Gas Supply Mechanism Session - · PDF fileGas Supply Mechanism Session Chair: ... Ben Sawford...

80

Gas Supply Mechanism Session Chair: Andrew Whittles (Low Emission Strategies) Ed Carter (National Grid) John Baldwin & Robert McKeon (CNG Services) Ben Sawford (Gasrec) Phil Lowndes (Gas Alliance Group)

Transcript of Gas Supply Mechanism Session - · PDF fileGas Supply Mechanism Session Chair: ... Ben Sawford...

Gas Supply Mechanism SessionChair:

Andrew Whittles (Low Emission Strategies)

Ed Carter (National Grid)John Baldwin & Robert McKeon (CNG Services)

Ben Sawford (Gasrec)Phil Lowndes (Gas Alliance Group)

Place your chosenimage here. The fourcorners must justcover the arrow tips.For covers, the threepictures should be thesame size and in astraight line.

Place your chosenimage here. The fourcorners must justcover the arrow tips.For covers, the threepictures should be thesame size and in astraight line.

Road Tanker Loading at Grain LNG

January 2014Ed Carter

3

Chicken & Egg!

4

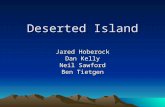

Grain LNG

Largest terminal in Europe and 8th largest in the World. 1,000,000m3 storage space 15 million tonnes per annum capacity (equivalent to 20% of UK gas

demand) 2 purpose built jetties (Qmax capable) Independent terminal operator, giving equitable customer service Key geographical location – close to London and at the gateway to/from

continental Europe Proven track record of delivering on its commitments and has over 30 years

experience in the LNG industry

Largest terminal in Europe and 8th largest in the World. 1,000,000m3 storage space 15 million tonnes per annum capacity (equivalent to 20% of UK gas

demand) 2 purpose built jetties (Qmax capable) Independent terminal operator, giving equitable customer service Key geographical location – close to London and at the gateway to/from

continental Europe Proven track record of delivering on its commitments and has over 30 years

experience in the LNG industry

5

Conversion to importation terminal

Originally built 1980 as apeak shaving plant

£140 million low costconversion

Purpose-built jetty 4.5km cryogenic corridor 55 berthing slots 20 yr fixed income

contract withBP/Sonatrach

~4% of UK demand

1959 1964 1980 2005 2008 2010

6

Phase 2 – Background / status

£390 million investment Tripling capacity to ~12% of UK demand Customers Centrica, GDF-Suez,

Sonatrach

Three tanks each of 190,000m3

Additional 110 berthing slots Commissioned November 2008 Ready for Difficult supply through Winter

1959 1964 1980 2005 2008 2010

7

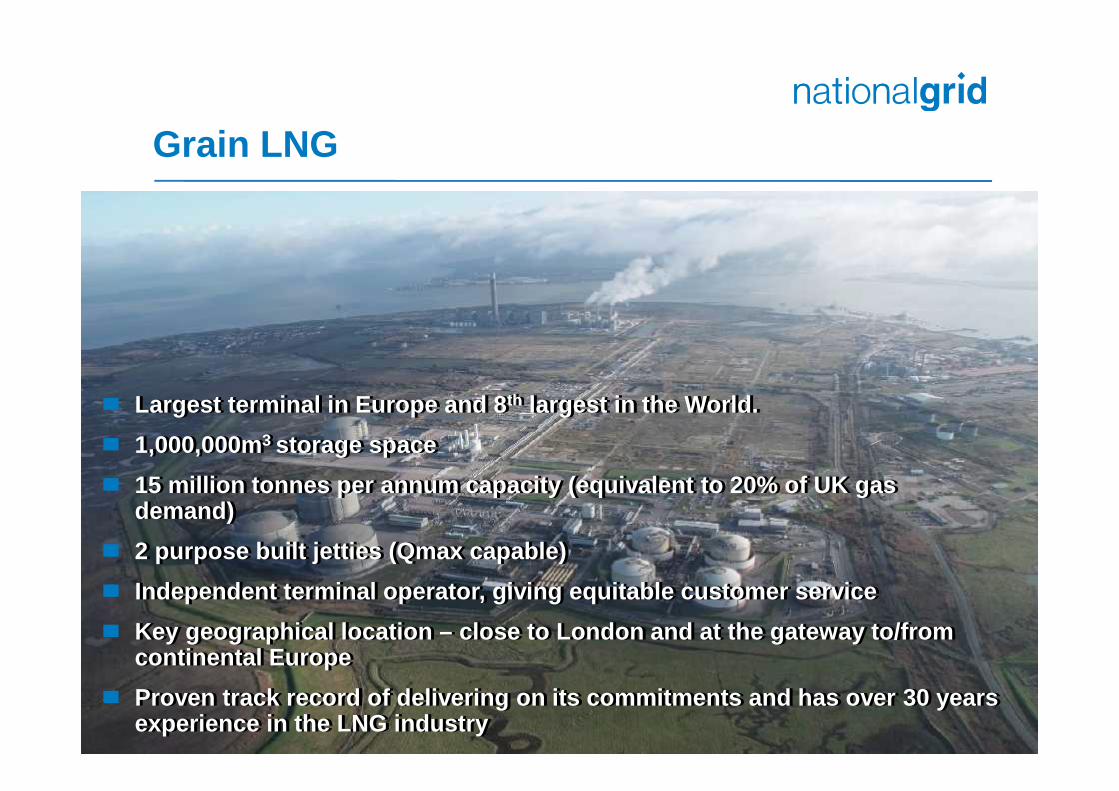

Phase 3

Commissioned December 2010 £310 million investment Total storage 1,000,000 m3

Total capacity ~20% of UK demand ~15mtpa of LNG (~20bcm/y of gas)

2nd jetty – Qmax compatible ~250 berthing slots sold Customers E.ON, Iberdrola &

Centrica

1959 1964 1980 2005 2008 2010

8

STFERGUS

TEESSIDE

BARROW

BACTON

THEDDLETHORPE

EASINGTON

ISLE OF GRAIN

DYNEVOR

AVONMOUTH

PARTINGTON

GLENMAVIS

Glenmavis• Commissioned 1971 – 1975• 2 tanks, 505 GWh• ~ 311 days to fill• Closed April 2012

Partington• Commissioned 1972• 4 tanks, 1122 GWh• ~ 459 days to fill• Closed April 2011

Dynevor• Commissioned 1983• 1 tank, 304 GWh• ~ 117 days to fill• Closed April 2009

Avonmouth• Commissioned 1978• 3 tanks, 876 GWh• ~ 374 days to fill

National Grid UK Peak LNG Storage Facilities

9

Market & Drivers Stricter environmental controls in

cities & ports LNG highly competitive against

gas oil on price Demand outstripping supply Facilitate Blue Corridor project

due to ideal location Enabling market for other areas

such as marine in the UK

Breakdown below in LNG equivalent

Total HFO Market = 3,564k tpa

Potential growth opportunities

Road Fuel ~ 200k tpa ( by 2020)

I&C ~ 600k tpa

Marine & Rail ~ 609k tpa

Avonmouth is currently UK’s only source of LNG for truck loading services

Historic Growth of NGVsin EU (~ 1.1M 2013)

DECC Energy Report - Gas/Diesel Oil 2011-2012

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2005 2006 2007 2008 2009 2010 2011 2012

Volu

me

(000

s To

nnes

)

Gas/Diesel OilLNG Equivelant

Grain LNG

10

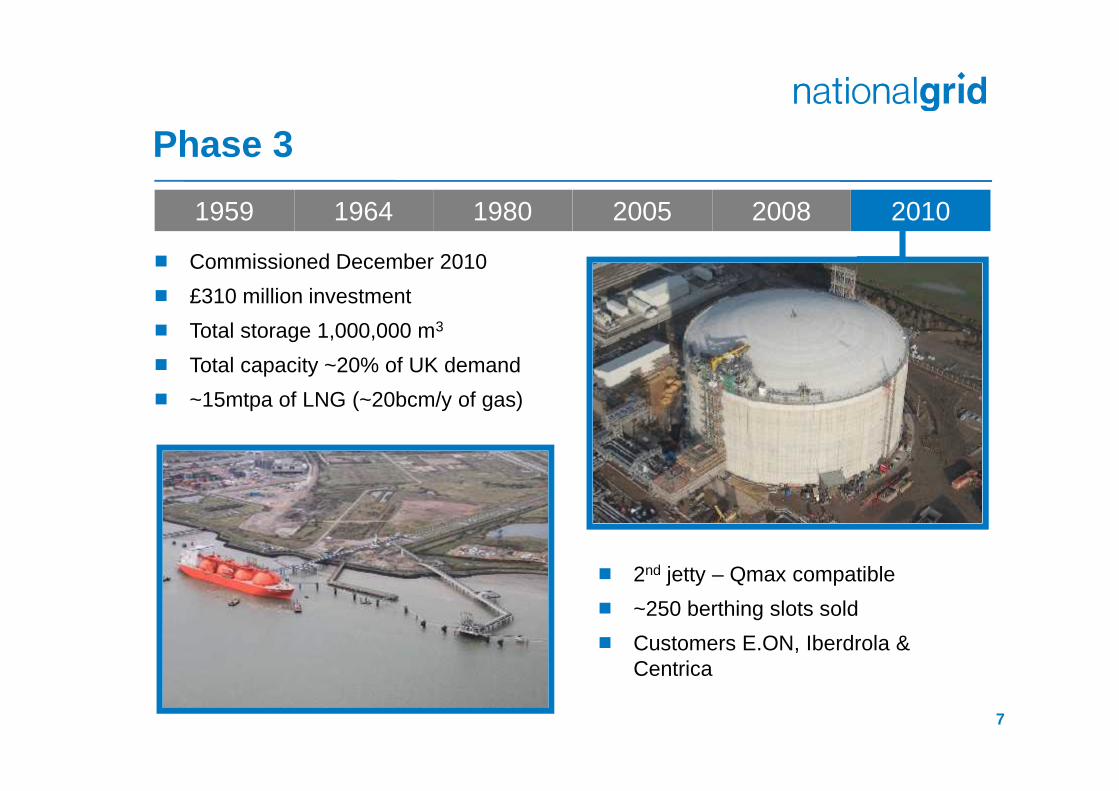

Truck Loading Facility

Go LIVE

Initial capacity up to 36 tankers/day

Expandable to 4 bays

Rear & Side loading

Weighbridge & Gas Chromatograph

Up to 40 m3 Tankers

Target go-live 2015

Regulatory consent given to the project

11

Truck LoadingCommercial & Business Model

GLNG intends to invest 100% on RTLF and take all the risk

Tanker Operators must secure LNG supply from Grain Shippers

Tanker Operators secure slots from Grain LNG

GLNG RTLF

Shippers Operators

Invests100%

BuysLNG

Buys RTLFServices from

Grain LNG

12

Challenges Speed to market LNG Supply

Uncertainty supply post Fukushima No quality or volume guarantees Competition

Rate of development of the LNG fuel truckmarket

Scalability Government Support

Tax regime guarantees Regulatory clarity on Small Scale LNG Planning – Perception of LNG

challenges UK safety standards Vs ‘perceived’ lack of

technical standards

13

Why Grain LNG?

GLNG has obtained board approval

GLNG currently has the capacity to cater for market demand

GLNG is in an ideal location to cater for UK and NW Europemarkets

GLNG has over 30 years experience in the LNG industryachieving consistent, flexible and reliable operational performance

GLNG is an independent terminal operator giving equitableservices

GLNG has 6 Shippers enhancing competition on supply

14

Any Questions?

Biomethane to GridMarket Update

30th January 2014

John BaldwinManaging DirectorCNG Services Ltd

0121 247 8160

Robert McKeonProject ManagerCNG Services Ltd

0121 707 8581

Biomethane Market Overview

1. CNG Services Ltd2. Project Review3. Market forecast4. Green Gas Certificates and CNG5. Conclusions

CNG SERVICES LTD

CNG Services Ltd

• Supports projects to injectbiomethane into the gas grid– Didcot, Poundbury, Vale Green,

Stockport, Doncaster, Minworthetc.

• Bio-CNG as a fuel for trucks– Own UK’s largest CNG filling

station– Sell Bio-CNG (20% biomethane)

We are independent from all makers of plant, vehicles, clean-up, compression....wehelp clients get the best solution for their projects

Our Biomethane Projects Team

• Biomethane Projects– Iain Ward, Lee Firth, Alison Cartwright, Terry Williamson, Robert

McKeon, Greg Lee• Pipelines and Compression Project

– Ian Roughley, Bob Ingmire, Mick Beddows (LTS), Phil Winnard,Tony Pym

• Commercial (RHI, NEA etc.)– Peter Rayson

• Project Support– Angela Bagshaw, Chris Toase, Christine Venables, Lauren Hamer

We support Biomethane Projects for a living

PROJECT REVIEW

Didcot – UK’s First BtG Project

Biogas upgrader

Propane StorageGas bag

Energy & quality Measurement

Propane Injector

Telemetry

H2S and

Siloxane filters

Flow of biogas - 100 m3/hrFirst gas to grid on 3rd Oct 2010

Anaerobic

Digesters

Poundbury• UK’s first commercial scale biomethane to

grid project• 500 m3/hr. into grid (around 1 million therms)• Membrane CO2 removal plant• SGN providing biogas to biomethane

conversion service• Development is a JV between Duchy of

Cornwall and some of its tenants

Prince Charles opened the project in Nov 12

Springhill (Vale Green) near Evesham• Approximately 600 m3/hr biogas• 490 kWh CHP• Go live – August 2013• CO2 separated via membrane and cryogenic system – used to grow more tomatoes

Future Biogas - Doncaster• Agricultural feedstock• Approximately 900 m3/hr biogas to biomethane• 499 kWh CHP• Went live Oct 2013

BioCore - Beccles

• Agricultural• Approximately 2,000 m3/hr biogas• 490 kWh CHP• Go live Q2 2014

Severn Trent Water - Minworth

• Sewage derived biogas• Approximately 1,200 m3/hr biogas• Existing 9 MWh CHP• Go live Q2 2014

ReFood - Widnes

• Food waste• Approximately 2,000 m3/hr biogas• Go live 2014

Project in Scotland

• Waste• 2 water wash plants, each capable

of 2,500 m3/hr biogas

Chesterfield Biogas selected to build UK’s largest biomethane-to-grid project.COMChesterfield BioGas (CBG) has announced a new order for its biogas upgraders which will be central to aground-breaking UK renewable energy project. The company, which is based in Sheffield, UK, is to supplygas-scrubbing water-wash upgraders and ancillary equipment to a site in UK.When commissioned in late 2014, not only will it be the first facility of its kind, it will be the largest of anybiogas-to-grid project so far announced or operating in the UK.Raw biogas - derived from anaerobic digestion (AD) will be converted to biomethane suitable for injection into thenational gas grid.Such is the anticipated raw biogas input from the AD, upgrading units will need to be coupled in parallel to optimise anoutput of up to 5,000 cubic metres per hour of 98% pure biomethane. The model being supplied is the Totara + , thelargest in the Greenlane® range.Included in the service elements of the contract are a 3-year warranty, a guarantee of 98% system availability, and amonthly site visit by a CBG engineer.The Greenlane water-wash process is proven in operation over the last 20 years and requires no heat and nochemicals. More 75 sites are operating successfully around the world, 30 of which employ the Totara model.When the project is completed in late 2014, CBG will have six similar systems of various capacities installed in the UK- more than all other types of biogas upgrading units operational in the country put together, and more than any othersingle supplier.

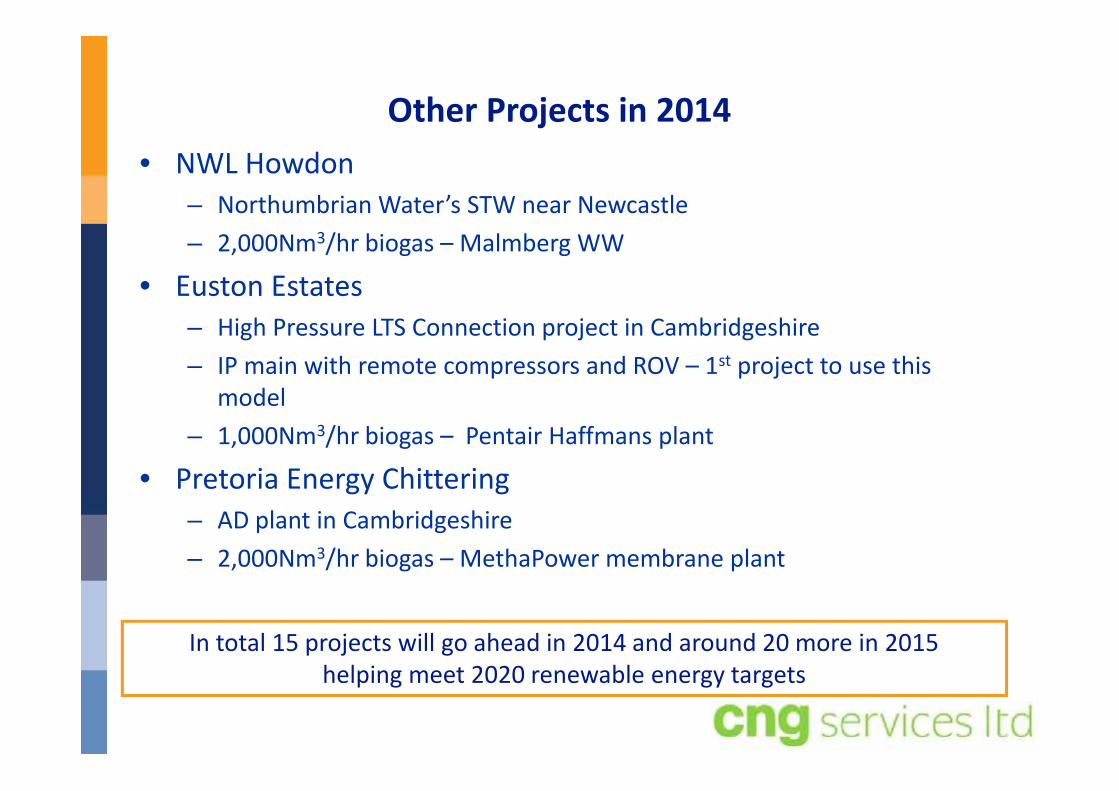

Other Projects in 2014• NWL Howdon

– Northumbrian Water’s STW near Newcastle– 2,000Nm3/hr biogas – Malmberg WW

• Euston Estates– High Pressure LTS Connection project in Cambridgeshire– IP main with remote compressors and ROV – 1st project to use this

model– 1,000Nm3/hr biogas – Pentair Haffmans plant

• Pretoria Energy Chittering– AD plant in Cambridgeshire– 2,000Nm3/hr biogas – MethaPower membrane plant

In total 15 projects will go ahead in 2014 and around 20 more in 2015helping meet 2020 renewable energy targets

MARKET FORECAST AND CONCLUSIONS

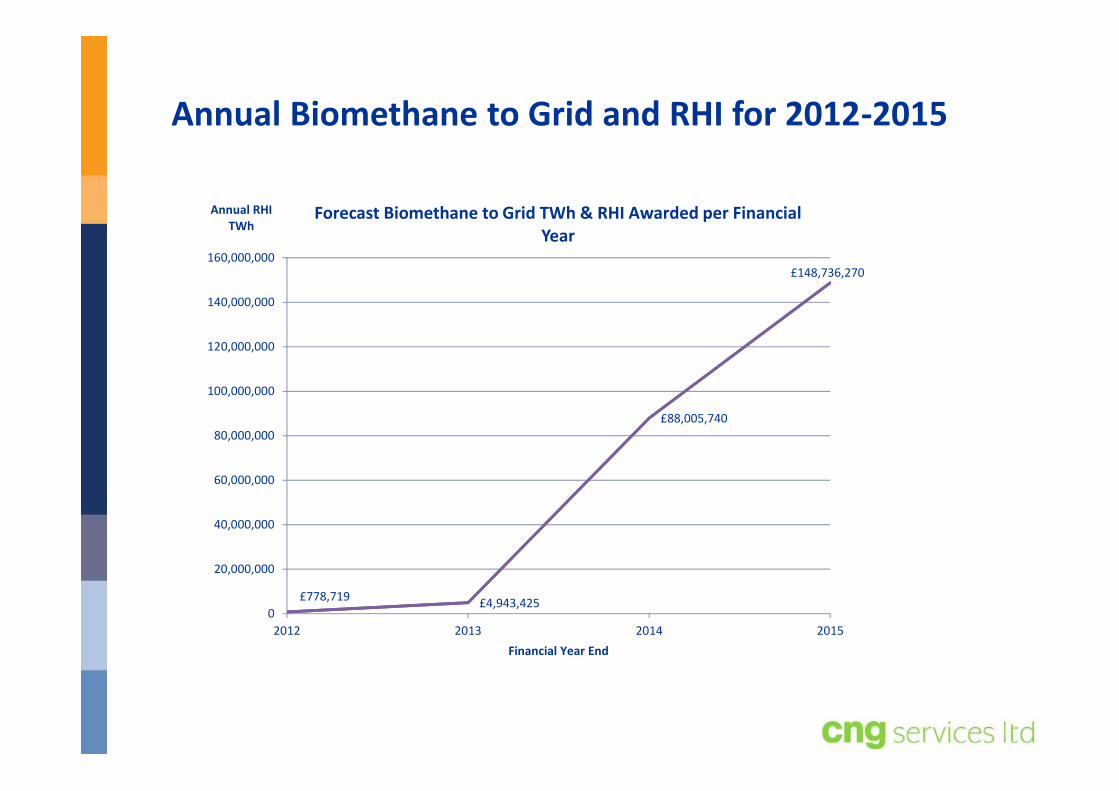

Annual Biomethane to Grid and RHI for 2012-2015

£778,719 £4,943,425

£88,005,740

£148,736,270

0

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

140,000,000

160,000,000

2012 2013 2014 2015

Annual RHITWh

Financial Year End

Forecast Biomethane to Grid TWh & RHI Awarded per FinancialYear

Feedstock Categories

Projects were also categorised according to sectors determined by the EUGreen Gas Grids Project:

1. Sewage Sludge2. Agricultural

a. Animal manure (slurry)b. Agricultural by-products and residuesc. Crops for Energyd. Agricultural biomass is modelled as one sub-group as projects will often contain

elements of all 3 streams3. Industrial Food Processing waste4. Food Waste (commercial, domestic, local authority)5. Biodegradable waste (e.g. from an MBT plant or garden waste collected by

local authority)

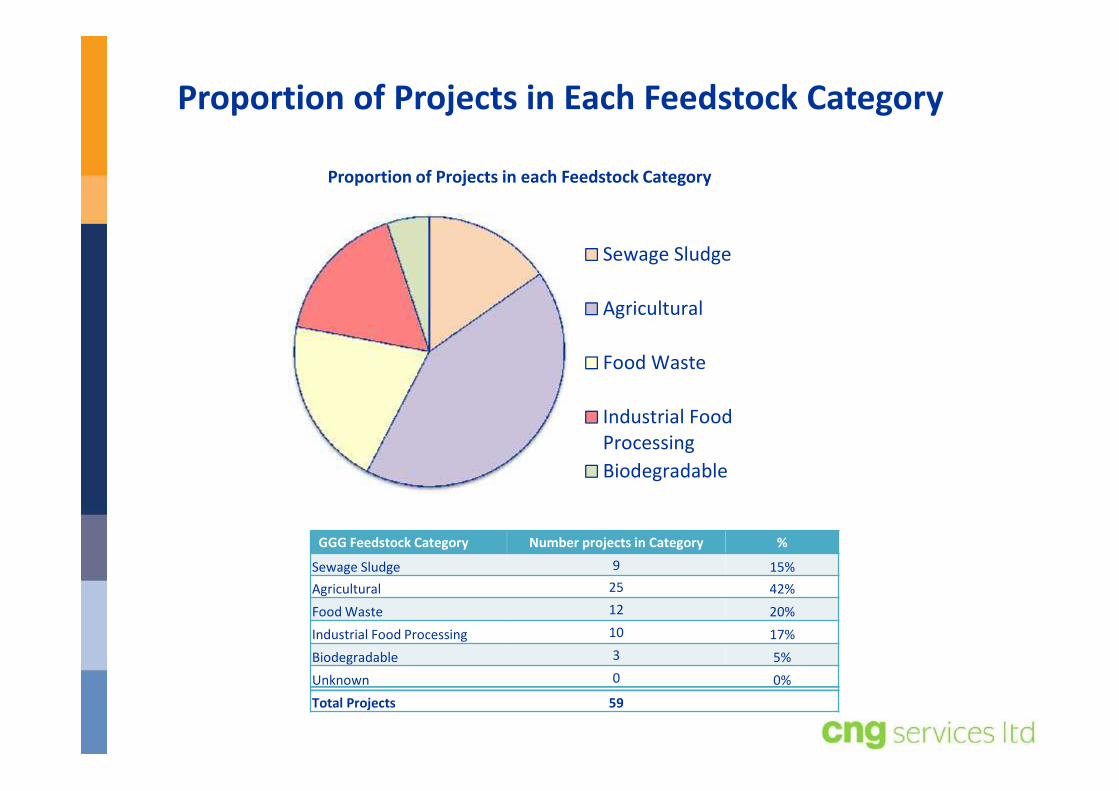

Proportion of Projects in Each Feedstock Category

Proportion of Projects in each Feedstock Category

Sewage Sludge

Agricultural

Food Waste

Industrial FoodProcessingBiodegradable

GGG Feedstock Category Number projects in Category %

Sewage Sludge 9 15%Agricultural 25 42%Food Waste 12 20%Industrial Food Processing 10 17%Biodegradable 3 5%Unknown 0 0%Total Projects 59

Biomethane Market Forecast

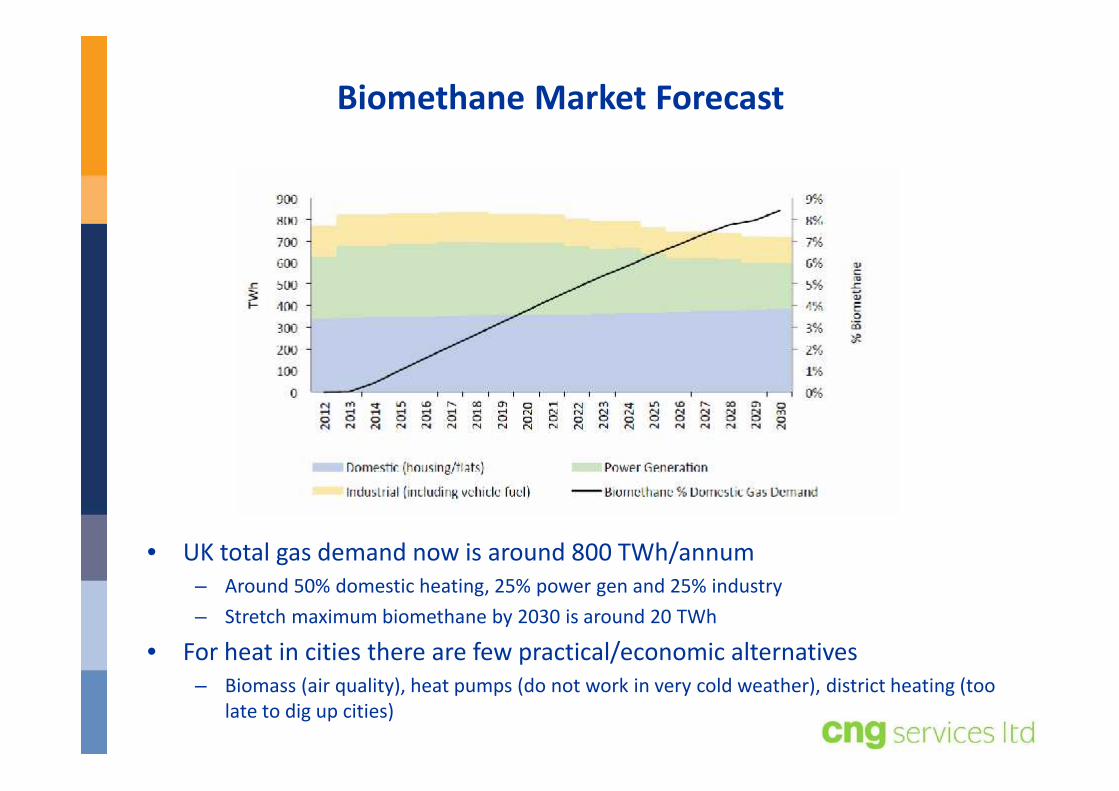

• UK total gas demand now is around 800 TWh/annum– Around 50% domestic heating, 25% power gen and 25% industry– Stretch maximum biomethane by 2030 is around 20 TWh

• For heat in cities there are few practical/economic alternatives– Biomass (air quality), heat pumps (do not work in very cold weather), district heating (too

late to dig up cities)

GREEN GAS CERTIFICATES

Green Gas Certificates

• GGCS tracks commercial transactions of biomethane throughthe supply chain

• Each unit of green gas injected into the grid displaces theneed for a unit of conventional gas

• Unique identifiers ensure there is no double-counting ordouble-selling of green gas

• Producers, network operators, suppliers and consumers canall participate on a voluntary basis

• Rules similar to those that operate in Germany andNetherlands where market more advanced

• In Germany, 350 CNG filling stations sell CNG with a GreenGas Certificate

• Range of RGGOs• Total amount kWh• Country• Technology (waste

water, AD)• Feedstock (food,

crop, slurries etc.)• Producer• Supplier• CO2 emissions• Pin Code

Certificate Information

REAL Green Gas Certificate Scheme

• Designed to allow ‘tracking ofbiomethane from injectionpoint to customer’

• Integrity - no ‘double counting’• Separate from the gas to

provide flexibility• Can only be used once

• National Grid• British Gas• E.ON• Thames Water (Didcot)• Adnams Biogroup (Adnams)• Milton Keynes City Council• CNG Services Ltd• http://www.greengas.org.uk/

GGCS Launch Members

GGCS is the only UK scheme associated with the recent agreementto harmonise registry Green Gas Certificate rules(http://www.greengasgrids.eu/info/news.html )

Gas shipper

AD DeveloperOrganicMaterial

GasDistribution

Network

Sale of

‘Certificates’Normal grid gas

Purchase ofbiomethane

energy

Inject gasinto grid

Processing viaAnaerobicDigesters

AD Developer Sells Certs Direct to Gas Consumer

Clean-up plantand grid injection

Gas can beused to fuel

trucks on CNGor for CHP

Sale of gas

Customer

Green Gas Certificates

• GGCS is not-for-profit and governed by its participants• Participants pay a small annual membership fee (£500)• A small gas throughput fee (0.01p/kWh)is levied as identifiers

are retired• GGCS does not legally confer any additional ‘value’ on the

green gas contracts that flows through it (apart from buses –see later)

• GGCS does indicate ‘origin’ of the gas• GGCS is closely linked to the RHI• Participants are independently

audited to ensure registrationsare accurate

Opportunities for Green Gas Certificates

• Green Gas Certificates are included in guidance of Dept forTransport Low Carbon Emission Buses (LCEB) – buses can useGGC as proxy for biomethane– The bus operator is allowed to claim a credit of 6p/km if a Green gas

Certificate is presented to match gas used

• John Lewis has called for ‘DEFRA and DECC need to recogniseGreen Gas Certificates for transport carbon reporting

• Opportunities for Green Gas Certificates in GovernmentAllowable Solutions programme for zero carbon buildings

• Sainsbury’s using for ‘carbon neutral store’ – next slide

Sainsburys

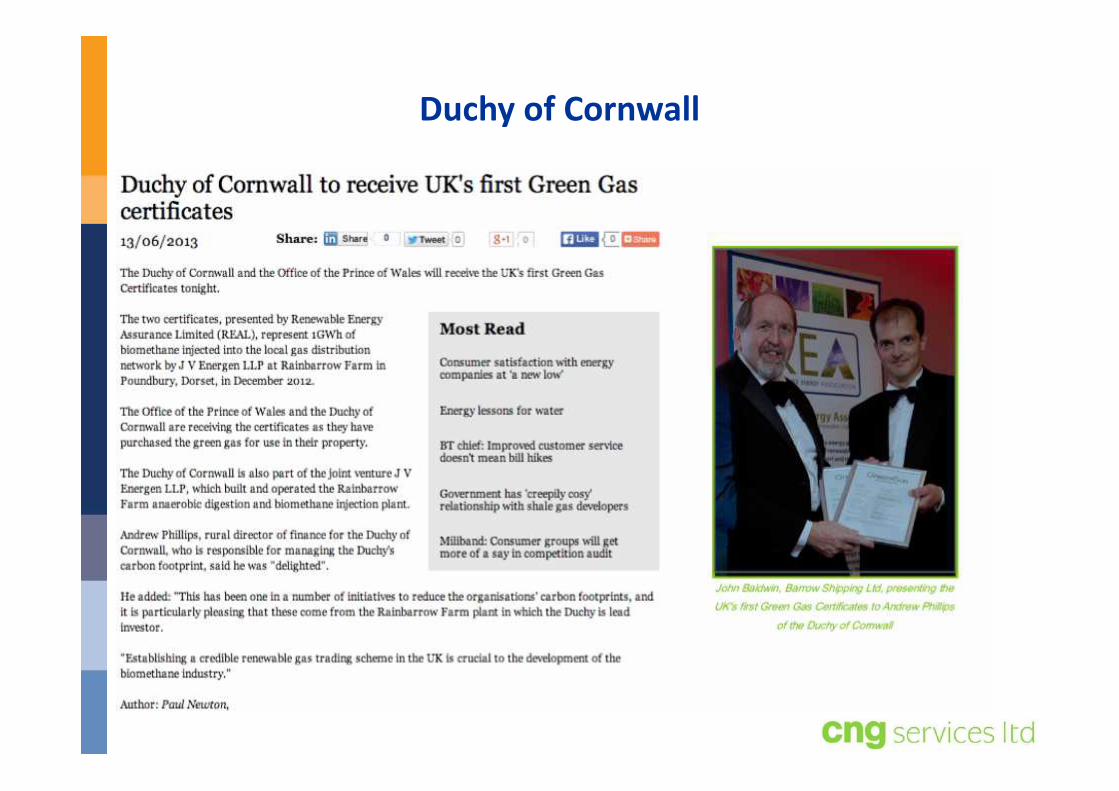

Duchy of Cornwall

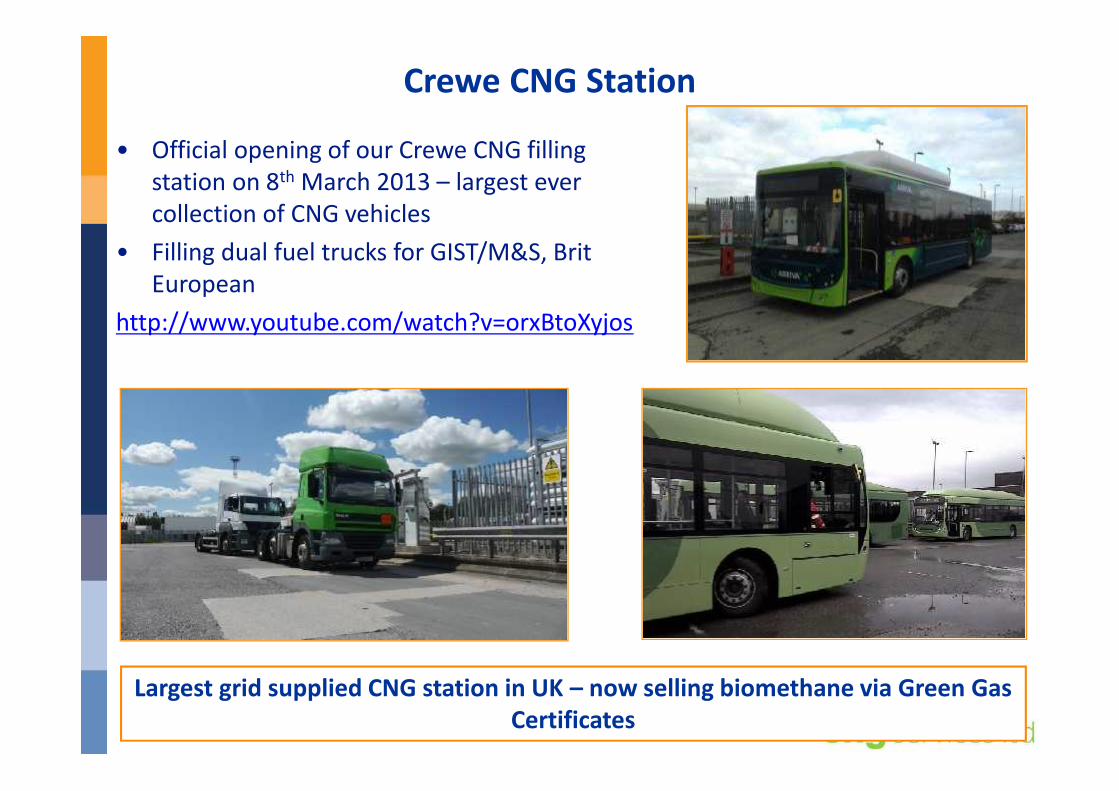

Crewe CNG Station

• Official opening of our Crewe CNG fillingstation on 8th March 2013 – largest evercollection of CNG vehicles

• Filling dual fuel trucks for GIST/M&S, BritEuropean

http://www.youtube.com/watch?v=orxBtoXyjos

Largest grid supplied CNG station in UK – now selling biomethane via Green GasCertificates

Brit European

• Provide transport services for JCB• Run 36 dual fuel diesel-CNG trucks• Purchase Green Gas Certificates to demonstrate gas sourced

from UK organic feedstock

UK Gas Distribution Network

• Extensive UK and Ireland Gas Network• Good for biomethane injection

• High Pressure LTS network ideal for CNG• it would cost >£15 billion to build NTS/LTS

• Shale gas industry about to start in UK• Reducing gas and oil imports

UK gas system – Local Transmission System

LTS is a vital national asset - ideal for CNGHigh Pressure CNG can help reduce diesel demand and CO2 emissions from

HGVs

• www.greengas.org.uk• Twitter: @GreenGasCert• Non for profit scheme

• http://greengastrading.co.uk/

• Multiple shareholders

Biomethane to Grid Conclusions

• It has taken 6 years but the regime looks good:• Over 50 projects in next 3 years is possible, all technologies

• Majority of biomethane from waste feedstock• Need to focus on reducing capital costs

• Grid Entry Unit costs reduced by 50% in last 5 years• New processes being developed for high pressure connections• 7 active biomethane equipment providers in UK – competition

• Green Gas Certificates• CNG for trucks and buses and CHP/District Heating for new housing• REAL not for profit scheme is helping to facilitate biomethane projects

The biomethane market is set to grow, delivering significant benefits andhelping meet 2020 renewable energy targets

THANK YOUFOR LISTENING

Low Carbon Truck Review and WorkshopLBM & LNG Distribution and Security of Supply30 January 2014

Gasrec - Introduction

• The leading supplier of bio-LNG in Europe - Gasrec owns andoperates its own biomethane liquefaction plant. Gasrec liquefies themethane from landfill and blends it with LNG to create bio-LNG andthereby offers enhanced CO2 savings

• Operates a vertically integrated supply chain – Gasrec produces itsown bio-methane (and is developing options to liquefy natural gas);it owns its own road tankers which deliver to its own refuelingstations

• Largest supplier of gas to transport in the UK - Gasrec has developed11 LNG/LCNG refueling stations, 5 in the last 6 months and suppliesfuel to more than 60% of gas powered HGVs on UK roads

• Secured TEN-T Grant – Gasrec has secured grants to build 5 refuelingstations in the UK and 2 mobile stations in continental Europe. Theknowledge gained by Gasrec will contribute to the development ofLNG refueling standards and LNG station deployment across Europe

• Experienced management team – Gasrec has an experiencedmanagement team and proprietary knowledge of all aspects of thesupply chain

Vertically Integrated Business Model

Supply Security Trading Distribution Sales andMarketing

• Collect and liquefymethane from landfill

• Developed plantdesign and operatingknow how

• Project developmentfor UK sourcedstranded gas supplied

• Purchase LNG from 3rd

parties under term andspot agreements

• Own LNG road tankerfleet and distribute bio-LNG

• Develop refuelingstations and sell bio-LNG and LNG asalternatives to dieselfor use in HGVs

• Bespoke station design

• Bias to open accessstations

Refueling Station Systems• Gasrec offers a range of refueling station options to match the

specific customer requirement and number of vehicles to berefueling in as cost effective way as possible.

• Open access station - developed at or close to strategiccustomer locations, Gasrec owns and operates thestation and sells bio-LNG, LNG, or L-CNG at thedispenser

• Dedicated station - designed and built by Gasrec andowned and operated by the site operator or by Gasrec.Typically this includes a full maintenance and repairservice

• Design recognition for rapid filling experience (sub 5min); mitigating vent to atmosphere; and, customerintegrated dispensing electronics (Triscan/SAP)

• Station options include purpose-built, factory assembled ormobile.

• G15 to G60 - Permanent facilities designed and built toGasrec’s specification. Pumped refueling for fastrefueling and full vent recovery with zero loss.

• G10 to G15 - Factory assembled semi-portable facility.Pumped refueling and full vent recovery. Option fordual fuelling of CNG and LNG in combination.

• G6 - Commonly available cryogenic storage tankadapted for LNG refueling. Typically decant filling andno vent recovery. Short term solution

Gasrec existing refueling stations (Dec 2013)

Gasrec designed and built refuelling stations:

1.Camden (Camden Council) - Dec 10

2.Enfield (Coca Cola) - Jun 12

3.Enfield (Tesco) - Feb 12

4.DIRFT (Gasrec) - April 13

5.Swindon (B&Q) - May 13

6.Scunthorpe (Nisa) - Jun 13

7.Tamworth (UPS) - Sep 13

8.Bristol (Sainsbury) - Oct 13

9.Lutterworth (Gasrec) - Dec 13

10.London (Arla) – Dec 13

11.Buckinghamshire (Arla) - Dec 133

1 1

1

3

3

1 2

1

4

• All open Access

• Hatfield – Supporting existing customer base on back to base operationsand tramping

• Southampton – combined LNG/CNG supporting exiting expandingcustomer needs

• Bridgwater (Somerset) – strategic location adjacent to M5 supportingexisting and future customer needs

• West Midlands (Solihul) M6/M42 – seeded through existing customersupport (LNG/CNG combined)

• Derby – regional infrastructure seeding and support to existing customer

• NW UK (Warrington) – supporting national infrastructure roll-out

Proposed 2014 UK Station Deployment

2014 – Station Deployment

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

HG

V re

gist

ratio

ns

High

Mid

Low

Vehicle deployment model

Trans-European Network Co-funding

• In October 2013 Gasrec was awarded EU funding tostudy the potential for bio-LNG as a fuel for HGVs

• The study co-funds the deployment of a nationalnetwork of 5 open-access refueling stations acrossthe UK and 2 units in continental Europe by the endof 2015

• Gasrec’s experience will be used to contribute tothe setting of LNG refueling standards and theroadmap for deploying LNG stations across theTEN-T network

• Dirft; Avonmouth; Thurrock; Wakefield; Livingston

Proposed TEN T refueling station locations

• Gasrec was originally formed in 2003 tocommercialise its technology and knowhow forlandfill gas liquefaction.

• Built as a commercial scale pilot plant; startedoperation in 2008.

• Capable of fuelling fleet of 1500 HGVs.• It remains the only landfill gas liquefaction plant

in Europe – Gasrec manages the gas collectionsystem; processes gas to remove impurities andliquefies to LBM.

• Gasrec has developed unique operatingknowledge and experience of landfill gasliquefaction over the 6 years of plant operation

• Accreditation for Gasrec processes and fuel fromthe UK Government

Albury - Bio-methane liquefaction (LBM)

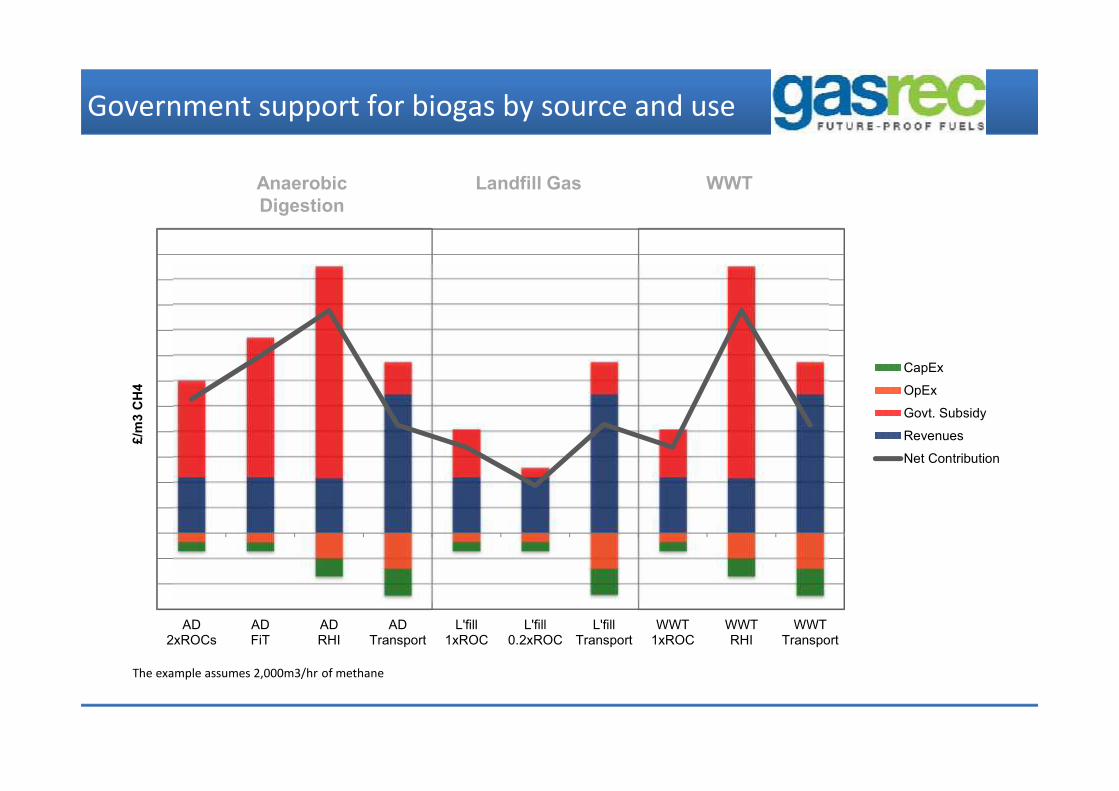

Government support for biogas by source and use

The example assumes 2,000m3/hr of methane

AD2xROCs

ADFiT

ADRHI

ADTransport

L'fill1xROC

L'fill0.2xROC

L'fillTransport

WWT1xROC

WWTRHI

WWTTransport

£/m

3C

H4

CapEx

OpEx

Govt. Subsidy

Revenues

Net Contribution

AnaerobicDigestion

Landfill Gas WWT

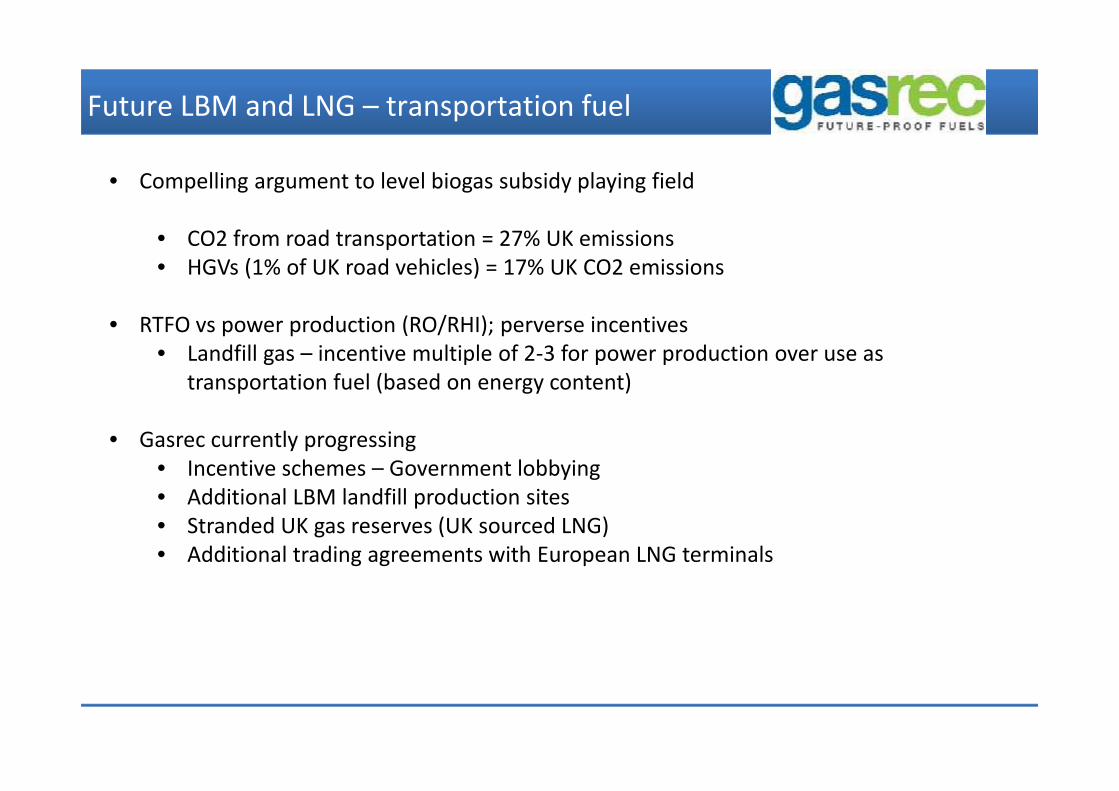

Future LBM and LNG – transportation fuel

• Compelling argument to level biogas subsidy playing field

• CO2 from road transportation = 27% UK emissions• HGVs (1% of UK road vehicles) = 17% UK CO2 emissions

• RTFO vs power production (RO/RHI); perverse incentives• Landfill gas – incentive multiple of 2-3 for power production over use as

transportation fuel (based on energy content)

• Gasrec currently progressing• Incentive schemes – Government lobbying• Additional LBM landfill production sites• Stranded UK gas reserves (UK sourced LNG)• Additional trading agreements with European LNG terminals

What’s important to Gasrec in 2014

• Strengthen the supply chain – Gasrec is looking to invest inadditional LBM and LNG production to diversify the sourcesof supply and provide greater supply security. Also placingorders for additional LNG road tankers.

• Offer a range of refueling stations - Building on itsoperating experience and knowledge of the UK marketdevelop a range of fit for purpose refueling stations designs

• Secure TEN-T locations – Work with industry leaders toidentify and build gas refueling infrastructure to supportEuro 5 and Euro 6 HGV deployment

• Gain subsidy equivalence for bio-methane to transport –Seek Government recognition of bio-methane to transportand adjustments to subsidies.

• Air Quality - Helping stakeholders and Governments meettheir carbon target and contribute to a air qualityimprovement

Contacts

19 Eastbourne TerracePaddington StationLondonW2 6LG

Gas Alliance Group

Gas Alliance – The Company

oFormed 2009

oMission Statement:

‘To provide the UK Bus & Commercial Vehiclesector with a complete Compressed Biomethanesolution which will reduce Carbon Footprint andOperating Costs’.

Gas Alliance - Partners

Gas Alliance Group

Gas Vehicle Alliance Gas Bus Alliance

• Partners: Wartzilla (Hamworthy)Crouchland FarmsScotia Gas NetworksCeres

Natural Gas - Fossil Fuel

Natural Gas - Biomethane

Biomethane - GA Feedstock

40% Manure

40% Waste Supermarket Food

20% Waste Sileage/Bedding

Anaerobic Digestion

o Bio-methane:• Non Fossil Fuel• Renewable Fuel

o Feedstock + Bacteria + Temperature =

Biogas

GA - Anaerobic Digester

Crouchland

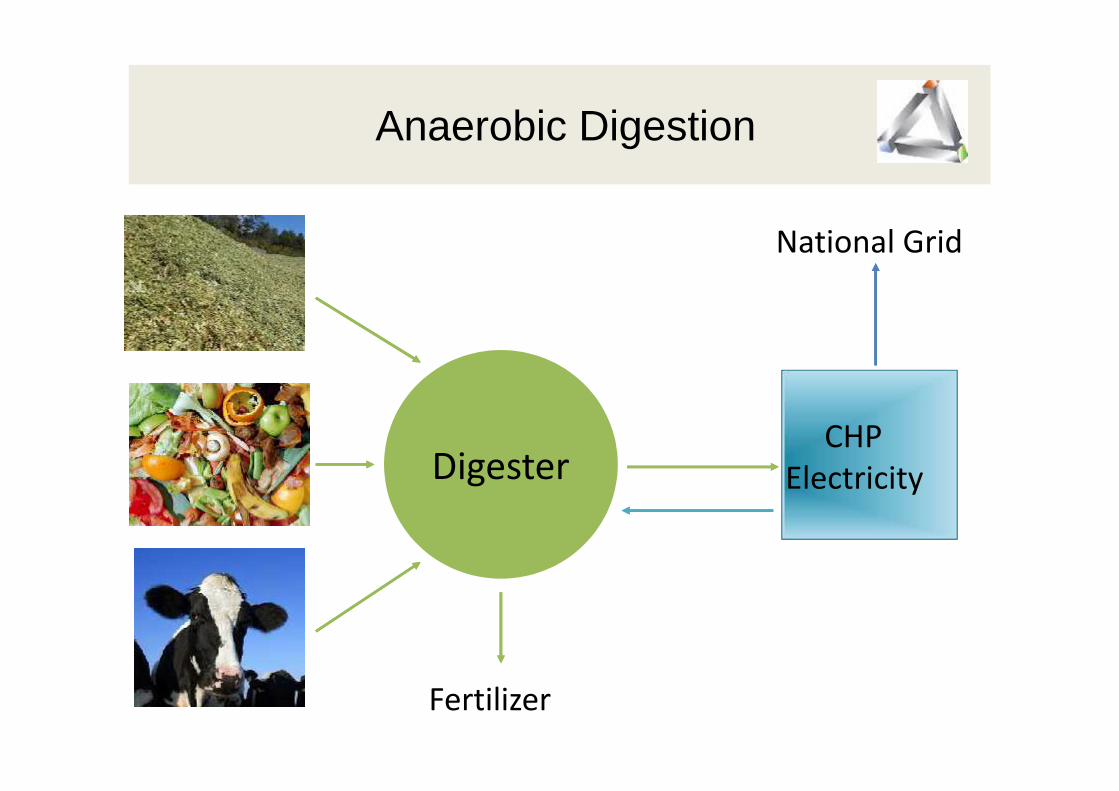

Anaerobic Digestion

DigesterDigesterCHP

Electricity

National Grid

Fertilizer

Anaerobic Digestion

Digester

CHPElectricity

Fertilizer

Gas CleaningProcess

UK National GasGrid Network

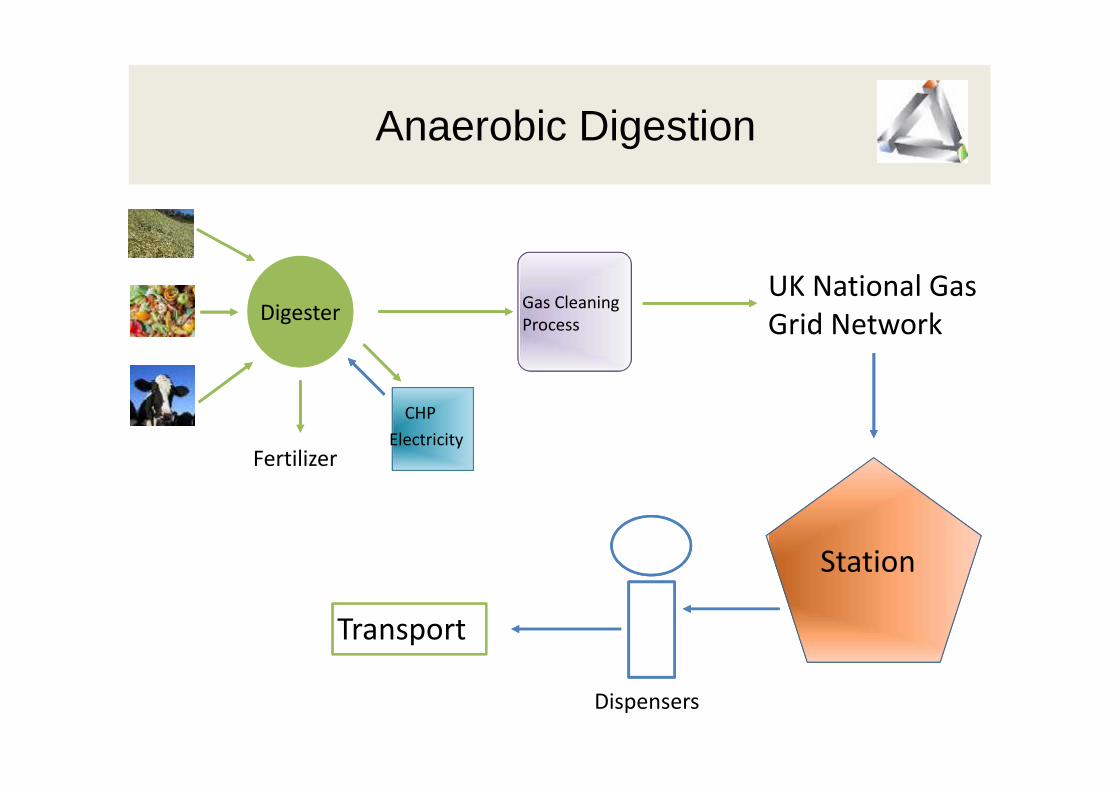

Anaerobic Digestion

Digester

CHPElectricity

Fertilizer

Gas CleaningProcess

UK National GasGrid Network

Station

Dispensers

Transport

Biomethane – Carbon Negative

o In 2014 Crouchland will collect all CO2produced from the Digester.

o Crouchland Biomethane will be CARBON NEGATIVE

Anaerobic Digestion

Digester

CHPElectricity

Fertilizer

Gas CleaningProcess

UK National GasGrid Network

Station

Dispensers

Transport

CO2Collection

Current Capacity

oSingle farm

o2200 cubic meters/houror

o1700 kgs/hour

o1 truck: 60 kgs/day

o Further 3 Projectsplanned for 2014

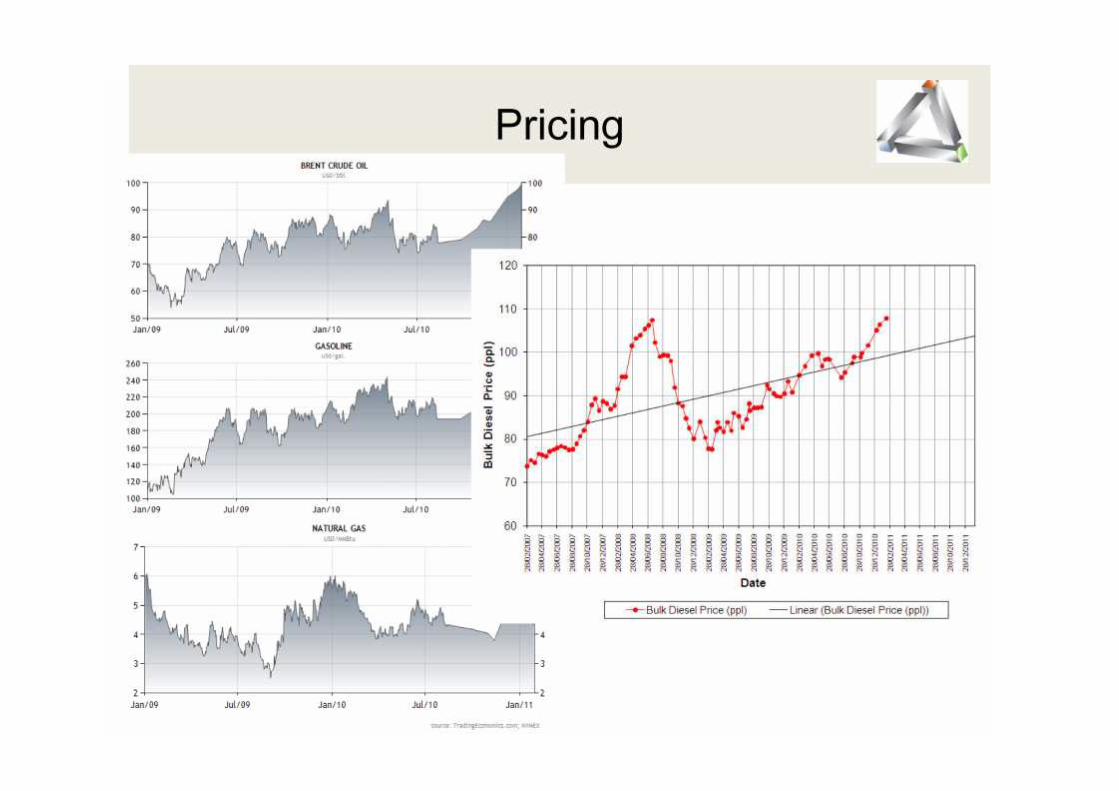

Pricing

Gas Alliance Model

o Utilitiy Surveyo 100% Compressed Bio-Methane

(CBM)o Gas Station – Design, Build & Maintaino Health & Safetyo Trainingo Project Managemento Fixed pricing modelso Future expansion included in priceo Guaranteed Carbon Neutral

Progress to Date

Truck Sector: VolvoM.BenzIvecoMAN

Duel Fuel Clean Air PowerPrinsG-volutionHardstaff

Fuel Bio-methane,CNGLiquid Natural Gas

Thank you for listening

![- Jun 14 [M Sawford] docx-1.docx · Web viewThis issue marks the departure of our former editor Sgt Catrin Sawford and welcomes our new one. Many new sections have been added including](https://static.fdocuments.in/doc/165x107/5aad00807f8b9a9c2e8db4dc/-jun-14-m-sawford-docx-1docxweb-viewthis-issue-marks-the-departure-of-our-former.jpg)