GCHP Housing Finance, Inc. -...

16

GCHP HOUSING FINANCE. INC. CONSOLIDATED FINANCIAL STATEMENTS DECEMBER 31.2013 and 2012 iJSAi Postlethwaite & Netterville A Professional Accounting Corporation www.pncpa.com

Transcript of GCHP Housing Finance, Inc. -...

GCHP HOUSING FINANCE. INC.

CONSOLIDATED FINANCIAL STATEMENTS

DECEMBER 31.2013 and 2012

iJSAi Postlethwaite & Netterville

A Professional Accounting Corporation

www.pncpa.com

GCHP HOUSING FINANCE, INC.

CONSOLroATED FINANCIAL STATEMENTS

DECEMBER 31,2013 and 2012

GCHP HOUSING FINANCE INC.

DECEMBER 31, 2013 and 2012

TABLE OF CONTENTS

Page

INDEPENDENT AUDITORS' REPORT 1

FINANCIAL STATEMENTS

Consolidated Statements of Financial Position 3

Consolidated Statements of Activities 4

Consolidated Statements of Cash Flows 5

Notes to Consolidated Financial Statements 6

liiSAi Postlethwaite & Netterville

A Professional Accounting Corporation Associated Offices in Principal Cities of the United States

www.pncpa.com

INDEPENDENT AUDITORS' REPORT

The Board of Directors GCHP Housing Finance, Inc.

We have audited the accompanying consolidated statements of financial position of GCHP Housing Finance, Inc. (the Company) as of December 31, 2013 and 2012, and the related consolidated statements of activities and cash flows for the years then ended, and the related notes to the consolidated financial statements.

Management's Responsibilitv for the Financial Statements

Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of intemal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditors' Responsibilitv

Our responsibility is to express an opinion on these consolidated financial statements based on our audits. We conducted our audits in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditors' judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error, fri making those risk assessments, the auditor considers intemal control relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's intemal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the fmancial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

-1-

30th Floor - Energy Centre • 1100 Poydras Street • New Orleans, LA 70163-3000 • Tel: 800.201.7332 One Galleria Blvd., Suite 2100 • Metairie, LA 70001 • Tel: 504.837.5990 • Fax: 504.834.3609

Opinion

In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the consolidated financial position of GCHP Housing Finance, Inc. as of December 31, 2013 and 2012, and the results of its operations and its cash flows for the years then ended in conformity with accounting principles generally accepted in the United States of America.

Other Reporting Required by Government Auditing Standards

In accordance with Government Auditing Standards, we have also issued our report dated April 28, 2014, on our consideration of the Company's internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not provide an opinion on the intemal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the the Company's intemal control over financial reporting and compliance.

Metairie, Louisiana April 28,2014

-2-

GCHP HOUSING FINANCE, INC. CONSOLIDATED STATEMENTS OF FINANCIAL POSITION

DECEMBER 31,2013 and 2012

ASSETS 2013 2012

Current assets Cash and cash equivalents Interest receivable Pledged contribution receivable

$ 139,009 2,488

$ 2,488

246,262 Total current assets 141,497 248,750

Other assets Loan receivable Cash and cash equivalents, restricted Property Deferred debt issuance costs long term

4,683,301 344,664 305,000

15,801

1,947,000 87,225

Total Assets $ 5,490,263 $ 2,282,975

LIABILITIES AND NET ASSETS

Current liabilities Accounts payable Interest payable Loans payable, current portion Deferred revenue

$ 5,035

174,060

$ 2,900 264

100,000

Total current liabilities 179,095 103,164

Long-term liabilities Interest payable Loans payable

18,186 4,736,301

8,239 1,900,000

Total long-term liabilities 4,754,487 1,908,239

Total Liabilities 4,933,582 2,011,403

Unrestricted net assets 556,681 271,572

Total liabilities and net assets $ 5,490,263 $ 2,282,975

The accompanying notes arc an integral part of these statements.

-3-

GCHP HOUSING FINANCE, INC. CONSOLIDATED STATEMENTS OF ACTIVITIES

FOR THE YEARS ENDED DECEMBER 31,2013 AND 2012

Revenue Contribution Management fee income Interest income

Total revenue

Expenses Accounting fees Legal and professional fees Bank fees Dues, licenses and fees Management fees Interest expense Amortization expense

Total expense

Change in net assets

Net assets at begirming of year

Net assets at end of year

The accompanying notes are an integral part of these statements.

2013 2012

$ 305,000 $ 387,262 55,940 -21,887 9,897

382,827 397,159

11,900 2,900 1,259 -3,186 11

75 -16,500 -59,531 37,527 5,267 7,139

97,718 47,577

285,109 349,582

271,572 (78,010)

$ 556,681 $ 271,572

-4-

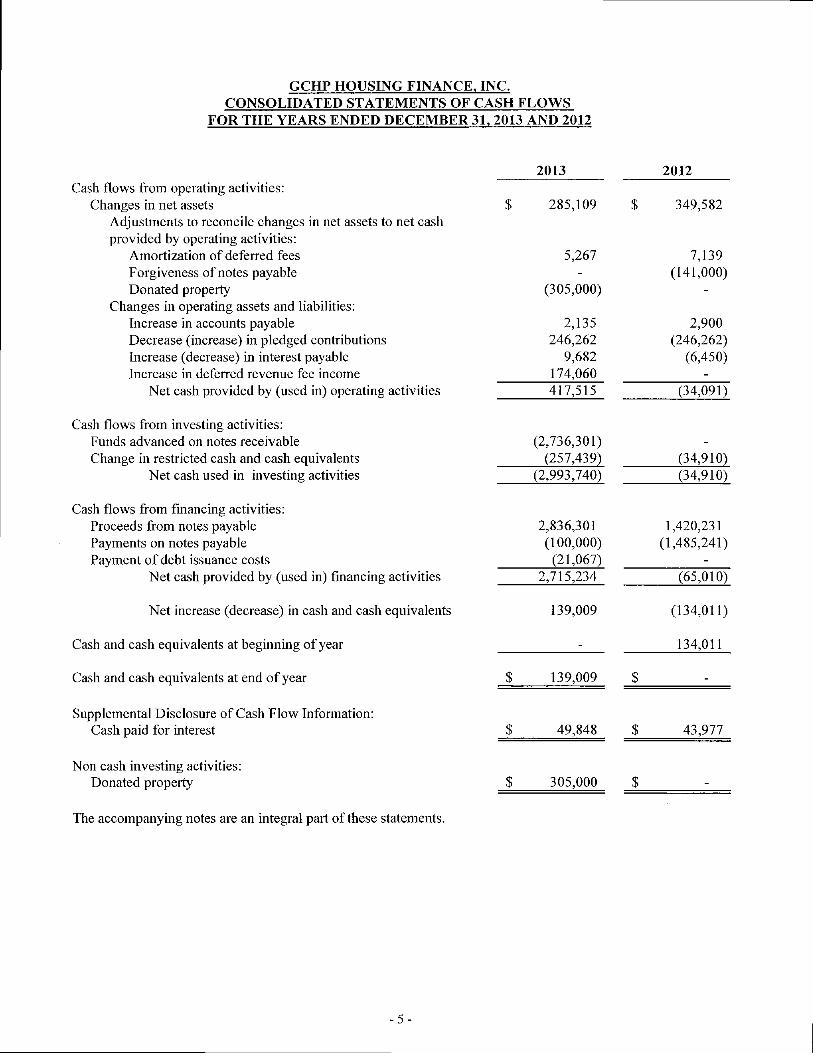

GCHP HOUSING FINANCE, INC. CONSOLIDATED STATEMENTS OF CASH FLOWS

FOR THE YEARS ENDED DECEMBER 31, 2013 AND 2012

The accompanying notes arc an integral part of these statements.

2013 2012 Cash flows from operating activities:

Changes in net assets Adjustments to reconcile changes in net assets to net cash provided by operating activities:

Amortization of deferred fees Forgiveness of notes payable Donated property

Changes in operating assets and liabilities: Increase in accounts payable Decrease (increase) in pledged contributions Increase (decrease) in interest payable Increase in deferred revenue fee income

$ 285,109

5,267

(305,000)

2,135 246,262

9,682 174,060

$ 349,582

7,139 (141,000)

2,900 (246,262)

(6,450)

Net cash provided by (used in) operating activities 417,515 (34,091)

Cash flows from investing activities: Funds advanced on notes receivable Change in restricted cash and cash equivalents

Net cash used in investing activities

(2,736,301) (257,439)

(2,993,740) (34,910) (34,910)

Cash flows from financing activities: Proceeds from notes payable Payments on notes payable Payment of debt issuance costs

2,836,301 (100,000)

(21,067)

1,420,231 (1,485,241)

Net cash provided by (used in) financing activities 2,715,234 (65,010)

Net increase (decrease) in cash and cash equivalents 139,009 (134,011)

Cash and cash equivalents at beginning of year _ 134,011

Cash and cash equivalents at end of year $ 139,009 $

Supplemental Disclosure of Cash Flow Information: Cash paid for interest $ 49,848 $ 43,977

Non cash investing activities: Donated property $ 305,000 $

-5-

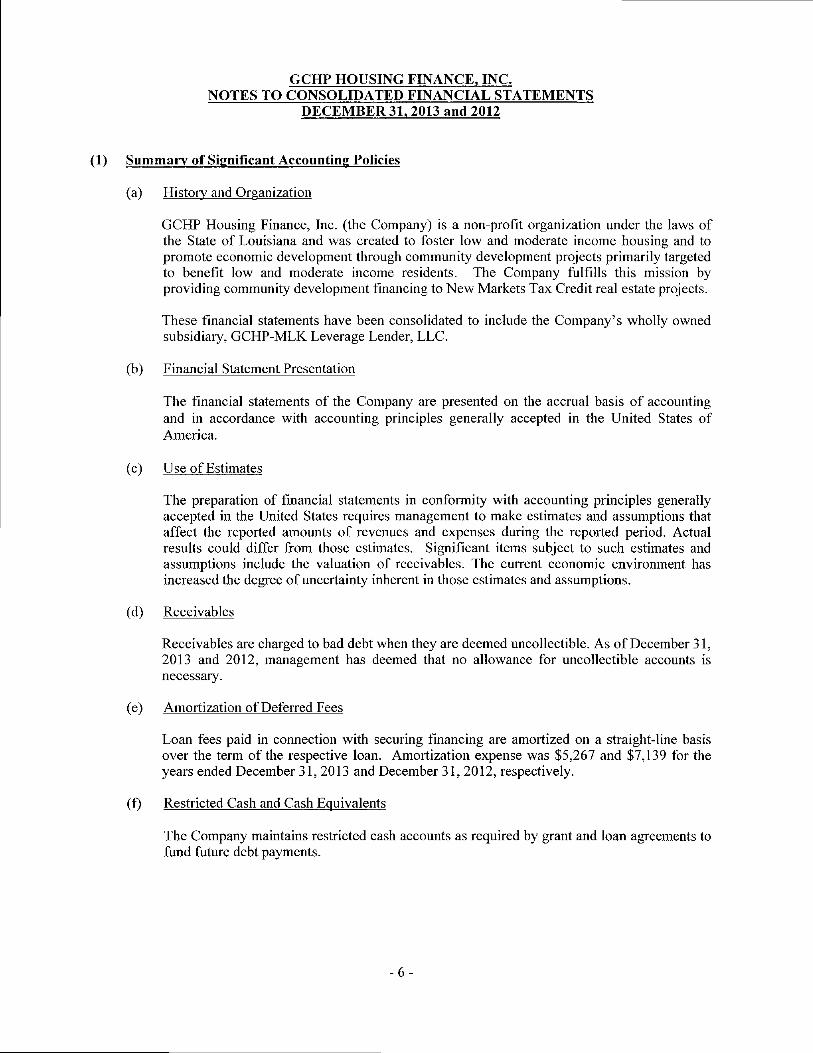

GCHP HOUSING FINANCE, INC. NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

DECEMBER 31, 2013 and 2012

(1) Summary of Significant Accounting Policies

(a) History and Organization

GCHP Housing Finance, Inc. (the Company) is a non-profit organization under the laws of the State of Louisiana and was created to foster low and moderate income housing and to promote economic development through community development projects primarily targeted to benefit low and moderate income residents. The Company fulfills this mission by providing community development financing to New Markets Tax Credit real estate projects.

These financial statements have been consolidated to include the Company's wholly owned subsidiary, GCHP-MLK Leverage Lender, LLC.

(b) Financial Statement Presentation

The financial statements of the Company are presented on the accrual basis of accounting and in accordance with accounting principles generally accepted in the United States of America.

(c) Use of Estimates

The preparation of financial statements in eonformity with accounting principles generally aceepted in the United States requires management to make estimates and assumptions that affect the reported amounts of revenues and expenses during the reported period. Actual results could differ from those estimates. Significant items subject to such estimates and assumptions include the valuation of receivables. The current economic environment has increased the degree of uncertainty inherent in those estimates and assumptions.

(d) Reeeivables

Receivables are charged to bad debt when they are deemed uncollectible. As of December 31, 2013 and 2012, management has deemed that no allowance for uncollectible accounts is necessary.

(e) Amortization of Deferred Fees

Loan fees paid in connection with securing financing are amortized on a straight-line basis over the term of the respective loan. Amortization expense was $5,267 and $7,139 for the years ended December 31, 2013 and December 31, 2012, respectively.

(f) Restricted Cash and Cash Equivalents

The Company maintains restricted cash accounts as required by grant and loan agreements to fund future debt payments.

-6-

GCHP HOUSING FINANCE, INC. NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

DECEMBER 31, 2013 and 2012

(1) Summary of Significant Accounting Policies (continued)

(g) Property

Property consists of land that was donated to the Company on May 28, 2013.

Impairment of long-lived assets is tested whenever events or changes in circumstances indicate that their carrying amount may not be recoverable. The carrying value of a long-lived asset is considered impaired when the anticipated undiscounted cash flows from such asset is separately identifiable and is less than its carrying value. In that event, a loss is recognized based on the amount by which the carrying value exceeds the fair market value of the long-lived asset. Fair market value is determined primarily using appraisals. Losses on long-lived assets to be disposed of are determined in a similar manner, except that fair market values are reduced for the estimated cost to dispose. There were no impairments of long-lived assets recorded by management during the years ended December 31, 2013 and 2012.

(h) Deferred Revenue

Deferred revenue consists of construction management fees received on the GCHP Poly Bar project at the time the financing on the project was closed. The fees are recognized into income ratably based on the percentage of completion of the project. For the year ended December 31, 2013, management fees of $55,940 were recognized as revenue.

(i) Tax Exempt Status

GCHP Housing Finance, Inc. has received notice from the Internal Revenue service of exemption from income tax under Section 501(c)(3) of the Internal Revenue Code ("IRC).

The Company applies the accounting for uncertainty in income taxes approach by defining criterion that an individual tax position must meet for any part of the benefit of that position to be recognized in a company's financial statements. This method requires recognition and measurement of uncertain income tax positions using a "more-likely-than-not" recognition threshold for all tax uncertainties. There were no uncertain tax positions at December 31, 2013 and 2012.

(2) Concentration of Credit Risk

Financial instruments that potentially subject the Company to credit risk include cash deposits in excess of federally insured limits. As of December 31, 2013 and 2012, the Company had $94,664 and $0 in uninsured balances, respectively.

-7-

GCHP HOUSING FINANCE, INC. NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

DECEMBER 31, 2013 and 2012

(3) Notes Receivable

Details of notes receivable are as follows as of December 31:

Note Receivable - FNBC MLK Investments, LLC Note receivable for $1,947,000 dated March 31, 2011. The Note bears interest at a rate per annum of 0.5% payable quarterly beginning July 1, 2011. The note matures March 30, 2051.

Note Receivable - FNBC NMTC #1, L.L.C. Note receivable for $2,736,301 dated June 27, 2013. The note bears interest at a rate per annum of 0.73% payable quarterly beginning September 10, 2013. The note matures June 27, 2053.

Total notes receivable Less current maturities

Total notes receivable, less current maturities

2013 2012

$ 1,947,000 $ 1,947,000

2,736,301

4,683,301 1,947,000

$ 4,683,301 $ 1,947,000

Accrued interest receivable on the above notes totaled $2,488 as of December 31, 2013 and 2012.

(4) Long-Term Debt

Details of long-term debt are as follows as of December 31: 2013 2013

Note Payable - New Orleans Redevelopment Authority

Note payable with New Orleans Redevelopment Authority (NORA) for $2,000,000 dated March 31, 2011. The Note bears interest at a rate per annum of 0.5% payable monthly and in arrears beginning July 1, 2011. Beginning on the Option Date, interest accrues at the Prime Rate plus 1%, adjusted annually, payable monthly and in arrears. Principal shall be paid out of monthly cash flow. The note matures March 31, 2051 and is collateralized by substantially all of the assets of the entity and by the entity's security interest in the Community Development Entity New Markets Investment 58. $ 2,000,000 $ 1,900,000

-8-

GCHP HOUSING FINANCE, INC. NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

DECEMBER 31,2013 and 2012

(4) Long-Term Debt (continued)

Note Payable - First NBC Bank Note payable with First NBC Bank for $2,000,000 dated March 31, 2011. The Note bears interest at an annual rate of 5.0% payable quarterly, on the last day of each quarter beginning June 30, 2011. The note matures June 30, 2013. The note is collateralized by the entity's security interest in the membership interest of the Community Development Entity New Markets Investment 58. This loan was paid in its entirety June 7,2013. - 100,000

Note Payable - First NBC Bank Note payable with First NBC Bank for $2,106,815 dated June 27, 2013. The Note bears interest at an annual rate of 4.5% payable quarterly, on the 10^ day of the last month of the quarter beginning September 10, 2013. The note matures June 27, 2015. The note is collateralized by the entity's security interest in the Bridge Loan Security and Pledge Agreement, the Deposit Account Security Agreement, and the Bridge Loan Repayment Guaranty. 2,106,815

Note Payable - GCHP, Inc. Note payable with Gulf Coast Housing Partnership Inc. for $629,486 dated June 27, 2013. The Note bears interest at an annual rate of 0%. The note matures June 27, 2023. 629,486

Note Payable - State of Louisiana, OCD Note payable with State of Louisiana, OCD for $1,000,000 dated November 27, 2013. The note has an interest rate of 1% per annum paid monthly in arrears on the tenth day of the month beginning six months after the initial date of advance of loan proceeds. Commencing eighteen months from the initial advance date, principal will amortize in equal monthly installments over the remaining term of the loan and through October 26, 2019 be deposited into a sinking fund. On October 27, 2019 all deposits in the sinking fiind will be paid to lender as a "Balloon Payment" and principal will be due to lender on the tenth of the month in arrears. The maturity date is November 27, 2043.

Total debt 4,736,301 2,000,000 Less current maturities ^ 100,000

Total debt, less current maturities $ 4,736,301 $ 1,900,000

-9-

GCHP HOUSING FINANCE, INC. NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

DECEMBER 31, 2013 and 2012

(5) Related Party Transactions

GCHP-Management, LLC and GCHP-MLK Development, LLC are subsidiaries of Gulf Coast Housing Partnership, Inc. whose President is also President of GCHP Housing Finance, Inc. The Company has contracted with GCHP-Management, LLC to provide management services. During the years ended December 31, 2013 and 2012, the Company was charged $19,400 and $2,900, respectively, for management services by GCHP-Management, LLC.

On May 28, 2013, GCHP-PolyBar, L.L.C., a subsidiary of Gulf Coast Housing Partnership, Inc., donated property to the Company with a fair value of $305,000.

During the year ended December 31, 2012, GCHP-MLK Development, LLC held promissory notes of $141,000 from the Company. On June 6, 2012, GCHP-MLK Development, LLC converted these notes to a charitable contribution. During the year ended December 31, 2012, GCHP-MLK Development, LLC pledged $246,262 to the Company that was received in 2013.

(6) Legal Matters

The Company is not involved in any legal action arising in the normal course of activities.

(7) Subsequent Events

Management has evaluated subsequent events through the date the financial statements were available to be issued, April 28, 2014, and noted no items requiring disclosure.

-10-

IlinAI Postlethwaite KWAI & Netterville

A Professional Accounting Corporation Associated Offices in Principal Cities of the United States

www.pncpa.com

ESPEPENDENT AUDITORS' REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS BASED

ON AN AUDIT OF FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WITH GO VERNMENT A UDITING S TAND ARBS

To the Board of Directors GCHP Housing Finance, Inc.

We have audited, in accordance with the auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards issued by the Comptroller General of the United States, the consolidated financial statements of GCHP Housing Finance, Inc. (the Company), which comprise the consolidated statements of financial position as of December 31, 2013, and the related consolidated statements of activities and cash flows for the year then ended, and the related notes to the consolidated financial statements, and have issued our report thereon dated April 28, 2014.

Intemal Control over Financial Reporting

In planning and performing our audit of the consolidated financial statements, we considered the Company's intemal control over financial reporting (intemal control) to determine the audit procedures that are appropriate in the circumstances for the purpose of expressing our opinions on the consolidated financial statements, but not for the purpose of expressing an opinion on the effectiveness of the Company's intemal control. Accordingly, we do not express an opinion on the effectiveness of the Company's intemal control.

A deficiency in internal control exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned ftinctions, to prevent, or detect and correct, misstatements on a timely basis. A material weakness is a deficiency, or a combination of deficiencies, in intemal control, such that there is a reasonable possibility that a material misstatement of the entity's financial statements will not be prevented, or detected and corrected on a timely basis. A significant deficiency is a deficiency, or a combination of deficiencies, in intemal control that is less severe than a material weakness, yet important enough to merit attention by those charged with govemance.

Our consideration of intemal control was for the limited purpose described in the first paragraph of this section and was not designed to identify all deficiencies in intemal control that might be material weaknesses or, significant deficiencies. Given these limitations, during our audit we did not identify any deficiencies in intemal control that we consider to be material weaknesses. However, material weaknesses may exist that have not been identified.

30th Floor - Energy Centre • 1100 Poydras Street • New Orleans, LA 70163-3000 • Tel: 800.201.7332 One Galleria Blvd., Suite 2100 • Metairie, LA 70001 • Tel: 504.837.5990 • Fax: 504.834.3609

Compliance and Other Matters

As part of obtaining reasonable assurance about whether the Company's consolidated financial statements are free from material misstatement, we performed tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements, noncompliance with which could have a direct and material effect on the determination of financial statement amounts. However, providing an opinion on complianee with those provisions was not an objective of our audit, and accordingly, we do not express such an opinion. The results of our tests disclosed an instance of noncompliance or other matters that is required to be reported under Government Auditing Standards and which is described in the aceompanying schedule of findings and questions costs as item 2013-1.

Purpose of this Report

The purpose of this report is solely to describe the scope of our testing of internal control and compliance and the results of that testing, and not to provide an opinion on the effectiveness of the entity's internal control or on compliance. This report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the entity's internal control and compliance. Accordingly, this communication is not suitable for any other purpose.

Metairie, Louisiana April 28,2014

GCHP HOUSING FINANCE, INC.

SCHEDULE OF FINDINGS AND QUESTIONED COSTS

YEAR-ENDED DECEMBER 31,2013

Findings Relating to the Financial Statements Reported in Accordance with Government Auditins Standards

2013-1 Timely Submission of Audit Report to Louisiana Legislative Auditor

Criteria:

Condition:

Under Louisiana statute, the Company is required to have an annual audit of its financial statements in accordance with US generally accepted accounting principles and to complete the audit and file it with the Legislative Auditor of the State of Louisiana by June 30 of each year.

The Company did not meet the June 30, 2014 deadline for reporting to the State of Louisiana.

Cause:

Effect:

The Company did not identify Federal Funds received from the State of Louisiana as funding requiring reporting to the Legislative Auditor.

The Company was not in compliance with the Louisiana statute requiring a timely filing of its audited financial statements.

Recommendation: The Company should implement a policy for determining the deadlines and filing dates for all audit reports.

Management's Response: In 2013, we expended Federal Funds that were passed through the State of

Louisiana. After consulting with our auditors, we determined that the amount of these expenditures was less than the federal single audit threshold, and that we were not required to file our audit report with the applicable federal agency. However, our discussions with our auditors did not identify the state source of revenues and the related filing requirements of the State of Louisiana for this source of funding. Although we completed our audit prior to the June 30, 2014 deadline, we did not file the audit with the LLA in a timely manner.

To ensure compliance with future filing requirements, management will implement procedures to better identify filing requirements for state sources of revenue to ensure compliance with all audit filing deadlines.