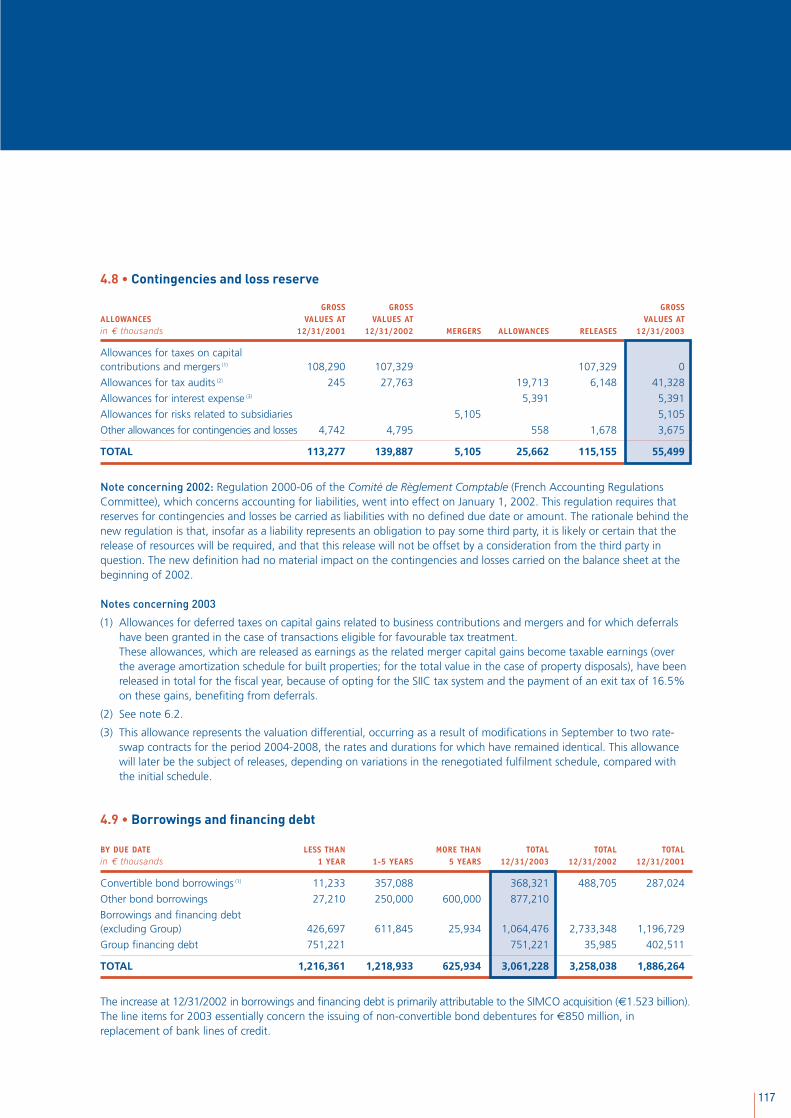

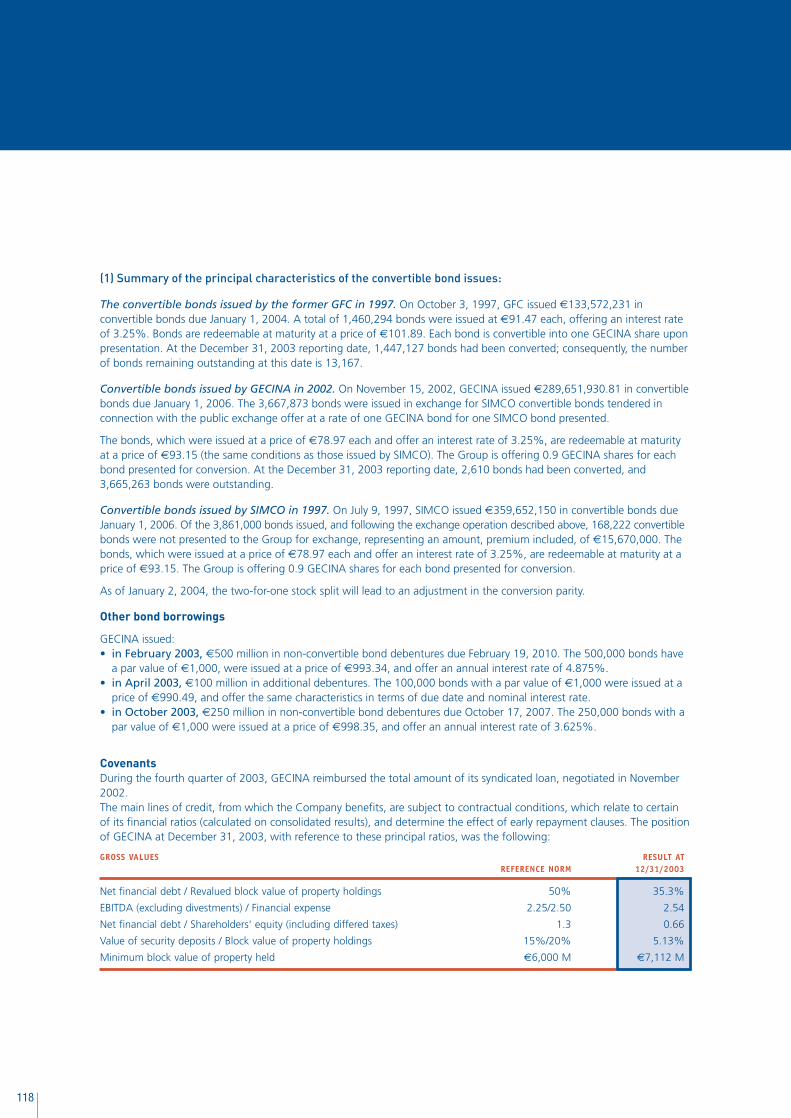

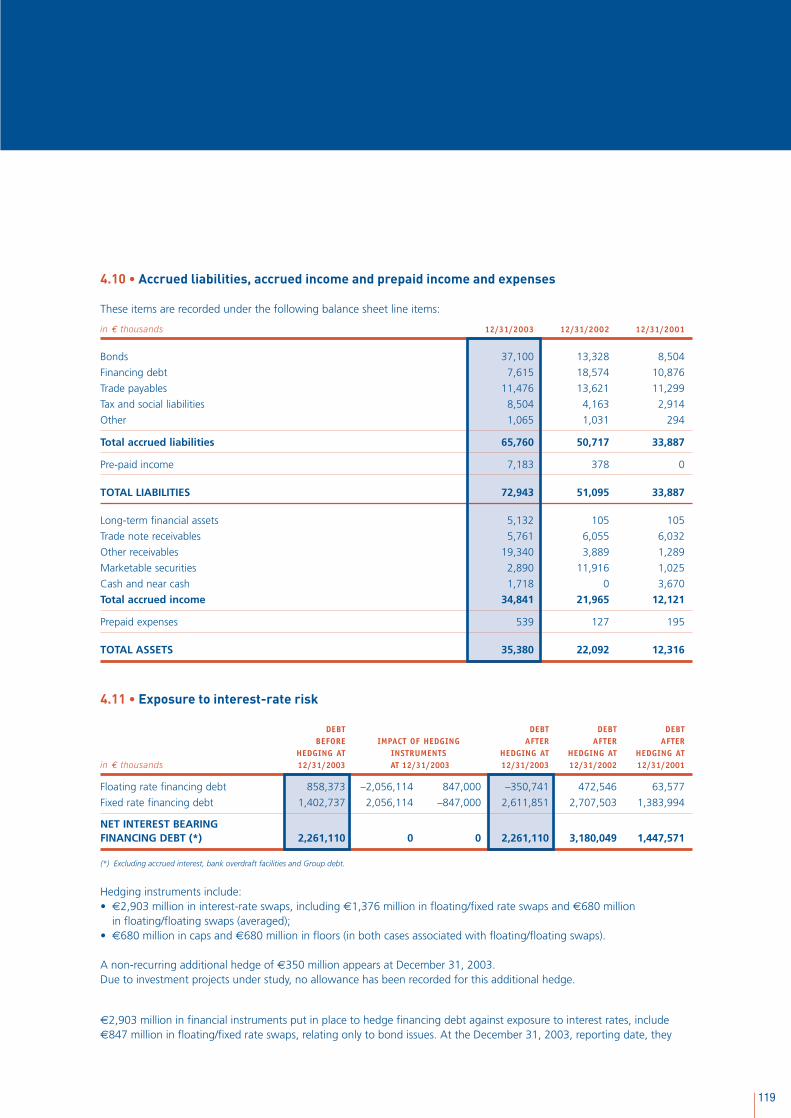

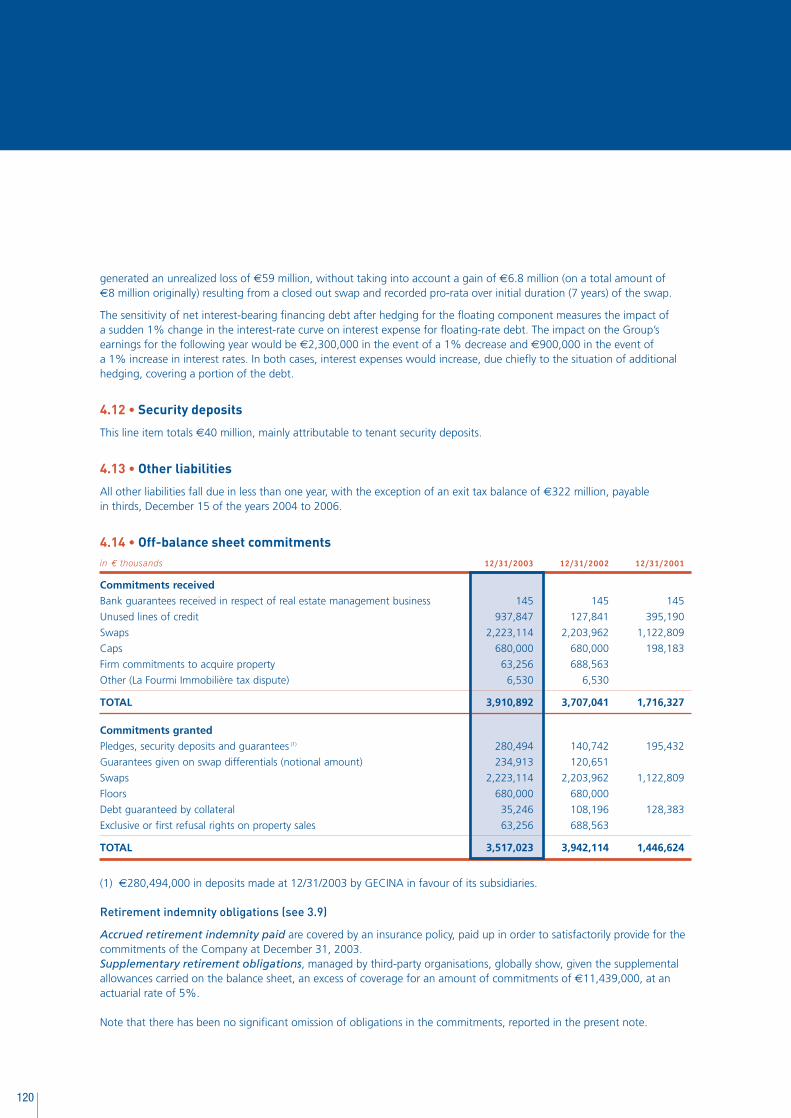

Gecina couv sp€¦ · whole operation, as well as administrative and financial management for the...

176

annual report 2003

-

Upload

truongtuyen -

Category

Documents

-

view

224 -

download

2

Transcript of Gecina couv sp€¦ · whole operation, as well as administrative and financial management for the...

annual report

2003

At the heart of new dynamic urban developmentQuality drives development and growthYear’s highlights: a Group on the road to successQuestions for Antoine Jeancourt-Galignani and Serge GrzybowskiCorporate management: recognized and complementary skillsStrategy: an objective of profitable redeploymentPortfolio highlights: major improvementFinancial highlights: objectives achievedGECINA and its shareholders: emphasis on the quality of informationHuman resources: integration facilitatedSustainable development: a commitment that involves everyoneCommercial real estate: an active and selective development policyResidential real estate: rationalization stepped upBackground: dynamic developmentFinancial report

2468

1012141618202122405859

Contents

2-4, quai Michelet 92300 Levallois-Perret

7, rue de l’Amiral-Serre78000 Versailles

11

Leader in the euro zone with realestate holdings valued at 7.8 billion euros,GECINA has a unique profile defined by a balance between its two rental activities:commercial real estate and residentialproperties. Offices and commercialpremises, which offer a high yield,combine with residential properties, asource of regular and diversified revenues,to ensure a profitable and safe investment.

GECINA’s rental real estateproperties represent a total area ofmore than 2.2 million sq.m., comprising900,000 sq.m. of commercial premisesand 19,000 apartments. Assets are notedfor the quality of their location: 90% are inParis and the surrounding region, and therest in Lyons.

GECINA’s profitable growth trendis driven by its teams’ experience and know-how. Asset management, buildingservice and maintenance, financial and realestate engineering, asset restructuringand development, marketing, etc. aresome of the areas in which the Group hasdeveloped expertise, fostering the implementation of an active policy to increase the value of assets and pursean opportunistic strategy of acquisitionsand divestments.

As a listed French real estateinvestment trust (SIIC)1 since 2003,GECINA is a tax free vehicle that provides a high yield. With a market capitalization of 3.8 billion euros in the hands of almost38,000 shareholders, GECINA is one of themost liquid real estate stocks. It is part of the SBF 120 and the Euronext 100 stockmarket indexes.

(1) Société d’Investissements Immobiliers Cotée.

2

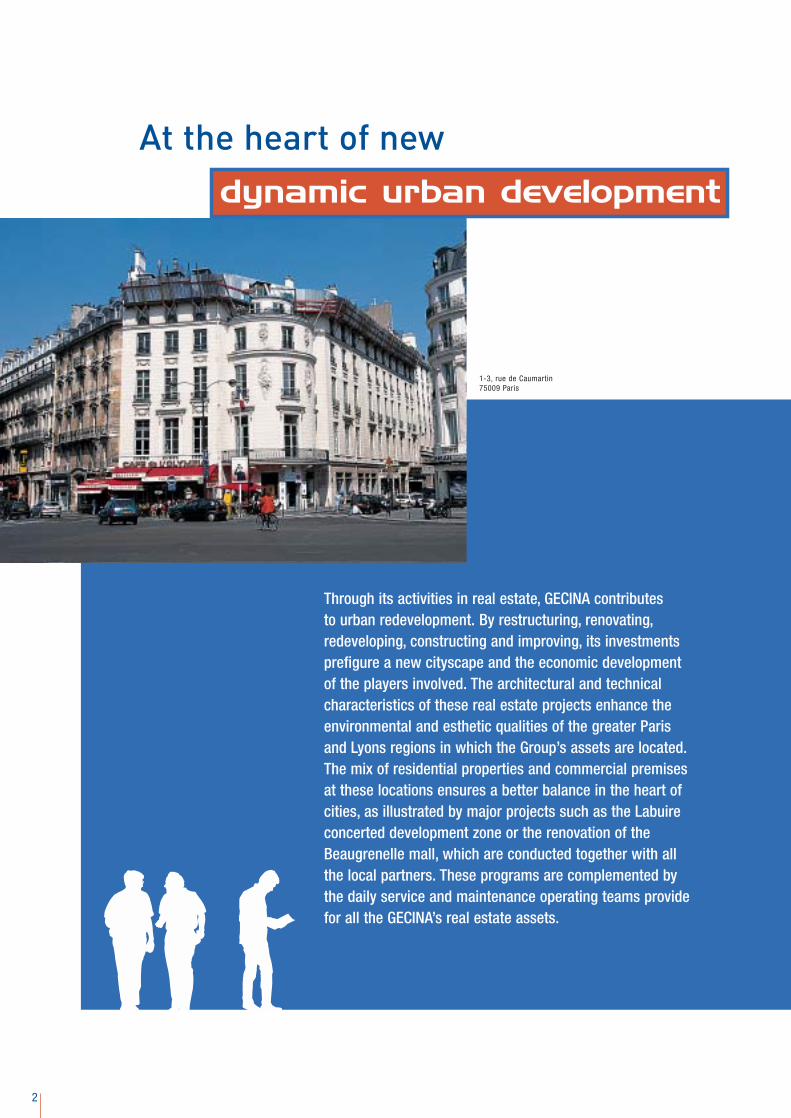

Through its activities in real estate, GECINA contributes to urban redevelopment. By restructuring, renovating,redeveloping, constructing and improving, its investmentsprefigure a new cityscape and the economic developmentof the players involved. The architectural and technicalcharacteristics of these real estate projects enhance theenvironmental and esthetic qualities of the greater Parisand Lyons regions in which the Group’s assets are located.The mix of residential properties and commercial premisesat these locations ensures a better balance in the heart ofcities, as illustrated by major projects such as the Labuireconcerted development zone or the renovation of theBeaugrenelle mall, which are conducted together with allthe local partners. These programs are complemented bythe daily service and maintenance operating teams providefor all the GECINA’s real estate assets.

At the heart of new dynamic urban development

1-3, rue de Caumartin75009 Paris

3

• In partnership with Lyonnaise de Banque,GECINA is involved, as planner, in the Labuireproject, a five hectare plot of land at thecorner of the boulevard Vivier-Merle and the avenue Félix-Faure in Lyons.

• The project aims to develop 140,000 sq.m. of offices, stores, housing and public facilities.

• The sale to real estate operators of propertyconcession rights, of which GECINA owns 60%, is scheduled from 2005.

The development of Labuire will

create a new neighborhood that

will be the setting for enhanced

living conditions. At the southern

end of the Lyons Part-Dieu central

business district, housing, stores,

small shops and services, parks

and offices will together create

the economic, social and

environmental components

needed to ensure an attractive

balance for quality urban living.

72-86, avenue Félix-Faure and 106, boulevard Vivier-Merle - 69003 Lyon

5 bis-7, rue Volney and 14-16, rue des Capucines- 75002 Paris

4

Quality drives development and growth

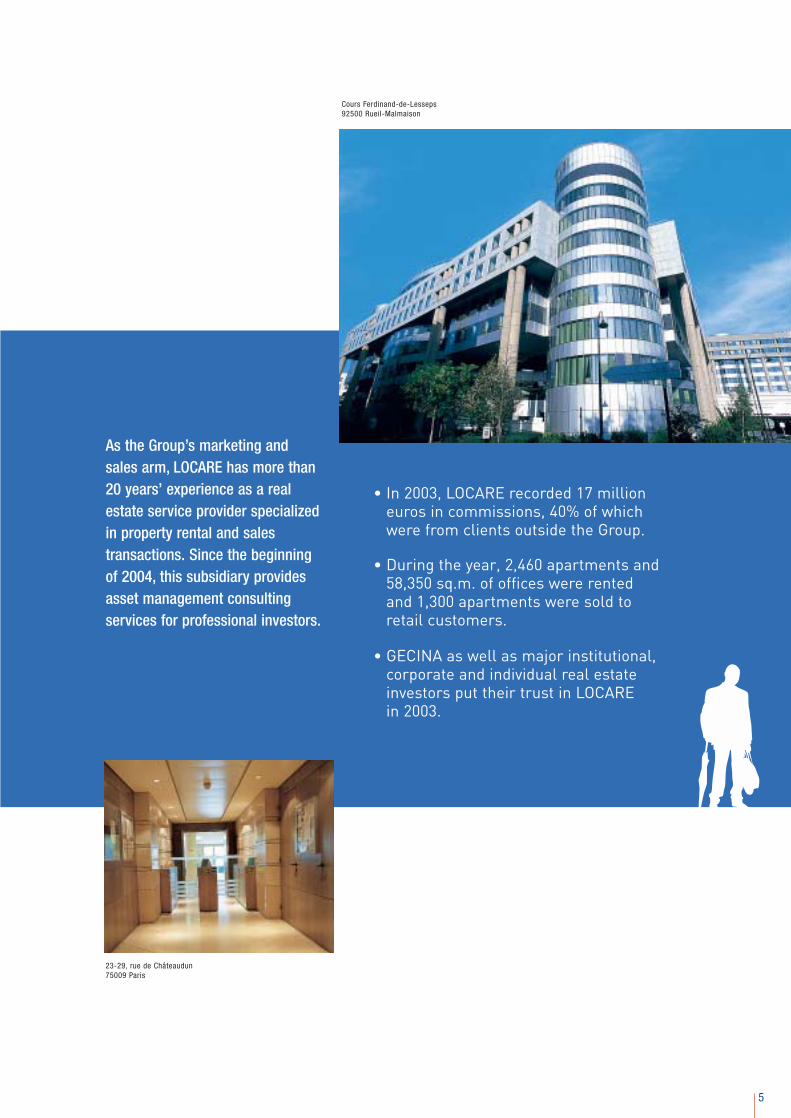

The process GECINA employs to create value is based onthe mastery of new businesses better able to take advantageof fluctuations in the real estate markets. Most activities arepiloted within the Company – acquisitions, divestments,development, marketing, asset management and, last butnot least, financial and real estate engineering. The size theGroup has attained has enabled it to bolster operationsthrough the addition of various support functions – Quality,Research, Strategy and Marketing, and Risk Management.These activities make GECINA more responsive and betterable to create value. They are made available to third parties through LOCARE, one of the top ten brokers in Paris,and COMPAGNIE FONCIERE DE GESTION, which is dedicatedto real estate management.

32-34, rue Guersant 75017 Paris

5

• In 2003, LOCARE recorded 17 millioneuros in commissions, 40% of whichwere from clients outside the Group.

• During the year, 2,460 apartments and58,350 sq.m. of offices were rentedand 1,300 apartments were sold toretail customers.

• GECINA as well as major institutional,corporate and individual real estateinvestors put their trust in LOCARE in 2003.

23-29, rue de Châteaudun75009 Paris

Cours Ferdinand-de-Lesseps 92500 Rueil-Malmaison

As the Group’s marketing andsales arm, LOCARE has more than20 years’ experience as a realestate service provider specializedin property rental and sales transactions. Since the beginningof 2004, this subsidiary providesasset management consulting services for professional investors.

6

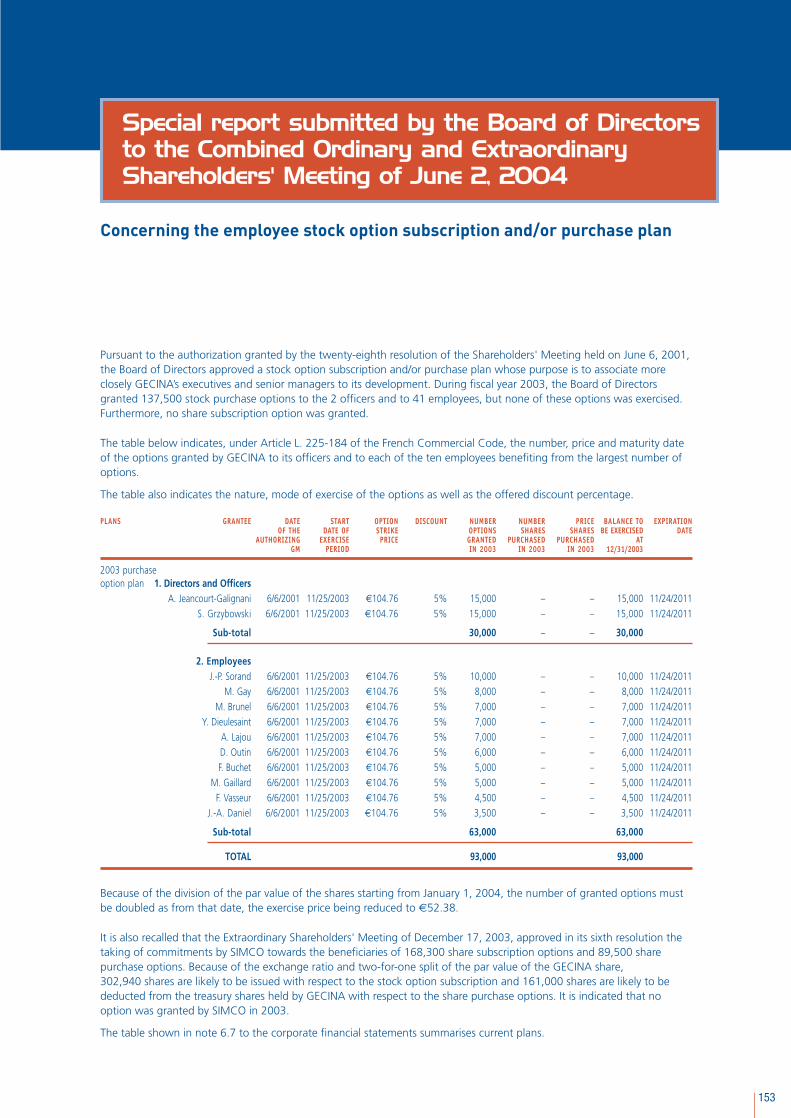

Year’s highlights

A Group on the road to success

2003JanuaryGECINA joined forces with Apsys, one of France’s majorcommercial real estate operators, to restructure the Beaugrenelle mall in Paris. With its financial partnersFoncière Euris and Francarep, Apsys now has a 50%interest in this asset, and GECINA holds the other 50%.In close cooperation with all the local players, the projectinvolves major restructuring and the extension of the mallto 40,000 sq.m.GECINA will continue to ensure the management of thewhole operation, as well as administrative and financialmanagement for the project.

Work started on the future headquarters of the GECINAGroup at 5bis-7, rue Volney / 14-16, rue des Capucines,Paris 2nd, in the central business district between theOpera, la place de la Madeleine and the place Vendôme.

February GECINA successfully launched its first bond issue in the amount of 500 million euros. Partial refinancing of the syndicated loan negotiated when SIMCO wasacquired in November 2002 allowed the Group to extendand diversify its sources of financing.

MayCrédit Foncier transferred its entire stake in GECINA(4.1%) to Prédica, the Crédit Agricole Group’s lifeinsurance company. Ownership of this equity holding, theresult of GECINA’s takeover bid on SIMCO, was required tobe maintained until May 16, 2003. Prédica then becameone of GECINA’s major shareholders with 9.4% of thecapital.

On May 28, GECINA signed the definitive sales contractfor 47 buildings, mainly residential Haussmann-styleproperties, in the amount of 563 million euros. Thisdivestment represented a total of 1,965 apartments, asstipulated in the agreement signed on October 14, 2002,with the American company Westbrook Partners.

JuneGECINA’s Annual Shareholders’ Meeting decided to renewthe terms as members of the Board for a period of threeyears of Laurent Mignon, Christian de Gournay, Azur-Vieand Antoine Jeancourt-Galignani, whose position asChairman of the Board of Directors was confirmed by theBoard at the meeting held after the Annual Shareholders’Meeting. The Annual Shareholders’ Meeting also ratifiedthe appointment of Anne-Marie de Chalambert as amember of the Board to replace GPA Vie, which resigned,for the remainder of the latter’s term.

JulyThe Axa Group sold its 6.2% equity interest in GECINA,after the expiration of the commitment not to sell on May16, 2003. These shares were placed with a wide circle ofinternational investors.In keeping with the calendar announced on July 31, 2003,the protocol agreement signed with Westbrook Partnerson October 14, 2002, was completed when the definitivesales contract was signed for 50 buildings that were

7

2004formerly SIMCO assets. This second part of the agreementrepresented a sale of assets in the amount of 575 millioneuros for almost 140,000 sq.m. of mainly residentialHaussmann-style properties for a total of 1,151 apartments.

GECINA published an increase in half-year rental incomeof more than 100%. For the first time, commercialrentals accounted for more than 50% of the Group’stotal rental income.

SeptemberGECINA opted for the new SIIC tax system withretroactive effect as of January 1, 2003. This systemallows the Group to benefit from a tax exemption on rental income and capital gains on real estatetransactions generated within the framework of itsactivities as a real estate investment trust. Conversely,GECINA should pay an exit tax of 569.4 million euros, a quarter of which is payable every December 15 from2003 to 2006.

OctoberGECINA Group brought its teams together at 34, rue dela Fédération, Paris 15th.

DecemberThe Shareholders’ Meetings of GECINA and SIMCOapproved the merger of SIMCO into GECINA.Announced as a possible complement to the takeover bidon SIMCO, the merger is a logical stage in the Group’sdevelopment. The parity of the merger was nine GECINAshares for ten SIMCO shares, the same as was proposedduring GECINA’s takeover bid on SIMCO in the autumnof 2002.

JanuaryOn January 2, the par value of GECINA shares wasdivided in half to 7.50 euros. Registered shares becamemandatory as of January 7.

The 6,300 sq.m. of GECINA’s former headquarters,located at 2ter, boulevard Saint-Martin, Paris 10th, wererented under satisfactory market conditions.

FebruaryThe Dauphiné Part-Dieu project was completed. The 13,000 sq.m. of office space are located near the Part-Dieu rail station in Lyons.

MarchIn the presence of Gérard Collomb, Senator-Mayor of Lyons, the project for the Labuire concertedredevelopment zone was presented at the 2004 MIPIM(international marketplace of real estate professionals),which was held in Cannes from March 9 to 12. In partnership with the “Grand Lyons” and the city of Lyons, GECINA and Lyonnaise de Banque joined forcesin SAS LABUIRE Aménagement as planner. The projectinvolves making five hectares of undeveloped land into140,000 sq.m. plots on which offices, stores, housingand public facilities can be built.

193, rue de Bercy 75012 Paris

8

Questions for

Antoine Jeancourt-Galignaniand Serge Grzybowski

How do you analyze GECINA’s annualresults, which for the first timeconsolidated SIMCO on a full year basis?Serge Grzybowski: GECINA reported good and veryencouraging results in 2003. The operating margin, i.e.the ratio between EBITDA (excluding net income fromsales of real estate holdings) and rental income, againimproved, rising to 77.7%. The impact of the adoptionof the SIIC tax system was a 42.6% increase in currentcash flow1 per share after tax. Even more convincing wasthe 9.1% rise in current cash flow before tax, in line with our objectives. In fact, if abstraction is made of the creation of shares at the end of the year following the merger of SIMCO into GECINA and the conversion of former GFC 3.25% bonds, pre-tax current cash flowper share stood at 15.3%.

How do you explain this performance?Antoine Jeancourt-Galignani: These results areconcrete proof of the benefits generated by the mergerof GECINA and SIMCO, as we had announced to the shareholders’ of both companies. But they also owea great deal, and increasingly so, to the policy implementedfor almost three years now that aims to rebalance our asset portfolio. The consistency and coherence of our strategic choices have thus been confirmed – a commercial focus that has been honed according tostrict criteria ensuring the yield, quality and the regularityof flows, an optimized residential activity, a relutive financialstructure, and an organization clearly defined by line of business.

S. G.: As we promised in this forum last year, SIMCO wascompletely integrated as of 2003. The legal merger ofthe two companies was approved by each company’sShareholders’ Meeting on December 17, 2003. This operation took effect on December 31, 2003. At the operational level, the process was already wellunderway during the year as the companies’ teams were

regrouped, the Executive Committee was named, and an organization was set up, with the addition of a significant marketing subsidiary, one of the tenlargest brokers in Paris, and new support functions(research, quality, etc.). I would like to take thisopportunity to associate the men and women in theGroup with this success and thank them for their efforts.

A. J.-G.: Let me add that the Group achieved theobjective it had set to reduce debt in 2003. At the end ofDecember, the revalued debt-equity ratio was once againlower than 40% and EBITDA covered financial expensemore than 2.5 times. GECINA now has financialresources that open the door to new opportunities.

On this point, there are frequent marketrumors about new external growthoperations? Is there any truth to them?A. J.-G.: GECINA is certainly not opposed to the prospectof external growth, a strategy that it has employedfrequently in the past. We carefully study any and allopportunities. But we have strict requirements in termsof the creation of value that neither we nor ourshareholders and the Board of Directors will forego.Today, this approach distances us from certain currentoperations, all the more so since the new GECINA nowhas the resources it needs to focus more on internalgrowth.

S. G.: The merger with SIMCO makes it possible to formteams of experts dedicated to the Group’s development.While carrying out a 1.5 billion euro divestment programin 2003, these teams conducted several developmentprojects representing a total of 90,000 sq.m. GECINAalso benefits from a preliminary agreement to acquiremore than 20,000 sq.m. of commercial real estatelocated in Paris. This investment totals 121 million euros.As you can see, the redeployment of the Group throughits internal resources is on the right track.

9

Antoine Jeancourt-GalignaniChairman

Serge GrzybowskiChief Executive Officer

Let’s talk some more about the SIICstatus GECINA has adopted. What is the benefit for shareholders? S. G.: It’s a great advantage. This new tax systempotentially gives us greater flexibility to pursue an arbitrage policy based on economic fundamentalswithout having to calculate the impact of taxes. Our arbitrage policy, in both the residential and commercial sectors, will be designed on the basis of our objectives to improve the overall return on ourassets. For example, tax savings in 2003 were greaterthan the first payment of the exit tax last December 15.

A. J.-G.: The SIIC option led to an immediate revaluation of the Group. As of December 31, post-tax diluted netrevalued block assets2 per share increased by 27.1% in a year. This option also enabled us to internationalize ourshareholding base, in particular with the arrival of Americanshareholders who are familiar with Real Estate InvestmentTrusts (REITs), an American vehicle that has approximatelythe same tax status as ours. Their joining our shareholderranks was accompanied by a reduction in GECINA’s share price discount vis-à-vis a sharp increase inrevalued net assets per share. This was one of the reasonsfor the positive trend in the share price over the last fewmonths. Finally, there was a significant rise in distribution. A dividend of 2.45 euros per share has been proposed to the Shareholders’ Meeting of June 2. This represents an increase of 22.5%, with the gross dividend proposed up 12.0% to 3.35 euros.

What message do you want to send to your shareholders?S. G.: There are many ways to create value for ourshareholders. We should, therefore, continue to improvethe return on assets in the next two years. At the end of this process, the breakdown of residential and commercial activities should stand at 30%-35% and 65%-70%. The objective of an operating margin of 80% is within our grasp.

A. J.-G.: The implementation of our strategy justifies an objective of double-digit growth in current cash flowper share. In 2004, the increase should be between 5%and 10%. The top of this range will be all the easier toattain if significant investments are made during the year.

Finally, GECINA’s reputation as a yield stock will beconfirmed in 2005. The tax reforms in France and ournew tax system together have a very positive impact for our shareholders. This will be particularly the case forindividual shareholders, who benefit not only from higherdividends as a result of SIIC bonds, but also the commonlaw tax exemption on dividends. They will benefit the most from the reform and we invite more of them to join us.

1 Cash flow excluding net income from sales of real estate holdings.2 On the basis of a block valuation, net selling prices, of real estate assets.

10

Corporate management

Recognized and complementary skills

GECINA’s Board of DirectorsAntoine Jeancourt-GalignaniChairman of the Board

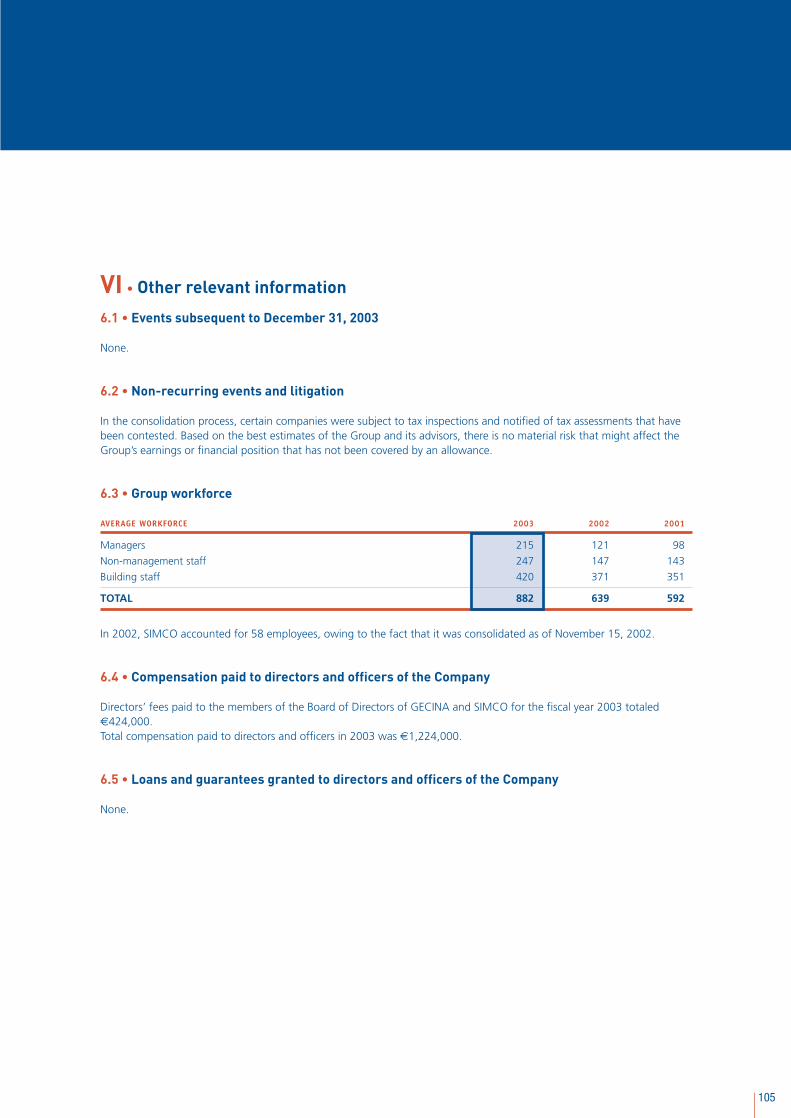

Michel Pariat Vice Chairman

Charles RuggieriChairman, Batipart

Christian de GournayChairman of the Executive Board, Cogédim

Bertrand Letamendia Chief Real Estate Officer, AGF

Azur Vie represented by Bruno LegrosChief Investment Officer, Azur GMF

GMF Vie represented by Sophie Beuvaden Chief Executive Officer Delegate,Finance division, Azur GMF

Anne-Marie de Chalambert1

Chairman and Chief Executive Officer,Generali Immobilier Conseil

Laurent MignonChief Executive Officer, AGF

Jean-Paul Sorand2

Chairman’s Delegate Director

Bertrand de Feydeau Chief Executive Officer,Economic Affairs, AssociationDiocésaine de Paris

Philippe Geslin Chairman, Banque Française de l’Orient

Françoise Monod Attorney

Prédica represented byJean-Pierre Bobillot Deputy Chief Executive Officer, Prédica

Appointments andCompensation Committee

Laurent Mignon, Chairman

Sophie Beuvaden

Christian de Gournay

Françoise Monod

Antoine Jeancourt-Galignani3

Audit CommitteePhilippe Geslin, Chairman

Bertrand Letamendia

Jean-Pierre Bobillot

Bruno Legros

(Details of directors’ compensation and terms ofoffice are provided in the management report. Theconditions of the organization and preparation ofthe Board and the Group’s internal control arepresented in the Chairman’s report.)

1 Director whose mandate the Shareholders’Meeting of June 2, 2004, is asked to renew.

2 Director with executive management functionssince December 20, 2002.

Quality and SustainableDevelopment Committee Charles Ruggieri, Chairman

Anne-Marie de Chalambert

Bertrand de Feydeau

Jean-Paul Sorand, Reporter

Executive Management Serge Grzybowski Chief Executive Officer

Independent StatutoryAuditorsErnst & Young Audit4

F-M Richard & Associés4

Mazars & Guérard5

Independent AlternateAuditors Patrick de Cambourg6

Sylvain Elkhaim7

Dominique Duret-Ferrari7

Board SecretaryJean-Alain Daniel

3 Appointments only.

4 Independent Statutory Auditor whose mandateexpires June 2, 2004, a fact of which theShareholders’ Meeting held on the same day isinformed.

5 Independent Statutory Auditor whose resignationas the Company’s third auditor is proposed to theShareholders’ Meeting of June 2, 2004, andwhose appointment for six years is proposed tothe Shareholders’ Meeting held on the same day.

6 Independent Alternate Auditor whose resignation isproposed to the Shareholders’ Meeting of June 2,2004, and whose appointment for six years isproposed to the Shareholders’ Meeting held on thesame day.

7 Independent Alternate Auditor whose mandateexpires June 2, 2004, a fact of which theShareholders’ Meeting held on the same day isinformed.

11

Antoine Jeancourt-GalignaniChairman

Serge Grzybowski Chief Executive Officer

Méka BrunelDevelopment Director

Yves Dieulesaint Director of Residential Property

Michel Gaillard Lyons Regional Director

Michel Gay Financial and Administrative Director

André LajouDirector of Commercial Property

Etienne Marcot Chief Executive Officer of LOCARE

Denis Outin Human Resources Director

From left to right and from top to bottom:Antoine Jeancourt-GalignaniSerge GrzybowskiMéka BrunelYves Dieulesaint Michel Gaillard Michel Gay André LajouEtienne Marcot Denis Outin

Executive Committee

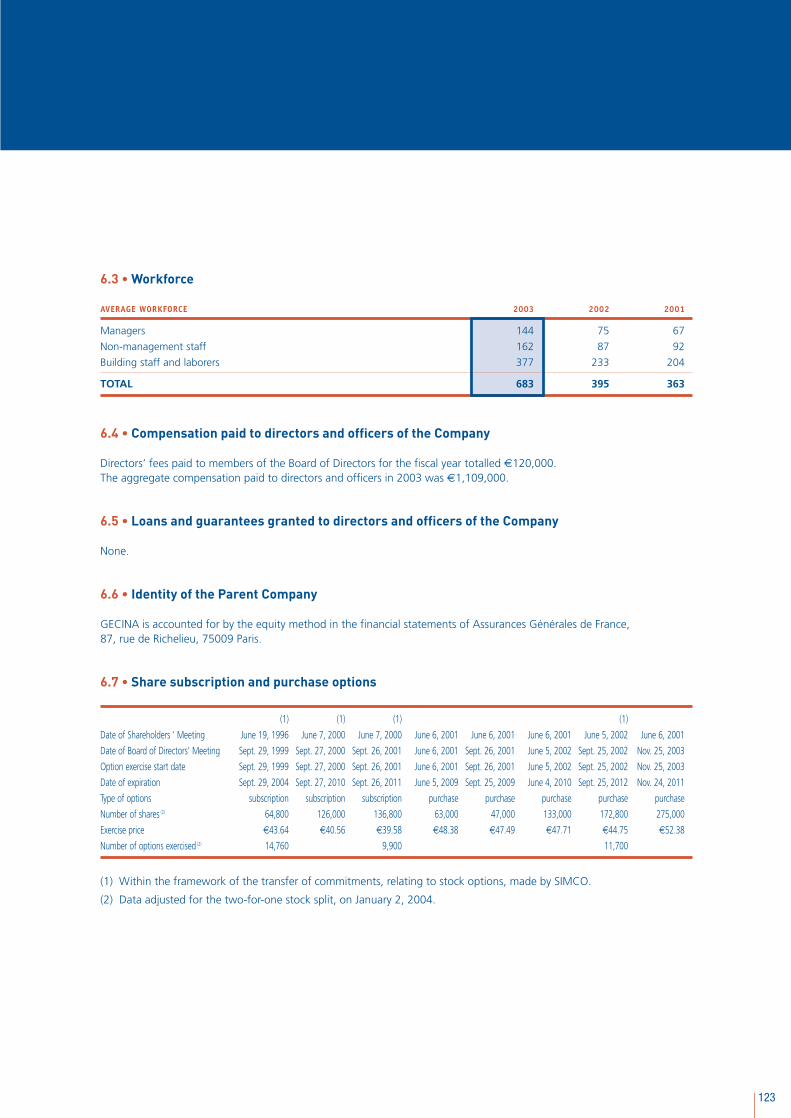

GECINA financing policy is designed to minimize theaverage weighted cost of capital and, in particular,of debt, within the framework of strict managementof interest rate, liquidity and counterparty risks. In 2003, the priority was debt reduction and the diversification of sources of financing, two majorfactors in restoring the Group’s financial capacity so as to pursue its growth.

For many years, GECINA has implemented a policythat targets regular growth in dividends, reflectingincreased current cash flow per share. The adoptionof the SIIC status confirms GECINA’s reputation as a yield stock, and within the framework of French tax reforms, will boost net income aftertaxes for all owners of shares, and most especially,individual shareholders.

The GECINA Group is resolutely engaged in a processthat targets the creation of value based on anenhanced return on assets. In 2004, GECINA defineda new multi-year arbitrage plan in the amount of 500 million euros. Comprised of residentialHaussmann-style properties in Paris, with a grossyield of less than 5%, these assets will be sold byunit in order to maximize the resources gleaned. Atthe same time, the high market values of commercialinvestments are exploited by the sale (for 200 millioneuros) of offices with mature rents and thereforelimited growth potential.

In 2003, GECINA took the steps required to createinternal growth relays. Capable of generating almost30 million euros in additional rental income on the basis of high yield properties, several assetdevelopment projects, representing a total of 90,000 sq.m. of commercial premises in Paris and Lyons, has been launch. At the same time,GECINA implements an opportunistic assetacquisition policy that represents real prospects forshort-term profitability. The Company targets officebuildings with an area of more than 10,000 sq.m.and with long-term rental flows.

Strategy

know-howprofitability

know-howdevelopment

know-howremuneration

know-howfinancing

12

1 Vente au détail par appartement.

132-4, quai Michelet 92300 Levallois-Perret

An objective of profitable redeployment

14

Portfolio highlights

Major improvement

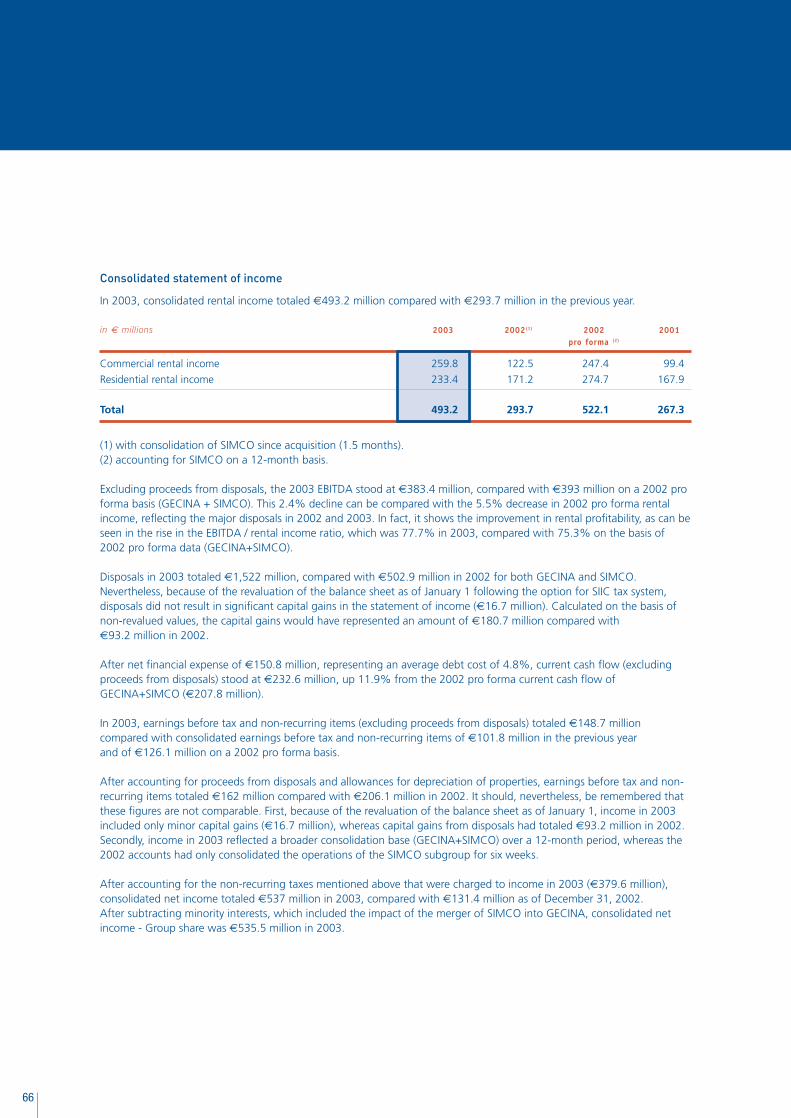

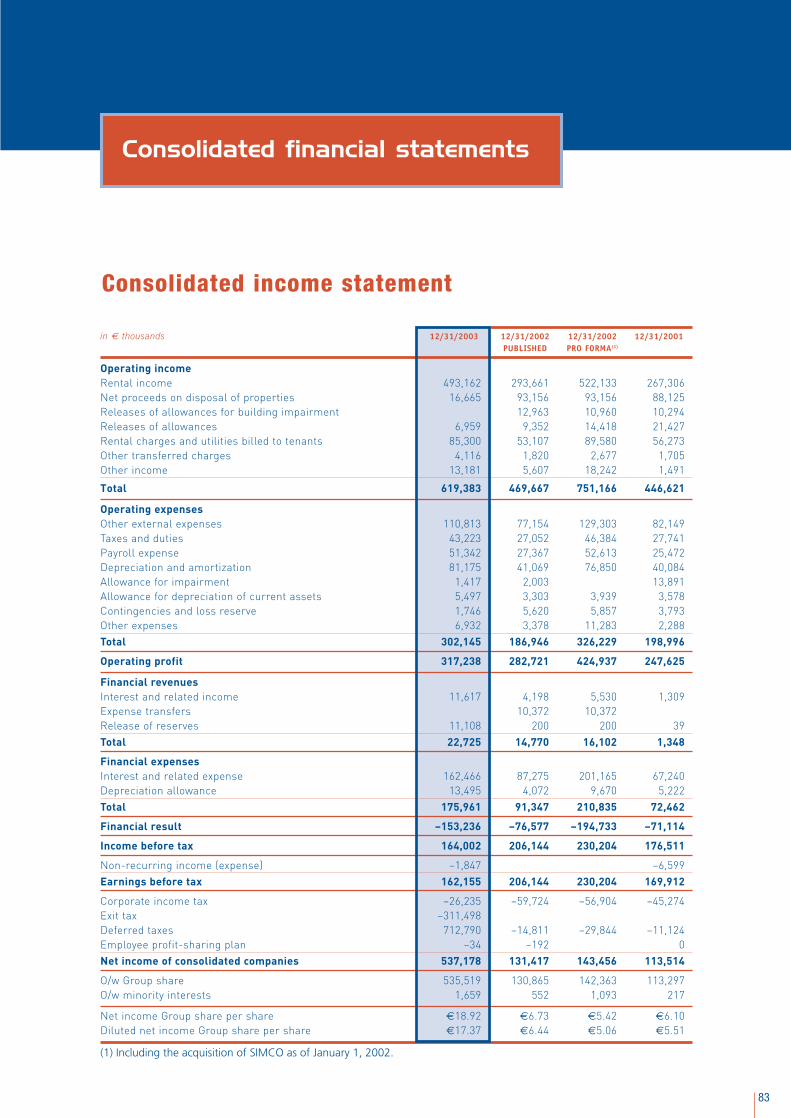

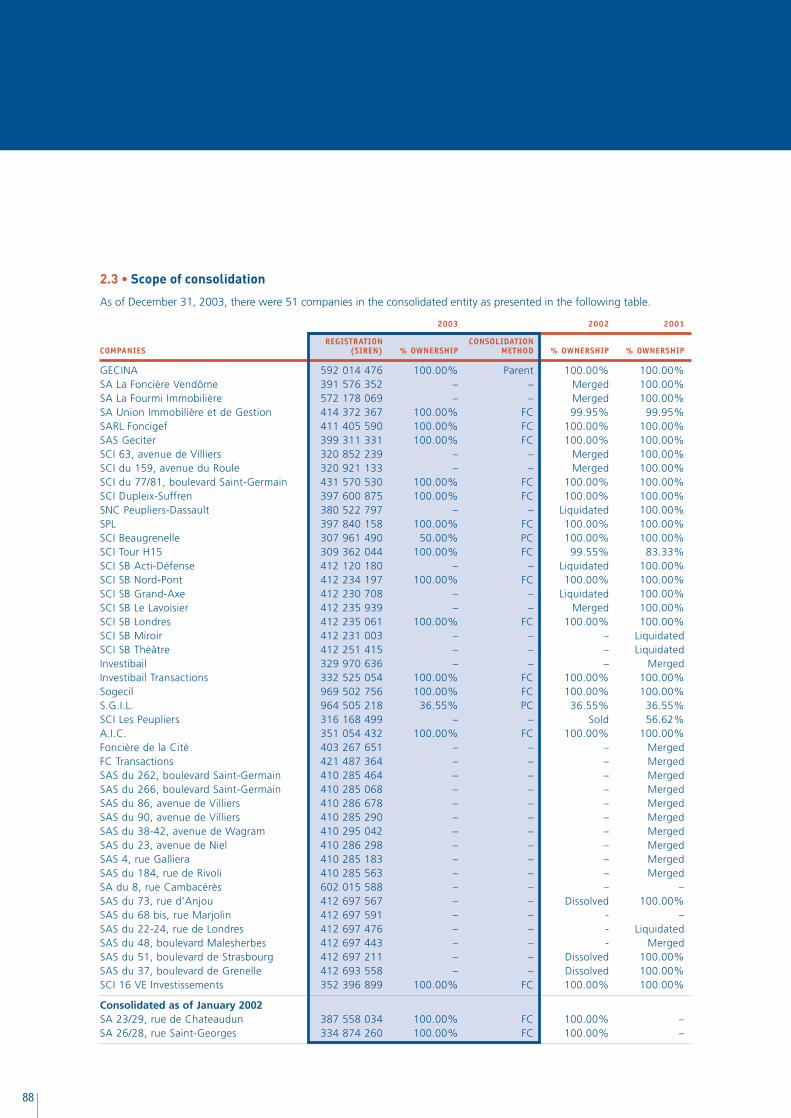

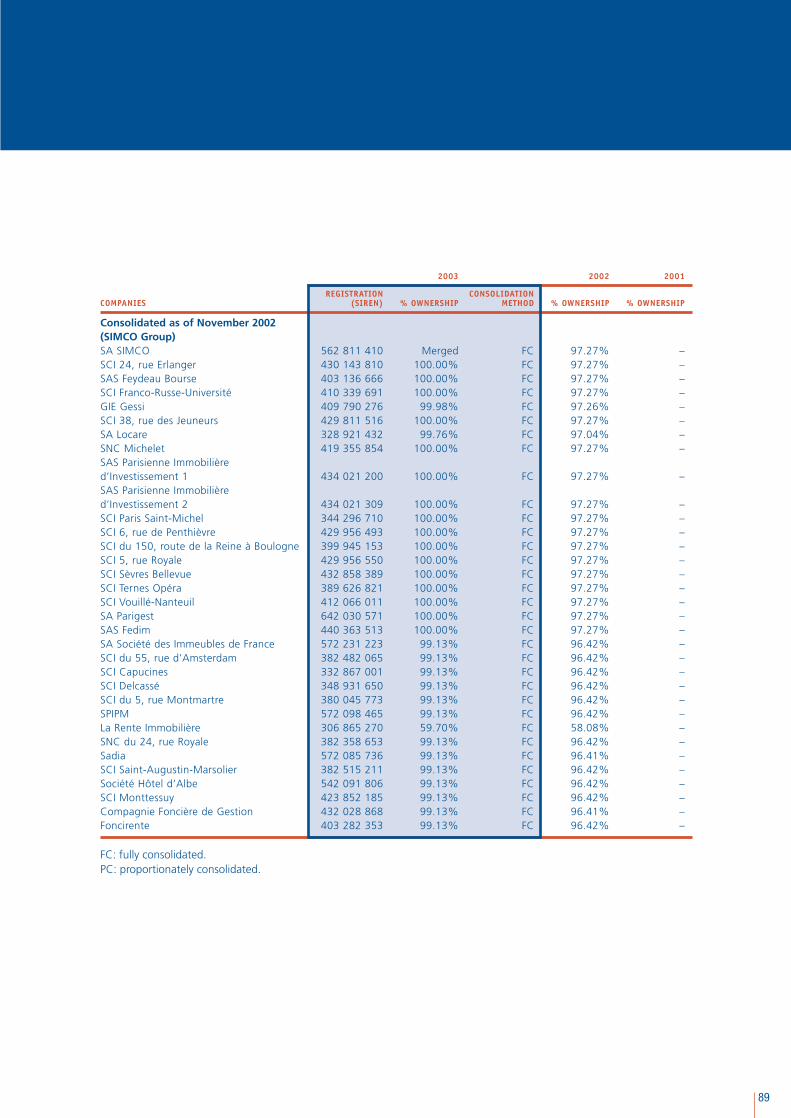

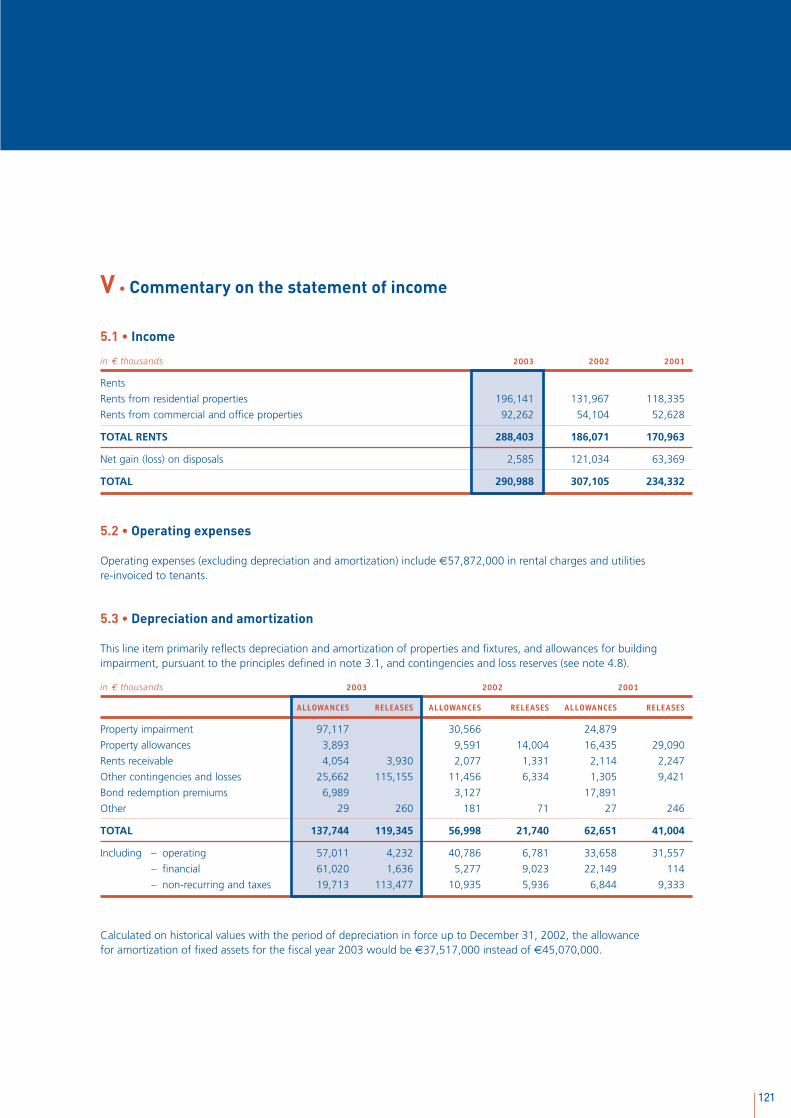

millions of euros unless otherwise stated 2001 2002 2003

• Rental income 267.3 293.7 493.2Commercial properties 99.4 122.5 259.8Residential properties 167.9 171.2 233.4

• Revalued block value of assets as of December 311 4,091.7 8,403.8 7,111.9Commercial properties 1,440.7 4,029.9 3,871.5Residential properties 2,652.0 4,373.9 3,240.4

• Revalued retail value of assets as of December 312 4,543.7 9,017.9 7,793.3Commercial properties 1,479.0 4,075.2 3,915.3Residential properties 3,064.7 4,942.7 3,878.1

• Gross return on assetsrental income/revalued block value of assets1 6.53 % 6.21 %3 6.93 %

• Total surface area of real estate assets as of December 31 1,722,868 sq.m. 2,771,699 sq.m. 2,248,710 sq.m.Commercial properties 536,189 sq.m. 1,014,167 sq.m. 929,621 sq.m.Residential properties 1,186,679 sq.m. 1,757,532 sq.m. 1,319,089 sq.m.

• Number of apartments as of December 31 16,671 24,400 19,044• Investments 50.9 4,354.1 131.4• Divestments 315.3 334.9 1,521.8

Consolidated data

Change in residential and commercial business

2001 2002 2003

37.2

62.8

41.7

58.3

47.352.7

1 On the basis of block valuation appraisals, net selling prices, of real estate assets.2 On the basis of unit valuation appraisals, net selling prices, of residential properties and of block valuation

appraisals, net selling prices, of commercial premises.3 On the basis of 2002 pro forma GECINA-SIMCO rental income of 522.1 million euros.

% of the Group’s rental income

2001 2002 2003

64.8

35.2

48.052.0

45.654.4

% of the revalued block value of assets1

Residential

Commercial

1 On the basis of block valuation appraisals, net selling prices, of real estate assets.

15

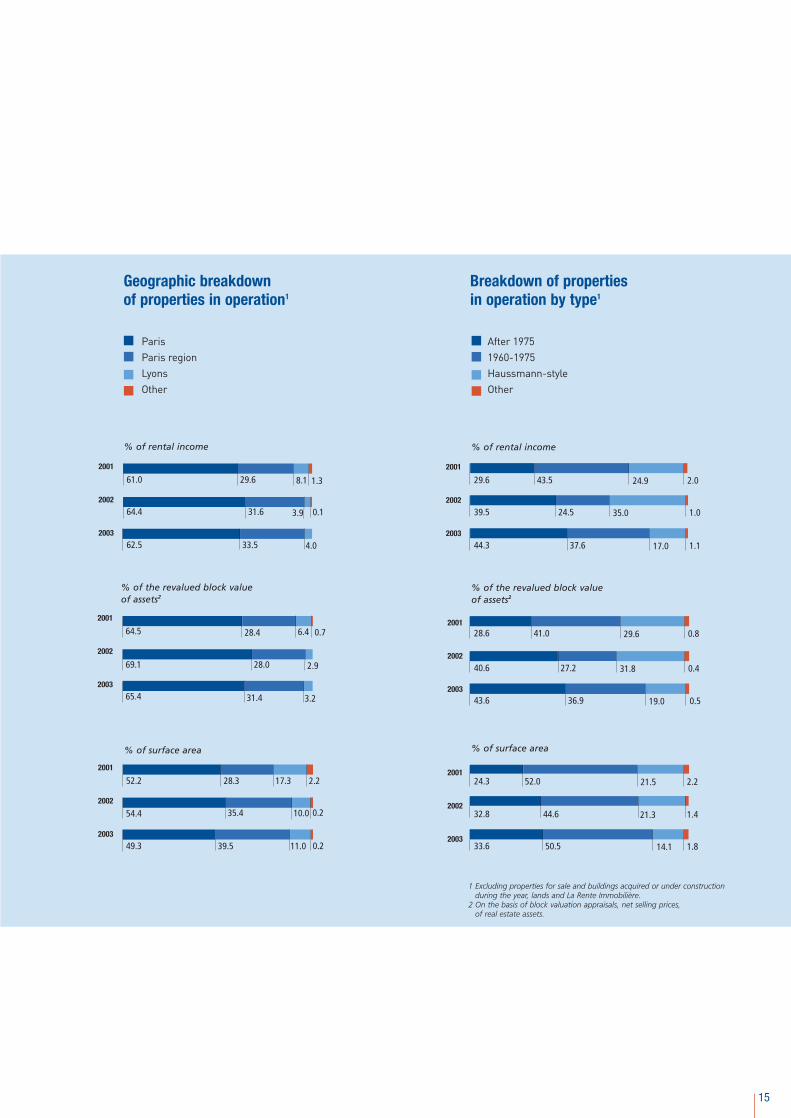

Geographic breakdown of properties in operation1

Breakdown of properties in operation by type1

% of rental income

2001

2002

2003

2001

2002

2003

% of the revalued block value of assets2

2001

2002

2003

% of surface area

50.533.6 14.1 1.8

44.632.8 21.3 1.4

52.024.3 21.5 2.2

1 Excluding properties for sale and buildings acquired or under constructionduring the year, lands and La Rente Immobilière.

2 On the basis of block valuation appraisals, net selling prices, of real estate assets.

After 19751960-1975Haussmann-styleOther

ParisParis regionLyonsOther

36.943.6 19.0 0.5

27.240.6 31.8 0.4

41.028.6 29.6 0.8

37.644.3 17.0 1.1

24.539.5 35.0 1.0

43.529.6 24.9 2.0

% of rental income

2001

2002

2003

33.562.5 4.0

31.664.4 3.9 0.1

29.661.0 8.1 1.3

% of the revalued block value of assets2

2001

2002

2003

31.465.4 3.2

28.069.1 2.9

28.464.5 6.4 0.7

2001

2002

2003

39.549.3 11.0

35.454.4 10.0 0.2

28.352.2 17.3 2.2

0.2

% of surface area

16

Financial highlights

Objectives achieved

70.8%

74.6%

77.7%

1.8

2.7

3.4

2001 2002 2003

Operating margin

3.8

12/31/2001 12/31/2002 12/31/2003 4/10/2004

GECINA’s stock market capitalization

Breakdown of gross financial debtas of December 31, 2003

Shareholding structureas of March 31, 2004

13.6% Azur GMF

23.9% AGF

9.7% Prédica (CréditAgricole Group)

4.2% Treasury stock11.1% Individual shareholders

18.7% Non-resident shareholders

18.8% Other institutional residents

14% Convertiblebonds

12% Financeleases

29% Bankloans

12% Commercialpaper

33% Bonds

EBITDA1 / rental income (%) billions of euros

1 Excluding net income from divestments.

17

millions of euros unless otherwise stated 2001 2002 2003

• EBITDA1 189.1 219.1 383.4• Net financial expense 65.9 72.7 150.8• EBITDA1 / net financial expense 2.87 x 3.01 x 2.54 x• Pre-tax current cash flow1 123.2 146.3 232.6• Current cash flow after tax1 90.6 110.3 229.0• Diluted pre-tax current cash flow1 2 130.7 151.5 242.4• Diluted current cash flow after tax1 2 93.6 112.5 238.9• Net income, Group share 113.3 130.9 535.5• Net financial debt as of December 31 1,421.0 3,993.0 2,513.0• Shareholders’ equity as of December 31 1,113.3 3,515.43 3,773.1• Revalued net block asset value after tax as of December 314 1,923.5 2,937.7 4,043.9• Revalued net unit asset value after tax as of December 315 2,215.4 3,329.8 4,725.3• Diluted revalued net block asset value after tax2 4 2,156.8 3,390.7 4,389.5• Diluted revalued net unit asset value after tax 2 5 2,448.7 3,782.7 5,070.9• Net financial debt / revalued net block asset value

as of December 314 34.73% 47.75% 35.33%• Net financial debt / revalued net unit asset value

as of December 315 31.27% 44.48% 32.25%• Net financial debt / shareholders’ equity as of December 31 1.28 x 1.98 x 0.65 x• Total dividends6 69.3 108.2 138.3

euros 2001 2002 2003

• Pre-tax current cash flow1 3.32 3.77 4.11• Diluted pre-tax current cash flow1 2 3.18 3.58 3.82• Current cash flow after tax1 2.44 2.83 4.04• Diluted current cash flow after tax 1 2 2.28 2.65 3.76• Net income, Group share 3.05 3.37 9.46• Diluted revalued net block asset value after tax2 4 52.87 54.53 69.28• Diluted revalued net unit asset value after tax2 5 60.02 60.83 80.03• Net dividend 1.80 2.00 2.456

• Gross dividend 2.70 3.00 3.356

2001 2002 2003

• Number of shares comprising the share capital as of December 31 38,476,100 54,092,752 58,038,246

• Number of shares excluding treasury shares as of December 31 36,796,524 52,652,818 56,432,164

• Diluted number of shares excluding treasury shares as of December 312 40,796,978 61,879,826 63,358,772

• Average number of shares 37,125,948 38,874,050 56,609,724• Diluted average number of shares2 41,126,402 42,331,052 63,536,332

Consolidated financial data

1 Excluding net income from divestments.2 Diluted by existing convertible bonds.3 After restatement of the balance sheet as of January 31, 2003.4 On the basis of block valuation appraisals, net selling prices, of real estate assets.5 On the basis of unit valuation appraisals, net selling prices, of residential properties and of block valuation appraisals, net selling prices,

of commercial premises.6 Subject to the approval of the Shareholders’ Meeting of June 2, 2004, and a dividend payment base of 56,412,164 shares.7 Data restated to account for the split of the par value of shares as of January 2, 2004.

Per share data7

Number of shares7

18

GECINA and its shareholders

In 2003, GECINA confirmed its status as a major stockinvestment in its sector at the European level with a15.45% increase in the share price, an increasinglydiversified shareholding structure and enhanced financialcommunication.

A SIIC with cloutIn less than three years, GECINA’s stock marketcapitalization has more than doubled, rising to 3.8 billioneuros in April 2004. This growth was accompanied by an expansion of its shareholding base, which is now halffreefloat. Together with AGF (23.95%), Azur GMF(13.64%) and Prédica, the Crédit Agricole Group’s life-insurance subsidiary (9.71%), non-resident investorsincreased their holdings significantly to 18.66% as of March 31, 2004, at the same level as residentinstitutional shareholders (18.64%). Individual shareholdersrepresent 11.06% of the capital, with an average of 174 shares.

At the same time, the liquidity of GECINA shares improvedmarkedly with an increase of more than 200% in tradingvolume in 2003. When the par value was divided in half on January 2, 2004, the average number of shares tradedsurpassed 110,000 per day in the first three months of 2004.

Registered sharesSince January 7, 2004, all GECINA shares must be registered shares. Approved by the Shareholders’ Meeting of December 17, 2003, this form enables shareholders to benefit from personalized services that includeannouncements of Shareholders’ Meetings, participation inShareholders’ Meetings without having to obtain a banker’scertificate freezing shares, and invitations to events forindividual shareholders. An in-house team manages “pure”registered shares with no custody fees and reducedbrokerage commissions. There are also “administered”registered shares that allow shareholders to continue towork with their brokers. The account is therefore managedunder the conditions practiced by the broker firm.

Regular and detailed informationIn 2003,GECINA continued to improve the quality of itsfinancial communication by adding new indicators tobolster its financial information. The number of pressreleases was increased and more diversity wasintroduced into the subjects announced (appointments,divestments, investments, new rentals, etc.) in order toprovide greater regularity and transparency with regardto major events in the life of the Group. Information isput online at www.gecina.fr as soon as it is announcedin order to ensure equal access to information for allshareholders, whatever their profile and nationality.

A grass-roots approach and dialogueGECINA is committed to establish and maintaindialogue with its shareholders. Throughout the year,management is in regular contact with the financialand economic press, financial analysts, investors andindividual shareholders.

With institutional shareholders, analysts andjournalists, these contacts take the form ofconferences, SFAF meetings organized on theoccasion of the publication of annual and half-yearresults, group or individual meetings.

A particular effort was made in 2003 to attractindividual shareholders. For the first time, GECINAtook part in the Actionaria shareholding promotionevent, which was held in Paris on November 21 and22, 2003. In addition, dedicated services were createdto maintain close contact:

■ a free telephone service for direct dialogue with theInvestor Relations team;

■ an e-mail address.

GECINA plans to continue to develop this area and isstudying new investor relations opportunities (visits toGECINA properties, shareholder meetings outside ofParis, etc.).

Emphasis on the qualityof information

GECINA shares

■ Number of shares: 58,053,246 as of March 31, 2004

■ ISIN code: FR0010040865

■ Stock Exchange: Euronext Paris, (Premier Marché)Service à Règlement Différé

■ Indexes: SBF 120, Euronext 100, MSCI, EPRA

GECINA shareholders’ calendar

■ May 27, 2004Participation in the conference on listed real estatecompanies organized by Kempen & Co in Amsterdam

■ June 2, 2004Shareholders’ Meeting to approve the 2003 financialstatements

■ June 8, 2004Dividend paid

■ July 28, 2004Publication of 2004 half-year results after the stockexchange closes

■ July 29, 2004SFAF financial analysts’ meeting on 2004 half-year results

■ October 15, 2004Publication of rental income in the third quarter of 2004

■ November 19-20, 2004GECINA stand at the Actionaria shareholding promotionevent in Paris

Contacts

Financial Communication

■ Financial analysts, investors and press relations: Laurence Bousquet + 33 1 40 40 52 21

■ Individual shareholders: Régine Willemyns + 33 1 40 61 66 46

Securities and Stock Market

Laurent Le Goff + 33 1 40 61 66 71

19

350

300

250

200

150

100

50

0

80

70

60

50

40

GECINA share price

Price in euros Trading volume (millions of euros)

euros millions of euros

01.99 01.00 01.01 01.02 01.03 01.04

20

Human resources

Optimized organizationAt the end of 2003, the GECINA Group employed 798 men and women, including 373 housekeepers. By focusing their efforts on the harmonization of workprocedures and methods, the seven working groupscreated in 2002 contributed to the success of themerger of the two companies in December 2003. Their missions mainly concerned the Group’s legal and accounting reorganization, IT, the search for newheadquarters, changes in marketing strategy, externaland financial communication, new third-party activitiesand labor and human resources issues.

In addition to the two functional divisions (HumanResources, Administration and Finance), five operationaldivisions were created in line with the Group’s strategy:the Residential Properties division, the CommercialProperties division, the Development division, Marketingand Sales, and the Lyons Region division. Managementof residential properties and commercial properties is thus clearly distinguished, since each categorycorresponds to a specific market approach and clientbase. The Development division is responsible for applying the Group’s strategy concerning its assetholdings and the appropriate arbitrage policy, and for exploring geographic expansion and productdevelopment.As a result of the alliance with the SIMCO Group,Marketing and Sales benefited significantly from the addition of a line of business targeting third parties.LOCARE, initially a SIMCO subsidiary, has recognizedexperience in organizing property rentals and sales,either of Group products or for major institutionalinvestors specialized in residential real estate.The managers, technicians, sales staff, etc. in the LyonsRegion division deal with all aspects of real estatemanagement in Lyons and the surrounding area.

New headquarters Since October 2003, GECINA and SIMCO teams worktogether in the Group’s new headquarters at 34, rue de laFédération, Paris 15th. This first move will be following by another when the Group takes possession of its newlyrenovated building at 14-16, rue des Capucines, Paris 2nd, in the autumn of 2004. The Lyons Region division (staff of 23 and 24 housekeepers) will remain in Lyons (29, quai Saint-Antoine, Lyons 2nd).

A common employment status, harmonized toolsIn 2003, the labor agreements existing at GECINA andSIMCO were harmonized, leading to the adoption of a newsocial and economic unity since the two companies mergedin December 2003. Since January 2004, employees in all the of the GECINA Group’s companies share the sameemployment status, which defines new conditions for working together.

This dynamic was complemented by the upgrade of ITsystems, to the advantage of the Group and its employees.Launched by a study in the first half of 2003, the convergenceof IT systems was effective as of January 5, 2004.

All the administrative staff was trained, first, to introducethem to the system and, then to allow them to exploit all itspossibilities. Upstream from such training programs workinggroups were formed and, over several weeks, they comparedwork processes in order to choose and improve those thatwere in the final selection. The leaders and members of theworking groups became facilitators in the in-house programsorganized to train Group employees.

During this period of integration, a special effort was made in internal communication in order to provide the staff withregular information and a new dynamic was created in the Group. The publication of a newsletter on the merger,the introduction of an intranet tool “mon.gecina.fr”, and the meetings held to inform management helped to create a Group spirit.

The prime objective in 2003 was the successfulintegration of the GECINA and SIMCO teams in a spirit of cooperation and mutual respect.

Integration facilitated

3-5, boulevard de la Madeleine - 75001 Paris

21

Sustainable development

Principles of actionThe principles of action that motivate Group employeesin the exercise of their jobs are based on respect for legalrequirements, the environment, health and safety. Valuesof mutual respect, fairness, solidarity and professionalismbolster GECINA’s integration of sustainable developmentat the heart of its redeployment strategy. Listening toclients, transparency vis-à-vis shareholders, dialogue withGECINA’s partners and suppliers are part of daily life forthe men and women who work for the GECINA Group.

Concrete measures Many measures are applied on a day-to-day basis. Thecompetitiveness of real estate proposals from the point ofview of environmental protection is a constant priority forthe Group. In 2003, GECINA invested 10.5 million eurosfor the maintenance and renovation of apartments andoffices (painting, plumbing, flooring, etc.), while capitalexpenditures for major restructuring and improvements in apartments and offices totaled 59.9 million euros.Within the framework of its sustainable development,GECINA pays special attention to issues of risk andsustainable development. A comprehensive analysis ofground pollution risks is a required stage in GECINA’sinvestigation of new investment possibilities. For thisreason, high-yield projects have been turned downbecause the buildings had been constructed on pollutedland and the economic, environmental or healthconsequences for the local population were unknown.The technical equipment and raw materials GECINA usesin its development projects are chosen for theirenvironmental properties and their durability. GECINAalso complies with current regulations that are specific to the real estate market (asbestos, lead in paint,Legionnaire’s disease, fire safety, elevators, etc.)1. A riskmanagement team is in charge of monitoring, controllingand advising on any possible environmental risks in orderto anticipate any incidents.

Specific services GECINA clients have access to a 24-hour emergencyassistance service since 2002. A telephone contact isprovided and skilled Company employees are on duty tofield the calls. The goal is to reduce the materialconsequences of any delayed response to an incidentthat might have negative consequences for GECINA orits clients. For maximum efficiency, a crisis cell has alsobeen set up with a pluridisciplinary team to deal withmajor events The unit combines skills in the field of IT,technical questions, legal requirements, communication,human resources, etc.

A committee for quality and sustainabledevelopment A committee for quality and sustainable developmentcomprised of four Board members was formed at thebeginning of 2003 to promote and pilot all initiatives insupport of quality and sustainable development. In 2003,it focused on risk management prevention in liaison withthe risk manager. In 2004, it will study the introductionof standards against which to measure quality and clientsatisfaction.

GECINA’s commitment is illustrated by a whole series of actions in response to the Group’s increased awareness of its environmental, social and society-based responsibilities.The creation of an autonomous Risk Management departmentin 2001 and, recently, of a committee of Directors dedicated to quality and sustainable development incorporate this objective at a practical level in the Group’s businesses.

1 GECINA’s industrial and environmental risks and its prevention policy are presented inthe management report.

A commitment that involves everyone

Commercial real estate

53%

79%

60%

of the Group’s rental income in 2003 was fromcommercial properties.

of commercialproperties wereconcentrated in primeParis business districtsas of December 31,2003.

of the Group’s rentalincome in 2003 wasfrom properties with a surface area of morethan 5,000 sq.m.

In the last two years, GECINAhas put together a portfolio of commercial propertiesthat is a source of growth and the creation of value in the medium term. Its highlyselective position enabled the Group to move forward in an uncertain economic environment in 2003.

22

23

An active and selective development policy

10-12, place Vendôme75001 Paris

24

3, place de l’Opéra75002 Paris

2003, a second year of rental marketadjustments in Ile-de-FranceWith weak growth in GDP, the year 2003 representedthe third worst economic performance since the SecondWorld War. The job market remained depressed.Unemployment continued to rise, reaching an averageestimated at 9.5% in 2003, versus 9.0% in 2002.

In such an economic environment, the market for officereal estate in Ile-de-France showed rather goodresistance. The fourth quarter of 2003, which wasparticularly active in terms of both supply and demand,offset the first three quarters, which were disappointing,making the year’s results better than expected.

In 2003, the supply increased, but at a slower pace thanin 2001 and 2002. As of December 31, 2003, CBRE-Bourdais estimated at 2,934,400 sq.m. the surfacearea immediately available in Ile-de-France, representing a moderate increase of 12%. This growth was nothomogeneous. Certain sectors recorded significantincreases of approximately 48% (close suburbs north,east and south of Paris) and 21% in Paris in a year,whereas other zones reported more contrasted trends: -2% at La Défense and -5% in the outlying suburbs1.

In Paris, the vacancy rate was the lowest in Ile-de-Franceat 5%. La Défense reported a vacancy rate of 8%.

Altogether, at 6.5%, this indicator for Ile-de-Francepractically stabilized after several years of rapid growth2.

With 1,708,200 sq.m. in placement (510,000 sq.m. inthe last quarter alone), demand was satisfied (space rentedor acquired by clients in Ile-de-France) at a level similar to that reported in 2001, and up 11.5% from 2002. Of this total, sales1 to occupants representedapproximately 300,000 sq.m. Transactions of more than5,000 sq.m. drove the market, showing strong growthcompared with 2002 – 810,000 sq.m. were placed in this segment, versus 630,000 sq.m. in 2002. Overall, 71 transactions of more than 5,000 sq.m. were recorded in 2003, compared with 47 in 2002. The strongestgrowth was reported in the 5,000 sq.m. to 10,000 sq.m.segment, with 41 transactions in 2003, up from 24 in 20022.

The choice of a site for corporate relocation is oftendecided on the basis of trends in rental costs. Despite relative stabilization in the third quarter, rentalscontinued their readjustment in 2003. The weightedaverage of rentals in Ile-de-France for new, restructuredor renovated buildings stood at 310 euros sq.m./year(excluding VAT and operating costs), down 9% in nominal value in a year1.

The most significant market corrections were observed in business districts in and around Paris. The average

3-5, boulevard de la Madeleine 75001 Paris

1 Source: CB Richard Ellis Bourdais.2 Source: Catella Property Group.

25

78-80, rue de la Villette69003 Lyon

value of transactions of more than 5,000 sq.m. amounted to 420 euros sq.m./year (excluding VAT and operating costs) in the business district west of Paris and 603 euros sq.m./year(excluding VAT and operating costs) in Paris1. Prime real estatefollowed a similar trend: - 5% to -7% in central Paris and - 7% to - 10% at La Défense2. This decline wasaccompanied by enhanced commercial advantages for renters,including rental franchises, contribution to works, progressiverent structures, etc. Conversely, new renters agreed to contractlong leases (6 to 9 years or more) for large surface areas.

An active market for offices in Lyons3

The year 2003 was marked by a sustained volume of transactions in Lyons, confirming this market’s reputation as a good investment. Commercial rental transactions totaled172,600 sq.m., up 8.5% from 2002 and at a higher level thanthe average of the last ten years. Space available in less than a year increased by 34% in 2003 to 268,500 sq.m. at the end of the year. This figure included 91,800 sq.m. of new offeringsand 176,700 sq.m. of previously occupied properties, for atotal vacancy rate of 5.9%. The increase in supply in 2003ensured stability in rental fees, which stood at 180 euros sq.m./year (excluding VAT and operating costs) for new constructionsand 121 euros sq.m./year (excluding VAT and operating costs)for previously occupied properties at the end of the year.

Prime office yields in Europe in 2003

Paris (central business district) 5.90%London West End 5.75%Frankfurt 4.80%Madrid 6.00%Source: CB Richard Ellis Bourdais.

Investment in offices was down slightly in 2003, with a total of 132,500 sq.m. versus 144,500 sq.m. in 2002. This contraction in investment was the resultof a reduction in office space supply that led to a general decrease in profitability rates. The continued major presence of German investmentfunds ensured support for market values in 2003.

Retail leases, a lackluster marketThe decline in consumer spending affected the development plans of major distributors, who focused on opening stores of less than 500 sq.m. in recognized commercial sectors. Luxury brands were particularly active in downtownareas, while retail parks in the suburbs attracted well-known brand names.

Rental income was down slightly with contrastingtrends. Rents for well-located stores of less than 500 sq.m. remained stable, or even rose slightly,whereas rents declined for retail premises between500 sq.m. and 2,500 sq.m. or in less desirablelocations.

1 Source: Catella Property Group.2 Source: CB Richard Ellis Bourdais.3 Source: Atis Real Auguste-Thouard.

Prime rentals in Europe in 2003 (sq.m./year - excluding VAT and operating costs)

London West End 850 eurosParis (central business district) 675 eurosFrankfurt (central business district) 420 eurosMadrid 312 eurosSource: CB Richard Ellis Bourdais.

>>

>>

26

47, rue Louis-Blanc92215 La Défense

A dynamic investment market

Despite the adjustment in the rental market, the Frenchmarket confirmed in 2003 that it continues to exert an attraction. Comparisons with other Europeanmarkets are to its advantage; rent levels have growthpotential in spite of their current decline; and themarket is fluid. 9.5 billion euros were invested in corporate real estate in France in 2003, the samevolume as in 2002 and 2001 (excluding the FranceTélécom portfolio)1. In an uncertain economicenvironment, investors preferred traditional products,which involve fewer risks. So 80% of investmentsconcerned offices, the most liquid asset, with 92% inIle-de-France, and 75% represented acquisitions thatwere already rented. Commercial space attracted 10%of the total invested in 2003, while warehousesaccounted for the remainder, i.e. 10%1.

Among the investors, German funds remained the mostactive market players, with 37% of investments in 2003.Their acquisitions were primarily composed of new or restructured buildings in good locations with securedrents. With 30% of total acquisitions, French investors, in particular real estate firms and insurance and life-insurance companies, remained active. North American and British investors accounted for 9%of total investments respectively. Lastly, in 2003, MiddleEastern funds returned to France, to represent 7.5% of acquisitions, and 65% of sales were negotiated

with French investors – occupants, developers, real estatefirms and insurance companies.

Among the foreign sellers, North Americans continued to glean capital gains on assets that have risen in value,representing 25% of total sales. The British, Dutch and Germans sold little in 20031.

Ile-de-France drained 78% of the amounts invested.Outside of Paris, it was the Lyons region that remainedthe most attractive with real estate resources that meetinternational standards and a rental market for previouslyoccupied properties. In 2003, this region accounted for 22% of French investments1.

Real estate continued to attract investment in 2003.Despite the rise in interest rates at the end of 2003, and a slight decrease in the immediate yield on officerentals of approximately 25 basis points, the spreadremained at 140 basis points to the advantage of realestate yields at the end of 2003.

A diversified market with many players

Corporate real estate assets are owned by many leasingoperators, including listed real estate firms, insurancecompanies, SCPI investment vehicles and a growingnumber of foreign operators. With a total of 45 million sq.m., Ile-de-France is considered to beEurope’s leading office market, ahead of London,

19, rue de la Villette 69003 Lyon

1 Source: CB Richard Ellis Bourdais.2 Source: Catella Property Group.

27

9-15, avenue Matignon75008 Paris

and also one of the most diversified2. Office space in Ile-de-France basically involves three main centralmarkets. The central Paris business district with 8.3 million sq.m. accounts for 18.4% of the total Ile-de-France market; the western suburbs of Paris with6.4 million sq.m. represents 14%; and the secondaryoffice areas of Paris (Front de Seine, Montparnasse, Garede Lyons/Bercy/Paris Rive Gauche) add 1.5 million sq.m. Atthe same time, other areas are emerging like thenorthwest suburbs of Paris (Clichy, Saint-Ouen and Saint-Denis), and in general, all the municipalities in the immediately surrounding suburbs, such as Montreuil,Charenton and Montrouge. Further out in the suburbs,there are micro markets at Saint-Quentin, Marne-la-Vallée,Vélizy-Villacoublay, etc.)1.

In 2003, Lyons confirmed its position as the second largestFrench office market after Ile-de-France. Rental office spacewas estimated at 4 million sq.m. at the end of 20032.

At the end of 2003, the GECINA Group owned 929,621 sq.m. of offices and stores, 803,937 sq.m. of which were in Paris and its suburbs, a figure thatrepresents less than 2% of office space (excluding stores) in Ile-de-France.

Although it is one of the largest listed French real estatefirms, GECINA does not have a dominant position in the commercial real estate market. At the same time,the Group’s office rental transactions accounted forapproximately 2% of the demand satisfied in Ile-de-France.

A quality portfolio

As of December 31, 2003, the GECINA Group’sportfolio of commercial assets was valued at 3.87 billion euros, with 3.78 billion euros located inParis and its suburbs. The value of commercial assets in the first, second, eighth, sixteenth and seventeentharrondissements, represented 51.9% of totalcommercial assets, while the value of assets in the western suburbs (Boulogne, Levallois, Issy-les-Moulineaux, etc.) accounted for 26.8%.

These assets form a varied offering in terms of both typesof office space (Haussmann-style, recent constructions,stores on the ground floor, etc.) and rental surface area(from small to large). This diversity makes it possible to satisfy a wide range of clients and provides a buffer in the event of an economic downturn. GECINA’s corporate clients work in many sectors, thereby reducingthe Group’s rental risks. In 2003, the ten largest rentersaccounted for only 14.0% of the Group’s rental income.With an annual rent of 13.3 million euros, the largestuser represented 2.7% of the Group’s rental income in 2003. The fifth and the tenth largest accounted for 6.0 million euros and 3.3 million euros, respectively,representing 1.2% and 0.7% of the Group’s rental income in 2003. At the same time, rents for the ten largest commercial properties contributed 15.7% of GECINA’s rental income in 2003.

Rental income by business sector in 2003

40% Services

4% Real estate

3% Insurance

3% Media, TV

6% Other

8% Banking

3% Telecommunications

4% Luxury - retail

13% Industry

13% Administration

3% Information technology

1 Source: Catella Property Group.2 Source: Atis Real Auguste-Thouard. .

28

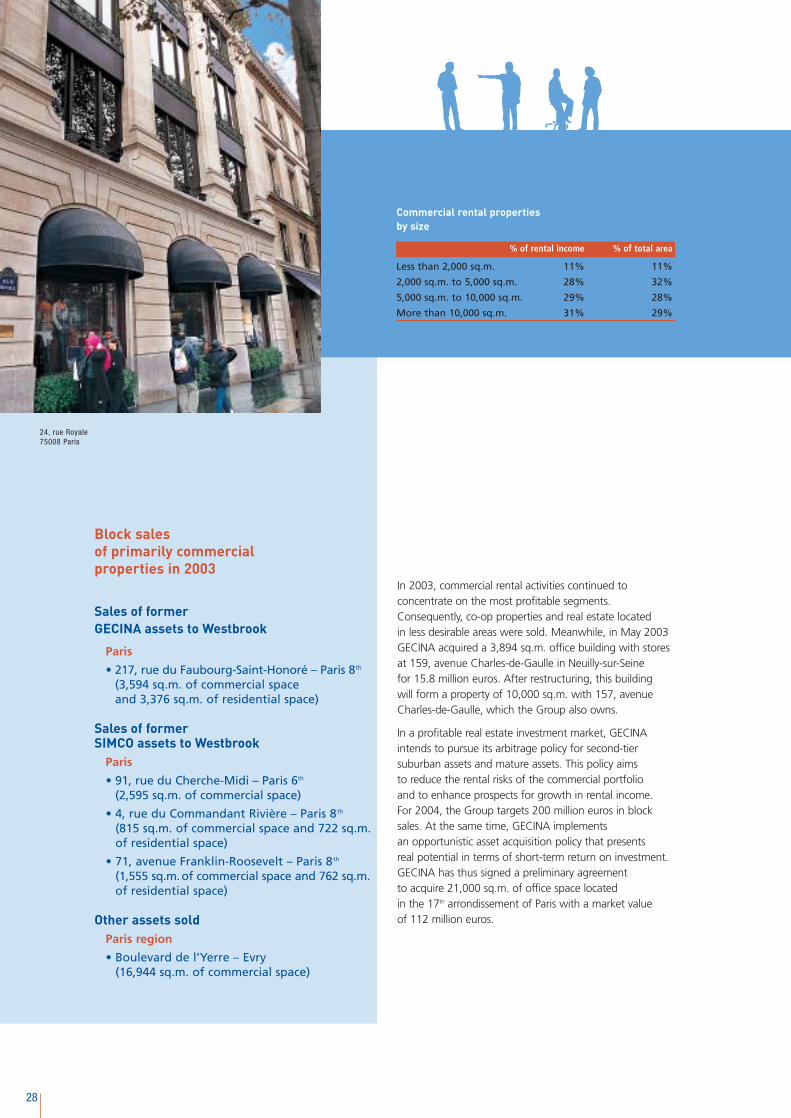

In 2003, commercial rental activities continued toconcentrate on the most profitable segments.Consequently, co-op properties and real estate located in less desirable areas were sold. Meanwhile, in May 2003GECINA acquired a 3,894 sq.m. office building with stores at 159, avenue Charles-de-Gaulle in Neuilly-sur-Seine for 15.8 million euros. After restructuring, this building will form a property of 10,000 sq.m. with 157, avenueCharles-de-Gaulle, which the Group also owns.

In a profitable real estate investment market, GECINAintends to pursue its arbitrage policy for second-tiersuburban assets and mature assets. This policy aims to reduce the rental risks of the commercial portfolio and to enhance prospects for growth in rental income. For 2004, the Group targets 200 million euros in blocksales. At the same time, GECINA implements an opportunistic asset acquisition policy that presents real potential in terms of short-term return on investment.GECINA has thus signed a preliminary agreement to acquire 21,000 sq.m. of office space located in the 17th arrondissement of Paris with a market value of 112 million euros.

Block sales of primarily commercial properties in 2003

Sales of former GECINA assets to Westbrook

Paris

• 217, rue du Faubourg-Saint-Honoré – Paris 8th

(3,594 sq.m. of commercial space and 3,376 sq.m. of residential space)

Sales of former SIMCO assets to Westbrook

Paris

• 91, rue du Cherche-Midi – Paris 6th

(2,595 sq.m. of commercial space)

• 4, rue du Commandant Rivière – Paris 8th

(815 sq.m. of commercial space and 722 sq.m. of residential space)

• 71, avenue Franklin-Roosevelt – Paris 8th

(1,555 sq.m.of commercial space and 762 sq.m. of residential space)

Other assets sold Paris region

• Boulevard de l’Yerre – Evry (16,944 sq.m. of commercial space)

% of rental income % of total area

Less than 2,000 sq.m. 11% 11%

2,000 sq.m. to 5,000 sq.m. 28% 32%

5,000 sq.m. to 10,000 sq.m. 29% 28%

More than 10,000 sq.m. 31% 29%

Commercial rental properties by size

24, rue Royale75008 Paris

29

8, avenue Delcassé 75008 Paris

4, allée Ferrand 92200 Neuilly-sur-Seine

Launch of development operationsIn 2003, GECINA developed a strategy to increase the value of its commercial portfolio, thereby meeting the criterion of a minimal gross yield of 7.5%. Mainly based on major restructuring operations in Lyonsand Paris, this strategy aims to maximize the creation of value in the Group in terms of both profitability and net asset value.

In Lyons, work was completed on the Dauphiné Part-Dieuproject, which was begun in the autumn of 2002. The delivery of this 13,000 sq.m. office building on landowned by GECINA took place on February 3, 2004, ahead of the scheduled date. The investment totaled 28.0 million euros.

In Paris, the Volney-Capucines office complex – 10,000 sq.m.of office space near the Opera and the place Vendôme – is being developed to become the Group’s future headquarters. Delivery is scheduled for the fourth quarterof 2004. This operation on a building acquired in July2002 represents an investment of approximately 25.5 million euros in addition to the acquisition price of 48.0 million euros.

In January 2003, GECINA launched a project to restructureand give new life to the Beaugrenellle mall in the 15th

arrondissement of Paris through a joint venture (50% - 50%) with a major commercial real estate operator, Apsys (see page 31).

Lastly, GECINA plans to build 8,281 sq.m. of offices and 2,190 sq.m. of stores at 122, avenue du GénéralLeclerc in Boulogne. Very close to major development projects in the western suburbs (restructuring of the Pontde Sèvres intersection, development of the site of the former Renault automobile plant), the operation wouldincrease the Group’s real estate holdings at this address to almost 20,000 sq.m. of offices and stores. Designed by the architectural firm of ARTE Charpentier et Associés, the project was granted a building permit in February2004. Delivery is scheduled for 2006. The preliminaryinvestment is estimated at 34.0 million euros for an estimated gross yield of more than 8.5%.

All of the Group’s development projects are major relays of growth from 2004 to 2007, representing a total of 90,000 sq.m. and a potential of additional rental income estimated at 27.0 million euros.

30

Good resistance of rental activitiesIn 2003, the GECINA Group’s rental income from commercial properties totaled 259.8 million euros, up 5.0% from GECINA-SIMCO’s 2002 pro forma commercial rental income. For the first time in 2003,commercial rental transactions accounted for more than50% of the Group’s rental income. Excluding propertiesfor sale and on a constant basis, rent revaluation stood at 3.1%.

Despite adjustments to market rental prices, the Group’sre-letting rates increased by 18.2% compared with thelevels in the previous leases. Re-let properties represented36,720 sq.m. in 2003. For example, 7,899 sq.m. at 14, boulevard Général Leclerc in Neuilly-sur-Seine were re-letfor 457.0 euros sq.m./year (excluding VAT and operatingcosts), representing an increase of 21.5% compared withthe previous rent. The Group also rented 2,950 sq.m. at55, avenue de Colmar in Rueil-Malmaison for 250.0 eurossq.m./year (excluding VAT and operating costs),representing an increase of 10.1%. GECINA’s formerheadquarters at 2ter, boulevard Saint-Martin, Paris 10th,rapidly found a renter for their 6,300 sq.m. at 354.0 eurossq.m./year (excluding VAT and operating costs).

In addition, all of the 2,164 sq.m. at 12, rue de Torricelli,Paris 17th, were rented for 457.0 euros sq.m./year (excluding VAT and operating costs). In a similar fashion,all of the 1,500 sq.m. in the restructured building at 9, avenue de Paris in Vincennes was rented for anaverage of 290.5 euros sq.m./year (excluding VAT and operating costs).

Following the market, vacancy rates increased slightly in 2003. The financial vacancy rate stood at 5.1% in December 2003, compared with 3.7% in December2002. The physical vacancy rate was 3.8% in December2003, while the rate for Ile-de-France leveled off at 6.5%.

In 2003, GECINA’s reversionary potential rental income,the gap between market prices and rents in the leases,declined owing to new portfolio rentals and adjustmentsin the rental market. This market was, nevertheless,estimated at 16.7 million euros as of December 31,2003, over the next four years provided that the currentlevel of market rents is maintained.

(%)

12.95 12.96 12.97 12.98 12.99 12.00 12.01 12.02 12.03

90.192.4

93.395.7 96.4

98.8 98.896.3 94.9

9, avenue de Paris94300 Vincennes

Financial occupancy rate of commercial properties

31

23-29, rue de Châteaudun75009 Paris

This potential will be liberated as leases expire, are broken or are renewed. Leases expiring in 2004represent 48,266 sq.m. with an average rent of 234.0 euros sq.m./year (excluding VAT and operatingcosts), versus a market rent of 259.0 euros sq.m./year(excluding VAT and operating costs). This estimate wasalso conducted for 2005, 2006 and 2007 on a lease to lease basis. Leases will expire in the next three yearsfor 82,435 sq.m., 80,655 sq.m. and 102,855 sq.m.,respectively, with an average rental price of 324.0 euros, 255.0 euros and 234.0 euros sq.m./year (excluding VAT and operating costs), compared with a market rental price of 374.0 euros, 305.0 euros and301.0 euros sq.m./year (excluding VAT and operatingcosts).

Beaugrenelle mall: a landmark project

After consulting the main French commercial real estate operators, GECINA joined forces with Asys, Eurisand Francarep in January 2003 to restructure and givenew life to the Beaugrenelle mall. The 50%-50% joint venture was formed through the sale of 50% of the shares of SCI Beaugrenelle, which owns the mall.The project involves the complete architectural and technical renovation of the site with an extension to 40,000 sq.m. An architectural firm was selected after competing projects were submitted in April 2003.The next step is to apply to the competent localauthorities for the building permit and the other requiredauthorizations. Completion is scheduled for 2007. The investment will total 115 million euros and is designed to meet the objective of a gross yield of more than 7.5%.

1995 1996 1997 1998 1999 2000 2001 2002 2003

-8.5n.s

-1.3

2.0

6.5 5.8

8.0

5.3

3.1

(%)

Growth in commercial rental income on a constantbasis and excluding properties for sale

32

Istarrdt

29,647 sq.m.

IIndarrdt

46,589 sq.m. IIIrdarrdt

2,464 sq.m.

IVtharrdt

603 sq.m.

Vtharrdt

158 sq.m.

VItharrdt

14,350 sq.m.

VIItharrdt

9,147 sq.m.

VIIItharrdt

128,933 sq.m.

IXtharrdt

27,852 sq.m. Xtharrdt

9,682 sq.m.

XItharrdt

2,549 sq.m.

XIItharrdt

20,836 sq.m.

XIIItharrdt

3,576 sq.m.XIVth

arrdt

11,694 sq.m.

XVtharrdt

53,613 sq.m.

XVItharrdt

18,647 sq.m.

XVIItharrdt

33,360 sq.m.

XVIIItharrdt

6,448 sq.m.

XIXtharrdt

7,750 sq.m.

XXtharrdt

1,041 sq.m.

PARIS428,940 sq.m.

PARIS REGION313,916 sq.m.

LYONS86,005 sq.m.

OTHER4,072 sq.m.

Commercial properties

Commercial properties comprising 929,621 sq.m. of offices and

stores, 832,933 sq.m. of which were in operation as of December 31, 2003.

Excellent locations with 285,028 sq.m.

in the first, second, eighth, ninth, sixteenth and seventeenth

arrondissements, and 242,596 sq.m. in the western suburbs

(Boulogne, Courbevoie, Levallois, etc.).

(in operation as of December 31, 2003)

33

%of rental income

% of revalued block value 1

% of rental income

% of revalued block value 1

1 On the basis of block valuationappraisals, net selling prices, of real estate assets.

2.2 %

ParisParis regionLyons

After 19751960-1975Haussmann-styleMiscellaneous

1.5 % 1.0 %2.0 %

69.2 % 63.5 %63.3 %66.4 %29.3 %31.4 %

19.2 %

15.5 %

20.0 %

15.5 %

Primarily commercial properties in operation

Paris 1st

7, place de Valois - 11, rue des Bons-Enfants 1800 0 0 1,028 1,028 GECITER55, boulevard de Sébastopol 1880 8 577 763 1,340 GECINA10/12, place Vendôme 1750 0 0 8,823 8,823 SIF16, rue Duphot 1988 0 0 1,405 1,405 GECINA8/10, rue Villedo 1970 0 0 1,366 1,366 GECITER1, boulevard de la Madeleine 1996 6 548 1,828 2,376 SIF3/5, boulevard de la Madeleine 2002 0 0 13,516 13,516 SIF

Paris 2nd

35, avenue de l’Opéra - 6, rue Danielle-Casanova 1878 10 545 1,739 2,284 GECITER64, rue Tiquetonne - 48, rue Montmartre 1850 52 4,484 5,719 10,203 GECINA26/28, rue Danielle-Casanova 1800 3 252 1,130 1,382 GECITER36, rue des Jeûneurs 1869 11 630 1,205 1,835 GECITER5, rue de Marivaux 1790 0 0 1,420 1,420 GECITER3, rue du Quatre-Septembre 1870 6 343 1,094 1,437 GECINA10, rue du Quatre-Septembre79, rue de Richelieu - 1, rue Ménars 1870 1 105 2,555 2,660 GECITER120, rue Réaumur 1880 0 0 1,198 1,198 GECITER6 bis, rue Bachaumont 1880 13 1,000 1,092 2,092 GECINA4, rue de la Bourse 1750 10 823 3,952 4,775 SAS FEYDEAU-

BOURSE38, rue des Jeûneurs 1870 5 307 3,617 3,924 SCI du 38 rue

des JEUNEURS37, boulevard des Capucines 1880 0 0 584 584 GECINA3, place de l’Opéra 1870 0 0 4,591 4,591 SCI TERNES-

OPERA31/35, boulevard des Capucines 1992 0 0 5,753 5,753 SCI CAPUCINES5, boulevard Montmartre 1995 17 1,342 6,135 7,477 SCI du 5 bld

MONTMARTRE29/31, rue Saint-Augustin 1996 6 445 4,805 5,250 SCI SAINT-

AUGUSTIN

75

Com

mer

cial

area

(sq

.m.)

Tota

lar

ea (

sq.m

.)

Com

pany

Res

iden

tial

area

(sq

.m.)

Num

ber

of a

part

men

ts

Year

Add

ress

or

buil

ding

nam

e

Dep

artm

ent

Cit

y

Geographic breakdown of commercial properties in operation

as of December 31, 2003

Breakdown of commercial properties in operation by type

as of December 31, 2003

34

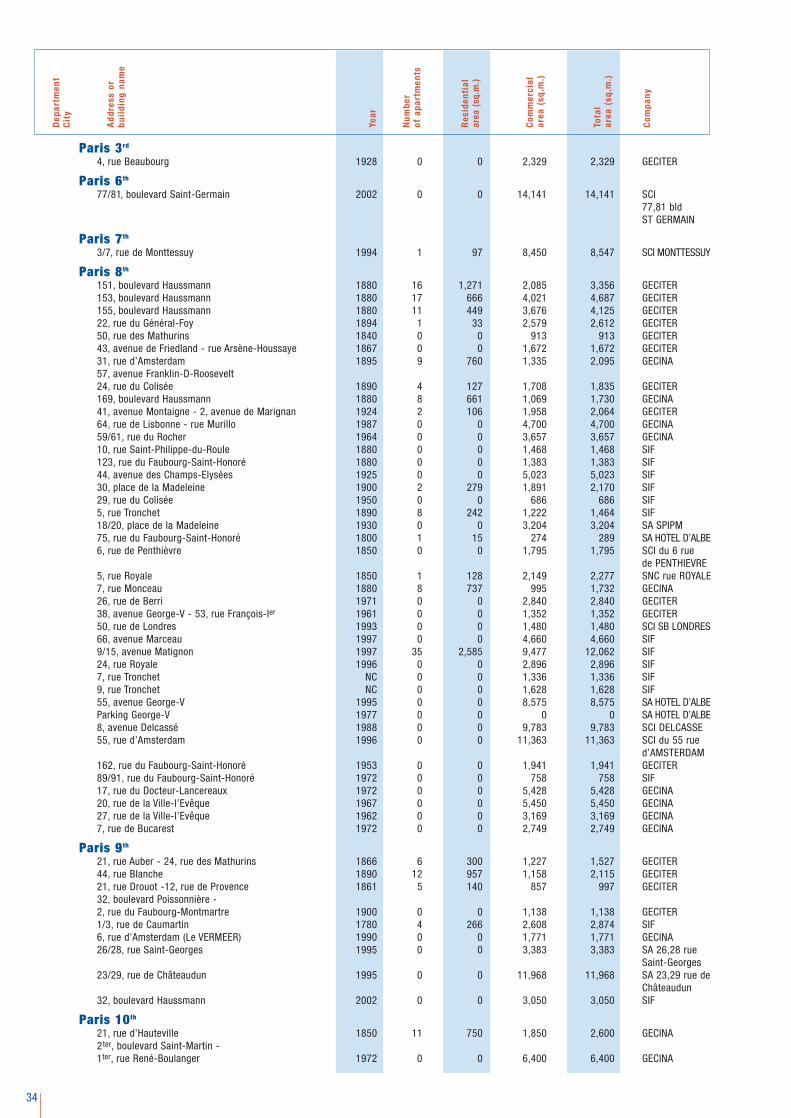

Paris 3rd

4, rue Beaubourg 1928 0 0 2,329 2,329 GECITER

Paris 6th

77/81, boulevard Saint-Germain 2002 0 0 14,141 14,141 SCI 77,81 bldST GERMAIN

Paris 7th

3/7, rue de Monttessuy 1994 1 97 8,450 8,547 SCI MONTTESSUY

Paris 8th

151, boulevard Haussmann 1880 16 1,271 2,085 3,356 GECITER153, boulevard Haussmann 1880 17 666 4,021 4,687 GECITER155, boulevard Haussmann 1880 11 449 3,676 4,125 GECITER22, rue du Général-Foy 1894 1 33 2,579 2,612 GECITER50, rue des Mathurins 1840 0 0 913 913 GECITER43, avenue de Friedland - rue Arsène-Houssaye 1867 0 0 1,672 1,672 GECITER31, rue d’Amsterdam 1895 9 760 1,335 2,095 GECINA57, avenue Franklin-D-Roosevelt 24, rue du Colisée 1890 4 127 1,708 1,835 GECITER169, boulevard Haussmann 1880 8 661 1,069 1,730 GECINA41, avenue Montaigne - 2, avenue de Marignan 1924 2 106 1,958 2,064 GECITER64, rue de Lisbonne - rue Murillo 1987 0 0 4,700 4,700 GECINA59/61, rue du Rocher 1964 0 0 3,657 3,657 GECINA10, rue Saint-Philippe-du-Roule 1880 0 0 1,468 1,468 SIF123, rue du Faubourg-Saint-Honoré 1880 0 0 1,383 1,383 SIF44, avenue des Champs-Elysées 1925 0 0 5,023 5,023 SIF30, place de la Madeleine 1900 2 279 1,891 2,170 SIF29, rue du Colisée 1950 0 0 686 686 SIF5, rue Tronchet 1890 8 242 1,222 1,464 SIF18/20, place de la Madeleine 1930 0 0 3,204 3,204 SA SPIPM75, rue du Faubourg-Saint-Honoré 1800 1 15 274 289 SA HOTEL D’ALBE6, rue de Penthièvre 1850 0 0 1,795 1,795 SCI du 6 rue

de PENTHIEVRE5, rue Royale 1850 1 128 2,149 2,277 SNC rue ROYALE7, rue Monceau 1880 8 737 995 1,732 GECINA26, rue de Berri 1971 0 0 2,840 2,840 GECITER38, avenue George-V - 53, rue François-Ier 1961 0 0 1,352 1,352 GECITER50, rue de Londres 1993 0 0 1,480 1,480 SCI SB LONDRES66, avenue Marceau 1997 0 0 4,660 4,660 SIF9/15, avenue Matignon 1997 35 2,585 9,477 12,062 SIF24, rue Royale 1996 0 0 2,896 2,896 SIF7, rue Tronchet NC 0 0 1,336 1,336 SIF9, rue Tronchet NC 0 0 1,628 1,628 SIF55, avenue George-V 1995 0 0 8,575 8,575 SA HOTEL D’ALBEParking George-V 1977 0 0 0 0 SA HOTEL D’ALBE8, avenue Delcassé 1988 0 0 9,783 9,783 SCI DELCASSE55, rue d’Amsterdam 1996 0 0 11,363 11,363 SCI du 55 rue

d’AMSTERDAM162, rue du Faubourg-Saint-Honoré 1953 0 0 1,941 1,941 GECITER89/91, rue du Faubourg-Saint-Honoré 1972 0 0 758 758 SIF17, rue du Docteur-Lancereaux 1972 0 0 5,428 5,428 GECINA20, rue de la Ville-l’Evêque 1967 0 0 5,450 5,450 GECINA27, rue de la Ville-l’Evêque 1962 0 0 3,169 3,169 GECINA7, rue de Bucarest 1972 0 0 2,749 2,749 GECINA

Paris 9th

21, rue Auber - 24, rue des Mathurins 1866 6 300 1,227 1,527 GECITER44, rue Blanche 1890 12 957 1,158 2,115 GECITER21, rue Drouot -12, rue de Provence 1861 5 140 857 997 GECITER32, boulevard Poissonnière - 2, rue du Faubourg-Montmartre 1900 0 0 1,138 1,138 GECITER1/3, rue de Caumartin 1780 4 266 2,608 2,874 SIF6, rue d’Amsterdam (Le VERMEER) 1990 0 0 1,771 1,771 GECINA26/28, rue Saint-Georges 1995 0 0 3,383 3,383 SA 26,28 rue

Saint-Georges23/29, rue de Châteaudun 1995 0 0 11,968 11,968 SA 23,29 rue de

Châteaudun32, boulevard Haussmann 2002 0 0 3,050 3,050 SIF

Paris 10th

21, rue d’Hauteville 1850 11 750 1,850 2,600 GECINA2ter, boulevard Saint-Martin - 1ter, rue René-Boulanger 1972 0 0 6,400 6,400 GECINA

Com

mer

cial

area

(sq

.m.)

Tota

lar

ea (

sq.m

.)

Com

pany

Res

iden

tial

area

(sq

.m.)

Num

ber

of a

part

men

ts

Year

Add

ress

or

buil

ding

nam

e

Dep

artm

ent

Cit

y

35

Paris 12th

193, rue de Bercy 1972 0 0 15,899 15,899 GECINA58/62, quai de la Rapée (parking) 1990 0 0 0 0 S.P.L.

Paris 14th

11, boulevard Brune 1973 0 0 2,781 2,781 GECINA37/39, rue Dareau 1988 0 0 4,857 4,857 GECINA69, boulevard Brune - 10/18, rue des Mariniers 1970 0 0 2,221 2,221 GECINA

Paris 15th

33, avenue du Maine (Tour MAINE-MONTPARNASSE -50th floor) 1991 0 0 1,822 1,822 GECINA7/11, place des Cinq-Martyrs-du-Lycée-Buffon 1992 0 0 8,355 8,355 SCI SB NORD-PONT28/28 bis, rue du Docteur-Finlay - 5, rue Sextius-Michel 1960 0 0 3,444 3,444 GECITER31, quai de Grenelle (MERCURE) 1973 0 0 8,250 8,250 GECINA34, rue de la Fédération 1973 0 0 6,579 6,579 GECINA

Paris 16th

43, avenue Marceau - 14, rue Bassano 1928 0 0 1,314 1,314 GECITER100, avenue Paul-Doumer 1920 0 0 294 294 GECINA58/60, avenue Kléber 1992 0 0 4,789 4,789 SA SADIA28, rue Dumont-d’Urville 1880 0 0 1,382 1,382 GECINA17, rue Galilée 1960 0 0 680 680 GECITER24, rue Erlanger 1965 0 0 5,956 5,956 SCI du 24 rue

ERLANGER

Paris 17th

63, avenue de Villiers 1880 8 406 2,912 3,318 GECITER12/12 bis, rue Torricelli 1800 0 0 2,620 2,620 GECITER45, avenue de Clichy - 2/4, rue Hélène 1991 0 0 3,900 3,900 GECINA32/34, rue Guersant 1992 0 0 13,175 13,175 SP216, rue Médéric 1970 0 0 1,338 1,338 GECINA251, boulevard Pereire 1973 0 0 2,792 2,792 GECINA

Paris 18th

88/92, boulevard Ney 1972 0 0 6,260 6,260 GECINA

Paris 19th

43 bis/45, rue d’Hautpoul 1977 12 786 2,988 3,774 GECINA96/100, rue Petit 1977 0 0 4,185 4,185 SA PARIGEST

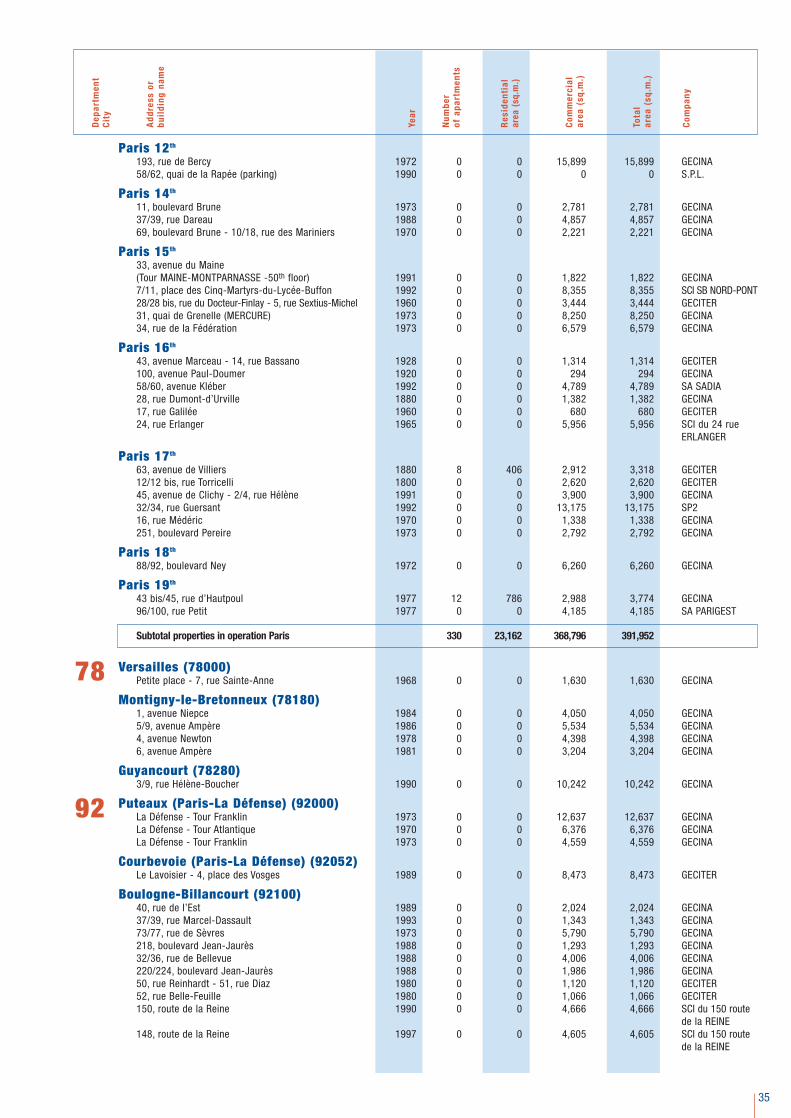

Subtotal properties in operation Paris 330 23,162 368,796 391,952

Versailles (78000)Petite place - 7, rue Sainte-Anne 1968 0 0 1,630 1,630 GECINA

Montigny-le-Bretonneux (78180)1, avenue Niepce 1984 0 0 4,050 4,050 GECINA5/9, avenue Ampère 1986 0 0 5,534 5,534 GECINA4, avenue Newton 1978 0 0 4,398 4,398 GECINA6, avenue Ampère 1981 0 0 3,204 3,204 GECINA

Guyancourt (78280)3/9, rue Hélène-Boucher 1990 0 0 10,242 10,242 GECINA

Puteaux (Paris-La Défense) (92000) La Défense - Tour Franklin 1973 0 0 12,637 12,637 GECINALa Défense - Tour Atlantique 1970 0 0 6,376 6,376 GECINALa Défense - Tour Franklin 1973 0 0 4,559 4,559 GECINA

Courbevoie (Paris-La Défense) (92052)Le Lavoisier - 4, place des Vosges 1989 0 0 8,473 8,473 GECITER

Boulogne-Billancourt (92100)40, rue de l’Est 1989 0 0 2,024 2,024 GECINA37/39, rue Marcel-Dassault 1993 0 0 1,343 1,343 GECINA73/77, rue de Sèvres 1973 0 0 5,790 5,790 GECINA218, boulevard Jean-Jaurès 1988 0 0 1,293 1,293 GECINA32/36, rue de Bellevue 1988 0 0 4,006 4,006 GECINA220/224, boulevard Jean-Jaurès 1988 0 0 1,986 1,986 GECINA50, rue Reinhardt - 51, rue Diaz 1980 0 0 1,120 1,120 GECITER52, rue Belle-Feuille 1980 0 0 1,066 1,066 GECITER150, route de la Reine 1990 0 0 4,666 4,666 SCI du 150 route

de la REINE148, route de la Reine 1997 0 0 4,605 4,605 SCI du 150 route

de la REINE

78

92

Com

mer

cial

area

(sq

.m.)

Tota

lar

ea (

sq.m

.)

Com

pany

Res

iden

tial

area

(sq

.m.)

Num

ber

of a

part

men

ts

Year

Add

ress

or

buil

ding

nam

e

Dep

artm

ent

Cit

y

36

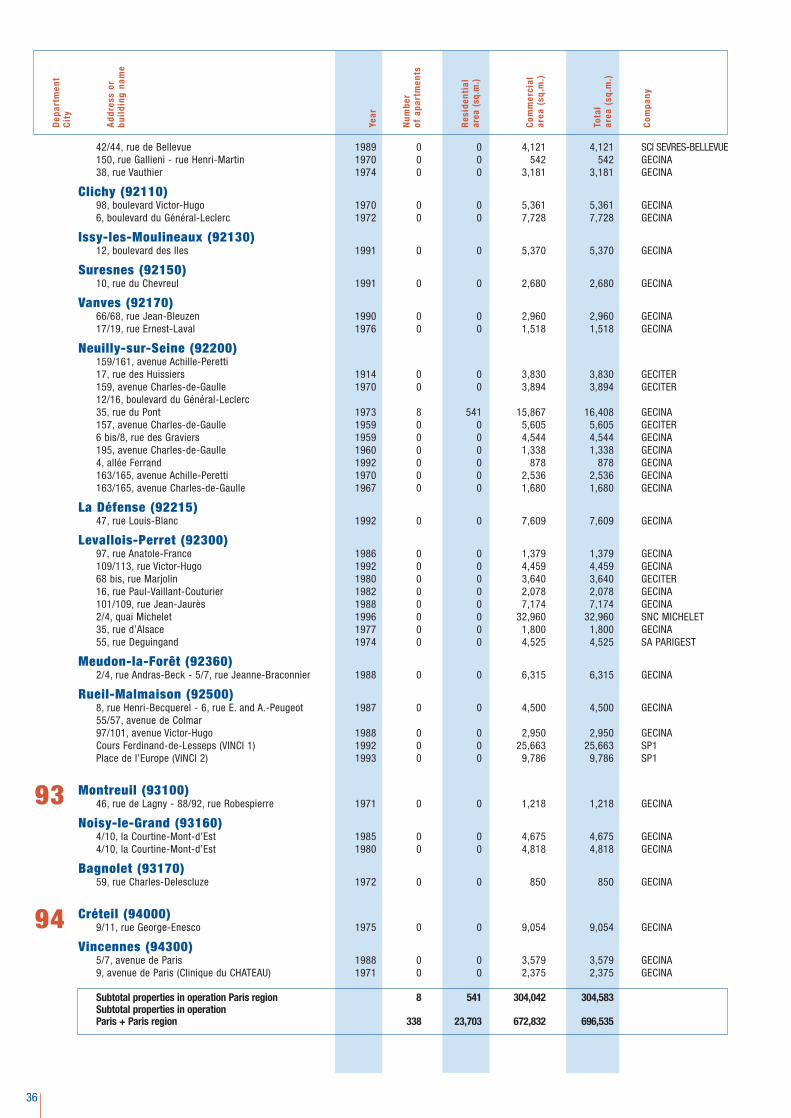

42/44, rue de Bellevue 1989 0 0 4,121 4,121 SCI SEVRES-BELLEVUE150, rue Gallieni - rue Henri-Martin 1970 0 0 542 542 GECINA38, rue Vauthier 1974 0 0 3,181 3,181 GECINA

Clichy (92110)98, boulevard Victor-Hugo 1970 0 0 5,361 5,361 GECINA6, boulevard du Général-Leclerc 1972 0 0 7,728 7,728 GECINA

Issy-les-Moulineaux (92130)12, boulevard des Iles 1991 0 0 5,370 5,370 GECINA

Suresnes (92150)10, rue du Chevreul 1991 0 0 2,680 2,680 GECINA

Vanves (92170)66/68, rue Jean-Bleuzen 1990 0 0 2,960 2,960 GECINA17/19, rue Ernest-Laval 1976 0 0 1,518 1,518 GECINA

Neuilly-sur-Seine (92200)159/161, avenue Achille-Peretti17, rue des Huissiers 1914 0 0 3,830 3,830 GECITER159, avenue Charles-de-Gaulle 1970 0 0 3,894 3,894 GECITER12/16, boulevard du Général-Leclerc35, rue du Pont 1973 8 541 15,867 16,408 GECINA157, avenue Charles-de-Gaulle 1959 0 0 5,605 5,605 GECITER6 bis/8, rue des Graviers 1959 0 0 4,544 4,544 GECINA195, avenue Charles-de-Gaulle 1960 0 0 1,338 1,338 GECINA4, allée Ferrand 1992 0 0 878 878 GECINA163/165, avenue Achille-Peretti 1970 0 0 2,536 2,536 GECINA163/165, avenue Charles-de-Gaulle 1967 0 0 1,680 1,680 GECINA

La Défense (92215)47, rue Louis-Blanc 1992 0 0 7,609 7,609 GECINA

Levallois-Perret (92300)97, rue Anatole-France 1986 0 0 1,379 1,379 GECINA109/113, rue Victor-Hugo 1992 0 0 4,459 4,459 GECINA68 bis, rue Marjolin 1980 0 0 3,640 3,640 GECITER16, rue Paul-Vaillant-Couturier 1982 0 0 2,078 2,078 GECINA101/109, rue Jean-Jaurès 1988 0 0 7,174 7,174 GECINA2/4, quai Michelet 1996 0 0 32,960 32,960 SNC MICHELET35, rue d’Alsace 1977 0 0 1,800 1,800 GECINA55, rue Deguingand 1974 0 0 4,525 4,525 SA PARIGEST

Meudon-la-Forêt (92360)2/4, rue Andras-Beck - 5/7, rue Jeanne-Braconnier 1988 0 0 6,315 6,315 GECINA

Rueil-Malmaison (92500)8, rue Henri-Becquerel - 6, rue E. and A.-Peugeot 1987 0 0 4,500 4,500 GECINA55/57, avenue de Colmar97/101, avenue Victor-Hugo 1988 0 0 2,950 2,950 GECINACours Ferdinand-de-Lesseps (VINCI 1) 1992 0 0 25,663 25,663 SP1Place de l’Europe (VINCI 2) 1993 0 0 9,786 9,786 SP1

Montreuil (93100)46, rue de Lagny - 88/92, rue Robespierre 1971 0 0 1,218 1,218 GECINA

Noisy-le-Grand (93160)4/10, la Courtine-Mont-d’Est 1985 0 0 4,675 4,675 GECINA4/10, la Courtine-Mont-d’Est 1980 0 0 4,818 4,818 GECINA

Bagnolet (93170)59, rue Charles-Delescluze 1972 0 0 850 850 GECINA

Créteil (94000)9/11, rue George-Enesco 1975 0 0 9,054 9,054 GECINA

Vincennes (94300)5/7, avenue de Paris 1988 0 0 3,579 3,579 GECINA9, avenue de Paris (Clinique du CHATEAU) 1971 0 0 2,375 2,375 GECINA

Subtotal properties in operation Paris region 8 541 304,042 304,583Subtotal properties in operation Paris + Paris region 338 23,703 672,832 696,535

93

94

Com

mer

cial

area

(sq

.m.)

Tota

lar

ea (

sq.m

.)

Com

pany

Res

iden

tial

area

(sq

.m.)

Num

ber

of a

part

men

ts

Year

Add

ress

or

buil

ding

nam

e

Dep

artm

ent

Cit

y

37

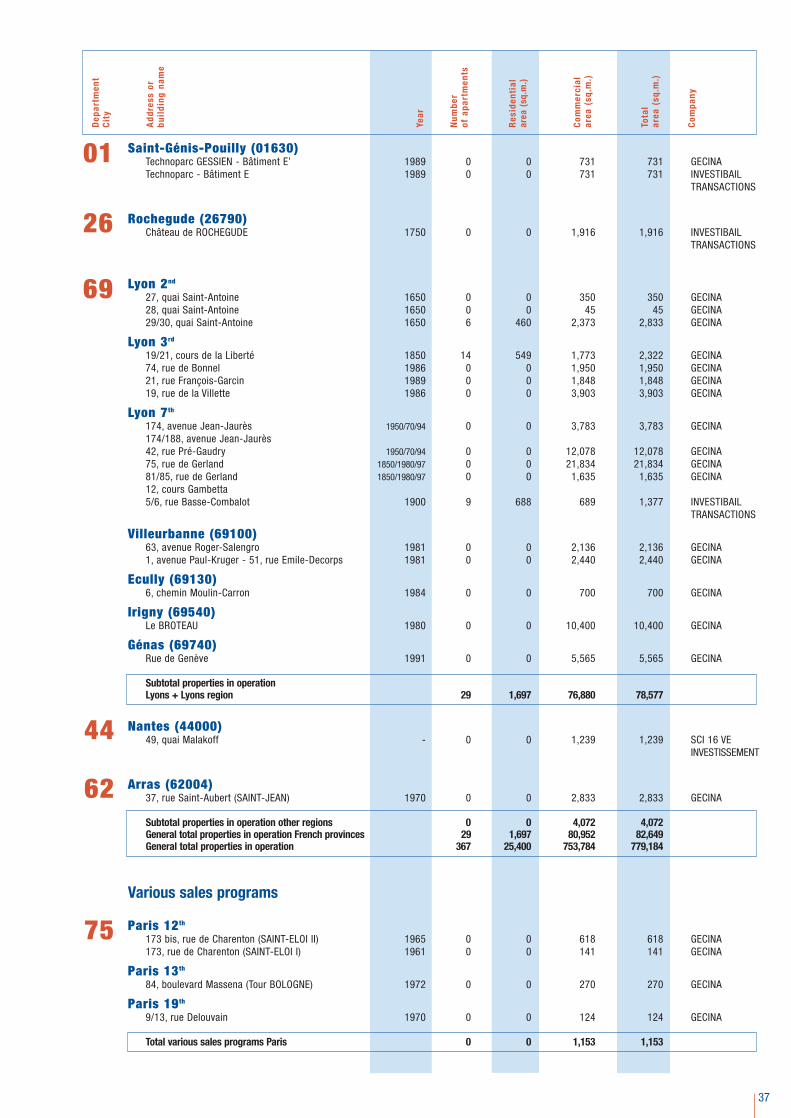

Saint-Génis-Pouilly (01630)Technoparc GESSIEN - Bâtiment E’ 1989 0 0 731 731 GECINATechnoparc - Bâtiment E 1989 0 0 731 731 INVESTIBAIL

TRANSACTIONS

Rochegude (26790)Château de ROCHEGUDE 1750 0 0 1,916 1,916 INVESTIBAIL

TRANSACTIONS

Lyon 2nd

27, quai Saint-Antoine 1650 0 0 350 350 GECINA28, quai Saint-Antoine 1650 0 0 45 45 GECINA29/30, quai Saint-Antoine 1650 6 460 2,373 2,833 GECINA

Lyon 3rd

19/21, cours de la Liberté 1850 14 549 1,773 2,322 GECINA74, rue de Bonnel 1986 0 0 1,950 1,950 GECINA21, rue François-Garcin 1989 0 0 1,848 1,848 GECINA19, rue de la Villette 1986 0 0 3,903 3,903 GECINA

Lyon 7th

174, avenue Jean-Jaurès 1950/70/94 0 0 3,783 3,783 GECINA174/188, avenue Jean-Jaurès42, rue Pré-Gaudry 1950/70/94 0 0 12,078 12,078 GECINA75, rue de Gerland 1850/1980/97 0 0 21,834 21,834 GECINA81/85, rue de Gerland 1850/1980/97 0 0 1,635 1,635 GECINA12, cours Gambetta5/6, rue Basse-Combalot 1900 9 688 689 1,377 INVESTIBAIL

TRANSACTIONS

Villeurbanne (69100)63, avenue Roger-Salengro 1981 0 0 2,136 2,136 GECINA1, avenue Paul-Kruger - 51, rue Emile-Decorps 1981 0 0 2,440 2,440 GECINA

Ecully (69130)6, chemin Moulin-Carron 1984 0 0 700 700 GECINA

Irigny (69540)Le BROTEAU 1980 0 0 10,400 10,400 GECINA

Génas (69740)Rue de Genève 1991 0 0 5,565 5,565 GECINA

Subtotal properties in operation Lyons + Lyons region 29 1,697 76,880 78,577