Gartner Research Circle_G-13516 Future of Mobility_SummaryV2

19

This presentation, including any supporting materials, is owned by Gartner, Inc. and/or its affiliates and is for the sole use of the intended Gartner audience or other authorized recipients. This presentation may contain information that is confidential, proprietary or otherwise legally protected, and it may not be further copied, distributed or publicly displayed without the express written permission of Gartner, Inc. or its affiliates. © 2012 Gartner, Inc. and/or its affiliates. All rights reserved. Study objectives: This study examines the current and future state of corporate mobile platforms. Participant summary: 780 IT and business leaders with personal knowledge of their organization’s workforce mobility strategy (i.e., devices, platforms, and applications) participated. [see Respondent Profile for detail] 2013 Future of Mobility, Data collected August 2013

-

Upload

ajquinonesp -

Category

Documents

-

view

22 -

download

0

description

fyi

Transcript of Gartner Research Circle_G-13516 Future of Mobility_SummaryV2

This presentation, including any supporting materials, is owned by Gartner, Inc. and/or its affiliates and is for the sole use of the intended Gartner audience or other authorized recipients. This presentation may contain information that is confidential, proprietary or otherwise legally protected, and it may not be further copied, distributed or publicly displayed without the express written permission of Gartner, Inc. or its affiliates. © 2012 Gartner, Inc. and/or its affiliates. All rights reserved.

Study objectives: This study examines the current and future state of corporate mobile platforms.

Participant summary: 780 IT and business leaders with personal knowledge of their organization’s workforce mobility strategy (i.e., devices, platforms, and applications) participated. [see Respondent Profile for detail]

2013 Future of Mobility, Data collected August 2013

1

Research Leads:

Ken Dulaney is a Vice President and Distinguished Analyst in Gartner Research, where his research areas include smartphones, tablet computers, notebook computers, industrial handhelds, wireless communications, mobile software and device management strategies. He has been recognized by Adweek magazine as one of the top 20 technology industry analysts.

Ken Dulaney VP Distinguished Analyst, Mobile Enterprise Strategy [email protected]

David Willis is a VP and Distinguished Analyst in Gartner Research. He is Chief of Research for Mobility and Communications and runs Gartner's Senior Research Board. Mr. Willis sets the direction and framework for worldwide integrative research across all aspects of mobile computing, mobile devices, networking, and telecommunications equipment and services. He has expertise in the management of mobile computing for large enterprises, including technology selection and policies.

David Willis VP Distinguished Analyst, Mobility and Communication [email protected]

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved

RESEARCH CIRCLE RESULTS: The Future of Mobility

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved 2

RESEARCH CIRCLE RESULTS: The Future of Mobility

Overview

• BYOD is an unstoppable trend with 70% offering now and 90% by 2020.

• Productivity is cited as the primary benefit of mobility

• Apple has taken the top spot for enterprise smartphone preference over Blackberry; Samsung Android is second

• Blackberry continues to lose ground in the enterprise

• Roughly 75% will develop custom applications beyond basic email and PIM

• Apple, Microsoft and Google will be the most strategic platforms for the future.

3

Key Charts

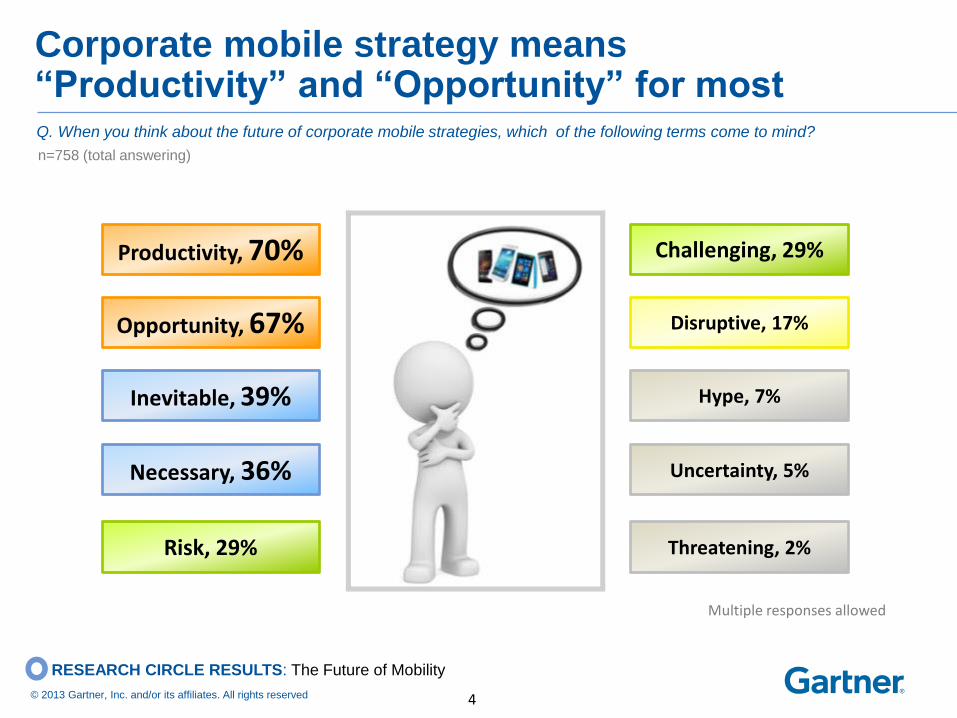

Q. When you think about the future of corporate mobile strategies, which of the following terms come to mind?

n=758 (total answering)

Multiple responses allowed

Productivity, 70%

Opportunity, 67%

Inevitable, 39%

Necessary, 36%

Risk, 29%

Challenging, 29%

Disruptive, 17%

Hype, 7%

Uncertainty, 5%

Threatening, 2%

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved 4

RESEARCH CIRCLE RESULTS: The Future of Mobility

Corporate mobile strategy means “Productivity” and “Opportunity” for most

n=780

Allow BYOD 69%

Do not 31%

Q. Does your organization allow Bring Your Own Device (BYOD) for smartphones?

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved 5

Q6. When do you anticipate your

organization will allow BYO smartphones? [among those involved in decisions]

n=140 29%

5%

44%

22%

Never

2020

2016

2014

RESEARCH CIRCLE RESULTS: The Future of Mobility

That figure will continue to grow to 90%+ by 2020.

Most companies allow BYOD for smartphones

Q. Does your organization intend to develop custom applications for smartphones?

Have developed custom

smarphone applications

37%

In the process, or plan to develop

37%

No plans at this time

26%

n=780

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved 6

Percentages are highest among larger,

aggressive companies.

Those not involved in strategic mobile

decisions seem to have an elevated view.

46%

36%

43%

37%

33%

49%

36%

29%

Not involved indecisions

Decision maker

Aggressive

Mainstream

Conservative

$3B+

$1B-<$3B

<$1B

RESEARCH CIRCLE RESULTS: The Future of Mobility

Three-quarters of organizations have developed or plan to develop custom applications

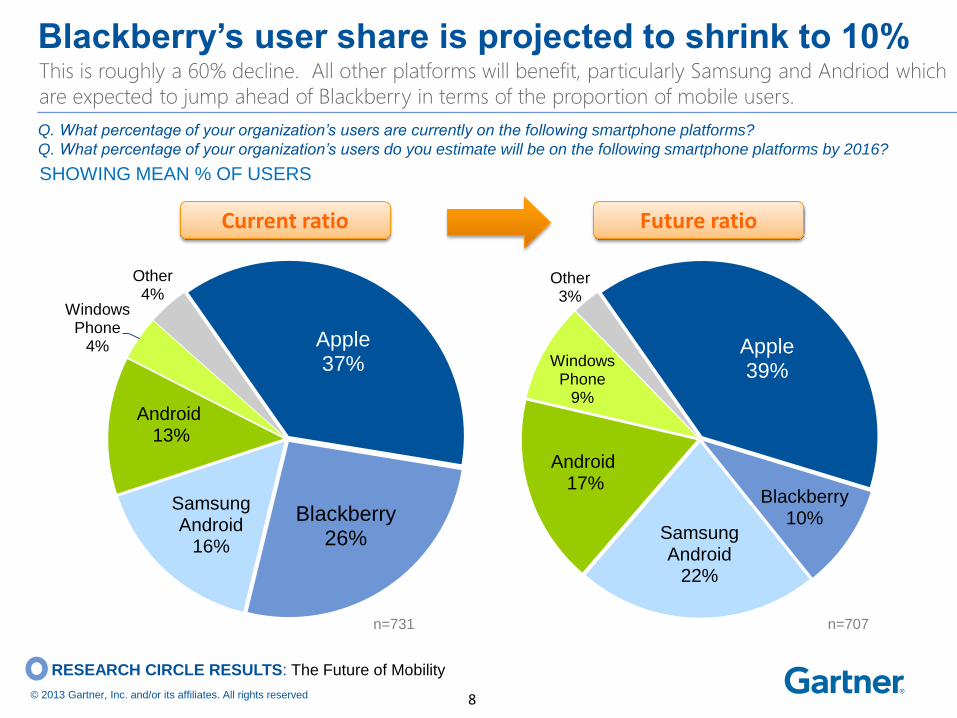

Q. What percentage of your organization’s users are currently on the following smartphone platforms?

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved 7

n=731 (excludes DK responses)

76%

61%

41%

35%

34%

9%

19%

34%

40%

39%

30%

31%

3%

14%

18%

10%

24%

5%

5%

10%

20%

3%

15%

15%

Other

Windows Phone

Android

Samsung Android

Blackberry

Apple

0% 1%-24% 25%-49% 50%-74% 75%+

91% 37.0

66% 26.1

65% 16.2

59% 12.5

39% 4.3

24% 3.9

MEAN

(average

proportion

of users)

Total %

of users

RESEARCH CIRCLE RESULTS: The Future of Mobility

Apple is present in 91% of respondent organizations , averaging 37% of their users;

Blackberry is present in 66% of respondent organizations, averaging 26% of users.

Corp. users most often operate on Apple & Blackberry

SHOWING MEAN % OF USERS

Apple 37%

Blackberry 26%

Samsung Android

16%

Android 13%

Windows Phone

4%

Other 4%

Q. What percentage of your organization’s users are currently on the following smartphone platforms?

Q. What percentage of your organization’s users do you estimate will be on the following smartphone platforms by 2016?

Current ratio

Apple 39%

Blackberry 10%

Samsung Android

22%

Android 17%

Windows Phone

9%

Other 3%

Future ratio

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved 8

n=731 n=707

RESEARCH CIRCLE RESULTS: The Future of Mobility

This is roughly a 60% decline. All other platforms will benefit, particularly Samsung and Andriod which

are expected to jump ahead of Blackberry in terms of the proportion of mobile users.

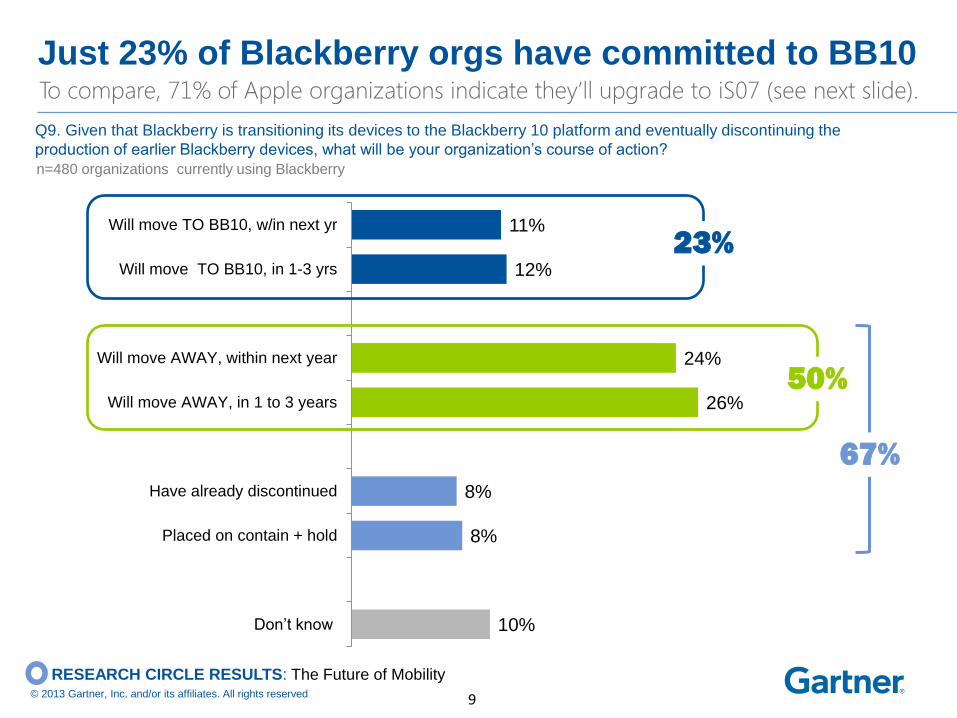

Blackberry’s user share is projected to shrink to 10%

10%

8%

8%

26%

24%

12%

11%

Don’t know

Placed on contain + hold

Have already discontinued

Will move AWAY, in 1 to 3 years

Will move AWAY, within next year

Will move TO BB10, in 1-3 yrs

Will move TO BB10, w/in next yr

Q9. Given that Blackberry is transitioning its devices to the Blackberry 10 platform and eventually discontinuing the

production of earlier Blackberry devices, what will be your organization’s course of action?

n=480 organizations currently using Blackberry

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved

23%

50%

9

67%

RESEARCH CIRCLE RESULTS: The Future of Mobility

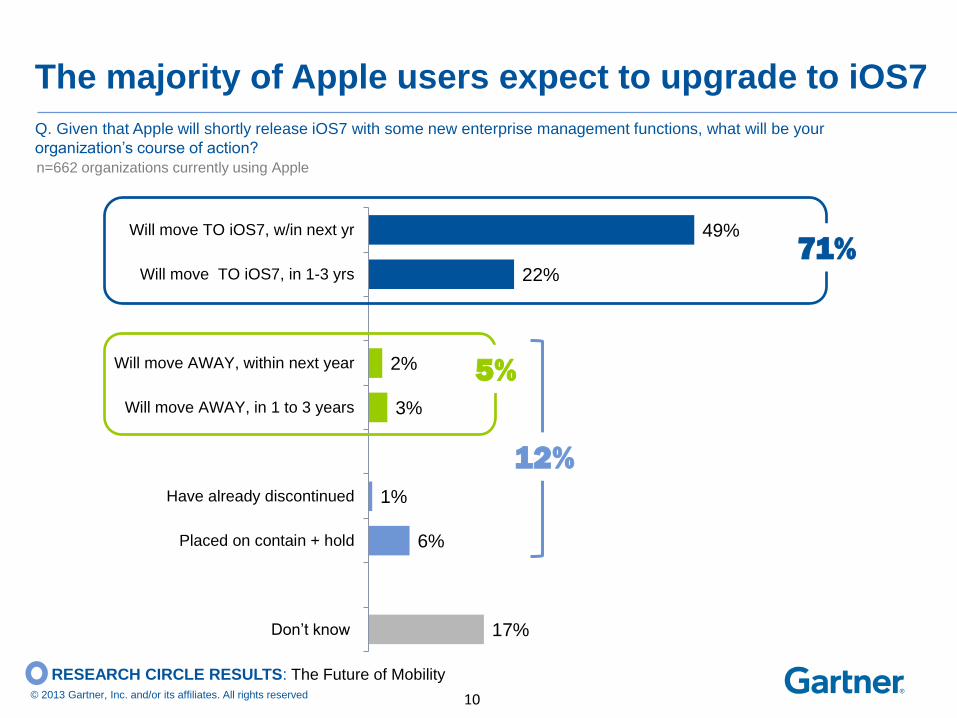

To compare, 71% of Apple organizations indicate they’ll upgrade to iS07 (see next slide).

Just 23% of Blackberry orgs have committed to BB10

17%

6%

1%

3%

2%

22%

49%

Don’t know

Placed on contain + hold

Have already discontinued

Will move AWAY, in 1 to 3 years

Will move AWAY, within next year

Will move TO iOS7, in 1-3 yrs

Will move TO iOS7, w/in next yr

Q. Given that Apple will shortly release iOS7 with some new enterprise management functions, what will be your

organization’s course of action?

n=662 organizations currently using Apple

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved

71%

5%

10

12%

RESEARCH CIRCLE RESULTS: The Future of Mobility

The majority of Apple users expect to upgrade to iOS7

Thank you! We thank you for being an active member of Gartner Research Circle.

ADDITIONAL RESOURCES:

To receive the full results, please email [email protected], with the subject line:

G-13516 data request_FULL RESULTS

For this study, we are able to provide a view of the results by region, industry and company size. Please email [email protected] to submit your request using the appropriate subject line:

G-13516 data request_REGION RESULTS

G-13516 data request_INDUSTRY RESULTS

G-13516 data request_COMPANY SIZE RESULTS

For additional queries on the data or survey instrument please contact [email protected]

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved

RESEARCH CIRCLE RESULTS: The Future of Mobility

12

Appendix: Methodology & Respondent Profile

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved 13

RESEARCH CIRCLE RESULTS: The Future of Mobility

Methodology

• This research was conducted via online survey August 21-30, 2013 among

Gartner Research Circle Members – a Gartner-managed panel comprised of IT

and business leaders, and, an external panel provided by Research Now.

• In total, 780 respondents participated. All respondents were screened for

personal knowledge of their organization’s workforce mobility strategy (i.e.

devices, platforms, and applications).

• The survey was developed collaboratively by a team of Gartner analysts

covering Mobility and Communications, and was reviewed, tested and

administered by Gartner’s Research Data Analytics team.

NOTE: The results of this study are representative of the respondent base and not necessarily the market as a whole.

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved 14

RESEARCH CIRCLE RESULTS: The Future of Mobility

11%

6%

1%

2%

2%

3%

3%

3%

3%

5%

6%

7%

8%

9%

14%

18%

Unknown

Other

Wholesale

Media

Telecommunications

Transportation

Utilities

Healthcare

Education

Retail

Insurance

Other Bus/Cons. Services

Government

Banking

IT Services & Software

Mfg & Natural Resources

Respondent profile – company characteristics

DK 8%

NonProf/Gov 7%

<$250M 24%

$250M to <$1B

13%

$1B to <$3B 13%

$3B to <$10B 13%

$10B or more 21%

n=780

Primary industry: 2012 Annual Revenue:

<1000 25%

1000-9999 32%

10,000+ 40%

DK 3%

# employees worldwide:

MEAN=5.6K

MEAN=$4.0B n=780

n=780

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved 15

RESEARCH CIRCLE RESULTS: The Future of Mobility

Respondent profile – region

14%

APAC

37%

EMEA

38%

N. America

7%

Latin America

n=780

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved 16

RESEARCH CIRCLE RESULTS: The Future of Mobility

Technology adoption profile

Aggressive 22%

Mainstream 58%

Conser- vative 20%

n=765 (total answering)

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved 17

RESEARCH CIRCLE RESULTS: The Future of Mobility

14%

46%

40%

Primarilybusiness-focused

Blend of businessand IT

Primarily IT-focused

Respondent profile – job function

IT roles:

IT Executive Leadership 37%

IT Infrastructure and Operations 14%

Applications 13%

BI & IM 7%

Enterprise Architecture 6%

PPM 6%

Security &Risk Management 6%

Business Process Improvement 4%

Vendor Relationships 2%

Other IT 6%

Business roles:

Business Leadership 26%

Strategy and Planning 22%

LOB Management 12%

R&D and Product Devel. 7%

Customer Service / CRM 5%

Product Management 4%

Finance 4%

SCM 3%

Competitive Intelligence 2%

Other business 15%

n=765 (total answering)

© 2013 Gartner, Inc. and/or its affiliates. All rights reserved 18

RESEARCH CIRCLE RESULTS: The Future of Mobility

12%

28%

31%

23%

6%

Aware or strategy,but not involved

Provide recom-mendations or advice

Part ofresponsible group

Leader ofresponsible group

Solely responsiblefor decisions

Q. To what extent are you personally knowledgeable about the decisions supporting your organization’s workforce mobility

strategy (i.e. devices, platforms, and applications)?

n=780

Decision

Makers

60%

Involvement workforce mobility strategy

Influencers