GE Capital Investor Meeting - General Electric Capital Investor Meeting July 28, 2009 "Results are...

32

GE Capital Investor Meeting July 28, 2009 "Results are preliminary and unaudited. This document contains “forward-looking statements”- that is, statements related to future, not past, events. In this context, forward-looking statements often address our expected future business and financial performance and financial condition, and often contain words such as “expect,” “anticipate,” “intend,” “plan,” “believe,” “seek,” “see,” or “will.” Forward-looking statements by their nature address matters that are, to different degrees, uncertain. For us, particular uncertainties that could cause our actual results to be materially different than those expressed in our forward-looking statements include: the severity and duration of current economic and financial conditions, including volatility in interest and exchange rates, commodity and equity prices and the value of financial assets; the impact of U.S. and foreign government programs to restore liquidity and stimulate national and global economies; the impact of conditions in the financial and credit markets on the availability and cost of GE Capital’s funding and on our ability to reduce GE Capital’s asset levels and commercial paper exposure as planned; the impact of conditions in the housing market and unemployment rates on the level of commercial and consumer credit defaults; our ability to maintain our current credit rating and the impact on our funding costs and competitive position if we do not do so; the soundness of other financial institutions with which GE Capital does business; the adequacy of our cash flow and earnings and other conditions which may affect our ability to maintain our quarterly dividend at the current level; the level of demand and financial performance of the major industries we serve, including, without limitation, air and rail transportation, energy generation, network television, real estate and healthcare; the impact of regulation and regulatory, investigative and legal proceedings and legal compliance risks, including the impact of proposed financial services regulation; strategic actions, including acquisitions and dispositions and our success in integrating acquired businesses; and numerous other matters of national, regional and global scale, including those of a political, economic, business and competitive nature. These uncertainties may cause our actual future results to be materially different than those expressed in our forward-looking statements. We do not undertake to update our forward-looking statements.” “This document may also contain non-GAAP financial information. Management uses this information in its internal analysis of results and believes that this information may be informative to investors in gauging the quality of our financial performance, identifying trends in our results and providing meaningful period-to-period comparisons. For a reconciliation of non-GAAP measures presented in this document, see the accompanying supplemental information posted to the investor relations section of our website at www.ge.com .” “In this document, “GE” refers to the Industrial businesses of the Company including GECS on an equity basis. “GE (ex. GECS)” and/or “Industrial” refer to GE excluding Financial Services.” 2 Key Messages GE Capital well run thru this recession, will provide attractive long term returns Funding and liquidity dramatically improved and future profile very manageable Portfolios performing as expected or slightly better, most below Fed Base Case 2010 stress test loss scenarios show losses similar to 2009 Historically, new regulation included grandfathering … believe we have strong support for our business model and will defend vigorously We don't see the need to raise external capital, even under adverse scenarios Post this cycle, GE Capital will emerge as competitively advantaged $400B business with attractive returns (2%+ ROI) 1 2 3 4 5 6 Much better Early in cycle, but OK Challenging • U.S. Consumer • U.K. Mortgage • Commercial loans and leases • Global Banking • Commercial Real Estate 7

Transcript of GE Capital Investor Meeting - General Electric Capital Investor Meeting July 28, 2009 "Results are...

GE Capital

Investor Meeting

July 28, 2009"Results are preliminary and unaudited. This document contains “forward-looking statements”- that is, statements related to future, not past, events. In this context, forward-looking statements often address our expected future business and financial performance and financial condition, and often contain words such as “expect,” “anticipate,” “intend,” “plan,” “believe,”“seek,” “see,” or “will.” Forward-looking statements by their nature address matters that are, to different degrees, uncertain. For us, particular uncertainties that could cause our actual results to be materially different than those expressed in our forward-looking statements include: the severity and duration of current economic and financial conditions, including volatility in interest and exchange rates, commodity and equity prices and the value of financial assets; the impact of U.S. and foreign government programs to restore liquidity and stimulate national and global economies; the impact of conditions in the financial and credit markets on the availability and cost of GE Capital’s funding and on our ability to reduce GE Capital’s asset levels and commercial paper exposure as planned; the impact of conditions in the housing market and unemployment rates on the level of commercial and consumer credit defaults; our ability to maintain our current credit rating and the impact on our funding costs and competitive position if we do not do so; the soundness of other financial institutions with which GE Capital does business; the adequacy of our cash flow and earnings and other conditions which may affect our ability to maintain our quarterly dividend at the current level; the level of demand and financial performance of the major industries we serve, including, without limitation, air and rail transportation, energy generation, network television, real estate and healthcare; the impact of regulation and regulatory, investigative and legal proceedings and legal compliance risks, including the impact of proposed financial services regulation; strategic actions, including acquisitions and dispositions and our success in integrating acquired businesses; and numerous other matters of national, regional and global scale, including those of a political, economic, business and competitive nature. These uncertainties may cause our actual future results to be materially different than those expressed in our forward-looking statements. We do not undertake to update our forward-looking statements.”

“This document may also contain non-GAAP financial information. Management uses this information in its internal analysis of results and believes that this information may be informative to investors in gauging the quality of our financial performance, identifying trends in our results and providing meaningful period-to-period comparisons. For a reconciliation of non-GAAP measures presented in this document, see the accompanying supplemental information posted to the investor relations section of our website at www.ge.com.”

“In this document, “GE” refers to the Industrial businesses of the Company including GECS on an equity basis. “GE (ex. GECS)” and/or “Industrial” refer to GE excluding Financial Services.”

2

Key MessagesGE Capital well run thru this recession, will provide attractive long term returns

Funding and liquidity dramatically improved and future profile very manageable

Portfolios performing as expected or slightly better, most below Fed Base Case

2010 stress test loss scenarios show losses similar to 2009

Historically, new regulation included grandfathering … believe we have strong support for our business model and will defend vigorously

We don't see the need to raise external capital, even under adverse scenarios

Post this cycle, GE Capital will emerge as competitively advantaged $400B business with attractive returns (2%+ ROI)

11

22

33

44

55

66

Much better Early in cycle, but OK Challenging

• U.S. Consumer • U.K. Mortgage

• Commercial loansand leases

• Global Banking

• Commercial Real Estate

77

3

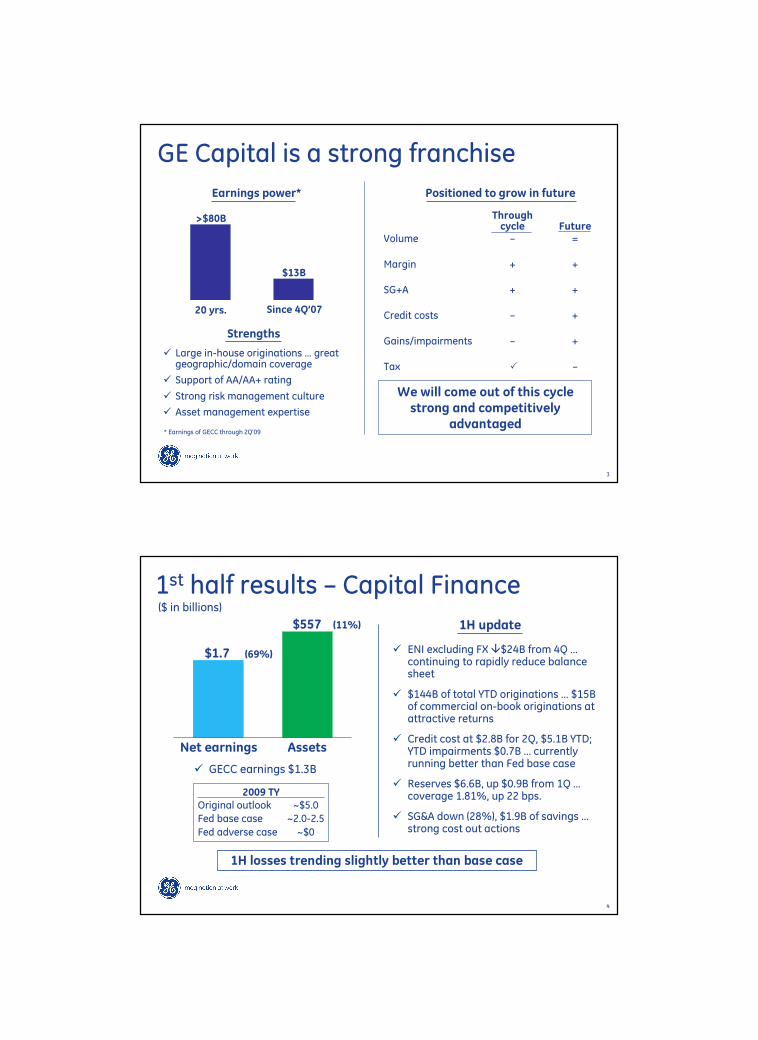

GE Capital is a strong franchise

Earnings power*

� Large in-house originations … great geographic/domain coverage

� Support of AA/AA+ rating

� Strong risk management culture

� Asset management expertise

>$80B

$13B

20 yrs. Since 4Q’07

Strengths

Throughcycle Future

Volume – =

Margin + +

SG+A + +

Credit costs – +

Gains/impairments – +

Tax � –

Positioned to grow in future

We will come out of this cycle strong and competitively

advantaged* Earnings of GECC through 2Q’09

4

1st half results – Capital Finance($ in billions)

1H update

� ENI excluding FX �$24B from 4Q …continuing to rapidly reduce balance sheet

� $144B of total YTD originations … $15B of commercial on-book originations at attractive returns

� Credit cost at $2.8B for 2Q, $5.1B YTD; YTD impairments $0.7B … currently running better than Fed base case

� Reserves $6.6B, up $0.9B from 1Q …coverage 1.81%, up 22 bps.

� SG&A down (28%), $1.9B of savings …strong cost out actions

$1.7

$557

Net earnings Assets

� GECC earnings $1.3B

(69%)

(11%)

1H losses trending slightly better than base case

2009 TYOriginal outlook ~$5.0

Fed base case ~2.0-2.5

Fed adverse case ~$0

5

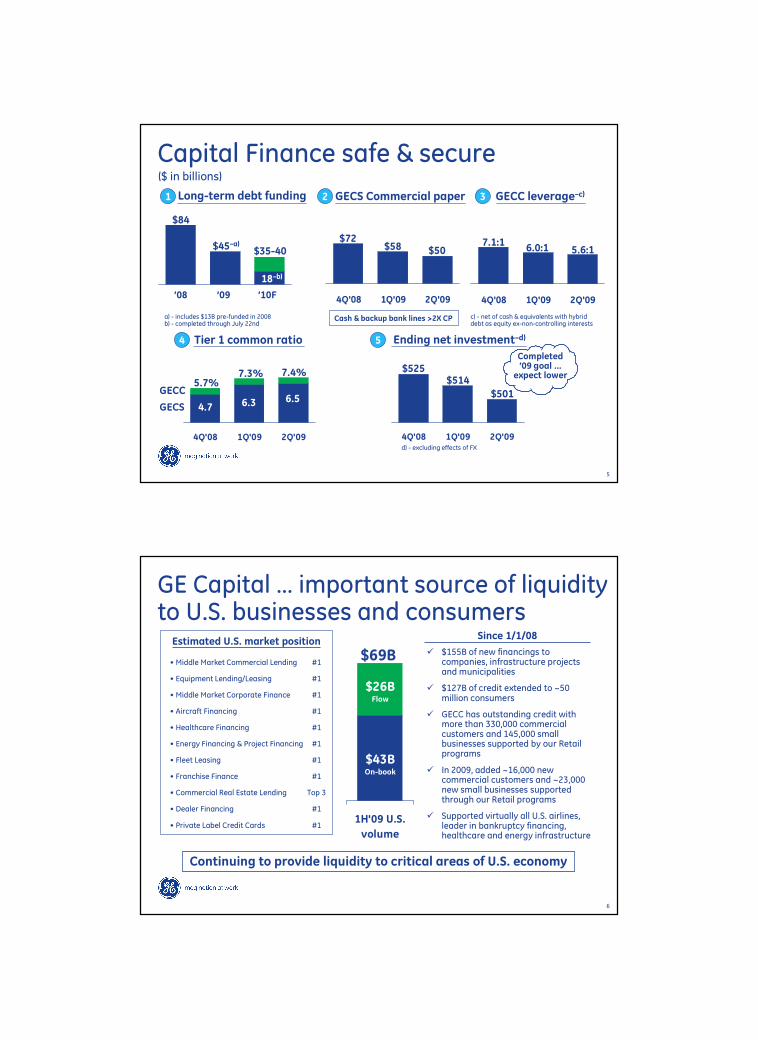

Capital Finance safe & secure

GECS Commercial paper

4Q'08 1Q'09 2Q'09

$72$58 $50

GECC leverage–c)

4Q'08 1Q'09 2Q'09

7.1:16.0:1 5.6:1

Long-term debt funding

’08 ’09 ’10F

$84

$45–a) $35-40

18–b)

4Q'08 1Q'09 2Q'09

Tier 1 common ratio

5.7%7.3% 7.4%

4.7 6.3 6.5GECC

GECS

1 2

4 5

3

c) - net of cash & equivalents with hybrid debt as equity ex-non-controlling interests

Ending net investment–d)

$525$514

$501

4Q'08 1Q'09 2Q'09

Completed’09 goal …

expect lower

Cash & backup bank lines >2X CPa) - includes $13B pre-funded in 2008b) - completed through July 22nd

($ in billions)

d) - excluding effects of FX

6

GE Capital … important source of liquidity to U.S. businesses and consumers

1H'09 U.S.

volume

Continuing to provide liquidity to critical areas of U.S. economy

$69B � $155B of new financings to companies, infrastructure projects and municipalities

� $127B of credit extended to ~50 million consumers

� GECC has outstanding credit with more than 330,000 commercial customers and 145,000 small businesses supported by our Retail programs

� In 2009, added ~16,000 new commercial customers and ~23,000 new small businesses supported through our Retail programs

� Supported virtually all U.S. airlines, leader in bankruptcy financing, healthcare and energy infrastructure

Since 1/1/08

$43BOn-book

$26BFlow

Estimated U.S. market position

• Middle Market Commercial Lending #1

• Equipment Lending/Leasing #1

• Middle Market Corporate Finance #1

• Aircraft Financing #1

• Healthcare Financing #1

• Energy Financing & Project Financing #1

• Fleet Leasing #1

• Franchise Finance #1

• Commercial Real Estate Lending Top 3

• Dealer Financing #1

• Private Label Credit Cards #1

7

2009 originations and collections

Dynamics

$92

$68

+24B

� Assumed TY sales/securitizations ~$20B� (41%) … $10B in 1H

� Assumed TY R/E equity sales ~$1.6B � (64%)

� Actual sales and collections out-paced new originations by ~$62B since 3Q’08

• TY’09 Planned volume:– Consumer: $112B - includes revolving credit

– Commercial: $41B

• Monthly pricing reviews

• Repositioning portfolio to higher yielding core businesses:

Sales/collections

Volume

$103

$85

+18B

Volume

1st half actual* 2nd half estimate

($ in billions)

Sales/collections

Sales

Collections

Business ’09YTD ROIAmericas ~3.0%

Asia ~3.3%

Europe ~2.4%

Banking ~2.6%

EFS ~10.0%

GECAS ~3.8%

*ex-FX

New volume returns

8

Playing offense

1H'09

$144B*

($ in billions)

Commercial

Consumer

Verticals

88

52

Dynamics

• 2Q volume � 10% from 1Q

• Strong 3Q mid-market pipeline growth … $16.1B �20%

• #1 Sales Finance franchise in U.S. ... winning deals from competitors @3%+ ROI, strong pipeline

• #1 PLCC provider in U.S. ... aligned with strategic retail partners

• Aviation emerging markets capabilities driving 80% new order placements … strong 2H pipeline…$1B+

• Helping customers grow …80+ on-site workshops;55+ tradeshows/conferences

Key 1H wins/renewalsGlobal Volume

*$68B on-book

4

9

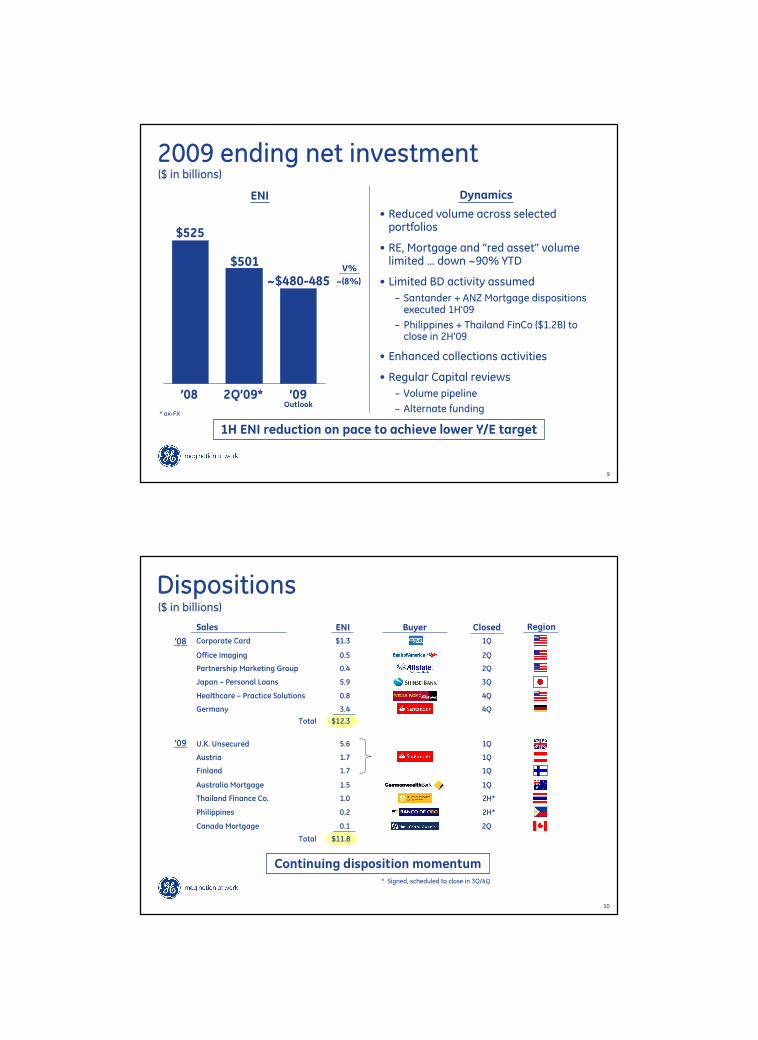

2009 ending net investment

Dynamics

($ in billions)

$525

ENI

V%

~(8%)~$480-485

• Reduced volume across selected portfolios

• RE, Mortgage and “red asset” volume limited … down ~90% YTD

• Limited BD activity assumed

– Santander + ANZ Mortgage dispositions executed 1H’09

– Philippines + Thailand FinCo ($1.2B) to close in 2H’09

• Enhanced collections activities

• Regular Capital reviews

– Volume pipeline

– Alternate fundingOutlook

1H ENI reduction on pace to achieve lower Y/E target

$501

’08 ’092Q’09*

* ex-FX

10

Dispositions($ in billions)

Sales ENI Buyer Closed

Japan – Personal Loans 5.9 3Q

Office Imaging 0.5 2Q

Healthcare – Practice Solutions 0.8 4Q

Corporate Card $1.3 1Q

Australia Mortgage 1.5 1Q

Partnership Marketing Group 0.4 2Q

Region

Continuing disposition momentum

Austria 1.7 1Q

Finland 1.7 1Q

U.K. Unsecured 5.6 1Q

Germany 3.4 4Q

Philippines 0.2 2H*

Thailand Finance Co. 1.0 2H*

* Signed, scheduled to close in 3Q/4Q

Canada Mortgage 0.1 2Q

Total $12.3

Total $11.8

’08

’09

11

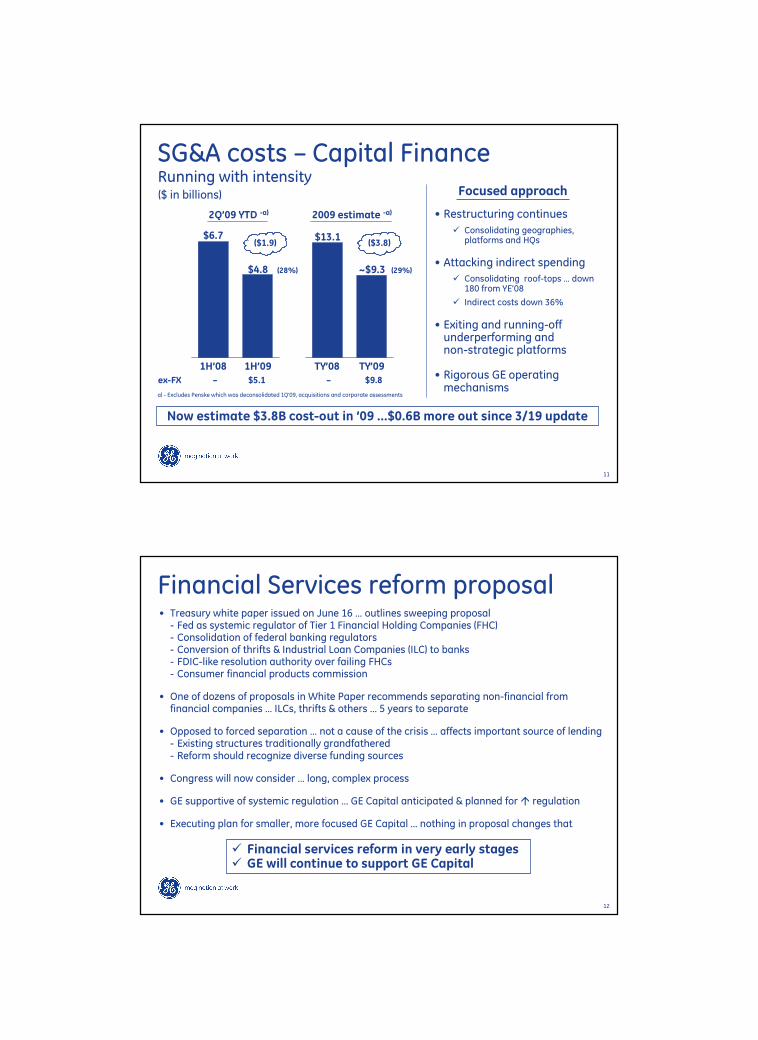

SG&A costs – Capital Finance Running with intensity

Focused approach

• Restructuring continues

� Consolidating geographies, platforms and HQs

• Attacking indirect spending

� Consolidating roof-tops … down 180 from YE’08

� Indirect costs down 36%

• Exiting and running-off underperforming andnon-strategic platforms

• Rigorous GE operating mechanisms

1H’09

$4.8

a) - Excludes Penske which was deconsolidated 1Q’09, acquisitions and corporate assessments

$6.7

2Q’09 YTD -a) 2009 estimate -a)

1H’08

($1.9)

ex-FX – $5.1 – $9.8

TY’09

~$9.3

$13.1

TY’08

($3.8)

(28%) (29%)

Now estimate $3.8B cost-out in ’09 …$0.6B more out since 3/19 update

($ in billions)

12

Financial Services reform proposal• Treasury white paper issued on June 16 … outlines sweeping proposal - Fed as systemic regulator of Tier 1 Financial Holding Companies (FHC)- Consolidation of federal banking regulators- Conversion of thrifts & Industrial Loan Companies (ILC) to banks- FDIC-like resolution authority over failing FHCs- Consumer financial products commission

• One of dozens of proposals in White Paper recommends separating non-financial from financial companies … ILCs, thrifts & others … 5 years to separate

• Opposed to forced separation … not a cause of the crisis … affects important source of lending- Existing structures traditionally grandfathered- Reform should recognize diverse funding sources

• Congress will now consider … long, complex process

• GE supportive of systemic regulation … GE Capital anticipated & planned for � regulation

• Executing plan for smaller, more focused GE Capital … nothing in proposal changes that

� Financial services reform in very early stages� GE will continue to support GE Capital

13

Update from March 19thmeeting

� Commercial Real Estate <Fed base case; Difficult environment

� U.K. Mortgage ~Fed base case; HPI trending better … early

� Global banks and Eastern Europe ~Fed base case; Profitable

� U.S. Consumer Better than Fed base case; Outperforming unemployment

� Total Losses/impairments <Fed base case; Continued reserve increases

Capital adequacy and funding Ratios strong and improving; Funding well ahead of plan

Other:

– Investment securities • Investment securities unrealized loss $2.0B lower• than 1Q

– Associated companies • JVs performing, $126MM associated companyimpairment (Cosmos $110MM)

– Goodwill • Goodwill tested 1Q; Annual update in 2H

Areas of interest 1H’09 loss update; Outlook

1st half losses slightly below Fed base case

14

Agenda

Funding & Liquidity

Portfolio Quality & Reserves

Business Reviews & Stress Testing

– Overview

– Real Estate

– Mortgage/U.S. Consumer

– Banks and JVs

GE Context

Q&A

Kathy Cassidy – GECC Treasurer

Jeff Bornstein – GECC CFO

Jim Colica

Ron Pressman

Mark Begor

Bill Cary

Keith Sherin – GE Vice Chairman & CFO

15

Funding & Liquidity

16

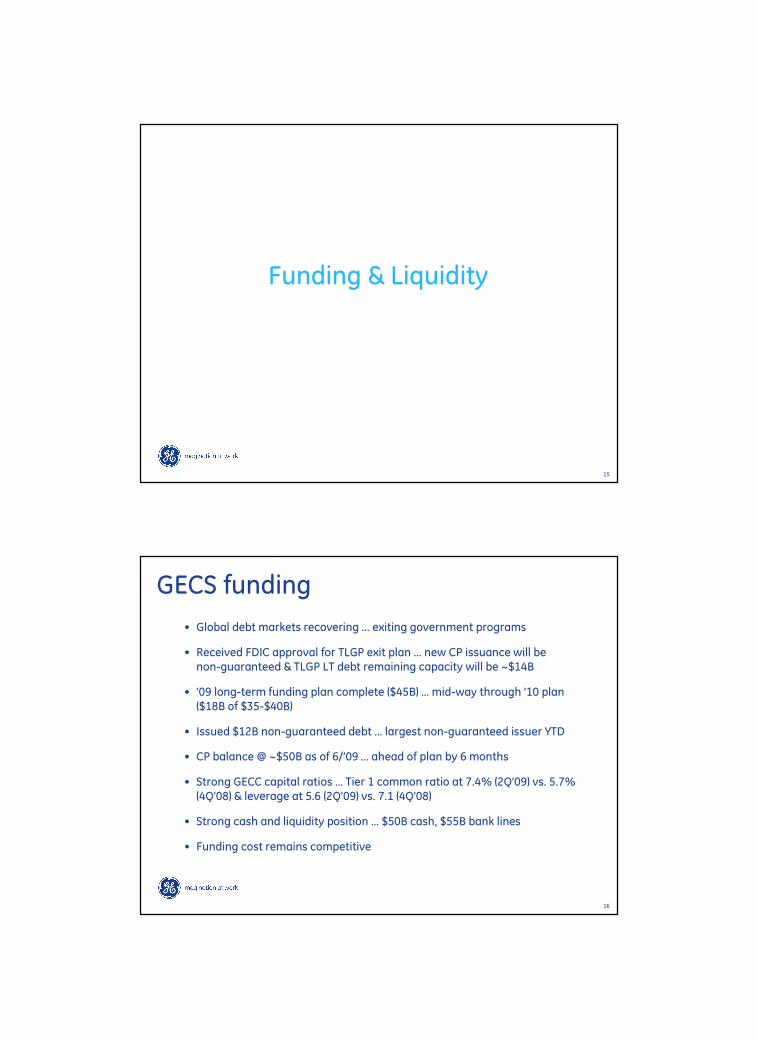

GECS funding

• Global debt markets recovering ... exiting government programs

• Received FDIC approval for TLGP exit plan … new CP issuance will benon-guaranteed & TLGP LT debt remaining capacity will be ~$14B

• ’09 long-term funding plan complete ($45B) … mid-way through ’10 plan ($18B of $35-$40B)

• Issued $12B non-guaranteed debt … largest non-guaranteed issuer YTD

• CP balance @ ~$50B as of 6/’09 … ahead of plan by 6 months

• Strong GECC capital ratios … Tier 1 common ratio at 7.4% (2Q’09) vs. 5.7% (4Q’08) & leverage at 5.6 (2Q’09) vs. 7.1 (4Q’08)

• Strong cash and liquidity position … $50B cash, $55B bank lines

• Funding cost remains competitive

17

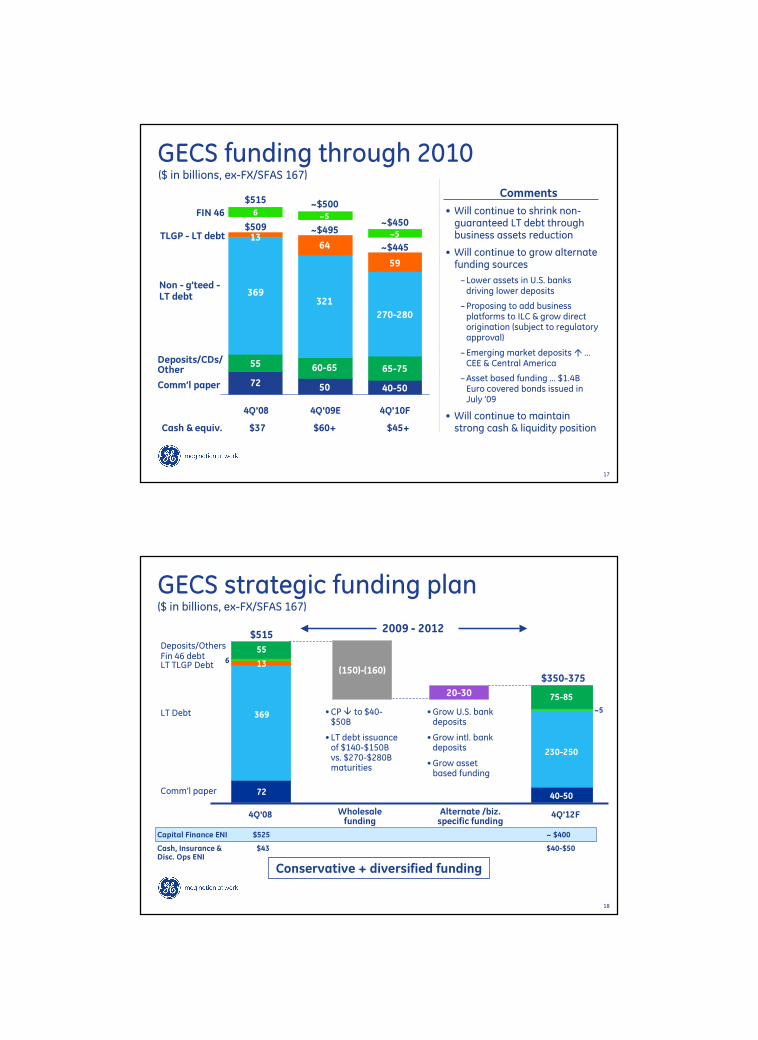

4Q'08 4Q'09E 4Q'10F

GECS funding through 2010($ in billions, ex-FX/SFAS 167)

Cash & equiv. $37 $60+ $45+

Comm’l paper

Deposits/CDs/ Other

Non - g’teed -LT debt

FIN 46

~$495

~$500~5

50

60-65

321

$509

$515

6

72

55

369

~$445

~$450~5

40-50

65-75

270-280

1364

59

TLGP - LT debt

• Will continue to shrink non-guaranteed LT debt through business assets reduction

• Will continue to grow alternate funding sources

–Lower assets in U.S. banks driving lower deposits

–Proposing to add business platforms to ILC & grow direct origination (subject to regulatory approval)

–Emerging market deposits � … CEE & Central America

–Asset based funding … $1.4B Euro covered bonds issued in July ’09

• Will continue to maintain strong cash & liquidity position

Comments

18

GECS strategic funding plan($ in billions, ex-FX/SFAS 167)

4Q'08

$515

20-30

(150)-(160)

Wholesale funding

Alternate /biz. specific funding

•CP � to $40-$50B

• LT debt issuance of $140-$150B vs. $270-$280B maturities

•Grow U.S. bank deposits

•Grow intl. bank deposits

•Grow asset based funding

369

2009 - 2012

Conservative + diversified funding

4Q'12F

$350-375

230-250

Deposits/OthersFin 46 debtLT TLGP Debt

LT Debt

Comm’l paper 72

556 13

75-85

40-50

~5

Capital Finance ENI $525 ~ $400

Cash, Insurance & $43 $40-$50Disc. Ops ENI

19

Beginning cash balance

Sources

LT debt issuances – TLGP

LT debt issuances – non-guaranteed

Alternate funding

Collections > originations

Capital infusion from GE

Total sources

Uses

TLGP LT debt maturities

CP reduction

Others incl. non-guaranteed LT debt maturities

Total uses

Ending cash balance

� ~2% of unsecured debt market� Conservative plan to diversify funding� TLGP maturity profile very manageable� Maintaining strong liquidity position

($ in billions, ex-FX)’09E

$37

52

15-20

5-10

40-45

10

~127-132

(1)

(22)

~(78)

~(101)

~$63-68

’10F

~$63-68

–

20

5-10

25-30

–

~55

(5)

0-(10)

(60)-(65)

(65)-(80)

~$45-60

GECS strategic funding plan by year

Notes:• Funding plan assumes outstanding commercial paper of $40-50B• Pre-funding : ’09 ($13.4B completed in ’08), ’10 (100%: ~$35-$40B in ’09), ’11 (50%: ~$20B in ’10) & ’12 (15%: ~$6B in ’11)

’11F

~$45-60

–

26

5-10

25-30

~2

~63

(20)

–

(40)-(45)

(60)-(65)

~$40-55

’12F

~$40-55

–

34

5-10

25-30

–

~69

(39)

–

(40)-(45)

(79)-(84)

~$25-40

20

GECC & GECS capital metricsTCE/TA ratio -a)

GECS

4Q’08 1Q’09 2Q’09

4Q’09E

Base Adv

4Q’10F

Base Adv

GECC

3.9

5.45.9 5.9

5.6

6.9

5.6

4.9%

6.6% 6.9% ~6.9%~6.6%

~8.1%

~6.9%

Tier 1 common ratio

GECS

4Q’08 1Q’09 2Q’09

4Q’09E

Base Adv

4Q’10F

Base

GECC

4.7

6.36.5

6.9

6.6

7.8

6.5

5.7%

7.3% 7.4%~8.0%~7.7%

~9.0%

~7.7%

Leverage -b)

GECC

4Q’08 1Q’09 2Q’09

4Q’09E

Base Adv

4Q’10F

Base

GECS

7.16.0 5.6

5.35.4 4.8 5.2

7.7

6.45.9 ~5.7 ~5.9

~5.1~5.7

• Strong tangible common equity ratios even in adverse case … well positioned relative to peer average

• Leverage commitments ahead of plan … GECC ~6:1 since 1Q’09 and can be maintained even in Fed adverse scenario

a) -Tangible Common Equity (TCE): Shareholders’ equity less goodwill & intangibles; Tangible Assets (TA): Total assets less goodwill & intangibles

b) -Net of cash & equivalents with hybrid debt as equity ex. non-controlling interests

Adv

Adv

• 2010 likely to be impacted by SFAS 167 requiring to account for securitizations on-book

• 2010 adverse case Tier 1 common ratio well above 4% threshold defined by the Fed as part of SCAP

21

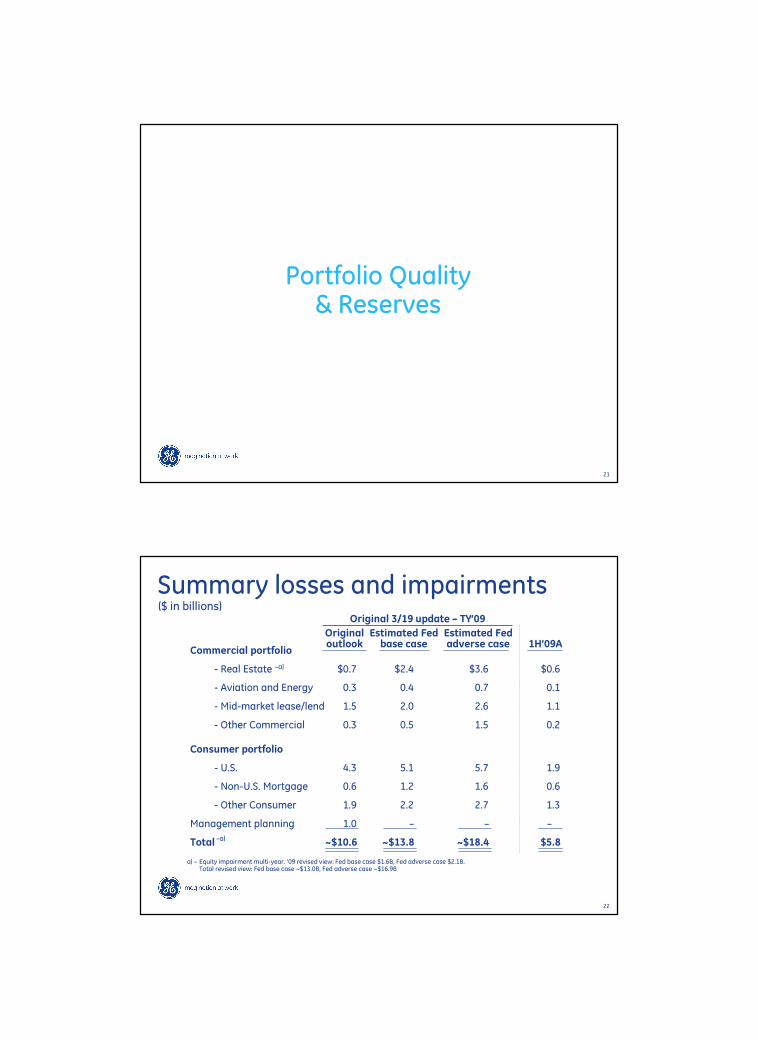

Portfolio Quality& Reserves

22

Commercial portfolio

- Real Estate –a) $0.7 $2.4 $3.6 $0.6

- Aviation and Energy 0.3 0.4 0.7 0.1

- Mid-market lease/lend 1.5 2.0 2.6 1.1

- Other Commercial 0.3 0.5 1.5 0.2

Consumer portfolio

- U.S. 4.3 5.1 5.7 1.9

- Non-U.S. Mortgage 0.6 1.2 1.6 0.6

- Other Consumer 1.9 2.2 2.7 1.3

Management planning 1.0 – – –

Total ~$10.6 ~$13.8 ~$18.4 $5.8

Summary losses and impairments($ in billions)

Originaloutlook

Estimated Fedbase case

Estimated Fedadverse case 1H’09A

Original 3/19 update – TY’09

a) – Equity impairment multi-year. ’09 revised view: Fed base case $1.6B, Fed adverse case $2.1B.Total revised view: Fed base case ~$13.0B, Fed adverse case ~$16.9B

–a)

23

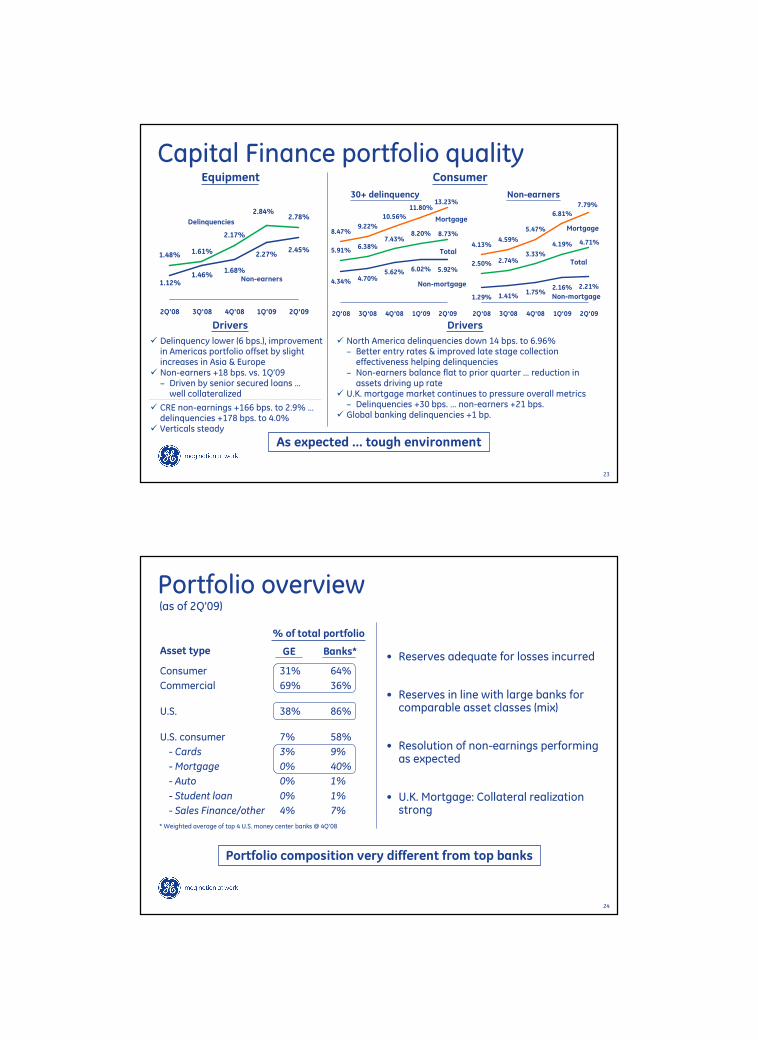

1.48% 1.61%

2.17%

2.78%

1.46%

2.45%

1.12%

1.68%

2.27%

2.84%

2Q'08 3Q'08 4Q'08 1Q'09 2Q'09

Capital Finance portfolio qualityEquipment Consumer

Delinquencies

Non-earners 4.34%

5.62% 6.02% 5.92%

5.91%6.38%

7.43%8.20%8.47%

9.22%

10.56%

11.80%

4.70%

8.73%

13.23%

2Q'08 3Q'08 4Q'08 1Q'09 2Q'09

� North America delinquencies down 14 bps. to 6.96%‒ Better entry rates & improved late stage collection effectiveness helping delinquencies

‒ Non-earners balance flat to prior quarter … reduction in assets driving up rate

� U.K. mortgage market continues to pressure overall metrics‒ Delinquencies +30 bps. … non-earners +21 bps.

� Global banking delinquencies +1 bp.

Total

Non-mortgage

� Delinquency lower (6 bps.), improvement in Americas portfolio offset by slight increases in Asia & Europe

� Non-earners +18 bps. vs. 1Q’09‒ Driven by senior secured loans … well collateralized

� CRE non-earnings +166 bps. to 2.9% … delinquencies +178 bps. to 4.0%

� Verticals steady

Drivers

Mortgage

1.75%2.16% 2.21%

2.50% 2.74%3.33%

4.19%4.13%4.59%

5.47%

6.81%

1.29% 1.41%

4.71%

7.79%

2Q'08 3Q'08 4Q'08 1Q'09 2Q'09

Drivers

Total

Non-mortgage

Mortgage

30+ delinquency Non-earners

As expected … tough environment

24

Portfolio overview

Asset type

Consumer 31% 64%

Commercial 69% 36%

U.S. 38% 86%

U.S. consumer 7% 58%

- Cards 3% 9%

- Mortgage 0% 40%

- Auto 0% 1%

- Student loan 0% 1%

- Sales Finance/other 4% 7%

* Weighted average of top 4 U.S. money center banks @ 4Q’08

• Reserves adequate for losses incurred

• Reserves in line with large banks for comparable asset classes (mix)

• Resolution of non-earnings performing as expected

• U.K. Mortgage: Collateral realization strong

Portfolio composition very different from top banks

% of total portfolio

(as of 2Q’09)

GE Banks*

25

4Q'08 1Q'09 2Q'09

Capital Finance reserve coverage($ in billions)

$5.3$5.7

$6.6

Allowancefor losses

Consumer

� Increased coverage to 2.91%

� U.S. Card & Sales Finance

– Coverage rate steady at 6.6%

– Reserves/non-earnings 192%

� Mortgage

– Coverage rate � 44% to 1.32%

– Reserves/non-earnings 17%

– Average LTV at origination 75%

� Reserves increased by $0.5B in 2Q’09 … coverage rate to 1.13%

– Coverage at RE +37 bps. to 1.24%

– Strong collateral will lead to ultimate loss significantly below non-earners

Commercial

Reserve coverage +$0.9B, +22 bps. vs. prior quarter

Comm’l.

Consumer 3.6

1.7

3.7

2.0

4.1

2.5

Reservecoverage 1.42% 1.59% 1.81%

* 2Q’09 write-offs annualized/2Q’09 allowance

17 mos.write-offsin reserves*

8 mos.write-offsin reserves*

26

U.S. Consumer- U.S. credit cards $10.1 6.18% 8% $178 10.3% 7% 10.3% x 10.1- Residential mortgages none 1,011 3.3% 43%

- Sales finance/other 14.9 6.83% 13% 285 3.3% 8% 3.3% x 14.9

25.0 6.57% 21% 1,474 4.5% 62% 6.11%

U.S. Commercial- Real Estate debt 27.6 1.47% 23% 43.1 0.67% 0.67% x 27.6- Real Estate construction 0.6 4.46% 0.5% 13.1 9.37% 9.37% x 0.6- Commercial loans 27.1 1.84% 23% 229.3 1.35% 1.35% x 27.1- Commercial leases 37.7 1.30% 32% 22.4 1.14% 1.14% x 37.7

$93.1 1.53% 79% $914 2.18% 38% 1.12%

Total $118.1 2.60% 100% $2.4T 3.60% 2.17%

U.S. financing receivables vs. topU.S. banks

GECCReservecoverageReceivables

%Portfolio

($ in billions, as of 2Q’09)Top banks average

ReservecoverageReceivables

%Portfolio

Top bankscoverageGECC assetcomposition

a)- Consumer data avg. of Top 3 Banksb)- Real estate data source Top 5 Bank as of 4Q’08, loss coverage est. split construction vs. non-constructionc) - Commercial loans and leases data source Top 5 Bank

17%

27%

U.S. reserves in line

b)

- (a

c)

27

Non-earnings

4Q'07 1Q'08 2Q'08 3Q'08 4Q'08 1Q'09 2Q'09

Capital Finance

$13.0B1.47%

3.59%

Non-earnings %financing receivables

2.80%

1Q’09 $10.0 $5.7 57%

Walk

Interbanca 0.4 – 0% (2)

Real Estate 0.8 0.2 23% (2)

Mortgage 1.0 0.3 30% (2)

Comm’l lending& leasing 0.7 0.4 48% –

U.S. Consumer – (0.1) n/a (1)

Banks andnon-mortgage 0.1 0.2 129% 1

2Q’09 $13.0 $6.6 51%

1.41%

• U.S. Consumer non-earning flat; reserves �due to � in 30+ and � collection effectiveness on 90+

Coverage walk ($MM)

Non-earners Reserves

Non-earnerscoverage %

Consumer

Commercial

Total

2.13%

1.73%1.53%

$10.0B

$8.0B$7.3B

$6.5B$6.1B

$5.4B

50.5%56.9%66.6%63.4%69.4%70.8%78.1%

6.4

4.53.2

2.51.91.91.7

6.6

5.5

4.74.8

4.64.23.7

ex-FX $12.1B

Non-earnings coverage %

28

Non-earnings definitions

Non-earning Est. lossexposure

1

2

4

3

Non-earnings: Receivables 90 days or more past due (or where collection has become doubtful)

100% recovery: 100% collateral coverage

Workout/cure: In active restructuring/ negotiation with our customer (often timing/technical default issues) … expect full recovery

Remaining collateral: Recovery based on enterprise values, liens on assets or other sources of recovery (guarantees, etc.) but less than 100% collateral coverage

Mortgage insurance: Partial recovery of loss on sale of assets from insurance

Estimated loss exposure: Exposure at risk in excess of collateral

5

6

Remainingcollateral/Mortgageinsurance

Workout/cure

Exposureafter fullrecovery

100%recovery

1

2

3

4

5

6

29

Non-earnings coverage

•100% collateral recovery

• Typically no specific reserve required

100% recovery Workout/cureCollateral on

remaining exposure

•Accounts in active restructuring/negotiation

• Typically no specific reserve required

• Typically requires a specific reserve to cover collateral gap

ExampleCompany “B”

•U.S. real estate industry

• Senior-secured loan

• $13MM non-earning @ 12/’08

• Property value $20MM+

•Loan restructured at higher pricing and enhanced foreclosure rights in 2Q’09

ExampleCompany “A”

•U.S. retailer

•ABL facility – A/R + inventory

•GE commitment $150MM

•Filed bankruptcy 3Q’08

•Business sold 3Q’08

•GE fully recovered outstandings

ExampleCompany “C”

•U.S. home security industry

•Corporate loan

•$34MM non-earning @ 12/’08

•$10MM specific reserve

•Business sold and proceeds of $25MM received in 2Q’09

24

3

30

Commercial non-earnings($ in billions)

Payoffs/payments $0.6

Cured 0.2

Foreclosed/recovery 0.2

Write-off 0.4

$1.4

Bankruptcy proceedings $0.4Customer paying 0.5Negotiation/restructure 0.3In process of liquidating collateral 0.3All other, net 0.3

$1.8Paying customer (0.5)

$1.3

Real Estate $0.1EFS 0.2GECAS 0.2CLL 1.3

$1.8

• Semgroup

• Balli

• Business Prop. loans

• Loans and leases

159

Non-earning reserve coverage

Commercial

4Q’08Non-earning

4Q’08Reserves

Exposure

Collateralvalue onremainingexposure

Loans inrecovery/workout

Expect fullrecovery

100%recovery

($ in billions)

$3.2

$1.7

228%coverage

1.1

0.5

0.8

0.8

Estimatedloss exposure

100% recovery $1.1 $0.5 ($0.6)

Loss in recovery/workout 0.5 0.4 (0.1)

Collateral onremaining exp. 0.8 0.5 (0.3)

Est. loss exposure 0.8 0.4 (0.4)

$3.2 $1.8 ($1.4)

Balance@ 4Q’08

Remaining@ 2Q’09 ∆∆∆∆

March 19 presentation (p. 159)

2Q’09 composition

Non-earnings roll-forward

1H reduction

• $3.2B reduced to $1.8B• Estimate $400MM remaining loss exposure

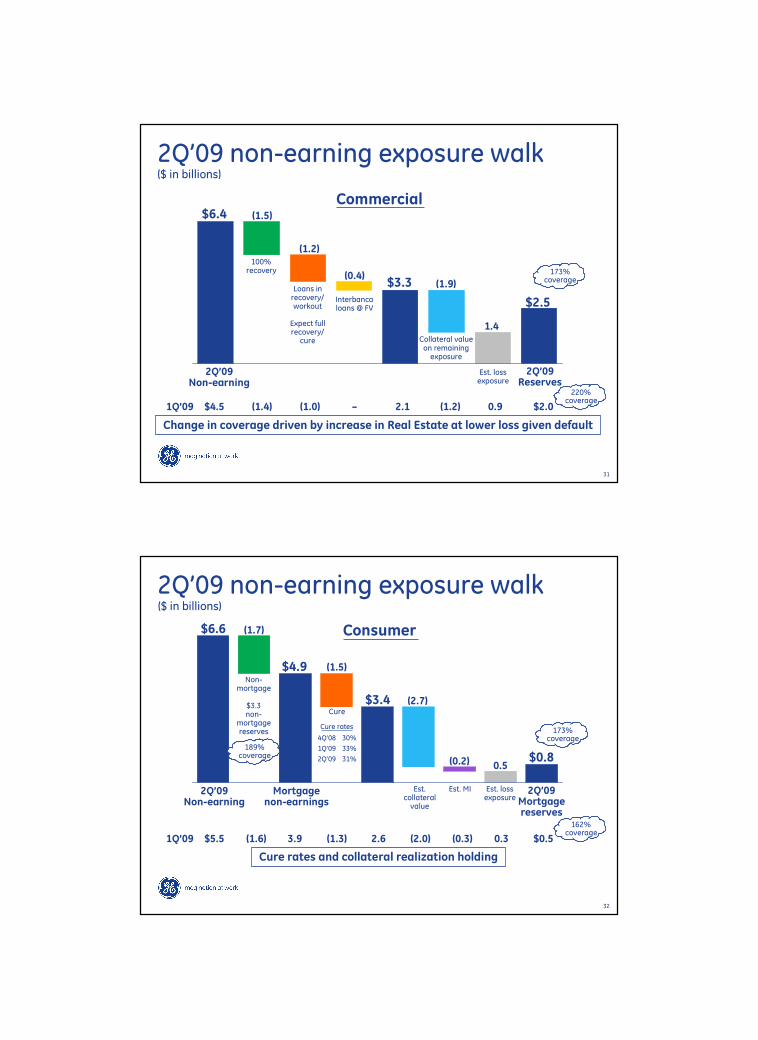

31

2Q’09 non-earning exposure walk($ in billions)

2Q’09Non-earning

2Q’09Reserves

Collateral value on remainingexposure

Loans inrecovery/workout

Expect fullrecovery/cure

100%recovery

$6.4

$2.5

(1.5)

(1.2)

(1.9)

1.4

Est. lossexposure

Commercial

173%coverage

1Q’09 $4.5 (1.4) (1.0) – 2.1 (1.2) 0.9 $2.0

$3.3

220%coverage

Interbancaloans @ FV

(0.4)

Change in coverage driven by increase in Real Estate at lower loss given default

32

2Q’09 non-earning exposure walk($ in billions)

2Q’09Non-earning

2Q’09Mortgagereserves

$6.6

$0.8

(1.7)

(1.5)

(2.7)

0.5

Consumer

173%coverage

$4.9

(0.2)

Mortgagenon-earnings

Est. MIEst.collateralvalue

Non-mortgage

$3.3non-

mortgagereserves

Cure rates

Est. lossexposure

189%coverage

1Q’09 $5.5 (1.6) 3.9 (1.3) 2.6 (2.0) (0.3) 0.3 $0.5

$3.4

162%coverage

4Q’08 30%

1Q’09 33%

2Q’09 31%

Cure

Cure rates and collateral realization holding

33

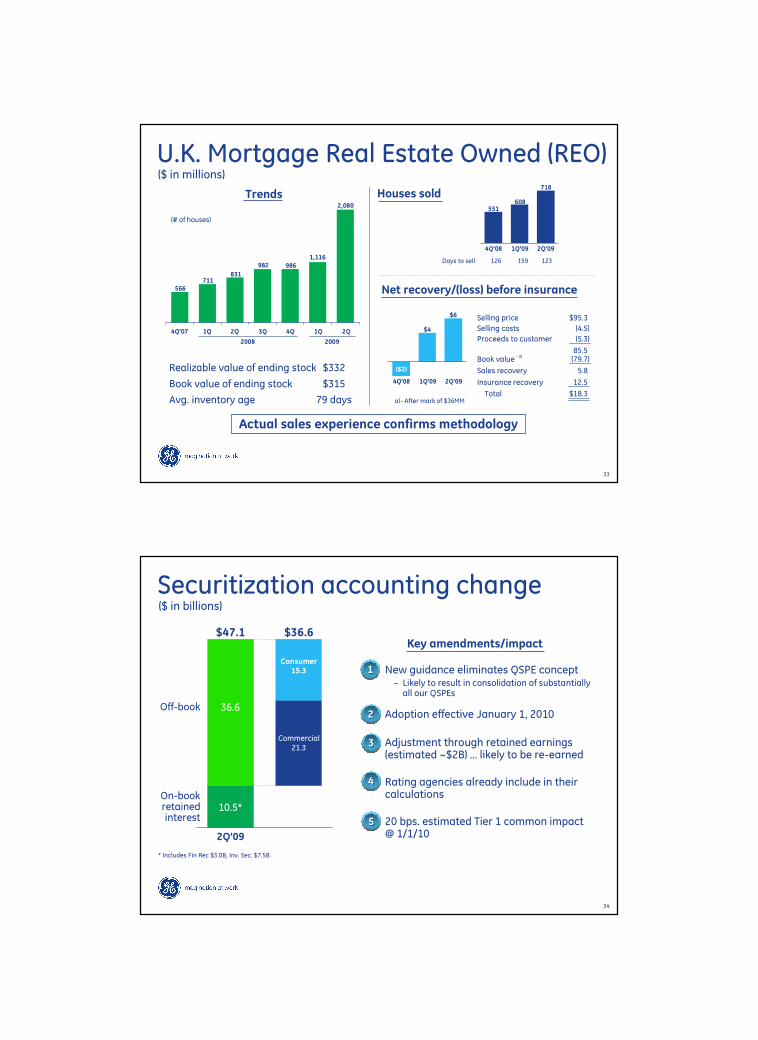

U.K. Mortgage Real Estate Owned (REO)

Trends

($ in millions)

2008

Days to sell 126 159 123

4Q’08 2Q’091Q’09

551

718

608

566

2,080

986

2Q1Q4Q3Q2Q1Q4Q’07

1,116982

831711

(# of houses)

2009

Selling price $95.3

Selling costs (4.5)

Proceeds to customer (5.3)

85.5Book value (79.7)

Sales recovery 5.8

Insurance recovery 12.5

Total $18.3

Net recovery/(loss) before insurance

Actual sales experience confirms methodology

Houses sold

Realizable value of ending stock $332

Book value of ending stock $315

Avg. inventory age 79 days

4Q’08 2Q’091Q’09

($2)

$6

$4

a)- After mark of $36MM

- a)

34

Securitization accounting change

$47.1

Consumer15.3 • New guidance eliminates QSPE concept

– Likely to result in consolidation of substantiallyall our QSPEs

– Adoption effective January 1, 2010

– Adjustment through retained earnings (estimated ~$2B) … likely to be re-earned

• Rating agencies already include in their calculations

• 20 bps. estimated Tier 1 common impact@ 1/1/102Q’09

($ in billions)

On-bookretainedinterest

Off-book

10.5*

36.6

Commercial21.3

Key amendments/impact

22

33

11

$36.6

* Includes Fin Rec $3.0B, Inv. Sec. $7.5B

44

55

35

Business Reviews& Stress Testing

36

Overview

37

Stress testing approach 2010

Consumer

• Mortgages, credit cards, auto, personal loans and sales credit financing

– By product, by geography – market specific macro assumptions for non-U.S. markets based on 3rd party or regulatory guidelines

– Consistent methodology applied across product types globally

Commercial

• Commercial Loans and Leases: Stress probabilities of default, recovery rates

• Commercial Real Estate: By market and property type

• Commercial Aircraft: Valuation by equipment type

• Energy loans and leases: Stress obligor ratings, increase severity, based on outlook

Bottoms up – asset by asset, business by business•Base case is business teams’ assumptions on losses and impairments

•Under Fed “Adverse” Case assumptions: 10.3% avg. unemployment, 10.7% peak unemployment (implied),

0.5% GDP growth

38

Commercial loans and leases – stress testing($ in millions)

Macro • GDP, unemployment

• Liquidity

Portfolio • Senior diversified positions

• Borrow leverage

• Sector diversification

• Asset value of collateral

Key drivers:

Base

Americas equipment $41 $458 1.1% $642 1.6%

Leveraged loans 40 743 1.9 1,093 2.8

Franchise finance 9 94 1.0 182 2.1

EU equipment 9 181 2.0 320 3.4

Asia Pacific 15 214 1.4 300 2.0

U.S. asset-based loans 9 73 0.8 122 1.3

All other 42 203 0.5 481 1.2

Total $165 $1,966 1.2% $3,140 1.9%

AdversePortfolio

2010 stress – credit costs2010 stress - key assumptions

GDP 0.5%

U/E avg. 10.3%

Defaults

Severity

• Two-year cumulative default rate of 15%

• Increased model LGD’s by 25%. Higher for certain products(e.g., Corporate Air)

Fed Adverse 4Q’09 est. fin. rec. ($B)

Lossrate %

Lossrate %

39

Losses and impairments outlook($ in billions)

Commercial portfolio

- Real Estate

Credit costs $0.9 $1.0 $0.5 $1.4

Impairments 0.7 1.1 1.4 1.5

- Aviation and Energy 0.4 0.7 0.2 1.0

- Mid-market lease/lend 2.0 2.6 2.0 3.1

- Other commercial 0.5 1.5 0.5 1.0

Consumer portfolio

- U.S. 5.1 5.7 4.8 5.0

- Non-U.S. mortgage 1.2 1.6 0.7 1.3

- Other consumer 2.2 2.7 2.1 3.2

Total ~$13.0 ~$16.9 ~$12.1 ~$17.5

Estimated base case

Estimated adverse case

2009 –a)

Estimated base case

Estimated adverse case

2010

a) – Adjusted for Real Estate equity impairments

40

Real Estate

41

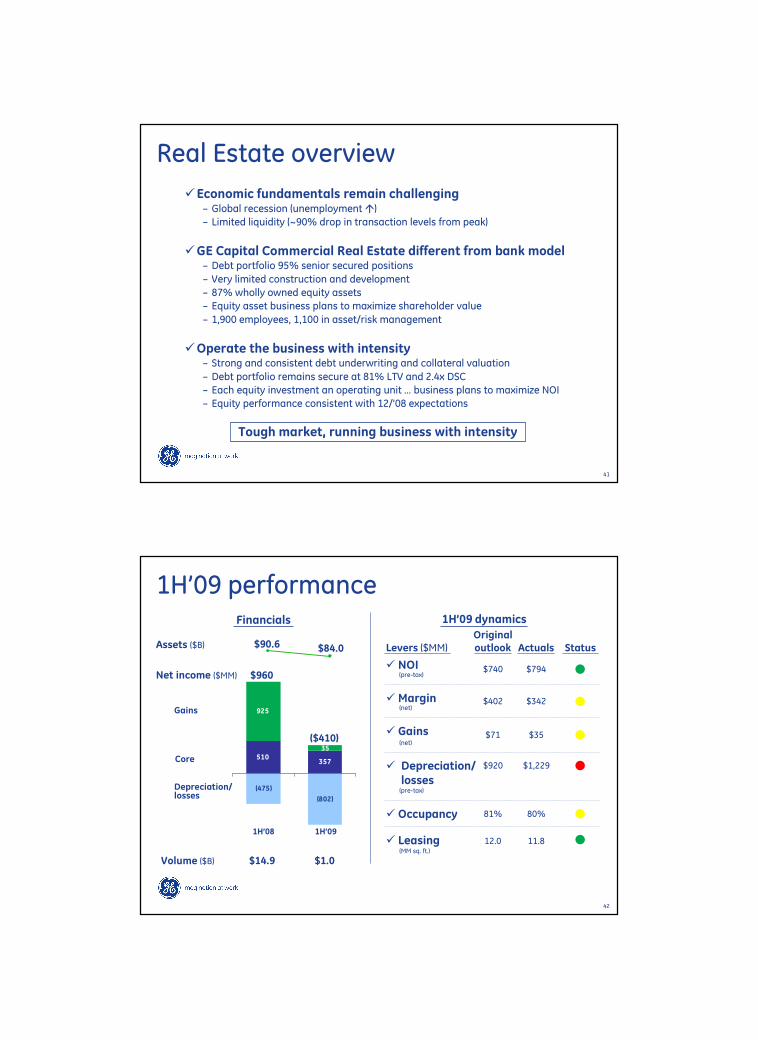

Real Estate overview

Tough market, running business with intensity

�Economic fundamentals remain challenging– Global recession (unemployment �)

– Limited liquidity (~90% drop in transaction levels from peak)

�GE Capital Commercial Real Estate different from bank model– Debt portfolio 95% senior secured positions

– Very limited construction and development

– 87% wholly owned equity assets

– Equity asset business plans to maximize shareholder value

– 1,900 employees, 1,100 in asset/risk management

�Operate the business with intensity– Strong and consistent debt underwriting and collateral valuation

– Debt portfolio remains secure at 81% LTV and 2.4x DSC

– Each equity investment an operating unit … business plans to maximize NOI

– Equity performance consistent with 12/’08 expectations

42

510

925

(475)

(802)

357

35

1H’09 performance

Assets ($B)

1H’09 dynamics

1H’091H’08

Net income ($MM)

$90.6 $84.0

$960

($410)

Gains

Depreciation/ losses

Financials

� NOI

�Margin

� Gains

� Depreciation/losses

� Occupancy

(pre-tax)

(net)

(net)

(pre-tax)

Levers ($MM)Originaloutlook Actuals Status

$740 $794

$402 $342

$71 $35

$920 $1,229

81% 80%

Volume ($B) $14.9 $1.0

Core

� Leasing(MM sq. ft.)

12.0 11.8

43

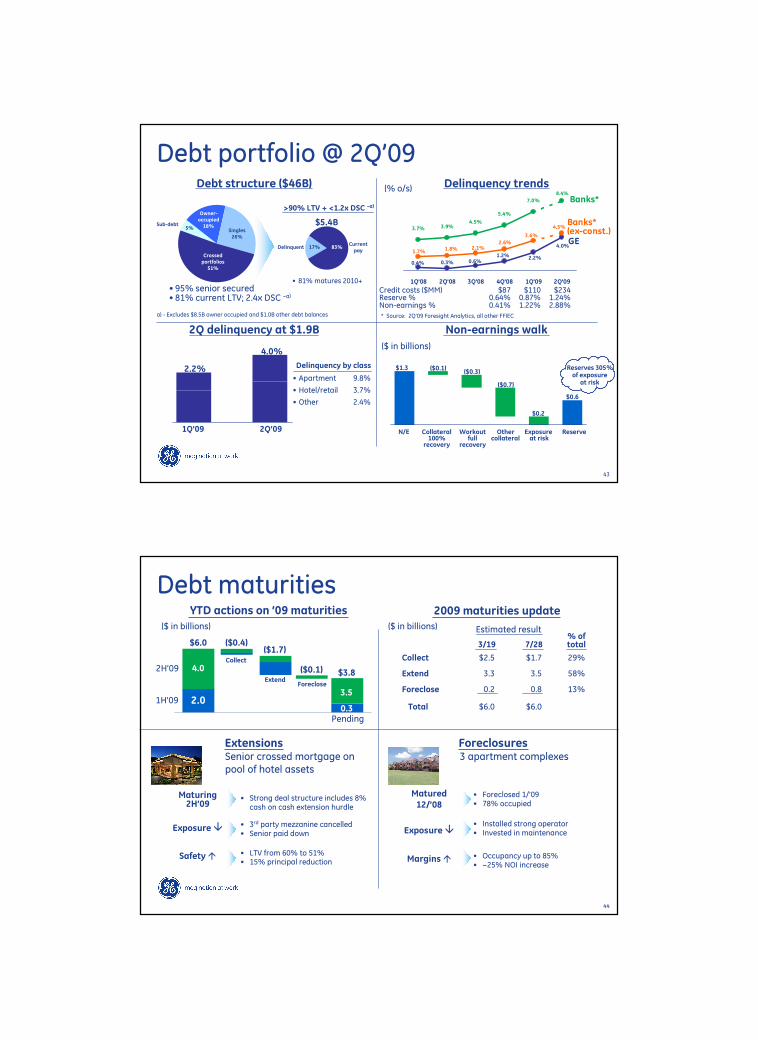

Debt portfolio @ 2Q’09

• Apartment 9.8%

• Hotel/retail 3.7%

• Other 2.4%

2.2%

4.0%

2Q’091Q’09

Non-earnings walk2Q delinquency at $1.9B

Reserves 305% of exposure

at risk

($ in billions)

3.7% 3.9%4.5%

5.4%

7.0%

0.4% 0.3% 0.6%1.2% 2.2%

4.0%1.7% 1.8% 2.1%

2.6%

3.6%

4.5%

1Q'08 2Q'08 3Q'08 4Q'08 1Q'09 2Q'09

(% o/s)

GE

Banks*

Delinquency trendsDebt structure ($46B)

Banks*(ex-const.)

* Source: 2Q’09 Foresight Analytics, all other FFIEC

Credit costs ($MM) $87 $110 $234Reserve % 0.64% 0.87% 1.24%Non-earnings % 0.41% 1.22% 2.88%

8.4%

• 81% matures 2010+• 95% senior secured• 81% current LTV; 2.4x DSC –a)

>90% LTV + <1.2x DSC –a)

DelinquentCurrentpay

$5.4B

17% 83%

a) - Excludes $8.5B owner occupied and $1.0B other debt balances

Sub-debt

$1.3 ($0.1)($0.3)

$0.6

$0.2

($0.7)

N/E Collateral Workout Other Exposure Reserve100% full collateral at risk

recovery recovery

5%

Owner-occupied18%

Singles26%

Crossedportfolios51%

Delinquency by class

44

Debt maturities2009 maturities update

$6.0

$0.2

$3.3

$2.5

3/19

$6.0Total

13%$0.8Foreclose

58%$3.5Extend

29%$1.7Collect

% of total7/28

Estimated result($ in billions)

$6.0

$3.8

3.5

0.3

2H’09

1H’09

($0.4)

2.0

Collect

YTD actions on ’09 maturities

4.0

($1.7)

Extend

Extensions

($0.1)

Foreclose

($ in billions)

Pending

Maturing2H’09

Safety �

Exposure �

Senior crossed mortgage on pool of hotel assets

• Strong deal structure includes 8% cash on cash extension hurdle

• 3rd party mezzanine cancelled• Senior paid down

• LTV from 60% to 51%• 15% principal reduction

Foreclosures3 apartment complexes

Matured12/’08

Exposure �

Margins �

• Foreclosed 1/’09• 78% occupied

• Occupancy up to 85%• ~25% NOI increase

• Installed strong operator• Invested in maintenance

45

• Leased 11.8MM sq. ft. YTD (8.5MM renewals;3.3MM new leases)

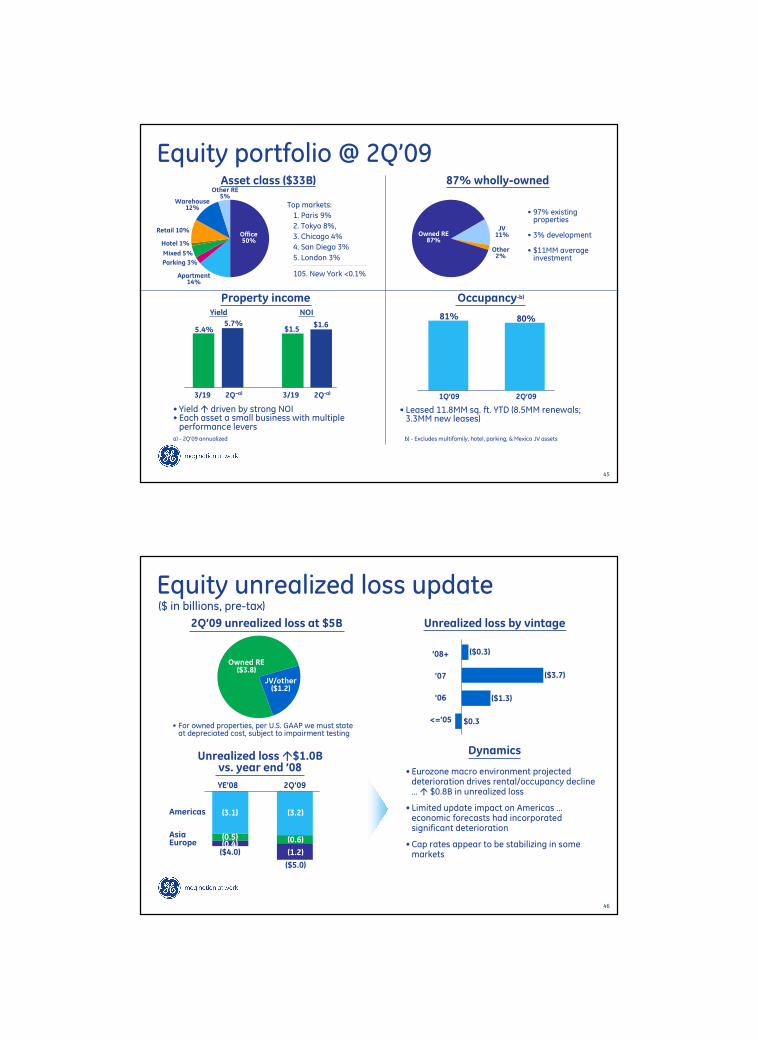

Equity portfolio @ 2Q’09

NOI

2Q-a)

$1.6

Yield

2Q–a)

5.7%

3/19 3/19

5.4% $1.5

Property income

a) - 2Q’09 annualized

1Q’09

81%

2Q’09

Occupancy-b)

80%

b) - Excludes multifamily, hotel, parking, & Mexico JV assets

• Yield � driven by strong NOI• Each asset a small business with multiple performance levers

Asset class ($33B) 87% wholly-owned

Top markets:

1. Paris 9%

2. Tokyo 8%,

3. Chicago 4%

4. San Diego 3%

5. London 3%

• 97% existing properties

• 3% development

• $11MM average investment

Owned RE87%

JV11%

Other RE5%

Warehouse12%

Retail 10%

Hotel 1%

Mixed 5%

Parking 3%

Apartment 14%

Other2%

Office50%

105. New York <0.1%

46

Equity unrealized loss update

Dynamics

• Eurozone macro environment projected deterioration drives rental/occupancy decline … � $0.8B in unrealized loss

• Limited update impact on Americas …economic forecasts had incorporated significant deterioration

• Cap rates appear to be stabilizing in some markets

2Q’09 unrealized loss at $5B Unrealized loss by vintage

($0.3)’08+

’07

’06

<=’05

($3.7)

($1.3)

$0.3

($ in billions, pre-tax)

Unrealized loss �$1.0Bvs. year end ’08

Americas

AsiaEurope

YE’08 2Q’09

($4.0)

($5.0)

(3.1) (3.2)

(0.5) (0.6)

(1.2)(0.4)

JV/other($1.2)

Owned RE($3.8)

• For owned properties, per U.S. GAAP we must state at depreciated cost, subject to impairment testing

47

Stress test update

� Macro environment continues to be challenging� We are committed to providing investor transparency� Losses will materialize over time, should outperform peers� Results remain manageable for GE Capital and GE

($ in billions, pre-tax)

• Goal to outperform Fed adverse losses through strong property level execution

• Highly experienced global team focused on maximizing asset values

Unrealized equity loss over time (est.)

$0.0$1.0

($5.0) $1.4

$2.6

b) - Owner occupied reported separately ($0.1B)c) - Amounts derived from current estimate

Unrealizedequity loss (5.0) (4.7) (5.9) (5.0) (7.7)

(Afterimpairments) n/a (4.0) (4.8) (3.1) (5.1)

Implied loss onaffected assets 26% 28% 31% 26% 34%

Adversecase

Basecase

Loss views

Adversecase

Basecase-c)

2009E-b) 2010F

3/19 7/28

$0.5

$1.9 1.5

1.4EquityDebt

0.9 1.0

1.4

0.5

$2.9

1H’09

$1.6$2.1

1.10.7

a) - Fed adverse case

Depreciation/potential impairment-a)

Current 2H’09E ’10F ’11F Staticloss 2011 YE

estimate view

48

Mortgage/U.S. Consumer

49

69% with MI

Overall portfolio performing …1H net income better than base case

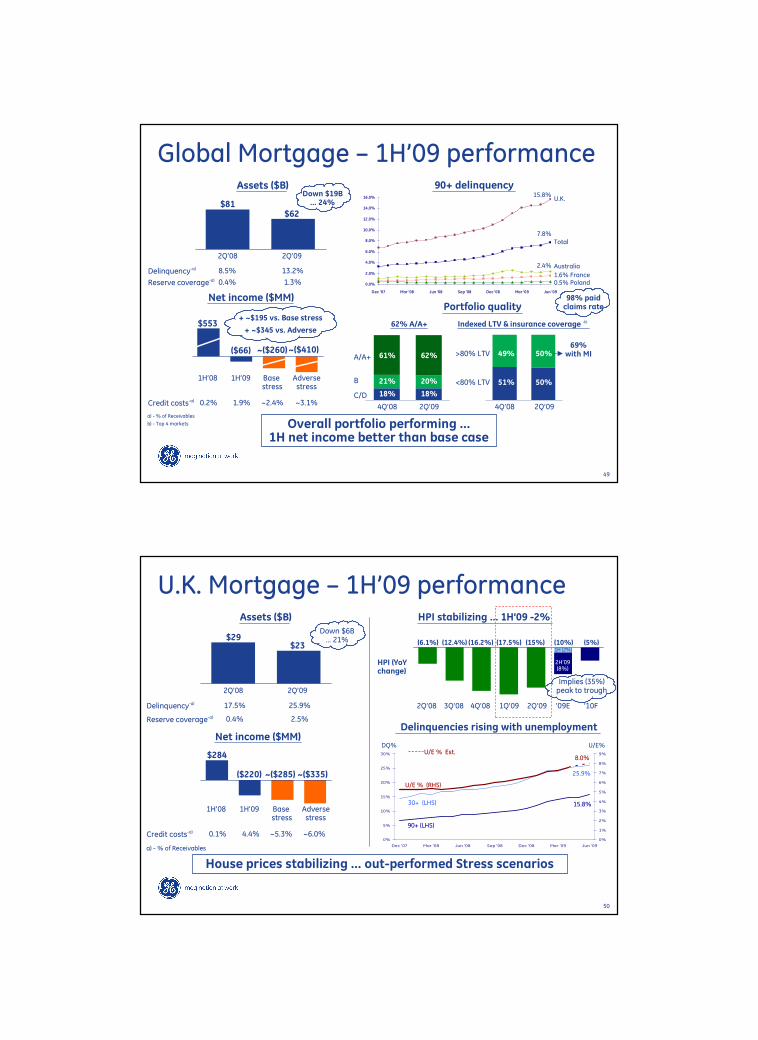

Global Mortgage – 1H’09 performance

a) - % of Receivables

b) - Top 4 markets

+ ~$195 vs. Base stress

+ ~$345 vs. Adverse

Down $19B … 24%

2Q’08 2Q’09

$81$62

Net income ($MM)

Reserve coverage-a) 0.4% 1.3%

1H’08 1H’09 Base stress

Adversestress

$553

($66)

Delinquency-a) 8.5% 13.2%

Credit costs-a) 0.2% 1.9% ~2.4% ~3.1%

~($260)~($410)

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

Dec '07 Mar '08 Jun '08 Sep '08 Dec '08 Mar '09 Jun '09

90+ delinquency

Total

0.5% Poland

Australia

1.6% France

U.K.15.8%

7.8%

2.4%

Portfolio quality

4Q’08 2Q’09

61% 62%

21% 20%

18% 18%

A/A+

B

C/D

62% A/A+ Indexed LTV & insurance coverage -b)

>80% LTV

<80% LTV

50%

50%

2Q’094Q’08

49%

51%

98% paidclaims rate

Assets ($B)

50

Implies (35%) peak to trough

HPI (YoYchange)

2Q’08 3Q’08 4Q’08 1Q’09 2Q’09 ’09E ’10F

(6.1%) (12.4%) (16.2%) (17.5%) (15%) (10%) (5%)

2H’09(8%)

1H (2%)

0%

5%

10%

15%

20%

25%

30%

Dec '07 Mar '08 Jun '08 Sep '08 Dec '08 Mar '09 Jun '09

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

Down $6B … 21%

House prices stabilizing … out-performed Stress scenarios

Assets ($B)

2Q’08 2Q’09

$29$23

Net income ($MM)

Reserve coverage-a) 0.4% 2.5%

1H’08 1H’09 Base stress

Adversestress

$284

($220)

Delinquency-a) 17.5% 25.9%

Credit costs-a) 0.1% 4.4% ~5.3% ~6.0%

HPI stabilizing … 1H’09 -2%

~($285) ~($335)

a) - % of Receivables

U.K. Mortgage – 1H’09 performance

Delinquencies rising with unemployment

30+ (LHS)

90+ (LHS)

U/E % (RHS)

25.9%

15.8%

8.0%

DQ% U/E%U/E % Est.

51

Portfolio overview ($22.7B) –a)

A 20%

B 37%

C 25%

D 12%

2009/2010 stressed scenarios

Indexed LTV distribution

Pre 200749%

‘08 17%

2007 34%

>100%28%

<80%38%

80-90%17%

90-100%17%

A+ 6%

Credit distribution(internal GE Scores)

a) - Financing receivablesb) - 87% mortgage insured

Aggressive REO, loss mitigation & collections actions producing results

7.4% 10%Unemployment(average)

Home price change �10%

Key assumptions

$472Credit cost $ $530$995

�29%

8.5%

1H’09ABase

Peak to trough(home price change)

�42%�43%

2009E 2010F

$1,125

�35%

9.0%

Adverse

�48%

10.5%

�25%

$800

�54%

Adverse

�9%

�28%

U.K. Mortgage ’09-’10 Stress scenarios

4.4%Credit cost % 3.1%4.8% 5.4% 4.6%

($ in millions)

–b)

Base

52

Retail Finance – 1H’09 performanceKey actions

1H’09 plan

1H’08 act.

$261 $252+245% V plan & $541 V adverse

1H’09 act.

1H’09 adverse

$73$(289)

Net income ($MM)

Strong 1H’09 performance … $179 above plan & $541 above stress

2Q’09 plan

2Q’08 act.

$54.7

$49.5

$(3.6B) V plan & $(5.2B) YoY

2Q’09 act.

$53.1

Served receivables ($B)

53.4

Controlled credit lines

$1,581

$932

Revolving$5,059

$3,877

Sales Finance

Raised cut-offs & tightened approvals

728 730744

Oct.’08 June ’09

Previous Year

Current Year

Risk adjusted open to buy ($B)$372

’07 NewVolume

$41

’08 Red.

($200)

2Q’09

$198

Net 1H Red.

($15)

($215B)

+20 FICO

750Avg. U.S. FICO: 693

Avg. FICO Approval rates %

’08

$213

(575 bps.)

48.3 52.446.6

(41%) (23%)

730768

51.346.7

Feb. ’09 Oct. ’08 June ’09Feb. ’09

$1,610

$990

$4,953$3,984

June ’09Feb. ’09 June ’09Feb. ’09

11

22

33

Increased collections intensity …Collectors per DQ accounts up 15% vs ’08

44

53

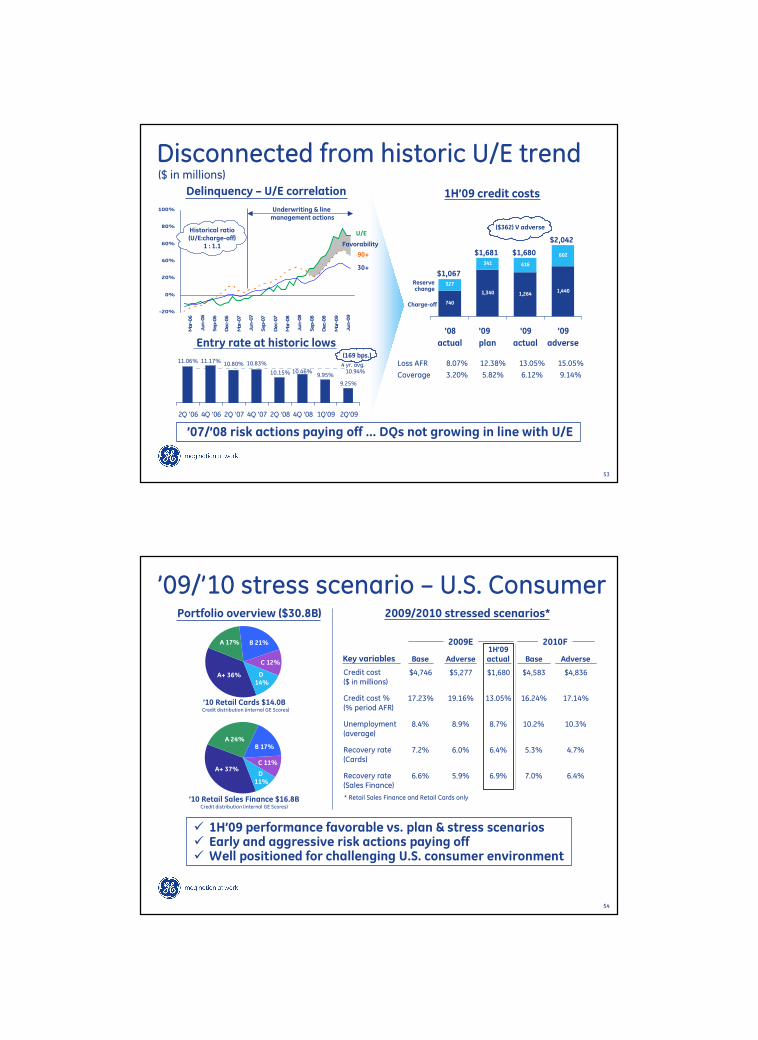

Disconnected from historic U/E trend($ in millions)

’07/’08 risk actions paying off … DQs not growing in line with U/E

-20%

0%

20%

40%

60%

80%

100%

Mar-06

Jun-06

Sep-06

Dec-06

Mar-07

Jun-07

Sep-07

Dec-07

Mar-08

Jun-08

Sep-08

Dec-08

Mar-09

Jun-09

Favorability

Underwriting & line management actions

Historical ratio(U/E:charge-off)

1 : 1.1

U/E

90+

30+

Reserve change

Charge-off

Delinquency – U/E correlation 1H’09 credit costs

Entry rate at historic lows

10.80% 10.83%

9.25%

9.95%

11.06% 11.17%

10.46%10.15%

2Q '06 4Q '06 2Q '07 4Q '07 2Q '08 4Q '08 1Q'09 2Q'09

(169 bps.)

4 yr. avg.10.94%

Loss AFR 8.07% 12.38% 13.05% 15.05%

Coverage 3.20% 5.82% 6.12% 9.14%

740

1,340 1,2641,440

327

341 416

602

'08

actual

'09

plan

'09

actual

'09

adverse

$1,067

$1,681 $1,680

$2,042

($362) V adverse

54

’09/’10 stress scenario – U.S. ConsumerPortfolio overview ($30.8B)

’10 Retail Cards $14.0B

Key variables

2009/2010 stressed scenarios*

’10 Retail Sales Finance $16.8B

A+ 36%

A 17% B 21%

C 12%

D 14%

A+ 37%

A 24%B 17%

C 11%

D 11%

Credit distribution (internal GE Scores)

Credit distribution (internal GE Scores)

Adverse Base AdverseBase

Credit cost %(% period AFR)

19.16% 16.24% 17.14%17.23% 13.05%

Unemployment(average)

8.9% 10.2% 10.3%8.4% 8.7%

1H’09actual

Recovery rate (Sales Finance)

5.9% 7.0% 6.4%6.6% 6.9%

Recovery rate (Cards)

6.0% 5.3% 4.7%7.2% 6.4%

2009E 2010F

� 1H’09 performance favorable vs. plan & stress scenarios� Early and aggressive risk actions paying off� Well positioned for challenging U.S. consumer environment

Credit cost($ in millions)

$5,277 $4,583 $4,836$4,746 $1,680

* Retail Sales Finance and Retail Cards only

55

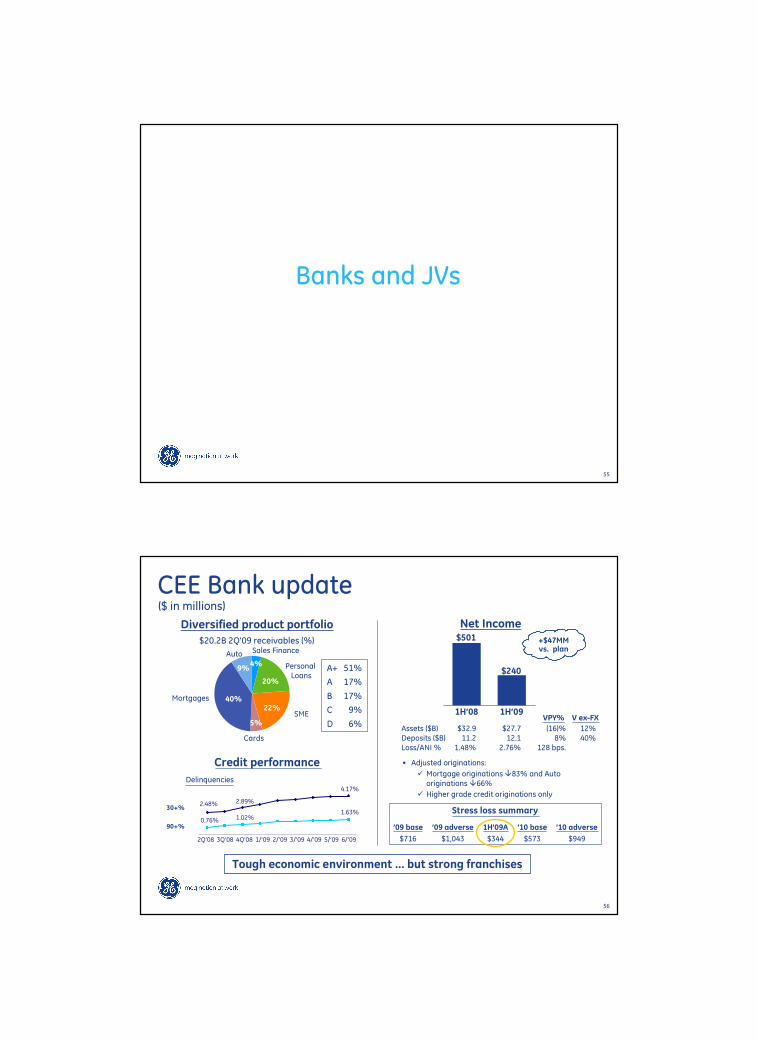

Banks and JVs

56

CEE Bank update

Assets ($B) $32.9 $27.7 (16)% 12%Deposits ($B) 11.2 12.1 8% 40%Loss/ANI % 1.48% 2.76% 128 bps.

1H’09

$240

1H’08

$501

VPY%

Net Income

Tough economic environment … but strong franchises

+$47MMvs. plan

($ in millions)

Diversified product portfolio

$20.2B 2Q’09 receivables (%)

Credit performance

Mortgages

Cards

SME

Personal Loans

Sales FinanceAuto

A+ 51%

A 17%

B 17%

C 9%

D 6%

30+%

90+%

9%4%

20%

22%

5%

40%

2.48% 2.89%

4.17%

0.76% 1.02%1.63%

2Q’08 3Q’08 4Q’08 1/’09 2/’09 3/’09 4/’09 5/’09 6/’09

• Adjusted originations:

� Mortgage originations �83% and Auto originations �66%

� Higher grade credit originations only

V ex-FX

Stress loss summary

’09 base ’09 adverse 1H’09A ’10 base ’10 adverse

$716 $1,043 $344 $573 $949

Delinquencies

57

GECC JVs and partnerships

Investment%

Ownership

2Q’09Inv.($B)

1H’09 GEearnings Strategic rationale/Performance comment

Penske Truck Leasing 50% $6.1 + 21 year partnership; strong brand/franchise

Hyundai – Korea 43% 3.5 + Performance above plan; gaining market share

Garanti Bank – Turkey 21% 2.2 + #3 bank in Turkey; strong margins and loss performance in 1H’09

Bank of Ayudhya – Thailand 33% 1.2 + #4 bank in Thailand; performing above plan

CAMGE – Spain 50% 0.9 + Profitable YTD with lower costs and better loss performance

GE Nissen – Japan 50% 0.8 + Challenged but performing

Dogus GE BV – Romania 50% 0.5 – Banking start-up partnership with Dogus/Garanti in Romania

Colpatria – Colombia 50% 0.4 + Performing above plan

AsiaSat – Hong Kong 37% 0.3 + Steady performance in ’09

Cosmos Bank – Taiwan 23% 0.2 – Remains challenged, performance improvement in 2Q from lowercosts; $110MM 1H impairment recorded

EFS project investments Various 6.5 + Structured equity in energy producing projects; performing to plan

Others Various 3.1 + ~60 small partnerships; ~$55MM avg. investment; $16MM1H impairment recorded

Total associated companies $25.7

� Solid strategic rationale

– Market entry into emerging markets

– Partners bring distribution, domain and capital

(Associated companies)

58

SummaryEnvironment remains challenging – GECC is prepared– Strong funding/liquidity actions and plans

Granular view of stressed losses … working aggressively. Reserves are appropriate and in line with bank peers

Expect profitable 2009 … losses better than Fed base case, more cost-out

Intense focus on risk management,work-out and restructuring– Rigorous GE Capital asset management

Playing offense … originations/margins increasing

GE Capital business model robust … earnings rebound as the economy recovers

22

33

44

11

55

FutureToday

ENI $540B ~$400B

Core55%

Global banks15%

Verticals15%

Restructuring15%

Core &verticals85%

Global banks15%

•More focused GE Capital - competitively advantaged

•Diversified portfolio and funding

66

2%+ ROI

59

GE Context

60

GE 2Q reported results vs. peers

Peer comparison

� Cash flow ahead of plan … $7.1B

� Aggressive cost out … $.06 EPS restructuring and other YTD

� Infrastructure backlog steady at $169B

� Services and global revenues strong

� Margins holding from 1 year ago

� GE Capital safe and secure

2Q V%

GE Infrastructure

S&P Industrials

2Q Highlights

GE Capital

S&P Financials

NBCU

Media peers

Flat

(35%)

(85%)

(75%)

(41%)/(24%)

(42%)

Execution through the recession and positioning for reset economy

a) – 2Q’09 estimated consensus

- a)

61

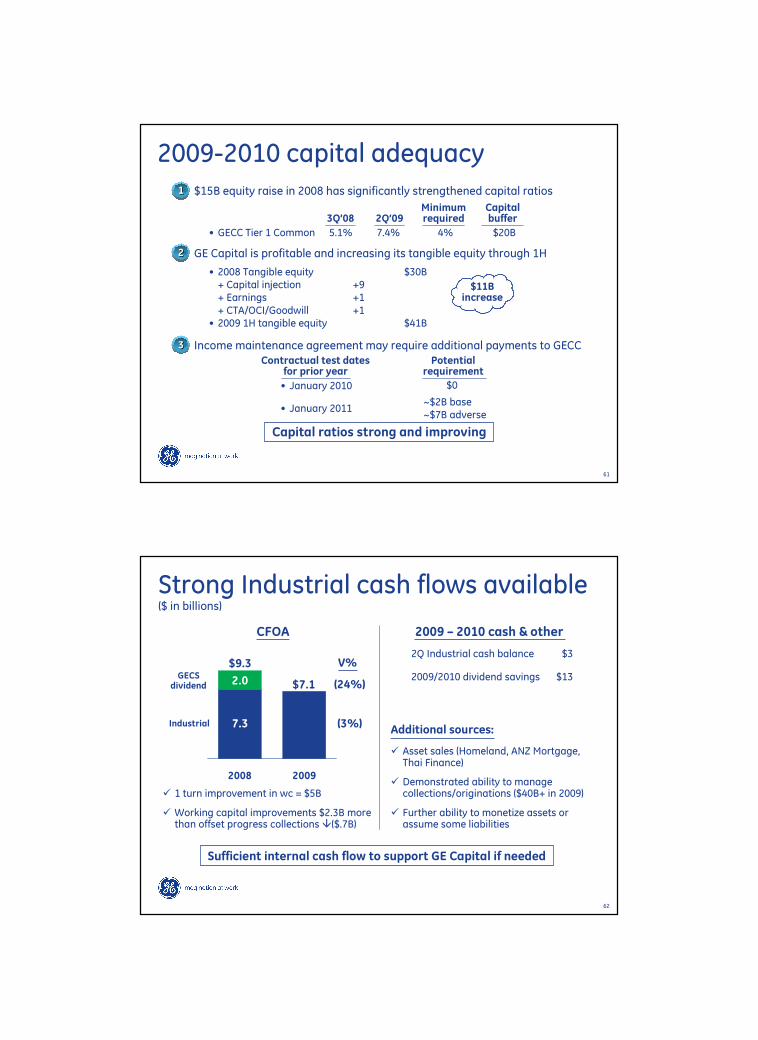

2009-2010 capital adequacy

• $15B equity raise in 2008 has significantly strengthened capital ratios11

3Q’08

• GECC Tier 1 Common 5.1% 7.4% 4% $20B

• January 2010

2Q’09Minimumrequired

Capitalbuffer

• GE Capital is profitable and increasing its tangible equity through 1H22

• 2008 Tangible equity $30B+ Capital injection +9+ Earnings +1+ CTA/OCI/Goodwill +1• 2009 1H tangible equity $41B

$11Bincrease

• Income maintenance agreement may require additional payments to GECC 33

Contractual test datesfor prior year

Potentialrequirement

Capital ratios strong and improving

• January 2011

$0

~$2B base~$7B adverse

62

Strong Industrial cash flows available($ in billions)

2008 2009

CFOA

$9.3

$7.1

7.3

GECSdividend

Industrial (3%)

(24%)

V%

2.0

� 1 turn improvement in wc = $5B

� Working capital improvements $2.3B more than offset progress collections �($.7B)

2009 – 2010 cash & other

Sufficient internal cash flow to support GE Capital if needed

� Asset sales (Homeland, ANZ Mortgage, Thai Finance)

� Demonstrated ability to manage collections/originations ($40B+ in 2009)

� Further ability to monetize assets or assume some liabilities

Additional sources:

2Q Industrial cash balance $3

2009/2010 dividend savings $13

63

Key Messages

GE Capital executing well in difficult environment

• Funding and liquidity are in great shape

– 2009 complete, ~45% of 2010 funding complete, exiting TLGP program

– $50B of cash and CP at $50B is six months ahead of schedule

• Our reserving is adequate and compares to banks when adjusted for mix

– Our reserve coverage is increasing and compares well to ultimate expected loss

– 1H nonearning experience supports our reserving assumptions

• 1H losses below Fed base case and overall cycle losses are manageable

– 2010 loss scenarios could be similar to 2009

– Any additional capital needs at GECC are very manageable with industrial cash flows

• GE is committed to GE Capital business model

– Investors can expect a conservative, focused and competitively advantaged GECC

– Financial services “white paper” does not change our strategy

![Investor Presentation - Analyst / Institutional Investor Meeting [Company Update]](https://static.fdocuments.in/doc/165x107/577c98301a28ab163a8b4855/investor-presentation-analyst-institutional-investor-meeting-company-update.jpg)