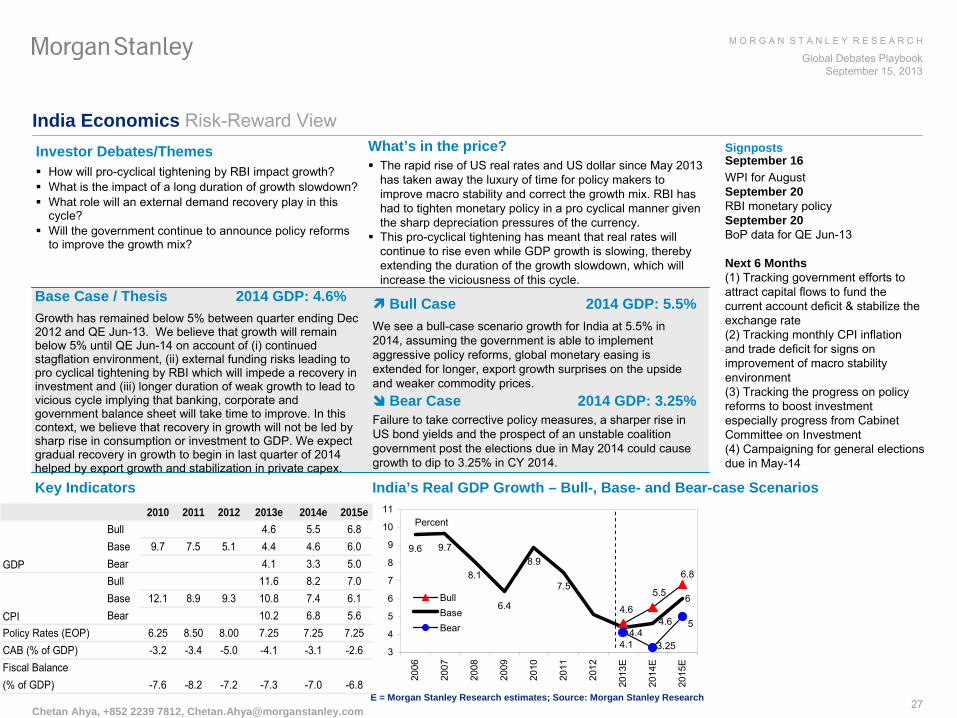

India Economics Risk-Reward View

Chetan Ahya, +852 2239 7812, [email protected]

Key Indicators India’s Real GDP Growth – Bull-, Base- and Bear-case Scenarios

E = Morgan Stanley Research estimates; Source: Morgan Stanley Research

Investor Debates/Themes

How will pro-cyclical tightening by RBI impact growth?

What is the impact of a long duration of growth slowdown?

What role will an external demand recovery play in this cycle?

Will the government continue to announce policy reforms to improve the growth mix?

What’s in the price?

The rapid rise of US real rates and US dollar since May 2013 has taken away the luxury of time for policy makers to improve macro stability and correct the growth mix. RBI has had to tighten monetary policy in a pro cyclical manner given the sharp depreciation pressures of the currency.

This pro-cyclical tightening has meant that real rates will continue to rise even while GDP growth is slowing, thereby extending the duration of the growth slowdown, which will increase the viciousness of this cycle.

Base Case / Thesis 2014 GDP: 4.6%Growth has remained below 5% between quarter ending Dec 2012 and QE Jun-13. We believe that growth will remain below 5% until QE Jun-14 on account of (i) continued stagflation environment, (ii) external funding risks leading to pro cyclical tightening by RBI which will impede a recovery in investment and (iii) longer duration of weak growth to lead to vicious cycle implying that banking, corporate and government balance sheet will take time to improve. In this context, we believe that recovery in growth will not be led by sharp rise in consumption or investment to GDP. We expect gradual recovery in growth to begin in last quarter of 2014 helped by export growth and stabilization in private capex.

Bull Case 2014 GDP: 5.5%We see a bull-case scenario growth for India at 5.5% in 2014, assuming the government is able to implement aggressive policy reforms, global monetary easing is extended for longer, export growth surprises on the upside and weaker commodity prices.

Bear Case 2014 GDP: 3.25%Failure to take corrective policy measures, a sharper rise in US bond yields and the prospect of an unstable coalition government post the elections due in May 2014 could cause growth to dip to 3.25% in CY 2014.

2010 2011 2012 2013e 2014e 2015eBull 4.6 5.5 6.8Base 9.7 7.5 5.1 4.4 4.6 6.0Bear 4.1 3.3 5.0Bull 11.6 8.2 7.0Base 12.1 8.9 9.3 10.8 7.4 6.1Bear 10.2 6.8 5.6

Policy Rates (EOP) 6.25 8.50 8.00 7.25 7.25 7.25CAB (% of GDP) -3.2 -3.4 -5.0 -4.1 -3.1 -2.6Fiscal Balance(% of GDP) -7.6 -8.2 -7.2 -7.3 -7.0 -6.8

GDP

CPI

9.6 9.7

8.1

6.4

8.9

7.5

4.6

5.5

6.8

4.44.6

6

4.1 3.25

5

3

4

5

6

7

8

9

10

11

2006

2007

2008

2009

2010

2011

2012

2013

E

2014

E

2015

E

BullBaseBear

Percent

Signposts September 16WPI for AugustSeptember 20RBI monetary policySeptember 20BoP

data for QE Jun-13

Next 6 Months (1) Tracking government efforts to attract capital flows to fund the current account deficit & stabilize the exchange rate(2) Tracking monthly CPI inflation and trade deficit for signs on improvement of macro stability environment (3) Tracking the progress on policy reforms to boost investment especially progress from Cabinet Committee on Investment(4) Campaigning for general elections due in May-14

M O R G A N S T A N L E Y R E S E A R C H

Global Debates PlaybookSeptember 15, 2013

28

Russia Economics Risk-Reward ViewInvestor Debates

Continued slowdown, stabilisation

or pickup?

Is inflation falling and will the CBR ease?

Will the authorities deliver promised structural reforms?

Is a reversal of political liberalisation

underway?

What’s in the price?

The government has downgraded its 2013 growth forecast from 3.6% to 2.4%, while consensus sees GDP growth at

2.3%Y. We see growth slowing to 2.2%Y from 3.4%Y in 2012, largely due to an investment slowdown.

Signposts2013-

CBR rate cut in 2013,- Rosneft

integration of TNK-BP,- execution of privatisation

deals;-

progress on improving Russia's ranking on the World Bank's ease of doing business index;- pension reform- anti-corruption campaign.

Jacob Nell, (7495) 287 2134, [email protected]; Alina Slyusarchuk, (44) 20 7677-6869, [email protected]

Key Indicators Investment Slowdown the Driver of Growth Disappointment

Base Case / Thesis 2013 GDP: 2.2%We revise growth down from 2.9%Y to 2.2%Y in 2013 and from 3.4%Y to 3.1%Y in 2014, largely due to weak investment. With a better harvest, and some investment recovery, supported by monetary easing, we think that Russian growth troughed in 2Q13 and will now pick up. Falling inflation opens the way for easier monetary policy. Still, we think that Governor Nabiullina

will err on the side of caution and pare the scale of the easing cycle from our previous forecast of 100bp to 75bp, which would take the policy rate (repo auction rate) to 4.75%. As a result of revenue weakness, we revise down our 2013 forecast for the fiscal balance from a 0.8% of GDP surplus to a 0.4% of GDP deficit, but tight expenditure control, high oil prices and fiscal policy room temper our concern.