Global and Local Healthcare Market Trends - Australian Self

33

ASMI 2012 Conference: Global and Local Healthcare Market Trends Francine Nieto Global Marketing Director, Consumer Health IMS Health

Transcript of Global and Local Healthcare Market Trends - Australian Self

ASMI 2012 Conference: Global and Local Healthcare Market Trends Francine Nieto

Global Marketing Director, Consumer Health

IMS Health

AGENDA

• Global OTC Context

• Local Trends

• Focus on the Consumer & Channel

• Highlights & Conclusions

Global and Local Healthcare Market Trends © IMS Health 2

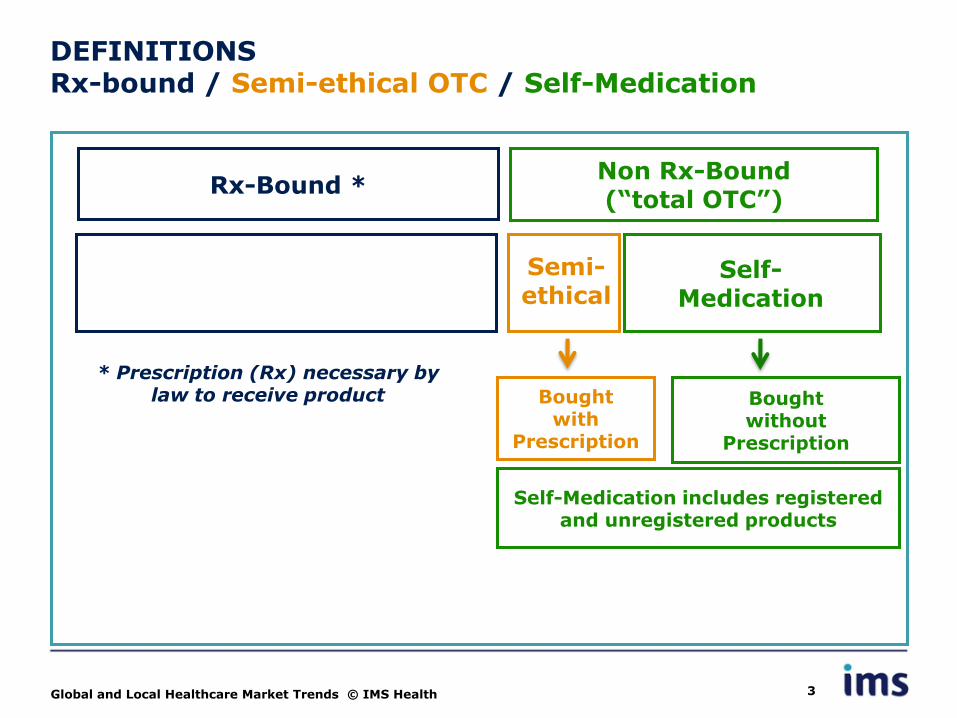

DEFINITIONS Rx-bound / Semi-ethical OTC / Self-Medication

Global and Local Healthcare Market Trends © IMS Health 3

Non Rx-Bound (“total OTC”)

Rx-Bound *

Self-Medication includes registered

and unregistered products

Bought with

Prescription

Bought without

Prescription

Self-Medication

* Prescription (Rx) necessary by law to receive product

Semi-ethical

THE BASIS The Basis for Figures in this presentation

Annual sales to Quarter 1 2012;

Sales in Dollars at manufacturer prices;

Growths based on previous years to quarter 1;

Growths use latest exchange rate for all countries across

all time periods

Global and Local Healthcare Market Trends © IMS Health 4

AGENDA

• Global OTC Context

• Local Trends

• Focus on the Consumer & Channel

• Highlights & Conclusions

Global and Local Healthcare Market Trends © IMS Health 5

Global and Local Healthcare Market Trends © IMS Health 6

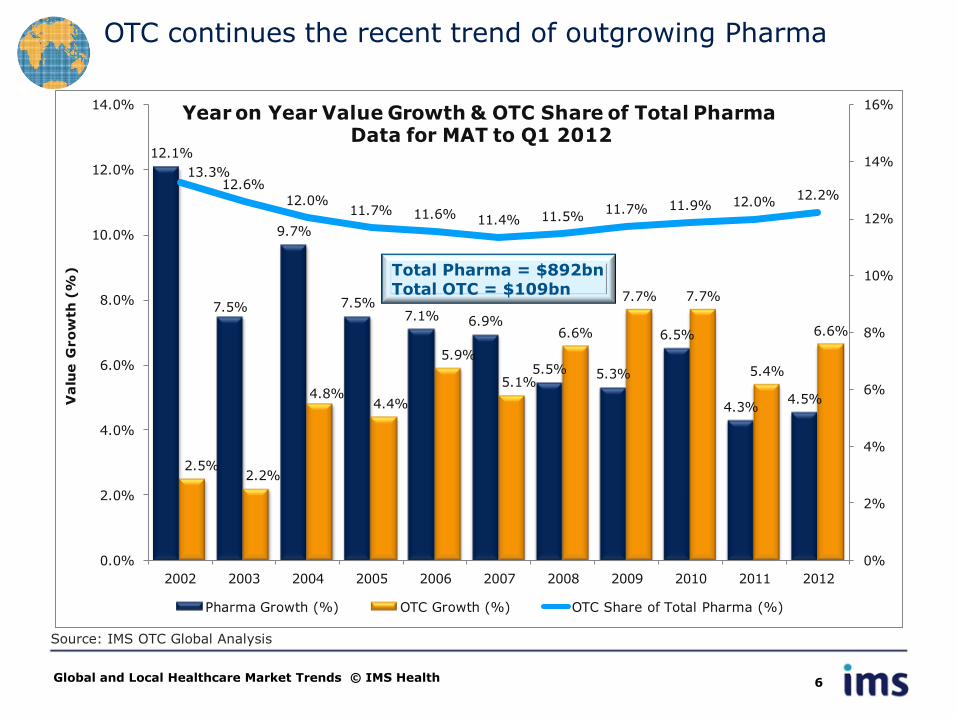

OTC continues the recent trend of outgrowing Pharma

Source: IMS OTC Global Analysis

12.1%

7.5%

9.7%

7.5%7.1% 6.9%

5.5% 5.3%

6.5%

4.3%4.5%

2.5%2.2%

4.8%4.4%

5.9%

5.1%

6.6%

7.7% 7.7%

5.4%

6.6%

13.3%12.6%

12.0%11.7% 11.6% 11.4% 11.5%

11.7% 11.9% 12.0%12.2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Va

lue

Gro

wth

(%

)

Year on Year Value Growth & OTC Share of Total Pharma Data for MAT to Q1 2012

Pharma Growth (%) OTC Growth (%) OTC Share of Total Pharma (%)

Total Pharma = $892bn Total OTC = $109bn

While Pharma growth experiences a number of constraints … OTC still benefits from a range of growth drivers

Global and Local Healthcare Market Trends © IMS Health 7

Top Corps contribution to growth falling rapidly

Low number and quality output from R&D

Generics dominating large therapy areas

Demand constrained by payers

Key players building strong brand identities

Payers keen to promote self medication

Emerging markets have the critical mass to influence growth

Companies seek to exploit switch opportunities

Increasing access through new channels

PHARMA

OTC

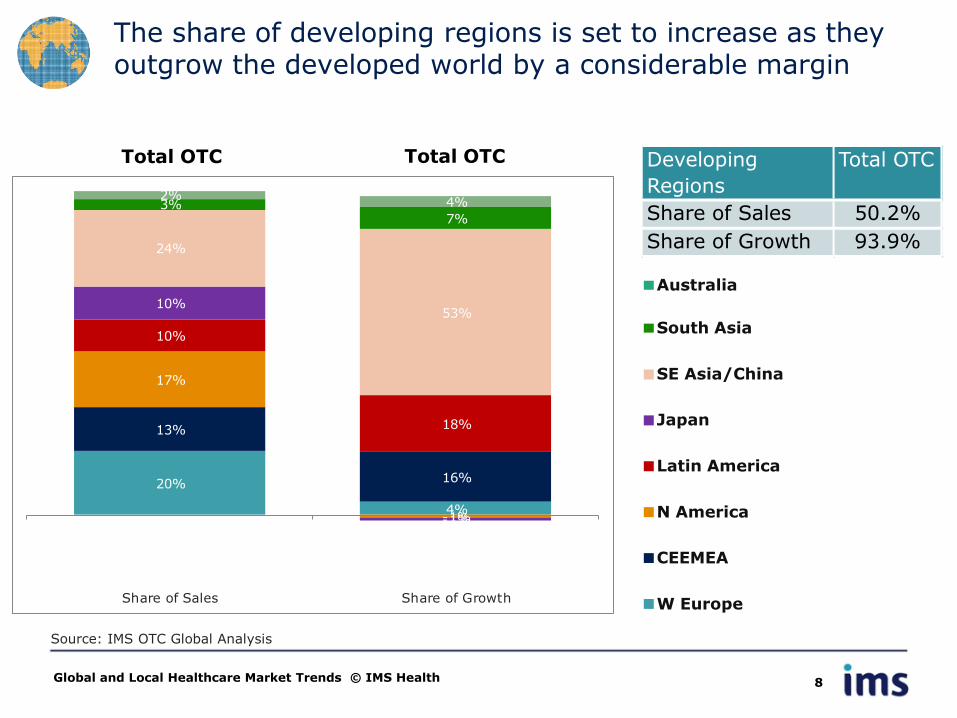

The share of developing regions is set to increase as they outgrow the developed world by a considerable margin

Global and Local Healthcare Market Trends © IMS Health 8

Source: IMS OTC Global Analysis

South Asia

SE Asia/China

Japan

Latin America

N America

CEEMEA

W Europe

Australia

20%

4%

13%

16%

17%

-1%

10%

18%

10%

-1%

24%

53%

3%7%

2%4%

Share of Sales Share of Growth

Total OTC Total OTC Developing

Regions

Total OTC

Share of Sales 50.2%

Share of Growth 93.9%

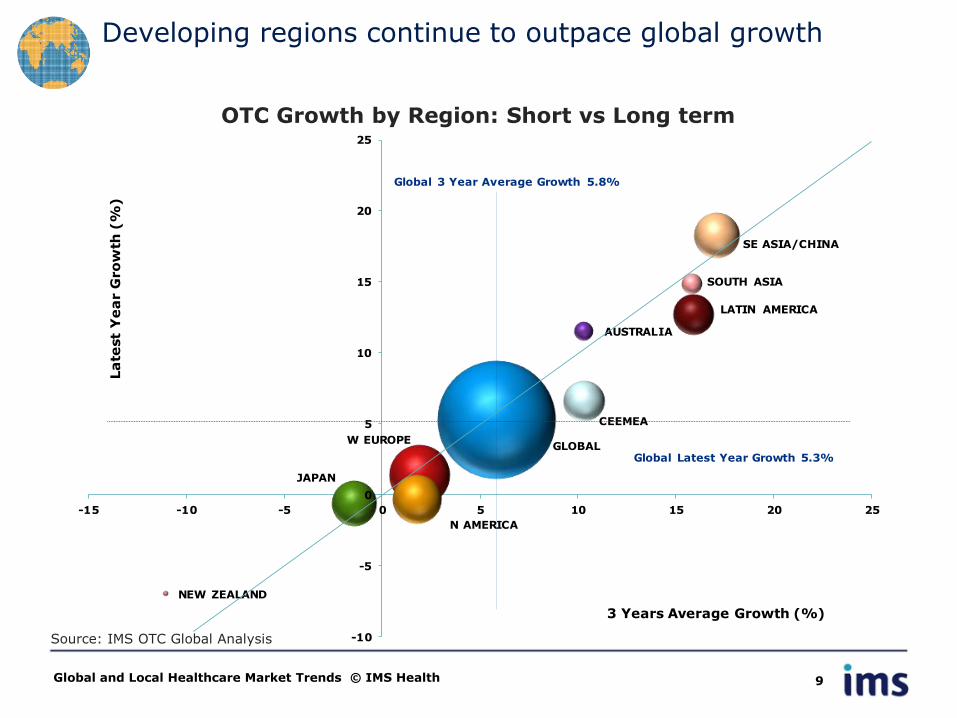

Developing regions continue to outpace global growth

Global and Local Healthcare Market Trends © IMS Health 9

Source: IMS OTC Global Analysis

OTC Growth by Region: Short vs Long term

GLOBALW EUROPE

CEEMEA

N AMERICA

JAPAN

LATIN AMERICA

SE ASIA/CHINA

SOUTH ASIA

AUSTRALIA

NEW ZEALAND

-10

-5

0

5

10

15

20

25

-15 -10 -5 0 5 10 15 20 25

La

test

Ye

ar G

ro

wth

(%

)

3 Years Average Growth (%)

Global Latest Year Growth 5.3%

Global 3 Year Average Growth 5.8%

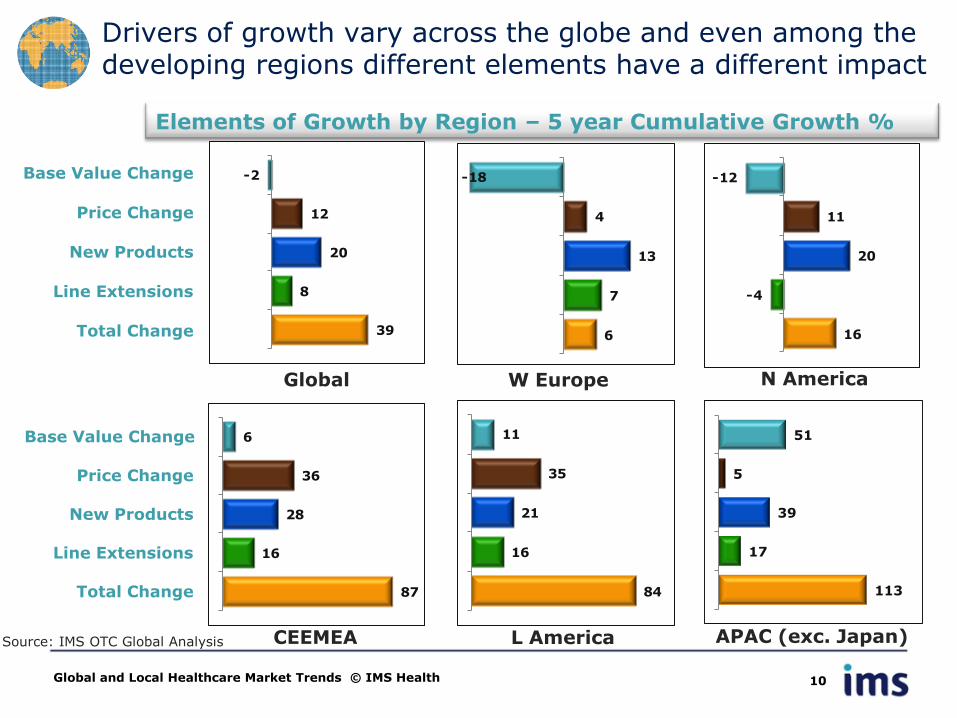

Drivers of growth vary across the globe and even among the developing regions different elements have a different impact

Global and Local Healthcare Market Trends © IMS Health 10

Base Value Change

Price Change

New Products

Line Extensions

Total Change

Base Value Change

Price Change

New Products

Line Extensions

Total Change

Global W Europe N America

CEEMEA L America APAC (exc. Japan) Source: IMS OTC Global Analysis

Elements of Growth by Region – 5 year Cumulative Growth %

39

8

20

12

-2

6

7

13

4

-18

16

-4

20

11

-12

87

16

28

36

6

84

16

21

35

11

113

17

39

5

51

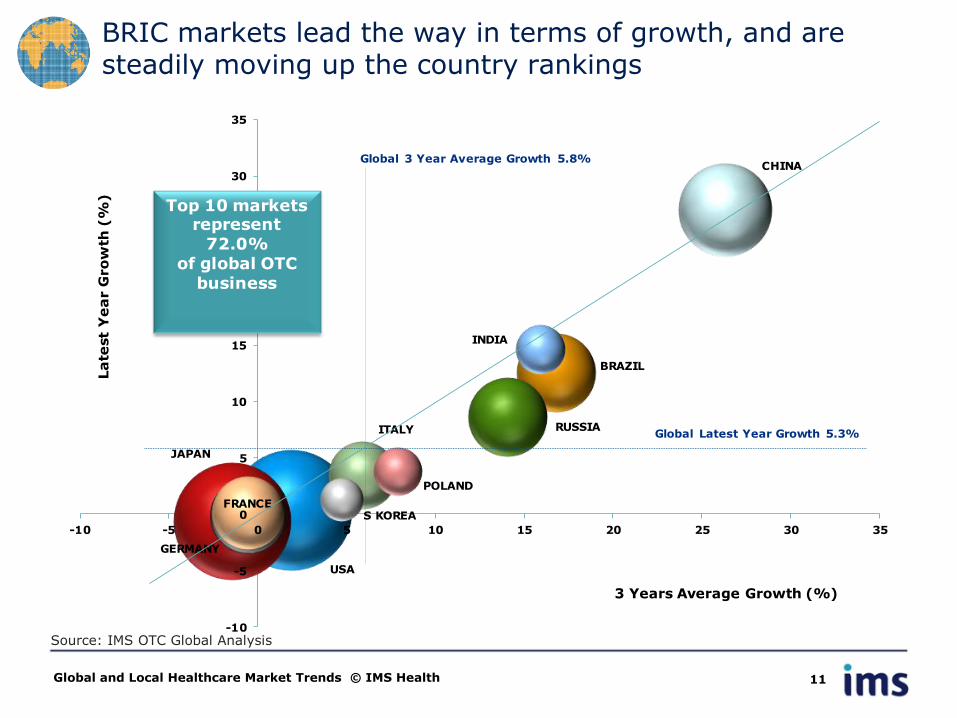

BRIC markets lead the way in terms of growth, and are steadily moving up the country rankings

Global and Local Healthcare Market Trends © IMS Health 11

Source: IMS OTC Global Analysis

USA

JAPAN

CHINA

BRAZIL

RUSSIA

GERMANY

FRANCE

ITALY

INDIA

POLAND

S KOREA

-10

-5

0

5

10

15

20

25

30

35

-10 -5 0 5 10 15 20 25 30 35

La

test

Ye

ar G

ro

wth

(%

)

3 Years Average Growth (%)

Global Latest Year Growth 5.3%

Global 3 Year Average Growth 5.8%

Top 10 markets represent

72.0%of global OTC

business

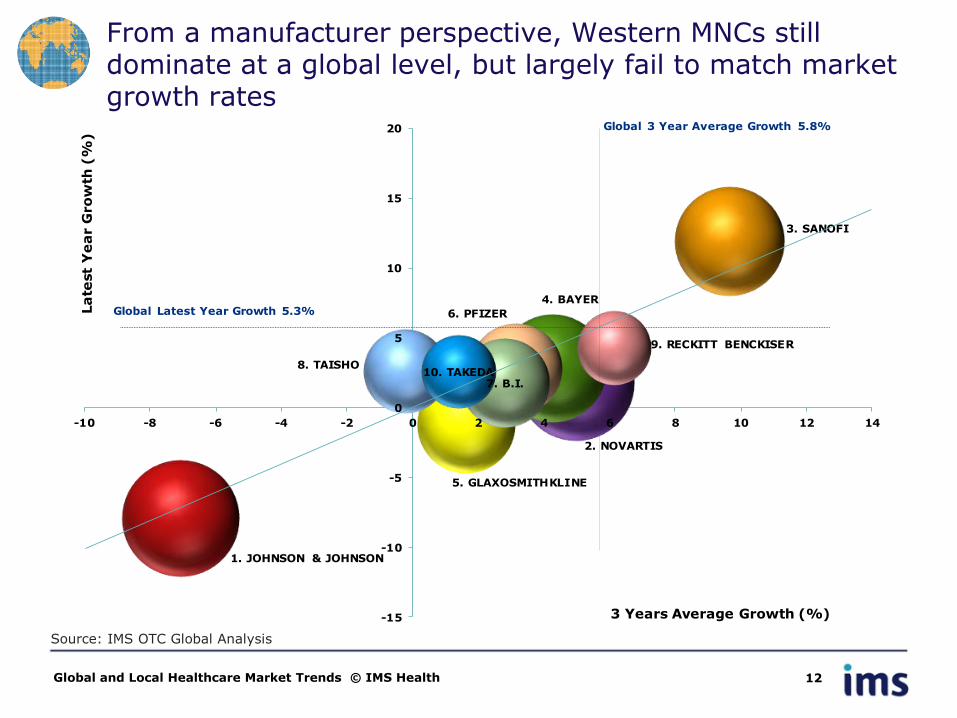

From a manufacturer perspective, Western MNCs still dominate at a global level, but largely fail to match market growth rates

Global and Local Healthcare Market Trends © IMS Health 12

Source: IMS OTC Global Analysis

1. JOHNSON & JOHNSON

2. NOVARTIS

3. SANOFI

4. BAYER

5. GLAXOSMITHKLINE

6. PFIZER

7. B.I.

8. TAISHO

9. RECKITT BENCKISER

10. TAKEDA

-15

-10

-5

0

5

10

15

20

-10 -8 -6 -4 -2 0 2 4 6 8 10 12 14

La

test

Ye

ar G

ro

wth

(%

)

3 Years Average Growth (%)

Global Latest Year Growth 5.3%

Global 3 Year Average Growth 5.8%

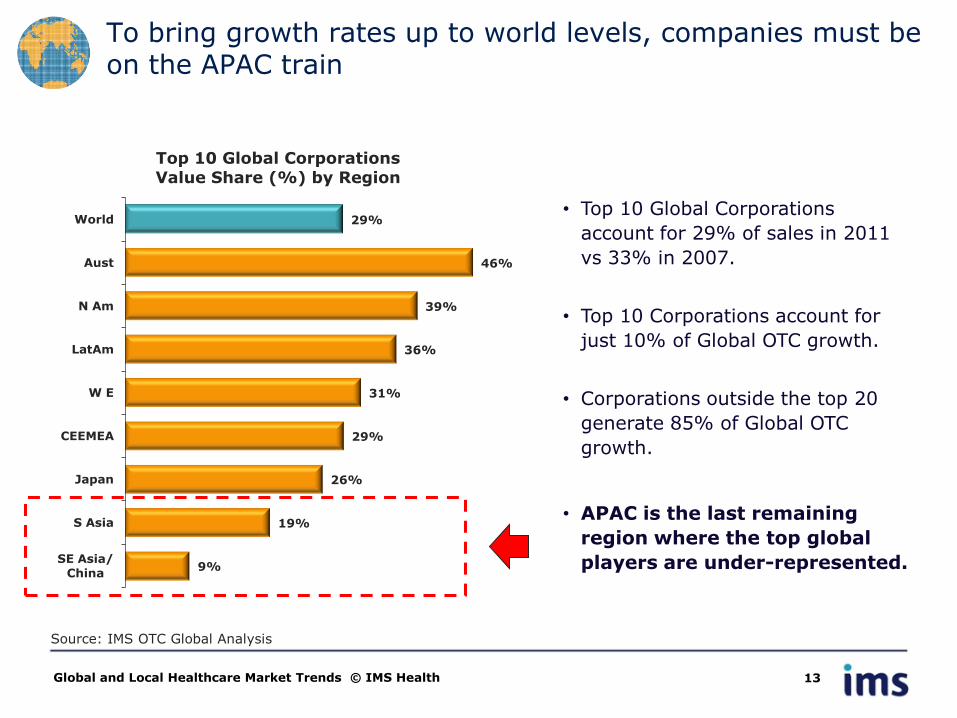

To bring growth rates up to world levels, companies must be on the APAC train

Global and Local Healthcare Market Trends © IMS Health 13

Source: IMS OTC Global Analysis

• Top 10 Global Corporations

account for 29% of sales in 2011

vs 33% in 2007.

• Top 10 Corporations account for

just 10% of Global OTC growth.

• Corporations outside the top 20

generate 85% of Global OTC

growth.

• APAC is the last remaining

region where the top global

players are under-represented.

29%

46%

39%

36%

31%

29%

26%

19%

9%

World

Aust

N Am

LatAm

W E

CEEMEA

Japan

S Asia

SE Asia/

China

Top 10 Global Corporations Value Share (%) by Region

AGENDA

• Global OTC Context

• Local Trends

• Focus on the Consumer & Channel

• Highlights & Conclusions

Global and Local Healthcare Market Trends © IMS Health 14

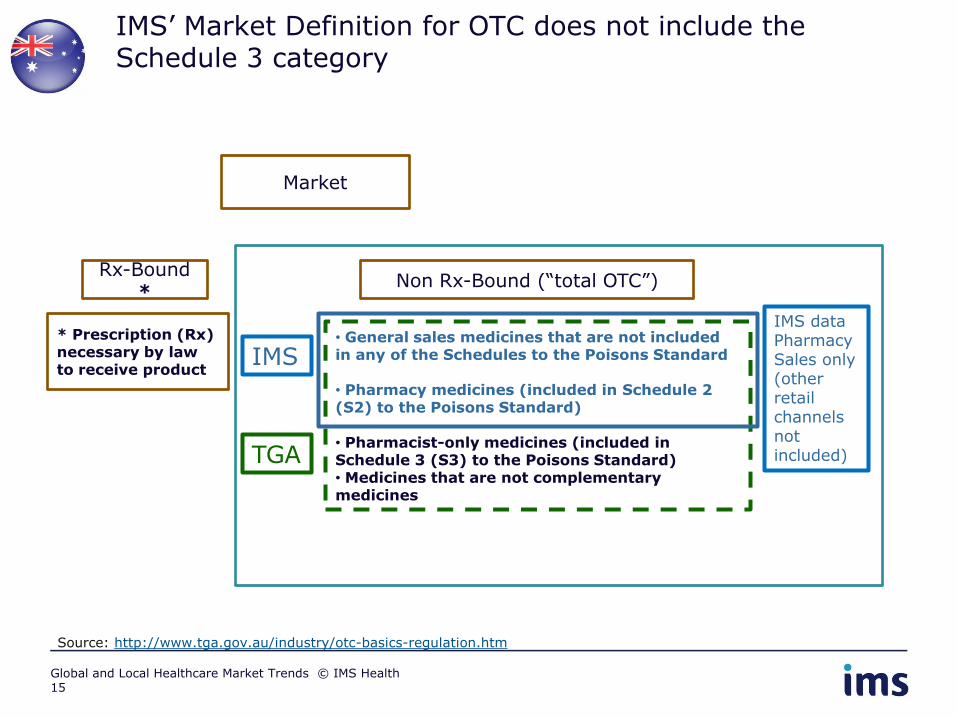

IMS’ Market Definition for OTC does not include the Schedule 3 category

Rx-Bound

*

Market

• General sales medicines that are not included in any of the Schedules to the Poisons Standard

• Pharmacy medicines (included in Schedule 2 (S2) to the Poisons Standard)

• Pharmacist-only medicines (included in Schedule 3 (S3) to the Poisons Standard) • Medicines that are not complementary medicines

* Prescription (Rx) necessary by law to receive product

Non Rx-Bound (“total OTC”)

Source: http://www.tga.gov.au/industry/otc-basics-regulation.htm

TGA

IMS

IMS data Pharmacy Sales only (other retail channels not included)

15 Global and Local Healthcare Market Trends © IMS Health

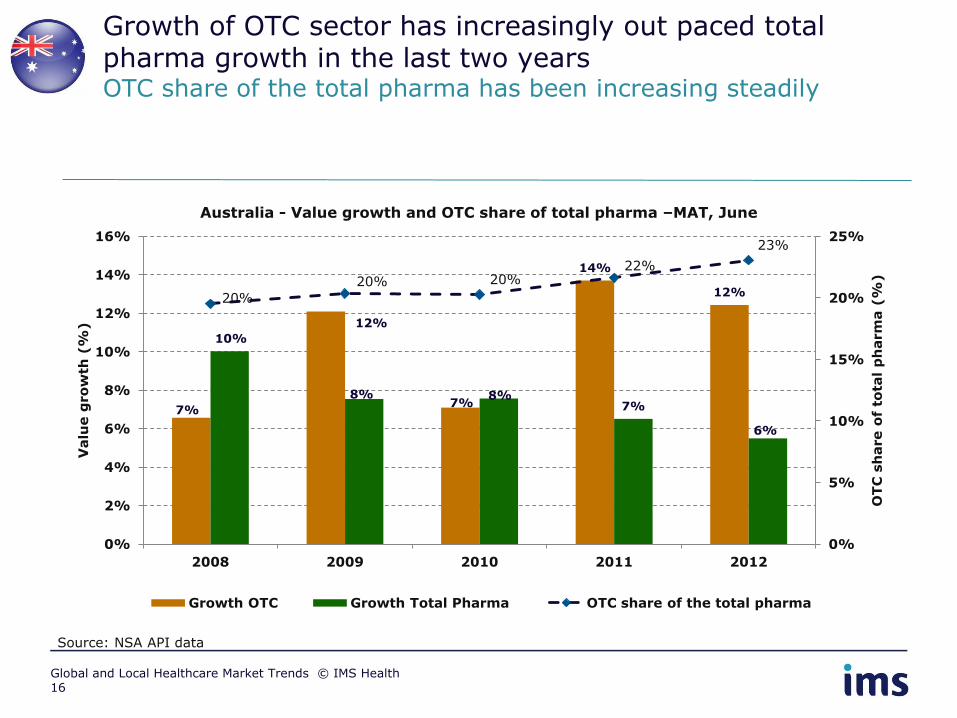

Growth of OTC sector has increasingly out paced total pharma growth in the last two years OTC share of the total pharma has been increasing steadily

Source: NSA API data

7%

12%

7%

14%

12%

10%

8% 8% 7%

6%

20%

20% 20% 22%

23%

0%

5%

10%

15%

20%

25%

0%

2%

4%

6%

8%

10%

12%

14%

16%

2008 2009 2010 2011 2012

OT

C s

hare o

f to

tal

ph

arm

a (

%)

Valu

e g

ro

wth

(%

)

Australia - Value growth and OTC share of total pharma –MAT, June

Growth OTC Growth Total Pharma OTC share of the total pharma

16 Global and Local Healthcare Market Trends © IMS Health

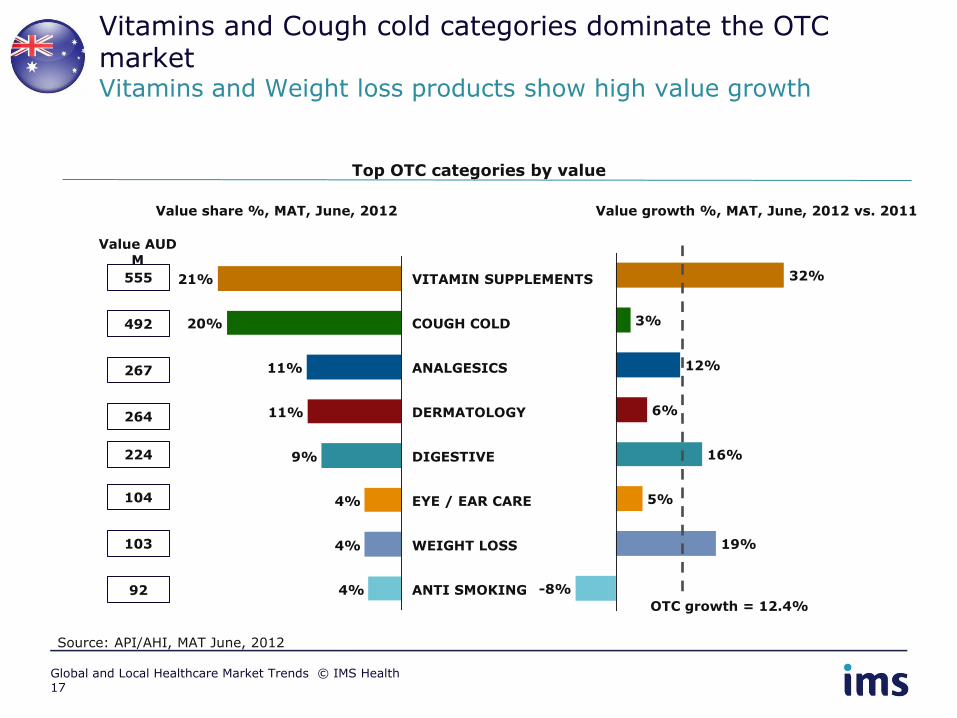

Vitamins and Cough cold categories dominate the OTC market Vitamins and Weight loss products show high value growth

Top OTC categories by value

Source: API/AHI, MAT June, 2012

WEIGHT LOSS 4%

EYE / EAR CARE 4%

DIGESTIVE 9%

DERMATOLOGY 11%

ANALGESICS 11%

COUGH COLD 20%

VITAMIN SUPPLEMENTS 21%

4% ANTI SMOKING -8%

19%

5%

16%

6%

12%

3%

32%

Value share %, MAT, June, 2012 Value growth %, MAT, June, 2012 vs. 2011

555

492

267

264

224

104

103

92

Value AUD M

OTC growth = 12.4%

17 Global and Local Healthcare Market Trends © IMS Health

-20

-15

-10

-5

0

5

10

15

20

25

30

0 10 20 30

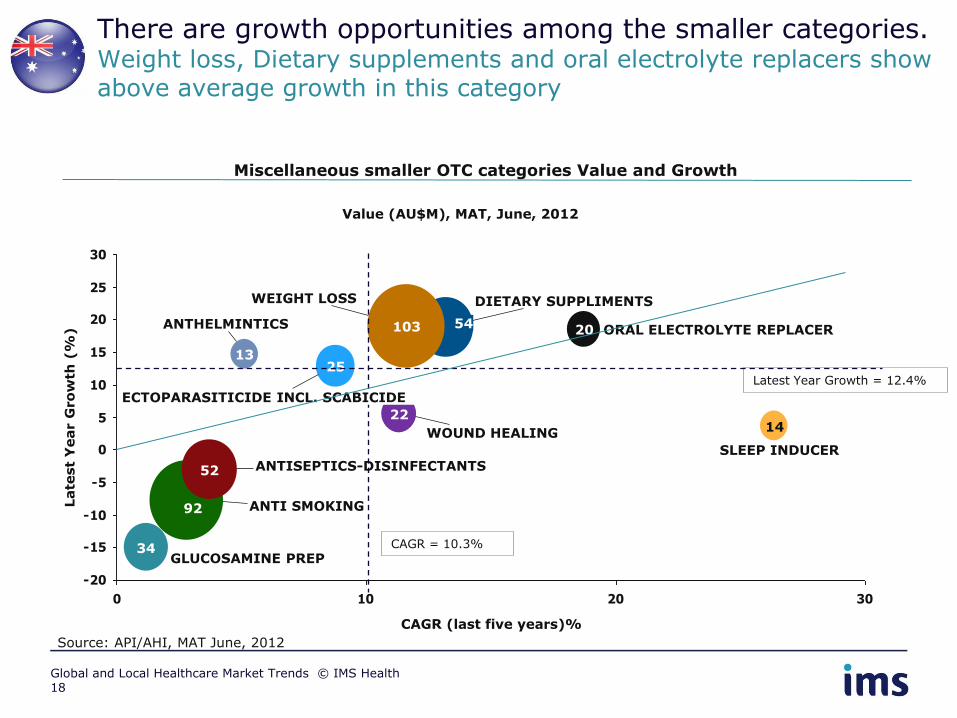

There are growth opportunities among the smaller categories. Weight loss, Dietary supplements and oral electrolyte replacers show above average growth in this category

Miscellaneous smaller OTC categories Value and Growth

Source: API/AHI, MAT June, 2012

Value (AU$M), MAT, June, 2012

Late

st

Year G

ro

wth

(%

)

CAGR (last five years)%

13

ANTHELMINTICS

14

SLEEP INDUCER

20 ORAL ELECTROLYTE REPLACER

22

WOUND HEALING

25

ECTOPARASITICIDE INCL. SCABICIDE

34 GLUCOSAMINE PREP

52 ANTISEPTICS-DISINFECTANTS

54

DIETARY SUPPLIMENTS

92 ANTI SMOKING

103

WEIGHT LOSS

Latest Year Growth = 12.4%

CAGR = 10.3%

18 Global and Local Healthcare Market Trends © IMS Health

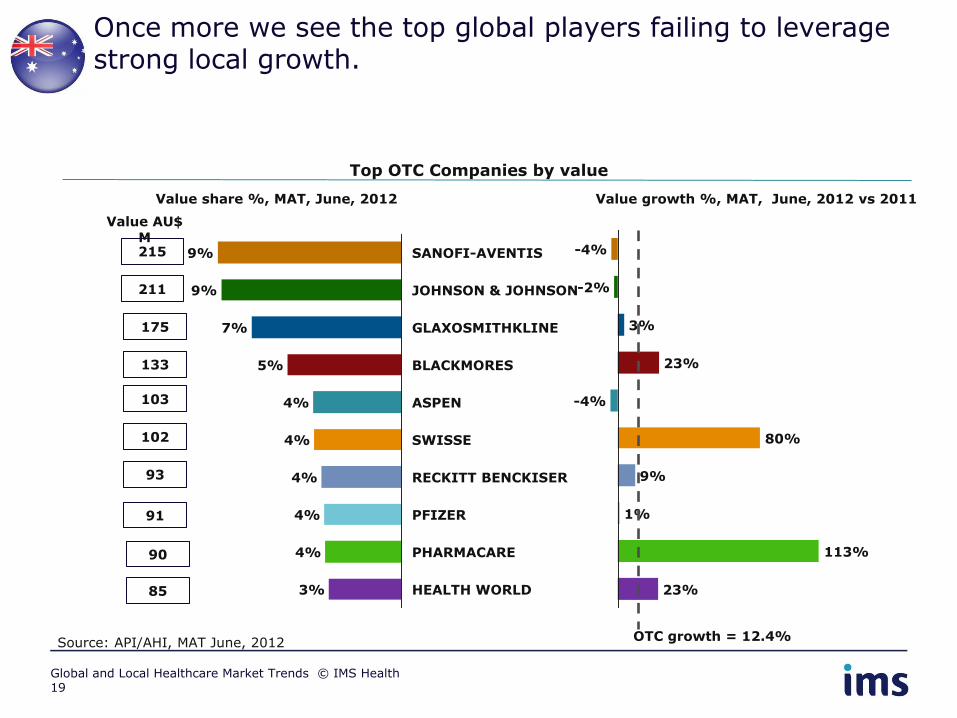

Once more we see the top global players failing to leverage strong local growth.

Top OTC Companies by value

Source: API/AHI, MAT June, 2012

PFIZER 4%

RECKITT BENCKISER 4%

SWISSE 4%

ASPEN 4%

BLACKMORES 5%

GLAXOSMITHKLINE 7%

JOHNSON & JOHNSON 9%

SANOFI-AVENTIS 9%

HEALTH WORLD

PHARMACARE 4%

3%

1%

9%

80%

-4%

23%

3%

-2%

-4%

113%

23%

Value share %, MAT, June, 2012 Value growth %, MAT, June, 2012 vs 2011

215

211

175

133

103

102

93

91

Value AU$ M

90

85

19 Global and Local Healthcare Market Trends © IMS Health

OTC growth = 12.4%

-30

-20

-10

0

10

20

30

40

50

60

70

80

90

100

110

120

130

-3 0 3 6 9 12 15 18 21 24 27 30 33 36 39 42 45

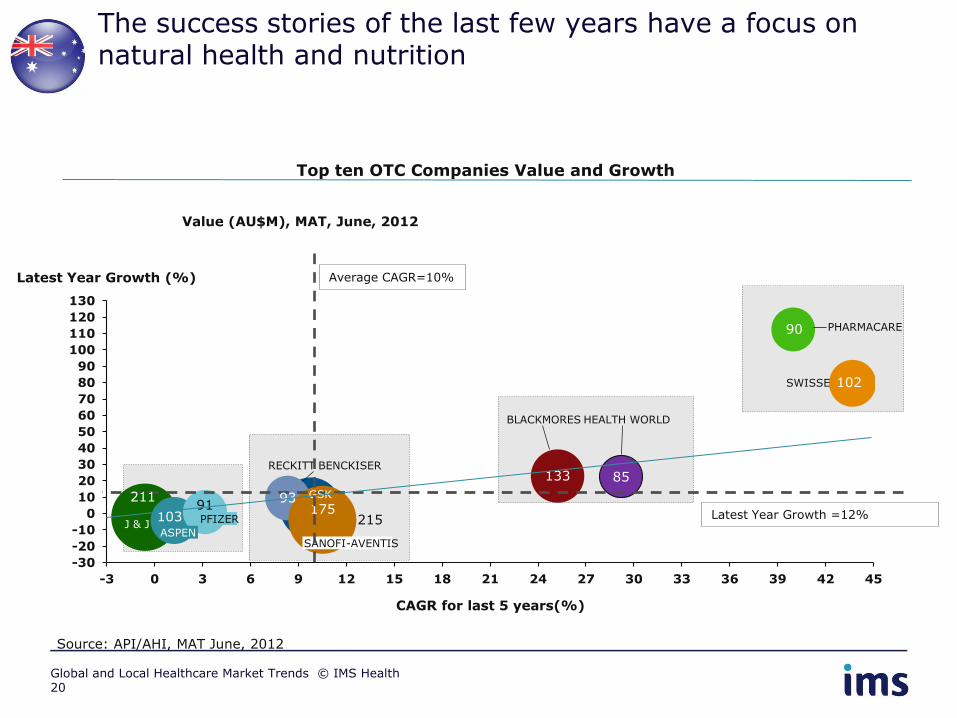

The success stories of the last few years have a focus on natural health and nutrition

Top ten OTC Companies Value and Growth

Source: API/AHI, MAT June, 2012

Value (AU$M), MAT, June, 2012

Latest Year Growth (%)

HEALTH WORLD

90 PHARMACARE

91 PFIZER

93

RECKITT BENCKISER

102 SWISSE

103 ASPEN

133

BLACKMORES

175 GSK 211

J & J 215

SANOFI-AVENTIS

CAGR for last 5 years(%)

85

Average CAGR=10%

Latest Year Growth =12%

20 Global and Local Healthcare Market Trends © IMS Health

Smaller companies have been growing and consistently contributing to overall OTC market growth Top three players are struggling to maintain their market share

Top OTC Companies Value, Growth and Contribution to growth

Source: API/AHI, MAT June, 2012

Value (AU$M), MAT, June

144 182 204 223 215 216 221 210 216 211 120 132 148 169 175 54 55 77

108 133 98 106 106

108 103 102 93 91

23 24

28 42

90 85 777

874 931

1,052

1,181

0%

2%

4%

6%

8%

10%

12%

14%

16%

0

500

1,000

1,500

2,000

2,500

3,000

2008 2009 2010 2011 2012

Gro

wth

(%

)

Valu

e (

AU

$M

) M

AT

Ju

ne

OTHERS

HEALTH

WORLD

PHARMACARE

PFIZER

RECKITT

BENCKISER

SWISSE

ASPEN

BLACKMORES

GSK

J & J

SANOFI-

AVENTIS

Growth

2% 1% 1%

-0.4%

1%

1% 1%

1.2% 1.6%

1%

1%

1%

2%

1%

0.4%

1%

1%

2% 0.4%

0.4%

1% 1%

6%

3%

6%

6%

-1%

1%

3%

5%

7%

9%

11%

13%

15%

2009 2010 2011 2012

Co

ntr

ibu

tio

n t

o G

ro

wth

(%

)

Contribution to Growth, MAT, June

21 Global and Local Healthcare Market Trends © IMS Health

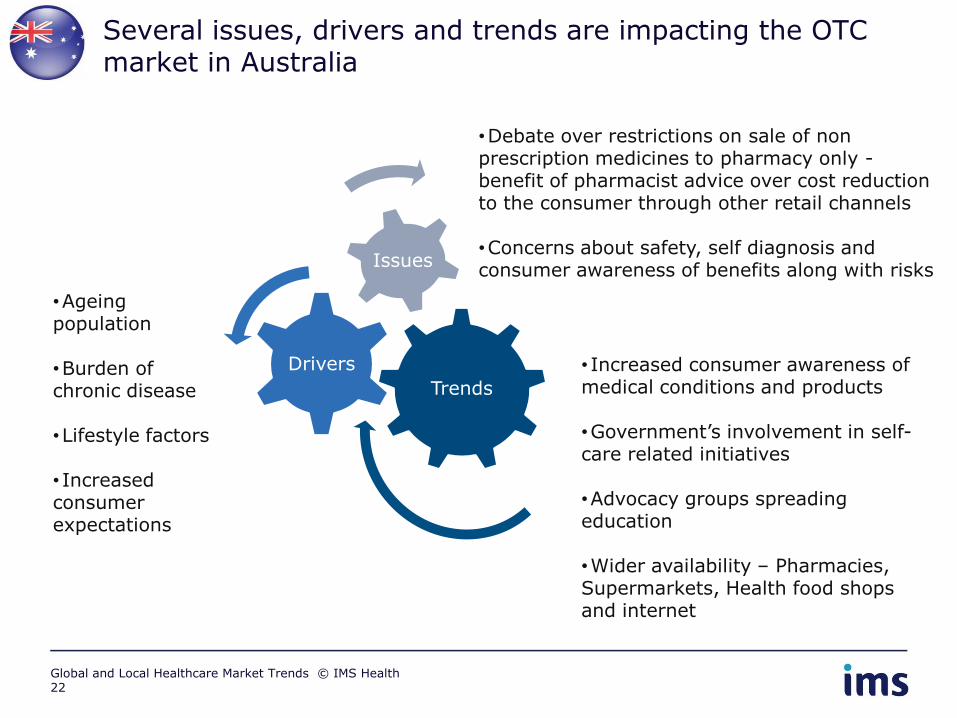

Several issues, drivers and trends are impacting the OTC market in Australia

Trends

Drivers

Issues

•Ageing population

•Burden of chronic disease

•Lifestyle factors

• Increased consumer expectations

•Debate over restrictions on sale of non prescription medicines to pharmacy only - benefit of pharmacist advice over cost reduction to the consumer through other retail channels

•Concerns about safety, self diagnosis and consumer awareness of benefits along with risks

• Increased consumer awareness of medical conditions and products

•Government’s involvement in self-care related initiatives

•Advocacy groups spreading education

•Wider availability – Pharmacies, Supermarkets, Health food shops and internet

22 Global and Local Healthcare Market Trends © IMS Health

AGENDA

• Global OTC Context

• Local Trends

• Focus on the Consumer & Channel

• Highlights & Conclusions

Global and Local Healthcare Market Trends © IMS Health 23

Many of the key OTC growth drivers influence the trend towards a stronger focus on the consumer

Global and Local Healthcare Market Trends © IMS Health 24

Top Corps contribution to growth falling rapidly

Low number and quality output from R&D

Generics dominating large therapy areas

Demand constrained by payers

Key players building strong brand identities

Payers keen to promote self medication

Emerging markets have the critical mass to influence growth

Companies seek to exploit switch opportunities

Increasing access through new channels

PHARMA

OTC

A shift in thinking from: “Pharmaceuticals for the Consumer” Towards: Consumer products about health & wellness ...applying consumer based thinking and involving the whole organisation R&D, regulatory, production, logistics

Focus on the consumer has always been part of OTC thinking but becomes more “centre stage”

Global and Local Healthcare Market Trends © IMS Health 25

There is a growing push in society towards preventative health and nutrition

Global and Local Healthcare Market Trends © IMS Health 26

Awareness

•Media campaigns have heightened awareness of unhealthy lifestyles

•Growing number of advertisements, magazines and blogs for self-medication with vitamins, minerals and other dietary supplements

Adoption

•Initially adopted by US, European and Japanese markets where consumers regularly take supplements with meals

•Emerging markets have also taken off

Payers

•Payers are recognising the long-term cost-benefits to preventative treatments

•Many health insurance providers encourage active lifestyles and healthy eating as part of their membership schemes

Future

•As a result more companies are entering into the space which has now become a separate market to just “nutrition”

•The market is expected to continue strong growth

27

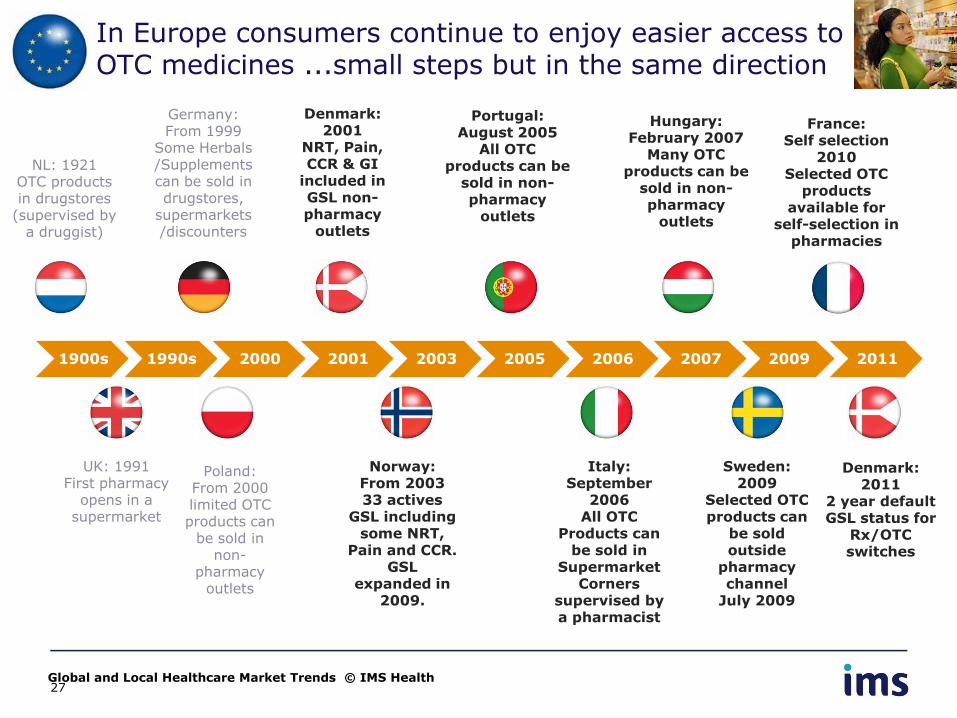

In Europe consumers continue to enjoy easier access to OTC medicines ...small steps but in the same direction

1900s 1990s 2000 2001 2003 2005 2006 2007 2009 2011

NL: 1921 OTC products in drugstores

(supervised by a druggist)

UK: 1991 First pharmacy

opens in a supermarket

Germany: From 1999

Some Herbals /Supplements can be sold in drugstores,

supermarkets /discounters

Poland: From 2000 limited OTC products can

be sold in non-

pharmacy outlets

Portugal: August 2005

All OTC products can be

sold in non-pharmacy

outlets

Italy: September

2006 All OTC

Products can be sold in

Supermarket Corners

supervised by a pharmacist

Hungary: February 2007

Many OTC products can be

sold in non-pharmacy

outlets

Sweden: 2009

Selected OTC products can

be sold outside

pharmacy channel

July 2009

Norway: From 2003 33 actives

GSL including some NRT,

Pain and CCR. GSL

expanded in 2009.

Denmark: 2001

NRT, Pain, CCR & GI

included in GSL non-pharmacy

outlets

Global and Local Healthcare Market Trends © IMS Health

France: Self selection

2010 Selected OTC

products available for

self-selection in pharmacies

Denmark: 2011

2 year default GSL status for

Rx/OTC switches

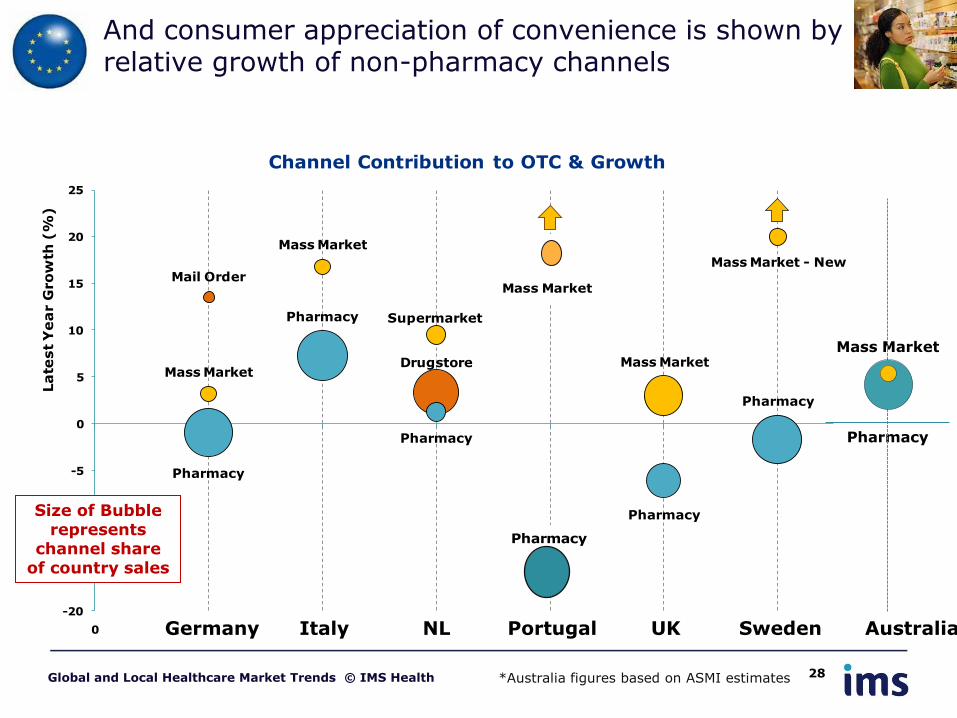

And consumer appreciation of convenience is shown by relative growth of non-pharmacy channels

Pharmacy

Mass Market

Mail Order

Mass Market

Pharmacy

Drugstore

Pharmacy

Supermarket

Mass Market

Pharmacy

Pharmacy

Mass Market

Mass Market - New

Pharmacy

-20

-15

-10

-5

0

5

10

15

20

25

0 1 2 3 4 5 6

La

test

Ye

ar G

ro

wth

(%

)

Channel Contribution to OTC & Growth

Germany Italy NL Portugal UK Sweden

Pharmacy

Mass Market

Australia

Pharmacy

Mass Market

28 Global and Local Healthcare Market Trends © IMS Health

Size of Bubble represents

channel share of country sales

*Australia figures based on ASMI estimates

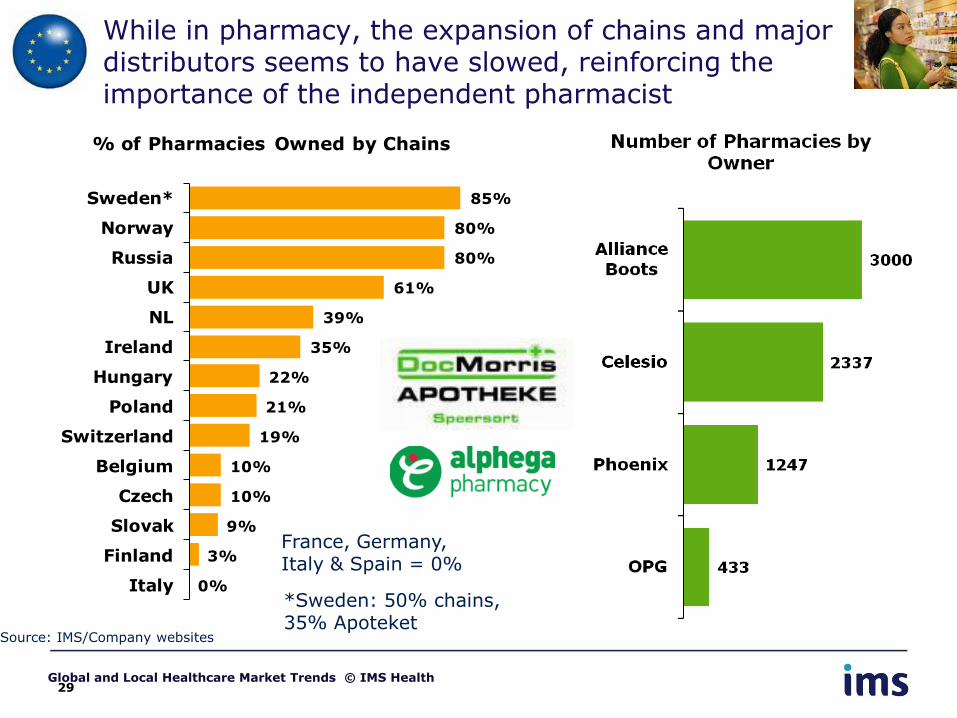

While in pharmacy, the expansion of chains and major distributors seems to have slowed, reinforcing the importance of the independent pharmacist

29

Source: IMS/Company websites

85%

80%

80%

61%

39%

35%

22%

21%

19%

10%

10%

9%

3%

0%

Sweden*

Norway

Russia

UK

NL

Ireland

Hungary

Poland

Switzerland

Belgium

Czech

Slovak

Finland

Italy

% of Pharmacies Owned by Chains

France, Germany, Italy & Spain = 0%

*Sweden: 50% chains, 35% Apoteket

Global and Local Healthcare Market Trends © IMS Health

As a result of the evolving channel environment, Excellence in Execution is key

Pharmacist

HCPs

Mass Market

Wholesalers

Consumers

Key Account Management:

Clear role for each brand within each

category.

Differentiated Customer calls:

Individual message for each store with suitable

frequency

Consistent Message: Building a strong brand identity in

a multi-media environment Maximising

commercial partnerships:

Leverage growth opportunities

Recommendation: How important is the HCP role and how to optimise within the

marketing mix

Global and Local Healthcare Market Trends © IMS Health 30

AGENDA

• Global OTC Context

• Local Trends

• Focus on the Consumer & Channel

• Highlights & Conclusions

Global and Local Healthcare Market Trends © IMS Health 31

• OTC remains attractive as it continues to outpace Pharma

• And as a result the market becomes more competitive

• Emerging markets will be crucial battlegrounds of the future as their importance on the global stage increases

• In more mature markets, innovation is the main growth driver

• Ever increasing trend towards ‘wellness’ and prevention

• Evidence that local players are benefiting from this trend

• The increased consumer and channel focus of the OTC market raises new opportunities ...and new challenges

• How to input real and responsible ‘consumer-focused thinking’

• Taking advantage of new distribution and “consumer access” opportunities ...without losing the relationship with pharmacy

• Excellence in execution is key for success

Highlights and Conclusions

32 Global and Local Healthcare Market Trends © IMS Health

For more information on the content of this presentation please contact:

Francine Nieto Marketing Director, Consumer Health IMS Health

Phone Number: + 44 (0) 20 3075 4102

Thank You!

Global and Local Healthcare Market Trends © IMS Health 33