German tax policy update September 2015 - EYFile/EY_G… · Legislation On 22 July 2015, the German...

13

German tax policy update September 2015 2015 Issue 3 German Tax & Legal Quarterly 3|15 Legislation After parliamentary summer recess, German tax policy makers have an ample agenda to work on in the remainder of 2015. The first bill to be completed by October 2015 is the Tax Amendment Act 2015 (Steueränderungsgesetz 2015), formerly known as the bill regarding amendments to various tax laws (Proto- kollerklärungsG). Its main content as proposed by Government is expected to remain unchanged (extension of the “group exemption” from the change- in-ownership rule) or to be only slightly amended (e.g. limitation regarding non-share considerations in certain group reorganizations or changes in the real estate transfer tax act). However, Parlia- ment has added more than 20 further single issues to the bill, many of a mainly technical nature. We would like to highlight the following expected additional changes: Content 01 Legislation 05 German tax authorities 06 German court decisions 09 Spotlight 11 EY publications and events • Real estate transfer tax: In a swift reaction to a recent decision of the Federal Constitu- tional Court, the valuation rules are changed for cases in which no consideration is paid (relevant for group reorganizations; for further details and recommendations, please see our specific article on the substitute assessment basis below). • Extension of the rules on the roll-over relief for reinvestments in certain assets: The old regulation required a newly acquired replacement asset located in Germany. As the European Court of Justice (ECJ) decided that this was against EU law, Germany will allow spreading the payment of the tax on the hidden reserves of the replaced asset to five equal instalments if the replacement asset is located in the EU or EEA. • VAT: new provisions on VAT taxation of public-sector corporations.

Transcript of German tax policy update September 2015 - EYFile/EY_G… · Legislation On 22 July 2015, the German...

German tax policy update September 2015

2015 Issue 3

German Tax & Legal Quarterly 3|15

Legislation

After parliamentary summer recess, German tax policy makers have an ample agenda to work on in the remainder of 2015. The first bill to be completed by October 2015 is the Tax Amendment Act 2015 (Steueränderungsgesetz 2015), formerly known as the bill regarding amendments to various tax laws (ProtokollerklärungsG). Its main content as proposed by Government is expected to remain unchanged (exten sion of the “group exemption” from the change in-ownership rule) or to be only slightly amended (e.g. limitation regarding nonshare considerations in certain group reorganizations or changes in the real estate transfer tax act). However, Parliament has added more than 20 further single issues to the bill, many of a mainly technical nature. We would like to highlight the following expected additional changes:

Content

01 Legislation

05 German tax authorities

06 German court decisions

09 Spotlight

11 EY publications and events

• Real estate transfer tax: In a swift reaction to a recent decision of the Federal Constitutional Court, the valuation rules are changed for cases in which no consideration is paid (relevant for group reorganizations; for further details and recommendations, please see our specific article on the substitute assessment basis below).

• Extension of the rules on the rollover relief for reinvestments in certain assets: The old regulation required a newly acquired replacement asset located in Germany. As the European Court of Justice (ECJ) decided that this was against EU law, Germany will allow spreading the payment of the tax on the hidden reserves of the replaced asset to five equal instalments if the replacement asset is located in the EU or EEA.

• VAT: new provisions on VAT taxation of public-sector corporations.

Legislation

The inheritance tax reform is extremely important especially for German family businesses. The objective of the reform is to adjust business relief provisions to a decision of the Federal Constitutional Court of December 2014. Government officially plans to finish the process by late November 2015, but difficult negotiations between Conservatives and Social Democrats could cause substantial delays.

The Federal Ministry of Justice is expected to present a proposal on an adjustment of the current rules regarding the discounting of provisions for commercial law purposes. The currently applicable interest rate is calculated as a seven-year average and the governing coalition is in general willing to stretch this period to approximately 12 years to reduce the impact of the low interest environment on companies’ balance sheets.

With the presentation of the final OECD BEPS reports, domestic BEPS implemen-tation will be on the German tax policy agenda as of October 2015. Officials of the Federal Ministry of Finance have announced the need for law changes regarding action points 2 (hybrid mismatch), 13 (country-by-country reporting) and 15 (multilateral instrument). It remains to be seen what additional issues might be added during the upcoming discussion. One such item could be a measure against “patent boxes” (similar to the one established in Austria, where deductibility of intercompany royalties is linked to the recipient being subject to a minimum tax level) as proposed by the state of Hesse. According to this proposal, royalties paid to any group affiliate should only continue to be deductible as an expense in Germany if such payments are subject to effective taxation comparable to the German level of taxation.

Furthermore, Germany is implementing all necessary legislation concerning the upcoming automatic exchange of financial account information for tax purposes. Several bills to regulate the information exchange with EU and certain non-EU countries are on their way to allow information collection according to the OECD Common Reporting Standard as of 2016 and information exchange as of 2017.

In recent months, the German Government has released a few domestic implementation laws on double tax treaties (DTT). This concerns e.g. the new or newly amended DTTs with China, France and the UK.

• With respect to the new DTT between Germany and China, the legislative process will probably not be finished before December 2015. According to the specific provisions of this treaty, the new DTT would thus not be applicable before January 2017. The new treaty e.g. reduces the withholding tax rate on qualifying dividends from shareholdings of at least 25% from 10 to 5%.

• The amended DTT with France rewrites the article on capital gains (introducing e.g. a rule for shares in companies with assets consisting mainly of real estate), restricts the application of the reduced withholding tax rate on dividends from certain investment funds and implements new provisions on cross-border workers.

• The amendment of the DTT with the UK includes the “Authorized OECD Approach” (AOA) on the allocation of income to permanent establishments and changes the taxation right of certain locally hired people.

• In August, Germany and Japan initialed a new DTT which eliminates withholding tax on dividends, interest and royalties if certain requirements are met, and introduces the “Authorized OECD Approach” (AOA). If both countries sign the treaty in early 2016, application as of January 2017 is a possibility.

Update on double tax treaties with China, France, the UK and Japan

EY German Tax & Legal Quarterly 3.15 | 2

Legislation

On 22 July 2015, the German Federal Ministry of Finance issued a discussion draft bill for the Investment Tax Reform (Investment-steuerreformgesetz). The draft contains a revised version of Sec. 8b (4) Corporate Income Tax Act in view of a planned taxation of capital gains from portfolio shareholdings (i.e., shareholdings under 10%). In addition, the draft aims to completely overhaul the German fund tax regime for mutual funds and to amend the treatment of socalled special funds (funds that can only have up to 100 investors not being individuals).

Highly relevant for a number of corporate taxpayers with portfolio investments is the discussed extension of the taxation of dividends from such shareholdings to include capital gains. That is, the general 95% tax exemption for capital gains derived by corporate taxpayers from the sale of shares would no longer be applicable if the sold shares represent a participation of less than 10% (“portfolio shareholding”). As with the current rules regarding portfolio dividends, the new draft rules also refer to the beginning of the respective calendar year for the classification as portfolio shareholding. However, the current practice of referring back additional purchases made in the course of the year to the beginning of the year would be abandoned: Unlike before, dividends and capital gains would generally be subject to tax even if the shareholding is increased to 10% or above through purchases made during the year.

Any losses resulting from the sale of portfolio shareholdings could only be offset with profits from portfolio shareholdings (dividends and capital gains) as well as any profits from taxable write-ups (separate loss offset regime).

The taxation of capital gains from portfolio shareholdings would only be applicable for profits generated from 1 January 2018. After the transitional period, any hidden reserves realized through the sale of portfolio shareholdings would then be subject to taxation, even if they include gains that would not have been subject to taxation under the current regulation. Consequently, taxpayers should now start to analyze their shareholding portfolios and review their investment and dividend policies.

Moreover, the draft discussion paper covers in particular the following amendments for investment funds:

• An equal treatment of German dividend withholding tax for German and foreign investment funds (to close down any potential argument in view of EU protective claims),

• Closedown of certain taxadvantaged investment opportunities for German corporate investors by investing into tailormade (special) investment funds, and

• Introduction of a lumpsum annual taxation for mutual funds (upfront taxation for the German individual investors) without the possibility to obtain a transparent tax status any longer. Such lumpsum upfront taxation is to a certain extent similar to the current lump sum taxation for non-transparent funds, but with a significantly lower lump-sum tax base.

The changes regarding investment funds would under the current draft only become applicable as of 1 January 2018. As these proposals are highly controversial, it is as yet unclear whether the proposals will eventually become law as proposed or whether changes will be made.

Investment tax reform: Draft bill suggests taxation of capital gains from portfolio shareholdings and amendments for investment funds as of 2018

EY German Tax & Legal Quarterly 3.15 | 3

EY German Tax & Legal Quarterly 3.15 | 4

Legislation

Under a German government draft bill, data privacy breaches are to be combatted more effectively. Consumer protection associations are to be given the right to sue companies for infringements of data privacy, although this will only apply in the context of advertising (e.g. personality profiles). Especially companies using consumers’ data for advertising purposes should review their privacy policies and their websites as under future legislation, the use of cookies may be viewed more critically.

The “Act on Improving Enforcement of Consumer Protection Regulations under Data Protection Legislation” (Gesetz zur Verbesserung der zivilrechtlichen Durchsetzung von verbraucherschützenden Vorschriften des Datenschutzrechts) (also referred to as “Verbandsklagegesetz” or “Associations’ Right of Action Law”, draft bill 18/4631) is planned for the end of 2015 and will give associations the right to take legal action against companies’ infringements of data privacy. Until now, this has been a matter for the supervisory authorities, who have been rather reluctant to act. Going forward, consumer protection associations will be entitled to issue a cease-and-desist warning, file for an interim injunction, or seek other injunctive relief. The Federation of German Consumer Organisations (Bundesverband Verbraucherzentrale) has already announced that it intends to clarify basic issues relating to data privacy law. This will include the protection of the personal data of minors, as well as scoring and the deletion of consumer data.

Under today’s laws and under the new Act, data privacy breaches occur, for instance, when certain uses of data are not covered by the original declaration of consent, or if companies use tools on their own website to identify users without requesting their consent. This includes e.g. the use of cookies, data analysis programs such as Google Analytics, or other methods such as browser fingerprinting. If a company’s use of these tools violates data privacy law, an interim injunction could result in the obligation to take the entire website offline with immediate effect.

In addition, companies can also face significant financial risks because the amounts in dispute attributed to data privacy infringe-ments could be high, which in turn would automatically increase the court costs. Coupled with widespread negative reporting in the media and the ensuing reputational damage, a breach of data privacy could thus do considerable harm to a company.

What companies need to observeCompanies may need to amend both their consent procedures and the notice they give under data privacy law. Typical issues include complex data analysis techniques applied in the use of social media tools or in ecommerce operations for consumers, the documentation and implementation of arrangements for deleting data as well as data transfers to third parties or to the company’s affiliates. As the time limits set in cease-and-desist warnings are very short (normally no longer than two weeks), companies should be prepared to reply swiftly to data privacy inquiries from consumer protection associations.

Under current regulations, a German-based company is required to appoint a Data Protection Officer (DPO) to assure compliance with data privacy laws if at least 10 employees can access personal data by automated processing (i.e., computer access to personal data of employees and/or customers). The DPO serves as a facilitator supporting the company and as the contact point for any inquiries by data protection authorities. If no DPO has been appointed by qualifying companies, this should be done as soon as possible. The appointed DPO can also be an external expert, which may be favorable in certain cases (reasons can include qualifications, employment law/ protection against dismissal and cost).

EU General Data Protection Regulation (GDPR)The future EU General Data Protection Regulation is also expected to provide for an associations’ right of action, enabling consumer protection associations to take legal steps against data privacy breaches. This would then invalidate existing German regulations after expiration of a transitional period.

The Council of EU Ministers of Justice agreed in June 2015 on a draft GDPR. Consultations are currently being held between the EU Council, Parliament and Commission. A final version is planned for the end of this year.

To prevent misuse of the associations’ right of action, the current draft includes inter alia a stipulation that any institutions, organizations or associations bringing action in this context must be “acting in the public interest”.

Data privacy law: Consumer protection groups to be given associations’ right of action in data privacy infringements

German tax authorities

From a practical point of view, the differentiation between ordinary corrections of e.g. a mistake in a tax filing according to Sec. 153 German General Tax Code (GGTC) and voluntary self-disclosures exempting from punishment according to Sec. 371, 378 (3) GGTC has become more and more important in the last couple of years. To provide more clarity, the German Federal Ministry of Finance issued a draft version for discussion purposes (Vorläufiger Diskussionsentwurf AEAO zu § 153 AO – Abgrenzung einer Berichtigung nach § 153 AO von einer strafbefreienden Selbstanzeige nach § 371 AO) on 14 July 2015.

What are the main risks? The tax authorities tend to regard ordinary (subsequent) corrections of tax filings as voluntary self-disclosures in particular where comparably high tax amounts are to be corrected or if the respective type of tax is not subject to regular interest payments, such as advance VAT returns or wage tax. The assumption of willful or intentional behavior is often governed by financial reasons as this classification opens the possibility of assessing tax evasion interest of 6% p.a. or – as a consequence of the stricter requirements for voluntary self-disclosures – a lump-sum surcharge on the “evaded” tax (if over EUR 25,000) of 10% to 20%.

Even though official guidance is only binding for tax authorities and not for tax courts or tax criminal courts, the intended clarifications should have a positive influence on the general practice of the tax authorities and open room for argumentation by the taxpayer. The issued draft provides a very detailed overview of the legal prerequisites of an ordinary correction according to Sec. 153 GGTC and a voluntary self-disclosure according to Sec. 371, 378 (3) GGTC. Some clarifications are very useful in practice. For example, the mere fact that a high amount of taxes is to be corrected or the fact that corrections are filed for a number of years cannot by itself justify the assumption of tax criminal relevance. Furthermore, the draft emphasizes the relevance of internal control and tax compliance systems for companies. The existence of a functioning compliance system should be regarded as evidence that no willful or grossly negligent act has been committed. However, all circumstances of each individual case have to be taken into consideration.

Another important issue addressed in the draft is the practical question after how much time the taxpayer has to file a correction according to Sec. 153 GGTC. As stated in law, this needs to happen with undue delay. The draft does not define a clear time span in this regard, but provides guidance with practical examples.

The proposal is still under review and the issuance of the final version has not been scheduled so far.

On 20 August 2015, the German Ministry of Finance (MOF) issued a decree according to which not only a German atypical silent partnership cannot itself be a CIT tax group parent, but the existence of atypical silent partnerships would also deny the availability of a CIT tax group membership to issuers of such silent partnership instruments. Grandfathering may be granted to structures already in place on 20 August 2015. An atypical silent partnership is a specific German tax classification of a special form of profit-participating loan, where broadly speaking the lender (silent partner) not only shares in the return on the underlying investment/business, but also has up- and downside participation, and some information rights that are similar to those of a limited partner in a limited partnership. The atypical silent partnership therefore is treated as a partnership between issuer and silent partner (rather than a debt instrument) also from a tax perspective. These instruments are not uncommon in the German market, and hence the potential impact of the new federal tax authority guidance (which replaces previously existing local guidance with a similar view) should not be underestimated. In particular in M&A situations, it needs to be ensured that atypical silent partnership structures at German target level are identified and terminated before a new tax group with an acquiring entity can be established.

Ordinary correction or voluntary self-disclosure? Discussion draft by the German Federal Ministry of Finance

Germany denies tax group benefits for entities that enter an “atypical silent partnership”-structure

EY German Tax & Legal Quarterly 3.15 | 5

EY German Tax & Legal Quarterly 3.15 | 6

German court decisions

The sale of a whole business or of a separate business unit is out of scope of VAT if it qualifies as a transfer of a going concern (TOGC). In this respect there must be a business or business unit that is carried on by a successor. Whether an individual case qualifies depends on the specific circumstances.

In the underlying case of the German High Court judgment dated 4 February 2015 (XI R 14/14), several separate legal entities cooperated in performing old age retirement home services. These entities sold their assets used for such services to another acquiring group of entities. The first instance court concluded that the sales of the various entities shall be looked upon from a group perspective and therefore concluded that each entity’s sale may therefore qualify as TOGC because seen from the group’s perspective, the old age retirement home service business was transferred as a whole. In contrast to that, the Federal High Court revised this judgment and ruled by decision XI R 14/14 that for the application of the TOGC provision, only the individual bilateral transaction must be considered. This meant for the claimant in the particular case that its sale of movable assets did not qualify as TOGC, even though from a group perspective it was part of a complete business transfer to another group of entities that continued operating the selling group’s business.

Products can already be considered defective in the sense of the German Product Liability Law (Produkthaftungsgesetz) if they belong to a group of products with potential defects. This means that in case of complaints the respective manufacturer is obliged to take back and replace all the products of such a lot even if the actual product itself is not defective. This consumer-friendly judgment has recently been rendered by the German Federal High Court (court decisions of 9 June 2015 - VI ZR 327 / 12 and 284/12) after the European Court of Justice (ECJ) had rendered corresponding preliminary rulings on 5 March 2015 (C-503/13 and C-504/13).

During standard quality checks, a manufacturer of cardiac pacemakers and implantable defibrillators found irregularities in one lot of pacemakers as well as in one lot of defibrillators, resulting in an increased frequency of errors. For the lots concerned, the manufacturer recommended exchanging any pacemakers and switching off a certain function of the defibrillators. Even though the actual defect of three patients’ pacemakers was not proven, they were exchanged. Subsequently, the health insurance companies of the three patients claimed reimbursement of the medical expenses incurred in connection with the exchange of the pacemakers.

As the product liability law is based on European provisions, the German Federal High Court asked the ECJ for a preliminary ruling:

1. Is a product, in this case a medical device implanted in the human body, already defective if the products in the same product group have a significantly increased risk of failure, but a defect has not been detected in the device which has been implanted in the specific case in point?

2. If the answer to the first question is “yes”: Do the costs of the operation to remove the product and to implant another pacemaker or another defibrillator constitute damage caused by personal injury in the meaning of the product liability law?

TOGC for VAT purposes – only the bilateral perspective between seller and purchaser counts

Damage claim for potential defects – liability for replacing or taking back all products within a lot can arise even if only very few products are found to be defective

German court decisions

The ECJ answered in favor of the users, in this case the patients. According to the EU Product Liability Directive, a product is seen as defective when it does not provide the safety a user is entitled to expect. Given the function of pacemakers and defibrillators and the particularly vulnerable situation of patients using such devices, patients are entitled to expect particularly high safety levels. With regard to the abnormal potential for damage for the persons concerned it is justified to classify all the products in the lot as defective without there being any need to show that the product in question is defective. The ECJ also made clear that the compen-sation for damage in this connection relates to all that is necessary to eliminate harmful consequences and to restore the level of safety which a person is entitled to expect. In order to protect consumer health and safety, the notion of “damage caused by death or personal injuries” within the meaning of the directive must be interpreted broadly.

The Federal High Court followed the decisions of the ECJ and ordered the manufacturer to pay damages in the case of the exchanged pacemakers. With regard to the defibrillators some other questions were still open. Therefore, the case was remitted to the court of appeal.

The decision leads to a considerable extension of the manufacturers’ liability according to product liability law. However, the decisions refer explicitly to medical devices and the potentially serious damage to the patients’ health so that this decision is probably currently only applicable to this product group.

However, the reasoning of the ECJ on the basis of the “abnormal potential for damage for the persons concerned” also applies to many other product groups. Unfortunately, the opinion of the court does not contain more detailed explanations with regard to the question when the mere risk of a defective product is sufficient for a damage claim according to the product liability law.

In its decision of 15 April 2015 (2 K 66/14), the local tax court of Hamburg held that an Austrian investor in a German partnership is entitled to benefit from the rules on tax-neutral contributions into a German corporation. Under the German reorganization tax act in its version valid until 2006, the German reorganization tax act provided for the option to tax-neutrally contribute partnership interests into a corporation against new shares in that corporation. Under these rules, the new shares could be sold tax free after a 7-year waiting period. Capital gains taxation was not triggered by the contribution as long as both the receiving entity (with respect to the underlying assets) and the former partner (with respect to the shares received as consideration) took over the book value of the assets thus indirectly transferred. However, the application of these rules required that the assets of the partnership as well as the new shares were subject to German corporate tax law after the transaction. In the case at hand, two Austrian-based corporations contributed their partnership interests into a German GmbH against new shares in that entity. As the double tax treaty (DTT) Germany-Austria allocated the taxing right for the newly received shares in the GmbH to Austria, the conditions for a tax-neutral contribution were not met. The case was brought before the local tax court of Hamburg, which referred the question whether the immediate capital gains taxation was a discriminatory treatment of the Austrian investors, in particular with respect to the European Court of Justice’s (ECJ) exit tax case law, to the ECJ. In its answer to the referred questions, the ECJ applied, quite surprisingly, the free movement of capital principle and held that for purposes of justification of the differential treatment, Member States are allowed to apply immediate capital gains taxation if the built-in gains in the transferred interests were not subject to German taxation after the contribution. The local tax court of Hamburg has now rendered its decision in the case stating that the condition of maintaining Germany’s taxing right in the transferred interest was actually met.

Due to a law change in 2006, the shares received as consideration are no longer required to be subject to German corporate taxation. Moreover, EU-/EEA-based investors are explicitly admitted to tax-neutral reorganizations involving the contribution of an interest in a German partnership. However, thirdcountry investors (e.g. from the US or Switzerland) are, according to the wording of the law, not covered by the rules on tax-neutral contributions. As the scope of the free movement of capital principle, which was invoked by the ECJ, covers third-country situations, the decision of the ECJ and subsequently the Hamburg local court should be of interest to third-country investors holding interests in German partnerships. However, this requires that Germany cannot rely on the so-called stand-still clause, which protects discriminatory rules being in place as of 31 December 1993 from being held inapplicable under the free movement of capital principle. It remains to be seen whether the law changes to the rules providing of a tax-neutral contribution of specific types of assets have changed the character of the rule to such an extent that invoking the stand-still clause is not possible for Germany.

Local tax court of Hamburg decides in an exit tax case – potential relevance for third-country investors in German partnerships

EY German Tax & Legal Quarterly 3.15 | 7

German court decisions

Real estate transfer tax (RETT) is not only triggered upon a direct acquisition of real estate, but also in the event of an indirect acquisition of real estate, i.e. if real estate is held through a partnership or a corporation. The assessment basis in the event of a direct acquisition of real estate is the consideration, e.g. the purchase price. However, an indirect acquisition of real estate held through a partnership or a corporation relies on a specific valuation method stipulated in the German Valuation Act to determine the value of the real estate which then represents the RETT assessment basis (the so-called “substitute assessment basis”). In most practical cases, this substitute assessment basis is significantly lower than the fair market value of the real estate.

In its decision dated 23 June 2015, the Federal Constitutional Court held that this substitute assessment basis violates the constitutional principle of equal taxation (1 BvL 13/11, 1 BvL 14/11). The court reasons that the value resulting from the substitute assessment basis differs significantly not only in average but also in many individual cases from the value of the regular assessment basis, which in most cases reflects the fair market value. This discrepancy is not consistent with the principle of equal taxation required by the German Constitution.

Consequently, the court imposed on the German legislator the obligation to remedy this discrimination by passing new provisions for the substitute assessment basis no later than 30 June 2016. While these new provisions have not been finally enacted at this point in time, the latest draft of the Tax Amendment Act 2015 (Steueränderungsgesetz 2015), which is to be completed by October 2015, suggests that the substitute assessment basis will be amended in a way that it reflects the fair market value of the real estate involved in the taxable transaction. In practice, this will mostly result in an increase of the tax basis compared to the current rules.

The new rules shall have retroactive effect from 1 January 2009. The current rules governing the substitute assessment basis remain applicable only for taxable transactions prior to 1 January 2009. Nevertheless, in our view there are good arguments that – for protection of taxpayers’ trust in the applicability of the old rules – only RETT assessment and valuation assessment notices issued after 23 June 2015 should be affected by the decision of the German Constitutional Court. The reason for our view is that, according to German tax law, a cancellation or amendment of an existing tax assessment may not be made to the taxpayer’s disadvantage if the Federal Constitutional Court determines the invalidity of a law or states that the law violates the constitution.

Taxpayers who have carried out or are intending to carry out transactions that trigger RETT subject to the substitute assessment basis should review the potential impact on the relevant RETT assessment notices.

• No action should be required with regard to RETT assessment notices and valuation assessment notices issued in relation to transactions that occurred between 1 January 2009 and 23 June 2015 which have already become non-appealable and which do not have to be amended in accordance with other procedural or material reasons.

• Taxpayers who recently received a request to file a return on the substitute assessment basis from the tax office (and where no RETT return has been filed so far) should discuss with the tax office whether the assessment procedure shall be continued or whether it shall be set on hold until the legislator has passed the new law.

• Whether objections against existing RETT assessment or valuation assessment notices should be filed should be considered carefully, taking these recent developments into consideration. In cases where an appeal against a RETT assessment or valuation assessment notice is currently pending, it should be carefully analyzed whether the appeal should be withdrawn.

For many types of transactions, in particular the acquisition of partnerships or corporations that own real estate, the new rules as currently drafted in the Tax Amendment Act 2015 (Steueränderungsgesetz 2015) would result in an increase of RETT to be paid. This also implies that the recent decisions of the Federal German Tax Court holding that for income tax purposes RETT is deductible in these transactions will gain even more practical importance.

Real estate transfer tax: Substitute assessment basis is declared unconstitutional

EY German Tax & Legal Quarterly 3.15 | 8

Spotlight

The tax authorities of a large number of countries, led and supported by the G20, have been stepping up the exchange of information among each other for some years now. In principle, this exchange is intended to facilitate and ensure taxation in the individual countries. Every company with international business should now be familiar with the fact that tax audit notes relating to expenses reported by a taxpayer are routinely sent to the tax office of the expense recipient and that information relating to investment income is exchanged.

A new approach is currently being pursued by Australia, Germany, France, the UK, Japan and Canada (the so-called “E-6” group). These countries and their respective tax authorities have agreed in a non-bureaucratic manner — i.e., without intergovernmental agreements — to exchange extensive information relating to multinational companies in the digital sector. Regardless of whether it relates to current taxation in the participating countries, all information which could provide insight into the entire business models of the companies concerned and their structures is exchanged. This also includes information relating to the current taxation of the company in the respective country providing the information.

What is the problem?The distribution of nonpublic information by certain tax authorities to third parties is not necessarily permitted among all countries. In Germany, for example, tax secrecy laws protect the taxpayer’s data, and noncompliance is punishable under law. In Germany, tax secrecy is based on the view that the taxpayer can be reasonably expected to disclose confidential information only if he or she can rely on it being treated confidentially by the tax office. The data to be disclosed may also include trade secrets such as transfer prices between group companies.

Noncompliance with tax secrecy laws for the purpose of exchanging information with foreign countries is permissible — along with other requirements — only if this is necessary for taxation abroad. While the tax authorities do not have to perform their own comprehensive audit under foreign law before submitting the documents, they must still establish whether the documents to be submitted are at all relevant for taxation abroad. Based on consistent precedents set by the German courts, inquiries that resemble mere “fishing expeditions” or that are not relevant in relation to overseas taxation are not permitted. A first cautionary example can be taken from the ongoing interim relief proceedings conducted by EY before the tax court of Cologne.

Increasing information exchange between countries – interim relief

EY German Tax & Legal Quarterly 3.15 | 9

Spotlight

The claimant is a German company (the Company) within an international group, operating in the digital economy. The Company has no business relationships or other points of contact with the countries participating in the E-6 exchange of information. The Company was informed that information relating to group structures, tasks and remuneration at the individual group companies, as well as the resulting taxation and any specific features, would be passed on to the other countries in the E-6 group. The Company did not receive any further explanation as to which specific information is to be shared in this regard.

During the administrative procedure, the Company was denied access to any of the files of the tax office and was thus unable to determine the scope of the information to be exchanged. The Company was able to acquire access to the file only after it had applied for a preliminary injunction from the tax court of Cologne. The file to be shared included 16 pages of preliminary information. The documents also revealed that additional specifically predefined requests, and additional related notifications are to be made after the preliminary information has been submitted.

The material to be exchanged contained information relating to tax matters dating back many years, as well as inaccurate assumptions made by tax officials in prior tax field audits, which had been rejected by the tax authorities a long time ago. Information was clearly not compiled on the basis of current relevance and accuracy.

It could not be identified which specific tax situation(s) in the other countries the information could be relevant for. Indeed, if the information had been relevant for taxation in other countries, the information to be submitted should have been checked for its relevance for the respective recipient country. The submission of identical data to all countries — imminent in the case at hand — suggests that no such relevance assessment had taken place.

The objective of the current exchange of information apparently lies in achieving a better understanding of companies’ business models and structures in general, as opposed to tackling any specific perceived case of abuse. Based on the information exchanged, the countries intend to prepare studies and related suggestions for the adjustment of applicable tax regulations.

In the ongoing proceedings, the Federal Central Tax Office was therefore able to make only a blanket assertion that the documents were likely to be relevant for taxation abroad. It did not provide a substantiated justification. Such a blanket assertion may not provide sufficient cause to justify the exchange of documents with other countries.

For German taxpayers, if there is a threat (or indication) of an exchange of information, an application for a provisional injunction can be made immediately. Otherwise, there will be the threat of an irreversible violation of the right to preservation of tax secrecy. Once information has been submitted, the situation can no longer be reversed.

What is next?The exchange of information within the European Union will expand in the future, with proposed amendments to the EU Mutual Assistance Directive for the automatic exchange of tax rulings. According to the proposed amendments, rulings issued by the German tax authorities are to be submitted automatically to other Member States, despite the fact that the situation to which the application for a ruling relates frequently contains sensitive information such as trade secrets. Germany and the Netherlands also recently signed a Memorandum of Understanding to spontaneously exchange tax rulings regardless of the expected amendment to the EU Mutual Assistance Directive.

This development impacts all companies operating in more than one EU Member State, regardless of sector or business model. For this reason, it is not just companies in the digital sector that should monitor developments relating to the exchange of information and the resulting consequences for their companies.

EY German Tax & Legal Quarterly 3.15 | 10

EY publications and events

Please find pdf-versions of the EY publications listed below by clicking on the related picture. The free EY Global Tax Guides app provides access to our series of global tax guides. www.ey.com/GL/en/Services/Tax/Global-tax-guide-app

Worldwide Personal Tax GuideIncome tax, social security and immigration 2014–15

Upcoming EY events

Worldwide corporate tax guide (2015 edition) The worldwide corporate tax guide summarizes the corporate tax systems in 161 jurisdictions.

Worldwide personal tax guide (2014-15 edition) The worldwide personal tax guide summarizes the personal tax systems and immigration rules for individuals in more than 160 jurisdictions.

Worldwide VAT, GST and sales tax guide (2015 edition) Inside this guide you will find extensive details of valueadded tax, goods and service tax and sales tax systems of 114 jurisdictions.

Year-end tax conferences

Tax controversy conference - roadshow

Human capital round table “Cross-border assignments”

• Review and outlook on developments in German tax law: New legislation, important tax court decisions and views of the German tax authorities In Duesseldorf, Hamburg, Frankfurt, Munich and Stuttgart, we plan to precede the year-end tax conference with a half-day update on the final OECD BEPS proposals.

Language: GermanDate and location: Berlin 11/12 November 2015Bremen 26 November 2015Cologne 08 December 2015Dortmund 25 November 2015Dresden 09 December 2015Düsseldorf 30 November 2015Frankfurt (Eschborn) 08 December 2015Freiburg 26 November 2015Hamburg 11 November 2015Hanover 02 December 2015Jena 01 December 2015Leipzig 03 December 2015Munich 24 November 2015Nuremberg 25 November 2015Ravensburg 08 December 2015Saarbrücken 01 December 2015Stuttgart 26 November 2015Villingen-Schwenningen 24 November 2015Event contact: Nico Schönberg, [email protected]

• Current hot topics in tax controversy – Report on experiences from recent tax audits and discussion of real cases with detailed industry-specific know-how regarding the tax authority approach

Language: GermanDate and location: 21 October 2015 in Stuttgart, 29 October 2015 in DüsseldorfEvent contact: [email protected]

• Current topics related to human capital related issues of cross-border assignments

Language: GermanDate: November 2015Location: Berlin, Hamburg, Hanover, StuttgartEvent contact: [email protected]

EY German Tax & Legal Quarterly 3.15 | 11

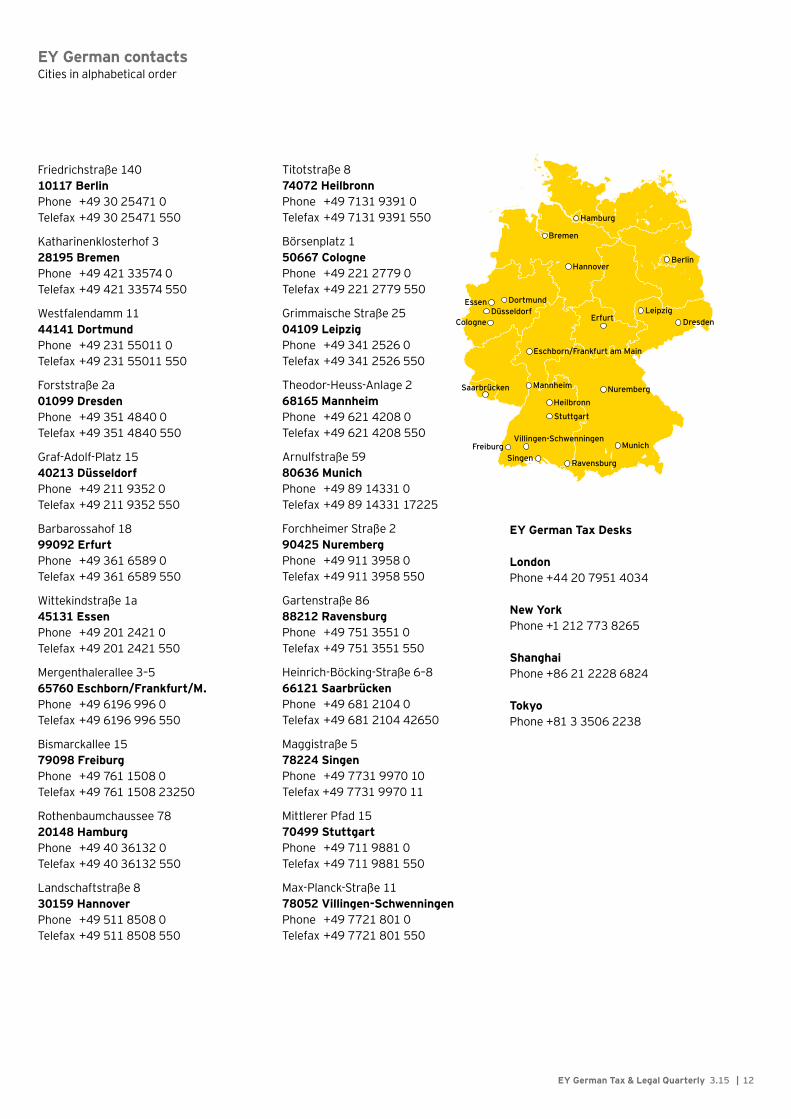

EY German contactsCities in alphabetical order

Hamburg

Bremen

Hannover

DortmundEssenDüsseldorf

Cologne

Eschborn/Frankfurt am Main

Mannheim

Heilbronn

Stuttgart

Saarbrücken

Freiburg Villingen-Schwenningen

Ravensburg

Munich

Nuremberg

Berlin

Leipzig Dresden Erfurt

Singen

Friedrichstraße 14010117 BerlinPhone +49 30 25471 0Telefax +49 30 25471 550

Katharinenklosterhof 328195 BremenPhone +49 421 33574 0Telefax +49 421 33574 550

Westfalendamm 1144141 DortmundPhone +49 231 55011 0Telefax +49 231 55011 550

Forststraße 2a01099 DresdenPhone +49 351 4840 0Telefax +49 351 4840 550

GrafAdolfPlatz 1540213 DüsseldorfPhone +49 211 9352 0Telefax +49 211 9352 550

Barbarossahof 1899092 ErfurtPhone +49 361 6589 0Telefax +49 361 6589 550

Wittekindstraße 1a45131 EssenPhone +49 201 2421 0Telefax +49 201 2421 550

Mergenthalerallee 3–565760 Eschborn/Frankfurt/M.Phone +49 6196 996 0Telefax +49 6196 996 550

Bismarckallee 1579098 FreiburgPhone +49 761 1508 0Telefax +49 761 1508 23250

Rothenbaumchaussee 7820148 HamburgPhone +49 40 36132 0Telefax +49 40 36132 550

Landschaftstraße 830159 HannoverPhone +49 511 8508 0Telefax +49 511 8508 550

Titotstraße 874072 HeilbronnPhone +49 7131 9391 0Telefax +49 7131 9391 550

Börsenplatz 150667 ColognePhone +49 221 2779 0Telefax +49 221 2779 550

Grimmaische Straße 2504109 LeipzigPhone +49 341 2526 0Telefax +49 341 2526 550

TheodorHeussAnlage 268165 MannheimPhone +49 621 4208 0Telefax +49 621 4208 550

Arnulfstraße 5980636 MunichPhone +49 89 14331 0Telefax +49 89 14331 17225

Forchheimer Straße 290425 NurembergPhone +49 911 3958 0Telefax +49 911 3958 550

Gartenstraße 8688212 RavensburgPhone +49 751 3551 0Telefax +49 751 3551 550

Heinrich-Böcking-Straße 6–866121 SaarbrückenPhone +49 681 2104 0Telefax +49 681 2104 42650

Maggistraße 5 78224 Singen Phone +49 7731 9970 10 Telefax +49 7731 9970 11

Mittlerer Pfad 1570499 StuttgartPhone +49 711 9881 0Telefax +49 711 9881 550

MaxPlanckStraße 1178052 Villingen-SchwenningenPhone +49 7721 801 0Telefax +49 7721 801 550

EY German Tax Desks

LondonPhone +44 20 7951 4034

New YorkPhone +1 212 773 8265

ShanghaiPhone +86 21 2228 6824

TokyoPhone +81 3 3506 2238

EY German Tax & Legal Quarterly 3.15 | 12

EY | Assurance | Tax | Transactions | Advisory

About the global EY organizationThe global EY organization is a leader in assurance, tax, transaction and advisory services. We leverage our experience, knowledge and services to help build trust and confidence in the capital markets and in economies the world over. We are ideally equipped for this task – with well trained employees, strong teams, excellent services and outstanding client relations. Our global purpose is to drive progress and make a difference by building a better working world – for our people, for our clients and for our communities.

The global EY organization refers to all member firms of Ernst & Young Global Limited (EYG). Each EYG member firm is a separate legal entity and has no liability for another such entity’s acts or omissions. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information, please visit www.ey.com.

In Germany, EY has 22 locations. In this publication, “EY” and “we” refer to all German member firms of Ernst & Young Global Limited.

© 2015 Ernst & Young GmbHWirtschaftsprüfungsgesellschaftAll Rights Reserved.

SRE 1509-482ED None

This publication contains information in summary form and is therefore intended for general guidance only. Although prepared with utmost care this publication is not intended to be a substitute for detailed research or the exercise of professional judgment. Therefore no liability for correctness, completeness and/or currentness will be assumed. It is solely the responsibility of the readers to decide whether and in what form the information made available is relevant for their purposes. Neither Ernst & Young GmbH Wirtschaftsprüfungsgesellschaft nor any other member of the global EY organization can accept any responsibility. On any specific matter, reference should be made to the appropriate advisor.

www.de.ey.com

PublisherErnst & Young GmbHWirtschaftsprüfungsgesellschaft Mittlerer Pfad 1570499 Stuttgart

Editorial TeamChristian Ehlermann, [email protected] Leissner, [email protected] Ortmann-Babel, [email protected]

About this quarterly reportThis quarterly report provides highlevel information on German tax developments relevant to foreign business investing in Germany.

Add to or remove from distribution listIf you would like to add someone to the distribution list, or be removed from the distribution list, please send an e-mail to [email protected]

Imagesistockphoto