GCC Fixed Income Chart Book: FY 2017 Review - nbad.com · PDF file2011 2012 2013 2014 2015...

31

GCC Fixed Income Chart Book: FY 2017 Review 09 January 2018

Transcript of GCC Fixed Income Chart Book: FY 2017 Review - nbad.com · PDF file2011 2012 2013 2014 2015...

GCC Fixed Income Chart Book: FY 2017 Review

09 January 2018

2

Disclaimer

The information contained herein has been prepared by First Abu Dhabi Bank P.J.S.C (“FAB”). FAB relies on information

obtained from sources believed to be reliable but does not guarantee its accuracy or completeness.

This presentation has been prepared for information purposes only and is not and does not form part of any offer for sale

or solicitation of any offer to subscribe for or purchase or sell any securities nor shall it or any part of it form the basis of or

be relied on in connection with any contract or commitment whatsoever.

Some of the information in this presentation may contain projections or other forward-looking statements regarding future

events or the future financial performance of FAB. These forward-looking statements include all matters that are not

historical facts. The inclusion of such forward-looking information shall not be regarded as a representation by FAB or any

other person that the objectives or plans of FAB will be achieved. FAB undertakes no obligation to publicly update or

publicly revise any forward-looking statement, whether as a result of new information, future events or otherwise.

3

Foreword

Welcome to our FY 2017 chart book for the GCC fixed income market. The idea is very simple – to give those of you who

follow this market a quick snapshot of some of the key points in terms of the following:

➢ Primary Market issuance in 2017 and the new issue trend over the past eight years

➢ Deal dynamics and relative value analysis

➢ Secondary Market performance of key instruments (snapshot from 30th December 2016 to 29th December 2017)

We have deliberately made the report text-light in an attempt to make it easier to digest. Hopefully you will find it both

interesting and useful.

If you have any feedback on the report, or indeed would like to discuss any of the points highlighted, please do contact me.

Regards,

Chavan Bhogaita / Rakesh Sahu

Market Insights & Strategy

Global Markets, FAB

+971 2 6110 127

Please click here to view our recent publications on MENA and Global Markets

4

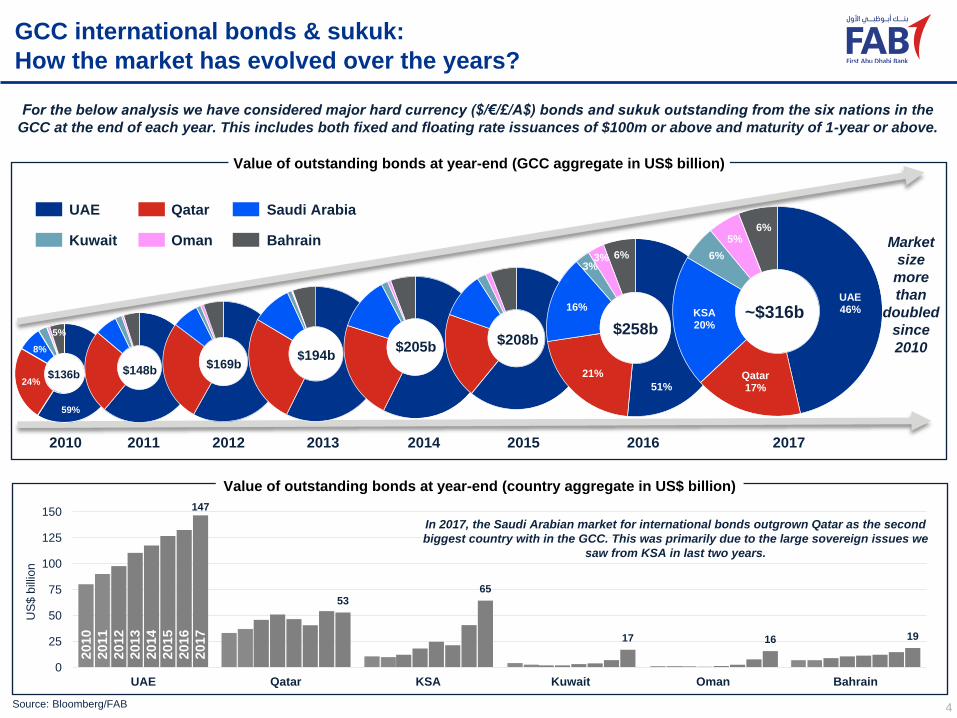

GCC international bonds & sukuk:

How the market has evolved over the years?

Source: Bloomberg/FAB

For the below analysis we have considered major hard currency ($/€/£/A$) bonds and sukuk outstanding from the six nations in the

GCC at the end of each year. This includes both fixed and floating rate issuances of $100m or above and maturity of 1-year or above.

Market

size

more

than

doubled

since

2010

59%

24%

8%

5%

51%

21%

16%

3%3% 6%

UAE46%

Qatar17%

KSA20%

6%

5%6%

UAE Qatar Saudi Arabia

Kuwait BahrainOman

2010

$136b

2011 2012 2013 2014 2015 2016 2017

$148b$169b

$194b$205b

$208b$258b

~$316b

Value of outstanding bonds at year-end (GCC aggregate in US$ billion)

147

5365

17 16 19

0

25

50

75

100

125

150

UAE Qatar KSA Kuwait Oman Bahrain

US

$ b

illio

n

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

In 2017, the Saudi Arabian market for international bonds outgrown Qatar as the second

biggest country with in the GCC. This was primarily due to the large sovereign issues we

saw from KSA in last two years.

Value of outstanding bonds at year-end (country aggregate in US$ billion)

5Source: Bloomberg/FAB

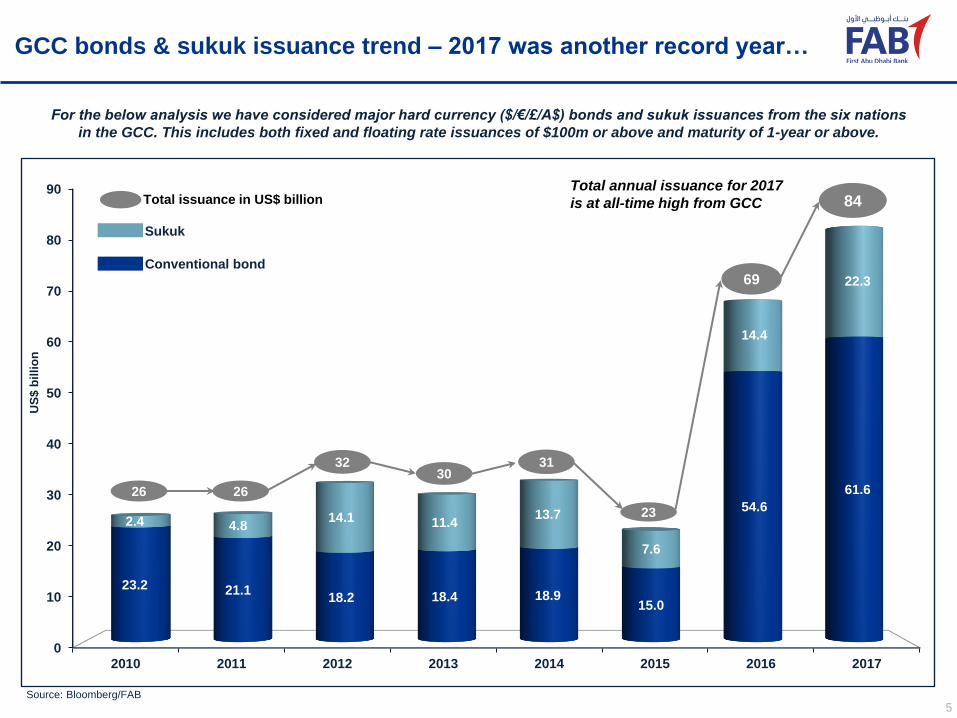

For the below analysis we have considered major hard currency ($/€/£/A$) bonds and sukuk issuances from the six nations

in the GCC. This includes both fixed and floating rate issuances of $100m or above and maturity of 1-year or above.

GCC bonds & sukuk issuance trend – 2017 was another record year…

0

10

20

30

40

50

60

70

80

90

2010 2011 2012 2013 2014 2015 2016 2017

23.2 21.118.2 18.4 18.9

15.0

54.6

61.6

2.4 4.814.1 11.4

13.7

7.6

14.4

22.3

Sukuk

Conventional bond

Total annual issuance for 2017

is at all-time high from GCC

26

84

26

3230

31

23

69

Total issuance in US$ billion

US

$ b

illi

on

6

Source: Bloomberg/FAB

…and witnessed highest amount of sovereign issuances in this market

GCC Sovereign issue trend

6.4 7.3 6.8

3.3 3.42.1

40.0

50.1

0

20

40

60

80

100

120

0

5

10

15

20

25

30

35

40

45

50

55

60

2010 2011 2012 2013 2014 2015 2016 2017

Sov bond issue in US$ bn (LHS)

Avg brent price in $/bbl (RHS)

Sov

as % of

total

GCC

issue

25% 28% 21% 11% 10% 9% 58% 60%

0 5 10 15 20 25 30 35 40 45 50 55

2016

2017Sov

issue

by

country

Kingdom of Saudi Arabia

Qatar

Kuwait Oman Abu DhabiBahrain

UAE ex AD

US$ bn

7

Sovereigns should continue to borrow in 2018, albeit at lower level

Source: IMF/Bloomberg/FAB

Economic growth across the GCC is expected to accelerate in 2018. Brent prices also stabilised near $60/bbl which should provide

some fiscal buffer. However, fiscal deficits still persist, although improving. Governments thus need to continue their borrowing.

-2.50%

-1.50%

-0.50%

0.50%

1.50%

2.50%

3.50%

4.50%

UAE KSA Qatar Kuwait Oman Bahrain GCC

2017 2018

Real GDP growth (IMF estimates)

0.05.0

10.015.020.025.030.035.040.045.050.055.060.065.070.075.080.085.090.095.0

100.0

UAE KSA Qatar Kuwait Oman Bahrain

2017 2018

Break-even Brent oil price in US$/barrel (IMF estimates)

-15.0%

-12.5%

-10.0%

-7.5%

-5.0%

-2.5%

0.0%

2.5%

UAE KSA Qatar Kuwait Oman Bahrain GCC

2017 2018

Govt. sector fiscal balance as % of GDP (IMF estimates)

-60.0%

-50.0%

-40.0%

-30.0%

-20.0%

-10.0%

0.0%

UAE KSA Qatar Kuwait Oman Bahrain GCC

2017 2018

Non-oil fiscal balance as % of GDP (IMF estimates)

2018 forecast, Bloomberg survey median ($58.00)

Current Brent price ($67.10)

Economies expected to

improve this year…

… but negative fiscal balances

still need debt funding

2017 average price ($54.75)

8

We expect corporate issuance to exceed sovereign issues in 2018

Corporate bond issuance could see an uptick this year and we back our rationale based on the following observations:

➢ Corporates & banks have a large refinancing need as some $60bn of loans and bonds maturing in 2018;

➢ They could seek to lock in the relatively low level of interest rates still available in international market as local rates are rising;

➢ They could capitalise on the demand from yield hungry international investors to diversify their sources of funding;

➢ And more importantly, GCC governments have now established US$ yield curves to provide pricing benchmark for issuers.

* Notes: International bonds & sukuk are the major hard currency ($/€/£/A$) deals from the GCC (fixed & floating; size >= $100m and tenor >= 1-year); Source: Bloomberg/FAB

0

20

40

60

80

100

120

140

160

180

200

2010 2011 2012 2013 2014 2015 2016 2017

5461

4655

66

94104

68

2626

3230

33

23

69

84

Debt issued by GCC entities (in US$ billion)

The loan and bond mix for GCC debt

capital market has shifted in last two years

and we expect this to continue in 2018

Loans International Bonds & Sukuk*

GCC 3-month interbank rates

0.90

1.10

1.30

1.50

1.70

1.90

2.10

2.30

2.50

2.70

2.90

0.90

1.10

1.30

1.50

1.70

1.90

2.10

2.30

2.50

2.70

2.90 KSA

UAE

Qatar

Kuwait

Oman

Bahrain

US$ Libor 3M

Rates have moved

higher by 10-30 bps

9

Global rates environment still accommodative for GCC issuers

Notes: * Rates are for 29-Dec-17; Source: Bloomberg/FAB;

We expect 2018 debt issuance from the GCC to remain

elevated, but lower than the record level we saw last year. We

think issuers would opt for longer duration, bearing in mind

the following factors:

➢ In Sep’17, the Fed lowered its expectation for long-term

interest rate from 3.0% to 2.75% and it remains unchanged

since. Furthermore, Fed still expects to raise rates at a

gradual pace and sees only three hikes in 2018.

➢ As a result, short-term rates have moved faster since

Sep’17 pushing the 5y-10y & 5y-30y spread to record lows.

➢ GCC issuers are increasingly diversifying their investor

base and allocating more to investors from US & Europe,

who usually bid for longer duration bonds for the yield.

1.00

1.25

1.50

1.75

2.00

2.25

2.50

2.75

3.00

3.25

2017 2018 2019 Longer Term

Implie

d F

ed F

unds T

arg

et

Rate

Year End Projection

Fed’s interest rate projection (FOMC Dots)

FOMC member dots

Dec'16 meeting median

Jun’17 meeting median

Dec'17 meeting median

(same as Sep’17)

Current Fed Funds Futures

implied interest rate*

Current OIS (overnight Index

Swap) implied interest rate*

Fed has lowered its

long-term rates

expectation

1.00

1.25

1.50

1.75

2.00

2.25

2.50

2.75

3.00

3.25

1.00

1.25

1.50

1.75

2.00

2.25

2.50

2.75

3.00

3.252Y: +69bps 5Y: +28bps 10Y: -4bps 30Y: -33bps

US treasury yields movement in 2017

Yield% Yield%

… Short-end yields

climbing fast on

Fed rate hikes…

Long-end yields remain

flattish on duration demand…

0

40

80

120

160

200

240

280

320

0

40

80

120

160

200

240

280

3205y30y

5y10y

Treasury yield spreads (in bps)

… As a result, treasury

yield spreads plunged

to record lows

10

And demand remain robust for primary issues from the GCC

0 5

10

15

20

25

30

35

KSA 2-tranche Sukuk (5y & 10y)

Kuwait 2-tranche (5y & 10y)

Oman 3-tranche (5, 10 & 30y)

Bahrain 3-tranche (7.5y sukuk, 12y & 30y)

Oman 7Y Sukuk

Mubadala 2-tranche (5y & 10y)

Inv. Corp. of Dubai 10Y Sukuk

Qatar Reinsurance Perp Bond

Equate Petrochemical 7Y Sukuk

National Bank Kuwait 5Y Bond

Omangrid 10Y Bond

QIB 5Y Sukuk

Dubai Islamic Bank 5Y Sukuk

Ahli Bank Qatar 5Y Bond

KIPCO 10Y Bond

Ezdan 5Y Sukuk

Majid Al Futtaim Perp Bond

Al Baraka Bank Perpetual Sukuk

FAB 5Y Green Bond

Gulf International Bank 5Y Bond

33.0

30.0

19.5

15.0

7.0

4.3

3.1

6.5

3.7

2.9

2.7

2.2

2.1

2.0

2.0

2.0

1.8

1.6

1.1

1.1

Amount in billion US$

Times oversubscribedOrderbookAmount issued

Source: Bloomberg/FAB

3.7x

3.9x

3.5x

2.9x

2.7x

2.9x

4.0x

2.1x

4.0x

3.6x

3.8x

5.0x

4.0x

2.4x

2.2x

3.9x

Fin

s &

Co

rp. B

on

ds

So

ve

reig

n/S

WF

Bo

nd

s

Some major primary deals of 2017

3.1x

14.4x

7.4x

3.9x

11Note: Credit ratings are in following order Moody’s/S&P/Fitch; NR is ‘not rated’; *For ADNOC Distribution & Emirates SembCorp the ratings are bond ratings; Source: Bloomberg/FAB

International appetite indeed appeared unscathed in recent deals…

…amid the startling political headlines that we witnessed from the region in the second half of 2017. Investor base for GCC deals are now well

diversified with more than 50% of the demand coming from outside the MENA region. The below deals are indeed a testimony to this.

0% 20% 40% 60% 80% 100%

KSA MENA

8%

Europe

26%

Asia

18%

US

48%

Abu Dhabi Sov (Aa2/AA/AA)

3-tranche deal in Oct

KSA Sov (A1/A-/A+)

3-tranche deal in Sep

ADNOC Distribution*

(NR/AA/AA) 2-tranche deal

in Oct

Emirates SembCorp*

(A2/A-/NR) deal in Nov

Emirates Reit (BB+)

deal in Dec

Oman’s Mazoon Electricity

(Baa2/NR/BBB-) deal in Oct

~$975m (2.4x)

$400m

~$2.1bn (5.3x)

$400m

~$5.0bn (10.0x)

$500m

~$11bn (3.6x)

$3.0bn

Orderbook (Oversubscription): ~$40bn (3.2x)

Deal size: $12.5bn

$30bn (3.0x)

$10bn

0% 20% 40% 60% 80% 100%

ADGB MENA

22%

Europe

29%

Asia

10%

US

39%

0% 20% 40% 60% 80% 100%

AND 5%37% 9%49%

0% 20% 40% 60% 80% 100%

ADGB0% 20% 40% 60% 80% 100%

Reit 54%15%31%

Geographic Distribution

0% 20% 40% 60% 80% 100%

Mazn 47%17%23%13%

0% 20% 40% 60% 80% 100%

Semb 3%26%29%12%

12

Regional geo-politics narrowed the GCC-EM spread in H2’2017

* Notes: Bloomberg/Barclays maintain the above indices on Bloomberg; BGCIOAS is the GCC US$ bond index & BEHGOAS is the EM IG US$ bond index; Source: Bloomberg/FAB

120

130

140

150

160

170

180

120

130

140

150

160

170

180

GCC US$ bond index* – Average credit rating ‘A’ Emerging Markets US$ Inv. Grade bond index* – Average credit rating ‘BBB+’

Qatar stand-off emerged

at the beginning on JuneSaudi anti-graft

crackdown begin

at the end of Oct,

followed by the

Lebanon crisis

Major trend we witnessed during June and November sell-off…

➢ The sell-off was primarily fast-money driven, while real-money was only

involved in the long-end (mostly 30yr papers), albeit at a very low volume

➢ Real-money from GCC and Asia bought on dips

➢ Regional banks support secondary market due to lack of primary allocation

Option a

dj. s

pre

ad (

OA

S)

in b

ps

Option a

dj. s

pre

ad (

OA

S)

in b

ps

13

GCC credits offer pick up vs Asia investment grade credits…

… even though aggregate credit quality of GCC bonds – at ‘A’ – is one notch higher than the aggregate

credit quality of Asian investment grade bonds.

* Notes: Bloomberg/Barclays maintain the above indices on Bloomberg; BGCIOAS is the GCC index & BAIGOAS is the Asia IG index; Source: Bloomberg/FAB

100

120

140

160

180

200

220

240

260

0

15

30

45

60

75

90

105

120

GCC US$ bond index* (RHS)

Avg. credit rating “A”

Asia US$ Inv. Grade bond index* (RHS)

Avg. credit rating “A-”Brent oil price per barrel (LHS)

Option a

dj. s

pre

ad (

OA

S)

in b

ps

US

$ p

er

barr

el

GCC credit spreads were inside

Asia inv. grade when oil was

trading around $60/barrel in 2015

Current GCC spreads, trading

outside Asia IG, indicate that markets

are pricing in the political risk and

not focusing on the fundamentals.

As a result we expect the GCC-Asia

spread to narrow in 2018 as:

1. Asia spreads are trading at the

tightest level; and

1. Investors would start focusing on

the credit fundamentals

14

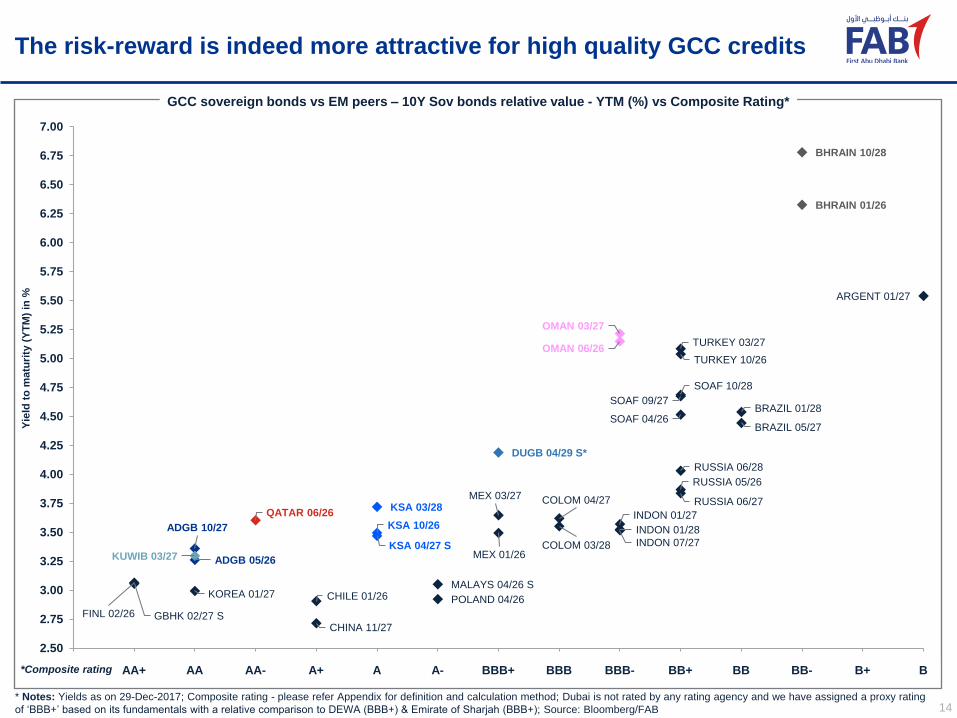

The risk-reward is indeed more attractive for high quality GCC credits

* Notes: Yields as on 29-Dec-2017; Composite rating - please refer Appendix for definition and calculation method; Dubai is not rated by any rating agency and we have assigned a proxy rating

of ‘BBB+’ based on its fundamentals with a relative comparison to DEWA (BBB+) & Emirate of Sharjah (BBB+); Source: Bloomberg/FAB

ADGB 05/26

ADGB 10/27

QATAR 06/26

KSA 10/26

KSA 04/27 S

KSA 03/28

KUWIB 03/27

DUGB 04/29 S*

OMAN 06/26

OMAN 03/27

BHRAIN 01/26

BHRAIN 10/28

MEX 01/26

MEX 03/27

CHILE 01/26MALAYS 04/26 S

CHINA 11/27

FINL 02/26

TURKEY 10/26

TURKEY 03/27

POLAND 04/26KOREA 01/27

INDON 01/27

INDON 07/27

INDON 01/28

SOAF 04/26

SOAF 09/27

SOAF 10/28

COLOM 04/27

COLOM 03/28

RUSSIA 05/26

RUSSIA 06/27

RUSSIA 06/28

BRAZIL 05/27

BRAZIL 01/28

GBHK 02/27 S

ARGENT 01/27

2.50

2.75

3.00

3.25

3.50

3.75

4.00

4.25

4.50

4.75

5.00

5.25

5.50

5.75

6.00

6.25

6.50

6.75

7.00

GCC sovereign bonds vs EM peers – 10Y Sov bonds relative value - YTM (%) vs Composite Rating*

AA+ AA AA- A+ A A- BBB BBB-BBB+ BB+ BB

Yie

ld t

o m

atu

rity

(Y

TM

) in

%

*Composite rating BB- B+ B

15

GCC sovereign bonds vs EM peers – 30Y relative value

30Y Sov bonds relative value - YTM (%) vs Composite Rating*

ADGB 10/47

DUGB 01/43*

QATAR 06/46

KSA 10/46

KSA 10/47

OMAN 03/47

BHRAIN 09/44

BHRAIN 09/47

MEX 01/47

MEX 02/48 KAZAKS 07/45

CHILE 06/47 MALAYS 04/46 S

COLOM 06/45

SOAF 10/46

SOAF 09/47

INDON 01/47

INDON 07/47

INDON 01/48

TURKEY 02/45

TURKEY 05/47

RUSSIA 09/43

RUSSIA 06/47

KOREA 06/44

BRAZIL 02/47

ARGENT 04/46

3.00

3.25

3.50

3.75

4.00

4.25

4.50

4.75

5.00

5.25

5.50

5.75

6.00

6.25

6.50

6.75

7.00

7.25

7.50

7.75

8.00

AA+ AA AA- A+ A A- BBB BBB-BBB+ BB+ BB

Yie

ld t

o m

atu

rity

(Y

TM

) in

%

*Composite rating BB- B+ B

* Notes: Yields as on 29-Dec-2017; Composite rating - please refer Appendix for definition and calculation method; Dubai is not rated by any rating agency and we have assigned a proxy rating

of ‘BBB+’ based on its fundamentals with a relative comparison to DEWA (BBB+) & Emirate of Sharjah (BBB+); Source: Bloomberg/FAB

16

Notes: * X-axis represents the composite rating (please refer Appendix for calculation method); Dubai is not rated by any rating agency and we have assigned a proxy rating of ‘BBB+’ based on

its fundamentals with a relative comparison to DEWA (BBB+) & Emirate of Sharjah (BBB+). The ratings have been arranged from higher to lower starting from ‘AA’, followed by ‘AA-’ and so on;

CDS levels are for 29-Dec-17 & in basis points; Source: Bloomberg/FAB

GCC sovereign credit ratings & CDS spreads versus peers

Bahrain

Turkey

Russia

Indonesia

India

Dubai*

SpainMalaysia

Italy

Poland

Kingdom of Saudi Arabia

China

Japan

South Korea

Abu Dhabi

Qatar

UKFranceAustria Belgium

Hong Kong

Kuwait

Brazil

0

20

40

60

80

100

120

140

160

180

200

220

240

260

280

CD

S (

bp

s)

The chart shows that Gulf sovereigns are rated favourably as

compared to many of their peers from the EMEA region.

AA+ AA AA- A+ A A-AAA BBB BBB-BBB+ BB+ BB BB-

Indeed Abu Dhabi and Kuwait have maintained their AA

ratings from all major rating agencies amid a persistent low oil

price environment. The ratings of these sovereigns underpin

the fact that they have substantial reserves and a range of

tools available to them to deal with the new normal of oil price

and other geo-political threats.

17Notes: Curves as on 29-Dec-2017; “S” in the ticker indicates that the bond is Islamic (sukuk); Source: Bloomberg/FAB

GCC sovereign curves

3.000

4.000

5.000

6.000

7.000

8.000

OMAN 3.875 03/22

BHRAIN 7.5 09/47

BHRAIN 6.125 07/22

BHRAIN 7 10/28

DUGB 6.45 05/22 S

DUGB 5.25 01/43OMAN 5.375 03/27

OMAN 6.5 03/47

2.500

2.750

3.000

3.250

3.500

3.750

4.000

4.250

4.500

4.750

5Y 10Y 30Y~5-year bonds ~10-year bonds ~30-year bonds

KUWIB 2.75 03/22

ADGB 2.5 10/22

QATAR 4.5 01/22

QATAR 4.625 06/46

KSA 2.894 04/22 S

KSA 4.625 10/47

ADGB 4.125 10/47

DUGB 5 04/29 S

18

GCC credit quality at a glance

Un

ite

d A

rab

Em

ira

tes

(U

AE

)

Em

ira

te o

f A

bu

Dh

ab

i

Ku

wa

it

Qa

tar

Kin

gd

om

of

Sa

ud

i A

rab

ia

Em

ira

te o

f R

as

Al-

Kh

aim

ah

Em

ira

te o

f S

ha

rja

h

Em

ira

te o

f D

ub

ai*

Su

ltan

ate

of

Om

an

Kin

gd

om

of

Bah

rain

3

4

5

6

7

8

9

10

11

12

13

14

15

Co

mp

os

ite

Ra

tin

g Mubad

ala

IPIC

TD

IC

Wa

ha

Ab

u D

ha

bi C

rud

e O

il P

ipe

lin

e

Qa

tari

Dia

r

Qa

tar

Pe

tro

leu

m

Eti

sa

lat

RA

SG

AS

Ind

us

trie

s Q

ata

r

Do

lph

in E

ne

rgy

QG

TS

(N

ak

ila

t)

SE

CO

SA

BIC

Eti

had

Oo

red

oo

(Q

tel)

Qa

tar

Rein

su

ran

ce

Sa

ud

i T

ele

co

m

Ta

qa

DE

WA

MA

F

DIF

C I

nve

stm

en

t

DP

Wo

rld

JA

FZ

Ald

ar

EQ

UA

TE

Pe

tro

ch

em

OM

GR

ID

Em

aa

r M

all

s G

rp

Ku

wa

it P

roje

cts

Co

Em

aa

r P

rop

Ma

zo

on

Ele

ctr

icit

y C

o

Du

ba

i In

v P

ark

Oil

an

d G

as

Ho

ldin

g

Ezd

an

Ho

ldin

g

Dam

ac

Inve

stc

orp

Mu

mta

lak

at

Bate

lco

Dar

Al

Ark

an

2

3

4

5

6

7

8

9

10

11

12

13

14

15

0 1 2 3 4 5 6 7 8 9 10111213141516171819202122232425262728293031323334353637383940

Co

mp

os

ite

Ra

tin

g

IsDB

FA

B

NB

K

QN

B

Al-

Hil

al

UN

B

Ind

Ba

nk

of

Ku

wa

it

Ku

wa

it In

tl B

an

k

AD

CB

AD

IB

Do

ha

Ba

nk

QIB

QII

B

Al

Ah

li B

an

k o

f K

uw

ait

KF

H

CB

K

Gu

lf B

an

k

INT

BO

Q

Intn

l B

an

k o

f Q

ata

r

Em

ira

tes

Is

lam

ic B

an

k

Ah

li B

an

k Q

SC

Bo

ub

ya

n b

an

k

CB

Q

Al

Kh

ali

j

NC

B

Sa

mb

a

Al

Ra

jhi

SA

BB

Riy

ad

Ba

nk

Du

ba

i Is

lam

ic B

an

k

No

or

Gu

lf In

v C

orp

Bu

rga

n B

an

k

Wa

rba

Ba

nk

Ma

sh

req

BS

F

Ara

b N

ati

on

al B

an

k

Sa

ud

i H

oll

an

di

Sa

ud

i In

v B

an

k

Gu

lf In

tl B

an

k

Co

m B

an

k o

f D

ub

ai

Ta

mw

ee

l

Ba

nk

of

Sh

arj

ah

Sh

arj

ah

Is

lam

ic B

an

k

RA

KB

AN

K

NB

F (

Fu

jair

ah

)

HS

BC

Ba

nk

Om

an

UA

B

Ah

li U

nit

ed

Ba

nk

Om

an

Ara

b B

an

k

Ba

nk

Mu

sc

at

NB

O

AB

C

Ba

nk

Dh

ofa

r

Ba

nk

So

ha

r

Ah

li B

an

k S

AO

G

Al

Ba

rak

a B

an

kin

g G

rou

p

NB

B

BB

K

GF

H

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

0 2 4 6 8 10 12 14 16 18 20 22 24 26 28 30 32 34 36 38 40 42 44 46 48 50 52 54 56 58 60

Co

mp

os

ite

Ra

tin

g

AA

AA-

A+

A

A-

BBB+

BBB

BBB-

BB+

BB

BB-

B+

AA+

B-

GCC Sovereigns GCC Corporates

AA+

AA

AA-

A+

A

A-

BBB+

BBB

BBB-

BB+

BB

BB-

B+

GCC Financials

AA+

AA

AA-

A+

A

A-

BBB+

BBB

BBB-

BB+

BB

AAA

BB-

B+

B

Notes: The ratings mentioned here are composite credit rating for each issuer. Please see appendix for the methodology of calculating composite credit rating; * Dubai is not rated by any rating agency and we

have assigned a proxy rating of ‘BBB+’ based on its fundamentals with a relative comparison to DEWA (BBB+) and Emirate of Sharjah (BBB+); Source: Bloomberg/FAB

19

GCC spread performance summary – FY 2017

Top 10 / bottom 10 bond/sukuk performers (z-spread, bps) in each category from 30th Dec 2016 to 29th Dec 2017

-80-70-60-50-40-30-20-1001020304050

+43

+24

+10

+8

+6

+5

-2

-3

-3

-5

-34

-36

-37

-39

-41

-45

-49

-59

-60

-77

Sovereigns

DUGB 43

DUGB 21 PUTA

DUGB 20

BHRAIN 22

DUGB 22 (S)

KSA 26

OMAN 22 *8/3/17

KSA 27 (S) *20/4/17

OMANGS 24 (S) *1/6/17

QATAR 30

KSA 23 *4/10/17

ADGB 47 *11/10/17

BHRAIN 29 *20/9/17

OMAN 26

BHRAIN 28

ADGB 27 *11/10/17

ADGB 22 *11/10/17

OMAN 47 *8/3/17

BHRAIN 47 *20/9/17

QATAR 23 (S)

-175-150-125-100-75-50-250255075100125

+98

+53

+44

+37

+32

+32

+16

+15

+8

-5

-79

-80

-81

-82

-91

-93

-131

-133

-142

-156

Financials

BGBKKK Jr Sub PERP

Nxt C: 30-09-2019

ALHILA (S) Jr Sub PERP

Nxt C: 30-06-2019

EBIUH Jr Sub PERP Nxt

C: 30-05-2019

AUBBI Jr Sub PERP Nxt

C: 29-04-2020

RAKBNK 19

DIBUH (S) Jr Sub PERP

Nxt C: 20-03-2019

EBIUH Jr Sub PERP Nxt

C: 17-09-2020

EBIUH 22 €

ADCBUH 23 Sub

NBOBOM Jr Sub PERP

Nxt C: 18-11-2020

QNBK 21

INTBOQ 20

QNBK 20

COMQAT 2.875 19

ABQKQD 21

ADCBUH Sub CALL Nxt C: 28-05-

2018

COMQAT 7.5 19

QIBKQD 22 (S) *23/5/17

QIBKQD 20 (S)

EBIUH Sub CALL Nxt C: 28-03-

2018

-250-200-150-100-50050100150200

+30

+0

-1

-3

-7

-9

-10

-10

-11

-13

-68

-68

-68

-69

-70

-72

-101

-129

-172

-213

Corporates

DAMACR 19 (S)

GMSEDU (S) Jr Sub

PERP Nxt C: 21-11-2018

DPWDU 37

JAFZSK 19 (S)

EMAAR 19 (S)

MAFUAE 19

ETISLT 19

ETISLT 21 €

INVCOR 20 (S)

KWIPKK 19

EMIRAT 25 SINK

QATIQD Sub PERP Nxt C: 13-

09-2022 *13/3/17

MUMTAK 21 (S)

OMGRID 27 *16/5/17

INTPET 41

KHDRWY 25 (S) SINK

OMGRID 25

KWIPKK 27 *23/2/17

ADNOUH 29 Sec *2/11/17

BATELC 20

Notes: (1) We have used a list of GCC public debt which are maturing in 2019 or beyond and for which FAB trading desk provides market price; (2) (S) in the ticker indicates Sukuk; (3) All

bonds/sukuks are $ denominated unless any other currency is highlighted in the ticker. (3) All bonds/sukuks are senior unsecured debt unless an abbreviation for the debt type is highlighted in the

ticker – e.g. – “Unsec” = Unsecured debt junior to Senior Unsecured debt; ; “Sub” = Subordinated; “Sr Sub” = Senior Subordinated; “Jr Sub” = Junior Subordinated; “Perp” = Perpetual; Callable,

Puttable and Sinkable highlighted as “Call”, “Puta”, & “Sink” respectively; (4) * highlights spread change from the 1st settlement date of the bond as it was issued in 2017; Source: FAB/Bloomberg

20

GCC’s major primary deals in 2017 and their performance

Secondary market performance since issue (change in z-spread and cash price since issue till 29-Dec-17)

ADNOUH 4.6 47 Sec SINK (10/10)

ESCWPC 4.45 35 Sec SINK (29/11)

ADGB 4.125 47 (2/10)

MUBAUH 3.75 29 (11/04)

FABUH 3 22 (27/03)

ADNOUH 3.65 29 Sec (26/10)

MUBAUH 3 24 (11/04)

ADGB 2.5 22 (2/10)

ADGB 3.125 27 (2/10)

INVCOR 5 27 (S) (25/01)

DAMACR 6.25 22 (S) (11/04)

MAFUAE 5.5 Jr Sub PERP NC5 (28/02)

BOSUH 4.23 22 (28/02)

DIBUH 3.664 22 (S) (7/02)

REITDU 5.125 22 (S) (5/12)

EBIUH 3.25 22 (7/11)

KUWIB 3.5 27 (13/03)

WARBAB 6.5 (S) Jr Sub PERP NC5 (7/03)

EQPCKW 3.944 24 (S) (13/02)

ALAHKW 3.5 22 (29/03)

KUWIB 2.75 22 (13/03)

KWIPKK 4.5 27 (16/02)

NTBKKK 2.75 22 (22/05)

KSA 4.625 47 (27/09)

INTLWT 5.95 39 Sec SINK (2/05)

KSA 3.628 27 (S) (12/04)

KSA 3.625 28 (27/09)

APICOR 3.141 22 (S) Unsec (25/10)

KSA 2.894 22 (S) (12/04)

ISDB 2.393 22 (S) (5/04)

KSA 2.875 23 (27/09)

ISDB 2.261 22 (S) (14/09)

DARALA 6.875 22 (S) (5/04)

OILGAS 7.5 27 (18/10)

OMAN 3.875 22 (1/03)

OMAN 3.875 22 (1/03)

MAZOON 5.2 27 (S) (23/10)

OMANGS 4.397 24 (S) (23/05)

OMGRID 5.196 27 (9/05)

BHRAIN 5.25 25 (S) (6/09)

BHRAIN 6.75 29 (6/09)

OMAN 6.5 47 (1/03)

GULINT 3.5 22 (18/01)

BHRAIN 7.5 47 (13/09)

QATIQD 4.95 Sub PERP NC5 (6/03)

BARKAB 7.875 (S) Sub PERP NC5 (23/05)

ABQKQD 3.5 22 (15/02)

QIBKQD 3.251 22 (S) (16/05)

ERESQD 4.875 22 (S) (29/03)

-100 -75 -50 -25 0 25 50 75 100 125 150 175 200

+196.0

+44.0

+19.1

-10.5

+143.5

+24.3

-2.5

-32.3

-28.8

-9.7

-35.6

-13.5

+10.5

-39.2

-11.6

-39.1

+90.0

-3.9

-5.1

-20.9

-20.6

-18.4

-17.2

-36.7

-42.7

-20.3

-17.7

-0.7

-26.2

-50.1

-49.0

-59.6

-29.8

-5.6

-7.7

-51.6

-59.5

-52.3

-99.4

-62.1

+5.9

+8.3

-13.3

+0.2

-14.5

-22.8

-2.7

-21.4

-23.9

-8.0 -7.0 -6.0 -5.0 -4.0 -3.0 -2.0 -1.0 0.0 1.0 2.0 3.0 4.0 5.0

-7.9

-2.9

-1.4

+0.7

-4.9

-4.2

-1.2

+0.5

+0.5

-0.5

+0.1

+0.3

+1.0

+1.3

+1.6

+2.6

-3.9

-1.1

-0.8

-0.7

-0.5

+0.1

+0.6

+1.3

+2.7

+3.2

-0.8

-0.2

+0.5

+1.1

+2.3

+2.5

+2.9

-0.3

+0.3

+1.2

+1.8

+2.3

+2.4

+4.5

-1.4

-1.3

-1.0

-0.7

0.0

+0.1

+0.2

+2.2

+2.9

Notes: (S) in the ticker indicates Sukuk; All bonds/sukuks are US$ senior unsecured debt of the issuer unless an abbreviation for the debt type is highlighted – e.g – “Unsec” = Unsecured debt; “Sub” =

Subordinated; “Sr Sub” = Senior Subordinated; “Jr Sub” = Junior Subordinated; “Perp” = Perpetual; Callable, Puttable and Sinkable highlighted as “Call”, “Puta”, & “Sink” respectively; Source: Bloomberg/FAB

Cash price change Bond/Sukuk (Pricing date in dd/mm) Z-spread change (in bps)*

Abu Dhabi

credits

UAE credits(Excluding Abu Dhabi)

Kuwait

credits

Saudi

credits

Oman

credits

Bahrain

credits

Qatar

credits

21

Sovereigns spread performance – Abu Dhabi

Notes: * Highlights spread change from the 1st settlement date of the bond as it was issued in 2017; Source: FAB/Bloomberg

AD

GB

19

AD

WA

20

SIN

K

AD

GB

21

AD

GB

22

*

11

/10

/17

AD

GB

26

AD

GB

27

*

11

/10

/17

AD

GB

47

*

11

/10

/17

-13

-26-18

+8

-10

+6

-3

0

15

30

45

60

75

90

105

120

135

150

165

180

z-s

pre

ad

(b

ps

)

MaturityLong

term

Short

term29-Dec-1730-Dec-16 Curve on 30-Dec-16 Curve on 29-Dec-17

22

Sovereigns spread performance – Kuwait

Notes: * Highlights spread change from the 1st settlement date of the bond as it was issued in 2017; Source: FAB/Bloomberg

KU

WIB

22

*2

0/3

/17

KU

WIB

27

*2

0/3

/17

-26

-30

40

50

60

70

80

90

100

110

120

130

z-s

pre

ad

(b

ps

)

MaturityLong

term

Short

term29-Dec-1730-Dec-16 Curve on 30-Dec-16 Curve on 29-Dec-17

23

Sovereigns spread performance – Qatar

QA

TAR

19

QA

TAR

20

QA

TDIA

20

QA

TAR

21

QA

TAR

22

QA

TAR

23

(S)

QA

TAR

26

QA

TAR

30

QA

TAR

40

QA

TAR

42

QA

TAR

46

+43

-22

-14

-21

-9

+43

-10

-34

-21-20

-19

0

20

40

60

80

100

120

140

160

180

200

220

z-s

pre

ad

(b

ps

)

Maturity

29-Dec-1730-Dec-16

Long

term

Short

term

Notes: If "Sukuk" the ticker contains "(S)" next to the maturity year; Source: FAB/Bloomberg

Curve on 30-Dec-16 Curve on 29-Dec-17

24

Sovereigns spread performance – Saudi Arabia

KSA

21

KSA

22

(S)

*

20

/4/1

7

KSA

23

*

4/1

0/1

7

KSA

26

KSA

27

(S)

*

20

/4/1

7

KSA

28

*

4/1

0/1

7

KSA

46

KSA

47

*

4/1

0/1

7

-26 -21

-5

-41-37

-17

-21-20

50

70

90

110

130

150

170

190

210

230

z-s

pre

ad

(b

ps

)

Maturity

Notes: * Highlights spread change from the 1st settlement date of the bond as it was issued in 2017; If "Sukuk" the ticker contains "(S)" next to the maturity year; Source: FAB/Bloomberg

Long

term

Short

term29-Dec-1730-Dec-16 Curve on 30-Dec-16 Curve on 29-Dec-17

25

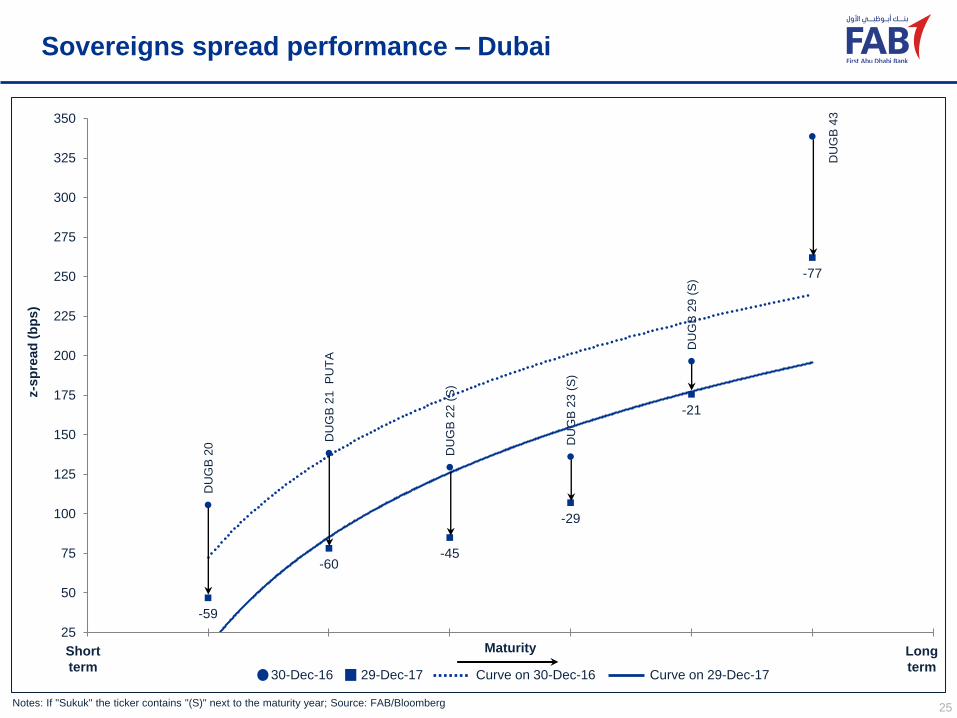

Sovereigns spread performance – Dubai

DU

GB

20

DU

GB

21

PU

TA

DU

GB

22 (

S)

DU

GB

23 (

S)

DU

GB

29 (

S)

DU

GB

43

-59

-60-45

-29

-21

-77

25

50

75

100

125

150

175

200

225

250

275

300

325

350

z-s

pre

ad

(b

ps

)

Maturity

29-Dec-1730-Dec-16

Long

term

Short

term

Notes: If "Sukuk" the ticker contains "(S)" next to the maturity year; Source: FAB/Bloomberg

Curve on 30-Dec-16 Curve on 29-Dec-17

26

Sovereigns spread performance – Sharjah

Notes: If "Sukuk" the ticker contains "(S)" next to the maturity year; Source: FAB/Bloomberg

SH

AR

SK

21

(S

)

SH

AR

SK

24

(S

)

-27

-19

60

70

80

90

100

110

120

z-s

pre

ad

(b

ps

)

MaturityLong

term

Short

term29-Dec-1730-Dec-16 Curve on 30-Dec-16 Curve on 29-Dec-17

27

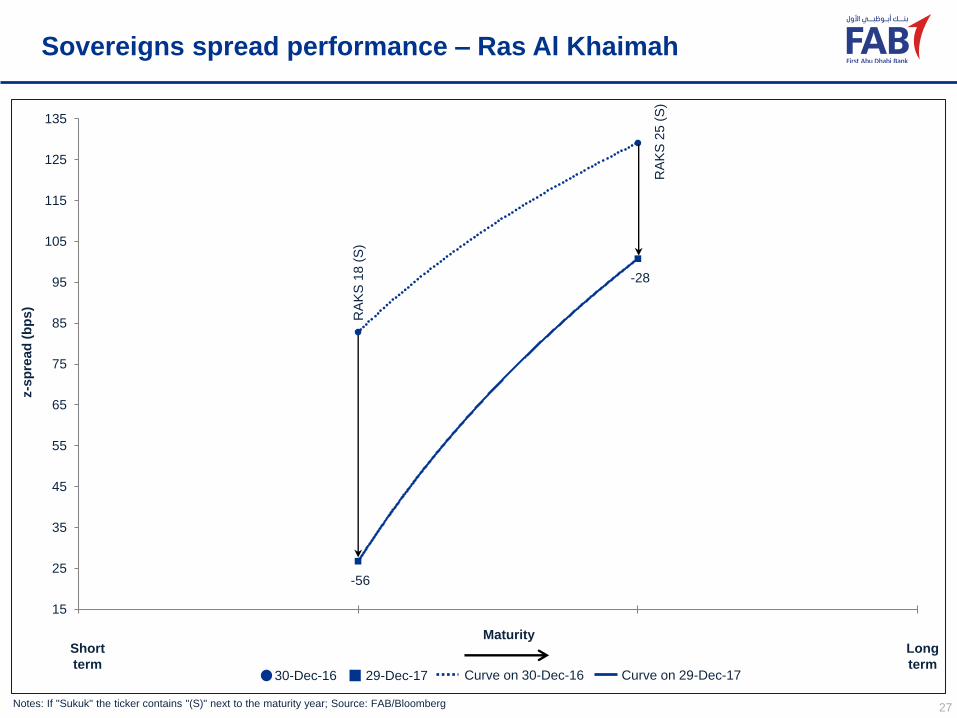

Sovereigns spread performance – Ras Al Khaimah

Notes: If "Sukuk" the ticker contains "(S)" next to the maturity year; Source: FAB/Bloomberg

RA

KS

18

(S

)

RA

KS

25

(S

)

-56

-28

15

25

35

45

55

65

75

85

95

105

115

125

135

z-s

pre

ad

(b

ps

)

MaturityLong

term

Short

term29-Dec-1730-Dec-16 Curve on 30-Dec-16 Curve on 29-Dec-17

28

Sovereigns spread performance – Oman

OM

AN

21

OM

AN

22

*

8/3

/17

OM

AN

GS

24

(S)

*1

/6/1

7

OM

AN

26

OM

AN

27

*

8/3

/17

OM

AN

47

*

8/3

/17

-32-39

-36

-2-12

+10

100

125

150

175

200

225

250

275

300

325

350

375

400

425

z-s

pre

ad

(b

ps

)

Maturity

29-Dec-1730-Dec-16

Long

term

Short

term

Notes: * Highlights spread change from the 1st settlement date of the bond as it was issued in 2017; If "Sukuk" the ticker contains "(S)" next to the maturity year; Source: FAB/Bloomberg

Curve on 30-Dec-16 Curve on 29-Dec-17

29

Sovereigns spread performance – Bahrain

BH

RA

IN 1

8 (

S) U

nse

c

BH

RA

IN 2

0 BH

RA

IN 2

1

BH

RA

IN 2

2

BH

RA

IN 2

3

BH

RA

IN 2

4 (

S)

BH

RA

IN 2

5 (

S) *

20

/9/1

7

BH

RA

IN 2

6

BH

RA

IN 2

8

BH

RA

IN 2

9 *

20

/9/1

7

BH

RA

IN 4

4

BH

RA

IN 4

7 *

20

/9/1

7

-28

-16

-33

-49

-20

-13 -32

-12

+5

-3

-28

+24

100

150

200

250

300

350

400

450

500

550

z-s

pre

ad

(b

ps

)

Maturity

29-Dec-1730-Dec-16

Long

term

Short

term

Notes: * Highlights spread change from the 1st settlement date of the bond as it was issued in 2017; If "Sukuk" the ticker contains "(S)" next to the maturity year; Source: FAB/Bloomberg

Curve on 30-Dec-16 Curve on 29-Dec-17

30

Appendix

Source: Bloomberg/FAB

➢ As mentioned in above slides, we have used “composite ratings” for the credit quality analysis – i.e. the average of the

ratings assigned by three leading rating agencies Moody’s, S&P and Fitch – in order to provide a more representative

view of the credit strength of each bank.

➢ The composite rating is calculated as follows:

• A score is assigned to the rating from each rating agency: AAA or equivalent being the best with a score of “1”,

followed by AA+ or equivalent as “2”, AA or equivalent as “3”, AA- or equivalent as “4” and so on;

• For example FAB is rated Aa3/AA-/AA- by Moody’s/S&P/Fitch. So the scores are 4/4/4;

• Hence the average of the scores is “4” which indicates a composite rating of “AA-” for FAB;

• In case the average score is not an absolute number – e.g. 4.33 (average of 4, 5, & 4 ) – the final score is derived by

rounding off the average score to the nearest whole number. In this case “4”.

Thank You

Contact:

Chavan Bhogaita / Rakesh Sahu

Market Insights & Strategy

Global Markets

First Abu Dhabi Bank

Tel: +971 2 6110 127

Market Insights & Strategy, FAB Global Markets

Please click here to view our recent publications

on MENA and Global Markets