Georgia Tax Credits - Tim Clancy

50

GEORGIA TAX CREDITS Tim Clancy, CPA November 13, 2014

-

Upload

windhampresentations -

Category

Business

-

view

170 -

download

1

Transcript of Georgia Tax Credits - Tim Clancy

GEORGIA TAX CREDITSTim Clancy, CPANovember 13, 2014

2

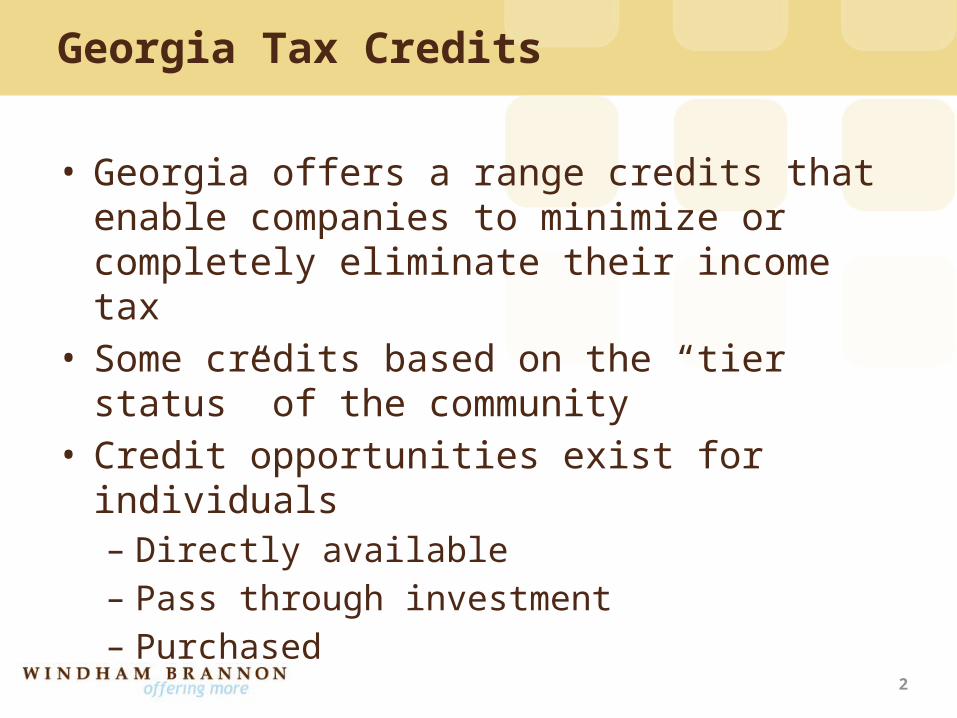

Georgia Tax Credits

• Georgia offers a range credits that enable companies to minimize or completely eliminate their income tax

• Some credits based on the “tier status” of the community

• Credit opportunities exist for individuals – Directly available– Pass through investment– Purchased

3

Film and Entertainment Credits

• Purpose: Entice film and game producers to come to Georgia– Additional benefits obtained from 2014 legislation for

game development– Future legislation

4

Film and Entertainment Credits

Film Production Company– Provided 20% tax credit on qualified expenditures• $500,000 minimum expenditures (i.e. labor, materials

services)– Additional 10% credit for use of Georgia promotional

logo in finished production– Obtain credits upon completion of production

5

Film and Entertainment Credits

Film Production Company– May sell credits in multiple blocks – One time transferability– Obtains comfort letter or state certified audit– Recognizes income on the sale of the credits

6

Film and Entertainment Credits

Taxpayers • Purchase credits through broker or CPA assistance• Rates vary - $.86 - $.91• Form IT-TRANS• Deemed to be paid ratably over year • Carry forward - 5 years• Short term capital gain recognition on federal return

7

Film and Entertainment Credits

Taxpayer Considerations– Timing of purchase and use of credit– Timing of deduction for state tax paid – Capital gain recognition – Holding period– Risk/transferability– Risk • Comfort letter• State certified audit• Recapture

8

Low Income Housing Tax Credit

• Purpose: To encourage the development of low income housing in Georgia– 15 states currently offer housing credits– Georgia • 2001 - Adopted credit• 2003 – Credits first available • Allows bifurcation of state credits from federal credit

– Available to individuals, corporations or trusts– Beneficial regardless of AMT position• Larger benefit for AMT taxpayers

– Carry forward – 3 years

9

Low Income Housing Tax Credit

Taxpayer– Purchase through broker or CPA assistance– Investment in entity taxable as partnership– Receive K-1 with allocation of credits– Attach K-1 to Georgia return

10

Low Income Housing Tax Credit

Taxpayer Considerations– Rates vary $.75 - $.85– BUY EARLY for lower rates– Consider tax position and time value of money– Years required in investment

11

Georgia Education Expense Credit

• Purpose– Allows parents

• To seek a private K-12 school that provides the best education they can find

• Obtain a scholarship to prevent financial barrier for obtaining education for the child

• Maximum annual scholarship capped at per pupil cost in Georgia public schools $8,983 for 2014

– Allows Taxpayers• Contribution to non-profit K-12 scholarship organization in

exchange for a state tax credit• May designate the private school where contribution is used• May not designate the child the scholarship is awarded to• 125 participating schools

12

Georgia Education Expense Credit

– Individual and corporate taxpayers receive Georgia income tax credits for contributions to qualified student scholarship organization (SSO) up to:• $1,000 (single)• $2,500 (married filing jointly)• $10,000 (individuals with ownerships in S Corp, LLC or

partnership)– Contributions are also eligible for federal income tax

deduction but added back for Georgia taxable income

13

Georgia Education Expense Credit

New for 2013– Owners of S-corps, LLCs and Partnerships allowed

contribution of $10,000• If both spouses earn income from pass through entities -

each can contribute up to $10,000 ($20,000 in total)– May select which pass-through entities to include

when computing Georgia income

14

Georgia Education Expense Credit

– May combine all Georgia income, loss and expense regardless of ownership in multiple entities

– May combine W-2 income from the pass-through as well as K-1 income

15

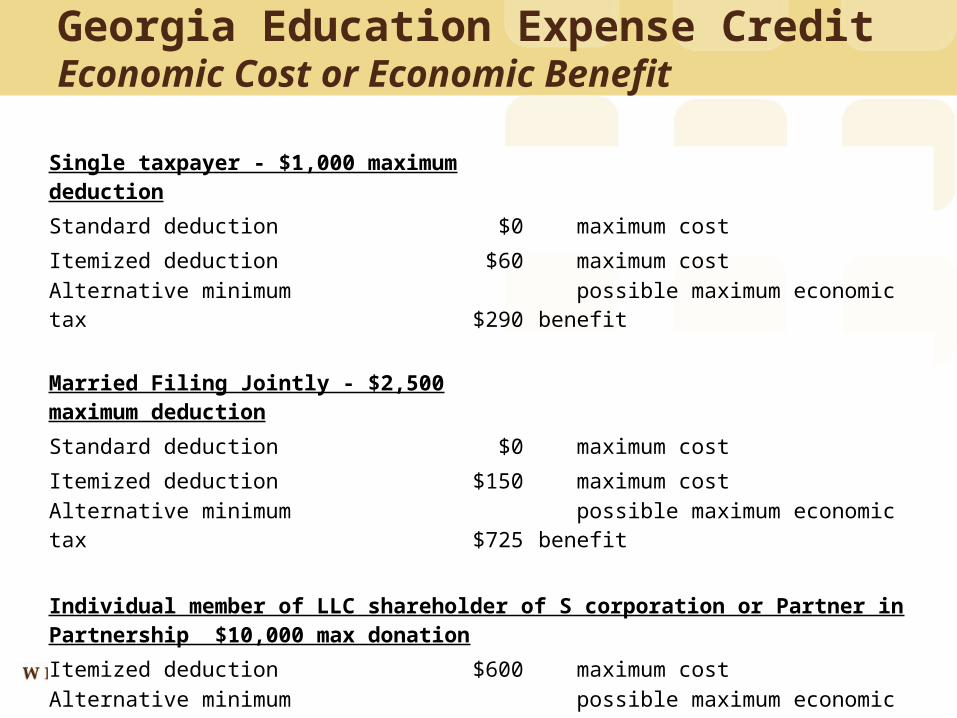

Georgia Education Expense CreditEconomic Cost or Economic Benefit

Single taxpayer - $1,000 maximum deduction

Standard deduction $0 maximum cost

Itemized deduction $60 maximum costAlternative minimum tax $290 possible maximum economic benefit

Married Filing Jointly - $2,500 maximum deduction

Standard deduction $0 maximum cost

Itemized deduction $150 maximum costAlternative minimum tax $725 possible maximum economic benefit

Individual member of LLC shareholder of S corporation or Partner in Partnership $10,000 max donation

Itemized deduction $600 maximum costAlternative minimum tax $2,900 possible maximum economic benefit

16

Georgia Education Expense Credit

– Corporate limitation to 75% of tax liability– Trusts may not pass credit through to beneficiaries– Carry forward provisions– Payment within 60 days of approval

APPLY EARLY!!!!

17

Retraining Tax Credit

• Purpose– Foster profitability and competitiveness of existing

Georgia businesses– Encourages workforce development– Offset costs of retraining employees • Implementation of new equipment • New technology• Operating systems

18

Retraining Tax Credit

• Available credit– One half of the direct cost of retraining– Up to $500 per approved training program per year for

each employee; may not exceed $1,250 per year per full-time employee

– Up to 50% of the tax liability

19

Retraining Tax Credit

• Eligible retraining programs– Newly installed equipment– Newly implemented technology• Computers• Platforms• Software implementations and upgrades• Total quality management• ISO 9000• Self directed work teams

20

Retraining Tax Credit

• Programs that are not eligible– Executive training– Management development training– Career development– Personal enrichment– Cross training of employees

21

Retraining Tax Credit

• Eligible costs– Instructor salaries– Employee wages during the retraining– Development of retraining program– Materials and supplies– Instructional media– Equipment used for retraining (not production)– Reasonable travel costs

22

Retraining Tax Credit

• Costs that are not eligible – Sales taxes– Training space– Employee paid training

23

Retraining Tax Credit

• Eligible employees– Georgia residents– First line employees or immediate supervisor– Continuously employed with company for minimum

16 weeks– Full time employees (25+ hours per week)

24

Retraining Tax Credit

– Carry forward – 10 years– Training over multiple years are claimed based on the

costs incurred for each year– Prior year training may be also approved

25

Retraining Tax Credit

• Administration– Technical college system of Georgia• Fulton – Atlanta Tech. Gwinnett Tech• DeKalb – Georgia Piedmont Tech• Gwinnett – Gwinnett Tech

– Vice President of Economic development determines eligibility and if documentation is adequate and complete

26

Retraining Tax Credit

• Procedures for Approval• Documentation requirements– Description of changes or new equipment– Purpose/objectives– Employees– Qualification of training provider– Employee performance evaluation– Training outline– Hours, costs incurred

27

Job Tax Credit

• Available to new and expanding companies in certain industries– Manufacturing – Warehousing and Distribution– Processing– Telecommunications– Broadcasting– Tourism– Research and Development– Biomedical Manufacturing– Services for the elderly and Persons with Disabilities

28

Job Tax Credit

– Based on calculation of increase in headcount – Calculate per location– Credits may be applied against • Income tax liabilities or • Withholding tax (limited)

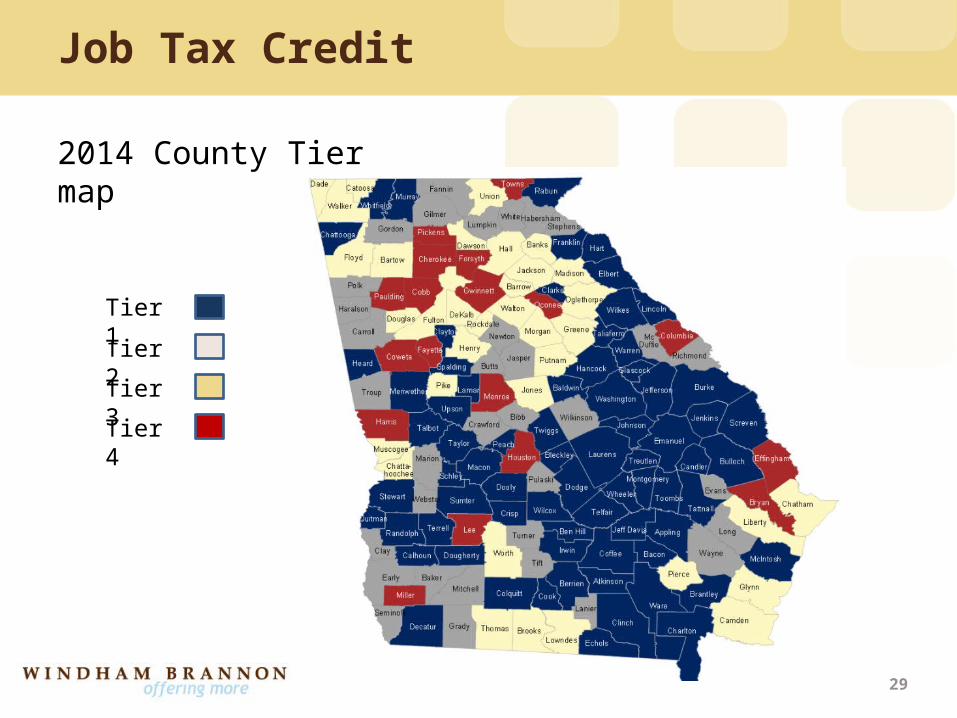

– Utilizes “county tier” based on • Unemployment rate• Per capita income • Poverty rate

29

Job Tax Credit

Tier 1

Tier 2

Tier 3

Tier 4

2014 County Tier map

30

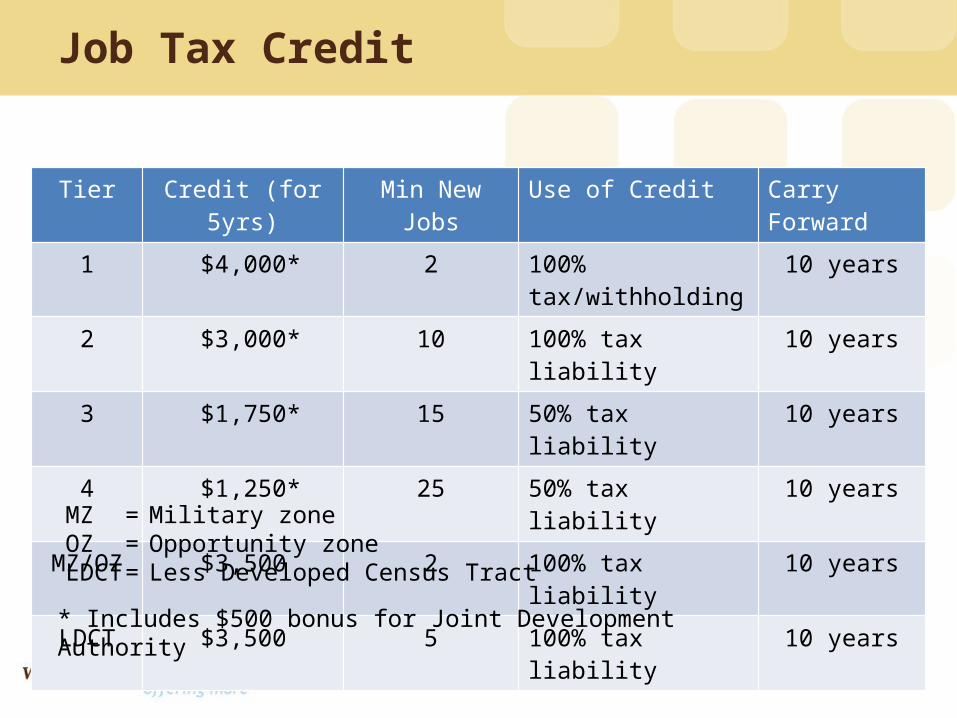

Job Tax Credit

Tier Credit (for 5yrs) Min New Jobs Use of Credit Carry Forward

1 $4,000* 2 100% tax/withholding 10 years

2 $3,000* 10 100% tax liability 10 years

3 $1,750* 15 50% tax liability 10 years

4 $1,250* 25 50% tax liability 10 years

MZ/OZ $3,500 2 100% tax liability 10 years

LDCT $3,500 5 100% tax liability 10 years

* Includes $500 bonus for Joint Development Authority

MZ = Military zoneOZ = Opportunity zoneLDCT = Less Developed Census Tract

31

Job Tax Credit

• Year 1 establishes 5 year period• Additional credits are accrued for additional jobs in

years 2-5• Jobs created outside of year 5 must meet new

threshold for job creation

32

Job Tax Credit

• Special Zones– Less Developed Census Tract (LDCT)– Opportunity Zones (OZ)– Military Zones (MZ)

• Additional benefits– Eligible for $3,500 tax credit– Use against 100% of tax liability– Excess credit applied to payroll withholding– Available to all businesses including retail

33

Job Tax Credit

• Employee qualifications– Full time employees– Offered health insurance benefits similar to existing

employees– Pay more than average wage of county with the lowest

average wage in state ($426/week for 2014)

34

Job Tax Credit

ExampleFacts: In Year 1, Create-It Corp has three locations. It increased its headcount by– Location #1 – 50 in Macon County (Tier 1) – Location #2 – 30 in Gwinnett County (Tier 4)– Location #3 – 20 in Gwinnett County (Tier 4)

In Year 2 an additional 3 employees were added at location #2.

What is the amount of credit earned by Create-it Corp?

35

Job Tax Credit

Determination is based on location NOT county

Location #1 – 50 jobs x $4,000 x 5 years = $1,000,000Location #2 – 33 jobs x $1,250 x 5 years = $206,250Location #3 – Does not qualify for credits

36

Investment Tax Credit

• Available to manufacturers and telecommunications businesses– Operate in Georgia for 3 years– Investment of $50,000 minimum

• Planned Project – Planned purchases– New facility or expansion of existing facility– Directly related to taxpayer’s manufacturing– < 3 years – Results in expansion of asset base

37

Investment Tax Credit

• Qualified capital investments– Land acquisition– Improvements– Buildings– Machinery & Equipment– Leased equipment may be eligible

• Purchases not qualified– Safety items– Materials used in repair, refurbishment– Furniture – Computer hardware or software

38

Investment Tax Credit

• Credit based on county tiers – Tier 1 – 5%– Tier 2 – 3%– Tier 3 – 2%– Tier 4 – 1%

• Recycling or pollution control equipment (3%-8%) • Optional investment tax credit – Purchases from $5 - $20 million– Range 6% - 10%

39

Investment Tax Credit

• Application due within 30 days of the completion of the project

• Project - < three years• 50% tax offset• 10 year carry forward • Generally can not be combined with – jobs credit – optional investment credit – headquarters credit

40

Port Tax Credit Bonus

• Eligible taxpayers– Increase import/export by 10% through Georgia ports– Claimed jobs credit or investment credit

• Credit available– Additional $1,250 per job up to 5 years– Increased investment credit rate to Tier 1 status (5%)

41

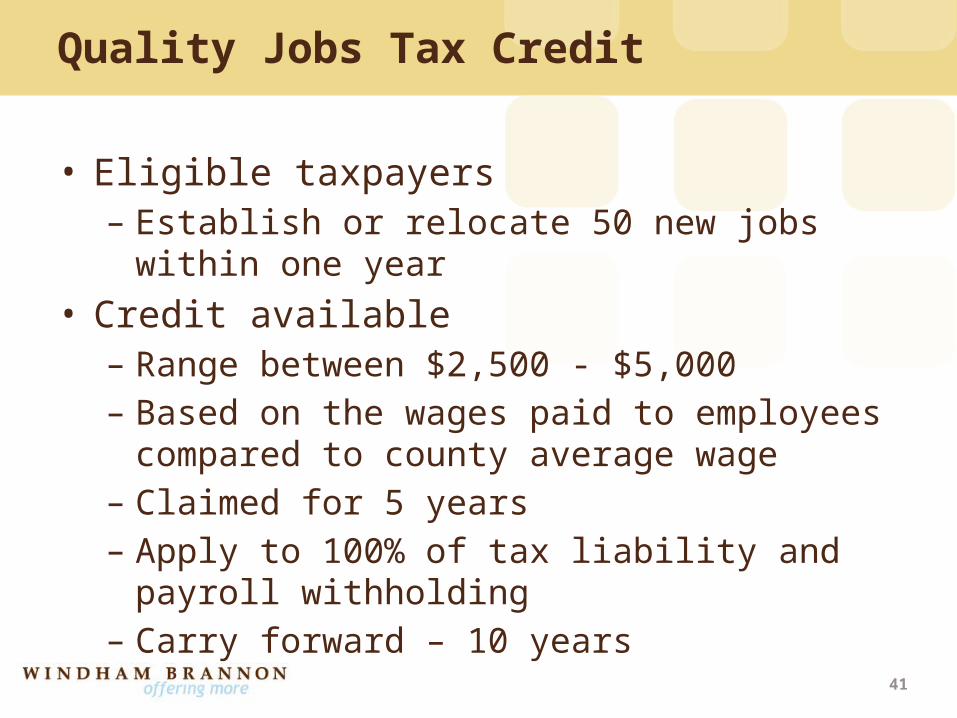

Quality Jobs Tax Credit

• Eligible taxpayers– Establish or relocate 50 new jobs within one year

• Credit available– Range between $2,500 - $5,000 – Based on the wages paid to employees compared to

county average wage– Claimed for 5 years– Apply to 100% of tax liability and payroll withholding– Carry forward – 10 years

42

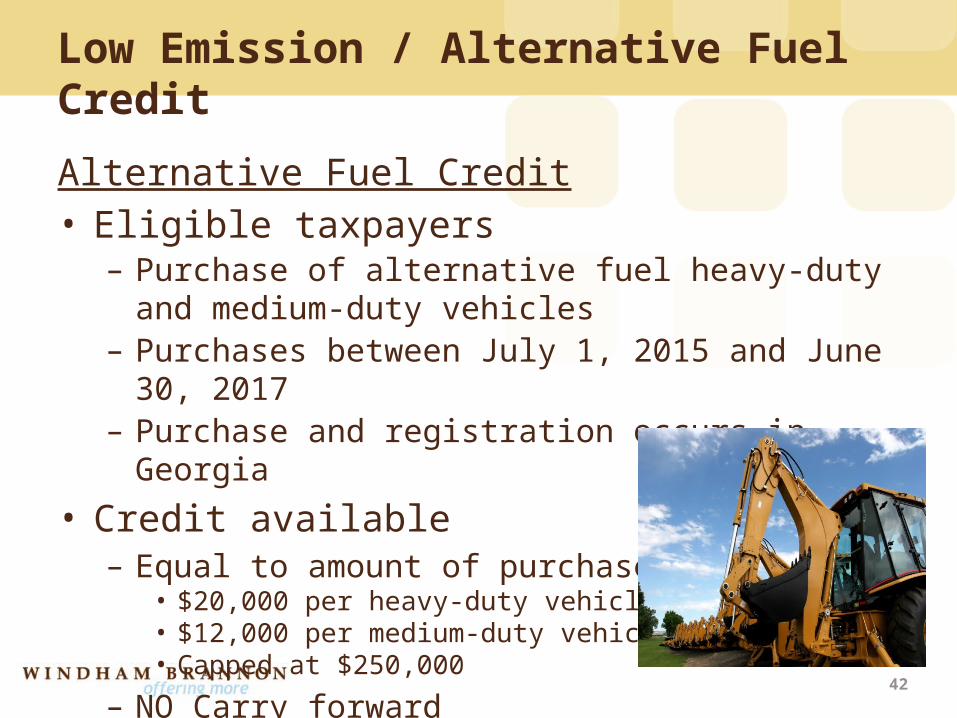

Low Emission / Alternative Fuel Credit

Alternative Fuel Credit• Eligible taxpayers– Purchase of alternative fuel heavy-duty and medium-duty

vehicles– Purchases between July 1, 2015 and June 30, 2017– Purchase and registration occurs in Georgia

• Credit available – Equal to amount of purchased vehicle

• $20,000 per heavy-duty vehicle• $12,000 per medium-duty vehicle• Capped at $250,000

– NO Carry forward

43

Low Emission / Alternative Fuel Credit

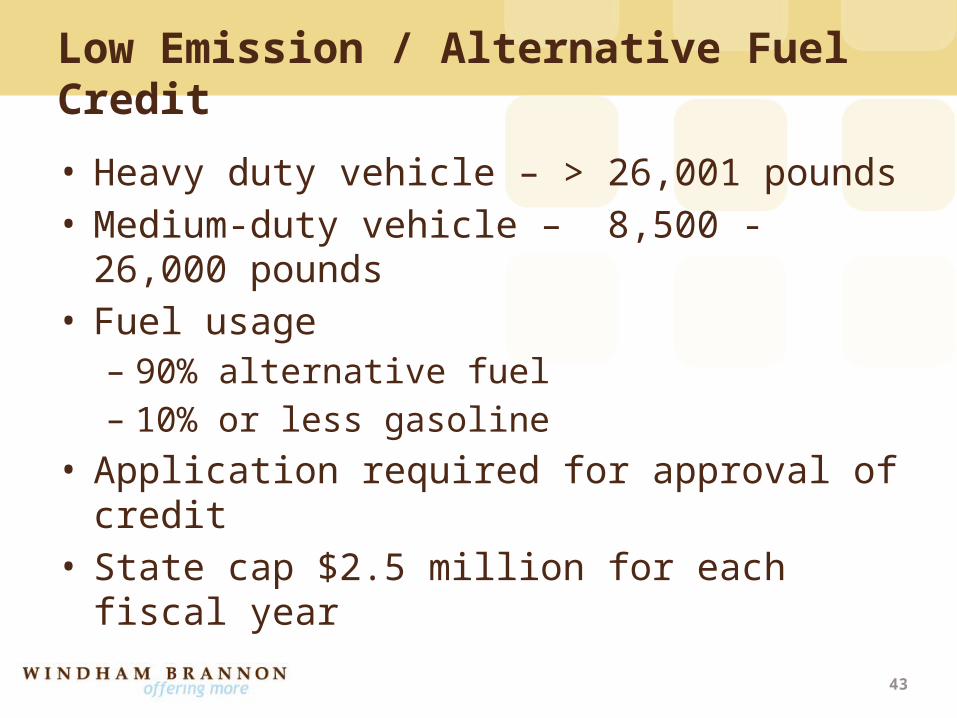

• Heavy duty vehicle – > 26,001 pounds• Medium-duty vehicle – 8,500 - 26,000 pounds• Fuel usage – 90% alternative fuel – 10% or less gasoline

• Application required for approval of credit• State cap $2.5 million for each fiscal year

44

Low Emission / Alternative Fuel Credit

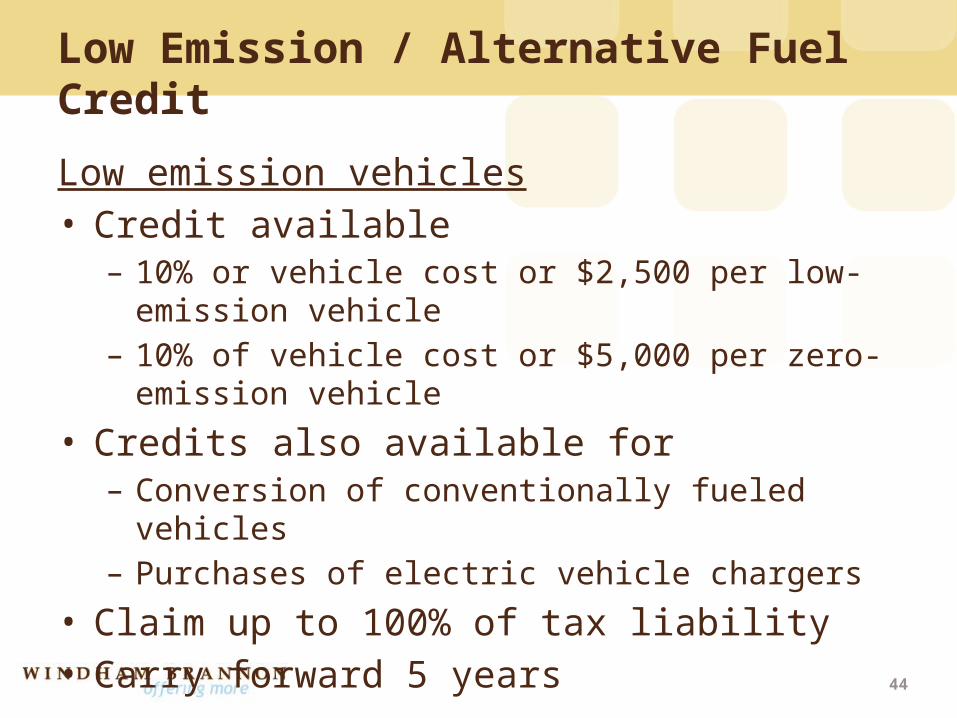

Low emission vehicles• Credit available– 10% or vehicle cost or $2,500 per low-emission vehicle– 10% of vehicle cost or $5,000 per zero-emission vehicle

• Credits also available for – Conversion of conventionally fueled vehicles– Purchases of electric vehicle chargers

• Claim up to 100% of tax liability• Carry forward 5 years

45

Child Care Tax Credit

• Eligible taxpayers– Purchase or build qualified child care facilities or– Provide or sponsor child care

• Credit available – 75% of employer’s direct cost – May claim up to 50% of tax liability– Carry forward 5 years

46

Other Tax Credits

• Research and Development credit– 10% credit of increased R&D expenses

• Qualified Health Insurance Expense Credit– $250 credit per employee• 50 or fewer employees• Provide high deductible health plan under IRC

Section 223• Taxes paid to other states (Individuals)

47

Other Tax Credit Considerations

Assignability of credit• Member of affiliated group under IRC section 1504 • Entity affiliated with an entity which– Owns or leases the land – Provides capital for construction of project and– Is grantor or owner under a management agreement

with the managing company

48

Other Tax Credit Considerations

Assignability of credit• No carryover of previously claimed credits may be

assigned• Remaining carryover transferred back if member

leave affiliated group• Election must be filed• Irrevocable election• Jointly liable

49

Other Tax Credit Considerations

Application for refundsCredits must be claimed within one year of the earlier of– Date the original return was filed – Date return due including extension

![Thomas L. Clancy, Jr. v. Wanda T. King, No. 112, September ... · Although [Clancy], individually, permitted the joint venture to use the name "Tom Clancy" in the series title in](https://static.fdocuments.in/doc/165x107/5e2e1bc7f48add5726276cd9/thomas-l-clancy-jr-v-wanda-t-king-no-112-september-although-clancy.jpg)