GBE Project Report

6

GBE Project Report Analysis of the French Wine Making Industry SUBMITTED TO: SUBMITTED BY: Prof. Pradip Chakrabar ty Hitaishi Gupta(043026)

-

Upload

deepanshu-chandra -

Category

Documents

-

view

226 -

download

0

Transcript of GBE Project Report

8/4/2019 GBE Project Report

http://slidepdf.com/reader/full/gbe-project-report 1/6

GBE Project Report

Analysis of the French

Wine Making Industry

SUBMITTED TO: SUBMITTED BY:

Prof. Pradip Chakrabarty Hitaishi Gupta(043026)

8/4/2019 GBE Project Report

http://slidepdf.com/reader/full/gbe-project-report 2/6

Analysis of French Wine Making Industry

FORE School of Management 2010-2012 |IMG

FRENCH BUSINESS ENVIRONMENT

ECONOMIC CONDITIONS

• World’s 5th largest economic power, at the heart of 495 million-strong consumer market.

• 3rd leading destination worldwide for FDI, 2nd only to the U.S. and the U.K.

• World’s 5th largest exporter of goods and services.

• 48% of French listed companies owned by international investors.

With a GDP of $2.865 trillion, France is the world’s fifth-largest economy. It has substantial

agricultural resources, a large industrial base, and a highly skilled work force. A dynamic services

sector accounts for an increasingly large share of economic activity and is responsible for nearly all

job creation in recent years. France became one of the first European countries to officially exit

recession by posting a 1.2% growth (quarter on quarter annualized) in the second quarter of 2009, and

then 1.2% growth (annualized) in the third. Government’s economic policy aims to promote

investment and domestic growth in a stable fiscal and monetary environment. Creating jobs and

reducing the high unemployment rate has been a top priority.

POLITICAL CONDITIONS After his inauguration in May 2007 as France's sixth president under the Fifth Republic, Nicolas Sarkozy

focused his first months in office on improving the performance of France's economy through

liberalization of labor markets, higher education, and taxes. Despite significant reform and

privatization over the past 15 years, the government continues to control a large share of economic

activity. Government spending, at 52.7% in 2008, is among the highest in the G-7. The government

continues to own shares in corporations in a range of sectors, including banking, energy production and

distribution, automobiles, transportation, and telecommunications. Befitting wine’s perceived luxury good

status, the general observation is that wine consumption per person increases as income increases.

CULTURAL AND LANGUAGE DIFFERENCES

The aspect of cultural differences seems to have no significant bearing in regard to the Europeancountries. Language problems, not cultural differences are perceived as a trade barrier with France. InFrance, the willingness to communicate in English seems not exceptionally high, and as few companieshave English-speaking employees, starting business with France is perceived as more difficult than withother EU Nations.

8/4/2019 GBE Project Report

http://slidepdf.com/reader/full/gbe-project-report 3/6

Analysis of French Wine Ma

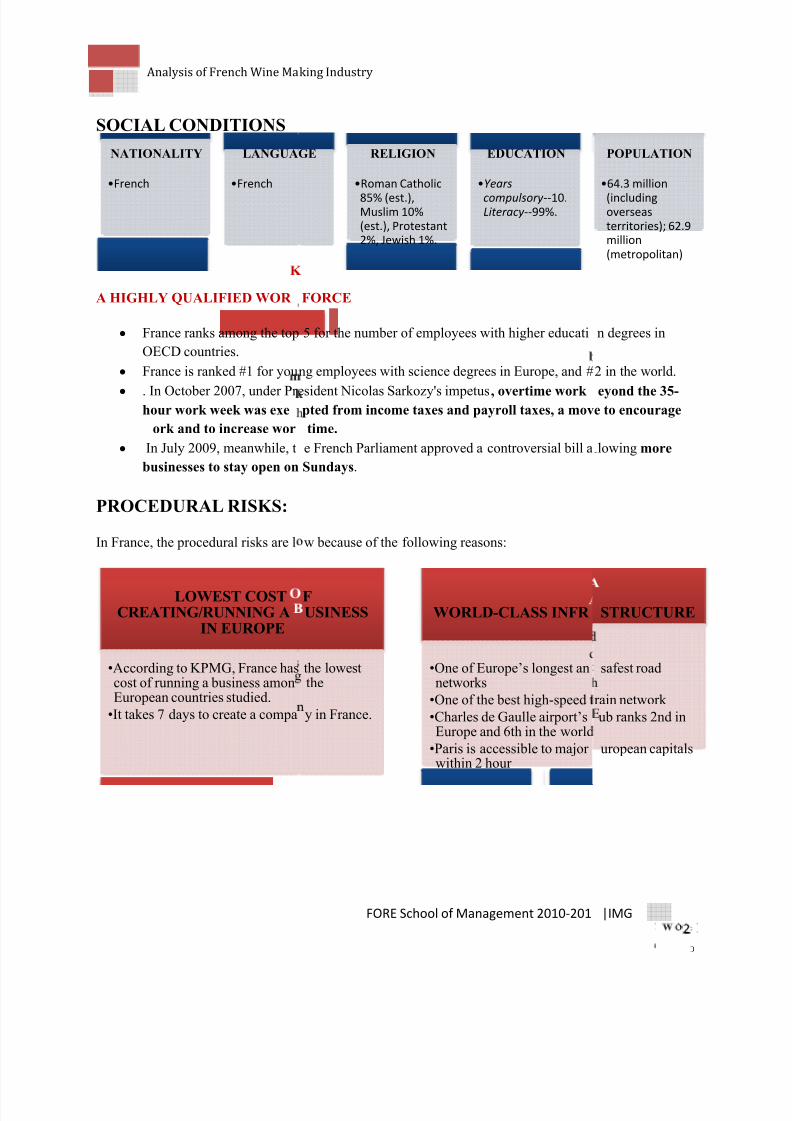

SOCIAL CONDITIONS

A HIGHLY QUALIFIED WOR

• France ranks among the top

OECD countries.

• France is ranked #1 for you

• . In October 2007, under Pr hour work week was exe

ork and to increase wor

• In July 2009, meanwhile, t

businesses to stay open on

PROCEDURAL RISKS:

In France, the procedural risks are l

NATIONALITY

•French

LANGUA

•French

LOWEST COST

CREATING/RUNNING A

IN EUROPE

•According to KPMG, France hascost of running a business amonEuropean countries studied.

•It takes 7 days to create a compa

king Industry

FORE School of Management 2010-201

FORCE

5 for the number of employees with higher educati

ng employees with science degrees in Europe, and #

esident Nicolas Sarkozy's impetus, overtime work pted from income taxes and payroll taxes, a mov

time.

e French Parliament approved a controversial bill a

Sundays.

w because of the following reasons:

GE RELIGION

•Roman Catholic

85% (est.),Muslim 10%

(est.), Protestant

2%, Jewish 1%.

EDUCATION

•Years

compulsory --10.Literacy --99%.

F

USINESS

the lowestthe

y in France.

WORLD-CLASS INFR

•One of Europe’s longest annetworks

•One of the best high-speed t

•Charles de Gaulle airport’sEurope and 6th in the world

•Paris is accessible to major within 2 hour

|IMG

n degrees in

2 in the world.

eyond the 35-e to encourage

llowing more

POPULATION

•64.3 million

(includingoverseas

territories); 62.9

million

(metropolitan)

STRUCTURE

safest road

rain network

ub ranks 2nd in

uropean capitals

8/4/2019 GBE Project Report

http://slidepdf.com/reader/full/gbe-project-report 4/6

Analysis of French Wine Making Industry

FORE School of Management 2010-2012 |IMG

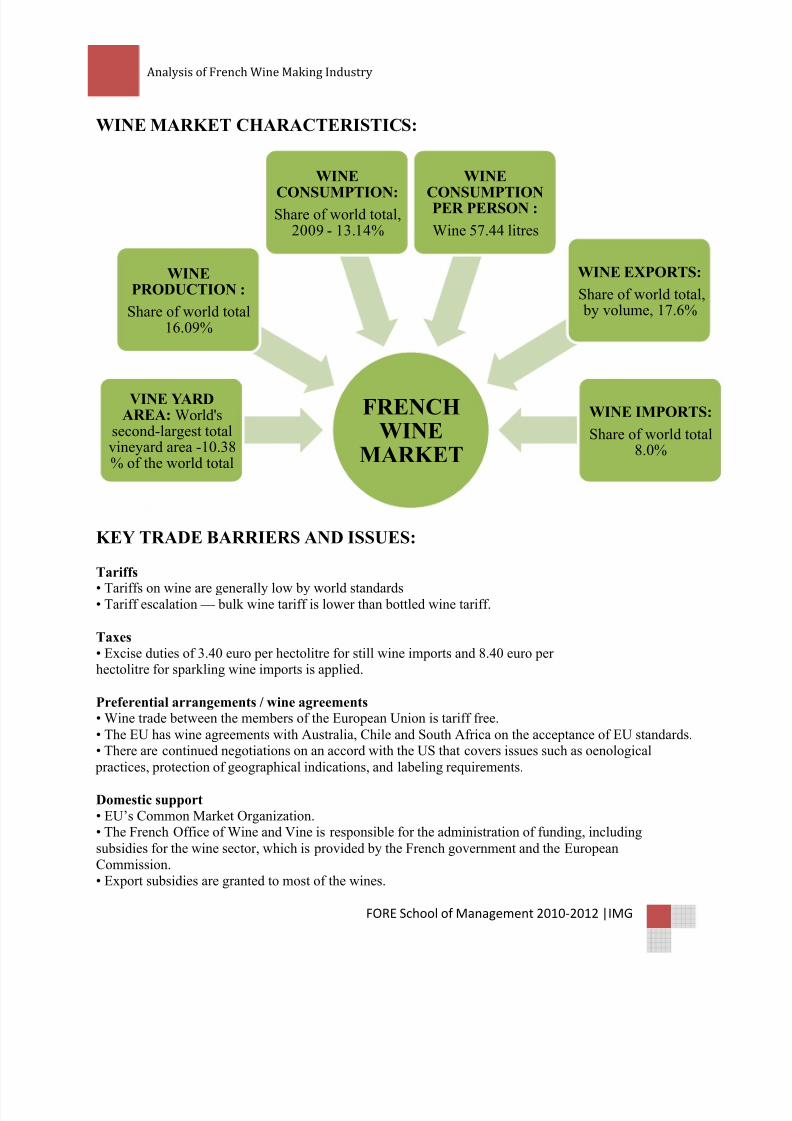

WINE MARKET CHARACTERISTICS:

KEY TRADE BARRIERS AND ISSUES:

Tariffs

• Tariffs on wine are generally low by world standards• Tariff escalation — bulk wine tariff is lower than bottled wine tariff.

Taxes

• Excise duties of 3.40 euro per hectolitre for still wine imports and 8.40 euro per hectolitre for sparkling wine imports is applied.

Preferential arrangements / wine agreements• Wine trade between the members of the European Union is tariff free.• The EU has wine agreements with Australia, Chile and South Africa on the acceptance of EU standards.• There are continued negotiations on an accord with the US that covers issues such as oenological practices, protection of geographical indications, and labeling requirements.

Domestic support

• EU’s Common Market Organization.• The French Office of Wine and Vine is responsible for the administration of funding, includingsubsidies for the wine sector, which is provided by the French government and the EuropeanCommission.• Export subsidies are granted to most of the wines.

FRENCH

WINE

MARKET

VINE YARD

AREA: World'ssecond-largest totalvineyard area -10.38% of the world total

WINE

PRODUCTION :

Share of world total16.09%

WINE

CONSUMPTION:Share of world total,

2009 - 13.14%

WINE

CONSUMPTIONPER PERSON :

Wine 57.44 litres

WINE EXPORTS:

Share of world total, by volume, 17.6%

WINE IMPORTS:

Share of world total8.0%

8/4/2019 GBE Project Report

http://slidepdf.com/reader/full/gbe-project-report 5/6

Analysis of French Wine Making Industry

FORE School of Management 2010-2012 |IMG

Intellectual property protection

French wines are entitled to the Appellation d’Origine Contrôlée (AOC; ‘controlled name of origin’),which is based on a hierarchy of specific geographic areas known to produce the best wines. To receiveany of these rigorous appellations, wines must be produced within specific areas and must meet standardsof grape variety, alcoholic content, quantity of harvest, and techniques of vine growing and wine making.Typical examples are Champagne and Burgundy wines, which have geographical indication of being

French wine producing regions.

Sanitary and phytosanitary regulationsMost important to wine trade are the EU regulations requiring that imported wines not produced withwine making practices authorized for the production of EU wine be labeled as such. That is, the process by which wine is produced can be a barrier to market access even though there may be noscientific evidence to suggest that these processes are any less safe than traditional processes. This can bean important barrier to ‘New World’ producers of wine who may be using wine making practices that areinnovative and not proven to be unsafe but are not yet recognized by the European Union.

Technical requirementsWhile different regions may have their own different classifications of wines, all wines produced inFrance are subjected to very strict labeling laws to protect consumers. The French Government hasinstituted regulations that limit alcohol advertising on radio, television, point of sale and eventsponsorship.

Technological Innovation

Another important factor affecting wine production is the development and adoption of technologicalinnovation in both grape growing and wine making. New World wine producers have enjoyed largeincreases in both the quantity and quality of wine produced due in part to the adoption of new andimproved technologies. In contrast, countries within the European Union have become locked intospecific production technologies through strict government regulation that has stifled any ability for

productivity improvements and to some extent reduced their competitiveness in international markets.

Organizations: L'Office national interprofessionnel des vins, abbreviated ONIVINS, is a French association of vintners.

CONCLUSION:

From the study of the French business environment, I would like to conclude that though starting a winemaking industry in France would have the following advantages:

• Low procedural risk (It takes 7 days to start a business in France).• Trade among EU Nations is tariff free. • Highly productive and qualified labour

• French wines have a good brand image.

• 17.6 % of the world’s wines is exported by France.

• 13.14 % of the world’s wine is consumed by France

8/4/2019 GBE Project Report

http://slidepdf.com/reader/full/gbe-project-report 6/6

Analysis of French Wine Making Industry

FORE School of Management 2010-2012 |IMG

But starting a wine making industry in France has the following disadvantages:

• LACK OF GOOD QUALITY: The appellation d’origine controlee (AOC) system is to be praised for its role in preserving wine diversity. But it fails to ensure quality.Marketing wines by AOC (e.g. Chablis) simply doesn’t work. It assumes that regulationsabout yield, site, pruning, harvesting and so on ensure a certain level of quality. Thatthey don’t is evidenced by the fact that all appellations still produce lots of rubbish wine,and that the average level attained is mediocrity. In the new world the brand owners arethe producers, and they have a very strong incentive to maintain quality.

• LANGUAGE BARRIERS: Lack of English speaking labour. Learning French iscompulsory.

• LACK OF INNOVATION: AOC also fails spectacularly for cheap wines, and has been part of the reason that France has largely failed to produce successful brands. Exportmarkets have grown fussy: the Australians have been able to make cheap wine through

innovation, which tastes OK, so the same is expected of the French.

• LACK OF ADVERTISING AND PROPER DEMAND ANALYSIS: The Frenchattitude has for too long been one of make the wine first, then try to sell it. It’s the wrongway round. Things have changed over recent years. There is now a global over-supply of wine. The UK marketplace has been wooed by the wines of Australia, Chile, Argentinaand South Africa, all of whom have been able to make cheap wines that taste good andwhich are easy to understand. They are also made in the sorts of quantities to match thedemands of the supermarkets (where most wine is now sold), and support promotionalcampaigns targeted around single brands. These days, people who want to succeed in selling their wines look at the market and what it wants before they even crush a grape.

• LACK OF COMMERCIAL DRIVE: The modern marketplace is a tough one. At thetop end, France has nothing to fear. It makes a diverse range of profound fine wines thatthe new world can’t even begin to match. But the bulk of its production is morecommercial wine, and this is currently very hard to sell because it is uncompetitive.Outside the fine wine sector, the French look doomed unless they can do somethingquickly to turn their wine industry around.

After considering all the advantages and disadvantages of starting a business in France, I would like tosuggest that one should not start a wine making industry in France.

REFERENCES:

• http://www.wineinstitute.org/resources/statistics

• http://www.intracen.org

• http://en.wikipedia.org/wiki/Economy_of_France

• http://en.wikipedia.org/wiki/French_wine