GD Express Carrier Berhad Initiate Coverage with BUY - MIDF · MIDF RESEARCH is a unit of MIDF...

15

MIDF RESEARCH is a unit of MIDF AMANAH INVESTMENT BANK Kindly refer to the last page of this publication for important disclosures 13 December 2016 | Initiate Coverage GD Express Carrier Berhad Initiate Coverage with BUY Going the last mile with GDEX Target Price (TP): RM2.06 INVESTMENT HIGHLIGHTS • GDEX is a market leader in domestic express delivery • Profits are forecasted to increase at a 3-yr CAGR of 16% • The company is a beneficiary of e-commerce growth • We initiate coverage with a BUY call and TP of RM2.06 Market leader in express delivery. According to our analysis, GDEX is ranked second in terms of domestic express delivery market share holding an 18% share. GDEX has outpaced the overall industry which expanded at a CAGR of 10% between 2012 and 2015, increasing its market share by 0.4ppt per year. Growing in tandem with the e-commerce industry. We are forecasting a 3-year FY17-FY19 profit CAGR of 16% contributed by: i) Fast growing e-commerce industry which is entering the growth phase of the industry life cycle, with CAGR estimated at 20.8% between 2015 and 2020. As an express delivery partner appointed by key e-commerce platforms, GDEX is poised to benefit from increasing parcel volumes. ii) Expansion in sorting capacity. We estimate that GDEX will expand its sorting capacity by 28%/30%/15% in FY17/FY18/FY19. The company is undergoing several initiatives to increase its sorting capacity at reasonable capital outlay, including reorganising the layout of its 67k sq. ft. HQ/sorting hub and investing in new semi- automated sorting lines. iii) M&A opportunities. GDEX has RM282m in dry powder and is prepared to deploy its net cash into value enhancing and synergistic assets. GDEX has already invested RM5.5m for a 30% stake in Web Bytes Sdn Bhd (Web Bytes) to enhance its technological offering to fend off new tech-based delivery start-ups. Initiate coverage with BUY and TP of RM2.06. We value the company using the discounted cash flow method (DCF). GDEX has consistently achieved PBT margins of 15-16% which are on average 10ppts higher compared to its peers. While our TP implies a forward price-to-earnings (PER) of 70x FY17 core earnings, we believe it is justified as GDEX is a beneficiary of the high growth e-commerce sector. RETURN STATS Price (9 Dec 2016) RM1.73 Target Price RM2.06 Expected Share Price Return +19.1% Expected Dividend Yield +0.3% Expected Total Return +19.4% STOCK INFO KLCI 1,641.42 Bursa / Bloomberg 0078/ GDX MK Board / Sector Main/ Trading Services Syariah Compliant Yes Issued shares (mil) 1,383.24 Par Value (RM) 0.05 Market cap. (RM’m) 2,393.00 Price over NA 6.06 52-wk price Range RM1.46 - RM1.8 Beta (against KLCI) 0.93 3-mth Avg Daily Vol 0.25m 3-mth Avg Daily Value RM0.42m Major Shareholders Mr. Teong Teck Lean 37.98% Yamato 22.85% Singpost 11.23%

Transcript of GD Express Carrier Berhad Initiate Coverage with BUY - MIDF · MIDF RESEARCH is a unit of MIDF...

MIDF RESEARCH is a unit of MIDF AMANAH INVESTMENT BANK

Kindly refer to the last page of this publication for important disclosures

13 December 2016 | Initiate Coverage

GD Express Carrier Berhad Initiate Coverage with BUY

Going the last mile with GDEX Target Price (TP): RM2.06

INVESTMENT HIGHLIGHTS

• GDEX is a market leader in domestic express delivery

• Profits are forecasted to increase at a 3-yr CAGR of 16%

• The company is a beneficiary of e-commerce growth

• We initiate coverage with a BUY call and TP of RM2.06

Market leader in express delivery. According to our analysis, GDEX is

ranked second in terms of domestic express delivery market share

holding an 18% share. GDEX has outpaced the overall industry which

expanded at a CAGR of 10% between 2012 and 2015, increasing its

market share by 0.4ppt per year.

Growing in tandem with the e-commerce industry. We are

forecasting a 3-year FY17-FY19 profit CAGR of 16% contributed by:

i) Fast growing e-commerce industry which is entering the growth

phase of the industry life cycle, with CAGR estimated at 20.8%

between 2015 and 2020. As an express delivery partner appointed

by key e-commerce platforms, GDEX is poised to benefit from

increasing parcel volumes.

ii) Expansion in sorting capacity. We estimate that GDEX will

expand its sorting capacity by 28%/30%/15% in FY17/FY18/FY19.

The company is undergoing several initiatives to increase its sorting

capacity at reasonable capital outlay, including reorganising the

layout of its 67k sq. ft. HQ/sorting hub and investing in new semi-

automated sorting lines.

iii) M&A opportunities. GDEX has RM282m in dry powder and is

prepared to deploy its net cash into value enhancing and synergistic

assets. GDEX has already invested RM5.5m for a 30% stake in Web

Bytes Sdn Bhd (Web Bytes) to enhance its technological offering to

fend off new tech-based delivery start-ups.

Initiate coverage with BUY and TP of RM2.06. We value the

company using the discounted cash flow method (DCF). GDEX has

consistently achieved PBT margins of 15-16% which are on average

10ppts higher compared to its peers. While our TP implies a forward

price-to-earnings (PER) of 70x FY17 core earnings, we believe it is

justified as GDEX is a beneficiary of the high growth e-commerce sector.

RETURN STATS

Price (9 Dec 2016) RM1.73

Target Price RM2.06

Expected Share Price Return

+19.1%

Expected Dividend Yield +0.3%

Expected Total Return

+19.4%

STOCK INFO

KLCI 1,641.42

Bursa / Bloomberg 0078/

GDX MK

Board / Sector Main/ Trading

Services

Syariah Compliant Yes

Issued shares (mil) 1,383.24

Par Value (RM) 0.05

Market cap. (RM’m) 2,393.00

Price over NA 6.06

52-wk price Range RM1.46 - RM1.8

Beta (against KLCI) 0.93

3-mth Avg Daily Vol 0.25m

3-mth Avg Daily Value RM0.42m

Major Shareholders

Mr. Teong Teck Lean 37.98%

Yamato 22.85%

Singpost 11.23%

MIDF RESEARCH Tuesday, 13 December 2016

2

INVESTMENT STATISTICS

FYE Dec FY15A FY16A FY17F FY18F FY19F

Revenue (RM’m) 196.8 219.8 257.1 297.0 346.0

EBIT (RM’m) 32.7 41.7 49.9 57.0 65.9

Pre-tax Profit (RM’m) 31.3 40.2 47.3 54.0 62.4

Core PAT (RM’m) 28.3 34.4 40.7 46.5 53.7

FD EPS (sen) 1.8 2.2 2.6 3.0 3.4

EPS growth (%) -30.7 21.7 18.1 14.3 15.5

PER(x) 92.8 76.2 64.5 56.5 48.9

Net Dividend (sen) 3.2 3.2 4.9 5.9 6.7

Net Dividend Yield (%) 0.5 0.5 0.3 0.3 0.2

Source: Company, MIDF Research

Source: Bloomberg

DAILY PRICE CHART

Tay Yow Ken, CFA [email protected]

03-2173 8384

MIDF RESEARCH Tuesday, 13 December 2016

3

A. KEY INVESTMENT MERITS

Growing its slice of the pie. We estimate that GDEX has steadily increased its market share among domestic

express delivery players, growing its market share by 1.2ppt annually between 2012 and 2015. The expansion of

market share is commendable, considering the overall industry grew by a compounded annual growth rate (CAGR) of

10% from RM727m to RM1.05b. This indicates that the company was able to propel itself ahead of competitors while

keeping pace with overall market growth. In addition, profitability margins have not been sacrificed in favour of

market share gains as pricing remained stable and costs contained.

Figure 1: Market share growth (2012-2015)

(Sources: Companies, MIDF Research)

Figure 2: Domestic express delivery companies’ market share (2015) and revenue & PBT margin trends

Note 1: International express delivery players such as DHL, FedEX and UPS are not included as a substantial portion of their revenue is derived

from international freight. Meanwhile, it is common for these players to outsource last mile delivery services to domestic players.

Note 2: Excludes interest income.

(Sources: Companies, MIDF Research)

37.9% 41.3% 43.7% 46.0%

16.8% 17.0% 17.5% 18.0%

45.3% 41.7% 38.8% 36.1%

0%

25%

50%

75%

100%

2012 2013 2014 2015

Others

GDEX

Pos Laju

RM824m RM933m RM1.05bRM727m

Pos Laju

46%

GDEX

18%

City-Link

15%

ABX

4%

Nationwide

9%

Skynet

8%

14%

15%

16%

15%*

13%

14%

14%

15%

15%

16%

16%

17%

0

50,000

100,000

150,000

200,000

250,000

FY2013 FY2014 FY2015 FY2016

Revenue (RM'000) PBT margin (%)

MIDF RESEARCH Tuesday, 13 December 2016

4

E-commerce (B2C) the growth engine. GDEX is well positioned to grow in tandem with the e-commerce industry

in Malaysia having derived 25% of its FY16 revenue from the segment. According to MITI and MDEC, e-commerce is

entering the growth phase of the industry life cycle. This suggests that the industry possesses ample mileage in terms

of growth potential, with a forecasted 5-year CAGR of 20.8% between 2015 and 2020. As an express delivery partner

appointed by key e-commerce platforms, GDEX is presented with the opportunity to benefit from the need to fulfil a

higher number of parcel deliveries.

Figure 4: Growth of GDEX’s key clientele for its e-commerce segment

Astro Go Shop 4QFY15 1QFY16 2QFY16 3QFY16 4QFY16 1QFY17 1HFY17

Revenue 25,000,000 37,000,000 38,000,000 52,000,000 62,000,000 63,900,000 74,100,000

Growth qoq (%)

48% 3% 37% 19% 3% 16%

Compounded quarterly rate 17%

Products sold 120,000 175,000 220,000 257,000 331,000 350,000 440,000

Growth qoq (%)

46% 26% 17% 29% 6% 26%

Compounded quarterly rate 20%

Lazada (USD$'m) FY13 FY14 FY15

GMV* 95 384 1,025

Growth yoy (%) N/A 305% 167%

Revenue 76 154 275

Growth yoy (%) N/A 104% 78%

Zalora (EUR'm) FY13 FY14 FY15

GMV 84 152 274

Growth yoy (%) N/A 80% 81%

Revenue 69 117 208

Growth yoy (%) N/A 70% 77%

Note: Figures for Lazada and Zalora include other Asian markets but is reflective of the Malaysian operations as one of the largest contributors.

(Sources: Astro, Rocket Internet, MIDF Research)

Figure 3: Malaysia e-commerce industry life cycle

(Sources: MITI, MDEC, MIDF Research)

E-commerce in Malaysia is at an inflection point, undergoing

a transformation from the introduction phase of the

industry life cycle into the growth phase, characterised

by accelerating sales and the

entry of new platforms.

Introduction Growth Mature Declining

Singapore,

China

US, Korea

Malaysia

E-commerce platform clients include

Astro Go Shop, Lazada, Zalora, 11Street, Gemfive and CJ Wow Shop which

recorded RM18.6m revenue in its maiden reporting quarter.

*Gross Merchandise Revenue (GMV)

MIDF RESEARCH Tuesday, 13 December 2016

5

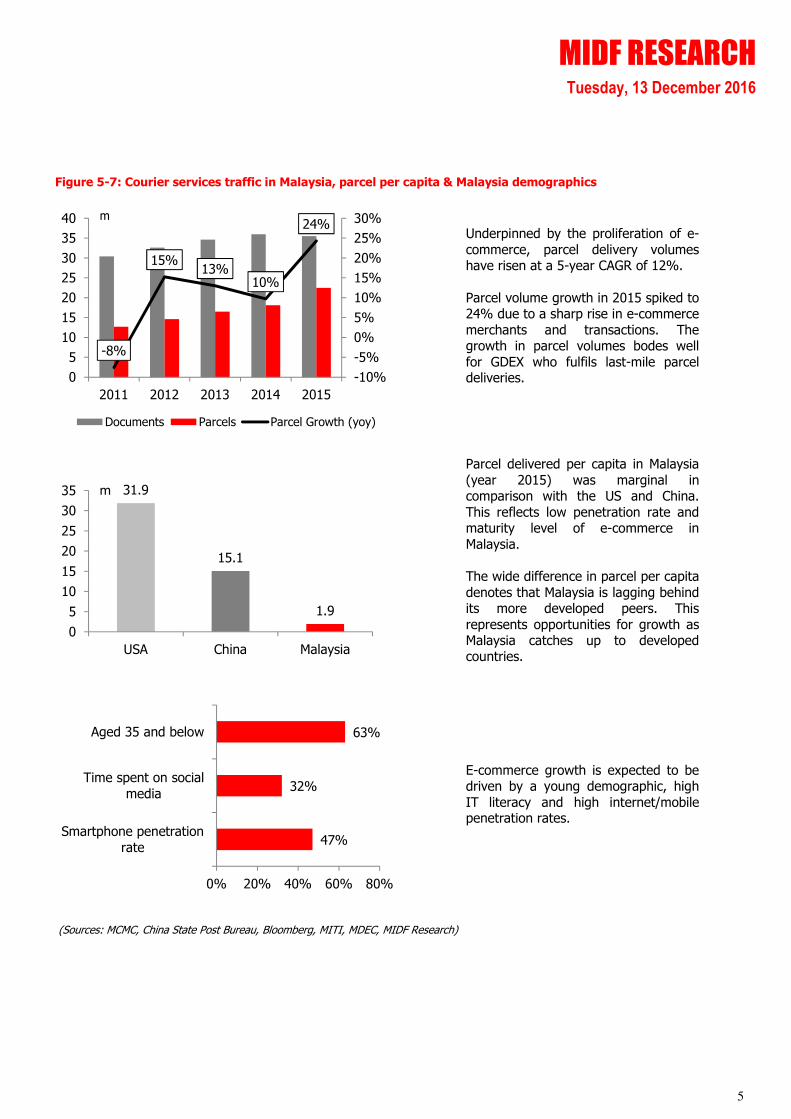

Figure 5-7: Courier services traffic in Malaysia, parcel per capita & Malaysia demographics

(Sources: MCMC, China State Post Bureau, Bloomberg, MITI, MDEC, MIDF Research)

-8%

15%13%

10%

24%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

0

5

10

15

20

25

30

35

40

2011 2012 2013 2014 2015

Documents Parcels Parcel Growth (yoy)

m

Underpinned by the proliferation of e-

commerce, parcel delivery volumes have risen at a 5-year CAGR of 12%.

Parcel volume growth in 2015 spiked to 24% due to a sharp rise in e-commerce

merchants and transactions. The growth in parcel volumes bodes well

for GDEX who fulfils last-mile parcel deliveries.

Parcel delivered per capita in Malaysia

(year 2015) was marginal in comparison with the US and China.

This reflects low penetration rate and maturity level of e-commerce in

Malaysia.

The wide difference in parcel per capita

denotes that Malaysia is lagging behind its more developed peers. This

represents opportunities for growth as Malaysia catches up to developed countries.

31.9

15.1

1.9

0

5

10

15

20

25

30

35

USA China Malaysia

m

47%

32%

63%

0% 20% 40% 60% 80%

Smartphone penetration

rate

Time spent on social

media

Aged 35 and below

E-commerce growth is expected to be driven by a young demographic, high

IT literacy and high internet/mobile penetration rates.

MIDF RESEARCH Tuesday, 13 December 2016

6

Express delivery partner model. GDEX differs from its peers by deriving the bulk of its parcel delivery revenue

from contracts with e-commerce platforms as opposed to retail customers (e.g. walk-in customers and individual e-

commerce merchants). The appointment as an express delivery partner allows GDEX to secure a higher quantity of

parcel volumes, which enables GDEX it to reduce unit costs through achieving better economies of scale.

Premium pricing through enhanced service offering. The company is constantly improving its reliability,

timeliness, customer service, range of services and technology. This has led to GDEX offering better service quality

and hence the ability to charge a premium in pricing. For example, GDEX offers cash on delivery (COD), same day

delivery and warehousing services which are not widely offered by competitors. As a result, GDEX is able to enjoy

higher PBT margins of 15-16% compared to its peer average of 4.5-6.5%.

Shaking off competition from start-ups. While there has been an influx of start-up express delivery firms

entering the market such as Ninjavan, Neonrunner and Zyllem which run app-based services, incumbents possess

several competitive advantages. Years of investments into sorting equipment, trucks and IT infrastructure have

allowed incumbents to handle significantly higher parcel volumes. This leads to lower unit cost, network reach

(especially in rural areas) and the ability to ramp-up capacity to meet peak season demand. Hence, we opine that

incumbents would be able to withstand the threat of new competition.

Figure 8-9: Contract vs. walk-in customer mix

(Sources: Company, MIDF Research)

Contract

80%

Retail

20%

GDEX

Contract

40%

Retail

60%

Peers

16% 16% 15% 16%

6.2% 5.7%4.5%

6.5%

0%

5%

10%

15%

20%

FY2013 FY2014 FY2015 FY2016

GDEX Express Delivery PBT margin (%) PBT margin peers (%)

MIDF RESEARCH Tuesday, 13 December 2016

7

Bottlenecks will be a thing of the past. Having witnessed a surge in demand in FY16 from the e-commerce

segment, the company’s average utilisation rate for its sorting facility rose to 90%. At times, the company faced

difficulty in coping with the large volume of orders, with sorting capacity stretched 10% above its designed capacity.

This occurred during promotional periods such as the #MYCYBERSALE campaign which saw a GMV of RM211m

(79%yoy increase) transacted over a period of only 5 days. To better prepare itself in handling such surges in volume,

GDEX has taken measures to increase its sorting capacity by 28%/30%/15% in FY17/FY18/FY19.

Scaling up at a reasonable cost. GDEX is undergoing several initiatives to increase its sorting capacity at

reasonable capital outlay. This includes reorganising the layout of its 67k sq. ft. HQ/sorting hub in PJ to maximise the

use of space, converting an empty parking lot into a loading bay, investing in semi-automated sorting lines, improving

the sorting process and conducting sorting at a number its 66 branches before delivery to its PJ hub. These

improvements are cost effective, expeditious and at minimal disruption to operations compared to developing an

entirely new facility. Meanwhile, management is looking to acquire a new parcel of land in the Klang Valley to build a

new international sorting hub in FY18-FY19.

Figure 10-11: Parcel sorting capacity & vehicle fleet

(Sources: Company, MIDF Research)

0%

20%

0% 8%

28%

30%

15%

0%

10%

20%

30%

40%

50%

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

FY13 FY14 FY15 FY16 FY17 FY18 FY19

Parcel sorting capacity (daily) Growth yoy (%)

19%

14%

28%

13%

19%14%

12%

0%

10%

20%

30%

40%

50%

0

200

400

600

800

1,000

1,200

FY13 FY14 FY15 FY16 FY17 FY18 FY19

Number of vehicles Growth yoy (%)

Management aims to

increase its vehicle fleet size by more than 10% p.a. by

allocating 40% of its yearly

capex budget to increase its delivery capacity.

The remaining 20% is

allocated for GDEX’s warehousing business. It

currently operates 130k sq.

ft. of warehouse space which is close to being fully

utilised

Parcel sorting capacity is set to rise by a CAGR of 17%

between FY16 and FY19 with capex allocation of

40%.

RM30m CAPEX budget for FY17 (73% of

FY16 CFO).

MIDF RESEARCH Tuesday, 13 December 2016

8

Resilient earnings from the conventional B2B business. With 25% of FY16 revenue derived from the rapidly

expanding e-commerce segment, the bulk or 75% of revenue still comprises of its bread and butter B2B business

which entails the express delivery of documents. GDEX has garnered a portfolio of clients consisting of major banks,

manufacturers, hospitals, telecommunication players as well as over 50,000 SMEs. While the segment is not expected

to grow as rapidly as the e-commerce segment due to migrations to cloud storage, the segment will still grow in line

with increased outsourcing activity for the transportation of documents.

On the hunt for more acquisitions. GDEX has a war chest of RM282m and is prepared to deploy this net cash into

value enhancing and synergistic assets. GDEX has already invested RM5.5m for a 30% stake in Web Bytes Sdn Bhd

(Web Bytes) which provides cloud based Retail Management Solutions (e.g. point of sales and inventory management

systems) through its Xilnex Brand. We believe more acquisitions could be on the cards for express delivery players,

integrated logistics businesses or warehouse/industrial land.

Adding value through tech. While the Web Bytes deal is not expected to immediately provide visible returns, we

understand that GDEX and Web Bytes will be co-developing software/mobile applications to enhance GDEX’s product

features such as offering real-time tracking, seamless creation of delivery orders and providing notifications direct to

mobile. These new features would increase GDEX’s competitiveness in facing technology-based competitors as well as

increasing its presence in the retail segment where it currently only derives 20% of its express delivery revenue.

Reputable strategic shareholders. Having displayed growth and efficiency, GDEX has attracted the likes of

Yamato Holdings Co Ltd (Yamato, 22.8% stake) and Singapore Post Ltd (Singpost, 11.2% stake) to as its strategic

shareholders. The former, Yamato, which purchased GDEX shares at RM1.74, is Japan’s largest and fifth globally in

terms of express delivery revenue. Thus far, Yamato’s involvement in GDEX has been confined to providing technical

and strategic advice. Moving forward, we believe it is likely that business collaborations, such as channelling parcel

volumes, cross border trucking and fresh produce deliveries could be established.

The Alibaba connection. It is worth noting that the world’s largest e-commerce player Alibaba holds an indirect

stake in GDEX via Singpost thus giving GDEX an advantage over its competitors when bidding for business. Moreover,

Alibaba has bought over Lazada, one of GDEX’s largest customers.

Figure 12-13: Web Bytes acquisition & GDEX strategic shareholders

(Sources: Company, MIDF Research)

RM5.5m to purchase 30% in Web Bytes to enhance GDEX’s tech offerings.

22.84% 11.23%

10.17% 30%

MIDF RESEARCH Tuesday, 13 December 2016

9

B. VALUATION

Initiate coverage with a BUY recommendation based on fully diluted TP of RM2.06. We initiate coverage

on GDEX with a BUY call and TP of RM2.06. Our valuation is derived from our discounted-cash flow (DCF) model

which assumes WACC of 8.5% and terminal growth rate of 3%.

Our TP indicates potential capital upside of +24%. GDEX has consistently achieved PBT margins of 15-16%

which are on average 10ppts higher compared to its peers due to its efficient cost structure and premium pricing

arising from value enhanced service offering. While our TP implies a forward Price-to-Earnings (PER) of 70x FY17 core

earnings, we believe it is justified as GDEX is a beneficiary of the high growth e-commerce sector. In addition, the

current share price of RM1.73 remains below Yamato’s entry price of RM1.74.

Figure 14: DCF valuation for GDEX

FYE June FY2017 FY2018 FY2019 FY2020 FY2021… FY2027

EBIT multiplied (1-tax rate) 56,843 64,998 75,077 79,582 84,357 119,661

Less: Capex -30,000 -25,000 -20,000 -15,000 -15,000 -15,000

Add: Depreciation 10,285 11,879 13,839 13,529 15,184 21,539

FCF 37,127 51,877 68,916 78,111 84,541 126,200

Sum of PV FCF 565,767

PV of terminal value 2,363,391

Enterprise value 2,929,157

Add: Net cash 295,223

Add: Cash from conversion of warrants 274,105

Total equity value 3,224,380

# of shares outstanding 1,383,240

# of warrant outstanding 179,154

Target price 2.06

Current price 1.73

Upside (%) 19.4%

WACC 8.5%

Terminal growth rate 3%

(Source: MIDF Research)

MIDF RESEARCH Tuesday, 13 December 2016

10

C. FINANCIAL HIGHLIGHTS

PAT forecasted to expand at a 3-year CAGR of 16%. Growth will be driven by the e-commerce segment which

is expected to grow at a similar CAGR. In addition, GDEX has shown that it is able to win market share from

competitors. The on-going expansion of its sorting capacity, vehicle fleet and warehouses would enable this growth.

In addition, we expect PAT margins to remain steady at over 15% despite the threat of new competitors as GDEX is

itself improving its service offering.

Consistent free cash flows despite capex drive. We forecast GDEX to continue generating free cash flow (FCF)

in FY17-FY19 despite capex drive to ramp up sorting capacity, warehousing space and vehicle fleet. GDEX has shown

good FCF generation, with RM43m made available to equity owners in FY16 translating into an FCF yield of 1.9%. We

do not rule our higher dividend payments in the future after it embarks on its capex drive putting its net cash pile of

RM282m into use.

Figure 15: GDEX revenue and PAT

(Sources: Company, MIDF Research)

Figure 16: Annual capex and net gearing

(Sources: Company, MIDF Research)

196,751219,757

257,116

296,969

345,969

28,296 34,444 40,670 46,480 53,662

21% 22%

18%

14% 15%

0%

5%

10%

15%

20%

25%

30%

35%

40%

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

FY15 FY16 FY17F FY18F FY19F

Revenue PAT PAT Growth (yoy)

13,645 17,033

1,205

43,447

9,99421,347

32,867

-5,100 -4,207 -7,010 -3,797

-30,000-25,000

-20,000-40,000

-20,000

0

20,000

40,000

60,000

FY2013 FY2014 FY2015 FY2016 FY2017 FY2018 FY2019

FCF Capex

MIDF RESEARCH Tuesday, 13 December 2016

11

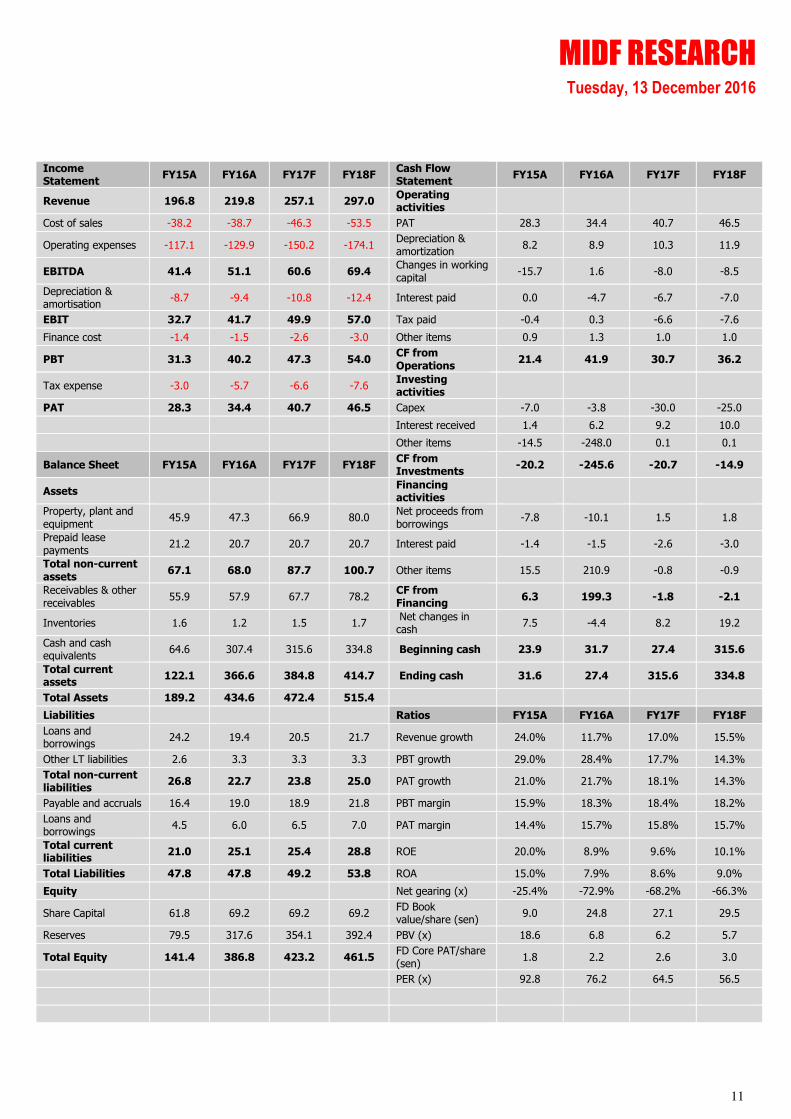

Income Statement

FY15A FY16A FY17F FY18F Cash Flow Statement

FY15A FY16A FY17F FY18F

Revenue 196.8 219.8 257.1 297.0 Operating activities

Cost of sales -38.2 -38.7 -46.3 -53.5 PAT 28.3 34.4 40.7 46.5

Operating expenses -117.1 -129.9 -150.2 -174.1 Depreciation & amortization

8.2 8.9 10.3 11.9

EBITDA 41.4 51.1 60.6 69.4 Changes in working capital

-15.7 1.6 -8.0 -8.5

Depreciation & amortisation

-8.7 -9.4 -10.8 -12.4 Interest paid 0.0 -4.7 -6.7 -7.0

EBIT 32.7 41.7 49.9 57.0 Tax paid -0.4 0.3 -6.6 -7.6

Finance cost -1.4 -1.5 -2.6 -3.0 Other items 0.9 1.3 1.0 1.0

PBT 31.3 40.2 47.3 54.0 CF from Operations

21.4 41.9 30.7 36.2

Tax expense -3.0 -5.7 -6.6 -7.6 Investing activities

PAT 28.3 34.4 40.7 46.5 Capex -7.0 -3.8 -30.0 -25.0

Interest received 1.4 6.2 9.2 10.0

Other items -14.5 -248.0 0.1 0.1

Balance Sheet FY15A FY16A FY17F FY18F CF from Investments

-20.2 -245.6 -20.7 -14.9

Assets

Financing activities

Property, plant and equipment

45.9 47.3 66.9 80.0 Net proceeds from borrowings

-7.8 -10.1 1.5 1.8

Prepaid lease payments

21.2 20.7 20.7 20.7 Interest paid -1.4 -1.5 -2.6 -3.0

Total non-current assets

67.1 68.0 87.7 100.7 Other items 15.5 210.9 -0.8 -0.9

Receivables & other receivables

55.9 57.9 67.7 78.2 CF from Financing

6.3 199.3 -1.8 -2.1

Inventories 1.6 1.2 1.5 1.7 Net changes in cash

7.5 -4.4 8.2 19.2

Cash and cash equivalents

64.6 307.4 315.6 334.8 Beginning cash 23.9 31.7 27.4 315.6

Total current assets

122.1 366.6 384.8 414.7 Ending cash 31.6 27.4 315.6 334.8

Total Assets 189.2 434.6 472.4 515.4

Liabilities

Ratios FY15A FY16A FY17F FY18F

Loans and borrowings

24.2 19.4 20.5 21.7 Revenue growth 24.0% 11.7% 17.0% 15.5%

Other LT liabilities 2.6 3.3 3.3 3.3 PBT growth 29.0% 28.4% 17.7% 14.3%

Total non-current liabilities

26.8 22.7 23.8 25.0 PAT growth 21.0% 21.7% 18.1% 14.3%

Payable and accruals 16.4 19.0 18.9 21.8 PBT margin 15.9% 18.3% 18.4% 18.2%

Loans and borrowings

4.5 6.0 6.5 7.0 PAT margin 14.4% 15.7% 15.8% 15.7%

Total current liabilities

21.0 25.1 25.4 28.8 ROE 20.0% 8.9% 9.6% 10.1%

Total Liabilities 47.8 47.8 49.2 53.8 ROA 15.0% 7.9% 8.6% 9.0%

Equity

Net gearing (x) -25.4% -72.9% -68.2% -66.3%

Share Capital 61.8 69.2 69.2 69.2 FD Book value/share (sen)

9.0 24.8 27.1 29.5

Reserves 79.5 317.6 354.1 392.4 PBV (x) 18.6 6.8 6.2 5.7

Total Equity 141.4 386.8 423.2 461.5 FD Core PAT/share (sen)

1.8 2.2 2.6 3.0

PER (x) 92.8 76.2 64.5 56.5

MIDF RESEARCH Tuesday, 13 December 2016

12

D. INVESTMENT RISKS

Severe recession. GDEX is involved in the delivery of documents and parcels between businesses (B2B) and

between businesses and end-users (B2C). GDEX is relatively insulated from business cycles due to the majority of

revenue being derived from B2B document transportation. However, a severe and prolonged downturn caused by

changes in economic and geopolitical conditions may hamper the company’s business. Protracted economic

uncertainty may cause businesses to downsize, hence reducing the requirement of document transportation.

Shortage of workers. GDEX is dependent a skilled force of drivers to operate its fleet of 654 trucks. At present,

GDEX has a workforce of 3,000 employees. Drivers perform daily deliveries following routes mapped out by GDEX’s

proprietary software to ensure efficiency and timeliness. A shortage of skilled drivers would adversely impact the

company’s operations in fulfilling pick-ups and deliveries. In addition, increases in minimum wage or delays in

obtaining driver permits could increase GDEX’s operating expenses or hinder operations.

E-commerce falling out of favour with consumers. The proliferation of e-commerce has allowed consumers to

make purchases at the convenience of their personal computers or mobile devices. With this convenience, the sector

has grown by leaps and bounds, benefitting parcel delivery players such as GDEX. A change in preference of

consumers or a large shift back to brick and mortar shopping would reduce the volume of parcels required to be

delivered. This would negatively impact GDEX which relies on the e-commerce sector for growth.

Intense competition from existing and new competitors. The entry of multiple competitors with large financial

backing could be a threat to GDEX. Competitors who are able to reduce prices in favour of market share would result

in reduced yields and intense bidding for contracts by e-commerce platforms. This would be unfavourable for GDEX

and could reduce its profitability margins. Start-ups with more advanced technology could also pose a threat, giving e-

commerce platforms or retail clients more options with differentiated services. Cognisant of this, GDEX has invested in

a software company to assist it in developing and enhancing its technology capabilities.

MIDF RESEARCH Tuesday, 13 December 2016

13

E. APPENDIX

GD Express Carrier Berhad (GDEX) is principally provides last mile express delivery and logistics services. The

company is currently one of company is currently one of the largest express delivery companies in Malaysia operating

from its 67k sq. ft. all-weather central clearing hub in Petaling Jaya. GDEX adopts a “Hub & Spoke” distribution

system through a comprehensive domestic network comprising of 211 stations. These include 1 sorting HQ, 66

branches, 1 affiliate station, 54 agents, 23 lodge-in centres and 67 reseller agencies.

Figure 17: Group structure

Figure 18: Corporate History

Established in

1996, but ran into difficulties

triggered by 1997 financial

crisis 2000 Entry of Teong Teck Lean as

controlling shareholder of

GDEX

2003 First local

express delivery company to

obtain ISO 9001: 2000

(Quality Management System)

2005 Successfully

listed GDEX on ACE MARKET of Bursa Malaysia

2008 First local

express carrier to deploy

conveyor systems for

both parcel and document sorting

2011 Entry of Singapore Post

as substantial shareholder

2013 Successfully transferred

listing to MAIN

MARKET of Bursa Malaysia

GD Venture (M) Sdn Bhd

GD Technosystem Sdn Bhd

GD Facilities and Assets Management Sdn Bhd

GD Logistics (M) Sdn Bhd

GD Express (Singapore) Pte Ltd

GDEX Regional Alliance Pte Ltd

GD Valueguard Sdn Bhd

GD Express Sdn Bhd

100%

100%

100%

100% 100%

100%

100%

100%

GD Express Carrier Bhd

MIDF RESEARCH Tuesday, 13 December 2016

14

Figure 19: Express delivery and logistics operational flow

Figure 20: Sorting hub & spoke distribution model

Customer calls GDEX Customer

Service for a pick-up service

GDEX assigns dispatch to pick-up shipments and bring them back to the GDEX station

Shipments from station are directed to the GDEX HQ Hub

The shipments are sorted and distributed at the GDEX HQ

hub

The sorted shipments are sent to the

designated GDEX stations

Shipments delivered to recipient

Customer delivers bulk materials to

GDEX warehouse

These materials are sorted systematically and repacked into customised GDEX

boxes

The boxes are sealed and addressed to the recipients

The boxes are sent to the GDEX

HQ Hub for sorting and distribution

The sorted boxes are sent to

designated GDEX stations

The boxes are then sent to the recipients

Customers Suppliers Intermediaries

Customer Driven

Shipper A

Shipper B

Shipper C

Receiver A

Receiver B

Receiver C

MIDF RESEARCH Tuesday, 13 December 2016

15

MIDF RESEARCH is part of MIDF Amanah Investment Bank Berhad (23878 - X).

(Bank Pelaburan)

(A Participating Organisation of Bursa Malaysia Securities Berhad)

DISCLOSURES AND DISCLAIMER

This report has been prepared by MIDF AMANAH INVESTMENT BANK BERHAD (23878-X). It is for

distribution only under such circumstances as may be permitted by applicable law.

Readers should be fully aware that this report is for information purposes only. The opinions contained

in this report are based on information obtained or derived from sources that we believe are reliable.

MIDF AMANAH INVESTMENT BANK BERHAD makes no representation or warranty, expressed or

implied, as to the accuracy, completeness or reliability of the information contained therein and it should

not be relied upon as such.

This report is not, and should not be construed as, an offer to buy or sell any securities or other

financial instruments. The analysis contained herein is based on numerous assumptions. Different

assumptions could result in materially different results. All opinions and estimates are subject to change

without notice. The research analysts will initiate, update and cease coverage solely at the discretion of

MIDF AMANAH INVESTMENT BANK BERHAD.

The directors, employees and representatives of MIDF AMANAH INVESTMENT BANK BERHAD may have

interest in any of the securities mentioned and may benefit from the information herein. Members of the

MIDF Group and their affiliates may provide services to any company and affiliates of such companies

whose securities are mentioned herein This document may not be reproduced, distributed or published

in any form or for any purpose.

MIDF AMANAH INVESTMENT BANK : GUIDE TO RECOMMENDATIONS

STOCK RECOMMENDATIONS

BUY Total return is expected to be >15% over the next 12 months.

TRADING BUY Stock price is expected to rise by >15% within 3-months after a Trading Buy rating has been

assigned due to positive newsflow.

NEUTRAL Total return is expected to be between -15% and +15% over the next 12 months.

SELL Total return is expected to be <-15% over the next 12 months.

TRADING SELL Stock price is expected to fall by >15% within 3-months after a Trading Sell rating has been assigned due to negative newsflow.

SECTOR RECOMMENDATIONS

POSITIVE The sector is expected to outperform the overall market over the next 12 months.

NEUTRAL The sector is to perform in line with the overall market over the next 12 months.

NEGATIVE The sector is expected to underperform the overall market over the next 12 months.

![Amanah Saham Nasional Berhad (ASNB) - MASTER ......ASB 3 Didik : Amanah Saham Bumiputera 3 – Didik [formerly kown as Amanah Saham Didik] ASN : Amanah Saham Nasional ASN Imbang 1](https://static.fdocuments.in/doc/165x107/611a65731f6af02a78680513/amanah-saham-nasional-berhad-asnb-master-asb-3-didik-amanah-saham.jpg)