GEICO: The “Growth Company” that made the “Value … · both Benjamin Graham and Warren...

30

GEICO: The “Growth Company” that made the “Value Investing” careers of both Benjamin Graham and Warren Buffett In 1948, we made our GEICO investment and from then on, we seemed to be very brilliant people. Benjamin Graham, 1976 Becky Quick (CNBC): “If you could keep one company that Berkshire owns, either a wholly- owned subsidiary, or that Berkshire owns a common equity in, which one would you keep and why?” Warren Buffett: “I would keep GEICO. It goes back to the -- 62 years ago it changed my life. It's also a wonderful company. I would have both things going for me, but that if I hadn't of gone to GEICO when I was 20 years-old and had a fellow there explain the insurance business to me, my life would be vastly different. So I just have to - - I'd have to choose GEICO.” CNBC interview March 13, 2013 Two of the greatest "Value" investors of all-time owe a substantial part of their wealth and public reputations – and deserved accolades - to a singular great “Growth” company, the Government Employees Insurance Company (GEICO). In the vernacular of investing, “Value” and “Growth” are most often associated with competing, mutually exclusive investing styles. It shouldn’t be so, but as a +30-year veteran in the investing “business” I can assure you that this investing-style division is deeply embedded in the investment management industry. Benjamin Graham’s deserved sobriquets include the “Father of Security Analysis” and the “Dean of Value Investing.” Of course Warren Buffett is known around the globe as the “Oracle of Omaha,” as well as Benjamin’s Graham’s greatest student. Like many of us in our chosen profession, we sit on the shoulders of the greats. We hope to never stop studying and learning from the masters. I was ever fortunate to get hooked on the stock market my junior year in college in 1984. My Investments 334 professor introduced me to, and encouraged me to read about the likes of Benjamin Graham, John Templeton, Warren Buffett, Philip Fisher, John Maynard Keynes, etc. The guiding principles of our investment philosophy at Wedgewood Partners are the classic tenets of both “Value” and “Growth” investing.

-

Upload

nguyendang -

Category

Documents

-

view

218 -

download

0

Transcript of GEICO: The “Growth Company” that made the “Value … · both Benjamin Graham and Warren...

GEICO:The“GrowthCompany”thatmadethe“ValueInvesting”careersofbothBenjaminGrahamandWarrenBuffett

In1948,wemadeourGEICOinvestmentandfromthenon,weseemedtobeverybrilliantpeople.

BenjaminGraham,1976

BeckyQuick(CNBC):“IfyoucouldkeeponecompanythatBerkshireowns,eitherawholly-ownedsubsidiary,orthatBerkshireownsacommonequityin,whichonewouldyoukeepand

why?”

WarrenBuffett:“IwouldkeepGEICO.Itgoesbacktothe--62yearsagoitchangedmylife.It'salsoawonderfulcompany.Iwouldhaveboththingsgoingforme,butthatifIhadn'tofgonetoGEICOwhenIwas20years-oldandhadafellowthereexplaintheinsurancebusinesstome,my

lifewouldbevastlydifferent.SoIjusthaveto--I'dhavetochooseGEICO.”CNBCinterviewMarch13,2013

Two of the greatest "Value" investors of all-time owe a substantial part of theirwealth and public reputations – and deserved accolades - to a singular great“Growth”company,theGovernmentEmployeesInsuranceCompany(GEICO).Inthevernacular of investing, “Value” and “Growth” are most often associated withcompeting,mutuallyexclusiveinvestingstyles.Itshouldn’tbeso,butasa+30-yearveteranintheinvesting“business”Icanassureyouthatthisinvesting-styledivisionisdeeplyembedded in the investmentmanagement industry. BenjaminGraham’sdeservedsobriquetsincludethe“FatherofSecurityAnalysis”andthe“DeanofValueInvesting.” Of courseWarrenBuffett isknownaround theglobeas the “OracleofOmaha,”aswellasBenjamin’sGraham’sgreateststudent.Likemanyofusinourchosenprofession,wesitontheshouldersofthegreats.Wehopetoneverstopstudyingandlearningfromthemasters.Iwaseverfortunatetogethookedonthestockmarketmyjunioryearincollegein1984.MyInvestments334 professor introduced me to, and encouraged me to read about the likes ofBenjamin Graham, John Templeton, Warren Buffett, Philip Fisher, John MaynardKeynes, etc. The guiding principles of our investment philosophy atWedgewoodPartnersaretheclassictenetsofboth“Value”and“Growth”investing.

2

Buffett’s evolving investment philosophy has oft been self-described as “85%Grahamand15%Fisher.”CharlieMunger’s“Growth”influenceonBuffettdeservesspecialmentiononthisscore.AnyonewhohasstudiedthecareersofeitherGrahamorBuffetthassurelycometorecognizethenotableinfluenceandimpactthatGEICOhashadonbothofthesemasters.Indeed,thenearlyfourscorehistoryofGEICOisabarnburnertaleofbirth,incrediblegrowth,tragicnear-failure,unlikelyrebirthandthen incredible growth once again. GEICOmay have bondedGraham andBuffettevenmorethantheirsignificantprofessor-studentbond.ThelonghistoryofGEICOoffers students of investing plenty of lessons on of both “Value” and “Growth”investing. Dare I say that the investment lessonsof theGEICO story aloneare sopoignant and instructive to apply to one’s own investment education that evenacavemancandoit!

GovernmentEmployeesInsuranceCompanyLeo Goodwin was born in 1886 in Lowndes Missouri. Son of a country doctor,educatedasanaccountant,LeoandhiswifeLillianGoodwinfoundedGEICOin1936.At the time,50year-oldGoodwinwasanaccountantatSanAntonio-basedUnitedServicesAutomobileAssociation(USAA).USAAwasfoundedin1922byagroupofU.S. Army officers in order to self-insure each other’s automobile insurance.Apparentlyatthetime,Armyofficerswereconsideredrecklessdrivers.Goodwin’sbrilliant insight was an expansion of USAA’s concept - bypassing commissionedinsurance salesmen and selling low cost auto insurance through the mail atdiscounts of -30% to -40% directly to federal, state and municipal governmentemployeesandcertaincategoriesofenlistedmilitaryofficers,whostatisticallyhadlower claims than the public as awhole. Themilitary list of potential customerswouldsoonexpandtoincludeactiveandreservecommissionedofficersandthefirstthree pay grades of non-commissioned officers, plus veterans on active duty.Governmentdefensecontractorsand facultymembersof collegesanduniversitiesweresoonsolicited.TheGoodwin’sfoundedGEICOwithFt.WorthbankerCleavesRhea.TheGoodwin’sputup$25,000inseedcapital,Rheaandhisrelativesputup$75,000.Goodwinandhiswifeworkedliterallyaroundtheclock,twelvehourseverydaywithnaryadayoff. On the weekends, Mr. Goodwin drove to military bases to pitch his carinsurance toyoungservice families. Mrs.GoodwinstayedbackatHQ(likely theirkitchentable)andtookthehelmasbookkeeper,underwriter,andchippedinonthemarketingfronttoo.Theircombinedsalarywasallof$250permonth.Withintheirfirstyeartheyhadwrittenover3,700policiesandcollected$104,000inpremiums.$27.62forcarinsurance-ah,thegood‘oldays!In1937theCompany’soperationswererelocatedtoWashington,D.C.inordertobeclosertothecountry’slargestpoolofgovernmentworkers.By1940policies in forcewould grow toover25,000andpremiumsgrew to $1.6million,plustheCompanyhadfinallybookeditsfirstunderwritingprofitof$5,000–

3

35 consecutive yearsof profits would then ensue. In the fall of 1941, a massivehailstorm descended upon the D.C. metro area damaging thousands of cars.Goodwin had the good business sense to quickly arrange with local auto repairshopstoworkaroundtheclockexclusivelyforGEICO.Inaddition,Goodwintruckedinhugeloadsofautoglass.GEICO’sreputationforcustomerserviceleftanindeliblemarkwiththelocals.By1946and1947,theCompanywasearningpremiumsof$2to$3millionperyear.Earningspershareof$1.29in1946boomedto$5.89persharein1947. WiththeCompany’s significant low-cost advantage, plus the emerging post-World War IIautomobile boom, the Company would go on to consistently post underwritingprofit for thenext35years in a row. TheCompany’s lowcost advantage in theircoreautomobileinsuranceofferingwouldpersistandendurefordecadestocome.Indeed,GEICO’sunderwritingand lossadjustmentexpensestypicallyamountedtojust 25% of premiums – at times 10-15 percentage points lower than theircompetitors,includingsuchdirectinsurancewritesasAllstateandStateFarm.Graham's journeywithGEICObegan in1948. At the time, the insurance industrywasreelingfromthesharppost-WorldWarIIinflationinducedunderwritinglosses.Inaddition,theRheafamilywaslookingtosellpartoftheir75%oftheirownershipstake. After being spurned by larger investment houses, GEICO’s investmentbankers and lawyers found their way to the Graham-Newman investmentpartnership. Graham was able not only to put aside his long-held disdain forinsurancecompanyinvestments,butthenhedidtheinexplicable–hebrokehisowninvestmentrules.Grahamrarelyallocatedmorethan5%ofhisinvestmentportfoliotoasingleinvestment.Graham,“breakingbadly,”sotospeak,putnearly25%ofhispartnership inGEICO. Thus, in1948Graham’s investmentpartnershippurchased50%ofGEICOfor$712,000. Graham’sone-halfpurchased interestamountedtoapurchaseof1,500sharesat$475pershare(a10%discounttobookvalue).Grahambecame Chairman of the Board. The investment banker in the deal (LorimerDavidson) joined the companyaspartof the transaction - andwould succeed theretiringGoodwinin1958asCEO.Later in 1948, the SECdetermined that an investment fundwas not permitted toownmorethan10%ofaninsurancecompany.TheSECdemandedthatthesalebenullified.TheRheafamilyrefusedtotakebacktheirshares.InwhatwouldturnouttobeasecondstrokeofluckforGraham-Newman,theSECthenruledthatthesalecould stand as long as Graham-Newman shares were purchased directly by thepartnership’s shareholders. The shares in GEICO were then distributed to thepartners/shareholdersofGraham-Newmaninthesummerof1948intheover-the-countermarket. GEICObecameapublicly traded stock. Theoriginaldistributionwasapproximately$27foroneshareofGEICO.In1949,theCompany’sprofitssurgedpastthe$1millionmark. Asanexampleofthelow-costadvantagewieldedbyGEICO,in1949theratiotounderwritingprofitstopremiumswas27.5%.Thesamemeasureforthe133stockcasualtycompanies

4

as calculatedbyA.M.Bestwas6.7%. By1950, theCompanyhadnearly144,000policiesinforceand$8millioninannualpremiums–andlicensedinjust15states(andofcourseD.C.).In1958,theCompany’saddressablemarketmorethantripledwhen they began to solicit nongovernmental, managerial, technical andadministrativeworkerswiththerequisiteoutstandingdrivingrecords.Overthenext25years,GEICOwouldcontinuetogrow,andgrow…andgrow.AtthetimeofGoodwin’sretirementin1958,aninvestmentof$1,000inGEICOhadgrownto $47,500. Graham and his colleagues would serve on the GEICO board forseventeenyears.In1965,Grahamresignedfromtheboard.In1971,JerryNewmanretired. NewmannominatedWarrenBuffet to takehisplaceon theGEICOboard.GrahamwrotethefollowingrecommendationtotheboardonBuffett’sbehalf:“…Iam100percentforthatidea.IhaveknownBuffettintimatelyformanyyears,andImustsaythatIhavenevermetanyoneelsewithhiscombinationofhighcharacterandbrilliant

businessqualities.Hisrecordaninvestmentfundmanagerisprobablyunequalled.Inaddition,IcanrecommendWarrenasagood-humored,easy-to-get-along-withperson,whocanlivenupyourdirectorsmeetings.Hewouldbesuretosupplymorethanhisshareofworthwhileideasfor

thebenefitoftheGEICOcompanies.”By 1972, at the Company’s then peak operating level, a single original Graham-Newmanshareof$27hadgrowninworthto$16,349–notquitetheclassicsinglecigar-puff,textbookGrahamandDoddsvillestock.Graham-Newman’soriginal1948investmentof$712,000wasworthover$400,000,00025years later. Grahamhadscored a Peter Lynchian 500-bagger. Over the 40-year partnership, the gain inGEICOwouldcometorepresentamuchlargerpercentageofthefirm'sprofitsthanitsotherinvestmentscombined.TheGEICOpeakin1972wouldbeshortlived,andwould not reach that level again over the next 10-plus years. Graham added thefollowing postscript to the 1971/1972 edition of his seminal bookTheIntelligentInvestor:

“Weknowverywelltwopartnerswhospentagoodpartoftheirliveshandlingtheirownandotherpeople’s funds inWall Street. Somehardexperiences taught them itwasbetter tobesafe and careful rather than to try tomake all themoney in theworld. They established aratheruniqueapproachtosecurityoperations,whichcombinedgoodprofitpossibilitieswithsoundvalues.Theyavoidedanythingthatappearedoverpricedandwererathertooquicktodisposeofissuesthathadadvancedtolevelstheydeemednolongerattractive.Theirportfoliowasalwayswelldiversified,withmore thanahundreddifferent issues represented. In thisway they did quitewell throughmany years of ups anddowns in the generalmarket; theyaveraged about 20% per annum on the several millions of capital they had accepted formanagement,andtheirclientswerewellpleasedwiththeresults.“Intheyearinwhichthefirsteditionofthisbookappearedanopportunitywasofferedtothepartners’ fund to purchase a half-interest in a growing enterprise. For some reason theindustrydidnothaveWallStreetappealat the timeandthedealhadbeenturneddownbyquiteafewimportanthouses.Butthepairwasimpressedbythecompany’spossibilities;what

5

wasdecisive for themwas that thepricewasmoderate in relation to current earnings andassetvalue.Thepartnerswentaheadwiththeacquisition,amountingindollarstoaboutone-fifth of their fund. They became closely identified with the new business interest, whichprospered.“Infactitdidsowellthatthepriceofitssharesadvancedtotwohundredtimesormorethanthepriceof thehalf-interest. Theadvance faroutstripped theactualgrowth inprofits, andalmost from the start the quotation appearedmuch too high in terms of the partners’ owninvestment standards. But since they regarded the company as a sort of “family business,”they continued to maintain a substantial ownership of the shares despite the spectacularprice rise. A large number of participants in their funds did the same, and they becamemillionairesthroughtheirholdinginthisoneenterprise,pluslater-organizedaffiliates.“Ironicallyenough,theaggregateofprofitsaccruingfromthissingleinvestment-decisionfarexceededthesumofalltheothersrealizedthrough20yearsofwide-rangingoperationsinthepartners’ specialized fields, involvingmuch investigation, endless pondering, and countlessindividualdecisions.“Are theremorals to this story of value to the intelligent investor? An obvious one is thatthere are several differentways tomake and keepmoney onWall Street. Another, not soobvious,isthatoneluckybreak,oronesupremelyshrewddecision–canwetellthemapart?-maycountformorethanalifetimeofjourneymanefforts.*Butbehindtheluck,orthecrucialdecision,theremustusuallyexistabackgroundofpreparationanddisciplinescapacity.Oneneedstobesufficientlyestablishedandrecognizedsothattheseopportunitieswillknockathis particular door. One must have the means, the judgment, and the courage to takeadvantageofthem.“Of course,wecannotpromisea likespectacularexperience toall intelligent investorswhoremainbothprudentandalertthroughtheyears.WearenotgoingtoendwithJ.J.Raskob’sslogan that we made fun of at the beginning: “Everybody can be rich.” But interestingpossibilities abound on the financial scene, and the intelligent and enterprising investorshould be able to find both enjoyment and profit in this three-ring circus. Excitement isguaranteed.

*Veracityrequirestheadmissionthatthedealalmostfellthroughbecausethepartnerswantedassurancethatthepurchasewouldbe100%coveredbyassetvalue. Afuture$300millionormoreinmarketgainturnedon,say$50,000ofaccountingitems.Bydumblucktheygotwhattheyinsistedon.

6

TheSecurityI(Still)LikeBest

TheSecurityILikeBest

WarrenBuffett,Buffet-Falk&Co.,1951

Davycouldn’thavebeenmorehelpfultomethatday,andfordecadesthereafter.Itreallychangedmylife.

WallStreetJournalinterviewAugust24,2014

Buffett entered the GEICO tale in 1950. While attending graduate school atColumbiaUniversityBuffett ran across an insurance filing that listedGraham (hisprofessor and burgeoning mentor) as GEICO’s Chairman. Here Buffett's tells hisstoryofthatfatefulvisitinhis1995Chairman’sLetter:I'vehada45-yearassociationwithGEICO,andthoughthestoryhasbeentoldbefore,it'sworthashortrecaphere.IattendedColumbiaUniversity'sbusinessschoolin1950-51,notbecauseIcaredaboutthedegreeitoffered,butbecauseIwantedtostudyunderBenGraham,then

teachingthere.ThetimeIspentinBen'sclasseswasapersonalhigh,andquicklyinducedmetolearnallIcouldaboutmyhero.IturnedfirsttoWho'sWhoinAmerica,findingthere,amongotherthings,thatBenwasChairmanofGovernmentEmployeesInsuranceCompany,tomean

unknowncompanyinanunfamiliarindustry.

AlibrariannextreferredmetoBest'sFireandCasualtyinsurancemanual,whereIlearnedthatGEICOwasbasedinWashington,D.C.SoonaSaturdayinJanuary,1951,Itookthetrainto

WashingtonandheadedforGEICO'sdowntownheadquarters.Tomydismay,thebuildingwasclosed,butIpoundedonthedooruntilacustodianappeared.IaskedthispuzzledfellowiftherewasanyoneintheofficeIcouldtalkto,andhesaidhe'dseenonemanworkingonthesixthfloor.

AndthusImetLorimerDavidson,AssistanttothePresident,whowaslatertobecomeCEO.

ThoughmyonlycredentialswerethatIwasastudentofGraham's,"Davy"graciouslyspentfourhoursorsoshoweringmewithbothkindnessandinstruction.Noonehaseverreceivedabetter

half-daycourseinhowtheinsuranceindustryfunctionsnorinthefactorsthatenableonecompanytoexceloverothers.AsDavymadeclear,GEICO'smethodofsellingdirectmarketinggaveitanenormouscostadvantageovercompetitorsthatsoldthroughagents,aformof

distributionsoingrainedinthebusinessoftheseinsurersthatitwasimpossibleforthemtogiveitup.AftermysessionwithDavy,IwasmoreexcitedaboutGEICOthanIhaveeverbeenabouta

stock.

WhenIfinishedatColumbiasomemonthslaterandreturnedtoOmahatosellsecurities,InaturallyfocusedalmostexclusivelyonGEICO.MyfirstsalescallonmyAuntAlice,whoalwayssupportedme100%wassuccessful.ButIwasthenaskinny,unpolished20-year-oldwholookedabout17,andmypitchusuallyfailed.Undaunted,Iwroteashortreportlatein1951aboutGEICOfor"TheSecurityILikeBest"columninTheCommercialandFinancialChronicle,a

leadingfinancialpublicationofthetime.Moreimportant,Iboughtstockformyownaccount.

Youmaythinkthisodd,butIhavekeptcopiesofeverytaxreturnIfiled,startingwiththereturnfor1944.Checkingback,IfindthatIpurchasedGEICOsharesonfouroccasionsduring1951,thelastpurchasebeingmadeonSeptember26.Thispatternofpersistencesuggeststomethatmytendencytowardself-intoxicationwasdevelopedearly.IprobablycamebackonthatSeptember

7

dayfromunsuccessfullytryingtosellsomeprospectanddecideddespitemyalreadyhavingmorethan50%ofmynetworthinGEICOtoloadupfurther.Inanyevent,Iaccumulated350sharesofGEICOduringtheyear,atacostof$10,282.Atyearend,thisholdingwasworth

$13,125,morethan65%ofmynetworth.YoucanseewhyGEICOwasmyfirstbusinesslove.Furthermore,justtocompletethisstrolldownmemorylane,IshouldaddthatIearnedmostofthefundsIusedtobuyGEICOsharesbydeliveringTheWashingtonPost,thechiefproductofacompanythatmuchlatermadeit

possibleforBerkshiretoturn$10millioninto$500million.

Alas,IsoldmyentireGEICOpositionin1952for$15,259,primarilytoswitchintoWesternInsuranceSecurities.ThisactofinfidelitycanpartiallybeexcusedbythefactthatWesternwassellingforslightlymorethanonetimesitscurrentearnings,aP/Eratiothatforsomereasoncaughtmyeye.Butinthenext20years,theGEICOstockIsoldgrewinvaluetoabout$1.3

million,whichtaughtmealessonabouttheinadvisabilityofsellingastakeinanidentifiably-wonderfulcompany.

UpongraduatingfromColumbia,GrahamrefusedtohirehisonlyA+studentinhis27yearsteachingatColumbia-evenforasalaryof$0.(BuffetthasoftquippedthatGrahamhadperfectlycalculatedBuffett'strueintrinsicvalueatthetime.)So,from1951 through 1954, Buffett tried his hand at being a stockbroker at his father’ssmall brokerage Buffett-Falk & Co. Finally, in 1954 Graham relented and hiredBuffettasasecurityanalystatGraham-Newman.BuffettwouldthenlaterformtheBuffettPartnershipafterleavingGraham-Newmanin1956.Buffett’s hiatus from GEICO as an investor would last over the proceeding twodecades,yettheCompany’sfortune-andlatermisfortunes-wereneverfarfromhismind. The GEICO under Graham’s tenure would dissolve into a morass by the1970’s.TheCompany’sunbridledgrowthhadbeguntosowtheseedsofitsdemise.By1974,theCompanywasreeling.TheCompany’sproblem’sactuallybeganinthelate1960’s. TheCompany’s longsuccesshadevenbegunto impressregulatorstothepointthattheCompanywasallowedtoincreasetheirpremium-to-surplusratiotoover5:1,upfromamoreconservative3:1. Thetimingof thenCEOArtPecktosignificantly relax the Company’s long-held core customer to now include non-bureaucrats would lead to staggering problems over the next 10 years – fraudincluded.Thecanaryinthecoalminewastheunderestimateofreservestothetuneof$10million–wipingouttheearlierreportedprofitof$2.5millionin1969.Theunderestimateofreservesfor1970was$25million.NormanGiddenreplacedPeckasCEOin1970.ThenewCEOtriedtogrowGEICOoutofitspoorunderwritingofthe late ‘60’s. Over the next few years’ new policy growth averaged 11%, +50%higherthanthe7%rateofgrowththatprevailedfrom1965through1970.Asthe1970’sbeganthegovernmenthadbeguntolegislateno-fault insuranceandmandated price reductions. Concomitant with new regulations, higher injuryawards and repair inflation, the Company’s underwriting executives continued tomakeaseriesofegregiouspricingerrorsextendingitsclienteletohigherrisk,blue-collarandyounger-agedcategories. Inadequateprovision for futureclaimsraised

8

theiruglyheadagain. TheCompanywaswoefullyunder reserved. Thusbeganastreamofsignificantlosses.In1974theCompanyreporteda$6millionloss–theirfirstunderwritinglossin28years.Matterswouldgetworseandreachacrescendoin1975. TheCompany lost$126million in1975and$40millionduring the firsthalfof1976.Bankruptcywasaveryrealrisk–andtheWashington,D.C.insurancecommissionerwas poised to declare GEICO bankrupt. Buffett even interceded in1975withavisit tothenCEONormGidden.Yet inexplicablyGiddenturnedadeafear to Buffett’s entreaties and warnings. GEICO was on the brink of the largestinsolvencyinthehistoryontheU.S.insuranceindustry.

(Note:$1,000investedin1948wasworth$47,500in1958.)

TheCompany’sshares,whichhadtradedashighas$61 in1972and$42 in1974,weredowntojustunder$5.Bythetimeofthe1976annualshareholdersmeetingat theWashingtonStatlerHilton,panicwas in theair andpitchforksweredrawn.Withinamonth,CEOGiddenwasbooted.Bythen,thestockwaslittlemorethan$2pershare.(Asadaside:TheGoodwin’shadbequeathedtheirstocktotheirsonLeo,Jr.,whohadmargined the stock to thehilt. Tragically, after the stockcrashed,hetook his life. Another aside, Shelby Davis, he of New York Venture fund famebecamethelargestshareholderinthelate1960’s–early1970’sandwasaddedtoGEICOboard. Davishadmarginedhispersonalholdings inGEICOandwere itnotforhissignificantholdingsinJapanesestocks(sharesofJohnTempletonatthetime)hecouldhavebeenwipedouttoo.)Enterthe“TheBabeRuthofInsurance.”InMay1976,theGEICOboardofdirectorshired former Traveler’s executive John Byrne as chairman, president and CEO.Byrne, brusque as they come, had recently cemented his industry chops atTraveler’s home and auto insurance lines. Byrne wasted little time in turningaroundGEICO’soperations. “OperationBootstrap”commencedpost-haste. Byrne

9

was ruthless in cutting costs, increasing rates and re-underwriting theCompany’sentire book of business. Thesemeasures included firing 4,000 of the Company’s7,000 employees, closing 100 offices, exiting the Massachusetts and Jew Jerseymarketsandimmediatelyraisingratesby40%.Byrnewasalsouniquelysuccessfulinputtingtogetheraconsortiumof27insurancecompanies,includingcompetitors,aswellasBerkshire’sNationalIndemnitytojointlyreinsureGEICO’sexistingbookofbusiness.ByrnewassosuccessfulthatGEICO’sstatutorycapitalbytheendof1976wasbackup to $137million and the Company’s surplus topped $250million – the highestlevelintheCompany’sthen43-yearhistory.GEICOreturnedtoprofitabilityinjustoneyear.Inthesameyear,1977,theCompanydeclaredadividend–just$.01.By1979, the Company’s profits reached $220million. Buffett’s Ruthian sobriquet ofByrnesprovedquitefitting.Shortly after taking the reigns at GEICO thatMay, Buffett reached out to his thendear friend Kay Graham, CEO of the Washington Post, to broker a meeting withByrne. Kay Graham reached out to Byrne, yet Byrne apparently snorted, “Who’sBuffett?” The next phone call that Byrne received was from none other thanLorimerDavidson(whowouldliveto97yearsofage)who’schoiceandoff-coloredwordsquicklyconvincedByrnetoaccepttheBuffettmeeting.BuffettandByrnemetlongintothenightatKayGraham’sGeorgetownresidencediscussingtheintricaciesofGEICOandByrne’splanforGEICO’ssurvival.BuffettwassoimpressedbyByrnethathestartedbuyingGEICOstocktheverynextmorning. The first order was for 500,000 shares at $2 1/8. Buffett opened upBerkshire’s thick wallet for even more. He ultimately invested $19 million in aSalomonBrothersledconvertiblepreferredstockissuanceof$75million,plus$4.1millionatanaveragepriceof$2.55pershare. Buffett’s fullyconvertedcost-basiswasjust$1.31pershare.ByrnewasinstrumentalwithSalomonintheconvertibledealaftereightotherinvestmentbanksbalkedatthedeal.BuffettplayednosmallrolehimselfparlayinghisgrowingreputationtohelpswayinsuranceregulatorsatbayfrompullingGEICO’sstatelicensees.By1980Buffetthadsized-upBerkshire’sinvestmentinGEICOto$45million(one-thirdofallofGEICO). By1981,GEICOwouldrepresent31%ofBerkshire’sentireequityportfolio.(ShadesofBuffett’s1964careerscoreinAmericanExpress’saladoilscandal.)Atthecloseof1982,Berkshire’s35%ownershipofGEICOrepresentedapproximately$250millionofannualinsurancepremiums–anamountlargerthanBerkshire’sowndirectpremiumvolume. As1984rolledaround,GEICOcontinuedto impress and accelerate. Berkshire’s GEICO ownership had reached 36%, andtheirinterestinGEICO’sdirectproperty/casualtyvolumeof$885millionamountedto$320million–morethandoubleBerkshire’sownpremiumvolume.1985wouldmarkthepeakofGEICO’sstockmarketvalueasapercentage(50%)ofBerkshire’scommonstockportfolio. Over thecourseof thenext tenyears,GEICO

10

would prosper. Mirroring the Company’s rebirth of profitable growth, cashdividendswouldbe increased for thenext seventeen consecutive years. By1994the dividend would reach $1.00 per share. GEICO’s rising stream of dividendswouldbuttress thecoffersofBerkshire to the tuneof$180milliondollars–morethanfourtimesBuffett’sinvestmentinjustdividendsalone!AlongthewaytoowasBuffett’sgrowingdesiretoownGEICOlock-stock-and-barrel.InBuffett’s1987Chairman’sLetterheinformedBerkshireshareholdersthatGEICO,along with Capital Cities/ABC and The Washington Post would now be deemed“permanent”holdings.Hewrote:However,ourinsurancecompaniesownthreemarketablecommonstocksthatwewouldnotselleventhoughtheybecamefaroverpricedinthemarket.Ineffect,weviewtheseinvestmentsexactlylikeoursuccessfulcontrolledbusinesses—apermanentpartofBerkshireratherthanmerchandisetobedisposedofonceMr.Marketoffersusasufficientlyhighprice.Tothat,Iwilladdonequalifier:Thesestocksareheldbyourinsurancecompaniesandwewould,ifabsolutely

necessary,sellportionsofourholdingstopayextraordinaryinsurancelosses.Weintend,however,tomanageouraffairssothatsalesareneverrequired.

By year-end 1987, the incredible success of Buffett’s GEICO investment (15Xbagger),TheWashingtonPost (27Xbagger) and the sizeofhisCapitalCities/ABCinvestmenthadacombinedmarketvalueof$1.7billion–orapproximately75%ofthenetworth atBerkshire. The after-taxoperating earnings growthatGEICOby1987hadincreasedto$9.01,fareclipsingBuffett’saveragestockcostof$6.67pershare. Fast forwarding to 1995, Berkshire’smarketable securities per-share overthe previous thirty years had grown from $4 per share to $22,088 per share – astunningcompoundedgrowthrateof33.4%.OnandoffagaininformaldiscussionsofaBerkshire-GEICOcombohadtakenplaceforquiteafewyears;however,thefirstformalacquisitiondiscussionswouldhaveto wait until late summer in 1994. Buffett had proposed a tax-free stock swap.GEICOexecutivesSamButlerandLouSimpsonbalkedattheproposalfordividendandtax-relatedreasons.ThenextproposalbyBuffett(reluctantly)wasanewissueof Berkshire convertible preferred. This proposal was nixed by GEICO on price.Negotiationscontinuedintothespringandsummerof1995.GEICOcounteredthattheywouldacceptanall-cashdealat$70pershare.Simplyput,GEICOwantedcashand Buffett didn’t have $2 billion in pocket change. While Buffett and MungernegotiatedwithGEICOontheeastcoast,eventswerestirringonthewestcoast.The Magic Kingdom would soon turn Berkshire Hathaway into an even greatermagickingdomofitsown.OnAugust1,1995,DisneyannouncedtheiracquisitionofCap Cities/ABC for $19 billion. At the time, Berkshire owned a cool 20 millionsharesofCapCities/ABC(13%oftheCompany). Thecashportionofthedealwas$65per share (plus1 shareofDisney stock). Buffet’s $345million investment inCap Cities/Disney was nowworth nearly $2.5 billion. Buffett’s elephant gun was

11

nowcash-cockedandheandMungerquicklyagreedtoGEICO’s$70non-negotiableprice. Shortly thereafter, August 25, brought the announcement of the GEICOacquisition. Buffett’s mentor once bought 50% of GEICO for $712,000 – Buffettuppedtheantenearly50yearslaterby$2.3billion.Fromtherealpaniclow’ssetinthe springof1976of $2.25,by the fall of1995,GEICO’s stockhad soared toover$300(split-adjusted).Bytheendof1995,Berkshire’sownershipinGEICOhadincreasedto51%viasharebuybacks. Buffett’s purchase of the remaining 49% inGEICO for $2.3 billion hadthus created an effective 48-bagger on Berkshire Hathaway’s earlier GEICOinvestmentof$46million.At the time of theGEICO acquisition, GEICOhad grown to the nation’s 7th largestautomobile insurer, insuring over 3.7 million autos. So now as a wholly ownedsubsidiary of Berkshire, Buffett gets his hands not only on GEICO’s underwritingprofits, but also the Company’s growing float of $3 billion. Buffett on the GEICOacquisition(andatutorialonfloat):

Since1967,whenweenteredtheinsurancebusiness,ourfloathasgrownatanannualcompoundedrateof20.7%.Inmoreyearsthannot,ourcostoffundshasbeenlessthannothing.

Thisaccessto"free"moneyhasboostedBerkshire'sperformanceinamajorway.

Anycompany'slevelofprofitabilityisdeterminedbythreeitems:(1)whatitsassetsearn;(2)whatitsliabilitiescost;and(3)itsutilizationof"leverage"thatis,thedegreetowhichitsassetsarefundedbyliabilitiesratherthanbyequity.Overtheyears,wehavedonewellonPoint1,havingproducedhighreturnsonourassets.Butwehavealsobenefittedgreatlytoadegreethatisnotgenerallywellunderstoodbecauseourliabilitieshavecostusverylittle.An

importantreasonforthislowcostisthatwehaveobtainedfloatonveryadvantageousterms.Thesamecannotbesaidbymanyotherpropertyandcasualtyinsurers,whomaygenerate

plentyoffloat,butatacostthatexceedswhatthefundsareworthtothem.Inthosecircumstances,leveragebecomesadisadvantage.

Sinceourfloathascostusvirtuallynothingovertheyears,ithasineffectservedasequity.Ofcourse,itdiffersfromtrueequityinthatitdoesn'tbelongtous.Nevertheless,let'sassumethatinsteadofourhaving$3.4billionoffloatattheendof1994,wehadreplaceditwith$3.4billionofequity.Underthisscenario,wewouldhaveownednomoreassetsthanwedidduring1995.Wewould,however,havehadsomewhatlowerearningsbecausethecostoffloatwasnegativelastyear.Thatis,ourfloatthrewoffprofits.And,ofcourse,toobtainthereplacementequity,

wewouldhaveneededtosellmanynewsharesofBerkshire.Thenetresult-moreshares,equalassetsandlowerearnings-wouldhavemateriallyreducedthevalueofour

stock.Soyoucanunderstandwhyfloatwonderfullybenefitsabusiness,ifitisobtainedatalowcost.

OuracquisitionofGEICOwillimmediatelyincreaseourfloatbynearly$3billion,withadditionalgrowthalmostcertain.WealsoexpectGEICOtooperateatadecentunderwritingprofitinmostyears,afactthatwillincreasetheprobabilitythatourtotalfloatwillcostusnothing.Ofcourse,wepaidaverysubstantialpricefortheGEICOfloat,whereasvirtuallyallofthegainsinfloat

depictedinthetableweredevelopedinternally.

12

GEICO hit the ground running in 1996. Under the direction of 35-year GEICOveteranTonyNicely(by2015,maybethemostnamedBerkshiremanagerinBuffet’sannual Chairman’s Letter) – and with the influence of Buffett, GEICO quicklyinstituted amost effective and elegant company-wide bonus plan to enhance thecompany’s moat-like low-cost advantage. Henceforth, the annual profit sharingcontributionandemployeebonusplanwouldbecalculatedbytwometrics–growthin voluntary auto policies and underwriting profitability on policies on GEICO’sbooksforatleastone“seasoned”year.1996wouldturnouttobeGEICO’sbestyearsince1976astheirvoluntaryautopoliciesgrew10%.Thesinglebestyearduringtheprevioustwentyhadbeenan8%growthinpolicies.1997sawonlyacceleratedgrowthonallfrontsatGEICO.Newvoluntarypoliciesclockedinatover900,000–nearly triple from 1993’s level of 350,000. Policies in force almost reached3,000,000 – up about 50% from 1993. GEICO employees enjoyed a whoppingcontribution of 27%of their base contribution to their profit sharing plan. 1998sawadramaticincreasetoexpandthegospelofGEICO’slow-costautoinsuranceasthe company’s marketing budget was increased to nearly $150 million – almostthreetimestheamountspentin1997.Buffettdidn’tletTonyNicelytakehisfootoffthegaspedalinboth1998and1999.The year before Buffett acquired GEICO; the company spent $33 million inmarketingandhadaforceof652telephonecounselors.Bytheendof1999,GEICOspent$242millioninmarketingandgrewtheircounselorstoover2,600. GEICO’sgrowthwentnearlyballistic.Newannualautopoliciesgrewnearly1.25millionand1.65millionin1998and1999,respectively.Autopoliciesinforceatyearend1999exceeded4.3million.GEICO’smarketsharehadbeenstuckatabout2%thedecadebeforeNicelytookthereignsin1993.Attheendof1999ithadquicklydoubledto4.1%. GEICO’s gain inmarket share had come at the expense of State Farm andAllstate. Theyear-overyeargrowthofpoliciesinforceatStateFarmhasbeenflatsince2003.Allstatehasfaredevenworse.Theircumulativepolicyinforcegrowthhasbeen-8%since2008,andflat latesince2005. ThetablebelowchroniclesthegrowthinGEICOoverthenexttwelveyears.

Source:RationalWalk

By 2015, Nicely’s last year at the helm, the growth at GEICO had been simplysuperlative under theBuffett-NicelyMurderer’sRow reign. Market sharewas upmorethanfive-fold-foldto11.5%.Annualautopremiumshadgrownnearlyseven-fold to $23 billion. Accumulated underwriting profit (pre-tax) clocked in at $12billion.Gecko,GEICO’sreptilianadman,plustheCavemanwouldmaketheirdebutsin1999and2004,respectively.By2012,thesetwopitchmenwouldhappilyspendover$1billioneachyearhawkingGEICO-orthreetimesasmuchasthecompany’s

13

three largest rivals combined. GEICO is on course to become thenation’s secondlargestautoinsurer.

TopAutoInsuranceAdvertisers2013

Source:SNLFinancial

14

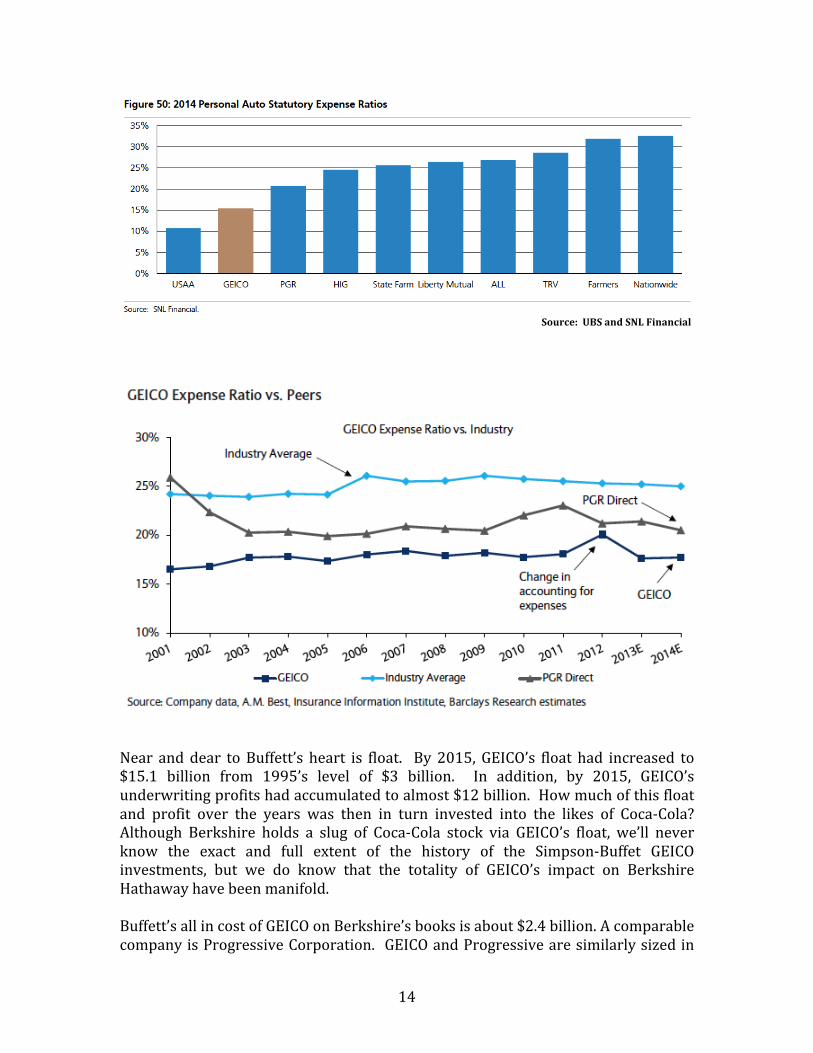

Source:UBSandSNLFinancial

Near anddear toBuffett’s heart is float. By 2015, GEICO’s float had increased to$15.1 billion from 1995’s level of $3 billion. In addition, by 2015, GEICO’sunderwritingprofitshadaccumulatedtoalmost$12billion.Howmuchofthisfloatand profit over the years was then in turn invested into the likes of Coca-Cola?Although Berkshire holds a slug of Coca-Cola stock via GEICO’s float, we’ll neverknow the exact and full extent of the history of the Simpson-Buffet GEICOinvestments, but we do know that the totality of GEICO’s impact on BerkshireHathawayhavebeenmanifold.Buffett’sallincostofGEICOonBerkshire’sbooksisabout$2.4billion.AcomparablecompanyisProgressiveCorporation. GEICOandProgressivearesimilarlysizedin

15

bothannualpremiumswrittenandpolicies in force. Themarket capitalizationofProgressiveiscurrently$19billion.CapitalizingGEICOatProgressives’marketcapto statutorysurplusofalmost3XvaluesGEICOconsiderablyhigher still. We takeBuffettonhiswordthatwhenhestatesthatthebookcostofGEICOisafractionofitseconomicworth.

Source:RationalWalk

Somemayoffer upBuffett’s investment inCoca-Cola as his greatest. Theywouldhave a compelling argument. By any measure, Buffett’s two and half-decadeinvestment of $1.3 billion in Coca-Cola, currently worth just over $17 billion,certainly merits consideration. Throw in the not-so-minor matter of about $4.6billion inaccumulatedCoca-Coladividendssince1988andperhaps thescaledoestipinCoca-Colas’favoroverGEICO. Heck,thehalf-dozenbillionindividendsfrom1998certainlysoothedthepainwaitingforCoca-Cola’sstocktorecoverbacktothe1998 exuberant highs of $43. Buffett’s current dividend yield to cost is amind-numbing41%. WhileBuffett’s investment inCoca-Cola isperhapssecondtononefor him in terms of raw size, the transformativenature of his GEICO investments,surelytrumpsCoca-Cola.DavidA.Rolfe,CFAChiefInvestmentOfficerApril,2013RevisedandUpdatedApril,2016

16

----------------------------------------------------------------------------------------------------------Sources:BerkshireHathawayAnnualReportsWarrenBuffett’sChairmanLettersCoca-ColaCompanyDocumentsGEICOCompanyDocumentsLaurenceArnold:BloombergJohnByrne,GEICOCEOBuffettcitedfor‘Brilliance,’Diesat805/10/13ProfessorRobertF.Bruner:CaseStudy2:WarrenE.Buffet,1995HartmanL.Butler,Jr.:AnHourWithBenjaminGraham,FinancialAnalystsJournalNov./Dec.1976BenjaminGraham:TheIntelligentInvestorAndrewKilpatrick:OfPermanentValueTheStoryofWarrenBuffett2012OdysseyEditionJanetLowe:BenjaminGrahamonValueInvesting:LessonsfromtheDeanofWallStreetJanetLowe:TheRediscoveredBenjaminGrahamRogerLowenstein:TheMakingofanAmericanCapitalistAliceSchroeder:TheSnowballWarrenBuffettandtheBusinessofLifeJasonZweig:WasBenjaminGrahamSkillfulorLucky?WallStreetJournalDecember12,2012Focusinvestor.com:GEICO:AnInvestmentLessonGrahaminvestor.com:TheIntelligentInvestorInsuranceHallofFame:JackByrneNewYorkTimes:LorimerA.Davidson,Ex-GEICOChiefDecember6,1999RobertG.Hagstrom:TheWarrenBuffettWay JohnRothchild:TheDavisDynasty:FiftyYearsofSuccessfulInvestingonWallStreet

17

18

19

20

21

22

GEICO:The“Growth”companythatmadethe“Value”careersofbothBenjaminGrahamand

WarrenBuffett

Presentedby

DavidA.Rolfe

ChiefInvestmentOfficerWedgewoodPartnersSt.Louis,Missouri

2016GuruFocusValueConferenceDoubleTreebyHiltonHotel

Omaha,NebraskaApril28,2016

23

GoodwinTimeline

• Foundedin1936inSanAntoniobyLeoandLillianGoodwin.

• $100,000inseedcapital.

• $25,000bytheGoodwin’sand$75,000bytheRheafamily.

• Typicalautopolicy$27.50.

• 1937:3,700policieswith$104,000inpremiums.

• 1937:CompanyrelocatedinWashington,D.C.

• 1940:Companybooksfirstunderwritinggain($5,000).$768,058inpremiumsand25,514policesinforce.

• 1941:HailstorminD.C.cementsCompany’sservicereputation.

• 1945:$1,638,562inpremiumsand51,697policiesinforce.

• 1940-1974:35consecutiveyearsofprofits.

24

Graham-NewmanTimeline

• 1948:MembersofRheawanttoselltheirportionofCompany.

• 1948:Graham-Newmanbuys50%ofGEICOfor$712,000.BenjaminGrahambecomesChairmanoftheBoard.

• 1948:SECfinallyapprovesthepurchaseviaadistributiontoGraham-Newman’spartners/shareholders.

• 1948:OriginalOTCdistribution$27foroneshare.

• 1949:Ratioofunderwritingprofittopremiumsearned27.5%.AccordingtoBest’sfor133stockcasualtyandsuretycompanies’ratioaveraged6.7%.

• 1950:GEICOlicensedin15states.144,000policiesinforce.$8millioninpremiums.

• 1958:Triplesaddressablemarketbysolicitingnon-governmentprofessionals.

• 1958:LeoGoodwinretires.ReplacedbyLorimerDavidson.$1,000investedinGEICOhadgrownto$47,500.

• 1965:GrahamretiresfromGEICOboard.

• 1971:JerryNewmanretiresfromGEICOboardandWarrenBuffettnominatedtoreplaceNewmanontheboard.

• 1972:AsingleoriginalGraham-Newmanshareof$27hadgrownto$16,349.

• 1972:Graham-Newman’soriginal$712,000investmentworthover$400,000,000–ormorethanallofGraham-Newmanpartnershipprofitscombined!

25

WarrenBuffettTimeline

• 1950:WhilestudyingunderGrahamatColumbiaUniversity,BuffettdiscoversthatGrahamisChairmanofGEICO.

• 1951:BuffetttravelstoGEICOinD.C.onaSaturdayandgetsadaylonginsurancetutorialfromLorimer“Davy”Davidson.

• 1951:Upongraduation,BuffettmovesbacktoOmahaandjoinshisfather’sbrokeragefirm.HespendsmostofhistimehawkingGEICOtofamilyandfriends.

• 1949-1951:DJIAralliesfrom162inmid-June1949to270bySeptember1951.Dividend-reinvestedreturnof93%.

• 1951:RejectingGraham’sadvicetowaitforapullbackinthestockmarketBuffettinvestsover50%ofhisnetworthinGEICO(350shares@$293/8).GEICOclosesat$37½atyear-end.

• GEICOmarketcapatBuffett’sfirstpurchase$7million.• Buffettwrites“TheSecurityILikeBest”inTheCommercialandFinancialChronicleonDecember6,1951

• 1952:BuffettsellshisGEICOstockat$435/8topurchaseWesternInsuranceSecuritiesvaluedatjust1Xearnings.

• Buffett’soriginal$10,282investmentinGEICOwouldgrowto$1.3millionoverthenext20years.

• Olza“Tony”NicelyjoinsGEICOin1961.BecomesChairman,CEOandPresidentin1993.Retiresafter54yearsin2015.

26

BerkshireHathawayTimeline–PartI

• 1974:CracksemergeinGEICOduetounbridledgo-gogrowth.

• 1974:No-faultinsurance,inflationandpoorunderwritingleavesGEICOwoefullyunderreserved.

• 1975:$124millioninlosses.

• 1975:Buffett’swarningsinapersonalvisittoCEOGiddengounheeded.

• 1976:$40millioninlossesfirsthalfoftheyear.

• 1976:Stockfallsfromhighof$61in1972,to$42in1974to$2inthespringof1976.Giddenout.JackByrnefromTravelersin.

• 1976:Byrnefires50%ofemployees,raisesratesby40%andtellsN.J.insurancecommissionerto“goimpregnateyourself.”

• 1976:BuffettlurkinginthewingsasksKayGrahamofWaPotobrokerameetingwithByrne.Byrnesays“Buffettwho?”andrefusesmeeting.DavyDavidsoncallsByrneandreadshimtheriotactforrefusingmeeting.BuffettandByrnemeetlateintothenightandmorningdiscussingGEICOatGraham’sGeorgetownestate.

• 1976:BuffettbeginsbuyingGEICOstocktheverynextmorning.Firsttrade500,000sharesat21/8.Buffett’sall-ininvestmentwouldcometo$19millioninaconvertiblepreferred,plus$4.1million@$2.55pershare.Buffett’sfullyconvertedcost-basiswasapprox.$1.31pershare(adjustedfor5-1stocksplitin1992).

• 1977:ByrnereturnsGEICObacktoprofitability.

27

BerkshireHathawayTimeline–PartII

• 1980:BuffettsizesupBerkshire’sGEICOinvestmentto$45million–or33%ofGEICO.

• 1981:GEICO31%ofBerkshire’sequityportfolio.

• 1982:Berkshire’s35%“look-through”ownershipof$250millioninGEICO’sannualinsurancepremiumsgreaterthanowndirectinsurancepremiums.

• 1984:Berkshire’s36%“look-through”ownershipof$320millioninGEICO’sannualinsurancepremiumsdoubleBerkshire’sowndirectinsurancepremiums.

• 1984:CumulativeGEICOdividends$180million.

• 1985:GEICOinvestment($596million)50%ofBerkshire’sequityportfolio–apeak.

• 1985:ByrneleavesGEICO.BillSnyderbecomesChairmanandCEO.

• 1987:Buffett’sChairman’sLetternamesGEICO(andCapCities/ABCandWaPo)“permanentholdings.”

• 1990:GEICOinvestmentworth$1,044,625,000.

28

BerkshireHathawayTimeline–PartIII

• 1994:GEICOinvestmentworth$1,678,250,000.

• 1994:BuffettinitiatesformalmergerandacquisitiondiscussionswithGEICO.

• 1994:BuffettproposesBerkshire-GEICOstockswap.GEICObalks.

• 1995:BuffettproposesnewissueofBerkshirepreferredasacquisitioncurrency.GEICObalks.GEICOwantsall-cashdeal$70.Buffettdoesnothavethecash.

• 1995:OnAugust1,DisneyannouncestheiracquisitionofCapCities/ABC.Buffett’sCapCities/ABCinvestmentof$345millionnowworthnearly$2.5billion.

• 1995:OnAugust25,BuffettannouncesBerkshire’sacquisitionoftheremaining49%ofGEICOfor$2.3billion.

• Fromtherealpaniclow’ssetinthespringof1976of$2.25,bythefallof1995,GEICO’sstockhadsoaredtoover$300(split-adjusted).

• 1995:Marketingbudget$35million.

• 1996:GEICO’sbestyearofpolicygrowth(+10%)in20years.

29

• 1997:Policygrowth16%.

• 1998:Marketingbudget+50%from1997$100million.

• 1999:Policygrowth+23%.

• 1999:BuffettandTonyNicelyincreasemarketingbudgetto$242millionfrom$33millionin1995.Newautopolicygrowthof1.65million.Policiesinforce+4.3million.

• 2001–2012Advertising:2001:$219million,2003:$238million,2004:$502million,2006:$631million,2007:$751million,2010:$900million(GeckoandCaveman),2011:$994million(industryrecord),2012:$1.1billion.

• 2013:5,000,000policiesinforce.

• 1996-2015:Marketshareupalmost5Xto11.4%.Annualautopremiumsup6.7Xto$23billion.Adspending+$1.2billionfrom$33million.Cumulativeunderwritingprofitssince1995$12.8billion.Floatup5Xto$15.1billion.ConservativevaluationofGEICO$22billion.

30

Theinformationandstatisticaldatacontainedhereinhavebeenobtainedfromsources,whichwebelievetobereliable,butinnowayarewarrantedbyustoaccuracyorcompleteness.Wedonotundertaketoadviseyouastoanychangeinfiguresorourviews.Thisisnotasolicitationofanyordertobuyorsell.We,ouraffiliatesandanyofficer,directororstockholderoranymemberoftheirfamilies,mayhaveapositioninandmayfromtimetotimepurchaseorsellanyoftheabovementionedorrelatedsecurities.Pastresultsarenoguaranteeoffutureresults.Theinformationprovidedinthismaterialshouldnotbeconsideredarecommendationtobuy,sellorholdanyparticularsecurity.