Gas Transmission and Distribution Development in Indonesia · Medan – SBU III Capacity = 46...

22

Gas Gas Transmission and Distribution Transmission and Distribution Development in Indonesia Development in Indonesia Uji Subroto Santoso Uji Subroto Santoso PT PGN (Persero) Tbk. PT PGN (Persero) Tbk.

-

Upload

duongthuan -

Category

Documents

-

view

217 -

download

0

Transcript of Gas Transmission and Distribution Development in Indonesia · Medan – SBU III Capacity = 46...

Gas Gas Transmission and Distribution Transmission and Distribution Development in IndonesiaDevelopment in Indonesia

Uji Subroto SantosoUji Subroto SantosoPT PGN (Persero) Tbk.PT PGN (Persero) Tbk.

- 2 -

Agenda2

• PGN’s Business Overview.

• Indonesia Gas Industry

• Natural Gas Development & Utilization

- 3 -

3

PGN’s Business Overview

- 4 -

Company Overview4

• PGN is an Indonesia state company in downstream natural gas business activities.

• PGN controls 87% market share of transmission business (743.14 MMScfd) and 93% of distribution (551.28 MMScfd), providing natural gas to its costumers on industrial, commercial and household sector.

• Listed on Indonesia Stock Exchange, and known as PGAS. The Republic of Indonesia currently retains a 55% of PGAS shares while the remaining is owned by the public.

Gas PurchaseGas Purchase

Upstream

Upstream

TransportationTransportation

PGNDistribution

SSWJ

PGNDistribution

SSWJ

• SSWJ (PGN)• Grissik – Duri (TGI)• Grissik – Singapore (TGI)

• SSWJ (PGN)• Grissik – Duri (TGI)• Grissik – Singapore (TGI)

• Retail & Industry

Customers

• IPP

• Retail & Industry

Customers

• IPP

PGNTransmission

PGNTransmission

• Chevron

• Singapore

• Chevron

• Singapore

Sales (GSA)Sales (GSA)

GTAGTA

GSPAGSPA

Gas Transmission Contract (GTA)

– Long-term contract

– Minimum ship-or-pay volumes

– Tariffs in US$

Gas Transmission Contract (GTA)

– Long-term contract

– Minimum ship-or-pay volumes

– Tariffs in US$

Gas Supply for Distribution Business Gas Supply for Distribution Business

Gas Sales & Purchase Agreement (GSPA)

–Long-term contract

–Take-or-pay volumes

–Fix price in US$

Gas Sales & Purchase Agreement (GSPA)

–Long-term contract

–Take-or-pay volumes

–Fix price in US$

Distribution – Sale of Gas to End UserDistribution – Sale of Gas to End User

Gas Sales Agreements (GSA)

– Minimum pay volumes

– Price in US$ & IDR

Gas Sales Agreements (GSA)

– Minimum pay volumes

– Price in US$ & IDR

Transmission–Transport Third Party’s Gas Transmission–Transport Third Party’s Gas

- 5 -

H1 2008 Industrial & Power PlantCustomer Consumption

H1 2008 Sales Volume by Customer Type

Chemical 20%

Power Plant 22%

Textile 4%

Food 7%

Ceramic 15%

Fabric Metal 4%

Others 4%

Basic Metal 6%

Glass 8%

Paper 9%

Wood 1%

99

Strong Distribution Customer Base

• Three customer categories: Household, Commercial, and Industrial .

• Industrial customers continue to dominate PGN’s customer base and drive PGN’s distribution business growth. As of June 30, 2008, sales volume of industrial customers was 544 MMScfd or equal to 98.7% of PGN’s sales.

- 6 -

Jakarta

Grissik

Pagardewa

Duri

Medan

KALIMANTAN

SUMATERA SULAWESI

JAWA

PAPUA

Grissik – Duri

Grissik – Singapore

Grissik – Pagardewa – Labuhan Maringgai – Muara Bekasi – Rawamaju (SSWJ II)

Pagardewa – Labuhan Maringgai – Cilegon (SSWJ I)

PLN – Medan

Transmission Pipeline Network

6

Completion of the SSWJ Gas Transmission Pipeline enables PGN and its 60%‐owned subsidiary, TGI, to operate transmission pipelines with a total length of 2109 km with capacity of 1,839 MMScfd. Of the capacity figure, 650 MMScfd is allocated for PGN internal use.

- 7 -

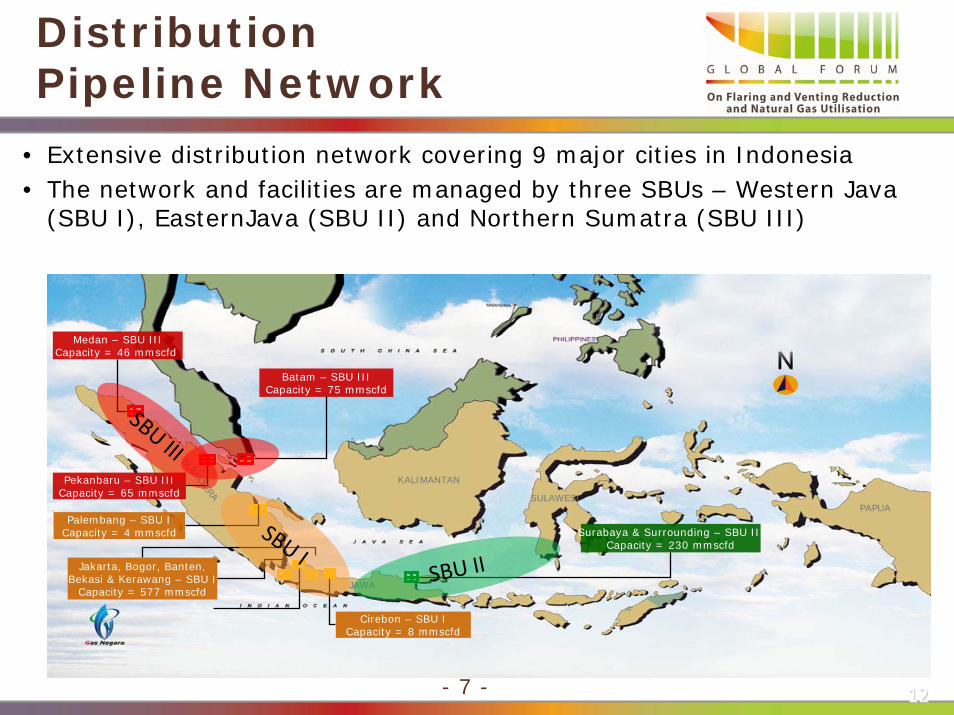

• Extensive distribution network covering 9 major cities in Indonesia• The network and facilities are managed by three SBUs – Western Java

(SBU I), EasternJava (SBU II) and Northern Sumatra (SBU III)

Distribution Pipeline Network

PAPUA

Medan – SBU IIICapacity = 46 mmscfd

Cirebon – SBU ICapacity = 8 mmscfd

Surabaya & Surrounding – SBU II Capacity = 230 mmscfd

Pekanbaru – SBU IIICapacity = 65 mmscfd

Palembang – SBU ICapacity = 4 mmscfd

Batam – SBU IIICapacity = 75 mmscfd

Jakarta, Bogor, Banten,Bekasi & Kerawang – SBU I

Capacity = 577 mmscfd

KALIMANTAN

SULAWESI

SUMATERA

JAWA

SBU III

SBU ISBU II

1212

- 8 -

8

Indonesia Gas Industry

- 9 -

Indonesia Gas Reserves

24.06

INDONESIA NATURAL GAS RESERVES (STATUS : 1 JANUARY 2008)

GAS RESERVES (TSCF)

Source: Directorate General Oil & Gas

• Indonesia has the largest proven natural gas reserves in Asia Pacific. As of Jan 2008, total gas reserves was 170.07 TSCF with 112.47 TSCF proven and 57.60 TSCF potential.

• Majority of the gas reserves are located in Sumatra and Kalimantan which far away from industrial areas.

- 10 -

Indonesia Gas Market Outlook

Contracted, Committed and Potential Gas Supply & Demand for Major Regions in Indonesia

55

J a k a r ta

G r is s ik

P a g a r d e w a

D u r i

D u m a i

M e d a n

K A L IM A N T A N

SUMATERA S U L A W E S I

J A W A

IR I A N J A Y A

S o u rc e : D irje n M ig a s

-1 1 8 .7-1 9 2 .2-1 8 3 .5B a la n c e

2 1 9 .72 1 9 .72 1 8 .5D e m a n d

1 0 12 7 .53 5S u p p ly

2 0 1 12 0 0 92 0 0 7Y e a r

R E G I I (N O R T H S U M A T E R A )

-1 1 8 .7-1 9 2 .2-1 8 3 .5B a la n c e

2 1 9 .72 1 9 .72 1 8 .5D e m a n d

1 0 12 7 .53 5S u p p ly

2 0 1 12 0 0 92 0 0 7Y e a r

R E G I I (N O R T H S U M A T E R A )

2-2 6-1 4 2 .3B a la n c e

1 9 31 9 5 .71 4 3D e m a n d

1 9 51 6 7 .90 .7S u p p ly

2 0 1 12 0 0 92 0 0 7Y e a r

R E G IV (C E N T R A L J A V A )

2-2 6-1 4 2 .3B a la n c e

1 9 31 9 5 .71 4 3D e m a n d

1 9 51 6 7 .90 .7S u p p ly

2 0 1 12 0 0 92 0 0 7Y e a r

R E G IV (C E N T R A L J A V A )

-7 9 1 .3-7 2 9 .7-5 6 7 .8B a la n c e

3 4 9 1 .83 4 9 1 .72 9 8 1 .6D e m a n d

2 7 0 0 .52 7 6 1 .92 4 1 3 .8S u p p ly

2 0 1 12 0 0 92 0 0 7Y e a r

R E G II I (C E N T R A L , S O U T H S U M A T E R A & W E S T J A V A )

-7 9 1 .3-7 2 9 .7-5 6 7 .8B a la n c e

3 4 9 1 .83 4 9 1 .72 9 8 1 .6D e m a n d

2 7 0 0 .52 7 6 1 .92 4 1 3 .8S u p p ly

2 0 1 12 0 0 92 0 0 7Y e a r

R E G II I (C E N T R A L , S O U T H S U M A T E R A & W E S T J A V A )

-1 4 1 .7-4 7 .6-1 4 5 .6B a la n c e

9 6 3 .77 4 7 .35 6 5 .4D e m a n d

8 2 1 .97 9 4 .84 1 9 .8S u p p ly

2 0 1 12 0 0 92 0 0 7Y e a r

R E G V (E A S T J A V A )

-1 4 1 .7-4 7 .6-1 4 5 .6B a la n c e

9 6 3 .77 4 7 .35 6 5 .4D e m a n d

8 2 1 .97 9 4 .84 1 9 .8S u p p ly

2 0 1 12 0 0 92 0 0 7Y e a r

R E G V (E A S T J A V A )

REG II (NORTH SUMATERA) (MMSCFD)

Year 2007 2009 2011

Supply 35 27.5 101

Demand 481.5 526.7 535.7

Balance -446.5 -499.2 -434.7

REG III (CENTRAL, SOUTH SUMATERA & WEST JAVA)

Year 2007 2009 2011

Supply 2,413.8 2,761.9 3,100.5

Demand 3,557.6 4,408.6 4,467.3

Balance -1,143.8 -1,646.7 -1,366.8

REG IV (CENTRAL JAVA)

Year 2007 2009 2011

Supply 0.7 167.9 195.0

Demand 198 256.3 259.9

Balance -197.3 -86.6 -64.9

REG V (EAST JAVA)

Year 2007 2009 2011

Supply 419.8 794.8 981.9

Demand 926.4 1,155.3 1,351.7

Balance -506.6 -360.4 -369.7

Source: Directorate General Oil & Gas

- 11 -

11

RITJDGBN

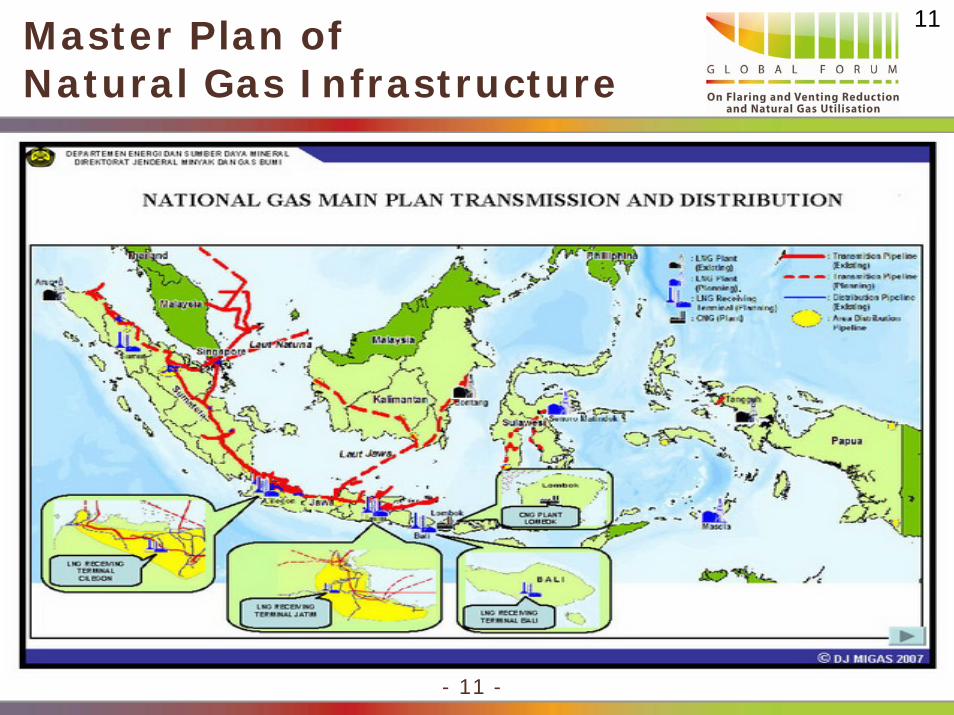

Master Plan of Natural Gas Infrastructure

- 12 -

12

Gas Production andUtilization in Indonesia

• Natural gas utilization (export and domestic) reached 2.805 TSCF in 2007 and expected to increase going forward.

• The GoI’s policy to promote domestic gas utilization by implementing Domestic Market Obligation to gas producers.

- 13 -

13

Natural Gas Development & Utilization

- 14 -

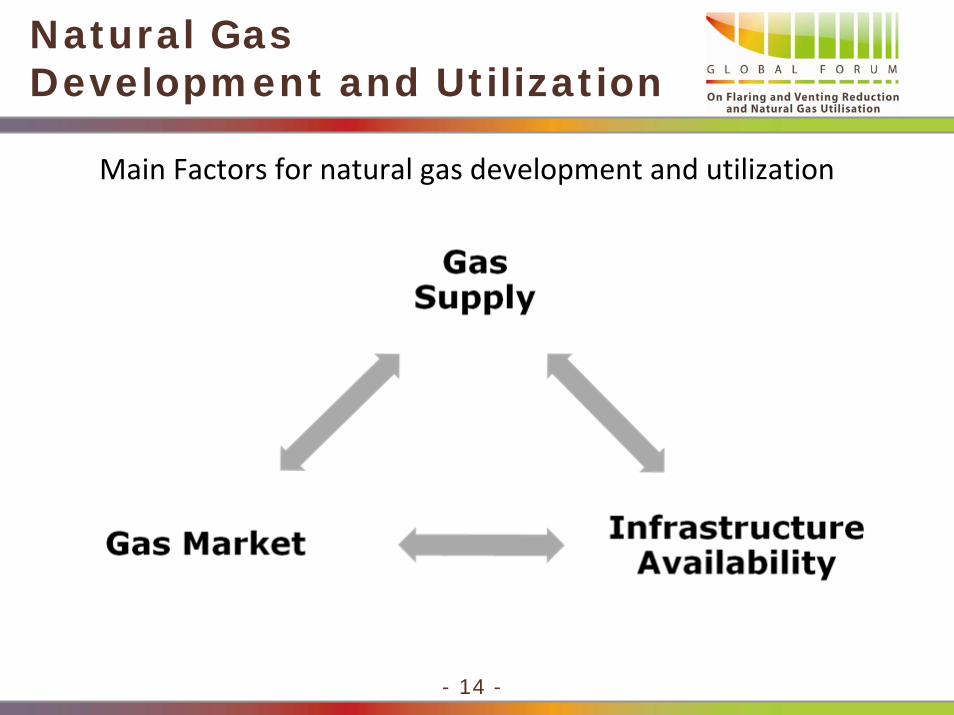

Main Factors for natural gas development and utilization

Natural Gas Development and Utilization

14

- 15 -

15

Security of Supply from Gas Producers

Certified gas volume

Supply period

Attractive Gas Price scheme

(1) Gas Supply

- 16 -

Gas Market Development

Opportunities & challenges•pricing dynamic promotes higher gas demand

•Gas price for industry•Environmental Issue•Limited gas infrastructures

- 17 -

Pricing Dynamics Promotes Gas Demand

Source: Pertamina

5.5

6.5

11.8

10.7

13.9

14.8

17.5

15.0

15.8

17.3

17.3

0 5 10 15 20

Distributed Gas

Kerosene (subsidized)

LPG (subsidized)

MFO (non‐subsidized)

HSD (subsidized)

LPG (non‐subsidized)

Gasoline (subsidized)

Diesel (non‐subsidized)

HSD (non‐subsidized)

Kerosene (non‐subsidized)

Gasoline (non‐subsidized)

USD / MMBtu

Relative Energy Price (as of November 1, 2008)

US$/MMBtu

5.49

15.76

PGN Gas Price Vs HSD Price

11/1/2008

Note: based on crude oil price of USD 68/barrel88

• Energy consumption in Indonesia reached 12.3 BScfd in 2007.

• Oil contribution to total energy consumption is declining due to the surging oil price and reducing oil subsidies in Indonesia.

• Oil subsidy reduction generates a major shift from oil to gas consumption of domestic industries.

Indonesia’s Energy Consumption by Energy Type

- 18 -

18

Optimization and Risk based infrastructure development

Gas pipelines categories as facilities for public interest by the law

Economic feasibility in transmission and distribution tender.

Other non‐pipe gas infrastructure development

Small scale LNG

CNG

Infrastructure Development

- 19 -

Third Parties Access (1)

Third parties access according Oil & Gas Law

Regulation by BPH Migas (Downstream Regulatory Agency)

Purpose of Open Access

Principles in Open Access implementation

Excess capacity

Technically Possible

Enhance economics viability

19

- 20 -

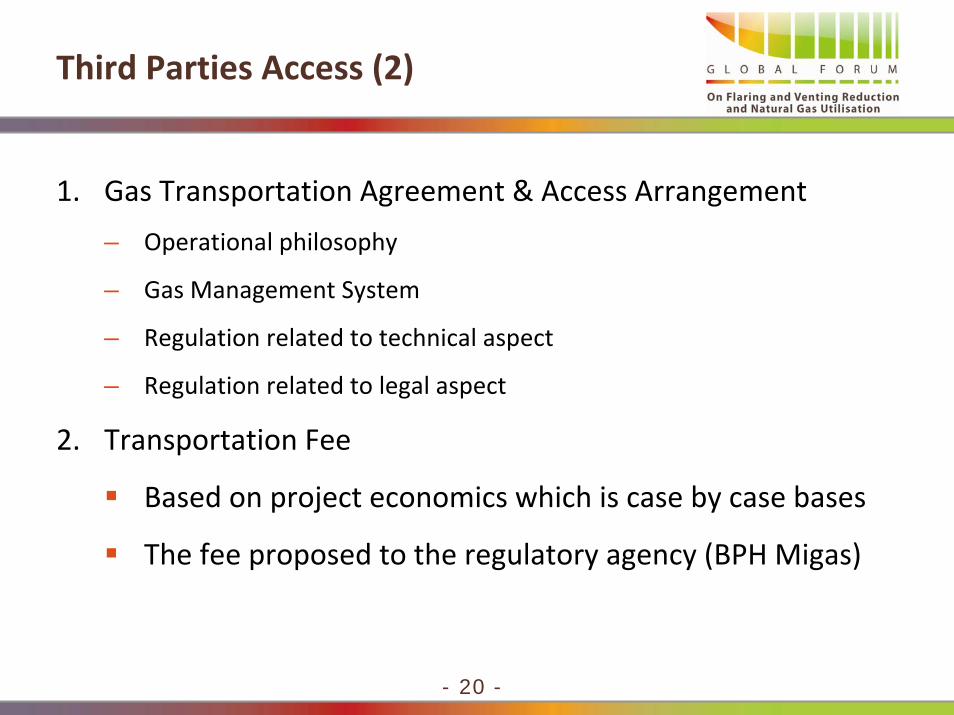

Third Parties Access (2)

1. Gas Transportation Agreement & Access Arrangement

– Operational philosophy

– Gas Management System

– Regulation related to technical aspect

– Regulation related to legal aspect

2. Transportation Fee

Based on project economics which is case by case bases

The fee proposed to the regulatory agency (BPH Migas)

- 21 -

REMARKS21

Given its low penetration and infrastructure coverage, natural gas infrastructure development is a very attractive investment opportunity in Indonesia Natural gas market in Indonesia is very attractive due to relatively cheaper gas price compared to oil based productTo accelerate nantural gas market development, new natural gas fields development is required. In addition there is also possibility to utilize other gas sources like CBM, Coal Gasification, and Flared Gas.To ensure economics of the gas infrastructure projects, gas availability with sufficient volume and supply period become key factors. Small scale LNG and CNG could be utilized as natural gas transportation mode for remote areas

- 22 -

22

PT Perusahaan Gas Negara (Persero) Tbk

Jl. K H Zainul Arifin No. 20, Jakarta 11140IndonesiaPh: 62 21 6334838 Fax: 62 21 6331632www.pgn.co.id

Thank YouThank You