The Consultants Business Consultants - Www.theconsultants.net.In

Upload

heather-blankenshipCategory

view

218download

2

Gas Natural’s unsuccessful bid for Iberdrola

© Utility Consultants Ltd 2003

Prepared by Utility Consultants Ltd

www.utilityconsultants.co.nz

Disclaimer

This research report is of a generalnature, and is not intended as specific

professional advice. Accordingly, neitherUtility Consultants, nor its’ directors andshareholders, shall be liable for any lossor damage arising from action or inaction

based on this research report.

Contents

Disclaimer

Contents

Introduction

Overviewof the deal

Contact us

Feedback

Regulatory &compliance

issues

Comparisonwith the Ruhrgas

acquisition

Introduction

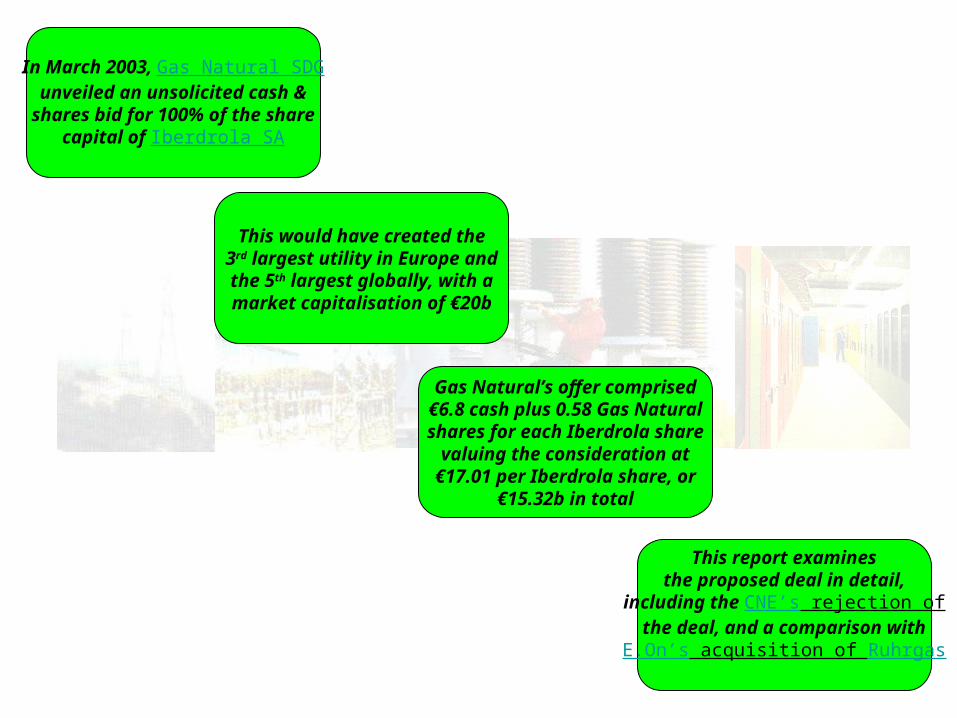

In March 2003, Gas Natural SDGunveiled an unsolicited cash &

shares bid for 100% of the sharecapital of Iberdrola SA

This would have created the3rd largest utility in Europe andthe 5th largest globally, with amarket capitalisation of €20b

Gas Natural’s offer comprised€6.8 cash plus 0.58 Gas Naturalshares for each Iberdrola share

valuing the consideration at€17.01 per Iberdrola share, or

€15.32b in total

This report examinesthe proposed deal in detail,

including the CNE’s rejection ofthe deal, and a comparison with

E.On’s acquisition of Ruhrgas

Overview ofthe deal

Introduction

Gas Natural

Iberdrola

The proposed deal

Iberdrola’sattractiveness

Gas Natural’sstrategy

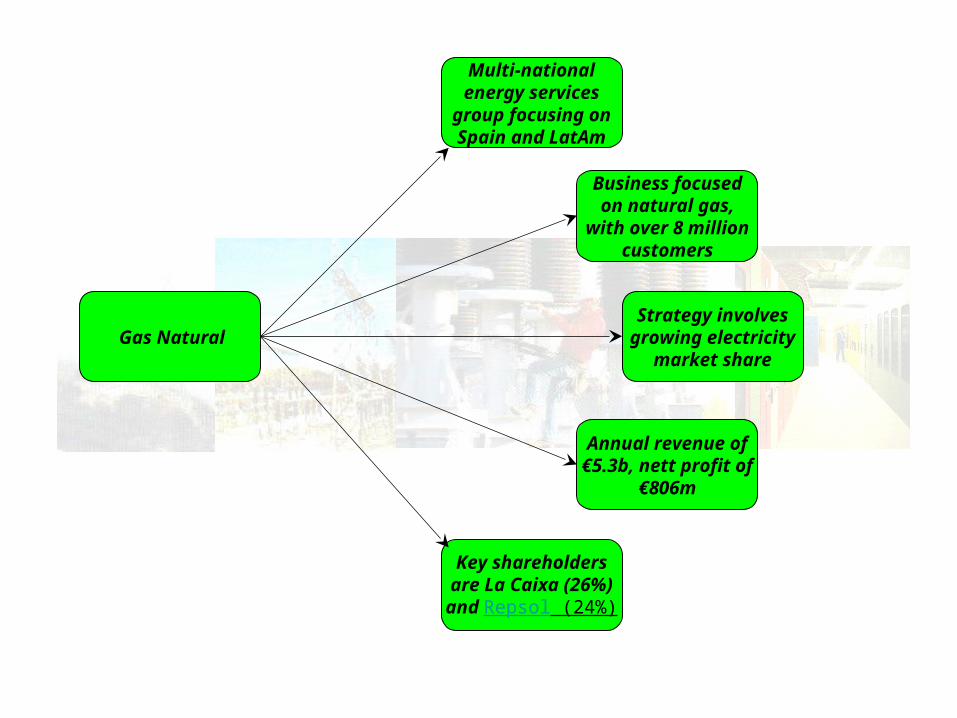

Gas Natural

Multi-nationalenergy services

group focusing onSpain and LatAm

Business focusedon natural gas,

with over 8 millioncustomers

Strategy involvesgrowing electricity

market share

Annual revenue of€5.3b, nett profit of

€806m

Key shareholdersare La Caixa (26%)and Repsol (24%)

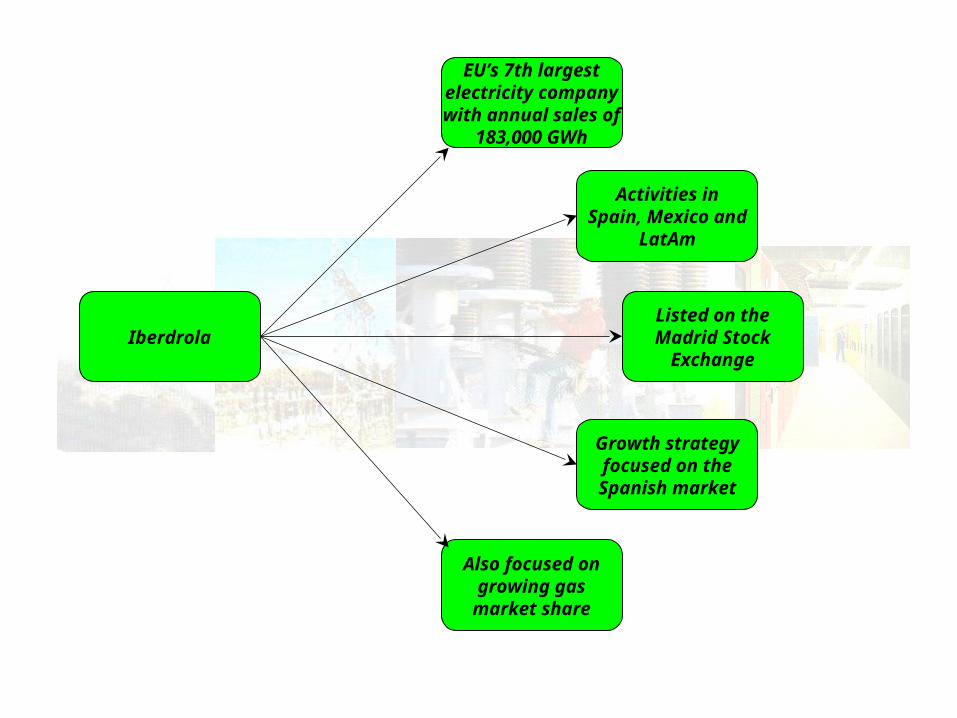

Iberdrola

EU’s 7th largestelectricity companywith annual sales of

183,000 GWh

Activities inSpain, Mexico and

LatAm

Listed on theMadrid Stock

Exchange

Growth strategyfocused on theSpanish market

Also focused ongrowing gasmarket share

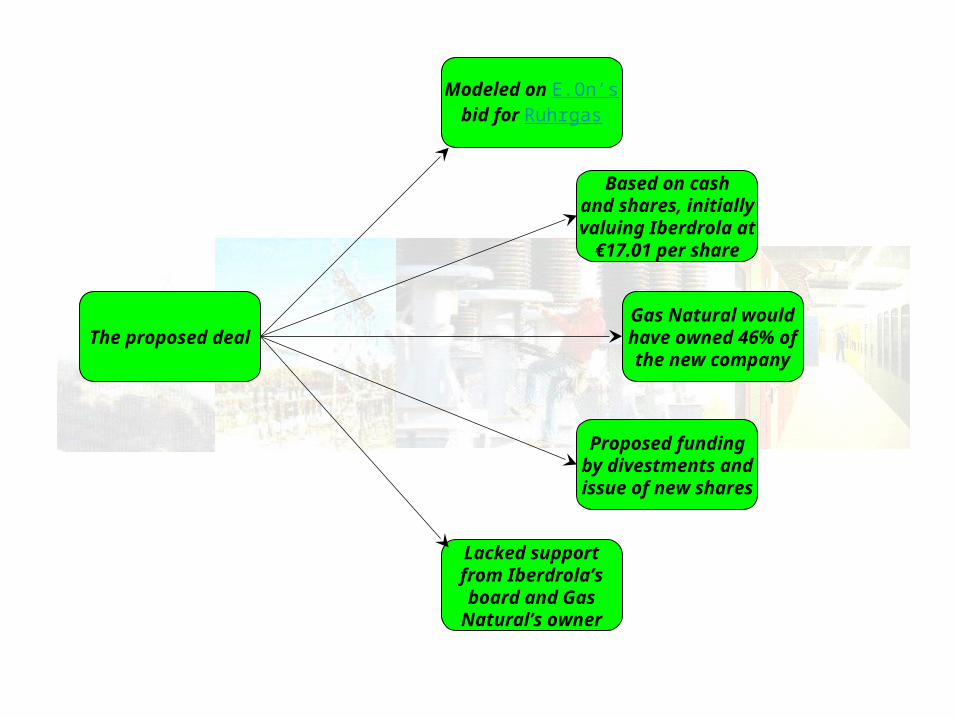

The proposed deal

Modeled on E.On’sbid for Ruhrgas

Based on cashand shares, initiallyvaluing Iberdrola at

€17.01 per share

Gas Natural wouldhave owned 46% ofthe new company

Proposed fundingby divestments andissue of new shares

Lacked supportfrom Iberdrola’sboard and GasNatural’s owner

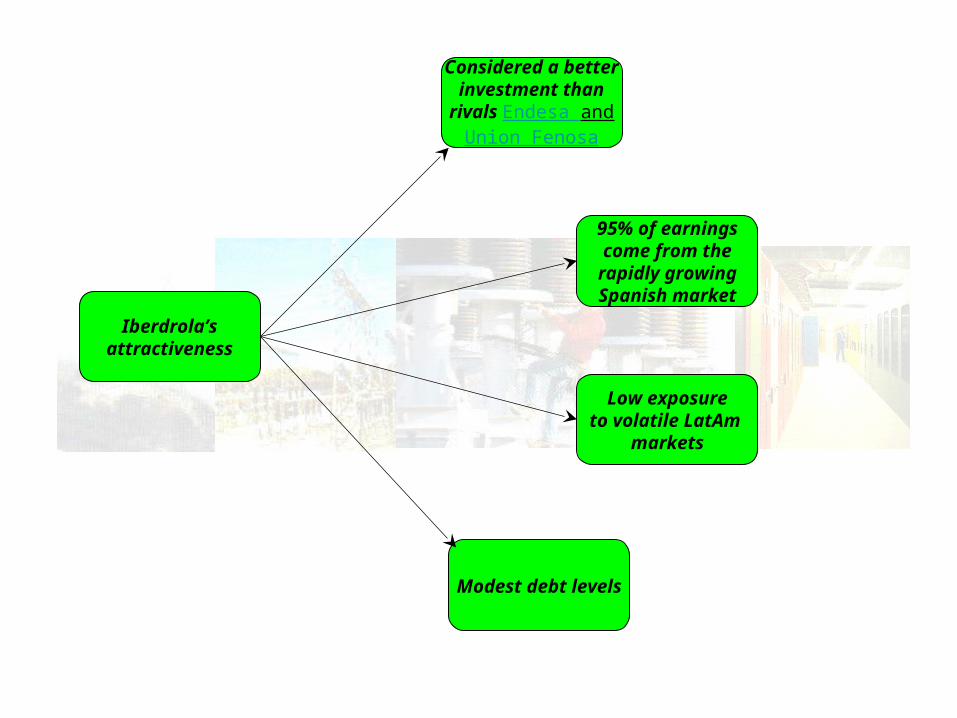

Iberdrola’sattractiveness

Considered a betterinvestment than

rivals Endesa andUnion Fenosa

95% of earningscome from the

rapidly growingSpanish market

Modest debt levels

Low exposureto volatile LatAm

markets

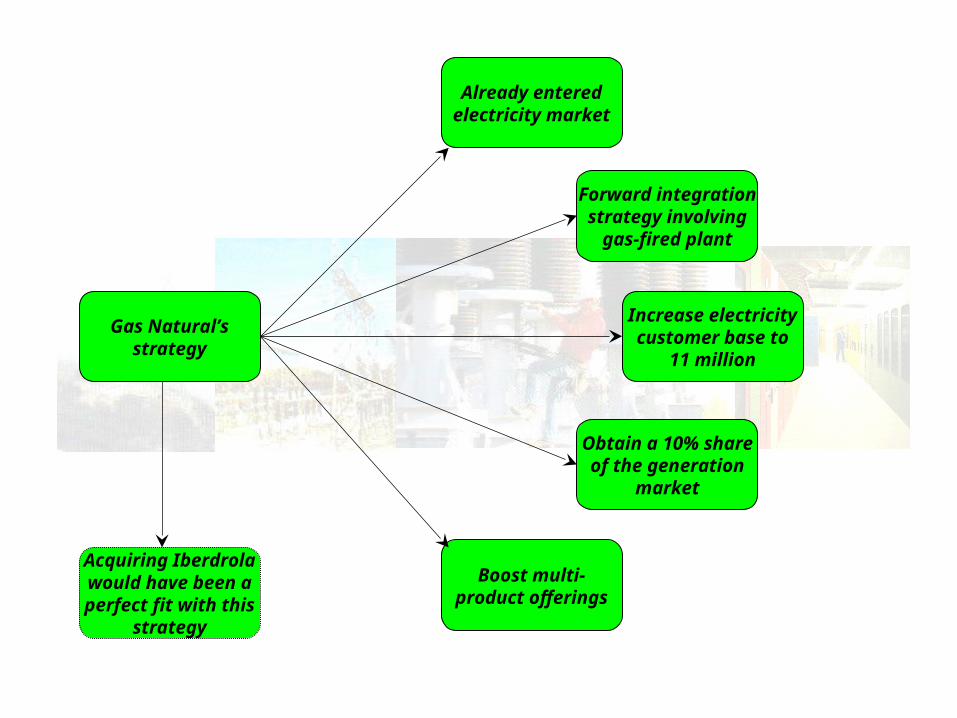

Gas Natural’sstrategy

Already enteredelectricity market

Forward integrationstrategy involving

gas-fired plant

Increase electricitycustomer base to

11 million

Obtain a 10% shareof the generation

market

Boost multi-product offerings

Acquiring Iberdrolawould have been aperfect fit with this

strategy

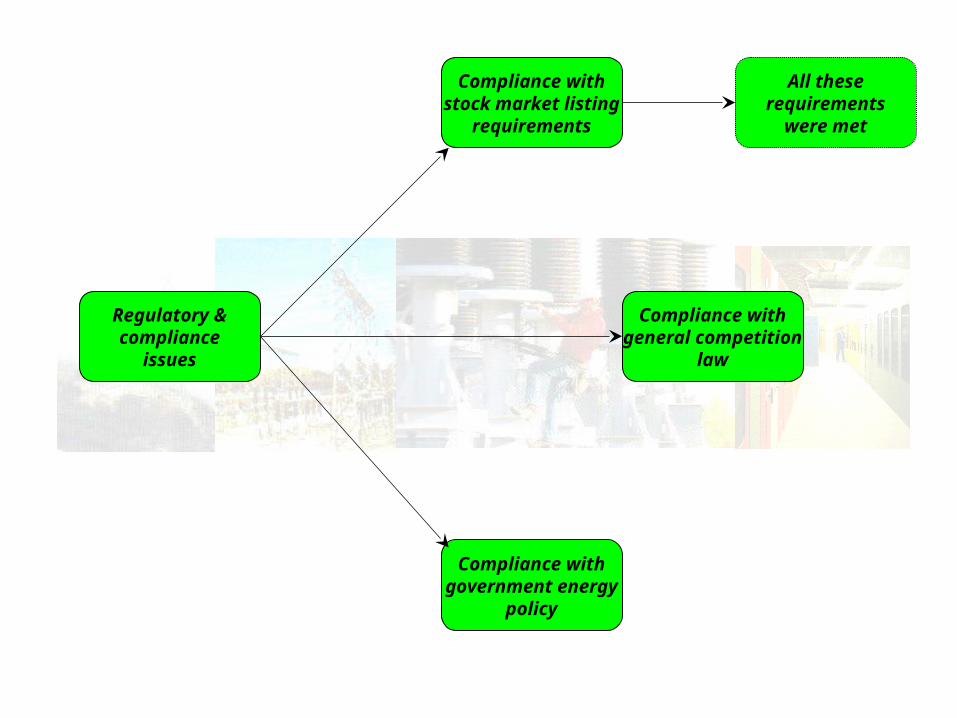

Regulatory &compliance issues

Regulatory &compliance

issues

Compliance withstock market listing

requirements

Compliance withgeneral competition

law

Compliance withgovernment energy

policy

All theserequirements

were met

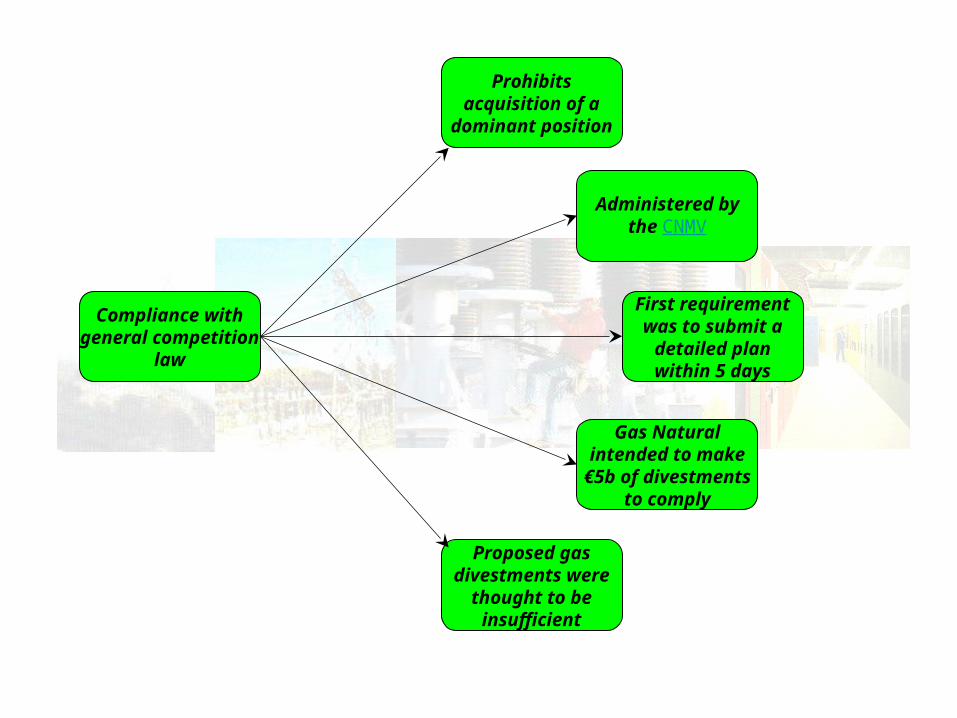

Compliance withgeneral competition

law

Prohibitsacquisition of a

dominant position

Administered bythe CNMV

First requirementwas to submit a

detailed planwithin 5 days

Gas Naturalintended to make

€5b of divestmentsto comply

Proposed gasdivestments were

thought to beinsufficient

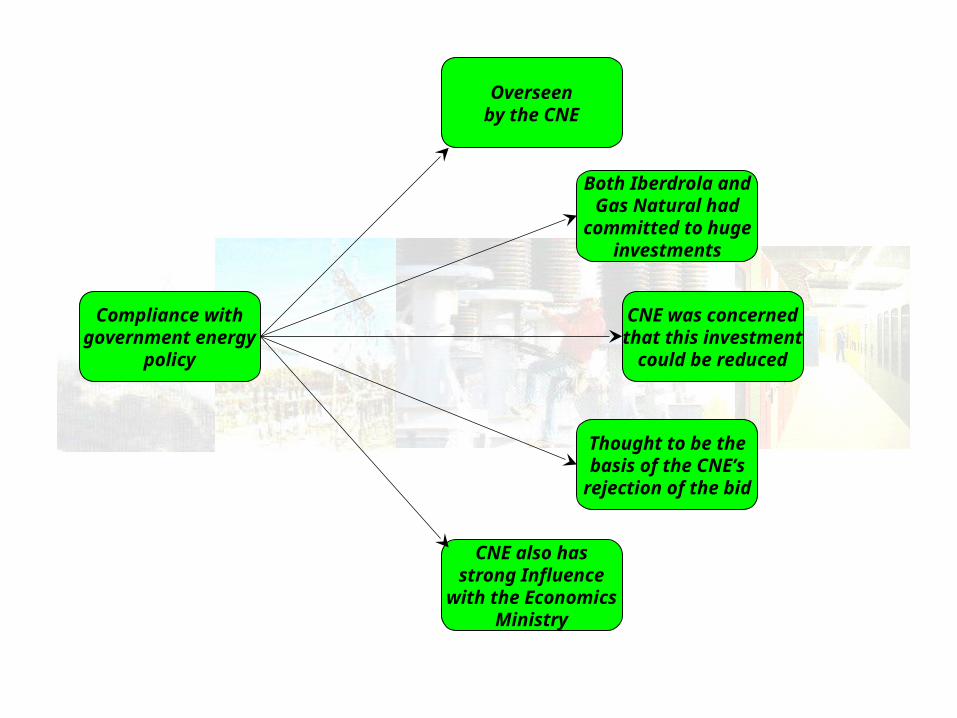

Compliance withgovernment energy

policy

Overseenby the CNE

Both Iberdrola andGas Natural had

committed to hugeinvestments

CNE was concernedthat this investment

could be reduced

Thought to be thebasis of the CNE’srejection of the bid

CNE also hasstrong Influence

with the EconomicsMinistry

Comparisonwith the Ruhrgas

acquisition

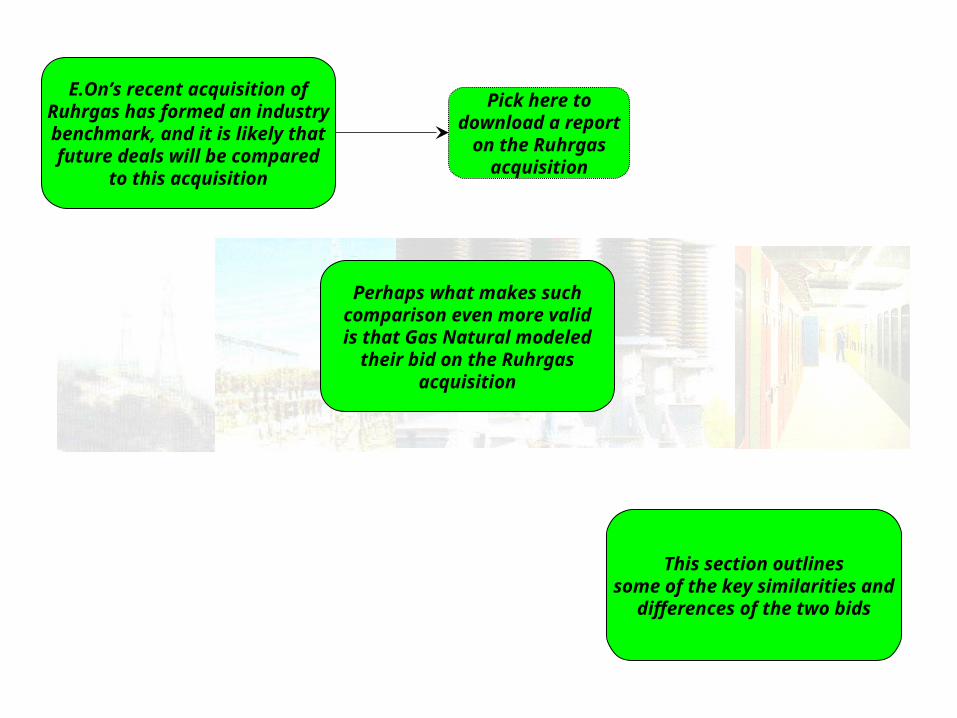

E.On’s recent acquisition ofRuhrgas has formed an industrybenchmark, and it is likely thatfuture deals will be compared

to this acquisition

Perhaps what makes suchcomparison even more validis that Gas Natural modeled

their bid on the Ruhrgasacquisition

This section outlinessome of the key similarities and

differences of the two bids

Pick here todownload a report

on the Ruhrgasacquisition

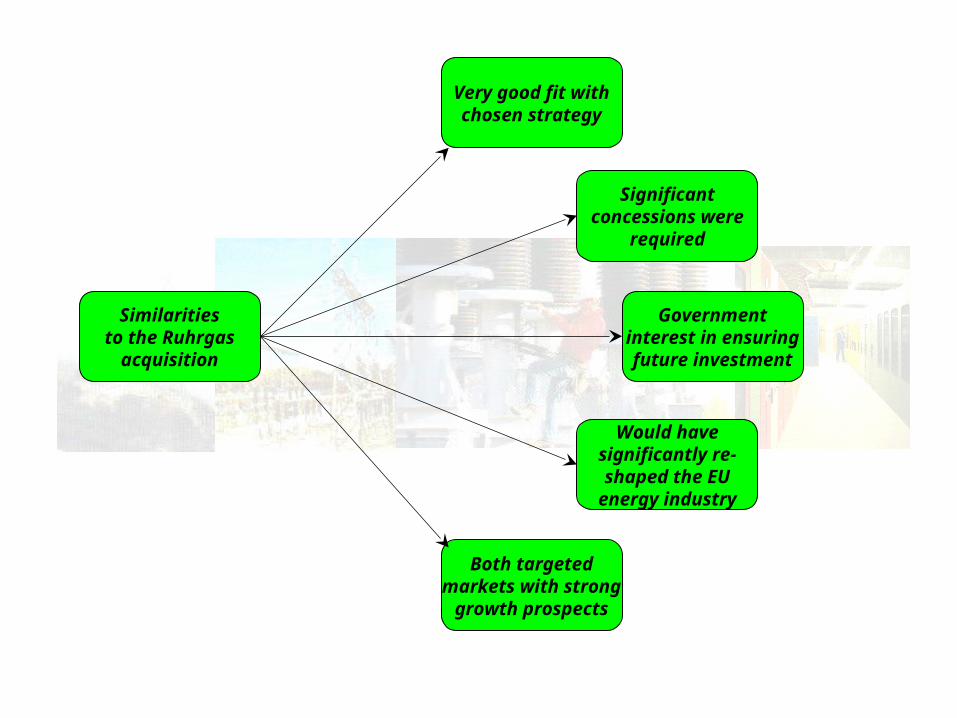

Similaritiesto the Ruhrgas

acquisition

Very good fit withchosen strategy

Significantconcessions were

required

Governmentinterest in ensuringfuture investment

Would havesignificantly re-shaped the EU

energy industry

Both targetedmarkets with strong

growth prospects

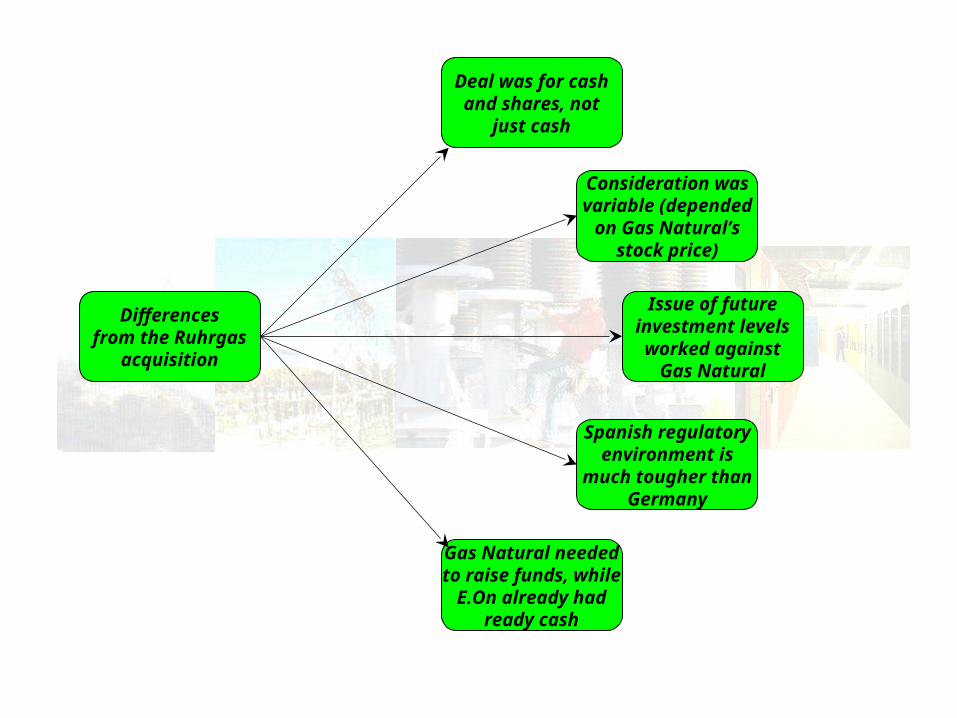

Differencesfrom the Ruhrgas

acquisition

Deal was for cashand shares, not

just cash

Consideration wasvariable (depended

on Gas Natural’sstock price)

Issue of futureinvestment levelsworked against

Gas Natural

Spanish regulatoryenvironment is

much tougher thanGermany

Gas Natural neededto raise funds, while

E.On already hadready cash

Feedback

Hi … I’m Phil Caffyn from Utility Consultants. I’d really like your feedback on this report, so please pick one of the buttons below to email me…

Excellent

Very good

Good

Average

Poor

Contact us

Phone us on+64-7-8546541

Pick here toemail a question

Pick here toreceive our free industry

newsletter Pipes &Wires

Pick here to visit ourwebsite (and see our

other research reports)