Gea%20group%20cmd%202013%20 %20praesentation%20gea%20cfo%20dr%20schmale%20final tcm11 25478

47

GEA Group Dr. Helmut Schmale, CFO Oelde, June 26-27, 2013 Capital Markets Day 2013 Accelerating Growth through focusing on Core

description

http://www.gea.com/global/en/binaries/GEA%20Group%20CMD%202013%20-%20Praesentation%20GEA%20CFO%20Dr%20Schmale%20FINAL_tcm11-25478.pdf

Transcript of Gea%20group%20cmd%202013%20 %20praesentation%20gea%20cfo%20dr%20schmale%20final tcm11 25478

GEA Group

Dr. Helmut Schmale, CFOOelde, June 26-27, 2013

Capital Markets Day 2013Accelerating Growth through focusing on Core

engineering for a better world

Disclaimer

Forward-looking statements are based on our current assumptions and forecasts. These statements naturally entail

risks and uncertainties, which may cause the actual results of operations, financial position or performance to diverge

significantly from the estimates given here. Factors that could cause such a divergence include changes in the

economic and business environment, fluctuations in exchange rates and interest rates, launches of competing

products, poor acceptance of new products or services, and changes in business strategy. We are under no obligation

to update forward-looking statements.

Due to rounding, the sum of percentages of order intake and sales by region as well as by customer industry may vary

from 100%.

2 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

engineering for a better world

Agenda

3 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

IV. Strategy update

II. GEA Bonus System: Strong Focus on Cash and ROCE

I. Actual Performance

III. Outlook

engineering for a better world

I. Actual PerformanceOrder Intake YTD May 2013

4 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

[in EUR million]

2012 2013

May

April

Q1

Jan – May -2%

+7%

+3%

-6%

YTD May 2012 YTD May 2013

GEA FS

GEA FT

GEA HX

GEA ME

GEA PE

GEA RT

Jan – May -2%

-13%

-10%

+13%

-3%

+1%

+1%

Q1 2013 yoy: -6%

-22%

-11%

+6%

-6%

-6%

0%

engineering for a better world

35% 38%

24% 22%

16% 16%

9% 10%

7% 7%

6% 4%

4%5%

YTD May 12 YTD May 13

Africa

Middle-East

Latin America

Eastern Europe& CIS

North America

Asia-Pacific

Western Europe26% 28%

9%11%

18%17%

6%7%

9% 7%

5% 5%

7% 5%

3% 3%

11% 11%

4% 4%

YTD May 12 YTD May 13

Other Industries

Climate &Environment

Marine

Chemicals

Pharma

Power

Oil & Gas

Food - Solid

Food - Beverages

Food - Dairy

I. Actual PerformanceOrder Intake YTD May 2013

5 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

-2 %

Order Intake per customer industry Order Intake per region

-2 %

+5%

-9%

-2%

+7%

-3%-37%+8%

+8%

7

-18%

-12%-21%-7%

-2%

+15%

+3%

-3%

abs. yoy abs. yoy

engineering for a better world

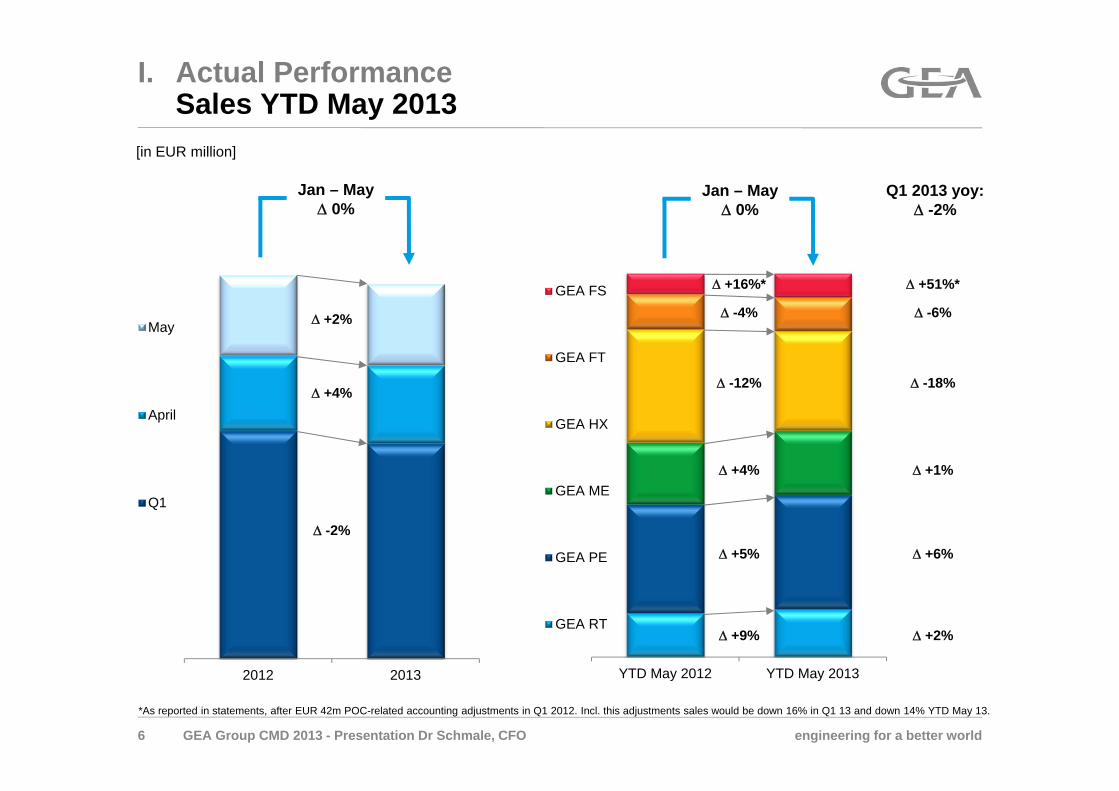

I. Actual PerformanceSales YTD May 2013

6 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

[in EUR million]

2012 2013

May

April

Q1

Jan – May 0%

+2%

+4%

-2%

YTD May 2012 YTD May 2013

GEA FS

GEA FT

GEA HX

GEA ME

GEA PE

GEA RT

Jan – May 0%

+16%*

-12%

+4%

-4%

+5%

+9%

*As reported in statements, after EUR 42m POC-related accounting adjustments in Q1 2012. Incl. this adjustments sales would be down 16% in Q1 13 and down 14% YTD May 13.

Q1 2013 yoy: -2%

+51%*

-18%

+1%

-6%

+6%

+2%

engineering for a better world

36%(36%)

24%(22%)

15%(14%)

10%(10%)

6%(7%)

5%(5%)

5%(5%)

Emerging markets* exposure: 42% (43%)

abs.: -1% YoY

Sales LTM perMay 2013:

EUR 5,715 m+1% YoY

I. Actual PerformanceRegional Sales LTM May 2013

7 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

China10% (10%) abs.: +1% YoY

USA14% (13%) abs.: +11% YoY

Germany10% (10%) abs.: -4% YoY

Top 3 Countries

Western Europe abs.: -1% YoY

Asia-Pacific abs.: +6% YoY

North America abs.: +10% YoY

Latin America abs.: -9% YoY

Eastern Europe & CIS abs.: -6% YoY

Middle East abs.: -9% YoY

Africa abs.: 0% YoY

* According to the definition of emerging/developing economies by International Monetary Fund.

engineering for a better world

I. Actual PerformanceStructural development since 2008

8 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

41%

55%

13%

6%14%

10%5%

5%8% 6%6% 3%

11% 11%

2% 3%

2008 L4Q per Q1 2013

Sales by Customer Industry

Other Industries

Climate &Environment

Marine

Chemicals

Pharma

Power

Oil & Gas

Food

43%35%

15%

15%

16%23%

12% 9%

6%7%

3% 5%5% 5%

2008 L4Q per Q1 2013

Sales by Region

Middle - East

Africa

Latin America

Eastern Europe& CIS

Asia - Pacific

North America

Western Europe

Strong increase of food exposureStrong increase of sales exposure with fast growing emerging markets from

engineering for a better world

I. Actual PerformanceStructural development since 2008

9 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

66%58%

12%

11%

10%18%

5% 9%4% 2%1% 1%2% 0%

2008 Q1 2013

Production Employee by Region

43%35%

15%

15%

16%23%

12% 9%

6%7%

3% 5%5% 5%

2008 L4Q per Q1 2013

Sales by Region

Middle - East

Africa

Latin America

Eastern Europe& CIS

Asia - Pacific

North America

Western Europe

Strong shift of production workforce from high cost regions such as Western Europe and North America to low cost regions, in particular Asia-Pacific andEastern Europe.

27% of workforcelocated in Asia-Pacific and Eastern Europe

15% of workforcelocated in Asia-Pacific

and Eastern Europe

engineering for a better world

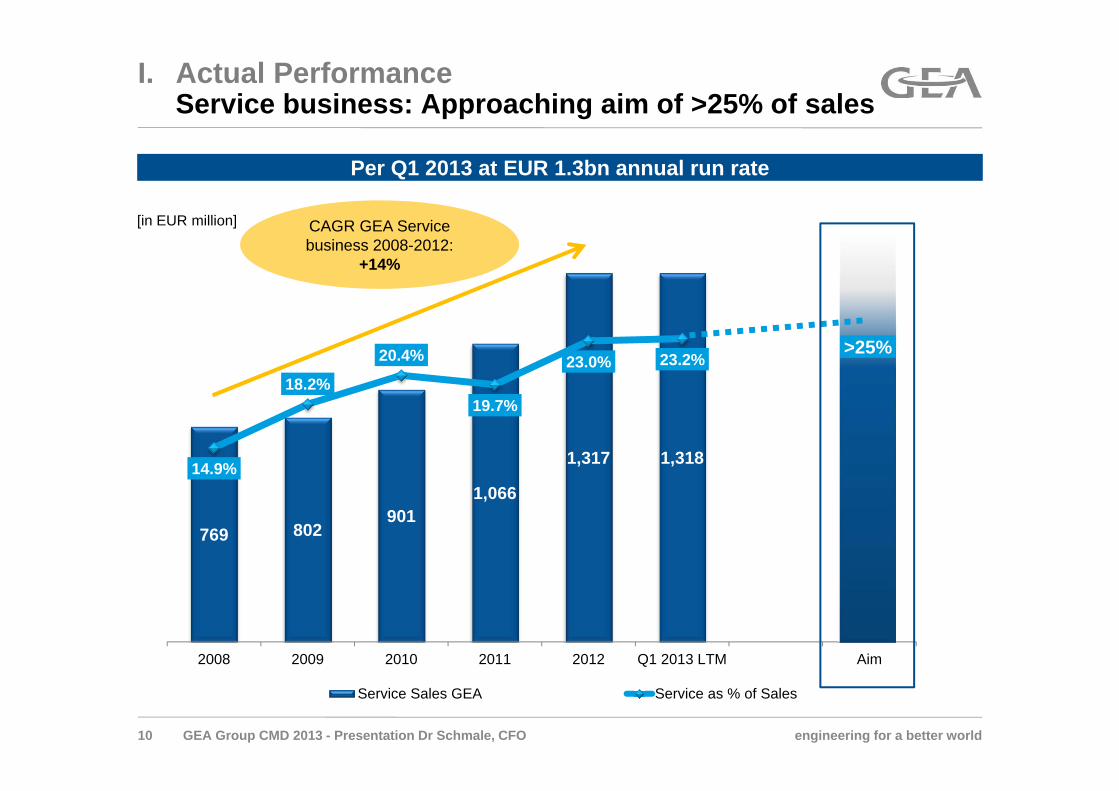

Per Q1 2013 at EUR 1.3bn annual run rate

I. Actual PerformanceService business: Approaching aim of >25% of sales

10 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

769 802901

1,066

1,317 1,31814.9%

18.2%

20.4%

19.7%

23.0% 23.2%25,0%

2008 2009 2010 2011 2012 Q1 2013 LTM Aim

Service Sales GEA Service as % of Sales

[in EUR million]

>25%

CAGR GEA Service business 2008-2012:

+14%

engineering for a better world

Agenda

11 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

IV. Strategy update

II. GEA Bonus System: Strong Focus on Cash and ROCE

I. Actual Performance

III. Outlook

engineering for a better world

II. GEA Bonus System - Three Bonus ComponentsStrong Focus on CFD Margin & ROCE to create value

12 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

2013 2014 20152011 2012

Weight of the three bonus components (%ppts of X, Y, Z) depends on management level scoring

engineering for a better world

II. GEA Bonus SystemStrong Focus on CFD Margin & ROCE to create value

13 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

engineering for a better world

II. GEA Bonus SystemStrong Focus on CFD Margin & ROCE to create value

14 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

ROCE Target: 19%

Min: -5% pts

Max: +5% pts

Target CFD-Margin8%

Max. CFD-Margin13,25%

Min. CFD-Margin4,5%

100%

Cap:250%

engineering for a better world

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50% 55%

II. GEA Bonus System Strong Focus on CFD Margin & ROCE to create value

15 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

Ø ROCE last 36 monthsGEA Group Set Point: 19%

GEA PE

GEA ME

GEA HX

GEA FT

GEA RTCas

h Fl

ow D

river

Mar

gin

(L36

M)

ROCE* (L36M)* Capital employed excl. Goodwill from the acquisition of the former GEA AG by the former Metallgesellschaft AG in 1999

ROCE* and Cash Flow Driver Margin Ø 2010-2012 vs. Ø 2009-2011

GEA

ROCE (L36M) for all Segments increased

Ø CFD-Margin last 36 monthsGEA Group Set Point: 8%

Ø 2009-2011

Ø 2010-2012

engineering for a better world

Ø CFD-Margin last 36 monthsGEA Group Set Point: 8%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50% 55% 60% 65%

II. GEA Bonus System Strong Focus on CFD Margin & ROCE to create value

16 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

Ø ROCE last 36 monthsGEA Group Set Point: 19%

GEA PE

GEA ME

GEA HX

GEA FT GEA RT

Cas

h Fl

ow D

river

Mar

gin

(LTM

)

ROCE* (LTM)

ROCE* and Cash Flow Driver Margin 2012 (LTM) vs. 2011 (LTM)

GEA

Cash Flow Driver Margin (LTM) of GEA, GEA FT, GEA HX and GEA RT improved

* Capital employed excl. Goodwill from the acquisition of the former GEA AG by the former Metallgesellschaft AG in 1999

ROCE declinedue to capex in new factories

ROCE decline due working capitalincrease in 2012

FY 2011 (LTM)

FY 2012 (LTM)

engineering for a better world

ROCE decline due working capitalincrease in 2012

ROCE 2011

ROCE 20120%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

22%

0,0 1,0 2,0 3,0 4,0 5,0 6,0 7,00%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

22%

0,0 1,0 2,0 3,0 4,0 5,0 6,0 7,0

GEA FT: 13.4%

GEA HX: 19.4%

GEA ME: 43.0%

GEA PE: 55.9%

GEA RT: 21.2%

GEA Group: 17.8%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

22%

0,0 1,0 2,0 3,0 4,0 5,0 6,0 7,0

II. GEA Bonus SystemStrong Focus on CFD Margin & ROCE to create value

17 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

Capital turnover (Sales / Capital Employed* average LTM)

EBIT

-Mar

gin

(LTM

)

* Capital employed excl. Goodwill from the acquisition of the former GEA AG by the former Metallgesellschaft AG in 1999

ROCE as product of EBIT-Margin and capital turnover 2012 (LTM)Higher capital employed

due to capex in newfactories only partially

balanced by higher margin

engineering for a better world

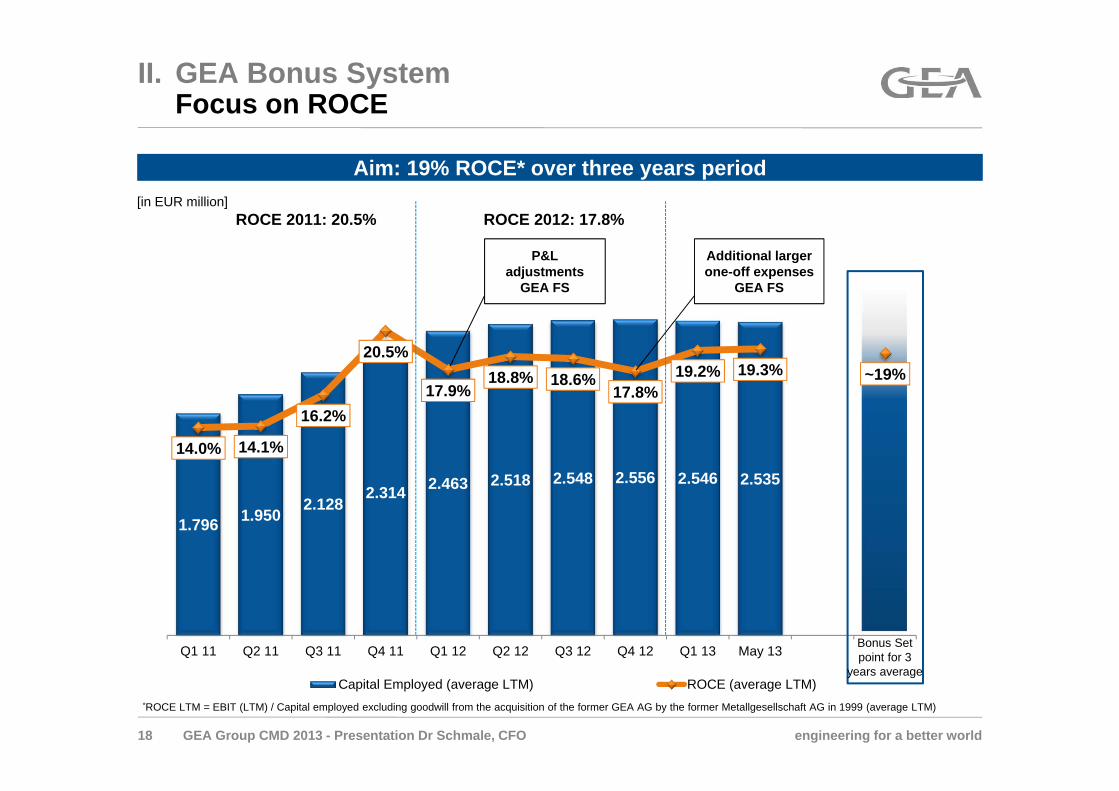

II. GEA Bonus SystemFocus on ROCE

18 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

1.796 1.950 2.1282.314 2.463 2.518 2.548 2.556 2.546 2.535

14.0% 14.1%

16.2%

20.5%

17.9%18.8% 18.6%

17.8%19.2% 19.3% ~19%

Q1 11 Q2 11 Q3 11 Q4 11 Q1 12 Q2 12 Q3 12 Q4 12 Q1 13 May 13

Capital Employed (average LTM) ROCE (average LTM)

[in EUR million]

*ROCE LTM = EBIT (LTM) / Capital employed excluding goodwill from the acquisition of the former GEA AG by the former Metallgesellschaft AG in 1999 (average LTM)

ROCE 2011: 20.5% ROCE 2012: 17.8%

P&L adjustments

GEA FS

Additional larger one-off expenses

GEA FS

Bonus Set point for 3

years average

Aim: 19% ROCE* over three years period

engineering for a better world

II. GEA Bonus SystemFocus on Cash Flow Driver

19 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

374298 283 319

252299 329

368

470 499

8.3%

6.2%5.6%

5.9%

4.5%

5.3%5.7%

6.4%

8.3%8.7%

~8%

Q1 11 Q2 11 Q3 11 Q4 11 Q1 12 Q2 12 Q3 12 Q4 12 Q1 13 May 13

Cash Flow Driver (average LTM) CFD-Margin (average LTM)

[in EUR million]

CFD-Margin 2011: 5.9% CFD-Margin 2012: 6.4%

P&L adjustments

GEA FS

AcquisitionsGEA FS andGEA Bock

Bonus Set point for 3

years average

Aim: ~ 8% Cash Flow Driver Margin over three years period

engineering for a better world20 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

166

129

81

115 122

6

7

4039

3.2%

2.9%

1.8%

2.1% 2.1%

3.2%3.1%

2.0%

2.9% 2.8%

0,0%

0,5%

1,0%

1,5%

2,0%

2,5%

3,0%

3,5%

0

20

40

60

80

100

120

140

160

180

2008 2009 2010 2011 2012 Aim

Capex GEA Capex GPC Capex as % of Sales (w/o) GPC Capex as % of Sales

II. GEA Bonus SystemComponents of Cash Flow Driver – Capex

[in EUR million]

~2%

Capex: Aim of ~2% of sales seen as sustainable

engineering for a better world

Further Working Capital reduction per May 2013

II. GEA Bonus SystemComponents of Cash Flow Driver – Working Capital

21 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

[in EUR million]

657

482567 555 566

445

647707 720

577

772 764 741

533

726 720

17.2%16.4%

15.0%

13.9%13.1%

12.4% 12.4% 12.4% 12.6% 12.6% 12.9%13.3% 13.3% 13.2% 12.9% 12.6%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0

100

200

300

400

500

600

700

800

900

Q3 09 Q4 09 Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Q4 11 Q1 12 Q2 12 Q3 12 Q4 12 Q1 13 May 13

Working Capital Working Capital (average LTM) as % of sales (LTM)

- 461 bps

engineering for a better world

Agenda

22 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

IV. Strategy update

II. GEA Bonus System: Strong Focus on Cash and ROCE

I. Actual Performance

III. Outlook

engineering for a better world

4

1 2 21

4 4

12

6

-4

1

7 8

-1

3

-1

67

6

97

4

9

7 6

2

5

13

10

18

14

11

43

5

10

8

10

14

19 1918

1210

-5

0

5

10

15

20

Aug

. 11

Sep

. 11

Okt

. 11

Nov

. 11

Dez

. 11

Jan.

12

Feb.

12

Mrz

. 12

Apr

. 12

Mai

. 12

Jun.

12

Jul.

12

Aug

. 12

Sep

. 12

Okt

. 12

Nov

. 12

Dez

. 12

Jan.

13

Feb.

13

Mrz

. 13

Apr

. 13

Mai

. 13

3 months 12 months

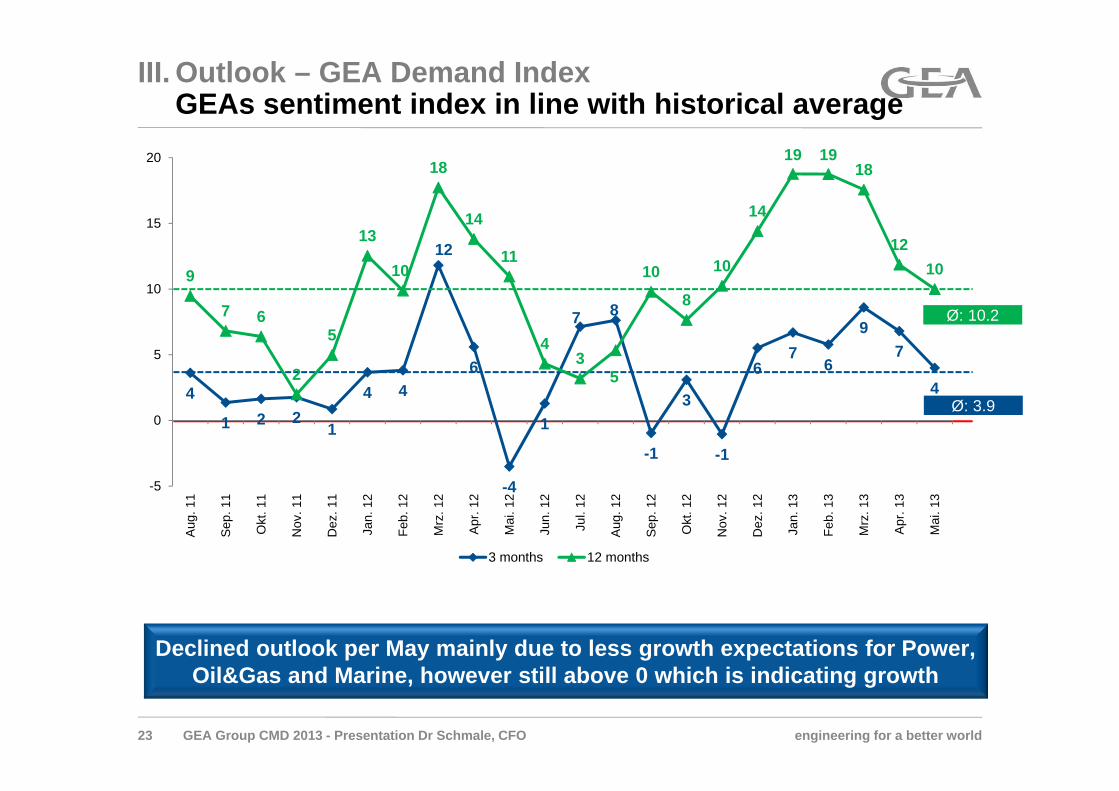

III. Outlook – GEA Demand IndexGEAs sentiment index in line with historical average

23 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

Declined outlook per May mainly due to less growth expectations for Power, Oil&Gas and Marine, however still above 0 which is indicating growth

Ø: 10.2

Ø: 3.9

engineering for a better world

III. OutlookKey Figures FY 2013

24 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

Sales: moderate growth

Calculation Cash Flow Driver Margin:

EBITDA – Capex - / + Working Capital (LTM)Sales Sales Sales

EBITDA: around EUR 700m

Assuming that there is no downturn in global economic growth, we are aiming at the following in the current fiscal year

Cash Flow Driver Margin: at least 8%

engineering for a better world

III. OutlookAdditional Financial Information for 2013

25 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

Tax rate in P&L after impact from tax around 22.5%loss carry forwards:

Impact from PPA in 2013 and in around EUR 25m p.a.subsequent years: thereof GEA FS around EUR 14m p.a.

Sustainable capex level: around 2.0% of sales

Working Capital LTM: approx. 12% - 14% of sales LTM

Interest result: interest rate for financial liabilities(excl. pensions) below 4% p.a.

Dividend policy: around 1/3 of net income

Depreciation & amortization in FY 2012: amounted to around EUR 145m in FY 2012

engineering for a better world

Agenda

26 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

IV. Strategy update

II. GEA Bonus System: Strong Focus on Cash and ROCE

I. Actual Performance

III. Outlook

GEA Group

Dr. Helmut SchmaleCFO

Capital Markets Day 2013Accelerating Growth through focusing on Core

engineering for a better world

Agenda

28 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

I. Separation from HX – Channelling GEA‘s resources

III. The GEA Vision – Driving Food and Process Industry Technologies

II. Portfolio review – Setting the stage for GEA’s long-term success

IV. Outlook – Taking GEA’s evolution to the next level

engineering for a better world29 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

In-depth review of GEA portfolio revealed: Technologies for food industry and technologically sophisticated process industries offer most compelling development opportunities

GEA to further extend leading position in these segments; Proportion of Group revenue accounted for by food technologies to be increased to ~70-75 percent

Strong performance of HX, but limited synergies between HX and remaining business units and different end-markets

Separation of HX provides opportunity to fully explore GEA’s and HX’s long-term potential

II. Separation from HXChannelling GEA‘s resources to unlock further growth

GEA reinforces core business and pursues separation from HX

engineering for a better world

Selling to('inter-segment')

HXAFC CS

PHE

ACC-H

S&T

WC

AT

HX business units

AFC ST

Sales FY 2012 EUR 1,608m

RefrigerationProcess Eng.

7

1

Mech. Separation

Refrigeration

Farm Technologies 13

124

Process Eng.Refrigeration

01

In EURm

Process Eng.

Refrigeration

Process Eng.Refrigeration

01

1

0

~ EUR31m inter-segment sales

Limited inter-company relations and limited future cross-applications synergy potentialKey message

Process Eng.

GEA Group CMD 2013 - Presentation Dr Schmale, CFO

II. Separation from HXHX has only limited business relations within GEA

30

engineering for a better world

Agenda

31 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

I. Separation from HX – Channelling GEA‘s resources

III. The GEA Vision – Driving Food and Process Industry Technologies

II. Portfolio review – Setting the stage for GEA’s long-term success

IV. Outlook – Taking GEA’s evolution to the next level

engineering for a better world32 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

Need to optimally allocate limited resources (management and financial)

Analytic approaches (technology and application mapping) to develop a reasoned vision of the desirable future set of activities (“Pick your battles”)

Maximize value creation for stakeholders as a consequence of targeted and harmonized orientation of the organization

II. Portfolio ReviewMotivation: Keep the growth effort focused!

engineering for a better world33 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

Long-term strategic direction Portfolio health checkStrategy “Focus & Grow” BUs

Strategy for remaining BUs

Initial top-down portfolio assessment based on pre-selected market, competition and financial criteria

Top-down identification of long-list of “subject to further review” BUs that are to be further analyzed

Bottom-up strategic analysis of long-listed “subject to further review” BUs

Definition of GEA Group long-term strategic direction based on strategic analysis and Executive Board workshops

Long-term strategic direction to serve as “guiding path”throughout strategy process

Which BUs support the vision?Vision of GEA? Uses and sources of free cash?

Development of long-term strategy for “focus & grow” businesses

Development of strategy for remaining businesses

1. 2. 3a

3b

Key questions

II. Portfolio ReviewThe three core questions asked

engineering for a better world

Product Leadership Operational Excellence

Customer Proximity• Given the importance of product

leadership for GEA, a technology mapping has already been carried out in order to analyze the position of GEA and secure it subsequently

• A complementary competency mapping has been initiated to systematically assess GEA's application knowledge and analyze it in the context of core technologies

• To ensure customer proximity a strategy by core applications across segments / BUs will be developed

II. Portfolio ReviewGEA’s DNA dimensions: Products and Customers

34 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

engineering for a better world35 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

HX

AFC SingleAFC Com-pact….….

ME

SeparationFlow Com-ponents….….

FT

Milking & CoolingFarm Equipment….

RT

ComponentsFreezers….….

PE

Concentra-tionChemical Drying ….….

FS

PPMPSL….

BUs BUsBUs BUsBUsBUs

Market Applications (e.g. cheese, beer, marine)

Technology & competence mapping

II. Portfolio ReviewFoundation: Holistic analysis of entire organization...

engineering for a better world

Evaluation and selection of suitable business models for GEA(e.g. component picker vs. solution provider)

36 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

Note: simplified representation for illustrative purposes

Milk intake, storage &

distribution

Bacteria removal

Whey drainage

Curd production

Pressing, brining & ripening

Pasteur-ization

Standard-ization

Definition process chain & key components by process step

Cutting & Slicing

Primary packagingSt

eps

Equi

pmen

t

Mapping GEA presence & competences

Adjacent equipment & technologies (e.g. plant design, measurement devices, automation control)

Evaluation of attractiveness

Customer interviews to understand buyer preferences (e.g. components, turnkey)

+

II. Portfolio Review...with analysis of production and buyer preferences…

engineering for a better world37 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

Attractive application “white spots”Attractive application “white spots”

Assessment of attractive “white spots” along all key applications based on: Strategic attractiveness Value potential

The selected strategic options for GEA outline a concrete strategic development path and a roadmap to its implementation

Evaluation of options for GEAEvaluation of options for GEA

Portfolio attractiveness Capturing sustainable trends? Reaching targets of GEA?Portfolio balance Risk vs. return? Cash generation vs. cash use? Short vs. long-term value creation?Implementation Can we finance it? What are the risks?

II. Portfolio Review…to determine GEA‘s future winning strategy

engineering for a better world

Cheese Fruit & Vegetables

Meat & Poultry Milk Powder

Fish & Shrimps …

Existing applications, e.g. New applications…

…

…

Cross-application technology

… … ...

Cross-application M&A

A B

C

New application with many expected "white spots”

Attractive "white spots" ("sweet spots")

II. Portfolio ReviewNext Step: Continously developing more applications

38 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

engineering for a better world

Agenda

39 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

I. Separation from HX – Channelling GEA‘s resources

III. The GEA Vision – Driving Food and Process Industry Technologies

II. Portfolio review – Setting the stage for GEA’s long-term success

IV. Outlook – Taking GEA’s evolution to the next level

engineering for a better world

III. The GEA VisionKey investment case post strategy implementation

40 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

Increasingly stringent hygiene and safety regulations in end markets

Growth driven by shift in consumer preferences towards functional, processed and convenience foods

Global leading positions with exceptionally high barriers to entry

Unrivalled quality and breadth of product range

Pure Play: Highly focused and resilient end market exposure

Balanced income split resting on strong food share of revenue of around 70-75 percent

1

2

3

4

5

6

engineering for a better world

54%

6%

11%

11%

5%6%

3%4%

35%

23%

15%

10%

7%5% 5%

72%

7%

6%4%

3%3%3%

2%

41

GEA Group by customerindustry

Food

Oil & Gas

Power

Pharma

ChemicalsMarine

Climate & Environment

Other

GEA Group excl. HX bycustomer industry

GEA Group by region GEA Group excl. HX by region

SalesFY 2012:

EUR 5,720m

Asia-Pacific

North America

LatinAmerica

Eastern Europe

Middle East Africa

Western Europe

Food

Oil & Gas Power

Pharma

Chemicals

MarineClimate & Environment

Other

SalesFY 2012:

EUR 4,142m

32%

26%

18%

10%

7%4%4%

SalesFY 2012:

EUR 4,142m

Asia-Pacific

North America

LatinAmerica

Eastern Europe

Middle East Africa

Western Europe

SalesFY 2012:

EUR 5,720m

GEA Group CMD 2013 - Presentation Dr Schmale, CFO

III. The GEA VisionPure Play: Focused and resilient end market exposure

engineering for a better world

Agenda

42 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

I. Separation from HX – Channelling GEA‘s resources

III. The GEA Vision – Driving Food and Process Industry Technologies

II. Portfolio review – Setting the stage for GEA’s long-term success

IV. Outlook – Taking GEA’s evolution to the next level

engineering for a better world43

Examples for Systematic capital allocationExamples for Systematic capital allocation

Organicgrowth

M&A

R&D spent for development of new technologies Expansion of service network Penetration of new markets Stronger focus on realization of intra-group

synergy potential

Bolt-on acquisitions (as in the past) Acquisition of adjacent products to strengthen GEA’s

current portfolio Acquisition of new technologies that can’t be

developed efficiently internally Partnerships or acquisitions to unlock potential from

regional expansion (e.g. distribution channels)

GEA Group CMD 2013 - Presentation Dr Schmale, CFO

IV. OutlookInvestment plan to bolster GEA’s strategy

Debt reduction Leveraging operating cash flow to reduce debt levels

engineering for a better world

Phase I Phase II Phase III Now: Phase IV

20132012

Strategy review of GEA's businesses around different key criteria

Decision about Separation of HX

Preparation of separation of HX

Full team of advisers will be mandated shortly

"Health checks" per BU to review and challenge business model

• End market characteristics

• Growth and profitability patterns

• Competitive positioning

• Sources of competitive advantage

• Optimal ownership from synergies perspective

44 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

IV. OutlookTimeline: GEA portfolio strategy process in four phases

45

engineering for a better world

Investor Relations CalendarUpcoming Roadshows and Conferences

46 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

July 8, 2013 Roadshow Italy Milano

August 1-2, 2013 Roadshow UK London

July 31, 2013 Roadshow Ireland Dublin

August 2, 2013 Roadshow Germany Frankfurt

September 3, 2013 Roadshow UK Edinburgh

September 4-6, 2013 Roadshow/Conference UK London

September 5, 2013 Roadshow Denmark Copenhagen

August 30, 2013 Conference Germany Frankfurt

September 16-19, 2013 Roadshow/Conference USA & Canada New York, Boston, Toronto

September 19 & 24-25, 2013 Roadshow/Conference Germany Frankfurt, Munich

engineering for a better world

Financial Calendar

47 GEA Group CMD 2013 - Presentation Dr Schmale, CFO

July 30, 2013 Interim Report Q2 2013

October 31, 2013 Interim Report Q3 2013