Georgia Tax Update - Tim Clancy

23

GEORGIA TAX UPDATE Is Georgia Becoming Taxpayer Friendly? Tim Clancy, CPA November 13, 2014

-

Upload

windhampresentations -

Category

Economy & Finance

-

view

245 -

download

1

Transcript of Georgia Tax Update - Tim Clancy

GEORGIA TAX UPDATEIs Georgia Becoming Taxpayer Friendly?Tim Clancy, CPANovember 13, 2014

2

3

4

5

6

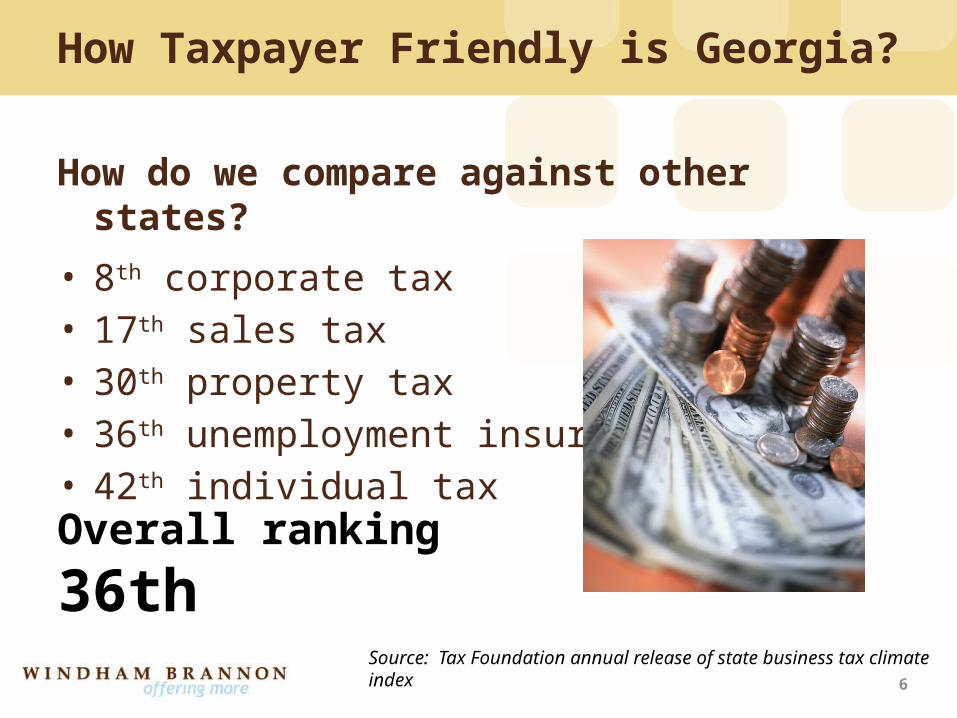

How Taxpayer Friendly is Georgia?

How do we compare against other states?

• 8th corporate tax• 17th sales tax • 30th property tax• 36th unemployment insurance • 42th individual tax

Overall ranking 36th

Source: Tax Foundation annual release of state business tax climate index

7

How Taxpayer Friendly is Georgia?

Corporate tax– Ability to apportion income – Single sales factor apportionment (2005)– No throwback (sales of tangible property)– Market based apportionment for sale of services– 6% rate (1969)– Credits and incentives offered

8

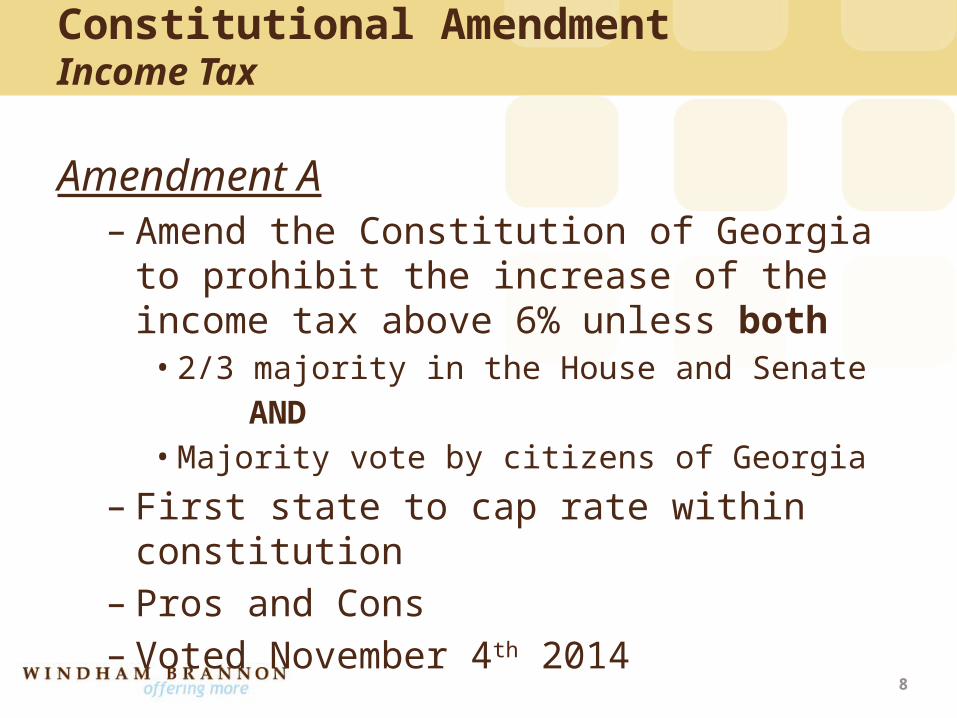

Constitutional AmendmentIncome Tax

Amendment A– Amend the Constitution of Georgia to prohibit the

increase of the income tax above 6% unless both• 2/3 majority in the House and Senate

AND• Majority vote by citizens of Georgia

– First state to cap rate within constitution– Pros and Cons– Voted November 4th 2014

9

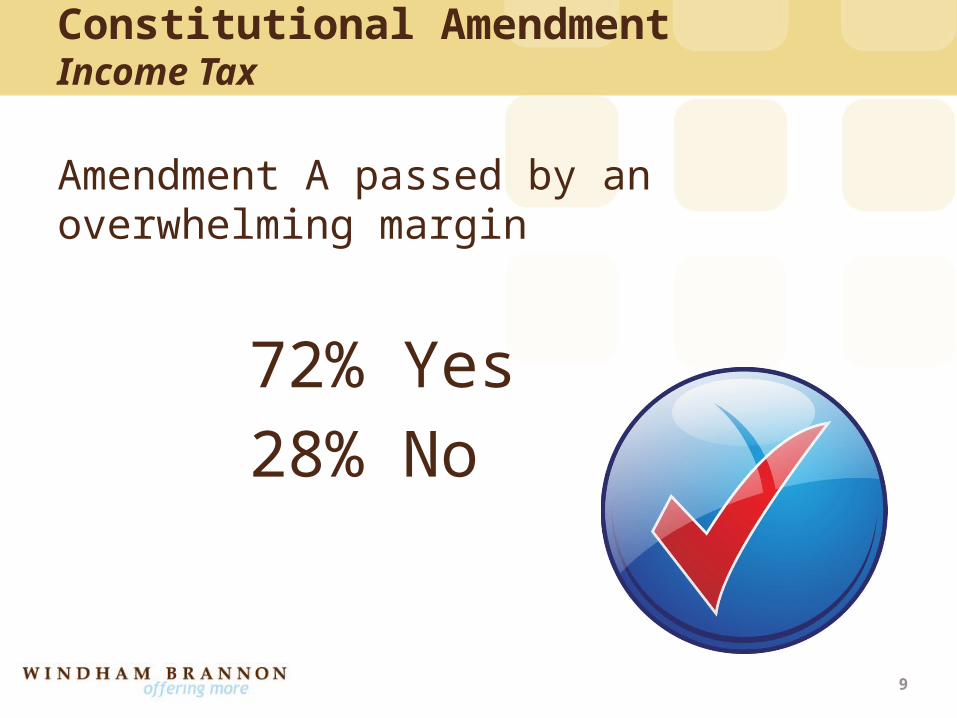

Amendment A passed by an overwhelming margin

72% Yes28% No

Constitutional AmendmentIncome Tax

10

Legislative DevelopmentsSales/Use Taxes

Taxability of Consumable Supplies– Provides full exemption to manufacturing supplies

consumed in production but not incorporated into final product

– Includes items such as but not limited to• Gasses,• Chemicals• Abrasive compounds• Sand paper

– Manufacturing “machinery and equipment” and other “safety machinery and equipment” are already exempt

– Comparative to other statesHB. 900 (Eff. 7-1-2014) amends O.C.G.A. 48-8-3.2

11

Exemption for energy used in manufacturing– Exemption from sales tax for “energy” used in

manufacturing– Energy is artificial gas, gasoline, electricity solid fuel,

wood, water, steam, ice and other materials necessary and integral for heat, light, power, refrigeration, climate control or processing

– Applies to energy which is necessary and integral to the manufacture of tangible personal property

HB. 386 (Eff. 1-1-2013)

Legislative DevelopmentsSales/Use Taxes

12

Exemption for energy used in manufacturing

Exemption applies to energy used to:– Operate machinery and equipment– Create conditions necessary for the manufacture of tangible

property– Perform actual part of the manufacture– Administrative and other ancillary activities that are located and

performed at the manufacturing plant so long as activities primarily benefit manufacture of property

– Convey, transport, handle, or store raw materials or goods– Heating, cooling, ventilation– Comfort and convenience of employees at site– Any other purpose

Legislative DevelopmentsSales/Use Taxes

13

Exemption for energy used in manufacturing

Does not apply to – Marketing sales and nonproduction activities– Executive offices

Phase in period– 25% Exempt 2013– 50% exempt 2014– 75% exempt 2015– 100% exempt 2016 and forward

Legislative DevelopmentsSales/Use Taxes

14

Taxability of postage fees – Background• “Delivery charges” were changed to include

postage (Eff. 1-1-2012 ) • Clarification vs. change in law

– HB. 816 (Eff. 7-1-2014) amends O.C.G.A. 48-8-2(10)• Postage will be considered nontaxable when it is a direct

cost pass through from printer to customer• Allows in-state direct mailers to be competitive

Legislative DevelopmentsSales/Use Taxes

15

Legislative DevelopmentsIncome Tax

IRC Conformity– HB 918 adopts computation of Federal Adjusted

Gross Income or Federal Taxable Income as enacted on or before January 1, 2014

– List of exceptions are provided• Bonus Depreciation• Domestic Production Deduction• Section 179 for real property

16

Legislative DevelopmentsTax Credits

Alternative fuel vehicle / Low emissions credit– Tax credit for purchase of heavy and medium duty

vehicles that run on liquid petroleum gas, natural gas or hydrogen fuel

– Purchases made between July 1, 2015 and June 30, 2017

– Registered Georgia vehicle– Limited to $20,000 per heavy duty

and $12,000 for medium duty vehicle

17

Qualified interactive entertainment production credit– Extends $25M of tax credits for game developers over the

2014 -2015 years– Qualification:

• Engaged in production related to interactive entertainment• Maintain offices in Georgia• Total aggregate payroll greater than $500,000• Income of less than $100 million• Approved by the Georgia Dept. of Economic Development

– Credits are transferable similar to Film Credits

HB. 958 (Eff. 4-14-2014; applicable to tax years beginning 1-1-1-2014)

Legislative DevelopmentsTax Credits

18

Legislative DevelopmentsGeorgia Tax Tribunal

• Tribunal commenced its existence September 2013• Provides low or no cost alternative for adjudicating

tax disputes with Dept. of Revenue• Available to individual or business taxpayers• Provides informal and less extensive procedures

19

• Addresses corporate, individual, sales/use, withholding and other taxes

• Does not have authority to accept– property tax– proposed assessments– payment plans– offer in compromise

Legislative DevelopmentsGeorgia Tax Tribunal

20

Has the mission been accomplished?• Use of remanding cases to DOR for 90 day pre-trial

settlement is working • Low number of full hearing or hearings with

continuance and most settled or entered as default• Individuals have often represented themselves;

business taxpayers require attorney

Legislative DevelopmentsGeorgia Tax Tribunal

21

What decisions are on the horizon?• Inglett & Stubbs International v. Georgia Dept. of

Revenue– Sales tax on products that were shipped from out of

state but stored in Georgia prior to being shipped overseas

• H. Alan Rosenberg v. Georgia Dept. of Revenue– Are taxpayers entitled to a state modification or credit

for taxes related to the Texas margin tax

Legislative DevelopmentsGeorgia Tax Tribunal

22

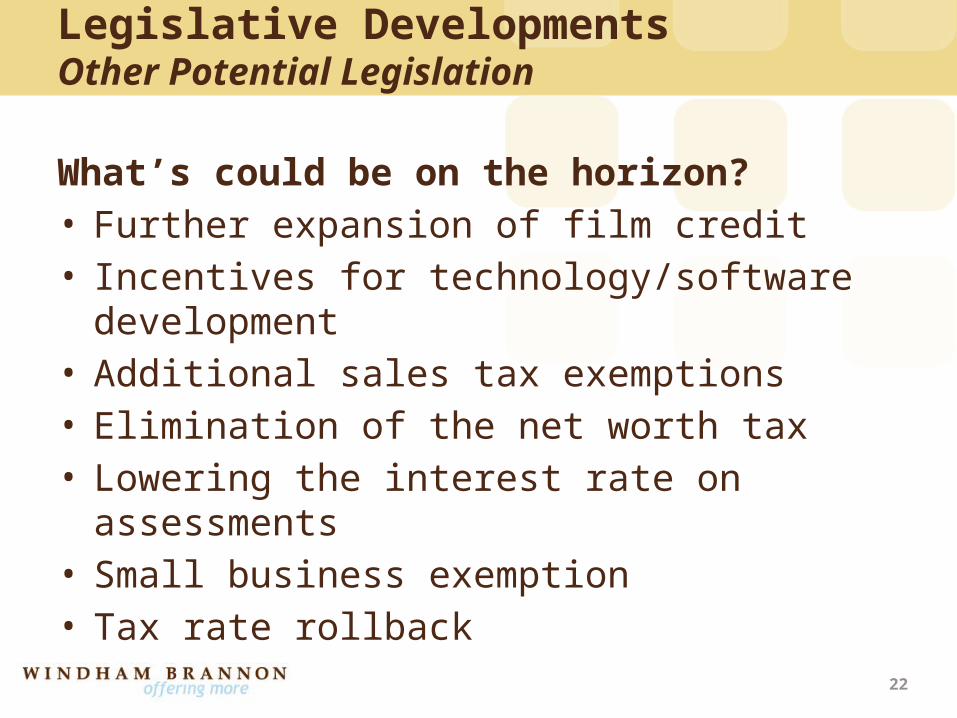

Legislative DevelopmentsOther Potential Legislation

What’s could be on the horizon?• Further expansion of film credit• Incentives for technology/software development• Additional sales tax exemptions• Elimination of the net worth tax• Lowering the interest rate on assessments• Small business exemption• Tax rate rollback

![Tom Clancy - Pericol Iminent [Ibuc.info]](https://static.fdocuments.in/doc/165x107/577cd3d31a28ab9e7897a272/tom-clancy-pericol-iminent-ibucinfo.jpg)