Gila County County...GILA COUNTY MANAGEMENT'S DISCUSSION AND ANALYSIS 4 As management of Gila...

59

Report of Independent Auditors and Financial Statements with Supplemental Information for Gila County June 30, 2013

Transcript of Gila County County...GILA COUNTY MANAGEMENT'S DISCUSSION AND ANALYSIS 4 As management of Gila...

Report of Independent Auditors and FinancialStatements with Supplemental Information for

Gila County

June 30, 2013

CONTENTS PAGEREPORTOFINDEPENDENTAUDITORS 1–3MANAGEMENT’SDISCUSSIONANDANALYSIS 4–12GOVERNMENT‐WIDESTATEMENTSGOVERNMENTALFUNDS Statementofnetposition 13 Statementofactivities 14FUNDSTATEMENTS Balancesheet 15 Reconciliationofthebalancesheetofgovernmentfunds tothestatementofnetposition 16 Statementofrevenues,expenditures,andchangesinfund balances 17 Reconciliationofthestatementofrevenues,expenditures,and changesinfundbalancesofthegovernmentalfundstothe statementofactivities 18PROPRIETARYFUND Statementofnetposition 19 Statementofrevenues,expenses,andchangesinfundnetposition 20 Statementofcashflows 21FIDUCIARYFUNDS Statementoffiduciarynetposition 22 Statementofchangesinfiduciarynetposition 23Notestofinancialstatements 24–50OTHERREQUIREDSUPPLEMENTARYINFORMATION Scheduleofagentretirementplans’fundingprogress 51 Notestoscheduleofagentretirementplans’fundingprogress 52 Budgetarycomparisonschedule–generalfund 53‐54 Budgetarycomparisonschedule–publicworksfund 55 Notestobudgetarycomparisonschedules 56

1

REPORTOFINDEPENDENTAUDITORSTheAuditorGeneraloftheStateofArizonaTheBoardofSupervisorsofGilaCounty,ArizonaReportontheFinancialStatementsWehave audited the accompanying financial statements of the governmental activities, the business‐typeactivities,eachmajorfund,andtheaggregateremainingfundinformationofGilaCounty,Arizona(the “County”), as of and for the year ended June 30, 2013, and the related notes to the financialstatements,whichcollectivelycomprisetheCounty’sbasicfinancialstatementsaslistedinthetableofcontents.Management’sResponsibilityfortheFinancialStatementsManagement is responsible for the preparation and fair presentation of these financial statements inaccordancewithaccountingprinciplesgenerallyacceptedintheUnitedStatesofAmerica;thisincludesthe design, implementation, andmaintenance of internal control relevant to the preparation and fairpresentationoffinancialstatementsthatarefreefrommaterialmisstatement,whetherduetofraudorerror.Auditor’sResponsibilityOurresponsibilityistoexpressopinionsonthesefinancialstatementsbasedonouraudit.WeconductedourauditinaccordancewithauditingstandardsgenerallyacceptedintheUnitedStatesofAmericaandthestandardsapplicableto financialauditscontained inGovernmentAuditingStandards, issuedbytheComptrollerGeneraloftheUnitedStates.Thosestandardsrequirethatweplanandperformtheaudittoobtain reasonable assurance about whether the financial statements are free from materialmisstatement.

2

Anauditinvolvesperformingprocedurestoobtainauditevidenceabouttheamountsanddisclosuresinthe financial statements. The procedures selected depend on the auditor's judgment, including theassessmentof therisksofmaterialmisstatementof the financialstatements,whetherdue to fraudorerror. Inmakingthoseriskassessments, theauditorconsiders internalcontrolrelevant totheentity'spreparationand fairpresentationof the financial statements inorder todesignauditprocedures thatare appropriate in the circumstances, but not for the purpose of expressing an opinion on theeffectiveness of the entity's internal control. Accordingly, we express no such opinion. An audit alsoincludes evaluating the appropriateness of accounting policies used and the reasonableness ofsignificantaccountingestimatesmadebymanagement,aswellasevaluatingtheoverallpresentationofthefinancialstatements.Webelievethattheauditevidencewehaveobtainedissufficientandappropriatetoprovideabasisforourauditopinions.OpinionsIn our opinion, the financial statements referred to above present fairly, in allmaterial respects, therespectivefinancialpositionofthegovernmentalactivities,thebusiness‐typeactivities,eachmajorfund,and the aggregate remaining fund information of Gila County, Arizona, as of June 30, 2013, and therespective changes in financial position, and, where applicable, cash flows thereof for the year thenendedinaccordancewithaccountingprinciplesgenerallyacceptedintheUnitedStatesofAmerica.OtherMattersRequiredSupplementaryInformationAccountingprinciplesgenerallyacceptedintheUnitedStatesofAmericarequirethatthemanagement’sdiscussionandanalysisonpages4through12;thebudgetcomparisonschedulesandrelatednotesonpages53through55;andthescheduleofagentretirementplans’fundingprogressandrelatednotesonpages51‐52bepresentedtosupplementthebasicfinancialstatements.Suchinformation,althoughnotapartof thebasic financial statements, is requiredby theGovernmentalAccountingStandardsBoardwhoconsidersittobeanessentialpartoffinancialreportingforplacingthebasicfinancialstatementsinanappropriateoperational,economic,orhistoricalcontext.We have applied certain limited procedures to the management’s discussion and analysis and theschedule of agent retirement plans’ funding progress described in the preceding paragraph inaccordancewithauditingstandardsgenerallyacceptedintheUnitedStatesofAmerica,whichconsistedof inquiries of management about the methods of preparing the information and comparing theinformation for consistency with management’s responses to our inquiries, the basic financialstatements,andotherknowledgeweobtainedduringourauditofthebasicfinancialstatements.Wedonotexpressanopinionorprovideanyassuranceontheinformationbecausethelimitedproceduresdonotprovideuswithsufficientevidencetoexpressanopinionorprovideanyassurance.

3

Our audit was conducted for the purpose of forming opinions on the financial statements thatcollectively comprise the County's basic financial statements. The budgetary comparison schedulesdescribedabovearetheresponsibilityofmanagementandwerederivedfromandrelatedirectlytotheunderlyingaccountingandotherrecordsusedtopreparethebasicfinancialstatements.Thebudgetarycomparisonscheduleshavebeensubjectedtotheauditingproceduresappliedintheauditofthebasicfinancial statements and certain additional procedures, including comparing and reconciling suchinformationdirectlytotheunderlyingaccountingandotherrecordsusedtopreparethebasicfinancialstatements or to the basic financial statements themselves, and other additional procedures inaccordancewithauditingstandardsgenerallyacceptedintheUnitedStatesofAmerica.Inouropinion,thebudgetary comparison schedules are fairly stated, in allmaterial respects, in relation to thebasicfinancialstatementsasawhole.Compliance Over the Use of Highway User Revenue Fund and Other Dedicated State TransportationRevenueMoniesInconnectionwithouraudit,nothingcame toourattention thatcausedus tobelieve that theCountyfailed tousehighwayuser revenue fundmonies receivedby theCountypursuant toArizonaRevisedStatutesTitle28,Chapter18,Article2,andanyotherdedicatedstatetransportationrevenuesreceivedby the County solely for the authorized transportation purposes, insofar as they relate to accountingmatters. However, our audit was not directed primarily toward obtaining knowledge of suchnoncompliance.Accordingly,hadweperformedadditionalprocedures,othermattersmayhavecometoourattentionregardingtheCounty’snoncompliancewiththeuseofhighwayuserrevenuefundmoniesandotherdedicatedstatetransportationrevenues,insofarastheyrelatetoaccountingmatters.OtherReportingRequiredbyGovernmentAuditingStandardsInaccordancewithGovernmentAuditingStandards,wehavealsoissuedourreportdatedAugust5,2016on our consideration of the County’s internal control over financial reporting and on our tests of itscompliance with certain provisions of laws, regulations, contracts, and grant agreements and othermatters. The purpose of that report is to describe the scope of our testing of internal control overfinancial reporting and compliance and the results of that testing, and not to provide an opinion oninternal control over financial reporting or on compliance. That report is an integral part of an auditperformed in accordance with Government Auditing Standards in considering the County’s internalcontroloverfinancialreportingandcompliance.

Scottsdale,ArizonaAugust5,2016

GILACOUNTYMANAGEMENT'SDISCUSSIONANDANALYSIS

4

As management of Gila County, we offer readers of the County's financial statements this narrativeoverviewandanalysisof the financialactivitiesof theCounty for the fiscalyearended June30,2013.Weencouragereaderstoconsidertheinformationpresentedhereinconjunctionwiththefinancialstatements.FinancialHighlights TheassetsoftheCountyexceededitsliabilitiesatthecloseofthecurrentfiscalyearby$70,301,201(net

position). Of this amount, $26,615,619 (unrestricted net position) may be used to meet thegovernment's ongoing obligations to citizens and creditors, $17,583,086 is restricted for specificpurposes(restrictednetposition),and$26,102,496isthenetinvestmentincapitalassets.

Asof thecloseof thecurrent fiscalyear, theCounty'sgovernmental funds reportedcombinedendingfundbalances of $41,549,815, a decrease of $150,052 in comparisonwith theprior year's balance of$41,699,867.

Attheendofthecurrentfiscalyear,unassignedfundbalancefortheGeneralFundwas$24,606,762or61%oftotalGeneralFundexpenditures.

OverviewoftheFinancialStatementsThis discussion and analysis is intended to serve as an introduction to the County's basic financialstatements.TheCounty'sbasic financial statementscomprise threecomponents:1)government‐widefinancial statements, 2) fund financial statements, and 3) notes to the financial statements. Requiredsupplementaryinformationisincludedinadditiontothebasicfinancialstatements.Government‐wide financial statements are designed to provide readers with a broad overview of theCounty'sfinancesinamannersimilartoaprivatesectorbusiness.ThestatementofnetpositionpresentsinformationonalloftheCounty'sassetsandliabilities,withthedifferencebetweenthetworeportedasnetposition.Overtime,increasesordecreasesinnetpositionmayserveasausefulindicatorofwhetherthefinancialpositionoftheCountyisimprovingordeteriorating.The statement of activitiespresents information showinghownet position changedduring the fiscalyear. All changes in net position are reported as soon as the underlying event giving rise to the changeoccurs,regardlessofthetimingofrelatedcashflows(fullaccrualaccounting).Thus,revenuesandexpensesarereported in this statement for some items that will result in cash flows in future fiscal periods (e.g.,uncollected taxes and earned but unused vacation leave). The statement of activities distinguishesfunctionsoftheCountythatareprincipallysupportedbytaxesandintergovernmentalrevenuesfromotherfunctionsthatareintendedtorecoverallorpartoftheircoststhroughuserfeesandcharges.

GILACOUNTYMANAGEMENT'SDISCUSSIONANDANALYSIS

5

ThegovernmentalactivitiesoftheCountyincludegeneralgovernment;publicsafety;highwaysandstreets;health;welfare;sanitation;cultureandrecreation;andeducation.The government‐wide financial statements not only include the County itself (known as the primarygovernment),butalso the legallyseparateGilaCountyLibraryDistrictandStreetLightingDistrictswhichfunction for all practical purposes asdepartmentsof theCounty, and thereforehavebeen includedas anintegralpartoftheCounty.Thebusiness‐typeactivitiesaccountforlandfilloperations.Thegovernment‐widefinancialstatementscanbefoundonpages13through14ofthisreport.Fundfinancialstatementsaregroupingsofrelatedaccountsthatareusedtomaintaincontroloverresourcesthat have been segregated for specific activities or objectives. The County, like other state and localgovernments,uses fundaccountingtoensureanddemonstrate finance‐relatedlegalcompliance.Allof thefunds of the County can be divided into three categories: governmental funds, Proprietary Funds, andFiduciaryFunds.Governmental funds are used to account for essentially the same functions reported as governmentalactivities in the government‐wide financial statements. However, unlike the government‐wide financialstatements, the governmental funds statements focus on near‐term inflows and outflows of spendableresources as well as the balances of spendable resources available at the end of the fiscal year. SuchinformationmaybeusefulinevaluatingtheCounty'snear‐termfinancialposition.Becausethefocusofgovernmentalfundstatementsisnarrowerthanthegovernment‐widestatements,itisusefultocomparetheinformationpresentedforgovernmentalfundswithsimilarinformationpresentedforgovernmental activities in the government‐wide financial statements. By doing so, readers may betterunderstandthelong‐termimpactofthegovernment'sneartermfinancingdecisions.Boththegovernmentalfundsbalancesheetandthegovernmentalfundsstatementofrevenues,expenditures,andchangesinfundbalances include a reconciliation to facilitate this comparison between governmental funds andgovernmental activities. The County maintains numerous individual governmental funds. Information ispresentedseparatelyinthegovernmentalfundsbalancesheetandinthegovernmentalfundsstatementofrevenues,expenditures,andchangesinfundbalancesfortwofundsthatareconsideredtobemajorfunds,GeneralandPublicWorks.Data fromtheothergovernmental funds iscombined intoasingle,aggregatedpresentation.Thebasicgovernmentalfundfinancialstatementscanbefoundonpages15through18ofthisreport.Proprietary Funds are used to report the same functions presented as business‐type activities in thegovernment‐widefinancialstatements.TheCountyusesanenterprisefundtoaccountforlandfilloperations.TheProprietaryFundfinancialstatementscanbefoundonpages19through21ofthisreport.

GILACOUNTYMANAGEMENT'SDISCUSSIONANDANALYSIS

6

FiduciaryFundsareusedtoaccountforresourcesheldbytheCountyforthebenefitofpartiesoutsidethegovernment. Fiduciary Funds are not reflected in the government‐wide financial statements because theresourcesofthosefundsarenotavailabletosupporttheCounty'sownoperations.TheaccountingusedforFiduciaryFundsismuchlikethatusedforProprietaryFunds.ThebasicFiduciaryFundsfinancialstatementscanbefoundonpages22and23ofthisreport.Notestothefinancialstatementsprovideadditionalinformationthatisessentialtoafullunderstandingofthe data provided in the government‐wide and fund financial statements. The notes to the financialstatementscanbefoundonpages24through50ofthisreport.Requiredsupplementary informationpresentsbudgetarycomparisonschedulesforthegeneralandmajorspecial revenue funds.This section also includes certain information concerning theCounty's progress infundingitsobligationtoprovidepensionbenefitstoitsemployees.Requiredsupplementaryinformationcanbefoundonpages51through56ofthisreport.Government‐wideFinancialAnalysisStatementofnetposition–Asnotedearlier,netpositionmayserveover timeasauseful indicatorofagovernment's financial position. At the close of the fiscal year, the County's assets exceeded liabilities by$70,301,201.

CondensedStatementofNetPosition(inthousands)

June30,2013and2012

GovernmentalActivities Business‐TypeActivities Total2013 2012 2013 2012 2013 2012

Currentandotherassets 46,070$ 47,280$ 7,031$ 6,419$ 53,101$ 53,699$Capitalassets 29,634 28,602 3,623 3,784 33,257 32,386

Totalassets 75,704 75,882 10,654 10,203 86,358 86,085

Currentliabilities 5,470 4,214 81 46 5,551 4,260Long‐termliabilities 7,151 8,855 3,355 2,702 10,506 11,557

Totalliabilities 12,621 13,069 3,436 2,748 16,057 15,817

NetpositionNetinvestmentincapitalassets 22,483 22,004 3,619 3,752 26,102 25,756Restricted 16,196 18,232 1,387 2,096 17,583 20,328Unrestricted 24,404 22,577 2,212 1,607 26,616 24,184

Totalnetposition 63,083$ 62,813$ 7,218$ 7,455$ 70,301$ 70,268$

GILACOUNTYMANAGEMENT'SDISCUSSIONANDANALYSIS

7

ThelargestportionofGilaCounty'snetpositionisunrestricted.Unrestrictednetpositionof$26,615,619or38%maybeused tomeetGilaCounty'songoingobligations to citizensand creditors.Thesecond largestportionis$26,102,496or37%ofthetotalnetpositionthatreflectsitsinvestmentincapitalassets(e.g.land,buildings,equipment,vehicles,andinfrastructure);lessaccumulateddepreciationandanyrelateddebtusedtoacquirethoseassetsthatisstilloutstanding.TheCountyusescapitalassetstoprovideservicestocitizens;consequently,theseassetsarenotavailableforfuture spending. Although the County's investment in its capital assets is reported net of related debt, itshouldbenotedthattheresourcesneededtorepaythisdebtmustbeprovidedfromothersources,sincethecapitalassetsthemselvescannotbeusedtoliquidatetheseliabilities.Attheendofthecurrentfiscalyear,theCountyisabletoreportpositivebalancesinallthreecategoriesofnetpositionforthegovernmentasawhole.Thefollowingprovidesanexplanationofgovernmentalactivities,assetsthatchangedsignificantlyovertheprioryear:

Current andotherassets– thenetdecreaseof$1.2millionwasprimarilydue to the spendingofpledged revenue obligations proceeds of $1.3 million held by trustee at June 30, 2012, for theconstructionprojects.

Noncurrentassets–thenetincreaseof$1millionwasmainlyduetotheadditionsofcapitalassetsas

mentionedabove.The following provides an explanation of business‐type activities, long‐term liabilities that changedsignificantlyovertheprioryear:

• Long‐termliabilities–thenetincreaseof$653,000wasprimarilyduetoanincreaseinthelandfillclosureandpostclosurecarecostspayable.

Statementofactivities – Already notedwas the statement of activities purpose in presenting how thegovernment'snetpositionchangedduringthecurrentfiscalyear.Forthefiscalyear,netpositionincreasedby$33,853.Thefollowingtablepresentsthechangesinnetposition.

GILACOUNTYMANAGEMENT'SDISCUSSIONANDANALYSIS

8

ChangesinNetPosition(inthousands)

YearsEndedJune30,2013and2012

GovernmentalActivities Business‐TypeActivities Total2013 2012 2013 2012 2013 2012

RevenuesProgramRevenues

Chargesforservices 3,454$ 3,640$ 1,615$ 1,516$ 5,069$ 5,156$Grantsandcontributions 17,546 20,105 ‐ ‐ 17,546 20,105

GeneralRevenues Propertytaxes 22,122 23,166 ‐ ‐ 22,122 23,166Countysalestax 5,905 5,659 ‐ ‐ 5,905 5,659Shareofstatesalestax 4,456 4,689 ‐ ‐ 4,456 4,689Sharedrevenue,statevehiclelicensetax 2,228 1,622 ‐ ‐ 2,228 1,622Sharedrevenue,stateliquorlicensetax 17 ‐ ‐ ‐ 17 ‐Paymentsinlieuoftaxes 3,392 3,459 ‐ ‐ 3,392 3,459Grantsandcontributionsnotrestrictedtospecificprograms ‐ 50 ‐ ‐ ‐ 50

Investmentincome 101 213 ‐ 20 101 233Miscellaneous 1,207 590 ‐ ‐ 1,207 590

Totalrevenues 60,428 63,193 1,615 1,536 62,043 64,729

ExpensesGeneralgovernment 20,025 19,741 ‐ ‐ 20,025 19,741Publicsafety 15,785 16,528 ‐ ‐ 15,785 16,528Highwaysandstreets 7,648 10,014 ‐ ‐ 7,648 10,014Health 2,491 1,136 ‐ ‐ 2,491 1,136Welfare 8,256 10,742 ‐ ‐ 8,256 10,742Sanitation 43 98 1,851 976 1,894 1,074Cultureandrecreation 1,554 1,491 ‐ ‐ 1,554 1,491Education 4,041 4,249 ‐ ‐ 4,041 4,249Interestonlong‐termdebt 315 326 ‐ ‐ 315 326

Totalexpenses 60,158 64,325 1,851 976 62,009 65,301

Changeinnetpositionbeforetransfers 270 (1,132) (236) 560 34 (572)Transfers ‐ 114 ‐ (114) ‐ ‐

Changeinnetposition 270 (1,018) (236) 446 34 (572)

NETPOSITION,beginningoftheyear 62,813 63,831 7,455 7,009 70,268 70,840

NETPOSITION,endoftheyear 63,083$ 62,813$ 7,219$ 7,455$ 70,302$ 70,268$

Revenues – Governmental activities revenues totaled $60.4 million for fiscal year 2013 which was adecreaseofover4%fromtheprioryear.Grantsandcontributionsandpropertytaxesaccountedforthemostsignificantdecreasesinrevenue.Thedecreaseingrantsandcontributionswaslargelyduetoareductioningrantawards.Thedecreaseinpropertytaxeswasduetodecreasedpropertytaxassessedvaluationsandadecreaseinthecurrentyearlevy.Chargesforservices,Countysalestax,statesalestax,andpaymentsinlieuoftaxesremainedrelativelystableascomparedtotheprioryear,withsmallchangesineachlineitem.State vehicle license tax andmiscellaneous revenue increased significantly as compared to theprior yearlargelyduetotheresultsofarecoveringeconomy.

GILACOUNTYMANAGEMENT'SDISCUSSIONANDANALYSIS

9

Business‐typeactivities'revenuesdidnotchangesignificantlyovertheprioryear.Amajorityoftherevenuegeneratedbythebusiness‐typeactivitiesisdonethroughcontractswithotherpoliticalsubdivisionsforuseofthelandfill.Expenses–Governmentalactivitiesexpensestotaled$60.2millionforfiscalyear2013,whichrepresentsadecrease of 6.5% over the prior year's total expenses. Expenses remained relatively unchanged over theprioryearduetothelackofmeritincreasesorchangesinstaffinglevels.Business‐typeactivities'expensesincreasedlargelyduetotheexpenseofthelandfillclosureandpostclosurecare costs. In the prior year, the County reduced $61 thousand in expenses for landfill closure and postclosurecarecosts;however,inthecurrentyear,theliabilitywasincreasedby$710thousandduetosomechanges inestimatesrelated to theclosureandpostclosurecarecosts,accounting for the$710 thousandincreaseincurrentyearexpenses.Financial analysis of the government's funds – As noted earlier, the County uses fund accounting toensureanddemonstratefinance‐relatedlegalcompliance.Governmental funds –The focusof theCounty'sgovernmental funds is toprovide informationonnear‐term inflows, outflows, and balances of spendable resources. Such information is useful in assessing theCounty'sfinancingrequirements.Inparticular,unassignedfundbalancemayserveasausefulmeasureofagovernment'snetresourcesavailableforspendingattheendofthefiscalyear.Asof theendof thecurrent fiscalyear, theCounty'sgovernmental fundsreportedcombinedending fundbalancesof$41,549,815,adecreaseof$150,052incomparisonwiththeprioryear'sbalanceof$41,699,867.TheGeneralFundisthechiefoperatingfundoftheCounty.Attheendofthecurrentfiscalyear,fundbalanceof the General Fundwas $26,284,699, an increase of approximately 4% over the prior year's balance of$25,379,775.Theincreasewaslargelyduetoareductionincurrentyearexpenditures.ExpendituresoftheGeneral Funddecreased over the prior year inmost departmentsdue to the 2013budget reduction andreductions of various grant funding. The County reduced the 2013 budget in an effort to preserve fundbalanceasaresultofexpecteddeclinesinfundingandtoadjustfordeclinesexperiencedinpreviousyears.Overall, Public Works Fund current year revenues remained relatively unchanged from the prior year.However,PublicWorksFundcurrentyearexpendituresincreasedby$2.4million.Thisoverallincreasewasaresultofthetwolargeroadconstructionprojects,theRussellRoadTurnLanesandWallatthenewpublicworkscomplexinGlobe,andthePineCreekCanyonreconstructionroadprojectinPine.ProprietaryFund–TheLandfillFundreportedadecreaseinnetpositionof$236,261.Thedecreasewaslargelyduetoanincreaseinlandfillclosureandpostclosurecarecostsinfiscalyear2013.

GILACOUNTYMANAGEMENT'SDISCUSSIONANDANALYSIS

10

GeneralFundbudgetaryhighlights–TheGeneralFundhadbudgetedexpendituresbeforeotherfinancingsources and uses of $58,809,435. Overall, actual General Fund expenditures were under budget by$18,278,115.TheCountyhadbudgeted$10,333,919forreservesandcontingencies,noneofwhichwasspentduring the current fiscal year, accounting for 57 percent of expenditures under budget. The Educationdepartment(SchoolSuperintendent)hadbudgetedexpendituresof$433,541whileactualexpendituresof$1,831,715wereoverbudgetduetonotbudgetingforthegrantspassedthroughtosubrecipients(schooldistricts). Grants passed through to subrecipients were recognized as revenues and correspondingexpenditures.Thisalsoaccounted formuchof the favorablevariance in intergovernmental revenues.TheGeneralFundhadbudgetedrevenuesof$38,292,117.Revenuesexceededbudgetby$3,174,371.The significant Countydepartments andother budgeted line itemsoverbudget areBoardof Supervisors$30,327,GeneralAdministration$122,950,Fairgrounds$6,323,andSchoolSuperintendent$1,413,174.TheCountywillstrivetoimproveitsbudgetingproceduresandcontrolinthefuture.Significant line items thatwere less than budget represent: County Attorney $1,909,904, County Sheriff$940,631, Professional Services $474,000, Superior Court – General $445,466, Recorder $416,140, andProbation $629,930. These line itemswere significantly less than budget due to reserves for unforeseenexpenditures.TheCountywillstrivetoimproveitsbudgetingproceduresandcontrolinthefuture.CapitalAssetandDebtAdministrationCapital assets include land, construction in progress, buildings, machinery and equipment, andinfrastructureassets(roads,highways,bridges,etc.).TheCounty’stotalcapitalassetsincreasedbyanetof$872,051duringthecurrentfiscalyearincomparisonwiththeprioryear’sbalanceof$32,385,512.Thenetincreasewasaresultofacquisitionofmachineryandequipmentof$627,444andconstructionofbuildingsandinfrastructureof$2,977,427,andtheaccumulateddepreciationof$2,732,820ontheseassetsaddedinfiscalyear2013.The County's investment in capital assets for its governmental activities as of June30, 2013, amounts to$29,633,964(netofaccumulateddepreciation),anetincreaseof4%fromtheprioryear.The County's investment in capital assets for its business‐type activities as of June 30, 2013, amounts to$3,623,599(netofaccumulateddepreciation),anetdecreaseof4%fromtheprioryear.Majorcapitalassetactivityduringthefiscalyearincluded:GovernmentalActivities:

During the fiscal year 2013, the County transferred $1.2 million from construction in progress toinfrastructureforthecompletionofroadandbridgeconstructionprojects.

AsofJune30,2013,constructioninprogressamountedto$1.4million.ThemoresignificantoftheconstructionprojectsincludetheTontoCreekBridge,PineCreekCanyonRoadReconstructionProject,andtheRussellRoadReconstructionproject.

GILACOUNTYMANAGEMENT'SDISCUSSIONANDANALYSIS

11

Acquisitionof$627thousandinmachineryandequipment. Completionofconstructionprojectsof$90thousandinbuildingsand$766thousandin

infrastructure. Accumulateddepreciationof$2,572,427addedinfiscalyear2013.

ThefollowingtableprovidesabreakdownoftheCounty'scapitalassetsasofJune30,2013and2012.

CapitalAssetsatYear‐End(NetofAccumulatedDepreciation)

(inthousands)June30,2013and2012

GovernmentalActivities Business‐TypeActivities Total2013 2012 2013 2012 2013 2012

Land 1,237$ 1,237$ 3,000$ 3,000$ 4,237$ 4,237$Constructioninprogress 1,352 385 ‐ ‐ 1,352 385Buildings 12,533 12,956 ‐ ‐ 12,533 12,956Improvementsotherthanbuildings 740 786 ‐ ‐ 740 786Machineryandequipment 4,311 5,171 585 737 4,896 5,908Infrastructure 9,461 8,068 39 47 9,500 8,115

Totalcapitalassets,net 29,634$ 28,603$ 3,624$ 3,784$ 33,258$ 32,387$

AdditionalinformationontheCounty'scapitalassetscanbefoundinNote5onpages35through37ofthisreport.Long‐termdebt–TheCounty'stotallong‐termliabilitiesincreasedbyanetof$193,665duringthecurrentfiscalyearincomparisonwiththeprioryear'sbalanceof$11,557,328.Thenetincreasewasaresultofregularscheduledprincipalandinterestpaymentsof$349,837,anetdecreaseof$165,691ofcompensatedabsencespayable,andanincreaseinlandfillclosureandpostclosurecarecostspayableof$709,193.Majorlong‐termdebtactivityduringthefiscalyearincluded:GovernmentalActivities:At the end of the current fiscal year, the County had total pledged revenue obligations outstanding of$6,895,000(excludingthepremiumonthebonds).Thisoutstandingbalanceconsistsofseries2009pledgedrevenuerefundingobligationsof$980,000torefundtheoutstanding1999seriescertificatesofparticipationandseries2009pledgedrevenueobligationsof$5,915,000tofinanceconstructioncostsforseveralcountybuildings.TheCountyhadlong‐termcapitalleasesof$70,750formachineryandcomputerequipment.Business‐typelongtermliabilitiesconsistofthelandfillclosureandpost‐closurecarecostsof$3,355,350andanequipmentleaseintheamountof$4,170.

GILACOUNTYMANAGEMENT'SDISCUSSIONANDANALYSIS

12

EconomicFactorsandNextYear'sBudgetsandRatesTheunemploymentrateforGilaCountyis9.8percentatJune2013whichishigherthanthepreviousyear'srateof8.2percent.Thiscomparestothestateunemploymentrateof8.3percent.Thereisalsoadecreaseinpropertyassessedvaluationswithnochangeintaxrateforthefiscalyear2013‐14.TheseeconomicfactorswereconsideredinpreparingtheCounty'sbudgetforthisfiscalyear2013‐14.RequestsforInformationThisfinancialreportisdesignedtoprovideagreateroverviewofGilaCounty'sfinancesforallthosewithaninterestinthegovernment'sfinances.Questionsconcerninganyoftheinformationprovidedinthisreportorrequestsforadditionalfinancialinformationshouldbeaddressedasfollows:

FinanceDirector

GilaCounty

1400Street

Globe,Arizona85501‐1483

13 Seeaccompanyingnotes.

GILACOUNTYSTATEMENTOFNETPOSITION

ASSETSJune30,2013

PrimaryGovernmentGovernmental Business‐TypeActivities Activities Total

Cashandinvestments 41,057,349$ 2,158,774$ 43,216,123$Receivables(netofallowancesforuncollectibles):

Propertytaxes 836,000 ‐ 836,000Accounts 281,383 129,331 410,714

Duefromothergovernments 3,423,633 ‐ 3,423,633Prepaiditem 172,546 ‐ 172,546Inventory 31,803 ‐ 31,803Restrictedcash ‐ 4,742,591 4,742,591Deferredcharges 267,743 ‐ 267,743Capitalassets,net

Nondepreciable 2,589,223 3,000,000 5,589,223Depreciable 27,044,741 623,599 27,668,340

Totalassets 75,704,421$ 10,654,295$ 86,358,716$

LIABILITIESANDNETPOSITION

Accountspayable 2,503,828$ 30,007$ 2,533,835$Accruedpayrollandemployeebenefits 1,749,071 23,616 1,772,687Compensatedabsences 1,217,713 22,863 1,240,576Noncurrentliabilities

Duewithinoneyear 310,000 4,170 314,170Dueinmorethanoneyear 6,840,897 3,355,350 10,196,247

Totalliabilities 12,621,509 3,436,006 16,057,515

NETPOSITIONNetinvestmentincapitalassets 22,483,067 3,619,429 26,102,496Restrictedfor:

Publicsafety 1,346,347 ‐ 1,346,347Highwaysandstreets 7,224,898 ‐ 7,224,898Health 240,176 ‐ 240,176Welfare 886,270 ‐ 886,270Sanitation 117,173 ‐ 117,173Education 1,966,446 ‐ 1,966,446Housing 97,769 ‐ 97,769Library 698,604 ‐ 698,604Judicialservices 2,898,099 ‐ 2,898,099Capitalprojects 223,043 ‐ 223,043Debtservice 326,366 ‐ 326,366Other 170,654 ‐ 170,654Landfillclosureandpostclosurecarecosts ‐ 1,387,241 1,387,241

Unrestricted 24,404,000 2,211,619 26,615,619

Totalnetposition 63,082,912$ 7,218,289$ 70,301,201$

Seeaccompanyingnotes. 14

GILACOUNTYSTATEMENTOFACTIVITIES

Functions/Programs ExpensesChargesforServices

OperatingGrantsand

Contributions

CapitalGrantsand

ContributionsGovernmentalActivities

Business‐TypeActivities Total

GovernmentalActivitiesGeneralgovernment 20,024,651$ 1,835,063$ 1,925,065$ ‐$ (16,264,523)$ ‐$ (16,264,523)$Publicsafety 15,785,047 660,726 3,022,027 3,217,028 (8,885,266) ‐ (8,885,266)Highwaysandstreets 7,648,649 584,890 186,590 ‐ (6,877,169) ‐ (6,877,169)Health 2,490,888 222,861 1,323,326 ‐ (944,701) ‐ (944,701)Welfare 8,256,214 90,666 4,165,686 ‐ (3,999,862) ‐ (3,999,862)Sanitation 42,974 ‐ ‐ ‐ (42,974) ‐ (42,974)Cultureandrecreation 1,554,579 ‐ ‐ ‐ (1,554,579) ‐ (1,554,579)Education 4,040,950 13,176 ‐ ‐ (4,027,774) ‐ (4,027,774)Interestandfiscalcharges 314,175 46,469 3,706,304 ‐ 3,438,598 ‐ 3,438,598Totalgovernmentalactivities 60,158,127 3,453,851 14,328,998 3,217,028 (39,158,250) ‐ (39,158,250)

Business–TypeActivities Landfill 1,851,326 1,615,065 ‐ ‐ ‐ (236,261) (236,261)Totalprimarygovernment 62,009,453$ 5,068,916$ 14,328,998$ 3,217,028$ (39,158,250)$ (236,261)$ (39,394,511)$

GeneralRevenuesTaxesPropertytaxes,leviedforgeneralpurposes 21,123,922$ ‐$ 21,123,922$Propertytaxes,leviedforstreetlightingdistricts 49,632 ‐ 49,632Propertytaxes,leviedforlibrarydistrict 948,904 ‐ 948,904Countygeneralandtransportationsalestax 5,904,939 ‐ 5,904,939Shareofstatesalestax 4,456,480 ‐ 4,456,480Sharedrevenue,statevehiclelicensetax 2,228,128 ‐ 2,228,128Sharedrevenue,stateliquorlicensetax 16,938 ‐ 16,938Paymentsinlieuoftaxes 3,391,781 ‐ 3,391,781Investmentincome 101,130 ‐ 101,130Miscellaneous 1,206,510 ‐ 1,206,510Totalgeneralrevenuesandtransfers 39,428,364 ‐ 39,428,364

Changeinnetposition 270,114 (236,261) 33,853

Netposition,July1,2012 62,812,798 7,454,550 70,267,348Netposition,June30,2013 63,082,912$ 7,218,289$ 70,301,201$

ProgramRevenuesPrimaryGovernment

Net(Expense)RevenueandChangesinNetPosition

GILACOUNTYBALANCESHEET

15 Seeaccompanyingnotes.

June30,2013Other Total

General PublicWorks Governmental GovernmentalFund Fund Funds Funds

ASSETSCashandinvestments 26,790,334$ 6,976,494$ 7,290,521$ 41,057,349$Receivables(netofallowancesforuncollectibles):

Accounts 80,396 ‐ 200,987 281,383Propertytaxes 836,000 ‐ ‐ 836,000

Duefrom: Otherfunds ‐ ‐ 64,506 64,506Othergovernments 1,355,681 736,779 1,331,173 3,423,633

Prepaiditem 172,526 ‐ 20 172,546Inventory ‐ 31,803 ‐ 31,803

Totalassets 29,234,937$ 7,745,076$ 8,887,207$ 45,867,220$

LIABILITIESANDFUNDBALANCESLiabilities

Accountspayable 1,310,411$ 581,994$ 611,423$ 2,503,828$Accruedpayrollandemployeebenefits 1,575,321 145,046 28,704 1,749,071Duetootherfunds 64,506 ‐ ‐ 64,506

Totalliabilities 2,950,238 727,040 640,127 4,317,405

FundBalancesNonspendable 172,526 31,803 20 204,349Restricted 1,505,411 6,986,233 8,571,859 17,063,503Unassigned 24,606,762 ‐ (324,799) 24,281,963

Totalfundbalances 26,284,699 7,018,036 8,247,080 41,549,815

Totalliabilitiesandfundbalances 29,234,937$ 7,745,076$ 8,887,207$ 45,867,220$

GILACOUNTYRECONCILIATIONOFTHEBALANCESHEETGOVERNMENTALFUNDS

TOTHESTATEMENTOFNETPOSITION

Seeaccompanyingnotes. 16

June30,2013

Totalfundbalanceforgovernmentalfunds 41,549,815$

Amountsreportedforgovernmentalactivitiesinthestatementofnetpositionaredifferentbecause:

Capitalassetsusedingovernmentalactivitiesarenotfinancialresourcesandtherefore,arenotreportedinthefunds. 29,633,964

Deferredchargesonissuanceoflong‐termliabilitiesarenotfinancialresourcesandthereforearenotreportedinthegovernmentalfunds. 267,743

Someliabilities,includingbondspayable,premiumonthebondsandcompensatedabsences,arenotdueandpayableinthecurrentperiodandtherefore,arenotreportedinthefunds. (8,368,610)

Netpositionofgovernmentalactivities 63,082,912$

GILACOUNTYSTATEMENTOFREVENUES,EXPENDITURES,ANDCHANGESINFUNDBALANCESGOVERNMENTALFUNDS

17 Seeaccompanyingnotes.

YearEndedJune30,2013Other Total

General PublicWorks Governmental GovernmentalFund Fund Funds Funds

REVENUESTaxes 24,812,225$ 3,005,463$ 1,040,969$ 28,858,657$Licensesandpermits 500,502 2,330 ‐ 502,832Intergovernmental 12,719,944 4,087,571 9,818,560 26,626,075Chargesforservices 1,919,497 283,825 241,644 2,444,966Finesandforfeitures 506,053 ‐ ‐ 506,053Donationsandcontributions ‐ ‐ 828,101 828,101Investmentincome 68,041 18,611 14,478 101,130Miscellaneous 940,226 27,843 675,527 1,643,596

Totalrevenue 41,466,488 7,425,643 12,619,279 61,511,410

EXPENDITURESCurrent:

Generalgovernment 17,741,885 ‐ 574,785 18,316,670Publicsafety 12,940,690 ‐ 2,339,833 15,280,523Highwayandstreets ‐ 6,444,122 180,162 6,624,284Health 1,128,169 ‐ 1,312,135 2,440,304Welfare 3,944,238 ‐ 4,272,933 8,217,171Cultureandrecreation 262,752 ‐ 1,235,594 1,498,346Education 1,831,715 ‐ 2,204,545 4,036,260Sanitation ‐ ‐ 4,269 4,269

Debtservice:Principalretirement 310,000 ‐ ‐ 310,000Interest 309,997 ‐ ‐ 309,997

Capitaloutlay 2,061,874 2,407,864 153,900 4,623,638

Totalexpenditures 40,531,320 8,851,986 12,278,156 61,661,462

Excessofrevenuesover(under)expenditures 935,168 (1,426,343) 341,123 (150,052) OTHERFINANCINGSOURCES(USES)

Transfersin 241,519 ‐ 271,763 513,282Transfersout (271,763) (241,519) ‐ (513,282)

Totalotherfinancingsources(uses) (30,244) (241,519) 271,763 ‐

Netchangeinfundbalances 904,924 (1,667,862) 612,886 (150,052)

FUNDBALANCES,beginningofyear 25,379,775 8,685,898 7,634,194 41,699,867

FUNDBALANCES,endofyear 26,284,699$ 7,018,036$ 8,247,080$ 41,549,815$

GILACOUNTYRECONCILIATIONOFTHESTATEMENTOFREVENUES,EXPENDITURES,ANDCHANGESINFUNDBALANCESOFTHEGOVERNMENTALFUNDS

TOTHESTATEMENTOFACTIVITIES

Seeaccompanyingnotes. 18

YearEndedJune30,2013Netchangeinfundbalances‐totalgovernmentalfunds (150,052)$

Amountsreportedforgovernmentalactivitiesinthestatementofactivitiesaredifferentbecause:

Governmentalfundsreportcapitaloutlaysasexpenditures.However,inthestatementofactivitiesthecostofthoseassetsisallocatedovertheestimatedusefullivesandreportedasdepreciationexpense.

Capitaloutlay 3,604,872Depreciationexpense (2,572,427)

1,032,445

Revenuesinthestatementofactivitiesthatdonotprovidecurrentfinancialresourcesarenotreportedasrevenuesinthefunds.Thisamountisthedifferenceintherevenuerecognizedinthestatementfromtheproceedsrecordedasrevenuesinthegovernmentalfunds. (1,083,169)

Issuanceoflong‐termdebtprovidescurrentfinancialresourcestogovernmentalfunds,butissuingdebtincreaseslong‐termliabilitiesinthestatementofnetposition.Repaymentofdebtprincipalisanexpenditureingovernmentalfunds,buttherepaymentreduceslong‐termliabilitiesinthestatementofnetposition.

Bondpremium 11,572Bondissuecosts (15,750)Principalrepaid 310,000

305,822Underthemodifiedaccrualbasisofaccountingusedinthegovernmentalfunds,expendituresarenotrecognizedfortransactionsthatarenotnormallypaidwithexpendableavailableresources.Inthestatementofactivities,however,whichispresentedontheaccrualbasisofaccounting,expensesandliabilitiesarereportedregardlessofwhenthefinancialresourcesareavailable.

Decreaseincompensatedabsences 165,068

Changeinnetpositionofgovernmentalactivities 270,114$

GILACOUNTYSTATEMENTOFNETPOSITIONPROPRIETARYFUNDS

19 Seeaccompanyingnotes.

ASSETSJune30,2013

Business‐TypeActivitiesLandfill

CURRENTASSETSCashandcashequivalents 2,158,774$Accountsreceivable,net 129,331

Totalcurrentassets 2,288,105

NONCURRENTASSETSRestrictedcashandcashequivalents 4,742,591Capitalassets

Nondepreciable 3,000,000Depreciable(net) 623,599

Totalnoncurrentassets 8,366,190

Totalassets 10,654,295$

LIABILITIESANDNETPOSITIONCURRENTLIABILITIES

Accountspayable 30,007$Accruedwagesandbenefits 23,616Compensatedabsences 22,863Capitalleasespayable 4,170

Totalcurrentliabilities 80,656

NONCURRENTLIABILITIESLandfillclosureandpostclosurecarecostspayable 3,355,350

Totalnoncurrentliabilities 3,355,350

Totalliabilities 3,436,006

NETPOSITIONNetinvestmentincapitalassets 3,619,429Restrictedforlandfillclosureandpostclosurecarecosts 1,387,241Unrestricted 2,211,619

Totalnetposition 7,218,289$

GILACOUNTYSTATEMENTOFREVENUES,EXPENSES,ANDCHANGES

INFUNDNETPOSITIONPROPRIETARYFUNDS

Seeaccompanyingnotes. 20

YearEndedJune30,2013Business‐TypeActivitiesLandfill

OPERATINGREVENUESChargesforservices 1,615,065$

OPERATINGEXPENSESPersonalservicesandemployeebenefits 516,872Professionalservices 75,449Supplies 119,291Utilities 15,440Repairsandmaintenance 101,131Other 862,749Depreciation 160,394

Totaloperatingexpenses 1,851,326

Changeinnetposition (236,261)

NETPOSITIONBeginningofyear 7,454,550

Endofyear 7,218,289$

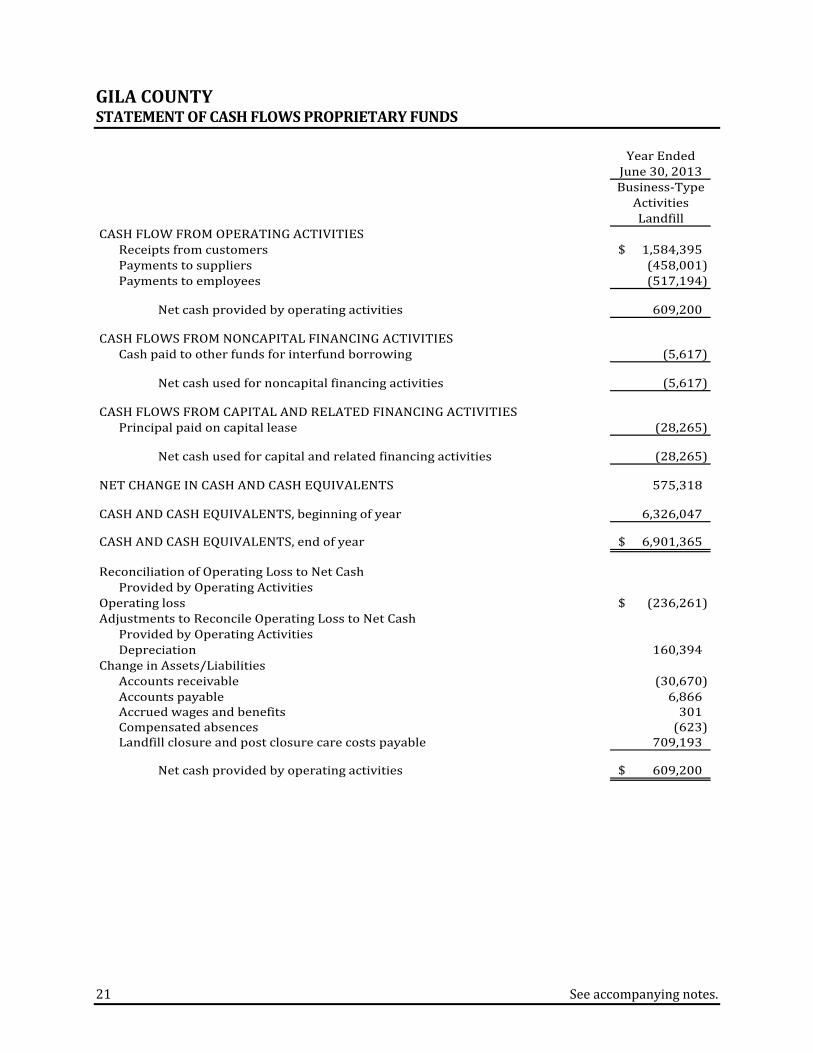

GILACOUNTYSTATEMENTOFCASHFLOWSPROPRIETARYFUNDS

21 Seeaccompanyingnotes.

YearEndedJune30,2013Business‐TypeActivitiesLandfill

CASHFLOWFROMOPERATINGACTIVITIESReceiptsfromcustomers 1,584,395$Paymentstosuppliers (458,001)Paymentstoemployees (517,194)

Netcashprovidedbyoperatingactivities 609,200

CASHFLOWSFROMNONCAPITALFINANCINGACTIVITIESCashpaidtootherfundsforinterfundborrowing (5,617)

Netcashusedfornoncapitalfinancingactivities (5,617)

CASHFLOWSFROMCAPITALANDRELATEDFINANCINGACTIVITIESPrincipalpaidoncapitallease (28,265)

Netcashusedforcapitalandrelatedfinancingactivities (28,265)

NETCHANGEINCASHANDCASHEQUIVALENTS 575,318

CASHANDCASHEQUIVALENTS,beginningofyear 6,326,047

CASHANDCASHEQUIVALENTS,endofyear 6,901,365$

ReconciliationofOperatingLosstoNetCashProvidedbyOperatingActivities

Operatingloss (236,261)$AdjustmentstoReconcileOperatingLosstoNetCash

ProvidedbyOperatingActivitiesDepreciation 160,394

ChangeinAssets/LiabilitiesAccountsreceivable (30,670)Accountspayable 6,866Accruedwagesandbenefits 301Compensatedabsences (623)Landfillclosureandpostclosurecarecostspayable 709,193

Netcashprovidedbyoperatingactivities 609,200$

GILACOUNTYSTATEMENTOFFIDUCIARYNETPOSITIONFIDUCIARYFUNDS

Seeaccompanyingnotes. 22

June30,2013Investment AgencyTrustFund Funds

ASSETSCashandcashequivalents ‐$ 643,818$Investments 35,373,260 ‐

Totalassets 35,373,260$ 643,818$

LIABILITIESDepositsheldforothers ‐$ 643,818$

Totalliabilities ‐ 643,818$

NETPOSITIONHeldintrustforinvestmenttrustparticipants 35,373,260$

GILACOUNTYSTATEMENTOFCHANGESINFIDUCIARYNETPOSITIONFIDUCIARYFUNDS

23 Seeaccompanyingnotes.

YearEndedJune30,2013InvestmentTrustFund

ADDITIONSContributionsfromparticipants 97,958,253$Investmentearnings 150,680

Totaladditions 98,108,933

DEDUCTIONSDistributionstoparticipants 99,506,252

Changeinnetposition (1,397,319)

NETPOSITION,July1,2012 36,770,579

NETPOSITION,June30,2013 35,373,260$

GILACOUNTYNOTESTOFINANCIALSTATEMENTS

24

Note1–SummaryofSignificantAccountingPoliciesThe accounting policies of Gila County conform to generally accepted accounting principles applicable togovernmentalunitsadoptedbytheGovernmentalAccountingStandardsBoard(GASB).A. ReportingEntityGilaCounty (the “County”) is ageneralpurpose localgovernment that isgovernedbya separatelyelectedboard of three county supervisors. The accompanying financial statements present the activities of theCounty(theprimarygovernment)anditscomponentunits.Component units are legally separate entities for which the County is considered to be financiallyaccountable. Blended component units, although legally separate entities, are so intertwinedwith theCounty that they are in substance part of the County's operations. Therefore, data from these units iscombinedwithdataoftheprimarygovernment.Discretelypresentedcomponentunits,ontheotherhand,arereportedinaseparatecolumninthegovernment‐widefinancialstatementstoemphasizetheyarelegallyseparatefromtheCounty.EachblendedcomponentunitdiscussedbelowhasaJune30year‐end.TheCountyhasnodiscretelypresentedcomponentunits.ThefollowingtabledescribestheCounty'scomponentunits:

ForSeparateReporting Financial

ComponentUnit Description;CriteriaforInclusion Method StatementsGilaCounty Providesandmaintainslibraryservicesforthe Blended NotavailableLibraryDistrict County'sresidents,theCounty'sBoardofSupervisors

servesastheboardofdirectorsandCountymanagementhasoperationalresponsibilitiesforthecomponentunit

GilaCountyStreet Operatesandmaintainsstreetlightinginareas Blended NotavailableLightingDistricts outsidelocalcityjurisdictions;theCounty'sBoard

ofSupervisorsservesastheboardofdirectorsandCountymanagementhasoperationalresponsibilitiesforthecomponentunit

RelatedOrganizationsTheEnvironmentalEconomicCommunityOrganizationandEasternArizonaCountiesOrganizationarelegallyseparate entities that were created to assist in the economic development of commercial and industrialenterprisesforGilaCounty.TheiroperationsarecompletelyseparatefromtheCountyandtheCountyisnotfinanciallyaccountablefortheseorganizations.Therefore,thefinancialactivitiesoftheseorganizationsarenotincludedintheaccompanyingfinancialstatements.

GILACOUNTYNOTESTOFINANCIALSTATEMENTS

25

Note1–SummaryofSignificantAccountingPolicies(continued)B. BasisofPresentationThebasicfinancialstatementsincludebothgovernment‐widestatementsandfundfinancialstatements.Thegovernment‐widestatements focuson theCountyasawhole,while the fund financialstatements focusonmajorfunds.Eachpresentationprovidesvaluableinformationthatcanbeanalyzedandcomparedbetweenyearsandbetweengovernmentstoenhancetheusefulnessoftheinformation.Government‐widestatements–provideinformationabouttheprimarygovernment(the“County”)anditscomponent units. The statements include a statement of net position and a statement of activities. Thesestatementsreportthefinancialactivitiesoftheoverallgovernment,exceptforfiduciaryactivities.Theyalsodistinguishbetweenthegovernmentalandbusiness‐typeactivitiesoftheCountyandbetweentheCountyanditsdiscretelypresentedcomponentunits.Governmentalactivitiesgenerallyare financedthroughtaxesandintergovernmental revenues. Business‐type activities are financed in whole or in part by fees charged toexternalparties.A statement of activities presents a comparison between direct expenses and program revenues for eachfunctionoftheCounty'sgovernmentalactivitiesandsegmentofitsbusiness‐typeactivities.Directexpensesarethosethatarespecificallyassociatedwithaprogramorfunctionand,therefore,areclearlyidentifiabletoaparticular function. The County does not allocate indirect expenses to programs or functions. Programrevenuesinclude: chargestocustomersorapplicantsforgoods,services,orprivilegesprovided, operatinggrantsandcontributions,and capitalgrantsandcontributions,includingspecialassessments.Revenues thatarenotclassifiedasprogramrevenues, including internallydedicatedresourcesandall taxesleviedorimposedbytheCountyarereportedasgeneralrevenues.Generally, the effect of interfund activity has been eliminated from the government‐wide financialstatementstominimizethedoublecountingofinternalactivities.However,chargesforinterfundservicesprovidedandusedarenoteliminatedifthepricesapproximatetheirexternalexchangevalues.Fund financial statements – provide information about the County's funds, including FiduciaryFundsandblendedcomponentunits.Separatestatementsarepresentedforthegovernmental,proprietary,andFiduciaryFundcategories.Theemphasisoffundfinancialstatementsisonmajorgovernmentalandenterprise funds, each displayed in a separate column. All remaining governmental and enterprisefundsareaggregatedandreportedasnonmajor funds.FiduciaryFundsareaggregatedandreportedbyfundtype.

GILACOUNTYNOTESTOFINANCIALSTATEMENTS

26

Note1–SummaryofSignificantAccountingPolicies(continued)ProprietaryFundrevenuesandexpensesareclassifiedaseitheroperatingornonoperating.Operatingrevenuesandexpensesgenerallyresultfromtransactionsassociatedwiththefund'sprincipalactivity.Accordingly,revenues,suchasusercharges,inwhicheachpartyreceivesandgivesupessentiallyequalvalues,areoperatingrevenues.Otherrevenues,suchassubsidies,resultfromtransactionsinwhichthepartiesdonotexchangeequalvaluesandareconsiderednonoperatingrevenuesalongwithinvestmentearningsandrevenuesgeneratedbyancillaryactivities.Operatingexpensesincludethecostofservices,administrativeexpenses,anddepreciationoncapitalassets.Otherexpenses, suchas interestexpense,areconsideredtobenonoperatingexpenses.TheCountyreportsthefollowingmajorgovernmentalfunds:TheGeneralFund is theCounty'sprimaryoperating fund. Itaccounts forall financial resourcesof thegeneralgovernment,exceptthoserequiredtobeaccountedforinanotherfund.ThePublicWorksFund,aspecialrevenuefund,accountsforroadconstructionandmaintenanceofmajorandnonmajorregionalroads,andisfundedbya1/2centCountysalestax,impactfees,andbyhighwayuserrevenue.TheCountyreportsthefollowingProprietaryFund:

TheLandfillFundaccountsfortheactivitiesoftheCounty'slandfilloperations.Additionally,theCountyreportsthefollowingfundtypes:

TheInvestmentTrustFundaccountsforpooledassetsheldandinvestedbytheCountyTreasureronbehalfoftheothergovernmentalentities.TheAgencyFundsaccountforassetsheldbytheCountyasanagentfortheStateandvariouslocalgovernments,andforpropertytaxescollectedanddistributedtothestateandlocalgovernments.

C. BasisofAccountingThegovernment‐wide,ProprietaryFund,andFiduciaryFundfinancialstatementsarepresentedusingtheeconomicresourcesmeasurementfocus,withtheexceptionofAgencyFunds,andtheaccrualbasisof accounting. The Agency Funds are custodial in nature and do not have a measurement focus.Revenues are recorded when earned and expenses are recorded at the time liabilities are incurred,regardlessofwhentherelatedcash flowstakeplace.Property taxesarerecognizedasrevenue in theyearforwhichtheyarelevied.Grantsanddonationsarerecognizedasrevenueassoonasalleligibilityrequirementstheproviderimposedhavebeenmet.

GILACOUNTYNOTESTOFINANCIALSTATEMENTS

27

Note1–SummaryofSignificantAccountingPolicies(continued)Underthetermsofgrantagreements,theCountyfundscertainprogramsbyacombinationofgrantsandgeneral revenues. Therefore, when program expenses are incurred, there are both restricted andunrestrictednetpositionavailabletofinancetheprogram.TheCountyappliesgrantresourcestosuchprogramsbeforeusinggeneralrevenues.Governmentalfundsinthefundfinancialstatementsarereportedusingthecurrentfinancialresourcesmeasurement focus and the modified accrual basis of accounting. Under this method, revenues arerecognized when measurable and available. The County considers all revenues reported in thegovernmental funds to be available if the revenues are collectedwithin 60 days after year‐end. TheCounty'smajorrevenuesourcesthataresusceptible toaccrualarepropertytaxes, intergovernmental,chargesforservices,andinvestmentincome.Expendituresarerecordedwhentherelatedfundliabilityis incurred, except for principal and interest on general long‐term debt, claims and judgments, andcompensatedabsences,whicharerecognizedasexpenditures to theextent theyaredueandpayable.General capital asset acquisitions are reported as expenditures in governmental funds. Issuances ofgenerallong‐termdebtandacquisitionsundercapitalleaseagreementsarereportedasotherfinancingsources.D. CashandInvestmentsForpurposesofitsstatementofcashflows,theCountyconsiderscashonhand,demanddeposits,cashon depositwith the CountyTreasurer, and only those highly liquid investmentswith amaturity of 3monthsorlesswhenpurchasedtobecashequivalents.Nonparticipating interest‐earning investment contracts are stated at cost.Moneymarket investmentsandparticipating interest‐earning investmentcontractswitha remainingmaturityof1yearor lessattimeofpurchasearestatedatamortizedcost.Allotherinvestmentsarestatedatfairvalue.E. PropertyTaxesCalendarTheCountyleviesrealandpersonalpropertytaxesonorbeforethethirdMondayinAugustthatbecomedueandpayableintwoequal installments.Thefirst installmentisdueonthefirstdayofOctoberandbecomesdelinquentafterthefirstbusinessdayofNovember.ThesecondinstallmentisdueonthefirstdayofMarchofthenextyearandbecomesdelinquentafterthefirstbusinessdayofMay.A lien assessed against real and personal property attaches on the first day of January precedingassessmentandlevy.

GILACOUNTYNOTESTOFINANCIALSTATEMENTS

28

Note1–SummaryofSignificantAccountingPolicies(continued)F. CapitalAssetsCapital assets are reported at actual cost or estimated historical cost if historical records are notavailable.AtJune30,2013,approximately30percentofthetotalgovernmentalactivitiescapitalassetsare statedatestimatedhistorical costbasedonprice levelsat timeofacquisition.Donatedassetsarereportedatestimatedfairvalueatthetimereceived.Capitalizationthresholds(thedollarvaluesabovewhichassetacquisitionsareaddedtothecapitalassetaccounts), depreciation methods, and estimated useful lives of capital assets reported in thegovernment‐widestatementsandProprietaryFundsareasfollows:

Capitalization Depreciation EstimatedThreshold Method UsefulLife

Land 5,000$ N/A N/ABuildings 5,000 Straight‐line 7‐30yearsImprovementsotherthanbuildings 5,000 Straight‐line 20yearsMachineryandequipment 5,000 Straight‐line 3‐25yearsInfrastructure 5,000 Straight‐line 7‐50years

G. NetPositionInthegovernment‐widefinancialstatements,netpositionarereportedinthreecategories;netpositioninvestedincapitalassets,netofrelateddebt;restrictednetposition;andunrestrictednetposition.Netpositioninvestedincapitalassets,netofrelateddebtisseparatelyreportedbecausetheCountyreportsall County assets which make up a significant portion of total net position. Restricted net positionaccountfortheportionofnetpositionrestrictedbypartiesoutsidetheCounty.Unrestrictednetpositionaretheremainingnetpositionnotincludedintheprevioustwocategories.H. FundBalanceClassificationsFund balances of the governmental funds are reported separately within classifications based on ahierarchyof theconstraintsplacedontheuseof thoseresources.Theclassificationsarebasedon therelative strength of the constraints that control how the specific amounts can be spent. Theclassificationsarenonspendable,restricted,andunrestricted,whichincludescommitted,assigned,andunassignedfundbalanceclassifications.Thenonspendablefundbalanceclassificationincludesamountsthatcannotbespentbecausetheyareeither not in spendable form such as inventories, or are legally or contractually required to bemaintainedintact.Restrictedfundbalancesarethosethathaveexternallyimposedrestrictionsontheirusagebycreditors,suchasthroughdebtcovenants,grantors,contributors,orlawsandregulations.

GILACOUNTYNOTESTOFINANCIALSTATEMENTS

29

Note1–SummaryofSignificantAccountingPolicies(continued)Theunrestrictedfundbalancecategoryiscomprisedofcommitted,assigned,andunassignedresources.Committedfundbalancesareself‐imposedlimitationsapprovedbytheCounty'sBoardofSupervisors,which is the highest level of decision‐making authoritywithin the County. The constraints placed oncommitted fund balances can only be removed or changed by the Board. Fund balances must becommittedpriortotheendofthefiscalyear.Assigned fund balances are resources constrained by the County's intent to be used for specificpurposes,butareneither restrictednor committed.TheBoardofSupervisorshasnotauthorizedanyoneparticularCountyemployeetomakeassignmentsofresourcesforaspecificpurpose.The unassigned fund balance is the residual classification for the General Fund and includes allspendableamountsnotreportedintheotherclassifications.Also,deficitsinfundbalancesoftheothergovernmentalfundsarereportedasunassigned.Whenanexpenditureisincurredthatcanbepaidfromeitherrestrictedorunrestrictedfundbalances,it's theCounty'spolicy touse restricted fundbalance first.For thedisbursementofunrestricted fundbalances, it is the County's policy to use committed amounts first, followed by assigned, and lastlyunassignedamounts.I. InvestmentIncomeInvestment income is composedof interest, dividends, andnet changes in the fair valueof applicableinvestments.J. CompensatedAbsencesCompensated absences consist of vacation leave and a calculated amount of sick leave earned byemployeesbasedonservicesalreadyrendered.Employeesmayaccumulateupto240hoursofvacationdependingonyearsofservice,butanyvacationhoursinexcessofthemaximumamountthatareunusedatyear‐endareforfeited.Uponterminationofemployment,allunusedandunforfeitedvacationbenefitsarepaidtoemployees.Accordingly,vacationbenefitsareaccruedasaliabilityinthegovernment‐wideandProprietaryFundfinancialstatements.Aliability is reported in the governmental funds' financial statements only if they have matured; forexample,asaresultofemployeeresignationsandretirementsbyfiscalyear‐end.

GILACOUNTYNOTESTOFINANCIALSTATEMENTS

30

Note1–SummaryofSignificantAccountingPolicies(continued)Employees may accumulate an unlimited number of sick leave hours. Generally, sick leave benefitsprovide for ordinary sick pay and are cumulative but are forfeited upon termination of employment.Becausesickleavebenefitsdonotvestwithemployees,aliabilityforsickleavebenefitsisnotaccruedinthe financial statements. However, upon retirement, employeeswhohave accumulated at least 1,000hours of sick leave receive a $3,000 bonus. The liability for the bonus related to the sick leave isrecorded in the government‐wide and Proprietary Fund financial statements. A liability for theseamounts is reported in the governmental funds' financial statements only if they have matured; forexample,asaresultofemployeeresignationsandretirementsbyfiscalyear‐end.Note2–IndividualFundDeficitsThefollowingSpecialRevenueFundshadfunddeficitsinexcessof$1,000asofJune30,2013:

Fund DeficitWIAStimulus (345,606)$CommunityHealthGrant (1,124)HealthStartProgram (7,874)Prop201SmokeFreeAZAct (12,851)HealthySteps (7,865)MarijuanaEradication (5,392)HomelandSecurity10Sheriff (27,672)SheriffBLESFProgram (110,885)CrimeVictimAssistanceProgram (11,483)AdultIntensiveProbationSupervision (20,282)StateAidEnhancement (34,731)HomelandSectyGrantGCSOFY13 (47,509)LibraryDistrictGrants (12,592)FacilitiesManagement (81,296)

These fund deficits resulted either from operations or a carryover deficit from prior years, but areexpectedtobecorrectedthroughnormaloperationsorthroughGeneralFundtransfersinfutureyears.

GILACOUNTYNOTESTOFINANCIALSTATEMENTS

31

Note3–DepositsandInvestmentsArizonaRevisedStatutes(A.R.S.)authorizetheCountytoinvestpublicmoniesintheStateTreasurer'sinvestmentpool;obligationsissuedorguaranteedbytheUnitedStatesoranyoftheseniordebtof itsagencies, sponsored agencies, corporations, sponsored corporations, or instrumentalities; specifiedstate and local government bonds and notes; interest‐earning investments such as savings accounts,certificatesofdeposit,andrepurchaseagreementsineligibledepositories;specifiedcommercialpaper,bonds,debentures,andnotesissuedbycorporationsorganizedanddoingbusinessintheUnitedStates;and certain open‐end and closed‐endmutual funds, including exchange traded funds. In addition, theCounty Treasurer may invest trust funds in certain fixed income securities of corporations doingbusinessintheUnitedStatesorDistrictofColumbia.Creditrisk–Statuteshavethefollowingrequirementsforcreditrisk:1. Commercial paper must be of prime quality and be rated within the top two ratings by a

nationallyrecognizedratingagency.2. Corporate bonds, debentures, and notes must be rated within the top three ratings by a

nationallyrecognizedratingagency.3. FixedincomesecuritiesmustcarryoneofthetwohighestratingsbyMoody'sinvestorsservice

and Standard andPoor's rating service. If only one of the above‐mentioned services rates thesecurity,itmustcarrythehighestratingofthatservice.

Custodialcreditrisk–Statutesrequirecollateral fordemanddepositsandcertificatesofdepositat101percentofalldepositsnotcoveredbyfederaldepositoryinsurance.TheCountywasnotsubjecttocustodialcreditrisk.Concentrationofcreditrisk–Statutesdonotincludeanyrequirementsforconcentrationofcreditrisk.Interest rate risk–Statutes require that publicmonies invested in securities and deposits have amaximummaturityof5years.Investmentsinrepurchaseagreementsmusthaveamaximummaturityof180days.Foreigncurrencyrisk–Statutesdonotallowforeigninvestments.Deposits–AtJune30,2013,thecarryingamountoftheCounty'sdepositswas$11,271,103.

GILACOUNTYNOTESTOFINANCIALSTATEMENTS

32

Note3–DepositsandInvestments(continued)Investments–TheCounty'sinvestmentsatJune30,2013,wereasfollows:

InvestmentType AmountU.S.AgencySecurities 52,939,409$CorporationObligations 18,252,967U.S.TreasuryNote 1,504,453

72,696,829$

Creditrisk–Creditriskistheriskthatanissuerorcounterpartytoaninvestmentwillnotfulfillitsobligations.TheCountydoesnothaveaformalpolicywithrespecttocreditrisk.AtJune30,2013,creditriskfortheCounty'sinvestmentswasasfollows:

InvestmentType Rating RatingAgency AmountU.S.AgencySecurities Aaa Moody's 52,939,409$CorporateObligations AA+ S&P 6,007,788CorporateObligations A+ S&P 3,001,590CorporateObligations A S&P 2,005,692CorporateObligations AA‐ S&P 1,261,217

AA S&P 2,993,300CorporateObligations A1 Moody's 2,983,380U.S.TreasuryNote Aaa Moody's 1,504,453

72,696,829$

CorporateObligations

Custodialcreditrisk–Foraninvestment,custodialcreditriskistheriskthat, intheeventofthecounterparty's failure, the County will not be able to recover the value of its investments orcollateral securities that are in the possession of an outside party. The County does not have aformalpolicywithrespecttocustodialcreditrisk.Concentrationofcreditrisk –Concentrationof credit risk is the riskof lossassociatedwith thesignificanceofinvestmentsinasingleissuer.TheCountydoesnothaveaformalpolicywithrespecttoconcentrationofcreditrisk.

GILACOUNTYNOTESTOFINANCIALSTATEMENTS

33

Note3–DepositsandInvestments(continued)Five percent or more of the County's investments at June 30, 2013, were in debt securities ofvariousU.S.agenciesasfollows:

PercentofCounty

U.S.Agency Amount InvestmentsFederalHomeLoanBankSystem 10,316,323$ 14.2%FederalFarmCreditBank 9,793,307 13.5%FederalNationalMortgageAssociation 16,302,700 22.4%FederalHomeLoanMortgageSystem 16,527,079 22.7%

52,939,409$

Interestraterisk–Interestrateriskistheriskthatchangesininterestrateswilladverselyaffectan investment's fair value.TheCountydoesnothavea formalpolicywith respect to interest raterisk.

InvestmentMaturitiesLessThanInvestmentType Amount 1Year 1‐5Years

U.S.AgencySecurities 52,939,409$ 8,961,691$ 43,977,718$CorporateObligations 18,252,967 8,015,802 10,237,165U.S.TreasuryNote 1,504,453 1,504,453 ‐

72,696,829$ 18,481,946$ 54,214,883$

A reconciliation of cash, deposits, and investments to amounts shown on the statement of netpositionandstatementoffiduciarynetpositionfollows:Cash,Deposits,andInvestments

Cashonhand 7,860$Amountofdeposits 11,271,103Amountofinvestments 72,696,829

83,975,792$

GILACOUNTYNOTESTOFINANCIALSTATEMENTS

34

Note3–DepositsandInvestments(continued)

StatementofFiduciaryNetStatementofNetPosition Position

Governmental Business‐Type Investment AgencyActivities Activities TrustFund Funds Total

Cashandinvestments 41,057,349$ 2,158,774$ 35,373,260$ 643,818$ 79,233,201$Restrictedcash ‐ 4,742,591 ‐ ‐ 4,742,591

41,057,349$ 6,901,365$ 35,373,260$ 643,818$ 83,975,792$

RestrictedcashrepresentsmoniessetasideaspartofthelandfilllineofcreditagreementdiscussedfurtherinNote6tothefinancialstatements.Note4–DuefromOtherGovernmentsAmounts due from other governments at June 30, 2013, in the statement of net position include$609,939inCountyexciseandtransportationtax,$309,907inHighwayUserRevenue,$152,142instate‐shared sales tax, $275,038 in auto lieu tax and license registration fees, $296,267 inWorkforceInvestmentActgrants,$270,291inStateofArizonareceivables,$254,961duefromtheTownofMiami,Arizona,$108,355inWomen,Infants,andChildren(WIC)grants,and$1,146,733inreimbursementsandchargesforservicesduefromvariousgovernmentagencies.

GILACOUNTYNOTESTOFINANCIALSTATEMENTS

35

Note5–CapitalAssetsCapitalassetactivityfortheyearendedJune30,2013,wasasfollows:

Beginning Decreases/ EndingBalance Increases Reclassifications Balance

GovernmentalActivitiesCapitalAssets,NetBeingDepreciated

Land 1,236,737$ ‐$ ‐$ 1,236,737$Constructioninprogress(estimatedcostto

complete$1,115,000) 384,670 2,120,860 (1,153,044) 1,352,486

Totalcapitalassets,netbeingdepreciated 1,621,407 2,120,860 (1,153,044) 2,589,223

CapitalAssets,BeingDepreciatedBuildings 26,859,855 90,409 ‐ 26,950,264Improvementsotherthanbuildings 1,067,752 ‐ ‐ 1,067,752Machineryandequipment 23,938,316 627,445 (196,083) 24,369,678Infrastructure 15,038,538 766,158 1,153,044 16,957,740

Totalcapitalassets,beingdepreciated 66,904,461 1,484,012 956,961 69,345,434

AccumulatedDepreciationforBuildings 13,904,255 513,162 ‐ 14,417,417Improvementsotherthanbuildings 281,845 45,991 ‐ 327,836Machineryandequipment 18,767,421 1,486,921 (196,083) 20,058,259Infrastructure 6,970,828 526,353 ‐ 7,497,181

Totalaccumulateddepreciation 39,924,349 2,572,427 (196,083) 42,300,693

Totalcapitalassets,beingdepreciated,net 26,980,112 (1,088,415) 1,153,044 27,044,741

Governmentalactivitiescapitalassets,net 28,601,519$ 1,032,445$ ‐$ 29,633,964$

GILACOUNTYNOTESTOFINANCIALSTATEMENTS

36

Note5–CapitalAssets(continued)Prior to2013, the county trackedexpenditures related to thedesign andengineering for a futureroadproject.In2013,itwasdeterminedthattheprojectwouldnotreachtheconstructionphase.

Beginning EndingBalance Increases Decreases Balance

Business‐TypeActivitiesCapitalAssets,NetBeingDepreciated

Land 3,000,000$ ‐$ ‐$ 3,000,000$

CapitalAssets,BeingDepreciatedMachineryandequipment 4,550,105 ‐ ‐ 4,550,105Infrastructure 169,340 ‐ ‐ 169,340

Totalcapitalassets,beingdepreciated 4,719,445 ‐ ‐ 4,719,445

AccumulatedDepreciationforMachineryandequipment 3,813,351 151,927 ‐ 3,965,278Infrastructure 122,101 8,467 ‐ 130,568

Totalaccumulateddepreciation 3,935,452 160,394 ‐ 4,095,846

Totalcapitalassets,beingdepreciated,net 783,993 (160,394) ‐ 623,599

Business‐typeactivitiescapitalassets,net 3,783,993$ (160,394)$ ‐$ 3,623,599$

Depreciationexpensewaschargedtofunctionsasfollows:GovernmentalActivities

Generalgovernment 870,522$Publicsafety 504,421Highwaysandstreets 1,008,229Health 50,584Welfare 39,043Sanitation 38,705Cultureandrecreation 56,233Education 4,690

2,572,427$

Business‐TypeActivitiesLandfill 160,394$

GILACOUNTYNOTESTOFINANCIALSTATEMENTS

37

Note5–CapitalAssets(continued)Construction commitments – The County has active construction projects as of June 30, 2013,with estimated costs to complete of $1,115,000 of which the more significant of these projectsincludes theTontoCreekBridge, PineCreekCanyonRoadReconstructionProject, and theRussellRoadReconstructionproject.Fundingwillbeprovidedfromtheprioryearbondissues.Note6–Long‐TermLiabilitiesThe followingscheduledetails theCounty's long‐term liabilityandobligationactivity for theyearendedJune30,2013:

DueBeginning Ending WithinBalance Increases Decreases Balance 1Year

GovernmentalActivitiesSeries2009pledgedrevenue

refundingobligations 1,025,000$ ‐$ (45,000)$ 980,000$ 45,000$Series2009pledgedrevenue

obligations 6,180,000 ‐ (265,000) 5,915,000 265,000Bondpremium 196,719 ‐ (11,572) 185,147 ‐Capitalleasespayable 70,750 ‐ ‐ 70,750 ‐Compensatedabsences

payable 1,382,781 1,756,425 (1,921,493) 1,217,713 1,200,000

GovernmentalActivitiesLong‐TermLiabilities 8,855,250$ 1,756,425$ (2,243,065)$ 8,368,610$ 1,510,000$

DueBeginning Ending WithinBalance Increases Decreases Balance 1Year

Business‐TypeActivitiesCapitalleasespayable 32,435$ ‐$ (28,265)$ 4,170$ 4,170$Landfillclosureand

postclosurecarecostspayable 2,646,157 709,193 ‐ 3,355,350 ‐

Compensatedabsencespayable 23,486 23,258 (23,881) 22,863 22,800

Business‐TypeActivitiesLong‐TermLiabilities 2,702,078$ 732,451$ (52,146)$ 3,382,383$ 26,970$

GILACOUNTYNOTESTOFINANCIALSTATEMENTS

38

Note6–Long‐TermLiabilities(continued)Series2009PledgedRevenueObligations–DuringtheyearendedJune30,2010,theCountyissued$8,000,000 in pledged revenue obligations with an interest rate of 3.0‐5.0 percent to financerenovation costs for a newly‐acquired county administration building and several other Countybuildings, and to advance refund the outstanding 1999 Series A certificates of participation. Theobligationsaregenerallynoncallable,withinterestpayablesemi‐annually.TheCounty'sobligationtomakepledgedrevenueobligationpaymentswillbepayablesolelyfrom,andsecuredby,apledgeandlienupontheCounty'sexcisetaxesthroughfiscalyear2029.Annualprincipalandinterestpaymentson the bonds are expected to require less than15%of pledged revenues. In the current year, totalprincipalandinterestpaid,andtotalpledgedresourceswere$620,000and$5,904,939,respectively.BondspayableatJune30,2013,wereasfollows:

Interest Original OutstandingDescription Rates Maturities Issue June30,2013

Series2009 3‐5% 7/1/2013‐2030 8,000,000$ 6,895,000$

The following schedule details debt service requirements to maturity for the County's pledgedrevenueobligationbondsatJune30,2013:YearEndingJune30 Principal Interest

2014 310,000$ 300,700$2015 335,000 291,1002016 340,000 281,3502017 350,000 267,7502018‐2022 1,980,000 1,116,5502023‐2027 2,430,000 658,8002028‐2029 1,150,000 87,000

Total 6,895,000$ 3,003,250$

Inprioryears,theCountydefeasedcertaincertificatesofparticipationbyplacingtheproceedsofnewbonds inan irrevocable trust toprovide forall futuredebt servicepaymentson theold certificates.Accordingly,thetrustaccountassetsandtheliabilityforthesedefeasedbondsarenotincludedintheCounty's financial statements. At June 30, 2013, $315,000 of the 1999 Series A certificates ofparticipationremainsandwasconsidereddefeased.

GILACOUNTYNOTESTOFINANCIALSTATEMENTS

39

Note6–Long‐TermLiabilities(continued)The followingscheduledetailsdebtservicerequirements tomaturity for theCounty'scapital leasespayableatJune30,2013:

Governmental Business‐TypeYearEndingJune30 Activities Activities

2014 27,425$ 4,930$2015 27,425 ‐2016 14,761 ‐2017 9,381 ‐

Totalminimumleasepayments 78,992 4,930Lessamountrepresentinginterest 8,242 760

Presentvalueofnetminimumleasepayments 70,750$ 4,170$

Landfillclosureandpostclosurecarecosts – State and federal laws and regulations require theCounty toplacea final coveron its six landfill siteswhentheystopacceptingwasteand toperformcertainmaintenanceandmonitoringfunctionsatthesitesfor30yearsafterclosure.Althoughclosureandpostclosurecarecostswillnotbepaiduntilnearorafterthedatethatthelandfillsstopacceptingwaste, the County reports a portion of these closure and post closure care costs in each operatingperiod.ThesecostswillbepaidfromtheLandfillFund.Theamountrecognizedeachyearisbasedonlandfillcapacityusedattheendofeachfiscalyear.The$3,355,350reportedaslandfillclosureandpostclosurecareliabilityatJune30,2013,representsthecumulative amount reported to date based on the approximate use of 38 percent of the estimatedcapacityoftheBuckheadMesaLandfilland50percentoftheRussellGulchLandfill.TheCountywillrecognize the remaining estimated cost of closure and post closure care of $1,195,645 as theremainingestimatedcapacityisfilled.Theseamountsarebasedonwhatitwouldcosttoperformallclosureandpostclosurecareinfiscalyear2013.TheCountyhasclosedfourofitslandfillsasofJune30,1996,andexpectstoclosethetworemaininglandfillsin2020and2034.Theactualcostsmayalsobehigherduetoinflation,changesintechnology,orchangesinregulations.TheCountyisplanningforexpansionoftheselandfillstoextendtheirusefullives.

GILACOUNTYNOTESTOFINANCIALSTATEMENTS

40

Note6–Long‐TermLiabilities(continued)Inordertocomplywithstateandfederallawsandregulations,theCountyobtainedaletterofcreditonJuly9,2009,toensurethecostsoflandfillclosure,postclosure,andpossiblecorrectiveactioncanbemet.Aspart of the agreement for the lineof credit, theCounty established amandatory sinkingfundwithanescrowagent.Thesinkingfundbalancewillequaltheestimatedlandfillclosureandpostclosure care costs when the landfills are expected to close. The current balance is reported in thebusiness‐typeactivitiesstatementofnetpositionandtheProprietaryFundstatementofnetpositionasrestrictedcash.Forfiscalyear2013,theCounty'sannualpaymentstocomplywiththisagreementwasapproximately$250,000.TheCountyenteredthisagreementasanalternativetocomplyingwiththelocalgovernmentfinancialtestrequirements.Insuranceclaims–TheCountyprovideslife,health,anddisabilitybenefitstoitsemployeesandtheirdependentsthroughtheArizonaLocalGovernmentEmployeeBenefitTrustcurrentlycomposedofsixmember counties. The Trust provides the benefits through a self‐funding agreement with itsparticipantsandadministerstheprogramandtheCountyisresponsibleforpayingthepremiumandrequires its employees to contribute a portionof that premium. If itwithdraws from theTrust, theCounty is responsible foranyclaimsrun‐outcosts, includingclaimsreportedbutnotsettled,claimsincurredbutnotreported,andadministrativecosts.IftheTrustweretoterminate,theCountywouldberesponsibleforitsproportionalshareofanyTrustdeficit.Compensatedabsences–During the year ended June 30, 2013, the County paid for compensatedabsences as follows: 55% from the General Fund, 10% from the PublicWorks Fund, 2% from theLandfillFund,and33%fromotherfunds.Compensatedabsencesarepaidfromvariousfunds inthesameproportionthatthosefundspaypayrollcosts.Specialusepermit–TheBuckheadMesaLandfillwas issueda specialusepermit from theUnitedStatesDepartmentofAgricultureForestService for thepurposeofusingandmaintainingasanitarylandfill,whichexpiresonDecember31,2019andhasannualfeesof$18,998.

GILACOUNTYNOTESTOFINANCIALSTATEMENTS

41

Note7–FundBalanceClassificationsoftheGovernmentalFundsThefundbalanceclassificationsofthegovernmentalfundsasofJune30,2013,wereasfollows:

Other TotalGeneral PublicWorks Governmental GovernmentalFund Fund Funds Funds

FundBalancesNonspendable

Prepaiditem 172,526$ ‐$ 20$ 172,546$Inventories ‐ 31,803 ‐ 31,803

Totalnonspendable 172,526 31,803 20 204,349

RestrictedforPublicsafety 831,859 ‐ 514,488 1,346,347Highwaysandstreets ‐ 6,986,233 19,193 7,005,426Health 198,868 ‐ 550,731 749,599Welfare ‐ ‐ 886,270 886,270Sanitation ‐ ‐ 117,173 117,173Education ‐ ‐ 1,966,446 1,966,446Housing ‐ ‐ 97,769 97,769Library ‐ ‐ 698,604 698,604Judicialservices 148,318 ‐ 2,749,781 2,898,099Capitalprojects ‐ ‐ 549,388 549,388Debtservice 326,366 ‐ ‐ 326,366Other ‐ ‐ 422,016 422,016

Totalrestricted 1,505,411 6,986,233 8,571,859 17,063,503

Unassigned 24,606,762 ‐ (324,799) 24,281,963

Totalfundbalance 26,284,699$ 7,018,036$ 8,247,080$ 41,549,815$

Note8–RiskManagementTheCountyisexposedtovariousrisksoflossrelatedtotorts;theftof,damageto,anddestructionofassets;errorsandomissions; injuries toemployees;andnaturaldisasters;butwasunable toobtaininsurance at a cost it considered to be economically justifiable. Therefore, theCounty joined and iscoveredby threepublic entity risk pools: theArizonaCounties Property andCasualtyPool and theArizona Counties Workers' Compensation Pool, which are described below, and the Arizona LocalGovernmentEmployeeBenefitTrust,whichisdescribedabove.

GILACOUNTYNOTESTOFINANCIALSTATEMENTS

42

Note8–RiskManagement(continued)TheArizonaCountiesPropertyandCasualtyPoolisapublicentityriskpoolcurrentlycomposedof11member counties. The pool provides member counties catastrophic loss coverage for risks of lossrelated to torts; theft of, damage to and destruction of assets; errors and omissions; and naturaldisasters;andprovidesriskmanagementservices.Suchcoverageincludesalldefensecostsaswellastheamountofanyjudgmentorsettlement.TheCountyisresponsibleforpayingapremium,basedonits exposure in relation to the exposure of the other participants, and a deductible of $25,000 peroccurrence for property claims and $25,000 per occurrence for liability claims. The County is alsoresponsibleforanypaymentsinexcessofthemaximumcoverageof$300millionperoccurrenceforproperty claims and $15million per occurrence for liability claims.However, lower limits apply tocertaincategoriesoflosses.Acountymustparticipateinthepoolatleastthreeyearsafterbecomingamember; however, itmaywithdraw after the initial three‐year period. If the poolwere to becomeinsolvent,theCountywouldbeassessedanadditionalcontribution.TheArizonaCountiesWorkers'CompensationPoolisapublicentityriskpoolcurrentlycomposedof11membercounties.Thepoolprovidesmembercountieswithworkers' compensation coverage, asrequired by law, and risk management services. The County is responsible for paying a premium,based on an experience rating formula, that allocates pool expenditures and liabilities among themembers.TheArizonaCountiesPropertyandCasualtyPooland theArizonaCountiesWorkers'CompensationPoolreceiveindependentauditsannuallyandanauditbytheArizonaDepartmentofInsuranceevery5 years. Both pools accrue liabilities for losses that have been incurred but not reported. Theseliabilitiesaredeterminedannuallybasedonanindependentactuarialvaluation.TheCountyhasnotexperiencedanysignificantdecreasesin insurancecoveragefromtheprioryearandhasnothadanysettlementsinexcessofcoverageinthepastthreeyears.Note9–PensionsandOtherPostemploymentBenefitsPlan descriptions – The County contributes to the four plans described below. The plans arecomponentunits of the State ofArizona andbenefits are establishedby state statute and theplansgenerallyprovideretirement, long‐termdisability,andhealthinsurancepremiumbenefits, includingdeath and survivor benefits. The retirement benefits are generally paid at a percentage, based onyears of service, of the retirees' average compensation. Long‐term disability benefits vary bycircumstance, but generally pay a percentage of the employee's monthly compensation. Healthinsurance premium benefits are generally paid as a fixed dollar amount per month towards theretiree'shealthcareinsurancepremiums,inamountsbasedonwhetherthebenefitisfortheretireeorfortheretireeandhisorherdependents.

GILACOUNTYNOTESTOFINANCIALSTATEMENTS

43

Note9–PensionsandOtherPostemploymentBenefits(continued)TheArizonaStateRetirementSystem–TheArizonaStateRetirementSystem(ASRS)administersacost‐sharing, multiple‐employer defined benefit pension plan; a cost‐sharing, multiple‐employerdefinedbenefithealthinsurancepremiumbenefitplan;andacost‐sharing,multiple‐employerdefinedbenefit long‐term disability plan that covers employees of the State of Arizona and employees ofparticipating political subdivisions and school districts. The ASRS is governed by the Arizona StateRetirementSystemBoardaccordingtotheprovisionsofA.R.S.Title38,Chapter5,Article2.ThePublicSafetyPersonnelRetirementSystem–The Public Safety Personnel Retirement System(PSPRS)administersanagentmultipleemployerdefinedbenefitpensionplanandanagentmultiple‐employerdefinedbenefithealthinsurancepremiumbenefitplanthatcoverspublicsafetypersonnelwho are regularly assigned hazardous duty as employees of the State of Arizona and participatingpolitical subdivisions. The PSPRS, acting as a common investment and administrative agent, isgoverned by a seven‐member board, known as The Board of Trustees, and the participating localboardsaccordingtotheprovisionsofA.R.S.Title38,Chapter5,Article4.The Corrections Officer Retirement Plan – The Corrections Officer Retirement Plan (CORP)administersanagentmultiple‐employerdefinedbenefitpensionplanandanagentmultiple‐employerdefinedbenefithealthinsurancepremiumbenefitplanthatcoversstate,county,andlocalcorrectionofficers; dispatchers; and probation, surveillance, and juvenile detention officers. The CORP isgoverned by The Board of Trustees of PSPRS and the participating local boards according to theprovisionsofA.R.S.Title38,Chapter5,Article6.TheElectedOfficialsRetirementPlan–TheElectedOfficialsRetirementPlan(EORP)administersacost‐sharing,multiple‐employer definedbenefit pensionplan and a cost‐sharing,multiple‐employerdefined benefit health insurance premium benefit that covers State of Arizona and county electedofficialsandjudges,andelectedofficialsofparticipatingcities.TheEORPisgovernedbyTheBoardofTrusteesofPSPRSaccording to theprovisionsofA.R.S.Title38, Chapter5,Article3. EORP’shealthinsurance premium benefit portion is not administered as its own formal trust. Therefore, inaccordance with GASB Statement No. 43, the County is required to disclose certain actuarialinformationrelatedtothehealthinsurancepremiumbenefitportionthatissimilartothatofanagentmultiple‐employerdefinedbenefitplan.However,theBoardofTrusteesobtainsanactuarialvaluationfor both EORP portions on their statutory basis as cost‐sharing plans, and therefore, actuarialinformationfortheCounty,asaparticipatinggovernmentemployer,isnotavailable.

GILACOUNTYNOTESTOFINANCIALSTATEMENTS

44

Note9–PensionsandOtherPostemploymentBenefits(continued)Each plan issues a publicly available financial report that includes its financial statements andrequired supplementary information.A report is availableon theirWebsiteormaybeobtainedbywritingorcallingtheapplicableplan.

ASRS

3300NorthCentralAvenue

P.O.Box33910Phoenix,AZ85067‐3910(602)240‐2000or1‐800‐621‐3778

PSPRS,CORP,andEORP3010EastCamelbackRoad,Suite200Phoenix,AZ85016‐4416(602)255‐5575