Glf d Pt l lGulfsands Petroleum plc Corporate Presentation · • Gulfsands is a profitable oil...

26

G lf d Pt l l Gulfsands Petroleum plc Corporate Presentation June 2008 June 2008

Transcript of Glf d Pt l lGulfsands Petroleum plc Corporate Presentation · • Gulfsands is a profitable oil...

G lf d P t l lGulfsands Petroleum plc

Corporate Presentation

June 2008June 2008

IntroductionIntroduction• Gulfsands is a profitable oil production, development

and exploration company with assets in Syria and theUSA and business development activities in IraqUSA, and business development activities in Iraq

• Strategic focus is on

• Maximising value of existing assets (e.g.Khurbet East)

• Growth through operated exploration in Block 26Growth through operated exploration in Block 26• Capture of exploration/ development projects in

Iraq* Reserves estimate as at 31 Dec 2007 by RPS Energy Plc (London)

• Production from Khurbet East Field will provide astep-change in Gulfsands attributable production, withthe balance shifting from primarily natural gas

** Reserves estimate as at 1 Jan 2008 by NSAI (Houston) and Collarini Associates (Houston)

production to a larger proportion of oil production

• Key executive positions relocated to London, due to

2

expected increased activity level in Middle East

Management TeamManagement TeamExecutive management

Executive Chairman Andrew West - Over 25 years experience in investment banking including senior positions at Smith Barney, Lehman

(until CEO appointed)Brothers, Guinness Mahon and Strand Partners.

- Long advisory involvement in the oil and gas sector.- Formerly Chairman of Sibir Energy PLC

President Mahdi Sajjad • Extensive experience in oil and gas, mining and industrial projects as well as capital markets in the MiddleEast, Europe, USA, Africa and Asia and as founder shareholder and financier of a number of companiesin these sectors.

• Formerly Senior Executive and Managing Director of International Development Corporation, and formerlyDirector of Oil & Minerals Development Corporation.

CFO Andrew Rose • Former CFO of Burren Energy, which was acquired by ENI for US$3.6 billion in January 2008.

• Was a key director in developing and building Burren from a small private company, through a LondonSt k E h li ti t f th UK’ t f l id ti i d d t il iStock Exchange listing, to one of the UK’s most successful mid tier independent oil companies,culminating in its sale to ENI.

• Extensive former experience in investment banking- was formerly Head of Corporate Finance for EasternEurope, Middle East and Africa at Societe Generale.

Director of Corporate Development Ken Judge • Corporate lawyer with extensive experience in oil and gas, mining and technology companies in theUnited Kingdom Middle East USA Australia Europe Canada Latin America and South East AsiaUnited Kingdom, Middle East, USA, Australia, Europe, Canada, Latin America and South East Asia.

• Currently a director of Carnarvon Petroleum Ltd and a number of UK and Canadian listed mining andtechnology companies.

Exploration Manager Jason Oden • Professional geophysicist with 23 years experience in upstream petroleum.

• Formerly worked in a series of technical and management roles with Suncor and BHP Billiton Petroleum-extensive experience in variety of successful exploration and development projects worldwide.

Non Executive management

Non-Executive Director David Cowan • Extensive experience as a lawyer in the area of corporate and securities law, with natural resourcesexperience, and with specific Middle East region experience in Syria, Iraq and Algeria.

3

• Currently a partner with Lang Michener LLP.

Shareholder structureShareholder structure

Top 10 holdersTop 10 holders1. Directors & Founders

23%

2. Schroders 12%

3. AR Kayed 9%

4. Swissfirst Bank 8%

5. Al Mashreq Inv 6%

Management

UK institutions

Previous management

6. Och Ziff 5%

7. George Robinson 4%

8. Hugh Sloane 4%

US investors

Retail shareholders

9. Matterhorn 4%

10. Artemis 3%

Total 78%

• 116,678,750 shares in issue

• Market cap of c. £233m

4

Gulfsands MissionGulfsands Mission• Vision – Gulfsands will become one of the pre-eminent E&P companies

in the Middle East, and will be viewed as a preferred operator and partnerpartner

• Strategy – Gulfsands will achieve these goals by maximising the value of existing assets, and by capturing new exploration and development opportunities in our core activity area that have the potential to add significant production revenues. To be pursued through organic growth and corporate acquisitions.

• Tactics - Develop existing discoveries and continue value-adding exploration in Block 26. Capture two high value exploration blocks in th ithi th t 18 th C t t l tthe core area within the next 18 months. Capture at least one new business development opportunity in Iraq within the next 12 months. Exploration and business development activities will be funded from production revenuesproduction revenues.

5

Gulfsands Petroleum 2008 HighlightsGulfsands Petroleum 2008 Highlights• Oil and Gas Discovery, Khurbet East in Syria Block 26

g gg g

― KHE-3 flows 3,420 barrels of oil/day average stabilised rate on drill-stem test― 3D seismic acquisition over Khurbet East Field completed, January 2008― Field commercial development agreed with Syria Government, 5 February 2008

KHE 4 d l t ll l t d i M h― KHE-4 development well completed in March― KHE-5H, the first horizontal well in the Field, flowed 2,014 bopd on equipment

restricted rate― KHE-6H, second horizontal well, spudded on 19 MayKHE 6H, second horizontal well, spudded on 19 May― “First Oil” from Khurbet East field expected by Q4 2008

• Corporate highlights• Corporate highlights― Appointment of Andrew Rose as CFO following departure of CEO John Dorrier

and CFO David DeCort― Investment of $19m by Och Ziff at (then) premium to share price, taking 5% y ( ) p p g

stake

6

Asset 1 – Block 26, SyriaAsset 1 Block 26, Syria• ~34% of Syria’s hydrocarbon production

comes from within the Block 26 boundaries (primarily previously existing SPC production)

Turkey

production)

• Gulfsands is operator of Block 26 Contract Syria

Block 26

• Original Contract awarded in 2003

― First Exploration Period Minimum Work Obligation (MWO) of Iraq

J d4 wells plus 2D Seismic Successfully completed in 2007

― Currently in the First Extension of the

Jordan

Saudi ArabiaCurrently in the First Extension of the Exploration Period MWO of 2 wells plus 3D seismic

expected to be completed during 2008

• A Development Area has been awarded over the Khurbet East Field25 year development period with additional102008

Current Period expires in 2010 Second Extension is available

• Block 26 Contract is a 50/50 JV with SNG

• 25 year development period with additional10 year Contractor option― 2P estimated ultimate recoverable oil reserves of

66 mmbbl and 3P EUR of 143 mmbbl

7

Overseas (subsidiary of Emerald Energy Plc)

Block 26 Contract - Oil Revenue DistributionBlock 26 Contract Oil Revenue Distribution

Based on US$105/barrel realised oil price and gross daily production ≤25,000 bbls/day

Government Royalty

G t P fit Oil

Government Revenue/barrel

Government Royalty

Contractor Profit Oil Share

Government Profit Oil Share Government

Revenue/barrel Government Profit Oil Share

Contractor Cost Recovery Share

Contractor Net Revenue/barrel

Contractor Net Revenue/barrel

Contractor Profit Oil Share

• The Block 26 Contractor Group (Gulfsands 50% and Emerald 50%) is entitled to recovery of all SPC approved exploration, development and operating costs p g

• Exploration and operating costs are fully recoverable within a calendar year • Development capital cost recovery is capped at 25% per year (i.e. 100% of capital costs recovered after 4 years)

• For example, based on a US$105/barrel realised oil price, the Contractor Group will receive in ~US$62barrel of revenue per barrel of produced oil while costs are being recovered

8

• After costs have been recovered, Contractor Group revenue is ~$32 barrel of produced oil

Khurbet East Location4 134 7004 134 700

Turkey

Khurbet East Location

y

R um eilan

U lla y an

B a dra n

M aa sh o k

Le la c D e rik

K aratcho k

O u de h

K ah ta n iye h

S ha m ou

Z ura ba

O u de h

K ah ta n iye h

S ha m ou

Z ura ba

4 084 700

I

Block 26 Ba b A l H a did

K h urb e t

N

M a t lo ut

So ued ie hSo ued ie h

Area selected for relinquishment prior to entry into First Extension

KHE-2

Souedieh

I raqN a our

A l B ardeh

Te l B ara k

Al B o ua b

A b u H ayd a r

Al B o ua b

A b u H ayd a r

Block 26KHE-3

KHE-1

4 034 700

Sh e ik h M a n sou r

A l H ol

Sh e ik S u le im a n Sh e ik h M a n sou r

A l H ol

Sh e ik S u le im a n

686 700 736 700636 700

S y r i a

0 30 km

Note; wells not shown in fields witha high density of drilling.

Khurbet East Field is located within 12 km of the Souedieh and Rumeilan Oil Fields, and the oil export

9

pipeline runs directly through the Field.

Khurbet East Oil Field horizonsKhurbet East Oil Field horizons

The large majority of the hydrocarbons produced in the area are from the “Massive”, with relatively smaller volumes from thesmaller volumes from the deeper Triassic reservoirs (Butmah and Kurrachine Dolomite).

Commercialisation of the Triassic reservoirs at Khurbet East will likely be aided by the presence of the “Massive” development infrastructure

10

Khurbet East Oil Field MapKhurbet East Oil Field Map

•Early Production Facility (EPF)KHE-6H

•Development of central portion of field KHE-6H

Horizontal Development Well

Horizontal Development WellRecently completed

•Full Field Development (FFD)

Development of northern

pCurrently drilling

•Development of northern and southern extensions

R i i ti t ti i•Reviewing options to optimise timing of development of underlying Triassic reservoirs

“Massive” Field outline and Faults, based on 3D seismic

10 km

11

Khurbet East Discovery and Appraisal

1920

KHE-2 (First Appraisal Well)

KHE-1 (Discovery Well)May 2007

KHE-3 (Second Appraisal Well)December 2007

1920

DST ~820 bopd (10m interval)

Top Massive No DST due to

mechanical restrictions

KHE 2 (First Appraisal Well)July 2007

DST ~3420 bopd(29m interval)

1920

(29m interval)

~1.2 km ~1.0 km

• KHE-1 discovery well 480 bopd of 35º API oil from Kurrachine Dolomite, followed up by two appraisal wells targeting the Massive Formation

• KHE-2 appraisal well flowed oil to surface from a limited (10m) test interval at 1085 bopd• KHE-3 establishes continuity of reservoir to the south and east of the discovery. Flowed 24º API oil to surface at ~3420 bopd• KHE-4 development well, not tested• KHE-5H first horizontal well flowed to surface at 2,014 bopd of 24º API oil on less than 10 psi drawdown• KHE 6H second horizontal well spudded awaiting results in late June 2008

12

• KHE-6H second horizontal well spudded – awaiting results in late June 2008

Khurbet East- Early Production FacilityKhurbet East Early Production Facility

10 000 bfpd capacit• ~10,000 bfpd capacity

• Oil trucked to nearbyOil trucked to nearby processing facility

• Civil work commenced in April 2008.

Facility construction expected to be complete in July/August 2008

• Initial production from 3 vertical wells (KHE-2, KHE-3, KHE-4) and 2 horizontal wells (KHE-5H and KHE-6H)

13

Khurbet East Development – The Future• Full Field Development with facility capacity

of 30,000-40,000 bfpd

• Further appraisal and development ofdeeper reservoirs

• Near-field exploration using recentlyacquired 3D seismic (primary candidate for2H 2008 exploration drilling)

14

Upside- Block 26 ExplorationUpside Block 26 Exploration• Approximately 240 km2 3D seismic acquired

in Naour West area, targeting leads identified on 2D seismic

Naour West Leads identified on 3D Seismic

identified on 2D seismic

― Seismic interpretation is ongong, with lead ranking in progressg p g

― Additional candidates for 2H 2008 exploration drilling

15

Khurbet East & Block 26 – Forward D illi /D l t PDrilling/Development Programme

Submit Khurbet East Report on Technical & Economic Factors

Formation of Block 26 Joint Operating Company*

Delivery of Khurbet East Reserves Study and Government agreement to Commercial Development

Drill KHE-3 appraisal well

Drill KHE-4 production well

Drill KHE-5H production wellD ill KHE 6H d ti ll

3D Seismic Acquisition and ProcessingExploration/appraisal /development drilling

Seismic interpretation, G&G studies

Drill KHE-6H production well

Procurement/Installation of Early Production Facilities at Khurbet East

Target First Oil from Khurbet East (Early Production Facility)

Q4 2007 Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009

(Early Production Facility)

Khurbet East Full Field Development (FEED)

* The Joint Operating Company will act for and on behalf of SPC and the Block 26 Joint

16

* The Joint Operating Company will act for and on behalf of SPC and the Block 26 Joint Venture to carry out and conduct Development operations in Block 26

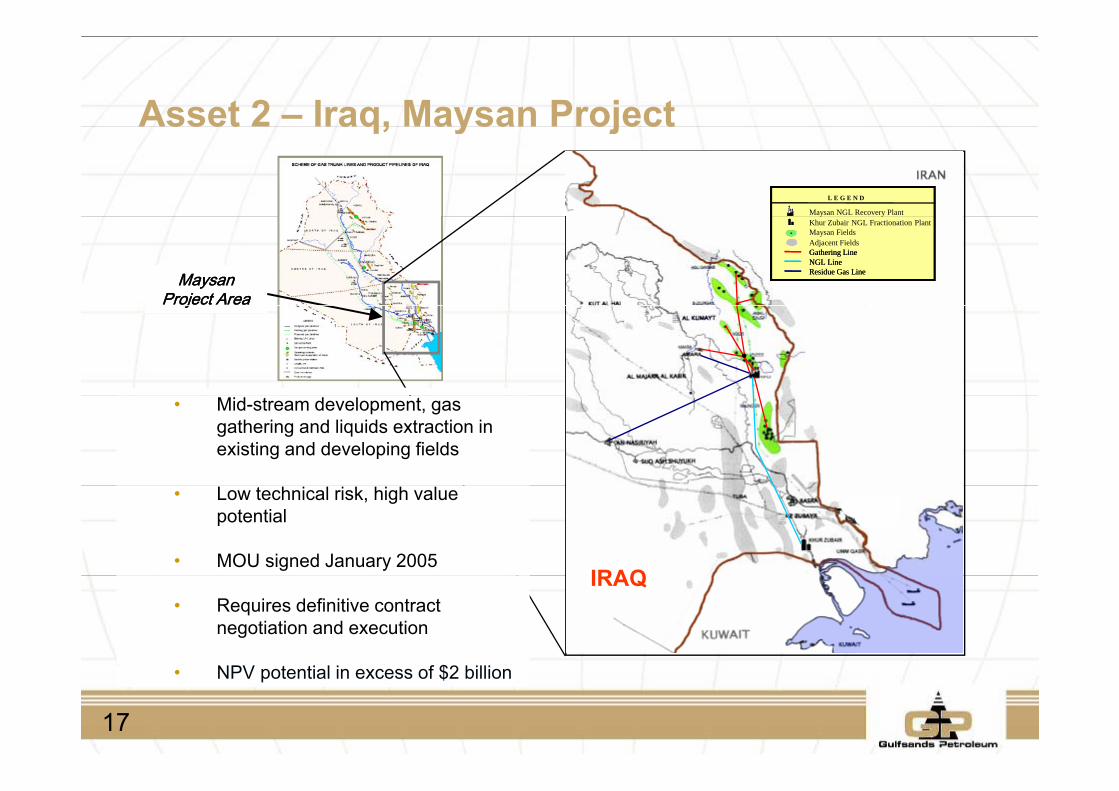

Asset 2 – Iraq, Maysan ProjectAsset 2 Iraq, Maysan Project

L E G E N D

Misan NGL Recovery Plant

L E G E N D

Maysan NGL Recovery Plant

Maysan Maysan Project AreaProject Area

yKhur Zubair NGL Fractionation PlantMisan FieldsAdjacent FieldsGathering LineNGL LineResidue Gas Line

y yKhur Zubair NGL Fractionation PlantMaysan FieldsAdjacent FieldsGathering LineGathering LineNGL LineNGL LineResidue Gas LineResidue Gas Line

jj

• Mid-stream development, gas gathering and liquids extraction in existing and developing fields

IRAQ

• Low technical risk, high value potential

• MOU signed January 2005IRAQ

• Requires definitive contract negotiation and execution

$

17

• NPV potential in excess of $2 billion

New Business Development - Maysan E l G P i (EGP) O t itiEarly Gas Processing (EGP) Opportunities

W. Qurnah DS6

• Estimated Quantities of Non-committed G C tl b i Fl dGas Currently being Flared:

– W. Qurnah DS6: 80 MMscfd– Majnoon: 40 MMscfd

• Project Target Fields: Buzurgan, Halfaya, Noor, Amara, Bin Omar, Majnoon, W. Q h– Nahr Bin Omar: 130 MMscfd

– Maysan: ≈100 MMscfd– TOTAL ≈ 350 MMscfd

Qurnah

• Total potential gas processed: 2.1 BCFGD

• Total potential NGL’s: 155,000 BPD

18

Asset 3 – Gulf of MexicoAsset 3 Gulf of Mexico• Currently producing unhedged net

2,800 boepd net to Gulfsandsp

• Focus on existing opportunities

• In-field and near-field wells, on high working interest properties (e.g. EI 57) and those with ( g )significant upside

• Selective work-overs and re-completions to enhance production and increase reserves

• 2P reserves of 6.8 MMBOE with PV10 of $226 million (01/01/2008 reserves report)

19

The next 12 monthsThe next 12 months• Commence Khurbet East development and production

• Further exploration of Block 26 in the Khurbet East area

• Acquire additional development project in Syria q p p j y

• Sign Maysan Project in Iraq

• Capture additional exploration blocks within focus area

20

Gulfsands Petroleum plc

Corporate PresentationCorporate Presentation

J 2008J 2008June 2008June 2008

This presentation is designed to provide information about Gulfsands Petroleum plc and its business and operations. It is intended as general information only and is not to be relied upon for any particular purpose. In particular, no information contained in this presentation constitutes, or shall be deemed to constitute, an invitation to invest or otherwise deal in any securities of Gulfsands Petroleum plc.

Although we endeavor to ensure that the content of this presentation is accurate and up-to-date, Gulfsands Petroleum plc gives no representation or warranty as to the accuracy or completeness of

any information contained in this presentation.any information contained in this presentation.

22

Syria: Block 26 Production Sharing Contracty g

• Exploration

― Current period – 3 years to August 2010 with a minimum commitment of 2 exploration wells and 250 km2 of 3D seismic

― Contractor option for additional 2 year period commencing August 2010, minimum commitment of 1 exploration well

• Production

― 25 year term and a 10 year extension (Contractor Option)

• RightsRights

― Access to surface facilities and pipelines at agreed tariff of $.75 per barrel

― Deep reservoirs in all areas of the block and shallow reservoirs in all areas except those from existing SPC discoveries

FISCAL TERMS

Government Royalty 12.5%

Contractor Cost Recovery Share 50% of post-Royalty revenue/oil

Contractor Profit Oil Share 35% after tax (for production ≤ 25000 bopd, sliding scale for higher rates)

Gulfsands (Operator) 50% Working Interest of Contractor Share

23

Other Productive Reservoirs - ‘Butmah’ R i A tReservoir - Assessment

0 1(frac) 1 0(frac) 0.5 0(frac) 0.01 1000(mD)

• Live oil/gas shows during drilling

C d ft d illi b k2850

G• Core recovered after drilling break

• Wireline logs and pressure samples indicate a hydrocarbon-bearing reservoir

Gas sample

Very good porosity and permeability interpreted in main pay zone

Gas sample recovered from near top of pay zone 2900Gas sample recovered from near top of pay zone

No definitive hydrocarbon-water contact identified

2900

24

Other Productive Reservoirs -‘Kurrachine Dolomite’ - Structure

The KHE-2 well did not drill to the Kurrachine Dolomite

KHE-1Area of structure at Kurrachine Dolomite reservoir ~15.5 km2

There is potential for oil pay in this reservoir

Cross-section based on seismic line KN-40

There is potential for oil pay in this reservoir in excess of the structural closure

This could be explained by

•Presence of 2 or more separate accumulations within the Kurrachine Dolomite, or

•A stratigraphic component to the trap, providing for additional hydrocarbon column

25

10 kmhydrocarbon column

Naour West Exploration 3DNaour West Exploration 3D

~240 km2 of high quality, explorationoriented 3D seismic data acquired overNaour West lead areaNaour West lead area

Several structural leads identified, withclosure at multiple levels

Base Cretaceous horizon, perspective view from southBase Cretaceous horizon, perspective view from south

26