General Autoregressive Conditiona l …scausa.com/SCADocs/WorkBench_Garch.pdfModified: August 25,...

115

Modified: August 25, 2005 General Autoregressive Conditional Heteroscedastic (GARCH) Modeling Using the SCAB34S-GARCH and SCA WorkBench Houston H. Stokes Department of Economics University of Illinois at Chicago Lon-Mu Liu Department of Information and Decision Sciences University of Illinois at Chicago William J. Lattyak Scientific Computing Associates Corp.

Transcript of General Autoregressive Conditiona l …scausa.com/SCADocs/WorkBench_Garch.pdfModified: August 25,...

Modified: August 25, 2005

General Autoregressive Conditional Heteroscedastic (GARCH) Modeling

Using the SCAB34S-GARCH and SCA WorkBench

Houston H. Stokes Department of Economics

University of Illinois at Chicago

Lon-Mu Liu Department of Information and Decision Sciences

University of Illinois at Chicago

William J. Lattyak Scientific Computing Associates Corp.

Table of Contents 1. GARCH MODELING USING SCAB34S AND WORKBENCH ...................................................................... 2

1.1 ARCH Models.................................................................................................................................................. 3 1.2 GARCH models ............................................................................................................................................... 4 1.3 Integrated GARCH models ............................................................................................................................ 4 1.4 GARCH-M models .......................................................................................................................................... 4 1.5 Non-normal Error Distributions.................................................................................................................... 5

1.5.1 Standardized Student-t Distribution .......................................................................................................... 6 1.5.2 Standard Cauchy Distribution................................................................................................................... 6 1.5.3 General Error Distribution........................................................................................................................ 6

1.6 Asymmetric GARCH models ......................................................................................................................... 7 1.6.1 Glosten-Jagannathan-Runkle (GJR) model............................................................................................... 7 1.6.2 Extended Threshold GARCH model .......................................................................................................... 8 1.6.3 Exponential GARCH model....................................................................................................................... 8 1.6.4 Zakoian Threshold GARCH model............................................................................................................ 9

1.7 Regression plus GARCH models ................................................................................................................... 9 1.8 Bivariate GARCH model.............................................................................................................................. 10

2. ESTIMATION OF GENERALIZED ARCH (GARCH) MODELS................................................................ 11 2.1 Two-Pass Estimation Method Using the SCA Statistical System.............................................................. 11 2.2 The One-Pass Method (Joint Estimation Method) Using SCAB34S......................................................... 12

3. SCA WORKBENCH: A GRAPHICAL USER INTERFACE......................................................................... 12

4. EXAMPLES OF GARCH MODELING USING SCA WORKBENCH ......................................................... 13 4.1 Analysis of the Wholesale Price Index (Enders 1995) ................................................................................ 13

4.1.1 Applying the automatic two-pass method ................................................................................................ 15 4.1.2 Applying the user-directed one-pass method........................................................................................... 18

4.2 GARCH Analysis of the S&P 500 Using the One-Pass Method ................................................................ 22 4.2.1 Considering the student-t distribution (FATTAIL) estimation option...................................................... 25 4.2.2 Considering a GARCH-M model for the S&P 500 monthly returns........................................................ 27

4.3 Regression plus GARCH Models Using IBM returns and S&P 500 Series ............................................. 29 4.3.1 Modeling IBM stock returns and the S&P 500 index using the automatic two-pass method .................. 29 4.2.2 Modeling IBM stock returns and the S&P 500 index using the user-directed one-pass method............. 33

4.4 Bivariate GARCH Models Using IBM returns and S&P 500 Series ........................................................ 35 4.4.1 Bivariate Modeling Approach Assuming Constant Correlations ............................................................ 35 4.4.2 Bivariate Modeling Approach Assuming Time-varying Correlations ..................................................... 39

5. A DETAILED DESCRIPTION OF THE GARCH APPLICATION INTERFACE IN WORKBENCH.... 45 Two-pass Estimation Method: ........................................................................................................................... 45 One-pass Estimation Method: ........................................................................................................................... 45

5.1 Data View for ARCH/GARCH Modeling ................................................................................................... 45 5.2 ARCH/GARCH Modeling Environment..................................................................................................... 48

5.2.1 Automatic two-pass method..................................................................................................................... 49 Regression Components ...................................................................................................................................... 51 5.2.2 User-directed two-pass method ............................................................................................................... 53 5.2.3 User-directed one-pass method ............................................................................................................... 56 Advanced Options/Settings View ......................................................................................................................... 59 MAX LAG in ML Sum ......................................................................................................................................... 61 Bivariate GARCH Model Specification................................................................................................................ 61 5.2.4 Results ..................................................................................................................................................... 63 5.2.5 Graphics .................................................................................................................................................. 65

6. A DETAILED DESCRIPTION OF THE GARCHEST COMMAND IN SCAB34S..................................... 66 Usage: ............................................................................................................................................................... 66

Required subroutine arguments: ....................................................................................................................... 66 Optional keywords and associated arguments: ................................................................................................. 66 Variables created if OPTIONS keyword is specified:........................................................................................ 71

7. A DETAILED DESCRIPTION OF THE GARCHEST COMMAND IN SCAB34S..................................... 73 Usage: ............................................................................................................................................................... 73 Required subroutine arguments: ....................................................................................................................... 73 Optional keywords and associated arguments: ................................................................................................. 74

8. A DETAILED DESCRIPTION OF THE CMAXF2 COMMAND IN SCAB34S .......................................... 77 Usage ..................................................................................................................................................................... 77

9. DESCRIPTION OF CUSTOMIZED SUBROUTINES IN THE GARCH APPLICATION ......................... 80 9.1 DSPGARCH User Subroutine...................................................................................................................... 80

Usage: ............................................................................................................................................................... 81 Required subroutine arguments: ....................................................................................................................... 81 Example:............................................................................................................................................................ 82

9.2 DSPDSCRB User Subroutine....................................................................................................................... 83 Usage: ............................................................................................................................................................... 83 Required subroutine arguments: ....................................................................................................................... 83 Example:............................................................................................................................................................ 83

9.3 DSP_ACF User Subroutine .......................................................................................................................... 84 Usage: ............................................................................................................................................................... 84 Required subroutine arguments: ....................................................................................................................... 84 Example:............................................................................................................................................................ 84

9.4 LAGRANGE User Subroutine..................................................................................................................... 85 Usage: ............................................................................................................................................................... 85 Required subroutine arguments: ....................................................................................................................... 85 Example:............................................................................................................................................................ 85

9.5 GARCHF User Subroutine........................................................................................................................... 86 Usage: ............................................................................................................................................................... 86 Required subroutine arguments: ....................................................................................................................... 86 Example:............................................................................................................................................................ 87

9.6 GRFGARCH User Subroutine..................................................................................................................... 88 Usage: ............................................................................................................................................................... 88 Required subroutine arguments: ....................................................................................................................... 88 Example:............................................................................................................................................................ 88

10. EXAMPLES OF SCAB34S COMMAND FILES FOR GARCH MODELING........................................... 89 10.1 SCA System script for the automatic two-pass example (Section 4.1.1)........................................... 89 10.2 SCAB34S script for the one-pass example (Section 4.1.2) ................................................................. 90 10.3 SCAB34S script for GARCH(1,1) Example (Section 4.2).................................................................. 93 10.4 SCAB34S script for GARCH(1,1) with FAT-TAIL option (Section 4.2.1) ...................................... 96 10.5 SCAB34S script for GARCH-M Model (Section 4.2.2) ..................................................................... 99 10.6 SCA script for Regression +GARCH Using Automatic Two-pass (Section 4.3.1)......................... 102 10.7 SCAB34S script for Regression plus GARCH Using the One-pass (Section 4.3.2) ....................... 103 10.8 SCAB34S script for Bivariate GARCH with Constant Correlations (Section 4.4.1) ................... 106 10.9 SCAB34S script for Bivariate GARCH with Time-varying Correlations (Section 4.4.2)............. 108

11. A DISCUSSION OF THE MCCULLOUGH – RENFRO GARCH BENCHMARK STUDY.......... 110

Coefficients ...................................................................................................................................................... 110 REFERENCES........................................................................................................................................................ 112

General Autoregressive Conditional Heteroscedastic (GARCH) Modeling Using the SCAB34S-GARCH and SCA WorkBench

In this document, we discuss Generalized Autoregressive Conditional Heteroscedastic (GARCH) modeling

and estimation provided by the B34S® ProSeries Econometric System, the SCAB34S applet collection

(GARCH module), and the SCA Statistical System.

The SCAB34S applet collection provides a subset of the capabilities in the B34S® ProSeries Econometric

System. It is organized in modular form and runs conveniently as an integrated component to SCA

WorkBench. The WorkBench product is a companion to the SCA Statistical System and SCAB34S software.

It offers macro management and a graphical user interface for GARCH modeling and other applications.

The SCAB34S product contains a number of procedures to perform common data manipulation tasks,

organizational tasks, and statistical analysis tasks. It also contains a comprehensive matrix programming

language that may be used to address a variety of general nonlinear and optimization problems. No attempt

will be made to cover all features of the SCAB34S product in this document nor the full range of applications

that may be solved using the B34S matrix programming facilities. Instead, we shall exclusively use the

graphical user interface of SCA WorkBench to specify, estimate, and diagnostically test GARCH models in

the SCAB34S and SCA Statistical Systems. WorkBench automatically specifies the program commands used

by SCAB34S based on user menu selections. A command file is then executed in the SCAB34S applet

collection and the results read back into WorkBench in a convenient fashion. For detailed information on the

capabilities of the B34S ProSeries Econometric System, refer to the book by Stokes (1997).

GARCH model specification in SCA WorkBench is intuitive and easy to use. It is also quite flexible,

providing options to estimate a variety of conditional heteroscedastic models including the autoregressive

conditional heteroscedastic (ARCH) model of Engle (1982), the generalized ARCH (GARCH) model of

Bollerslev (1986), the integrated GARCH (IGARCH) model of Nelson (1990, 1991), the GARCH-M model of

Engle, Lilien, and Robins (1987), the GJR-GARCH model of Glosten-Jagannathan-Runkle (1993), the

exponential GARCH (EGARCH) model of Nelson (1991), and a variety of threshold GARCH models.

WorkBench also provides facilities to override starting values for model parameters, adjust constraints on

model parameters, and specify several preferences for nonlinear estimation. This is very important in GARCH

model estimation since the likelihood function tends to be very sensitive especially to starting values.

Two estimation approaches are discussed, a two-pass method and a joint estimation method. We explore

the differences between these two estimation approaches and comment on when one method may be preferred

over the other. The calculation of standard errors for GARCH model parameters is a complex subject that has

2

gained increased research interest. We do not address this subject in detail in this document. However, we do

indicate the computation method for standard errors employed in the SCAB34S product and compare these

numbers to several published works. For an applied and in-depth discussion of GARCH modeling and

methodology, refer to Liu (2005) or Tsay (2002).

1 GARCH MODELING USING SCAB34S AND WORKBENCH

In conventional time series and econometric models, the variance of the disturbance term is assumed to be

constant. However, many economic and financial time series exhibit periods of unusually high volatility

followed by periods of relative tranquility. In such situations, the assumption of a constant variance is

inappropriate. Engle (1982, 1995), Bollerslev (1986), Bollerslev-Ghysels (1996) and others developed a class

of models that address such concerns and also allow for modeling both the level (the first moment) and the

variance (the second moment) of a process.

The first moment equation can be a non-seasonal ARIMA, seasonal ARIMA, or dynamic regression

model. In econometric literature, the dynamic regression model with one explanatory variable is typically

written as

pt 0 i t i j t j t

i 0 j 1Y C X Y (B)a− −

= == + ω + φ + θ∑ ∑

l (1)

where tY is the dependent variable that is differenced to stationarity, t i{X , i 1, ..., }− = l is a lagged variable that

can be expanded to include multiple explanatory variables regressed upon tY , and jφ are the autoregressive

parameters in the first moment model. In econometric literature, the moving average operator (B)θ is

typically expressed as q1 q(B) 1 B Bθ = + θ + ⋅⋅ ⋅ + θ . The SCAB34S software package employs this convention for

expressing (B)θ in (1) for the one-pass (joint) estimation method.

If the regressor variables t iX − ’s are omitted from (1) , the model is simplified to a Box-Jenkins ARIMA

model as

pt 0 j t j t

j 1Y C Y (B)a−

== + φ + θ∑ (2)

or

t 0 t(B)Y C (B)aφ = + θ (3)

where p1 p(B) 1 B Bφ = − φ − ⋅⋅⋅ − φ , and q

1 q(B) 1 B Bθ = + θ + ⋅⋅ ⋅ + θ .

3

In the typical Box-Jenkins framework, the ARIMA model is also expressed as in (3), but (B)θ is defined

as

q1 q(B) 1 B Bθ = − θ − ⋅⋅ ⋅ − θ . (4)

It is important to note that the sign of the moving average operator (B)θ is reversed between these two

formulation conventions. It is equally important to note that in the SCAB34S software package, the ARIMA

formulation for the moving average operator (B)θ in (4) is employed for the two-pass estimation method.

Whereas the two-pass method is not able to use non-normal error distributions, or handle various GARCH

extensions such as asymmetric models or GARCH-M models, the two-pass method using the model form in

(4) is able to handle multiplicative ARIMA models, intervention models, and the generalized form of a transfer

function model.

Now that we have defined the first moment model, the remainder of this document focuses on the second

moment equation that is used to model volatility in financial applications.

1.1 ARCH Models

ARCH models attempt to explain variance clustering in the residuals and imply nonlinear dependence among

the squared errors of the first moment model. Engle (1982) relaxes the constant conditional variance

assumption in traditional Box-Jenkins ARIMA models and allows it to follow a process as below

2 2 2t t t t 0 1 m t mt 1a , and a a −−= σ ε σ = α +α + ⋅⋅⋅ + α (5)

where 2 2t t t 1 t t 1 t t 1E(a | F ) Var(a | F ) Var(Y | F )− − −σ = = = . Letting 2 2

t t t t 1e a E(a | F )−= − (which is the same as

2 2t t te a= −σ ), equation (5) can also be written as an AR(m) model as below

2 2 2t 0 1 m t m tt 1a a a e−−= α +α + ⋅⋅⋅ + α + (6)

where te is a white noise process. A model with 2tσ as shown in (6) is referred to as an autoregressive

conditional heteroscedastic (ARCH) model, or ARCH(m) model. For such models, it is required that 0 0α > ,

and i 0α ≥ for i > 0.

The log likelihood function of an ARCH model, with the assumption that tε follows a Normal distribution

is n 2 2 2

t t tt m 1

( ) 0.5 ( ) 0.5(a / )= +

α = − σ − σ∑ l ln . (7)

4

In practice, there is substantial evidence showing that the Normality assumption may not always be

satisfactory. Non-normal distributions, such as the Student-t distribution (Bollerslev, 1987), Generalized Error

Distribution (GED) (Nelson, 1991) or standard Cauchy distribution may also be considered. These alternative

error distributions and their modifications to the likelihood functions will be discussed later.

1.2 GARCH Models Although the ARCH model is simple, it restricts the model for the conditional variance 2

tσ (or equivalently

th ) to follow a pure AR process and hence it may require more parameters to adequately represent the

conditional variance process in comparison with other more generalized models. Bollerslev (1986) extends

Engle’s original work by allowing the conditional variance to follow an ARMA process. This model is known

as a generalized ARCH model, or GARCH model. A GARCH(r, m) model can be written as

2 2 2 2 2t t t t 0 1 m t m 1 r t rt 1 t 1a , and a a − −− −= σ ε σ = α +α + ⋅⋅⋅ + α +β σ + ⋅⋅⋅ + β σ (8)

where 0 i j0, 0, 0α > α ≥ β ≥ , and max(m, r)i ii 1 ( ) 1= α +β <∑ . The latter constraint on i iα +β ensures that the

unconditional variance of ta is finite, even though its conditional variance evolves over time. It is easy to see

that model (8) reduces to an ARCH(m) model if r=0. Under the Normality assumption of tε , the log

likelihood function of α for a GARCH(r, m) model is the same as that in (7).

1.3 The Integrated GARCH (IGARCH) model In financial time series, the conditional volatility ( 2

tσ ) is often persistent and therefore may cause a unit root

condition in the model Such a special case of a GARCH model is referred to as the integrated GARCH

(IGARCH) model (Nelson, 1990, 1991). Similar to ARIMA models, the primary characteristic of an

IGARCH model is that the impact of past squared shocks on 2ta is persistent. As an example, an

IGARCH(1,1) model can be written as

2 2 2t t t t 0 1 1t 1 t 1a , and (1 )a − −= σ ε σ = α + −β +β σ (9)

where 0 0α > and 11 0> β > . More complicated restrictions can be estimated using a B34S program to

explicitly specify the model form and a direct call to CMAX2.

1.4 GARCH-M Models In financial markets, the return of a security may be influenced by its volatility. Engle, Lilien, and Robins

(1987) extend the basic GARCH framework to model such a phenomenon. This class of models, called the

5

GARCH-in-mean (GARCH-M) model, is particularly useful in the study of security markets. As an example,

a simple GARCH(1,1)-M model can be written as

t t t t t tY a , a= µ + δσ + = σ ε (10)

2 2 2t 0 1 1t 1 t 1a − −σ = α +α +β σ

where tY represents the return of a security, and µ and δ are constant parameters to be estimated. The

parameter δ is called the risk premium parameter. If δ is positive, it implies that the return is positively

related to its volatility, and vice versa.

The GARCH(1,1)-M model in (10) shows that the mean of first moment model is inferenced upon

conditional standard deviation tσ in the second moment model. The model can alternatively be specified so

that the first moment model is inferenced by the conditional variance 2tσ in the second moment model such

that

2t t tY a= µ + δσ + (11)

Both forms of the GARCH-M model are supported by the GARCH application environment. The same

likelihood function developed earlier under the Normality assumption also applies for the estimation of a

GARCH-M model.

1.5 Non-normal Error Distributions Until now, we have assumed that error distribution of tε for the various symmetric conditional heteroscedastic

models followed a standard Normal distribution. It was further shown that the likelihood function given the

Normalility assumption remained the same for ARCH, GARCH, IGARCH and GARCH-M models. We now

present the possibility of non-normal error distributions. There is substantial evidence showing that the

Normality assumption may not always be satisfactory for GARCH models. When non-normality conditions

are present in the distribution of tε , alternative standardized error distributions such as the Student-t

distribution (Bollerslev, 1987), Generalized Error Distribution (GED) (Nelson, 1991) or standard Cauchy

distribution may be considered. In this section, we shall derive the likelihood function for ARCH, GARCH,

IGARCH and GARCH-M models based on the above assumptions for the distribution of tε . These likelihood

functions can then be used for estimation of model parameters.

6

1.5.1 Standardized Student-t Distribution

In some applications, it is more appropriate to assume that tε follows a heavy-tailed distribution such as a

standardized Student-t distribution (Bollerslev, 1987). This is also known as a fat-tail GARCH model. The

conditional log likelihood function of α with a pre-specified ν degrees of freedom can be expressed as

2n 2tt2t m 1 t

a1 1( ) 1 ( )2 2( 2)= +

ν + α = − + + σ∑ ν − σ

l l ln n . (12)

If we wish to estimate ν jointly with other parameters, then the conditional log likelihood function based on

becomes

[ ] m 1 n( , ) (n m) ( (( 1) / 2)) ( ( / 2)) 0.5 ( 2) ( | a ,..., a )+α ν = − Γ ν + − Γ ν − ν − + αl l l l ln n n (13)

where the second term is given in (12) above.

1.5.2 Standard Cauchy Distribution

We may also employ the standard Cauchy distribution as the underlying distribution for tε . It is important to

note that the mean, variance, skewness, and kurtosis of a Cauchy distribution are undefined, and only the

median and mode of the distribution exist (which are both zero in this case).

The standard Cauchy distribution is equivalent to a Student-t distribution with one degree of freedom.

Compared to the standard Normal distribution, the standard Cauchy distribution is “shorter” and has fatter

(i.e., thicker) tails, thus favoring increased occurrences of extreme values that are associated with high

volatility. Assuming that tε follows the standard Cauchy distribution with median zero, the log likelihood

function for ARCH, GARCH, IGARCH and GARCH-M models can be derived as

n

2 2 2t=m+1 t t t

1( ) [ (a / )]

α = ∑ π σ + σ

l ln . (14)

1.5.3 General Error Distribution

Instead of a Student-t distribution or standard Cauchy distribution, Nelson (1991) employs another commonly

used distribution, the Generalized Error Distribution (GED), as the underlying distribution for tε . The GED

includes the Normal distribution as a special case, along with many other distributions, some more fat tailed

than the Normal (e.g., the double exponential), some more thin tailed (e.g., the uniform).

Assuming that tε follows a standardized GED, the log likelihood function for an ARCH, GARCH,

IGARCH, or GARCH-M model can be derived as

7

n n1 2 tt

tt m 1 t m 1

a( ) (n m)[ ( / ) (1 ) (2) ( (1/ ))] 0.5 ( ) 0.5

ν−

= + = +α = − ν λ − + ν − Γ ν − σ −∑ ∑

λσl l l l ln n n n . (15)

Similar to the Student-t distribution that assumes tε following a fat-tail distribution, the generalized error

distribution allows for tε to follow symmetric long-tail distributions, including the fat-tail, thin-tail as well as

Normal distributions. Consequently, the generalized error distribution is also a means of confirming the error

distribution as Normal or not.

1.6 ASYMMETRIC GARCH MODELS

While ARCH/GARCH models provide a venue for modeling conditional heteroscedastic volatility with a

Normal or Non-normal error distributions, these models assume that positive and negative shocks have the

same effect on volatility because it depends on the square of previous shocks. Therefore the models discussed

in the previous sections are referred to as symmetric ARCH/GARCH models. In practice, the price of

financial assets often reacts more pronouncedly to “bad” news than “good” news. Such a phenomenum leads

to a so called leverage effect, as first noted by Black (1976). The term “leverage” stems from the empirical

observation that the volatility (conditional variance) of a stock tends to increase when its returns are negative.

This effect is particularly important for option markets. Asymmetric GARCH models are designed to capture

leverage effects.

The asymmetric GARCH models discussed in this section include GJR-GARCH models of Glosten,

Jagannathan and Runkle (1993), exponential GARCH (EGARCH) models of Nelson (1991), and some other

threshold GARCH models.

1.6.1 The Glosten-Jagannathan-Runkle (GJR) Model

To capture the leverage effect, Glosten, Jaganathan, and Runkle (1993) show how to allow good news and bad

news to have different effects on volatility by using t 1a − as a threshold. A GJR-GARCH(1,1) model can be

generally expressed as m m r2 2 * 2 2

t 0 i t i i jt i t i t ji 1 i 1 j 1

a (a ) a−− − −= = =

σ = α + α + α + β σ∑ ∑ ∑I (16)

where t i(a ) 1− =I if t ia 0− < and t i(a ) 0− =I if t ia 0− ≥ . It is useful to note that the GJR-GARCH model is a

special case of threshold GARCH (TGARCH) models.

8

1.6.2 Extended Threshold GARCH (ETGARCH) Model

The GJR GARCH model in (16) can be extended to include threshold relationships on 2t j−σ , j=1,2, …, r (Tsay,

2002; page 133) as follows: m m r r2 2 * 2 2 * 2

t 0 i t i i j t j jt i t i t j t ji 1 i 1 j 1 j 1

a (a ) a (a )− −− − − −= = = =

σ = α + α + α + β σ + β σ∑ ∑ ∑ ∑I I (17)

where t i(a ) 1− =I if t ia 0− < , and t i(a ) 0− =I if t ia 0− ≥ . We shall refer to the above model as the extended

threshold GARCH (ETGARCH) model, more specifically, ETGARCH(r,m) model. In the above model, *iα

and *iβ represent the leverage effects associated with t ia − . When m=1 and r=1, we have the ETGARCH(1,1)

model as

2 2 * 2 2 * 2t 0 1 t 1 1 1 t 1 1t 1 t 1 t 1 t 1a (a ) a (a )− −− − − −σ = α +α + α +β σ + β σI I . (18)

In the above ETGARCH model, if it is found that the leverage effect *1β is significant, but *

1α is not, the

ETGARCH(r,m) model in (17) may be simplified to the following model if the term * 2mt i ii 1 t i(a ) a−= −α∑ I is

dropped m r r2 2 2 * 2

t 0 i j t j jt 1 t j t ji 1 j 1 j 1

a (a )−− − −= = =

σ = α + α + β σ + β σ∑ ∑ ∑ I . (19)

In the above simplified ETGARCH model, *jβ represents the leverage effect of t ja − .

1.6.3 The Exponential GARCH (EGARCH) Model

A problem with standard GARCH models is that it is necessary to ensure that all of the estimated coefficients

are positive. Nelson (1991) proposes the exponential GARCH (EGARCH) model that does not require non-

negativity constraints. In addition, the EGARCH model allows for the asymmetric effect of news or shocks on

the conditional volatility. The EGARCH(r, m) model in simplified form is

2 2 2t 0 1 t 1 t 1 m t m t m 1 t 1 r t r( ) (| | ) (| | ) ( ) n( )− − − − − −σ = α +α ε −γ ε + ⋅⋅ ⋅ + α ε −γ ε +β σ + ⋅⋅⋅ + β σl l ln n (20)

The EGARCH model originally proposed by Nelson (1991) was in a more general form than the above. By

using a suitable function g, the EGARCH model of Nelson (1991) can be written as

2 2 2t 0 1 t 1 2 t 2 m t m 1 t 1 r t r( ) g( ) g( ) g( ) ( )− − − − −σ = α +α ε + α ε + ⋅⋅ ⋅ + α ε +β σ + ⋅⋅⋅ + β σl ln n (21)

where t t ta /ε = σ and 1 1α = . Nelson choose the function tg( )ε to be a linear combination of tε and t| |ε such

as

t t t tg( ) [| | E(| |)]ε = δε + λ ε − ε (22)

9

where δ and λ are constant terms to be estimated. In the above function, both tε and t t| | E(| |)ε − ε are i.i.d

variable with zero mean. Also, note that t i tE(| |) E(| |) 2 /−ε = ε = π for all i.

In the SCAB34S package, both the simplified and generalized forms of the EGARCH model may be

specified. For the generalized form in the SCAB34S package, the function t ig( )−ε is defined as

t i t i t i t ig( ) (| | E(| |) , i 1, 2, ...− − − −ε = ε − ε − γ ε = (23)

where the leverage effect γ is equivalent to /−δ λ in (22). Using this formulation, the 1α in (21) is an

estimated coefficient, and the estimates of the 1 m, . . ., α α , 1 r, . . ., β β and γ in (20) and those in (21) are the

same.

1.6.4 The Zakoian Threshold GARCH (ZTGARCH) Model

A threshold GARCH model, proposed by Zakoian (1994), treats the conditional standard deviation as a linear

function of shocks and lagged standard deviations. For an asymmetric ZTGARCH(r,m) model, it takes the

following form: m r

t 0 i t i j t ji t ii 1 j 1

( a a )+ + − −− −−

= =σ = α + α −α + β σ∑ ∑ (24)

where t ta max(a , 0)+ = and t ta min(a , 0)− = are the positive and negative parts of an ta . To meet the needs of

the non-negativity constraints, all the coefficients in (24) are constrained to be positive.

As a special case of (24), if i ii+ −α = α = α for all i , the conditional standard deviation then is simplified to

m rt 0 i t i j t j

i 1 j 1| a |− −

= =σ = α + α + β σ∑ ∑ (25)

which is analogus to the GARCH(r,m) model discussed earlier. The above model is referred to as a symmetric

ZTGARCH(r,m) model and was discussed in Taylor (1986) and Schwert (1989). More detailed discussion on

the properties of the asymmetric ZTGARCH model can be found in Rabemananjara and Zakoian (1993).

1.7 Regression plus GARCH Models

For ARCH/GARCH modeling, the first moment model may be specified in the context of a regression model

with the inclusion of one or more independent variables. The second moment model, for the one-pass

estimation method, may be specified using any of the GARCH functional forms including the GARCH

extensions described in the previous sections. In most econometric literature, the first moment equation is

restricted to the following lag regression model

10

pt 0 i t i j t j t

i 0 j 1Y C X Y (B)a− −

= == + ω + φ + θ∑ ∑

l (26)

or in the case of a GARCH-M model,

pt 0 i t i j t j t t

i 0 j 1Y C X Y (B)a− −

= == + ω + φ + δσ + θ∑ ∑

l, (27)

where (B)θ is typically defined as q1 q(B) 1 ... Bθ = + θ + + θ for the one-pass estimation method. In some

literature, the tσ shown above is replaced by 2tσ . The joint log likelihood function, as defined for a particular

GARCH approach in the previous sections, is maximized.

A regression model with GARCH errors may also be estimated using a two-pass method. The models

allowed for the two-pass method can be more general than that shown in (27).

1.8 Bivariate GARCH Extension

A Bivariate GARCH model is the multivariate form of the generalized univariate volatility model. This

approach allows two series, in essence, to be jointly modeled as a vector ARMA process in both the first

moment and second moment. It is also possible to extend the approach to include more than two series,

however, there are issues related to dimensionality that may introduce some challenges in using higher

dimensioned multivariate volatility models in practical applications. It is also of interest to note that Bivariate

GARCH models can be estimated as a constant correlation model, or they may be estimated with time-varying

correlations. Refer to Tsay (2002) for well organized discussion of multivariate volatility models and their

benefits in financial analysis such as computing the Value at Risk of a financial position involving multiple

assets. The general Bivariate GARCH model is presented below.

( ) ( )

t 1t 11t11 12 1 11 12 11 12

21 22 t 2 21 22 2t 21 22 22t

11 t 1011 12

22 t 2021 22

x e(B) (B) a (B) (B) (B) (B)(B) (B) y a (B) (B) e (B) (B)

B B(B) (B)

σφ φ θ θ µ µ = + + φ φ θ θ µ µ σ

σ αβ β =

σ αβ β

21t11 12221 22 2t

e(B) (B)(B) (B) e

α α + α α

(28)

The Bivariate GARCH model, if estimated with constant correlations is estimated by maximizing the

following likelihood function. The correlations between the second moments is represented by the scalar

parameter, ρ .

11

n 211 t 22 t

t m 1n2 2 2

1 t 11 t 2 t 11 t 1t 2 t 11 t 22 tt m 1

LF .5 ( ( ) ( ) (1 ))

.5 /(1 )( ((e / ) (e / ) 2 e e / ))

= +

= +

= − σ + σ + −ρ∑

− −ρ σ + σ − ρ σ σ∑

ln ln ln (29)

The Bivariate GARCH model, if estimated with time-varying correlations assumes the same model

defined in (28). However, an alternative likelihood function is considered that computes the correlations

between the second moments at time tρ . Therefore, tρ is represented as a vector when time-varying

correlations are considered.

t t

t t

t 0 1 t 1 2 1(t 1) 2(t 1) 11(t 1) 22(t 1)

g gt t

g gt t

n 211t 22 t t

t m 1n 2 2 2

t 1 t 11 t 2 t 11 t t 1 t 2 t 11t 22 tt m 1

g q q q e e /

e /(1 e ) for 0

(e 1) /(1 e ) for 0

LF .5 ( ( ) ( ) (1 ))

.5 / (1 )((e / ) (e / ) 2 e e / )

− − − − −

= +

= +

= + ρ + σ σ

ρ = + ρ >

ρ = − + ρ <

= − σ + σ + −ρ∑

− −ρ σ + σ − ρ σ σ∑

ln ln ln

(30)

2 ESTIMATION OF GENERALIZED ARCH (GARCH) MODELS

Two-pass Estimation Using the SCA Statistical System

The SCA Statistical System provides automatic Box-Jenkins ARIMA modeling capabilities as well as

traditional user-directed modeling capabilities. If a single time series model is entertained, the automatic

modeling capabilities in the SCA System (e.g., IARIMA command) may be employed in a convenient manner

to estimate an ARCH/GARCH model using the two pass estimation method. Here, the SCA IARIMA

command is used to determine the model form, ARCH or GARCH, and estimate the model parameters. If a

model with independent variables is entertained, the SCA System combines the IARIMA and IESTIM

commands to arrive at the first moment model. The respective Box-Jenkins ARIMA models for the first and

second moment equations can also be specified by the user in a traditional manner using the TSMODEL and

ESTIMATE commands in the SCA System.

Note that since the model for the first moment equation in a GARCH-M class of models involves 2tσ , the two-

pass method cannot be employed to estimate such class of models. In addition, the error distribution is

assumed to follow a standard Normal distribution.

12

One-pass Method (Joint Estimation) Using SCAB34S

The SCAB34S product provides joint estimation of GARCH models and their extensions using the

GARCHEST, GARCH, and BGARCH commands. Since SCAB34S also provides comprehensive matrix

programming capabilities, experts can specify any GARCH model variation and call the nonlinear

optimization routines in SCAB34S directly. The later is beyond the scope of this document. For more

information on the capability of the B34S matrix command see Stokes (2002).

The GARCHEST command combines both univariate model specification and estimation in one

command. For all GARCH models and their variations discussed in this document, the GARCHEST

command may be used. If more estimation flexibility is desired, the GARCH command can be used to

calculate the maximum likelihood function inside a B34S user-defined program where the user can use a

number of optimization routines to obtain the answers. While this approach is more complex and slower, the

user is able to fully control the estimation process. The BGARCH command is a hybrid of the GARCHEST

and GARCH commands. The Bivariate GARCH parameters are specified in BGARCH but the estimation is

performed by a direct call to the nonlinear optimization solvers in SCAB34S.

Unlike some other software systems that use general optimizers to solve the system, SCAB34S allows the user

the choice of using a constrained optimizer that can avoid the problem of negative values for the second

moment equation during the estimation process.

3 SCA WorkBench: A Graphical User Interface SCA WorkBench provides a convenient graphical user interface to the SCA Statistical System and SCAB34S

products for GARCH modeling. The WorkBench product builds the data loading steps and GARCH

commands for these statistical engines based on the user’s menu selections. The associated commands are

then organized in either an SCA macro procedure or SCAB34S program file depending on whether the SCA

System (two-pass method) or the SCAB34S GARCH module (one-pass method) is used for estimation.

The ARCH/GARCH modeling environment in WorkBench is organized by tabs.

The Automatic Two-Pass Method tab is used to automatically identify and estimate ARCH/GARCH

models in the SCA System using a two-pass method. The User-directed Two-Pass Method allows the user to

individually specify the first moment and second moment equations and estimate the models in the SCA

System using the two-pass estimation method. The User-Directed One-Pass Method tab is used to specify a

variety of GARCH model approaches and estimate the models in the SCAB34S product . The Results tab

13

displays the output from the model estimation and diagnostics. The Graphs tab displays a variety of high

resolution graphics such as time series plots, residual plots, autocorrelation plots, and others.

Once the SCA macro procedure or SCAB34S program file is created by SCA WorkBench, you may save the

file for future reference or make changes directly to the commands and re-execute the script from SCA

WorkBench.

4 EXAMPLES OF GARCH MODELING USING SCA WORKBENCH This section provides examples of various GARCH modeling approaches using SCA WorkBench and its

interface to the SCA Statistical System and SCAB34S products. The first example analyzes the price data

from Enders (1995) and discusses the differences between the two-pass and one-pass estimation methods. The

remaining examples replicate several of the GARCH analyses found in Tsay, R.S. (2002), Analysis of

Financial Time Series.

The data files used for the examples discussed in this section are installed under the WorkBench

installation folder in a sub-directory named Finance. The command files built by SCA WorkBench for the

illustrated examples are presented later in Section 10 of this document.

4.1 Analysis of the Wholesale Price Index (Enders 1995)

The percent change of the wholesale price index (Enders, 1995) is used to demonstrate the two-pass and one-

pass estimation methods exposed in the SCA WorkBench program. If you are working through this example,

the first step is to set the working directory by selecting the System Profile item under WorkBench’s System

menu. In the Environment tab of the System Profile dialog box, click on the Browse button associated with the

working directory text box. Using the Define Working Directory dialog box, move to the

C:\SCAWORKB\FINANCE directory that contains financial data sets distributed with WorkBench. If

WorkBench is installed under a different directory, the Finance subdirectory is located under the WorkBench

installation directory. An example of the dialog boxes associated with modifying the working directory is

shown below.

14

After the working directory is modified and the new profile is saved, click on the ARCH/GARCH Analysis

item under the Apps menu to enter the graphical user interface for GARCH modeling as demonstrated below.

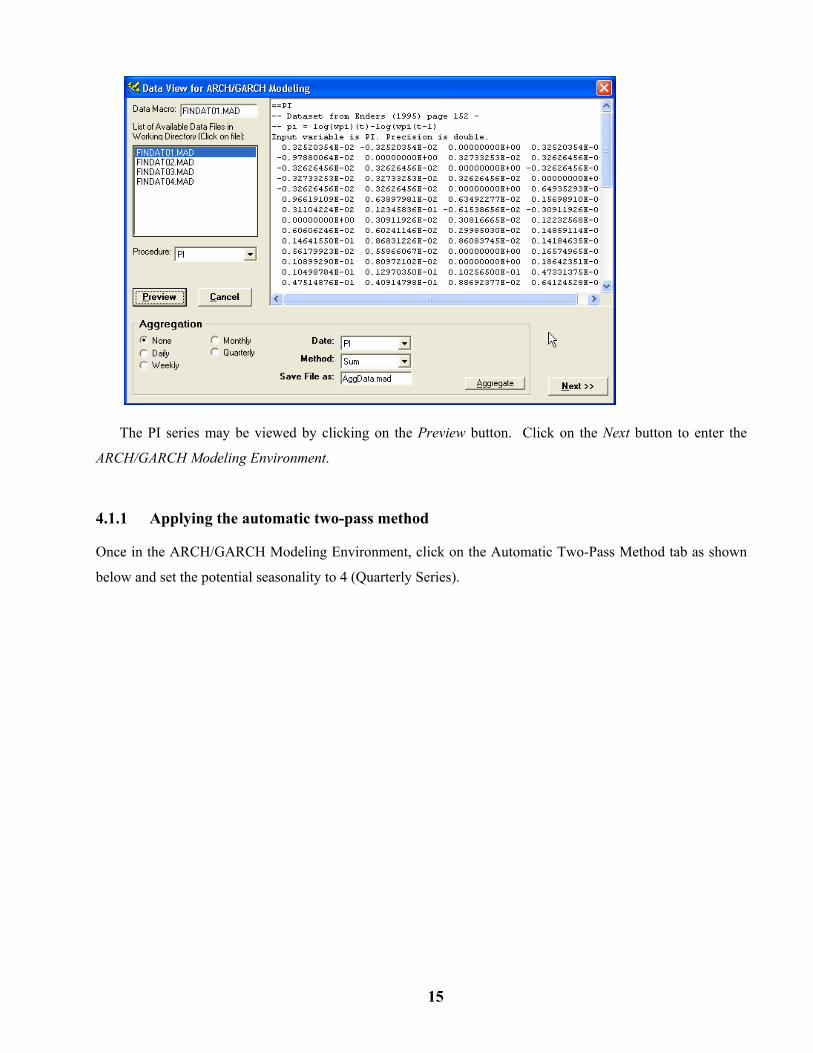

After you click on the ARCH/GARCH Analysis item, it is necessary to select the data to analyze. The Data

View for ARCH/GARCH Modeling dialog box will automatically pop-up and display all SCA data macro files

in the working directory. The wholesale price index data (PI series) is located in the FINDAT01 data macro

file under the PI procedure. Please select this data set as illustrated below.

15

The PI series may be viewed by clicking on the Preview button. Click on the Next button to enter the

ARCH/GARCH Modeling Environment.

4.1.1 Applying the automatic two-pass method

Once in the ARCH/GARCH Modeling Environment, click on the Automatic Two-Pass Method tab as shown

below and set the potential seasonality to 4 (Quarterly Series).

16

By selecting the Show/Create Graphs option, we can later validate if our assumptions are correct by

inspection of various diagnostic graphs.

Click on the Execute button and an expert system approach will be employed to determine the first

moment model and the model for the squared standardized residuals. WorkBench builds a sequence of

commands for the automatic two-pass method that is executed in the SCA System. After the SCA System

determines the appropriate ARIMA model and estimates its parameters based on its IARIMA (expert system

ARIMA modeling) capability, the residuals from the first moment model are stored. The residuals and then

standardized and squared. The IARIMA command is used for a second time to identify an ARIMA model for

the squared standardized residual series. The SCA IARIMA command is quite effective and in most cases

provides an ideal way to proceed.

A portion of the output (first moment model summary) is shown below. The user can scroll through the

output and view full diagnostics for the estimated models, print/save the output, view/edit the command file

used by the SCA engine, or go to the User-directed Two-Pass Method to make modifications to the models

estimated.

17

The table provided below is a summary of the first moment and second moment models that were

automatically identified and estimated for the PI series. For the first moment part of the model, an IMA(1,4)

model was selected with the estimate of 1 0.6178 (t=8.71)=θ and 4 1828 (t=2.05)= −θ . For the second

moment equation, what would be considered an ARCH(4) model was selected.

First Moment Model Summary (Differencing = 1) Parameter Factor Order Value Std.Error t-Value MA 1 1 .6012 .0708 8.49 MA 2 4 -.1828 .0892 -2.05 Second Moment Model Summary Parameter Factor Order Value Std.Error t-Value CNST 1 0 .0001 .00004 3.02 D-AR 1 4 .2131 .0903 2.36 MA 1 1 -.0878 .0885 -.99 MA 2 2 -.1956 .0900 -2.17

Several graphs have been automatically created and may be reviewed by clicking on the Graphs tab, as

shown below. The diagnostic graphs are organized in four sections. The first section provides visual

information about the series analyzed including a time series plot, an autocorrelation plot, and a partial

18

autocorrelation plot. The other sections provide diagnostics for the first moment model and second moment

model.

Note that the two-pass method does not produce standard residuals ( t t tˆ ˆ ˆe a /= σ ) nor does it produce a time plot

of the estimated conditional standard deviation series, Sigma.

4.1.2 Applying the user-directed one-pass method

Enders (1995, page 155) selected an ARIMA(1,0,4) first moment model for the PI series whereas the

automatic ARIMA capability of the SCA System selected a differencing operator instead of an autogressive

term. The equations with parameter estimates presented in Enders’ work is provided below. The standard

errors for the parameter estimates are provided under the coefficients.

1 1 4

21 1

.0013 .7968 .4014 0.2356(.0012) (.1141) (.1585) (.1202)1.5672 5 .2226 .6633(9.34 6) (.1067) (.1515)

− − −

− −

= + + − +

= − + +−

t t t t t

t t t

a a a

h E a hE

π π

19

Since the PI series has already been brought into the ARCH/GARCH Modeling Environment, simply click

on the User-Directed One-Pass Method tab to continue the example. The models can then be defined for the

one-pass method. Since a GARCH model is to be specified, select GARCH under the Model Option frame.

Next, specify the parameters for the first moment and second moment equations as shown below.

The WorkBench program will attempt to determine the number of residuals to drop in the maximum

likelihood estimation based on the maximum autoregressive lag or the expected number of missing residuals.

In some cases, the user must pre-specify the number of beginning residuals to omit in the maximum likelihood

summation when non-linear convergence issues arise. Unfortunately, this is often data driven and therefore

may require some trial and error in deciding the appropriate number of residuals to omit.

To adjust the MAX Lag in ML Sum, click on the Advanced Options/Setting under the View frame and edit

the estimation settings. It is also important to examine the output for warning/error messages that may occur

in estimating the GARCH model. For instance, the messages may indicate that the maximum number of

iterations were exceeded. If you should see messages of this kind, you should increase the default settings. In

the Default Estimation Settings grid, make the changes as follows:

20

Now, to estimate the model and generate various diagnostics, click on the Execute button. When the

SCAB34S engine finishes, you will automatically be placed in the Results tab where you can review the

estimation results. Below is a summary of the GARCH model estimation using the one-pass (joint estimation)

method.

Nonlinear Estimation Summary: GARCH Model ---------------------------------------------------------------------- Number of observations: 129 Number of iterations: 520 Number of Function Evals 530 Number of Gradiant Evals 522 Number of Terms Dropped: 10 Final Functional Value: 487.875 1/Condition of Hessian: 0.26955E-10 AIC (Based on LLF): -1128.63529045 Parameter Order Coefficient Std. Err. t-Value p-Value Comments C1 0 0.00176281 0.00493765 0.36 0.7217 CONS_1 AR 1 0.77451087 0.70309654 1.10 0.2729 AR MA 1 -0.38251331 0.23529208 -1.63 0.1067 MA MA 4 0.25331855 0.13801479 1.84 0.0690 MA C2 0 0.00001426 0.00002692 0.53 0.5974 CONS_2 ARCH 1 0.23291643 0.23712987 0.98 0.3280 GMA GARCH 1 0.66689634 0.29384342 2.27 0.0251 GAR

21

Standardized Error Distn. : Normal Distribution Sum of Squared Residuals : 0.01506806 Volatility of Variance : 0.52111244 Unconditional Variance : 0.00014229 Unconditional Standard Dev: 0.01192857 Diagnostic testing of standardized residuals Number of Cases : 119 Minimum Value : -2.629609 Maximum Value : 4.604357 Mean : 0.083269 Standard Deviation : 1.001289 Skewness : 0.531101 Kurtosis : 2.570206 Cumulant (6th Order): 22.874863 First Quartile : -0.529092 Third Quartile : 0.592427 Sample ACF and PACF for Standardized Residuals ---------------------------------------------------------------- Lag ACF t-Val LB-Q P-Value PACF t-Val 1 0.011 0.12 0.01 0.903 0.011 0.12 2 -0.039 -0.43 0.20 0.903 -0.039 -0.43 3 0.040 0.43 0.40 0.940 0.041 0.44 4 0.084 0.91 1.28 0.864 0.082 0.89 5 -0.146 -1.57 3.97 0.554 -0.146 -1.58 Diagnostic testing of Squared standardized residuals Sample ACF and PACF for Squared Standardized Residuals ---------------------------------------------------------------- Lag ACF t-Val LB-Q P-Value PACF t-Val 1 0.000 0.00 0.00 0.999 0.000 0.00 2 -0.022 -0.24 0.06 0.970 -0.022 -0.24 3 -0.021 -0.23 0.12 0.990 -0.021 -0.23 4 0.179 1.95 4.12 0.390 0.178 1.94 5 -0.027 -0.28 4.21 0.520 -0.029 -0.31 LaGrange Multiplier Tests Variable: Squared Standardized Residuals ---------------------------------------- Lag LM-Value P-Value 1 0.000 0.999 2 0.058 0.972 3 0.116 0.990 4 3.803 0.433 5 3.822 0.575

The results are comparable between the above output and Ender’s estimation results. Slight differences

are acceptable due to non-linear estimation settings and optimization algorithms.

Of some concern is the computational method to arrive at the appropriate standard errors for the model

parameters. The B34S CMAXF2 calculates the standard error of the parameters as the square root of the

absolute value of the diagonal elements of the inverse of the Hessian as calculated by the IMSL routine

22

DBONF. The SE calculation is susceptible to differences in the computational algorithm used to solve the

model. IMSL reports that their Hessian is a BFGS approximation of the Hessian at the solution.

4.2 GARCH Analysis of the S&P 500 Using the One-Pass Method

This example uses the monthly excess returns of the S&P 500 index from 1926-1999 to illustrate a

GARCH(1,1) model specification and estimation. This example was also used in Tsay (2002), Analysis of

Financial Time Series: Example 3.3 – page 97.

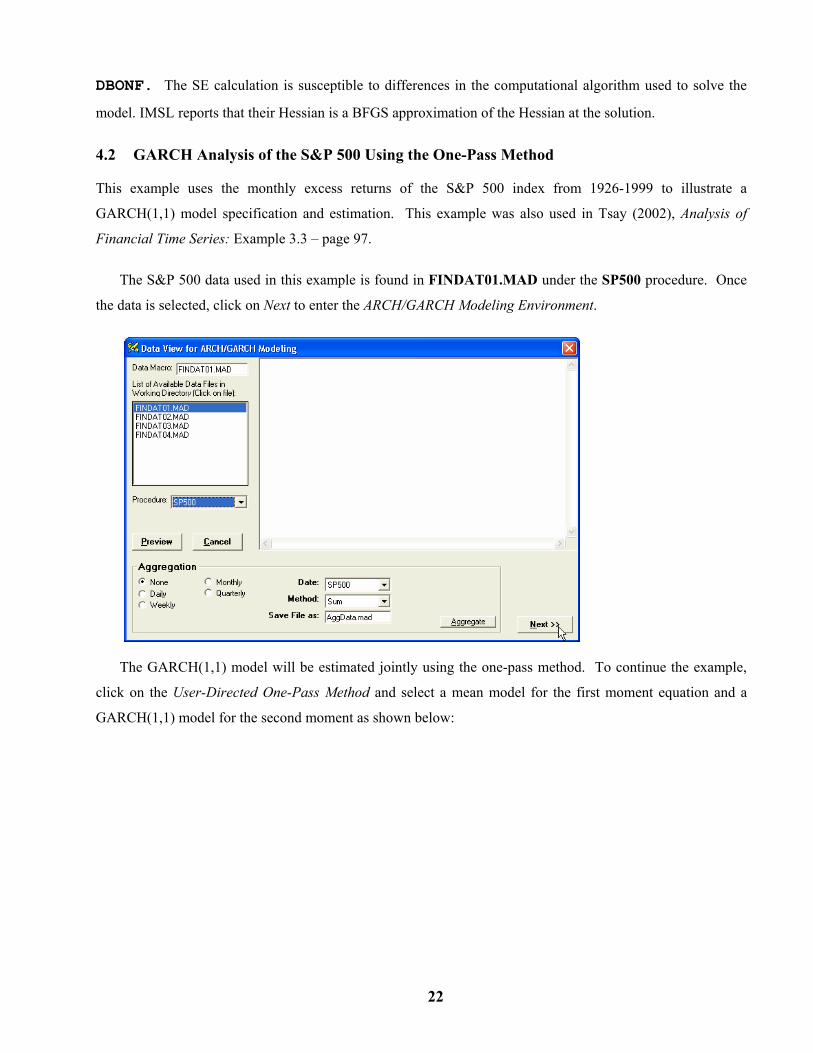

The S&P 500 data used in this example is found in FINDAT01.MAD under the SP500 procedure. Once

the data is selected, click on Next to enter the ARCH/GARCH Modeling Environment.

The GARCH(1,1) model will be estimated jointly using the one-pass method. To continue the example,

click on the User-Directed One-Pass Method and select a mean model for the first moment equation and a

GARCH(1,1) model for the second moment as shown below:

23

In his example, Tsay deletes the first four residuals. To do this in WorkBench, go to the Advanced

Options/Settings view area, and modify the value for the Max Lag in ML Sum under the Default Estimation

Settings grid. The modified setting is shown below:

24

Now, click on the Next button to estimate the model. You may also select the Show/Create Graphs option

for more detailed diagnostics. Once the SCAB34S engine finishes, you will be placed in the Results tab where

you may review the model summary and associated diagnostics. A portion of the output is shown below:

Nonlinear Estimation Summary: GARCH Model ---------------------------------------------------------------------- Number of observations: 792 Number of iterations: 36 Number of Function Evals 51 Number of Gradiant Evals 38 Number of Terms Dropped: 4 Final Functional Value: 1988.600 1/Condition of Hessian: 0.00000025 AIC (Based on LLF): -4486.18247426 Parameter Order Coefficient Std. Err. t-Value p-Value Comments C1 0 0.00766466 0.00151899 5.05 0.0000 CONS_1 C2 0 0.00007859 0.00002594 3.03 0.0025 CONS_2 ARCH 1 0.11846988 0.01860770 6.37 0.0000 GMA GARCH 1 0.85863535 0.01914510 44.85 0.0000 GAR Standardized Error Distn. : Normal Distribution Sum of Squared Residuals : 2.69744855 Volatility of Variance : 0.21642254 Unconditional Variance : 0.00343248 Unconditional Standard Dev: 0.05858735

25

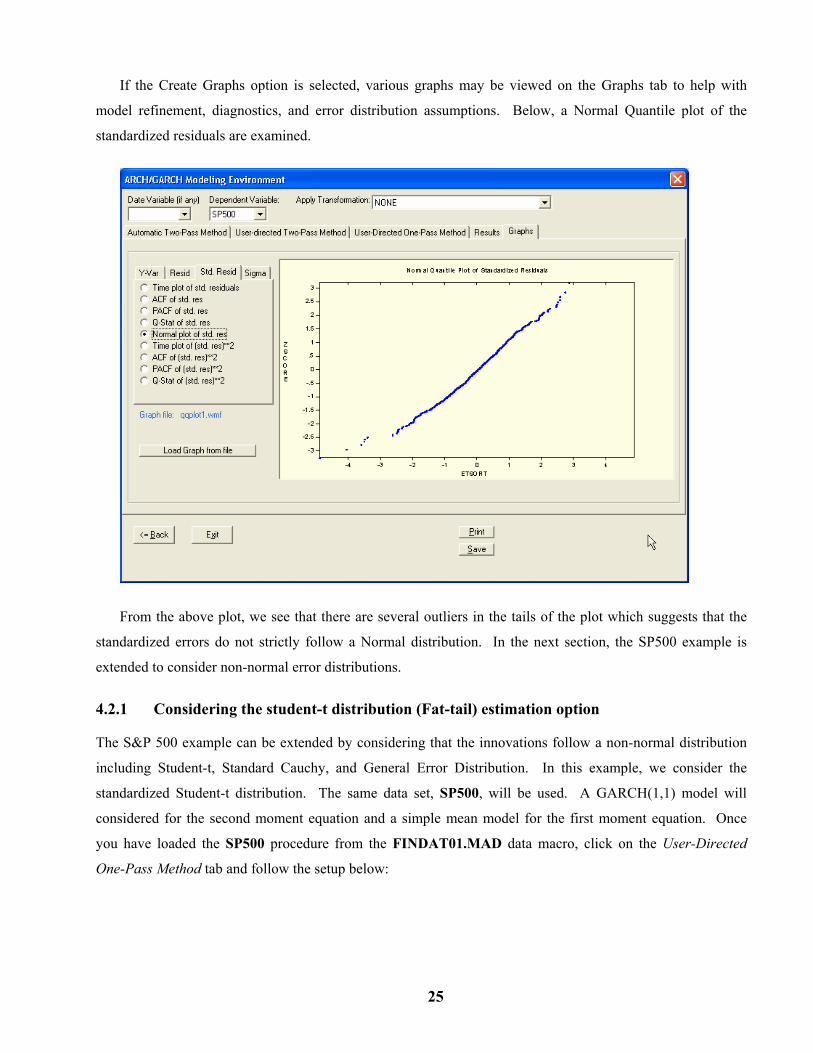

If the Create Graphs option is selected, various graphs may be viewed on the Graphs tab to help with

model refinement, diagnostics, and error distribution assumptions. Below, a Normal Quantile plot of the

standardized residuals are examined.

From the above plot, we see that there are several outliers in the tails of the plot which suggests that the

standardized errors do not strictly follow a Normal distribution. In the next section, the SP500 example is

extended to consider non-normal error distributions.

4.2.1 Considering the student-t distribution (Fat-tail) estimation option

The S&P 500 example can be extended by considering that the innovations follow a non-normal distribution

including Student-t, Standard Cauchy, and General Error Distribution. In this example, we consider the

standardized Student-t distribution. The same data set, SP500, will be used. A GARCH(1,1) model will

considered for the second moment equation and a simple mean model for the first moment equation. Once

you have loaded the SP500 procedure from the FINDAT01.MAD data macro, click on the User-Directed

One-Pass Method tab and follow the setup below:

26

Next, more iterations will be needed to satisfy the convergence criteria. After you have specified the

model above, click on the Advanced Options/Settings view area and make the following modifications to the

Default Estimation Settings grid.

To estimate the GARCH(1,1) model under the assumption that the innovations follow a standardized

Student-t distribution, click on the Execute button. The model estimates and diagnostics will be displayed in

27

the Results tab when the SCAB34S engine has completed. It should be noted that FAT-TAIL estimation is

CPU intensive and it will take some time for the engine to return to WorkBench. Depending on your

processor speed, estimation may take several minutes to return (a 2GhZ machine takes approximately 45

seconds to execute this example).

Nonlinear Estimation Summary: GARCH Model ---------------------------------------------------------------------- Number of observations: 792 Number of iterations: 620 Number of Function Evals 636 Number of Gradiant Evals 622 Number of Terms Dropped: 1 Final Functional Value: 1730.110 1/Condition of Hessian: 0.24452E-08 AIC (Based on LLF): -4613.43414381 Parameter Order Coefficient Std. Err. t-Value p-Value Comments C1 0 0.00830924 0.00157401 5.28 0.0000 CONS_1 C2 0 0.00016910 0.00005381 3.14 0.0017 CONS_2 ARCH 1 0.12270036 0.02647065 4.64 0.0000 GMA GARCH 1 0.81930093 0.03290197 24.90 0.0000 GAR D.F. 0 6.50587826 0.46563938 13.97 0.0000 VD Standardized Error Distn. : t-Distribution (Exact) Sum of Squared Residuals : 2.70670274 Volatility of Variance : 0.24806268 Unconditional Variance : 0.00291563 Unconditional Standard Dev: 0.05399657

The results from Tsay (2002, page 99) are provided below:

2 2 21 1

.0083

.00017 .1227 .8193− −

= +

= + +t t

t t t

r a

aσ σ

4.2.2 Considering a GARCH-M model for the S&P 500 monthly returns

A GARCH-M model may be entertained by an analyst considering that the return of an asset may depend upon

its volatility. This example looks at this phenomenon using a GARCH(1,1)-M model specification for the

monthly excess returns of the S&P 500 index. Again, we use the same data set which is the SP500 procedure

found in the FINDAT01.MAD data macro file.

To specify a GARCH-M model, click on the User-Directed One-Pass Method tab, choose the GARCH-M

model option, and modify the model information as shown below. Be sure to unselect the Cond. StdDev. Box

to use the conditional variance in the log likeliood function opposed to the default conditional standard

deviation.

28

To estimate the GARCH-M model, click on the Execute button. As with the FAT-TAIL option, a

GARCH-M model is CPU intensive and will take some time to complete. This example took approximately

25 seconds on a 2Ghz. Computer. The results are presented below:

Nonlinear Estimation Summary: GARCH-M Model ---------------------------------------------------------------------- Number of observations: 792 Number of iterations: 353 Number of Function Evals 371 Number of Gradiant Evals 355 Number of Terms Dropped: 1 Final Functional Value: 1989.142 1/Condition of Hessian: 0.39470E-09 AIC (Based on LLF): -4547.26382905 Parameter Order Coefficient Std. Err. t-Value p-Value Comments C1 0 0.00259727 0.00223813 1.16 0.2462 CONS_1 Delta 0 1.97279196 0.82937374 2.38 0.0176 MU C2 0 0.00013680 0.00003287 4.16 0.0000 CONS_2 ARCH 1 0.13495986 0.02066926 6.53 0.0000 GMA GARCH 1 0.82188077 0.02125851 38.66 0.0000 GAR Standardized Error Distn. : Normal Distribution Sum of Squared Residuals : 2.72436841 Volatility of Variance : 0.25972847 Unconditional Variance : 0.00316969 Unconditional Standard Dev: 0.05630001

The results from Tsay (2002, page 101) are provided below:

29

2

2 2 21 1

.0028 1.99

.00016 .1328 .8137− −

= + +

= + +t t t

t t t

r a

a

σ

σ σ

4.3 Regression plus GARCH Models Using IBM returns and S&P 500 Series

It is often of interest to examine the behavior of a series based on its relationship to leading indicators or other

stochastic variables. The examples in this section illustrate how to incorporate regression variables in the first

moment model while entertaining a GARCH process in the second moment model. The excess monthly

returns of the IBM stock price is modeled as a function of the S&P 500 index in the first moment model.

4.3.1 Modeling IBM stock returns and the S&P 500 index using the automatic two-pass method

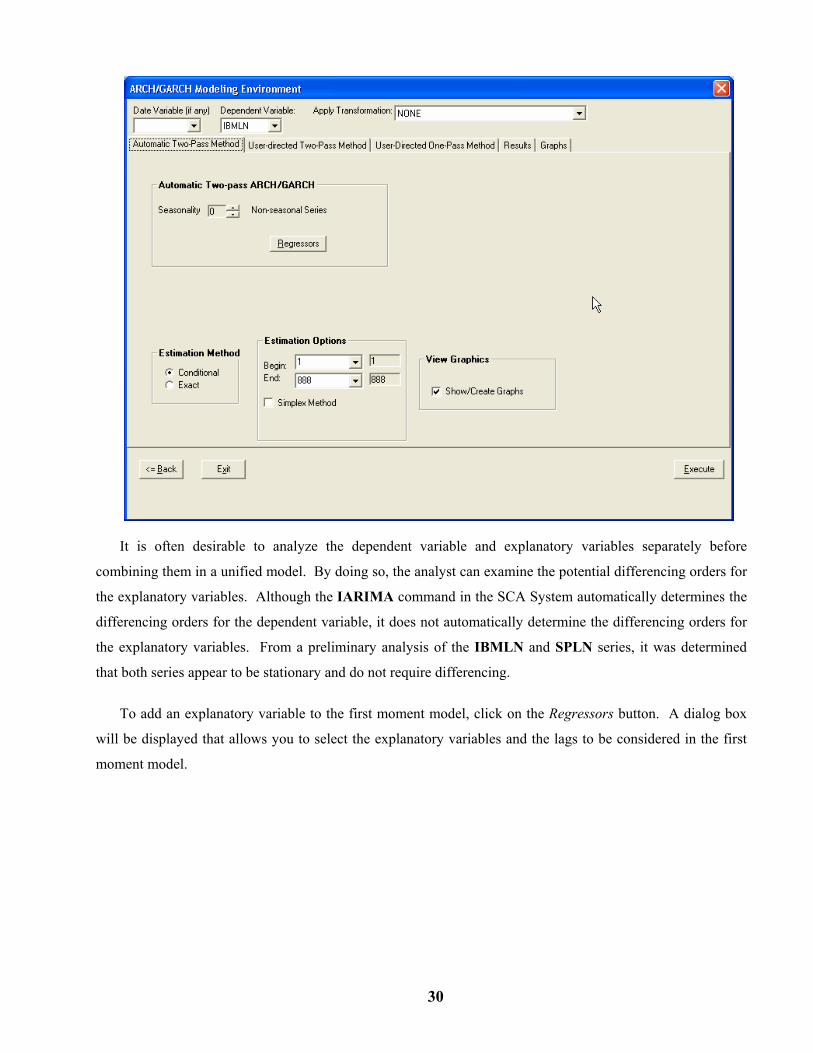

The data for this example is found in the FINDAT01.MAD data macro file under the M_IBMLN2 procedure

name. Once the M_IBMLN2 procedure is selected for the ARCH/GARCH Analysis application, click on the

Automatic Two-Pass Method tab.

The IBMLN series is the monthly returns of the IBM stock price from January 1926 through December

1991. It is contended that the S&P 500 monthly returns is related to the IBM stock price, however we are not

certain at what lags this potential relationship exists. One method that can be used to examine the lag

relationship between the IBMLN and SPLN series is to employ the automatic model identification capabilities

of the SCA System via the automatic two-pass method.

The IBMLN monthly series does not exhibit a seasonal behavior, therefore in the Automatic Two-Pass

Method tab, the series is marked as non-seasonal. If the user is unsure whether seasonality is present, the

dependent series can be marked as a monthly series and the SCA System will consider seasonal terms in the

model. If the seasonal parameters are not significant, the automatic modeling procedure will not include them.

30

It is often desirable to analyze the dependent variable and explanatory variables separately before

combining them in a unified model. By doing so, the analyst can examine the potential differencing orders for

the explanatory variables. Although the IARIMA command in the SCA System automatically determines the

differencing orders for the dependent variable, it does not automatically determine the differencing orders for

the explanatory variables. From a preliminary analysis of the IBMLN and SPLN series, it was determined

that both series appear to be stationary and do not require differencing.

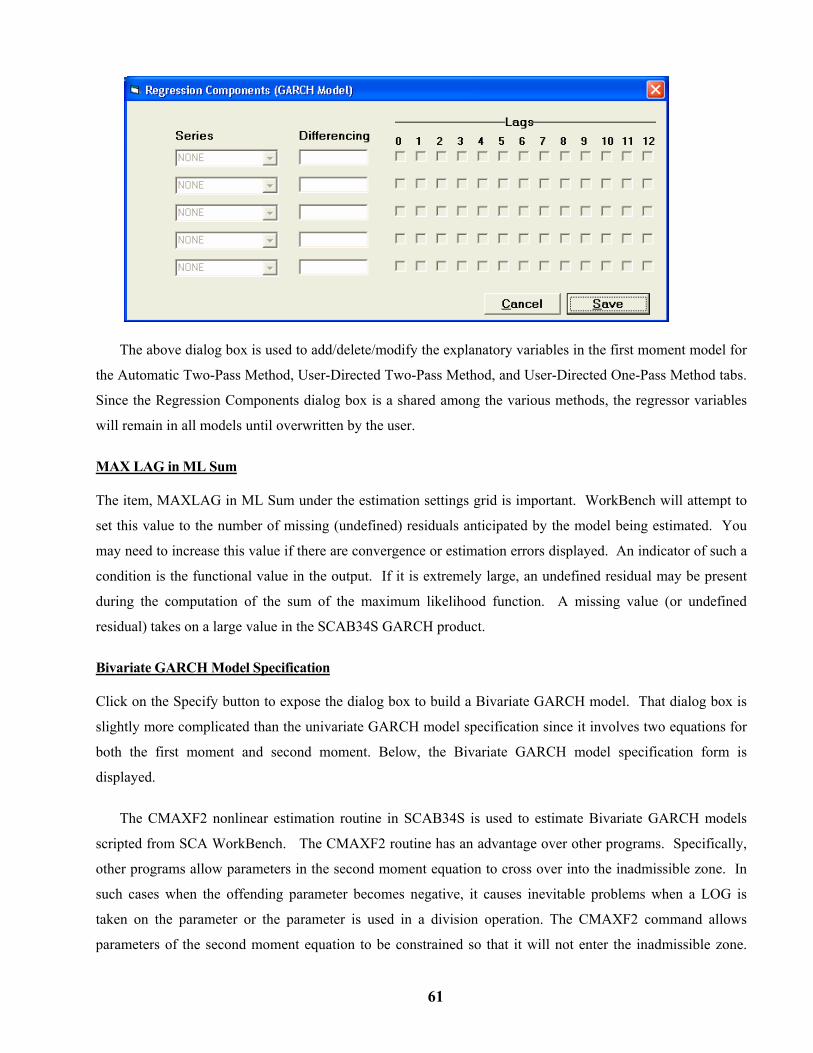

To add an explanatory variable to the first moment model, click on the Regressors button. A dialog box

will be displayed that allows you to select the explanatory variables and the lags to be considered in the first

moment model.

31

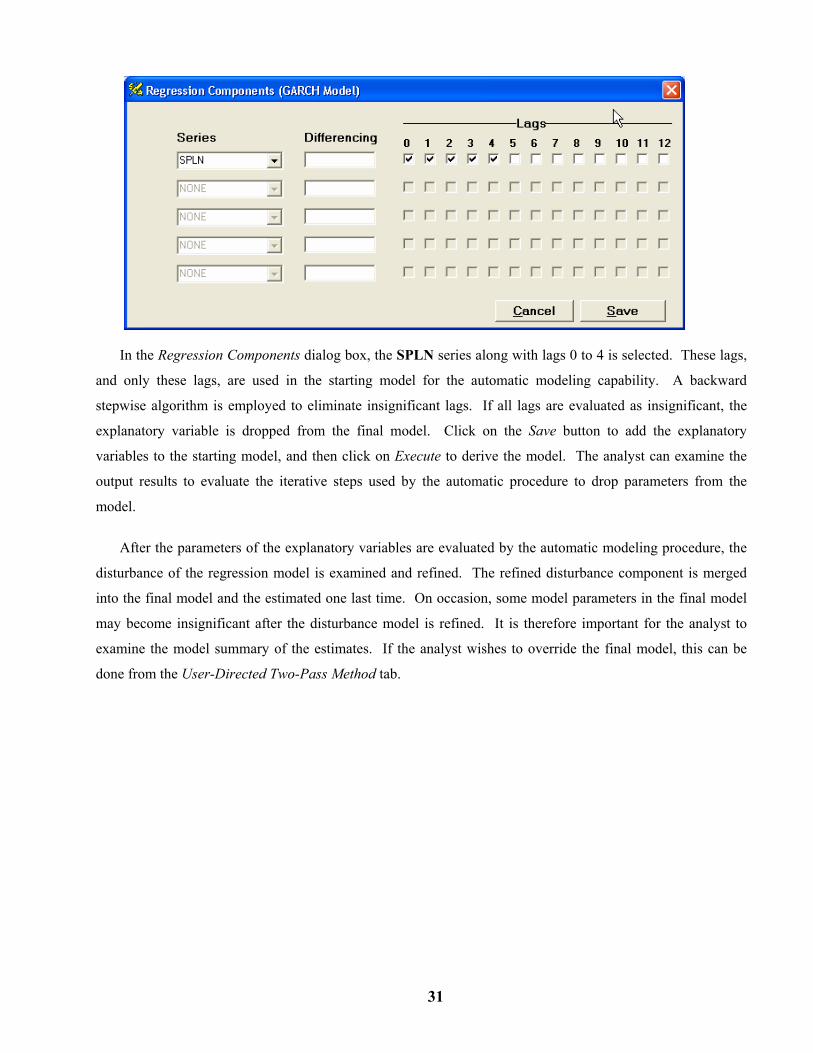

In the Regression Components dialog box, the SPLN series along with lags 0 to 4 is selected. These lags,

and only these lags, are used in the starting model for the automatic modeling capability. A backward

stepwise algorithm is employed to eliminate insignificant lags. If all lags are evaluated as insignificant, the

explanatory variable is dropped from the final model. Click on the Save button to add the explanatory

variables to the starting model, and then click on Execute to derive the model. The analyst can examine the

output results to evaluate the iterative steps used by the automatic procedure to drop parameters from the

model.

After the parameters of the explanatory variables are evaluated by the automatic modeling procedure, the

disturbance of the regression model is examined and refined. The refined disturbance component is merged

into the final model and the estimated one last time. On occasion, some model parameters in the final model

may become insignificant after the disturbance model is refined. It is therefore important for the analyst to

examine the model summary of the estimates. If the analyst wishes to override the final model, this can be

done from the User-Directed Two-Pass Method tab.

32

The final model identified by the automatic two-pass method is displayed in the Results tab. Here, lags 0, 1,

and 2 are retained in the final model. Lags 3 and 4 were deleted. A summary of the parameter estimates for

the first moment and second moment equations is presented below.

First Moment Model Summary (No differencing) Parameter Factor Order Value Std.Error t-Value CNST 1 0 .8384 .1758 4.77 SPLN-0 1 0 0.7517 .0309 24.35 SPLN-1 1 1 0.0684 .0310 2.21 SPLN-2 1 2 -.0646 .0309 -2.09 Second Moment Model Summary Parameter Factor Order Value Std.Error t-Value CNST 1 0 26.7360 1.9848 13.47

33

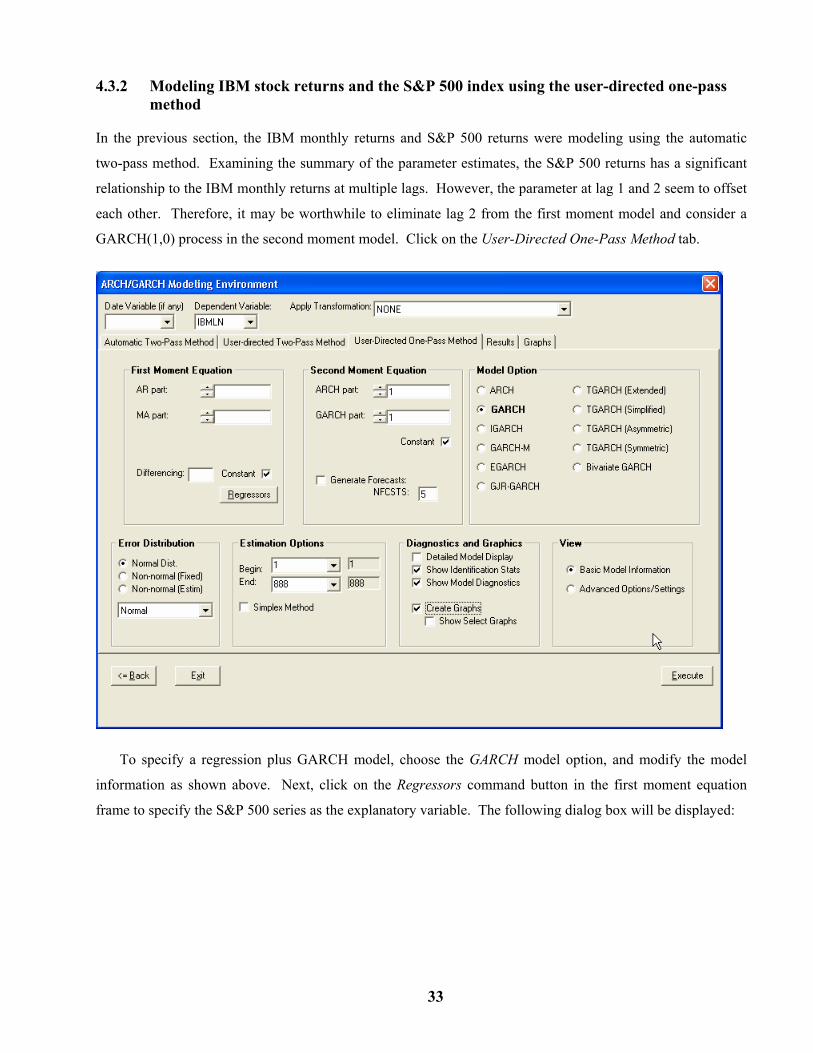

4.3.2 Modeling IBM stock returns and the S&P 500 index using the user-directed one-pass method

In the previous section, the IBM monthly returns and S&P 500 returns were modeling using the automatic

two-pass method. Examining the summary of the parameter estimates, the S&P 500 returns has a significant

relationship to the IBM monthly returns at multiple lags. However, the parameter at lag 1 and 2 seem to offset

each other. Therefore, it may be worthwhile to eliminate lag 2 from the first moment model and consider a

GARCH(1,0) process in the second moment model. Click on the User-Directed One-Pass Method tab.

To specify a regression plus GARCH model, choose the GARCH model option, and modify the model

information as shown above. Next, click on the Regressors command button in the first moment equation

frame to specify the S&P 500 series as the explanatory variable. The following dialog box will be displayed:

34

Using the dropdown box, select the SPLN series and put checks in the lag 0 box only as shown. To add

the regression component to the first moment equation, click on the Save button. You may add/delete/modify

regression components in the model through this dialog box.

For this example, the default starting values and parameter constraints are fine. The starting values for the

regression parameters are automatically derived using OLS estimation. The starting values and parameter

constraints can be modified by selecting the Advanced Options/Settings option in the View frame. Once the

first moment and second moment equations are specified, click on the Execute button to estimate the model

and generate the model diagnostics. The results are provided below:

Nonlinear Estimation Summary: GARCH Model ---------------------------------------------------------------------- Number of observations: 888 Number of iterations: 32 Number of Function Evals 48 Number of Gradiant Evals 34 Number of Terms Dropped: 1 Final Functional Value: -1888.006 1/Condition of Hessian: 0.00032559 AIC (Based on LLF): 2966.49672120 Parameter Order Coefficient Std. Err. t-Value p-Value Comments C1 0 0.87664543 0.16913978 5.18 0.0000 CONS_1 SPLN 0 0.75020949 0.03100246 24.20 0.0000 INPUT 1 C2 0 2.73574407 0.33594045 8.14 0.0000 CONS_2 ARCH 1 0.07452358 0.01355494 5.50 0.0000 GMA GARCH 1 0.82749572 0.01487442 55.63 0.0000 GAR Standardized Error Distn. : Normal Distribution Sum of Squared Residuals : 23923.58681429 Volatility of Variance : 0.15418985 Unconditional Variance : 27.92125424 Unconditional Standard Dev: 5.28405661

35

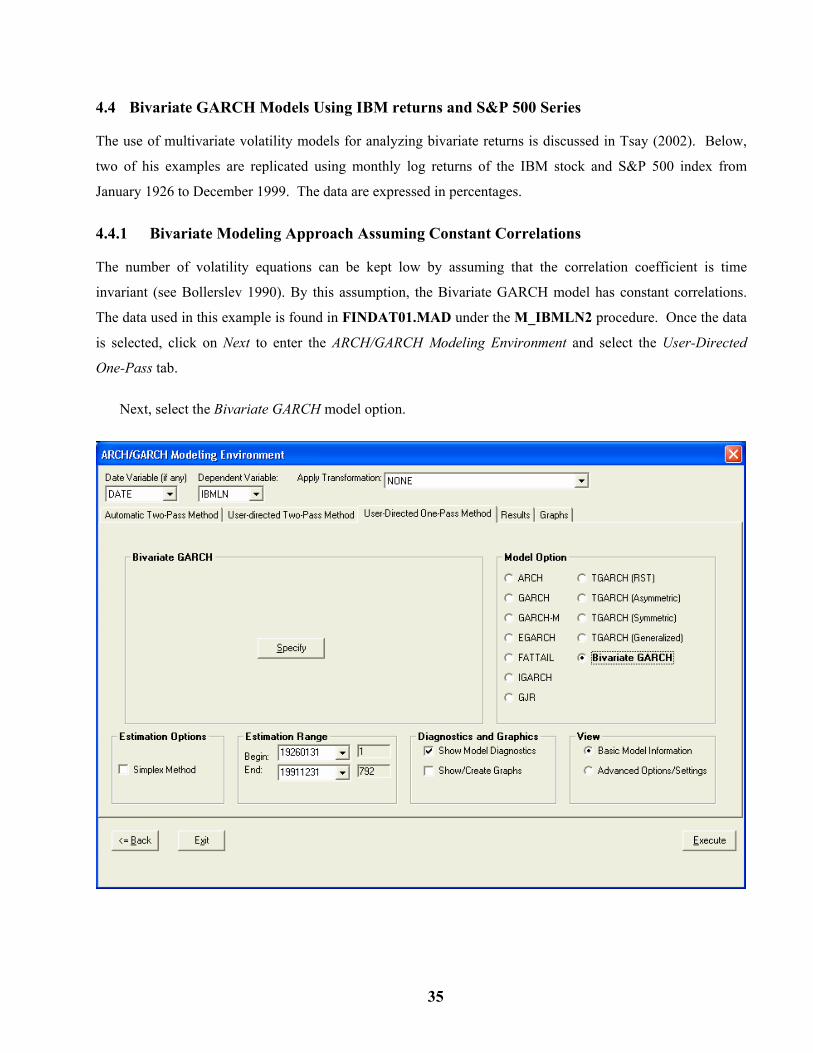

4.4 Bivariate GARCH Models Using IBM returns and S&P 500 Series

The use of multivariate volatility models for analyzing bivariate returns is discussed in Tsay (2002). Below,

two of his examples are replicated using monthly log returns of the IBM stock and S&P 500 index from

January 1926 to December 1999. The data are expressed in percentages.

4.4.1 Bivariate Modeling Approach Assuming Constant Correlations

The number of volatility equations can be kept low by assuming that the correlation coefficient is time

invariant (see Bollerslev 1990). By this assumption, the Bivariate GARCH model has constant correlations.

The data used in this example is found in FINDAT01.MAD under the M_IBMLN2 procedure. Once the data

is selected, click on Next to enter the ARCH/GARCH Modeling Environment and select the User-Directed

One-Pass tab.

Next, select the Bivariate GARCH model option.

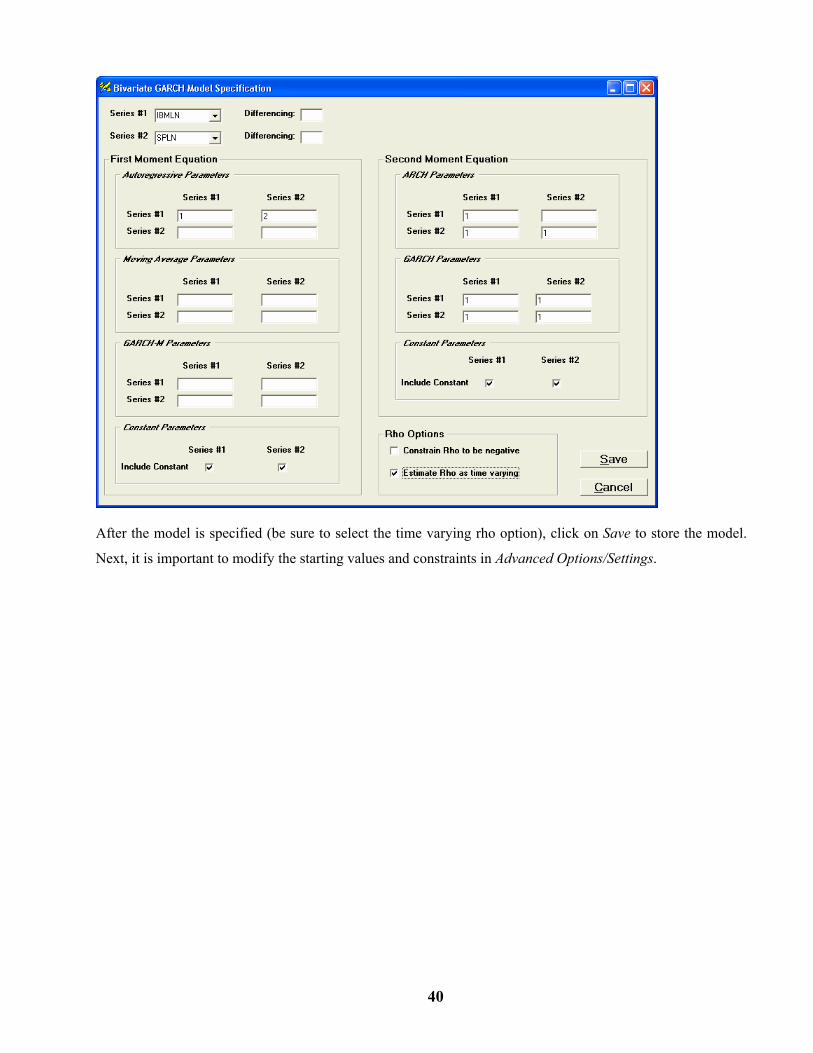

36

Click on the Specify button to expose the dialog box to build a Bivariate GARCH model. That dialog box

is slightly more complicated than the univariate GARCH model specification since it involves two equations

for both the first moment and second moment.

Above, Series #1 is set to the IBM monthly returns (IBMLN) and Series #2 is set to the S&P 500 index.

As in the univariate GARCH case, the orders of the parameter are specified in the text boxes provided. Here, a

multivariate GARCH(1,1) model is specified with constant correlations. After the Bivariate GARCH model is

specified, click on Save and you will be returned to the GARCH modeling environment.

Now, select the Advanced Options/Settings option and overwrite the Maxlag in ML Sum so that it equals 3.

The default starting values and constraints will be used.

37

Now, click on Execute to estimate the Bivariate GARCH model. It may take a few minutes to complete

since these types of models are computationally intensive. When estimation has completed, you will be placed

in the Output viewer. The complete output provides diagnostic statistics for both model identification and for

evaluating the fit of the model employed. A portion of the output is displayed below.

38

The SCAB34S GARCH program constrains the ARCH/GARCH parameters to be positive during

estimation since the parameters have a theoretical lower bound of zero. The final functional value obtained

here (3698.99) differs slightly from the RATS results (3691.21) stated in Tsay for this reason. If desired, you

may override the lower bounds of the GAR12_1, GAR21_1 and GMA21_1 model parameters using the

Advanced Options/Settings option. Please note however that you will then allow those model parameters to

enter the inadmissible zone and possibly make the estimation unstable.

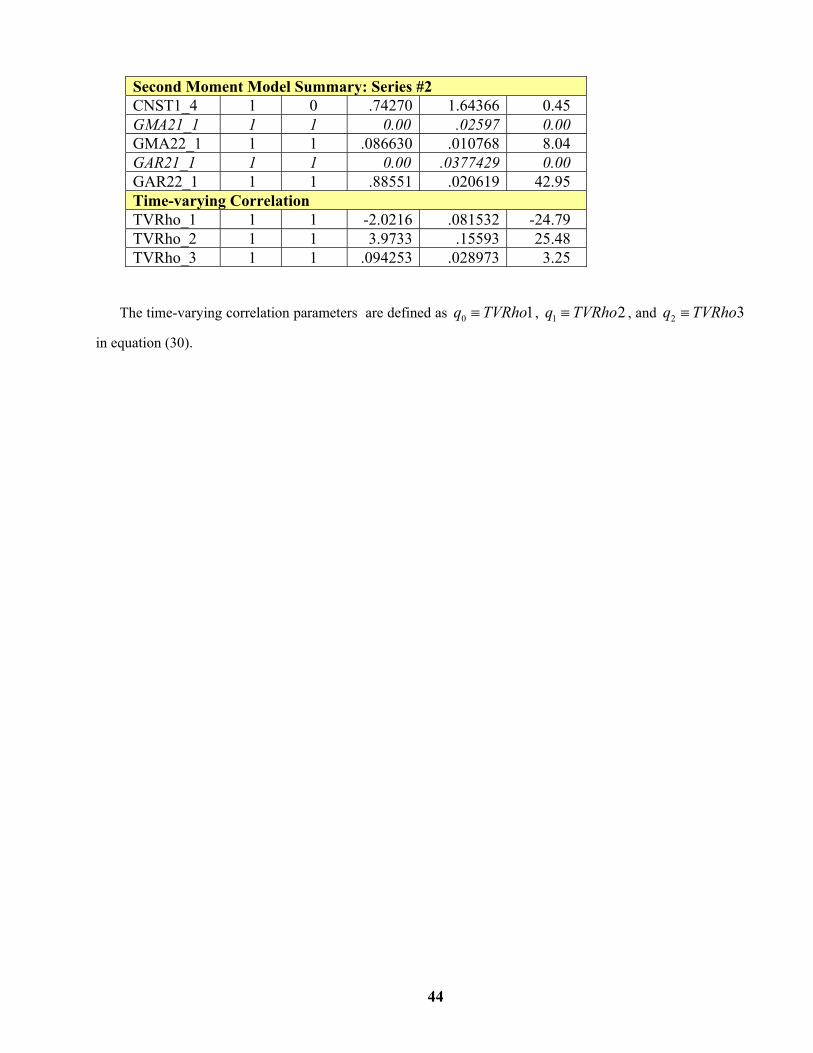

First Moment Model Summary (No differencing): Series #1 Parameter Factor Order Value Std.Error t-Value CNST1_1 1 0 1.28139 .20015 6.40 AR11_1 1 1 .072210 .02459 2.94 AR11_2 1 2 .051038 .034804 1.47 AR12_2 1 2 -0.11419 .043722 -2.61 First Moment Model Summary (No differencing): Series #2 CNST1_2 1 0 .68502 .14645 4.68 Second Moment Model Summary: Series #1 Parameter Factor Order Value Std.Error t-Value CNST1_3 1 0 3.2582 .631996 5.16 GMA11_1 1 1 .082307 .0079985 10.29

39

GAR11_1 1 1 .841529 .0079779 105.48 GAR12_1 1 1 0.00 .01182 0.00 Second Moment Model Summary: Series #2 CNST1_4 1 0 .793620 .24928 3.18 GMA21_1 1 1 0.00 .005846 0.00 GMA22_1 1 1 .079812 .017067 4.67 GAR21_1 1 1 0.00 .027117 0.00 GAR22_1 1 1 .8894 .016578 53.65 Constant Correlation Rho 1 1 .60165 .022304 26.97

4.4.2 Bivariate Modeling Approach Assuming Time-varying Correlations

When studying the relationship of two or more assets over an elongated time period, the correlation coefficient

of a multivariate GARCH model may not be constant. This especially true for this example where the

S&P500 index is a weighted average of various stocks. The composition of the index may change over time as

may the individual weighting of the stocks.

To continue the example from the previous section, once again select the M_IBMLN2 from the

FINDAT01.MAD file.

Next, select the Bivariate GARCH model option under the User-Directed One-Pass Method tab and modify

the model as shown:

40

After the model is specified (be sure to select the time varying rho option), click on Save to store the model.

Next, it is important to modify the starting values and constraints in Advanced Options/Settings.

41

The starting values of most model parameters need to be changed for estimation purposes. As in the

previous example, the Max Lag in ML Sum value should be set equal to 3. The above form does not show all

parameter starting values and constraints. Therefore, the settings used in this example are provided below for

reference.

Parameter Label LCL UCL Initial Value

AR11_1 -100000.0 100000.0 .08

AR12_2 -100000.0 100000.0 -.07

GAR11_1 0.0 100000.0 .87

GAR12_1 0.0 100000.0 .01

GAR21_1 0.0 100000.0 .01

GAR22_1 0.0 100000.0 .92

GMA11_1 0.0 100000.0 .08

GMA21_1 0.0 100000.0 .04

42

GMA22_1 0.0 100000.0 .05

CNST1_1 -100000.0 100000.0 1.4

CNST1_2 -100000.0 100000.0 0.7

CNST_2_1 -100000.0 100000.0 2.95

CNST2_2 -100000.0 100000.0 2.05

Rho_1 -100000.0 100000.0 -2.0

Rho_2 0.0 100000.0 3.0

Rho_3 0.0 100000.0 0.1

The starting values of Bivariate GARCH models influence estimation greatly. If you employ the time-varying GARCH option, it is recommended that you first estimate the Bivariate GARCH model with constant correlations, and then use those estimates as starting values for the more complex time-varying correlation model.

After setting the initial values for the model parameters, click on Execute to estimate the model. It will

take a minute or two to estimate this model. When it has completed, the output window will be displayed.

43

In reviewing the estimated results, we note that the functional value is (3685.44) which is better than the

constant correlation model (3698.99). We also note that the estimated coefficients of GAR12_1, GAR21_1,

and GMA21_1 are zero. Tsay (2002) allows these parameters to be negative in his example. You may modify

the starting values and lower bounds of these parameters if you wish to replicate the results in Tsay. However,

in general, it is not recommended unless there is valid reasons to allow these parameters to overstep its

theoretical limits.

First Moment Model Summary (No differencing): Series #1 Parameter Factor Order Value Std.Error t-Value CNST1_1 1 0 1.30938 .20899 6.27 AR11_1 1 1 .070150 .027758 2.53 AR12_2 1 2 -0.69000 .031585 -2.18 First Moment Model Summary (No differencing): Series #2 CNST1_2 1 0 .671625 .142150 4.72 Second Moment Model Summary: Series #1 Parameter Factor Order Value Std.Error t-Value CNST1_3 1 0 3.95296 .59568 6.64 GMA11_1 1 1 .100807 .0021885 4.61 GAR11_1 1 1 .80876 .044682 18.10 GAR12_1 1 1 0.00 .044206 0.00

44

Second Moment Model Summary: Series #2 CNST1_4 1 0 .74270 1.64366 0.45 GMA21_1 1 1 0.00 .02597 0.00 GMA22_1 1 1 .086630 .010768 8.04 GAR21_1 1 1 0.00 .0377429 0.00 GAR22_1 1 1 .88551 .020619 42.95 Time-varying Correlation TVRho_1 1 1 -2.0216 .081532 -24.79 TVRho_2 1 1 3.9733 .15593 25.48 TVRho_3 1 1 .094253 .028973 3.25

The time-varying correlation parameters are defined as 0 1q TVRho≡ , 1 2q TVRho≡ , and 2 3q TVRho≡

in equation (30).

45

5 A DETAILED DESCRIPTION OF THE GARCH APPLICATION INTERFACE IN WORKBENCH

SCA WorkBench provides a graphical user interface to the SCA Statistical System, and the SCAB34S Applet

Collection or the B34S ProSeries Econometric System for advanced ARCH and GARCH modeling. Below is

a summary of the forms of ARCH/GARCH models that may be specified through the SCA WorkBench

interface

Two-pass Estimation Method:

Model Form Estimation Source ARCH SCA System (EXPERT) GARCH(*) SCA System (EXPERT)

(*) A GARCH model estimated using the two-pass method is not directly comparable to a GARCH model

estimated using the one-pass (joint) method.

One-pass Estimation Method:

Model Form Estimation Source ARCH SCAB34S Applet Collection (GARCH) or B34S ProSeries GARCH SCAB34S Applet Collection (GARCH) or B34S ProSeries GARCH-M SCAB34S Applet Collection (GARCH) or B34S ProSeries GARCH (Integrated) SCAB34S Applet Collection (GARCH) or B34S ProSeries GARCH (non-normal dist) SCAB34S Applet Collection (GARCH) or B34S ProSeries GARCH (Glosten) SCAB34S Applet Collection (GARCH) or B34S ProSeries GARCH (Exponential) SCAB34S Applet Collection (GARCH) or B34S ProSeries GARCH (Threshold) SCAB34S Applet Collection (GARCH) or B34S ProSeries GARCH (Bivariate) SCAB34S Applet Collection (GARCH) or B34S ProSeries

5.1 Data View for ARCH/GARCH Modeling When you enter the ARCH/GARCH Modeling environment, you must select an SCA data macro (*.MAD) as

a data source. If your data is organized in plain ASCII format, WorkBench will automatically convert it into a

temporary SCA data macro. The temporary file is then accessible from the file list box. To view files with