GLOBAL ADVANCED TECHNOLOGY PARTNER FOR CORE BUSINESS ... · GLOBAL ADVANCED TECHNOLOGY PARTNER FOR...

62

GLOBAL ADVANCED TECHNOLOGY PARTNER FOR CORE BUSINESS OPERATIONS Investors Presentation November 2017

Transcript of GLOBAL ADVANCED TECHNOLOGY PARTNER FOR CORE BUSINESS ... · GLOBAL ADVANCED TECHNOLOGY PARTNER FOR...

GLOBAL ADVANCED TECHNOLOGY PARTNER FOR CORE BUSINESS OPERATIONS

Investors Presentation

November 2017

| 2

This presentation has been produced by Indra for the sole purpose expressed therein. Therefore, neither this presentation nor any of

the information contained herein constitutes an offer sale or exchange of securities, invitation to purchase or sale shares of the

Company or any advice or recommendation with respect to such securities.

Its content is purely for information purposes and the statement it contains may reflect certain forward-looking statements,

expectations and forecasts about the Company at the time of its elaboration. These expectations and forecasts are not in

themselves guarantees of future performance as they are subject to risks, uncertainties and other important factors beyond the

control of the Company that could result in final results materially differing from those contained in these statements. The Company

does not assume any obligation or liability in connection with the accuracy if the mentioned estimations and is not obliged to update

or revise them.

This document contains information that has not been audited. In this sense, this information is subject to, and must be read in

conjunction with, all other publicly available information.

This disclaimer should be taken into consideration by all the individuals or entities to whom this document is targeted and by those

who consider that they have to make decisions or issue opinions related to securities issued by Indra.

Disclaimer

| 3

What is Indra?

Our Strategic Plan

Our delivery & new value levers going forward

Detailed vertical Description

Annex 1: Last quarterly results

Annex 2: VTO of Tecnocom

01

02

03

04

05

06

Index

| 4

Indra: A global Consulting and Technology company 01. Whats is Indra?

€2.7Bn Revenues 2016

34,000 employees

+140 countries

Global

consulting

and technology

company

Business Model

based on our

Proprietary

Products and

R&D

Technology Partner for core business operations

Information Technology (55% of total sales)

Leading Digital company

in Spain and Latam

Energy & Industry

Financial Services

Public Administration & Healthcare

Telecom & Media

Transport & Defence (45% of total sales)

Leading worldwide provider

of proprietary solutions in niche areas

Transport & Traffic

Defence & Security

| 5

We deliver core business operations technology in various industries

01. Whats is Indra?

15%

18%

8%

15%

22%

23%

T&D IT

Sales 2016

Transport & Traffic

• Air Traffic Management

systems and

Communications,

Navigation and

Surveillance systems

• Transport: Railway

management systems,

Urban traffic systems,

highways, tunnels and

traffic control systems

Defence & Security

• Electronic Defence

• Air surveillance

• Military simulation

• Maritime surveillance

• Satellite Communications

Telecom & Media

• Operations and business

support systems

• New media and digital

television solutions

Financial Services

• Insurance and banking core

systems

• Operations transformation and

process efficiency services

Public Admin

& Healthcare

• Comprehensive offer on electoral processes

• Educational and justice management systems

• Healthcare management platform

Energy & Industry

• Energy: generation, distribution and

commercial management solutions

• Industry management solutions

| 6

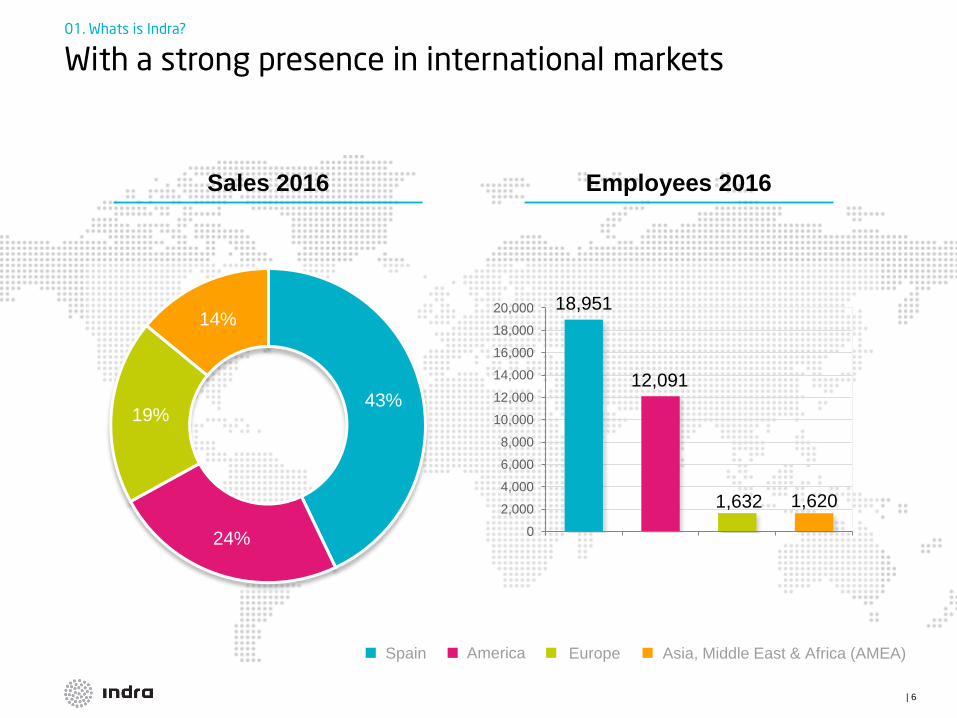

18,951

12,091

1,632 1,620

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

With a strong presence in international markets 01. Whats is Indra?

43%

24%

19%

14%

Sales 2016 Employees 2016

Spain America Europe Asia, Middle East & Africa (AMEA)

| 7

14%

26%

18%

18%

8%

17%

Transport

& Traffic

Financial

Services

PPAA & Healthcare

Energy

& Industry

Telecom

& Media

Defence

& Security

Revenues breakdown by regions and verticals 2016 01. Whats is Indra?

30%

11%

12% 13%

8%

26%

Spanish revenues breakdown

International revenues breakdown

Transport

& Traffic

Financial

Services

PPAA & Healthcare

Energy

& Industry

Telecom

& Media

Defence

& Security

64%

51%

41%

54%

33%

25%

43%

36%

46%

59%

46%

67%

75%

57%

Transport

& Traffic

Financial

Services

PPAA

& Healthcare

Energy

& Industry

Defence

& Security

Telecom

& Media

Total

Spain International

| 8

3,013 2,651 2,744

2,938 2,850 2,709

268 131 229

6.9%(2) 1.6%(1) 6.0%

-92(3) -641(3) 70

81(3) 30(3) 5

47 -50 184

663 700 523

Main figures 2014-16 01. Whats is Indra?

(1) Before non-recurrent items of €687M

(2) Before non-recurrent items of €246M

(3) After non-recurrent items

FY15 FY16 FY14

Order Intake (€M)

Revenues (€M)

EBITDA (€M)

EBIT margin

Recurrent

Net profit Reported (€M)

NWC (DoS)

FCF (€M)

Net Debt (€M)

| 9

Main Shareholders 01. Whats is Indra?

(*) Board of Directors representation

CNMV data. Identified shareholders

with a position in excess of 3%

18.7%

10.5%

9.4%

3.5%

3.4% 3.2%

3.0%

48.3%

Sociedad Estatal de Participaciones

Industriales S.E.P.I (*)

Fidelity Management Research

Corporación Financiera Alba (*)

Others

T. Rowe Price Associates

Norges Bank

Schroders

Allianz Global Investors

| 10

Diagnostic before our strategic plan: we grew in sales despite the crisis in Spain…

02. Our Strategic Plan

We overcame the Spanish crisis

by internationalizing our business

3,000

2,000

1,000

0

Spain - corporations

International

2014

2,938

461

685

1,791

2007

2,168

864

606

698

Spain - public sector

+13%

-47%

+157%

+36%

Spain - public sector

as % of Total Revenues 16% 40%

Sales evolution by geography, 2007 – 2014 (€M)

| 10

| 11

… at the expense of our profitability and cash flow conversion 02. Our Strategic Plan

0

1

2

3

4

5

2014

1.6

2007

3.3

-4

0

4

8

12

16

2007 2014

6.9

-1.4

11.1

Profitability decreased... ...and cash flow eroded

Free cash flow margin (%) Recurrent EBIT margin (%)

-4.2 pps

-1.7 pps

240 204 Recurrent

EBIT (€M) 72 47

Free Cash

Flow (€M)

150 663 Net Debt (€M)

When including

non-recurrent items

| 12

We understood the main causes that impacted our profitability performance

02. Our Strategic Plan

Complex macro

economic

environment & new

industry dynamics

Issues derived from

our strong focus on

growing outside of

Spain

Worst crisis in decades in Spain, our home market

• And worse global conditions than originally expected

outside of Spain

Scenario worsened by new industry dynamics

which have put pressure on pricing and margins

• Global players competing everywhere

• Pressure on client budgets

• Commoditization of traditional technology

In a context of aggressive growth and sales

replacement, we...

• ...lost our focus on cost efficiency

• ...widened our portfolio and focused less on our

value-added segments

• ...didn't quickly react to adjust our go-to-market

strategy

• ...and ended up in an expensive delivery model

| 13

We launched our strategic plan in July 15 02. Our Strategic Plan

Enabler for strategy

implementation

Growth accelerators

Base for sustainable

and profitable growth

Short term

must-dos

Cultural change to be more focused on profitability 06

Growth in new businesses 05

Products

and projects

portfolio

02 Go-to-market

strategy 03 Delivery

model 04

Cost reduction to capture savings and increase Indra's competitiveness

(Plan €180-200m) 01

In p

rogre

ss

Done

| 14

We are refocusing our product and project portfolio based on four levers

02. Our Strategic Plan

Prioritize existing

products portfolio

by focusing on

high value-added

products

Prioritize existing portfolio by focusing

on core business operation products

• Increase share of proprietary

products and end-to-end projects

Push to develop value-added

products focused on core business

operations for our clients

• We already have a strong

portfolio and want to keep

evolving it

Increase standardization

Increase

standardization Industrialize and standardize our offer

to capture economies of scale and

build expertise

• Reduce current portfolio of

products and projects

• Standardize and modularize

projects and products

• Take advantage of greater

standardization in production

processes

Demand

minimum project

requirements

Re-organize

business portfolio

Prioritize valuable projects for Indra

based on a selective funnel procedure

Demand a minimum size / profitability

for our projects to avoid fragmentation

inefficiencies

Complement business portfolio by

including selective investments and

divestments

• Based on cash flow generation

| 15

We are transforming our go-to-market strategy to achieve our target projects and products portfolio

02. Our Strategic Plan

Increase standardization

By re-balancing our business mix towards our own value-added products,

we will increase both profitability and cross-selling activities

Complement geographies' go-to-market

strategies with business specialized

expertise to maximize returns from the

targeted portfolio

Reinforce skills of commercial teams

Train and reinforce sales teams on new vertical offerings, with

specialized teams to deliver the best approach for the client

Selectively leverage third party channels

Take advantage of packaged solutions (e.g. inCMS, inGen...)

to facilitate sales through distribution channels

Increase revenue share per client

Prioritize flagship clients in order to cross-sell

and up-sell other projects and products

Reinforce commercial push

for value-added products

Push for targeted portfolio of

high value product and projects

Assess risk and price accordingly

Increase exhaustive control on offers and requisites

Assess risk in new projects / geographies and clients that

are new for Indra to avoid previous mistakes

Go-to-market

Strategy

| 15

| 16

We are improving the delivery model to increase both profitability and customer references

02. Our Strategic Plan

Industrialized

production Standardized products

that will be produced

efficiently

• In terms of costs,

timings and scope

New high-end tools and

processes for project

management

• Deployed across

all our verticals

Indra will focus on

minimizing errors and,

as a result, overruns

in projects

• Improving Indra's

profitability

Keep improving customer

experience so as to increase

• Loyalty among our

current client base

• Positive external

references to trigger

new sales

Industrialized

production

Customer

experience

and loyalty

Rigorous

project

management

Overrun

minimization

| 17

Defence &

Security

Transport &

Traffic

Energy &

Industry

Financial

Services

TMT

Public Admin

& Healthcare

We launched Minsait in February 2016 to grow in new digital businesses

02. Our Strategic Plan

Go-to-

market

Digital

solutions

Digital

platforms

Human

capital

Business Consultants

Technology Consultants Experts in Cyber Designers

Specific Own Property Solutions (Smart Home, Mobile Sales,...)

Digital platforms (i.e. Sofia2...)

New business

models

Relationship with

clients and citizens

Risk Management &

Cybersecurity

Redefining

operations

Consultoría + Sectores + Otros canales (por productos)

| 17

| 18

We are driving cultural change to be more focused on profitable growth and cash

02. Our Strategic Plan

Individuals

and teams are

engaged for

results

Reinforce

rigorous

project

management

Result-oriented behaviors • Based on accountability...

• ...and linking employee

remuneration to profitability

KPIs

Cultural change to be more focused on profitable growth

and cash generation

Processes and tools • Redefine offer approval

processes

• Reinforce controlling to support

performance measurement

People

People skilled and ready for

new strategy • Promote specialized vertical

business know-how

• Reinforce trainings and

people development

A cash flow target has already been set to define Indra's top

management team variable compensation

+ +

| 18

| 19

2,938 CAGR1

2.5%-4.5%

204 (6.9%) 10%-11%

47 (1.6%)

~200 (~6%)

2.5x ~1.0x

2018 2014

Revenues (€M)

Recurrent EBIT margin (€M)

(% of revenues)

FCF (€M)

(% of revenues)

Net Debt / EBITDA

2018 Targets for our Strategic Plan 02. Our Strategic Plan

1. Organic growth. Constant exchange rates as of 2014 (average FX in 2014).

| 20

• Global and local investment recovery

• Proprietary product portfolio and proven track-record

to boost international sales

• Strengthening of commercial partnerships and

optimization

of production and purchasing processes

509 3%-5%

• Take advantage of Single European Sky through

SESAR

and iTEC

• Push for Nation Wide projects

• Maintain growth and leadership in CNS equipment

620 3%-5%

• Product mix change towards higher value-added solutions and improving client mix

– More focus on private and global clients – More focus on national public clients in Public

Admin • Leverage Indra Digital's offering • Take advantage of optimized delivery model

1,809 2%-4%

Rationale

Defence & Security

Transport & Traffic

IT verticals

2018 Sales Targets by businesses 02. Our Strategic Plan

1. Organic growth. Constant exchange rates as of 2014 (average FX in 2014).

Sales

2014 (€M)

Expected CAGR1

2014 – 2018 (%)

| 21

Our performance since July 2015 (I) 03. Our delivery & new value levers going forward

• Revenue pressure in IT & Transport because of

• Macro headwinds (forex, oil and raw materials

price influence in public budgets, delays in

Spanish public budgets in 2015, 2016, 2017?,…)

• Slower portfolio rotation

• Strategy and portfolio of Transport division under

review

• More transformation required in terms of our

commercial capabilities, cultural change and portfolio

simplification.

• More than expected provisions for onerous

projects

• Our operations have improved…..

• New commercial strategy with a global customer

targeting

• Prioritized portfolio of core solutions and strict

offering process, bringing better quality of the

backlog

• Defence and Security growth beyond guidance

• Better understanding of cost levers, with the majority

of the cost reduction plan successfully implemented

• … and are reflected in our financial results

• Sounder balance sheet after write offs

• Improvement in operating margins

• Stable and recurrent FCF generation

• Deleverage delivery

Restructuring is mostly behind us – we have set the base for future profitable

growth, although we will continue with transformation of our operations

Highlights Lowlights

| 21

| 22

Our performance since July 2015 (II) 03. Our delivery & new value levers going forward

2014 2015 2016

% Change

14/16

Clients 710 699 642 -9,6%

Billables 961 838 673 -30,0%

Inventories 231 70 69 -70,1%

6,6x

2,3x

3Q15 4Q16

2018

76

163

181 184

1Q16 2Q16 3Q16 4Q16

2018

~200

€M

Balance Sheet (€M) Margin Improvement

45

162

1,6%

EBIT FY15

6,0%

EBIT FY16

+4,4pp

LTM FCF Evolution (€M) Net Debt / EBITDA LTM (x)

~1.0x

| 23

New value levers going forward 03. Our delivery & new value levers going forward

• Operating leverage on revenue growth

• Higher direct margin on

• Better mix and quality backlog

• Less low-profitability and onerous projects

• Pending cost savings from Investor Day plan

Management

Priorities

FY17

Levers for

EBIT Margin

expansion

• Generate profitable growth from our proprietary differential core offer

• Focus on our core businesses and solutions

• Seize Macro tailwinds, Defense budgets growth and digital business opportunities

• Increase commercial intensity and operational transformation in key geographies

• AMEA as high growth engine geography based on proprietary offer

• LATAM improvement in commercial positioning (focus on local private customers and T&D growth)

and better quality backlog

• Continue with operational transformation all across the board

• Continuous monitoring of low profitability and onerous projects

• Maintain cost efficiency once the Investor Day cost savings plan is almost fully captured

• Evolve current delivery model towards a global one with a more efficient management of resources

| 24

Detailed vertical description 04. Detailed vertical description

Defence

& Security

IT Verticals

Transport

& Traffic

| 25

Global and local investment recovery: changing economic cycle will strengthen Indra's business

04. Detailed vertical description

On top of these macro trends, Defence value is migrating

from platforms to systems and data

Increased uncertainty and local conflicts foster investments

in Defence and Security

• Asymmetric warfare scenarios, global terrorist and piracy threats

• Huge raise in cyber attacks

• Tension increasing in Eastern Europe with NATO countries raising

their defence budgets

• ISIS activity in North Africa and Middle East

• Increasing migratory pressure towards Europe

• Drug smuggling circuits in LatAm

Better Spanish perspectives implying increased investment

in Defence

Major multiyear programs will help us to develop new

offerings

298 278 318

0

500

Top 89 countries in Defence spending (€Bn)1

2011 2014 2018

Global investment cycle recovery Spanish investment cycle recovery

-2%

/ year

-2%

/ year

Remotely Piloted

Aircraft Systems

(RPAS)

Total:

c.€250M

Space

Surveillance &

Tracking Radar

NH90 Helicopters

F110 Frigate

8x8 Armoured

Vehicles

1. Sum of procurement and RTD&E – Research, Testing, Development & Evaluation, stated in constant €. Source: Jane's Defence Budgets October 2014, Kongsberg Gruppen, Pareto Securities Equity Research.

Electronic

Defence Updates

(Vetronics)

Santiago’s Project

| 25

| 26

Defence and Security: we recovered our sales by strongly internationalizing our offering

04. Detailed vertical description

335

152 113 118

187 197

298

311 382 408

369 402

633

463

495 526

556 599

0

100

200

300

400

500

600

700

2007 2012 2013 2014 2015 2016

Spain

International

% International

sales

Sales (€M)

~50% ~70%

7%

/year

| 27

Defence and Security: we recovered our sales by strongly internationalizing our offering

04. Detailed vertical description

Main accessible geographies for European players

are Europe, AMEA and LatAm

Electronic

Defence

5

12

6

6

9

3

Maritime Surveillance

Indra's accessible

market size (2015 €Bn)

SATCOM

Cyber Defense

Air Surveillance

Training and Simulation

Electronic Defence

3

6

8

10

3

6

Expected market growth

(% CAGR 2015-18)

Systems

provider

Prime

Indra is a specialist provider in selected

market segments

Air

Surveillance

Military

Simulation

Maritime

Surveillance

Cyber

Defence

Satellite Communications

Note: SATCOM: Satellite Communications. Source: Strategic Defence Intelligence, IHS Jane's.360, Visiongain, Indra Analysis.

| 27

| 28

European

competitor

Air

Surveillance

Military

Simulation

Maritime

Surveillance

Electronic

Defence

Satellite

Communication

Indra

A

B

C

D

E

Indra’s position

in Europe #2 #2 #2 #4 #4

We are a significant European player in the market segments of activity...

04. Detailed vertical description

Source: Strategic Defence Intelligence, IHS Jane's.360, Visiongain, Companies' websites. Indra Analysis.

| 29

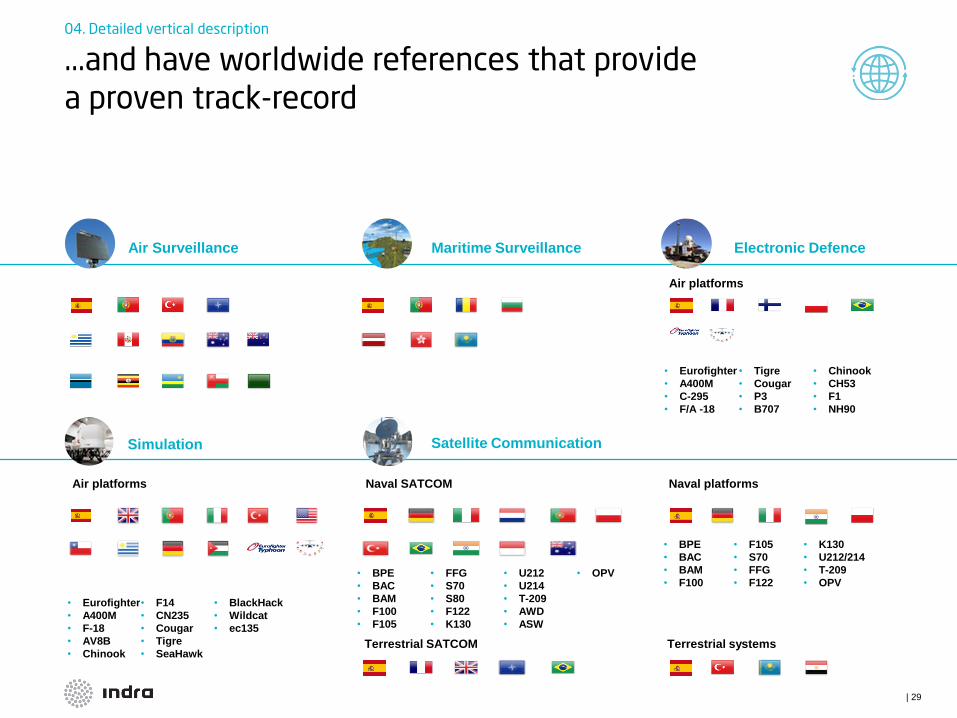

...and have worldwide references that provide a proven track-record

04. Detailed vertical description

Air platforms

Air platforms

Air Surveillance Maritime Surveillance Electronic Defence

• Eurofighter

• A400M

• C-295

• F/A -18

• Tigre

• Cougar

• P3

• B707

• Chinook

• CH53

• F1

• NH90

Terrestrial systems

Naval platforms

• BPE

• BAC

• BAM

• F100

• F105

• S70

• FFG

• F122

• K130

• U212/214

• T-209

• OPV

• BPE

• BAC

• BAM

• F100

• F105

• FFG

• S70

• S80

• F122

• K130

• U212

• U214

• T-209

• AWD

• ASW

• OPV

Naval SATCOM

Satellite Communication

Terrestrial SATCOM

Simulation

• Eurofighter

• A400M

• F-18

• AV8B

• Chinook

• F14

• CN235

• Cougar

• Tigre

• SeaHawk

• BlackHack

• Wildcat

• ec135

| 30

We will keep strengthening our network of commercial partners

04. Detailed vertical description

Air platforms Naval platforms Terrestrial platforms

| 31

Transport & Traffic: Consolidated position in Air Traffic Management (ATM)

04. Detailed vertical description

% ATM of Transport

& Traffic sales

Sales (€M)

~40%

158

316 279 271 280 270

236

351 333

399 394 355 394

667 611

670 674 625

0

100

200

300

400

500

600

700

800

2007 2012 2013 2014 2015 2016

ATM

Transport

| 32

ATM is an attractive market due to its sustained growth and stability

04. Detailed vertical description

Note: ATM: Air traffic management. CNS: Communication, Navigation & Surveillance. Source: Markets&Markets, Infinity Reports, Indra.

€3Bn

Global

Large

projects &

equipment

Sustained

growth

Technological

lead

(Europe)

High entry

barriers

Market dynamics Global market size

CNS

Equipment

4%

ATM

Systems

2%

Expected growth

rate 2015 – 2018

(%/year)

| 33

We are one of the most relevant partners at SESAR... and will materialize this through iTEC deployment

04. Detailed vertical description

Phase I Phase II SESAR 2020

Indra as one of the three

main industrial partners

Expecting to start in 2016, Indra

to keep a leading position

iTEC members

potential new entrants

iTEC: The system developed by Indra along with its air navigation

service provider partners (DFS, NATS, ENAIRE, LVNL)

to deploy the SESAR capabilities

Indra as one of the founding members of the

Single European Sky R&D Joint Undertaking

The iTEC Alliance aiming to cover an

important portion of the Single European Space

Note: SESAR: Single European Sky ATM Research. iTEC: interoperability Through European Collaboration. DFS: Deutsche Flugsicherung. NATS: National Air Traffic Services. LVLN: Luchtverkeersleiding Nederland. Source: Indra.

iTEC members: Spain, Germany, Netherlands, UK Potential new entrants: Norway, Poland, Lithuania, Bulgaria and Romania

| 34

We are maintaining growth and leadership in CNS equipment by boosting our flagship products

04. Detailed vertical description

Note: MSSR: Monopulse Secondary Surveillance Radar. PSR: Primary Surveillance Radar. ILS: Instrument Landing System. DVOR: Doppler VHF Omnidirectional Range . DME: Distance Measurement Equipment. Source: Indra.

• Competitive and latest technology product

• Most-sold PSR in 2014 (outside of US)

• Flagship and leader product globally (outside of US)

• >175 installations worldwide

• References in China, India, Australia, Indonesia, Turkey,

Poland, Spain, Latin America...

• DVOR: low cost and highly reliable equipment ready for

the most severe conditions

• DME: highly reliable distance measuring equipment

• Flagship and leader product globally (outside of US)

• Proven, reliable landing system that has guided aircraft

to well over 100 millions safe landings

• In more than 1,200 runways worldwide in the most demanding airports

Surveillance

Navigation

ILS

DVOR

DME

PSR

MSSR

| 35

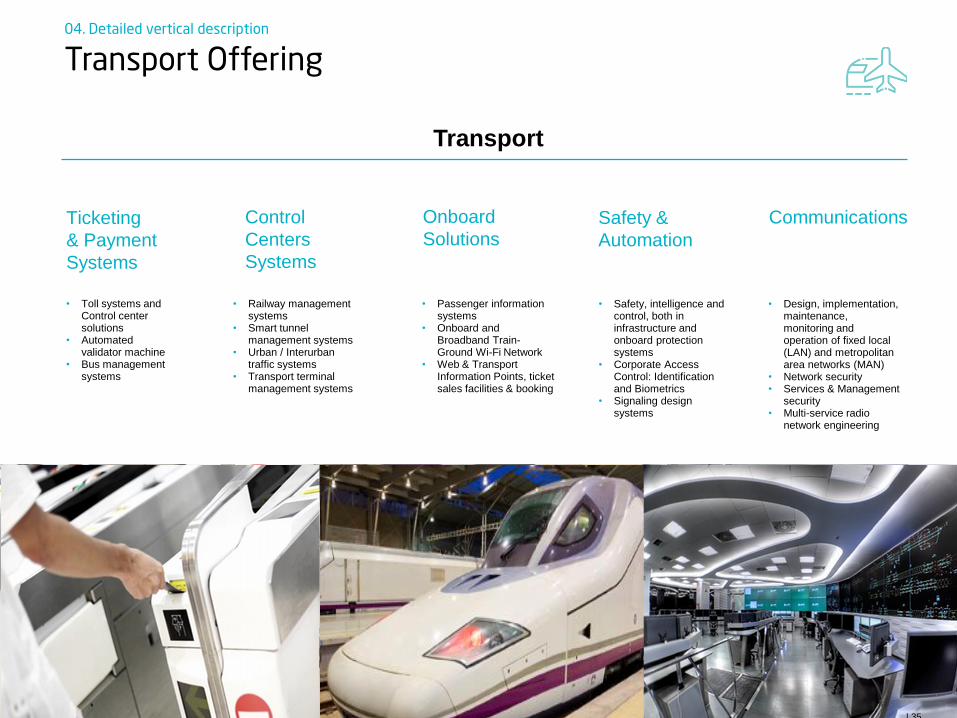

Transport Offering 04. Detailed vertical description

Safety &

Automation

Communications Onboard

Solutions Ticketing

& Payment

Systems

Control

Centers

Systems

• Passenger information systems

• Onboard and Broadband Train-Ground Wi-Fi Network

• Web & Transport Information Points, ticket sales facilities & booking

• Design, implementation, maintenance, monitoring and operation of fixed local (LAN) and metropolitan area networks (MAN)

• Network security • Services & Management

security • Multi-service radio

network engineering

• Safety, intelligence and control, both in infrastructure and onboard protection systems

• Corporate Access Control: Identification and Biometrics

• Signaling design systems

• Railway management systems

• Smart tunnel management systems

• Urban / Interurban traffic systems

• Transport terminal management systems

• Toll systems and Control center solutions

• Automated validator machine

• Bus management systems

Transport

| 35

| 36

296 517 503 516 458 398

215

369 355 298 251

212

276

464 470 475 488

476

354

460 479 453

426

400 1,140

1,811 1,808

1,742 1,621

1,485

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2007 2012 2013 2014 2015 2016

Energy&Industry

Financial Services

Telecom&Media

Public Administrations & Healthcare

IT: Rebalancing our portfolio torwards on proprietary solutions

04. Detailed vertical description

% IT

of Total Sales

Sales (€M)

~ 50% ~ 60% ~ 55%

-5%

/year

| 37

Our vision on IT value creation: core business operations with value-added digital solutions

04. Detailed vertical description

Core business operations Digital

Billing

Telcos

Network

Management

Network

Management

... Billing Utilities

Channel

Management

Operations – Mobility

Media

Channel

Management

Core

Operations

Official

Reporting

Customer Management

Key drivers Key drivers

Efficiency

Reliability

Industrialized delivery

Proof of value

Innovation – trial & error

Agility

Plant

Management

Core business

operations

Industry

& Retail Energy TMT

Financial

Services

| 38

We have a presence in very attractive market segments

04. Detailed vertical description

We will focus our strategy on boosting our portfolio of proprietary products

~60

~120

Vertical

Solutions ~40

IT Outsourcing,

AM & ITO

BPO BPO 6.1%

IT Outsourcing,

AM & ITO 4.4%

Vertical

Solutions 6.8%

Product

development

AM, ITO, & IT

Outsourcing

BPO

Proprietary

products 3rd party

software

Global Market Size

(2015 €Bn)

Expected Market Growth

(% CAGR 2015-18)

| 38

| 39

We have developed a unique portfolio of proprietary products for core business operations

04. Detailed vertical description

By re-balancing our business mix towards our own value-added products,

we will increase both profitability and cross-selling activities

Portfolio of proprietary products... ...balanced across the maturity curve

Energy

& Industry

Media TV

Elections

OSS solutions

TMT

Financial

Services

Public Admin

& Healthcare

Cash flo

w g

enera

tion

Maturity

Elections

Set of products supporting core business operations across the industry's whole value chain

Last generation software co-developed by partnering up with key clients

Leading products implemented by our people all over the globe

Extended life cycle

Product

development

catalyzed

Impact with digital complementation

| 39

| 40

Through Minsait we are complementing our vertical offer with high value-added solutions and catalyze its evolution

04. Detailed vertical description

Strategy

Value proposition

Business model

Business plan

Operational model

Action plan

Implementation of business

solutions

Architecture

Design

Technology implementation

Support

Solutions portfolio

Product design and evolution

Specialized support

Business consulting

Technology Digital solutions

Strategy

Consultants

Management

Consultants Product Designers

& Experts

Technology

Consultants

Solutions

Architects

Experience

Designers

Data

Scientists

Cybersecurity

Experts

| 40

Annex I: Last quarterly results

| 42

REVENUES UP +8% IN REPORTED TERMS

Reported +8%

9M17 Sales Growth 3Q17 Sales Growth

Local Currency +8%

Organic Terms (Ex-Tecnocom)(1) -1%

Reported +19%

Local Currency +20%

Organic Terms (Ex-Tecnocom)(1) +7%

(1) Sales excluding Tecnocom and in local currency

(*) Displayed data includes Tecnocom consolidation since April 18th, 2017

€M €M

1.951

13167

15

2.116

9M16 FX Impact Tecnocom Underlying

growth

9M17*

619

7

85 40

737

3Q16 FX Impact Tecnocom Underlying

growth

3Q17*

Annex I. Last quarterly results Results

9M17

| 43

REVENUES BY VERTICAL

Local Currency / Reported

T&D

IT

Revenues (€M)

Energy & Industry

Financial Services

Telecom & Media

PPAA & Healthcare

Transport & Traffic

Defence & Security

(*) Displayed data includes Tecnocom consolidation since April 18th, 2017

446 403

401 40821% +2% / +2% 19%

-4% / -4%847 811

23% 19%-10% / -10%

161 171

298 355

352

437

293

3411.104

1.305

9M16 9M17*

8%

15%

18%

15%

8%

17%

21%

16%

+5% / +6%

+19% / +19%

+23% / +24%

+16% / +16%

+17% / +18%

Annex I. Last quarterly results Results

9M17

| 44

Annex I. Last quarterly results

(*) Displayed data includes Tecnocom consolidation since April 18th, 2017

REVENUES BY REGION

Spain

America

Europe

AMEA

Local Currency / Reported

Revenues (€M)

255 306

352359

481467

863985

1.951

2.116

9M16 9M17*

44%

13%

18%

25%

47%

14%

17%

22%

+2% / +2%

+20% / +20%

+14% / +14%

-6% / -3%

+8% / +8%

Results

9M17

| 45

Annex I. Last quarterly results

238 304

389446

452

528

1.001

1.074

2.080

2.351

9M16 9M17*

48%

11%

19%

22%

46%

13%

19%

22%

+15% / +15%

+28% / +27%

+7% / +7%

+14% / +17%

+13% / +13%

ORDER INTAKE UP +13% IN REPORTED TERMS

Local Currency / Reported Local Currency / Reported

Order Intake by Region (€M) Order Intake by Vertical (€M)

Energy & Industry

Financial Services

Telecom & Media

PPAA & Healthcare

Defence & Security

T&D

Transport & Traffic

(*) Displayed data includes Tecnocom consolidation since April 18th, 2017

444 386

45435922%

-21% / -21% 15%

-17% / -17%898

745

21% 16%-13% / -13%

137 173

308

493

401

514336

427

9M16 9M17*

19%

16%

21%

22%

7%

21%

22%

18%

+25% / +26%

+60% / +60%

+27% / +28%

+26% / +27%

+35% / +36%

1.183

1.607

Results

9M17

| 46

Annex I. Last quarterly results

BRAZIL

Revenues

EBIT(*)

EBIT Margin(*)

6 out of the 7 onerous projects already closed/finished

(local currency)

Order Intake

(*) EBIT includes contingencies

Results

9M17

| 47

Annex I. Last quarterly results

34

46

EBIT 3Q16 EBIT 3Q17*

5,5%

6,3%

35,5%

+0,8pp

104124

EBIT 9M16 EBIT 9M17*

5,3%

5,8%

18,7%

+0,5pp

EBIT MARGIN EVOLUTION

9M EBIT margin by Divisions 9M EBIT Margin Evolution

IT T&D

EBIT Margin Evolution Ex-Tecnocom

(*) Displayed data includes Tecnocom consolidation since April 18th, 2017

3Q EBIT Margin Evolution

12,0%13,0%

9M16 9M17*

0,3%1,4%

9M16 9M17*

46

119

EBIT 3Q17* EBIT 9M17*

7,0%

6,1%

Results

9M17

| 48

Annex I. Last quarterly results

115,4

153,8

9M16 9M17*

33%

-79 -85

-23

137

47

2

-5

140

-5

-26

75

1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17

STRONG OPERATING FCF GENERATION DUE TO OPERATING IMPROVEMENT AND 3Q17 NWC

Quarterly FCF (€M)

Accumulated FCF LTM (€M)

9M15: €-187M 9M16: €44M

OPERATING FCF BEFORE WC (€M)

9M17: €44M

(*) Displayed data includes Tecnocom consolidation since April 18th, 2017

-114-136

-50

76

163 181 184132

104

184

1H15 9M15 FY15 1Q16 1H16 9M16 FY16 1Q17 1H17* 9M17*

Results

9M17

| 49

Annex I. Last quarterly results

523

44

185 16

680

Net Debt FY16 9M17* Free Cash Flow Tecnocom Payment Net Debt Tecnocom &

Others

Net Debt 9M17*

NET DEBT BRIDGE

Net Debt Bridge – Cash Flow (€M)

Net Debt Bridge – Tecnocom’s split(€M)

(*) Displayed data includes Tecnocom consolidation since April 18th, 2017

523

154 1631

2427 11

201

680

Net Debt FY16 Operating Cash

Flow

Net Working

Capital

Other Operating

Changes

Capex Taxes Net interest &

Subsidies

Financial

Investments & Non-CF items &

Others

Net Debt 9M17*

FCF = €44M

Results

9M17

| 50

Annex I. Last quarterly results

NET WORKING CAPITAL EVOLUTION

Net Working Capital (DoS)

2 945 -81-1 10

Accounts Receivable Accounts Payable Inventory

(*) Displayed data includes Tecnocom consolidation since April 18th, 2017

77 74

-82 -80

9 11

5 4

FY16 9M17*

+1

-3

+2

76 74

-76 -80

10 11

10 4

1H17* 9M17*

-4

-2

+1

Results

9M17

| 51

Annex I. Last quarterly results

5.9x6.6x

5.4x4.7x

3.1x 3.1x2.3x 2.3x 2.9x 2.5x

2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17

825 837

700659 659 666

523

532

745

680

NET DEBT EVOLUTION

Net Debt

Net Debt (€M)

Net Debt/EBITDA LTM (Times)(2)

ND/ EBITDA LTM(2)

(1) Non-recourse factoring (2) 2Q17 and 3Q17 ratio includes LTM EBITDA Indra & LTM EBITDA Tecnocom (part of this data is considered as if Tecnocom would have been managed by the former Managament) (3) 2Q17 and 3Q17 ratio includes Indra Net Debt and LTM EBITDA Indra, both excluding Tecnocom effect

(Factoring)(1) (187) (162)

(173) (176)

(187)

(187)

(187)

(187)

(187)

2,4x

Indra Stand-alone

ND/ EBITDA LTM(3)

Indra Stand-alone

Net Debt

554

(187)

460

1,9x

Results

9M17

| 52

Annex I. Last quarterly results Results

9M17

638

18

342

135

823

Cash 2017 2018 2019 Beyond

2020

171

439

135

823

Credit Facilities 2017 2018 2019 Beyond 2020

1.568

Available Credit Facilities

DEBT STRUCTURE 9M17* 2016

Total % of total (€M)

(€M)

Gross Debt Maturity Profile

Total % of total

(*) Displayed data includes Tecnocom consolidation since April 18th, 2017

Net Debt

Available Facilities

(€M)

Annex II: Voluntary tender offer

for the acquisition of

100% of the share

capital of TECNOCOM

| 54

Deal terms review Annex II. VTO of Tecnocom

Key transaction terms

• Announcement of the VTO: 29/11/2016

• Transaction settlement expected on Q2 2017

• Offer price per share: €4.253 paid with mixed consideration: cash (60%) and Indra shares (40%)

• €2.55 in cash and 0.1727 Indra shares per each Tecnocom share3

• Offer price represents:

• 12% premium vs. previous closing price (€3.81 as of 28 November 2016)

• 28% premium vs. the 3-month volume weighted average price (€3.324)

• Transaction subject to the following conditions:

• Approval from the relevant anti-trust authorities

• Minimum VTO acceptance rate of 50.01% of Tecnocom share capital (excluding Irrevocable

Commitments), and 70.01% of total share capital

• Indra’s General Shareholders Meeting approval of the capital increase related to the transaction

Price considerations

Condition

precedents

Transaction

structure • Voluntary Tender Offer (“VTO”)

Timetable

• Indra has subscribed Irrevocable Commitments with Tecnocom shareholders representing 52.7% of the share

capital, by which they commit to irrevocably tender their shares in the context of the VTO

Irrevocable

Commitments

Valuation

• The VTO values the 100% share capital1 of Tecnocom in €305m (“Equity Value”) and the entire company in

€336m (“Firm Value”)2

• Implicit transaction multiple: 14.3x Firm Value / EBIT’ 17E (pre synergies)2

• Implicit transaction multiple: 5.2x Firm Value / EBIT’ 17E (post synergies)2

• Double digit EPS accretion since year 1 (ex. restructuring costs)

1 Excluding treasury shares as of 2 September 2016 (3.2m shares) 2 Firm Value calculated as Equity value plus net debt as of 9M 16 (€27.2m) plus minorities as of H116 (€3.7m); EBIT pre-synergies based on the estimates of brokers included in Bloomberg´s consensus

(Ahorro Corporación and JB Capital Markets) for that year (€23.5m); EBIT post-synergies calculated as broker consensus EBIT plus €41m of estimated fully-phased synergies 3 Exchange ratio calculated as the mid-point of (i) the average of closing prices and (ii) the volume weighted average price of the five trading days prior to November 28th

4 Bloomberg from 29 august 2016 until 28 November 2016

| 55

Overview of Tecnocom Annex II. VTO of Tecnocom

Banking & Insurance

51% Industry 18%

TME 22%

Public Adm. 9%

Business overview

Revenue breakdown 9M 2016

Spain 81%

International

19%

1 Information and Communications Technology; 2 Based on Tecnocoms public result presentations / Recurring EBITDA excludes provisions; 3 Based on Tecnocom’s annual accounts (calculated as Operating profit plus

depreciation & amortisation); 4 Defined as EBT plus D&A, impairments, financial expenses, provisions minus change in working capital and taxes; 5 Net debt / LTM recurring EBITDA

Financial overview

€m 2014 2015 9M 2015 9M 2016

Revenues 372 406 291 300

% growth 9.2% +3.1%

Recurring EBITDA2 17 22 17 21

% margin 4.5% 5.4% 5.9% 6.9%

EBITDA3 15 22 17 20

% margin 4.1% 5.4% 5.7% 6.5%

EBIT 7 12 9 12

% margin 1.8% 2.8% 3.1% 3.9%

Consolidated net income (12) 4 1 5

% margin - 0.9% 0.4% 1.8%

Operating cash flow4 19 27 n.a. n.a.

Net debt 39 27 59 27

Net debt / recurring EBITDA 2.6x 1.2x 3.0x5 1.1x5

General

overview

ICT1 consulting firm with presence in Iberia and LatAm

Direct presence in +9 countries

+6,500 employees

Consolidated positioning both in niche areas such as

Payment Systems and traditional IT levers such as

Outsourcing

Consolidated

position in

Payment

Systems

c.90% of the Spanish financial institutions as

customers

Strong position in LatAm

Relevant

player in the

Spanish IT

sector

82% revenues coming from recurring services

Blue chip,

diversified

and loyal

client base

+1,000 clients with top 10 < 40% of revenues

+16 years of presence in key clients

22 IBEX-35 companies as clients

60% of revenues from clients with investment

grade

By geography By vertical

Ladislao Azcona

19%

Luis Solera 6%

Leonardo Sánchez

5%

Other Board members

2% Abanca

20%

KPN 11%

33%

Trasury stock 4%

Shareholding base

Free Float

| 56

Acquisition rationale Annex II. VTO of Tecnocom

1

Substantial improvement of Indra’s positioning in the Spanish IT market, providing the

Group with increased operational leverage

Fully-aligned with Indra’s strategy to reinforce its proprietary and digital-focused

offering (payment systems)

Highly complementary blue chip client base

2

Significant value creation potential through the implementation of cost synergies

Meaningful revenue synergies based on cross-selling and up-selling to both

companies' respective customer bases

Further potential cost savings derived from higher production efficiencies

3 Similar cultures leading to an easier integration process

Reinforcement of existing talent base in key growth areas

Industrial

rationale

Significant

synergetic

potential

Other

advantages

| 57

Industrial rationale – Substantial increase of Indra’s operating leverage and positioning in IT

Annex II. VTO of Tecnocom 1

30%

70%

34%

66%

Consolidation of IT

market position in

Spain and increased

critical mass

Scalability of the

delivery model Larger scalability and profitability enhancements derived from the evolution of Indra’s delivery model

Significant boost to

Financial Services

segment

Consolidation of Indra´s position the Financial services

segment

Value-added sector with high growth prospects fuelled

by the development of Fintech and the ongoing sector

transformation

Financial Services evolution over total IT revenues pre &

post acquisition (2015)

Increases exposure to

private sector in Spain

Improvement of Indra’s national IT private-public mix,

increasing private sector exposure to c.78% post

transaction

Private IT revenues in Spain3 pre & post acquisition

(2015)

Spanish IT ranking by 2015 sales2 (€m)

€1,621 m

1 FY 2015; 2 Based on Computing Consulting report, Registro Mercantil and Company information; 3Assumes all public revenues of Tecnocom are generated in Spain

€2,028m

€488m €685m

819

823819 810

398 317

317

1,136

Ithaca

+T

rium

ph

Acc

entu

re

Ithaca

Ieci

sa

Eve

ris

Trium

ph

+39%

c.75% c.78%

IT revenues in Spain would increase from €819m1 to

€1,136m1 (+39%)

Significant improvement of operating leverage on

existing fixed costs

| 58

Industrial rationale – Fully aligned with Indra’s strategy to reinforce its proprietary and digital-focused offering

Annex II. VTO of Tecnocom 1

itecban

Indra High value-added offer proposition

Reinforcement of Indra’s Financial Services offering

through Tecnocom’s proprietary Payment Systems’

solutions

Focus on proprietary

solutions

Payment systems is a

fast growing niche

market with meaningful

room for further

penetration

Key data and main own solutions

+100m Cards under

management

+7k ATM

+500 Professionals

+100k POS

Strong growth prospects as a result of the digital

transformation

Significant impact not only within the Financial

Institutions environment but also in other sectors

such as retail, utilities and telco

Significant potential for further penetration in Spain and

LatAm

Payment system industry revenues1 ($ trillion)

1 Industry reports from BNP Paribas, J.P. Morgan, Morgan Stanley, PwC; 2 IDC (2015) ; 3 PwC and IE Business School joint publication (2015)

0.3 0.3 0.4 0.4 0.1 0.2 0.2 0.2 0.4 0.4 0.4 0.5 0.5

0.6 0.7 0.7

2011 2012 2013 2014

America LatAm Europe & ME Asia

1.3 1.5

1.7 1.8

SIA SAT

SFC

+ Core

solutions in

Payment

Systems

+12%

CAGR

‘11-’14

+15%

CAGR

‘15-’192

Non-cash transactions penetration by country (2013)3

59% 57%

45%

16% 15%

| 59

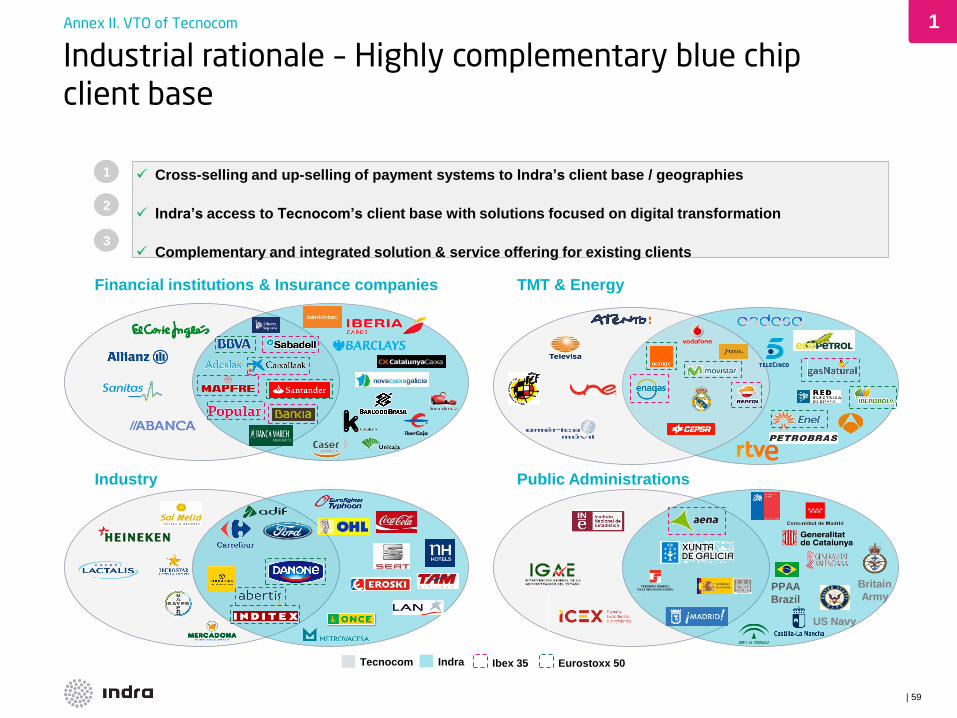

Industrial rationale – Highly complementary blue chip client base

Annex II. VTO of Tecnocom 1

Financial institutions & Insurance companies TMT & Energy

Industry Public Administrations

PPAA

Brazil

US Navy

Britain

Army

Tecnocom Indra Ibex 35 Eurostoxx 50

Cross-selling and up-selling of payment systems to Indra’s client base / geographies

Indra’s access to Tecnocom’s client base with solutions focused on digital transformation

Complementary and integrated solution & service offering for existing clients

1

2

3

| 60

Significant synergy potential – Strong value creation for Indra

Annex II. VTO of Tecnocom 2

Revenue

synergies

• Better competitive positioning based on an overlapping geographical footprint

and complementary client base

• Potential revenue synergies from cross-selling and up-selling (specially in

Financial Services, Industry and Utilities)

Operating

synergies

• Potential SG&A expenses optimization through commercial and overheads

costs

• Further potential costs savings derived from higher production efficiencies and

enhancement of operating model (combination on capacity utilization, average

pyramid, offshore leverage, etc)

• Integrate real state footprint (facilities rationalization)

• Other potential synergies including: optimization of R&D efforts and capex

thanks to enhanced scalability, etc.

€10.5m

€30.5m

Total Quantified annual fully-phased synergies of c.€41m1 achieved by year 2

| 61

Overview of the combined entity (LTM Sep-16 pre-synergies) Annex II. VTO of Tecnocom

1 Last twelve months figures as of September 2016 based on public information 2 Tecnocom revenues in the Industry segment 3 Tecnocom revenues in the TMT & Energy segment

Revenue breakdown by

vertical (Sept. 2016 – LTM)1

Revenue breakdown by

region (Sept. 2016 – LTM)1

22%

17%

15% 8%

15%

23%

49%

11%

23%

17% 19%

21%

14%

25%

20%

Defence & Security

Financial Services

Public Admin. & Healthcare TMT

+ =

44% 56%

0 0 0 0

49%

51%

Spain

International + = 80%

20% 0 0 0 0

25%

2

3

Sept. 16 - LTM (€mm)1 Indra Tecnocom Indra + Tecnocom (pre-syn.) Delta (%)

Revenues 2,732 415 3,147 +15.2%

Recurring EBITDA 218 25 243 +11.5%

% margin 8.0% 6.1% 7.7%

Recurring EBIT 151 14 165 +9.3%

% margin 5.5% 3.4% 5.2%

Investor Relations [email protected]

Avda. de Bruselas 35

28108 Alcobendas,

Madrid Spain

T +34 91 480 50 00

F +34 91 480 50 80

www.indracompany.com