GIC HOUSING FINANCE LIMITED - :: IDBI Capitalidbicapital.com/pdf/GICHousing_DLOF.pdf · Draft...

169

Draft Letter of Offer (Private and Confidential) For equity shareholders of the Company only GIC HOUSING FINANCE LIMITED (Incorporated on 12 th December, 1989 under the Companies Act, 1956 as GIC Grih Vitta Limited and renamed to GIC Housing Finance Limited on 16 th November, 1993. A certificate for commencement of business was issued on 12 th January 1990.) Registered and Corporate Office: Universal Insurance Building, 3 rd Floor, Sir P.M. Road, Fort, Mumbai - 400 001. Tel: (022) - 2285 1765-7, (022) - 2285 3866/8 Fax: (022) - 2288 4985. E-mail: [email protected]; website: www.gichfindia.com Issue of 2,69,25,533 Equity Shares of Rs.10 each for cash at a premium of Rs. [•] per Equity Share aggregating to Rs. [•] lacs on rights basis to the existing Equity Shareholders of GIC Housing Finance Ltd. (the “Company”/GICHFL”) in the ratio of One Equity Share for Every One Equity Share (i.e. 1:1) held as on the record date i.e. [•], 2006. The face value of the Equity Shares is Rs. 10/- per share and the Issue Price is [•] times the face value PRICE BAND: Rs.37 TO Rs.42 PER EQUITY SHARE OF FACE VALUE OF RS. 10 GENERAL RISKS Investment in equity and equity related securities involve a degree of risk and investors should not invest any funds in this issue unless they can afford to take the risk of losing their investment. Investors are advised to read the risk factors carefully before taking an investment decision in this Issue. For taking an investment decision, investors must rely on their own examination of the Issuer and the Issue including the risks involved. The securities have not been recommended or approved by the Securities and Exchange Board of India (SEBI) nor does SEBI guarantee the accuracy or the adequacy of this document. The attention of investors is drawn to the statement of Risk Factors appearing on page nos. [•] to [•] of this Letter of Offer. ISSUER’S ABSOLUTE RESPONSIBILITY The Issuer, having made all reasonable inquiries, accepts responsibility for, and confirms that this Letter of Offer contains all information with regard to the Issuer and the Issue, which is material in context of the Issue, that the information contained in this Letter of Offer is true and correct in all material respects and is not misleading in any material respect, that the opinions and intentions, expressed herein are honestly held and that there are no other facts, the omission of which makes this document as a whole or any of such information or the expression of any such opinions or intentions misleading in any material respect. LISTING The Company's existing Equity Shares are listed on BSE (the designated stock exchange), NSE and CSE. The Company has passed resolution for delisting of its equity shares from CSE and MSE in its AGM on September 15, 2005 and made application for delisting to CSE & MSE. MSE vide their letter dated December 21, 2005 has granted delisting approval. Delisting approval from CSE is yet to be received by the Company. The Equity Shares to be issued through this Issue would be listed on BSE and NSE. The Company has received the in-principle approvals for listing from BSE and NSE vide their letters dated _________ and _________. LEAD MANAGER TO THE ISSUE REGISTRAR TO THE ISSUE IDBI CAPITAL MARKET SERVICES LIMITED 5 th Floor, Mafatlal Centre, Nariman Point, Mumbai-400021 Tel: (022) 56371212 / 15 Fax (022) 2288 5850 Website: www.idbicapital.com E-mail: [email protected] SHAREPRO SERVICES (INDIA) PVT. LIMITED Satam Estate, 3 rd Floor, Above Bank of Baroda, Cardinal Gracious Raod, Chakala, Andheri (East), Mumbai-400 099. Tel: (022) 2821 5168 / 2834 8218 / 2832 9828 Fax:(022) 2837 5646 Website: www.shareproservices.com E-mail: [email protected] ISSUE OPENS ON: [•] 2006 LAST DATE FOR RECEIVING REQUESTS FOR SPLIT FORMS [•] 2006 ISSUE CLOSES ON: [•] 2006

Transcript of GIC HOUSING FINANCE LIMITED - :: IDBI Capitalidbicapital.com/pdf/GICHousing_DLOF.pdf · Draft...

Draft Letter of Offer (Private and Confidential)

For equity shareholders of the Company only

GIC HOUSING FINANCE LIMITED

(Incorporated on 12th December, 1989 under the Companies Act, 1956 as GIC Grih Vitta Limited and renamed to GIC Housing Finance Limited on 16th November, 1993. A certificate for commencement of business was

issued on 12th January 1990.) Registered and Corporate Office: Universal Insurance Building,

3rd Floor, Sir P.M. Road, Fort, Mumbai - 400 001. Tel: (022) - 2285 1765-7, (022) - 2285 3866/8 Fax: (022) - 2288 4985.

E-mail: [email protected]; website: www.gichfindia.com Issue of 2,69,25,533 Equity Shares of Rs.10 each for cash at a premium of Rs. [•] per Equity Share aggregating to Rs. [•] lacs on rights basis to the existing Equity Shareholders of GIC Housing Finance Ltd. (the “Company”/GICHFL”) in the ratio of One Equity Share for Every One Equity Share (i.e. 1:1) held as on the record date i.e. [•], 2006. The face value of the Equity Shares is Rs. 10/- per share and the Issue Price is [•] times the face value

PRICE BAND: Rs.37 TO Rs.42 PER EQUITY SHARE OF FACE VALUE OF RS. 10

GENERAL RISKS Investment in equity and equity related securities involve a degree of risk and investors should not invest any funds in this issue unless they can afford to take the risk of losing their investment. Investors are advised to read the risk factors carefully before taking an investment decision in this Issue. For taking an investment decision, investors must rely on their own examination of the Issuer and the Issue including the risks involved. The securities have not been recommended or approved by the Securities and Exchange Board of India (SEBI) nor does SEBI guarantee the accuracy or the adequacy of this document. The attention of investors is drawn to the statement of Risk Factors appearing on page nos. [•] to [•] of this Letter of Offer.

ISSUER’S ABSOLUTE RESPONSIBILITY The Issuer, having made all reasonable inquiries, accepts responsibility for, and confirms that this Letter of Offer contains all information with regard to the Issuer and the Issue, which is material in context of the Issue, that the information contained in this Letter of Offer is true and correct in all material respects and is not misleading in any material respect, that the opinions and intentions, expressed herein are honestly held and that there are no other facts, the omission of which makes this document as a whole or any of such information or the expression of any such opinions or intentions misleading in any material respect.

LISTING The Company's existing Equity Shares are listed on BSE (the designated stock exchange), NSE and CSE. The Company has passed resolution for delisting of its equity shares from CSE and MSE in its AGM on September 15, 2005 and made application for delisting to CSE & MSE. MSE vide their letter dated December 21, 2005 has granted delisting approval. Delisting approval from CSE is yet to be received by the Company. The Equity Shares to be issued through this Issue would be listed on BSE and NSE. The Company has received the in-principle approvals for listing from BSE and NSE vide their letters dated _________ and _________.

LEAD MANAGER TO THE ISSUE REGISTRAR TO THE ISSUE

IDBI CAPITAL MARKET SERVICES LIMITED 5th Floor, Mafatlal Centre, Nariman Point, Mumbai-400021 Tel: (022) 56371212 / 15 Fax (022) 2288 5850 Website: www.idbicapital.com E-mail: [email protected]

SHAREPRO SERVICES (INDIA) PVT. LIMITED Satam Estate, 3rd Floor, Above Bank of Baroda, Cardinal Gracious Raod, Chakala, Andheri (East), Mumbai-400 099. Tel: (022) 2821 5168 / 2834 8218 / 2832 9828 Fax:(022) 2837 5646 Website: www.shareproservices.com E-mail: [email protected]

ISSUE OPENS ON: [•] 2006 LAST DATE FOR RECEIVING REQUESTS FOR SPLIT FORMS [•] 2006 ISSUE CLOSES ON: [•] 2006

TABLE OF CONTENTS

Section Description Page Nos. I DEFINITION & ABBREVIATIONS Conventional /General Terms Offer Related Terms Company / Industry Related Terms Abbreviations Forward Looking Statements

II RISK FACTORS III INTRODUCTION

Industry Overview Company Overview Selected Financial Information

IV GENERAL INFORMATION Company Board of Directors Issue Management Team

V CAPITAL STRUCTURE VI PARTICULARS TO THE ISSUE

Objects of the Issue Capital Adequacy Ratio Basic Terms of Issue Basis of Issue Price Statement of Tax Benefits

VII ABOUT THE ISSUER COMPANY Industry Overview Business Overview Details of Properties of the Company Debt Profile of the Company Key Industry Regulations

VIII HISTORY & CORPORATE STRUCTURE OF THE COMPANY IX MANAGEMENT

Board of Directors & related details Compliance with Corporate Governance Management Organisation Structure Key Management Personnel

X PROMOTERS / PRINCIPAL SHAREHOLDERS XI FINANCIAL STATEMENT

Financial information Financial information of Group Companies

Management Discussion & Analysis of Financial condition and Results of Operations as Reflected in Financial Statement

XII LEGAL & OTHER INFORMATION Outstanding litigations & Material Developments Government Approvals/ Licensing Arrangements

XIII OTHER REGULATORY & STATUTORY DISCLOSURES XIV TERMS OF ISSUE

Issue Procedure General Instructions

XV OTHER INFORMATION Material Contracts

Declaration

i

I. DEFINITIONS AND ABBREVIATIONS Conventional/ General Terms Act : The Companies Act, 1956 as amended

Equity Shares :

The Issued, Subscribed and Paid Up Equity Share Capital of the Company and the additional equity shares of the Company offered pursuant to the Rights Issue

Equity Shareholders : Means a holder/beneficial owner of equity shares of the GIC

Housing Finance Limited as on the Record Date i.e. [•]. Depository : A depository registered with SEBI under the SEBI (Depository and

Participant) Regulations, 1996, as amended from time to time. Guidelines / SEBI Guidelines / SEBI (DIP) Guidelines

: SEBI (Disclosure and Investor Protection) Guidelines, 2000 and subsequent amendments thereto

ISIN : International Securities Identification Number allotted by the

depository

Price Band : Being the price band of a minimum price of Rs.37 and the maximum price of Rs.42

Promoters :

General Insurance Company Limited, National Insurance Company Limited, The New India Assurance Company Limited, The Oriental Insurance Company Limited, United India Insurance Company Limited and IFCI Ltd.

Sole Lead Manager/IDBI Capital : IDBI Capital Market Services Limited Registrars / Registrars To The Issue/ Registrar And Share Transfer Agent / R&T Agents

: Sharepro Services (India) Pvt. Ltd.

Rights Issue/Issue : Present Issue of 2,69,25,533 Equity Shares of Rs. 10 each at a premium of Rs. [•] per share.

UIN : Unique Identification Number Offer Related Terms CAF : Composite Application Form Bankers to the Issue : IDBI Ltd. LOF / Letter of Offer : Letter of Offer of the Company for the Rights Issue of 2,69,25,533

Equity Shares of Rs. 10 each at a premium of Rs. [•] per share Record Date : [•], 2006 Company/ Industry Related Terms Articles or AOA : Articles of Association of the Company

Board : The Board of Directors of the Company or the Committee authorized to act on its behalf

Company/Issuer/GICHFL : GIC Housing Finance Limited Memorandum or MOA : Memorandum of Association Abbreviations Act : The Companies Act, 1956 and amendments thereto ACA : Associates of Chartered Accountants AY : Assessment Year ALM : Assets Liability Management AGM : Annual General Meeting

AS : Accounting Standard as issued by The Institute of Chartered Accountants of India

ii

BSE/Designated Stock Exchange : The Bombay Stock Exchange Ltd. CAF : Composite Application Form CAR : Capital Adequacy Ratio CBI : Central Bureau of Investigation CDSL Central Depository Services (India) Limited COD : Chief of Department CSE : The Calcutta Stock Exchange Association Limited DEMAT : Dematerialized (Electronic/Depository as the context may be) DP : Depository Participant DPG : Deferred Payment Guarantee DRT : Debt Recovery Tribunal EBIDTA : Earnings Before Interest Depreciation and Tax EGM : Extra-Ordinary General Meeting EMI : Equated Monthly Instalments EPS : Earnings Per Share

FEMA : Foreign Exchange Management Act 1999, and the subsequent amendments thereto

FERA : Foreign Exchange Regulation Act, 1973

FII :

Foreign Institutional Investor As Defined Under SEBI (Foreign Institutional Investors) Regulations, 1995 registered with SEBI and as defined under FEM (Transfer or Issue of Security by a Person Resident Outside India) Regulations, 2000 and under other applicable laws in India

FY : Financial Year FDR : Fixed Deposit Receipt GoI / Government : Government of India GIC : General Insurance Company Ltd. GIC AMC : GIC Assets Management Company Ltd. HDFC : Housing and Development Finance Corporation HFC : Housing Finance Company HUDCO : Housing and Urban Development Corporation HUF : Hindu Undivided Family ICWA : Institute of Cost and Work Accountants IFCI : IFCI Ltd. ICICI : Industrial Credit and Investment Corporation of India IVCS : IFCI Venture Capital Fund Ltd. IT : Income Tax Act, 1961 Lead Manager to the Issue IDBI Capital Market Services Ltd. LoF : Letter of Offer MIS Management Information System New India : The New India Assurance Company Limited NHB : National Housing Bank NI : Negotiable Instrument NICL : National Insurance Company Limited NPA : Non Performing Assets NR : Non Resident NRE ACCOUNT : Non Resident External Account NRI : Non Resident Indian NRO ACCOUNT : Non Resident Ordinary Account NSDL : National Securities Depository Limited NSE : National Stock Exchange of India Limited MSE : Madras Stock Exchange OICL : Oriental Insurance Company Ltd. OCB : Overseas Corporate Bodies

iii

PAT : Profit after Tax

PAN/GIR No. : Income Tax Permanent Account Number/General Index Reference Number

PBIDT : Profit before Interest, Depreciation and Tax QAC : Quality Assurance & Control RI : Resident Indian RBI : Reserve Bank of India SBI : State Bank of India SEBI : Securities and Exchange Board of India SEBI (SAST) Regulations, 1997 : SEBI (Substantial Acquisition of Shares and Takeovers)

Regulations, 1997 and subsequent amendments thereto Stock Exchanges : BSE and NSE referred to collectively SUUTI : Specified Undertaking Unit Trust of India USD : United States Dollars UTI : Unit Trust of India In this Letter of Offer, all references to “Rs.” or “INR” refer to Rupees, the lawful currency of India. References to the singular also refer to the plural and one gender also refers to any other gender wherever applicable.

iv

Forward-Looking Statements Statements included in this Letter of Offer which contain words or phrases such as “will”, “aim”, “will likely result”, “believe”, “expect”, “will continue”, “anticipate”, “estimate”, “intend”, “plan”, “contemplate”, “seek to”, “future”, “objective”, “goal”, “project”, “should”, “will pursue” and similar expressions or variations of such expressions, that are “forward-looking statements”. Actual results may differ materially from those suggested by the forward looking statements due to risks or uncertainties associated with the Company’s expectations with respect to, but not limited to, the Company’s ability to successfully implement its strategy, its growth and expansion, technological changes, its exposure to market risks, general economic and political conditions in India which have an impact on its business activities or investments, the monetary and interest policies of India, inflation, deflation, unanticipated turbulence in interest rates, foreign exchange rates, equity prices or other rates or prices, the performance of the financial markets in India and globally, changes in domestic and foreign laws, regulations and taxes and changes in competition in the industry. For further discussion of factors that could cause the Company’s actual results to differ, see the section entitled “Risk Factors” beginning on page no. [•] of this Letter of Offer. By their nature, certain market risk disclosures are only estimates and could be materially different from what actually occurs in the future. As a result, actual future gains or losses could materially differ from those that have been estimated. In accordance with SEBI requirements, the Company will ensure that investors are informed of material developments until such time as the grant of listing and trading permission by the Stock Exchanges for the equity shares being issued. Use of Market Data Unless stated otherwise, macroeconomic and industry data used throughout this Letter of Offer has been obtained from publications prepared by Government sources, industry sources and data generally available in the public domain. Such publications generally state that the information contained therein has been obtained from sources believed to be reliable but that their accuracy and completeness are not guaranteed and their reliability cannot be assured. Although we believe that industry data used in this Letter of Offer is reliable, it has not been independently verified.

v

II. RISK FACTORS An investment in Equity Shares involves a high degree of risk. The investor should carefully consider all of the information provided in this Letter of Offer, including the risks and uncertainties described below, before making an investment in the Company’s Equity Shares. If any of the following risks actually occur, Company’s business, results of operations and financial condition could suffer, the trading price of the Company’s Equity Shares could decline and the investors may lose all or part of their investment. Note: Unless specified or quantified in the relevant risk factors below, we are not in a position to quantify the financial or other implications of any risks mentioned herein under: (The Letter of Offer also includes statistical data regarding the Housing Finance Industry. This data has been obtained from industry publications, reports and other sources that the Company and the Lead Manager believe to be reliable. Neither the Company nor the Lead Manager has independently verified such data.) A. INTERNAL RISK FACTORS The Company is yet to receive the confirmation from IFCI Ltd., one of the Promoters for participating in the present Rights Issue

Management Perception: Except for the above, other Promoters have given their consent to participate in the Rights Issue. IFCI’s Board Meeting is being held on January 30, 2006 and the confirmation for participation in the present Rights Issue is one of the agenda items. The Company is involved in certain legal proceedings The Company is involved in certain legal proceedings claims in relation to certain civil criminal and taxation matter incidental to the business of the Company. These legal proceedings are pending at different levels of adjudication before various courts and tribunals. Further more a claim is determined against the Company and the Company is required to pay all or a portion of disputed amount, it could have a material adverse effect on our results and operations and the cash flows. Similarly delay in recovery of bad loans and lengthy legal procedures may affect the liquidity position of the Company. Please refer to page no. __ for further details. Following transactions in the Equity Shares of the Company has been taken place by the Promoters / Promoter Group during last 6 months:

Sr. No.

Name of the shareholder No. of shares bought

No. of shares sold

Date of transaction

Price (in Rs.)

Nil 5000 05.10.05 46.86 Nil 10000 06.10.05 46.84 Nil 10000 07.10.05 46.36 Nil 10000 11.10.05 44.93 Nil 5000 13.10.05 44.99 Nil 10000 16.01.06 51.87 Nil 5000 17.01.06 51.82 Nil 5000 17.01.06 51.82 Nil 10000 18.01.06 51.38 Nil 10000 19.01.06 51.44

1 Oriental Insurance Company Ltd

Nil 10000 20.01.06 54.31

vi

50000 Nil 14.12.05 49.68 31382 Nil 14.12.05 49.85 23436 Nil 14.12.05 49.85 16000 Nil 15.12.05 49.89 3350 Nil 16.12.05 49.82

2. General Insurance Corporation of India

5203 Nil 20.12.05 49.70 NHB vide their Direction No. NHB-HFC.DIR.11/CMD/2005 dated October 1, 2005 increased the risk weightage for the standard individual housing loan assets from 50% to 75% due to which, CAR as on 31st March 2006 would be below the minimum stipulated level of 12% unless fresh capital will be infused. If the CAR as on March 31, 2006 would fall below the minimum stipulated level, the company would be subject to certain penalties from NHB. Management Perception: Steps are being initiated to infuse addition capital through Rights Issue to fulfill the Capital Adequacy Requirements. The Promoters of the Company and Companies promoted by the Promoters are involved in certain legal proceedings The Promoters of the Company and the Companies promoted by the Promoters are involved in certain legal proceedings and the Company can give no assurance that the legal proceedings will be decided in favour of our Promoters and the Companies promoted by them. Please refer to page no. __ for further details. Company has not been able to get updated information on the litigations as well as operations of its Promoters and the Companies Promoted by them. Management Perception: Adequate steps have been taken to obtain the necessary information form Promoters and the companies promoted by them. M/s Khandelwal Jain & Co., Chartered Accountants in their inspection report dated June 4, 2005 made the following major findings;

i. In ALM Report the mismatch arises during the time bucket of 0-3 years and 3-5 year. The Company had not explained to us as to how they are going the bridge the gap. Further the Company also does not have any policy to bridge the mismatch.

ii. In Thane branch, few of the Loans accounts have not been classified as NPA and certain accounts are wrongly classified as NPA

iii. Delay has been observed in filing of NHB returns iv. The Company does not carry out Concurrent Audit in respect of the Housing Loans provided by the

Company.

Management Perception:

i. The Company proposes to bridge short-term gap through short-term borrowings. The ALM Policy being finalized.

ii. The Recovery module and system was malfunctioning for certain period of time due to which NPA classification was done manually, lead to the crisis. However the same has since been rectified. Generation of recovery report has since been computerized for all branches.

iii. The filing of certain returns was delayed. However in the year 2004-05 all the returns were filed on time. iv. There is no Concurrent Audit carried out by the Company, however internal audit are carried out by

independent Chartered Accountant firms on quarterly basis.

vii

The housing finance companies, including GICHFL face Market Risk because of lack of hard data and historical performance measures to assess the real risk. This is typical of developing markets like India. Management Perception: The setting up of Credit Information Bureau of India Ltd. (CIBIL) is a step in the direction of mitigating this risk. Housing companies, including GICHFL face credit risk on account of the inherent nature of the business. Management Perception: GICHFL has a strong credit control mechanism in place with clear policies and guidelines in respect of security of any loan proposal. The effective appraisal system is in place and followed uniformly. These measures minimizes the credit risk to a great extent. GICHFL faces Asset Liability Mismatch caused due to difference in maturity profile of assets and liabilities. Assets generated by HFCs have an average tenor of 10-15 years as against this; liabilities contracted are of a lesser tenor. Management Perception: The average tenor of the Assets generated by GICHFL is 13 years, whereas funds from banks are available for a maximum tenor of 7-8 years. This is a peculiar risk faced by Housing Finance companies. The borrowing of GICHFL are largely linked to benchmarks like the PLR of banks and institutions and hence our debts is mainly floating in nature, exposing us to interest rate risk. Management Perception: The interest rate risk of the Company is minimized due to the fact that in the past 2 years around 80% of the loans disbursed has floating rate of interest. NPAs (Net) of the Company account 5.84% of the total Loans as on September 30, 2005. Any further increase in the NPA levels may affect the liquidity position of the Company adversely. Management Perception: The Company has identified loans given to builders as one of the major reasons for NPAs. Accordingly, from the financial year 2000-01, the Company has stopped sanctioning loans under this category. Currently 98% of the loan portfolio of the Company is to individual housing loan category in which the Net NPAs have reduced to 4.58% as on December 31 2005 as compared to 5.90% in March 31 2005. The Company has a contingent liability not provided for on account of three tax disputes in appeal amounting to Rs. 31. 20 lacs as on March 31, 2005. To the extent of this contingent liability becomes actual liability, it will adversely affect our results of operations and financial condition. Management Perception: The Company has already paid the said dues to the Income Tax Department and there will not be any cash outflow from the Company on account of this contingent liability. The investments made by the Company during the period 1995-1997 in equity shares (unquoted), redeemable preference shares (unquoted) and non convertible bonds worth Rs. 13785 lacs have been reduced to Rs. 139 lacs as on September 30, 2005.

viii

Management Perception: The Company has been writing off the investments in the books over a period of time to reflect the diminution in the value of investments. Further, as a policy the company has not been making fresh investments since 2001, except in short term money market mutual funds. The Company's name reflects that General Insurance Corporation of India (GIC) is one of the major shareholders in the Company whereas the holding of GIC in the Company is only 8.03%. Management Perception: GIC Housing Finance Limited was promoted by GIC and the erstwhile subsidiaries of GIC namely, NICL, OICL, New India and United India. GIC alongwith its erstwhile subsidiaries, was holding 33% of the equity capital in GICHFL. Subsequently the Government of India delinked NICL, OILC, New India and United India from GIC thereby diluting GICs stake in GICHFL. As a result the equity stake held by GIC was split between these entities. Hence as on date GIC only holds 8.03% equity stake while its four erstwhile subsidiaries cumulatively hold 25.91% equity stake. B. EXTERNAL RISK FACTOTRS Risk of Competition The Company faces competition from Banks and Cooperative Sector in the business who offers Housing Finance at the competitive rates. Share of Housing Finance Companies in the housing finance sector was 50.78% in 2001, which decreased to 38.58% in 2004. Whereas the share of Cooperative Sector was increased from 38.81% in 2001 to 55.70% in 2004. The housing finance industry has witnessed the entry of banks in the past few years. These banks have access to cheap funds and are therefore able to lend to customers at lower interest rates resulting in intense competition in the housing finance industry, and finer spreads. The Company specializes in providing housing finance with focus and core competence in housing finance. Banks on the other hand have banking as their main business activity and housing finance is an ancillary business for them. The housing finance industry depends on:

a) Prices in the real estate market, b) Interest rate prevalent in the market and c) Fiscal benefits provided by the Government from time-to-time.

Any changes in the above may affect the disbursements and consequently the margins of the Company. In view of the large population, the Company expects demand for housing to outstrip supply and hence any change in the above factors will not have a major effect on the Company's business. The Company has presence in semi-urban areas of the country, which present an opportunity for the Company to garner more business. Further, the Union Budget has emphasized on Housing in the Rural Sector, which provides an added avenue for generating business. Any change in the government policies may affect the performance of the company NHB vide their Direction No. NHB (ND)/DRS/REGU/DIR/01-69/2004 dated January 1, 2004 reduced the classification period of NPA from 180 days to 90 days. This will result in additional provisioning of the NPA of the HFC, which will result in decline in their profits. Further NHB vide their Direction No. NHB-HFC.DIR.11/CMD/2005 dated October 1, 2005 increased the risk weightage for the standard housing loan assets from 50% to 75% due to with the CAR of the HFC has declined. Any such further change in the policies by the government or the regulatory authority will adversely affect the performance of the Company.

ix

NOTES TO RISK FACTORS

Pre-issue Networth (as on 30/09/2005) Rs. 13831 Lacs Adjusted Pre-issue Net Asset Value (as on 30/09/2005) Rs. 51.41 Issue Size Rights Issue of 2,69,25,533 Equity Shares of Rs.

10/- each for cash at a premium of Rs. [•] per Equity Share aggregating Rs. [•] lacs.

2. There is no interest of Promoters/Directors/Key Management Personnel other than as stated in this Letter of

Offer. 3. No transactions of the Equity Shares of the Company has been taken place by the Promoters / Promoter Group

during last 6 months except as mentioned herein:

Sr. No.

Name of the shareholder No. of shares bought

No. of shares sold

Date of transaction

Price (in Rs.)

Nil 5000 05.10.05 46.86 Nil 10000 06.10.05 46.84 Nil 10000 07.10.05 46.36 Nil 10000 11.10.05 44.93 Nil 5000 13.10.05 44.99 Nil 10000 16.01.06 51.87 Nil 5000 17.01.06 51.82 Nil 5000 17.01.06 51.82 Nil 10000 18.01.06 51.38 Nil 10000 19.01.06 51.44

1. Oriental Insurance Company Ltd

Nil 10000 20.01.06 54.31 50000 Nil 14.12.05 49.68 31382 Nil 14.12.05 49.85 23436 Nil 14.12.05 49.85 16000 Nil 15.12.05 49.89 3350 Nil 16.12.05 49.82

2. General Insurance Corporation of India

5203 Nil 20.12.05 49.70

4. For Related party disclosures under Accounting Standard 18 issued by the Institute of Chartered Accountants of India please refer to para under ‘Related Party Transactions’ on page no. [•] of this Letter of Offer.

5. The Lead Manager and the Company shall update this Letter of Offer and keep the shareholders/public informed of any material changes till the listing and trading commencement.

1

III. INTRODUCTION INDUSTRY

Industry Overview Housing is the one of the basic needs for every human being. Housing is an important component and a measure of socio–economic status of the people. It is regarded as a critical sector in terms of policy initiatives and interventions. The relevance of housing as a social need is long recognized and has therefore influenced the policy making at different levels, viz. national, state and local levels. This is reflected in the efforts of the Government undertaken to improve the housing and habitat conditions by way of financial allocations in the Five Year Plans and fiscal measures related to housing announced in the Union Budgets. In India, housing is basically a state level activity though the Central Government is responsible for the formulation of a broad policy framework for the housing sector and overseeing the effective implementation of the same. The importance of the housing sector can be judged by this fact that we consider house as the best investment and want to invest our hard earned money or saving in a house.

Housing Finance The Housing Finance Companies (HFCs) have stepped up their lending over the years contributing significantly to the growth of the housing sector, however they are still far from realising their full potential. Their strength lies in their specialised set of skills in lending exclusively for housing. The performance of the HFCs in recent years has been overshadowed by the competing banking sector with aggressive lending abilities, the relatively high cost of funds, higher regulatory capital requirement and lower degree of penetration in terms of geographical presence and market segments of the HFCs. Till June 30, 2004 there were 45 HFC’s registered with NHB. The Indian housing finance sector is crowded with players of all sizes and nature ranging from government organisations, insurance companies, banks, housing finance companies and co-operative organisations like HUDCO and NHB to others. Major players in the Industry are HDFC, LIC Housing Finance, Dewan Housing, Can Fin Homes, SBI Home Finance and Gujarat Rural Housing.

COMPANY OVERVIEW GIC Housing Finance Limited was incorporated as 'GIC Grih Vitta Limited' on 12th December 1989. The Company was issued the Certificate for Commencement of Business dated 12th January 1990. The name is changed to its present name vide fresh Certificate of Incorporation issued on 16th November 1993. The Company was formed with the objective of entering in the field of direct lending to individuals and other corporates to accelerate the housing activities in India. The primary business of GICHFL is granting housing loans to individuals and to persons/entities engaged in construction of houses/flats for residential purposes. The Company was promoted by General Insurance Corporation of India and its erstwhile subsidiaries namely, National Insurance Company Limited, The New India Assurance Company Limited, The Oriental Insurance Company Limited and United India Insurance Company Limited together with erstwhile UTI, ICICI, IFCI, HDFC and SBI, all of them contributing to the initial share capital. HDFC, SBI, ICICI and SUUTI have since sold off their holding in the Company and have ceased to be the Promoters of the Company. GIC Housing Finance Limited is in the business of providing housing finance to individuals and those into construction business. GICHFL offers the following products to its customers: Own Your Home Scheme: This scheme is perfectly suited to individual home loan borrowers, aiming to own a house. The Company offers a bouquet of options to the borrower in terms of tenure, rate of interest and value added services.

2

Home loan to NRI: This product specifically caters to the needs of NRIs who want to purchase their own home in India. Generally these transactions prove to be very fruitful to the Company because of the creditworthiness of the NRI as well as the high value of the transaction. Tailor made products: The Company has designed tailor made products to suit individual needs and specifications depending on various criteria. Loans Sanctioned and Disbursement The company has cumulatively approved loans of Rs. 2781 crores comprising 76411 units upto March 31, 2005. Cumulative disbursement till March 31, 2005 stands at Rs. 2427 crores. Loans sanctioned and disbursed during the last 4 years and till the half year ended September 30, 2005 is given below:

(Rs. Lacs)

Particulars 2002 2003 2004 2005 Till half year ended September 30, 2005

Loans Sanctioned 25743 33285 55076 80461 20131 Loans Disbursed 22519 29559 44881 65923 23519 Loans Outstanding Total amount of housing finance outstanding as on September 30, 2005 is Rs. 171149 lacs. Out of the total outstanding on September 30, 2005, 98.34% is granted to individuals and 1.41% is outstanding with corporate clients. A clients wise breakup of the loans outstanding at the FY ended 2002, 2003, 2004, 2005 and as on September 30, 2005 is given below:

(Rs. lacs)

Particulars 2002 2003 2004 2005 Half year ended September 30,

2005 Individuals 64769 79604 106624 154542 168303 Corporates 5254 4494 3644 2776 2415 Others 815 660 631 500 430 Total 70838 84758 110899 157819 171149

3

SELECTED FINANCIAL INFORMATION Following selected financial data have been prepared in accordance with Indian Accounting Standards, in conjunction with our financial statements and related notes and "Management's Discussions and Analysis". The audited financial statements have been prepared in Indian rupees and have been prepared in accordance with Indian Accounting Standards for the fiscal years ended 2001,2002, 2003, 2004, 2005 and six months period ending on 30th September, 2005.

GIC Housing Finance Ltd.

Statement of Profits and Losses Rs. in lacsParticulars For the Financial Year SIX MONTHS 2000-2001 2001-2002 2002-2003 2003-2004 2004-2005 30.09.2005 Income: Operating Income 9,095 9,163 9,676 9,920 12,453 7,583 Investment and other Income 85 74 77 90 108 38

Total (A) 9,180 9,237 9,753 10,010 12,561 7,621 Expenditure: Interest 6,849 7,599 7,272 6,990 7,865 4,784 Staff Expenses 153 162 199 185 236 128 Other Expenses 347 383 450 567 808 425 Miscellaneous expenses written off 6 6 5 5 10 5 Depreciation 72 56 43 40 44 23 Non-Performing assets written off 965 342 823 200 - - Provision for Non-performing assets (Net) 145 521 201 565 1,524 386

Total (B) 8,537 9,069 8,993 8,552 10,487 5,751 Net Profit Before Tax and Extra ordinary

Items (A-B) 643 168 760 1,458 2,074 1,870 Less:Taxation 210 150 235 526 856 473 Deferred Tax Assets - (102) (136) (180) (558) (124) Fringe Benefit Tax - - - - - 3 Extraordinary Items - - - - - -

Net Profit After Tax and Extra ordinary items 433 120 661 1,112 1,776 1,518

4

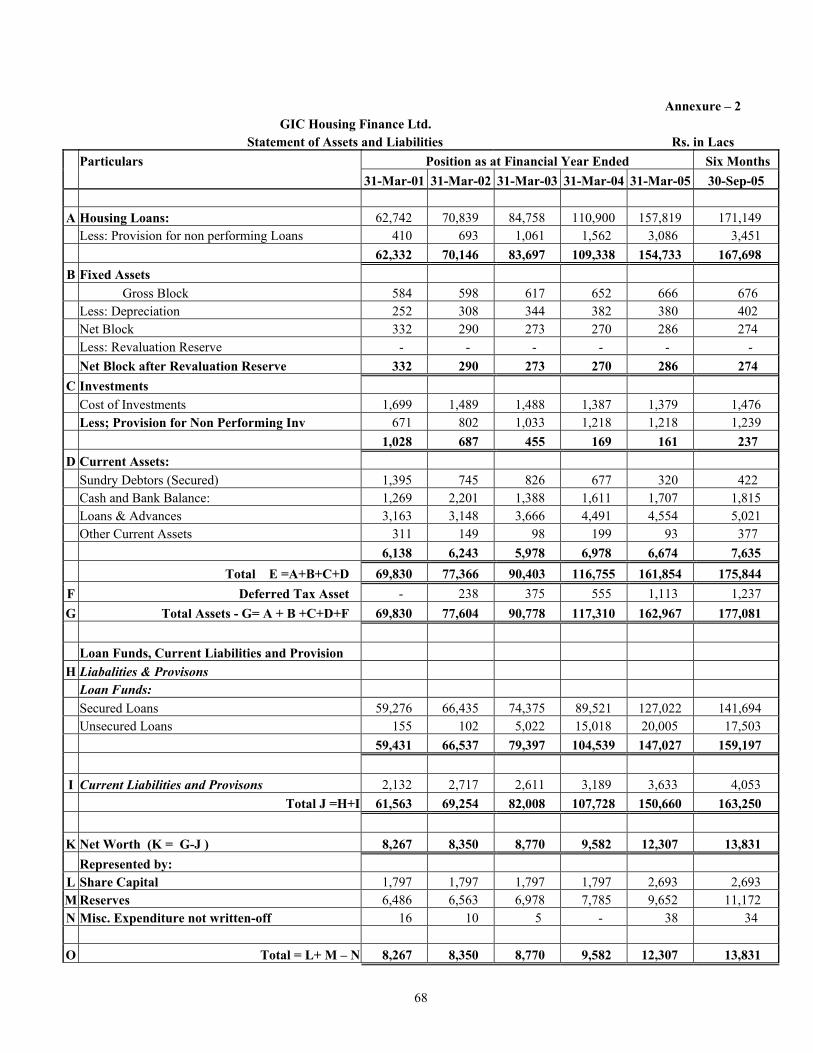

GIC Housing Finance Ltd.

Statement of Assets and Liabilities Rs. in lacs Particulars Position as at Financial Year Ended Six Months 31-Mar-01 31-Mar-02 31-Mar-03 31-Mar-04 31-Mar-05 30-Sep-05 A Housing Loans: 62,742 70,839 84,758 110,900 157,819 171,149 Less: Provision for non performing Loans 410 693 1,061 1,562 3,086 3,451 62,332 70,146 83,697 109,338 154,733 167,698 B Fixed Assets Gross Block 584 598 617 652 666 676 Less: Depreciation 252 308 344 382 380 402 Net Block 332 290 273 270 286 274 Less: Revaluation Reserve - - - - - - Net Block after Revaluation Reserve 332 290 273 270 286 274 C Investments Cost of Investments 1,699 1,489 1,488 1,387 1,379 1,476 Less; Provision for Non Performing Inv 671 802 1,033 1,218 1,218 1,239 1,028 687 455 169 161 237 D Current Assets: Sundry Debtors (Secured) 1,395 745 826 677 320 422 Cash and Bank Balance: 1,269 2,201 1,388 1,611 1,707 1,815 Loans & Advances 3,163 3,148 3,666 4,491 4,554 5,021 Other Current Assets 311 149 98 199 93 377 6,138 6,243 5,978 6,978 6,674 7,635 Total E =A+B+C+D 69,830 77,366 90,403 116,755 161,854 175,844 F Deferred Tax Asset - 238 375 555 1,113 1,237 G Total Assets - G= A + B +C+D+F 69,830 77,604 90,778 117,310 162,967 177,081 Loan Funds, Current Liabilities and Provision

H Liabalities & Provisons Loan Funds: Secured Loans 59,276 66,435 74,375 89,521 127,022 141,694 Unsecured Loans 155 102 5,022 15,018 20,005 17,503 59,431 66,537 79,397 104,539 147,027 159,197 I Current Liabilities and Provisons 2,132 2,717 2,611 3,189 3,633 4,053 Total J =H+I 61,563 69,254 82,008 107,728 150,660 163,250

K Net Worth (K = G-J ) 8,267 8,350 8,770 9,582 12,307 13,831 Represented by: L Share Capital 1,797 1,797 1,797 1,797 2,693 2,693 M Reserves 6,486 6,563 6,978 7,785 9,652 11,172 N Misc. Expenditure not written-off 16 10 5 - 38 34

O Total = L+ M – N 8,267 8,350 8,770 9,582 12,307 13,831

5

IV. GENERAL INFORMATION

GIC HOUSING FINANCE LIMITED (Incorporated on 12th December, 1989 under the Companies Act, 1956 as GIC Grih Vitta Limited and renamed to GIC Housing

Finance Limited on 16th November, 1993. A Certificate for Commencement of Business was issued on 12th January 1990.) Registered and Corporate Office: Universal Insurance Building,

3rd Floor, Sir P.M. Road, Fort, Mumbai - 400 001. Tel: (022) - 2285 1765-67, (022) - 2285 3866/8 Fax: (022) - 2288 4985.

E-mail: [email protected]; website: www.gichfindia.com Registration No. 11-54583

Address of the Registrar of Companies: Registrar of Companies Mumbai, Maharashtra. Dear Shareholder(s), Pursuant to the resolutions passed by the Board of Directors of the Company at its meeting held on December 26, 2005 and resolution passed by the shareholders in the Extra Ordinary General Meeting held on January 23, 2006, it has been decided to make the following offer to the Equity Shareholders of the Company: Right Issue of 2,69,25,533 Equity Shares of Rs.10 each for cash at a premium of Rs. [•]/- per Equity Share aggregating to Rs. [•] lacs on rights basis to the Equity Shareholders of GIC Housing Finance Limited (the “Company”/ “GICHFL”) in the ratio of One Equity Share for every One Equity Share held on the record date i.e. [•], 2006. The company has fixed the price band of Rs.37 to Rs.42, the Floor Price being Rs.37 and Cap Price being Rs.42. The Issue Price will be fixed on or before the fixation of Record Date. Statutory Declaration In the reasonable opinion of the Board, there are no circumstances that have arisen since the date of the last financial statement disclosed in the Letter of Offer, that materially or adversely affect or are likely to affect the performance or profitability of the Company or value of its assets or its ability to pay its liabilities within the next twelve months. Important 1. This Issue is applicable only to those shareholders whose names appear as beneficial owners as per the list to be

furnished by Depositories in respect of the Equity Shares held in the electronic form and on the Register of Members of the Company in respect of the Equity Shares held in physical form at close of business hours on [•], 2006, i.e. the Record Date.

2. Shareholders' attention is drawn to RISK FACTORS appearing on Page [•] of this Letter of Offer. 3. Please ensure that the CAF is received with this Letter of Offer. 4. Please read this Letter of Offer and the instructions contained therein and in the CAF carefully, before filling in

the CAF. The instructions contained in the CAF are an integral part of this Letter of Offer and must be carefully followed. Application is liable to be rejected if it is not in conformity with the terms of the Letter of Offer and/or the CAF.

5. All enquiries in connection with this Letter of Offer or CAF should be addressed to the Registrars to the Issue, Sharepro Services (India) Pvt. Ltd., quoting the registered Folio Number/DP ID/Client ID number and the Serial Number of the CAF and his/her full name and address.

6. In case the original CAF is not received, lost or misplaced by the shareholder, the Registrars/Company will issue a duplicate CAF on the request of the shareholder who should furnish the registered Folio Number/DP ID/Client ID number and his/her full name and address to the Registrars/Company. Please note that those applicants who are making the application in the duplicate CAF should not utilize the original CAF for any purpose including renunciation, even if it is received/found subsequently. In case the original and the duplicate CAFs are lodged for subscription, allotment will be made on the basis of the duplicate CAF and the original CAF will be ignored.

7. The Rights Issue will be kept open for a minimum period of 30 days. If extended, it will be kept open for a maximum period of 60 days.

6

8. The Lead Manager and the Company shall make all information available to the Equity Shareholders and no selective or additional information would be available for a section of the Equity shareholders in any manner whatsoever including at presentations, in research or sales reports etc. after filing of the draft Letter of Offer with SEBI/Stock Exchange

9. The Lead Manager and the Company shall update the Letter of Offer and keep the public informed of any material changes till the listing and trading commences.

10. All the legal requirements as applicable till the filing of the Letter of Offer with the Designated Stock Exchange have been complied with.

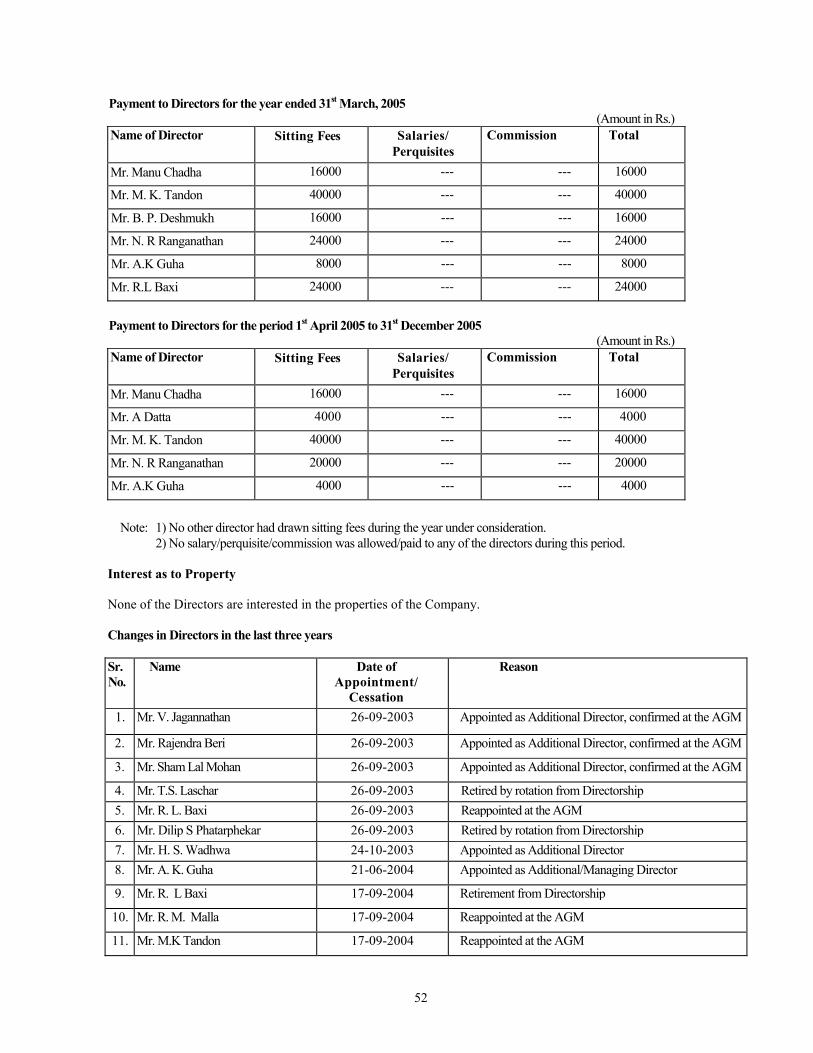

BOARD OF DIRECTORS:

Sr. No. Name of the Director Position held 1. Mr. R.K Joshi Nominee Director 2. Mr. B Chakrabarti Non Executive Director 3. Mr. M.K Garg Non Executive Director 4. Mr. M Ramadoss Non Executive Director 5. Mr. V Ramasaamy Non Executive Director 6. Mr. Manu Chadha Independent & Non Executive Director 7. Mr. R.M. Malla Non Executive Director 8. Mr. M.K. Tandon Independent & Non Executive Director 9. Mr. B. P. Deshmukh Independent & Non Executive Director

10. Mr. Arun Datta Independent & Non Executive Director 11. Mr. N. R Ranganathan Nominee Director 12. Mr. A. K Guha Executive Director

For more details regarding our Board of Directors please refer to page no. [•] of this draft Letter of Offer. Issue Schedule ISSUE OPENS ON LAST DATE FOR RECEIVING

REQUESTS FOR SPLIT FORM ISSUE CLOSES ON

[•] 2006 [•] 2006 [•] 2006 ISSUE MANAGEMENT TEAM Company Secretary and Compliance Officer Mr. S. Sridharan Company Secretary and Asst Vice President GIC Housing Finance Limited, 3rd Floor, Universal Insurance Building, Sir P.M. Road, Fort, Mumbai - 400 001 Tel: (022) 2288 1783 Fax: (022) 2288 4985 Email: [email protected]

7

Bankers to the Company Bank of India D.N. Road Branch, Sadhana Reyon House, Fort, Mumbai-400001 Tel No: (022) 2261 4878 Fax No: (022) 2261 0168 HDFC Bank Limited Motwani Chembers, Manikji Wadia Building Mumbai-400 023. Tel No: (022) 5657 3602 Fax No: (022) 2270 3392 ISSUE MANAGEMENT TEAM Lead Manager to the Issue: IDBI Capital Market Services Limited 5th floor, Mafatlal Centre, Nariman Point, Mumbai – 400 021 Tel: (022) 5637 1212 Fax: (022) 2288 5848 E-mail: [email protected] Website: www.idbicapital.com Contact Person: Mr. Saurabh Jain Registrar to the Issue: Sharepro Services (India) Pvt. Ltd. Satam Estate, 3rd Floor, Above Bank of Baroda, Cardinal Gracious Raod, Chakala, Andheri (East), Mumbai-400 099. Tel: (022) 2821 5168/2834 8218/ 2832 9828 Fax:(022) 2837 5646 Website: www.shareproservices.com Contact Person: Mr. Ashok Gupta Legal Advisers to the Issue: ANS Law Associates Advocates & Solicitors 41-A Filmcenter 68, Tardeo Road Mumbai-400 034 Tel: (022) 5660 4761/62 Fax:(022) 5660 4763 Contact Person: Mr. Sharad Abhyankar Email: [email protected]

8

Bankers to the Issue: IDBI Ltd. 224, Mittal Court, A- Wing, 2nd Floor, Nariman Point, Mumbai – 400 021 Tel.: (022) 5658 8273 Fax: (022) 2288 0131 Auditors of the Company: M/s M.P. Chitale & Company Chartered Accountants 1st Floor, Hamam House, Ambalal Doshi Marg, Fort, Mumbai-400001. Tel No: (022) 2265 1186 Fax No: (022) 2265 5334 Email: [email protected] INTER SE ALLOCATION OF RESPONSIBILITIES Not Applicable CREDIT RATING This being a rights issue of Equity Shares, credit rating is not required. TRUSTEES This being a rights issue of Equity Shares, appointment of Trustees is not required. MONITORING AGENCY Not Applicable APPRAISING ENTITY Not Applicable MINIMUM SUBSCRIPTION i. If the Company does not receive the minimum subscription of 90% of the Issue, the entire subscription

amount shall be refunded to the applicants within 42 days from the date of closure of the Issue. ii. If there is a delay in refund of subscription amount by more than 8 days after the Company becomes liable to

pay the subscription amount (i.e. 42 days after closure of the Issue), the Company will pay interest for the delayed period, at rates prescribed under sub-sections (2) and (2A) of Section 73 of the Companies Act, 1956.

9

V. CAPITAL STRUCTURE OF THE COMPANY

No. of shares Nominal Value

Issue Amount

A. Authorised Capital* 10,00,00,000 Equity Shares of Rs.10/- each 50,00,000 Redeemable Cumulative Participating or Non Participating Preference Shares of Rs. 100/- each

100,00,00,000/-

50,00,00,000/-

-- --

B. Issued Capital - 2,69,25,533 Equity Shares of Rs.10/- each - NIL Redeemable Cumulative Participating or Non

Participating Preference Shares of Rs. 100/- each

26,92,55,330

NIL

--

C. Subscribed and Paid-up Capital - 2,69,25,533 Equity Shares of Rs.10/- each - NIL Redeemable Cumulative Participating or Non Participating Preference Shares of Rs. 100/- each

26,92,55,330

NIL

--

D. Present Rights Issue in the ratio of one Equity Share for every Equity Share held as on [•] (Record Date) - 2,69,25,533 Equity Shares of Rs.10/- each at a premium of Rs. [•]/- per share

26,92,55,330 [•]

E. Post Issue Capital 5,38,51,066 Equity Shares of Rs.10/- each

53,85,10,660

--

F. Share Premium Account Before the Offer After the Offer

37,29,66,466

[•]

* The Company has reclassified its Authorised Capital in its AGM on September 15, 2005 from Rs. 150 crores

divided into 5,00,00,000 Equity Shares of Rs.10/- each and 1,00,00,000 Redeemable Cumulative Participating or Non Participating Preference Shares of Rs. 100/- each to Rs. 150 crores divided into 10,00,00,000 Equity Shares of Rs.10/- each and 50,00,000 Redeemable Cumulative Participating or Non Participating Cumulative Preference Shares of Rs. 100/- each.

NOTES TO CAPITAL STRUCTURE:

1. Share Capital History:

Sr. No

Date of allotment

No. of shares

Cumulative number of

Equity Share

Face Value (Rs.)

Issue Price (Rs.)

Consideration

Particulars

1 Incorporation 11 11 10 10 Cash Initial subscription to the Memorandum

2 30/03/1991 500000 5000011 10 10 Cash First Allotment 3 02/12/1993 500011 10000022 10 10 Cash Rights Issue 4 10/01/1995 8004900 18004922 10 50 Cash Initial Public Offering and

Allotment to Promoters 5 30/06/2004 (53800) 17951122 10 - - Forfeited and Cancelled 6 27/11/2004 8975561 2,69,25,533 10 16 Cash Rights Issue of one Equity Share

for every two Equity Shares held at Rs. 16 per share (including Premium)

10

3. Promoters’ Contribution and Lock-in: The present issue being a rights issue, provisions of Promoters’ contribution and lock-in are not applicable. 4. Present Rights Issue:

Type of Instrument Ratio Face Value (Rs.)

No. of shares

Issue Price (Rs.)

Consideration

Equity Shares 1:1 10/- 2,69,25,533 [•] Cash 5. Shareholding pattern of the Company as on December 31, 2005 is given below:

Category No. of Shares Held % of Share Holding Promoter's Holding Promoters Indian Promoters 11370531 42.23

Sub Total 11370531 42.23 Non Promoter's Holding Institutional Investors Mutual Funds and UTI 5500 0.02 Banks, Financial Institutions, Insurance Companies 509123 1.89

FIIs 1396068 5.19 Sub Total 1910691 7.10

Others Private Corporate Bodies 3996980 14.84 Indian Public 9541487 35.44 NRIs / OCBs 105844 0.39

Sub Total 13644311 50.67 Grand Total 26925533 100.00 Notes: a) The following Promoters have communicated their intention to subscribe to their own entitlement in this

rights issue in full.

Name of the Promoter Date of Letter New India Assurance Company Limited January 13, 2006 General Insurance Corporation of India January 23, 2006 The Oriental Insurance Company Limited January 10, 2006 United India Insurance Company Limited January 25, 2006 National Insurance Company Limited January 27, 2006

b) IFCI Ltd., one of the Promoters is yet to give their consent to participate in the present Rights Issue

c) The allotment to the Promoters even if they subscribe to unsubscribed portion to the fullest extent will not

result in public shareholding falling below the permissible minimum level. Thus the provisions of Clause 17 of SEBI (Delisting of Securities) Guidelines, 2003 are not applicable.

7. The Company has not issued any warrant, option, convertible loan, debenture or any other securities

convertible at a later date into equity, which would entitle the holders to acquire further equity shares of the Company.

11

8. The Equity Shares of the Company are being traded in compulsory dematerialised mode. The market lot of the equity shares is 1 (one).

9. No transactions of the Equity Shares of the Company has been taken place by the Promoters / Promoter

Group during last 6 months except as mentioned herein:

Sr. No.

Name of the shareholder No. of shares bought

No. of shares sold

Date of transaction

Price (in Rs.)

Nil 5000 05.10.05 46.86 Nil 10000 06.10.05 46.84 Nil 10000 07.10.05 46.36 Nil 10000 11.10.05 44.93 Nil 5000 13.10.05 44.99 Nil 10000 16.01.06 51.87 Nil 5000 17.01.06 51.82 Nil 5000 17.01.06 51.82 Nil 10000 18.01.06 51.38 Nil 10000 19.01.06 51.44

1 Oriental Insurance Company Ltd

Nil 10000 20.01.06 54.31 50000 Nil 14.12.05 49.68 31382 Nil 14.12.05 49.85 23436 Nil 14.12.05 49.85 16000 Nil 15.12.05 49.89 3350 Nil 16.12.05 49.82

2. General Insurance Corporation of India

5203 Nil 20.12.05 49.70

10. The ten largest shareholders two years prior to the date of filing of this Letter of Offer with Stock Exchanges are as follows:

Sr. No.

Name of the Shareholders Number of Equity Shares

Percentage of shareholding (%)

1. IFCI Ltd. 1575000 8.74% 2. National Insurance Company Ltd. 1197000 6.64% 3. The New India Assurance Company Ltd. 1197000 6.64% 4. The Oriental Insurance Company Ltd. 1197000 6.64% 5. United Indian Insurance Company Ltd. 1197000 6.64% 6. General Insurance Corporation Ltd. 1071422 5.95% 7. SU UTI 985793 5.47% 8. CD Equisearch Pvt. Ltd. 558630 3.10% 9. EXIM Scrip Dealers Pvt. Ltd. 289901 1.61%

10. UTI – SUS 1999 164716 0.91%

12

11. The ten largest shareholders as on 10 days prior to the date of filing of the Letter of Offer with Stock Exchanges are as follows:

Sr. No.

Name of the Shareholders Number of Equity Shares

Percentage of shareholding

(%) 1. IFCI Ltd. 2200000 8.17% 2. General Insurance Corporation Ltd. 2162769 8.03% 3. The New India Assurance Company Ltd. 1936750 7.19% 4. United Indian Insurance Company Ltd. 1886750 7.01% 5. The Oriental Insurance Company Ltd. 1597512 5.93% 6. National Insurance Company Ltd. 1586750 5.89% 7. Caledonia Investments Plc 1336068 4.96% 8. Tata Investment Corporation Ltd. 665400 2.47% 9. CD Equifinance Pvt. Ltd. 642000 2.38%

10. Dilip B. Desai 316480 1.17%

12. The ten largest shareholders as on the date of filing of the Letter of Offer with Stock Exchanges are as follows:

Sr. No.

Name of the Shareholders Number of Equity Shares

Percentage of shareholding

(%) 1. IFCI Ltd. 2200000 8.17% 2. General Insurance Corporation Ltd. 2162769 8.03% 3. The New India Assurance Company Ltd. 1936750 7.19% 4. United Indian Insurance Company Ltd. 1886750 7.01% 5. National Insurance Company Ltd. 1586750 5.89% 6. The Oriental Insurance Company Ltd. 1567512 5.82% 7. Caledonia Investments Plc 1336068 4.96% 8. Tata Investment Corporation Ltd. 665400 2.47% 9. CD Equifinance Pvt. Ltd. 642000 2.38%

10. Dilip B. Desai 316480 1.17% 13. The Company/Promoters/Directors/Lead Merchant Bankers have not entered into buyback or similar

arrangements for purchase of securities issued by the Company. 14. IDBI Capital Market Services Ltd., Lead Manager to the Issue is holding 140267 Equity Shares of the

Company amounting to 0.52% of the total Pre-Issue Capital of the Company as on December 31, 2005. IDBI Capital Market Services have not traded in the Equity Shares of the Company after its appointment as the Lead Manager to the Issue.

15. The entire price of Rs. [•]/- per share is payable on application. Since the shares allotted will be fully paid –

up at the time of allotment, the Forfeiture Clause of SEBI (DIP) Guidelines will not be applicable to the Equity Shares being allotted in terms of this Letter of Offer.

16 The Company has not availed of “bridge loans” to be repaid from the proceeds of the Issue, for incurring

expenditure on the Objects of the Issue. 17. The present Rights Issue is being made in the ratio of one equity share to every one equity share held (ie,

1:1) and will not lead to creation of fractional entitlement. 18. The total number of shareholders as on the date of filing the Letter of Offer with the stock exchange is

24175.

13

19. At any given time there shall be only one denomination for the shares of the Company and the disclosures and accounting norms specified by SEBI from time to time will be complied with.

20. The Company shall not make any further issue of capital whether by way of issue of bonus shares,

preferential allotment, rights issue or public issue or in any other manner during the period commencing from the submission of the Letter of Offer to SEBI for the Rights Issue till the securities referred in the Letter of Offer have been listed or application money refunded on account of failure of the Issue.

21 The Company does not propose to alter the capital structure by way of split or consolidation of the

denomination of the shares or the issue of shares on a preferential basis or issue of bonus or rights or further public issue of shares or any other securities within a period of six months from the date of opening of the present Issue.

14

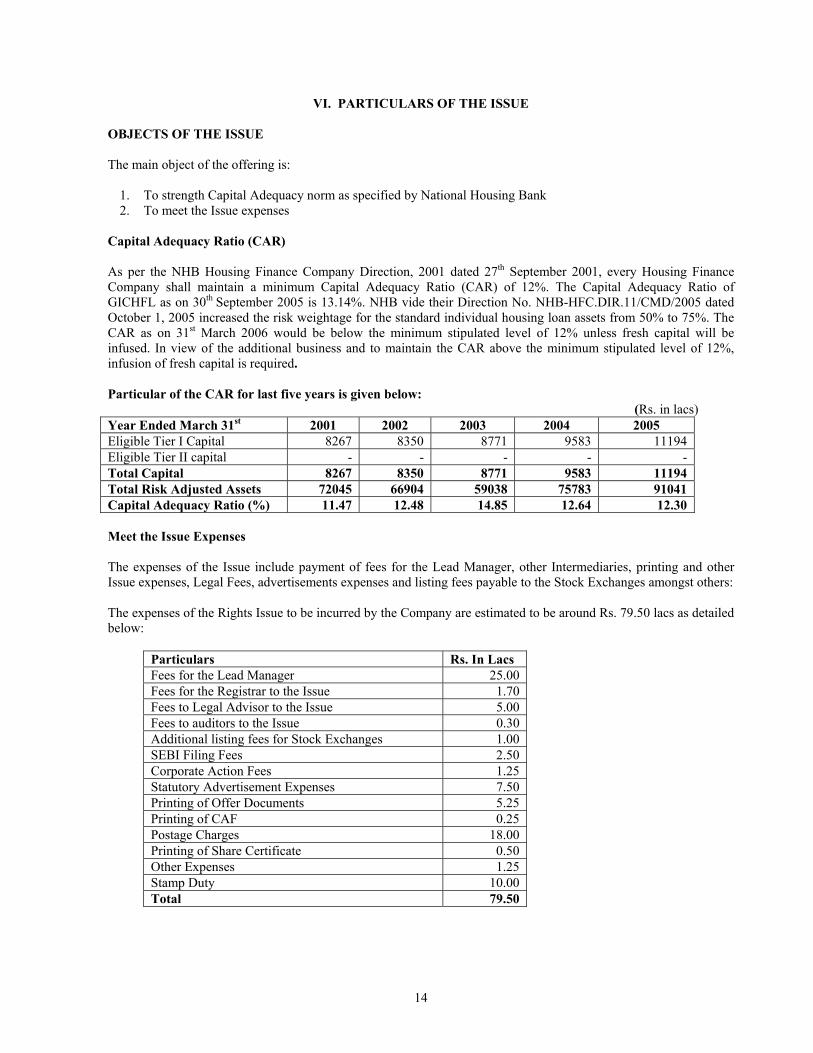

VI. PARTICULARS OF THE ISSUE OBJECTS OF THE ISSUE The main object of the offering is:

1. To strength Capital Adequacy norm as specified by National Housing Bank 2. To meet the Issue expenses

Capital Adequacy Ratio (CAR) As per the NHB Housing Finance Company Direction, 2001 dated 27th September 2001, every Housing Finance Company shall maintain a minimum Capital Adequacy Ratio (CAR) of 12%. The Capital Adequacy Ratio of GICHFL as on 30th September 2005 is 13.14%. NHB vide their Direction No. NHB-HFC.DIR.11/CMD/2005 dated October 1, 2005 increased the risk weightage for the standard individual housing loan assets from 50% to 75%. The CAR as on 31st March 2006 would be below the minimum stipulated level of 12% unless fresh capital will be infused. In view of the additional business and to maintain the CAR above the minimum stipulated level of 12%, infusion of fresh capital is required. Particular of the CAR for last five years is given below: (Rs. in lacs) Year Ended March 31st 2001 2002 2003 2004 2005 Eligible Tier I Capital 8267 8350 8771 9583 11194 Eligible Tier II capital - - - - - Total Capital 8267 8350 8771 9583 11194 Total Risk Adjusted Assets 72045 66904 59038 75783 91041 Capital Adequacy Ratio (%) 11.47 12.48 14.85 12.64 12.30 Meet the Issue Expenses The expenses of the Issue include payment of fees for the Lead Manager, other Intermediaries, printing and other Issue expenses, Legal Fees, advertisements expenses and listing fees payable to the Stock Exchanges amongst others: The expenses of the Rights Issue to be incurred by the Company are estimated to be around Rs. 79.50 lacs as detailed below:

Particulars Rs. In Lacs Fees for the Lead Manager 25.00 Fees for the Registrar to the Issue 1.70 Fees to Legal Advisor to the Issue 5.00 Fees to auditors to the Issue 0.30 Additional listing fees for Stock Exchanges 1.00 SEBI Filing Fees 2.50 Corporate Action Fees 1.25 Statutory Advertisement Expenses 7.50 Printing of Offer Documents 5.25 Printing of CAF 0.25 Postage Charges 18.00 Printing of Share Certificate 0.50 Other Expenses 1.25 Stamp Duty 10.00 Total 79.50

15

Means of Finance and Deployment of funds The funds of Rs. [•] raised by the Company through the proposed Rights Issue will be deployed as under:

Particulars Rs. In Lacs Housing Finance Activities [•] Issue Expenses [•] Total [•]

BASIC TERMS OF ISSUE The Equity Shares now being offered are subject to the terms of this Letter of Offer, the CAF, the Memorandum and Articles of the Company, approvals under the Foreign Direct Investment scheme of Government of India, FEMA, if applicable, Guidelines issued by SEBI, the Act, the guidelines, notifications and regulations for the Issue of capital and for the listing of securities issued by the Government and/or other Statutory Authorities and bodies from time to time and such terms and conditions as may be incorporated in the Letter of Allotment/Share Certificate or any deed or document executed by the Company regarding the Rights Issue. The principal terms and conditions of the Issue are as follows: i. Present Issue: Rights Issue of 2,69,25,533 equity shares of Rs. 10/- each in a ratio of 1:1 ii. Face Value: Each Equity Share shall have a face value of Rs.10/-. iii. Issue Price: Rs. [•]/- per Share. The company has fixed the price band of Rs.37 to Rs.42, the Floor Price being Rs.37 and Cap Price being Rs.42. The Issue Price will be fixed on or before the fixation of Record Date.

16

BASIS OF THE ISSUE PRICE Qualitative Factors Profit making and dividend paying Company since 1995 Quantitative Factors 1. Earning per Share (EPS)

Financial Year EPS (Rs.)

Weight used

2002-03 3.67 1 2003-04 6.17 2 2004-05 7.60 3 Weighted Average 6.47

2. Price Earnings Ratio (P/E Ratio) Price Earning Ratio at EPS for the financial period ended March 31, 2005 based on the price of January 16, 2006

6.84

3. Industry P/E

Highest 27.2 Average 23.3 Lowest 4.3

(Source: Capital Market Vol. XX/22 Jan 02 to Jan. 15, 2006 Segment: Finance - Housing) 4. Return on networth

Financial Year Return on Net Worth (%)

Weight used

2002-03 7.54% 1 2003-04 11.61% 2 2004-05 14.44% 3 Weighted Average 12.34%

5. Net Asset Value (NAV) per share

As on 30/09/2005 (Rs.) 51.41 After the issue based on 30th September, 2005 results [•] 6. Minimum Return on Networth after Issue required for maintaining Pre-Issue EPS of Rs. 7.60 EPS Minimum Return of Networth after

Issue Rs. 7.60 [•]

17

7. Peerset Analysis There are few companies is in the same line of business as GICHFL. A comparison with some of the Housing Finance Companies is as follows:

(Figures as on March 31, 2005) Name of the Company Income

(Rs. In Lacs)

PAT (Rs. In Lacs)

Equity (Rs. In Lacs)

EPS (Rs.)

P/E (x)

Price as on 27/12/2005

LIC Housing Finance Ltd. 106870 14370 8499 16.2 10.1 196.45 Dewan Housing Finance Ltd. 16380 2710 5109 5.0 9.6 64.50 GIC Housing Finance Ltd. 12560 1776 2693 7.6 5.6 55.05 Can Fin Homes 12730 2110 2050 10.0 4.4 52.70 GRUH Finance 8550 1670 2650 6.0 10.9 86.90 (Source: Capital Market Vol. XX/22 Jan 02 to Jan. 15, 2006 Segment: Finance Housing, Company Data and BSE)

18

TAX BENEFITS TO THE COMPANY AND ITS SHAREHOLDERS The Company has received tax benefit certificate from M/s M. P. Chitale & Co, Chartered Accountants specifying the tax benefits available to the Company and its shareholders under the Direct Tax Laws. The contents of the same are given below. Unless otherwise specified, sections referred to are sections of the Income Tax Act, 1961. To the Company A Under the Income Tax Act, 1961 1. In accordance with and subject to the provisions of Section 112 of the Income Tax Act, 1961, long term

capital gain accruing to the Company will be subject to tax as stated below instead of normal rate of 35% (plus applicable surcharge) applicable to the Company.

(a) If long term capital gain is computed with indexation @ 20% (plus applicable surcharge) (b) If long term capital gain is computed without indexation @ 10% (plus applicable surcharge)

The Company is eligible to claim exemption in respect of tax on long term capital gains u/s. 54EC and

54ED if the amount of capital gains is invested in certain specified bonds / securities subject to the fulfillment of the conditions specified in those sections.

2. The Company is not liable to pay long term capital gains tax in respect of shares of the company held by

then for a period of more than twelve months by virtue of Section 10(38) of the Act, subject to the fulfillment of the following conditions:

(a) The transaction of sale of such equity share is entered into on or after 1 October, 2004. (b) The transaction is chargeable to securities transaction tax under Chapter VII of the Finance (No.2)

Act, 2004. 3. Short term capital gains arising on transfer of equity shares of a company would be liable to tax at the rate

of 10% (plus applicable surcharge and education cess) by virtue of Section 111 A if the following conditions are satisfied:

(a) the transaction of sale of such equity share is entered into on or after 1 October, 2004. (b) the transaction is chargeable to securities transaction tax under Chapter VII of the Finance (No.2) Act,

2004. 4. Benefits of unabsorbed business/ long term capital losses and allowances

Company has unabsorbed losses/ allowances under the Act, which can be carried forward for set off against the income under the Act of future years as under: (i) As per Section 72 of the Act, Company can carry forward the unabsorbed business losses for a

period of eight assessment years immediately succeeding the assessment year in which the loss was first computed.

(ii) As per Section 32 of the Act, Company can carry forward the unabsorbed depreciation allowance of earlier years for an indefinite period to be set off against business income under the Act of future years.

(iii) As per Section 74 of the Act, Company can carry forward the unabsorbed long term capital losses for a period of eight assessment years immediately succeeding the assessment year in which the loss was first computed to be set off against long term capital gains under the Act of future years.

5. The Company is entitled to a deduction of 40% of its profits from the business of providing long term

finance u/s 36(1) (viii) of the Income-tax Act, 1961. The said deduction is subject to the condition that the Company is required to create and maintain a special reserve to the extent of the deduction. If the aggregate amount carried to such reserve exceeds twice the amount of the paid up share capital and general reserves of the Company, the deduction is restricted to such amount only.

19

6. Dividend Income received from Domestic Companies is exempt under section 10(34) of the Income-tax

Act, 1961. 7. In accordance with and subject to the provisions of Section 10(35) of the Act, the following income shall be

exempt in the hands of the Company:

(i) Income received in respect of the units of a Mutual Fund specified under Clause (23D) of Section 10 of the Act; or

(ii) Income received in respect of units from the Administrator of the specified undertaking; or (iii) Income received in respect of units from the specified company.

Under Wealth Tax Act, 1957 The Company is liable to pay wealth tax as per the provisions of Wealth Tax Act, 1957 at the rate of 1% in respect of certain assets owned by the Company, subject to the basic exemption of Rs.15 lacs. To the Resident Members of the Company B. Under the Income Tax Act, 1961 1. Dividend Income received from Domestic Companies is exempt under section 10(34) of the Income-tax

Act, 1961.

2. The shareholders are not liable to pay long term capital gains tax in respect of shares of the company held by then for a period of more than twelve months by virtue of Section 10(38) of the Act, subject to the fulfillment of the following conditions: (a) The transaction of sale of such equity share is entered into on or after 1 October, 2004. (b) The transaction is chargeable to securities transaction tax under Chapter VII of the Finance (No.2)

Act, 2004. Proviso to the section specifies that in case of individual and HUF, where the total income as reduced by such short term capital gains is below the maximum amount not chargeable to tax, then such short term capital gains shall be reduced by the amount by which the total income as so reduced falls short of the maximum amount which is not chargeable to tax and the tax on the balance of such short term capital gains shall be computed at the rate of ten percent.

3. Short term capital gains arising on transfer of the company’s shares would be liable to tax at the rate of 10% (plus applicable surcharge and education cess) by virtue of Section 111 A if the following conditions are satisfied: (a) the transaction of sale of such equity share is entered into on or after 1 October, 2004 (b) the transaction is chargeable to securities transaction tax under Chapter VII of the Finance (No.2)

Act, 2004. Further, the public issue of shares of the Company would also qualify as an eligible issue of capital and long term capital gains would qualify for the benefit of Section 54ED of the Act if the capital gains are invested in shares of the Company.

Under Wealth Tax Act, 1957 Shares held in Domestic Company are not “asset” under the Wealth-Tax Act 1957, hence not liable to wealth tax in the hands of the holder of the said shares

20

To The Non-Resident Members Of The Company C. Under the Income Tax Act, 1961 1. Under Section 115E of the Act, where shares in the company are acquired or subscribed for in convertible

foreign exchange by a Non Resident Indian, capital gains arising to the non-resident Indian on transfer of shares held for a period exceeding 12 months, shall, of the Act, be concessionally taxed at the rate of 10% (plus applicable surcharge and education cess). (Reference may also be made to the provisions of Section 115D of the Act).

2. Under section 115F of the Income Tax Act, 1961 the Long Term Capital gain as referred to in 1 above shall

be exempted from income tax entirely / proportionately if he/she invest all or a portion of the net consideration in specified assets as defined in section 115C (f) of the Income Tax Act, 1961 within 6 months of the date of transfer. The amount so exempted shall, however, be chargeable to tax under the provisions of section 115F(2) if the specified assets are transferred or converted in to money within three years from the date of acquisition thereof as specified in the said section.

3. Under provisions of Section 115G of the Act, it shall not be necessary for a Non-Resident Indian to furnish

his return of Income if his only source of income is investment income or long term capital gains or both arising out of assets acquired, purchased or subscribed in convertible foreign exchange and tax deductible at source has been deducted there from.

4. As per Section 115-I of the Act, a non-resident Indian (i.e. an individual being a citizen of India or person of

India origin who is not a “resident”) elects not to be governed by the provision of Chapter XII-A of the Income Tax Act, 1961, than his/her total income shall be computed and charged in accordance with other provisions of the Act.

5. By virtue of Section 10(34) of the Act, income earned by way of dividend income from domestic company

referred to in Section 115-O of the Act, are exempt from tax in the hands of the shareholders. 6. Where any Double Taxation Avoidance Agreement [DTA] entered into by India with any other country

provides for a concessional tax rate or exemption in respect of income from the investment in the company’s shares, those beneficial provisions shall prevail over the provisions of the Income Tax Act, 1961 in that regard.

Under Wealth Tax Act, 1957 Share held in Domestic Company are not “asset” under the Wealth-Tax Act 1957, hence not liable to wealth tax in the hands of the holder of the said shares To The Foreign Institutional Investors (FII's) D. Under the Income Tax Act, 1961 1. Under Section 115AD (1)(b)(ii) of the Act, Income by way of Short Term Capital Gain arising from the

transfer of shares held in the Company for a period of less than twelve months will be taxable @ 30% (plus applicable surcharge).

2. Under Section 115AD (1)(b)(iii) of the Act, Income by way of Long Term Capital Gain arising from the transfer of shares held in the Company will be taxable @ 10% (plus applicable surcharge)

3. Income by way of dividend received on shares of the Company is exempt u/s. 10(34) of the Income Tax Act, 1961."

4. Where any Double Taxation Avoidance Agreement [DTA] entered into by India with any other country provides for a concessional tax rate or exemption in respect of income from the investment in the company’s shares, those beneficial provisions shall prevail over the provisions of the Income Tax Act, 1961 in that regard.

21

Notes:

i. All the above benefits are as per the current tax laws as amended by the Finance Act, 2005. ii. The current position of tax benefits available to the company and to its shareholders is provided for

general information purposes only. In view of the individual nature of tax consequences, each investor is advised to consult his/ her own tax advisor with respect to specific tax consequences of his /her participation in the issue.

iii. The tax benefits listed above are not exhaustive and are based on information explanations and representations obtained from the Company and on the basis of our understanding of the business activities and operations of the company. While all reasonable care has been taken in the preparation of this opinion, M. P. Chitale & Co. accepts no responsibility for any errors or omissions therein or for any loss sustained by any person who relies on it.

iv. Unless otherwise specified, sections referred to are sections of the Income Tax Act, 1961 (the Act). M. P. Chitale & Co Chartered Accountants Place: Mumbai Date: January 25, 2006

22

VII. ABOUT THE ISSUER COMPANY INDUSTRY OVERVIEW Housing is the one of the basic needs for every human being. Housing is an important component and a measure of socio–economic status of the people. It is regarded as a critical sector in terms of policy initiatives and interventions. The relevance of housing as a social need is long recognized and has therefore influenced the policy making at different levels, viz. national, state and local levels. This is reflected in the efforts of the Government undertaken to improve the housing and habitat conditions by way of financial allocations in the Five Year Plans and fiscal measures related to housing announced in the Union Budgets. In India, housing is basically a state level activity though the central government is responsible for the formulation of a broad policy framework for the housing sector and overseeing the effective implementation of the same. The importance of the housing sector can be judged by this fact that we consider house as the best investment and want to invest our hard earned money or saving in house. Current Scenario Housing India’s total population of 102.86 crore as per Census of India, 2001, consists of 19.20 crores households residing in 18.72 crores housing units. It may be observed therein that the average number of persons per house in urban area has declined continuously from 6.06 in 1951 to 5.50 in 2001. On the contrary, the scenario in rural sector has been somewhat fluctuating. The figure was 5.52 in 1951, which increased to 6.03 in 1981, but declined to 5.50 in 2001. Occupancy i.e., the number of persons per house, in both the urban and rural areas has become almost equal by 2001. The percentage of pucca houses in urban areas increased from 64.0 percent in 1971 to 74.8 percent in 2001, whereas the percentage of semi-pucca and kutcha houses in the urban areas has declined during this period. The percentage of pucca houses in rural areas increased from 18.5 percent in 1971 to 35.4 percent in 2001. In absolute terms the number of pucca houses in rural areas has increased from 33.34 million units in 1991 to 47.48 million by the year 2001. This implies that use of permanent building materials for the construction of walls and roofs is becoming more popular in rural areas also. The tendency to own a house has shown an increasing trend among the urban households. The percentage of houses owned by the rural households is above 95 percent. A percentage wise tenure status in urban and rural areas are given below:

Particulars 1961 1971 1981 1991 2001 Urban Owned 46.2 47.1 53.5 65.9 71.5 Rented 53.8 52.9 46.5 34.1 28.5 Rural Owned 93.6 93.8 93.0 94.5 95.4 Rented 6.4 6.2 7.0 5.5 4.6

Source: Census of India

Housing Finance The Housing Finance Companies (HFC) have stepped up their lending over the years contributing significantly to the growth of the housing sector, however they are still far from realising their full potential. Their strength lies in their specialised set of skills in lending exclusively for housing. The performance of the HFCs in recent years has been overshadowed by the competing banking sector with aggressive lending abilities, the relatively high cost of funds, higher regulatory capital requirement and lower degree of penetration in terms of geographical presence and market segments of the HFCs. Till June 30, 2004 there were 45 HFC’s registered with NHB. The Indian housing finance sector (the sector) is crowded with players of all sizes and nature ranging from government organisations, insurance companies, banks, housing finance companies and co-operative organisations

23

like HUDCO and NHB to others. Major players in the Industry are HDFC, LIC Housing Finance, Dewan Housing, Can Fin Homes, SBI Home Finance and Gujarat Rural Housing. Though the sector has been witnessing increased competition, there is scope for contribution from all institutions active in housing finance. Cost of funds notwithstanding, efficient customer servicing is emerging as the cutting edge in the industry. The sector has witnessed increased awareness among the borrower community about the industry practices and there are increased expectations about transparency and information disclosures from the perspective of depositors as well as borrowers. With these developments, the market is expected to mature further with the businesses becoming more robust and stable. The housing finance companies have also been resorting to securitisation as a measure to improve their Liquidity, Capital Adequacy, and better Asset-Liability Management. As a funding source, the HFCs have availed refinance from NHB, mostly under the Liberalised Refinance Scheme (introduced by NHB with effect from April 2002) customized to the market demand. The aggregate housing loans outstanding (comprised of housing loans outstanding of HFCs, Banks, and Co-operative Sector) as on March 31, 2004 was 153219.12 crores. The graphical break of the same is as below:

0100002000030000400005000060000700008000090000

2001 2002 2003 2004

Years

(Rs.

Cro

res)

HFCsBanks Cooperative Sector

Source: Report on Trends and Progress of Housing in India – June 2004 The aggregate outstanding housing loans of HFCs, which were Rs.49,238 crores as on March 31, 2003 increased by 20.1 per cent and stood at Rs.59,111 crores as on March 31, 2004. Term wise housing loans outstanding of HFCs for 2003-2004 is given below: (Rs. Crores)

Term of Housing Loans 2002-2003 % of total 2003-2004 % of total Upto 1 year 2695.31 5.5% 4089.14 6.9% 1 to 3 Years 4670.82 9.5% 7849.98 13.3% 3 to 5 Years 4510.48 9.2% 6839.28 11.6% 5 to 7 years 4620.91 9.4% 4910.42 8.3% Above 7 years 32740.45 66.5% 35422.62 59.9% Total 49237.97 100% 59111.44 100%